www.kingandshaxson.com investment opportunities in tradable instruments: treasury bills,...

TRANSCRIPT

www.kingandshaxson.com

Investment Opportunities in Tradable Instruments:Treasury Bills, Certificates of Deposit Gilts, Supranational and Corporate Bonds.

2

www.kingandshaxson.com

A heightened focus on Treasury since the onset of the crisis:

- Risk aversion

- Counterparty lending lists

Principles of Treasury Management remain unchanged:

“Security, Liquidity, Yield…In that order!”(DCLG investment principles)

Investment Landscape

3

www.kingandshaxson.com

Treasury Bills - Secure, Liquid and Yield more than the DMADF.

Certificates of Deposit (CD’s) - Negotiable deposit issued by banks, building societies

Gilts, Supranational and Corporate Bonds - Medium/longer term fixed flow of interest

What are the benefits of negotiable instruments?

4

www.kingandshaxson.com

Liquidity

Certificates of Deposit Same Day 2 weeks - 1 Year

Treasury Bills Same Day 1 week - 6 Months

Gilts T+1 3 months - 50 years

Supranational bonds T+3 3 months - 50 years

Corporate bonds T+3 3 months - 40 years

Range of investments

Maturity

Custodian service required

Crest, for CDs, T bills and gilts

Euroclear, for Supranational and Corporate bonds

5

www.kingandshaxson.com

Current Yields

Certificate of Deposit

Treasury bills

Gilts Supranational

1 month 0.68% 0.32%

3 months 1.06% 0.42%

6 months 1.38% 0.43%

1 year 1.89% 0. 41% 0.89%

5 years 1.58% 2.70%

10 years 2.00% 3.09%

6

www.kingandshaxson.com

Treasury Bills

7

www.kingandshaxson.com

Treasury Bills

Short-term securities issued by HM Treasury on a discount basis

Issued below 100, but you get 100 back on maturity

Difference equals your interest return

Very low risk in both duration and credit: extremely liquid.

8

www.kingandshaxson.com

Treasury Bills

Issued, by tender, usually to central, clearing and investment banks, 1, 3 and 6 month bills

Best rates available through primary market

Bids are submitted on a Friday, before 11.00am with settlement on the next working day

Secondary market can be expensive

9

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Purchase / Sale Proceeds Calculation

Deal Rate x No of Days to Maturity36,500( )1 +

Nominal

10

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

Purchase / Sale Proceeds Calculation

Deal Rate x No of Days to Maturity36,500( )1 +

£10m

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

11

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

Purchase / Sale Proceeds Calculation

0. 41 x No of Days to Maturity36,500( )1 +

£10m

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

12

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

Purchase / Sale Proceeds Calculation

0.41 x 18236,500( )1 +

£10m

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

13

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

Purchase / Sale Proceeds Calculation

74.6236,500( )1 +

£10m

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

14

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

1.00204438356( )£10m

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Purchase / Sale Proceeds Calculation

15

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

£9,979,597.87

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Purchase / Sale Proceeds Calculation

16

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

£9,979,597.87

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Receive at maturity

Purchase / Sale Proceeds Calculation

17

www.kingandshaxson.com

Treasury Bill – Worked Example : Purchase

£ 9,979,597.87

Return is £10,000,000 - £ 9,979,597.87 = £20,402.13

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Receive at maturity

Purchase / Sale Proceeds Calculation

18

www.kingandshaxson.com

Nominal: £10m

Deal Rate: 0.41%

Trade Date: 03/02/2012

Value Date: 06/02/2012

Maturity Date: 06/08/2012

Treasury Bill – Worked Example : Purchase

£9,979,597.87

Purchase / Sale Proceeds Calculation

Return is £10,000,000 - £ 9,979,597.87 = £20,402.13

182 days

Receive at maturity

19

www.kingandshaxson.com

Certificates of Deposit (CD’s)

20

www.kingandshaxson.com

Negotiable form of deposit. Interest rate remains fixed, there is no obligation to hold to maturity.

Issued by UK and international banks and building societies on a daily basis

Same interest calculation at maturity as a fixed deposit:

Certificates of Deposit (CD’s)

Interest CalculationPrincipal x Interest Rate

36,500( ) x Number of Days

21

www.kingandshaxson.com

Secondary market access:

Ability to lend to counterparties that do not take cash in the form of fixed deposits – fulfilling unused counterparty limits.

The ability to liquidate an investment at any point;- To crystallise a capital return- Due to counterparty credit concerns- Or to raise cash – unexpected payment

Certificates of deposit (CDs)

22

www.kingandshaxson.com

Fitch Moody's S&P

Counterparty ST LT ST LT ST LT

Barclays F1 A P-1 Aa3 A-1 A+

Lloyds F1 A P1 A1 A-1 A

RBS F1 A P-1 A2 A-1 A

Rabobank F1+ AA P-1 Aaa A-1+ AA

Standard Chartered F1+ AA- P-1 A1 A-1+ AA-

Nordea Bank (Finland) F1+ AA- P-1 Aa2 A-1+ AA-

Overseas Chinese Banking Corp. F1+ AA- P-1 Aa1 A-1+ AA-

Bank of Nova Scotia F1+ AA- P-1 Aa1 A-1+ AA-

Bank of Montreal F1+ AA- P-1 Aa2 A-1 A+

National Australia Bank F1+ AA P-1 Aa2 A-1+ AA-

ING Bank F1+ A+ P-1 Aa3 A-1 A+

Ratings correct as at 6th February

2012

23

www.kingandshaxson.com

The CD market Yield Curve

00.20.4

0.60.8

11.21.4

1.61.8

2

1 week 2 week 3 week 1 month 2 month 3 month 6 month 9 month 1 year

Time

Yie

ld

Yield

The Yield Curve

24

www.kingandshaxson.com

The Yield Curve

Buy at 1.06%

The CD market Yield Curve

00.20.4

0.60.8

11.21.4

1.61.8

2

1 week 2 week 3 week 1 month 2 month 3 month 6 month 9 month 1 year

Time

Yie

ld

Yield

25

www.kingandshaxson.com

The Yield Curve – 6 weeks later

Buy at 1.06%Sell at 0.85%

The CD market Yield Curve

00.20.4

0.60.8

11.21.4

1.61.8

2

1 week 2 week 3 week 1 month 2 month 3 month 6 month 9 month 1 year

Time

Yie

ld

Yield

26

www.kingandshaxson.com

Sale Proceeds Calculation36,500 + (Issue Rate x Original No of Days)

36,500 + (Deal Rate x Days to Run)( )Nominal x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

27

www.kingandshaxson.com

Sale Proceeds Calculation36,500 + (Issue Rate x Original No of Days)

36,500 + (Deal Rate x Days to Run)( )£10m x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

28

www.kingandshaxson.com

Purchase/Sale Proceeds Calculation 36,500 + (1.06% x Original No of Days)

36,500 + (Deal Rate x Days to Run)( )£10m x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

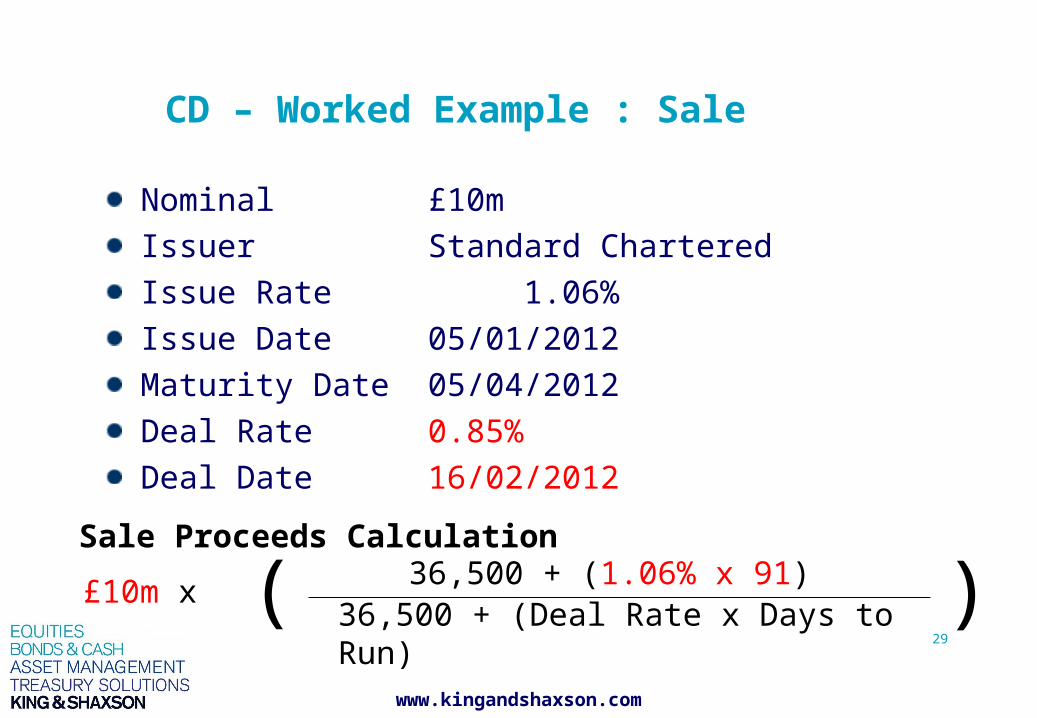

29

www.kingandshaxson.com

Sale Proceeds Calculation 36,500 + (1.06% x 91)

36,500 + (Deal Rate x Days to Run)( )£10m x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

30

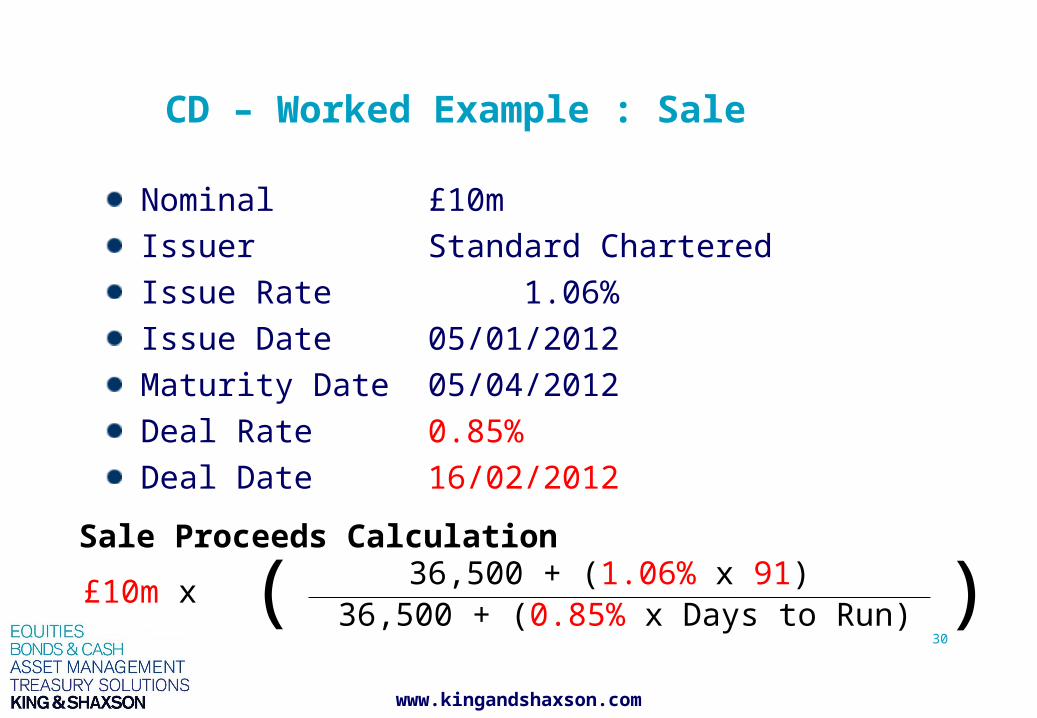

www.kingandshaxson.com

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

Sale Proceeds Calculation 36,500 + (1.06% x 91)

36,500 + (0.85% x Days to Run)( )£10m x

31

www.kingandshaxson.com

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

Sale Proceeds Calculation 36,500 + (1.06% x 91)

36,500 + (0.85% x 49)( )£10m x

32

www.kingandshaxson.com

Sale Proceeds Calculation 36,500 + (96.46)

36,500 + (41.65)(

)£10m x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

33

www.kingandshaxson.com

Sale Proceeds Calculation 36,596.46

36,541.65)( )£10m x

CD – Worked Example : Sale

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

34

www.kingandshaxson.com

Sale Proceeds Calculation

1.00149993226( )£10m x

CD – Worked Example : Sale

£10,014,999.32=

Nominal £10m

Issuer Standard Chartered

Issue Rate 1.06%

Issue Date 05/01/2012

Maturity Date05/04/2012

Deal Rate 0.85%

Deal Date 16/02/2012

35

www.kingandshaxson.com

CD – Worked Example : Summary

Purchased 05/01/2012 at 1.06%

Sold 16/02/2012 at 0.85%

Held for 42 Days

Cost £10,000,000.00

Sale proceeds £10,014,999.32

Gain £14,999.32

Return 1.30% p.a.

36

www.kingandshaxson.com

CD – Worked Example : Summary

Purchased 05/01/2012 at 1.06%

Sold 16/02/2012 at 0.85%

Held for 42 Days

Cost £10,000,000.00

Sale proceeds £10,014,999.32

Gain £14,999.32

Return 1.30% p.a.

Return = 1.30% pa for 42 days.

37

www.kingandshaxson.com

The Yield Curve – 6 weeks later

Re-invest anywhere along the curve

Reinvest at 0.68

The CD market Yield Curve

00.20.4

0.60.8

11.21.4

1.61.8

2

1 week 2 week 3 week 1 month 2 month 3 month 6 month 9 month 1 year

Time

Yie

ld

Yield

38

www.kingandshaxson.com

Conventional Fixed and Corporate

Bonds

39

www.kingandshaxson.com

Types of fixed bond:

UK Gilt: HM Treasury AAA-rated, Sterling-denominated bond.

Supranational: Joint and several liability of leading developed nations e.g. World Bank or EIB.

Corporate bond: Issued by Banks, Building Societies and Corporate institutions.

Conventional Fixed and Corporate Bonds

40

www.kingandshaxson.com

Guarantees to pay holder a coupon every 6 months until maturity on same dates each year

Fixed flow of interest income and at maturity a fixed capital repayment.

Coupon refers to the cash payment per £100 nominal that holder will receive each year.

Conventional Fixed and Corporate Bonds

41

www.kingandshaxson.com

Fixed income – accrued interest

A holder of £1,000,000 nominal of UKT 5.25% 2012:

- Receives two coupon payments of £26,250 a year on 7th March and 7th September

- Interest accrued since last interest payment date is paid in addition to the capital price.

42

www.kingandshaxson.com

Fixed income – accrued interest

UKT 5.25% 2012 example : Last coupon payment: 7th December 2011Next coupon payment: 7th June 2012

Purchased on 6th February 2012.

Accrued Interest Calculation =

Nominal x

Coupon 2

(Days in coupon period

x No of days accrued)( )

43

www.kingandshaxson.com

Fixed income – accrued interest

UKT 5.25% 2012 example : Last coupon payment: 7th December 2011

Next coupon payment: 7th June 2012

Purchased on 6th February.

Accrued Interest Calculation

£1m x

5.25%2(183

x 61)( ) = £8,750.00

183 days

61 days have accrued since 7th Dec

44

www.kingandshaxson.com

Fixed income – accrued interest

45

www.kingandshaxson.com

Corporate Bond Issues

Issuer

Rating Coupon Maturity Yield

Fitch (Fixed)

BNG (Bank Nederlandse Gementeen) AAA 2.375% 23rd Dec 2015 1.98%

UK Rail AAA 1 ¼% 22nd Jan 2015 1.10%

IBRD (The World Bank) AAA 1.125% 10th Dec 2013 0.63%

EBRD (European Bank for

Reconstruction & Development) AAA 1.875% 10th Dec 2013 0.86%

British Petroleum A 4% 29th Dec 2014 1.80%

Lloyds TSB A 6 3/8% 15th Apr 2014 4.39%

RBS A 6 3/8% 29th Apr 2014 4.30%

46

www.kingandshaxson.com

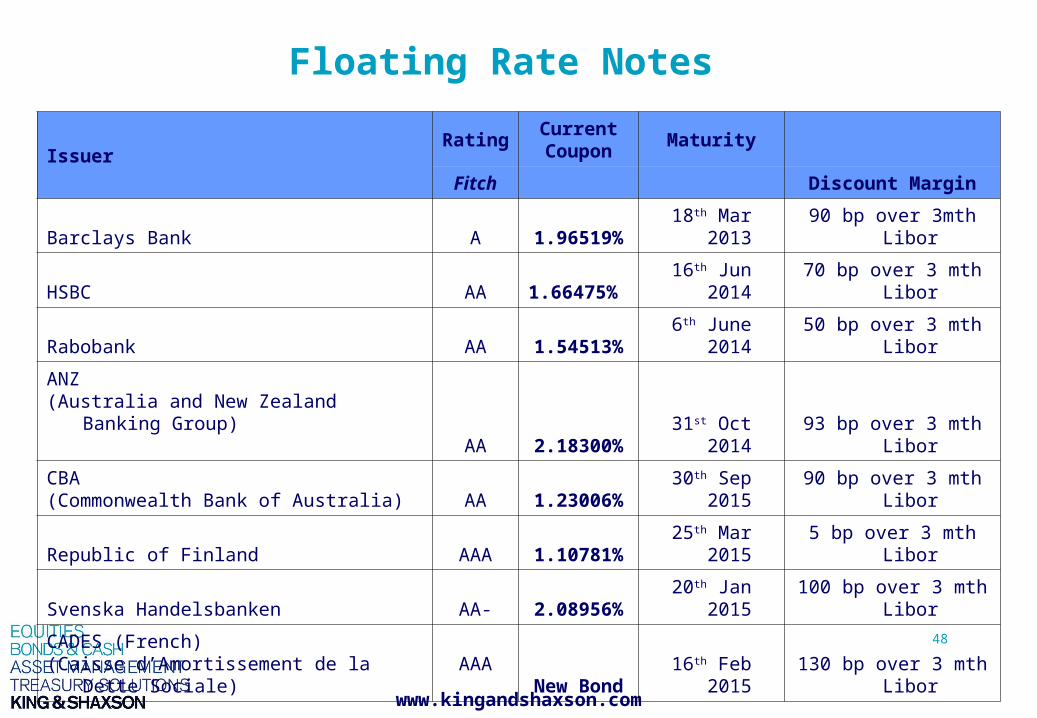

Floating Rate Notes (FRN’s)

47

www.kingandshaxson.com

FRN’s Floating Rate Notes

Dealt at a spread over LIBOR (Published after 11am by the BBA)

Re-set at a fixed margin over LIBOR every 3 months, until maturity.

E.g. The EIB 19th February 2015 FRN re-sets at +0.10% over 3 month LIBOR until maturity.

Last coupon payment: 20/02/2012

3m Libor at re-fix; 1.07081

Current coupon rate: 1.17081

Next coupon payment: 21/05/2012

3 month return.

48

www.kingandshaxson.com

Floating Rate Notes

IssuerRating

CurrentCoupon

Maturity

Fitch Discount Margin

Barclays Bank A 1.96519% 18th Mar 2013 90 bp over 3mth Libor

HSBC AA 1.66475% 16th Jun 2014 70 bp over 3 mth Libor

Rabobank AA 1.54513% 6th June 2014 50 bp over 3 mth Libor

ANZ (Australia and New Zealand Banking Group)

AA 2.18300% 31st Oct 2014 93 bp over 3 mth Libor

CBA(Commonwealth Bank of Australia) AA 1.23006% 30th Sep 2015 90 bp over 3 mth Libor

Republic of Finland AAA 1.10781% 25th Mar 2015 5 bp over 3 mth Libor

Svenska Handelsbanken AA- 2.08956% 20th Jan 2015100 bp over 3 mth

Libor

CADES (French)(Caisse d’Amortissement de la Dette Sociale)

AAA New Bond 16th Feb 2015

130 bp over 3 mth Libor

www.kingandshaxson.com

SummaryNegotiable instruments offer additional avenues of investment, including:

• Increased Liquidity

• High quality credit, without sacrificing yield

• Counterparty diversification.

www.kingandshaxson.com

Any questions?

51

www.kingandshaxson.com

Contact Details

King & Shaxson Limited5th Floor, Candlewick House120 Cannon StreetLONDON, EC4N 6AS Telephone: 020 7929 5300Fax: 020 7283 6835

Alan SimkinsTelephone: 020 7426 5966Email: [email protected]

Paul TurnerTelephone: 020 7929 8529Email: [email protected]

52

www.kingandshaxson.com

King & Shaxson Capital Limited Reg. No. 2863591and King & Shaxson Limited Reg. No. 869780, members of the London Stock Exchange, and King & Shaxson Asset Management Limited Reg. No. 3870667. The Registered Office for all companies is 6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS. All companies are registered in England and are part of the PhillipCapital Group.

King & Shaxson Capital Limited (FSA Reg. No. 169760), King & Shaxson Limited (FSA Reg. No. 179213), and King & Shaxson Asset Management Limited Reg. No. 3870667 (FSA Reg. No. 193698) are Authorised and Regulated by the Financial Services Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS.

53

www.kingandshaxson.com

Disclaimer

General

Past performance is no guarantee of future performance and the value of investments and the income from them may go down as well as up and is not guaranteed. The value of foreign currency dominated investments may be affected by exchange rates. The level of yield may be subject to fluctuation and is not guaranteed.

No Offer

The information contained in this document does not constitute and offer to buy or sell securities of any type. Nothing in this document should be construed as an offer, or the solicitation of an offer, to purchase or subscribe to sell any investment or to engage in any other transaction.

No basis for decision making

All information contained in this presentation has been prepared by King & Shaxson on the basis of publicly available information, internally developed data and other sources believed to be reliable. It is for general information purposes only and should not be considered an individualised recommendation or personalised investment, tax or legal advice. The information is subject to change without notice. Reasonable care has been taken to ensure that the materials are accurate and that the opinions stated are fair and reasonable. All opinions and estimates constitute our judgement as of the date of publication and do not constitute general or specific investment advice. All numbers are unaudited unless otherwise stated. Furthermore, please note that King & Shaxson and/or its affiliates and employees may have interests or positions in relevant securities or may have a relationship with the issuers.