world bank documentdocuments.worldbank.org/curated/en/589591468760240369/pdf/multi…fourth power...

TRANSCRIPT

Document of

The World Bank

Report No: 22318-UG

PROJECT APPRAISAL DOCUMENT

ONA

PROPOSED INTERNATIONAL DEVELOPMENT ASSOCIATION CREDIT

IN THE AMOUNT OF SDR 48MILLION (US$62MILLION EQUIVALENT)

TO THE REPUBLIC OF UGANDA

FOR THE UGANDA

FOURTH POWER PROJECT

June 8, 2001

Africa Energy TeamAfrica Regional Office

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUVALENTS

(Exchange Rate Effective Aue B 2001)

Currency Unit - Ugah Shalinp (Usth)Ush 1750 - US$S

USSI - I7S0 Ush

FISCAL YEARJuly I - to mne 30

ABBREVIATIONS AND ACRONYMS

AfDB African Development BankBOOT Build4)wn-Opsrate-TransferCAS Country Assistance StrategyDFID Department for Intematonal Develphmt (UK)DPP Derailed Procuremnee PlanDRIC Divestiture and RefoTrm Irmplementation CommittieEA Environmentat AnalysisEdF Electricite de FranceEIRR Economic Internal Rate of ReturuEMP Environtnental Management PlanERA Electricity Regulatory AuthorityFIRRI Fisheries Resource Reearclh InstituteFM¢I Financial Manalgement InitiativeGDP Gross Domestic ProductGENCO Uganda Generation Company Lrd.GOU Gosrernmcnt of UgandaGPN General Procurement NoticeHIPC Heavily Indebted Poor CountryIDA International Development AssociationIFC International Finance CorporationIPP independent Power ProducersMEMOD Mlinistry of Energy and Minerat DevelopmentIFPED Mlinistry of Finartca and Econonic Planning

NDF Nordic Developmnent FundNEMIA National Environment Management AgencyNORAD Norwegian Agency for Development CorporationOECF Overseas Economic Corporation fundOPP Overall Procurement PlanPAD Project Appraisal DocumentPEAP Poverty Eradication Action PlanPERD Public Enterprise Reform and DivestiturePIP Procurement Implkmcntation PlanPIU Project Implementation UnitPNR Project 'Management Reports

PPF Project Preparation facilityRCC Roller Compacted ConcreteSCADA Suppavisory Control and Data AcquisitionSDR Special Drawing RightsSIDA Swedish International Developmett AgencySIL Specific Investnent LoanSOE Statement of ExpenditureTRANSCO Uganda Electricity Transn-ission Company Lid.UEB Uanda Elecricity BoardUNDB United Nations Devloptnent BausinesUNDP Untited Nations Developmtent ProgramUTL Uganda Telecomtnticationa Ltd.WRD Water Resources Depaament

WEIGHTS AND MEASURES

I kilometer 0.621 milesI square kilometer (krnt2 ? 0.386 square milesI kilovolt (kV) = 1,000 voltsI mepawatt (MW) - 1,000 kilowattsI megavolt ampere (MVA) = 1,000 kilovolt amperesI gigawatt hour (GOh) = I million kilowatt hoursI ton of oil equivalent (to,) 1 t0500000 kilcatories

Vice Prmident: Callisto E. ,adahvoCountry tatager/Director: Iamte W. Adams

Sector MaragerDirector: M. AnrandaCovintdassantv__Task Team LeaderTaskr staner: Paisi Kotioren

UGANDAFOURTH POWER PROJECT

CONTENTS

A. Project Development Objective Page

1. Project development objective 22. Key performance indicators 2

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project 22. Main sector issues and Governnent strategy 43. Sector issues to be addressed by the project and strategic choices 11

C. Project Description Summary

1. Project components 142. Key policy and institutional reforms supported by the project 153. Benefits and target population 164. Institutional and implementation arrangements 16

D. Project Rationale

i. Project alternatives considered and reasons for rejection 182. Major related projects financed by the Bank and other development agencies 223. Lessons learned and reflected in the project design 234. Indications of borrower commitment and ownership 245. Value added of Bank support in this project 25

E. Summary Project Analysis

1. Economic 252. Financial 293. Technical 334. Institutional 335. Environmental 376. Social 397. Safeguard Policies 40

F. Sustainability and Risks

1. Sustainability 412. Critical risks 413. Possible controversial aspects 43

G. Main Conditions

1. Effectiveness Condition 432. Other 44

H. Readiness for Implementation 46

I. Compliance with Bank Policies 46

Annexes

Annex 1: Project Design Summary 47Annex 2: Detailed Project Description 5 1Annex 3: Estimated Project Costs 55Annex 4: Cost Benefit Analysis Summary, or Cost-Effectiveness Analysis Summary 56Annex 5: Financial Summary for Revenue-Earning Project Entities, or Financial Summary 66Annex 6: Procurement and Disbursement Arrangements 84Annex 7: Project Processing Schedule 93Annex 8: Documents in the Project File 94Annex 9: Statement of Loans and Credits 96Annex 10: Country at a Glance 98Annex 1 1: Letter of Power Sector Policy 100

MAP(S)Uganda Fourth Power Project - IBRD 31399

UGANDA

FOURTH POWER PROJECT

Project Appraisal Document

Africa Regional OfficeAFTEG

Date: June 8, 2001 Team Leader: Paivi KoljonenCountry Manager/Director: James W. Adams Sector Manager/Director: M. Ananda CovindassamyProject ID: P002984 Sector(s): GG - Oil & Gas Adjustment, PP - Electric

Power & Other Energy Adjustment, VY - OtherEnvironment

Lending Instrument: Specific Investment Loan (SIL) Theme(s): EnergyPoverty Targeted Intervention: N

Program Financing Data[ ] Loan [X] Credit [ ] Grant [ ] Guarantee [ ] Other:

For LoanslCredits/Others:Amount (US$m): 62.00

Proposed Terms (IDA): Standard CreditGrace period (years): 10Financing Plan (US$m): Source Local Foreign TotalBORROWER 3.34 0.00 3.34IDA 2.86 59.14 62.00BORROWING AGENCY 1.14 4.86 6.00NORDIC DEVELOPMENT FUND 0.70 10.60 11.30NORWEGIAN AGENCY FOR DEV. COOP. (NORAD) 1.30 5.40 6.70

Total: 9.34 80.00 89.34

Borrower: THE REPUBLIC OF UGANDAResponsible agency: GENCO AND THE MINISTRY OF ENERGY AND MINERAL DEVELOPMENTThe Uganda Electricity Generation Company Ltd. (GENCO)Address: P.O. Box 1101 Jinja, Kampala, UgandaContact Person: Mr. John Mugyenzi, Acting Managing DirectorTel: 256 43 121416 Fax: 256 43 130154 Email: [email protected]

Other Agency(ies):Ministry of Energy and Mineral Development (MEMD)Address: Amber House, Kampala Road, P.O. Box 7270, Kampala, UgandaContact Person: Mr. Fred Kabagambe-Kaliisa, Permanent SecretaryTel: 256 41 234733 Fax: 25641 234732 Email: psmemd@[email protected] disbursements (Bank FY/US$m):

FY 2001 2002 2003 2004 2005 2006Annual 0.00 14.84 20.28 22.76 4.12

Cumulative 0.00 14.84 35.12 57.88 62.00

Project implementation period: 10/31/2001-06/30/2004Expected effectiveness date: 10/31/2001 Expected closing date: 12/31/2004

-OPD Re- Ma,d~ .

A. Project Development Objective

1. Project development objective: (see Annex l)

The objectives of the project are to: (a) improve power supply to meet demand by supporting criticallyneeded investments in the sub-sector; and (b) strengthen Borrower capacity to manage reform,privatization, and development in the power and the petroleum sub-sectors. The project would bridge theelectricity supply deficit during the period 2003-2005. After that time, the Government plans for theprivate sector to take over financing of system expansion. The project complements three other Bankoperations now in progress. These operations are all supporting the Government's reform and privatizationprogram for the power sub-sector.

2. Key performance indicators: (see Annex 1)

Output Indicators

* An increase of between 80 and 120 MW in the capacity of the Kiira hydro power plant by early2004;

* Rehabilitation of critical aspects of power system transmission and generation by early 2004;T raining of a rninimum of 15 staff at MEMD and that of the recently established power sectorregulator, Electricity Regulatory Authority (ERA) by end-2003;

* Establishment of petroleum sector monitoring guidelines by mid-2003;* Procurement of equipment to test the quality of petroleum supply, by end-2002; ando Establishment of the operating regime for Lake Victoria by end 2003.

Outcome Indicators

R Reduction of load shedding by early 2004;I Increase in the number of new residential connections to 15,000 annually by end-2004;R Reduction of system losses from 30 percent in 2000 to 24 percent by end-2004;

* Reduction in undelivered energy due to outages in the transmission system by 30 percent at theend-2003;

* Implementation of transparent legal, regulatory, and monitoring arrangements for the power andpetroleum sub-sectors by end-2002; and

* Improvement in the Government's fiscal sustainability.

B. Strategic Context1. Sector-related Country Assistance Strategy (CAS) goal supported by the project: (see Annex I)Document number: IDAIR2000-187 [IFC/R2000-202] Date of latest CAS discussion: 11/30/00

Economic and Sector Background

Uganda's economic performance during the past decade has been impressive. The average real rate of GDPgrowth has been about 6.7 percent per annum since 1990/91. During the period 1992-2000, this growthrate brought about an annual 3.6 percent increase in real GDP per capita and over a 20 percent decline inpoverty. Also, on an average annual basis, consumer price inflation fell from 38 percent in 1990/91 to -0.2percent in 1998/99. Since President Museveni came to power in 1986, the reform program has focused onestablishing fiscal discipline and opening up the economy by promoting greater reliance on market forces.This program has been successful both in establishing fiscal discipline and in restructuring public

-2 -

expenditure. The Government also has made progress in trade liberalization, privatization, civil service,and financial sector reforms. At the same time, there is an impressive ongoing decentralization effort,which should improve public service delivery by, among other things, promoting better matching of publicservices with local needs. Furthermore, the country's high stock of debt, a significant constraint toeconomic development in the past, has become a smaller obstacle due to Uganda's participation in theinitiative for Heavily Indebted Poor Country (HIPC) initiative.

Despite notable past economic achievements, the Government is concerned that the lack of adequate energysupply in recent years will be a serious obstacle to equitable, sustainable growth of the economy. Themodem segment of Uganda's energy sector - electricity and petroleum - is small. Despite Uganda's vasthydropower resources, concentrated on the White Nile River, only 5 percent of the population has access toelectricity. In fact, a mere 12 percent of the domestic population concentrated in the Kampala metropolitanarea, and in the nearby towns of Entebbe and Jinja -- consumes about 72 percent of total electricity that thepublic electricity system produces.

Recent surveys indicate that private sector managers perceive the quality and adequacy of power supply tobe the most serious constraints to private investment. A shortage of electricity has arisen because theexpansion of Uganda's generating capacity has not kept pace with its rapid economic growth in recentyears. The commissioning of the Kiira hydro power station in August 2000 increased installed capacity to260 MW and has helped to alleviate supply constraints. However, the power utility still has to curtailpower supply during the daily peak periods. With continued strong economic growth and concurrent highelectricity demand growth -- projected at about 8 percent per year -- Uganda needs to better utilize itsdomestic energy resources, mainly hydropower.

Regarding petroleum fuels, the Government liberalized both the importation and pricing in 1994. However,the regulatory framework governing the sector is still inadequate and the capacity to monitor the sector isweak. Because Uganda is land-locked, the cost of delivering petroleum products to markets is significantlyhigher than in many other sub-Saharan African countries. This higher cost mainly results from the hightransit cost of importing products through Kenya and Tanzania. The cost of oil imports was about USS122 million in 1999, amounting to the equivalent of 27 percent of the country's export revenue. As theeconomy continues to grow and modernize, petroleum demand is likely to rise rapidly, from the currentlevel of some 500 million liters per year, absorbing even more of the country's export earnings. Therefore,the provision of incentives for greater efficiency in petroleum supply is critical to improve the country'sbalance of payments as well as the energy balance.

Development Goal Supported by the Project

In November 2000, the Bank presented a new Country Assistance Strategy (CAS) for Uganda to theBoard. This strategy emerged from consultations with the Government, private sector, civil society, andother donors. It seeks to build on the 1997-2000 CAS by continuing to focus on poverty reduction throughsustained growth. The overriding objective is to support Uganda's economic transfonnation and povertyreduction strategy in line with the Government's Poverty Eradication Action Plan (a progress report,IDA/SEC M2001-0219, was discussed by the Board on April 17, 2001). An important component of thisplan is the creation of an enabling environment for economic growth and structural transfornation.Consequently, the Government has identified improving access to and quality of power. transport, andtelecommunications as priorities for the country's development.

The proposed project is included in the CAS and it is an integral part of the CAS emphasis oninfrastructure improvement. More specifically, for the power sector, the CAS plans to improve

- 3 -

infrastructure delivery through the least-cost development of the power system, sector reform, andprivatization. The expansion and rehabilitation of the power system is required to encourage privateindustry investment in Uganda by alleviating concern about the lack of adequate power. In parallel, powersector reform and privatization is necessary for commercial operation of the sector and to reduce theburden of the sector on public finances. The proposed project will continue supporting the sector reformprocess that the Government initiated under the Third Power Project, including the unbundling andprivatization of the Uganda Electricity Board (UEB). The Government is now in the process of privatizingUEB by granting private operators concessions for its distribution and generation businesses.

In addition to the proposed project, there are three energy-related projects that help promote the CAS in thepower sector: the Bujagali Private Hydropower Project; the Energy for Rural Transfornation Project; andthe Privatization and Utility Sector Reform Project.

1. The proposed Bujagali Hydropower Project includes the construction of: (a) a 200/250 MWrun-of-the-river power plant on a Build-Own-Operate-Transfer basis, at Bujagali Falls locatedabout 8 kilometers downstream of the Nalubaale and Kiira Hydropower Plants; and (b) about 100km of 220 kV and 132 kV transmission lines and associated substations. The project sponsor isAES Corporation (AES), Arlington, VA, and AES Sirocco, Limited, a wholly owned subsidiary ofAES. The privately owned and operated project company (Nile Independent Power) will sellelectricity to UEB (or its successors) under a 30-year Power Purchase Agreement. According tocurrent plans, this US$530 million project should be completed in 2005/2006. In addition toprivate equity, the International Finance Corporation (IFC) would partly fund the project, with thesupport of an International Development Association (IDA) Partial Risk Guarantee.

2. The Energy for Rural Transformation Project, has two objectives. The first is to improve the ruralquality of life and facilitate significant rural non-farm income by accelerating rural electrificationfrom the present 1 percent to about 10 percent in ten years. The second is to develop Uganda'sindigenous, renewable energy resources on a cost-effective basis. The financing of the total projectcost of US$375 million would come from the following sources: IDA (US$75 million APL, witha first phase of US$30 million) GEF (US$30 million total), the private sector, the Government andbilateral donors ($195 million).

3. The objective of the ongoing Privatization and Utility Sector Reform Project is to improve thequality, coverage, and economic efficiency of commercial and utility services through privatization,private participation in infrastructure, and an improved regulatory framework. The project willachieve this objective in part by promoting a higher level of private investment along with betterquality of telecommunications, water, electricity and transport services and expanded access of thepopulation to them. The financing for the US$95 million project is coming from IDA (US$48million) and the Government of Uganda (US$47 million).

2. Main sector issues and Government strategy:

Uganda faces several challenges in the power and petroleum sectors:

Power Sector

Background: The Government established the Uganda Electricity Board (UEB) in 1948 as aquasi-independent, vertically-integrated monopoly to generate, transmit, distribute and supply electricitywithin Uganda and to other countries in the region. The enactment of the Electricity Act of 1999 removed

- 4 -

the legal monopoly the UEB had in the power sector. However, the UEB continued to operate generation,transmission and distribution facilities until March 31, 2001. After that date the Government divided theUEB into three independent corporate entities - one each for generation, transmission, and distribution.These government-owned entities now operate the country's power system. This system includes the 180MW Nalubaale power station (formerly Owen Falls), the Kiira power station with 80 MW installedcapacity, and about 10 MW in diesel and mini-hydro capacity. It also consists of: an interconnected 132kV and 66 kV transmission network; a 33 kV sub-transmission network; a distribution network at voltages11 kV and below; and isolated diesel generators and distribution systems. Total generation was about1,520 GWh in 2000 and the system peak was 242 MW in August 2000. Consumer demand at peak timesexceeds available grid connected generating capacity by about 20 MW currently. Supplementary power tofill the deficit comes from privately-owned generators that are mainly diesel-driven.

Issue # 1: Poor Performance. The power sector has for a long time suffered from a number offundamental problems that have led the Government to develop plans for its reform. These problemsinclude:

* Poor supply reliability characterized by extensive load shedding and reductions in voltage

* Inadequate investment in all parts of the sector and an inability to finance future requiredinvestments, particularly in distribution,

* Poor commercial performance characterized by collections being received from less than 50percent of the electricity sent out from the power stations

H High technical and non-technical losses, which are about 35 percent of electricity generated.

3 High accounts receivable, which are currently equivalent to almost seven months of billings.

* Low productivity despite the retrenchment, in 1998, of about 30 percent of UEB's employees.Currently, UEB's successor companies combined have about 1,800 employees serving fewer than170,000 customers.

These inefficiencies have left UEB and its successor companies in a weak position. Now they are, bynormal standards, close to insolvency. UEB has not been able to generate an adequate cash flow from itsaverage retail tariff of about US 5.6 cents/kWh. To reduce non-technical (i.e. commercial) losses, UEBhas established campaigns to reduce electricity theft and engaged private debt collectors to improvecollection performance. However, these losses and non-payment of utility bills remain serious problemsand ongoing programs in these areas need reinforcement. Various factors such as an inadequate billingsystem, metering inaccuracies, and the existence of un-metered supply have exacerbated the problem. Thepublic sector, which consumes roughly 10 percent of the electricity, is a major defaulter on its paymentobligations to the power utility. In order to reduce the technical losses to economic levels, heavyinvestments in the network, especially for distribution, will be necessary over the coming years.

The major cause of the poor state of the power sector has been UEB's lack of management and financialautonomy from the Government. This situation has hindered the development of a commercial businessorientation, accountability and modem utility management practices. Government influence intariff-setting, investment decisions, personnel deployment, and other areas have made it difficult to developthe performance incentives necessary to improve service.

- 5 -

Strategy: Realizing the potential deleterious impact of a weak power sector on economic growth, theGovernment has begun the implementation of a comprehensive reform and privatization program(Govemment's Power Sector Policy statement is attached in Annex 11). The Government approved apower sector restructuring and privatization policy in June 1999. The 1999 Electricity Act and the PublicEnterprise Reform and Divestiture Statute provide the legal basis for this policy and provide for the verticalunbundling of UEB and its conversion from a Statutory Corporation to a public company limited by shares.The Electricity Act also provided for the establishment of an independent power sector regulator. Thisentity has been in place since April 2000. As a prelude to the privatization, in April 1999, the Governmentappointed a new management team with private sector experience to manage UEB. The new management'scommercial approach has made improvements in UEB's performance (see Section E.2 for details). Thepreparatory work for restructuring and privatizing UEB began in April 2000 with the hiring ofPrivatization Advisers.

In March 2001, the Governnent divided UEB into three independent corporate entities, one each forgeneration, transmission, and distribution. The division of UEB into these entities also affected theallocation of the former UEB's assets. The Government has re-allocated these assets according to therequirements of the 1999 Electricity Act. As a result, the Distribution Company now owns all powersupply assets operating at 33 kV and below, along with assets associated with the retailing of electricity.The Transmission Company owns all assets operating above 33 kV. The Uganda Electricity GenerationCompany owns the Nalubaale and Kiira hydro power stations. During a transitional period, the UEBStatutory Corporation will retain some liabilities that the Government could not delegate to the successorcompanies without the prior permission of counter-parts to the contract (for example some multilateral andbilateral long-term debt). Upon settlement of these liabilities, or their delegation to one of the successorcompanies with permission of the counter parts, UEB will cease to exist, according to the 1999 ElectricityAct. The diagram below illustrates the current sector structure, which will be in place until the generationand distribution businesses are concessioned out to the private sector.

Current Power Sector Structure

Shareholders:Minister Responsible

for Finance andMinister Responsible

for Privatization

|Uganda Electricity | ganda Electricity ||Uganda Electricity lDistribution company Transmission Generation Company

Ltd. Company Ltd . L td.

In addition to the unbundling of UEB into separate generation, transmission, and distribution companies,the restructuring policy requires the privatization of the generation and distribution businesses through theestablishment of long-tern concessions. Under concession arrangements the existing assets will remain inpublic ownership but the private companies will have the right to operate and expand them.

Upon establishment of the concessions, the power sector will have the following structure:

One distribution company that a private company will operate as a concession;

- 6 -

* One generation company that a private company will operate as a consession, including theexisting Nalubaale and Kiira hydro stations;

* Two separate Government-owned holding companies for the existing generation anddistribution assets; and

* A separate Government-owned transmission company acting as a single buyer that will holdexisting power purchase agreements (i.e. Bujagali and the future generation concessioncompany). The Government's medium term objective is, however, for the private sector tooperate the transmission company as a concession and also to allow for direct contractingbetween the generation and distribution companies.

In addition, the Electricity Act allows Independent Power Producers (e.g. Bujagali) and rural energy supplycompanies to apply for operating licences.

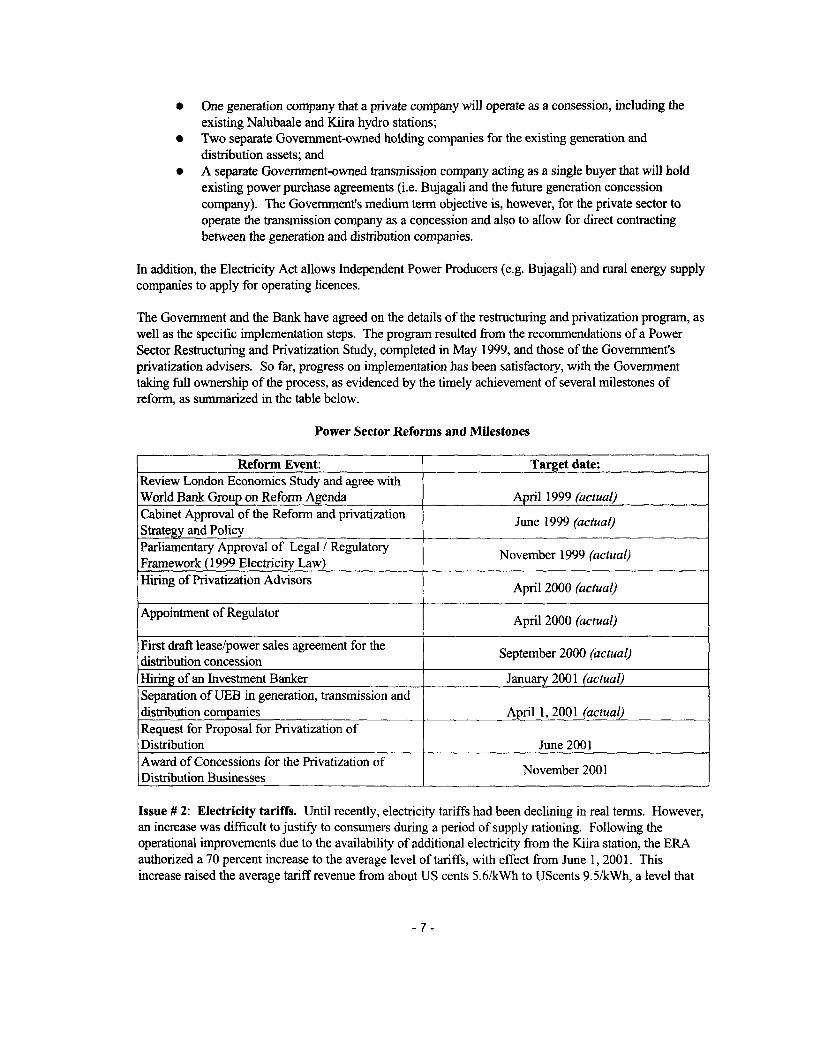

The Government and the Bank have agreed on the details of the restructuring and privatization program, aswell as the specific implementation steps. The program resulted from the recommendations of a PowerSector Restructuring and Privatization Study, completed in May 1999, and those of the Government'sprivatization advisers. So far, progress on implementation has been satisfactory, with the Governmenttaking full ownership of the process, as evidenced by the timely achievement of several milestones ofreform, as summarized in the table below.

Power Sector Reforms and Milestones

Reform Event: Target date:Review London Economics Study and agree withWorld Bank Group on Reform Agenda April 1999 (actual)Cabinet Approval of the Reform and privatization June 1999 (actual)Strategy and PolicyParliamentary Approval of Legal / Regulatory November 1999 (actual)Framework (1999 Electricity Law)Hiring of Privatization Advisors April 2000 (actual)

Appointment of Regulator April 2000 (actual)

First draft lease/power sales agreement for the September 2000 (actual)distribution concessionHiring of an Investment Banker January 2001 (actual)Separation of UEB in generation, transmission anddistribution companies April 1, 2001 (actual)Request for Proposal for Privatization ofDistribution June 2001Award of Concessions for the Privatization of November 2001Distribution Businesses

Issue # 2: Electricity tariffs. Until recently, electricity tariffs had been declining in real terms. However,an increase was difficult to justify to consumers during a period of supply rationing. Following theoperational improvements due to the availability of additional electricity from the Kiira station, the ERAauthorized a 70 percent increase to the average level of tariffs, with effect from June 1, 2001. Thisincrease raised the average tariff revenue from about US cents 5.6/kWh to UScents 9.5/kWh, a level that

- 7 -

would be adequate to ensure the financial viability of the project. This increase was necessary to improvethe power sector's financial position and to ensure that sufficient revenue would be generated by the sectorentities to finance investment in rehabilitation and expansion of the system. At the same time, the ERAalso approved improvements to the structure of the tariffs, through the removal of cross subsidies betweenthe different consumer groups. Most notably, it removed the subsidy from industrial to residentialconsumers. This new tariff structure should provide better incentives for suppliers to extend electricityservice to rural areas. The ERA also approved an automatic tariff adjustment mechanism to prevent theerosion of the tariff due to fluctuations in foreign exchange rates and domestic inflation. Under thismechanism, the Distribution Company can adjust the retail tariffs quarterly on the basis of an ERAendorsed formula.

Issue # 3: Inadequate and Unreliable Electricity Supply. As noted earlier, inadequate, unreliableelectricity supply is stifling economic growth. Although the supply situation has improved since thecommissioning of 80 MW at Kiira in August 2000, the utility is still forced to curtail about 20 MW during2-3 peak hours daily. There is no adequate reserve margin, which in turn prevents the utility fromadequately maintaining its generating assets. Furthermore, a number of the generation and transmissionsubstations are old and in poor condition due to lack of adequate maintenance. System interruptionstherefore occur frequently.

Because of economic expansion, Uganda's electricity demand is expected to increase rapidly. In February2001, Electricite de France (EdF) updated Uganda's electricity demand forecast. The base case forecastestimates energy demand to grow at an annual average rate of 10 percent during the period 2001 to 2010.After taking account of decreasing losses, the forecast indicates that the system's energy requirement willincrease by about 8 percent per year. This rate appears reasonable given expected annual GDP growth rateof around 7 percent, continued strong industrial production, and the current peak load shedding. Anotherindication of the market's growth potential is the recent survey of private industries. This survey indicatedthat industries have installed up to 100 MW of back-up capacity in response to the poor quality of UEB'ssupply and the continued load shedding. With improved service from the grid system provider, theseindustries are likely to rely less and less on their own generators and instead, gradually increase puchasesfrom the grid system. The high and low annual demand growth scenarios are 9 percent and 11 percentrespectively (assumptions are in Annex 4). A comparison of the forecast with the available generationindicates that the existing system will not be able to balance demand and supply.

Strategy: The Government's long-term strategy is to develop Uganda's large hydro power resourcesthrough Independent Power Producers (IPPs). Based on current plans, the first IPP plant (Bujagali) shouldbe operational around the year 2005/2006. To meet the growing demand in the meantime, a newhydroelectric generation plant -- the Kiira power station (formerly the Owen Falls Extension) -- is underconstruction. It is constructed adjacent to, but not connected to the existing Nalubaale plant. The plant isdesigned for 5 x 40 MW generating units (please refer to illustration of the plant at the end of Annex 2).The Third Power project financed the construction of a new dam, a power house, a diversion canal, aspillway, civil works for generating units 11 through 15, and the installation of 80 MW (Units 11 & 12) ofgenerating capacity. The Swedish International Development Agency (SIDA) and Norwegian Agency forDevelopment Corporation (NORAD) are financing the installation of Unit 13. The addition of this unit bythe end of 2002, will increase the installed system capacity to 300 MW.

The Government plans to install the remaining two units to complete the Kiira plant. Since the civil workstructures are already in place, these two units can begin operation with a short lead time. The units willprovide 80 MW of additional capacity. The additional power will reduce the need for electricity rationingbefore the first IPP comes on-line. However, even this extra power is only a partial solution; the forecast

- 8 -

indicates that demand will outstrip supply until Bujagali comes on strearm. To fuirther reduce the supplydeficit, the Energy for Rural Transformation Project will explore the possibility of generation from smallrenewable energy sources, such as sugar mills, that are close or already connected to the main grid. Energyefficiency measures will supplement this increase in generation capacity. These measures include ongoingprograms for reducing non-technical losses and improving billing and collections. One of the ongoingprograms is the distribution strengthening and technical loss reduction project, with fimancing from theAfrican Development Bank (AfDB). To reduce interruptions in the transmission system, the Governmentplans to rehabilitate a number of critical transmission substations, the old substations at the Nalubaalehydropower plant, and extend the Supervisory Control and Data Acquisition (SCADA) system to cover thewhole transmission system.

The table below shows the energy and capacity balance for Uganda over the period 2000-2007.

Energy and capacity balance for Uganda over the period 2000-2007

Year: 2000 2001 2002 2003 2004 2005 2006 2007

Energy Demand (GWh)Domestic 909 1005 1110 1232 1370 1520 1672 1836

Kenya 210 175 99 99 99 99 99 99

Tanzania 21 21 21 21 21 21 21 21

Rwanda 1 1 1 1 1 1 1 1

Total Demand 1141 1202 1231 1353 1491 1641 1793 1957Required Generation 1554 1627 1665 1801 1953 2117 2277 2369Demand at Peak (MW)

Domestic 242 262 283 303 324 344 377 410

Kenya 10 10 10 10 10 10 10 10

Tanzania 5 5 5 5 5 5 5 5Rwanda 1 1 1 1 1 1 1 1Total 258 278 299 319 340 360 393 426

Installed Capacity (MW)

Hydro Total 260 260 300 380 380 380 580 580

Existing Cogen 7 7 7 7 7 7 7 7Kakira (available to the grid) 0 0 0 12 12 15 19 19

Total from the Grid 267 267 307 399 399 402 606 606Energy Produced (GWh)

Hydro Total 1527 1527 1527 1654 1539 1704 2846 3108Existing cogen 15 17 17 17 17 17 17 17

Kakira 0 0 0 80 80 105 140 140Works Units -4 -4 -5 -6 -6 -7 -9 -9Total from the Grid 1538 1539 1539 1744 1629 1819 2994 3256Losses (%) 31 29 28 26 25 24 22 18

Reserve Margin (less LU)(%) (12) (18) (11) 13 6 1 44 33Surplus/(Deficit) (GWh) (16) (88) (126) (57) (324) (298) 717 886

Notes:1. Energy and peak demand according to EdF's "base" forecast.2. Hydro production is based on "average" water flow.3. The installation of Units 14 and 15 by end-2003.4. The availability of power from Bujagali by 2006.5. Export sales at their current levels.

-9-

6. LU=Largest generating unit.

The table above shows that the system will continue to operate on a negative reserve margin until the Kiirapower plant has been completed at the end of 2003. After that time, the system will have adequate capacityreserves but it will not be able to meet energy demand fully until the commissioning of Bujagali. However,as discussed later in Section D, the Government has indicated that, at this stage, it is not willing to installlarge scale oil thermal plant, because of the high cost of fuel and problems transporting large amounts offuel through Kenya and Tanzania. Furthermore, investment in such a plant would, in effect, duplicateinvestments in back-up diesel generators, which industries already have made.

Issue # 4: Low Access to Electricity-Particularly in Rural Areas. Uganda currently has one of thelowest levels of per capita electricity consumption (44 kWh/year) in the world. This ievel reflects the factthat only an estimated 4-5 percent of population has access to public electricity supply. Currently there areonly about 170,000 customers connected to electricity lines. Most of these customers live in urban areas.In the recent past, UEB connected fewer than 10,000 customers per year. Even under the best ofcircumstances, restructuring of the power sector alone is unlikely to improve the rural access pictureperceptibly. For example, an optimistic assumption for growth in the number of rural householdsconnected to the main grid during the period 2001 to 2010 is an average annual rate of 15 percent. At thisrate, the total number of rural households connected to the main grid would increase from about 30,000 in2001 to about 125,000 in 2010. Under this assumption, rural access would increase from 1 percent to 3percent.

Strategy: The Government, in consultation with the Bank, has adopted a commercially-oriented approach-- with the Government playing the role of a market enabler to increase rural electrification. The mainelements of this strategy are: (i) level playing field for private sector participants; (ii) a regulatoryframework that supports private sector development; (iii) cost recovery and cost-based tariffs; and (iv) atransparent subsidy transfer and financing mechanism. In line with this approach, the Government hasinitiated discussions with the Bank for financial support for rural electrification. The Banks analyses sofar have concluded that Uganda offers good prospects for a commercially oriented rural electrificationprogram with the private sector taking the leading role. However, the first step is to establish a supportiveinstitutional and regulatory framework. The Bank and the Government plan to support such a developmentunder the Energy for Rural Transformation Project. The Bank appraised the proposed project in May2001, at which time the Government began the implementation of its recently completed RuralElectrification Strategy.

Issue # 5: Hydrology. Uganda's existing hydro power plants are located along the Nile river, which flowsout of lake Victoria. The long-term level of Lake Victoria naturally varies over a range of about twometers. Despite Uganda's ability to regulate outflows from the lake using the Nalubaale Dam, thisregulation capability is generally not used because of a bilateral agreement between Uganda and one of theriparian countries. This agreement regulates the quantity of flow discharged from the lake (through thepowerhouse or dam spillway) according to an "agreed curve". The purpose of this curve, which relates thewater outflow to lake levels, is to reproduce the natural outflow which would have occurred prior to theconstruction of the Nalubaale power plant and spillway in 1954. While Uganda has some flexibility toregulate flows on a weekly basis to match power demands, it cannot utilize Nalubaale's very largecapability to regulate flows on a seasonal or yearly basis to optimize the use of Lake Victoria outflows forpower generation.

There have been proposals for regulating the outflow from Lake Victoria but as yet no detailed studies havebeen carried out. The objective of such regulation would be to enhance hydropower production at

- 10-

Nalubaale, Kiira and any subsequent plants downstream. There may also be potential benefits todownstream riparian countries through increased dry year flows and flood attenuation. From Uganda'sviewpoint the main benefit of such a regulation policy is the ability to firm up energy production of theNalubaale, Kiira, and Bujagali power plants. This would allow delaying the construction of subsequentnew plants until system demand exceeded "average energy" rather than "firm energy". It could be possibleto further increase these benefits by short term variations in operating policy. For example, there could bean increase in the outflow for two or three years prior to installing new power plants (drawing fromstorage), thus allowing the postponement of new investment in generation capacity. Then, during theperiod immediately after installation of the new plants, there could be a reduction in outflows to allowrecovery of lake level (replenishing storage). Outflows would then be gradually increased to average levelsin line with system demand increases. Under the proposed project, the Government has requested financingfor a study that would evaluate the impact of this regulation policy on the power investment program andon the downstream riparian countries.

Petroleum Sector

Issue # 6: Lack of Monitoring of Petroleum Operations. In 1994, the Government liberalized thedownstream petroleum sector but the legal and regulatory framework governing the sector is stillinadequate and the capacity to monitor the sector is weak. Some six years after the liberalization, Ugandastill has no law or mechanism to enforce anti-competitive behavior. The only law in effect at the momentwhich relates to the downstream sub-sector is the Petroleum Act of 1957. It appears that only the oilcompanies have benefited from the liberalized market since 1994. It has not resulted in much increasedcompetition, lower consumer prices, or improved quality at the pump. In 1999, the Government preparedan analysis that indicated an increase in the oil companies' margins from about US$0.24/literpre-liberalization to in excess of US$0.30/liter after liberalization. Consumer prices per liter have rangedbetween $0.7 and $0.9 for petrol; $0.5 and $0.7 for kesosene; and $0.6 and $0.8 for diesel during theperiod January 2000 to date. Regarding the quality of the products, there is a problem of product alterationespecially for kerosene and diesel. A procedure called bio-coding, which the Government recentlyintroduced to control petroleum smuggling, has established that products imported through the properchannels are sometimes mixed with smuggled ones. A major deficiency in the management of the sector isthe Government's lack of capacity to adequately control the quality of petroleum products entering thecountry.

Strategy: The Government is committed to improving the operation of the petroleum sector by enhancingcompetition through a number of measures: (i) actively monitoring and disseminating market information tothe public; (ii) establishing a legal and regulatory framework; and (iii) attracting new entrants to themarket. To this end, Government has initiated the drafting of a new Petroleum Supply Law with theassistance of GTZ. It has requested IDA assistance in implementing the law including the establishment ofa body to monitor petroleum operations. This assistance will include technical assistance for: Preparingand setting up the new regulatory framework and monitoring; building institutional capacity; and acquiringequipment.

3. Sector issues to be addressed by the project and strategic choices:

The project will address the following issues: promoting further power sector reform and development;increasing and improving supply of electricity, including the optimization of Lake Victoria's outflows; andpromoting further petroleum sector reform and development.

Promoting Further Power Sector Reform and Development. The Government has demonstrated

- 11 -

ownership of sector reform and its progress in implementing agreed reform measures has been steady. Theproposed project will facilitate the Government's privatization program by financing critically neededgeneration capacity and transmission rehabilitation. This financing will ensure availability of generation tosupport the private sector distribution company's efforts to increase coverage. Also, the project willfinance training and advisory services for increasing the Government's capacity to deal with the complexissues related to power sector reform and utility privatization. The Privatization and Utility Reform projectis providing complementary assistance. Furthermore, to ensure sustainability of the proposed project, forwhich a reformed power sector is essential, several key decisions on the project will depend on theGovernment maintaining its comnmitment.

The project would also, together with the NORAD-financed Regulatory Support Project, support thesetting-up of the legal and regulatory framework -- in particular, technical assistance and training to therecently established Electricity Regulatory Authority. The Bank and the Borrower will identify specificactivities to be financed during the course of implementation.

Increasing and Improving Supply of Electricity to Meet Demand: The project will install Units 14 and15 at the existing Kiira power station. These units will provide up to 80 MW in additional installedcapacity by the end of 2003. The project also will facilitate the speedy commissioning of Unit 13 byfinancing the civil works that SIDA and NORAD could not finance due to unavailability of funds. Thecredit for the proposed project would allocate about US$ 2.5 million (3.2% of the total) to the retroactivefinancing of the initial portion of the required civil works. Such advanced procurement is necessary tocomplete installation of Unit 13 on time to meet growing demand.

Finally, the proposed project will finance the rehabilitation of critically needed transmission systemimprovements to reduce losses and blackouts. Analysis indicates that the existing transmission networkcapacity combined with current investments in new capacity should provide the main load centers withsufficient power. However, the appraisal mission established that although some rehabilitation of theelectromechanical equipment at Nalubaale power station was carried out under the Second Power Project,some of the original (1954) equipment remains un-refurbished. Hence, the proposed project will financethe rehabilitation of the necessary critical circuit breakers and spare units for the transformers. It also willrehabilitate and extend several other grid substations for effective distribution of the increased supply.Finally it will upgrade and extend the SCADA system to reduce the time required to identify a fault andrestore supply after fault rectification.

Optimizing Lake Victoria Outflows: The project will finance the required studies to provide theGovernment with information on the merits of the short-and long-term regulation of Lake Victoria outflowsto Uganda and the downstream riparian countries. The study would contribute to a strategy to manage thehydrology in an environmentally satisfactory way for Uganda and all riparian countries.

Furthering Petroleum Sector Reform and Development: The project will provide technical assistance tothe Government for the overall reform and development of the subsector, including the establishment andimplementation of a monitoring and regulatory function. The project will also finance the procurement ofpetroleum quality monitoring equipment. This assistance will complement that of the GTZ, which isfinancing the drafting of a new Petroleum Supply Bill. The Government will submit the Bill to Parliamentprior to the implementation of this component.

Strategic Choices

Public vs. Private Sector Project: Given the cost of power shortages to the economy, the proposed

- 12 -

project will finance a public sector investment because it is the fastest way to increase generation capacity.The project team considered the installation of the two generating units by the private sector. However, theteam rejected this alternative because it would require more lead time than a public sector project. Since itis expected that the operation of the Kiira power station would be offered to a private sector concessionairethrough tendering by the end of 2001, procurement of the units by the private concessionaire could onlystart during 2002, meaning at least a one year delay in installation. This would lead to intensified powerrationing. The Government therefore decided not to delay the installation until the generationconcessionaire has been selected.

Sector Reform: The dialogue between the Bank and the Government of Uganda on power sector refornshas been going on for several years. The Government recognizes that it can justify additional investment inthe sector only with major reform of the sector. In view of this, the proposed assistance strategy includesthree elements. First, release of funds by IDA for the installation of the generating units will take placeonly after Government has approved a satisfactory list of pre-qualified firms for the distributionconcession. It should be noted that confidence of generation availability is a crucial aspect in investorreadiness to be involved in a distribution business. Hence, the second element is that the project will assistthe reform program by improving the availability of power in the short to medium term, before privatesector financing becomes available. Third, the proposed project will provide technical assistance for theimplementation of the reform program in coordination with the Privatization and Utility Sector ReformProject, the proposed Bujagali IPP Project, and other donor assistance programs.

Project Size: A third strategic choice in the design of the project is the phasing of the financing forinvestment in new generating units. During project preparation an analysis indicated that under "base case"assumptions -- for the capital cost of the unit; the commissioning date of Bujagali; and the inflows to thelake prior to the planned commissioning dates of the new units -- only one of the two would beeconomically justified at present. The Bank and the Government agreed, however, to include the two unitsin the project but make the disbursement for the second unit conditional on demonstration of its viability ata later stage, likely to be towards the end of 2001. At that time, the Bank and the Government will reviewthree key factors: the capital cost of the additional unit based on bids received; the most probable on-linedate for Bujagali; and the latest lake level (and hence implications for short-term outflow). The appraisalteam's analysis shows that the viability of the second unit is mostly sensitive to when Bujagali comes onstream. However, the short-term outflows from lake Victoria, will also have an impact. In addition, ifUganda were to negotiate a change to the agreement with the riparian countries on flows, making largeroutflows from the lake to the river possible, the energy generation capability of the second unit wouldincrease markedly thereby improving its economics.

- 13 -

C. Project Description Summary

1. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed costbreakdown):

Indicative Bank- % oflomponent 0 Sector Costs % of financing Bank-

l_____________________________ : 0r(US$M) Total (US$M) financingA. POWER SYSTEM EXPANSION PH - Hydro 83.87 93.9 56.82 91.6AND REHABILITATION

Al. Investment:a. Installation of Units 14 and 15 Kiirab. Upgrade of SCADA andTelecormmunications Systemc. Transmission Rehabilitationd. Civil Works for Unit 13e. Hydromechanical for Unit 13

A2. Institutional Supporta. Project Design and Supervisionb. Study on Unit 15

B. ENVIRONMENTAL Natural 0.21 0.2 0.00 0.0MONITORING Resources

Managementa. Environmental Officerb. Environmental Monitoring

C. POWER SECTOR Institutional 2.35 2.6 2.34 3.8DEVELOPMENT AND REFORM Development

C1. Equipment and Training

C2. Consultanciesa. Water Management Studyb. Consultancies and Workshopsc. Studies

C3. ERA Assistance

- 14 -

D. PETROLEUM SECTOR Oil & Gas 0.97 1.1 0.90 1.5DEVELOPMENT AND REFORM Adjustment

D. 1. Quality monitoring equipment,training, and information

D2. Consultancy Services for designand implementation of legal andregulatory system.

E. PROJECT PREPARATION Electric Power & 1.94 2.2 1.94 3.1FACILITY (PPF) Other Energy

Adjustment

Total Project Costs 89.34 100.0 62.00 100.0Interest during construction 0.00 0.0 0.00 0.0

Front-end fee 0.00 0.0 0.00 0.0Total Financing Required 89.34 100.0 62.00 100.0

2. Key policy and institutional reforms supported by the project:

The project will support the ongoing reforms in the power and petroleum sub-sectors in particular, theprivatization through long-term concessions of the power distribution and generation businesses and theimplementation of a modem legal and regulatory framework for the petroleum sub-sector. Most of theassistance will be in the form of capacity-building and training, both in-house and outside Uganda.

In the power sector, the Government has made several legal and institutional changes up-front, including:(i) amendment of the Public Enterprise Reform and Divestiture (PERD) Statute to improve theprivatization process; (ii) enactment of legislation to create a separate electricity regulatory agency; (iii)adoption of procedures for competitive and transparent divestitures; and (iv) adoption of transparentguidelines for the use of divestiture proceeds; (v) filled management positions at UEB with a qualifiedmanagement team to manage the utility on a commercial basis in the interim period before privatization;and (vi) separated UEB into three corporate entities. In addition, GOU has decided to adopt evolvingapproaches towards the regulation of utilities framework. In the short term, it will create sector-specificregulatory agencies to ensure autonomous arrangements for each sector. In the longer-term, theGovernment is looking into a broader concept of multi-sector agencies in an effort to increase the efficiencyof regulation. In the petroleum sector, the Govermment is in the process of modemizing its PetroleumSupply Law and creating effective market monitoring arrangements.

Finally, the project will help build the institutional capacity for project implementation and management bysupporting: (i) the Project Implementation Unit (PIU), which is in charge of the implementation of thegeneration and transmission components of the project; and (ii) the MEMD's project implementation team.The project will also promote Uganda to make better use of regional energy trade opportunities.

- 15-

3. Benefits and target population:

The primary beneficiaries will be electricity consurners in Uganda, who will receive more electricity and abetter quality of service. In particular, private industry will benefit from increased grid supply and reducedload shedding. All taxpayers who subsidize UEB, will benefit from power sector reform and improvedfinancial management of the power industry. In particular:

* Increased power supply with improved reliability will facilitate higher economic growth;* Power sector reform and privatization will improve the sector's performance thereby reducing the

power sector's drain on public expenditures, and thus freeing-up resources for the implementationof the Government's poverty eradication program; and

* Fewer blackouts and brownouts will reduce the need to operate expensive back-up generators.Thus, industry will benefit from reduced cost of electricity. Also, increased power supply willallow for increasing the access to electricity.

4. Institutional and implementation arrangements:

Implementation Agencies by Project Component:

Part A. Power System Expansion and Rehabilitation

A.1. Expansion of the Kiira power plant through: (a) the acquisition and installation of two 40 MWpower generation units (Units 14 and 15), (b) completion of the installation of Unit 13, including theacquisition of related equipment and civil works (IDA financed).

3 The Uganda Electricity Generation Company Ltd.

A.2. Upgrading of the Uganda Electricity Transmission Company's supervisory control and dataacquisition and telecommunications systems through: (a) the acquisition and installation of hardwareand software; (b) installation of remote and terminal units and data collecting equipment; and (c)extension of telecommnunications systems (NDF financed).

3 The Uganda Electricity Transmission Company Ltd.

A.3 (a). Rehabilitation of substations at Nalubaale (NDF financed).

* The Uganda Electricity Generation Company Ltd.

A.3 (b) Rehabilitation of the Nkenda, Nkonge, and Opuyo substations (NORAD financed).

* The Transmission Company Ltd.

A.4. Design and supervision of activities of the Project. (IDA financed)

* The Uganda Electricity Generation Company Ltd.

A.5 Strengthening the management of the Project through the technical advisory services, and (b) thecarrying out of a technical and economic evaluation to deternine the viability of Unit 15 (IDAfinanced).

- 16 -

* The Uganda Electricity Generation Company Ltd.

Part B. Environmental Monitoring

* The Uganda Electricity Generation Company Ltd.

Part C. Power Sector Development and Reform

* MEMD

Part D. Petroleum Sector Development and Reform

* MEMD

Project Management Arrangements

The existing Project Implementation Unit (PIU), located at the UEB Statutory Corporation, will provideimplementation support to the Generation and Transmission companies (for Parts A and B). The unitrecently received strengthening under the ongoing Third Power project. A dedicated individual withinternational experience has been hired as Project Manager to head the Unit. The Unit also includes aproject accountant, and staff with procurement expertise. An environmental officer started work on June 1,2001. The Implementation Unit has proven experience in implementing similar projects as it providessupport to the implementation of all the ongoing power sector projects.

MEMD has assigned the Assistant Commissioner for Energy Efficiency as a full time Project Coordinatorresponsible for the implementation of its components. Other members of MEM'Ys project implementationteam include a deputy project coordinator (the Assistant Commissioner for Petroleum) and an accountant.In issues relating to power sector privatization, MEMD will consult with the Minister of State for Finance(privatization) responsible for privatization. In implementing the Water Management Study, MEMD willco-ordinate with the Ministry of Water, Lands, and Environment. MEMD has experience inimplementing similar projects through participation in previous IDA and donor financed projects.

Accounting, Financial Reporting, and Auditing Arrangements

* An independent auditor, acceptable to the Bank, will audit project accounts, including special accountsand all disbursements under Statements of Expenditure annually. The auditor will apply auditingstandards acceptable to IDA; and

* The implementing agencies will submit the annual audit report to IDA within six months of the end ofeach fiscal year.

Monitoring and Evaluation Arrangements

* The implementing agencies will prepare quarterly project management reports and semi-annualprogress reports on the basis of the agreed project implementation plan;

* The Bank's supervision missions will take place twice a year and there will be a mid-term review of theproject in 2003. The project's co-financiers (NDF and NORAD) have agreed to participate in thesemissions to the extent possible;

* Implementation progress and achievement of objectives will be monitored on the basis of agreed

- 17-

indicators and targets; and* The Government will transmit to IDA a completion report, within six months of credit closing.

D. Project Rationale

1. Project alternatives considered and reasons for rejection:

Previous studies have established that the generation system in Uganda should be based on hydro power.This is a function of two factors. The first is the abundant power potential available for development onthe Victoria Nile. The second is the relatively high cost of alternative thermal generation - a consequenceof Uganda's landlocked location. The development of a generation system in Uganda was studied in detailin 1997 by Kennedy and Donkin, as part of the IDA-financed Third Power project. The study provided along-term approach to defining the evolution of the generation system. It concluded that developing thehydropower resources on the Nile is the least-cost option for Uganda. It consequently outlined a long-termdevelopment plan for the power system and recommended the development of Bujagali in 2003 as the nextpower generation project. The plan included Kiira Units 14 and 15 in all the expansion sequences itanalyzed. The least-cost plan recommended the installation of Unit 14 before Bujagali and Unit 15 after it.

However, substantial power shortages have resulted from a combination of: High load growth; delays incompleting the first phase of the Kiira power plant (3x4OMW Units 11-13); and a delay in the dateBujagali will come on stream. The power shortages will continue until the commissioning of Bujagali nowexpected in 2005/2006. The Government is considering an immediate further extension at Kiira (2x40MWUnits 14 & 15) as a partial stop-gap solution. Since the required civil works (for example, thepowerhouse) already are complete, the two units could be operational before the end of 2003.

The viability of this extension is, however, not clear cut because energy production of the additional units isstrongly influenced by the amount of flow available from the Lake Victoria over the short term. This, inturn, is a function of the uncertain hydrological regime (an analysis of the hydrology by Mr. DennisCreamer, Water Resources Specialist, is available in project files). Moreover, the Government hasemphasized that the installation of new stop-gap generation should not detract from the economic viabilityof Bujagali for which the decision to proceed in principle has been taken. Therefore after commissioning ofBujagali, the operating regime of the generating plants should reflect that power from Bujagali would bedispatched first to meet the domestic load and export commitments; other plants would provide peak andsurplus energy. However, there is a general agreement that additional firm energy arising from the newKiira units could affect the next hydropower addition after Bujagali, by delaying it slightly or reducing itscapacity.

Four alternatives were studied to compare the costs of reducing the energy shortfall before Bujagali:

* A) Installation of no additional generation prior to Bujagali. Instead, shortages are dealt with,as has been the case in the past, by relying on industrial, commercial and high-incomeresidential consumers to continue running their own existing back-up generation for essentialservices. A few new consumers would also install small- to-medium sized diesel plants to meetessential services. This plan would inevitably lead to some loss of economic activity as someloads would not be served either by the grid or by private back-up generators. It should benoted that under this scenario GENCO would not have adequate capacity to serve peak loads,and would also have insufficient hydroelectric energy to meet the system demand. It would,however, have some flexibility to schedule outages to times of day when effect on economicproductivity would be less.

- 18 -

* B) Installation of a 40 MW distillate fired gas turbine power plant to meet the projected loadgrowth prior to Bujagali under most hydrological scenarios, such that no new back-upgeneration by consumers would need to be installed. After Bujagali comes on line, the fullcapacity of this gas turbine would not be needed in the grid system in the short to mediumterm.

* C) Installation of Kiira Unit 14. Considerable back-up energy generation by consumers wouldstill be required under lower flow hydrological scenarios. Also, some additional back-upgeneration capacity would need to be installed by new consumers, though less than inalternative A). The additional capacity of Unit 14 would give the GENCO improvedcapability to schedule outages at times of day when effect on economic productivity is less. Itcould also consider an energy exchange program with Kenya such that Uganda exportedenergy in peak load periods in return for a greater quantity of imported energy during off-peakperiods. After Bujagali comes on stream, the additional energy generation of Unit 14 wouldneed to be considered as surplus, available for export until the domestic demand had grownsufficiently to absorb it. By that time, the firm energy component of this additional energywould allow some delay or reduced size in the next hydropower plant after Bujagali.

* D) Installation of both Kiira Units 14 and 15. Since Unit 15 does not provide additionalenergy except for above average hydrological scenarios, the amount of additional back-upgeneration capacity installed by consumers would probably not decline in comparison withalternative C) above. However, in higher flow scenarios, the additional energy from Unit 15would save fuel in back-up plant before Bujagali, and increase surpluses available for exportafter Bujagali. It would also allow for an additional small delay in the next plant after Bujagalior alternatively a small reduction in its size.

Table 1: Present Value of Total System CostsAlternative A Alternative B Alternative C Alternative D

No Expansion of Gas Turbine Unit 14 Units 14&15Generation

US$ million US$ million USS million US$ millionInvestmnent, O&M & Fuel $0 $92 $25 $45Hydro Investment $579 $579 $570 $568(Bujagali & next)Surplus Energy Revenue ($187) ($184) ($194) ($202)Reduced Exports $40 $26 $38 $38Existing Back-up Diesel $42 $5 $38 $37(fuel cost)New Back-up Diesel $26 so $11 $4Value of Unserved Energy $18 $0 $8 $3PV of Total System Cost $519 $519 $496 $494(discounted at 12%)Note:1. Assumptions are detailed in Annex 4.2. Hydro investment includes Bujagali and the next hydro plant after it.3. The investment cost of each alternative are included in "Investment, 0 & M & Fuel."

- 19 -

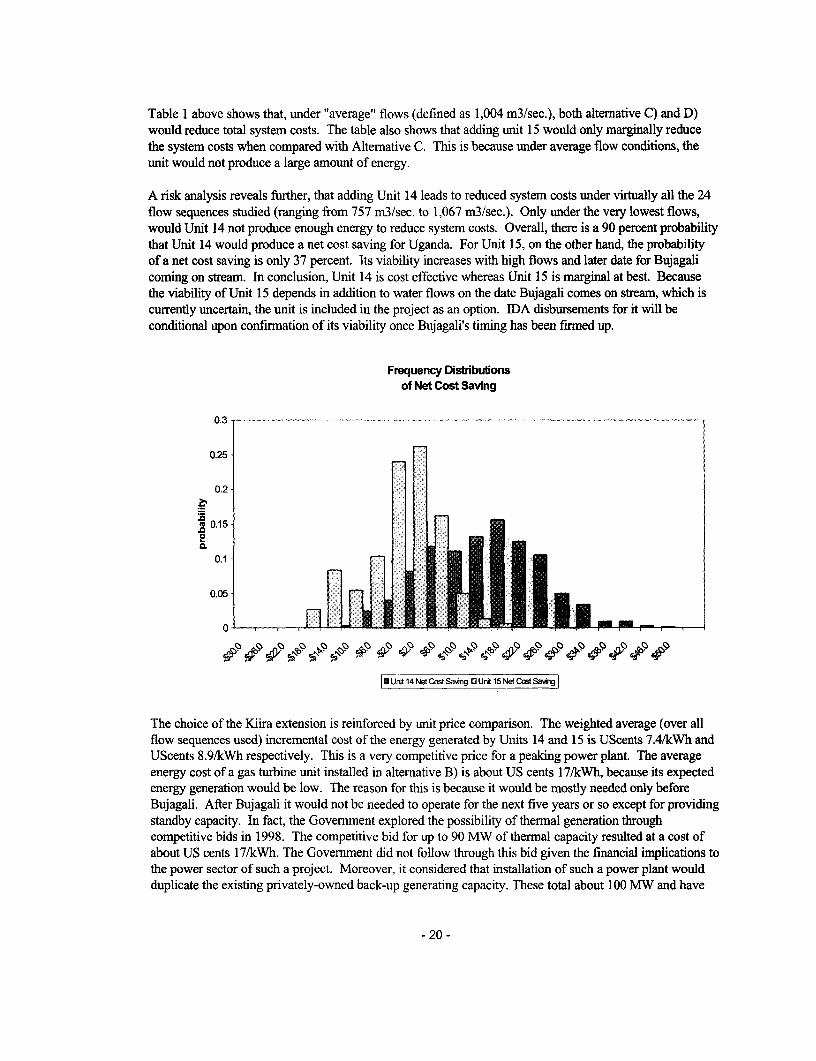

Table I above shows that, under "average" flows (defined as 1,004 m3/sec.), both alternative C) and D)would reduce total system costs. The table also shows that adding unit 15 would only marginally reducethe system costs when compared with Alternative C. This is because under average flow conditions, theunit would not produce a large amount of energy.

A risk analysis reveals further, that adding Unit 14 leads to reduced system costs under virtually all the 24flow sequences studied (ranging from 757 m3/sec. to 1,067 m3/sec.). Only under the very lowest flows,would Unit 14 not produce enough energy to reduce system costs. Overall, there is a 90 percent probabilitythat Unit 14 would produce a net cost saving for Uganda. For Unit 15, on the other hand, the probabilityof a net cost saving is only 37 percent. Its viability increases with high flows and later date for Bujagalicoming on stream. In conclusion, Unit 14 is cost effective whereas Unit 15 is marginal at best. Becausethe viability of Unit 15 depends in addition to water flows on the date Bujagali comes on stream, which iscurrently uncertain, the unit is included in the project as an option. IDA disbursements for it will beconditional upon confirmation of its viability once Bujagali's timing has been firmed up.

Frequency Distributonsof Net Cost Saving

0.3 - .. . - --. --- .

0.25

0.2

U 0.15..l.r0.1

0.1

0.05

0 4-- ~ ~0

a Unt 14 Net Cost Saving 13 Unk 15 Net Cost Sawig

The choice of the Kiira extension is reinforced by unit price comparison. The weighted average (over allflow sequences used) incremental cost of the energy generated by Units 14 and 15 is UScents 7.4/kWh andUScents 8.9/kWh respectively. This is a very competitive price for a peaking power plant. The averageenergy cost of a gas turbine unit installed in alternative B) is about US cents 17/kWh, because its expectedenergy generation would be low. The reason for this is because it would be mostly needed only beforeBujagali. After Bujagali it would not be needed to operate for the next five years or so except for providingstandby capacity. In fact, the Government explored the possibility of thermal generation throughcompetitive bids in 1998. The competitive bid for up to 90 MW of thermal capacity resulted at a cost ofabout US cents 17/kWh. The Government did not follow through this bid given the financial implications tothe power sector of such a project. Moreover, it considered that installation of such a power plant wouldduplicate the existing privately-owned back-up generating capacity. These total about 100 MW and have

- 20 -

been the source of supply for about 77 percent of the larger businesses during the shortage of grid-basedsupply.

The above analysis assumes that energy losses will decline from the high level of about 35 percent in 2000to about 25 percent by 2005, as forecast by EdF. Reduction in the level of losses is critical for the viabilityof the project. Therefore, the project includes the rehabilitation of the most critical elements of thetransmission network and the installation of a SCADA to improve the management of transmission outageswith a view of reducing their impact on the economy. In the distribution network, major loss reductionwork is best left for the future private sector concessionaire. It is expected that by the time this project isoperational in late 2003, the private concessionaire will have initiated loss reduction programs mainlythrough reduction of theft, but also some rehabilitation and extension of the network. In the meantime, theUganda Electricity Distribution Company is implementing an AfDB-fmanced loss reduction program inKampala which is expected to be completed ahead of this project in 2003.

- 21 -

2. Major related projects financed by the Bank andlor other development agencies (completed,ongoing and planned).

Latest SupervisionSector Issue Project (PSR) Ratings

____________________ ___________ ______ ________(Bank-financed projects only)Implementation Development

Bank-financed Progress (IP) Objective (DO)

Increase power generation capacity Third Power project - Credit S S2268-UG)Third Power project S SSupplemental- Credit 2268-1.(approved in January 2000)

Divestiture and reform of public Privatization and Utility Sector N/A N/Autilities Reform project (approved in

September 2000)Increase access to modem energy Rural Transfornation project

(proposed)Increase power generating capacity Bujagali Power projectthrough a private IPP (proposed)

Technical assistance for privatization Enterprise Development Project S Sand private sector development - Credit 231 5-UG

(closed in June 2000)

Other development agenciesNorway, Sweden, OECF, DFID, AfDF Cofinancing of Third Power

projectAfrican Development Fund Distribution rehabilitation &

loss reductionDFID Technical Assistance to UEB

Norway Technical assistance for powersector legal reform and to UEBand ERA, and cofinancing ofFourth Power project

Netherlands Mini-hydro

GEF/UNDP Solar PV & microfinance

Finland Feasibility study on peat powerplant

Norway and Sweden Generator and turbine for KiiraUnit 13

CDC Mini-hydro

- 22 -

NDF Cofinancing of Power II, PowerIII and the Fourth Powerproject

Japan Rural Electrification

PPIAF Rural Electrification Strategyand the Country FrameworkReport

Germany (GTZ) Legal reform of the petroleumsector

Sweden Rural electrificationIFC Rural electrificationDANIDA Transmission linesGEF/USDA KiiraAIB Transmission StudiesAFD Study on Rural ElectricityEIB Petroleum StudyIP/DO Ratings: HS (Highly Satisfactory), S (Satisfactory), U (Unsatisfactory), HU (Highly Unsatisfactory)

3. Lessons learned and reflected in the project design:

Key lessons learned in the Project Completion Report (PCR) for the Second Power project:

Lesson 1: Bank's over optimism about UEB's implementation capacity led to an unrealistictimetable for project implementation.

* Reflected in design: The project will finance assistance for project implementation, includingprocurement. Bidding documents for the project's main component and the pre-qualification of thecontractor were finalized before Board presentation.

Lesson 2: Measures to improve institutional and financial performance have to be initiatedup-front and they should be comprehensive. Weaknesses in power sector management, includinglack of autonomy and commercial orientation of UEB's operations, should have been addressed.

* Reflected in design: The Government already has initiated a comprehensive reform andprivatization program. In line with the agreed implementation plan for the privatization of thepower sector, the Government restructured and unbundled UEB before Board presentation. Amajor tariff increase was approved before the project began implementation.

Lesson 3: The Bank should have been more decisive in enforcing compliance with financialcovenants, especially the covenant requiring UEB to maintain an agreed relationship betweenaccounts receivable and its annual operating revenues.

* Reflected in design: The proposed project requires that the Government take key actionsregarding sector reform and tariffs before implementation begins. Furthermore, the commercialorientation of the power sector entities should improve with the ongoing privatization. As thepublic sector will implement the proposed project, prior to turning the operation of the system toprivate concessions, the project will focus on ensuring that an adequate public sector management,with accountability, is in place.

- 23 -

Global lessons

Three main lessons emerge from the Bank's power sector operations:

Lesson 1: Increasing private participation relieves Government budgets, improves service qualityand expands access.

* Reflected in design: The Government has successfully initiated the reform and privatization of thepower distribution and generation businesses. The proposed project will aid this privatizationthrough improving supply capacity.

Lesson 2: Implementing reform requires political commitment.

* Reflected in design: The Government has demonstrated its commitment to reform by starting theimplementation of a satisfactory Power Sector Reform and Privatization Program, including theenactment of a new Electricity Law and the unbundling of UEB.

Lesson 3: Expanding access to modern energy requires specific focus on reform design andimplementation.

e Reflected in design: The government has adopted a satisfactory commercially-oriented approachtowards rural electrification -- with the government playing the role of a market enabler. The mainelements of this strategy are: (i) level playing field for private sector participants; (ii) enablingregulatory framework; (iii) cost recovery and cost-based tariffs; and (iv) transparent subsidytransfer and financing mechanism.

4. Indications of borrower commitment and ownership:

The Government has clearly demonstrated its commitment to a coherent power sector reform strategy andto the proposed project. Uganda's very good track record for implementing the macroeconomic reformprogram, is now being followed by similar performance in utility sector reforms. The expression ofGovernment commitment at the highest level (the President) in favor of ambitious privatization, has madepossible the achievements to date. The private sector and Parliamentarians have also endorsed theprivatization process, on the condition that their concem about transparency will be addressed. The recentprivatization of Uganda Telecommunications Ltd. (UTL), with bids awarded in February 2000, gavefurther testimony of GOU's commitment to address these concems.

In the power sector, the Government has recently completed recruitment of an investment bank formarketing and closing the transactions of the generation and distribution privatization. Preparatory workfor UEB restructuring and privatization began in April 2000. Since that time the Government hascompleted the following activities:

* Inventory and valuation of UEB assets and liabilities;* Analysis of the investment needs of the power sector;* Legal and environmental due diligence work;* Preparation of pro-forma financial statement;* Creation of financial and tariff models for the successor companies and future concessions;* Drafted concession contracts, licenses, power purchase agreements and regulations required to

affect the privatization and handed-over these to the Electricity Regulatory Agency (ERA);

- 24 -

* Made recommendations on tariff adjustment and restructuring to the ERA;* Completed unbundling of UEB into three separate corporate entities;* ERA has approved a 70 percent tariff increase and improved the structure of tariffs by eliminating

cross-subsidies from industries to households.

As an indication of its commitment to the project, the Government has accelerated project preparation overthe past months. Following the appointment of UEB's new management team in the middle of 1999, thepreparation of the project's power system components picked up speed. Procurement is now well advanced.Consultants for the design and supervision of the project are in place. Contractors for the installation ofUnits 14 and 15 have been pre-qualified and bidding documents are being issued. Bids for the transmissionrehabilitation components have been received. A project manager and an environment officer have beenappointed. Finally, UEB, from its own resources, has financed a preliminary assessment of the powersector's financial position. Both implementing agencies prepared their respective draft projectimplementation plans ahead of negotiations. Similarly, MEMD has accelerated its preparation. Acompetent project coordinator is in place. MEMD is in the process of engaging a consultant to preparebidding documents for the petroleum monitoring equipment; it has drafted a training plan for the first year;prepared draft TORs for the studies included in the project; and improved its procurement filingarrangements as agreed with IDA. MEMD has also facilitated quick turn-around time on decisionsrequiring co-ordination with other Government agencies.

5. Value added of Bank support in this project:

The key value added arises from the Bank's experience in sector refonn and privatization. Bankparticipation has helped to accelerate reform. Several donors (NORAD, DflD, GTZ, SIDA, JICA, AfDB,NDF, DANIDA) have assisted the Government and the UEB in financing needed investments and providingtechnical assistance to sector reform. However, the Government needs the financial and coordinatingresources of the Bank to implement a broad based sector reform, such as the privatization of UEB. TheBank has also facilitated the adoption of an optimal power sector expansion sequence to meet demand.This is particularly important as the project is located in an international waterway. Bank involvement hasalso served as a catalyst for securing other donor financing to the project. Finally, Bank participation willincrease transparency in procurement.

E. Summary Project Analysis (Detailed assessments are in the project file, see Annex 8)

1. Economic (see Annex 4):* Cost benefit NPV=US$32 million; ERR = 20 % (see Annex 4)o Cost effectivenessO Other (specify)

A. Economic Analysis of Generating Units 14 and 15

The economic analysis for the project includes: (i) a cost-effectiveness analysis for the expansion of thepower system to bridge the electricity supply deficit in an interim period before the next major hydropowerplant is commissioned: and (ii) a cost benefits analysis to calculate the economic intemal rate of return tothe project's proposed investments.

Cost-Effectiveness Analysis