wtm/rka/efd-dra-i/9-11/2016 before the securities and exchange board of ... · before the...

TRANSCRIPT

Order in the matter of Valecha Engineering Limited Page 1 of 62

WTM/RKA/EFD-DRA-I/9-11/2016

BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA

ORDER

UNDER SECTIONS 11, 11B AND 11(4) OF THE SECURITIES AND EXCHANGE

BOARD OF INDIA ACT, 1992 READ WITH REGULATION 11 OF THE SECURITIES

AND EXCHANGE BOARD OF INDIA (PROHIBITION OF FRAUDULENT AND

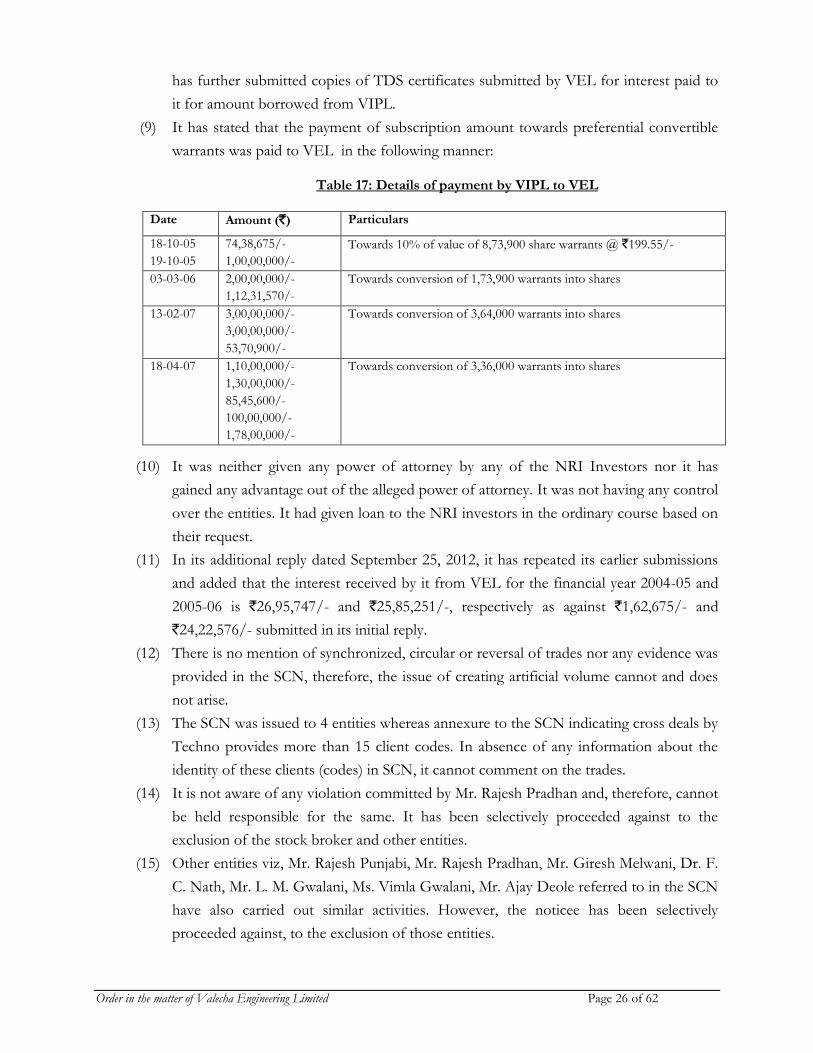

UNFAIR TRADE PRACTICES RELATING TO SECURITIES MARKET)

REGULATIONS, 2003.

In respect of:

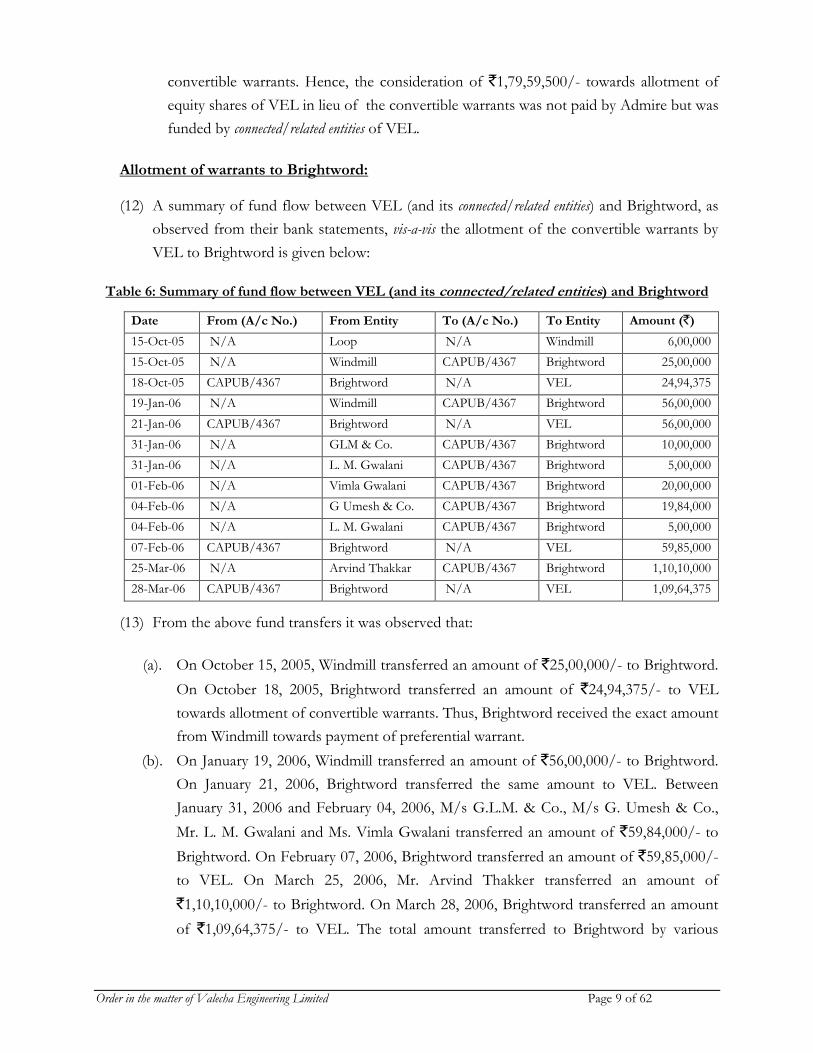

Sl. No. Name of the Noticees PAN Order Number

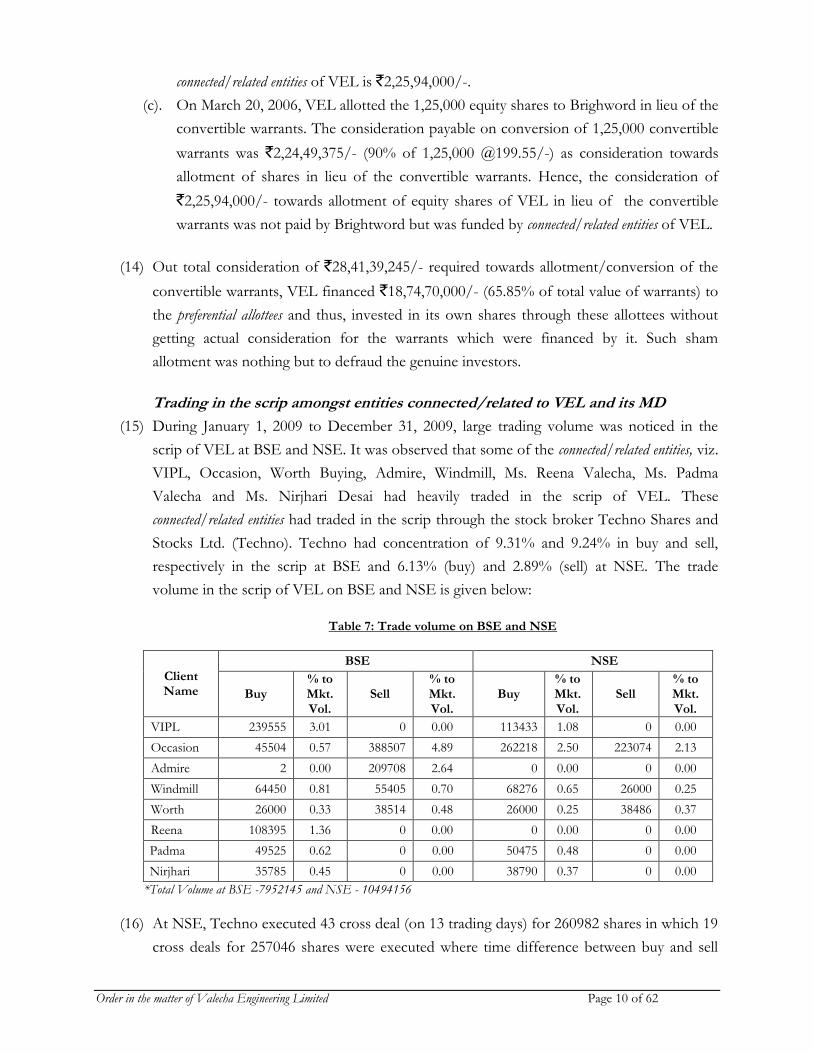

1. Valecha Engineering Limited AAACV2288G

09/2016

2. Mr. Jagdish K. Valecha AAAPV6661L

3. F2Fun & Fitness (I) Pvt. Ltd. AABCS3522M

4. Loop Engineering Consultants Pvt. Ltd. AAACL5624Q

5. Core Real Estate Pvt. Ltd. AAACC6003A

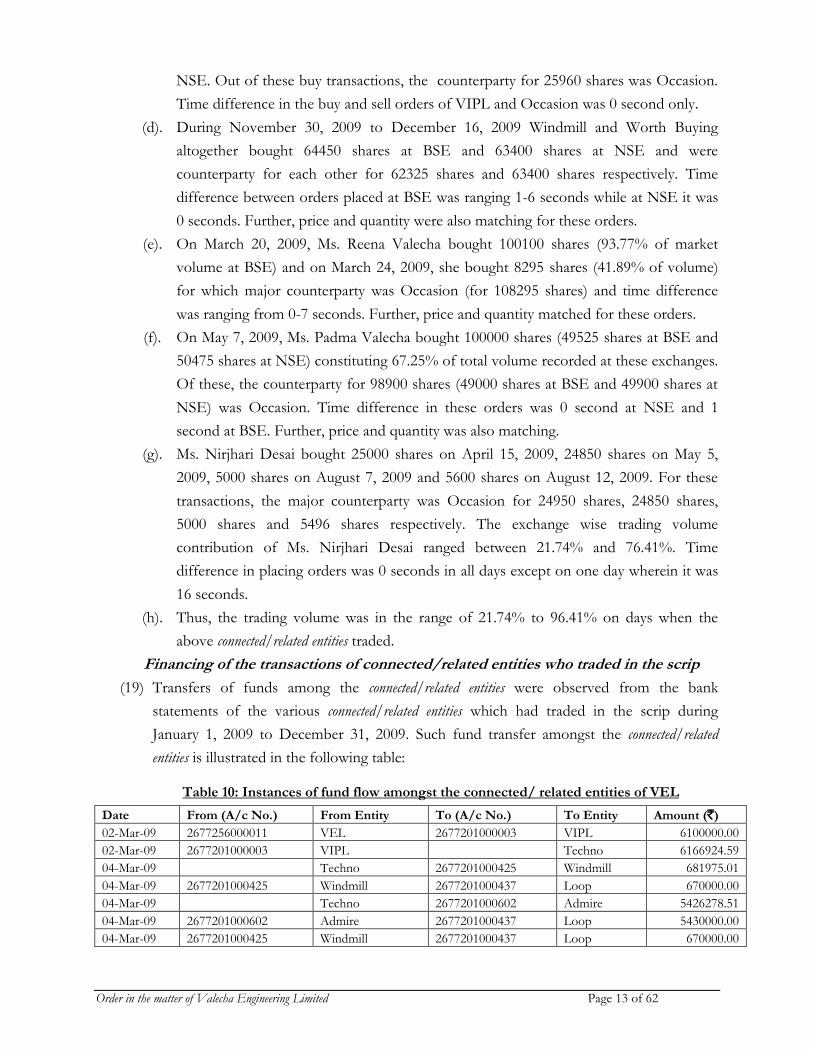

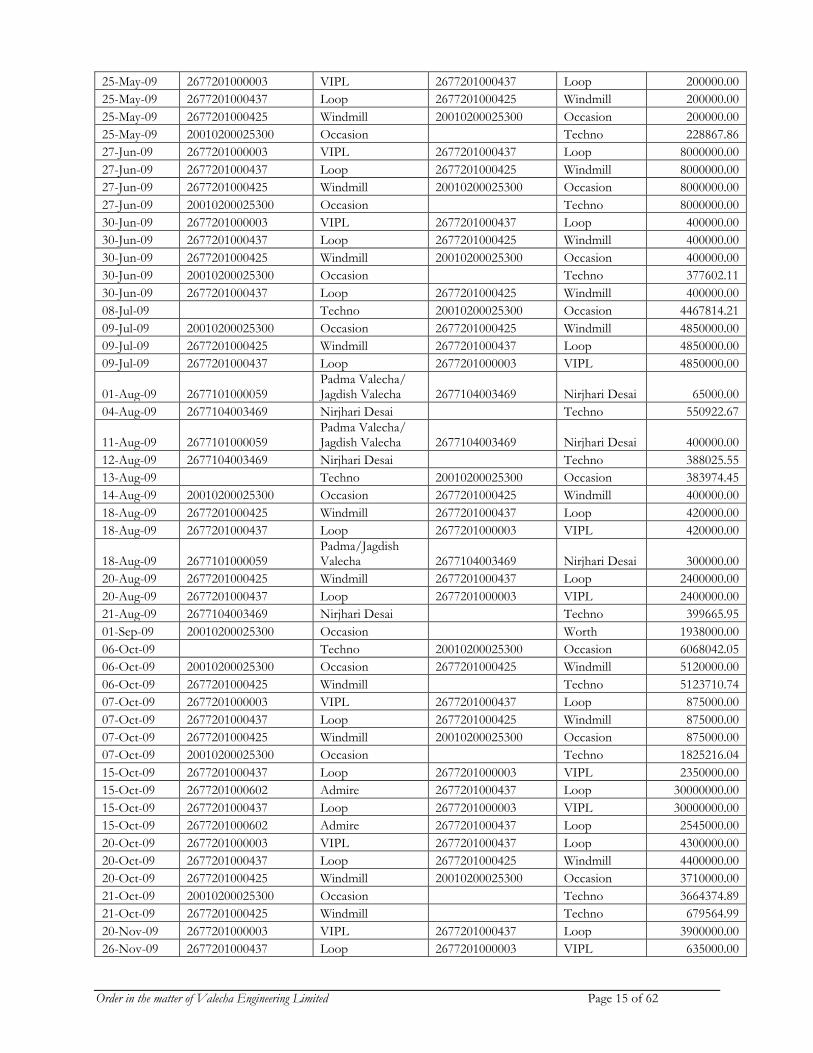

6. Brightword Consultancy Pvt. Ltd. AACCB6976B

7. Valecha Investment Private Limited AAACV2759G

10/2016

8. Occasion Impex Private Limited AABFO3272H

9. Worth Buying Trading Private Limited AAACW6052B

10. Admire Consultants Private Limited AAFCA3804N

11. Windmill Exports Pvt. Ltd. AAACW1526E

11/2016

12. Ms. Nirjhari Desai ALDPD0455A

13. Ms. Reena Valecha AACPV8423E

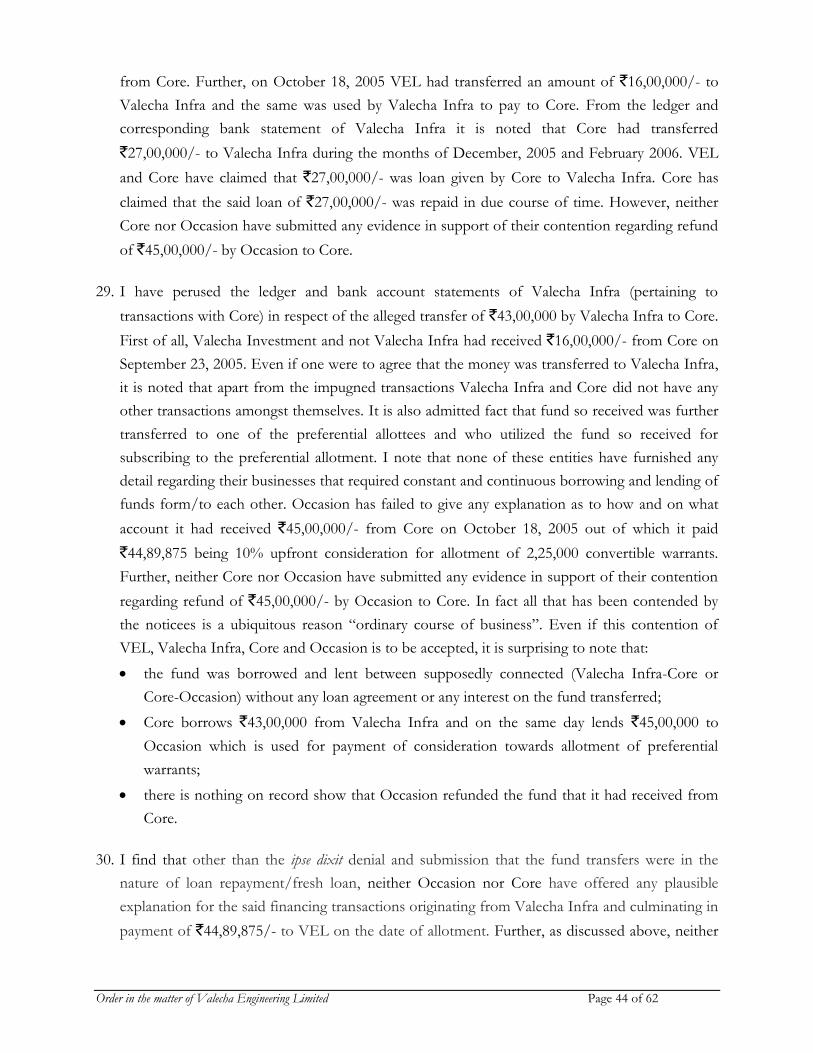

14. Ms. Padma Valecha AAFPV7356K

In the matter of dealing in the scrip of Valecha Engineering Limited Appearances for the Noticees:

Sl. No. Name of the Noticees Authorized Representative

1. Valecha Engineering Ltd. (VEL) Mr. Vinay Chouhan, Advocate

Mr. Prashant Ingle, Advocate

Ms. Kavita Valecha Sharma, Company

Secretary

2. Mr. Jagdish K. Valecha (Mr. Jagdish Valecha)

3. F2Fun & Fitness (I) Pvt. Ltd. (F2Fun)

4. Valecha Investment Private Limited (VIPL)

5. Ms. Reena Valecha

6. Ms. Padma Valecha

7. Ms. Nirjhari Desai Mr. Joby Mathew, Advocate

Mr. Runa Roy, Advocate

Order in the matter of Valecha Engineering Limited Page 2 of 62

Mr. Jinal Bhatt, Company Secretary

8. Loop Engineering Consultants Pvt. Ltd. (Loop) None

9. Core Real Estate Pvt. Ltd. (Core) None

10. Brightword Consultancy Pvt. Ltd. (Brightword) None

11. Occasion Impex Private Limited (Occasion) None

12.. Worth Buying Trading Private Limited (Worth Buying) None

13. Admire Consultants Private Limited (Admire) None

14. Windmill Export Pvt. Ltd. (Windmill) None

1. Securities and Exchange Board of India (“SEBI”) conducted investigation into the trading in the

scrip of Valecha Engineering Ltd. (hereinafter referred to as “VEL” or the company) for the

period January 1, 2009 to December 31, 2009 (hereinafter referred to as the “investigation

period”).

2. The investigation in the matter, inter alia, revealed that:

(1) On October 19, 2005 VEL had made preferential allotment of convertible warrants at the

rate of `199.55/- per warrant/share inter alia to the following entities:

Table 1: Details of allotment of convertible warrants

Name of the entities Date of incorporation No. of Warrants

VIPL 01/10/1982 8,73,900

Occasion 11/07/2005 2,25,000

Worth Buying 14/10/2005 1,00,000

Admire 21/02/2005 1,00,000

Brightword 25/02/2005 1,25,000

(2) Except VIPL, which is promoter of VEL, all the other above mentioned companies

('preferential allottees') were incorporated in the year 2005 with an authorized capital of

`1,00,000/- each. Further, these 5 companies were connected to VEL or its managing

director (MD) Mr. Jagdish Valecha and to each other through common address, common

telephone number, common directors, etc.

(3) Prior to and also after the preferential allotment, substantial funds were transferred from

VEL to the 'preferential allottees' through several 'connected entities' (who were noted to be inter se

connected amongst themselves on the basis of inter se fund transfers, common directors, etc. and also with

VEL, preferential allottees on the basis fund transfer, shareholding, promoter, etc.) and then back to

VEL. Later during 2009, substantial non- genuine trading in the scrip amongst the said

'connected entities,' 'preferential allottees' and the certain other entities connected/ related to VEL

and its MD, Mr. Jagdish Valecha was observed. Trades in the scrip were done through a

Order in the matter of Valecha Engineering Limited Page 3 of 62

common sub-broker Mr. Rajesh Pradhan, who was an employee of VEL. The basis of

connection/ relation amongst all such entities is mentioned in the following table:

Table 2: The basis of connection/relation amongst the above companies/entities

Sl. No. Name Role Key Person/Director Connection/ Relation

1 F2Fun Transferring fund

Mr. Jagdish Valecha

Promoted by Mr. Jagdish Valecha (MD of VEL), Mr. G. Ramachandran (Independent Director of VEL) and VIPL.

2 Loop Transferring fund

Mr. Hansa H Pardiwala; Mr. Mahipal Singh Pariharwala

Fund Transactions with VIPL

3 Core Transferring fund

Ms. Sujita Pradhan (w/o Mr. Rajesh Pradhan, an employee of VEL); Ms. Nirjhari Desai

Promoted by Mr. Jagdish Valecha (MD of VEL) and VIPL.

4 Brightword Allottee of convertible warrants

Ms. Sujita Pradhan; Ms. Nirjhari Desai

- Ms. Sujita Pradhan is wife of Mr. Rajesh Pradhan who is an employee of VEL. - Mr. Rajesh Pradhan, the employee of VEL traded in the scrip as sub-broker for the trades of Ms. Reena Valecha, (wife of Mr. Jagdish Valecha, the MD of VEL), Ms. Padma Valecha, mother of Mr. Jagdish Valecha and Ms. Nirjhari Desai, a friend of Mr. Jagdish Valecha who was holding her Power of Attorney - Both these directors are also directors in Admire and Windmill. - Ms. Sujita Pradhan is also a director in Occasion.

5 VIPL

Allottee of convertible warrants; traded in the scrip

Mr. Umesh Valecha Promoter of VEL

6 Occasion

Allottee of convertible warrants; traded in the scrip

Ms. Sujita Pradhan; Mr. Ajay Deole.

- Mr. Ajay Deole is common director in Worth Buying and Occasion. - Brightword and Windmill are major shareholders of Occasion. - Ms. Sujita Pradhan, wife of Mr. Rajesh Pradhan is also a director in Core, Admire, Windmill and Brightword. - Mr. Ajay Deole was an employee of F2Fun, which is promoted by VIPL and Mr. Jagdish Valecha, MD of VEL.

Order in the matter of Valecha Engineering Limited Page 4 of 62

7 Worth Buying

Allottee of convertible warrants; traded in the scrip

Mr. Ajay Deole; Mr. Anil Lulla; and Mr. Uday S Sane

- Same address as D.M. Harish & Co. (a partnership firm of Mr. Anil Harish, Chairman of VEL). - Promoters of Worth Buying viz. Mr. Anil Lulla and Mr. Uday Sane are employees of D. M. Harish & Co. - Mr. Ajay Deole was an employee of F2Fun, which is promoted by VIPL and Mr. Jagdish Valecha, MD of VEL.

8 Admire

Allottee of convertible warrants. Traded in the scrip

Ms. Sujita Pradhan and Mr. G.M. Gwalani (father-in-law of Mr. Jagdish Valecha)

- Phone number (26607476) belongs to Mr. B. L. Pradhan (father of Mr. Rajesh Pradhan who is an employee of VEL). - Ms. Sujita Pradhan, wife of Mr. Rajesh Pradhan is also a director in Occasion, Windmill and Brightword.

9 Windmill Traded in the scrip

Ms. Sujita Pradhan; Mr. G. M. Gwalani

- Common phone number (26733625) as VEL. - Common directors as Admire and Brightword.

10 Ms. Nirjhari Desai

Traded in the scrip

--

- NRI friend of Mr. Jagdish Valecha; - Gave Power of Attorney in his favour. - Received funds from Mr. Jagdish Valecha and his mother Ms. Padma Valecha - Received funds from VIPL, promoter of VEL wherein Mr. Jagdish Valecha was managing director.

11 Ms. Padma Valecha

Traded in the scrip

-- Mother of Mr. Jagdish Valecha

12 Ms. Reena Valecha

Traded in the scrip

-- Wife of Mr. Jagdish Valecha

13 Ms. Kapil Valecha

Traded in the scrip

-- Son of Mr. Jagdish Valecha

14 Mr. Karan Valecha

Traded in the scrip

-- Son of Mr. Jagdish Valecha

15 Mr. Anil Harish

Traded in the scrip

-- Chairman of VEL

16 Mr. Ratna Harish

Traded in the scrip

-- Mother of Mr. Anil Harish, Chairman of VEL.

17 Mr. Rajesh Pradhan

Traded in the scrip as sub-broker

-- Employee of VEL

Fund transfer by VEL directly and through its connected/related entities to the

preferential allottees prior to the preferential allotment and on conversion of warrants -

Allotment of warrants to VIPL: (4) A summary of fund flow between VEL and VIPL, as observed from their bank statements,

Order in the matter of Valecha Engineering Limited Page 5 of 62

vis-a-vis the allotment of the convertible warrants by VEL to VIPL is stated below:

Table 3: Summary of fund flow between VEL and VIPL

Date From (A/c) From To (A/c) To Amount (`)

17-Oct-05 2677256000011 VEL 2677201000003 VIPL 7500000

18-Oct-05 2677201000003 VIPL 2677201000603 VEL 7438675

19-Oct-05 2677256000011 VEL 2677201000003 VIPL 10000000

19-Oct-05 2677201000003 VIPL 2677201000603 VEL 10000000

03-Mar-06 2677256000011 VEL 2677201000003 VIPL 20000000

03-Mar-06 2677201000003 VIPL 2677201000603 VEL 20000000

03-Mar-06 2677256000011 VEL 2677201000003 VIPL 15000000

03-Mar-06 2677201000003 VIPL 2677201000603 VEL 11231570

13-Feb-07 2677256000011 VEL 2677201000003 VIPL 30000000

13-Feb-07 2677201000003 VIPL 2677201000603 VEL 30000000

13-Feb-07 2677256000011 VEL 2677201000003 VIPL 30000000

13-Feb-07 2677201000003 VIPL 2677201000603 VEL 30000000

13-Feb-07 2677256000011 VEL 2677201000003 VIPL 5370000

13-Feb-07 2677201000603 VIPL 2677201000603 VEL 5370900

18-Apr-07 2677256000011 VEL 2677201000437 Loop 17500000

18-Apr-07 2677201000437 Loop 2677201000003 VIPL 17900000

18-Apr-07 2677201000003 VIPL 2677201000603 VEL 11000000

18-Apr-07 2677256000011 VEL 2677201000003 VIPL 9800000

18-Apr-07 2677201000603 VIPL 2677201000603 VEL 13000000

18-Apr-07 2677201000603 VIPL 2677201000603 VEL 8545600

18-Apr-07 2677256000011 VEL 2677201000003 VIPL 10000000

18-Apr-07 2677201000603 VIPL 2677201000603 VEL 10000000

18-Apr-07 2677256000011 VEL 2677201000003 VIPL 18000000

18-Apr-07 2677201000603 VIPL 2677201000603 VEL 17800000

(5) From the above fund transfers it was observed that:

(a) Just before and on the date of preferential allotment, VIPL received an amount of

`1,75,00,000/- in two tranches from VEL (i.e., `75,00,000/- on October 17, 2005 and

`1,00,00,000/- on October 19, 2005). VIPL transferred an amount of `1,74,38,675/- in

two tranches (i.e., `74,38,675/- and `1,00,00,000/- on October 18 and 19, 2005,

respectively) to VEL towards part of consideration for allotment of convertible warrants.

(b) On March 20, 2006, upon conversion of 1,73,900 warrants (out of 8,73,900 convertible

warrants allotted to VIPL) VEL allotted equity shares to VIPL. The consideration

payable by VIPL on or prior to such allotment was `3,12,31,570/-. It was observed that

prior to such allotment of equity shares upon conversion of warrants, VEL had

transferred `2 crore to VIPL on March 03, 2006 which was transferred back to it by

VIPL on the same day. Again, on March 06, 2006 VEL had transferred `1,50,00,000/-

Order in the matter of Valecha Engineering Limited Page 6 of 62

to VIPL out of which VIPL transferred back an amount of `1,12,31,570/- to VEL on

the same day. Thus, the consideration of `3,12,31,570/-payable by VIPL for allotment

of equity shares upon conversion of 1,73,900 warrants was funded by VEL itself.

(c) On February 27, 2007, upon conversion of 3,64,000 warrants (out of the remaining

7,00,000 convertible warrants allotted to VIPL) VEL allotted equity shares to VIPL. The

consideration payable by VIPL on or before such allotment of equity shares was

`6,53,72,580/- It was observed that prior to such allotment of equity shares, VEL had

transferred `6,53,70,000/- in three tranches to VIPL on February 13, 2007 and received

back `6,53,70,900/- in three tranches from VIPL on the same day. Thus, the amount of

`6,53,70,000/- out of total consideration `6,53,72,580/-payable in lieu of 3,64,000

convertible warrants was funded by VEL itself.

(d) On April 18, 2007, upon conversion of the remaining 3,36,000 warrants allotted to VIPL

VEL allotted equity shares to VIPL. The consideration payable by VIPL on or before

such allotment of equity shares was `6,03,43,920/-. On April 18, 2007, VEL transferred

an amount of `5,57,00,000/-, including through Loop, in four tranches. On the same

day, VIPL transferred an amount of `6,03,45,600/- in five tranches to VEL. Thus, the

amount of `5,57,00,000/- out of total consideration `6,03,45,600/- payable in lieu of

3,36,000 convertible warrants was funded by VEL itself.

(e) In the above manner, VEL transferred funds amounting to `17,31,70,000/- to VIPL

(directly or indirectly) on various occasions which amounted to 99.30% of the total

consideration for 8,73,900 convertible warrants allotted to VIPL for allotment/

conversion of warrants.

Allotment of warrants to Occasion:

(6) On October 17, 2005, Valecha Infrastructure Pvt. Ltd. (Valecha Infra - a group company

of VEL) transferred an amount of `43,00,000/- to Core and Core in turn transferred

`45,00,000/- to Occasion. Occasion transferred an amount of `44,89,875/- to VEL on the

same day which was the amount payable on allotment of 2,25,000 convertible warrants by

VEL to it. Thus, the convertible warrants allotted to Occasion were not paid for by it to

the extent of `44,89,875/- but was paid by Core, a connected/related entity of VEL.

Allotment of warrants to Worth Buying: (7) A summary of fund flow between VEL (and its connected/related entities) and Worth Buying

during the relevant time, as observed from their bank statements, is given in the following

table:

Order in the matter of Valecha Engineering Limited Page 7 of 62

Table 4: Summary of fund flow between VEL (and its related entities) and Worth Buying

Date From (A/c No.) From Entity To (A/c No.) To Entity Amount (`)

18-Oct-05 N/A F2 Fun 1020110000032 Worth Buying 20,00,000

19-Oct-05 1020110000032 Worth Buying N/A VEL 19,95,500

08-May-06 N/A Anil Harish 1020110000032 Worth Buying 18,00,000

11-May-06 N/A Rajesh Punjabi 1020110000032 Worth Buying 19,10,000

11-May-06 1020110000032 Worth Buying N/A VEL 18,00,000

11-May-06 1020110000032 Worth Buying N/A VEL 19,00,000

19-Apr-07 2677256000011 VEL 2677201000437 Loop 1,43,00,000

19-Apr-07 2677201000437 Loop 1020110000032 Worth Buying 1,43,00,000

21-Apr-07 1020110000032 Worth Buying N/A VEL 1,42,59,500

(8) From the above fund transfers it was observed that:

(a). On October 18, 2005, i.e., one day before the date of preferential allotment, Worth

Buying received an amount of `20,00,000/- from F2Fun. On October 19, 2005, Worth

Buying transferred `19,95,500/-to VEL. This was exactly the amount payable towards

allotment of 1,00,000 convertible warrants to VEL by Worth Buying.

(b). On May 08, 2006, Worth Buying received `18,00,000/- from Mr. Anil Harish and on

May 11, 2006, Worth Buying received `19,10,000/- from Mr. Rajesh Punjabi. On May

11, 2006, Worth Buying transferred an amount of `37,00,000/- to VEL in two tranches.

On February 27, 2007, VEL allotted 10,000 equity shares to Worth Buying in lieu of the

convertible warrants. The consideration payable on conversion of 10,000 convertible

warrants was `17,95,950/-.

(c). On April 18, 2007, VEL allotted the 90,000 equity shares to Worth Buying in lieu of the

remaining 90,000 convertible warrants. On April 19, 2007, VEL transferred an amount

of `1,43,00,000/- to Loop and on the same day Loop transferred the same amount to

Worth Buying. On April 21, 2007, Worth Buying transferred `1,42,59,500/- to VEL.

The consideration payable on conversion of 90,000 convertible warrants was

`1,61,63,550/- as consideration towards balance and full payment for allotment of shares

in lieu of the convertible warrants.

(9) Hence, the consideration of `1,42,59,500/- towards allotment of equity shares of VEL in

lieu of the convertible warrants allotted to Worth Buying was not paid by Worth Buying.

Thus, an amount of `1,43,00,000/- (71.52% of the total value of convertible warrants) was

financed by VEL to Worth Buying, whereas an amount of `38,00,000/- (19% of total value

of warrant) was arranged by the entities related to VEL. Therefore, more than 90% of

value of warrants issued to Worth Buying were financed by VEL and/or its connected/related

entities.

Order in the matter of Valecha Engineering Limited Page 8 of 62

Allotment of warrants to Admire:

(10) A summary of fund flow between VEL (and its connected/related entities) during the relevant

time, as noticed from their bank statements, is stated below:

Table 5: Summary of fund flow between the related entities of VEL and Admire

Date From (A/c No.) From Entity To (A/c No.) To Entity Amount (`)

17-Oct-05 CA-437 Loop 2677201000602 Admire 2000000

18-Oct-05 2677201000602 Admire VEL 1995500

12-Dec-05 Giresh Melwani 2677201000602 Admire 9922624

12-Dec-05 2677201000602 Admire VEL 9922624

07-Jan-06 CA-437 Loop 3067 F. C. Nath 1750000

07-Jan-06 3067 F. C. Nath 2677201000602 Admire 1750000

07-Jan-06 2677201000602 Admire VEL 1750000

12-Jan-06 CA-437 Loop 3067 F. C. Nath 2050000

12-Jan-06 3067 F. C. Nath 2677201000602 Admire 2050000

12-Jan-06 2677201000602 Admire VEL 2050000

16-Jan-06 CA-437 Loop 3067 F. C. Nath 1600000

16-Jan-06 3067 F. C. Nath 2677201000602 Admire 6200000

16-Jan-06 2677201000602 Admire VEL 4182000

23-Jan-06 Giresh Melwani 2677201000602 Admire 54876

25-Jan-06 2677201000602 Admire VEL 54876

(11) From the table above fund transfers it was observed that:

(a). On October 17, 2005, Loop transferred an amount of `20,00,000/- to Admire and

Admire in turn transferred `19,95,500/- to VEL on October 18, 2005. The total

consideration payable on preferential warrants was `19,95,500/-. Thus, Admire received

the exact amount from Loop towards payment of preferential warrant.

(b). Mr. Giresh Melwani (NRI investor in Admire personally known to Mr. Jagdish Valecha,

MD of VEL) transferred an amount of `99,77,500/- in two tranches (`99,22,624/- on

December 12, 2005 and `54,876/- on January 23, 2006) to Admire and Admire in turn

transferred the said amount to VEL.

(c). Loop transferred an amount of `54,00,000/- in three tranches to Dr. F. C. Nath who in

turn transferred `1,00,00,000/- to Admire.

(d). Admire transferred `79,82,000/- to VEL in three tranches as consideration towards

allotment of shares in lieu of the convertible warrants.

(e). The total consideration payable on conversion of 1,00,000 warrants was `1,79,59,500/-

(90% of 1,00,000 @199.55/-). The total amount transferred to Admire by various

connected/related entities of VEL is `1,79,59,500/-.

(f). On March 20, 2006, VEL allotted the 1,00,000 equity shares to Admire in lieu of the

Order in the matter of Valecha Engineering Limited Page 9 of 62

convertible warrants. Hence, the consideration of `1,79,59,500/- towards allotment of

equity shares of VEL in lieu of the convertible warrants was not paid by Admire but was

funded by connected/related entities of VEL.

Allotment of warrants to Brightword: (12) A summary of fund flow between VEL (and its connected/related entities) and Brightword, as

observed from their bank statements, vis-a-vis the allotment of the convertible warrants by

VEL to Brightword is given below:

Table 6: Summary of fund flow between VEL (and its connected/related entities) and Brightword

Date From (A/c No.) From Entity To (A/c No.) To Entity Amount (`)

15-Oct-05 N/A Loop N/A Windmill 6,00,000

15-Oct-05 N/A Windmill CAPUB/4367 Brightword 25,00,000

18-Oct-05 CAPUB/4367 Brightword N/A VEL 24,94,375

19-Jan-06 N/A Windmill CAPUB/4367 Brightword 56,00,000

21-Jan-06 CAPUB/4367 Brightword N/A VEL 56,00,000

31-Jan-06 N/A GLM & Co. CAPUB/4367 Brightword 10,00,000

31-Jan-06 N/A L. M. Gwalani CAPUB/4367 Brightword 5,00,000

01-Feb-06 N/A Vimla Gwalani CAPUB/4367 Brightword 20,00,000

04-Feb-06 N/A G Umesh & Co. CAPUB/4367 Brightword 19,84,000

04-Feb-06 N/A L. M. Gwalani CAPUB/4367 Brightword 5,00,000

07-Feb-06 CAPUB/4367 Brightword N/A VEL 59,85,000

25-Mar-06 N/A Arvind Thakkar CAPUB/4367 Brightword 1,10,10,000

28-Mar-06 CAPUB/4367 Brightword N/A VEL 1,09,64,375

(13) From the above fund transfers it was observed that:

(a). On October 15, 2005, Windmill transferred an amount of `25,00,000/- to Brightword.

On October 18, 2005, Brightword transferred an amount of `24,94,375/- to VEL

towards allotment of convertible warrants. Thus, Brightword received the exact amount

from Windmill towards payment of preferential warrant.

(b). On January 19, 2006, Windmill transferred an amount of `56,00,000/- to Brightword.

On January 21, 2006, Brightword transferred the same amount to VEL. Between

January 31, 2006 and February 04, 2006, M/s G.L.M. & Co., M/s G. Umesh & Co.,

Mr. L. M. Gwalani and Ms. Vimla Gwalani transferred an amount of `59,84,000/- to

Brightword. On February 07, 2006, Brightword transferred an amount of `59,85,000/-

to VEL. On March 25, 2006, Mr. Arvind Thakker transferred an amount of

`1,10,10,000/- to Brightword. On March 28, 2006, Brightword transferred an amount

of `1,09,64,375/- to VEL. The total amount transferred to Brightword by various

Order in the matter of Valecha Engineering Limited Page 10 of 62

connected/related entities of VEL is `2,25,94,000/-.

(c). On March 20, 2006, VEL allotted the 1,25,000 equity shares to Brighword in lieu of the

convertible warrants. The consideration payable on conversion of 1,25,000 convertible

warrants was `2,24,49,375/- (90% of 1,25,000 @199.55/-) as consideration towards

allotment of shares in lieu of the convertible warrants. Hence, the consideration of

`2,25,94,000/- towards allotment of equity shares of VEL in lieu of the convertible

warrants was not paid by Brightword but was funded by connected/related entities of VEL.

(14) Out total consideration of `28,41,39,245/- required towards allotment/conversion of the

convertible warrants, VEL financed `18,74,70,000/- (65.85% of total value of warrants) to

the preferential allottees and thus, invested in its own shares through these allottees without

getting actual consideration for the warrants which were financed by it. Such sham

allotment was nothing but to defraud the genuine investors.

Trading in the scrip amongst entities connected/related to VEL and its MD

(15) During January 1, 2009 to December 31, 2009, large trading volume was noticed in the

scrip of VEL at BSE and NSE. It was observed that some of the connected/related entities, viz.

VIPL, Occasion, Worth Buying, Admire, Windmill, Ms. Reena Valecha, Ms. Padma

Valecha and Ms. Nirjhari Desai had heavily traded in the scrip of VEL. These

connected/related entities had traded in the scrip through the stock broker Techno Shares and

Stocks Ltd. (Techno). Techno had concentration of 9.31% and 9.24% in buy and sell,

respectively in the scrip at BSE and 6.13% (buy) and 2.89% (sell) at NSE. The trade

volume in the scrip of VEL on BSE and NSE is given below:

Table 7: Trade volume on BSE and NSE

Client Name

BSE NSE

Buy % to Mkt. Vol.

Sell % to Mkt. Vol.

Buy % to Mkt. Vol.

Sell % to Mkt. Vol.

VIPL 239555 3.01 0 0.00 113433 1.08 0 0.00

Occasion 45504 0.57 388507 4.89 262218 2.50 223074 2.13

Admire 2 0.00 209708 2.64 0 0.00 0 0.00

Windmill 64450 0.81 55405 0.70 68276 0.65 26000 0.25

Worth 26000 0.33 38514 0.48 26000 0.25 38486 0.37

Reena 108395 1.36 0 0.00 0 0.00 0 0.00

Padma 49525 0.62 0 0.00 50475 0.48 0 0.00

Nirjhari 35785 0.45 0 0.00 38790 0.37 0 0.00

*Total Volume at BSE -7952145 and NSE - 10494156

(16) At NSE, Techno executed 43 cross deal (on 13 trading days) for 260982 shares in which 19

cross deals for 257046 shares were executed where time difference between buy and sell

Order in the matter of Valecha Engineering Limited Page 11 of 62

orders ranged between 0-38 seconds only.

(17) The details of the cross deals among VIPL, Admire, Occasion, Worth Buying, Windmill,

Ms. Nirjhari Desai, Ms. Padma Valecha and Ms. Reena Valecha and other connected/related

entities of VEL are given below at Tables-8 and 9 for BSE and NSE, respectively:

Table 8: Cross deals by the noticees on BSE

Trade Date

Trade Quantity

Buy Order Time

Buy Client Code

Buy Client PAN

Sell Order Time

Sell Client Code

Sell Client PAN Time Difference

27-02-09 209704 15:10:25 V0857 AAACV2759G 15:10:24 A498 AAFCA3804N 0:00:01

27-02-09 26054 15:11:44 V0857 AAACV2759G 15:11:43 W0010 AAACW1526E 0:00:01

27-02-09 100 15:11:44 V0857 AAACV2759G 15:11:51 W0010 AAACW1526E 0:00:07

20-03-09 99900 9:55:11 R2094 AACPV8423E 9:55:11 O017 AABFO3272H 0:00:00

20-03-09 100 9:55:11 R2094 AACPV8423E 9:55:18 O017 AABFO3272H 0:00:07

24-03-09 8295 9:55:06 R2094 AACPV8423E 9:55:03 O017 AABFO3272H 0:00:03

25-03-09 64385 9:55:03 K1513 AEEPV8425N 9:55:03 O017 AABFO3272H 0:00:00

25-03-09 64500 9:55:38 K1121 ADMPV1447K 9:55:38 O017 AABFO3272H 0:00:00

15-04-09 24950 10:13:17 N396 ALDPD0455A 10:13:17 O017 AABFO3272H 0:00:00

22-04-09 25 9:56:09 R476 AOHPK0343M 14:41:14 O017 AABFO3272H 4:45:05

22-04-09 25 9:56:11 A297 AEXPK3543D 14:41:14 O017 AABFO3272H 4:45:03

22-04-09 25 9:56:07 K1473 AYYPS2012C 14:41:14 O017 AABFO3272H 4:45:07

07-05-09 49000 15:18:39 P1808 AAFPV7356K 15:18:40 O017 AABFO3272H 0:00:01

12-05-09 46 10:14:18 N396 ALDPD0455A 10:34:54 N0382 AACPP2588E 0:20:36

12-08-09 5496 14:17:56 N396 ALDPD0455A 14:17:40 O017 AABFO3272H 0:00:16

23-09-09 193 15:01:18 O017 AABFO3272H 13:42:59 P1210 ADCPV3079R 1:18:19

23-09-09 507 15:01:45 O017 AABFO3272H 13:42:59 P1210 ADCPV3079R 1:18:46

30-09-09 24400 9:55:05 W0010 AAACW1526E 9:55:02 O017 AABFO3272H 0:00:03

30-09-09 600 14:37:54 T093 AACCT3286G 9:55:02 O017 AABFO3272H 4:42:52

01-12-09 9950 9:55:04 W0010 AAACW1526E 9:55:10 W011 AAACW6052B 0:00:06

07-12-09 10700 9:55:08 W011 AAACW6052B 9:55:05 W0010 AAACW1526E 0:00:03

10-12-09 14675 9:55:07 W011 AAACW6052B 9:55:10 W0010 AAACW1526E 0:00:03

14-12-09 25000 9:55:06 W0010 AAACW1526E 9:55:05 W011 AAACW6052B 0:00:01

16-12-09 2000 11:16:08 W0010 AAACW1526E 11:16:10 W011 AAACW6052B 0:00:02

*Client codes: C0361- Core; L0711 – Loop; V1370 – VEL; V0857- VIPL; W0010- Windmill; W011- Worth Buying; O017 – Occasion; B1195 – Brightword; R2094 - Reena Valecha; A498 – Admire; P1808 - Padma Valecha; N396 – Nirjhari Desai; K1513 - Kapil Valecha

Table 9: Cross deals by the noticees on NSE

Trade

Date

Trade

d

Quant

ity

Buy

Order

Time

Buy

Client

Code

Buy Client

PAN

Sell Order

Time

Sell Client

Code

Sell Client PAN Time

Differenc

e

24-03-09 29000 10:56:51 K1121 ADMPV1447K 10:57:13 O017 AABFO3272H 00:00:22

24-03-09 27085 10:57:03 K1513 AEEPV8425N 10:57:13 O017 AABFO3272H 00:00:10

24-03-09 1915 10:57:03 K1513 AEEPV8425N 10:58:14 O017 AABFO3272H 00:01:11

22-04-09 25960 10:12:55 V0857 AAACV2759G 10:12:56 O017 AABFO3272H 00:00:01

05-05-09 2500 10:02:32 N396 ALDPD0455A 10:02:33 O017 AABFO3272H 00:00:01

05-05-09 22350 10:02:32 N396 ALDPD0455A 10:02:33 O017 AABFO3272H 00:00:01

07-05-09 5000 15:20:17 P1808 AAFPV7356K 15:20:18 O017 AABFO3272H 00:00:01

07-05-09 5000 15:20:17 P1808 AAFPV7356K 15:20:18 O017 AABFO3272H 00:00:01

07-05-09 5000 15:20:17 P1808 AAFPV7356K 15:20:18 O017 AABFO3272H 00:00:01

07-05-09 5000 15:20:17 P1808 AAFPV7356K 15:20:18 O017 AABFO3272H 00:00:01

07-05-09 29900 15:20:17 P1808 AAFPV7356K 15:20:18 O017 AABFO3272H 00:00:01

Order in the matter of Valecha Engineering Limited Page 12 of 62

07-08-09 5000 12:31:10 N396 ALDPD0455A 12:31:02 O017 AABFO3272H 00:00:08

29-09-09 420 15:26:48 O017 AABFO3272H 15:25:43 K1473 AYYPS2012C 00:01:05

30-09-09 24975 09:55:11 W0010 AAACW1526E 09:55:11 O017 AABFO3272H 00:00:00

30-09-09 1 14:38:00 T093 AACCT3286G 09:55:11 O017 AABFO3272H 04:42:49

15-10-09 100 14:07:26 O017 AABFO3272H 13:25:34 T108 ALTPB8351R 00:41:52

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 1000 14:19:15 O017 AABFO3272H 14:18:42 P1410 AACPD6288K 00:00:33

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 101 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 50 14:19:15 O017 AABFO3272H 14:17:46 S4177 ATLPP4298B 00:01:29

15-10-09 91 14:19:15 O017 AABFO3272H 14:17:59 P1210 ADCPV3079R 00:01:16

15-10-09 5876 15:27:18 W0010 AAACW1526E 15:27:56 O017 AABFO3272H 00:00:38

30-11-09 2500 15:11:59 W0010 AAACW1526E 15:11:44 W011 AAACW6052B 00:00:15

03-12-09 9900 09:55:06 W0010 AAACW1526E 09:55:08 W011 AAACW6052B 00:00:02

07-12-09 11000 09:55:05 W011 AAACW6052B 09:55:05 W0010 AAACW1526E 00:00:00

10-12-09 15000 09:55:06 W011 AAACW6052B 09:55:06 W0010 AAACW1526E 00:00:00

14-12-09 25000 09:55:05 W0010 AAACW1526E 09:55:05 W011 AAACW6052B 00:00:00

(18) From the tables above, it is observed that:

(a). VIPL, Occasion, Admire and Worth Buying entered into negotiated deals on 15 trading

days on BSE, wherein VIPL traded on 1 day, Occasion traded on 8 days, Admire

traded on 1 day and Worth Buying on 5 days. Similarly, on NSE, VIPL, Occasion, and

Worth Buying had entered into negotiated deals on 13 trading days wherein VIPL

traded on 1 day, Occasion traded on 8 days and Worth Buying traded on 5 days.

(b). Ms. Nirjhari Desai, Ms. Reena Valecha, Ms. Padma Valecha and Windmill entered into

negotiated deals on 13 trading days on BSE, wherein Ms. Nirjhari Desai entered on 3

days, Ms. Reena Valecha on 2 days, Ms. Padma Valecha on 1 day and Windmill on 7

days. Similarly, on NSE these noticees entered into negotiated deals on 10 trading days

wherein Ms. Nirjhari Desai entered on 2 days, Ms. Padma Valecha on 1 day and

Windmill on 7 days.

(c). On February 27, 2009, VIPL bought 235860 shares (96.41% of market volume) at

BSE. Of these buy transactions of VIPL, counterparties in respect of 2,35,858 shares of

VEL were Admire (209704 shares) and Windmill (26154 shares). Time difference in the

buy and sell orders in their transactions was between 1-7 second only with the

matching price and quantity. On April 22, 2009, VIPL bought 26020 shares of VEL at

Order in the matter of Valecha Engineering Limited Page 13 of 62

NSE. Out of these buy transactions, the counterparty for 25960 shares was Occasion.

Time difference in the buy and sell orders of VIPL and Occasion was 0 second only.

(d). During November 30, 2009 to December 16, 2009 Windmill and Worth Buying

altogether bought 64450 shares at BSE and 63400 shares at NSE and were

counterparty for each other for 62325 shares and 63400 shares respectively. Time

difference between orders placed at BSE was ranging 1-6 seconds while at NSE it was

0 seconds. Further, price and quantity were also matching for these orders.

(e). On March 20, 2009, Ms. Reena Valecha bought 100100 shares (93.77% of market

volume at BSE) and on March 24, 2009, she bought 8295 shares (41.89% of volume)

for which major counterparty was Occasion (for 108295 shares) and time difference

was ranging from 0-7 seconds. Further, price and quantity matched for these orders.

(f). On May 7, 2009, Ms. Padma Valecha bought 100000 shares (49525 shares at BSE and

50475 shares at NSE) constituting 67.25% of total volume recorded at these exchanges.

Of these, the counterparty for 98900 shares (49000 shares at BSE and 49900 shares at

NSE) was Occasion. Time difference in these orders was 0 second at NSE and 1

second at BSE. Further, price and quantity was also matching.

(g). Ms. Nirjhari Desai bought 25000 shares on April 15, 2009, 24850 shares on May 5,

2009, 5000 shares on August 7, 2009 and 5600 shares on August 12, 2009. For these

transactions, the major counterparty was Occasion for 24950 shares, 24850 shares,

5000 shares and 5496 shares respectively. The exchange wise trading volume

contribution of Ms. Nirjhari Desai ranged between 21.74% and 76.41%. Time

difference in placing orders was 0 seconds in all days except on one day wherein it was

16 seconds.

(h). Thus, the trading volume was in the range of 21.74% to 96.41% on days when the

above connected/related entities traded.

Financing of the transactions of connected/related entities who traded in the scrip

(19) Transfers of funds among the connected/related entities were observed from the bank

statements of the various connected/related entities which had traded in the scrip during

January 1, 2009 to December 31, 2009. Such fund transfer amongst the connected/related

entities is illustrated in the following table:

Table 10: Instances of fund flow amongst the connected/ related entities of VEL

Date From (A/c No.) From Entity To (A/c No.) To Entity Amount (`)

02-Mar-09 2677256000011 VEL 2677201000003 VIPL 6100000.00

02-Mar-09 2677201000003 VIPL Techno 6166924.59

04-Mar-09 Techno 2677201000425 Windmill 681975.01

04-Mar-09 2677201000425 Windmill 2677201000437 Loop 670000.00

04-Mar-09 Techno 2677201000602 Admire 5426278.51

04-Mar-09 2677201000602 Admire 2677201000437 Loop 5430000.00

04-Mar-09 2677201000425 Windmill 2677201000437 Loop 670000.00

Order in the matter of Valecha Engineering Limited Page 14 of 62

04-Mar-09 2677201000437 Loop 2677201000003 VIPL 6100000.00

04-Mar-09 2677201000602 Admire 2677201000437 Loop 3100000.00

04-Mar-09 2677201000437 Loop 2677201000425 Windmill 3100000.00

04-Mar-09 2677201000425 Windmill 2677201000602 Admire 3100000.00

24-Mar-09 Techno 20010200025300 Occasion 2300754.07

25-Mar-09 20010200025300 Occasion 2677201000425 Windmill 2300000.00

25-Mar-09 2677201000425 Windmill 2677201000437 Loop 2300000.00

25-Mar-09 2677201000437 Loop 2677201000003 VIPL 2300000.00

26-Mar-09 Techno 20010200025300 Occasion 1680268.08

26-Mar-09 20010200025300 Occasion 2677201000425 Windmill 1680000.00

28-Mar-09 2677201000425 Windmill 2677201000437 Loop 1680000.00

28-Mar-09 2677201000437 Loop 2677201000003 VIPL 1680000.00

30-Mar-09 Techno 20010200025300 Occasion 3045812.25

31-Mar-09 20010200025300 Occasion 2677201000425 Windmill 3045000.00

31-Mar-09 2677201000425 Windmill 2677201000437 Loop 3040000.00

31-Mar-09 2677201000437 Loop 2677201000003 VIPL 3040000.00

02-Apr-09 2677201000003 VIPL 2677201000437 Loop 6000000.00

02-Apr-09 2677201000437 Loop 2677201000425 Windmill 6000000.00

02-Apr-09 2677201000425 Windmill 20010200025300 Occasion 6000000.00

02-Apr-09 20010200025300 Occasion Techno 6000000.00

11-Apr-09 20010200025300 Occasion Techno 10933.17

13-Apr-09 Techno 20010200025300 Occasion 377539.50

16-Apr-09 20010200025300 Occasion 2677201000425 Windmill 375000.00

17-Apr-09 2677201000425 Windmill 2677201000437 Loop 375000.00

17-Apr-09 2677201000437 Loop 2677201000003 VIPL 375000.00

17-Apr-09 2677201000003 VIPL 2677104003469 Nirjhari Desai 1000000.00

18/Apr/09 2677104003469 Nirjhari Desai Techno 1005236.60

18-Apr-09 Techno 20010200025300 Occasion 994738.40

21-Apr-09 20010200025300 Occasion 2677201000425 Windmill 1000000.00

21-Apr-09 2677201000425 Windmill 2677201000437 Loop 1000000.00

21-Apr-09 2677201000437 Loop 2677201000003 VIPL 1000000.00

22-Apr-09 2677256000011 VEL 2677201000003 VIPL 2300000.00

22-Apr-09 2677201000003 VIPL RTGS Techno 3600000.00

24-Apr-09 Techno 20010200025300 Occasion 1557526.12

24-Apr-09 20010200025300 Occasion 2677201000425 Windmill 1550000.00

24-Apr-09 2677201000425 Windmill 2677201000437 Loop 1550000.00

25-Apr-09 2677201000437 Loop 2677201000003 VIPL 1550000.00

25-Apr-09 2677201000003 VIPL RTGS Techno 1051796.45

02-May-09 2677201000003 VIPL 2677104003469 Nirjhari Desai 1130000.00

08-May-09 Techno 20010200025300 Occasion 959884.73

08-May-09 20010200025300 Occasion 2677201000425 Windmill 960000.00

08-May-09 2677201000425 Windmill 2677201000437 Loop 950000.00

08-May-09 2677201000437 Loop 2677201000003 VIPL 950000.00

08-May-09 2677104003469 Nirjhari Desai Techno 964379.29

08-May-09 2677201000003 VIPL 2677104003469 Nirjhari Desai 600000.00

11-May-09 Techno 20010200025300 Occasion 3970919.12

13-May-09 20010200025300 Occasion 2677201000425 Windmill 3970000.00

13-May-09 2677201000425 Windmill 2677201000437 Loop 3970000.00

13-May-09 2677201000437 Loop 2677201000003 VIPL 3970000.00

20-May-09 2677104003469 Nirjhari Desai Techno 311058.09

Order in the matter of Valecha Engineering Limited Page 15 of 62

25-May-09 2677201000003 VIPL 2677201000437 Loop 200000.00

25-May-09 2677201000437 Loop 2677201000425 Windmill 200000.00

25-May-09 2677201000425 Windmill 20010200025300 Occasion 200000.00

25-May-09 20010200025300 Occasion Techno 228867.86

27-Jun-09 2677201000003 VIPL 2677201000437 Loop 8000000.00

27-Jun-09 2677201000437 Loop 2677201000425 Windmill 8000000.00

27-Jun-09 2677201000425 Windmill 20010200025300 Occasion 8000000.00

27-Jun-09 20010200025300 Occasion Techno 8000000.00

30-Jun-09 2677201000003 VIPL 2677201000437 Loop 400000.00

30-Jun-09 2677201000437 Loop 2677201000425 Windmill 400000.00

30-Jun-09 2677201000425 Windmill 20010200025300 Occasion 400000.00

30-Jun-09 20010200025300 Occasion Techno 377602.11

30-Jun-09 2677201000437 Loop 2677201000425 Windmill 400000.00

08-Jul-09 Techno 20010200025300 Occasion 4467814.21

09-Jul-09 20010200025300 Occasion 2677201000425 Windmill 4850000.00

09-Jul-09 2677201000425 Windmill 2677201000437 Loop 4850000.00

09-Jul-09 2677201000437 Loop 2677201000003 VIPL 4850000.00

01-Aug-09 2677101000059 Padma Valecha/ Jagdish Valecha 2677104003469 Nirjhari Desai 65000.00

04-Aug-09 2677104003469 Nirjhari Desai Techno 550922.67

11-Aug-09 2677101000059 Padma Valecha/ Jagdish Valecha 2677104003469 Nirjhari Desai 400000.00

12-Aug-09 2677104003469 Nirjhari Desai Techno 388025.55

13-Aug-09 Techno 20010200025300 Occasion 383974.45

14-Aug-09 20010200025300 Occasion 2677201000425 Windmill 400000.00

18-Aug-09 2677201000425 Windmill 2677201000437 Loop 420000.00

18-Aug-09 2677201000437 Loop 2677201000003 VIPL 420000.00

18-Aug-09 2677101000059 Padma/Jagdish Valecha 2677104003469 Nirjhari Desai 300000.00

20-Aug-09 2677201000425 Windmill 2677201000437 Loop 2400000.00

20-Aug-09 2677201000437 Loop 2677201000003 VIPL 2400000.00

21-Aug-09 2677104003469 Nirjhari Desai Techno 399665.95

01-Sep-09 20010200025300 Occasion Worth 1938000.00

06-Oct-09 Techno 20010200025300 Occasion 6068042.05

06-Oct-09 20010200025300 Occasion 2677201000425 Windmill 5120000.00

06-Oct-09 2677201000425 Windmill Techno 5123710.74

07-Oct-09 2677201000003 VIPL 2677201000437 Loop 875000.00

07-Oct-09 2677201000437 Loop 2677201000425 Windmill 875000.00

07-Oct-09 2677201000425 Windmill 20010200025300 Occasion 875000.00

07-Oct-09 20010200025300 Occasion Techno 1825216.04

15-Oct-09 2677201000437 Loop 2677201000003 VIPL 2350000.00

15-Oct-09 2677201000602 Admire 2677201000437 Loop 30000000.00

15-Oct-09 2677201000437 Loop 2677201000003 VIPL 30000000.00

15-Oct-09 2677201000602 Admire 2677201000437 Loop 2545000.00

20-Oct-09 2677201000003 VIPL 2677201000437 Loop 4300000.00

20-Oct-09 2677201000437 Loop 2677201000425 Windmill 4400000.00

20-Oct-09 2677201000425 Windmill 20010200025300 Occasion 3710000.00

21-Oct-09 20010200025300 Occasion Techno 3664374.89

21-Oct-09 2677201000425 Windmill Techno 679564.99

20-Nov-09 2677201000003 VIPL 2677201000437 Loop 3900000.00

26-Nov-09 2677201000437 Loop 2677201000003 VIPL 635000.00

Order in the matter of Valecha Engineering Limited Page 16 of 62

02-Dec-09 Techno 2677201000425 Windmill 444773.55

08-Dec-09 Techno 20010200025300 Occasion 2407862.27

15-Dec-09 20010200025300 Occasion 2677201000425 Windmill 2135000.00

16-Dec-09 2677201000425 Windmill 2677201000437 Loop 1850000.00

16-Dec-09 2677201000437 Loop 2677201000003 VIPL 7875000.00

24-Dec-09 2677201000425 Windmill Techno 400000.00

(20) From the above fund transfers it was observed that:

(a). On March 2, 2009 VIPL received `61,00,000/- from VEL and transferred

`61,66,924.59/- to Techno to meet its pay-in obligation towards shares bought on

February 27, 2009 (Friday) where counterparties were Admire and Windmill. On March

4, 2009, Techno transferred `68,19,750.01/- and `54,26,278.51/- to Windmill and

Admire respectively towards sales proceed for shares sold on February 27, 2009. On the

same day, Admire and Windmill transferred `54,30,000/- and `6,70,000/-, respectively

to Loop and, in turn, Loop transferred `61,00,000/- to VIPL on the same day. In this

manner, fund was returned to VIPL.

(b). On April 17, 2009, Ms. Nirjhari Desai received `10,00,000/- from VIPL and paid

`10,05,236.60/- to Techno on April 18, 2009 to meet her pay-in obligation towards

shares bought on April 15, 2009 where the counterparty was Occasion. Techno

transferred `9,94,738.40/- to Occasion on same day towards sales proceed and Occasion

transferred `10,00,000/- to VIPL on April 21, 2009 through the layer of Windmill and

Loop.

(c). Similarly, it was observed that the funds were also transferred from Ms. Padma Valecha

and Mr. Jagdish Valecha to Ms. Nirjhari Desai who in turn transferred funds to Techno

to meet her pay-in obligation. A summary of such fund transfers is as following:

Table 11: Fund transfer from Ms. Padma Valecha to Ms. Nirjhari Desai

Date From (A/c No.) From Entity To (A/c No.) To Entity Amount (`)

01-08-09 2677101000059 Padma/Jagdish Valecha 2677104003469 Nirjhari Desai 65,000.00

04-08-09 2677104003469 Nirjhari Desai NA Techno 5,50,922.67

11-08-09 2677101000059 Padma/Jagdish Valecha 2677104003469 Nirjhari Desai 4,00,000.00

12-08-09 2677104003469 Nirjhari Desai NA Techno 3,88,025.55

(21) It was also observed that whenever Occasion bought shares, the ultimate source of funds

for its pay-in obligation was VIPL through layers of Loop and Windmill. Similarly, sale

proceeds of Occasion were transferred back to VIPL through Loop and Windmill. Also,

sale proceeds of Admire were transferred to VIPL through Loop.

(22) VEL or its management was having control over the connected/related entities and the fund

was transferred for meeting the pay-in obligations of sellers to connected/related sellers. Thus,

Order in the matter of Valecha Engineering Limited Page 17 of 62

no actual transfer of beneficial ownership of shares so traded amongst connected/related

entities took place and artificial volumes in the scrip was created.

3. Pursuant to the investigation, SEBI issued three show cause notices (SCNs) dated November 01,

2011 to VEL, its MD Mr. Jagdish Valecha and connected/related entities, details of which are as

under:

Table 12: Details of SCNs

Sl.

No.

Name of

the entity

SCN Allegation Violation

1. VEL IVD/ID4/AM/MR

/VEL/33717/2011

Dated November

01, 2011

VEL, in connivance with Mr. Jagdish Valecha,

F2Fun, Loop, Core and Brightword have

defrauded the investors by irregularly issuing

preferential convertible warrants through unfair

manner. VEL issued the convertible warrants

without getting actual consideration. The issuance

of warrants without receiving actual consideration

is irregular and adversely affected the interest of

investors in securities market and rights of the

existing shareholders of company.

Regulations

3(a), (b), (c)

and (d), and

4(1) of the

Securities and

Exchange

Board of India

(Prohibition of

Fraudulent and

Unfair Trade

Practices

relating to

Securities

Market)

Regulations,

2003 (the

PFUTP

Regulations)

read with

section 12A(a),

(b) and (c) of

the Securities

and Exchange

Board of India

Act, 1992 (the

SEBI Act).

2. Mr. Jagdish

Valecha

3. F2Fun

4. Loop

5. Core

6. Brightword

7. VIPL IVD/ID4/AM/MR

/VEL/33718/2011

Dated November

01, 2011

VIPL, Occasion, Worth Buying and Admire in

connivance with the other related entities have

defrauded the investors by subscribing to

convertible warrants on preferential basis through

unfair manner and assisted VEL in investing in its

own shares without getting actual consideration.

Further, these noticees have allegedly indulged in

financing transactions and executed sham

transactions with the funds received from VEL

thereby creating artificial volumes.

8. Occasion

9. Worth Buying

10. Admire

11. Windmill IVD/ID4/AM/MR

/VEL/33719/2011

Dated November

01, 2011

Windmill, Ms. Nirjhari Desai, Ms. Padma Valecha

and Ms. Reena Valecha, in connivance with the

other related entities indulged in

financing/executing sham transactions with the

funds received from VEL/VIPL thereby creating

artificial volumes and defrauding investors. Such

acts were fraudulent, unfair intentional and not

co-incidental and have lead to artificial

appearance of trading at the stock exchange and

also artificial appearance of discovery of price,

thereby misguiding the genuine investors.

12. Ms. Nirjhari Desai

13. Ms. Reena Valecha

14. Ms. Padma Valecha

4. Vide the said SCNs, the noticees were called upon to show cause as to why appropriate

directions in terms of sections 11(4) and 11B of the SEBI Act, 1992 read with regulation 11 of

Order in the matter of Valecha Engineering Limited Page 18 of 62

the PFUTP Regulations, 2003 should not be initiated against them for the violations as

mentioned therein, which may include debarring them from accessing the securities market and

prohibiting them from buying, selling or otherwise dealing in securities for an appropriate period

of time.

5. The aforementioned noticees replied to the respective SCNs issued to them as mentioned in the

following table:

Table 13: Replies of the noticees.

Sl. No. Name of the noticee Date of reply

1 VEL January 04, 2012, September 25, 2012, December 17, 2012 and

December 10, 2013 and April 23, 2015

2 Mr. Jagdish Valecha January 04, 2012, September 25, 2012, December 17, 2012 and

December 10, 2013

3 F2Fun January 04, 2012, September 25, 2012, December 17, 2012 and

December 10, 2013

4 Loop January 25, 2012

5 Core January 25, 2012

6 Brightword January 25, 2012

7 VIPL January 04, 2012, September 25, 2012, December 17, 2012 and

December 10, 2013

8 Occasion January 27, 2012

9 Worth Buying January 27, 2012

10 Admire January 27, 2012

11 Windmill January 25, 2012

12 Ms. Nirjhari Desai June 12, 2012

13 Ms. Reena Valecha January 04, 2012, September 25, 2012, December 17, 2012 and

December 10, 2013

14 Ms. Padma Valecha January 04, 2012, September 25, 2012, December 17, 2012, December

10, 2013

6. The noticees also sought copy of the Investigation Report, copies of statements of Ms. Sujita

Pradhan, Ms. Nirjhari Desai, Mr. Ajay Deole, Dr. F. C Nath and Mr. Rajesh Punjabi, and copies

of all the correspondences between the persons/entities related to the matter with SEBI

including but not limited to Ms. Sujita Pradhan, Ms. Nirjhari Desai, Mr. Ajay Deole, Dr. F. C

Nath and Mr. Rajesh Punjabi.

7. The noticees were also granted opportunities of personal hearing on several occasions. The

authorised representatives of VEL, Mr. Jagdish Valecha, F2Fun, VIPL, Ms. Reena Valecha, Ms.

Padma Valecha and Ms. Nirjhari Desai appeared before me and made oral submissions appeared

before me and made oral submissions on February 03, 2015. Further, the aforementioned

noticees also submitted certain documents on March 04, 2015, April 17, 2015 and April 23,

Order in the matter of Valecha Engineering Limited Page 19 of 62

2015. However, Loop, Core, Brightword, Occasion, Worth Buying and Windmill did not appear

for the personal hearing either personally or through any authorised representatives. The

replies/submissions of the noticees are inter alia as under:

I. Valecha Engineering Ltd. (VEL):

(1) The assumption that VEL and its promoters/related entities had issued warrants to

certain entities without receiving the actual consideration is contrary to factual position.

VEL had received the requisite consideration from the respective allottees towards the

subscription.

(2) As regards the allegation of financing, it had provided finances to VIPL (promoter of

VEL). Over the years, VEL had been raising/borrowing funds from VIPL for its

temporary use. Flow of funds between VEL and VIPL is duly captured in the books of

both the companies and also in their annual reports and the bank entries pointed out in

the SCN are part of various other bank entries which have taken place between VEL

and VIPL. The outstanding amounts from time to time, the interest thereon and TDS

on such interest are as follows:

Table 14: Liability of VEL to VIPL

Date Amount payable by

VEL to VIPL (`) Interest paid during the financial

year by VEL to VIPL (`) TDS Deducted(`)

31/03/05 15,28,727/- 1,62,675/- 3,65,050/-

30/09/05 6,65,37,249/-

31/03/06 1,60,51,462/- 24,22,576/- 54,366/-

31/03/07 2,78,81,462/- 13,16,411/- 17,86,873/- (VIPL to VEL)

2,95,403/- 4,00,974/-

20/04/07 81,462/-

(3) The payments made by VEL to VIPL on October 17, 2005 (`75,00,000/-), on October

19, 2005 (`1,00,00,000/-), on March 03, 2006 (`1,50,00,000/- and `2,00,0000/-), on

February 13, 2007 (`3,00,00,000/-; `3,00,00,000/-; `53,70,000/-), on April 18, 2007

(`1,80,00,000/-) were all part of repayments of outstanding amounts payable by VEL to

VIPL. In support of its submission, VEL submitted a copy of its ledger and copies of

the TDS certificates for interest paid for the loans given/taken by VEL from VIPL.

(4) As regards providing finances to other entities, namely, Admire, Core, Loop, Occasion,

Worth Buying and Brightword, these companies have NRI investors and the same is

enumerated in the following table:

Table 15: Details of companies and their NRI investors

Sl. No. Name of Company NRI Investor

1. Admire Dr. F.C. Nath and Mr. Giresh Melwani

2. Core Ms. Nirjhari Desai

Order in the matter of Valecha Engineering Limited Page 20 of 62

3. Loop Dr. F.C. Nath

4. Occasion Ms. Nirjhari Desai

5. Worth Buying Dr. F.C. Nath and Mr. Rajesh Punjabi

6. Brightword Mr. Narendra Mulji

(5) The NRI investors, namely, Ms. Nirjhari Desai, Dr. F. C. Nath and Mr. Rajesh Punjabi,

were personally known to Mr. Jagdish Valecha [the Managing Director (MD) of VEL]

and were interested in investing in VEL by acquiring warrants/shares of VEL by way of

preferential issue.

(6) The said NRI investors had requested the directors of VEL to assist them in setting

up/acquiring companies in which they would bring finances for acquiring shares of

VEL. Hence, the directors of VEL in consultation with these NRI investors, helped

them in identifying the companies and selected these companies (Admire, Core, Loop,

Occasion and Worth Buying) and requested certain trustworthy local representatives to

make the initial investment and accept directorship to facilitate the process and

represent the companies. It was in this background, the preferential allotment was made

to the said allottee companies, after receiving the requisite subscription amounts from

the said companies.

(7) The linkages with the aforementioned companies are only to the extent of business

transactions carried out in normal course of business.

(8) As regards transfer of funds from VEL to Loop, the same was a temporary loan given

by VEL to Loop in the ordinary course of business which was repaid subsequently

within a period of 4 months by Loop to VEL. However, it was not aware of fund

movement between Loop and others including VIPL.

(9) It also denied having any knowledge about fund movement between Occasion and

others. It has confirmed that the transfer of funds by Occasion to VEL was towards

initial 10% subscription amount of convertible warrants and has contended that the

allegation in the SCN is qua the initial 10% subscription amount only and there is no

allegation qua the receipt of balance 90% subscription amount. Further, the

independent fund transactions between Occasion and other entities cannot be treated as

fund transactions between Occasion and VEL.

(10) It had no knowledge about transfer of funds between Worth Buying and others. The

transfer of funds from Worth Buying to VEL was with regard to subscription of

warrants.

(11) The transfer of funds from VEL to Loop was a temporary loan given by VEL to Loop

in the ordinary course of business and the said amount was repaid by Loop to VEL

subsequently within 4 months. It is not aware about the amount transferred by Loop to

Worth Buying.

Order in the matter of Valecha Engineering Limited Page 21 of 62

(12) VEL has denied that it had financed 71.46% of the total value of convertible warrants

to Worth Buying. In fact, Worth Buying had paid the consideration amount to VEL

towards allotment of warrants and VEL had not funded the said amount as insinuated.

It has further stated that there is nothing on record to show that VEL had given

monies/funds to Worth Buying and independent fund transactions between Worth

Buying and other entities cannot be treated as fund transactions between Worth Buying

and VEL.

(13) It has no knowledge about transfer of funds between Admire and others. However, the

transfer of funds from Admire to VEL was with regard to allotment of warrants and

there is nothing on record to show that VEL had given monies/funds to Admire and

independent fund transaction between Admire and other entities cannot be treated as

fund transactions between Admire and VEL.

(14) It has no knowledge about transfer of funds between Brightword and others. However,

the transfer of funds from Brightword to VEL was with regard to allotment of warrants

and there is nothing on record to show that VEL has given monies/funds to

Brightword. Independent fund transactions between Brightword and other entities

cannot be treated as fund transaction between Brightword and VEL

(15) VEL has denied that it financed `18,74,70,000/- out of `28,47,08,805/- (65.85% of

total value of preferential warrants) to the preferential allottees and also denied that it

invested in its own shares through these entities without getting actual consideration.

(16) All the allottees are independent and investments made by them in VEL's shares cannot

be treated as investment made by VEL in its own shares.

(17) It is not having any control over Worth Buying and Occasion.

(18) None of the allottees entities or their promoters/major shareholders, viz. Dr. F. C.

Nath, Mr. Rajesh Punjabi and Ms. Nirjhari Desai have denied that the shares of VEL

held by the said allottee companies pursuant to preferential allotment did not belong to

them or that they have not dealt in the said shares through their entities.

(19) The said NRIs have sought preferential allotment of warrants of VEL, subscribed to the

same and have actually converted the warrants into shares after paying the requisite

amounts and post conversion of warrants into shares, they have sold the shares through

their entities and remitted the amounts from the bank accounts of the respective entities

to their own individual bank accounts.

(20) VEL has denied that it was given any power of attorney by any of the NRIs or that

VEL has gained any advantage through the use of power of attorney.

(21) Vide its letter dated September 25, 2012, VEL has stated that the mother-in-law of Ms.

Nirjhari Desai had never held shares of VEL, as alleged by Ms. Nirjhari Desai.

However, the shares were held by Ms. Nirjhari Desai only which were sold

subsequently. It has further stated that at no point of time any amount was deposited by

Order in the matter of Valecha Engineering Limited Page 22 of 62

Ms. Nirjhari Desai with it.

(22) The interest paid to VIPL for the financial year ending 2004-05 and 2005-06 is

`26,95,747/- and `25,85,251/- respectively as against `1,62,675/- and `24,22,576/-

submitted in its initial reply. It has submitted the TDS certificate for the financial year

ending March 31, 2005 evidencing payment of `26,95,747/- as interest. It has also

submitted a certificate from its statutory auditor M/s D. M. Jani & Co., Chartered

Accountants, dated August 21, 2012 inter alia confirming and certifying the details of

loans given to/taken from VIPL and interest charged/paid.

(23) As regards financing by VIPL to Occasion through Core, it has stated that VIPL was

borrowing/lending from/to Core in the ordinary course of business.

(24) As regards financing by F2Fun (a company promoted by VIPL) to Worth Buying, it has

stated that F2Fun had given the said amount in the ordinary course to Worth Buying

and the said amount was repaid by Worth Buying to F2Fun subsequently.

(25) The other entities viz., Mr. Rajesh Punjabi, Mr. Rajesh Pradhan, Mr. Giresh Melwani,

Dr. F. C. Nath, Mr. L. M. Gwalani, Ms. Vimla Gwalani, Mr. Ajay Deole referred in the

SCN have also carried out similar activities. However, VEL has been selectively

proceeded against, to the exclusion of those entities.

(26) No reliance can be placed on the statement of Mr. Dinesh Valecha recorded under

section 11C(5) of the SEBI Act, 1992 since as per the copies furnished by SEBI those

proceedings were neither before the investigating authority nor the investigating

authority has signed them during the statement recording.

II. Mr. Jagdish Valecha:

(1) He has adopted the reply of VEL and submitted that the reply of VEL be read as part

and parcel of his reply.

(2) He has not acted in connivance with VEL in any manner.

(3) VEL made the preferential allotment in the ordinary course of business, transparently

and with full disclosures and in consonance with the applicable provision of the SEBI

Regulations and Guidelines.

(4) VEL did not finance any of the allottees out of its own funds. The allegations regarding

financing, etc. are contrary to factual position on record and are based on mere surmises

and conjectures.

(5) The NRI investors were interested in investing in VEL by acquiring warrants/shares of

VEL by way of preferential allotment. These NRI investors were known to him and Mr.

Dinesh Valecha (director of VEL) personally and they requested him to assist them in

setting up/acquiring companies in which they would bring in finances for acquiring

shares of VEL.

(6) To facilitate the investment by these NRI investors, they requested him to recommend

Order in the matter of Valecha Engineering Limited Page 23 of 62

known and trustworthy individuals who can be requested to make initial investments to

acquire or set up such companies and also to hold directorships of these companies so

that the requirements of complying with the requisite rules and regulation of the

Companies Act, 1956 and other such compliances can be met in India, as it is

impractical for these NRI investors to come to India only for these procedural

compliances.

(7) Keeping this in view and as requested by them, he had in consultation with them

identified the companies viz. Admire, Occasion, Worth Buying and Brightword and

requested certain trustworthy local representatives to make the initial investment and

accept directorships to facilitate the process and represent the companies and to help

out these NRI investors in investing in India through these companies and in VEL.

(8) He had no direct/indirect interest or any involvement in the management or decision

making of these corporate entities.

(9) He was holding the power of attorney given by Ms. Nirjhari Desai (an NRI investor)

and had acted within the powers conferred on him by the said power of attorney. Ms.

Nirjhari Desai was informed about the action taken by him in exercising the power of

attorney bestowed on him and the funds transferred by Ms. Nirjhari Desai to her

entities in India were utilized as per the instructions of Ms. Nirjhari Desai and the

profits earned out of her investments were also deposited in the bank accounts of Ms.

Nirjhari Desai or the entities owned by her.

(10) He had requested Mr. Ajay Deole, Mr. Anil Lulla and Mr. Uday Sane to accept

directorship in Worth Buying and Occasion in order to facilitate the process and

represent the companies and to help out the NRIs investors in investing in India

through these companies. He has also submitted that the NRIs enjoyed the dividends

received by them from their investments.

(11) He was not having any control over Worth Buying and Occasion and also refuted the

stand taken by Ms. Nirjhari Desai that she became aware of her investments in these

companies on November 05, 2010.

(12) He has not used the power of attorney for transfer of funds for allotment/conversion

of warrants without the knowledge of the NRI investors. Further, the sale proceeds of

the shares have been remitted to the accounts of the NRI investors from the accounts

of the allottee companies owned by the NRI investors.

(13) He denied having control over the allottee companies and also denied that loans were

given without the knowledge of the NRIs.

(14) The loans/funds given by the alleged promoter entities cannot be treated/equated as

loans/funds given by VEL.

(15) All the allottees are independent entities and investments made by them in the shares of

VEL cannot be treated as investment made by VEL in its own shares.

Order in the matter of Valecha Engineering Limited Page 24 of 62

(16) The mother-in-law of Ms. Nirjhari Desai never held shares of VEL and at no point of

time made any deposits with VEL. In fact, shares of VEL were held in the name of Ms.

Nirjhari Desai only which were sold on her directions, with her knowledge and consent.

The deposits were placed by her with other companies (and not with VEL) with her

knowledge and consent. He has also denied the allegation of Ms. Nirjhari Desai about

liquidation of deposits for purchasing 79,575 shares of VEL by misusing the power of

attorney. He claimed that at all points of time, Ms. Nirjhari Desai was kept informed by

e-mails about the actions taken by him by using the power of attorney.

(17) All the funds transferred by Ms. Nirjhari Desai to her entities in India were utilized as

per her instructions and the profits earned by her out of the investments made from her

funds were also deposited in her bank accounts or the bank accounts of her entities.

(18) He has denied the allegation of Ms. Nirjhari Desai about the misuse of power of

attorney and ignorance of selling of the shares of VEL and stated that all along Ms.

Nirjhari Desai/Mr. Mehul Desai (her husband) were always informed and aware of the

same. To substantiate the same, he has submitted printouts of the e-mails exchanged

between Mr. Rajesh Pradhan (who was liasioning with them) and Mr. Mehul Desai.

(19) Sometime around July 2004 an "Agreement for Sale" dated July 01, 2004 was executed

between Ms. Padma Valecha, Mr. Jagdish Valecha and Ms. Reena Valecha (collectively

referred to as “sellers”) and Ms. Nirjhari Desai whereby the sellers had sold their

shareholding of 998 shares in Core (99.8% of the total equity capital). The said

agreement was duly executed by Ms. Nirjhari Desai and she had issued three different

cheques signed by her for a total amount of `99,800/- in favour of the sellers towards

the consideration for the shares purchased. Pursuant to the execution of the sale

agreement and payment of consideration, Ms. Nirjhari Desai became held of 99.8% of

share capital of Core. He further stated that Ms. Nirjhari Desai in her capacity as the

director of Core is the signatory to the Annual Report 2003-04 and annual return and

other documents.

(20) There is no evidence in the SCN to support the allegation regarding his role.

(21) Other entities viz., Mr. Rajesh Punjabi, Mr. Rajesh Pradhan, Mr. Giresh Melwani, Dr. F.

C. Nath, Mr. L. M. Gwalani, Ms. Vimla Gwalani, Mr. Ajay Deole referred in the SCN

have also carried out similar activities however, the noticee has been selectively

proceeded against, to the exclusion of those entities.

(22) No reliance can be placed on the statement of Mr. Dinesh Valecha recorded under

section 11C(5) of the SEBI Act, 1992, since as per the copies furnished by SEBI those

proceedings were neither before the investigating authority nor the investigating

authority has signed them during the statement recording.

Order in the matter of Valecha Engineering Limited Page 25 of 62

III. Valecha Investment Private Limited (VIPL):

(1) VIPL is one of the promoters of VEL, holding 78,25,000 shares of VEL and the

shareholding has almost remained static except occasional purchases. It has not sold the

shares of VEL for the last ten years and more. The alleged purchase of shares of VEL

was a delivery based trade.

(2) It purchased shares of VEL on market through its Techno. It has further submitted that

the deals in question were negotiated deal with Admire and Windmill. Since the deal was

negotiated and the Techno was the common stock broker, the deals were executed as

cross deals.

(3) It paid Techno out of its own funds for the purchase of shares and it received the shares

in its demat account. Therefore, the trades were delivery based and there was a change

of beneficial ownership.

(4) It was not aware that Mr. Rajesh Pradhan, an employee of VEL, was the sub-broker of

Techno. Since, Mr. Rajesh Pradhan was an employee of VEL and assisted it in the past

to open its accounts with the broker, it placed orders through him. VIPL denied that

Mr. Rajesh Pradhan facilitated it in creating artificial volume.

(5) With respect to fund transfers it has stated that it has been borrowing and lending funds

to various entities including VEL, Loop and Ms. Nirjhari Desai in the ordinary course

of business.

(6) It has denied funding or receiving funds from Occasion or Windmill. It was not aware

about the use of funds by Loop raised from it. It also denied having any control over

the entities as alleged.

(7) With regard to the transfer of funds between VEL and VIPL, it has stated that over the

years VEL has been raising/borrowing funds from VIPL for its temporary use and the

outstanding amounts from time to time are as follows:

Table 16: Details of liability of VEL to VIPL

Date Amount payable by

VEL to VIPL (`) Interest paid during the financial

year by VEL to VIPL (`) TDS Deducted(`)

31/03/05 15,28,727/- 1,62,675/- 3,65,050/-

30/09/05 6,65,37,249/-

31/03/06 1,60,51,462/- 24,22,576/- 54,366/-

31/03/07 2,78,81,462/- 13,16,411/- 17,86,873/- (VIPL to VEL)

2,95,403/- 4,00,974/-

20/04/07 81,462/-

(8) The payments received by it on October 17, 2005 (`75,00,000/-), on October 19, 2005

(` 1,00,00,000/-), on March 03, 2006 (` 1,50,00,000/- and ` 2,00,0000/-) , on February

13, 2007 (` 3,00,00,000/- and `3,00,00,000/- and `53,70,000/-), on April 18, 2007

(`1,80,00,000/-) were all part of receipt of outstanding amounts receivable from VEL. It

has also submitted copy of the ledger account for loan payment and interest received. It

Order in the matter of Valecha Engineering Limited Page 26 of 62

has further submitted copies of TDS certificates submitted by VEL for interest paid to

it for amount borrowed from VIPL.

(9) It has stated that the payment of subscription amount towards preferential convertible

warrants was paid to VEL in the following manner:

Table 17: Details of payment by VIPL to VEL

Date Amount (`) Particulars

18-10-05

19-10-05

74,38,675/-

1,00,00,000/-

Towards 10% of value of 8,73,900 share warrants @ `199.55/-

03-03-06 2,00,00,000/-

1,12,31,570/-

Towards conversion of 1,73,900 warrants into shares

13-02-07 3,00,00,000/-

3,00,00,000/-

53,70,900/-

Towards conversion of 3,64,000 warrants into shares

18-04-07 1,10,00,000/-

1,30,00,000/-

85,45,600/-

100,00,000/-

1,78,00,000/-

Towards conversion of 3,36,000 warrants into shares

(10) It was neither given any power of attorney by any of the NRI Investors nor it has

gained any advantage out of the alleged power of attorney. It was not having any control

over the entities. It had given loan to the NRI investors in the ordinary course based on

their request.

(11) In its additional reply dated September 25, 2012, it has repeated its earlier submissions

and added that the interest received by it from VEL for the financial year 2004-05 and

2005-06 is `26,95,747/- and `25,85,251/-, respectively as against `1,62,675/- and

`24,22,576/- submitted in its initial reply.

(12) There is no mention of synchronized, circular or reversal of trades nor any evidence was

provided in the SCN, therefore, the issue of creating artificial volume cannot and does

not arise.

(13) The SCN was issued to 4 entities whereas annexure to the SCN indicating cross deals by

Techno provides more than 15 client codes. In absence of any information about the

identity of these clients (codes) in SCN, it cannot comment on the trades.

(14) It is not aware of any violation committed by Mr. Rajesh Pradhan and, therefore, cannot

be held responsible for the same. It has been selectively proceeded against to the

exclusion of the stock broker and other entities.

(15) Other entities viz, Mr. Rajesh Punjabi, Mr. Rajesh Pradhan, Mr. Giresh Melwani, Dr. F.

C. Nath, Mr. L. M. Gwalani, Ms. Vimla Gwalani, Mr. Ajay Deole referred to in the SCN

have also carried out similar activities. However, the noticee has been selectively

proceeded against, to the exclusion of those entities.

Order in the matter of Valecha Engineering Limited Page 27 of 62

IV. F2Fun and Fitness (I) Pvt. Ltd. (F2Fun):

(1) VEL and VIPL are its promoter group company and it has neither subscribed to the

preferential warrants issued by VEL nor has been involved in trading in the scrip of

VEL at any point of time.

(2) The transfer of funds amounting to `20,00,000/- to Worth Buying was in the ordinary

course of business and had no nexus with the preferential allotment made by VEL. The

said amount was repaid by Worth Buying subsequently. It has submitted a copy of the

bank statement and ledgers evidencing repayment by Worth Buying.

(3) VEL and VIPL are its promoter group companies and not Mr. Jagdish Valecha or his

family members in their individual capacities.

(4) It has not connived with anybody including VEL to defraud the investors in any

manner and it was not involved in any manner in the alleged irregular issuance of

preferential convertible warrants through unfair manner.

(5) The other entities viz., Mr. Rajesh Punjabi, Mr. Rajesh Pradhan, Mr. Giresh Melwani,

Dr. F. C. Nath, Mr. L. M. Gwalani, Ms. Vimla Gwalani, Mr. Ajay Deole referred in the

SCN have also carried out similar activities. However, the noticee has been selectively

proceeded against, to the exclusion of those entities.

(6) Reliance cannot be placed on the statement of Mr. Dinesh Valecha recorded under

section 11C(5) of the SEBI Act, 1992, since as per the copies furnished by SEBI those

proceedings were neither before the investigating authority nor the investigating

authority has signed them during the statement recording.

V. Loop Engineering Consultants Pvt. Ltd. (Loop):

(1) It has neither subscribed to the preferential warrants issued by VEL nor has been

involved in trading in the scrip of VEL.

(2) The receipt of `1,75,00,000/- on April 18, 2007 from VEL was the temporary advance

raised by it from VEL and the transfer of `1,79,00,000/- to VIPL on the same day was

as an extension loan to VIPL.

(3) The transfer of `1,43,00,000/- from Loop to Worth Buying was the temporary advance

given to Worth Buying which was repaid by Worth Buying subsequently and the receipt

of `1,43,00,000/- was the temporary advance availed from VEL.

(4) The transfer of `20,00,000/- from Loop to Admire was a temporary loan given to

Admire which was repaid subsequently.

(5) The transfer of funds (`17,50,000/- on January 07, 2006, `20,50,000/- on January 12,

2006 and `16,00,000/- on January 16, 2006) to Dr. F. C. Nath was towards repayment

of loan borrowed by it from Dr. F. C. Nath.

(6) The transfer of `6,00,000/- on October 15, 2005 from Loop to Windmill was a

Order in the matter of Valecha Engineering Limited Page 28 of 62

temporary advance given to Windmill which was repaid subsequently.

(7) It was not controlled by VEL or the related entities of VEL and it was functioning

independently and the loans were raised/given in the ordinary course of business.

(8) It has not connived with anybody including VEL to defraud the investors in any

manner and it was not involved in any manner in the alleged irregular issuance of

preferential convertible warrants through unfair manner.

VI. Core Real Estate Pvt. Ltd. (Core):

(1) It has neither subscribed to the preferential warrants issued by VEL nor has been

involved at any point of time in trading in the scrip of VEL.

(2) The erstwhile promoters (Mr. Jagdish Valecha, Ms. Reena Valecha and Ms. Padma

Valecha) transferred their shareholding to Ms. Nirjhari Desai and since July 2004, Ms.

Nirjhari Desai was its promoter.

(3) The transfer of `45,00,000/- by Core to Occasion on October 18, 2005, was part of

business transaction carried out in normal course of business which was repaid

subsequently.

(4) The receipt of `43,00,000/- by it from VIPL was towards repayment of loan to the tune

of `16,00,000/- and the remaining `27,00,000/- was an extension of loan to it by VIPL.

(5) In July 2004, Ms. Nirjhari Desai acquired 99.98% of its shares from the erstwhile

promoters. Subsequently, Ms. Nirjhari Desai was involved as a director in the affairs of

Core and also signed the annual reports of Core for the financial year 2003-04. In