xbrl reference guide

TRANSCRIPT

PRESENTED BY

Guidance for the

Application and

Conversion

Capabilities of

XBRL

Foreword

Dear Financial Executive,

We are on the threshold of a revolution in corporate reporting.

That is how SEC Chairman Christopher Cox describes the use of interactive data to improveinternal and external financial reporting.

One important tool for interactive data is eXtensible Business Reporting Language (XBRL). Iknow something about XBRL because I helped implement it at Microsoft. We were the first U.S.company to submit our annual report in XBRL.

This reference guide is intended to give you some background on XBRL, and has been preparedto show you how you can implement XBRL in your company. It includes the following docu-ments:

• An SEC transcript of Chairman Cox’s remarks at the 12th XBRL International Confer-ence;

• The SEC’s final rule on XBRL, dated February 3, 2005, “XBRL Financial ReportingProgram on the EDGAR System”;

• “Financial Reporting in the XBRL Age: A Step-by-Step XBRL Implementation,” a FERFExecutive Report that I co-authored;

• “EDGAR Online Provides New Investment Analysis Capabilities with XBRL-TaggedData,” a Gartner white paper dated December 1, 2005; and

• “A ‘Revolution’ in Corporate Reporting?” from the January/February issue of FinancialExecutive magazine.

This reference guide will provide you with all that you need to get started.

Best wishes,

Taylor HawesController, Global Platforms and OperationsMicrosoft Corporation

ChairmanFEI’s Committee on Finance and Information Technology (CFIT)

i

RR DONNELLEY

Table of Contents

1. SEC TRANSCRIPT OF CHAIRMAN COX’S REMARKS AT THE 12TH XBRLINTERNATIONAL CONFERENCE 1

2. SEC FINAL RULES ON XBRL 4

I. BACKGROUND 5

II. THE AMENDMENTS 6

A. Form of XBRL Submissions 6

B. Description of XBRL Data 6

C. Timing of XBRL Submissions 7

D. Official Filings Still Required 8

E. Voluntary Program Content and Format 8

F. XBRL Data Must Correlate to Standard XBRL Taxonomies 11

G. Use of Tagged Data 12

H. Liability Issues 13

III. PAPERWORK REDUCTION ACT 14

IV. COST-BENEFIT ANALYSIS 16

A. Benefits 16

B. Costs 18

V. FINAL REGULATORY FLEXIBILITY ANALYSIS 19

A. Reasons for, and Objectives of, the Amendments 19

B. Significant Issues Raised by Public Comment 19

C. Small Entities Subject to the Amendments 20

D. Projected Reporting, Recordkeeping, and Other Compliance Requirements 20

E. Agency Action to Minimize Effect on Small Entities 21

VI. CONSIDERATION OF IMPACT ON THE ECONOMY, BURDEN ONCOMPETITION AND PROMOTION OF EFFICIENCY, COMPETITION,AND CAPITAL FORMATION 21

VII. STATUTORY BASIS AND TEXT OF AMENDMENTS 22

VIII. EXHIBITS 23

3. SEC PRESS RELEASE OFFERING INCENTIVES FOR COMPANIES TO FILEFINANCIAL REPORTS WITH INTERACTIVE DATA 44

ii

RR DONNELLEY

Table of Contents

4. SEC PRESS RELEASE EXTENDING THE DEADLINE FOR COMPANIES TO JOININTERACTIVE DATA TEST GROUP 45

5. OCTOBER 2005 FERF EXECUTIVE REPORT: FINANCIAL REPORTING IN THEXBRL AGE: A STEP-BY-STEP XBRL IMPLEMENTATION 46

I. PURPOSE AND INTRODUCTION 47

II. XBRL’S ADOPTION EVOLUTION 48

III. EXTERNAL REPORTING AND XBRL 48

IV. Internal Reporting and XBRL 51

V. Taking XBRL to the Next Level 53

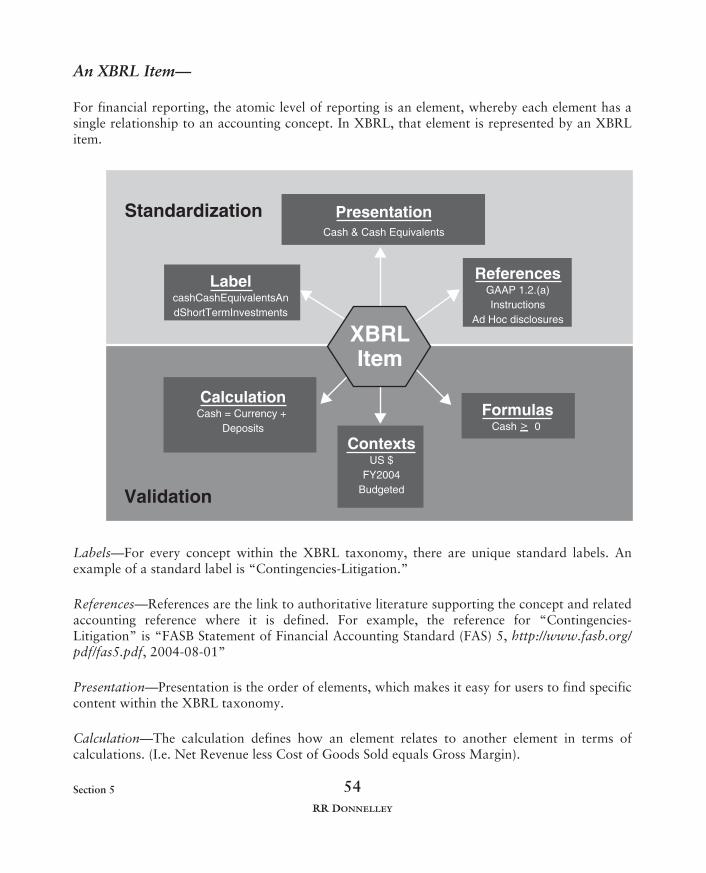

VI. What’s in a Number? The Specifics of XBRL 53A. An XBRL Item 54B. XBRL Financial Reporting Taxonomies Architecture 55

VII. An XBRL Implementation; Step-by-Step Project Plan 57A. Step 1-Identify a Team: Accountant and XML Developer 58B. Step 2-Assess Scope of Reporting and Determine Taxonomy 58C. Step 3-Compare and Map 10-K/10-Q to Taxonomies 59D. Step 4-Extend the Taxonomy as Necessary 60E. Step 5-Create an Instance Document and Validate Calculations 60F. Step 6-Review and Validate Instance Document 61G. Step 7-Publish the Instance Documents and Taxonomy 62

VIII. Conclusion 63

IX. About the Authors, CFIT and FERF 64

6. DECEMBER 2005 GARTNER WHITE PAPER 66

7. A ‘REVOLUTION’ IN CORPORATE REPORTING 75

iii

RR DONNELLEY

Speech by SEC Chairman:Remarks at the 12th XBRL International Conference

by

Chairman Christopher Cox

U.S. Securities and Exchange Commission

Tokyo, JapanNovember 7, 2005

Good afternoon. This is an exciting conference about some exciting opportunities. We really areon the threshold of a “Revolution in Corporate Reporting,” which is, appropriately, the title ofthis program.

In my tenure as Chairman of the Securities and Exchange Commission, I intend to bring oursystem of corporate disclosure and financial reporting into the 21st century. And while I musttell you that the views I express here are my own, and do not necessarily represent those of theCommission or its staff, you should know that every appointment I make as Chairman will beconsistent with this vision of tapping the possibilities of interactive data.

Interactive data promises more than simply a revolution in corporate reporting. For the SEC aswell as for financial regulatory agencies around the world, corporate reporting is not an end initself, but a means to achieving our missions. Those missions include protecting investors,encouraging capital formation, and promoting healthy markets.

Every one of those missions will be better achieved with the widespread adoption and use ofinteractive data. Interactive data will also make disclosures more useful to investors, and to everymarket participant. The information contained in SEC reports could be made instantly search-able by analysts and investors alike. Because not just the disclosure documents, but the datawithin them will be searchable and retrievable, interactive data will dramatically improve theusefulness of the entire disclosure exercise.

In our capital markets, better information usually makes for better choices. It can also help topromote honesty and integrity. As Justice Brandeis opined many years ago, “sunlight is the bestdisinfectant.” He made that statement in an influential book credited for inspiring the creationof the Securities and Exchange Commission.

Interactive data could make it possible for issuers to reduce the cost of substantiating the num-bers that appear in their financial statements. It would assist regulators in maintaining theintegrity of the markets. In the academic realm of economics, scholars often assume the ideal of“perfect information” in an effort to explain the workings of a well-functioning market. Inter-active data will help us take a giant step toward realizing that ideal. Interactive data promises yetanother revolution in the field of international accounting standards.

Section 11

RR DONNELLEY

The global debates over the “right” way to do accounting might never be settled. We may neverhave a global accounting Esperanto. But if the development of taxonomies for data tagging pro-gresses sufficiently, some day in the future it may well be possible for the users of financialinformation to render it according to any accounting regime they choose: US GAAP, IFRS, orany other system.

Instead of being forced to resolve genuinely difficult financial issues on a Procrustean bed ofarbitrary rules which don’t suit the user’s analytical purpose, accountants, analysts and investorsaround the world could all view that information from multiple perspectives.

At the SEC, our assessment of interactive data began in July of last year. But the Commission’sinterest in using technology in our disclosure program has a much longer history. The EDGARsystem, our core technology, was originally designed in the late 80s. Over time, the EDGARsystem has become out of date. It’s essentially the same now as it was a decade ago.

It goes without saying that there have been tremendous advances in computer technology andelectronic communications since EDGAR was born. During the time that EDGAR has stood still,a single 3 minute recording of music that used to require a cassette or a compact discs has beenshrunk to near invisibility, so that today literally thousands of songs can fit on a device the sizeof a credit card.

When EDGAR was born, the way most people searched the news was to manually go throughhuge stacks of newspapers and magazines. Today, almost anyone at home or in any publiclibrary can not only search the entire planet for news that is seconds old, but also have the newsrobotically sorted for them in real time via the Internet, based on their specific interests.

In the EDGAR era, business correspondence was delivered by mail which took days to arrive —or, if it was truly important, it came by overnight express. That same urgent correspondencetoday can be transmitted instantly to any country on earth, at virtually zero marginal cost, froma handheld device.

Technology is fueling a radical change in the way that business and individuals receive, process,and interact with data. It’s high time that the SEC’s financial reporting caught up with theinformation revolution. Indeed, my hope is that together we can all help lead a new revolution.In the global business environment of the 21st century, people and firms need to communicate24/7. They need to find seamless ways to accommodate different reporting systems, differentlanguages, and different regulatory environments. Not just businesses and regulators, but invest-ors, too, want faster access to more and better information than ever before.

At the SEC, our XBRL Voluntary Program was launched earlier this year as a tentative first step.The program was designed to encourage all of the participants to help us assess the potential forusing interactive data both within and outside the Commission.

For our registrants, it’s an opportunity to explore the costs and benefits of using interactive data.They’re helping us understand the impact of using XBRL on their financial reporting systems,

Section 1 2

RR DONNELLEY

and on their internal financial controls and processes. We’re also learning how XBRL can helpcompanies communicate with their shareholders and the markets generally.

In the months ahead, I expect that investors and analysts will continue to pilot the use of inter-active data applications. That will help us assess how this new flexible format might help themto improve their own analyses and decisions.

For software providers and other technology providers, this is an opportunity to showcase thecapabilities of XBRL and interactive data and tangibly demonstrate the impact to the afore-mentioned parties. For the SEC, this is our opportunity to assess how the use of interactive datacan help us improve our internal review of information, and how it can help us make it availablein more useful form to the public.

It’s fitting that this 12th XBRL International Conference is taking place in Japan. After all,XBRL has already received significant support from the Japanese government. In fact, as manyof you know, the Bank of Japan plans to implement a voluntary XBRL filing program for over500 regulated entities, possibly as early as next January. In addition, the counterpart of the SECin Japan — the Financial Services Agency — has already formed a committee to accelerate theuse of XBRL in financial disclosure. The FSA anticipates introducing an XBRL-based filing sys-tem for financial statements in the near future. The SEC and the FSA have a bilateral Memo-randum of Understanding that permits us to partner on issues such as this, and so I expect thatJapan’s experiences using XBRL will form an important part of our dialogue in the monthsahead.

As we progress with the SEC’s own assessment of interactive data, we will continue to workclosely with all of you. Because of the leadership that you’ve shown over the past 5 years, wenow stand on the threshold of some truly breathtaking changes in our global financial markets.

I’d especially like to thank those of you who have provided feedback to the Commission duringour Voluntary Program. We need your continued support. Going forward, the single most sig-nificant way you can help is to participate in the XBRL filing program at the SEC. Keep in mindthat the program isn’t limited to registrants that file reports with the SEC. We are anxious toreceive XBRL documents of any kind, both for our own internal assessment, and for publicationto the market at large via our website. And keep providing us with feedback on your experi-ences. The comments we receive will be instrumental in determining the next steps in ourimplementation of XBRL disclosure.

So let us know what’s working for you, and where change is required. If you haven’t seen it, thelatest opportunity for your feedback is in the form of a Request for Information that the SECissued last month. We’re looking for specific information on XBRL-enabled software, and we’dvery much appreciate your views.

Above all, continue with your enthusiastic contributions to the global development of the XBRLstandard. Have no doubt — you are changing the world ... for the better.

Section 13

RR DONNELLEY

SEC FINAL RULES ON XBRL

SECURITIES AND EXCHANGE COMMISSION

17 CFR Parts 228, 229, 232, 240, 249 and 270

Release Nos. 33-8529, 34-51129, 35-27944, 39-2432, IC-26747; File Number S7-35-04

RIN 3235-AJ32

XBRL Voluntary Financial Reporting Program on the EDGAR System

AGENCY: Securities and Exchange Commission.

ACTION: Final rule.

SUMMARY: We are adopting rule amendments to enable registrants to submit voluntarily sup-plemental tagged financial information using the eXtensible Business Reporting Language(XBRL) format as exhibits to specified EDGAR filings under the Securities Exchange Act of1934 and the Investment Company Act of 1940. Registrants choosing to participate in thevoluntary program also will continue to file their financial information in HTML or ASCIIformat, as currently required. To participate in the program, volunteers need to submit theirXBRL formatted information in accordance with the amendments. The voluntary program isintended to help us evaluate the usefulness of data tagging and XBRL to registrants, investors,the Commission and the marketplace.

EFFECTIVE DATE: March 16, 2005.

FOR FURTHER INFORMATION CONTACT: If you have questions about the amendments,please contact one of the following members of our staff: Brigitte Lippmann or Mark W. Green,Division of Corporation Finance (202-942-2910), Jeffrey W. Naumann, Office of the ChiefAccountant (202-942-4400), or Toai P. Cheng (202-942-0590) or David S. Schwartz(202-942-0721), Division of Investment Management, Securities and Exchange Commission,450 Fifth Street, NW, Washington, DC 20549. If you have technical questions about theEDGAR system, please contact the EDGAR Filer Support Office (202-942-8900) or RichardHeroux, EDGAR Program Manager (202-942-8800), in the Office of Information Technology.

We also invite public inquiries and comments regarding the voluntary program through the useof an Internet electronic mailbox at http://www.sec.gov/spotlight/xbrl.htm. Because electronicmail (e-mail) on the Internet is not secure, you should not send confidential or sensitiveinformation.

SUPPLEMENTARY INFORMATION: We are adopting1 amendments that will add Rules 4012

and 4023 to Regulation S-T, revise Rules 114 and 3055 under Regulation S-T,6 Item 6017 underRegulation S-K,8 Item 6019 under Regulation S-B,10 Rules 13a-1411 and 15d-1412 under the Secu-rities Exchange Act of 1934 (“Exchange Act”)13 and Rules 8b-1,14 8b-215 and 30a-216 under theInvestment Company Act of 1940 (“Investment Company Act”).17 We also are adoptingamendments that revise Forms 20-F18 and 6-K19 under the Exchange Act and add new Rule8b-33 under the Investment Company Act.

Section 2 4

RR DONNELLEY

I. BACKGROUND

On September 27, 2004, we proposed to adopt amendments to Regulation S-T to allow regis-trants to supplement their Commission filings by furnishing financial data on the Commission’sElectronic Data Gathering, Analysis and Retrieval System (“EDGAR”) as an exhibit usingeXtensible Business Reporting Language (“XBRL”),20 beginning with the 2004 calendaryear-end reporting season.

All registrants who file with the Commission are generally required to file electronically onEDGAR.21 The EDGAR database, accessible on our Web site at http://www.sec.gov, providesready access to a broad range of registrant information. Electronic submissions are governed byRegulation S-T, in conjunction with the EDGAR Filer Manual22 and the electronic filing provi-sions of applicable rules, regulations, and forms. Since we first adopted rules to implement theoperational phase of EDGAR, we have continually sought to make EDGAR more useful to theinvesting public. Proponents of the XBRL reporting standard assert that it offers benefits for allparticipants in the financial information supply chain, from registrants, who would benefit frompotential efficiencies in preparing their filings, and improved transparency of their filings, result-ing in broader analyst coverage, more market exposure and greater investor confidence, to regu-lators and investors, who would benefit from ready access to tagged financial data for analyticaland review purposes.23

The amendments that we adopt today will permit volunteers to submit on EDGAR supplementalexhibits using XBRL for the purpose of allowing registrants, the Commission and others to testand evaluate tagging technology. The voluntary program will permit any registrant to participatemerely by submitting an XBRL exhibit in the required manner. The XBRL exhibits will be pub-licly available but will be considered furnished rather than filed. Although XBRL exhibits will berequired to accurately reflect the information that appears in the corresponding part of the offi-cial filing, the purpose of submitting XBRL data is to test the related format and technology and,as a result, investors and others should continue to rely only on the official version of a filingand not rely on the XBRL data in making investment decisions. We will include cautionarylanguage to this effect on the Commission’s Web site.

We received 28 comment letters relating to the Proposing Release from various constituencies,including issuers, accounting firms, financial analysts, filing agents and associations representingthe interests of such constituencies.24 Commenters expressed general overall support for theCommission’s approach to implementing the voluntary program and investigating tagged data.Commenters also supported our approach of not limiting the program by size or specificindustry.25 The final rules include a number of changes from the proposed rules to address thecomment letters, including commenters’ recommendations to encourage participation in theprogram and provide volunteers with greater flexibility. For example, we have addressed com-menters’ requests to allow volunteers the option of whether to submit the notes to the financialstatements in XBRL in the voluntary program.26 There were many additional comments address-ing the development of the voluntary program and the XBRL technology, including taxonomydevelopment, auditor attestation and audit opinions. We discuss specific comments where appli-

Section 25

RR DONNELLEY

cable in this release; otherwise we may consider these comments in the future based on our expe-rience with the voluntary program.

We emphasize that we are in the preliminary phases of testing XBRL and we may amend thevoluntary program as the technology becomes more mature and based on our experience withthe program.

II. THE AMENDMENTS

In conjunction with establishing the voluntary filing program, we are adding new Rule 401 toRegulation S-T that will allow filers, on a voluntary basis, to furnish supplemental financialinformation using XBRL. The revision to Rule 11 of Regulation S-T, adopted as proposed,makes “XBRL-Related Documents” a defined term that means documents related to presentingfinancial information in XBRL format that are part of a voluntary submission in electronicformat in accordance with new Rule 401. New Rule 401 generally provides that a registrantparticipating in the voluntary program (a “volunteer”) may submit XBRL-Related Documents inelectronic format if they meet all the conditions of the rule. Appendix L to the EDGARLink FilerManual will provide instructions and guidance on the preparation, submission, and validation ofEDGAR-acceptable electronic filings with attached XBRL-Related Documents.27 The EDGARsystem upgrade to Release 8.10 is scheduled to become available on February 7, 2005 to, amongother things, enable EDGAR to process XBRL-Related Documents when the voluntary programbecomes effective on March 16, 2005.28

A. Form of XBRL Submissions

The amendments require that volunteers furnish XBRL-Related Documents as an exhibit toeither the Exchange Act or Investment Company Act filing from which they were derived, or asan exhibit to a filing on Form 8-K29 or Form 6-K,30 as applicable, that references, and is sub-mitted no earlier than, the related filing.31 The Forms 8-K and 6-K alternative does not apply tovolunteers that are registered management investment companies because they are generally noteligible to file those forms.32 XBRL-Related Documents will be identifiable as Exhibit 100 to thecorresponding filing.

B. Description of XBRL Data

Rule 401, as adopted, contains three requirements for disclosure that must appear in the filingwith which the XBRL-Related Documents are submitted. These requirements were not includedin the rule as proposed. First, Rule 401 requires volunteers to describe the XBRL-RelatedDocuments (whether they are filed as an exhibit to the related official filing or to a Form 8-K orForm 6-K that references such filing) either as “unaudited” or, for quarterly financial statements,“unreviewed.” Second, Rule 401 requires volunteers to provide cautionary language advisinginvestors that the purpose of furnishing XBRL data is to test the format and the technology and,as a result, investors should not rely on the XBRL data in making investment decisions. This

Section 2 6

RR DONNELLEY

additional disclosure will complement the similar cautionary statements we plan to add to ourWeb site as described in the Proposing Release. Finally, Rule 401 provides that, if a reason to filea Form 8-K or Form 6-K or an amendment to a Form 8-K or Form 6-K is to submit as an exhibitXBRL-Related Documents that present information related to financial information filed as partof a different filing (e.g., a Form 8-K that references a previously filed Form 10-Q33), volunteersmust reference the official filing from which the data in the XBRL-Related Documents wasderived.34 These disclosures should be provided, as applicable, in:

• the exhibit index of the Forms 10-K,35 10-Q, 10,36 10-SB,37 10-KSB,38 10-QSB39 or 20-F,

• Item 2.02 or 8.01 of Form 8-K, or

• the body of the Forms 6-K, N-CSR40 or N-Q.41

We received several comments and recommendations regarding disclosure about furnishingXBRL data.42 One commenter agreed that it is reasonable to require registrants to describe theofficial filings to which the XBRL exhibits correspond because investors may not be aware thatExhibit 100 reflects XBRL data.43 Another commenter44 recommended that volunteers submit aletter describing management’s basic decisions involving the use of taxonomies and policiesabout creating instance documents, including the correlation to printed financial statements andother relevant resources, the selection of taxonomies, additions and adjustments to the basetaxonomy or taxonomies, and the level of tagging detail.45 Another commenter believed thatvolunteers should be encouraged to disclose:

• that the financial information in the XBRL-Related Documents is appropriately tagged,

• the source of the tagged information (e.g., the financial statements, MD&A),

• the extent of tagging used, including whether there have been any changes in the extent oftagging or the use of extensions as compared to XBRL-Related Documents furnished forprevious fiscal periods, and

• whether any extensions meet the XBRL International technical specification.46

To facilitate participation, we have decided not to require such disclosure for the voluntaryprogram; however, we encourage volunteers to provide the additional disclosure recommendedby the commenters.

C. Timing of XBRL Submissions

The XBRL-Related Documents may be submitted at the same time as the official EDGAR filingto which they relate, either as an exhibit to the official filing or, for operating companies, as anexhibit to a Form 8-K or Form 6-K47 filed simultaneously. Alternatively, the XBRL-RelatedDocuments may be filed subsequent to the official EDGAR filing to which they relate, either in alater amendment to the official filing or, for operating companies, as an exhibit on Form 8-K or

Section 27

RR DONNELLEY

Form 6-K. Volunteers will not be permitted to submit the XBRL-Related Documents before theyfile the related official document. Although the amendments do not establish a deadline forsubmitting or amending XBRL data, volunteers are encouraged to submit the XBRL-RelatedDocuments with the official document or shortly after the official document is filed. Volunteerswill be free to submit their XBRL exhibits regularly or from time to time and can stop or start asthey choose. If a volunteer amends the XBRL-Related Documents it submitted earlier, it shouldamend the filing to which the XBRL-Related Documents are attached as an exhibit.48

Many commenters asserted that allowing volunteers to submit their XBRL-tagged financial state-ments after they file the related official filing will be important to securing volunteers.49 Com-menters recommended that a reasonable period of time be allowed for submitting XBRL-RelatedDocuments and suggested periods typically ranging from 30 days up to 90 days.50 One com-menter recommended that no deadline be required.51 Other commenters approved of a delay, butdid not specify a time period.52

As proposed, we have not implemented a submission deadline for furnishing XBRL data. One ofthe reasons for this decision is that volunteers may wish to furnish XBRL-Related Documentsthat relate to historical financial information from their previous Commission filings. While itwould be preferable for registrants to submit all XBRL-Related Documents promptly, data ele-ments in the submission would include date information and the voluntary program includessafeguards against reliance on the data. In addition, we recognize that registrants may be dis-couraged from participating in the voluntary program if we impose deadlines, especially duringthe early stages of the program when volunteers are testing the technology.

Some commenters recommended that rather than amend submissions, the volunteers be allowedto “withdraw” them from EDGAR.53 However, submissions to EDGAR cannot, as a practicalmatter, be withdrawn after public dissemination.

D. Official Filings Still Required

The XBRL-Related Documents submitted in the voluntary program will be supplemental sub-missions and will not replace the required HTML or ASCII version of the financial informationthey contain. Volunteers will be required to continue to file their official EDGAR filings.

E. Voluntary Program Content and Format

XBRL-Related Documents must contain only voluntary program content (“Voluntary ProgramContent”) that appears in voluntary program format (“Voluntary Program Format”) as furtherdescribed below.

Voluntary Program Content must consist of mandatory content (“Mandatory Content”) andmay be accompanied by optional content (“Optional Content”).

Section 2 8

RR DONNELLEY

Mandatory Content consists of a complete set of information for all periods presented in thecorresponding official EDGAR filing from one or more of the following categories (as filed in thecorresponding official EDGAR filing):54

• the complete set of financial statements (the only exceptions are that notes to the financialstatements and schedules related to the financial statements may be omitted55 unless thevolunteer is a registered management investment company, in which case it must includeSchedule I – Investments in Securities of Unaffiliated Issuers);56

• earnings information set forth in Form 6-K or Items 2.02 or 8.01 of Form 8-K (whethercontained in the body of the Form 8-K or Form 6-K or in an exhibit, and whether filed orfurnished); or

• financial highlights or condensed financial information57 (if the volunteer is a registeredmanagement investment company).

Optional Content can consist only of a complete set of information that is:

• for all periods presented in the corresponding official EDGAR filing;

• related to financial information in the corresponding official EDGAR filing that issimultaneously submitted as Mandatory Content; and

• from one or more of the following categories (as filed in the corresponding officialEDGAR filing):58

• audit opinions;59

• interim review reports;60

• reports of management on the financial statements;

• certifications; or

• Management’s Discussion and Analysis of Financial Condition and Results of Oper-ations (“MD&A”),61 Management’s Discussion and Analysis or Plan of Operation,62

Operating and Financial Review and Prospects63 or Management’s Discussion ofFund Performance (“MDFP”).64

Voluntary Program Content is in Voluntary Program Format if:

• each data element (i.e., all text and all line item names and associated values, dates andother labels) contained in the XBRL-Related Documents reflects the same information inthe corresponding official EDGAR filing (i.e., the HTML or ASCII version);

• no data element in the corresponding official EDGAR filing is changed, deleted or sum-marized in the XBRL-Related Documents;

• the XBRL-Related Documents correlate to the appropriate version of a standard taxon-omy, supplemented with extension taxonomies as specified in the EDGAR Filer Manual;

Section 29

RR DONNELLEY

• each data element contained in the XBRL-Related Documents is matched with the appro-priate tag in accordance with any applicable taxonomy; and

• the XBRL-Related Documents contain any additional mark-up related content (e.g., theXBRL tags themselves, identification of the core XML documents used and othertechnology related content) not found in the corresponding official EDGAR filing that arenecessary to comply with the EDGAR Filer Manual requirements.

We had proposed to require volunteers to furnish in XBRL format a complete set of financialstatements, including notes to the financial statements. This approach would have provided acomprehensive test of the capacity of the XBRL format for financial information to replicate theHTML and ASCII versions. The proposal also asked for comment on whether volunteers shouldbe permitted to omit the notes to the financial statements. Many commenters disagreed with theproposal to require a complete set of the notes to the financial statements in XBRL format.65

Several commenters expressed the view that the taxonomy development of the notes to thefinancial statements is not detailed enough in the standard taxonomies to facilitate easytagging.66 As a result, commenters generally believed that volunteers would need to create sub-stantial extensions, which would be burdensome and could discourage registrants from partic-ipating in the program.67 Several commenters recommended allowing volunteers to submitfinancial statements in XBRL format that omit the notes to the financial statements.68 Othercommenters indicated that the notes to the financial statements should be included in XBRLformat, noting, however, that the Commission could limit the notes required to be tagged orallow the use of a single tag for all notes.69 Some commenters recommended that volunteers beafforded flexibility in determining the level of detail to which the notes to the financial state-ments are tagged.70

Although we consider the notes to the financial statements to be an integral part of the financialstatements for filing purposes, we have determined not to mandate them for purposes of thevoluntary program. Recognizing the technical issues presented by tagging the notes to the finan-cial statements, and in light of the other safeguards in the rules, we are providing volunteers withadditional flexibility to determine whether or not to include the notes to the financial statements.If volunteers do choose to tag the notes to the financial statements in their XBRL-RelatedDocuments, they must tag all the notes so that they meet the requirements of Voluntary ProgramContent. Representing the entire set of notes to the financial statements with a single tag doesnot appear to be useful to users because of the difficulty of consuming such a large volume ofdata in that format. Consequently, we encourage volunteers that choose to tag the notes to thefinancial statements to tag at a level that provides practical data to users and furthers the goal oftesting the capabilities of the XBRL technology.

As proposed, investment company volunteers would have been required to submit the schedulesrelated to the financial statements when submitting the financial statements in XBRL format.One commenter voiced the concern that, because the XBRL taxonomy for investment companiesmay not be sufficiently developed to support tagging of these schedules, requiring inclusion ofthe related schedules would force investment company volunteers to create a substantial set oftaxonomy extensions, which would discourage participation in the program.71 We generally

Section 2 10

RR DONNELLEY

agree and have modified the rules to limit the related schedules that registered managementinvestment company volunteers must submit in XBRL format with the financial statements toSchedule I – Investments in Securities of Unaffiliated Issuers.72 We believe that this schedulemust be provided in XBRL format because the information is critical to an understanding ofinvestment company financial statements and to testing the XBRL program with regard toinvestment company filings.

Some commenters requested clarification of the requirement to provide XBRL data containingthe “same information” as in the official filing to which it relates.73 In response to these com-ments, as discussed above, we have revised proposed Rule 401 to provide more detailedspecification of the various respects in which the information in the XBRL-Related Documentsmust be the “same” as that in the official filing to which it relates. We have explained that noinformation in the corresponding official filing may be deleted, changed or summarized in theXBRL format. For example, if the revenue line item in the related official filing’s income state-ment is broken down into different segments, the XBRL data must also contain the revenue lineitems for each segment; the volunteer cannot only include the total revenue line item. If a volun-teer submits MD&A or MDFP in XBRL format, all text in addition to the tables and schedulesmust be tagged. We did not take the approach suggested by some commenters to require that theXBRL data be “consistent with”74 or “materially the same”75 as the official filing because webelieve that this could cause uncertainty, reduce the disclosure provided in an XBRL format, andimpair our pursuit of the objectives of the voluntary program.

One commenter recommended that the voluntary program exclude XBRL tagging of earningsreleases, selected financial data and schedules of ratio of earnings to fixed charges because thereare no clear standards regarding the content and presentation of such information.76 This com-menter also was concerned that some volunteers may interpret the proposed rule to allow XBRL-Related Documents to contain partial financial presentations so long as the elements of such apresentation are “the same information” as presented in (i.e., consistent with) the complete set ofannual or interim financial statements or in MD&A. As noted above, we have clarified thatpartial financial presentations are not permissible content for XBRL submissions. Also, in viewof the goals of the voluntary program to test and evaluate data tagging, we would like to test awide variety of XBRL data. Therefore, volunteers will be able to present, among otherinformation, earnings information, MD&A, MDFP, financial highlights, management oraccounting reports and certifications77 in XBRL format.

F. XBRL Data Must Correlate to Standard XBRL Taxonomies

The voluntary program requires all volunteers to use the appropriate version of a standard taxon-omy, supplemented with extension taxonomies as specified by the EDGAR Filer Manual. TheXBRL Consortium has publicly announced that it will finalize the following standard taxono-mies, which have all completed at least one review and comment period, by the end of the firstquarter of 2005:78

• Commercial and Industrial;79

• Banking and Savings Institutions;

Section 211

RR DONNELLEY

• Insurance; and

• Investment Companies.80

We have chosen March 16, 2005 as the effective date for the program, since this is the date bywhich accelerated filers with December 31 fiscal year ends are required to file their Form 10-Ks.We will provide notice on our Web site of the taxonomies supported for the voluntary programand expect that additional standard taxonomies will be permitted on the EDGAR system as theyare finalized.81 The final standard taxonomies will be incorporated into the EDGAR system andvolunteers may not attach the standard taxonomies to filings made on EDGAR.

Commenters generally believed that the draft U.S. GAAP taxonomies are sufficiently developedfor use in the voluntary program, but acknowledged that most volunteers will need to createextensions to meet their reporting requirements.82 Some commenters believed there are sufficientsoftware tools available in the market to create such extensions, but noted that the softwarerequires further development for satisfactory end-user implementation.83 One commenter, whilestrongly supporting the voluntary program, recommended that the XBRL specification for thestandard taxonomies be changed to eliminate the required use of what the commenter describedas its complex proprietary structure.84 This commenter believed that the full XBRL specificationwill not be useful to financial analysts because the customized extensions must be analyzed todetermine comparability among companies. We expect that the voluntary program will enable usto better analyze the adequacy of the standard taxonomies and whether it would be desirable todevelop our own taxonomy for some or all regulatory reporting requirements.85

G. Use of Tagged Data

As discussed in the Proposing Release, we had considered developing an application, such as astandard style sheet, so that users would be able to view XBRL data in a human readable formaton our Web site. This application would have converted XBRL files into a document that wouldhave the appearance of traditional financial information, such as a balance sheet or incomestatement.

Commenters generally did not support a standard style sheet.86 Some commenters believed that astandard style sheet was not feasible because it would not be able to render extensions.87 A stylesheet that could not render extensions would not display all the information tagged from thecorresponding official EDGAR filing.

We have decided to commence the voluntary program without providing a style sheet or otherrendering application on our Web site. Users of EDGAR data on http://www.sec.gov will be ableto download the XBRL data to perform their own financial analysis if they have appropriatesoftware.88 We plan to continue to analyze rendering and other capabilities and we may addthese features in the future. Users will continue to be able to view the official filing in ASCII orHTML format, as they can today.

Section 2 12

RR DONNELLEY

H. Liability Issues

Because the voluntary program is experimental, contains other appropriate safeguards, andshould not unnecessarily deter volunteers from participating, the revised rules provide limitedprotections from liability under the federal securities laws. Commenters generally supported theproposed liability protections;89 however, several commenters requested clarification as furtherdiscussed below. Accordingly, we are adopting Rule 402 as proposed with minor clarifyingrevisions.90

Rule 402(a) generally will provide that XBRL-Related Documents submitted in the program:

• are not deemed filed for purposes of Section 18 of the Exchange Act91 or Section 34(b) ofthe Investment Company Act92 or otherwise subject to the liability of these sections;93

• are not deemed incorporated by reference;94

• are subject to all other liability and anti-fraud provisions of the Exchange Act and Invest-ment Company Act;95 and

• are deemed filed for purposes of Rule 103 of Regulation S-T.96

Rule 402(b) provides additional relief from liability under the Securities Act, Exchange Act,Public Utility Holding Company Act, Trust Indenture Act and Investment Company Act forinformation in a volunteer’s XBRL-Related Documents that complies with the content andformat requirements of Rule 401, to the extent that the information in the corresponding portionof the official EDGAR filing was not materially false or misleading.97

Rule 402(b) also provides additional relief from liability to volunteers that fail to comply withthe content and format requirements of Rule 401 if:

• the volunteer has made a good faith and reasonable attempt to comply with the contentand format requirements,

• as soon as reasonably practicable after the volunteer becomes aware that the informationin the XBRL-Related Documents does not comply with the content and format require-ments, the volunteer amends the XBRL-Related Documents to correct the problem, and

• the information in the corresponding official EDGAR filing was not materially false ormisleading.

As discussed earlier, several commenters asked us to clarify the reference in proposed Rule402(b) to presenting information in the XBRL-Related Documents that “reflects the sameinformation as appears in the corresponding portion of the official version of the filing to whichthey relate.”98 Accordingly, Rule 402(b), as adopted, clarifies the reference by specifying that theinformation must comply with the content and format requirements of Rule 401.

Section 213

RR DONNELLEY

One commenter asserted that proposed Rule 402(b) established a “negligence” standard andsuggested that we establish an “actual knowledge” standard instead. We have decided to adoptthe standard as proposed. A volunteer that fails to satisfy Rule 402(b) still may rely on theliability protections of Rule 402(a). In addition, the Commission has provided similar pro-tections to those in Rule 402 in other appropriate circumstances and it appears that these pro-tections are workable for filers in those circumstances.99

Finally, for purposes of the voluntary program, new paragraph (f) of Rules 13a-14 and 15d-14under the Exchange Act and new paragraph (d) of Rule 30a-2 under the Investment CompanyAct provide that XBRL-Related Documents are not subject to the certification requirements ofthese rules.100

One commenter voiced concern that investment companies would be discouraged from partic-ipating in the voluntary program if they were required to provide additional certifications whenfiling amendments whose sole purpose was to submit XBRL-Related Documents attached asexhibits.101 The commenter emphasized that the concern applied to investment companies inparticular because operating companies can file a Form 8-K rather than an amendment to submitXBRL-Related Documents after the corresponding official EDGAR filing has been filed. Rule12b-15 under the Exchange Act102 and Rule 8b-15 under the Investment Company Act103 gen-erally provide that any amendment to a filing that required a certification must contain anothercertification. We clarify that, consistent with the exclusion of XBRL-Related Documents fromthe disclosure certification requirements discussed above, an amendment whose sole purpose isto submit XBRL-Related Documents attached as exhibits for the voluntary program is not sub-ject to the certification requirements of Rule 12b-15 under the Exchange Act and Rule 8b-15under the Investment Company Act.

Two of the items these certifications must address are internal control over financial reportingand disclosure controls and procedures.104 In this regard, several commenters asked us to clarifythat XBRL-Related Documents are not subject to the internal control over financial reportingand disclosure controls and procedures provisions105 that we have adopted after passage of theSarbanes-Oxley Act.106 We clarify that, for purposes of the voluntary program and consistentwith the exclusion of XBRL-Related Documents from the disclosure certification requirementsdiscussed above, XBRL-Related Documents are not subject to any of the internal control overfinancial reporting provisions adopted under Section 404 of the Sarbanes-Oxley Act or the dis-closure controls and procedures provisions.107

III. PAPERWORK REDUCTION ACT

The new and amended rules contain “collection of information” requirements within the mean-ing of the Paperwork Reduction Act of 1995 (“PRA”).108 We published a notice requestingcomment on the collection of information requirements in the Proposing Release, and submitteda request to the Office of Management and Budget (“OMB”) for review in accordance with thePRA.109 OMB approved the request on a pilot basis. An agency may not conduct or sponsor, and

Section 2 14

RR DONNELLEY

a person is not required to respond to, an information collection unless it displays a currentlyvalid OMB control number.

The title of the new collection of information is “Voluntary XBRL-Related Documents” (OMBControl No. 3235-0611). This collection of information stems from already existing regulationsand forms adopted under the Exchange Act and Investment Company Act that set forth financialdisclosure requirements for annual and periodic reports as well as current reports.110 The newand amended rules will allow registrants to furnish specified financial information in XBRL-Related Documents as exhibits to their current or periodic reports filed on EDGAR. The speci-fied financial information already is required under existing periodic and annual report require-ments, but will be tagged using XBRL. During the voluntary program, registrants will continueto include this information in ASCII or HTML format in their official EDGAR filings, but alsowill furnish the XBRL tagged data as exhibits to these filings. The XBRL-Related Documentswill consist of an instance document, a schema file,111 and linkbase files.112 Submission of XBRL-Related Documents will be voluntary and the information submitted will not be kept con-fidential.

We estimate for PRA purposes that each of 80 participants will submit four sets of XBRL-Related Documents per year that will result in an internal preparation burden of 60 hours peryear and an external cost of $6,333 per year.113 We base this estimate on discussions regardingXBRL and data tagging in general.114

Two commenters responded to our request for comments on the PRA.115 Neither commenteraddressed specifically our actual estimates.

One commenter stated that our cost estimates are based on current manual processes, ignorecosts to those other than preparers and do not address the cost savings the commenter expectswill accrue in connection with preparation, distribution and analysis of financial informationover time as XBRL and the process efficiencies it enables take hold. As to non-preparer costs, thecommenter asserted that public accounting firms will need to invest in training and skilldevelopment to enable them to provide the assurance on XBRL data that the public ultimatelywill expect.116 These comments do not raise issues for our PRA estimates because our estimatesare based on registrant costs.

Similarly, the other commenter asserted that our cost estimates fall short because they are basedon the need of most registrants to automate what are today almost entirely manual reportingprocesses, take into account the cost to prepare but not consume information and omit antici-pated cost savings over time as adoption of XBRL spreads to more internal and external proc-esses of information exchange.117

We note that for PRA purposes we estimate the average yearly cost to a registrant that partic-ipates in the voluntary program over a three-year period.118 Consequently, our estimates areintended to reflect both initial cost and on-going cost over a three-year period. In calculatingthese costs, we have tried to take into account, among other things, the current state of reporting

Section 215

RR DONNELLEY

process automation, automation that likely would be introduced in connection with the initialcost incurred and the efficiencies that likely would be realized over the course of three years.

As reflected throughout this release, we also received comments, not specifically in response tothe PRA, directed at the substance of the new and amended rules. As previously discussed, wehave revised the proposals in response to these comments. As noted earlier, we are adding toproposed Rule 401 requirements to label XBRL data as “unaudited” or “unreviewed,” providecautionary language concerning reliance on XBRL-Related Documents and, in some cases, refer-ence the official filing from which XBRL data was derived. In this regard, we note the revision toproposed Rule 401 to make it optional, rather than required, to tag financial statement footnoteswould reduce the burden.119 Therefore, on balance, we do not change our estimates.

Compliance with the amendments is mandatory for those who wish to participate in the volun-tary program. There is no retention period for the information disclosed.

IV. COST-BENEFIT ANALYSIS

The adopted voluntary program reflects our desire to increase EDGAR’s efficiency and utility.The tagging of financial and other information submitted to us through EDGAR has the poten-tial to improve the analysis of that information. In order to evaluate data tagging, we are allow-ing registrants to furnish XBRL-Related Documents as exhibits to their official EDGAR filings.

A. Benefits

We believe that tagged financial information may allow more efficient and effective retrieval,research and analysis of financial information through automated means. The adopted voluntaryprogram will assist us in assessing whether using XBRL tagged financial information enhancesthe analysis of financial information included in Commission filings. The voluntary program alsowill facilitate our ability to assess the technical requirements of processing XBRL-RelatedDocuments using EDGAR.

Today, a number of companies use the financial information provided on EDGAR to createdatabases of tagged information that they resell to users of the information. Allowing registrantsto tag their own financial data has the potential to reduce third party participation in the taggingprocess and may reduce the cost of access to tagged information. Data tagging by registrantsmay make the tagging process more accurate. Additionally, the voluntary program may benefitregistrants and the public by permitting experimentation with data tagged using XBRL. In thefuture, increased availability of accurate, tagged financial information could reduce the cost ofresearch and analysis and create new opportunities for companies that compile, provide andanalyze data to provide more value added services.

Enhanced access to tagged information has the potential to increase analyst coverage andinvestor interest in a registrant’s securities, which could increase liquidity in the market and

Section 2 16

RR DONNELLEY

lower the cost of capital. These benefits, however, are difficult to quantify and may only be real-ized if a significant number of registrants provide data in XBRL format. Many of the com-menters cited one or more of these or related potential benefits.

As to related benefits, commenters stated, among other things, that:

• XBRL will lower the cost of producing information through automation;120

• XBRL will free resources from manual reporting to do work that adds value to thebusiness;121

• XBRL-tagged data will motivate registrants to provide comparable information;122

• registrants that use XBRL internally will have improved internal reporting processes;123

and

• tagged data may assist auditors.124

One commenter asserted that, in order to realize the benefit of enhanced financial analysis,XBRL must be revised by:

• restructuring the taxonomies to break down items into a more hierarchical format with-out alternative classification locations that can lead to non-comparable data;

• enabling end-users to validate and read the level of adherence to the standard industrialtaxonomies without high-level XBRL processing; and

• eliminating duplicate elements in the standard industrial taxonomies so end users can mapto a spreadsheet template or EDGAR web site/style sheet without complex programmingcode.125

Another commenter stated that the Commission should be able to assess more effectivelywhether the benefits of full-scale implementation justify the costs by taking steps in the initialimplementation of XBRL to assess:

• how XBRL is being used by investors and analysts;

• whether the structure of the XBRL specification facilitates broad-based use by sophisti-cated users and third-party software developers; and

• whether adequate safeguards are in place to ensure that the data is prepared and dis-seminated correctly.126

We acknowledge these commenters’ concerns and suggestions. We plan to monitor the voluntaryprogram accordingly.

Section 217

RR DONNELLEY

B. Costs

The voluntary program will lead to some additional costs for registrants choosing to furnishXBRL-Related Documents as exhibits to their periodic and current reports. Some companiesmay already tag their financial information using XBRL, in which case the additional cost ofsubmitting XBRL-Related Documents will be minimal. The proposals do not dictate thatcompanies follow any particular procedure; however, some participants may choose to acquireadditional software or hire consultants to assist them with data tagging. Based on discussionswith software providers and others familiar with XBRL, we estimate that between 60 and 100registrants will participate in the voluntary program at an annual cost per registrant based onour PRA estimates.127 Based on the foregoing discussion, we estimate the aggregate cost to regis-trants that choose to participate in the voluntary program will be between $1,009,980 and$1,683,300 in the first year.128

Due to the recent development of the technology, we have had limited data to quantify the costof implementing data tagging using XBRL. Further, methods of tagging data may vary consid-erably, making accurate cost estimates difficult. In the future, there may be additional costs toparticipants in the EDGAR data stream, including lower demand for data tagging and data dis-semination. The availability of registrant tagged data, however, may provide these participantswith alternative business opportunities.129

In the Proposing Release, we sought comments and supporting data on our estimates. Wereceived no comments specifically on the estimates we provided in our cost-benefit discussion.130

Three commenters expressly cited software and personnel costs as we did in the ProposingRelease.131 Some commenters cited other specific types of costs.

For example, two commenters suggested that the initial cost of participating in the voluntaryprogram would be significant.132 Two commenters suggested that costs would go down overtime,133 while one commenter stated that the costs would remain significant.134

Two commenters emphasized that XBRL is complex. One commenter asserted that its complex-ity has the potential to cause errors in both preparation and dissemination of financial data.135

The other commenter stated that the XBRL specification, though openly disclosed, is so complexthat it virtually requires use of specialized software tools to create, access and validate data and,as a result increases costs, reduces transparency, raises the potential for erroneous data use,unduly complicates the analytical process, restricts analytical creativity and violates the easyequal access nature of EDGAR.136

One commenter suggested that registrants that participate in the voluntary program at the outsetmay face a costly reworking of their XBRL implementation as methods and procedures arerefined and, to minimize this, the Commission could encourage experimentation but shouldoversee full implementation of XBRL by a small subset of registrants to make any appropriateadjustments before broad implementation.137

We intend to monitor the voluntary program as to complexity, ongoing adjustments and othermatters.

Section 2 18

RR DONNELLEY

V. FINAL REGULATORY FLEXIBILITY ANALYSIS

We prepared this Final Regulatory Flexibility Analysis (“FRFA”), in accordance with the Regu-latory Flexibility Act.138 This FRFA relates to amendments we are adopting that allow regis-trants, on a voluntary basis, to tag financial information in specified filings using XBRL. Theamendments set forth the method by which a registrant participating in the voluntary programmay furnish XBRL-Related Documents as an exhibit to its official EDGAR filing.

A. Reasons for, and Objectives of, the Amendments

The purpose of the amendments is to further our ability to assess the feasibility and desirabilityof using tagged data on a more widespread basis in EDGAR filings. We believe the program toaccept XBRL-Related Documents through EDGAR on a voluntary basis will better enable us tostudy the extent to which XBRL enhances the comparability of that data, its usefulness forfinancial analysis, and our staff’s ability to review and assess filings. In addition, the voluntaryprogram will help us assess the effect of XBRL data tagging on the quality and transparency offinancial information as well as the compatibility of XBRL data tagging with the Commission’sfinancial reporting requirements.

B. Significant Issues Raised by Public Comment

The Initial Regulatory Flexibility Act Analysis (“IRFA”) appeared in the Proposing Release. Werequested comment on any aspect of the IRFA, including the number of small entities that wouldbe affected by the proposals, the nature of the impact, and how to quantify the impact of theproposals.

Two commenters specifically responded to our request.139 Both commenters stated that:

• it is difficult to quantify the impact of the proposed rules on small entities;

• the impact will include the initial investment for first-time creation of an instance docu-ment followed by more efficient creation of subsequent instance documents;

• small entities that participate will benefit from greater market visibility due to the abilityof analysts to incorporate their results quickly into their analysis; and

• additional exemptions should not be required during the early stages of the voluntaryprogram and the extension of the program throughout calendar 2005 will enable moresmall entities to participate after their initial reporting under the Sarbanes-Oxleyrequirements.

One of the commenters asserted that many small entities may choose to defer participation untilsystem developers provide the ability to create XBRL documents as a standard output option,thereby making the process much easier and cheaper.140 Similarly, the other commenter statedthat it expected small entities, having documented their reporting processes and controls, to

Section 219

RR DONNELLEY

automate their systems and in doing so implement XBRL-enabled streamlining of theirreporting.141

C. Small Entities Subject to the Amendments

The voluntary program may have an impact on three broad categories of small entities: all filers;participants in the voluntary program; and non-filers that interact with EDGAR. Filers includeoperating companies and investment companies. Under Exchange Act Rule 0-10, for purposes ofthe Regulatory Flexibility Act, an issuer, other than an investment company, that on the last dayof its most recent fiscal year, has total assets of $5 million or less is a “small business” or “smallorganization.”142 We estimate there are approximately 2500 small operating company issuers.Under Rule 0-10 under the Investment Company Act, an investment company is a small entity ifit, together with other investment companies in the same group of related investment companies,has net assets of $50 million or less as of the end of its most recent fiscal year.143 We estimatethat there are approximately 186 investment companies that file reports on Forms N-CSR andN-Q that meet this definition. These and other filers may be affected by any change to theEDGAR system.

A small subset of these operating and investment company issuers may voluntarily participate inthe program; however, we estimate that number will be very low.

Finally, the dissemination of XBRL data may have an impact on those entities that interact withthe EDGAR data stream. We are aware that entities have developed certain products and serv-ices based on data in EDGAR; many entities disseminate, re-package, analyze and sell theinformation. The Commission does not regulate all these entities and therefore it is currently notfeasible to accurately estimate the number or size of these potentially affected entities. We soughtcomment on the number of small entities that would be impacted by the proposal and did notreceive any additional information that would allow us to accurately estimate the number or sizeof these potentially affected entities.

D. Projected Reporting, Recordkeeping, and Other Compliance Requirements

The voluntary program is an experiment to determine the feasibility of using XBRL on a broaderbasis. Therefore, the cost of participating, the burden on the EDGAR system and the possibleeffect on those entities that use the EDGAR data stream are somewhat speculative at this point.

As the amendments relate to a voluntary filing program, no registrant is required to file XBRL-Related Documents. If a voluntary participant already uses XBRL to tag data, it may incurminimal additional cost to participate. Other participants who wish to volunteer may have topurchase software or retain a consultant to assist in tagging data. The inclusion of XBRL-Related Documents on EDGAR may also have effects on other filers, including small entities,who use the system.

The voluntary program may have some effect on any entity that interacts with the data dissem-ination stream. Allowing filers to submit information in XBRL, even voluntarily, may have an

Section 2 20

RR DONNELLEY

impact on entities providing EDGAR-based services and products. The limited, voluntary natureof the program will help the Commission assess the impact, if any, on these entities.

E. Agency Action to Minimize Effect on Small Entities

The Regulatory Flexibility Act directs us to consider significant alternatives that would accom-plish the stated objective, while minimizing any significant adverse impact on small entities. Thepurpose of the proposals is to further our ability to assess the feasibility and desirability of usingtagged data on a more widespread basis. Provision of the XBRL-Related Documents is volun-tary. We have considered different or simpler requirements for small entities. For tagged data toprovide benefits such as ready comparability, however, the data tagging system cannot havealternative requirements. Similarly, in order to achieve the benefits of data tagging, use of a sin-gle data tagging technology is necessary. If we determine to require data tagging in the future, wewill look to the results of the voluntary program to find alternatives to minimize any burden onsmall entities. Two commenters stated that additional exemptions should not be required forsmall entities during the early stages of the voluntary program.144

VI. CONSIDERATION OF IMPACT ON THE ECONOMY, BURDEN ONCOMPETITION AND PROMOTION OF EFFICIENCY, COMPETITION,AND CAPITAL FORMATION

Section 23(a)(2) of the Exchange Act145 requires us, when adopting rules under the ExchangeAct, to consider the impact that any new rule would have on competition. In addition, Sec-tion 23(a)(2) prohibits us from adopting any rule that would impose a burden on competitionnot necessary or appropriate in furtherance of the purposes of the Exchange Act. Furthermore,Section 2(b)146 of the Securities Act, Section 3(f)147 of the Exchange Act, and Section 2(c)148 ofthe Investment Company Act require us, when engaging in rulemaking where we are required toconsider or determine whether an action is necessary or appropriate in the public interest, toconsider, in addition to the protection of investors, whether the action will promote efficiency,competition, and capital formation.

In the Proposing Release, we considered the amendments in light of the standards set forth in theabove statutory sections. We requested comment on whether the proposals, if adopted, wouldpromote efficiency, competition and capital formation or have an impact or burden on competi-tion. We also requested commenters to provide empirical data and other factual support for theirviews if possible. No commenter addressed anti-competitive effects.149 Some commentersaddressed efficiency and capital formation which we considered and addressed in the cost-benefitsection.

The adopted amendments seek to implement a voluntary program and are intended to help usevaluate the usefulness to registrants, investors and the Commission of data tagging in general,and XBRL in particular. We believe that the amendments will promote efficiency because taggeddata may allow more efficient and effective retrieval, research and analysis of financialinformation through automated means. Because the program is voluntary and the amendments

Section 221

RR DONNELLEY

are designed to permit filers to provide information in a format that we believe has the potentialto be more useful to investors, we believe the amendments do not impose any burden oncompetition that is not necessary or appropriate in furtherance of the purposes of the ExchangeAct.

VII. STATUTORY BASIS AND TEXT OF AMENDMENTS

We are adopting the amendments outlined above under Sections 19(a) and 28 of the SecuritiesAct, Sections 3, 12, 13, 14, 15(d), 23(a), 35A and 36 of the Exchange Act, Section 20(a) of thePublic Utility Holding Company Act, Section 319(a) of the Trust Indenture Act, Sections 8, 30and 38 of the Investment Company Act and Section 3(a) of the Sarbanes-Oxley Act.

List of Subjects in CFR Parts 228, 229,232, 240, 249 and 270

Reporting and recordkeeping requirements, Securities.

For the reasons set forth above, we amend title 17, Chapter II of the Code of Federal Regulationsas follows:

PART 228 – INTEGRATED DISCLOSURE SYSTEM FOR SMALL BUSINESSISSUERS

1. The authority citation for Part 228 continues to read in part as follows:

Authority: 15 U.S.C. 77e, 77f, 77g, 77h, 77j, 77k, 77s, 77z-2, 77z-3, 77aa(25), 77aa(26), 77ddd,77eee, 77ggg, 77hhh, 77jjj, 77nnn, 77sss, 78l, 78m, 78n, 78o, 78u-5, 78w, 78ll, 78mm, 80a-8,80a-29, 80a-30, 80a-37, 80b-11, and 7201 et seq.; and 18 U.S.C. 1350.

* * * * *

2. Amend §228.601 by:

a. Revising the exhibit table; and

b. Adding paragraph (b)(100).

The revision and addition read as follows.

§ 228.601 (Item 601) Exhibits.

(a) * * *

Section 2 22

RR DONNELLEY

EXHIBIT TABLE

Securities Act Forms Exchange Act Forms

SB-2 S-2 S-3 S-43 S-8 10-SB 8-K5 10-QSB 10-KSB

(1) Underwriting agreement . . . . . . . . . X X X X X(2) Plan of purchase, sale,

reorganization, arrangement,liquidation or succession . . . . . . . . . . X X X X X X X X

(3) (i) Articles of Incorporation . . . . . . . X X X X X X(ii) Bylaws . . . . . . . . . . . . . . . . . . . . . . . X X X X X X(4) Instruments defining the rights of

security holders, includingindentures . . . . . . . . . . . . . . . . . . . . . . X X X X X X X X X

(5) Opinion on legality . . . . . . . . . . . . . X X X X X(6) No exhibit required . . . . . . . . . . . . . N/A N/A N/A N/A N/A N/A N/A N/A N/A(7) Correspondence from an

independent accountant regardingnon-reliance upon a previously issuedaudit report or completed interimreview . . . . . . . . . . . . . . . . . . . . . . . . . X

(8) Opinion on tax matters . . . . . . . . . . X X X X(9) Voting trust agreement and

amendments . . . . . . . . . . . . . . . . . . . . X X X X(10) Material contracts . . . . . . . . . . . . . X X X X X X(11) Statement re: computation of per

share earnings . . . . . . . . . . . . . . . . . . . X X X X X X(12) No exhibit required . . . . . . . . . . . . N/A N/A N/A N/A N/A N/A N/A N/A N/A(13) Annual report to security holders

for the last fiscal year, Form 10-Q or10-QSB or quarterly report tosecurity holders1 . . . . . . . . . . . . . . . . X X X X

(14) Code of ethics . . . . . . . . . . . . . . . . . X X(15) Letter on unaudited interim

financial information . . . . . . . . . . . . . X X X X X X(16) Letter on change in certifying

accountant4 . . . . . . . . . . . . . . . . . . . . X X X X X X(17) Letter on departure of director . . . X(18) Letter on change in accounting

principles . . . . . . . . . . . . . . . . . . . . . . X X(19) Reports furnished to security

holders . . . . . . . . . . . . . . . . . . . . . . . . X(20) Other documents or statements to

security holders or any documentincorporated by reference . . . . . . . . . X X

Section 223

RR DONNELLEY

Securities Act Forms Exchange Act Forms

SB-2 S-2 S-3 S-43 S-8 10-SB 8-K5 10-QSB 10-KSB

(21) Subsidiaries of the small businessissuer . . . . . . . . . . . . . . . . . . . . . . . . . . X X X X

(22) Published report regarding matterssubmitted to vote of securityholders . . . . . . . . . . . . . . . . . . . . . . . . . X X

(23) Consents of experts and counsel . . X X X X X X2 X2 X2

(24) Power of attorney . . . . . . . . . . . . . . X X X X X X X X X(25) Statement of eligibility of trustee . . X X X X(26) Invitations for competitive bids . . . X X X X(27) through (30) [Reserved] . . . . . . . . .(31) Rule 13a-14(a)/15d-14(a)

Certifications . . . . . . . . . . . . . . . . . . . . X X(32) Section 1350 Certifications . . . . . . . X X(33) through (98)[Reserved] . . . . . . . . . .(99) Additional exhibits . . . . . . . . . . . . . X X X X X X X X X(100) XBRL-Related Documents . . . . . . X X X X

1 Only if incorporated by reference into a prospectus and delivered to holders along with theprospectus as permitted by the registration statement; or in the case of a Form 10-KSB, wherethe annual report is incorporated by reference into the text of the Form 10-KSB.

2 Where the opinion of the expert or counsel has been incorporated by reference into a pre-viously filed Securities Act registration statement.

3 An issuer need not provide an exhibit if: (1) an election was made under Form S-4 to provideS-2 or S-3 disclosure; and (2) the form selected (S-2 or S-3) would not require the company toprovide the exhibit.

4 If required under Item 304 of Regulation S-B.

5 A Form 8-K exhibit is required only if relevant to the subject matter reported on the Form 8-Kreport. For example, if the Form 8-K pertains to the departure of a director, only the exhibitdescribed in paragraph (b)(17) of this section need be filed. A required exhibit may beincorporated by reference from a previous filing.

(b) * * *

(100) XBRL-Related Documents. An electronic filer that participates in the voluntary XBRL(eXtensible Business Reporting Language) program may submit XBRL-Related Documents(§232.11 of this chapter) in electronic format as an exhibit to: the filing to which they relate; anamendment to such filing; or a Form 8-K (§249.308 of this chapter) that references such filing, ifthe Form 8-K is submitted no earlier than the date of that filing.

Section 2 24

RR DONNELLEY

PART 229 – STANDARD INSTRUCTIONS FOR FILING FORMS UNDERSECURITIES ACT OF 1933, SECURITIES EXCHANGE ACT OF 1934 ANDENERGY POLICY AND CONSERVATION ACT OF 1975 – REGULATIONS-K

3. The authority citation for Part 229 continues to read in part as follows:

Authority: 15 U.S.C. 77e, 77f, 77g, 77h, 77j, 77k, 77s, 77z-2, 77z-3, 77aa(25), 77aa(26), 77ddd,77eee, 77ggg, 77hhh, 77iii, 77jjj, 77nnn, 77sss, 78c, 78i, 78j, 78l, 78m, 78n, 78o, 78u-5, 78w,78ll, 78mm, 79e, 79j, 79n, 79t, 80a-8, 80a-9, 80a-20, 80a-29, 80a-30, 80a-31(c), 80a-37,80a-38(a), 80a-39, 80b-11, and 7201 et seq.; and 18 U.S.C. 1350, unless otherwise noted.

* * * * *

4. Amend §229.601 by:

a. Revising the exhibit table; and

b. Adding paragraph (b)(100).

The revision and addition read as follows.

§ 229.601 (Item 601) Exhibits.

(a) * * *

Webmaster’s note: The exhibit table that followed was too wide to fit the website page format.Click to view table.

(b) * * *

(100) XBRL-Related Documents. An electronic filer that participates in the voluntary XBRL(eXtensible Business Reporting Language) program may submit XBRL-Related Documents(§232.11 of this chapter) in electronic format as an exhibit to: the filing to which they relate; anamendment to such filing; or a Form 8-K (§249.308 of this chapter) that references such filing, ifthe Form 8-K is submitted no earlier than date of that filing.

PART 232 – REGULATION S-T – GENERAL RULES AND REGULATIONSFOR ELECTRONIC FILINGS

5. The authority citation for Part 232 continues to read as follows:

Authority: 15 U.S.C. 77f, 77g, 77h, 77j, 77s(a), 77sss(a), 78c(b), 78l, 78m, 78n, 78o(d), 78w(a),78ll(d), 79t(a), 80a-8, 80a-29, 80a-30, 80a-37, and 7201 et seq.; and 18 U.S.C. 1350.

* * * * *

Section 225

RR DONNELLEY

6. Amend §232.11 by adding the following definition in alphabetical order.

§ 232.11 Definition of terms used in part 232.

* * * * *

XBRL-Related Documents. The term XBRL-Related Documents means documents related topresenting information in eXtensible Business Reporting Language that are part of a voluntarysubmission in electronic format in accordance with §232.401.

7. Amend §232.305 by revising paragraph (b) to read as follows:

§ 232.305 Number of characters per line; tabular and columnar information.

* * * * *

(b) Paragraph (a) of this section does not apply to HTML documents or XBRL-Related Docu-ments (§232.11).

8. Amend Part 232 by adding an undesignated center heading and text to §§232.401 and232.402 to read as follows:

XBRL-Related Documents

§ 232.401 XBRL-Related Document submissions.

(a) An electronic filer that participates in the voluntary XBRL (eXtensible Business ReportingLanguage) program may submit XBRL-Related Documents (§232.11) in electronic format as anexhibit to: the filing to which they relate; an amendment to such filing; or, if the electronic filer iseligible to file a Form 8-K (§249.308 of this chapter) or a Form 6-K (§249.306 of this chapter), aForm 8-K or a Form 6-K, as applicable, that references the filing to which the XBRL-RelatedDocuments relate if such Form 8-K or Form 6-K is submitted no earlier than the date of that fil-ing. The XBRL-Related Documents must comply with the content and format requirements ofthis section, be submitted as an exhibit to a form that contains the disclosure required by thissection and be submitted in accordance with the EDGAR Filer Manual and, as applicable, one ofItem 601(b)(100) of Regulation S-K (§229.601(b)(100) of this chapter), Item 601(b)(100) ofRegulation S-B (§228.601(b)(100) of this chapter), Form 20-F (§249.220f of this chapter), Form6-K or §270.8b-33 of this chapter.

(b) XBRL-Related Documents must consist of mandatory content and may consist of optionalcontent but only if the optional content accompanies the mandatory content in the same sub-mission.

Section 2 26

RR DONNELLEY

(1) Mandatory content consists of a complete set of information for all periods presented in thecorresponding official EDGAR filing from one or more of the following categories (as filed in thecorresponding official EDGAR filing):

(i) The complete set of financial statements (the only exceptions are that notes to the financialstatements and schedules related to the financial statements may be omitted unless the electronicfiler is a registered management investment company in which case it must include Schedule I –Investments in Securities of Unaffiliated Issuers (§210.12-12 of this chapter));

(i) Earnings information set forth in Form 6-K or Items 2.02 or 8.01 of Form 8-K (whether con-tained in the body of the Form 6-K or Form 8-K or in an exhibit, and whether filed orfurnished); or

(ii) Financial highlights or condensed financial information set forth in Item 8(a) of Form N-1A(§239.15A and §274.11A of this chapter), Item 4.1 of Form N-2 (§239.14 and §274.11a-1 ofthis chapter) or Item 4(a) of Form N-3 (§239.17a and §274.11b of this chapter), as applicable.

(2) Optional content can consist only of a complete set of information that is:

(i) For all periods presented in the corresponding official EDGAR filing;

(ii) Related to financial information in the corresponding official EDGAR filing that is simulta-neously submitted as mandatory content (as specified in paragraph (b)(1) of this section); and

(iii) From one or more of the following categories (as filed in the corresponding official EDGARfiling):

(A) Audit opinions (as specified by Rule 2-02 of Regulation S-X (§210.2-02 of this chapter));

(B) Interim review reports (as specified by Rule 10-01(d) of Regulation S-X (§210.10-01(d) ofthis chapter));

(C) Reports of management on the financial statements;

(D) Certifications;

(E) Management’s discussion and analysis of financial condition and results of operations (asspecified by Item 303 of Regulation S-K (§229.303 of this chapter));

(F) Management’s discussion and analysis or plan of operation (as specified by Item 303 ofRegulation S-B (§228.303 of this chapter));