www.probonopartner.org copyright 2015 pro bono partnership. all rights reserved. no further use,...

TRANSCRIPT

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

THE COMPLIANCE CHECKLIST:PRACTICAL STEPS FOR MEETING THE REQUIREMENTS OF THE NY

NONPROFIT REVITALIZATION ACT

Presented for the Not-for-Profit Leadership Summit

May 4, 2015

Maurice K. Segall, Esq.

Judy Siegel, Esq.

Courtney Darts, Esq.

Pro Bono Partnership

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

Pro Bono Partnership• Free business legal services for nonprofit organizations through

the services of our staff and volunteer attorneys

• To be eligible, an organization must be:

• Nonprofit and tax-exempt (or seeking (501(c)(3) status);

• Providing services in New York, New Jersey, or Connecticut;

• Engaging in activities that benefit the disadvantaged or otherwise providing important social services, or arts, educational, or environmental programs;

2

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

Pro Bono Partnership cont’d.• Providing programs or services with a demonstrable impact;

• A group with genuine legal needs that the Partnership can address; and

• Unable to pay for legal services without significant impairment of program resources.

• To apply to become a client, visit www.probonopartner.org and click on “Request Legal Assistance”

3

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

4

What Assistance is Available?

• Non-litigation, business law matters in areas such as:

• Corporate structure and governance• Contracts• Employment law• Environmental law• Intellectual property law• Mergers, dissolutions, or bankruptcy• Real estate (including lease reviews) • Regulatory compliance (e.g., registration, annual reporting, charitable solicitation,

lobbying)• Tax law and tax exempt status

• More information at www.probonopartner.org

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

5

Goals of Revitalization Act

• Increase fiscal transparency• Prevent private benefit• Provide an enforcement mechanism for

the Attorney General’s office

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

6

Mechanisms to Accomplish Revitalization Act Goals

• Added new sections to the not-for-profit corporation law– Section 712 -- Audit Oversight– Section 715 – Related Party Transactions– Section 715-a -- Conflict of Interest Policy– Section 715-b – Whistleblower Policy

• Expanded definitional section 102

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

7

Today’s Key Takeaway

Every New York nonprofit needs to have a plan for complying with these new requirements

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

8

CHANGES TO YOUR BYLAWS

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

9

Simple Updates to Bylaws

• Board meetings – video or Skype participation permitted

• Unanimous written consent – e-mail and fax permitted

• Notice and waivers of notice – e-mail and fax permitted

• Member proxies – e-mail and fax permitted

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

10

Simple Updates to Bylaws (cont’d)

• Ordinary real estate transactions – review and approval can be delegated to a committee or approved by a simple majority of the board

• Note: If real estate transaction includes substantially all of the nonprofit’s assets, still need approval of 2/3 of the entire board

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

11

Committees• NPRA eliminated old categories of

“standing” and “special” committees• New designations are “committees of the

board” and “committees of the corporation”

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

12

Committees (cont’d)• Committees of the board consist only of

board members, must have at least three members, are elected by the board, and can act for the board– A non-director can participate in the

committee’s activities as a non-member advisor, but cannot vote.

• Committees of the corporation can include non-board members and cannot act for the board

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

13

Committees (cont’d.)• Nonprofits should look at the authority and

functions of their existing committees and update their bylaws and/or committee charters as needed

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

14

CONFLICTS OF INTEREST

AND

RELATED PARTY TRANSACTIONS

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

15

Conflict of Interest Policyand Related Party Transactions

• Interwoven

• Found in various sections of the Revitalization Act

• Should be something the Board identifies and focuses on regularly.

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

16

Purpose of Conflict of Interest Policy

• Ensure that the corporation’s directors, officers and key employees act in the corporation’s best interest

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

17

Who is a Key Employee?

• A person who exercises substantial control over the affairs of the corporation or is a family member of a person in such a position

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

18

Leads to Checklist Items 1-3

• Maintain a master list of directors, officers and key employees

• Identify the person responsible for maintaining the master list of directors, officers and key employees

• Analyze and identify who is a key employee

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

19

Examples of Key Employees

• Directors and officers• CEO/CFO/COO/Treasurer/Executive Director• A founder of an organization• A person in charge of a substantial source of revenue for

a program• A person who manages or supervises a program or

discrete segment of the business or of the budget• includes any entity in which a disqualified person holds

more than 35% of the combined voting power, profits, interest, or beneficial interest

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

20

Related Party Transactions

• No not-for-profit corporation can enter into a related party transaction unless the transaction is determined to be “fair, reasonable and in the best interest of the corporation at the time of the determination.”

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

21

What is a Related Party Transaction?

• Any transaction in which a related party has a financial interest and in which the corporation or any affiliate of the corporation is a participant

• Also includes any transaction in which a related party has an indirect financial interest

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

22

Who is a Related Party?

• A Related Party is:– A director, officer or key employee of the

corporation or the corporation’s affiliate– Any relative of the any of the above; or– Any entity in which any of the individuals

above has at least 35% ownership interest.

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

23

Checklist Items 4 and 5

• Identify relatives of officers, directors and key employees

• Identify entities in which officers, directors and key employees hold at least a 35% ownership interest

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

24

Related Party Transactions Involving Charitable Corporations Where

Related Party has a “Substantial Financial Interest”

• “Substantial financial interest” not defined in the law

• Board or an authorized committee of the board must:– Consider alternatives to the extent available– Approve the transaction by a majority vote of directors

present at the meeting– Contemporaneously document the basis for the

decision

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

25

Checklist Numbers 6, 7 and 8

• Prepare form for reporting potential or actual related party transaction (and/or conflict of interest)

• Prepare worksheet(s) that provides framework for assessing alternative transactions and use it each time a Related Party Transaction needs to be considered

• Prepare and use checklist for board minutes to ensure Related Party Transaction analysis properly recorded

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

26

Conflict of Interest Policy

• Can be contained either in the bylaws or a separate resolution

• Sets forth procedures for board to follow to ensure that conflicts do not exist and to approve transactions when a conflict arises

• Requires board members to complete conflict of interest disclosure prior to election and annually thereafter

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

27

Checklist Number 9

• Prepare annual disclosure form for officers, directors and key employees to keep corporation apprised of any potential conflicts of interest or related party transactions

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

28

Conflict of Interest Policy

• Gives board discretion to define what constitutes a conflict of interest– Does not just have to be financial interest, board can

expand

• Lets board define exceptions to conflict of interest– De minimis transactions– Ordinary course transactions

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

29

Conflict of Interest Policy

• Requires that if there is a Related Party Transaction, the transaction must be approved by the board (or a committee) and– The conflict must be disclosed to the board– The board member must recues themselves from the board vote– The related party cannot try and influence the vote– The board must approve the transaction on the basis that it is in

the best interest of the corporation– A basis for that decision must be noted in the minutes of the

meeting or another document

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

30

Who Can Approve Related Party Transactions?

• Revitalization Act is unclear • Most conservative approach is to say that

only “Independent Directors” can vote on Related Party Transactions or transactions where there might be a conflict of interest

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

31

Who is an Independent Director?

“Independent director” means a director who within each of the last three years:– Has not been an employee of the nonprofit or any of its affiliates;– Has had no relatives serving as “key employees” of the nonprofit

or any of its affiliates;– Who has not received, and does not have a relative who has

received, more than $10,000 compensation from the nonprofit (other than reimbursement for reasonable expenses); and

– Has neither been employed by, nor has had a substantial financial interest in, any entity that has either paid or received payments from the nonprofit exceeding the lesser of $25,000 or 2% of the entity’s gross revenues. (“Compensation” does not include charitable donations.)

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

32

MANAGING AUDITS

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

33

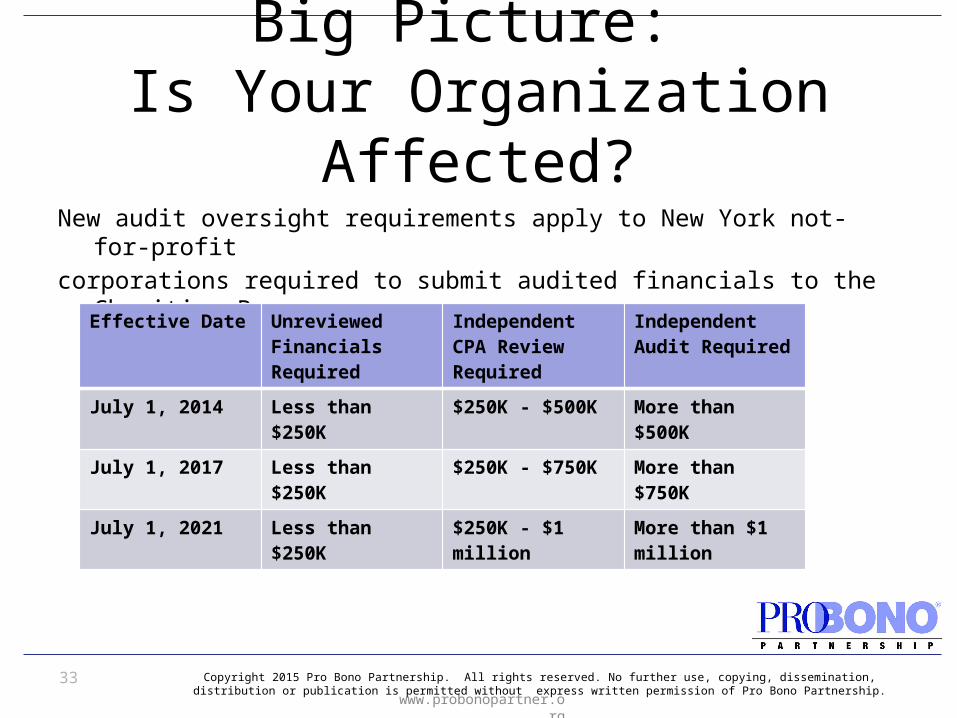

Big Picture: Is Your Organization Affected?

New audit oversight requirements apply to New York not-for-profit

corporations required to submit audited financials to the Charities Bureau

Effective Date Unreviewed Financials Required

Independent CPA Review Required

Independent Audit Required

July 1, 2014 Less than $250K $250K - $500K More than $500K

July 1, 2017 Less than $250K $250K - $750K More than $750K

July 1, 2021 Less than $250K $250K - $1 million More than $1 million

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

34

Who Oversees the Audit?

• Either a designated Audit Committee consisting entirely of “independent” directors; or

• The Board of Directors, with only “independent” directors participating in the deliberations and voting.

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

35

The Audit Committee Charter

• If your audit is managed by an audit committee (or if audit oversight is delegated to your finance committee), create or amend the committee charter to specify the committee’s authority and responsibilities

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

36

Annual Preparation

• Every year, distribute a disclosure statement to the entire board to confirm which of your board members meet the definition of an “independent” director (usually done in conjunction with annual review of conflict of interest policy)

• Determine if any of the directors do not qualify as “independent” and thus are ineligible to either serve on Audit Committee or oversee audit at board level

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

37

Committee or Board Responsibilities: Less Than $1

Million in Annual Revenue

• Retain or renew the retention of an independent CPA to conduct the audit

• Once audit is completed, review the audit and any related management letter with the auditor

• Keep minutes!• Audit Committee should report regularly to the

rest of the Board

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

38

Committee or Board Responsibilities: More Than $1 Million in Annual Revenue

• Retain or renew the retention of an independent CPA to conduct the audit

• Review the scope and planning of audit with auditor prior to start of the audit

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

39

Committee or Board Responsibilities: More Than

$1 Million in Revenue (cont’d)• Once audit is completed, review and discuss

with the auditor:– The audit and any related management letter;– Any material risks and weaknesses in internal

controls identified by the auditor;– Any restrictions on the scope of the auditor’s

activities or access to requested information;

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

40

Committee or Board Responsibilities: More Than

$1 Million in Revenue (cont’d)• Once audit is completed, review and discuss

with the auditor (cont’d):– Any significant disagreements between the

auditor and management; and– The adequacy of the organization’s

accounting and financial reporting processes

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

41

Committee or Board Responsibilities: More Than

$1 Million in Revenue (cont’d)• Keep minutes!

• Audit Committee should report regularly to the rest of the Board

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

42

AG Recommends that Audit Committee or Board Also:

• Ensure that proper federal and state compliance and tax filings are submitted on time and all taxes or fees are paid

• Review the organization’s internal and financial controls on a periodic basis

• Assure the conduct of appropriate risk assessments and risk response plans

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

43

AG Recommendations (cont’d)

• Institute and oversee any special investigatory work as needed, and ensure responses to investigations

• Periodically review the organization’s insurance coverage and determine its adequacy

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

44

AG Recommendations (cont’d)

• Monitor any legal matters that could impact the reputation and financial health of the organization

• Identify and monitor related party transactions and periodically review the organization’s policies on conflicts of interest and related party transactions, ethics, and whistleblower protections, updating as needed

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

45

Whistleblower Policy – Are You Required to Have One?

• If your nonprofit has 20 or more employees and over $1 million in annual gross revenue, you must have a whistleblower policy that meets statutory requirements.

• Either adopt a new policy or have your existing policy reviewed by counsel to make sure it:– Has procedures for reporting suspected violations of laws or

corporate policies and for maintaining confidentiality of reported information

– Designates an employee, officer, or director to administer the policy

– Requires distribution of the policy to all directors, officers, employees, and “volunteers who provide substantial services to the corporation”

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

46

Contact Us

237 Mamaroneck AvenueSuite 300White Plains, NY 10605 Phone: 914-328-0674

280 Trumbull Street28th FloorHartford, CT 06103 Phone: 860-541-4951

300 Lanidex PlazaSuite 3203Parsippany, NJ 07054 Phone: 973-240-6955

New York & Fairfield County Connecticut (except Fairfield County)

New Jersey

www.facebook.com/PBPartnership

www.twitter.com/PBPartnership

www.linkedin.com/company/pro-bono-partnership

www.probonopartner.org

Copyright 2015 Pro Bono Partnership. All rights reserved. No further use, copying, dissemination,distribution or publication is permitted without express written permission of Pro Bono Partnership.

47

Please Note• Any tax advice contained in this communication (including any

attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein.

• This presentation is provided as a general informational service to clients and friends of Pro Bono Partnership. It should not be construed as, and does not constitute, legal advice on any specific matter, nor does this presentation create an attorney-client relationship. You should seek advice based on your particular circumstances from an independent legal advisor.