world bank documentdocuments.worldbank.org/curated/en/634491468782115205/pdf/multi... · ntc...

TRANSCRIPT

FILE COPY

Report No. :11242 Type: (MIS)Title: THE LOCAL TAX ON SERVICFS IN RlAuthor: SILVEIRA, RICARDOExt.: 0 Room: Dept.:OLD INU WORKING PAPER

INURD WP#7

URBAN DEVELOPMENT DIVISIONPOLICY, PLANNING AND RESEARCH STAFF

THE WORLD BANK

THE LOCAL TAX ON SERVICES IN BRAZIL

by

Ricardo Silveira

October 1989

WORKING PAPER

The INURD Working Papers present preliminary research findings and are intended for internalreview and discussion. The views and interpretations in these Working Papers are those of theauthor(s) and should not be attributed to the World Bank, to its affiliated organizations or to anyindividual acting on their behalf.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Copyright 1989 0The World Bank1818 H Street, N.W.

All Rights ReservedFirst Printing October 1989

This is a document published informally by the World Bank. In order that the informationcontained in it can be presented with the least possible delay, the typescript has not been prepared inaccordance with the procedures appropriate to formal printed texts, and the World Bank accepts no responsibilityfor errors.

The World Bank does not accept responsibility for the views expressed herein, which are thoseof the author and should not be attributed to the World Bank or to its affiliated organizations. The findings,interpretations, and conclusions are the results of research supported by the Bank; they do not necessarilyrepresent official policy of the Bank. The designations employed, the presentation of material, and any mapsused in this document are solely for the convenience of the reader and do not imply the expression of anyopinion whatsoever on the part of the World Bank or its affiliates concerning the legal status of any country,territory, city, area, or of its authorities, or concerning the delimitations of its boundaries or nationalaffiliation.

Most of the information used in this report was gathered during a mission to Brazil in October1987. Thirteen cities of various sizes and income levels were visited by the mission: Curitiba, AlmiranteTamendare and Arucaria in the south; Rio de Janeiro, Petropolis, Belo Horizonte, Ibirite and Divinopolis in thesoutheast; and Recife, Jaboatso, Olinda, Paulista and Palmares in the northeast. The mission counted on theassistance of Mr. Luis Villela (consultant) in Rio de Janeiro. Mr. Fabricio de Oliveira (consultant) provideda background paper on the ISS situation in the state of Hinas Gerais, as well as field assistance (INT/86/006).While this report was being drafted, major constitutional reforms were taking place in Brazil--some ofconsequence to the fiscal tax code and local goverrment administration. The report atteipts to docusent someof these reforms, but it does not reflect the final draft of the new constitution.

The principal author is Ricardo Silveira from the Infrastructure and Urban DevelopmentDepartment of the World Bank. Coements and suggestions by Per Ljung, William Dillinger and Fabricio de Oliveira(CEDEPLAR) are gratefully acknowledged. Any errors remain the responsibility of the author.

THE LOCAL TAX ON SERVICES IN BRAZIL

Acrony=s and Abreviations

CIATA Program of Incentives for Technical andAdministrative Improvement

FGV Getulio Vargas FoundationIBGE Brazilian Institute of Geography and

StatisticsICM State Value-Added TaxIOF Tax on Financial OperationsIPTU Tax on Real PropertyIR Federal Income TaxISC Tax on CommunicationISS Tax on ServicesNTC National Tax CodeOTN Treasury NoteSEF Secretariat of Economics and FinanceSERPO Federal Service of Data ProcessingUFR Recife's Fiscal Value UnitUNIF Rio de Janeiro's Fiscal Value UnitUPF Fiscal Value Unit

- ii -

THE LOCAL TAX ON SERVICES IN BRAZIL

Table of Contents

Page No.

I. INTRODUCTION ................ 1History of the ISS .... . . . . . . . . . . . . . . . 1

II. FINANCING MUNICIPALITIES IN BRAZIL . . . . . . . . . . . . . . 2

III. ISS PERFORMANCE .5... . . . . . . . . . . . . . . . . . . . S

A. The Importance of ISS in Local Government Finances . . . 5

B. Allocative Efficiency and Fiscal Incidence . .. . . . . . 5Allocative Efficiency . .. . . . . . . . . . . . . . . 5Fiscal Incidence .... . . . . . . . . . . . . . .. 6

C. Yield . . . . . . . . . . . . . . . . . . . . . . . . . . 7

D. Bovancy .10

IV. THE ADMINISTRATION OF THE ISS .12

A. The Lezislative Framework .. 12Classes of Taxpayers .. 14ISS and Business Location . . . . . . . . . . . . . . . 14

B. Tax Base. Rates and Fees . . . . . . . . . . . . . . . . . 15Construction Industry . . . . . . . . . . . . . . . . . 15Self-Employed Professionals . . . . . . . . . . . . . . 15Single-Profession Partnerships . . . . . . . . . . . . . 16Rate-Setting for Firms . . . . . . . . . . . . . . . . . 16

C. Exemptions . . . . . . . . . . . . . . . . . . . . . . . . 17

D. The Fiscal Registry .19Registration Procedures . . . . . . . . . . . . . . . . 19Maintenance of Registry . . . . . . . . . . . . . . . . 19Incentives to Register .19

E. Billing and Collections .. 20Professionals and Single-Professional Partnerships . . . 20Self-declaration by firms . . . . . . . . . . . . . . . 20Bank Collection .. 20Fiscal Substitution . . . . . . . . . . . . . . . . . . 21Collection Efficiency .. 21

F. Tax Enforcement . . . . . . . . . . . . . . . . . . . . . 22Auditors and Merit Pay .. 22Audit Strategies . . . . . . . . . . . . . . . . .. 22

- iii -

lUpdating the Fiscal Registry . . . . . . . . . . . . . . 22Accounting Requirements . . . . . . . . . . . . . . . . 23Tax Evasion and Penalties . . . . . . . . . . . . . . . 23Taxpayer Recourse . . . . . . . . . . . . . . . . . . . 24

V. PROJECT CIATA . . . . . . . . . . . . . . . . . . . . . . . . 26

A. Obiectives and Implementation . . . . . . . . . . . . . . 26

B. Proiect Performance ................. . . 27

VI. CONCLUSION .. ... . - 30

Yield.. . .... 30Administration . . . . . . . . . . . . . . . . . . . . . 30Constitutional Changes . . . . . . . . . . . . . . . . . 33

TABLES

Table 1 - Share of Taxes in GDP . . . . . . . . . . . . . . . i . . . 8Table 2 - Regional Distribution of Population, GDP and Taxes (1980) . 9Table 3 - Share of Major Taxes in Each Jurisdiction and Their Buoyancy 11Table 4 - List of Services Liable of ISS . . . . . . . . . . . . . . 13Table 5 - Fiscal Performance of CIATA Municipalities . . . . . . . . 28

BOXES

Box 1 - Tax Rates for the City of Rio de Janeiro . . . . . . . . . . 18Box 2 - Infractions .24

FIGURES

Figure 1 - Resources for Government Expenditure by Level of Government 2Figure 2 - Tax Revenues by Level of Government . . . . . . . . . . . 3Figure 3 - Tax Revenues per Capita by Region . . . . . . . . . . . . 4Figure 4 - Municipal Revenues per Capita by Region . . . . . . . . . 4Figure 5 -Municipal Tax Revenues in the Capital Cities . . . . . . . 5Figure 6 - Municipal Tax Revenues in the Interior Cities . . . . . . 5Figure 7 - Share of Taxes in GDP .6Figure 8 -Distribution of ISS Collections in the Capitals . . . . . 10Figure 9 - Distribution of ISS Collections in the Interior . . . . . 10

ANNEXES

Annex 1 - Tables . . . . . . . . . . . . . . . . . . . . . . . . . . 35Annex 2 - Forms .38Annex 3 - The Expanded ISS List .43Annex 4 - Variation in ISS Rates .50Annex 5 - Merit Pay System for Auditors . . . . . . . . . . . . . . . 61

THE LOCAL TAX ON SERVICES IN BRAZIL

I. INTRODUCTION

1.01 This report is part of a series of case studies on alternativebusiness tax instruments used to finance local governments in developingcountries. The broad objective of these studies is to derive a set of guidelinesto be used in the design of fiscal instruments by project officers of the Bankand policy-makers in member countries. The purpose of this report is to describethe Brazilian 'Tax on Services' (ISS), a tax which falls within the authorityof local governments and represents their largest source of non-transfer revenue.

1.02 The ISS may be evaluated in terms of its performance andadministrative procedures. For purpose of this paper, performance is judged byeconomic efficiency, yield, and buoyancy criteria. Since performance dependsto a great extent on the administration of ths tax, we concentrate on aspectsof taxpayer identification, billing, collection and enforcement procedures, aswell as on the related policy issues of det..rmination of the tax base, rate/feesetting, and exemption patterns.

History of the ISS

1.03 The ISS dates back to the early 19th century--the years after thearrival of the Portuguese Royal family in Brazil--when the first tax on serviceswas created. At first, its incidence was rather limited, reaching only stores,warehouses and ships. Over the years, however, the tax was continuouslybroadened-I until 1860, when it included nearly all lucrative activities andbegan to be called the "Tax on Industries and Professions."

1.04 In 1891, with the first Republican Constitution, the tax wastransferred to the jurisdiction of the states, though some states relinquishedthis right in favor of their municipalities. The Constitution of 1934 maintainedthe tax under state autonomy, but allowed the creation of a municipal tax on"Public Entertainment." It was not until 1946, with the re-awakening offederalist ideals, that the tax returned to the local fiscal jurisdiction, whichupheld its complete autonomy over rate-setting. In fact, irresponsible rate-setting by municipalities, then, is one of the reasons for the extinction of thetax as a municipal fiscal instrument in 1965.

1.05 It was replaced by the Tax on Services (ISS) created in 1966, withstrict limitations on tax rates and the types of liable services. Upperboundaries on rates were set by the central government, and dutiable serviceswere specifically restricted in a central government list. At present,1V localgovernments enjoy total autonomy insofar as the ISS tax rates; however, the ISSlist of dutiable services remains restrictive.

L/ In 1831, the base expanded to also Include fashion houses, and auctionhouses; by 1836, the tax covered all stores selling goods or services.

2/ Most of the information used in this report was gathered prior to the fiscalreiorms of 1988/89.

II. FINANCING MUNICIPALITIES IN BRAZIL

2.01 The public sector in Brazil is divided into three tiers: central,state, and municipal. The country is organized politically into one federaldistrict, 23 states, some 4,000 municipalities,1' and three federal territories,which function basically as states. Also, a large share of the public sectoris concentrated in public enterprises that operate at all levels of government.Federal agencies and enterprises alone are estimated to account for roughly halfof all central government expenditures and over three fourths of investment.±I

2.02 The Brazilian constitution is vague about the distribution offunctional responsibilities to each level of government. Conceptually, statesand municipalities are free to perform any activi:y not specifically disallowedby the higher tier of government. However, this has led to considerableoverlapping in the provision of a number of public services. The constitutionplaces the responsibility of providing "local public services' on themunicipalities, but this attribution itself, lacks a clear definition. It isoften interpreted to mean housing and related services, and these are in factsupplied mostly by municipalities. However, primary education and some essentialcomponents of health care are also provided by local governments.

2.03 T h e e x t e n t o fresponsibilities of each level of RESOURCES FOR GOVERNMENT EXPENDITURESgovernment can be sensed from the BY LEVEL OF GOVERNMENTrelative size of their total 19OMSexpenditutes. Municipalities spend 2000

16.7 parcent of public sector 1500expenditures.f1 However, they accountfor only 4.5 percent of public 1000revenues, whereas states account for36.5 percent of expenditures and about go39 percent of revenues. Thus, localgovernments must depend largely on- 1975 1980

transfers to meet their implicit Y__duties. This is especially true of CENTL RAL STAT LOL

smaller municipalities in the interiorof the country, since the two salient __S_#

local taxes--on real property (IPTU) Fi 1Lue 1and services (ISS)--are essentially afunction of population density andaffluence.

2./ The Brazilian territory is politically divided, in its entirety, Intomunicipalities. The seat oL umilcipal government is the district within themunicipality where the executlve and legislative bodies function.

A/ Fernando Rezende, Financas Publicas (Sao Paulo: Ed. Atlas, 1986).

E/ These are tax-financed expenditures only. Resources being defined as taxrevenues ner of Intergovernmental transfers (public enterprises excluded).

- 3 -

2.04 Over time, the role of local governments in tax revenues hasexperienced a continuous decline- -the local share fell by over 40 percent in theperiod 1960-84- -while its share of expenditures in public spending ebout doubled.In 1984, federal and state transfers accounted for almost three fourths ofmunicipal expenditures, as compared with less than one third in 1960.

TAX REVENUESBY LEVEL OF GOVERNMENT

2000 BILLONS OF 1960 CRLZEIROS

1000

500

1960 MC0I97 18 1984

YEAR

CENTRAL M STATE 5 LOCAL

SURCE: ANNEX I-C

Figure 2

2.05 Despite built-in inflation adjustment provisions for most taxes andfees, the performance of local government revenue tends to be unstable. Lagsin mechanisms of revenue indexation contribute to temporary drops in realrevenues, and since the price adjustment of tax revenues is slower than that ofrecurrent expenditures, the financial position of local governments iscontinuously exposed to wide fluctuations. Per capita tax revenues generallygrew in real terms in the sixties and seventies, and declined sharply asinflation accelerated and t'hLe economy faltered in the early eighties: between1960-80, real per capita revenues rose at a rate of 5.1 percent p.a.; in the nextfour years, they fell 9.7 percent p.a.

- 4 -

TAX REVENUES PER CAPITABY REGION

35O

250

ISO.

300

so50

C~~~~~~~R;C

I_AcL WSTTE s LOC

Figure 3

2.06 There is a great degree of spacial variance in thte fiscal performanceof local taxes. For the country as a whole, locally raised recurrent revenuesrepresent only 30 percent of total municipal revenues and cover less than 40percent of recurrent expenditures. The larger and richer municipalities in theSouth-Southeast account for nearly 90 percent of all local taxes, and threecities within this region--Sao Paulo, Rio de Janeiro, and Belo Horizonte- -accountfor almost one-half. Recurrent non-transfer revenues per capita also vary widelyaround the average of US$11.91 for Brazil; ranging from US$3.36 in the Northeastto US$19.61 in the Southeast (in 1984).

MUNICIPAL REVENUES PER CAPITABY REGION

rW6s

so-

4

Figure 4

III. ISS PERFORMANCE

A. The Imoorcance of ISS in Local Government Finances

3.01 A time-series analysts of the roles of ISS and IPTU in the Braziliancapitals reveals a continuous increase in the importance of the ISS as a sourceof locally raised revenues. Between 1972-1984, the share of ISS in total localrevenues of capital cities increased by about 62 percent, while IPTU declinedby nearly 36 percent. In other (non-capital) municipalities, the ISS showsequally impressive results, increasing its share by some 45 percer.t. The reasonsfor the strong ISS performance relative to the IPTU are both political andeconomic.

MUNICIPAL TAX REVENUES MUNICIPAL TAX REVENUESIN THE CAPiTAL CITIES IN THE INTERIOR CITIES

ISS 54%

ipt ~~~~~~~~~~~~~OHER 32% OTERS

1972 1984 1972 1984

Es C UESiO "W EENJs IfEN OF OWN REVENUESTEE INCLUDES tAMES AN EtES l THEN INCLUDES TAXES AND fEESOUNCE: ANNEX I-S ~~~~~~~~~~~~~~~O URCE: ANNEX 1-D

Figure 5 Figure 6

3.02 Because the IPTU is a eirect tax, it is politically costly to enforceregular collection and assessments of the base. Thus, in periods of highinflation and/or elections, real IPTU collections tend to falter. Between 1976-83, real IPTU revenues declined by 4.1 percent p. a. in the capitals, and remainedstagnant in other cities. The ISS, on the other hand, benefited greatly frombeing an indirect tax (and therefore politically expedient) and from the fastgrowth in services output (4.0 percent p.t.), and achieved a 3.7 percent p.a.real increase in the capitals and 3.8 percent p.a. in other cities. Both taxesexperienced a decline relative to domestic output.

B. Allocative Efficiency and Fiscal Incidence

Allocative Efficiency

3.03 One of the objectives of tax policy should be to introduce the leastamount of interference in the allocation of resources. Because receipts fromselected service activities constitute the base for the ISS, the allocation ofresources in the economy is inevitably affected. The tax imparts a wedge between

- 6 -

the relative prices of services and goods as perceived by consumers andproducers. More formally, if we define PTP and P' to be the prices of a taxedservice as perceived by producers and consumers, respectively, and Po the priceof a ron-taxed good, then:

PTP/ /- MRT of T for N f MRS of T for N - PTC/PN;61

since pTP 7 pTC

3.04 The above analysis assumes that the ISS introduces inefficiency toan otherwise efficient allocation of resources. In fact, because the ISS taxesa sector of the economy which is not reached by the state value added tax (IGM)or by any other indirect business tax, it may be argued that it helps restoreeconomic efficiency.

3.05 In any case, the impact of the ISS on resource allocation is minorfor the economy as a whole, given its low average rate and small contributionto public revenues. Revenues from ISS represented slightly more than 2 percentof total government (tax and fees) revenues in 1984 and averaged a mere.28 percent of GDP between 1975-84, in contrast to the state value added tax(ICM), which averaged 4.81 percent. Even as a share of the value of output ofservices, ISS remained a modest 0.54 percent.

Fiscal IncidenceSHARE OF TAXES fN GOP

(percent)3.06 The service firm is a _ _ _

vehicle through which individuals asconsumers and suppliers of services o.. ....derive benefits from the use of urbaninfrastructure. Taxes imposed on 0.

business to pay for these benefits areultimately borne by individuals in 02 ._. .

their capacities as consumers (through e . ..higher prices), resource suppliers(through lower factor returns), and t ; 10 tot84

firm owners (through reduced returns Yearto equity). The welfare reduction to -ss +IPTV

each of these economic agents dependson relative price elasticities of Figure 7supply and demand.

3.07 Without a careful analysis of Brazilian household budgets and taxincidence, we cannot determine the precise equity impact of the ISS. However,scholars generally agree that most indirect taxes on consumption such as the ISS

f/ The MRS of T for N Is defined as the amount of T which must be given up bya consumer for an additional amount of N. The MRT is the amount by vhich theoutput of T must be reduced In order to produce an additional amount of N.

- 7 -

have a tendency to be regressive. Despite the probable positive correlationbetween the share of services axpenditures in household budgets and incomelevels, we expect the tax-to-income ratio to decrease as we move from lower tohigher income groups. This is so because of the low variance in ISS rates andthe relatively higher propensity to save in upper income groups.

3.08 Even though the ISS is probably regressive, it may still bedesirable on grounds of fiscal fairness inasmuch as it is the only municipal taxto effectively reach informal enterprises, a segment of the urban economy whichis otherwise untouched by fiscal instruments. By stretching the overall taxbase, lower tax rates and fees are made possible. This in turn reduces theincentives for tax evasion and contributes to higher yields than otherwiseachievable.

C. Yield

3.09 Despite the predominance of the ISS in local revenues, its yieldis still meager when compared with state and federal indirect taxes. The reasonsfor the low yield capacity of the ISS relative to the state business tax, theICM, are found in the nature and breadth of their bases. In contrast to the ICM,which taxes tangible sales, the ISS taxes intangible ones, which are thereforeless traceable. As discussed in Section IV-F of this report, enforcement of theISS through audits is a very serious problem, and auditing procedures largelydetermine the success or failure of the tax.

3.10 The scope of the ISS base is another obstacle to its productivity.In the case of the ICM, the base is broad, including industrial and agriculturalgoods, and commercial activities; whereas in the ISS, the base is restricted byfiscal legislation to a subset of the service sector, which is subjectivelyclassified as "strictly municipal. I For instance, the legislation excludescommunication, financial, and commercial services that are exclusively under thedomain of the federal and state tax systems.11

Z/ CommunlcatIon, financial, and transport services are taxed at the federallevel by the Tax on Communications (ISC), the Tax on Financial Operations (IOF),and the Tax on Road Transport (ISTR), respectively. Commerce Is taxed at thestate level by the ICM.

- 8 -

Table 1: SHARE OF TAXES IN GDP(Percent)

Year 1976 1977 1978 1979 1980 1981 1982 1983 1984 Average

ISS 0.26 0.29 0.30 0.29 0.27 0.28 0.31 0.27 0.25 0.28IPTU 0.29 0.33 0.39 0.36 0.28 0.26 0.26 0.21 0.19 0.29ICM 4.84 4.82 5.06 4.72 4.70 4.73 5.08 4.61 4.72 4.81

Sources: SEF (Brasilia: 1976-86).Oliveira, INURD Backgroumd Paper

3.11 In addition to the constitutional restrictions on the kinds ofservices that are taxable by the ISS, municipalities themselves createconstraints that severely limit their ability to raise ISS revenues.Municipalities not only set rates that are, on average, very low,A' but alsoallow a large number of potential taxpayers to be exempted from paying taxes.These exemptions are rationalized on the grounds of cost effectiveness;collection costs, it is said, would exceed revenue. This is partly true, butonly because tax rates are too low to begin with, and underdeclarations areunfortunately too common.

./ The tax rate on services has a median of 5 percent for firms, while theaverage ICM tax rate Is 17 percent (note, however, that a direct comparison ofthe two rates Is not very llluminating slnce the ISS taxes gross receipts, whilethe ICM Is a VAT).

Table 2: REGIONAL DISTRIBUTION OFPOPULATION, GDP, AND TAXES (1980)

(Percent)

GDPRegion Population GDP Services ISS ICM

North 4.94 3.10 2.80 0.70 1.60Northeast 29.25 12.00 12.40 9.40 11.90Center-West 6.34 5.50 6.80 5.00 4.90Southeast 43.47 62.40 62.90 74.20 64.50South 16.00 17.00 15.10 10.70 17.10Brasil 100.00 100.00 100.00 100.00 100.00

Sources: FIBGE, Anuario Estatistico do Brasil (1980).SEF (Brasilia: 1980).FGV, Conjuntura Economica (1987).

3.12 The aggregate picture of ISS yield performance conceals the fact that,as a tax system, the ISS works reasonably well in the Southeast region of thecountry and in many of the capitals, but not so well in the North-Northeast andin the interior of the states. In 1984, nearly 85 percent of all ISS revenueswere raised in the southern regions and 72 percent in the capital cities. Agreat deal of the observed variance in ISS revenues can be explained by thevariance in tax base. However, relative tax bases do not tell the completestory; after all, the regional share of service output at the national levelexceeds the share of ISS collections--in national ISS collections--by 50 percentin the North-Northeast, and by 41 percent in the South. The Southeast's shareof service output, on the other hand, is 15 percent smaller than its share ofISS collections.

3.13 Some justification for the high variation in ISS revenues is foundin the wide differences in political and administrative settings among regions.Rapid economic development in many parts of the country has brought new economicstructures into coexistence with old political structures and inadequateadministrative capacity. The problem of ISS taxation is especially serious inthe small rural municipalities, where the system of federal and state transfersprovides little incentives for local fiscal efforts which are politically costly.In such municipalities, already small tax bases are made even smaller by vote-motivated exemptions and poor collection practices. Small cities are also wheretax evasion is most widespread, and audit coverage is too limited to promptcompliance.

-10 -

DISTAI8UTION OF ISS COLLECTIONS DISTRIBUTION OF ISS COLLECTIONIN THE CAPITALS, BY REGIONS IN THE INTERIOA. EY REGIONS

D. Buoyancy of an GIMan

taxgsoe sevcsadra8rpry Thisgurisitoa ditiuin9ffsa

authorTyels fsa reprsnedacnraliing shaift from/67 tsabihedpeiu conmstittoa

arrangement.

3.15 For the most part, the increase in concentration of fiscal revenuesat the central level was merely a reflection of the constitutional centralizationof public policy decision-making. To some extent, however, it was also linkedto the relationship between the base of the predominant taxes in each fiscal4urisdiction and economic growth. State and local taxes tend to be significantlyless buoyant than federal income tax (IR), and income grew rapidly in the sixtiesand seventies.12t The ICM, ISS and IR have bouyances of 0.91, 1.09, and 1.41,respectively.

3.16 There are two basic reasons for the relatively low buoyancy of theICN tax. First, services- -which grew faster than the rest of the economy in the

2/ That reform of the tax code specified the following central government taxes:Income Tax, Tax on Industrialized Products, Tax on Financial Operations, ImportTax, Export Tax, Rural Property Tax, Communications Tax, Road Transport Tax, Taxon Minerals, Electricity Tax, and Fuels Tax.

JXQ/ Growth in real Income averaged 6.6% p.a. between 1964 and 1984.

- 13 -

Table 3: SHARE OF MAJOR TAXESIN EACH JURISDICTION/_

AND THEIR BUOYANCY (1984)

Revenue Share in OwnTax Fiscal Jurisdiction (%) Buoyancy

IR 53.96 1.41ICM 96.59 0.91ISS 59.53 1.09IPTU 40.48 0.07

/A Share of each tax in total tax collections ofcentral (IR), state (ICM) or local governments(ISS, IPTU).

Sources: SEF (Brasilia: 1976-84).FGV, Conjuntura Economica (Rio: 1987).Oliveira, INURD Background Paper.

period observed--are excluded from che ICM tax base. Secondly, the use of theICM as an instrument of economic policy has led to an increasing number ofexemptions and rate reductions intended to stimulate targeted economicactivities, such as the export of manufacturing goods (which are now totallyexempted from paying ICM).

3.17 The relatively high buoyancy of the ISS is largely due to growthrates in the output of services that are higher than in the rest of the economy.However, factors such as a fairly restricted list of taxable services,widespread (and growing) numbers of exemptions, and poor collection practicesmake the elasticity of the ISS tax to the output of services substantially lowerthan to income.

3.18 The high income elasticity of the IR (which taxes income, itself)is attributed to successive increases in the tax rates.

- 12 -

IV. THE ADMINISTRATION OF THE ISS

4.01 The administration of all local taxes fall within rhe responsibilityof the Municipal Finance Secretariat. Although some municipalities might havea self-contained ISS department within the Secretariat, ISS administration inmost cities involves the cooperation of several departments dispersed in thefinance complex:

a) Revenue and Cadastre Department (registers taxpayers andrecords payments).

b) Active Debt Department (controls delinquent accounts).c) Auditing Department (audits tax payments and notifies taxpayer

of infractions and penalties). In large municipalities,auditing is usually subdivided by geographic areas or by typesof service.

d) Legal Department (prepares and executes delinquent accounts).

4.02 Because of the high degree of integration in the administration oftaxes in most municipalities, it is difficult to determine the precise cost ofadministering the ISS. In Belo Horizonte, where the system is more self-contained, it is estimated that costs amount to one fifth of the fiscal yield,with the highest personnel costs incurred by the auditing department (in which,incidentally, most revenues are probably generated).

4.03 The technical level required by the ISS administrators variesgreatly among cities. In large cities, activities linked to identification andregistration of taxpayers usually require, at a minimum, the completion of highschool and some light technical training in bookkeeping, administration or law.Officials working in the legal and auditing departments were invariably collegegraduates, most with accounting and law degrees. In small cities, however,college graduates are seldom found in the administration of the ISS.

A. The Legislative Framework

4.04 The ISS was introduced to the cast of municipal taxes in 1965through Constitutional Amendment 18. In 1966, Law #5172 instituted the'National Tax Code' (NTC), which defined the ISS tax base as "services of anynature provided by self-employed professionals or firms, with or without a fixedlocation.' At first, the types of services local governments could tax werelimited by Decree 406 of 1958 to a list of 29 items, and then ircreased to 66items by Decree 834 of 1969.11'

4.05. The limitation on the exact nature of liable services imposed bythe ISS list is still controversial among jurists and municipal administrators.To many, the list merely exemplifies the types of services which can be taxed,but time and again, the courts have upheld the restrictive nature of the list.

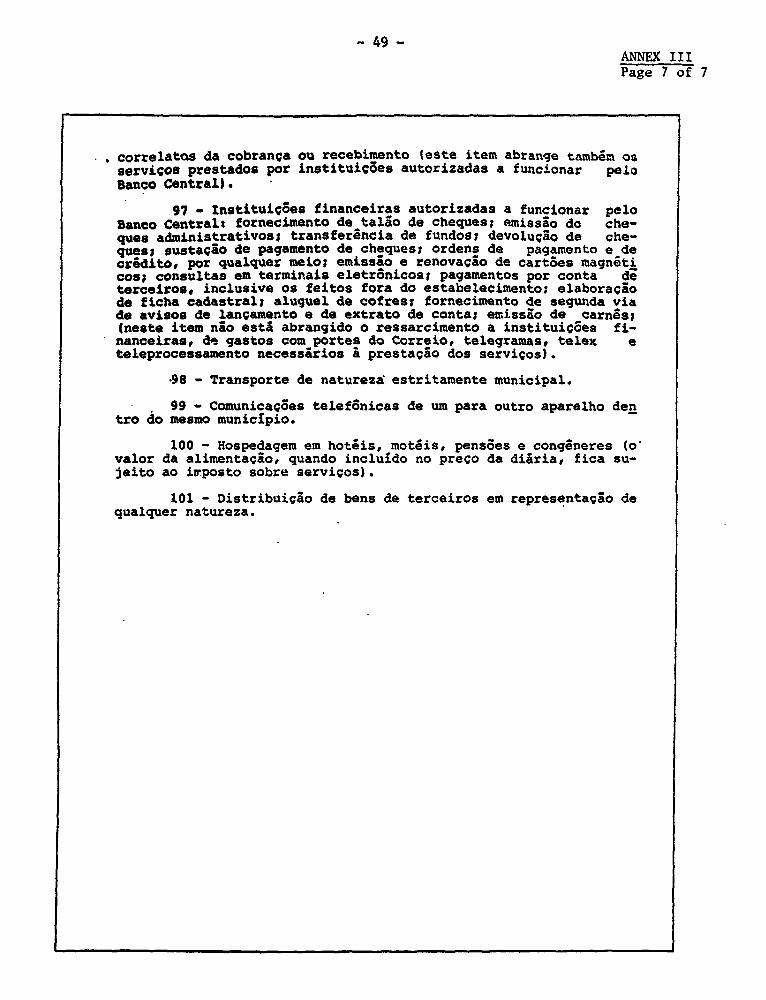

DJ In 1988, the list was expanded to 101 Items (see Annex III).

Table 4: LIST OF SERVICES LIABLE OF ISS

1. Physicians, dentists and veterinarians. 26. Baths, massages, gymnastics. 46. Dry cleaners and laundry services.

Z. Nurses, psychologists, hearing 27. Local transport and communications. 47. Washing, drying, galvanizing, etc., ofspecialists, obstetricians. objects not destlned for coamerce or

28. Public entertainment: manufacturing.3. Clinical laboratories.

a) theaters, carnivals, discos circus; 48. Installation of equipment for final4. Hospitals, sanatoriums, health posts, b) paid expositionst user.

blood banks, rest clinics. c) billiard clubs, bowling alleys, andother games; 49. Installation of carpets, and curtains.

S. Lawyers. d) balls, shows, festivals, recitals;e) sporting events, Intellectual 50. Studios of photography,

6. Agents: industrial property. competitionsl cinematography, vLdeotaping,f) muslcal events; recording.

7. Agents: artistic/liter4ry property. g) transmission of music.51. Photocopy services and any copy

8. Appraisers. 29. Catering services. services not Included in item 50.

9. Translators. 30. Tourist agencies. 52. Real estate rental agency.

10. Free-lance agents expeditLig bureaucratic 31. Intermediation services except those noted 53. Graphic services.processes. in items 58 and 59.

54. Discipline school for animals, anLmal11. Economlsts. 32. Agent services except those noted in items treatment, storage (kennels).

58 and 59.12. Accountants, auditors, CPAs, bookkeepers. 55. Forestry services.

33. Technical analysis.13. Technical/consulting organizations (i.e., 56. Decoration (exteriors and Interiors--

finance, administration, data processing). 34. Organizatlon of conventions, commercial except cost of materials).shows and similar events.

14. Secretarial, short-hand, datllography. 57. Tire retreading.35. Advertising and publicity in general.

15. Administration of business or property, 58. Intermediation of foreign exchange andincluding mutual funds (excluding services 36. Storage and warehousing services. insurance.executed by financial organizations).

37. Deposits (except financial). 59. Intermediation (except services16. Recruitment of personnel. provided by financial institutlons,

38. Storage or parking of vehicles. brokerage houses, and those provided17. Engineers, architects, urbanlsts. by item 58).

39. Hotels, inns, motels including food, if18. TechnLeians in engineering firm: drawing, part of the price of room. 60. Book and magazine binding.

projecting, calculatlng.40. Maintenance of equipment (lf maintenance 61. Aero-photometry.

19. Executlon of hydraulic engineering works, includes repair, then see Item 41).Including complementary works. 62. Billing (including of royaltles).

41. Repair of any object (excluding the cost20. Demolition, maintenance of buildings of parts whlch is subject to 1CM). 63. Distribution of movies and videotapes.

(includ.ng elevators), bridges, roads.42. Engine overhaul (parts not included). 64. Distribution and sale of lottery

21. Cleaning of buildings. tickets.

22. Floor cleaning and waxing. 43. Palnting services (except for real estate 65. Funeral companies.Included in previous item).

23. Dlsinfecting services. 66. Taxidermist44. Education (all levels and nature of

24. Polishing objects. program).

25. Barbers, beauty salons, skin trea. :,. 45. Tailors and seamstresses, when providingservices to final users.

- 14 -

4.06 A second layer of limitations is imposed on the ISS by the centraland state governments. Services that are not strictly municipal are consideredoutside the fiscal jurisdiction of local governments and are automaticallyexcluded from taxation, even if included in the "ISS list." This is the case,for instance, of transport services, which are included in the list, but may ormay not fall within the authority of local governments, depending on thejurisdiction of the area covered by the service.

Classes of Taxpayers

4.07 For tax purposes, the law recognizes two classes of economic agentsthat provide services to the public: the self-employed professional and thefirm. All professionals providing taxable services in exchange forremuneration, in kind or currency, are liable to pay ISS, unless employment ismaintained with a firm. For instance, if self-employed, an economist providingservices is reached by the ISS; however, the same economist is not liable to ISSif employed by a firm. In turn, the liability of the firm depends on whetheror not it provides a taxable service. The professional nature of the providerof a service is of the essence for ISS purposes, and it is determined not onlyby the type of economic activity performed, but also by the frequency ar,dregularity of the activity.

4.08 The definition of a "firm' encompasses, not only legal entitiessuch as corporations, but also professionals employing other professionals ofthe same or lower levels of skill. The maximum number of employees allowedbefore being classified as a firm varies from city to city; in Rio de Janeiro,for instance, an individual provider of services employing more than one personof lower skills or another professional of same skill level, constitutes a firmfor ISS purposes.

ISS and Business Location.

4.09 To be liable to ISS, the taxpayer does not necessarily have tomaintain a fixed business location. For fiscal purposes, the tax is due at thelocation where the service was provided--the place of business--which under thelaw, is understood as being the location at which the service originated, ratherthan the firm's headquarters or the place of delivery of the service.J1 Whenthere exists no fixed business establishment, the address of the taxpayer iswhere the ISS is due. This provision has two objectives: to reduce theprobability of conflicts on matters of fiscal jurisdiction, and to preventdouble-liability of taxpayers.

12/ Article 35 (IV) of the civll code Introduces some confusion to the rule ofplace of business by stating that: "incorporated businesses pay ISS at[headquarters] the place where the board of directors meets and where the centraladministratlon functions. " In practice, many municipalities have draftedsections in theLr municipal tax codes to place the tax liability at the "placeof business.n

- 15 -

4.10 There is one exception to the above rule of business location forpurposes of ISS liability. Article 12b of Decree 406/68 stipulates that in thecase of civil construction, the tax is due where the service is actuallyperformed, rather than at the place of business. This exception only appliesto engineering work that involves new construction, expansion and refurbishing(but not to demolition or maintenance services, which are taxed at the place ofbusiness).

B. Tax Base. Rates and Fees

4.11 As specified in the National Tax Code, the price of servicesprovided to consumers is the base used in the calculation of the ISS tax.However, firms that provide services to the construction industry, and self-employed professionals are treated differently by the law.

4.12 The value of the tax may be separated from the price of the serviceand charged directly to the consumer. However, this practice is limited andusually forbidden when the law allows for deductions or requires taxwithholding.

Construction Industrv

4.13 In the case of services related in any way to construction,demolition or maintenance of engineering structures (items 19 and 20 of the ISSlist), the tax base consists of the value of the service net of the cost ofmaterials, as well as the value of services provided by subcontractors alreadytaxed by the ISS.

Self-Eftl=ved Professionals

4.14. For self-employed professionals, the tax is not directly relatedto the value of services, but instead, is set in terms of a 'Fiscal ReferenceValue' (Unidade Padrao Fiscal, UPF). The real value of UPFs is usually keptconstant by adjusting them according to an indexed treasury instrument (OTN).Municipalities can adjust the local UPFs at a pace faster than the rate ofchange in OTNs, but such adjustments are less common and require locallegislative approval. A fixed fee, expressed in terms of locally denominatedUPFs, is imposed for each professional and is generally higher for those withhigher skills or longer career histories. For instance, in Recife, capital ofthe state of Pernambuco, professionals with college degrees pay an annual taxof 0.75 UFR,1I whereas other professionals pay between 0.30-0.40 UFR, dependingon the skill requirement for their profession.

4.15 The rationale for not taxing the price of services provided byself-employed professionals has both a practical and a juridical basis. Anyattempt to tax the self-employed based on the value of their services would be

DJ UFR or Unidade Financeira do Recife is the reference value for the clty ofRecife and corresponds to 3.5 OTNs; one 07W worth CZ$424.51 in October 1987.Therefore, the ISS tax on self-employed professionals ranged between US$8.74-21.84 p.a. In October 1987.

- 16 -

plagued by widespread tax evasion. Moreover, many self-employed are neithertechnically prepared nor financially able to keep fiscal books. At any rate,tax audits would not be cost effective for the municipality, except in the caseof highly paid professionals. The juridical reason for not taxing the value ofpersonal services is derived from a constitutional provision which reserves thisparticular tax base for the central government.

Single-Profession Partnerships

4.16 Federal legislation (Decree 406, Article 9) extended the taxationof services on the basis of reference values, rather than price, to firms thatprovide services itemized under numbers 1, 2, 3, 5, 6, 11, 12 and 17 of the ISSlist. Essentially, this sub-list covers skill-intensive professions in thefields of medicine, engineering, economics, business administration and law.

4.17 The differential treatment accorded to these 'Single-ProfessionPartnerships' (Sociedades Uniprofessionais) is rationalized on the basis thathuman, rather than physical capital is the most important factor in theproduction of such services. Thus, each individual in the firm provides aservice as if he or she were acting as a self-employed professional, withrelatively little contribution from capital or other factors. In Rio deJaneiro, for instance, firms with less than three low-skill employees per high-skill partner>/ or other high-skill employee would pay 1.0 UNIF-1 per month, perprofessional partner or high-skill employee. Firms with three or more low-skillemployees would pay 1.0 UNIF per month, per partner or high-skill employee, and0.4 UNIF per month, per low-skill employee exceeding the pre-stated limit.

4.18 It is not uncommon to find municipalities that incorrectlycategorize firms of professionals outside the restricted high-skills list assingle-profession partnerships, entitled to the same tax treatment enjoyed byself-employed professionals.

Rate-Setting for Firms

4.19 Very often, municipal administrators are unaware of their fiscalpowers regarding ISS rate-setting. The confusion in this area was caused by alaw (Complementary Act 34, 1967) that imposed rate limits of 2 percent forengineering work, 10 percent for games and public entertainment, and 5 percentfor all other services. Although this law was later revoked, many localgovernments still maintain these limits for most services. The new constitutionmight reintroduce ceilings on the ISS rates.

IV High-skill here means a profession Included in items 1, 2, 3, 5, 6, 11, 12and 17. All high-skill partners must belong to the same high-skill profession(thus the term single-profession partner).

II/ UNIF (Unidade de Valor Fiscal do Municipio do Rio de Janeiro) is thereference value for Rio de Janeiro; in October 1987 It was worth 2.34 OTNs, orCZ$991.65.

- 17 *

4.20 Where rates have been changed, they have been almost invariablylowered and do not seem to reflect the local administration's judgment of usageof public services or ability to pay for them. Given the low tax rates for mostservices, it is not surprising that, as far as the ISS is concerned, a numberof firms in the lower end of gross revenues Is not fiscally cost-effective.

4.21 Rates for firms in Rio de Janeiro currently range between 5 percentand 10 percent, with 5 percent being the median (see Box 1).1' The rates formore than two thirds of the services in the ISS list for Rio are the same aswhen they were first set by the central government. In other cities whereservices are not a significant share of output, even less care is exercised inthe setting up of rates. Belo Horizonte, for instance, preserves the originalISS rates for some four-fifths of the list, while maintaining an equally low 5percent median (see Annex IV for a national comparison of ISS rates and fees).

4.22 The law determines the tax liability based primarily on the nature ofthe service, and only secondarily, on the characteristics of the provider ofservices. Therefore, in the case of multipurpose firms, the tax is calculatedfor each service performed by applying the proper tax rate to the price of eachservice.

C. Exemptions

4.23 Since ISS fees are so low, local governments are inclined to exemptmany categories of low-skilled, self-employed professionals. It is a commonpractice to exempt large numbers of professionals considered to be of low taxyield, rather than attempt to raise the yield through revisions of the feesystem. Similarly, firms engaged in low fiscal yield services might be exemptedfrom paying ISS. On the other hand, cities also use the ISS as a bargaininginstrument to bring business into their borders. As a result, some potentiallyhigh-gross receipts firms are often taxed at very low rates, or even exemptedfrom paying ISS altogether. This is the case, for instance, of hotels in thecity of Rio de Janeiro, which are exempted from paying TSS until 1990.

4.24 A study by Ribeiro de Morais 11 examines the municipal legislation ofseveral municipalities and concludes that local governments tend to exempt:

a) providers of services with low gross receipts;b) services provided by low-skill professionals working in their own

place of residence and without employees;c) sport activities;d) theatre and circus shows.

JAI The 'all other services" category which is taxed at 5 percent inlcudes mostservices provided In Rio de Janelro.

JZ/ Ribeiro de Morals, B. Doutrina na Pratica do Im2wsto Sobre Servicos, SaoPaulo, Revistas dos Tribunals, 1985, pp. 563-584.

- 18 -

TAX PATES FMU TB! CITY OF RtIO DE JAMEIRO

Service 4.X)

1. Advertisement and publicityt

a) Services performed by media print, radlo, TV . 0. .b) Services provided by advertdsing agencies 1 1.0a) Special services such as market research sales promotions and public relations . S.0

2. Execution of civil construction, hydraulic works, sdiilar works and aervices toasstst these works or to complement them . 2.0

3. Demolition services, maintenance, cleaning and repairs of buildings (exceptelevators)i services to maintaLn and repair roads, bridges and similar structures . 2.0

4. Consulting services related civil construction, hydraulic wvrks andother construction works , . 2 0

5. Services related to technological research and development. 0.5

6. Upairs, maintenance and conservation of air, sea and rail vehicles(Lnrluding paintg) . 2.0

7. Cocmercal Leasing.. 2.0

8. Data proOessing and icrofilming.. 2.0

9. Real Estate intermediation .. 3.0

10. Tourism (including comaissions on the sale of tickets), industriaL transporteervicesg services related to credit card operations- .S. -

11. Bosptals, linics, resting homes, blood banks, milk banks, first aidposts and related services provided by pharmacis .. 30-

-12. Nedielfhaospital services 1rovlded to firms or indtviduals with price ftxed..by contract and paid for by periodical tontributions.w - Z 0

IS. 6amse and amusement services of any kind . . . . . . . . . . . . . . . . . . .. . .. 10.0

14.i Distribution and sole of lottery tickets .. . . IO-.

S5. Aero-PhotogrMmetry, topography and related services . ... 3

16. Dry cleaning and laundry services . .2 .0

i7. Piblic exhibition of movies.. 2.

18. All other.,servtces. . . . . . . . . . . . . . .. .50. . . . . . . .. . .

Box 1

4.25 Although the National Tax Code places the ISS within the jurisdictionof local governments, the central government reserves the right (by lecree406/68, Article 11) to issue exemptions from any municipal and state tax. Themost relevant exemption established by the central government has been on civilconstruction works, hydraulic works, and related services of engineeringconsultants, when the work has been contracted with central, state or municipalgovernments, or with government enterprises.

- 19 -

D. The Fiscal Registry

4.26 Nearly all municipal tax codes require that every individual and firmproviding services register in fiscal registries before initiating operation.The obligation to register is indeper,dent of either ISS exemption or place ofbusiness. As long as the service is provided in the municipality, providersmust register. Municipal registries in most capitals have already beencomputerized, and standardized information is readily accessible to all finance-related departments of the local administration. Many small cities have alsopurchased and installed computers, but the operation of computer systems outsidethe capitals has been plagued with problems, mostly related to inappropriatetechnology and lack of trained personnel.

Registration Procedures

4.27 Although procedures for registering vary from city to city, registriesgenerally contain the name and address of the self-emfloyed professional orfirm; (and of partners and directors), type(s) of services performed, and dateof commencement of operations. Professionals must present their national IDcards, income tax ID number, and in the case of regulated professions, proof ofability to perform the services (e.g. diplomas, certificates, proof of membershipin professional associations, etc.). Firms must provide the following: a copyof the registrar of incorporation, or other documents establishing the formationof the firm; proof of registration with relevant agencies controlling theactivity; national ID cards of partners, directors and the president; and companyincome tax ID (see Annex II-A).

Maintenance of Registry

4.28 Professionals and firms remain obligated to notify local governmentsof any change in the information contained in the registry within 30 days of thechange. In the event that business operations come to an end, the municipalitymust be informed, also within 30 days, otherwise their liability to ISS willcontinue.

4.29 Discovery and subsequent maintenance of the registry is mostly doneon a voluntary basis by the providers of services. Except for ad hoc revisionsof the city's economic registry (usually done in conjunction with projects toupdate real property cadastres), most new registrations are self-declarationsof professionals and firms.

Incentives to Register

4.30 The incentives to register are fairly strong, reason why nearly allpotential service providers aware of their tax obligations eventually register.Self-employed professionals need to be registered in order to receive socialsecurity benefits, and firms are required to show proof of ISS registration inorder to obtain a license to do business (see Annex II-B). Those who do notregister are usually violators with respect to several other taxes as well, andtend to operate in the fringes of the economy.

- 20 -

4.31 Effective pressure on professionals and firms to register may alsoresult from government scrutiny of the firms' expenditure accounts. A registeredfirm may not deduct the cost of services provided by a professional who is notregistered, unless 5 percent of the value of the service is withheld for theprofessional and paid by the firm together with its own ISS bill. Sinceprofessional fees are very low, it is unlikely that professionals consider itcost-effective to simply disregard registration and opt for the default procedureoutlined above. An unregistered firm is rendered technically unable to withholdISS from professionals and thus will be reluctant to hire the services ofunregistered professionals, unless it is prepared to exclude the cost of theseservices from its accounts. In order to deduct the cost of services receivedfrom firms, (i.e. for income tax purposes) the beneficiary of these services musthave an approved fiscal receipt--which is numbered and contains the ISSregistration number of the provider of the service. We did not have theopportunity to determine how this cross-check actually works; however, anecdotalevidence suggests that it works reasonably well in the formal sector.

E. Billing and Collections

4.32 Billing of the ISS is primarily based on tax declarations submittedby the providers of services. Applicable fees and rates are determined at thetime of registration.

Professionals and Single-Professional Partnerships

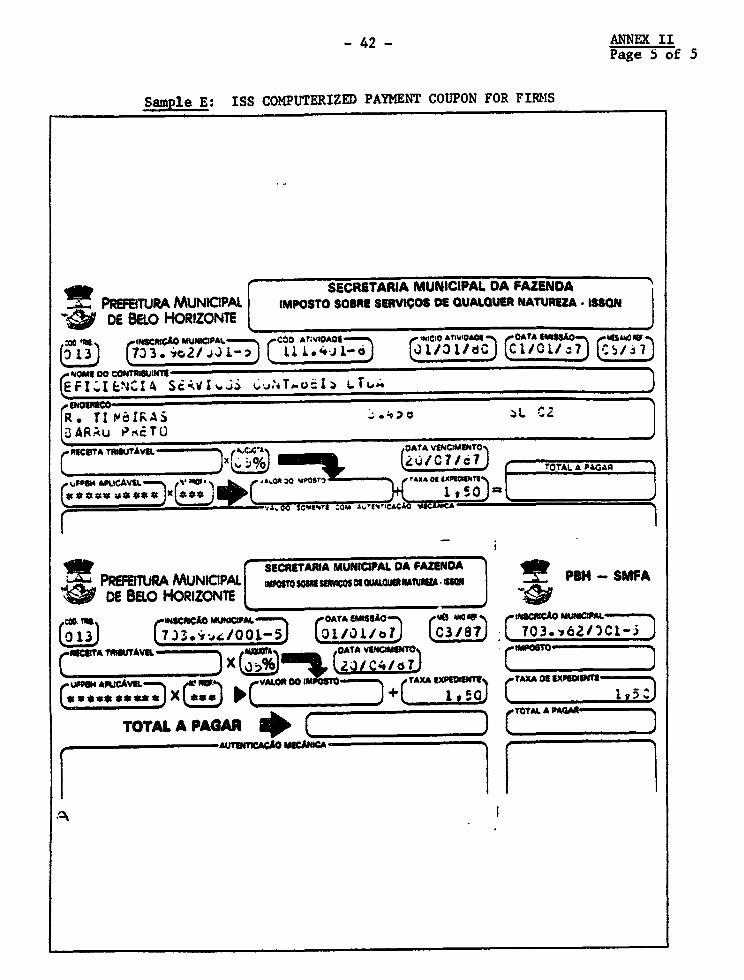

4.33 Taxpayers subject to fixed ISS fees--such as self-employedprofessionals and single-profession partnerships fill up a 'payment slip' (guiade pagamento, see Annex II-C) and pay at authorized banks or at the city'streasury. In cities where the registry has become computerized, a bill (seeAnnex II-D) is sent to each taxpayer to be settled in a single payment or ininstallments, which are usually indexed to expected inflation. It is speculatedthat most ISS evasion by self-employed professionals is due not to unwillingnessto pay taxes, but rather to negligence. Evidence indicates that where billingbecame computerized, and shifted from a passive to an active system of mailingbills to each potential taxpayer, collection efficiency rose markedly.

Self-declaration by Firms

4.34 In the case of firms (other than single-professional ones), paymentis based on a self-declaration of the month's gross receipts. The tax amountowed to the municipality is calculated by the firm and paid at authorized banksor at the city's treasury (see Annex II-E).

Bank Collection

4.35 The option to make tax payments at banks, which is not always availablein smaller municipalities, may sometimes represent a high cost to the city. Inmost places where arrangements for tax payments at banks have been made, themoney is immediately made available to the city. In some cities, however, fundsare held by the banks for up to five working days as payment for the service--representing a substantial loss of purchasing power, given typical inflationrates of up to 20 percent per month.

- 21 -

Fiscal Substitution

4.36 In order to expedite the collection process and reduce the incidenceof underestimation, some municipalities have initiated the practice of 'fiscalsubstitution' (substituicao tributaria). This involves billing one firm for theestimated value of the ISS owed by those firms with which a contractualrelationship is maintained. In Rio de Janeiro, for instance, as of August 1987(Law #1044), firms leasing equipment to other firms who, in turn, sublease ortemporarily rent the equipment to the public (as in the case of Xerox machines),are required to withhold taxes for the lessee. Taxes are based on an estimateof gross receipts derived from the use of the equipment, which is calculatedfrom the value of the lease agreement plus the normal trade profit margin.

Collection Efficiency

4.37 Since the number of persons filed in the fiscal registry bears littlerelationship to the final number of taxpayers, due to the multiple purposes ofthe registry, the high incidence of exemptions, and poor record-keeping ofindividuals who change residence, it is difficult determine collection efficiencyfor self-employed professionals.1 81 Where data is available, it suggests thatabout 70 percent of due fees are paid. It is not meaningful to talk aboutcollection efficiency for firms; since firms calculate and declare their own taxliability and pay accordingly, taxes paid are by definition exactly equal totaxes due. The relevant issues are the estimation of the tax liability by thefirm and the incidence of tax evasion.

F. Tax Enforcement

4.38 Because the ISS paid by firms is based on self-declarations of grossreceipts, taxpayers are tempted to underdeclare the price and volume oftransactions. In Recife, for instance, it is estimated that more than two-thirdsof registered ISS firms are less than candid about their receipts - translatinginto losses to the municipality of at least one-fourth as much as it is actuallycollected.

4.39 Enforcement of the ISS is shared by the audit and legal personnel,whose officials largely determine the success or failure of the tax. In somecities, the ISS is effectively a voluntarily tax; no efforts are made to elicitregistration, and no auditors are hired to supervise the accounts of the firms.This occurs mostly in places where other major sources of revenue are availableand where politicians feel that strict enforcement of the law might not bepolitically cost-effective. However, in major cities, where services represent

W[/ In Rio de Janeiro, only some 97,000 professionals paid taxes in 1985, outof a total of more than 800,000 registered in the ISS cadastre (many of whichno longer live In Rio or work In the stated profession). In Recife, where greatefforts have been taken to update the professional cadastre, and where activebilling Is practiced, nearly 65 percent of the registered Individuals are ISStaxpayers, and 80 percent of the tax bills mailed to them are actually paid.

- 22 -

a large share of output, audit departments comprise the bulk of ISS personnel.

Auditors axid Merit Pay

4.40 In our sample of municipalities, the number of auditors varied fromnone in Almirante Tamandare, to over one hundred in Rio de Janeiro (working inthe office and in the field). According to the director of audits in the cityof Recife, the optimum ratio of auditors to firms should be about 1:200 (theirpresent ratio is 1:300). Auditors in major cities are usually very well paidby national standards (initial salaries for auditors start at US$1,000 in Riode Janeiro), with prospects of steep salary scales. In many cities, the basepay for auditors is rather low, but merit scales can push earnings up overtwenty-fold. In Recife, the monthly base pay is a mere US$100, but productivityearnings may increase salaries up to nearly US$2,000 (see Annex V for adescription of the merit pay system in Belo Horizonte and Recife). Requirededucational levels for tax auditors are quite high in capitals and large cities.In Rio de Janeiro, Belo Horizonte, Recife, and Curitiba, all auditors have atleast a college degree (usually in accounting or law), and a number of them hadundertaken some additional professional courses or finished graduate studies.

4.41 The financial return to the work of tax auditors is sizable: inPetropolis, each auditor brings about US$480,000 p.a.in direct revenues, and inCuritiba, close to US$600,000. It is impossible to determine how much ISSrevenue can be attributed to the demonstration effect of the audit unit as awhole, but it may be assumed to be very large.

Audit Strategies

4.42 Audit strategies vary widely among cities. Some municipalities employ3ophisticated procedures to monitor fluctuations in real tax declarations as afunction of socioeconomic variables, while others continuously draw firms atrandom for audits. In Belo Horizonte, the selection is based on unexpectedfluctuations in gross receipts and variations in the expected fiscal yield ofan audit. Rotation of auditors is a common feature in most medium and largecities. For administrative purposes, 'audit groups' (inspetorias) are segregatedby geographical location or by types of services. In either case, auditors arerarely allowed to stay in the same group for extended periods of time, in fearthat a continuous relationship with a set of firms might render the auditor toopredictable, or worse, too neighborly. In nearly all places visited, littleattention was paid to the relatively low-yield, professional fee.

UDdating the Fiscal Registry

4.43 The first step in the enforcement process is to corroborate that theexisting list of registered taxpayers is complete. To locate those who fail toregister despite the incentives for self-registration mentioned earlier, auditorsmay also request the assistance of the central government to detect potentialtaxpayers who declare federal income tax but fail to meet their localobligations. A project coordinated by the Finance Ministry (Projeto Integracao)establishes a link with the central government and provides local governmentswith a roster of service-related firms and professionals, together with theirdeclared gross incomes. Already computerized municipalities are then able to

- 23 -

compare and update their registry files based on the roster used by the federalincome tax system (the federal income tax ID number is common to the ISS and toincome tax returns).

4.44 Some registry updating is also accomplished during the maintenance ofreal estate cadastres, and the normal rounds of auditors.

Accounting Re3Auirements

4.45 Accounting requirements by the fiscal authorities vary widely acrossthe country according to the nature of the service provided by the firm. Ingeneral, municipalities demand that three books be kept by all firms:

a) Registry of Purchases: records the purchase of all goods andservices by the firm;

b) Registry of Fiscal Documents and Occurrences: records all fiscaldocuments and their usage, also flags fiscal audits anddiscrepancies found by the auditor;

c) ISS Registry: records the total daily business transactions byday of the month, with respective fiscal numbers, includingexempted service, ISS withheld for other firms or professionals,and the total ISS paid in the month--sometimes also stating thebank in which payment was made.

4.46 In the case of firms providing civil construction services, specialbooks are usually required to record purchases of materials and services, andcalculate ISS liability. This is done because the tax base for constructionservices is net of the cost of goods and services used by the firm. SpecialISS registry books are also required of financial institutions and firms subjectto fixed ISS fees.

4.47 Production and issuance of fiscal receipts are closely monitored andchecked against the Registry of Fiscal Documents and the ISS Registry. Numberedreceipts must conform with models provided by the municipality and must containdetailed information about the firm, the nature of the service performed, andthe place where the receipt was printed.

Tax Evasion and Penalties

4.48 The several cross-checks available to the municipal authorities ensurea fairly complete fiscal registry. The problem plaguing the ISS is not thatfirms fail to pay taxes, but that they almost invariably understate grossreceipts. Because the ISS has a variable tax base that is self-declared, thereis a great incentive for taxpayers to underdeclare, unless strict enforcementmechanisms are in place. The enforcement system consists of (severe) locallylegislated penalties for delayed payment or misstated gross receipts, and anaudit unit to conduct checks and impose fines.

4.49 Penalties for noncompliance of ISS and enforcement procedures varyamong cities. Generally, local governments deal with late payments by price-indexing the tax due and imposing penalties over the indexed value of the dueamount. Fines increase with time (in our sample of cities, reaching up to 60

- 24 -

percent of the tax due after a three-month delay) and usually become very severeif administrative or legal action is undertaken.

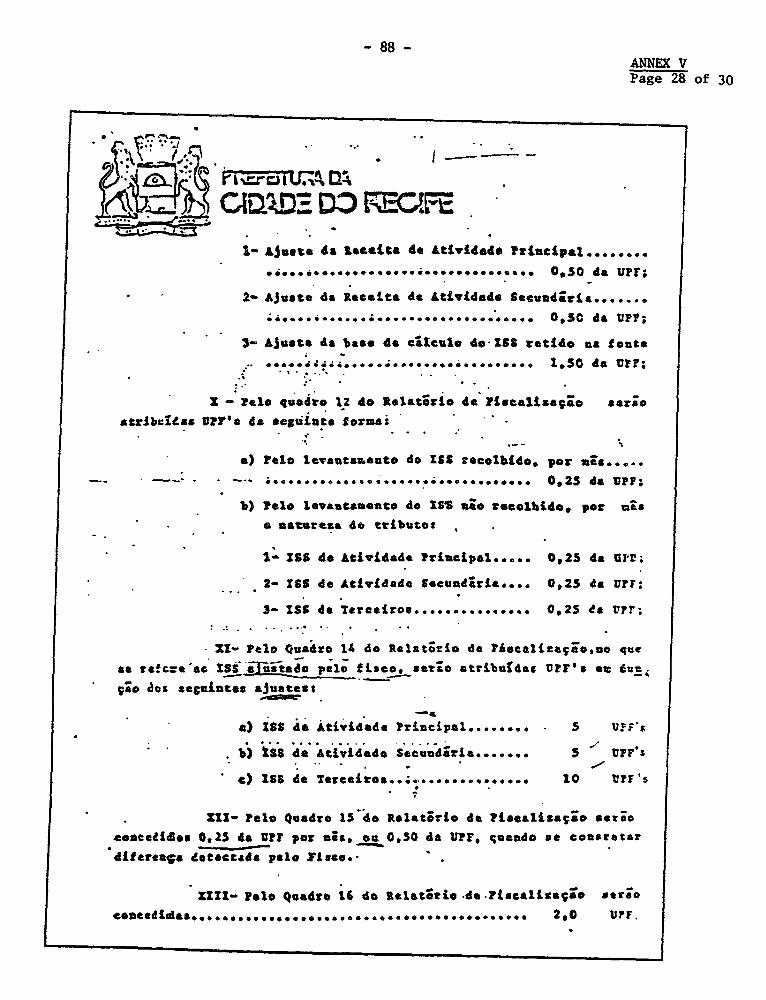

4.50 Infractions involving the action of auditors are severely punishedwhen they are discovered. Cities participating in project CIATA (details ofCIATA on Chapter V) are recommended the following schedule of fines:

PercentInfraction o1f-Tax Base

1. ---Failure to regi-ster in the -ISS registry-or-to inform of changes in status .............................. 2.5

2. Absence of required fiscal book(s), errorsin the ISS accounting system, lack of ISSregistration number on fiscal documents ................ 0.5 - 1.0

-3.- Missing fisa receipt(s), refusal to show--..fiscal book(s), removal of books from placeof business.' 20

:4'.- If, intent to defraud the government:is established-,- a-- - -- fine of 1.00-lO p,ercent .on the differen-ce between , -- .--

-the ta paid and takxdae, to be imposed independent

-:. -Eines of udp to-- 200 :percent on he- tax due fbrfailure`to WWithholdor pay the tax,- to be imposed-:d e-pen.et ofitems 1,2:and -3.

Box 2

4.51 The audit process is initiated by an administrative order (auto deinfracao) directing the firm to present fiscal book(s) within a pre-establishedreasonable time to the auditor in charge. During the fiscal action, book(s)remain(s) at the auditor's disposal and may not leave the establishment untila formal administrative release is issued.

Taxoayer Recourse

4.52 Following the confirmation of an infraction and the imposition offines, the firm may invoke its right to an administrative review, and if stilldissatisfied, may petition to have the case examined by a 'Municipal TaxCouncil,' usually composed of local administrators and members of the generalpublic. The last recourse available to the taxpayer is the judiciary sphere ofpower. In Rio de Janeiro and in Belo Horizonte, between one-fourth and one-third of the cases brought to the first recourse are decided in favor of the

- 25 -

taxpayer, and of those taken to the second recourse, 15 to 20 percent aredecided in favor of taxpayers. In smaller cities, the share of decisionsfavorable to the firnm tends to be much smaller, perhaps because many of thepetitions to review infraction cases are carried out informally by theadministration; only more serious offenses reach the formal administrativeprocesses.

- 26 -

V. PROJECT CIATA

5.01 Project CIATA (Convenio de Incentivo ao Aperfecionamento TecnicoAdministrativo) is coordinated by the Secretariat of Economics and Finance (SEF),a department in the Ministry of Finance. The role of SEP is to advise statesand municipalities on technical matters related to taxes and fiscaladministration, as well as to organize and execute fiscal cadastres for stateand local goverment staff. Over the years, assistance has been provided mostlyin the areas of tax legislation, rationalization of fiscal documentation, fiscalaccounting and fiscal cadastres/registries. CIATA, which was was set up 14 yearsago, has been implemented in nearly 1,300 municipalities--about one third of allBrazilian local governments.

5.02 Since the project involves the conversion from manual to computerizedsystems, SEF has sought technical cooperation from the 'Federal Service of DataProcessing' (SERPRO) or its state-level counterparts in many of the largermunicipalities covered by CIATA. Overall, the partnership with SERPRO seems tohave been successful, in light of significant improvements in fiscalcadastres/registries, billing, collection and technical training. However, somelocal administrators are raising questions concerning the adequacy of their dataprocessing equipment; in fact, the mission had the opportunity to observesituations of clearly deficient technology setup.

A. Objectives and ImRlementation

5.03 Project CIATA grew out of the realization that the great majority ofBrazilian municipalities are unable to finance locally a substantial share oftheir budgets, to some extent, because of inefficiencies in the fiscaladministration.

5.04 The objectives of CIATA are as follows:

a) provide the municipalities with two sets of registries-a realestate cadastre and a socioeconomic registry--prepared by modernmethods, with the intent to achieve greater fiscal fairness andadditional municipal revenues;

b) improve the technical capacity of the local administration;c) introduce fiscal legislation compatible with the financial

potential and need of each municipality;d) rationalize municipal fiscal systems;e) establish procedures for continuous maintenace/improvement of the

CIATA technology.

The project is implemented at the three levels of government:

a) the central government, through SEF is responsible for determiningthe basic parameters of the project, and coordinating all projectactivities at, the national level, including all norms related tocadastres/registries, data processing, billing and collection;

- 27 -

b) the state governments, through their finance secretariats, isresponsible for coordinating project activities within theirrespective territories;

c) The municipal government, through the office of the mayor, isresponsible for providing local support to the project, followingall basic parameters laid out by CIATA, and assuring the continuityof the project after implementation;

5.05 Actual execution of the project in each municipality is theresponsibility of SERPRO (or its state-level counterparts). During theimplementation phase, SERPRO trains local functionaries, prepares maps, executesand coordinates field identification and registration of fiscal units, compilesand processes data, mails automated bills for IPTU, municipal fees and (in somecities) ISS, and develops billing and collection systems for non-automatedmunicipalities. In the post-implementation phase, SERPRO transfers the requiredtechnical know-how needed to make the municipality self-sufficient in CIATAprocedures; including those for maintenance of fiscal cadastres/registries andannual evaluation of fiscal performance. Moreover, SERPRO continuously providestechnical training to keep local functionaries abreast of changes in CIATA.

B. Project Performance

5.06 This paper will not detail the actual procedures for the preparationof the fiscal cadastre/registry, which in fact, is the most substantial componentof the CIATA project. The bulk of the work on the fiscal cadastre/registryinvolves collecting and processing real estate data, since compilation ofsocioeconomic data relevant to the identification of ISS taxpayers is technicallysimple and takes a relatively small amount of time."/

5.07. On the whole, project CIATA is achieving many of its objectives. Injust under 14 years, it was able to provide technical assistance to some 1,300municipalities, most of which now have a standard fiscal code, a fairlycomprehensive fiscal cadastre/registry and modern procedures for billing andcollection (at varying degrees of efficiency).

5.08 A sample of municipalities that have participated in the CIATA projectin 1982 shows that, in the short run, fiscal performance indeed improved as aresult of CIATA. After implementation, total ISS revenue jumped by 77 percentin the first year, and by 13 percent in the second year, whereas IPTU receiptsrose by some 50 percent in the first year new appraisal values becameeffective .21

IV For details on CIATA procedures on the preparation of the real estatecadastre, see William Dillinger's forthcoming INU Discussion Paper on theBrazilian Tax on Property.

2Q/ The sample from whlch these conclusions were derived was small, and taxrevenues varled considerably between large and small cities.

- 28 -

Table 5: FISCAL PERFORMANCE OF CIATA MUNICIPALITIES(CR$ '000)

Municipality 1981 1982 1983 1984

ISS

Sao Luiz (MA) 119,306 413,997 1772,560 3,394,918Alterosa (MG) 269 239 733 1,587Camanducaia (MG) 385 728 1,255 2,190Carlos Chagas (MG) 504 1,177 1,616 5,557Nova Era (MG) 2,127 6,127 8,366 22,988Varginha (MG) 31,733 63,466 135,767 425,440Sertania (PE) 161 237 1,177 735Tabira (PE) 18 34 80 185Trinidade (PE) 25 32 109

Average 17,170 60,751 213,509 428,190Indexed Average/_ 345,376 611,870 691,330 428,190Growth Rate 77.2% 13.0% -38.1%

Indexed Brazil/ag 1,383,915 1,521,471 1,035,372 998,740Indexed Brazil (interior)/a 410,554 417,034 282,475 282,953Growth Rate (Brazil) 9.9% -31.9% -3.55%Growth Rate (interior) 1.6% 32.3% 0.2%

IPTU

Sao Luiz (MA) 41,350 77,213 473,054 882,234Alterosa (MG) 836 1,986 4,127 8,139Camanducaia (MG) 4,033 11,509 18,032 54,516Carlos Chagas (MG) 2,110 4,351 7,550 12,375Nova Era (MG) 3,763 7,820 13,813 26,244Varginha (MG) 7,730.5 15,461 39,762 89,101Sertania (PE) 225 293 359 7,120Tabira (PE) 392 333 992 1,572Trinidade (PE) 77 549 1,375 2,093

Average 6,724 13,279 62,118 120,377Indexed Average/a 135,257 133,748 201,135 120,377Growth Rate -1.1% 50.4% -40.2%

Indexed Brazil/a 966,020 994,899 766,849 665,000Growth Rate (Brazil) 3.0% -22.9% -13.3%

Sample of cities which have participated in the CIATA project in 1982/a Thousands of 1984 CruzeirosSources: SEF (Brasilia 1981-86)

- 29 -

5.09 A comparison of the fiscal performance of these cities with thenational average over the same period--including and excluding the capitals--seems to confirm that the project does improve the chances of a municipalityoutperforming the average (see Table 5). The initial increases in ISS revenuesin CIATA cities is specially significant when contrasted with the rest of thecountry, which showed moderate growth in 1982 and an actual decline (of 32%) in1983.

5.10 Most of the increase in IPTU revenue came from new additions to taxrolls and the reappraisal of properties, rather than from changes in tax rates,or improvements in collection and billing. Data on the efficiency of collectionis not available for the cities in our random sample. However, in the citiesvisited by the mission, the CIATA's impact has been erratic, though positive onthe whole. The impact on the reappraisal of properties is positive on twocounts: a) it increases the accuracy of the measurement and description of theproperty and surrounding improvements, b) it forces the local government torevalue the property, though usually at significantly below-market value.

5.11 To the extent that data permits a conclusion, it appears that CIATAhas been a relatively successful technical aid program for local governments,but with few prospects of permanently raising local government revenues, sincethis is mostly a political, rather than a technical problem in Brazil. In thelong run, most of the gains made by CIATA tend to dissipate, as local governmentsallow appraisal values of properties to lag behind inflation, and aseadastre/registry maintenance is de-emphasized. Though real revenues from IPTUand ISS increased substantially by the first anniversary of project completion,they fell after just a few years. In our sample of Table 5, real revenues fromIPTIJ and ISS dropped by 38 and 40 percent, respectively, just two years afterproject completion.

- 30 -

VI. OaNCLUSION

6.01 On the whole, the ISS may be considered a good, and in the context ofthe present constitutional setup and transfer system, an indispensable taxavailable to local governments. Brazilian cities depend on local governmentsto provide a large share of required public services. However, transfers fromthe central and state governments are often not in tune with the expenditureresponsibilities of the average municipality. The timing of transfers is notalways suitable, and then there is a substantial, uncertain amount of funds thatis tied to political patronage. Since cities are very restricted in the kindsof fiscal instruments they have at their disposal, and since most of theinstruments available are politically difficult to manage, budgeting is adifficult exercise. The ISS, being an indirect tax and thus politically lessvisible than most revenue alternatives, is able to provide some degree ofstability and maneuverability to local finances. Compared with the property tax,the ISS is much less affected by inflation since the assessment base (ie., theprice of service) is automatically adjusted for inflation (except in the caseof self-employed professionals) and tends to grow at least as fast as the overalllevel of economic activity.

6.02 The two most notable characteristics of the ISS in the context oflocal taxes are its fair yield capacity and administrative simplicity.

Yield

6.03 Despite a relatively small base, low rates, and many exemptions, theISS was able to yield (in 1984) US$4.03 per capita, thus bringing in nearly one-half more than IPTU, the next best source of non-transfer municipal revenues.This represents some 12 percent of municipal recurrent revenues, and nearly 34percent of locally generated revenues. ISS yields are substantial in thecapitals, and in the South-Southeast regions of the country, but well belowpotential in small municipalities, and in the North-Northeast regions.

6.04 The ISS has been the target of criticism for its small significancein the finances of the underdeveloped areas of the country. To a large extent,the unsatisfactory performance of the ISS outside the South-Southeast regions(particularly in small cities) is the result of the economic characteristics ofthese municipalities, the lack of political will to tax and fiscal-administrativeshortcomings. Since the base of the ISS is the price of services, it should notbe expected to provide a significant contribution to the recurrent revenues ofsmall or rural based communities. As these communities develop, however,services will become a larger share of output, and ISS yields will naturallyrise.

Administration

6.05 It is difficult to isolate administrative weaknesses of municipalfiscal systems from political motivations. As long as the present system oftransfers from state and central governments prevails, the incentive for citiesto increase the share of locally generated revenues is substantially diminishedby the political cost of introducing administrative changes which could improve

- 31 -

local tax effort. At present, a significant share of funds available to localgovernments come from what is properly called "negotiated transfers". These aretransfers untied to revenue sharing formulas and are dispensed solely on thebasis of political patronage.

6.06 If the system of transfers changes, or if public awareness of thebenefits generated from tax payments improves so that the net political cost ofincreasing local yields is reduced, technical obstacles will then have to betackled in a number of areas of the ISS administration.

a) Identification. Expand the fiscal registry to include allproviders of services in the informal sector and improve theexisting mechanisms for maintaining taxpayers' records throughperiodic economic census and cross-checks with the federal incometax system.

b) Rate and Fee Setting. Develop a new system of fee-setting forthe self-employed that better reflects ability to pay, and makethe system more progressive by increasing the number of feebrackets and substantially raising fees at the higher (andpresumably more able to pay) brackets. Impose a general increasein tax rates for firms and fees for professionals aiming toachieve, on average, greater parity with the ICM tax rate, andthus, a better distribution of the fiscal burden between goods andservices.