world financial symposium - iata - · pdf fileyesterday, effective today); and ... oman to...

TRANSCRIPT

World Financial Symposium 2017World Financial Symposium 2014

World Financial Symposium 27 – 28 September 2017

Convention Center Dublin (CCD) – Ireland

World Financial Symposium 2017World Financial Symposium 2014

Complex Taxes

World Financial Symposium 2017World Financial Symposium 2014

IATA Taxation Advocacy: An Interactive Workshop

Charlotte FantoliAssistant Director, Industry Taxation, IATA

Gregory LeshchukManager, Industry Taxation, IATA

World Financial Symposium 2016

Introduction In 2017, airlines and their customers are forecast to generate $123 billion in tax revenues globally

(up from $118 billion in 2016). That’s the equivalent of 45% of the industry’s GVA (Gross Value Added), paid to governments.

Passenger demand for air travel is highly price elastic (i.e. sensitive to changes in price). A 10% increase in price can lead to a reduction in demand of up to 15%.

Unwarranted or excessive taxation on air transport has a negative impact on economic and social development

IATA does not object to the payment of non-discriminatory, justly and equitably levied taxes. We do object most strenuously to taxes that are discriminatory (single out the aviation) or that are imposed contrary to ICAO and standard international principles

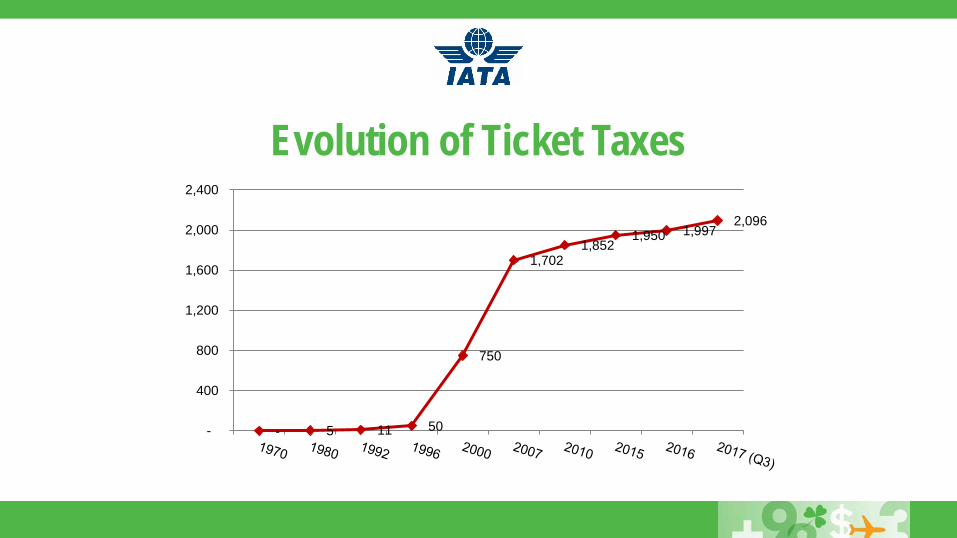

World Financial Symposium 2016- 5 11 50

750

1,702 1,852

1,950 1,997 2,096

-

400

800

1,200

1,600

2,000

2,400

Evolution of Ticket Taxes

World Financial Symposium 2016

Countering Ticket Taxes Article 15 of the Convention on International Civil Aviation (Chicago Convention)

“No fees, dues or other charges shall be imposed by any contracting State in respect solely of the right of transit over or entry into or exit from its territory of any aircraft of a contracting State or persons or property thereon”

ICAO’s Policies on Taxation in the Field of International Air Transport (Doc. 8632) “each Contracting State shall reduce to the fullest practicable extent and make plans to eliminate…all forms of

taxation on the sale or use of international transport by air, including taxes on gross receipts of operators and taxes levied directly on passengers or shippers”

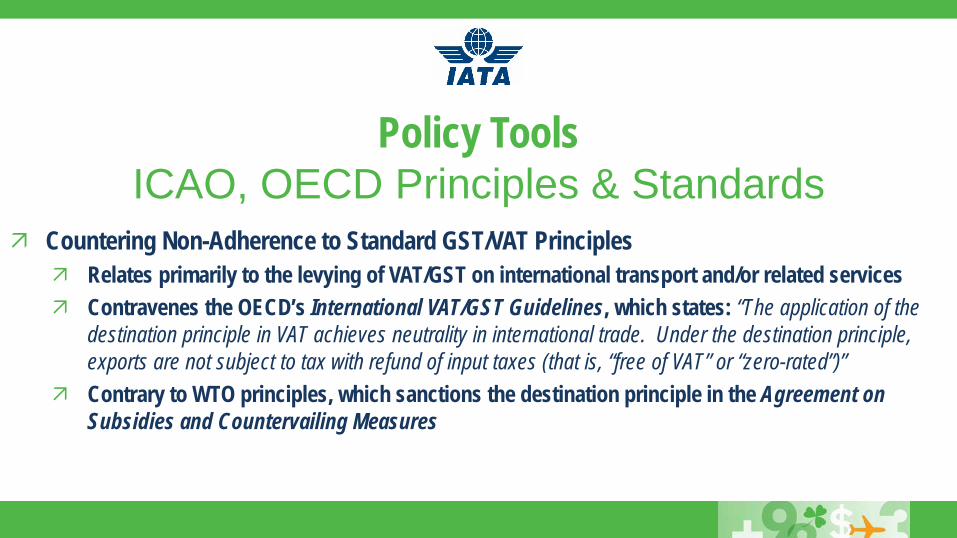

Policy ToolsICAO, OECD Principles & Standards

World Financial Symposium 2016

Countering Non-Adherence to Standard GST/VAT Principles Relates primarily to the levying of VAT/GST on international transport and/or related services Contravenes the OECD’s International VAT/GST Guidelines, which states: “The application of the

destination principle in VAT achieves neutrality in international trade. Under the destination principle, exports are not subject to tax with refund of input taxes (that is, “free of VAT” or “zero-rated”)”

Contrary to WTO principles, which sanctions the destination principle in the Agreement on Subsidies and Countervailing Measures

Policy ToolsICAO, OECD Principles & Standards

World Financial Symposium 2016

Countering Non-Adherence to Standard Treatment of Income from International Transport Attempts to tax, locally, income generated from international transport and related/ancillary services Article 8 of the OECD Model Tax Convention on Income and on Capital & the UN Model Double Taxation

Convention: “Profits from the operation of ships or aircraft in international traffic shall be taxable only in the Contracting State in which the place of effective management of the enterprise is situated.”

OECD Commentary to Article 8 further states: “Activities that the enterprise does not need to carry on for the purposes of its own operation of ships or aircraft in international traffic but which make a minor contribution relative to such operation and are so closely related to such operation that they should not be regarded as a separate business or source of income of the enterprise should be considered to be ancillary to the operation of ships and aircraft in international traffic.”

Policy ToolsICAO, OECD Principles & Standards

World Financial Symposium 2016

With respect to analyzing the impact of a new tax (or an increase to an existing tax), IATA typically undertakes a passenger impact analysis, followed by an economic impact analysis.

Data resources include IATA’s TTBS and Passenger Intelligence Services As a summary, the steps involved in such an analysis include:

Examining passenger volumes and average airfares for the territory associated with the tax (based on class of travel if applicable);

Calculating the increase in average airfare resulting from the tax; Using price elasticities of demand based on geography and type of flight (e.g. long haul vs. short haul), determining the impact

on passenger levels; and Determining the associated economic impact (e.g. GDP, employment, investment) based on revised passenger levels and

relative to a baseline

Economic AnalysisHighlighting the Negative Overall Impact

World Financial Symposium 2017

Economic Analysis: Collateral

World Financial Symposium 2016

Impact AnalysisNew USD 2 Departure Tax

1. Domestic Air Travel ImpactPeriod: Sept. 2014 - Sept. 2015USD

Average Fare Grand Total Reported + Est. Pax % Increase (USD 2) Price Elasticity Passenger Impact - DomesticTotal 85.44$ 539,448.0 2.34% -0.8 (10,102.57)

2. International Air Travel ImpactPeriod: Sept. 2014 - Sept. 2015USDDestination Grand Average Average Fare Grand Total Reported + Est. Pax % Increase (USD 2) Price Elasticities Passenger Impact - International1 Central America 926.02$ 51.0 0.216% -0.5 (0.06) 2 Caribbean 1,014.33$ 24.0 0.197% -0.5 (0.02) 3 South America 1,430.98$ 345.0 0.140% -0.5 (0.24) 4 Europe 414.25$ 122,180.0 0.483% -0.7 (412.92) 5 Africa 595.83$ 2,559.0 0.336% -0.7 (6.01) 6 Middle East 499.88$ 5,766.0 0.400% -0.8 (18.46) 7 Asia 175.38$ 2,818,434.2 1.140% -0.8 (25,712.24) 8 Australasia 357.76$ 84,806.0 0.559% -0.8 (379.27) 9 North America 686.74$ 32,914.0 0.291% -0.5 (47.93)

Total 3,067,079.2 (26,577.14)

Pax Decrease as % of Total Air Departures -1.02%

Illustrative ExamplePassenger Demand Impact

World Financial Symposium 2017

Value of Aviation Collateral

World Financial Symposium 2016

Irrespective of the country or region, there are many common challenges faced by airlines when dealing with Governments, including: Lack of sufficient public consultation and industry input, if any at all (e.g. Governments requesting comments

on draft legislation within 48 hours or less); Insufficient lead time provided when introducing new taxes or revising existing taxes (e.g. tax enacted

yesterday, effective today); and Lack of knowledge of industry standards and operations (e.g. difference between imposing on a flown basis

vs. a ticketed basis). These challenges increase the direct and indirect costs of tax compliance by airlines IATA highlights best practices from countries in a region and conveys the need for Smarter

Regulations

Common Challenges

World Financial Symposium 2017World Financial Symposium 2014

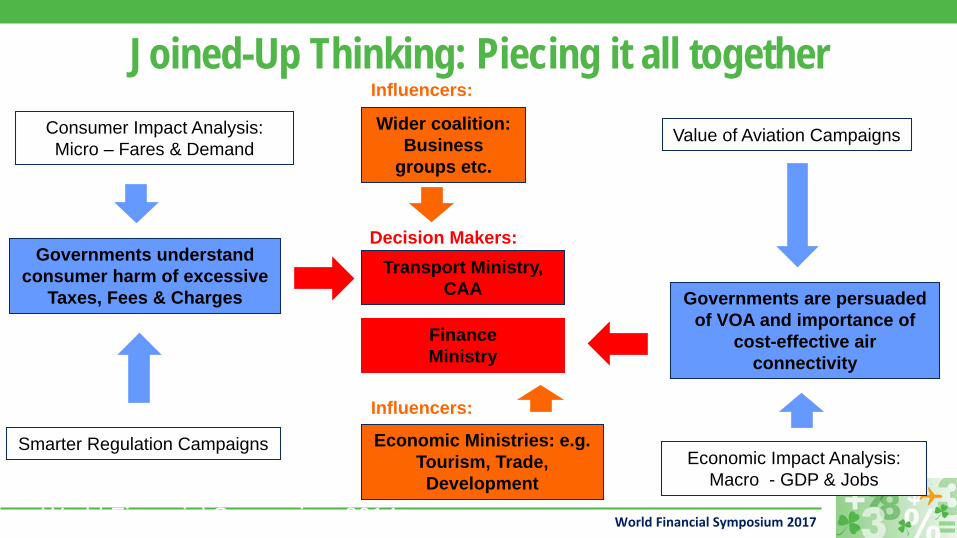

Consumer Impact Analysis:Micro – Fares & Demand

Governments are persuaded of VOA and importance of

cost-effective air connectivity

Value of Aviation Campaigns

Economic Impact Analysis: Macro - GDP & Jobs

Governments understand consumer harm of excessive

Taxes, Fees & Charges

Smarter Regulation Campaigns

Transport Ministry, CAA

Finance Ministry

Decision Makers:

Economic Ministries: e.g. Tourism, Trade, Development

Wider coalition:Business

groups etc.

Influencers:

Influencers:

Joined-Up Thinking: Piecing it all together

World Financial Symposium 2017

Swedish Green Tax Scottish Air Departure Tax Myanmar Tourism Tax Liberian Services Tax Colombian Connectivity Tax

ExamplesRecent Taxes Challenged

World Financial Symposium 2017

Questions?

World Financial Symposium 2017World Financial Symposium 2014

Recent Global Tax Developments

Mark BradfordHead of Taxation, Qantas

Muharrem UnsalVP Taxation, Singapore Airlines

Charlotte FantoliAssistant Director, Industry Taxation, IATA

World Financial Symposium 2017

Indirect Tax DevelopmentsSweden Air Travel Tax: Background & Actions

Nov 2015: Launch of investigation on a new ‘Green’ Tax on air tickets Series of stakeholder meetings in 2016 June 2016: IATA met with the Government Commission Nov 2016: Release of the Government Report recommending a tax on air tickets and

opening a public consultation (close on 1 Mar 2017) Dec16 – Mar 17: Global Advocacy campaign, including a multi-disciplinary workshop

in Stockholm in Feb Consultation

Global media campaigns against the tax 26 Aug 2017: Announcement that tax will be introduced

World Financial Symposium 2017World Financial Symposium 2014

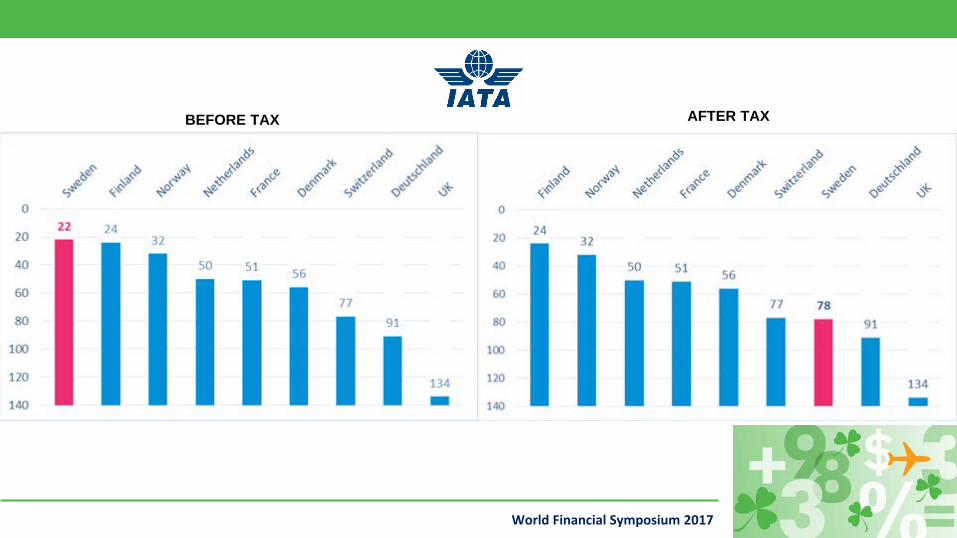

BEFORE TAX AFTER TAX

World Financial Symposium 2017

Indirect Tax DevelopmentsSweden Air Travel Tax: Tax details

Effective as of 1 April 2018 SEK 60, SEK 250, SEK 430 (equiv. U$ 7.54, U$ 31.40, U$ 50.25) / dep pax

Next steps Confirmation of the effective date of 1 April 2018 Will the tax be levied on a sales basis or passenger uplift basis? The applicable exemptions The remittance timelines and procedures

World Financial Symposium 2017

Indirect Tax DevelopmentsUK APD vs Scotland ADT: Background

The UK Government has devolved the administration of its APD to regions In Dec 2016, the Scottish Government announced its’ intention to:

• Replace the APD by a Scottish Air Departure Tax (ADT) eff 1 April 2018• Cut the rates by 50%

Status May 2016: Consultation 1 Feb 2017: Call for evidence on the ADT (Scotland) Bill Dec 2016 15 Sep 2017: Consultation 2

World Financial Symposium 2017

Indirect Tax DevelopmentsAustria Air Transport Levy: Implemented in 1 January 2011 Rates EUR 8, 20, 35 / pax depending on destination Since its introduction, the tax has been on IATA’s radar Various lobbying efforts to reduce or eliminate the tax First result was a small increase of the lower rates in Jan 2013 to EUR 7.50 and 15 1 Jan 2018 rates reduced by 50% to EUR 3.50, 7.50 and 17.50 Savings of USD 63 million p.a. Use and promote this example (in addition to earlier tax reductions in e.g.

Ireland, Netherlands) with other States

World Financial Symposium 2017

Background: International air transportation and related services should be zero-rated for the purpose

of VAT and GST to be allowed to right of reclaimGCC* States: IATA letters sent to each GCC States in May 2016 GCC VAT Framework Treaty signed by all 6 States Consistent standard rate of 5% International air transportation is zero-rated 1 January 2018:

Saudi Arabia VAT Law and Regulations published, and online registration open since 28 August 2017

UAE VAT Decree Law was published in August Oman to follow likely 2nd half of 2018, then others in 2019

* Gulf Cooperation Council States: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates

Indirect Tax Developments: VAT & GST

World Financial Symposium 2017

Egypt VAT: Introduced on 1 July 2016 Standard rate of 14% (since 1 July 2017, 13% previously) Exemption allowed for international and domestic passenger air transport

Cargo? Only 0% when payment for the export is done outside Egypt IATA is currently in discussions with the tax authorities to:

Change the status of cargo Allow cargo airlines to register for VAT

* Gulf Cooperation Council States: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates

Indirect Tax Developments:VAT & GST

World Financial Symposium 2017

Tax Developments:India Goods & Services Tax

Background & Actions: Summary of meetings and submissionsImplementation: The Tax details Problems Interim industry solutionNext steps: Industry clarification and guidelines Solution? Audits and litigation?

World Financial Symposium 2017

India GST:Summary of meetings and submissions:2014: 25 Nov: DEL meeting with Joint Secretary, MOF TRU II (ST) Written pre-meeting submission 14 Nov and post-meeting summary 19 Dec.2015: 15 Jul: IATA Director General meeting with Finance Minister Mr. Jaitley 23 Jul: Letter from IATA Director General to Finance Minister Mr. Jaitley 1 Sep: Letter to new Joint secretary, MOF TRU II 31 Oct: IATA online mygov.in submission on GST Implementation Plan

on business processes (Payment, Registration, Refund, Return) 30 Nov: Feedback on India Draft National Civil Aviation Policy

World Financial Symposium 2017

2016: 22 Mar: Meeting DEL with Chairman of the CBEC 14 Jun: Draft GST Law released 9 Aug: Letter regarding draft Law to GST Commissioner 20 Sep: Meeting DEL with GST Commissioner 19 Oct: IATA Director General meeting with Finance Minister Mr. Jaitley 30 Nov: Model GST Law released2017: Feb: IATA India GST White Paper 4 Apr: Meeting with Chairman of GST Working Group for Transport & Logistics (T&L) 7 Apr: Follow-up submission to T&L with industry recommendations May: Revised GST Law released 1 Jun. IATA DG letter to Finance Minister Mr. Jaitley Aug: Re-submission of industry FAQs to GST Law Committee 11-12 Sep: Meetings with GST Convener and MOCA

World Financial Symposium 2017

India GST:Implementation: The Tax details

Implemented 1 July 2017 Dual level means: CGST, SGST, UGST, IGST Rates: 5% for lowest fare economy and 12% for premium travel 18% applies to cargo exports

Problems Definition of ‘Continuous journey’ – stop-over, multi-segment and return journeys GST base – exclusion of taxes, fees, charges Applicability of GST to ancillary services Registration requirements – offline carriers in a State GST invoicing requirements and distinction between

B2C and B2B customers

World Financial Symposium 2017

India GST:Interim industry solution: Interim code ‘K3’ assigned All GST collected as IGST only As B2C (airlines responsible for B2B and invoicing individually)

Next steps: Industry clarification and guidelines When final solution is available, interim code will be replaced

by new codes for CGST, SGST, UGST, IGST

World Financial Symposium 2017

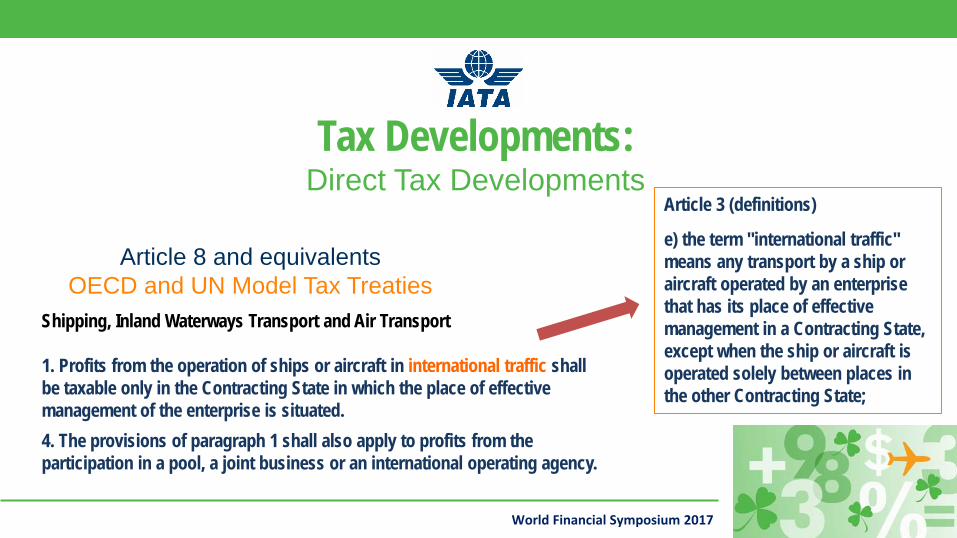

Tax Developments:Direct Tax Developments

Shipping, Inland Waterways Transport and Air Transport

1. Profits from the operation of ships or aircraft in international traffic shall be taxable only in the Contracting State in which the place of effective management of the enterprise is situated. 4. The provisions of paragraph 1 shall also apply to profits from the participation in a pool, a joint business or an international operating agency.

Article 8 and equivalentsOECD and UN Model Tax Treaties

Article 3 (definitions)

e) the term "international traffic" means any transport by a ship or aircraft operated by an enterprise that has its place of effective management in a Contracting State, except when the ship or aircraft is operated solely between places in the other Contracting State;

World Financial Symposium 2017

Tax Developments:Direct Tax Developments

Income taxes outside Treaties/Article 8

“Corporate social responsibility contributions”

Brazil CSLL

El Salvador

Greece

India

Venezuela

“Domestic Corporate Law” Africa OHADA States

- revised company tax act

World Financial Symposium 2017

Tax Developments:Direct Tax Developments

Global response to Base Erosion Profit Shifting Driven by the OECD Overview Industry CbC reporting ‘exemption’ Status & Next steps

Ticket TaxesA Continuing Source of Discomfort

27 September 2017

Distinguished PanelistsHenry Coles, IATASeverine Guffroy, Air FrancePablo Londono-Betancur, ATPCONathalie Rodier, Air Canada

ModeratorsNathan Bittner, Ryan LLCJeff Mullins, Ryan LLC

ContextTaxes impact all aspects of your organization• Ticket taxes are ~20% of a customer’s cost of travel, and often more.

• Taxes potentially represent a significant above-the-line compliance risk if they are not accurately collected and remitted in accordance with the law.

• With profit margins less than 5%, an airline would need to generate more than USD $24 million in revenue to pay a tax bill of USD $1 million.

Key challenges• Operations: Is Tax a strategic partner in your major operational / product changes?• Technology: Do you provide Tax the level of technology support it needs?• External: Does Tax require an external source of information for its processes?

2

3

ObjectiveThe landscape of systems, products, and regulations is a complex and constantly evolving system. Tax departments drive compliance by managing this complexity across the global enterprise.

Ryan recently released a white paper that sparked an interest in the interplay between the CFO, Tax, and other departments from a “top-down” perspective.

ApproachExamine Tax’s relationship with other departments from the “inside out.”

Survey distributed to Industry Taxation Meeting participants.

Results discussed at the Industry Taxation Meeting.

4

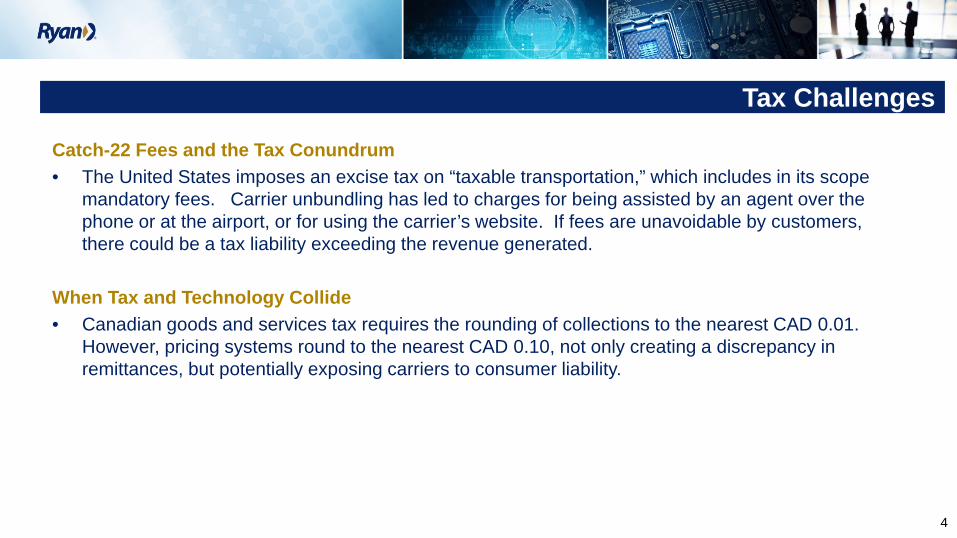

Tax Challenges

Catch-22 Fees and the Tax Conundrum• The United States imposes an excise tax on “taxable transportation,” which includes in its scope

mandatory fees. Carrier unbundling has led to charges for being assisted by an agent over the phone or at the airport, or for using the carrier’s website. If fees are unavoidable by customers, there could be a tax liability exceeding the revenue generated.

When Tax and Technology Collide• Canadian goods and services tax requires the rounding of collections to the nearest CAD 0.01.

However, pricing systems round to the nearest CAD 0.10, not only creating a discrepancy in remittances, but potentially exposing carriers to consumer liability.

5

What is Top of Mind for Tax?Panel Questions

1. What are the costs / risks associated with Tax not meeting its reporting challenges?

2. What controls ensure existing processes and new product lines meet tax requirements?

3. How can you help Tax engage with other departments on projects with tax implications?

4. How do you ensure Tax is properly positioned to opine on significant law changes?

6

What should you take away?

7

© 2017 Ryan, LLC. All rights reserved. All logos and trademarks are the property of their respective companies and are used with permission.

This document is presented by Ryan, LLC for general informational purposes only, and is not intended as specific or personalized recommendations or advice. The application and effect of certain laws can vary significantly based on specific facts, and professional advice of any nature should be sought only from appropriate professional advisors. This document is not intended, and shall not be deemed, to constitute legal, accounting or other professional advice.