world trade - documents online home pagedocsonline.wto.org/dol2fe/pages/formerscriptedsearch/... ·...

TRANSCRIPT

WORLD TRADE

ORGANIZATIONWT/GC/62G/AG/1328 June 2002(02-3644)

General Council Committee on Agriculture

Marrakesh Ministerial Decision on Measures Concerning the Possible Negative Effects of the Reform Programme on Least-Developed and Net Food-Importing

Developing Countries

INTER-AGENCY PANEL ON SHORT-TERM DIFFICULTIES IN FINANCING NORMAL LEVELS OF COMMERCIAL IMPORTS OF

BASIC FOODSTUFFS

Report of the Inter-Agency Panel

WT/GC/62G/AG/13Page 2

TABLE OF CONTENTS

I. INTRODUCTION 3

A. ESTABLISHMENT OF THE PANEL 3B. TERMS OF REFERENCE 3C. COMPOSITION OF THE PANEL 4D. PROCEEDINGS 4

II. ISSUES BEFORE THE PANEL 5

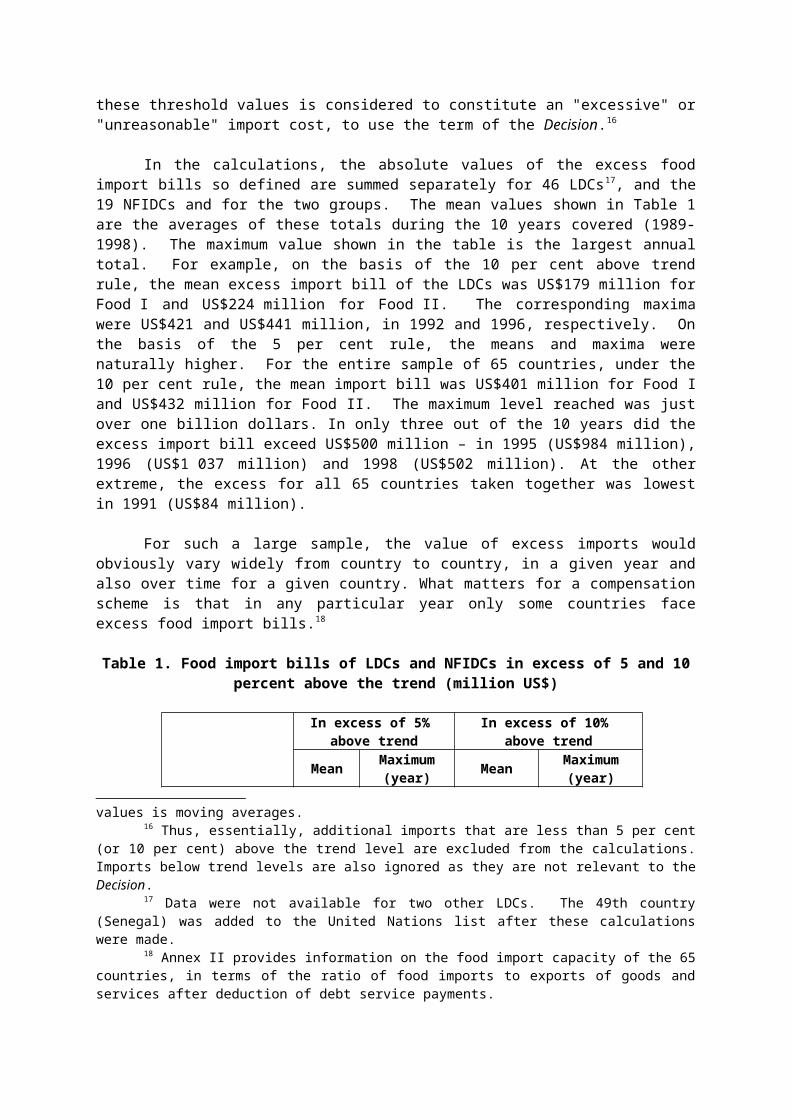

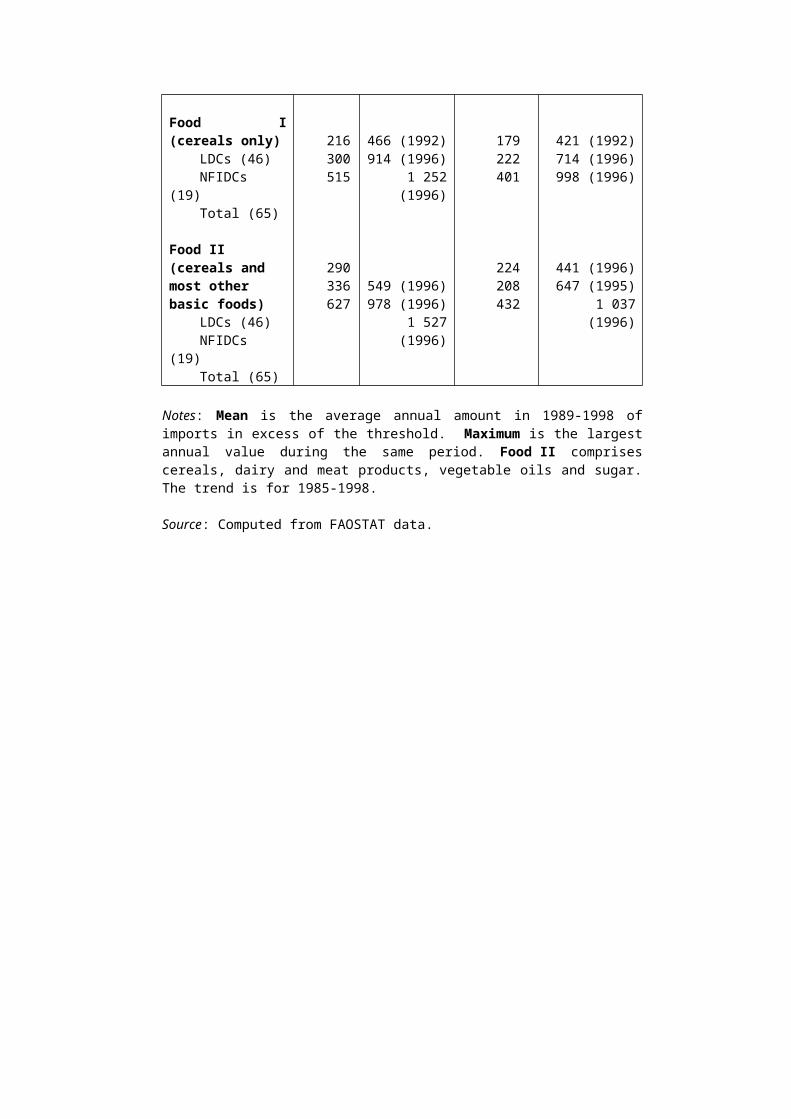

A. AVAILABILITY AND FINANCING COSTS OF EXTERNAL SUPPLIES OF BASIC FOODSTUFFS 51. Background 52. Price trends on the international markets for basic foodstuffs 53. Trends in the cost of cereal imports by LDCs and NFIDCs 114. Short-term difficulties in financing normal levels of commercial imports of basic foodstuffs 14

B. ACCESS TO SHORT-TERM MULTILATERAL FINANCING FACILITIES 191. The Compensatory Financing Facility of the IMF 192. World Bank facilities 243. Other sources of concessional financing 25

C. PROPOSALS FOR THE ESTABLISHMENT OF A REVOLVING FUND 261. Main elements of revolving fund proposals 262. FAO contributions 283. Analysis of concept and feasibility of the revolving fund proposal 30

D. OTHER OPTIONS 391. An ex-ante food import financing scheme 392. Commodity price risk management 403. Integrated Framework studies 40

III. CONCLUSIONS AND RECOMMENDATIONS 41

IV. ANNEXES 45

1. Decision on Measures Concerning the Possible Negative Effects of the Reform Programme on Least-Developed and Net Food-Importing Developing Countries 45

2. Proposals to Implement the Marrakesh Ministerial Decision in favour of LDCs and NFIDCs (G/AG/W/49, G/AG/W/49/Add.1 and G/AG/W/49/Add.1/Corr.1) 46

3. Replies by the Members involved to Questions Posed by the Panel 54

4. Submissions by the Food and Agriculture Organization of the United Nations (FAO) 86

5. Submissions by the International Monetary Fund (IMF) 113

6. Submission by the International Grains Council (IGC) 117

7. Submission by UNCTAD 120

8. Submission by the World Bank 131

9. Submission by the World Food Programme (WFP) 142

10. Submission by the Arab Monetary Fund 146

11. Submission by the Asian Development Bank 147

WT/GC/62G/AG/13

Page 3

I. INTRODUCTION

A. ESTABLISHMENT OF THE PANEL

1. The establishment of the Inter-Agency Panel on Short-Term Difficulties in Financing Normal Levels of Commercial Imports of Basic Foodstuffs ("the Panel") was approved by the fourth WTO Ministerial Conference at Doha in November 2001 following a recommendation by the WTO Committee on Agriculture in the context of the implementation of the Marrakesh Ministerial Decision on Measures Concerning the Possible Negative Effects of the Reform Programme on Least-Developed and Net Food-Importing Developing Countries ("the Marrakesh NFIDC Decision").1

2. The recommendation adopted by the Doha Ministerial Conference provides:

"that an inter-agency panel of financial and commodity experts be established, with the requested participation of the World Bank, the IMF, the FAO, the International Grains Council and the UNCTAD, to explore ways and means for improving access by least-developed and WTO net food-importing developing countries to multilateral programs and facilities to assist with short-term difficulties in financing normal levels of commercial imports of basic foodstuffs, as well as the concept and feasibility of the proposal for the establishment of a revolving fund in G/AG/W/49 and Add.1 and Corr.1. The detailed terms of reference, drawing on the Marrakesh NFIDC Decision, should be submitted by the Vice-Chairman of the WTO Committee on Agriculture, following consultations with Members, to the General Council for approval by not later than 31 December 2001. The inter-agency panel shall submit its recommendations to the General Council by not later than 30 June 2002." 2

B. TERMS OF REFERENCE

3. The following detailed terms of reference of the Panel were subsequently agreed by the Committee on Agriculture and approved by the General Council:

"1. To examine the terms and conditions of existing facilities of the international financial institutions (namely: IMF and the World Bank) to which least-developed and WTO net food-importing developing countries could have recourse in order to address short-term difficulties in financing normal levels of commercial imports of basic foodstuffs, principally cereals, rice, basic dairy products, pulses, vegetable oils and sugar, during periods of rising world prices for such basic foodstuffs, including, as appropriate, other relevant sources of concessional financing; this examination shall take into account, inter alia, such submissions as may be submitted to the Panel by least-developed and WTO net food-importing developing countries, donors and the relevant international financial institutions, by no later than end-March 2002;"

"2. To examine the concept and feasibility of the proposal for the establishment of a revolving fund in documents G/AG/W/49 and Add.1 and Corr.1, together with any further elaboration of those proposals as may be submitted to the Panel by the sponsoring Members concerned before the end of March 2002;"

"3. In the light of its review and examination under paragraphs (1) and (2) above and having regard to the Marrakesh NFIDC Decision, to make such recommendations for the consideration of the WTO General Council as the Panel considers appropriate 1 Decision of 14 November 2001 concerning Implementation-Related Issues and Concerns (see

WT/MIN(01)/17, dated 20 November 2001, paragraph 2.2).2 See G/AG/11, dated 28 September 2001, Section B, paragraph III(b).

WT/GC/62G/AG/13Page 4

regarding: ways and means for improving access by least-developed and WTO net food-importing developing countries to multilateral programmes and facilities to assist with short-term difficulties in financing normal levels of commercial imports of basic foodstuffs."

"4. In carrying out its task the Panel may consult with such bodies or institutions as it considers appropriate;"

"5. The Panel shall submit its report and recommendations to the WTO General Council by no later than 30 June 2002."3

C. COMPOSITION OF THE PANEL

4. The Chairman of the Panel was nominated by the WTO Committee on Agriculture and taken note of by the General Council.4 The Members of the Panel were nominated by the respective heads of the FAO, IMF, International Grains Council, World Bank and UNCTAD, in response to letters by the WTO Director-General inviting them to designate from their staff a financial or commodity expert to participate in the work of the Panel on a personal and independent basis.

5. The Panel has the following composition:

Chairman: Mr. Yoichi Suzuki of Japan

Members: Mr. Mehmet Arda (UNCTAD)

Alternate: Mr. Lamon Rutten

Mr. Germain Denis (IGC - International Grains Council)

Alternate: Mr. Richard Woodhams

Mr. Panos Konandreas (FAO)

Mr. John Nash (World Bank)

Mr. Grant B. Taplin (IMF - International Monetary Fund)

D. PROCEEDINGS

6. The Panel requested the Members involved to respond to a number of written questions.5 The responses by four WTO Net Food-Importing Developing Countries ("the NFIDCs") (Cuba, Egypt, Jordan and Tunisia) and six donors (Argentina, Australia, Canada, European Communities, Japan and the United States) are attached.6 The Chairman of the Panel invited the Members involved to an informal meeting on 28 May 2002 to provide a progress report. At an informal meeting on

3 See G/AG/12 (dated 10 December 2001) and WT/GC/M/72 (dated 6 February 2002), paragraphs 61-63.

4 See WT/GC/M/72 (dated 6 February 2002), paragraph 63.5 The Members involved comprise the donors, the least-developed countries ("the LDCs") and the

NFIDCs (Barbados, Botswana, Côte d'Ivoire, Cuba, Dominica, Dominican Republic, Egypt, Honduras, Jamaica, Jordan, Kenya, Mauritius, Morocco, Pakistan, Peru, Saint Kitts and Nevis, Saint Lucia, Saint Vincent and the Grenadines, Senegal, Sri Lanka, Trinidad and Tobago, Tunisia and Venezuela).

6 See Annex 3.

WT/GC/62G/AG/13

Page 5

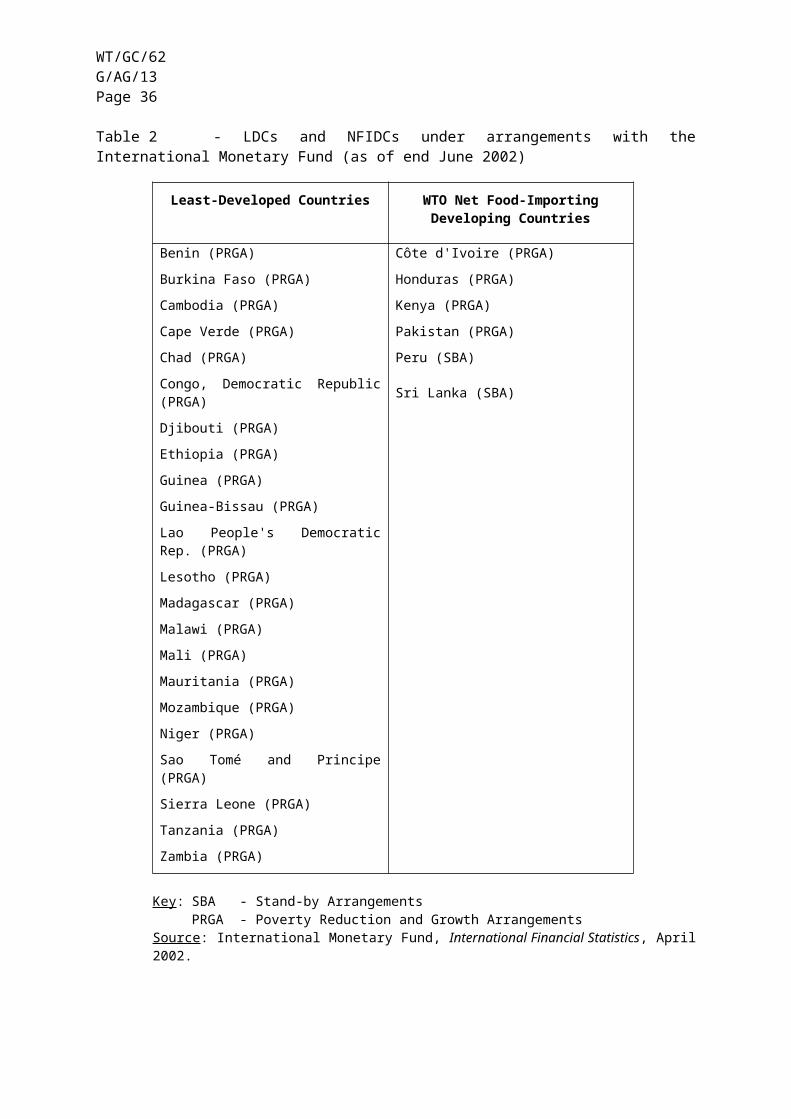

24 June 2002, the Panel presented a draft report to the Members involved, with a number of Members making preliminary remarks thereon.

II. ISSUES BEFORE THE PANEL

A. AVAILABILITY AND FINANCING COSTS OF EXTERNAL SUPPLIES OF BASIC FOODSTUFFS

1. Background

7. In the Marrakesh NFIDC Decision, the progressive implementation of the Uruguay Round Agreements as a whole was seen as generating increasing opportunities for trade expansion and economic growth to the benefit of all participants. Generally, improving the overall allocation of resources either within or among individual sectors or between countries is an integral part of the longer-term economic adjustment process that can be facilitated by the results of multilateral trade negotiations. However, the impact and benefits from trade liberalisation may not necessarily be spread evenly, even when there are net gains to be reaped for economies as a whole.

8. The NFIDC Decision recognized that during implementation of the Uruguay Round agricultural trade reform programme, some LDCs and NFIDCs may experience negative effects in terms of the availability of adequate supplies of basic foodstuffs on reasonable terms and conditions, including short-term difficulties in financing normal levels of commercial imports of basic foodstuffs. The particular concern was that some of the developing countries which were highly dependent on supplies of subsidized food imported from the major industrialized countries might need temporary assistance to make the necessary adjustments to expected higher import prices for food, although output from their farming sectors could be stimulated by higher prices. 1

9. Generally, world agricultural markets are influenced by many factors besides government policies and trade agreements. For crop sectors, for example, weather conditions affecting either export availabilities or import requirements may significantly impact global supply and demand balances and prices. Longer-term factors such as population growth, urbanisation, diet diversification and economic conditions also influence the composition and level of import requirements. In the context of the Marrakesh NFIDC Decision, we specifically address increased financing needs for food imports arising from higher world market prices, increasing food deficits or a shift from imports on concessional terms or food aid to commercial food imports.

2. Price trends on the international markets for basic foodstuffs

(a) Cereals

10. The entry into force of the WTO Agreement on Agriculture in January 1995 coincided with the beginning of a period of surging prices on the international markets for cereals. From the early months of 1995 prices continued to strengthen and, in 1996, escalated to historically high levels. Export prices peaked at around mid-1996 after which world market prices declined quickly. Wheat export prices peaked at US$ 258 per tonne in May 1996 (Figure 1 below). Taking account of export subsidies they had been as low as US$ 70 per tonne in 1993.

Figure 1 - Export prices for wheat and maize, 1990-2002 (US$ per tonne)

1 The concerns of the LDCs and NFIDCs stem partly from their dependence on the world market for a large share of their food consumption. In the case of cereals, NFIDCs imported 35 per cent of total consumption in 1998-2000. For the LDCs the dependence on cereal imports was 14 per cent compared to 11 per cent for the rest of the developing countries.

WT/GC/62G/AG/13Page 6

50

100

150

200

250

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Wheat: US Hard Winter

Maize: US Yellow Corn

US$/tonne

Note: Prices are export (fob) prices before deducting export subsidies, if any.

Source: International Grains Council.

11. The surge of world cereal prices was short-lived and followed by a sustained decline. By mid-1998 prices of wheat and maize had declined almost to the lowest levels since the 1970s. Currently, export prices of wheat are around US$ 125-130 per tonne (US Hard Red Winter) and US$ 90-95 per tonne for maize (US Yellow Corn). We note that in real terms international prices for cereals have shown a long-term declining trend since the mid-1970s. Cereal prices at their peak in 1996 were not nearly as high as during the "world food crisis" in the 1970s when adjusted for inflation. 2

12. The 1995-97 phase of surging grain prices was preceded by a number of government actions, which impacted longer-term market adjustments. In the United States, wheat stocks had accumulated in the mid-1980s to levels which were considered to be unsustainable. One of the main objectives of the 1985 United States farm legislation was to reduce excessively high grain stocks in an effort to reduce budgetary expenditures. Deficiency payments were tied to farmers' participation in set-aside programmes (acreage reduction programmes). Export subsidies were introduced via the Export Enhancement Program (EEP) and the Targeted Export Assistance Program (TEAP). In the following years, wheat stocks, in particular public stocks, declined significantly.

2 See also the contributions by the International Grains Council (Annex 6) and the World Bank (Annex 8) which complement this section.

WT/GC/62G/AG/13

Page 7

13. In the European Communities, government (intervention) stocks of wheat had increased considerably in the late 1980s and early 1990s. As part of the 1992 reform of the Common Agricultural Policy, the European Communities sought to reduce agricultural surpluses. The reforms in the arable sector included compensatory payments for reductions of price supports based on historical acreage and yields, as well as compensation payments on mandatory set-aside. Although these reforms did not modify the export restitution mechanism itself, after 1992/93 intervention stocks of wheat also significantly declined in the European Communities.

14. In response to these policy changes and other factors, the aggregate area harvested to wheat in the five major exporting countries (United States, European Communities, Canada, Australia and Argentina, which account for a combined world market share of approximately 90 per cent) declined by 13 per cent between 1990 and 1994. Assuming average yields, this decline accounted for approximately 25 million tonnes of wheat. Concurrently, there was a steep fall in the output of CIS countries' (former Soviet Union) as well. As a result, world wheat production decreased from 590 million tonnes in 1990 to 530 million tonnes in 1995.

15. There was also a number of short-term factors at play that fuelled the 1995-97 surge in grain prices, such as the severe drought affecting United States winter wheat and China's substantial wheat purchases. In effect, in early 1996, international wheat prices carried a risk premium, with prices shooting up to extraordinary levels. Wheat prices dropped quickly as from May 1996 when the weather conditions improved in the United States and the markets received favourable crop reports from other exporters.

16. In the European Communities, export taxes on wheat and barley were introduced in 1995 to stabilize domestic prices. In practice, this measure put additional pressures on the overall availability of supplies on world markets.

17. With respect to the implementation of specific limitations on the use of export subsidies arising from the Uruguay Round Agreement of Agriculture, we note the following:

First, the implementation of WTO export subsidy reduction commitments was phased in over a period of six years for developed countries, starting in 1995. Implementation of these commitments by developing countries is still underway, ending in 2004/05. In addition, a number of the commitments were front-loaded, with the implication that there was additional scope for providing export subsidies in the early years of the implementation period.3 Other things being equal, the phasing-in of export subsidy reductions, in conjunction with the front-loading provisions, have reduced their possible short-term price impact.

Second, international grains prices began to surge before the beginning of the implementation period. The implementation of export subsidy reduction commitments by major wheat exporters began only in the second half of 1995. When these commitments

3 The base level for reductions is the average level of export subsidies in 1986-90, but in the subsequent years export subsidy use for grains continued to increase in a number of countries. To facilitate implementation of reductions from the higher export subsidy levels applied in the early 1990s, the Uruguay Round participants agreed on modalities allowing "front-loading" of export subsidy reduction commitments. The modalities regarding front-loading allowed commitments to be higher than the base levels (1986-90) in the early years of the implementation period, coupled with the requirement that the reductions had to be caught up to meet the agreed overall reduction by the end of the implementation period (21% for subsidized volumes and 36% for budgetary outlays on export subsidies for developed countries from base period levels). For example, the Schedules of Canada, the European Communities and the United States show that their respective export subsidy reduction commitments for wheat/wheat flour are front-loaded in significant amounts both in terms of subsidized quantities and budgetary outlays.

WT/GC/62G/AG/13Page 8

on cereals entered into force, they had already lost their market effect in terms of binding constraints due to the high world prices prevailing at the time.

Third, at the end of the implementation period for developed countries in 2000/01, despite relatively low prices on the international grain markets, there was only a limited use of export subsidies. All exporters concerned were well within their export subsidy commitment levels for wheat/wheat flour and coarse grains.4 With the prevailing grain prices and exchange rates in 2000/01, the export subsidy ceilings for grains could not have had a significant negative impact, if any, on the terms of trade of LDCs and NFIDCs.

18. In sum, there was a coincidence of the entry into force of the WTO commitments in agriculture and surging world market prices for cereals in 1995-97. The weight of the evidence available to us leads us to conclude that the surge was triggered by a number of short-term and long-term factors, which were only partly related to the Uruguay Round reform programme in agriculture. In particular, it cannot be excluded that some reductions in grain stocks may have been made in anticipation of export subsidy reduction commitments entering into force in 1995. We also note that export subsidies have been used in periods when world market prices have been low rather than when world prices have been high. Since the use of export subsidies has been inversely related to world prices, they could not have been of significant value to countries experiencing difficulties in financing food imports in years of high prices as experienced during 1995-97.

(b) Other basic foodstuffs

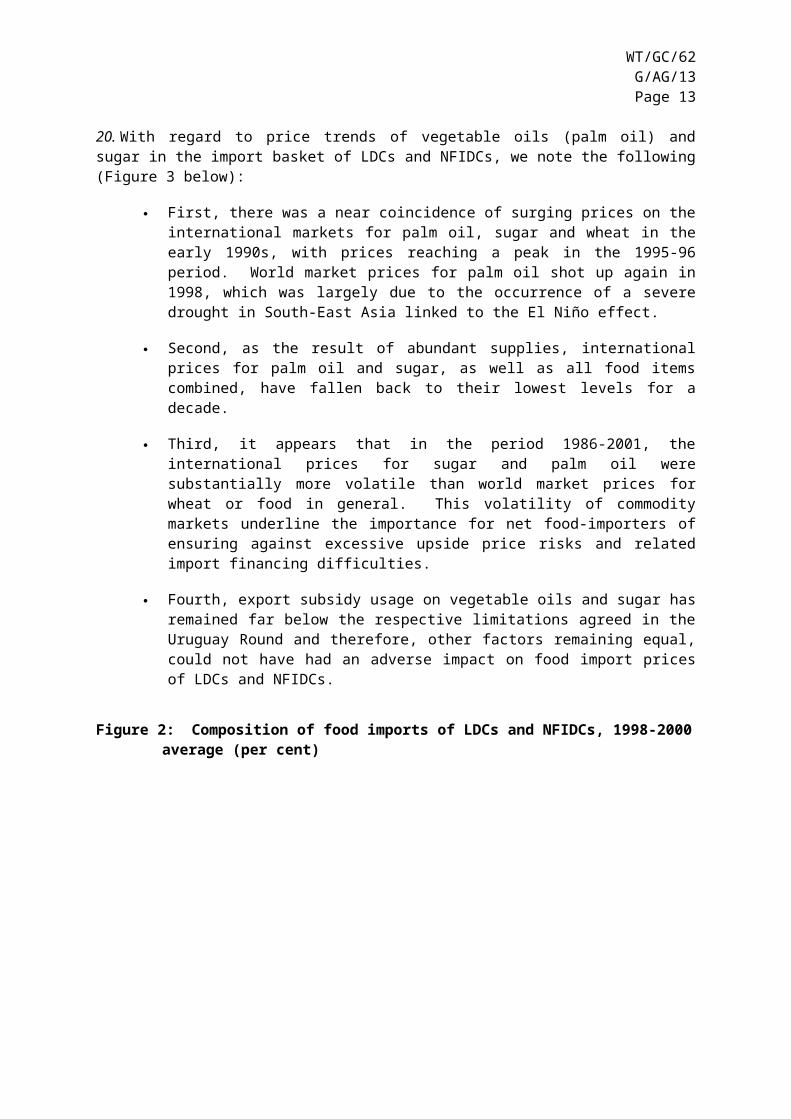

19. The scope of the Marrakesh NFIDC Decision comprises other basic food items, such as dairy products, pulses, vegetable oils and sugar, which are specifically listed in the Panel's terms of reference. Although cereals represented the main share of the aggregate food import values of the LDCs and NFIDCs (cereal imports in LDCs and NFIDCs accounted, respectively, for some 39 per cent and 35 per cent of their total food imports in 1998-2000 according to FAO data), vegetable oils and oilseeds accounted for about 17 per cent for both groups of countries (Figure 2 below). In this regard, the Panel notes that the composition of food imports of LDCs and NFIDCs differed considerably from other developing countries, where cereals and vegetable oils account for 25 per cent and 11 per cent respectively. This is essentially a reflection of their higher average income levels and larger proportions of higher value food commodities and processed products.

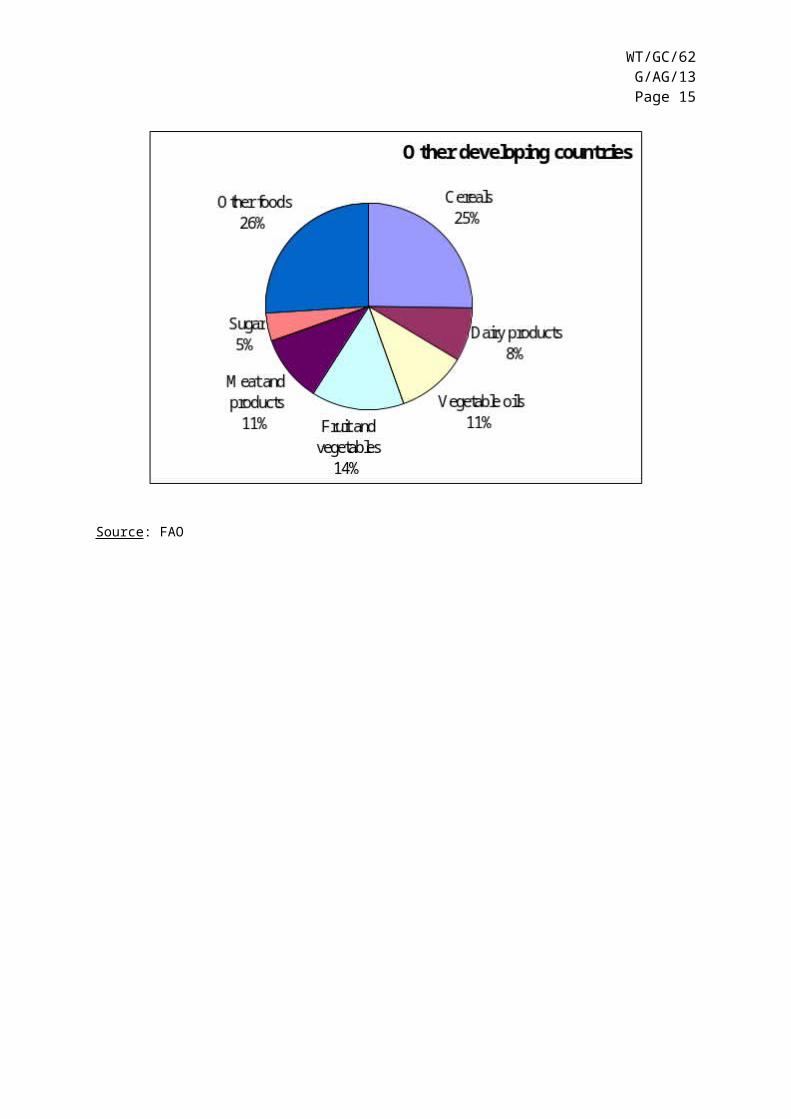

20. With regard to price trends of vegetable oils (palm oil) and sugar in the import basket of LDCs and NFIDCs, we note the following (Figure 3 below):

First, there was a near coincidence of surging prices on the international markets for palm oil, sugar and wheat in the early 1990s, with prices reaching a peak in the 1995-96 period. World market prices for palm oil shot up again in 1998, which was largely due to the occurrence of a severe drought in South-East Asia linked to the El Niño effect.

Second, as the result of abundant supplies, international prices for palm oil and sugar, as well as all food items combined, have fallen back to their lowest levels for a decade.

Third, it appears that in the period 1986-2001, the international prices for sugar and palm oil were substantially more volatile than world market prices for wheat or food in general. This volatility of commodity markets underline the importance for net food-importers of ensuring against excessive upside price risks and related import financing difficulties.

4 See document TN/AG/S/8, dated 9 April 2002.

WT/GC/62G/AG/13

Page 9

Fourth, export subsidy usage on vegetable oils and sugar has remained far below the respective limitations agreed in the Uruguay Round and therefore, other factors remaining equal, could not have had an adverse impact on food import prices of LDCs and NFIDCs.

Figure 2: Composition of food imports of LDCs and NFIDCs, 1998-2000 average (per cent)

WT/GC/62G/AG/13Page 10

Source: FAO

WT/GC/62G/AG/13

Page 11

Figure 3 - International food prices, 1986- 2001 (1986 = 100)

Notes: Food includes: cereals, oils, protein meals, meat, sugar, and bananasWheat; U.S. number 1 HRW, fob Gulf of MexicoPalm Oil; Malaysia and Indonesian, cif NW EuropeSugar; International Sugar Agreement price

Source: IMF

3. Trends in the cost of cereal imports by LDCs and NFIDCs

21. The rising costs of food imports by LDCs and NFIDCs is a central element of the rationale for the establishment of a Revolving Fund. This is set out in the NFIDC proposals as follows:

"The main objective of the Agreement on Agriculture was to decrease the structural surpluses generated in the past by production and trade-distorting policies in agriculture. It is, therefore, obvious that if this fundamental objective of the Agreement on Agriculture [AoA] is successful, the effect for the NFIDCs and LDCs will be an increase in the cost of their food imports.

According to the data provided by FAO (…), these two groups of countries are facing much higher cereal import bills than before. Taking the two years prior to 1995 as a benchmark (i.e. the average of the two marketing years 1993/94 and 1994/95), the increase in the cereal import bills in 1995/96 to 1996/97 amounted to 36.6 per cent for the two groups of countries taken together. Nearly all of this increase (35.1 per cent) was due to increases in the per unit cost of imported cereals, as volumes changed only marginally. Moreover, even after the world prices returned to more normal levels since the 1997/98 marketing year, the cereal

WT/GC/62G/AG/13Page 12

import bills of these two groups of countries remained at a much higher level than they were prior to 1995.

In view of the above, the causality between policy reforms under the Uruguay Round and higher food import bills for the LDCs and NFIDCs is clear."5

22. A number of donor countries have objected to the revolving fund proposal being premised on the establishment of a causality link between the Uruguay Round reform programme in agriculture and negative effects experienced by LDCs and NFIDCs.6 In their view, the 1995-1997 price spike may have been an isolated occurrence and the fact that markets returned quickly to lower levels reveals a resilience in the world food system which may in fact have been enhanced by the Uruguay Round.

23. In this regard, on the basis of statistical data provided by FAO (Table 1 below), we note the following:

First, there has been no clear upward trend in the aggregate food import bills of LDCs and NFIDCs since the beginning of the WTO reform process in agriculture in 1995.

Second, in the period during which prices for cereals were escalating (1995/96 to 1996/97), there was a surge in the aggregate cereal import cost of LDCs and NFIDCs. During this period, the aggregate volumes of cereal imports was maintained by the NFIDCs, but not by the LDCs. The Panel did not examine the reasons for this, including whether this may have reflected improved domestic cereal supply situations in some LDCs in that period.

Third, in the critical period of 1995-97, a significantly increased proportion of the combined cereal import volumes of LDCs and NFIDCs was sourced commercially, while the volume of food aid shipments was lower. Even after the critical years, commercial cereal imports have remained at higher levels than before the high-price period. This illustrates the contribution that predictable levels of targeted food aid in times of rising world market prices for cereals can make to meeting the food needs of LDCs and NFIDCs.

Fourth, the cereal import bills for LDCs and NFIDCs have somewhat "normalised" since 1998/99, as prices on world cereal markets have stabilised (albeit at generally depressed levels) while food aid shipments increased.

Fifth, price fluctuations unrelated to the WTO reform process on agriculture such as those experienced during 1995-97 are likely to reoccur.

5 See G/AG/W/49 (dated 19 March 2001), page 1 (Annex 2).6 See G/AG/11 (dated 28 September 2001), pages 8-14.

WT/GC/62G/AG/13

Page 13

Table 1 - Cereal import costs of LDCs and NFIDCs, 1993/94 – 2001/02

1993/94 1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02estimate f'cast

Import bill (US $ million)LDCs 1365 2147 2495 2023 2468 2214 1773 1871 1882NFIDCs 3567 4238 5806 5344 4941 4363 3828 4240 4007LDCs & NFIDCs 4932 6384 8301 7367 7409 6576 5601 6110 5889% change over 1993/94-1994/95 -12.8 12.8 46.7 30.2 30.9 16.2 -1.0 8.0 4.1

Total volume imported (000 tonnes) LDCs 11764 14068 13296 11772 15281 16927 15981 15264 15409NFIDCs 26584 26783 26601 28525 31955 33437 30588 32886 30226LDCs & NFIDCs 38348 40851 39897 40297 47236 50363 46569 48151 45635% change over 1993/94-1994/95 -3.2 3.2 0.8 1.8 19.3 27.2 17.6 21.6 15.2

Food aid (000 tonnes)LDCs 3970 4344 3313 2699 2863 4006 4139 3568 4505% of total imports 33.7 30.9 24.9 22.9 18.7 23.7 25.9 23.4 29.2NFIDCs 1830 1310 645 503 631 780 773 1149 1149% of total imports 6.9 4.9 2.4 1.8 2.0 2.3 2.5 3.5 3.8LDCs & NFIDCs 5800 5654 3958 3202 3493 4786 4912 4717 5654% change over 1993/94-1994/95 1.3 -1.3 -30.9 -44.1 -39.0 -16.4 -14.2 -17.6 -1.3

Commercial imports (000 tonnes)LDCs 7794 9724 9983 9072 12418 12920 11842 11696 10904NFIDCs 24754 25473 25956 28022 31324 32657 29815 31737 29076LDCs & NFIDCs 32548 35197 35940 37095 43743 45577 41657 43433 39980% change over 1993/94-1994/95 -3.9 3.9 6.1 9.5 29.1 34.6 23.0 28.2 18.0

Per unit import cost (US $/tonne) 1/

LDCs 116.0 152.6 187.6 171.9 161.5 130.8 110.9 122.6 122.2NFIDCs 134.2 158.2 218.3 187.4 154.6 130.5 125.1 128.9 132.6LDCs & NFIDCs 128.6 156.3 208.1 182.8 156.8 130.6 120.3 126.9 129.0% change over 1993/94-1994/95 -9.7 9.7 46.1 28.3 10.1 -8.3 -15.6 -10.9 -9.4

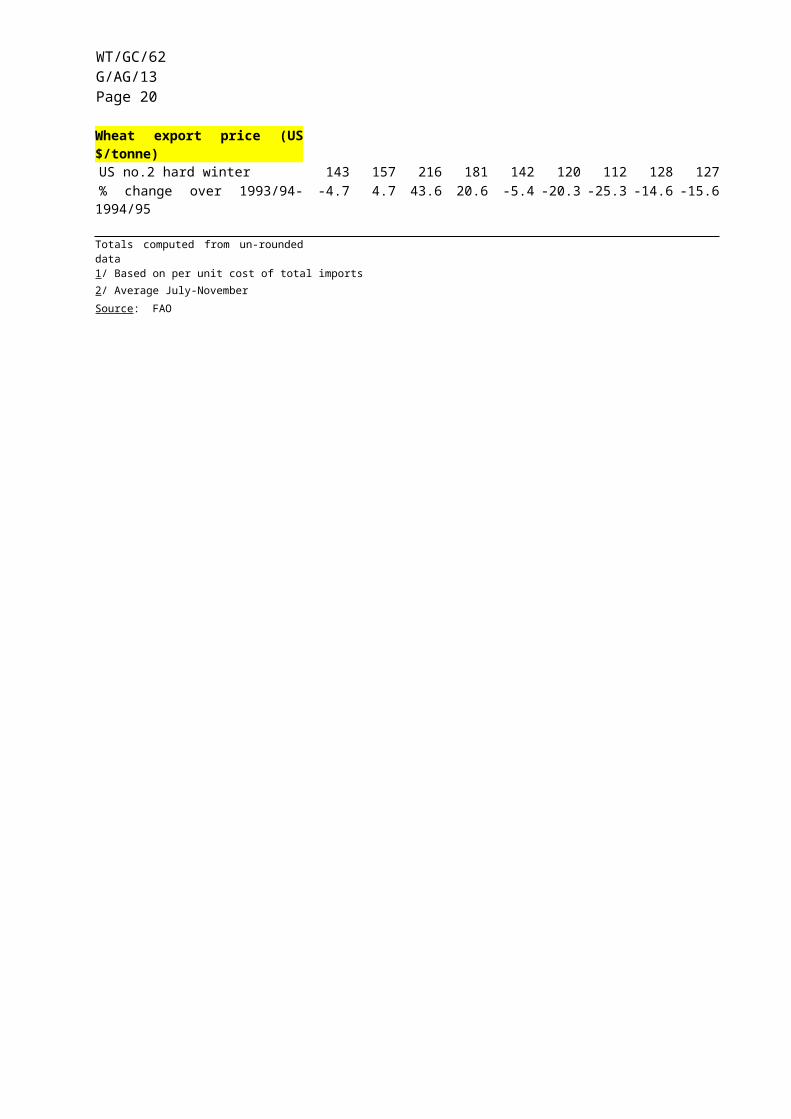

Wheat export price (US $/tonne)US no.2 hard winter 143 157 216 181 142 120 112 128 127% change over 1993/94-1994/95 -4.7 4.7 43.6 20.6 -5.4 -20.3 -25.3 -14.6 -15.6

Totals computed from un-rounded data1/ Based on per unit cost of total imports 2/ Average July-NovemberSource: FAO

WT/GC/62G/AG/13Page 14

4. Short-term difficulties in financing normal levels of commercial imports of basic foodstuffs

24. The possibility that LDCs and NFIDCs may experience "short-term difficulties in financing normal levels of commercial imports of basic foodstuffs" as the consequence of the Uruguay Round reform programme in agriculture, underlines both the Marrakesh NFIDC Decision and the Panel's terms of reference. Since the concepts of "normal levels of commercial imports of basic foodstuffs" and "short-term difficulties in financing" are not defined, the Panel has invited the Members involved to submit their views. The Panel also asked Members involved how they see the role of food aid for attenuating short-term financing difficulties of food imports.7

(a) Normal levels of commercial imports of basic foodstuffs

25. Several donor countries refer to the Usual Marketing Requirement (UMR) in the FAO "Principles of Surplus Disposal and Consultative Obligations of Member Nations" to determine what constitutes normal levels of commercial imports of basic foodstuffs.8 The UMR is based on an average of total commercial imports of the commodity concerned, usually in the preceding five years, taking into account the economic and balance-of-payments position of the importing country. In Australia's view, the UMR could be calculated for different commodities on the basis of accepted commercial import statistics. For Canada and the European Communities, however, this method would exclude factors such as population and/or income growth, and changes in consumer preferences.

26. For their part, NFIDCs have proposed a variety of methods to determine normal levels of commercial imports of basic foodstuffs.9 Cuba suggests that defining "normal levels" would require a country-by-country analysis, based on minimum consumption levels recommended by specialized health institutions in each country. Alternatively, the concept could be defined by taking average imports of basic foodstuffs over a representative number of years, although this average could be influenced by the purchasing power of the country in question during the relevant period, and by any food donations received.

27. Tunisia considers that normal levels of commercial imports should correspond to a country's import needs for a given year. These needs would depend on available local production and on increases in domestic demand. For Tunisia "normal levels" should not be limited to traditional imports calculated as an average for past years. Similarly, Jordan identified some specific volume requirements for five basic foodstuffs, in addition to strategic reserves of wheat and barley.

28. Egypt considers that normal levels of commercial imports of basic foodstuffs could be defined in terms of the import bill by a formula: IB = (C x P – DP – A) x p, where IB is the import bill of a basket of basic foodstuffs, C = per capita consumption, P = population, DP = domestic production, A = food aid and p = price. Egypt considers that a five-year moving average of import bills could be used to smooth out short-term fluctuations. In the Panel's view, normal levels of commercial food imports are usually seen in terms of volumes rather than values.

29. While the concept of the UMR is based on the notion of “normal levels of commercial imports”, we note that its purpose is entirely different from that envisaged under the Marrakesh NFIDC Decision. The UMR represents a commitment by a country receiving food aid to import an amount of the same commodity commercially to allay fears of displacement of commercial imports by other exporting countries. Since the UMR is defined in terms of the average commercial imports over the past five years, this may result in levels, which are lower than the trend level of imports in the current

7 See Panel questions 1 and 8, Annex 3.8 See responses by Australia, Canada, the European Communities and Japan to question 1 (Annex 3).9 See responses by Cuba, Egypt, Jordan and Tunisia to question 1 (Annex 3).

WT/GC/62G/AG/13

Page 15

year if there is an upward trend. This is normally the case for the majority of net food-importing developing countries.

30. Moreover, there are provisions in the "Principles of Surplus Disposal and Consultative Obligations of Member Nations" for waiving UMRs or adjusting the five-year historical average where the importing country concerned faces balance-of-payment difficulties, changes of production in relation to consumption of a commodity, where a case can be made that the preceding five years were not representative, and other special factors.10 For these reasons the UMR may often bear little direct relationship to the level of imports required to meet domestic consumption needs.

(b) Criteria to determine short-term difficulties in financing normal levels of commercial imports of basic foodstuffs

31. The Panel notes that the sponsors of the revolving fund proposal appear to equate short-term financing difficulties with surges in food import bills during times of high world market prices.

32. In the view of Egypt, for example, the triggering mechanism for the Marrakesh NFIDC Decision should be based on "the totality of effects and factors", that is on unexpected levels of food import bills of LDCs and NFIDCs on an individual basis. Egypt considers that a country effectively experiences short-term difficulties when the difference between the actual food import bill and the five-year moving average reaches 10 per cent. However, several countries have questioned the use of import bills to determine the existence of short-term financing difficulties. Canada and the European Communities stress that increases in imports or in import bills above "normal" levels do not necessarily imply difficulties in financing these imports. Import bills may increase due to economic expansion, driven by growing demand and availability of financial resources to finance imports.

33. Australia and Canada raise the issue whether the revolving fund should be designed to address financing difficulties that threaten food security, or whether it should offset the negative impact of price or currency spikes. According to Canada, the situation foreseen in the Marrakesh NFIDC Decision is one where private or government importers are unable to obtain financing to pay for imports of basic foodstuffs. Similarly, Cuba defines short-term difficulties as a lack of financing to ensure food security. Japan considers that short-term financing difficulties depend on whether a country can import the UMR through commercial trade, even when prices are rising or there is a shortage of foreign currency.

34. For Canada, Cuba, the European Communities and Tunisia, short-term financing difficulties are often linked to balance-of-payments problems. For its part, Jordan considers short-term difficulties should be determined based on foreign exchange reserves as well as on an increase in import bills above a three-year average by at least 25 per cent on a monthly basis. Some of the possible causes for short-term financing difficulties identified by the Members involved include unexpected exchange rate depreciation, increases in import prices, decreases in export prices, the seasonality of export revenues, debt service payments, unilateral measures, structural market transformations, natural disasters, changes in international aid and financial support, wars, conflicts, and political and/or financial crises.

35. While we do not consider it necessary to seek to resolve the question of how to define short-term difficulties in financing commercial food imports, we note that most submissions from Members involved do not seem to support basing the definition of short-term financing difficulties solely on excess food import bills; some countries pointing out difficulties with this approach.

10For a more complete description of the establishment of UMRs, see FAO, Reporting procedures and consultative obligations under the FAO principles of surplus disposal. A guide for members of the FAO Consultative Subcommittee on Surplus Disposal, Rome 2001, paras. 15-17 and Appendix H thereto.

WT/GC/62G/AG/13Page 16

(c) Experiences with respect to short-term financing difficulties

36. The Panel invited LDCs and NFIDCs to submit their experiences with respect to short-term financing difficulties of normal levels of commercial imports of basic foodstuffs, to explain how these were caused by the Uruguay Round reform programme in agriculture, and to describe how the difficulties were addressed. Four countries, Cuba, Egypt, Jordan and Tunisia, have provided information on their short-term financing difficulties.11

37. Cuba submits that importation of basic foodstuffs should be a consistent and continuous process. To ensure that this is the case, a stable source of financing is required to provide the resources required to cover the cash-flow deficits of importers. Since Cuba's economy is dependent on commodities (including cane sugar, nickel and tobacco), fishery products and tourism, it is difficult to reconcile the need for stable food imports throughout the year with the seasonality of its export revenues. Additional factors affecting Cuba's ability to import foodstuffs include the lack of funding from multilateral sources for food supply programmes, the distance, which separates Cuba from its supply markets and resulting high freight costs, and the trade embargo led by the United States. As a result, Cuba has had to resolve its financing difficulties by negotiating with suppliers of basic foodstuffs, resorting to export credit and credit insurance schemes offered by the official agencies in the supplier countries, obtaining costly trade credits, and allocating resources to the detriment of other priorities. None of these alternatives provide the predictability needed to solve Cuba's short-term difficulties. During the 1995/96 increase in food prices, Cuba had to negotiate intensely with its usual suppliers and with banks and financial institutions in order to obtain private financing to ensure a minimum level of essential food imports. The financed value of food imports during that period increased by approximately 26 per cent from one year to the next, with an additional cost of US$ 150 million. This increasing trend continued, and in 1999 the growth in the value of food imports financed through private and bank credits reached 36 per cent compared 1997. Because of the urgency of obtaining credits to import foodstuffs, Cuba has had to pay charges well above market levels - up to 18 per cent in interest in 1997.

38. Egypt indicates that as part of the reforms related to the results of the Uruguay Round, it reduced or eliminated various forms of support previously granted to farmers and exporters. In response, a transformation in cropping patterns occurred, away from subsidized towards more profitable crops. The volume of production of basic items such as sugar and wheat decreased at the time when world cereal prices started increasing towards their peak in the 1996/1997 season. Simultaneously, a long-planned reduction in the volumes of food aid granted to Egypt became effective. In order to reduce the impact of the situation on the local population and on the national treasury, Egypt adopted a series of compensatory measures, including the reduction of applied tariffs on wheat and corn, the temporary re-institution of a rationing system for the poor, a substantial reduction in nationally-held food stocks, a reduction of imports of less essential items, and recourse to short-term commercial buyer credits available from a number of non-national financial institutions.

39. Jordan states that during 1993 - 2000, the performance of its agricultural sector declined due to climatic factors. Especially the production of wheat and barley decreased significantly, and as a consequence, imports of basic foodstuffs increased. An emergency relief programme was needed to assist the most affected farmers, herders and producers of tree crops. As a result of the Gulf crisis, which led to the return of large numbers of expatriate workers and an increase in the size of the population, and due to the high prices during the 1995-96 period, the import bill of basic foodstuffs increased dramatically. The considerable increase in debt servicing requirements in the late 1980s was a major factor contributing to Jordan's economic crisis, and debt volumes and their impact on foreign reserves constitute an imbalance impeding the economic development process. These imbalances in Jordan's economy and the volatility of world prices of basic foodstuffs during the 1995-

11 See responses to question 2 and 3 (in the case of Jordan), Annex 3.

WT/GC/62G/AG/13

Page 17

96 period led the competent authorities to seek assistance to reinforce strategic inventories and normal levels of imports of basic foodstuffs inter alia through export guarantee programmes and food aid. To address its economic crisis, Jordan negotiated an arrangement with the IMF in 1989, and began implementing an economic reform programme.

40. Tunisia reports that while cereals normally accounted for an average of 34 per cent of imports, this share rose to 46 per cent in 1995 and 54 per cent in 2001. This was chiefly a result of the increase in the quantity of cereal imports in the wake of the decline in agricultural production in 1994 and 1995, and the considerable increase in the price of imports, particularly cereals (an increase of 27 per cent). In Tunisia, these imports were financed through foreign credit granted under market conditions, which increased the balance-of-payments deficit and the debt burden. They have required a mobilization of financial resources to the detriment of a number of development projects, in particular those aimed at promoting the use of natural resources and improving competitiveness in the agricultural sector.

41. The Panel notes that shifts in cropping patterns away from basic foodstuffs towards more profitable crops should lead to an increase in the resources available, among other things, to finance imports, at least in the long run. However, it is evident that the four responding NFIDCs (Cuba, Egypt, Jordan and Tunisia) did encounter real difficulties in financing normal levels of commercial food imports, although they appear to have little relation with the Uruguay Round reform programme in agriculture. The experiences described above show that the coping strategies differed considerably from country to country, and that access to the existing multilateral financing facilities has not formed any significant part of these strategies, except in the context of Jordan's economic crisis.12

(d) Food aid

42. Food aid is one of the aspects addressed by the Marrakesh NFIDC Decision in its own right. 13 For the purposes of its report, we have examined food aid only to the extent that it relates to short-term difficulties in financing normal levels of commercial food imports.14

43. The Food Aid Convention (FAC) provides a safety net in terms of food aid availability. The aggregate annual commitments decreased from a total of 7.517 million tonnes under the Food Aid Convention, 1986 to 5.35 million tonnes (wheat equivalent) under the Food Aid Convention, 1995. Under the new Food Aid Convention 1999, the minimum annual volume and value commitments of FAC members amount to a total of 4.895 million tonnes (wheat equivalent) and €130 million, respectively. In the period 1986-2001, annual shipments by the members of the Convention exceeded, often significantly, their combined commitments, except in 1994/95 when there was a shortfall.

44. The fact that these commitments are expressed mainly in volume terms is significant in times of high world market prices for cereals, as it provides assurances of minimum supplies of food aid irrespective of world food price and supply fluctuations. The Food Aid Convention, 1999 also has stronger provisions to cover transportation and other operation costs associated with food aid transactions, especially when food aid is directed to LDCs and in emergencies. All food aid to LDCs covered by members' commitments under the FAC is to be provided in the form of grants. Overall, food aid provided in the form of grants under the current Convention is to represent not less than 80 per cent of a member's contributions and, to the extent possible, members are to seek progressively to exceed this percentage. When allocating their food aid, FAC members undertake to give priority to the least-developed countries and low-income countries, many of which are on the present WTO list of net food-importing developing countries. Other eligible food aid recipients include lower middle-

12 See Jordan's response to question 3 (Annex 3).13 See paragraphs 3(i) and 3(ii) of the Marrakesh NFIDC Decision (Annex 1).14 See also the Panel's observations in this regard in paragraph 23 above.

WT/GC/62G/AG/13Page 18

income countries and all other countries included in the WTO list of net food-importing developing countries at the time of negotiation of the Food Aid Convention 1999.

45. In a contribution by the World Food Programme (WFP) to the Panel, WFP distinguishes between two types of food aid: targeted food aid and programme food aid.15 Targeted food aid comprises both emergency food aid, designed to relieve hunger in disaster situations, and project food aid, which is distributed to identified beneficiary groups to support specific development and disaster prevention activities. Programme food aid is usually supplied as a resource transfer for balance-of-payments or budgetary support objectives. It is not targeted to specific beneficiary groups but is sold to those who can afford it. According to WFP, programme food aid is neither effective nor efficient, and financial transfers are a much less costly way of dealing with balance-of-payments problems. While virtually all targeted food aid is provided in the form of grants, some programme food aid is not provided on fully grant terms (i.e. on concessional terms).

46. Several Members involved also distinguish between the impacts of targeted food aid and programme food aid.16 Most Members involved recognize that targeted food aid is useful, especially to address emergency situations. Argentina, Canada, the European Communities, as well as the World Bank, stress that long-term food aid is not a viable solution, and can be counterproductive because of effects on domestic markets. They point out that it tends to respond to the need to reduce surpluses in donor countries rather than responding to needs in recipient countries. Thus, it is abundant during times of low prices, and scarce when prices are high, possibly even exacerbating recipient countries' short-term financing difficulties. The United States considers that concessional food aid can act as a bridge between grant food aid and commercial sales, helping countries transition to market economies.

47. Cuba, Egypt, Jordan and Tunisia note that food aid can be an effective tool to address situations of food insecurity. However, Cuba stresses that food aid is on the decline, and diminishes especially during times of high prices, and is thus not sufficient to address the problems faced by LDCs and NFIDCs. Egypt indicates that ideally, food stocks held by major suppliers should be drawn down in the form of food aid when LDCs and NFIDCs have the highest needs, but that in view of the impracticability and expense of maintaining such stocks, the revolving fund had been proposed instead. Tunisia indicates that certain countries, including Tunisia, are not eligible to receive food aid, and proposes that eligibility criteria be reviewed.

48. Regarding the relationship between food aid and short-term difficulties in financing commercial imports of basic foodstuffs, Australia submits that unless short-term financing difficulties coincide with a shortage of food, the need for food aid does not arise. In its view, food aid addresses chronic and sustained malnutrition or emergency food shortages, whereas the revolving fund proposal deals with the impact of price or currency movements on food availability within a country for which programme food aid, if available, could be of relevance. Australia indicates that food aid and the revolving fund proposal thus address two different sets of problems, which may be experienced separately or simultaneously. While countries might need financial assistance when faced with financing difficulties, dumping developed-country food surpluses into an economy under stress might harm agricultural development.

49. The Panel notes that, to some extent, food aid effectively helps countries with limited resources by reducing requirements to commercially finance needed food imports. The fundamental principles in effectively providing food aid include that it be given to countries with limited resources to purchase food commercially (thus minimizing displacement of commercial imports of other exporters), targeted to poor persons, and that it be provided in a way that does not interfere with the

15 See Annex 9.16 See responses to question 8 (Annex 3).

WT/GC/62G/AG/13

Page 19

well functioning of domestic markets. To the extent that targeted food aid leads to additional consumption (by people who could not afford food otherwise), it will have no, or at most minimal, effect on a country's domestic market, imports and financing needs.

(e) Export credits

50. In its responses to our question about how LDCs and NFIDCs managed to weather the 1995-97 price spike, Jordan submits that its strategy included efforts to seek bilateral assistance through donors' export credit guarantee programmes. 17

51. Since officially supported agricultural export credits ("export credits") as such were not within the purview of the Panel's terms of reference, the Panel simply notes the following on the basis of OECD Secretariat reports: the total export credits for agricultural products increased from US$11 billion in 1995 to US$18 billion in 1998; for bulk cereals, export credits increased by US$465 million or 22 per cent over the same period18; but, the share of export credits accorded to LDCs and NFIDCs remains very low.19

B. ACCESS TO SHORT-TERM MULTILATERAL FINANCING FACILITIES

52. The Panel's terms of reference require us to examine the terms and conditions of existing facilities of the IMF and the World Bank to which least-developed and WTO net food-importing developing countries could have recourse in order to address short-term difficulties in financing normal levels of commercial imports of basic foodstuffs, principally cereals, rice, basic dairy products, pulses, vegetable oils and sugar, during periods of rising world prices for such basic foodstuffs, including, as appropriate, other relevant sources of concessional financing.

1. The Compensatory Financing Facility of the IMF

(a) Operation

53. The IMF provides financial assistance to its members through a variety of facilities. The principal financing facility in the event of temporarily higher food prices is the Compensatory Financing Facility (CFF), particularly its cereals element.20 The CFF is a special facility that provides financial assistance to countries that experience balance-of-payments difficulties arising from either a shortfall in aggregate export receipts or an excess in cereal import costs. Compensatory financing in the event of a cereal import price rise is released based on the following conditions: The excess in cereal import costs must be considered temporary and largely beyond the control of the country concerned. Unless the balance-of-payments position of the country concerned is satisfactory apart from cereal import costs, access to the CFF is considered in the context of a wider economic programme with the IMF. The functioning of the CFF, as well as the criticisms raised by NFIDCs are described below.21

17 See Jordan's responses to questions 2 and 3 (Annex 3).18 See OECD (2000), Agricultural Outlook 2000-2005, p. 51.19 See EC negotiating proposal regarding export competition of 18 September 2000 (G/AG/W/34, dated

11 June 1998, paragraph 10). The EC notes that its observation is based on an OECD survey using confidential data.

20 For a concise history of the CFF since its creation in 1963, see contribution by the IMF (Annex 5). See also "Review of the Compensatory and Contingency Financing Facility (CCFF) and Buffer Stock Financing Facility (BSFF) -- Preliminary Considerations", IMF, December 1999 at www.imf.org//external/np/ccffbsff/review/index.htm.

21 The panel was mindful that a review of the CFF was contemplated for the first half of 2003.

WT/GC/62G/AG/13Page 20

(i) Temporary excess in cereal import cost beyond the control of the country concerned

54. The excess in cereal import cost ("cereal import excess") is the difference by which the value of cereal imports in the "excess year" exceeds the arithmetic average of the value of cereal imports for the five-year period centred on the excess year. The calculation of the cereal import costs is thus based on data on actual imports for the two years prior to the current excess year; an estimate of the value of the cereal imports of the current year, and a projection of cereal import costs for the two subsequent years. The value of cereal imports excludes food aid as well as any cereal imports which are financed with concessional credit.

55. The eligibility criteria under the CFF require further that the cereal import excess be temporary, i.e. the price shock on the international cereal market must be considered to be reversible. If the price shock were to be a permanent feature, the Poverty Reduction and Growth Facility (PRGF) of the IMF would be the principal facility to assist low-income countries.22 In the view of the Panel, the experience in the past decades suggests that price increases on the international cereal markets tend to be temporary, and the most recent price "shock", which began in 1995, was reversed within less than two years.

56. Price fluctuations on the world market for cereals are typically considered by the IMF to be outside the control of governments, unless the country concerned is a dominant producer of cereals. The Panel notes that none of the LDCs or NFIDCs is a dominant producer of wheat, rice or coarse grains. Also, for the purposes of the CFF, it is irrelevant whether price increases for cereals on the world market are due to the Uruguay Round reform programme in agriculture or some other cause.

57. The CFF is available for two categories of balance-of-payments problems. One category consists of countries that have satisfactory balance-of-payments positions, except for the export shortfall or surge in cereal import costs. The second category comprises countries that have balance-of-payments difficulties that extend beyond the export shortfall or surge in cereal import costs. Experience has shown that most drawings under the CFF are likely to fall into this second category. In this case, access to the CFF would be in the context of an IMF-supported economic programme (arrangement), either already in place or approved along with the request for CFF support.

(ii) Export earnings

58. Compensation for an excess in cereal import payments is triggered only to the extent that the import excess is not offset by a decline in other imports or an increase in receipts of merchandise and services exports. Should it emerge that the cereal import excess was "overcompensated", the IMF requires prompt repurchase (repayment) of the loan.23 This might include situations where, for example, the cereal price hike was overestimated or export earnings were underestimated.

(iii) Access limits

59. Purchases (loans) under the cereal element are limited to the excess in cereal import cost of the country concerned and the applicable access limit under the cereal element, whatever is lower. As the result of the modifications of the CFF that were approved by the IMF's Executive Board in November 2000, the complex system of access limits has been simplified. Access limits are now 45 per cent of the country's quota for either an export shortfall or a cereal import excess, or 55 per cent of the quota for the two factors combined.

22 The PRGF is the IMF's concessional lending instrument: terms are 10 years, with 5 ¼ years grace, interest at 0.5 percent per annum.

23 A prompt repurchase was triggered in the case of Algeria and Bulgaria, the two most recent cases of countries having made purchase under the cereal element of the CFF.

WT/GC/62G/AG/13

Page 21

(iv) Disbursement and repayment

60. It may take two to three months between a request for a purchase under cereal element of the CFF and disbursement of funds. Normally, two disbursements are made within six months. On the other hand, a purchase under the CFF can also be made in anticipation of a projected excess in cereal import costs. There is the expectation of repayment of 2 ¼ - 4 years, but in any case, repurchases (i.e. repayment of the loan) are due 3¼ to 5 years after a purchase is made; the interest rate is currently about 3.05 per cent per year.

(b) Perceived inadequacies of the Compensatory Financing Facility

(i) General

61. The Panel observes that there has been very little use of the cereal element of the CFF in recent years. In the period from January 1993 to September 1999, there were six purchases by four countries (Algeria, Bulgaria, Moldova and South Africa). None of these countries is an LDC or an NFIDC. During the phase of rapidly increasing international prices for cereals in 1995-97, only Algeria and Bulgaria made a purchase under the cereal element.24 As regards the reasons, the IMF advises that such infrequent use was not due to a lack of resources available under the CFF.

62. We note that, in principle, all LDCs and listed NFIDCs have access to the resources of the IMF, except Cuba and Tuvalu, since these countries are not currently members of the IMF.

63. In the view of a number of NFIDCs, the CFF has certain inadequacies for it to be a useful resource in times of financing difficulties of imports of basic foodstuffs. The main points raised relate to its product coverage, conditionality and lack of concessionality.

(ii) Product coverage

64. Several of the NFIDCs have noted with concern that the CFF covers only cereals whereas the product coverage envisaged by the NFIDC Decision encompasses all basic foodstuffs.25

65. We note that there may be situations where there is a coincidence of temporary and reversible price increases of various foodstuffs, including grains, outside the control of governments resulting in balance-of-payments difficulties or where international cereal prices do not rise but prices for other foodstuffs do. There is thus a possibility that the limited product coverage of the CFF could be a factor constraining LDCs and NFIDCs experiencing short-term difficulties in financing normal levels of commercial food imports.

(iii) Conditionality

66. For some, a perceived shortcoming of the CFF is that it requires "conditionality". IMF loans are usually provided under an "arrangement," which sets out the policies that a country intends to pursue, which forms the basis of access to the loan. Arrangements are based on economic programmes formulated by countries in consultation with the IMF. Loans are then disbursed in instalments as the programme is implemented. As a result of the November 2000 review of the CFF referred to above, conditionality has been strengthened. Access to the CFF will now be generally available only in the context of an arrangement.

24 In the period of January 1993 to September 1999, the export shortfall element of the CFF was more frequently used than its cereal element. Amongst the countries having drawn on the export shortfall element are three NFIDCs (Dominican Republic, Jordan and Pakistan) and one LDC (Rwanda).

25 G/AG/11 (dated 28 September 2001), Annex 1.

WT/GC/62G/AG/13Page 22

67. We recall the relevant provisions of the Marrakesh NFIDC Decision regarding access to the resources to the international financial institutions, which provide as follows:

"Ministers recognize that as a result of the Uruguay Round certain developing countries may experience short-term difficulties in financing normal levels of commercial imports and that these countries may be eligible to draw on the resources of international financial institutions under existing facilities, or such facilities as may be established, in the context of adjustment programmes, in order to address such financing difficulties. In this regard Ministers take note of paragraph 37 of the report of the Director-General to the CONTRACTING PARTIES to GATT 1947 on his consultations with the Managing Director of the International Monetary Fund and the President of the World Bank (MTN.GNG/NG14/W/35)."26

We remark that the text of the Decision refers to "existing facilities, or such facilities as may be established, in the context of adjustment programmes". In our view, this provision reflects that access to the resources of the IMF and World Bank is often conditioned by adjustment programmes designed to rectify the underlying economic problems.

68. We note that in the majority of cases, it is expected that future purchases under the CFF would be contingent on undertaking an economic programme under one of the following IMF arrangements: Stand-by Arrangements, Extended Arrangements, or arrangements under the Poverty Reduction and Growth Facility (PRGF). As Table 2 below shows, 6 of the 22 NFIDCs and 22 out of 49 LDCs currently have arrangements with the IMF. So far as countries under arrangements are concerned, it is conceivable that, in the event of temporary cereal price increases on world markets, access to the CFF would entail little "extra" conditionality.

69. We further note that stand-alone access to the CFF is possible. In cases where the balance-of-payments position is satisfactory, apart from the cereal import excess or export shortfall, the IMF allows access to the CFF without an arrangement involving conditionality. In addition, access to the CFF, as to any other IMF facility, entails an assessment of the country's capacity to repay the IMF.

26 See the Marrakesh NFIDC Decision, paragraph 5 (Annex 1).

WT/GC/62G/AG/13

Page 23

Table 2 - LDCs and NFIDCs under arrangements with the International Monetary Fund (as of end June 2002)

Least-Developed Countries WTO Net Food-Importing Developing Countries

Benin (PRGA) Côte d'Ivoire (PRGA)

Burkina Faso (PRGA) Honduras (PRGA)

Cambodia (PRGA) Kenya (PRGA)

Cape Verde (PRGA) Pakistan (PRGA)

Chad (PRGA) Peru (SBA)

Congo, Democratic Republic (PRGA) Sri Lanka (SBA)

Djibouti (PRGA)

Ethiopia (PRGA)

Guinea (PRGA)

Guinea-Bissau (PRGA)

Lao People's Democratic Rep. (PRGA)

Lesotho (PRGA)

Madagascar (PRGA)

Malawi (PRGA)

Mali (PRGA)

Mauritania (PRGA)

Mozambique (PRGA)

Niger (PRGA)

Sao Tomé and Principe (PRGA)

Sierra Leone (PRGA)

Tanzania (PRGA)

Zambia (PRGA)

Key: SBA - Stand-by ArrangementsPRGA - Poverty Reduction and Growth Arrangements

Source: International Monetary Fund, International Financial Statistics, April 2002.

WT/GC/62G/AG/13Page 24

(iv) Lack of concessionality

70. One of the modifications that proponents identified that might make access to the CFF more attractive and consistent with the Marrakesh NFIDC Decision would be to make its resources concessional in terms of interest rate and repayment period.27

71. The CFF is a non-concessional facility in the sense that purchases under it are subject to charges ("interest") on the use of the IMF's General Resources (GRA).28 Currently, those charges are 3.05 percent per year. Still, the IMF generally recommends against poor countries using GRA resources. The issue, however, of whether or not a financing facility is "concessional" depends on the choice of benchmarks. A loan could be considered "concessional", for example, if it was provided at a rate of charge more favourable that the rate of charge governments may have to pay when borrowing from commercial banks.29

2. World Bank facilities

72. Most of the World Bank’s lending and non-lending services are aimed at the root cause of long-term food insecurity: poverty.30 Some investment projects are also aimed at improving trade and distribution facilities, or improving a country’s trade finance infrastructure, thereby reducing vulnerability to disruptions of imports. The World Bank has no facilities that are specifically designed to help countries cope with price shocks, as is the CFF of the IMF. The World Bank does have, however, several instruments to provide urgent assistance when a country is struck by an emergency that seriously dislocates its economy and calls for a quick response, as well as adjustment loans which can provide balance-of-payments support for critically needed imports, including food. Because these facilities reduce the vulnerability of developing and transition economies to food shortages, they are relevant to the deliberations of this Panel.

73. One such type of World Bank instruments is the Import Rehabilitation Loan. This is a quick-disbursing loan to provide support for the government budget and balance-of-payments in periods of crisis. It is specifically targeted at imports that are vital to the functioning of the economy and preservation of a minimal level of well-being of the population. It is a species of adjustment loan, and can include an element of reform conditionality. For example, the Critical Import Rehabilitation Loan was made to Bulgaria in 1997 to help finance primarily grain and oil imports when both domestic production and normal import supply channels were severely disrupted by inappropriate economic policy and political crisis, exacerbated by drought. The loan was conditional on the new Bulgarian Government undertaking a series of basic reforms in economic policy.

74. The World Bank also provides several other types of adjustment loans, which disburse to finance general import expenditures in times when balance-of-payment support is needed for any reason, though in most cases the major reason for the need for special assistance to finance imports is poor macroeconomic management. These loans are specifically designed to support a well-defined reform programme and to help pay for its transitional costs.

75. Other lending and non-lending instruments for emergency recovery assistance have as their objective to restore assets and production levels in the disrupted economy. World Bank emergency

27 See G/AG/11 (dated 28 September 2001), paragraph 6 and G/AG/W/49/Add.1 (dated 23 May 2001), page 4 (Annex 2).

28 The IMF uses "Commercial Interest Reference Rates" published by the OECD in calculating concessionality for the purposes of the debt ceilings used in IMF-supported programs. These rates are based on industrial country government debt yields.

29 On the other hand, commercial banks may provide financing more expeditiously than the IMF under the CFF.

30 See also contribution by the World Bank (Annex 8).

WT/GC/62G/AG/13

Page 25

assistance may take the form of: immediate support in assessing the emergency's impact and developing a recovery strategy; restructuring of the World Bank's existing portfolio for the country, to support recovery activities; redesign of projects not yet approved, to include recovery activities; and, provision of an Emergency Recovery Credit/Loan (ERC/ERL).

76. A very important benefit of a number of World Bank actions in response to a crisis (e.g., restructuring the portfolio to increase disbursements in the near term) has not been the direct elements financed, but the indirect element of providing foreign exchange. The foreign exchange provided enables countries to import food, medicine and other essentials, an ability, which may be reduced by the loss of export earnings and need for emergency imports that characterize drought periods or international food price spikes.

77. Emergency Recovery Loans may include quick-disbursing components, but ERLs are mainly to finance investments to rebuild physical assets and restore economic and social activities after emergencies. ERL activities address restoration of assets and production, rather than relief. They are usually used to finance transport, seeds, fertilizer, etc. which facilitate the capacity of the country or affected farmers to prepare for the following year's crop. As one example, the ERC for Zimbabwe, as a part of the Bank's response to the 1992 drought (US$200 million, combined with other fund reallocations to total roughly US$350 million) was used to deal with multiple elements of the response to the drought, with one of its major contributions being to provide balance-of-payment support that enabled the Government to do many things, including import food, that were not an explicit part of the project. The World Bank made a special (US$10 million) grant to Somalia to finance World Food Programme (WFP) and UNICEF actions in the country that were specifically linked to the provision of food. The food was WFP's, but the delivery was financed by the World Bank.

78. In addition to emergency assistance, the World Bank may support free-standing investment projects for prevention and mitigation in countries prone to specific types of disasters.

3. Other sources of concessional financing

79. Regional financial institutions were contacted by the Panel to enquire about any facilities that address short-term difficulties in financing normal levels of commercial food imports. 31 Two of these institutions, the Arab Monetary Fund and the Asian Development Bank, provided information about their financial facilities.32

(a) The Arab Monetary Fund

80. The Arab Monetary Fund (AMF) provides lending facilities to its member countries that are intended to contribute to the financing of overall balance-of-payments deficits rather than targeting a specific element occasioning such deficits. However, the AMF's facilities include the Compensatory Loan, designed to assist eligible member countries in partly financing an unexpected balance-of-payments deficit arising from either a shortfall of exports or an increase in agricultural imports, particularly cereals. Such a rise in imports must be attributable to reversible exogenous factors beyond the control of the government in question.

81. Access under the Compensatory Loan is limited to 50 per cent of the member country's paid-up subscription in the AMF's capital. The loan is subject to a 4.75 per cent interest charge and is

31 Letters were sent to the Arab Monetary Fund, the Asian Development Bank, the African Development Bank, the Inter-American Development Bank and the Islamic Development Bank.

32 The information submitted by the Arab Monetary Fund and by the Asian Development Bank is attached to this report as Annexes 10 and 11, respectively.

WT/GC/62G/AG/13Page 26

repayable within three years in four equal half-yearly instalments, the first being due 18 months after the date of the loan disbursement.

82. The eligibility criteria require that the member country has a balance-of-payments need, identified by an overall balance-of-payments deficit and a level of foreign reserves below six months of imports of goods and services. The request for the Compensatory Loan should be made during the shortfall year, or the following year. Eventually, a request can be made during the year where the authorities foresee an increase of imports resulting from a shock (or an export shortfall). The increase in imports of foodstuffs is calculated as the difference between the import cost in the shortfall year and the arithmetic average of import costs during the three years centred on the shortfall year.

83. So far, some 12 compensatory loans have been extended to eight AMF member countries, in large part to finance an increase in the value of cereal imports or as a result of drought.

84. In addition, the Arab Trade Financing Progamme (AFTP), an AMF sister-institution, is specialized in the provision of credit aimed at financing inter-Arab imports and exports of virtually all goods and commodities. ATFP charges concessional interest rates compared to market rates for similar transactions.

(b) The Asian Development Bank

85. The Asian Development Bank (ADB) provides various loans to developing member countries, but does not have a special financing facilities for the event of financing difficulties of commercial food imports.

C. PROPOSALS FOR THE ESTABLISHMENT OF A REVOLVING FUND

86. The Panels' terms of reference require us to examine the concept and feasibility of the proposals for the establishment of a revolving fund that were submitted by a group of 17 NFIDCs (Côte d'Ivoire, Cuba, Dominican Republic, Egypt, Honduras, Jamaica, Kenya, Mauritius, Morocco, Pakistan, Peru, Senegal, Sri Lanka, St. Lucia, Trinidad and Tobago, Tunisia and Venezuela).33

1. Main elements of revolving fund proposals

87. The first proposal (G/AG/W/49) takes up three of the areas addressed by the Marrakesh NFIDC Decision, namely food aid, technical and financial assistance, as well as access to the resources of the international financial institutions. In addition, it addresses the issue of establishing binding commitments and reviewing the implementation of these commitments. The second submission (G/AG/W/49/Add.1) elaborates on the concept of the revolving fund intended to address the lack of suitably conditioned short-term financing.34

88. In their first proposal, the sponsors envision the establishment of an inter-agency revolving fund with two components. The first, variable component of this fund would ensure that adequate financing at concessional terms was made available to LDCs and NFIDCs during times of high world market prices for basic foodstuffs. This component would be comprised of existing and/or new financing facilities, as appropriate. The purpose of the second, fixed component of the revolving fund would be to provide technical and financial assistance to LDCs and NFIDCs for specific projects linked to improving agricultural productivity and related infrastructure. The elaborated proposal

33 G/AG/W/49 (dated 19 March 2001) and Add.1 (dated 23 May 2001) and Add.1/Corr.1 (dated 27 June 2001) (Annex 2). In response to questions by the Panel, the proposals were further elaborated by the Cuba, Egypt and Tunisia (Annex 3). Jordan indicates that it supports the proposal (response to question 4, Annex 3).

34 In the proposal, the revolving fund is also referred to as the food financing facility.

WT/GC/62G/AG/13

Page 27

(G/AG/W/49/Add.1) drops the idea of a technical/financial assistance window for agricultural projects. Instead, proponents call on donors to set aside a greater proportion of multilateral and bilateral aid programmes for this purpose.

89. However, in their responses to the Panel's questions, Cuba and Tunisia suggest that part of the resources of the revolving fund should be used to finance capacity building. In their view, the revolving fund should address the long-term problems through projects aimed at increasing productivity and efficiency in basic food production in the countries in question.35

90. In the first proposal, the creation of a financing facility is to be combined with a stockholding scheme for cereals. According to this proposal, in years of plentiful supplies, producing countries would commit to setting aside sufficient national food reserves, in accordance with the normal import requirements as determined by FAO, in addition to volumes required for food aid, emergencies and essential nutritional assistance projects. During times of high world market prices, these reserves would be released to LDCs and NFIDCs at reasonable prices, and thus, together with food aid, would help them meet their normal import requirements. The idea of physical stocks of food grains is not taken up again in the second proposal.36

91. The main elements of the proposal for the establishment of a new short-term financing facility for food imports (revolving fund) are as follows.

(a) Capitalization

92. The proposal estimates initial capital requirements for the revolving fund of around US$1.2 billion, based on an FAO study of the revolving fund.37 The funds are proposed to be drawn from multilateral financial organizations, the G-7 and other donors, as well as major developing countries. During years when import bills are manageable, the proposal indicates that donors could set aside the resources, but not disburse them. Contributions to the revolving fund are to be inscribed in WTO Members' schedules as binding and legally enforceable commitments. Proponents suggest that the Members concerned be required to make regular annual notifications in respect of these commitments.

(b) Eligibility and repayment terms

93. Access to the resources of the revolving fund is to be determined on a country-by-country basis, after a fair assessment of requirements, in accordance with guidelines to be established. The proponents suggest that in periods of surges in import bills, each country's compensation package could be capped in order to maintain the revolving fund's long-term financial viability. The fund's resources would be repayable, which would reduce the initial capital required. Repayments of financial resources received by beneficiaries would be under a medium-term scheme on terms more favourable than market conditions.

35 See Cuba's responses to questions 5 and 8, and Tunisia's response to question 7 (Annex 3).36 In its response to question 8, Egypt indicates that ideally, food stocks held by major suppliers could

be drawn down in the form of food aid when NFIDCs and LDCs have a need. However, in view of the impracticality and expense of maintaining such stocks, the idea of the revolving fund had been proposed instead (Annex 3).