world olefins market: anticipating massive middle east ... - singapore/cmai... · massive middle...

TRANSCRIPT

2008 APIC – CMAI Seminar2008 APIC – CMAI SeminarSingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubaiSingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubai

Steve ZingerSteve ZingerManaging Director Managing Director -- AsiaAsia

Service Leader Service Leader –– Asia OlefinsAsia [email protected]@cmaiglobal.com

APIC Marketing Seminar by CMAIAPIC Marketing Seminar by CMAISingapore, May 27, 2008Singapore, May 27, 2008

World Olefins Market: Anticipating Massive Middle East Capacity and

Satisfying Asian Demand

World Olefins Market: Anticipating World Olefins Market: Anticipating Massive Middle East Capacity and Massive Middle East Capacity and

Satisfying Asian DemandSatisfying Asian Demand

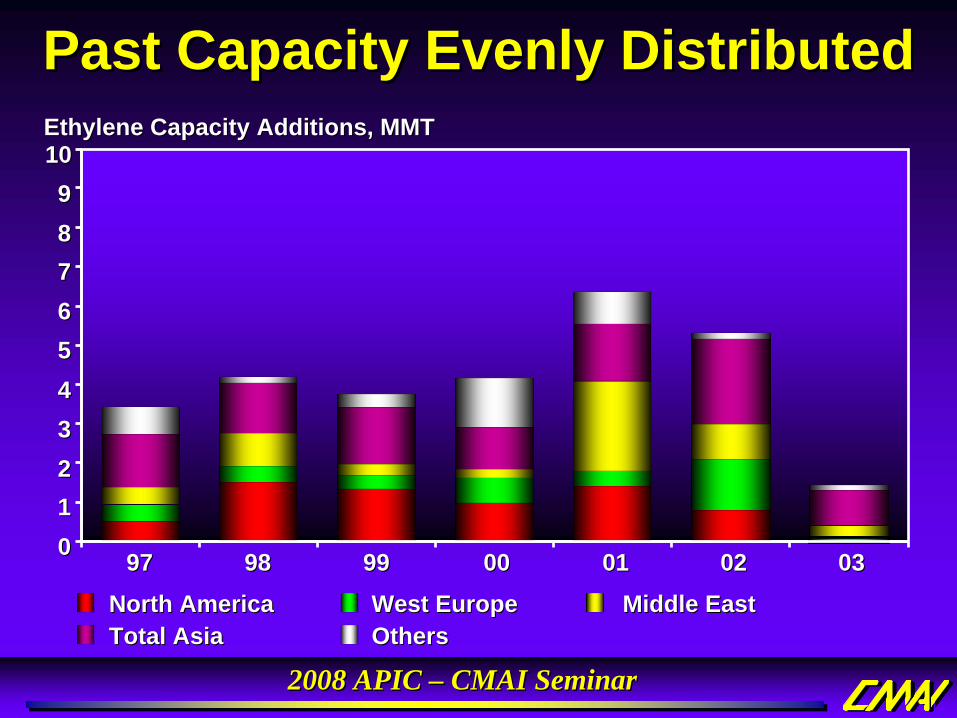

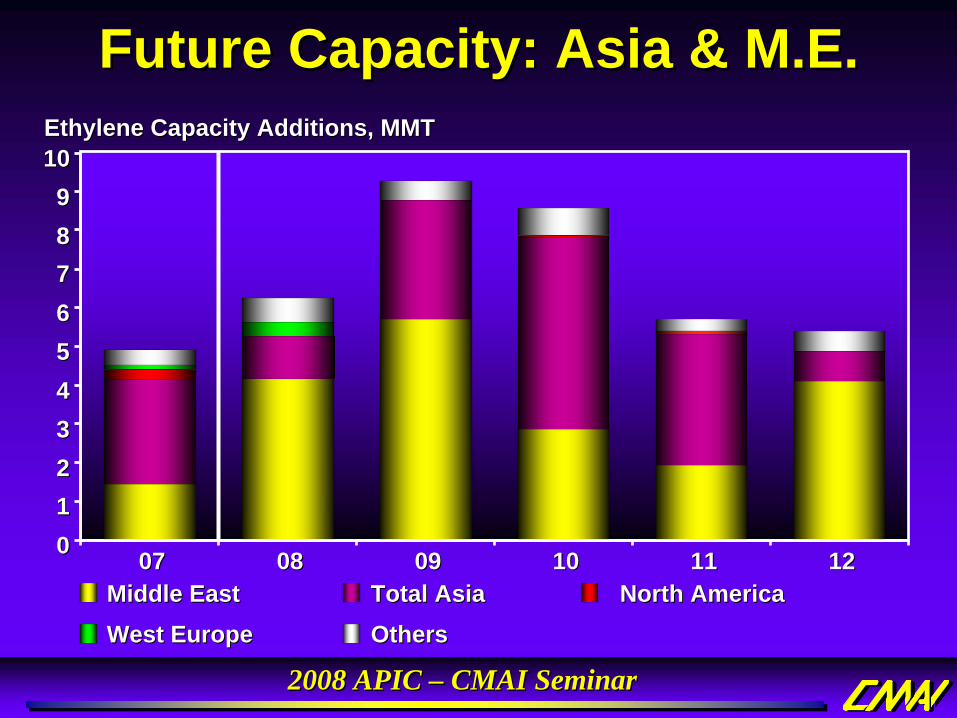

The global olefin markets are now anticipating massive amounts of new Middle East and Asia capacity to start impacting the market by the end of this year. Much of this capacity will be absorbed by rapid demand growth for petrochemicals in Asia, but too much new olefin capacity coming on-line ahead of demand growth during the 2009-2011 period.

The Middle East is investing in large amounts of new ethylene capacity due to very low-cost feedstock availability and the desire to diversify the local economies and provide local employment. The Middle East will also invest heavily in the propylene industry because of the use of heavier cracker feedstocks and the implementation of several on-purpose propylene technologies.

In Asia, China will continue to be the main driver for growth in manufacturing, thirst for raw materials, and ultimately demand for consumer goods. In 2009, China will invest in about 9 million metric tons of new ethylene capacity, inclusive of 3 plants using coal-to-olefins technology. The olefin industries in Japan, Korea, and Taiwan will continue to be very dependent on the growth patterns in China, but new olefin investments in these areas will be very small over the next 5 years in order to avoid competition with the large investments in China and the Middle East. In Southeast Asia, Singapore and Thailand will start-up large amounts of new ethylene capacity in 2009-2011, but other investments are under consideration in Vietnam, Philippines, and Indonesia. India resembles “China” with its strong GDP growth and large population growth, and several significant olefin projects are planned in India over the next five years.

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Past Capacity Evenly DistributedPast Capacity Evenly DistributedPast Capacity Evenly Distributed

North AmericaNorth America West EuropeWest Europe Middle EastMiddle EastTotal AsiaTotal Asia OthersOthers

97 97 98 98 99 99 0000 0101 0202 030300112233445566778899

1010Ethylene Capacity Additions, MMTEthylene Capacity Additions, MMT

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Future Capacity: Asia & M.E.Future Capacity: Asia & M.E.Future Capacity: Asia & M.E.

Middle EastMiddle East Total AsiaTotal Asia North AmericaNorth America

West EuropeWest Europe OthersOthers

0707 0808 0909 1010 1111 121200112233445566778899

1010Ethylene Capacity Additions, MMTEthylene Capacity Additions, MMT

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Asia & Middle East FocusAsia & Middle East FocusAsia & Middle East Focus

• Middle East Capacity Additions– Saudi Arabia– Iran– Others

• Asia Capacity Additions– China– Japan/Korea/Taiwan– Southeast Asia– India

• Global Market Impact

•• Middle East Capacity Middle East Capacity AdditionsAdditions–– Saudi ArabiaSaudi Arabia–– IranIran–– OthersOthers

•• Asia Capacity Asia Capacity AdditionsAdditions–– ChinaChina–– Japan/Korea/TaiwanJapan/Korea/Taiwan–– Southeast AsiaSoutheast Asia–– IndiaIndia

•• Global Market ImpactGlobal Market Impact

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

The Olefin Story in Middle EastThe Olefin Story in Middle EastThe Olefin Story in Middle East• Over 9 MMT new ethylene and

4 MMT new propylene coming on-line in 2008-9

• Low feedstock costs produce ethylene at $100-200 per ton

• Diversifying economy & providing jobs are a key investment factor

• Mostly PE, MEG, and PP; but other derivatives coming

• Heavier cracker feedstocks produce significant propylene

• Propane dehydro, metathesis and HS FCC more common

•• Over 9 MMT new ethylene and Over 9 MMT new ethylene and 4 MMT new propylene coming 4 MMT new propylene coming onon--line in 2008line in 2008--99

•• Low feedstock costs produce Low feedstock costs produce ethylene at $100ethylene at $100--200 per ton200 per ton

•• Diversifying economy & Diversifying economy & providing jobs are a key providing jobs are a key investment factorinvestment factor

•• Mostly PE, MEG, and PP; but Mostly PE, MEG, and PP; but other derivatives comingother derivatives coming

•• Heavier cracker feedstocks Heavier cracker feedstocks produce significant propylene produce significant propylene

•• Propane dehydro, metathesis Propane dehydro, metathesis and HS FCC more commonand HS FCC more common

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

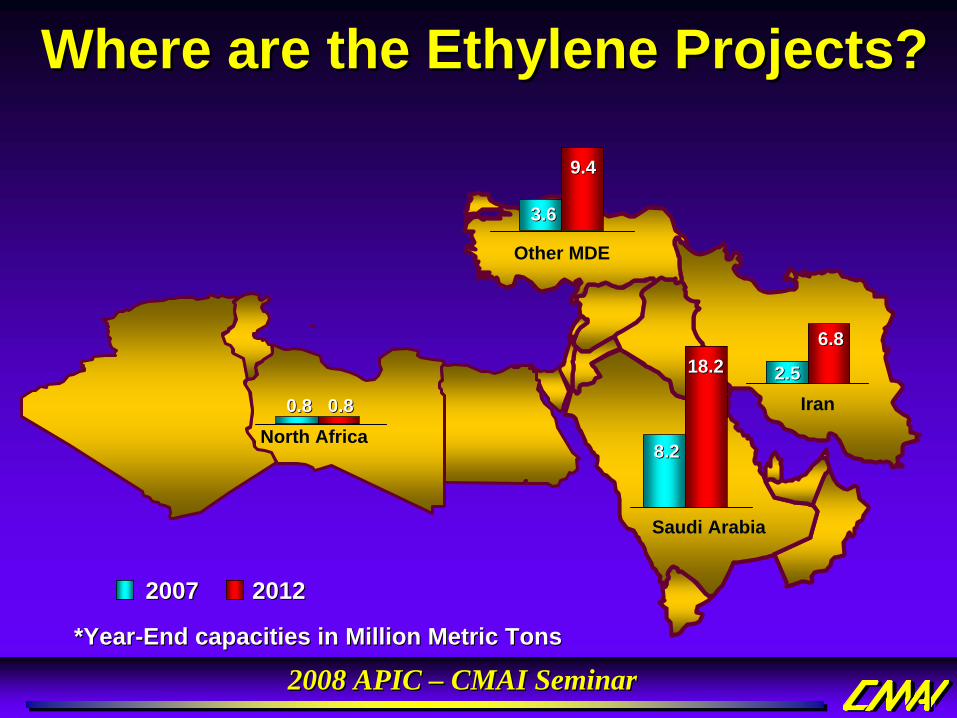

Where are the Ethylene Projects?Where are the Ethylene Projects?Where are the Ethylene Projects?

3.63.6

Other MDE

0.80.8North Africa

2.52.5

8.28.2

20072007

*Year*Year--End capacities in Million Metric TonsEnd capacities in Million Metric Tons

Saudi Arabia

9.49.4

0.80.8

6.86.818.218.2

20122012

Iran

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

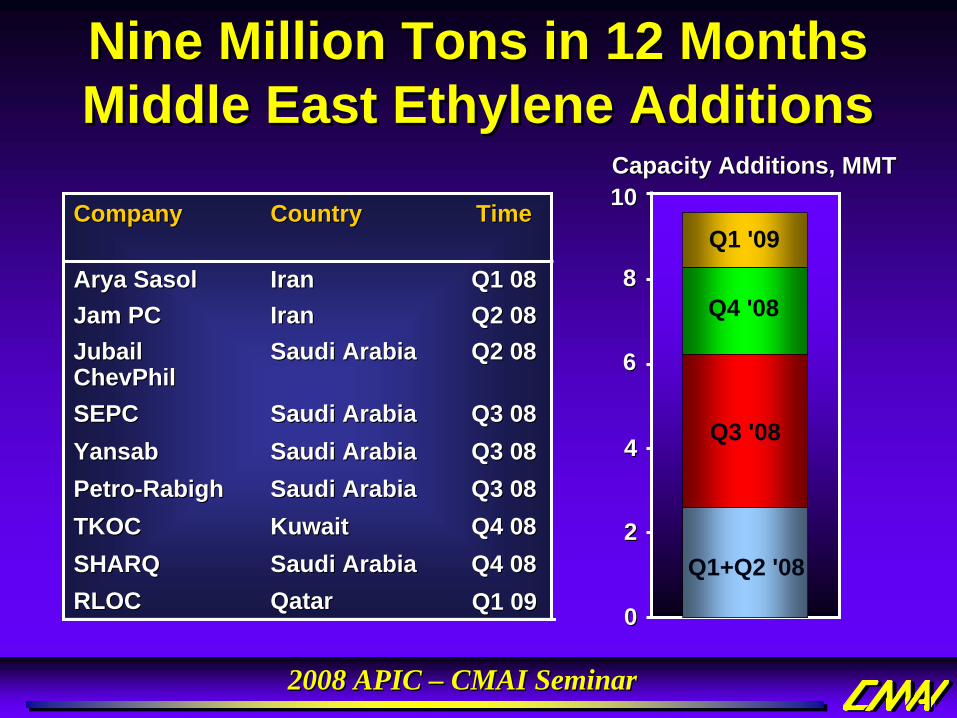

Nine Million Tons in 12 MonthsMiddle East Ethylene AdditionsNine Million Tons in 12 MonthsNine Million Tons in 12 MonthsMiddle East Ethylene AdditionsMiddle East Ethylene Additions

Q2 08Q2 08Saudi ArabiaSaudi ArabiaJubail Jubail ChevPhilChevPhil

TimeTimeCountryCountryCompanyCompany

Q3 08Q3 08Saudi ArabiaSaudi ArabiaPetroPetro--RabighRabighQ3 08Q3 08Saudi ArabiaSaudi ArabiaYansabYansabQ3 08Q3 08Saudi ArabiaSaudi ArabiaSEPCSEPC

Q4 08Q4 08KuwaitKuwaitTKOCTKOC

Q1 09Q1 09QatarQatarRLOCRLOCQ4 08Q4 08Saudi ArabiaSaudi ArabiaSHARQSHARQ

Q2 08Q2 08IranIranJam PCJam PCQ1 08Q1 08IranIranArya SasolArya Sasol

00

22

44

66

88

1010Capacity Additions, MMTCapacity Additions, MMT

Q1+Q2 '08

Q4 '08

Q3 '08

Q1 '09

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

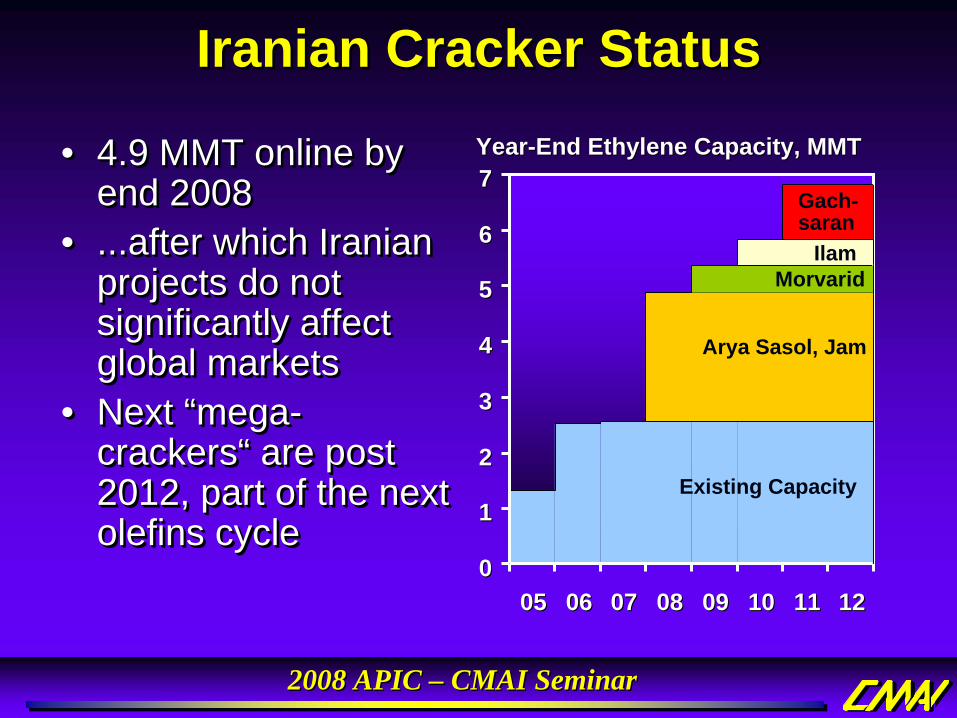

Iranian Cracker StatusIranian Cracker StatusIranian Cracker Status

• 4.9 MMT online by end 2008

• ...after which Iranian projects do not significantly affect global markets

• Next “mega-crackers“ are post 2012, part of the next olefins cycle

•• 4.9 MMT online by 4.9 MMT online by end 2008end 2008

•• ...after which Iranian ...after which Iranian projects do not projects do not significantly affect significantly affect global marketsglobal markets

•• Next Next ““megamega--crackerscrackers““ are post are post 2012, part of the next 2012, part of the next olefins cycleolefins cycle

00

11

22

33

44

55

66

77

0505 0606 0707 0808 0909 1010 1111 1212

YearYear--End Ethylene Capacity, MMTEnd Ethylene Capacity, MMT

Arya Sasol, Jam

Existing Capacity

Gach-saran

IlamMorvarid

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

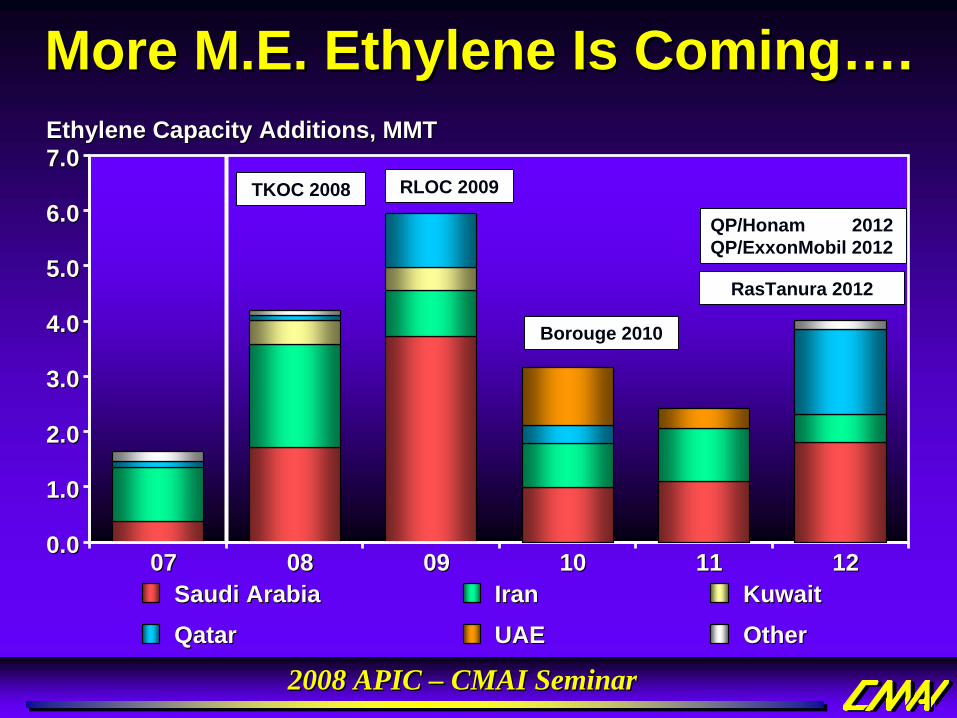

More M.E. Ethylene Is Coming….More M.E. Ethylene Is ComingMore M.E. Ethylene Is Coming……..

OtherOtherUAEUAEQatarQatarKuwaitKuwaitIranIranSaudi ArabiaSaudi Arabia

0707 0808 0909 1010 1111 12120.00.0

1.01.0

2.02.0

3.03.0

4.04.0

5.05.0

6.06.0

7.07.0Ethylene Capacity Additions, MMTEthylene Capacity Additions, MMT

QP/Honam 2012QP/ExxonMobil 2012

Borouge 2010

RasTanura 2012

TKOC 2008 RLOC 2009

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

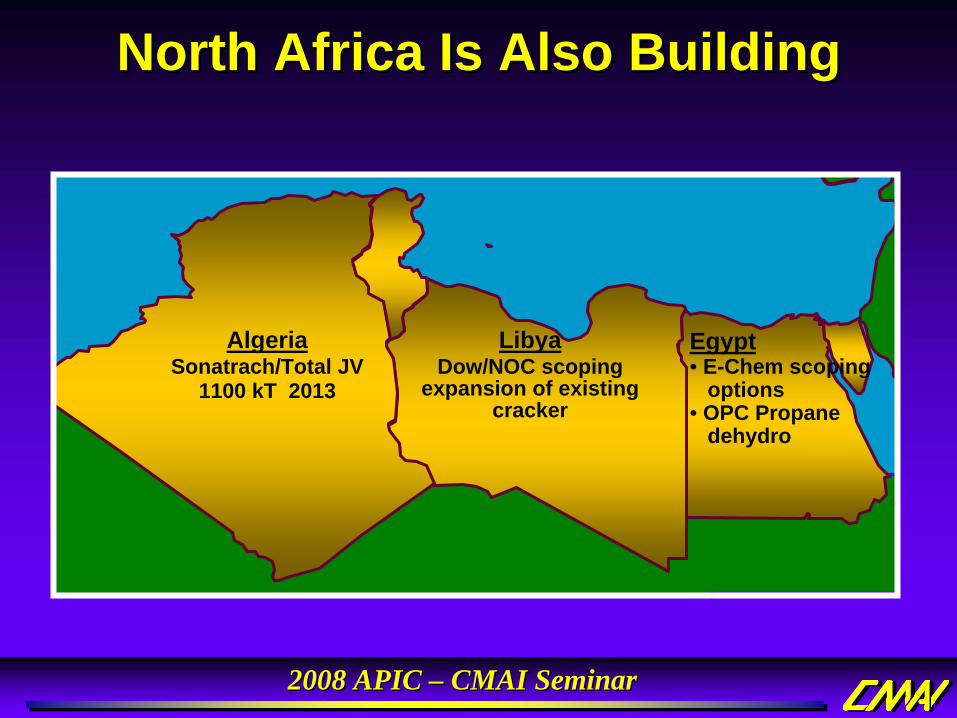

North Africa Is Also BuildingNorth Africa Is Also BuildingNorth Africa Is Also Building

AlgeriaSonatrach/Total JV

1100 kT 2013

LibyaDow/NOC scoping

expansion of existing cracker

Egypt• E-Chem scoping

options• OPC Propane

dehydro

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

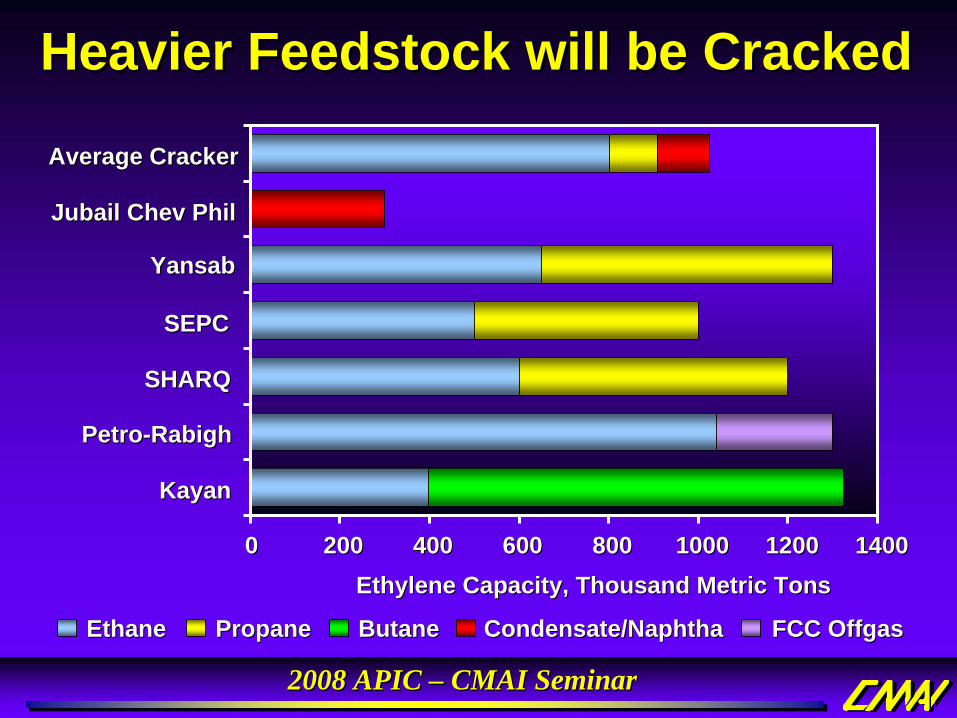

EthaneEthane PropanePropane ButaneButane Condensate/NaphthaCondensate/Naphtha FCC OffgasFCC Offgas

Heavier Feedstock will be CrackedHeavier Feedstock will be CrackedHeavier Feedstock will be Cracked

00 200200 400400 600600 800800 10001000 12001200 14001400

KayanKayan

PetroPetro--RabighRabigh

SHARQSHARQ

SEPCSEPC

YansabYansab

Jubail Chev PhilJubail Chev Phil

Average CrackerAverage Cracker

Ethylene Capacity, Thousand Metric TonsEthylene Capacity, Thousand Metric Tons

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

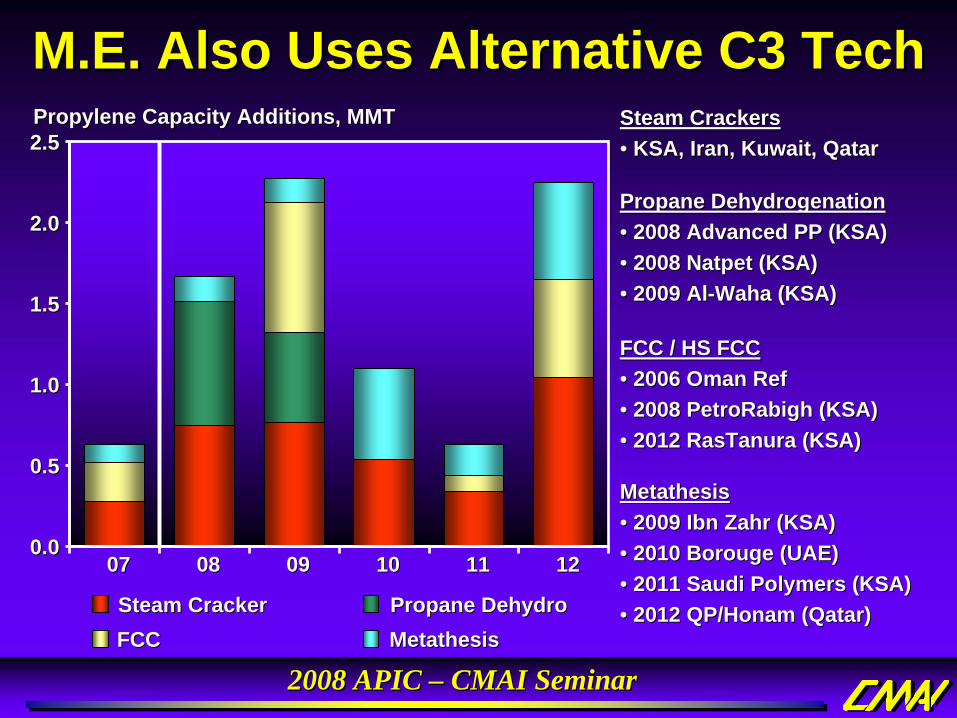

M.E. Also Uses Alternative C3 TechM.E. Also Uses Alternative C3 TechM.E. Also Uses Alternative C3 Tech

Steam CrackerSteam Cracker Propane DehydroPropane DehydroFCCFCC MetathesisMetathesis

0707 0808 0909 1010 1111 12120.00.0

0.50.5

1.01.0

1.51.5

2.02.0

2.52.5Propylene Capacity Additions, MMTPropylene Capacity Additions, MMT

MetathesisMetathesis•• 2009 Ibn Zahr (KSA)2009 Ibn Zahr (KSA)•• 2010 Borouge (UAE)2010 Borouge (UAE)•• 2011 Saudi Polymers (KSA)2011 Saudi Polymers (KSA)•• 2012 QP/Honam (Qatar)2012 QP/Honam (Qatar)

FCC / HS FCCFCC / HS FCC•• 2006 Oman Ref2006 Oman Ref•• 2008 PetroRabigh (KSA)2008 PetroRabigh (KSA)•• 2012 RasTanura (KSA)2012 RasTanura (KSA)

Propane DehydrogenationPropane Dehydrogenation•• 2008 Advanced PP (KSA)2008 Advanced PP (KSA)•• 2008 Natpet (KSA)2008 Natpet (KSA)•• 2009 Al2009 Al--Waha (KSA)Waha (KSA)

Steam CrackersSteam Crackers•• KSA, Iran, Kuwait, QatarKSA, Iran, Kuwait, Qatar

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

The Olefin Story in AsiaThe Olefin Story in AsiaThe Olefin Story in Asia

• China will continue to have explosive growth

• Japan, Korea, Taiwan will feed the Chinese giant

• SE Asia continues to attract investors

• India possibly the next China

•• China will continue to China will continue to have explosive growthhave explosive growth

•• Japan, Korea, Taiwan Japan, Korea, Taiwan will feed the Chinese will feed the Chinese giantgiant

•• SE Asia continues to SE Asia continues to attract investorsattract investors

•• India possibly the next India possibly the next ChinaChina

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

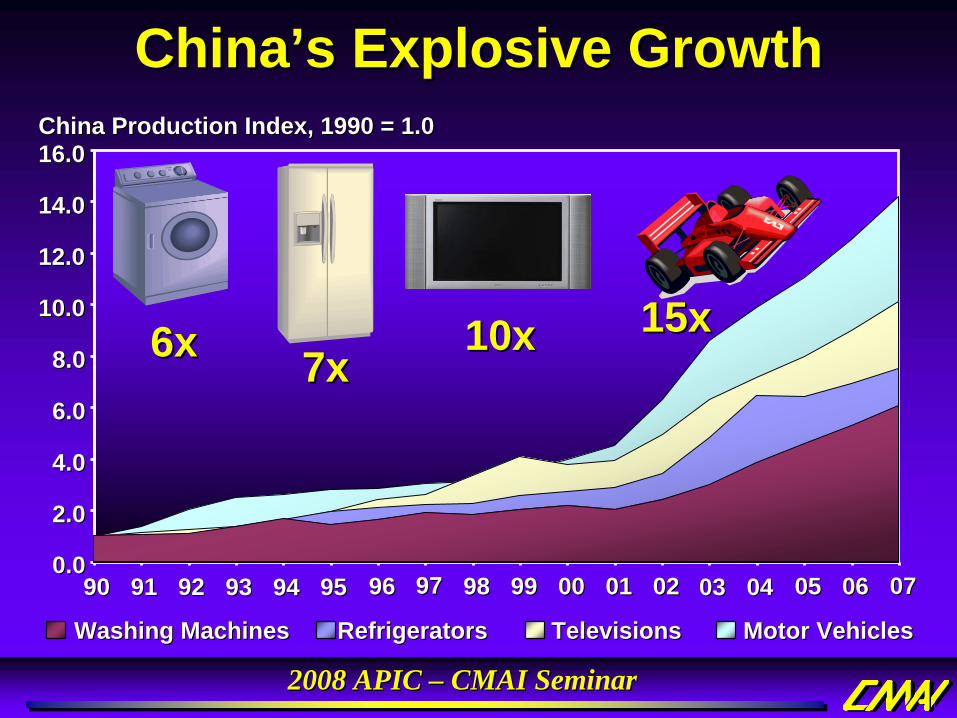

China’s Explosive GrowthChinaChina’’s Explosive Growths Explosive Growth

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 07070.00.0

2.02.0

4.04.0

6.06.0

8.08.0

10.010.0

12.012.0

14.014.0

16.016.0China Production Index, 1990 = 1.0 China Production Index, 1990 = 1.0

Motor VehiclesMotor VehiclesTelevisionsTelevisionsRefrigeratorsRefrigeratorsWashing MachinesWashing Machines

6x6x 7x7x10x10x 15x15x

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

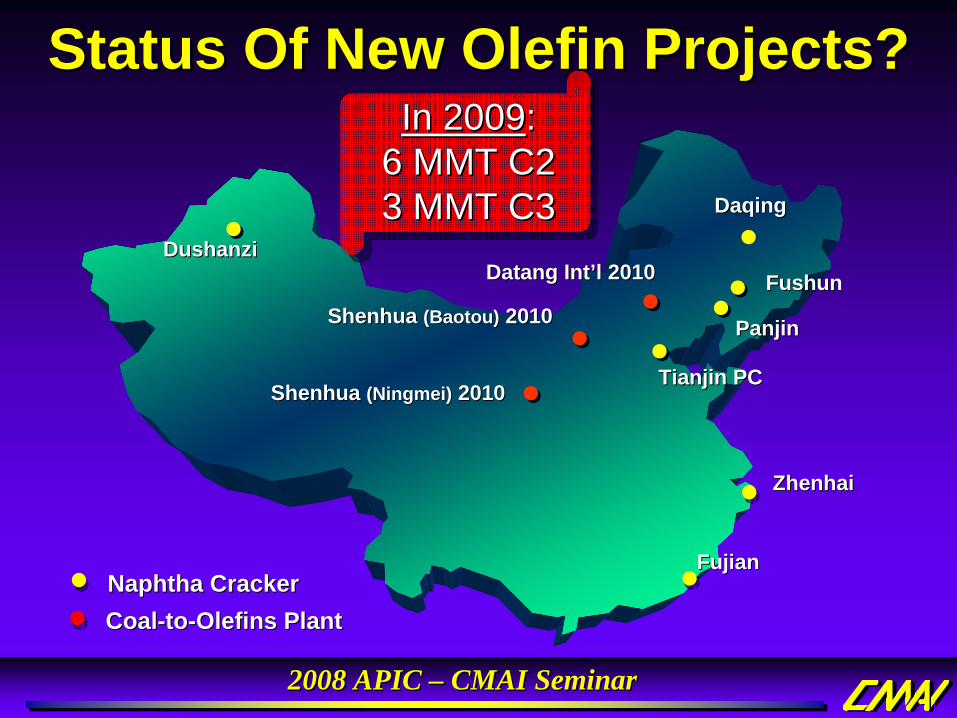

Status Of New Olefin Projects?Status Of New Olefin Projects?Status Of New Olefin Projects?

DushanziDushanzi

FujianFujian

ZhenhaiZhenhai

DaqingDaqing

FushunFushun

PanjinPanjin

Tianjin PCTianjin PC

In 2009In 2009: : 6 MMT C2 6 MMT C2 3 MMT C33 MMT C3

Naphtha CrackerNaphtha Cracker

Shenhua Shenhua (Ningmei)(Ningmei) 20102010

Shenhua Shenhua (Baotou)(Baotou) 20102010

Datang IntDatang Int’’l 2010l 2010

CoalCoal--toto--Olefins PlantOlefins Plant

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Why Does China Like Coal?Why Does China Like Coal?Why Does China Like Coal?

• Second largest coal reserves in the world

• National energy and petrochemical security

• Development provides inland jobs

•• Second largest coal Second largest coal reserves in the worldreserves in the world

•• National energy and National energy and petrochemical securitypetrochemical security

•• Development provides Development provides inland jobsinland jobs

• Coal is cheaper than crude oil based industry

•• Coal is cheaper than Coal is cheaper than crude oil based crude oil based industryindustry

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

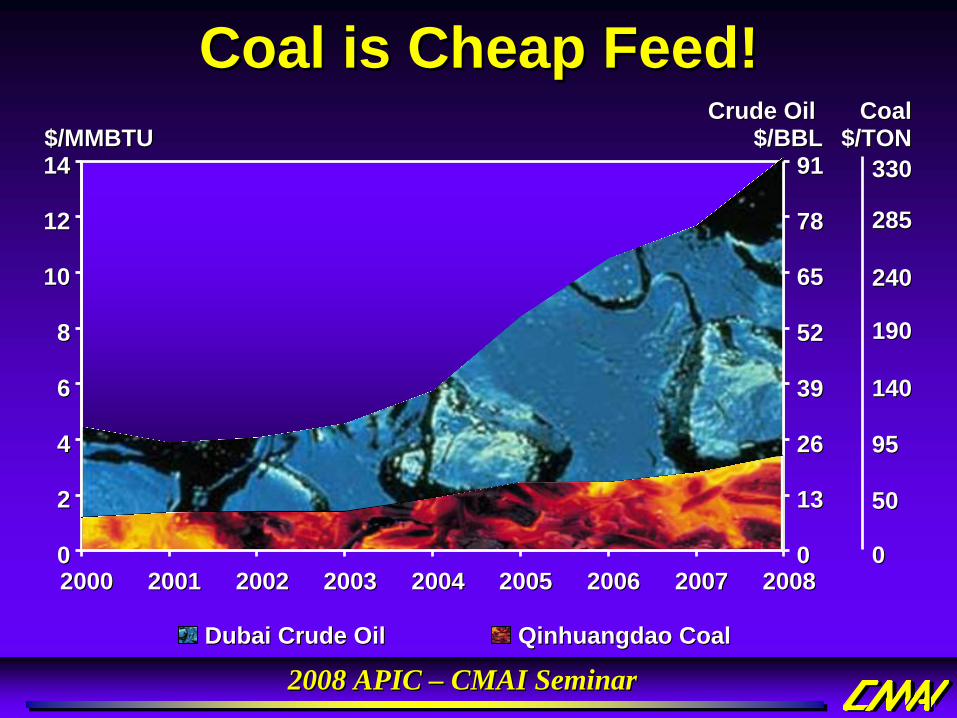

Coal is Cheap Feed!Coal is Cheap Feed!Coal is Cheap Feed!

Dubai Crude OilDubai Crude Oil

20002000 20012001 20022002 20032003 20042004 20052005 20062006 20072007 2008200800

22

44

66

88

1010

1212

1414$/MMBTU$/MMBTU

00

1313

2626

3939

5252

6565

7878

9191

Crude Oil Crude Oil $/BBL$/BBL

Qinhuangdao CoalQinhuangdao Coal

CoalCoal$/TON$/TON

330330

285285

240240

5050

9595

140140

190190

00

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

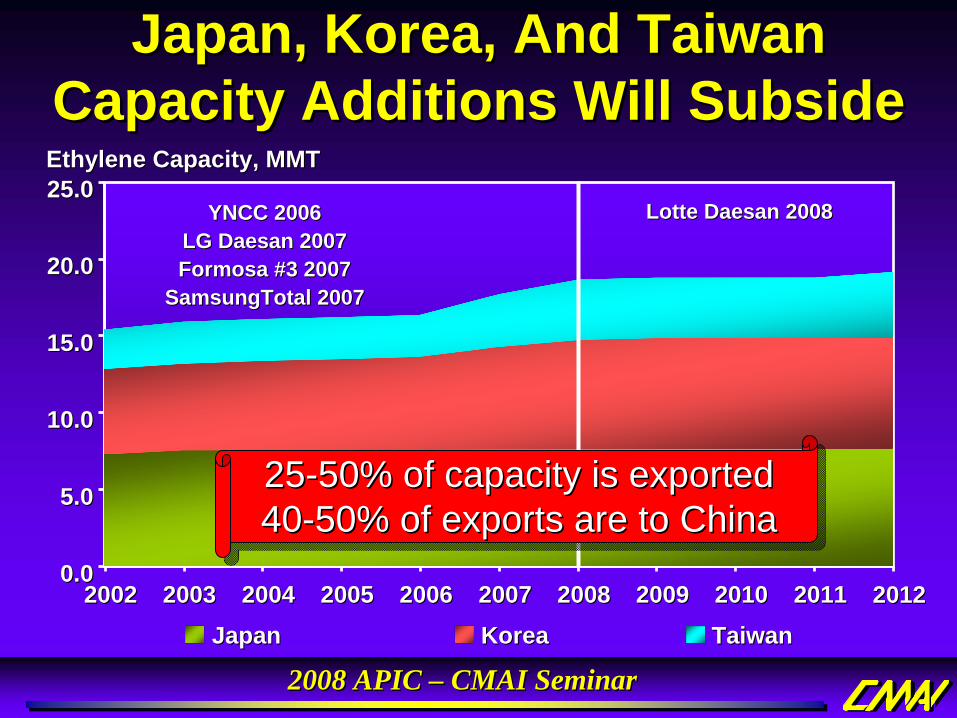

Japan, Korea, And TaiwanCapacity Additions Will Subside

Japan, Korea, And TaiwanJapan, Korea, And TaiwanCapacity Additions Will SubsideCapacity Additions Will Subside

TaiwanTaiwanKoreaKoreaJapanJapan

Ethylene Capacity, MMTEthylene Capacity, MMT

0.00.0

5.05.0

10.010.0

15.015.0

20.020.0

25.025.0

20022002 20032003 20042004 20052005 20062006 20072007 20082008 20092009 20102010 20112011 20122012

YNCC 2006YNCC 2006LG Daesan 2007LG Daesan 2007Formosa #3 2007Formosa #3 2007

SamsungTotal 2007SamsungTotal 2007

Lotte Daesan 2008Lotte Daesan 2008

2525--50% of capacity is exported 50% of capacity is exported 4040--50% of exports are to China50% of exports are to China

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

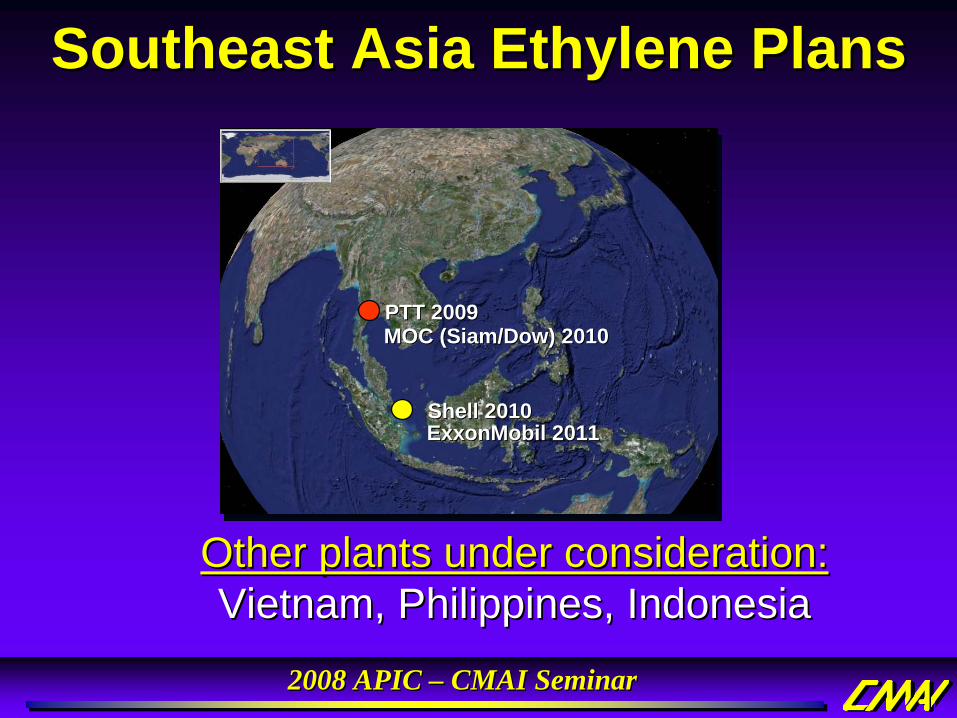

Southeast Asia Ethylene PlansSoutheast Asia EthyleneSoutheast Asia Ethylene PlansPlans

Shell 2010Shell 2010ExxonMobil 2011 ExxonMobil 2011

PTT 2009PTT 2009MOC (Siam/Dow) 2010MOC (Siam/Dow) 2010

Other plants under consideration: Other plants under consideration: Vietnam, Philippines, IndonesiaVietnam, Philippines, Indonesia

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Is India The Next China As A Major Petrochemical Player?Is India The Next China As A Is India The Next China As A Major Petrochemical Player?Major Petrochemical Player?

• How is India like China?+ Strong GDP Growth+ Large Population+ Transformation of poor to

middle class

•• How is India How is India likelike China?China?++ Strong GDP GrowthStrong GDP Growth++ Large PopulationLarge Population++ Transformation of poor to Transformation of poor to

middle classmiddle class

• How is India unlike China?– Poorer infrastructure– / + Different political landscape+ Growing population

•• How is India How is India unlikeunlike China?China?–– Poorer infrastructurePoorer infrastructure–– / + Different political landscape/ + Different political landscape++ Growing populationGrowing population

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

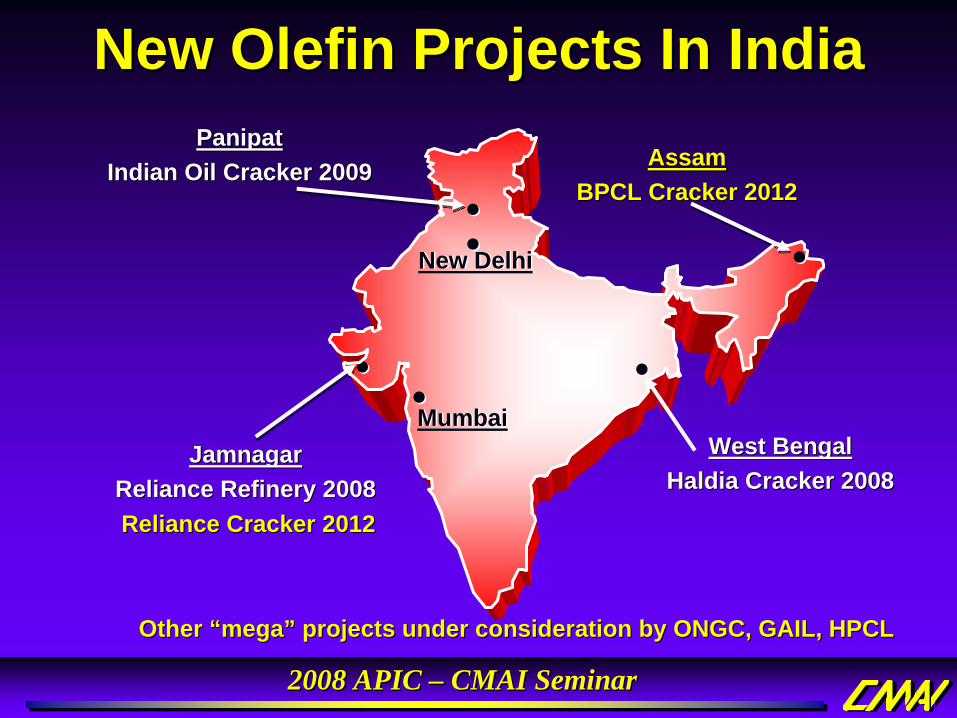

New Olefin Projects In IndiaNew Olefin Projects In IndiaNew Olefin Projects In India

New DelhiNew Delhi

MumbaiMumbaiJamnagarJamnagar

Reliance Refinery 2008Reliance Refinery 2008

PanipatPanipatIndian Oil Cracker 2009Indian Oil Cracker 2009 AssamAssam

BPCL Cracker 2012BPCL Cracker 2012

Other Other ““megamega”” projects under consideration by ONGC, GAIL, HPCLprojects under consideration by ONGC, GAIL, HPCL

West BengalWest BengalHaldia Cracker 2008Haldia Cracker 2008

Reliance Cracker 2012Reliance Cracker 2012

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

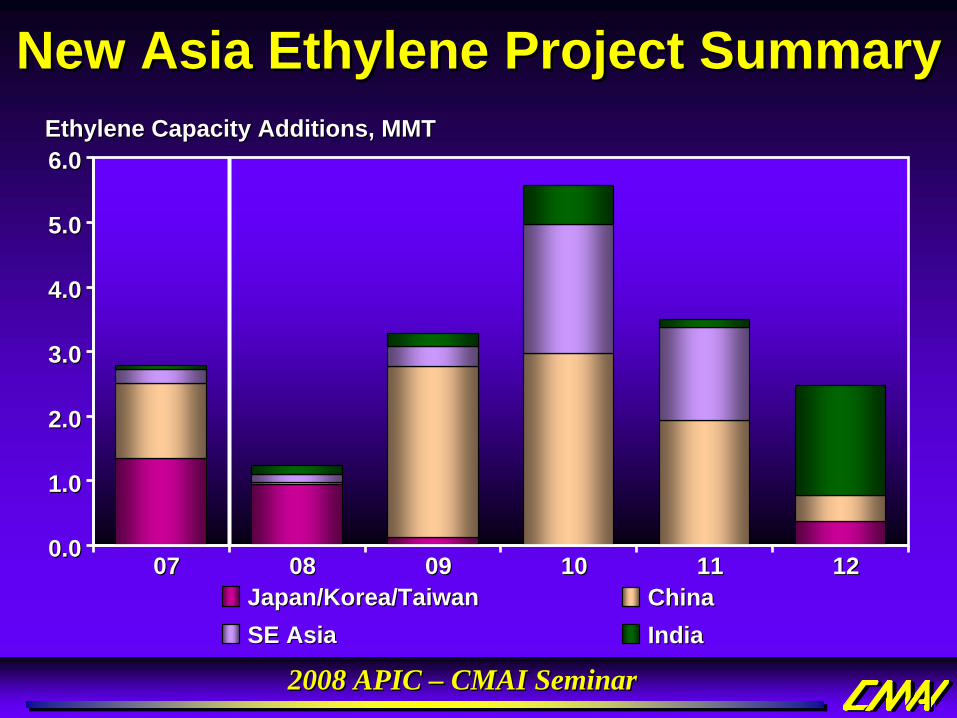

New Asia Ethylene Project SummaryNew Asia Ethylene Project SummaryNew Asia Ethylene Project Summary

Japan/Korea/TaiwanJapan/Korea/Taiwan ChinaChinaSE AsiaSE Asia IndiaIndia

0707 0808 0909 1010 1111 12120.00.0

1.01.0

2.02.0

3.03.0

4.04.0

5.05.0

6.06.0Ethylene Capacity Additions, MMT Ethylene Capacity Additions, MMT

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

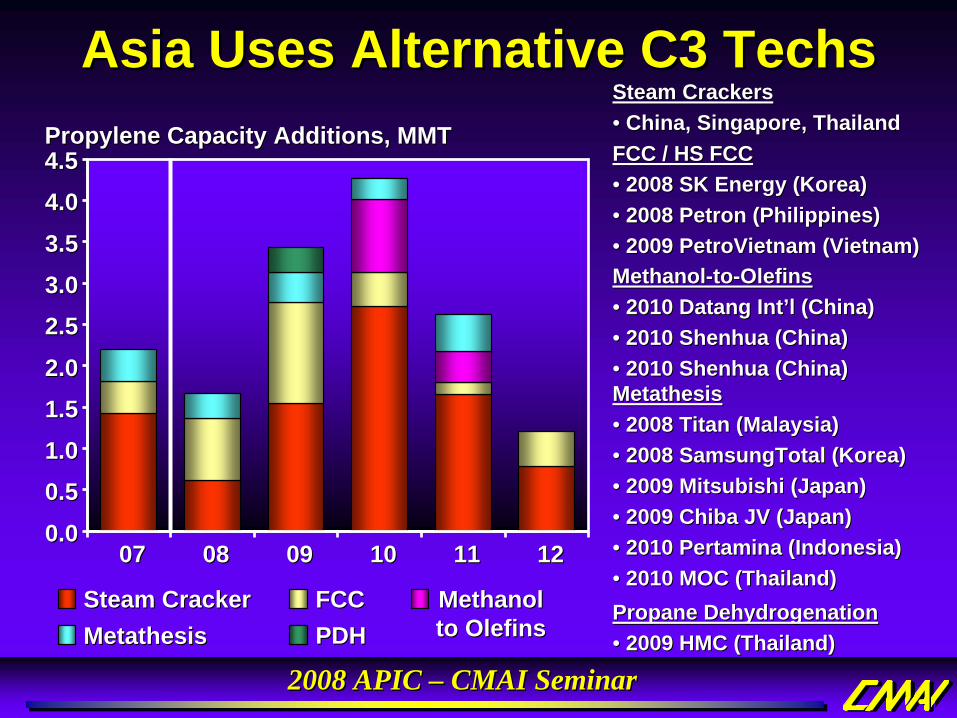

Asia Uses Alternative C3 TechsAsia Uses Alternative C3 TechsAsia Uses Alternative C3 Techs

Steam CrackerSteam Cracker FCCFCC Methanol Methanol to Olefinsto OlefinsMetathesisMetathesis PDHPDH

0707 0808 0909 1010 1111 12120.00.00.50.51.01.01.51.52.02.02.52.53.03.03.53.54.04.04.54.5Propylene Capacity Additions, MMTPropylene Capacity Additions, MMT

MetathesisMetathesis•• 2008 Titan (Malaysia)2008 Titan (Malaysia)•• 2008 SamsungTotal (Korea)2008 SamsungTotal (Korea)•• 2009 Mitsubishi (Japan)2009 Mitsubishi (Japan)•• 2009 Chiba JV (Japan)2009 Chiba JV (Japan)•• 2010 Pertamina (Indonesia)2010 Pertamina (Indonesia)•• 2010 MOC (Thailand)2010 MOC (Thailand)

FCC / HS FCCFCC / HS FCC•• 2008 SK Energy (Korea)2008 SK Energy (Korea)•• 2008 Petron (Philippines)2008 Petron (Philippines)•• 2009 PetroVietnam (Vietnam)2009 PetroVietnam (Vietnam)

Propane DehydrogenationPropane Dehydrogenation•• 2009 HMC (Thailand)2009 HMC (Thailand)

Steam CrackersSteam Crackers•• China, Singapore, ThailandChina, Singapore, Thailand

MethanolMethanol--toto--OlefinsOlefins•• 2010 Datang Int2010 Datang Int’’l (China)l (China)•• 2010 Shenhua (China)2010 Shenhua (China)•• 2010 Shenhua (China)2010 Shenhua (China)

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

Olefins… The Next Five YearsOlefinsOlefins…… The Next Five YearsThe Next Five Years

• Production costs?

• Trade flow?

• Operating rates and margins?

•• Production costs?Production costs?

•• Trade flow?Trade flow?

•• Operating rates and Operating rates and margins?margins?

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

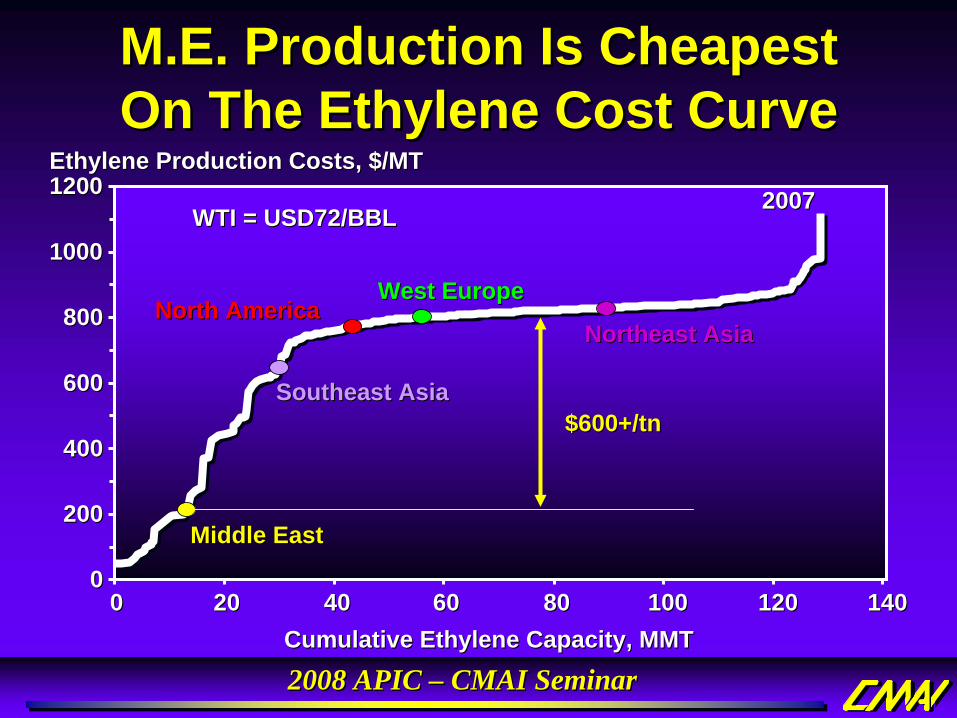

M.E. Production Is Cheapest On The Ethylene Cost CurveM.E. Production Is Cheapest M.E. Production Is Cheapest On The Ethylene Cost CurveOn The Ethylene Cost Curve

Cumulative Ethylene Capacity, MMTCumulative Ethylene Capacity, MMT

West EuropeWest Europe

Southeast AsiaSoutheast Asia

Northeast AsiaNortheast AsiaNorth AmericaNorth America

00 2020 4040 6060 8080 100100 120120 140140

20072007

00

200200

400400

600600

800800

10001000

12001200Ethylene Production Costs, $/MT Ethylene Production Costs, $/MT

Middle EastMiddle East

$600+/tn$600+/tn

WTI = USD72/BBLWTI = USD72/BBL

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

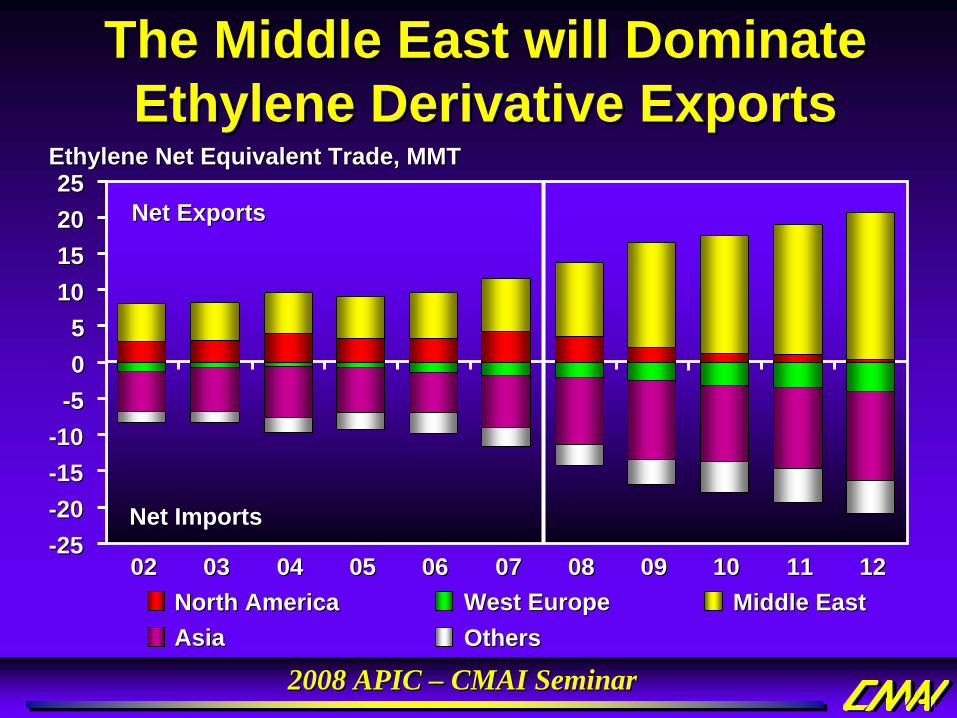

The Middle East will Dominate Ethylene Derivative Exports

The Middle East will Dominate The Middle East will Dominate Ethylene Derivative ExportsEthylene Derivative Exports

North AmericaNorth America West EuropeWest Europe Middle EastMiddle EastAsiaAsia OthersOthers

Ethylene Net Equivalent Trade, MMTEthylene Net Equivalent Trade, MMT

--2525--2020--1515--1010

--550055

1010151520202525

0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212

Net ExportsNet Exports

Net ImportsNet Imports

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

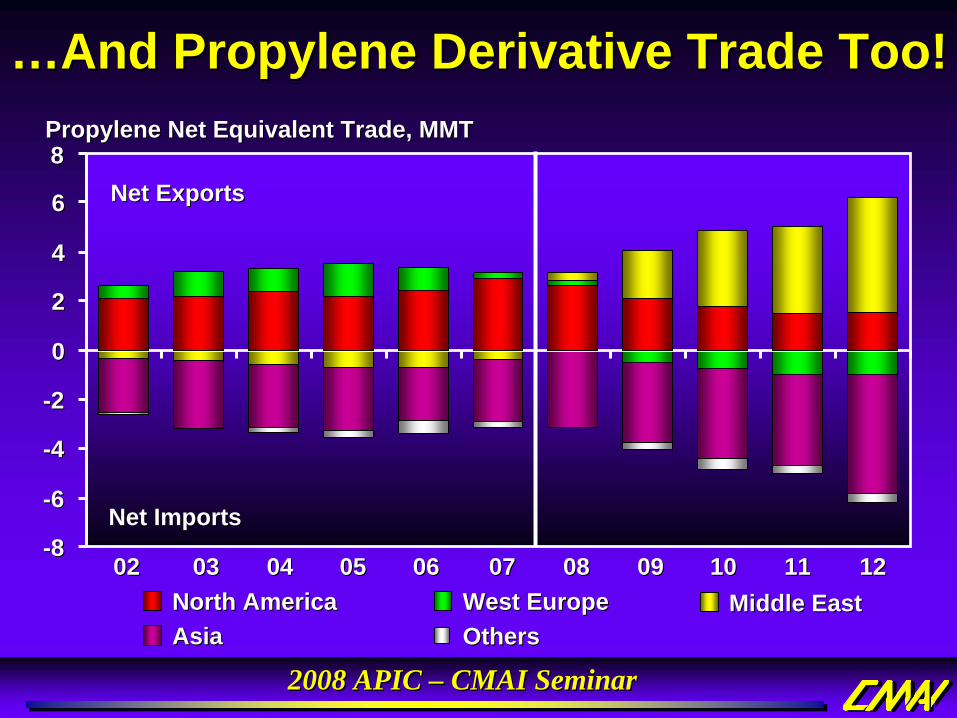

……And Propylene Derivative Trade Too!And Propylene Derivative Trade Too!

North AmericaNorth America West EuropeWest Europe Middle EastMiddle EastAsiaAsia OthersOthers

Propylene Net Equivalent Trade, MMTPropylene Net Equivalent Trade, MMT

--88

--66

--44

--22

00

22

44

66

88Net ExportsNet Exports

Net ImportsNet Imports

0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

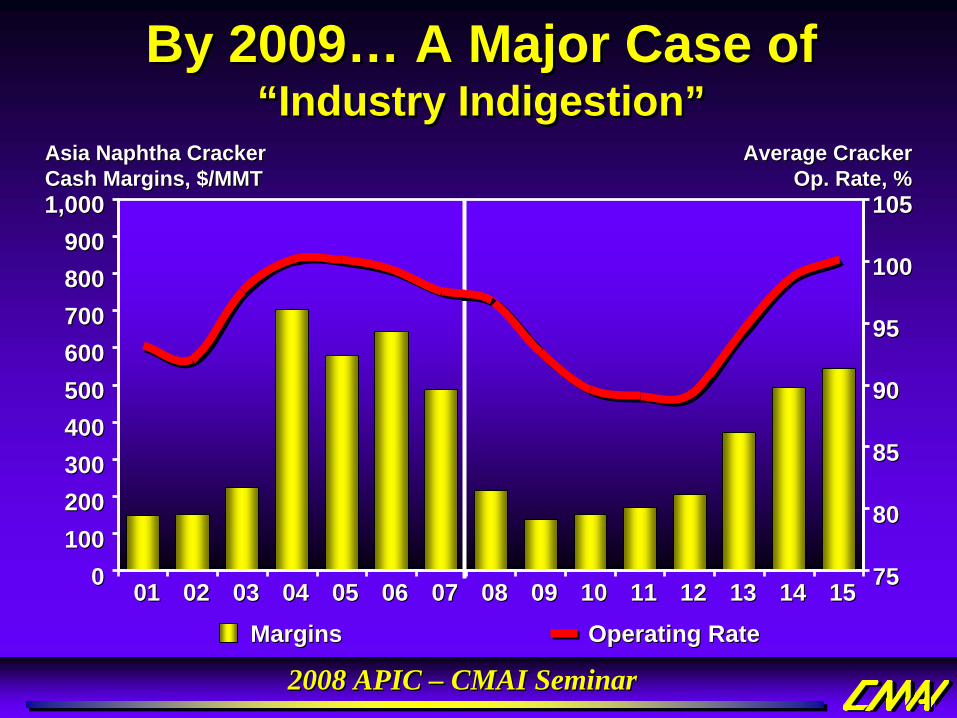

By 2009… A Major Case of “Industry Indigestion”

By 2009By 2009…… A Major Case of A Major Case of ““Industry IndigestionIndustry Indigestion””

MarginsMargins Operating RateOperating Rate0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212 1313 1414 151500

100100200200300300400400500500600600700700800800900900

1,0001,000

Asia Naphtha Cracker Asia Naphtha Cracker Cash Margins, $/MMTCash Margins, $/MMT

7575

8080

8585

9090

9595

100100

105105

Average CrackerAverage CrackerOp. Rate, %Op. Rate, %

2008 APIC – CMAI Seminar2008 APIC – CMAI Seminar

ConclusionsConclusionsConclusions• Most olefin investment in

the Middle East or Asia– Make friends with the

Middle East and Asian Olefin Giants!

•• Most olefin investment in Most olefin investment in the Middle East or Asiathe Middle East or Asia–– Make friends with the Make friends with the

Middle East and Asian Middle East and Asian Olefin Giants!Olefin Giants!

• Upcoming margin trough is unavoidable for olefins & olefin derivative producers– Look for opportunities to compete (survive)!

• Align with customers with differentiated products• Venture with low feedstock costs in ME, Africa, & Russia• Feedstock flexibility to LPG, Condensates• Alternative feedstocks & technologies• Refinery integration & synergies• Propylene & butadiene co-products

•• Upcoming margin trough is unavoidable Upcoming margin trough is unavoidable for olefins & olefin derivative producersfor olefins & olefin derivative producers–– Look for opportunities to compete (survive)!Look for opportunities to compete (survive)!

•• Align with customers with differentiated productsAlign with customers with differentiated products•• Venture with low feedstock costs in ME, Africa, & RussiaVenture with low feedstock costs in ME, Africa, & Russia•• Feedstock flexibility to LPG, CondensatesFeedstock flexibility to LPG, Condensates•• Alternative feedstocks & technologiesAlternative feedstocks & technologies•• Refinery integration & synergiesRefinery integration & synergies•• Propylene & butadiene coPropylene & butadiene co--productsproducts