world energy outlook 2016 energy policies of iea countries … · powerpoint presentation author:...

TRANSCRIPT

© OECD/IEA 2016 © OECD/IEA 2016

Energy Policies of IEA Countries In-depth Review of Poland 2016

Ms Theresia Vogel, IDR team leader

SLT, 5 December 2016

World Energy Outlook 2016 and In-depth Review of

Poland’s energy policies 2016

Dr. Fatih Birol

IEA Executive Director Warsaw, 25 January 2017

www.iea.org © OECD/IEA 2016 © OECD/IEA 2016

© OECD/IEA 2016

Key points of orientation:

Middle East share in global oil production in 2016 at highest level for 40 years

Transformation in gas markets deepening with a 30% rise in LNG

Additions of renewable capacity in the power sector higher in 2015 than coal, gas, oil and nuclear combined

Energy sector in the spotlight as the Paris Agreement enters into force

Billions remain without basic energy services

There is no single story about the future of global energy; policies will determine where we go from here

The global energy context today

© OECD/IEA 2016

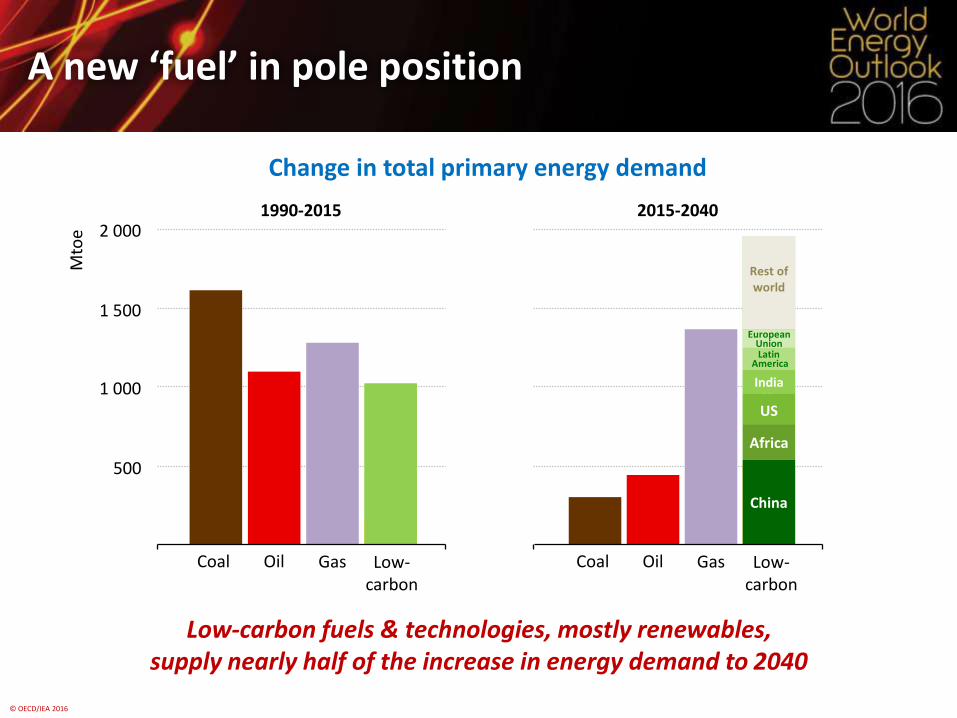

Change in total primary energy demand

Low-carbon fuels & technologies, mostly renewables, supply nearly half of the increase in energy demand to 2040

Low- carbon

Oil Gas Coal

A new ‘fuel’ in pole position

500

1 000

1 500

2 000 1990-2015 2015-2040

Mto

e

Low- carbon

Oil Gas Coal

Nuclear

Nuclear

Ren

ewab

les

Ren

ewab

les

Rest of world

European Union Latin

America

India

US

Africa

China

© OECD/IEA 2016

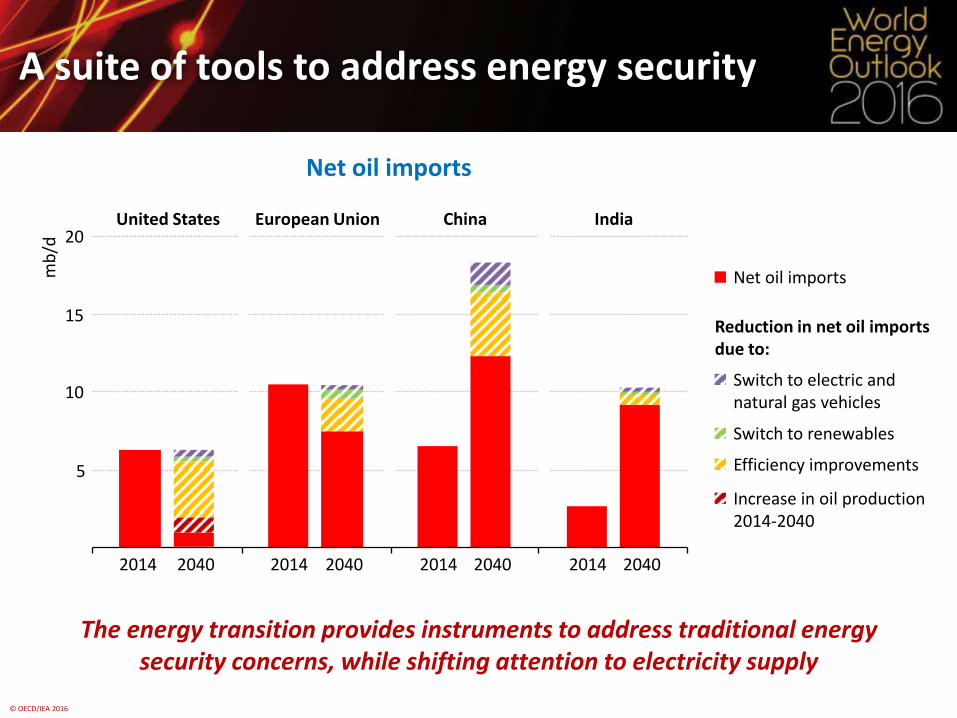

Net oil imports

The energy transition provides instruments to address traditional energy security concerns, while shifting attention to electricity supply

A suite of tools to address energy security

5

10

15

20

2014 2040

mb

/d

Switch to electric and natural gas vehicles

Switch to renewables

Efficiency improvements

Increase in oil production 2014-2040

Net oil imports

United States

2014 2040

European Union

2014 2040

China

2014 2040

India

Reduction in net oil imports due to:

© OECD/IEA 2016

-3

0

3

6 mb/d

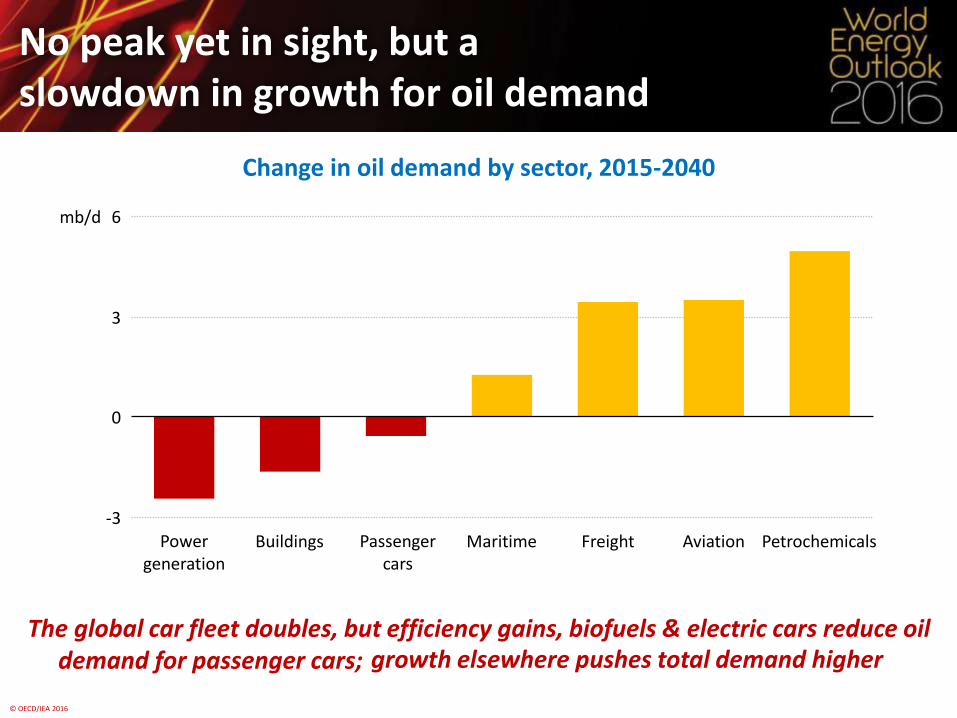

The global car fleet doubles, but efficiency gains, biofuels & electric cars reduce oil

Change in oil demand by sector, 2015-2040

No peak yet in sight, but a slowdown in growth for oil demand

Power generation

Buildings Passenger cars

Maritime Freight Aviation Petrochemicals

demand for passenger cars;

growth elsewhere pushes total demand higher

© OECD/IEA 2016

A wave of LNG spurs a second natural gas revolution

Share of LNG in global long-distance gas trade

Contractual terms and pricing arrangements are all being tested as new LNG from Australia, the US & others collides into an already well-supplied market

2014 685 bcm

2040 1 150 bcm

2000 525 bcm

LNG 53%

Pipeline Pipeline LNG 42%

Pipeline

LNG 26%

© OECD/IEA 2016

Coal demand in key regions

The peak in Chinese demand is an inflexion point for coal; held back by concerns over air pollution & carbon emissions, global coal use is overtaken by gas in the 2030s

Coal: a rock in a hard place

500 1 000 1 500 2 000 2 500 3 000

Southeast Asia

European Union

India

United States

China

Mtce

2014

Decreasing demand

Change 2014-2040:

Increasing demand

© OECD/IEA 2016

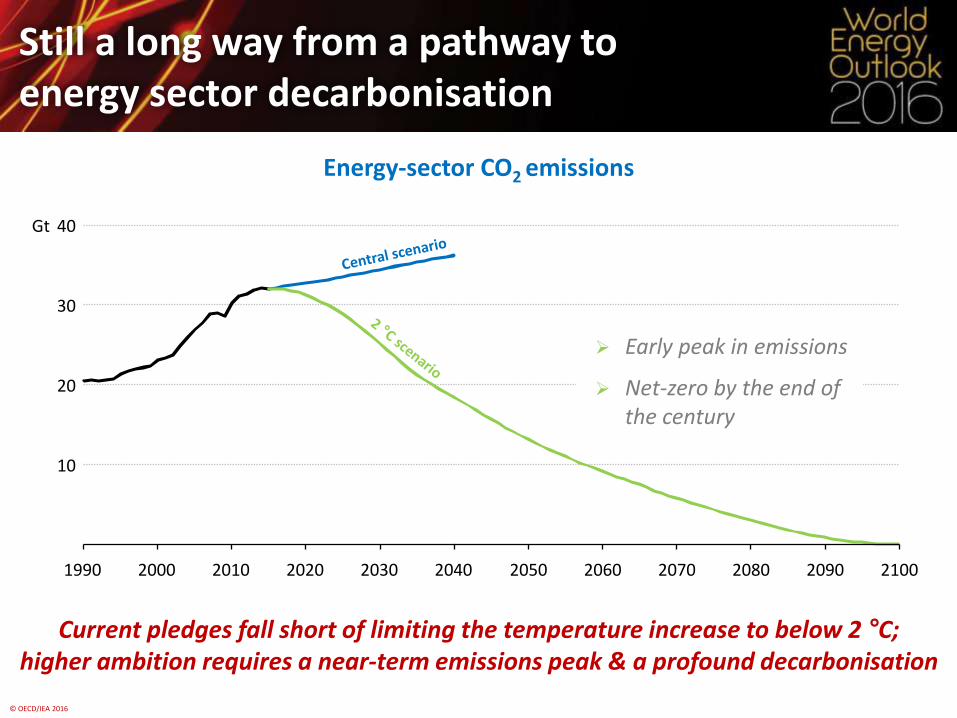

Current pledges fall short of limiting the temperature increase to below 2 °C; higher ambition requires a near-term emissions peak & a profound decarbonisation

Energy-sector CO2 emissions

Still a long way from a pathway to energy sector decarbonisation

10

20

30

40

1990 2000 2010 2020 2030 2040

Gt

2060 2080 2100 2050 2070 2090

Early peak in emissions

Net-zero by the end of the century

© OECD/IEA 2016

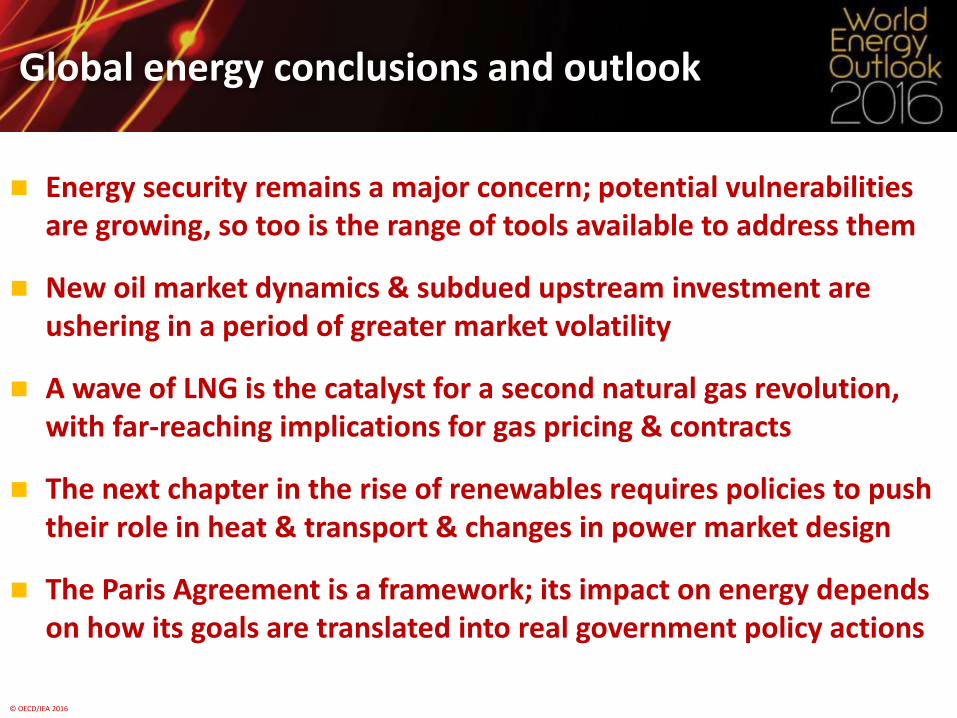

Energy security remains a major concern; potential vulnerabilities are growing, so too is the range of tools available to address them

New oil market dynamics & subdued upstream investment are ushering in a period of greater market volatility

A wave of LNG is the catalyst for a second natural gas revolution, with far-reaching implications for gas pricing & contracts

The next chapter in the rise of renewables requires policies to push their role in heat & transport & changes in power market design

The Paris Agreement is a framework; its impact on energy depends on how its goals are translated into real government policy actions

Global energy conclusions and outlook

© OECD/IEA 2016

Turning to Poland

From a global energy context

to energy policy in Poland

© OECD/IEA 2016

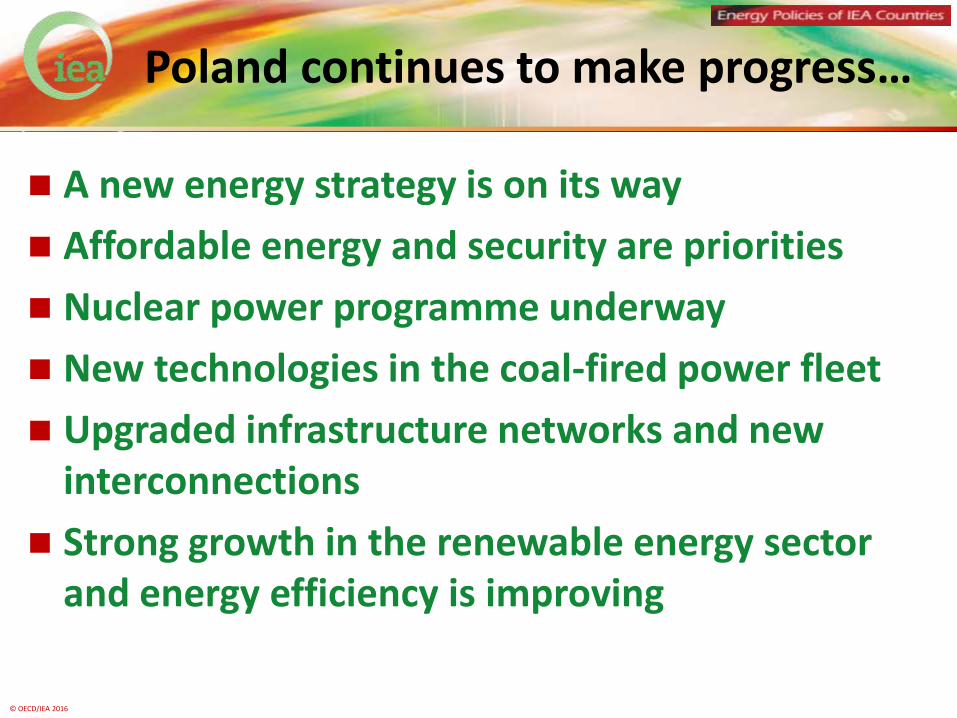

A new energy strategy is on its way

Affordable energy and security are priorities

Nuclear power programme underway

New technologies in the coal-fired power fleet

Upgraded infrastructure networks and new interconnections

Strong growth in the renewable energy sector and energy efficiency is improving

Poland continues to make progress…

© OECD/IEA 2016

Local air quality a major problem in places

Future growth of renewables is uncertain

Need for more competition in energy markets

Uncertainty around timing of nuclear developments

More resources needed for energy research, development & innovation

But challenges remain

© OECD/IEA 2016

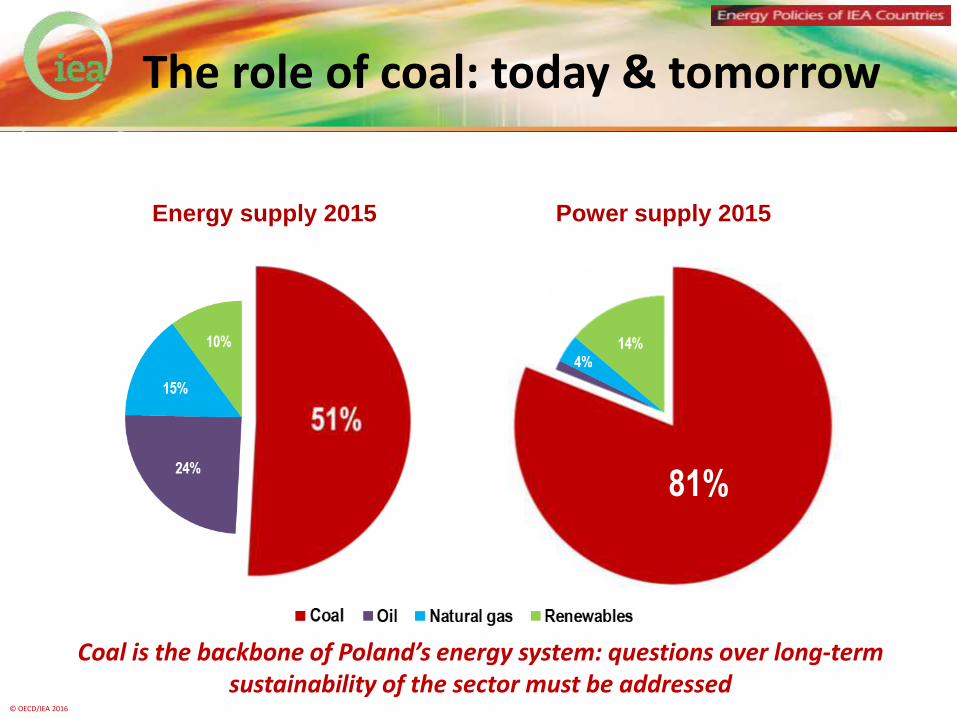

Coal is the backbone of Poland’s energy system: questions over long-term sustainability of the sector must be addressed

Energy supply 2015

81%

The role of coal: today & tomorrow

Power supply 2015

© OECD/IEA 2016

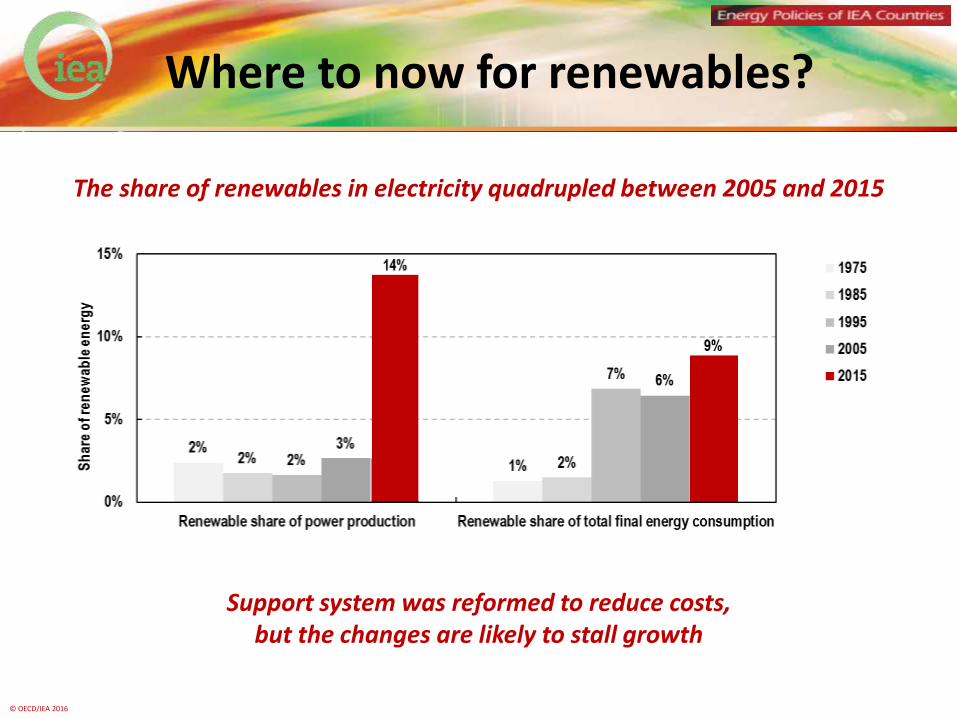

Support system was reformed to reduce costs, but the changes are likely to stall growth

The share of renewables in electricity quadrupled between 2005 and 2015

Where to now for renewables?

© OECD/IEA 2016

Adopted Polish Nuclear Power Programme in 2014: develop and deploy nuclear energy by the end of 2024

Public opinion generally favourable towards nuclear power, incl. near possible sites

Poland adopted a National Plan for Radioactive Waste and Nuclear Spent Fuel Management in October 2015

Government and nuclear industry are developing manpower

But…Decisions on technology and financing needed to allow industry make investment decisions

Nuclear power

© OECD/IEA 2016

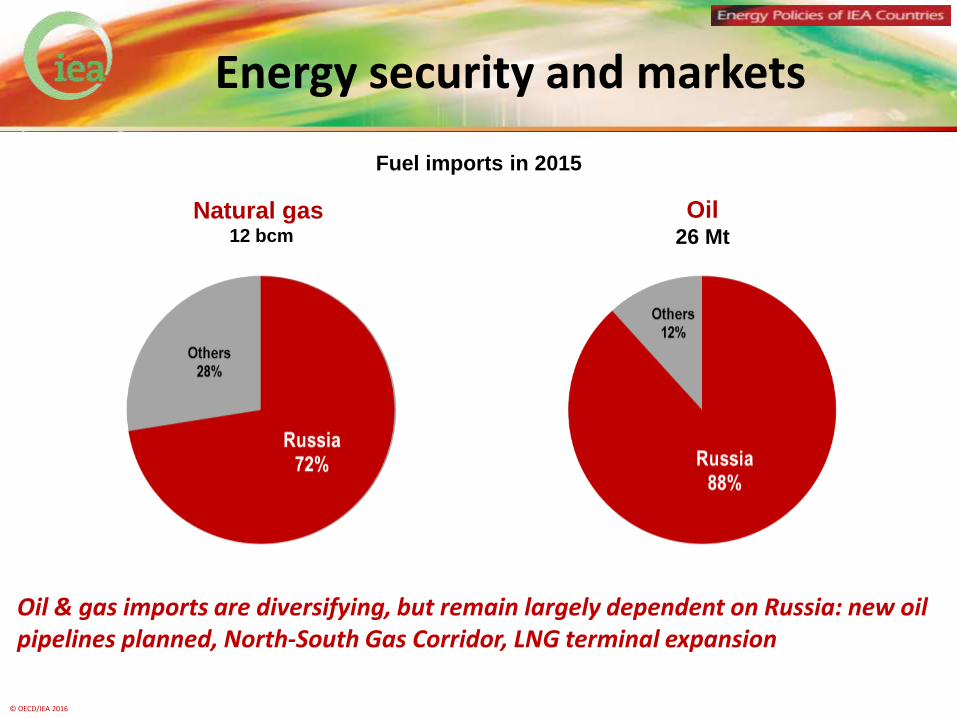

Oil & gas imports are diversifying, but remain largely dependent on Russia: new oil pipelines planned, North-South Gas Corridor, LNG terminal expansion

Energy security and markets

Fuel imports in 2015

Natural gas 12 bcm

Oil 26 Mt

© OECD/IEA 2016

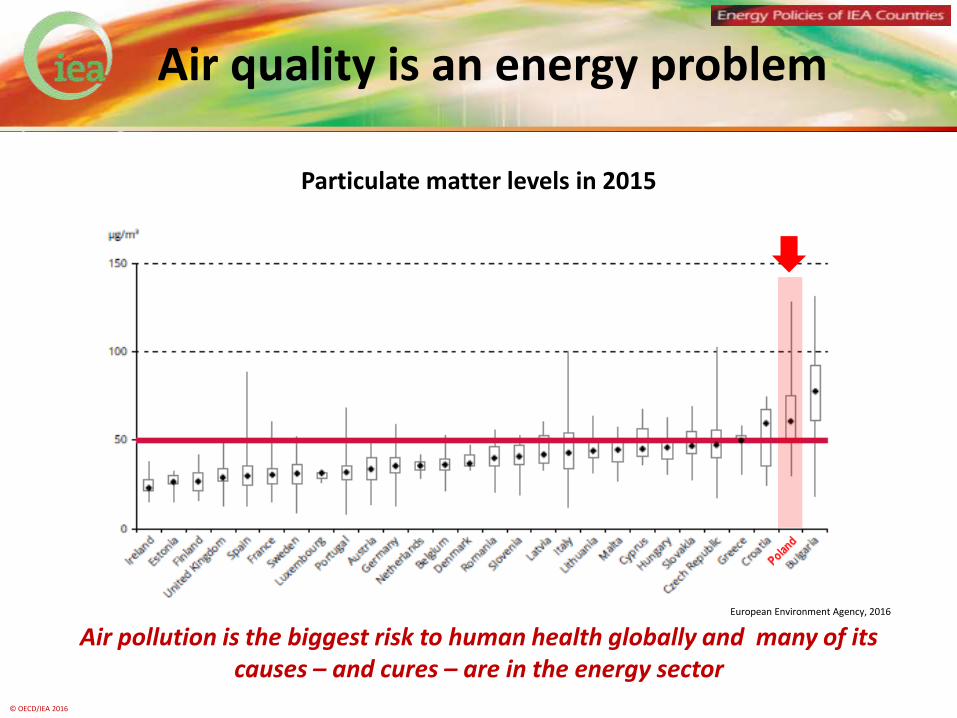

Particulate matter levels in 2015

Air pollution is the biggest risk to human health globally and many of its

causes – and cures – are in the energy sector

Air quality is an energy problem

European Environment Agency, 2016

© OECD/IEA 2016

0

200

400

600

800

1 000

1 200

1 400

2010 2011 2012 2013 2014 2015

Tho

usa

nd

car

s

Others*

Germany

UnitedKingdom

France

Norway

Netherlands

Japan

China

United States

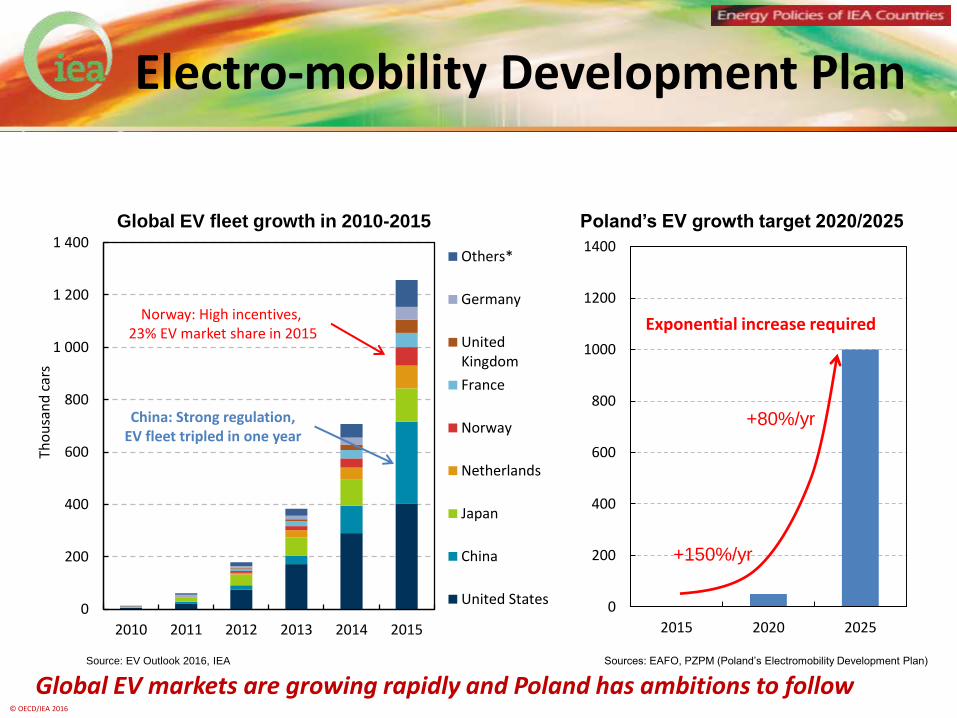

Global EV markets are growing rapidly and Poland has ambitions to follow

0

200

400

600

800

1000

1200

1400

2015 2020 2025

Exponential increase required

Poland’s EV growth target 2020/2025 Global EV fleet growth in 2010-2015

Norway: High incentives, 23% EV market share in 2015

+150%/yr

+80%/yr China: Strong regulation, EV fleet tripled in one year

Source: EV Outlook 2016, IEA Sources: EAFO, PZPM (Poland’s Electromobility Development Plan)

Electro-mobility Development Plan

© OECD/IEA 2016

Finalise the long-term energy strategy balancing Poland’s energy security, environmental and economic needs

Coal: stabilise the mining sector; close old polluting plants; build new supercritical ones; and replace household boilers

Introduce measures to secure the short- and long-term security of the electricity system.

Maintain efforts to diversify natural gas supply by taking advantage of global market dynamics

Finalise the timeline, technology choice and partners as well as finance mechanisms for the nuclear energy programme.

IDR key recommendations

© OECD/IEA 2016

http://www.iea.org/publications/countryreviews/

http://www.iea.org/publications/freepublications/

Download this report and other IEA publications for free

© OECD/IEA 2016