world bank documentdocuments.worldbank.org/curated/en/632161468116370703/pdf/multi... · eib...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-5239-TA

MEMORANDUM AND RECOMMENDATION

!OF THE

PRESIDENT OF THE

INTERNATIONAL DEVELOPMENT ASSOCIATION

TO THE

EXECUTIVE DIRECTORS

ON A PROPOSED CREDIT OF SDR 33.7 MILLION

TO THE

UNITED REPUBLIC OF TANZANIA

FOR A

PETROLEUM SECTOR REHABILITATION PROJECT

DECEMBER 13, 1990

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

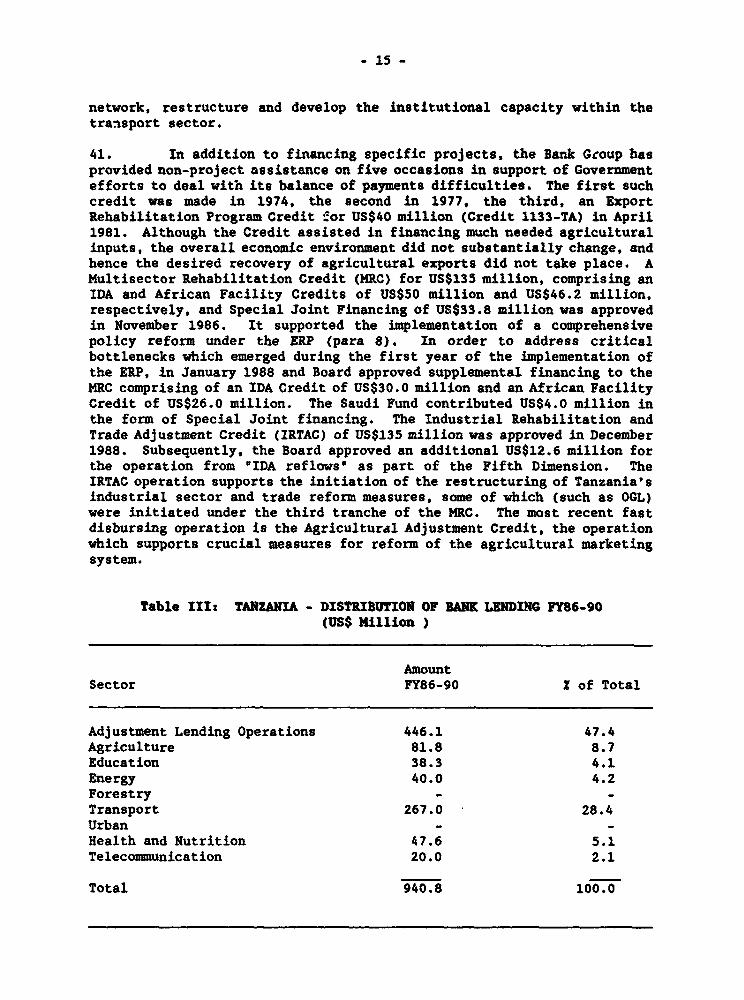

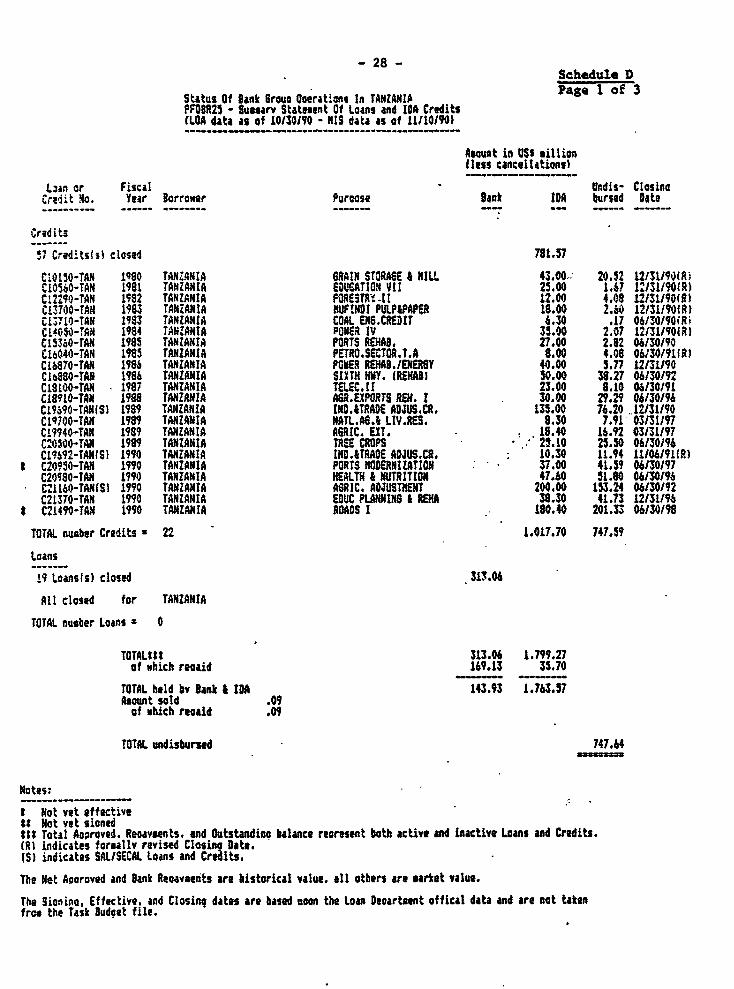

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

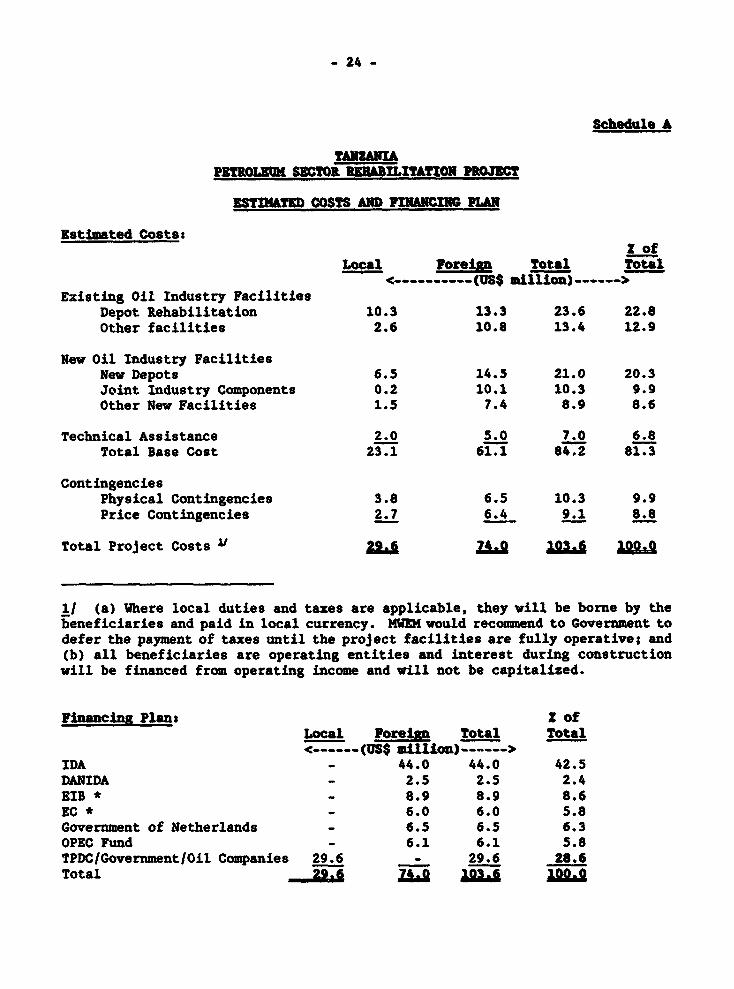

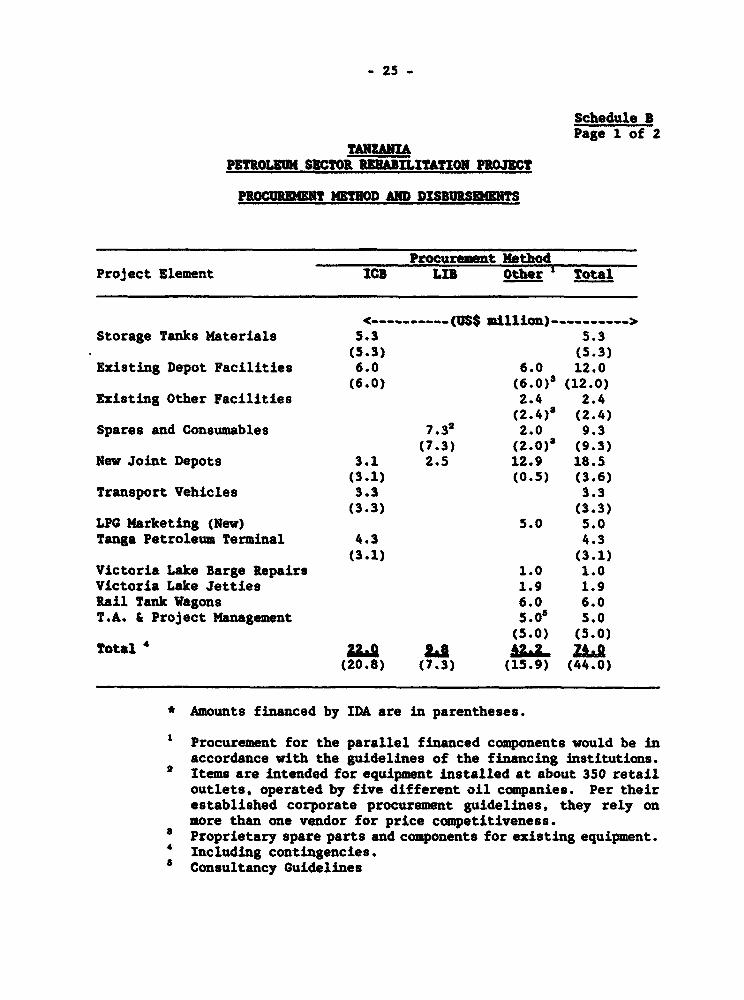

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

C ,ECY EQ2UAET

Currency Unit - Tanzanian Shilling (TSh)US$1.00 = TSh 130.0 (at time of appraisal)US$1.00 = TSh 195.0 (October 1990)TSh1.O = US$0.0051

PETRCIPhL ABBRVTIOS MD ACRONM USED

EC European CommunitiesEIB European Investment BankERP - Economic Recovery ProgramESAP Economic and Social Action ProgramGOT 2 Government of TanzaniaIBRD International Bank for Reconstruction and

DevelopmentIDA International Development AssociationIRTAC Industrial Rehabilitation and Trade Adjustment

CreditLPG Liquified petroleum gasMRC = Multisector Rehabilitation CreditMWEM Ministry of Water, Energy and MineralsPSC Project Supervisory CommitteePWG Project Working GroupTAZARA - Tanzania Zambia Railway AuthorityTIB Tanzania Investment BankTIPER 2 Tanzanian and Italian Refinery Company LtdTPDC t Tanzania Petroleum Development CorporationTRC 2 Tanzania Railway Corporation

VEIGHTS AND EEASURES

1 metric ton (mt) . 1,000 kilograms (kg), 7.19barrels, 1,143 cubic meter

1 ton of oil equivalent (toe) - 10 million kilocalories (39.7million Btu)

1 US gallon - 3.785 liters1 liter - 0.26 US gallon

Fiscal Year

Government/TIB: July 1 - June 30TPDCt January 1 - December 31Oil Companies: January 1 - December 31

This report was prepareu by Zia Mian ('PTIE), task manager untilcompletion of negotiations, T. S. Nayar, Principal Engineer (AFTIE) andEric Daffern, Principal Financial Analyst (AF6IE) task manager since Mr.Mian's departure. Secretarial support was provided by Mrs. Joan Panditand Mrs. Adriana Arriagada. Messrs. Franco Batzella and KennethNewcombe acted as lead advisors. Messrs. David Cook (AF6IE) and StephenDenning (AF6DR) were the managing Division Chief and Country Director.

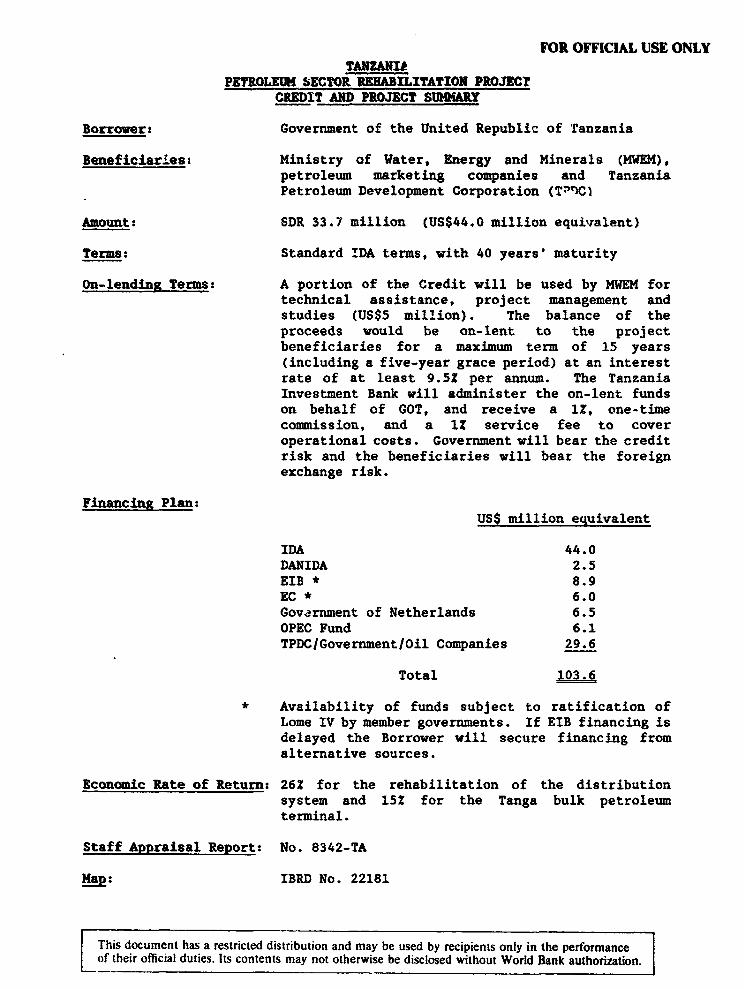

FOR OFFICIAL USE ONLYTANZANI*

PETROLEUM SiECTOR REHABILITATION PROJECTCREDIT AND PROJECT SUMMARY

Borrower: Government of the United Republic of Tanzania

Beneficiar5es: Ministry of Water, Energy and Minerals (MWEM),petroleum marketing companies and TanzaniaPetroleum Development Corporation (T'nCl

Amount: SDR 33.7 million (US$44.0 million equivralent)

Terms: Standard IDA terms, with 40 years' maturity

On-lending Terms: A portion of the Credit will be used by MWEM fortechnical assistance, project management andstudies (US$5 million). The balance of theproceeds would be on-lent to the projectbeneficiaries for a maximum term of 15 years(including a five-year grace period) at an interestrate of at least 9.5? per annum. The TanzaniaInvestment Bank will administer the on-lent fundson behalf of GOT, and receive a 1Z, one-timecommission, and a 1I service fee to coveroperational costs. Government will bear the creditrisk and the beneficiaries will bear the foreignexchange risk.

Financing Plan:US$ million equivalent

IDA 44.0DANIDA 2.5EIB * 8.9EC * 6.0Govarrnment of Netherlands 6.5OPEC Fund 6.1TPDC/Government/Oil Companies 29.6

Total 103.6

* Availability of funds subject to ratification ofLome IV by member governments. If EIB financing isdelayed the Borrower will secure financing fromalternative sources.

Economic Rate of Return: 26Z for the rehabilitation of the distributionsystem and 15? for the Tanga bulk petroleumterminal.

Staff Appraisal Report: No. 8342-TA

MLan: IBRD No. 22181

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

MEMORAUDUM AND TION OT ME PUESIDENTOF THE INTERNATION&L DEVELOHENT ASSOCIATION

TO THE EXECUTIVE DIRECTORSON A PROPOSED CREDIT TO THE UNITED REPUBLIC OF TANZANIA

FOR A PETROLEUN SECTOR RHRBILITATION PROJECT

1. The following memorandum and recommendation on a proposeddevelopment credit to the United Republic of Tanzania for SDR 33.7 million(US$44 million equivalent) is submitted for approval. Part I of the documentdiscusses the country's economic performance and development prospects, andthe Bank Group's assistance strategy. Part II of the document describes theproposed credit.

I. Country Policies and Bank Group Assistance Strategy

Background

2. In the first six years after Tanzania achieved independence in1961, its economic policy objectives stressed growth in per capita income andnational self sufficiency in skilled manpower, relying mainly on marketforces. The economy, which was predominantly dependent on subsistenceagriculture and a few estate crops, registered rapid growth. Despite thisgrowth, the country continued to depend on external financing, made littleimprovement in income distribution and did not diversify its economicstructure. Disappointed with these results, in 1967 the Governmentreassessed its development objectives and strategies, introduced sweepingchanges and embarked on a new epoch of economic management.

3. The new priorities, as enunciated in the Arusha Declaration, weredirected towards establishing a socialist society, with emphasis to be givento broad-based rural development, self-reliance in development efforts, andthe development of an educational system geared to the needs of the people.The Arusha Declaration emphasized that the State, with guidance from theParty, should play the leading role, especially in the reform and creation ofappropriate institutions. This led in the late 19609 and early 1970s to thenationalization of large-scale industry, commerce and finance, the formationof Ujamaa (communal) villages, and the replacement of farmers' cooperativeswith state-run crop marketing authorities responsible for all aspects ofmarketing of Tanzania's main export crops. The Government also embarked uponan ambitious program of industrialization based upon import substitution andthe creation of heavy industries.

4. Despite the abrupt major institutional changes, Tanzania managedto achieve significant improvements in the social sectors during the 1960sand early 1970s. Tanzania's commitment to social sectors and longer termdevelopment issues attracted sizeable amounts of aid from the donorcommunity. Significant results were achieved in the areas of education andhealth with well-publicized improvements in literacy, access to primaryeducation, infant survival, and health care in general. By the end of the1970s, the Government had made substantial progress towards achieving itssocial and equity objectives through the development of social services. Theenrollment rate in primary schools increased from 32 percent in 1965 to

-2

almost 60 percent by 1975, life expectancy rose by nearly 5 years and accessto safe watei. improved in both rural and urban areas. Significant reductionswere registered in net income disparities through the tax structure and adramatic compression in net salary ranges in the public sector.

5. The Economic Crisis. In the second half of the 1970s, however, theTanzanian economy entered a period of economic decline from which it is onlynow beginning to recover. The overall downturn in the economy was caused inpart by a series of external factors including successive droughts, the rapidincrease in oil prices, the collapse of the East African Community and thewar with Uganda. But the crisis drew attention to the policy andinstitutional weaknesses and the underlying distortions. These included,inter alia, an overvalued exchange rate, inadequate incentives and resourcesfor the agricultural sector, a poorly devised and implementedindustrialization strategy, excessive administrative controls over economicactivity and the continued growth in the size of the public sector withoutdue regard to the limited financial and administrative capacity.

The Adjustment Process

6. Economic Survival Plans and the Structural Adiustment Program(1980-1982). In response to the rapidly deteriorating economic situation,the Gcvernment launched Economic Survival Plans in 1980 and 1981, and aStructural Adjustment Program (SAP) in 1982. However, these policy reformefforts were insufficient to reverse the situation. The adjustment of theexchange rate, for example, was insufficient to remove the overvaluation, andthe increase in agricultural producer prices fell short of the prevailingrate of inflation. The 1984/85 budget, however, provided the firstindication of a new pragmatism in the Government's economic management. Theexchange rate was devalued by a third, parastatal subsidies were cut, animport liberalization program was initiated, and restrictions on the movementof grain were eased. Simultaneously, cooperatives (which had been abolishedin 1976) were re-established and were assigued many of the responsibilitiesand assets of the abolished crop authorities. Positive responses to thesemeasures encouraged the Government to consider a more comprehensive andsystematic policy reform program.

7. The Economic Recuvery Program (ERP) 1986-b9. In mid-1986,following a review of the SAP experience in light of the disappointingperformance of the economy, and after extensive consultations with the Bankand the IMF, the Government introduced a new Economic Recovery Program (ERP)aimed at remedying the defects of earlier policies. The ERP was endorsed bythe first Consultative Group (CG) meeting in nine years. The objectives ofthe ERP were: (a) to increase the output of food and export crops byproviding appropriate price and non-price incentives for production, byimproving marketing structures, and by increasing budgetary and foreignexchange resources available to agriculture; (b) to improve the physicalinfrastructure by directing resources to rehabilitation rather than newinvestments; (c) to increase industrial production by improving capacityutilization through improved mechanisms for allocation of scarce foreign

-3-

exchange; and (d) to restore domestic and external equilibrium by pursuingprudent fiscal, monetary and trade policies.

8. The ERP envisaged that the Tanzanian economy would achieve positivegrowth rates in per capita income, a sustainable external balance of paymentsposition with both higher export and import levels, an acceptably low rate ofinflation, and restored levels of physical and social infrastructure within5-7 years. To this end, the Government made significant policy changes atboth the macro and sectoral levels, including: (i) substantial exchange rateadjustments and introduction and subsequent expansion of a window for non-administrative allocation of foreign exchange (the Open General Licensingsystem); (ii) significant adjustments in interest rates, resulting in realpositive rates for some instruments; (iii) a major reduction in the number ofprice controlled items; (iv) real increases in producer prices for exportcrops and reforms in agricultural marketing (e.g., eliminating all remainingrestrictions on the transport and marketing of grain; and for sometraditional export crops allowing cooperatives to export directly, withoutresort to the marketing boards); (v) liberalization of most transport tariffsand support for private transport fleets; and (vi) institutional changesaimed at encouraging and facilitating the activities of the private sector.

9. The ERP was supported by significant inflows of externalassistance, including an August 1986 IMF Standby Arrangement and a November1986 IDA Multisector Rehabilitation Credit (MRC, Crs. 1741-TA and A03Y-TA) ofUS$135 million. A PFP elaborating on the ERP policies was endorsed by theCommittee of the Whole and the IMF Board in October 1987, and facilitatedTanzania's access to the IMF's Structural Adjustment Facility. In January1988, IDA provided an additional of US$30 million for the ERP as supplementalfinancing for the NRC. A second PFP that facilitated Tanzania's access toIMP resources in the context of the second annual arrangement under the SAF,was endorsed by the Committee of the Whole and IMF Board in November 1988.In December 1988, the Board approved further support for the ERP through theIndustrial Rehabilitation and Trade Adjustment Credit (IRTAC, Cr. 1969-TA)for US$135 million. More generally, the ERP attracted considerable supportfrom the international community including a significant increase inconcessional capital flows, particularly for import support.

10. The combination of policy and insti_utional reforms and increasedexternal assistance resulted in a substantial improvement in the economy.The rate of growth of real GDP exceeded the population growth rate in 1986for the first time since 1980, and is estimated to have grown at 4 percentp.a. in 1987 and 1988, and at slightly above four percent for 1989,indicating not only continued real per capita growth, but also a slightacceleration of the pace of economic recovery. Moreover, much of the obviousgrowth in economic activity taking place throughout the country is outside ofthe formal sector and is most likely not fully captured in the GDPstatistics. An exchange rate depreciation of over 85 percent in less thantwo years improved resource allocation and reduced excess demand for imports.Inflation has not risen from the pre-ER? level in spite of the significantdevaluation and the removal of price controls. The behavior of the parallelmarket exchange rate provided a clear, quantifiable indicator of the extentof the macroeconomic adjustment, appreciating in real terms by about 30percent from 1986 through 1988. Increased availability of fuel andtransport, the liberalization of food grain trade, and improvements in farminput supplies have resulted in improved availability and more competitive

supplies of the staple foods. Increased transport capacity, partieularly inthe private sector, together with the continuation and expansion of the own-funded import scheme, have resulted in a much improved availability of basicconsumer goods throughout the country and have acted as a considerableincentive for production of export crops. Manufactured and other non-traditional exports have also begun to increase rapidly.

11. Generally, the ERP stabilization measures were successfullyimplemented and have resulted in a significant reduction of economicdistortions. But these are only ITItial steps which need to and are beingfollowed by further policy and institutioaal changes for tha nascent recoveryto be intensified and sustained. In the monetary area, for example, theGovernment failed to limit overall credit growth, with the result that theERP targets of reduced inflation will take longer to achieve. Moreover,because of inappropriate credit allocation, saw dynamic segments of theeconomy have been relatively starved of liquidity. e roots of the creditproblem are in the structural flaws of the agricultural marketing andfinancial system (paras 18 and 21); these are complex institutional problems,which are now at the top of the Government's policy reform agenda aAdpriority issues in our assistance strategy as discussed below.

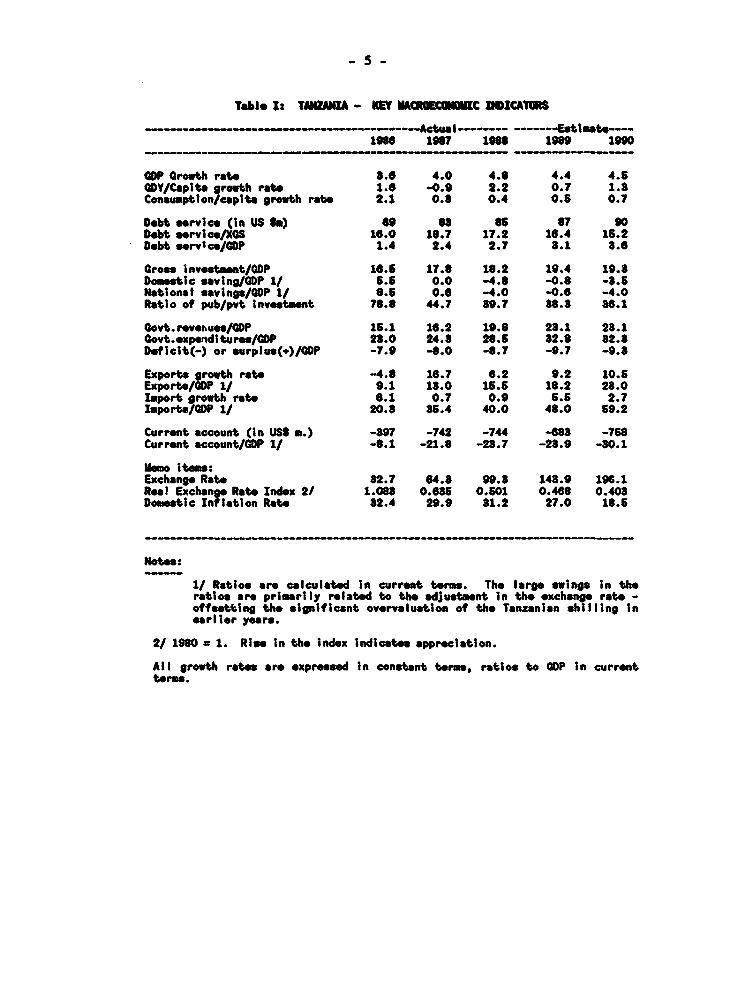

Table Is TZUNUNA - ET MACROECDSZC IDICAI$

1is" 1987 1988 1989 1990

GOP Growth rate 8.6 4.0 4.8 4.4 4.5GDY/Capit. growth rate 1.6 -0.9 2.2 0.7 1.8Consumptlon/capita growth rate 2.1 0.3 0.4 0.6 0.7

Debt servce (in US o) 69 88 8S 87 90Debt s.rvieo/XGS 16.0 16.7 17.2 16.4 15.2Debt servloo/GDP 1.4 2.4 2.7 8.1 8.6

oross Investment/GOP 16.6 17.8 16.2 19.4 19.BDomestic saving/GOP 1/ 6.6 0.0 -4.8 -0.8 -8.5National savingn/GDP 1/ 8.5 0.6 -4.0 -0.6 -4.0Ratio of pub/pvt Investment ?8.8 44.7 89.7 88.3 88.1

GOvt.revev.us/GDP 15.1 16.2 19.8 28.1 23.1Govt.expenditures/GDP 28.0 24.8 28.6 32.8 82.8Deficit(-) or surplus(*)/GDP -7.9 -4.0 -8.7 -9.7 -9.8

Exports 9rowth rate -4.6 16.7 6.2 9.2 10.5Export*/GDP 1/ 9.1 18.0 15.5 18.2 28.0Import growth rate 6.1 0.7 0.9 5.6 2.7Importe/GDP 1/ 20.8 85.4 40.0 48.0 59.2

Current account (in US1 i.) -897 -742 -744 -688 -758Current account/GDP 1/ -8.1 -21.8 -28.7 -28.9 -80.1

memo Items:ExchangC Rate 82.7 64.8 99.8 148.9 196.1Rel Exchang Rate Index 2/ 1.088 0.685 0.601 0.468 0.403Domestic nf lation Rate 82.4 29.9 81.2 27.0 18.6

Notes:

1/ Ratio* are calculated In current terms. The large swings in theratios are primarily related to the adjustment in the exchange rate -offsetting the significant overvaluation of the Tanzanian shilling inearlier years.

2/ 1980 = 1. Rise In the Index indicates appreciation.

All growth rates are expressed In constant terms, ratios to GOP In currentterms.

- 6 -

Vey Development Issues and Government Policies under ERP II (Economic andSocial Action Program) 1990-92

12. In order to consolidate the ERP stabilization measures andsustain economic growth, the macroeconomic adjustment program needs to becontinued and completed. Equally important, crucial structural andinstitutional improvements need to occur at all levels of the economicsystem. Consequently, the Government prepared a second phase of its ERPcalled the "Economic and Social Action Program" (ESAP) for the period1990-92. The ESAP was presented at the last CG meeting, in Paris inDecember 1989. The policies of the Government introduced under theprogram were welcomed and significant additional resources were pledgedfor the first year of the ESAP. The main features of the ESAP include,inter alia: (i) continued adjustment of the exchange rate; (ii) continuedtrade policy reform; (iii) reform of agricultural marketing;(iv) financial sector restructuring; (v) public sector management reform;(vi) industrial restructuring; (vii) rehabilitation of the physicalinfrastructure in support of the directly productive sectors; and(viii) rehabilitation of the delivery system for social services.

Macroeconomic Management

13. The ESAP explicitly recognizes the need to continue to move fromdirect to indirect economic management instruments. Indeed, the shiftfrom administrative mechanisms has been at the core of the policy changes.But the indirect instruments need to be further developed and the capacityof the Government to use them needs to be strengthened. The developmentof these instruments, their application to reduce distortions andincreasing the relative incentives for economically efficient activitieswill continue to be the focus of our macroeconomic dialogue.

14. The Foreign Exchange Management Regime. In the short term, thekey adjustment required is the adoption of an appropriate foreign exchangerate regime. Since April 1986, the exchange rate has devalued from Tsh 17to Tsh 195 per US dollar (October 1990). This represents significantprogress towards depreciating the Tanzanian shilling in real terms. Forthe future, it is important for the Government to adopt an exchange ratemanagement regime whereby the exchange rate is continuously reviewed andadjusted in line with developments in the balance of payments in general,and in the OGL and in exports incentives in particular, and which accountsfor, inter alia, terms of trade and inflationary developments. Workingwith the DMF towards the establishment of a responsive foreign exchangemanagement regime is a key component of our strategy.

15. Money and Credit. During the ERP, the annual limits for moneyand credit expansion were exceeded. As a result, tha Government was notable to reduce inflation, but managed to contain it at 28 percent perannum, despite the massive exchange rate adjustment. The excessive growthin credit was largely the result of the financial difficulties of themarketing boards, in particular the National Milling Corporation and to alesser extent, the tobacco and cotton marketing boards owing to theirinstitutional rigidities, transportation, storage and processing problems.The Government's objective is to reduce the rate of monetary growth whileensuring adequate supply of credit to the more productive sectors of theeconomy. This not only requires an appropriate fiscal policy but also the

-7-

elimination of the financial difficulties of the marketing b3ards throu3hthe restructuring of the agricultural marketing system (para 19).

16. Government Budget. The Government was successful under the ERPin controlling expenditure, and focussed the public investment program onrehabilitation and completion of ongoing projects rather than on newinvestments. It also succeeded in containing the overall budgetarydeficit within the set limits. However, serious issues remain to beaddressed (paras 23). Practically all Government activities areunderfunded. Furthermore, although recurrent transfers to parastatalshave largely been terminated, heavy claims are now being made on thebudget for parastatal restructuring and in respect of earlier parastataloverdrafts guaranteed by the Government.

17. On the revenue side, the first phase of reform of customstariffs and sales taxes was initiated under IRTAC. Focus now is onadditional measures for correcting the remaining structural deficienciesin the tax system (e.g., extensive use of exemptions) and itsadministration (e.g., poor collection and compliance rates) so as tofurther improve the revenue performance.

18. Pricing and Distribution Policies. To encourage domesticsavings and efficient financial resource use, the Government made thestructure of interest rates positive in real terms. The Governmentexpects to be able to reduce interest rates by lowering the rate ofinflation through appropriate budgetary and monetary policies. The numberof categories of goods subject to price control was reduced to 10,considered basic necessities, comprising less than 15 percent of theconsumer price index basket. As goods were decontrolled, the regulationsthat *confine' goods to specified parastatals for their importation andwholesale distribution were also dismantled. Our strategy is to continueto work with the Government to continue the processes of price decontroland deconfinement.

Maior Sectoral Issues

19. Agriculture. Restoration of growth and increased exportearnings will depend primarily on the performance of the agriculturalsector, and hence on the package of incentives for agriculture. Under theERP, the Government has raised the real level of producer prices, linkingthem more closely to developments in world market prices. Improvements inthe efficiency of agricultural marketing would also be critical. Domesticfoodgrains trade from the farmgate to the consumer was liberalized in thepast three and a half years, and this was a major factor in the increasedproduction. As part of ESAP, the Government has begun to implement aprogram for fundamental changes to improve the structure of export cropand agricultural input marketing (under the Bank-supported TanzaniaAgricultural Adjustment Program. For some crops, it has permittedcooperative unions and other bodies to participate in export marketing andto import inputs either directly or through agents. As further measures,the program focuses on diversification of marketing channels and otherimprovements in the efficiency of export crop marketing. The key featuresof the program are: (i) to reduce the role of the marketing boards tomanaging auctions or open tender systems and providing quality control andmarket intelligence; and (ii) to introduce multiple channels of marketing

- 8 -

by allowing private traders, farmers' associations, primary cooperativesocieties and cooperative unions to trade freely among themselves and toretain ownership until final sale of their crop. The next phase of theprogran will require reforming the cooperatives. Studies are now underwayto develop a reform progrwa for these marketing agents.

20. Financial Sector Reform. The increased reliance on indirectinstruments of economic management and the reduced role of the Governmentin directly productive activities must be accompanied by a restructuredrole for the financial sector in the mobilization and allocation ofresources. At present, however, the sector is afflicted by a number ofmajor problems including the poor financial condition of the bankinginstitutions, the inadequate capacity for resource mobilization andserious inefficiencies in credit allocation (primarily to publicenterprises and cooperatives, ignoring the private sector). Consequently,the Government has undertaken a comprehensive sector review with Bank andIMF assistance and is preparing an action program for the reform of thesector. The main objectives of the Government's reforms are to diversifyfinancial channels and services, improve resource mobilization, restorethe financial viability and increase the efficiency of the bankinginstitutions. The reform is also expected to cover the overall system formanaging and regulating financial institutions including the functioningof the Bank of Tanzania (the central bank), the restructuring of theNational Bank of Commerce, overhauling the system for providingagricultural credit and parastatal finance, establishment of newspecialized financial institutions and introducing new instruments andservices. The Bank plans to support the setion program in this key sectorwith a Financial Restructuring Credit (para. 46).

21. Industry. The Government's objectives in the industrial sectorare to improve capacity utilization while at the same time ensuring thatresources are directed towards the more productive and efficient firms inthe sector. In this regard, external sector policies and fiscal andmonetary policies are of critical importance. In addition, specificinterventions are being prepa.ed to assist in the progressiverestructuring of particular subsectors, commencing with textiles, leatherand agro-processing. These are potentially viable sub-sectors that couldbe expected to recover quickly and provide substantial supply responses.The strategy is to continue the subsectoral approach by carrying out moresubsectoral studies and developing and implementing additional subsectoralrestructuring programs. Reforms in the management and operation ofparastatals are also necessary to ensure that they are responsive to priceand other macroeconomic signals.

22. Infrastructure. A major objective of ESAP is the rehabilitationof physical infrastructure. The main emphasis under the Government'srecovery program in regard to roads was the rehabilitation of thecountry's network of highways, secondary roads, feeder roads and accessroads, which are of particular importance to the evacuation ofagricultural production to processing centers and ports. Closely linkedwith rehabilitation is improving the capacity of central and localgovernment authorities to maintain the road network, both in regard tostretches that are still in rea,onable condition and those that arerecently rehabilitated. The Government with Bank assistance prepared anIntegrated Roads Project (IRP), which was approved by the Board on May 31,

- 9 -

1990. A comprehensive road transport policy paper was prepared by theGovernment and its recommendations have made an important contribution tothe further improvement of policies in this area. A two- stage programfor the rehiabilitation of the Tanzanian railway system has also beenprepared and endorsed by donors who committed sufficient funds for thefirst stage of the program which has been completed. A second phase wasappraised in July 1990. The railway rehabilitation program is animportant ingredient in the rehabilitation of the petroleum distributionsystem, which itself is needed to complement the road and other projects.The challenge for the Government under ESAP is to implement these agreedtransport rehabilitation programs.

Public Sector Management

23. The public sector has always been cast in the leading role inthe Tanzania's development strategy. However, despite impressiveachievements in the past, the sector Is no longer able to fulfill thatrole, and, in fact, has become a drag on the recovery of the economy. Ifrecovery is to be sustained, it is necessary to address critical problemsin four broad areas: (i) central government public expenditurepriorities; (ii) local government finance and management, (iii) publicservice pay, staffing levels, and management, and (iv) the parastatalsector.

24. Central Government Expenditures. Central government programsare over-extended and under-funded. Among the main causes are: the rapidexpansion of commitments, revenue weakness, crowding out of ministerialprograms by debt service and emergency funding for parast-.tals, and theoverexpansion of staffing. The Government needs to focus recurrentexpenditures on priority programs, and resolve She financial difficultiesof parastatals as quickly as possible. Though it has been significantlyscaled back and focussed on the completion of existing projects, thePublic Investment Program (PIP) requires further rationalization toreflect rehabilitation priorities more effectively. The Government andthe Bank jointly carried out a public expenditure review (PER). Therecommendations of this study constitute a basis for the restructuring ofthe public expenditure and the formulation of a medium-term strategy forpublic expenditures, covering both recurrent and development outlays underESAP.

25. Public Service. For at least one and a half decades theTanzanian Government expanded its total employment twice as fast as theunderlying revenue base. By 1984, total employment in public service,excluding the armed forces, was about 300,000, a level that has remainedconstant since then. Over the years, as the budget situation deterioratedand inflation rose, pay levels failed to keep pace and differentialsbecame compressed, severely distorting the incentive structure andreducing public service morale and productivity. The average wage haslost 80 percent of its value since 1976. The ratio of after-tax incomesbetween top salary and minimum wage was as low as about 4:1 in 1987/88,though this has improved to 9X1 currently. The Government has moved toeliminate ghost workers (about 28,000 were eliminated from Government payroles in 1989), but further retrenchment is required if pay levels are tobe restored. In addition, the Government's capacity to effectively managethe public service and restore discipline needs to be strengthened.

- 10 -

26. Local Government. After being in abeyance for over a decadeduring the period of decentralization, local governments (district andurban councils) were reintroduced in 1983/1984 and given responsibilitiesfor, inter alia, primary education, health care and water supplies. Witha few exceptions, urban and district councils have performed poorly.Their staffs are too large, paid on the same eroded scales as centralgovernment, and poorly motivated. They have generally not succeeded incollecting much revenue of their own and remain heavily dependent ontransfers from central government. Financial and establishment controlsand overall management are weak.

27. Parastatals. With over 400 different agencies, Tanzania'sparastatal sector is too large, poorly managed, and for the most part aninefficient user of resources and a burden on the economy. Lifting theburden of the public sector by reducing its size and making it operatemore efficiently is one of the most important and difficult tasks facingpolicy makers in the next five years. Among other actions, utilities needto adjust their tariffs; insolvent financial institutions need to berestored to health (or done away with), and many public enterprises needto be scaled back or abolished. The Bank and the Government jointlyreviewed the parastatal sector and a report, 'Parastatals in Tanzania:Towards a Reform Program', was issued in July 1988. The Bank is assistingthe Government to develop a reform program based on the results of thestudy. Our proposed lending program includes an adjustment lendingoperation intended to support the -implementation of reform programs toimprove public sector management.

Longer term Development Issues

28. Population and Human Resource Development. In addition to theissues discussed above, Tanzania faces a number of medium tolong-term issues, some of which have short-term aspects which Governmentprograms must begin to address. Tanzania faces a critical problem interms of the rapid rate of population growth (3.2 percent per annum). Iffertility does not decline, the rate of population growth will have graveimplications for: (i) the country's resource base, particularly land andthe environment; (ii) per capita incomes and living standards; and(iii) pressures on public services, particularly education, health andhousing facilitie.,. Our assistance strategy will focus on helpingTanzania to slow down the population growth rate by supporting efforts forfamily planning and/or monitoring an education campaign.

29. Closely related is the issue of human resource developmentincluding, inter alia, the strengthening of the analytical and monitoringcapabilities to pursue both immediate and longer term development goals.Key issues in this regard are: (i) mobilizing resources for the socialsectors (cost-recovery and community participation); and (ii) moreefficient use of existing resources (for example, focussing on maintenanceand rehabilitation of existing social service facilities, beforeexpansion). Both the Education Rehabilitation (FY90) and the HumanResources Development (FY93S) projects will aim to address these issues.

30. Women play a very important role in Tanzania's economy bygrowing most of the food and finding most household fuel and water. Buttheir access to development programs is limited, la-gely by tradition. We

- 11 -

plan to prepare an assessment paper on women's potential role inTanzania's development, the policy and institutional framework affectingtheir welfare and productivity, the strategy and action programs for theirinvolvement in the development process. The study will be an input intothe Country economic memorandum planned for FY91, which will serve as amain vehicle for a dialogue with the Government. On the project side, theAgricultural Research and Agricultural Extension (FY89), Population,Health and Nutrition FY91, and Smallscale Enterprise FY92S projects, willall pay special attention to women's needs and issues.

31. Entrepreneurial and Private Sector Development. Two decades ofcentralized investment planning and extensive Government interventions ineconomic activities have suppressed free enterprise and resulted inactivities, technologies and organizational designs unsuited to theeconomic needs of Tanzania. There is an active informal sector but theformal private sector, which had little encouragement, remains very smalloutside of the petroleum sector. With the shift from direct to indirectinstruments of economic management, and with the Government concentratingon provision of infrastructure and services, the future tempo and patternof economic activity will increasingly be determined by the skills,talents and ideas generated by individuals and private enterprises. Inaddition to the Government's commitment to the private sector through thisproject, we will use our economic and sector work and IFC lendingoperations: (i) to determine effective mechanisms of promotingentrepreneurial activity in the Tanzania environment; (ii) to assist inthe formation of appropriate policies which will provide for equal accessto credit and other services necessary for entrepreneurial development;(iii) to facilitate the transformation from the informal to formal privatesector; and (iv) to provide resources for private sector investment. Thereform programs to improve the financial and industrial sectors wouldfacilitate the channeling of financial resources to the private sector.

32. Environment. Helping Tanzania to address its environmentalproblems is a priority in our assistance strategy. The country is endowedwith a wealth of natural resources. However, the exploitation of theseresources is proceeding largely in an unmanaged and destructive manner.The key issues include deforestation, soil erosion, wildlife conservation,and institutional capacity and legal framework. With the help of theSwedish International Development Authority and the International Union ofConservation of Nature, the Government is carrying out an environmentalassessment to develop an environmental strategy and an action plan. Theplan will form the basis for assistance by the Bank and other donors whoare expressing keen interest in helping Tanzania to deal with itsenvironmental problems. Meanwhile, on the basis of what is already known,the Bank is using ongoing lending operations and the existing work programto begin and in some instances continue to help to address some of thecritical short and medium-term issues, particularly in the areas ofreforestation and institution building.

33. Poverty Alleviation. The extensive poverty which existed inTanzania many years preceding its adjustment program is still evident.Bank efforts will focus on poverty reduction as a major goal, and on thesocial dimensions of the adjustment process. We will aim to assist theGovernment to ensure that low-income groups have opportunities toparticipate in the Economic Recovery Program and that vulnerable groups

- 12 -

will not be adversely affected. So far, even in the short term, themeasures implemented in the context of the ERP and the related increase inthe concessional capital inflows have been beneficial to the poor. Therehave been no visible adverse economic and/or social effects associatedwith the ERP. Deflationary forces emerged from the supply response.availability of imports and increased competition resulting from the tradeliberalization measures. Fiscal and monetary restraint coupled withrealistic interest rates have provided a check on inflationary pressures.Moreover, though more progress is required, higher producer prices of themain exports resulting from continued exchange rate adjustment and fromimprovements in marketing efficiency, have raised farm incomes and ruralpurchasing power. In urban areas, food grain prices have remained stablebecause of substantial reductions in marketing costs resulting from graintrade liberalization. Our strategy will focus on those areas likely toneed particular attention during the recovery process including thepoorest groups, women and children, and those expected to be displacedfrom public employment in the next phases of the ERP.

Growth Prospects

34. In the coming years the Tanzania economy is expected to achieve:

Table Ili TANZANIA - GROWTH PROSPRCTS

1990-1995 1995-2000

(annual averages)

Real GDP growth 4-4.5Z 4-4.5?Real per capita growth 1.2-1.72 1-1.7ZExport volume growth 9.5-10.5Z 9-10XImport volume growth 2.7-3.2? 3.2-4.5ZCurrent account deficit/GDP 35-26? 25-20?

Reduced distortions, improved allocation of foreign exchange, in additionto infrastructural and institutional improvements, should lead tosignificant improvements in the efficiency of resource use. Inparticular, the improved policy environment should lead to: (i) betterutilization of imported inputs, particularly in industry because of thereallocation of resources away from low and negative value-addedactivities toward more efficient export-oriented enterprises;(ii) increased utilization of existing capacity in low import-intensiveactivities; and (iii) an allocative shift in favor of agriculture, a lessimport-intensive sector. This would result in sustained positive percapita income growth; substantial export volume growth, in the short runfrom improved performance of traditional exports and later emanatingparticularly from increased non-traditional exports and tourism; areduction in import dependence; and an improved current account position.

35. For many years, Tanzania will continue to face large externalimbalances. Thus, the Government's adjustment program will continue to

- 13 -

require an active exchange rate policy coupled with large amounts ofexternal financing and debt alleviation to support sustained growth. Thecomposition and terms of external flows needed to support the ERP are asimportant as the absolute volume: (i) the present mix of about 50/50between import support and specific investments in rehabilitation projectsis appropriate and needs to be maintained, but should be reviewed on aregular basis; (ii, in some instances donors should be prepared to fund upto 100 percent of the capital costs of the projects they support; and(iii) donors should be prepared to finance some recurrent costs for alimited period.

36. Agriculture will remain the main source of incremental growth.However, the country needs to develop other sources of growth and increaseits export earnings in order to achieve its longer term developmentobjectives. Potential areas include: ti) development of non-traditionalexports, especially mineral exports; and (ii) development of the touristindustry which hitherto has been inhibited by lack of appropriate policyincentives and inadequate infrastructural facilities.

Performance Indicators

37. As already discussed, we have identified key componentsaffecting the implementation of the adjustment program. Inadequateperformance in these critical areas would trigger an evaluation of theimpact on the program and the development prospects of the economy and, ifwarranted, a reassessment of the level and orientation of our assistancestrategy. The key indicators for judging progress on the implementationof Tanzania's adjustment program include: (i) maintaining an exchangerate consistent with appropriate demand in the expanding tradeliberalization facility (OGL) and with growth in non-traditional exports;(ii) maintaining fiscal prudence consistent with virtually zero netborrowing from the domestic banking system, and beginning the process ofpublic expenditure and public sector management restructuring;Ciii) implementing the reforms of the agricultural marketing system inaccordance with the agreements reached in the context of the IDA-FinancedAgricultural Adjustment Credit (Cr. 2116-TAN) (para 18); (iv)restructuring of the financial sector in accordance with therecommendations of the financial sector review and maintaining a positiveinterest rate structure; and (v) implementing a rehabilitation program forimproving the efficiency of the transport sector in accordance with thescope and schedule to be agreed in the context of the proposed IntegratedRoads Project (para. 21).

Bank Group Operations

38. The Bank's involvement with Tanzania can be divided into threedistinct periods: (i) from 1961, until the end of the 1970s, when theBank strongly supported Tanzania's overall development strategyemphasizing growth with greater income equality and quickly becameinvolved in almost all sectors of the economy (by the late 1970s, ourprogram had expanded to over six projects per year and over US$100 millionin commitments, about 40 percent of which was IBRD); (ii) from 1980 to1986, when the Bank scaled back its assistance program as the economycontinued to deteriorate and we were unable to reach an agreement with theGovernment on the policy and institutional changes necessary to restore

- 14 -

growth; and (iii) from 1986, with the launching of the ERP, when weentered a third period in our involvement with Tanzania characterized byimproved dialogue and expanded assistance (annual Bank disbursements haveincreased from US$69 million in FY86 to US$137 million in FY90). Sincethe beginning of this period, we have been incorporating the lessonslearnt from our previous association. Particular emphasis has been givento develop and implement an integrated strategy between the macro,sectoral, and project components, with a policy-focused economic andsector work (ESW) program playing a crucial role (paras 42 and 43).

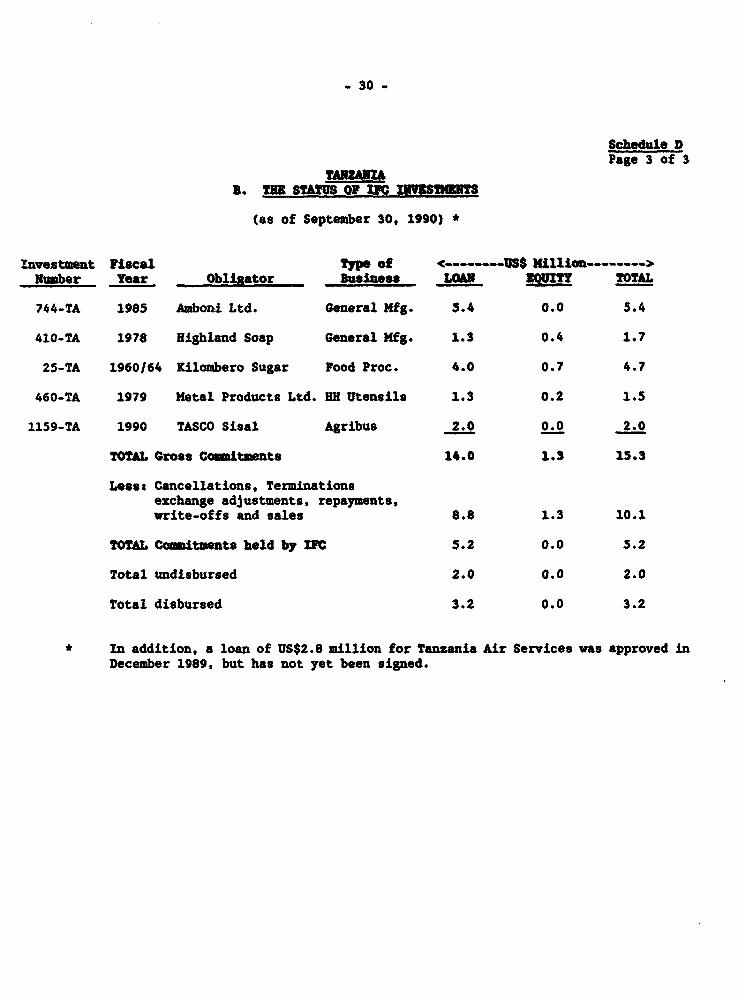

39. Lending Operations through end of FY90. Tanzania joined theBank, the Association, and the International Finance Corporation in 1962.Beginning with an IDA credit for education in 1963, 79 IDA credits and 19Bank loans, two of these on Third Window terms, amounting to US$2,112.33million have so far been approved for Tanzania. In addition, Tanzania hasbeen a beneficiary of 11 loans totalling US$244.8 million which wereextended for the development of the common services and development bankoperated regionally by Tanzania, Kenya, and Uganda through theirassociation in the former East African Community. IFC investments inTanzania have included the Kilombero Sugar Company, soap manufacturing,metal product manufacturing and the Amboni sisal rehabilitation project.

40. Bank Group lending in Tanzania has centered on agriculturetransport and communications, industry and energy and education andmanpower development. Since FY81, new Bank Group lending has beenfocusseJ primarily on the rehabilitation and use of existing productivefacilities and the expansion of infrastructure and services (such as powergeneration and education facilities) of long-term use to the economy.Projects have included technical assistance and training for bettermaintenance and use of existing facilities and more effective resourceuse. Lending during FY82-90 included a Second Petroleum ExplorationProject, a Petroleum Sector Technical Assistance Project, Third and FourthTechz.cal Assistance Projects (focussed on key manpower gaps in theagricultural sector), Dar es Salaam Sewerage and Sanitation(Rehabilitation) Project, a Coal Engineering Project, a Fourth PowerProject (hydroelectric), a Port Rehabilitation Project, a Sixth Highway(Rehabilitation) Project, involving rehabilitation of high priority roadsand assistance to the trucking industry, a Power Rehabilitation Project torestore Tanzania's power system, and a Second Telecommunications Project,to rehabilitate and improve the efficiency of the telecommunicationsystem, an Agricultural Export Rehabilitation Project, to improveTanzania's agricultural export performance, a National Agricultural andLivestock Research Project, to develop the national research services, aNational Agricultural and Livestock Rehabilitation Project, to strengthenthe agricultural extension service and cashew and coconut, a TreecropsProject to improve production of these crops through breeding anddeveloping of disease-resistant and high-yielding plants, a Health andNutrition Project to strengthen Government capacity to deliver health andnutrition services, a Ports Modernization project to help expand thephysical facilities and strengthen the managerial and operationalcapabilities of the Tanzania Harbors Authority, an Education Planning andRehabilitation project to rehabilitate the educational system andstrengthen capacity to plan and implement appropriate education policies,and an Integrated Roads Project to restore Tanzania's essential road

- 15 -

network, restructure and develop the institutional capacity within thetransport sector.

41. In addition to financing specific projects, the Bank Group hasprovided non-project assistance on five occasions in support of Governmentefforts to deal with its balance of payments difficulties. The first suchcredit was made in 1974, the second in 1977, the third, an ExportRehabilitation Program Credit Cor US$40 million (Credit 1133-TA) in April1981. Although the Credit assisted in financing much needed agriculturalinputs, the overall economic environment did not substantially change, andhence the desired recovery of agricultural exports did not take place. AMultisector Rehabilitation Credit (MRC) for US$135 million, comprising anIDA and African Facility Credits of US$50 million and US$46.2 million,respectively, and Special Joint Financing of US$33.8 million was approvedin November 1986. It supported the implementation of a comprehensivepolicy reform under the ERP (para 8). In order to address criticalbottlenecks which emerged during the first year of the implementation ofthe ERP, in January 1988 and Board approved supplemental financing to theMRC comprising of an IDA Credit of US$30.0 million and an African FacilityCredit of US$26.0 million. The Saudi Fund contributed US$4.0 million inthe form of Special Joint financing. The Industrial Rehabilitation andTrade Adjustment Credit (IRTAC) of US$135 million was approved in December1988. Subsequently, the Board approved an additional US$12.6 million forthe operation from 'IDA reflows' as part of the Fifth Dimension. TheIRTAC operation supports the initiation of the restructuring of Tanzania'sindustrial sector and trade reform measures, some of which (such as OGL)were initiated under the third tranche of the MRC. The most recent fastdisbursing operation is the Agricultural Adjustment Credit, the operationwhich supports crucial measures for reform of the agricultural marketingsystem.

Table III: TANZANIA - DISTRIBUTION OF BANK LENDING FY86-90(US$ Million )

AmountSector FY86-90 Z of Total

Adjustment Lending Operations 446.1 47.4Agriculture 81.8 8.7Education 38.3 4.1Energy 40.0 4.2Forestry _ _Transport 267.0 28.4Urban - -Health and Nutrition 47.6 5.1Telecommunication 20.0 2.1

Total 940.8 100.0

- 16 -

Bank Assistance Strategy

42. The main challenges facing Tanzanias' economy are: (i) toaccelerate growth by consolidating policy reform and restructuring keyinstitutions including, inter alia, agricultural marketing boards and thecooperatives, financial institutions and parastatals; (it) to rehabilitatekey infrastructure and services; (iii) to restore social services (health,education, water) to the level of development achieved in the 1970s; and(iv) to address medium to long-term development issues, especiallysubstantial reduction in its high population growth rate, povertyalleviation, human resource development and effective protection of itsenvironment. The Bank's overall assistance strategy has six major andclosely related components: (a) improve the efficiency and effectivenessof economic management and resource allocation; (b) reduce and rationalizethe role of the public sector; Ic) reduce sectoral and physicalconstraints; (d) develop entrepreneurship; (e) address social and longer-term development issues; and (f) mobilize adequate external resources.

Vehicles for Implementing the Strategy

43. Economic and Sector Work (ESW) Strategy. The planned ESW is acrucial component of the Bank's assistance strategy to Tanzania. It isdesigned to provide the analytical underpinning for the Bank's policydialogue on the key ESAP and longer term development issues. It isimperative for the Bank to carry out comprelensive analyses, identifypolicy options and clearly demonstrate the expeeted benefits and costs ofthe recommended agenda of policy and institutional reforms needed tosustain the ESAP and eventual economic growth and development. The paceof adjustment in Tanzania is very dependent on the quantity and quality ofour ESW. The recent experience with regard to the industrial sector studywhich facilitated the ongoing IRTAC, and the review of the food grainmarketing system which facilitated an important reform of the system,clearly demonstrated the indispensability of and the payoffs which canresult from an investment in ESW. In addition to facilitating aneffective dialogue with the Government, donors look to the Bank forleadership in this important work.

44. Over the last three years, we have undertaken a number of majorsector studies: (i) a review of food grain and agricultural exportmarketing systems; (ii) a transport sector study which focussed theattention to the Government and the donor community on the issues in thetransport sector; (iii) a parastatal sector study to underpin the dialogueon the reform of state enterprises; (iv) a review of the publicexpenditure to facilitate restructuring of the public expenditure programand improve resource allocation; and (vi) a number of specific subsectorstudies in the areas of trade, tariffs and taxes which are importantinputs into the ESAP. We are completing an economic report, that willanalyze some of the medium and longer-term issues facing Tanzania and setthe stage for the next phase of the reform program. During FY91 and FY92,we plan to undertake structural studies, and carry out reviews andassessments of debt management, food security, environment and land use,education sector, small-scale enterprises, mining, transport sector,population policy, women in development, and AIDS. These assessmenta andstudies also facilitate preparation and implementation of our lending

- 17 _

operations, both adjustment as well as investment projects. In developingand carrying out the ESW program, we will aim to make it as collaborativeas possible, and rely on economists from local universities and researchinstitutions.

45. Cooperation with the IMF. Continued close cooperation andcoordination between Government, the DMF and the Bank in the furtherdevelopment and implementation of the ESAP is clearly critical. We willcontinue to work with the Government and the IMF on the preparation ofpolicy framework papers and ensuring that an appropriate macro frameworkis maintained.

46. Lending Strategy. The planned FY91-95 lending operations aredirectly linked to the Bank's assistance strategy. The five-year lendingprogram includes one quick-disbursing adjustment lending operaLion eachyear, in continuing support of the anticipated policy and institutionalreforms which Tanzania needs to carry out. The policy based-lendingoperations will focus on development issues that are especially criticalto the further implementation of the ERP, as already discussed (paras 11-32). In FY89, we focussed on trade reform and industrial restructuringand in FY90, we focused on the reform of the agricultural marketingsystem. We expect our next operations to focus on financial sectorreform, public sector restructuring and on further restructuring of theindustrial sector, in that order.

47. Complementing the adjustment lending operations are highpriority specific investment operations focussed on rehabilitating of keyeconomic services and physical infrastructure, and tackling long-termdevelopment issues. We began this process with agricultural services (IDAcredits have recently been approved for research and extensionrehabilitation projects); transport (with Board approval of the creditsfor the Ports and Integrated Roads projects in February and May 1990,respectively) and in health and education (with credits approved in Marchand May 1990, respectively). Our five-year lending program provides forbroadening this approach to cover energy, railways, urban infrastructure,forestry and human resource development, and as needed, to intensify itwith follow up specific investment projects. In designing these futureprojects we will focus on projects which help to build and strengthen thecore planning, implementation, management and monitoring capacities ofspecific institutions. During the transitional period of three to fiveyears, about 60 percent of IDA lending would be for adjustment operations.Thereafter, with a supportive policy framework largely in place, and withthe results of the reform program being felt over a wide spectrum ofeconomy, IDA lending would begin to shift emphasis to investmentoperations as the main lending vehicles, and the proportion of adjustmentlending would correspondingly decline.

48. Supervision Strategy. Capacity for project implementation inTanzania had virtually collapsed w4.th the general deterioration of theeconomy and is still weak, due to shortage of skilled and experiencedmanpower and weak institutions. In the short run, our assistance strategycalls for: (i) project design which takes into account the skills gap;(ii) intensified supervision effort (we have substantially increased theamount of resources allocated for supervision); and (iii) provision forselective technical assistance. For the medium to longer term, we expect

- 18 -

our planned assistance in the public sector management, education andhuman resource development to help address this problem.

49. Aid Coordination Strategy. Tanzania's adjustment program needssubstantial amounts of external financing well beyond any one donor'sresources. Consequently, the Bank's assistance strategy also focuses onassisting Tanzania to mobilize appropriate external financing (in terms ofquantity and quality) through cofinancing arrangements, and formal andinformal aid coordination efforts. Tanzania meets the eligibility andqualification criteria for the Special Program of Assistance (SPA) fordebt distressed countries in Sub-Saharan Africa. We will work closelywith the Government and the donors to translate pledges of assistance toTanzania under the SPA into actual disbursements. The Bank plans tomaintain the cycle of annual CG meetings for Tanzania. The Bank has alsoassisted the Government in organizing effective donor meetings at thesectoral level, including transport, agriculture and energy. Similarmeetings will be organized for other key sectors. Finally, the Bank plansto keep in regular and close contact with other donors to facilitateeffective coordination of donor programs.

Stummary Assessment

50. There is a strong consensus that Tanzania made good progress inthe implementation of the initial three-year phase of its ERP.Nevertheless, much more remains to be done to address the many remainingstructural issues, and rehabilitate the country's key economic and socialservices and infrastructure. Recognizing this need, the Government haslaunched a second phase of the ERP, the ESAP, to build on the steps takento date. The macroeconomic scenario and Bank assistance strategy outlinedabove are based on two critical assumptions: (i) that the Governmentcontinues to move ahead with the economic reform at a reasonable pace; and(ii) that other donors including the IMF continue to provide the necessarysupport in terms of both quantity and quality. This, indeed, does appearto be the most likely scenario.

51. However, there are risks to bear in mind. Although Tanzaniamade substantial progress in the implementation of the first phase of itsERP, the consensus within Tanzania for reform is still tenuous, althoughstrengthening. Given the extent of the remaining distortions andseriousness of the economic situation, some donors are restive about thepace of the adjustment program. But the Government is convinced that thepace is at the edge of social, political, institutional and administrativefeasibility. Government commitment to continue with the adjustment effortis firm. The prospects for sustaining the program should be measuredagainst where the country has come from, its accomplishments to date andthe resolve to continue.

52. The Bank's assistance strategy as described above assumes thepresent pace of adjustment to be an acceptable core of reform. Thepolitical changes taking place in Tanzania, including inter alia,President Mwinyi's consolidation of power now as Chairman of the rulingParty as well as President and Head of State, and the appointment of like-minded pragmatists in key Government ministries, are providing a window ofopportunity to engage the Government in a challenging dialogue forbroadening and deepening the adjustment process, and the most likely

- 19 -

prospects are for continuing to make progress in this regard. If theefforts for a faster pace of adjustment succeed, additional externalfinancing may be needed, and the prospects are that it will beforthcoming. If on the other hand, the pace should slacken and render theprogram insufficient or in the unlikely extreme, reverse the adjustmentmeasures, IDA will reassess its assistance strategy, including theorientation and level of the lending program. Bank assistance would belimited to a core program of specific investment projects focussed onrehabilitation of the vital infrastructure and work on development issuesof continued relevance (e.g., road maintenance, environmental protection,health and education).

- 20 -

II. The Proposed Crpdit

53. The proposed Credit would be on standard IDA terms, with 40years' maturity, and would assist in rehabilitation of the petroleumsector. The project would be cofinanced by five other donors who arecontributing US$30 million equivalent: DANIDA, US$2.5 million; EIB,US$8.9 million; EC, US$6.0 million; Government of Netherlands, US$6.1million; and the OPEC Fund, US$6.1 million. In addition, the Governmentof Italy will provide US$12.0 million in parallel financing.

54. Sector Background and Strategy. The Economic Recovery Program(ERP) launched by the Government of Tanzania (GOT) has led to a majorexpansion of output in agriculture and other sectors. However, progressunder the ERP is constrained because transport problems and fuel shortageshave prevented the increased production of export crops and the higherindustrial output from being fully translated into export earnings. IDAis supporting Government efforts to solve these problems through projectsfor rehabilitation of ports and roads, through a rail rehabilitationproject (recently appraised), and through the proposed petroleumrehabilitation project. The present petroleum distribution system isslow, unreliable, expensive and its deteriorated condition threatens theenvironment. Most oil products are distributed by road, at several timesthe equivalent rail cost. Rail transport of petroleum, when used, iscombined with general goods trains and hence is slow. Lack of investmentfunds by the private sector has led to significant deterioration ofphysical facilities such as depots, jetties and barges, and in mans casesretailers have had to cannibalize pumps and other equipment to keepcrucial installations in operation.

55. The Government's objective in the petroleum marketing sub-sectoris to improve the availability of petroleum products throughout thecountry, reduce the cost of supply and improve the efficiency of theprivate sector supply and distribution system. The strategy to achievethis is to reduce the cost of imported petroleum by improved purchasingarrangements, upgrade dilapidated distribution facilities, make -greateruse of the railways for bulk petroleum product transport, enhance theability of the private sector in management of the distribution system.and ensure a policy framework that would give sufficient incentives forthe petroleum products to be efficiently distributed to places where theyare needed. As the major policy measure to achieve this, Tanzania hasrecently adopted a petroleum pricing policy that will avoid subsidies,generate revenues for the national budget, send users clear signals oneconomic cost, and give incentives to private petroleum marketers torenovate their facilities while maintaining financial viability.

56. Government has made a number of improvements in petroleumprocurement practices. Petroleum products are now purchased competitivelyas a result of their inclusion in the Open General License window andthrough the OPEC Fund financing of imports. Crude oil for processing atthe refinery at Dar es Salaam is procured under a collateralized financingarrangement. GOT has agreed to arrange for consultants to study andrecommend improvements in the system of purchasing crude oil, thefinancing arrangements (currently linked to coffee exports) and therelated coffee marketing arrangements. The proposed project will address

- 21 -

the transport and distribution issues in the strategy, and will place aheavy emphasis on using private sector companies to achieve this. Theproject will be cofinanced by Denmark, the Netherlands, the EC, EIB andthe OPEC Fund. Italy will finance in parallel the rehabilitation of theoil refinery.

57. Rationale for IDA Involvement. The proposed project isconsistent with the Bank Group strategy for Tanzania, which gives priorityto rehabilitating and modernizing the existing critical infrastructure.Because the dilapidated condition of the petroleum industry has made thesupply of petroleum costly and unreliable, the rehabilitation of thepetroleum sub-sector is important to the success of the Government'sEconomic Recovery Program. IDA's involvement and support would act as acatalyst to attract private petroleum company investments and donorcofinancing. It would also ensure compatibility with low-cost options forthe transport of petroleum products to neighboring landlocked countries.

58. Project Objectives. The proposed project would improve theavailability of petroleum products throughout Tanzania by improving theefficiency and effectiveness of the petroleum industry in the country.This objective would be achieved by reducing transportation costs,modernizing and rehabilitating the supply and distribution network,strengthening the technical and management capacity of the relatedinstitutions and developing and implementing an appropriate petroleumpricing policy. Finally, improvements and strengthening of the storageand handling facilities would reduce current levels of oil pollution, andreduce the threat to the environment from spillage and leakages. Thespecific objectives of the project aret (i) to reduce the haulage cost ofpetroleum products; (ii) to improve the performance of the oil industry;(iii) to implement an appropriate petroleum pricing policy; (iv) toImprove national and transit petroleum trade; (v) to reduce oil pollutionand the threat to the environment; and (vi) to improve the technical andmanagerial skills and capability of petroleum industry personnel.

59. Project Description. The proposed project would improve thepetroleum companies' ability to provide services throughout Tanzania bymaking funds, especially foreign currency, available to the establishedoil companies and to TPDC for high priority investments. Theseinvestments would include: (i) rehabilitation of existing storage depotsand construction of nei depots for petroleum products; (ii) themodification of existing and construction of new railway loading andunloading facilities that will permit the use of dedicated "block" trains,which will carry only petroleum products; (iii) the installation of anoffshore loading facility and the construction of a new petroleum terminalat Tanga, which will enable Tanga to be used as a direct import point,thereby reducing handling and transport charges; (iv) the rehabilitationof existing jetty facilities and repairs to the existing 400-ton barge G..Lake Victoria; (v) acquisition of much needed equipment and materials,including 87 railway wagons geared to carry petroleum and LPG, ndequipment and spare parts to rehabilitate and modernize the existingretail outlets of the oil companies; and (vi) the provision of LPG fillingand marketing facilities. In addition to funds for investment projects,the proposed project would finance technical assistance and trainingdesigned to strengthen the project beneficiaries and implementingagencies. The funds for the investment projects would be lent through the

- 22 -

Tanzania Investment Bank ('IB). Because of its weak portfolio and highlevel of arrears, TIB is not creditworthy for Bank/IDA lending; however,its size and experience in similar lending makes it the best suitedfinancial institution in Tanzania to undertake this job. TIB willfunction as the administrator of the loan, and vill receive a one-time onepercent commission and a one percent service fee to cover the costsrelated to this. Government will accept the credit risk, and thebeneficiaries will bear the foreign exchange risk. The project would becarried out over seven years. The total cost of the project is estimatedat US$103.6 million, of which US$74.0 million would be in foreigncurrency. A breakdown of the costs and the financing plan is shown inSchedule A. Amounts and methods of procurement and of disbursements, andthe disbursement schedule are shown in Schedule B. A timetable of keyproject processing events and the status of Bank Group operations inTanzania are given in Schedules C and D respectively. A map is alsoattached. The Staff Appraisal Report, No. 8342-TA, dated December 13,1990 is attached.

60. Agreed Actions. Of the actions agreed to between the Governmentand IDA, the principal items includes (i) agreement on the principalfeatures of the petroleum product pricing policy and a system for thereview and adjustment of prices, as needed; (ii) that GOT will arrange forconsultants to study and recommend improvements in the system ofpurchasing crude oil, the financing arrangements (currently linked tocoffee exports), and the related coffee marketing arrangements; (iii)yearly (in September) review of project implementation, oil prices and theprice adjustment mechanism, and progress in the rehabilitation of TRC;(iv) the establishment and suitable staffing of a Railway CoordinationCommittee; and (v) that GOT will either conclude agreements with EIB andEC by Dec. 31, 1991 for the financing of rail tank wagons and new depotfacilities, or ensure that adequate funds for these are available fromother sources on satisfactory terms and conditions. There are threeconditions of effectiveness: (i) that Government will sign a subsidiaryagreement with TIB and that TIB will sign subsidiary financing agreementswith at least two oil companies; (ii) that contracts between TPDC and TCRand TAZAMA, satisfactory to IDA, will be executed on the use, maintenance,operations and management of railway tank wagons owned by TPDC; and (iii)the appointment of an experienced Project Manager. There are twoconditions of disbursement: (i) on disbursement of funds for the Tangabulk oil terminal, that the agreement between GOT and the OPEC Fund hasbeen executed, and that detailed engineering and construction costs,acceptable to IDA, have been provided for work under this component; and(ii) on the disbursement of funds by TIB to the oil companies, that asatisfactory financing plan for the investments to be financed under theproject by each oil company is in place prior to respective di oursements.

61. Project Benefits and Risks. Availability of petroleum productsin the interior of Tanzania must be improved substantially for the ERP tobe sustained. The proposed project is the least-cost option for makingpetroleum products reliably available throughout the country.Improvements in household petroleum fuel supply (e.g. LPG) will relievefuelwood pressure equivalent to 35,000 hectares of natural woodlands whichwould otherwise be required to supply equivalent energy on a sustainedbasis over a 20 year re-generation cycle. Principal benefits of theproject are the cost savings to be derived from: (a) direct import ofproducts at Tanga instead of transhipment by road; (b) bulk transport ofpetroleum by rail in properly managed block trains instead of piece-meal

- 23 -

movement mainly by road; and (c) sustained Involvement a.d improvedefficiency of the private companies in the petroleum sector. An importantbenefit of the project is to minimize and contain damage to theenvironment, which is currently threatened by the deterioratec conditionof transport, supply and distribution network. The internal economic rateof return (ERR) for the rehabilitation project is estimated at about 26percent, excluding benefits from transit trade. For the Tanga petroleumterminal, the ERU is estimated at 15 percent.

62. Because project preparation proceeded with the benefit ofdetailed consultation with and between Government, oil marketing companiesand railways officials, the risk of delays through misunder,tandingproject objectives and components has been min4mized. The risks ofprocurement delays are limited because the goods to be acquired are eitherreplacement parts or equipment of standard specification. Risks thatdelays in the 'parallel-financed item (the refinery modification) willdelay implementation of some of the IDA and co-financed components will beminimized by close monitoring by the project management team in MWEM.

63. There could be some delay in the implementation of certaincomponents due to insufficient coordination among the various implementingagencies (such as the petroleum marketing companies and TPDC) and otherGovernment agencies such as the railway parastatals. A projectsupervisory comittee is being established with representation fromImplementing agencies, and a full-time project implementation team headedby an experienced project manager within MWEM would be providcC toovercome this problem and monitor the progress of the projectcontinuously. Technical assistance funds are provided to hire, ifnecessary from outside Tanzania, the Project Manager and a PetroleumProducts Transport Specialist with suitable experience.

64. Recommendation. I am satisfied that the proposed Credit wouldcomply with the Articles of Agreement of Association and recomiend thatthe Executive Directors approve the proposed Credit.

Barber B. ConablePresident

AttachmentsWashington, D. C.

December 13, 1990

- 24 -

Scedaule ATUIA~~~~~~~

PETROLI SECTOxR U LIST PROJECT

ESTIMATED COSTS A1D FINANCIG PUN

Netbuated Costs:X of

Local Foreigm Total Total--- (USS million) ------

Existing Oil Industry FacilitiesDepot Rehabilitation 10.3 13.3 23.6 22.8Other facilities 2.6 10.8 13.4 12.9

New Oil Industry FacilitiesNew Depots 6.5 14.5 21.0 20.3Joint Industry Components 0.2 10.1 10.3 9.9Other New Facilities 1.5 7.4 8.9 8.6

Technical Assistance 2.0 5.0 7.0 6.8Total Base Cost 23.1 61.1 84.2 81.3

ContingenciesPhysical Contingencies 3.8 6.5 10.3 9.9Price Contingencies 2.7 6.4 9.1 8.8

Total Project Costs v 2L2 l

11 (a) Where local duties and taxes are applicable, they will be borne by thebeneficiaries and paid in local currency. WNM would recommend to Government todefer the payment of taxes until the project facilities are fully operative; and(b) all beneficiaries are operating entities and interest during constructionwill be financed from operating income and will not be capitalized.

Financinx Plant S ofLocal Foreign Total Total

<-- (US$ million)- __-IDA - 44.0 44.0 42.5DANIDA - 2.5 2.5 2.4RIB * - 8.9 8.9 8.6EC * - 6.0 6.0 5.8Government of Netherlands - 6.5 6.5 6.3OPEC Fund - 6.1 6.1 5.8TPDC/Government/Oil Companies 29.6 - 29.6 28.6Total ..2-A 2i& JaLl JQsQ

- 25 -

Schedule BPage 1 of 2

PETROLEUM SECTOR RUAUILITATION PROJECT

PROCUREMENT MNEOD AND DISBDSDMENNS

Procurement MethodProject Element ICB LIs Other Total

<------(Us1$ million)---------->Storage Tanks Materials 5.3 5.3

(5.3) (5.3)Existing Depot Facilities 6.0 6.0 12.0

(6.0) (6.0)3 (12.0)Existing Other Facilities 2.4 2.4

(2.4)8 (2.4)Spares and Consumables 7.32 2.0 9.3

(7-3) (2.0)' (9.3)New Joint Depots 3.1 2.5 12.9 18.5

(3.1) (0.5) (3.6)Transport Vehicles 3.3 3.3

(3.3) (3.3)LPG Marketing (New) 5.0 5.0Tanga Petroleum Terminal 4.3 4.3

(3.1) (3.1)Victoria Lake Barge Repairs 1.0 1.0Victoria Lake Jetties 1.9 1.9Rail Tank Wagons 6.0 6.0T.A. & Project Management 5.0w 5.0

(5.0) (5.0)Total 4 L. LA aLL. 1L%

(20.8) (7.3) (15.9) (44.0)

* Amounts financed by IDA are in parentheses.

1 Procurement for the parallel financed components would be inaccordance with the guidelines of the financing institutions.

2 Items are intended for equipment installed at about 350 retailoutlets, operated by five different oil companies. Per theirestablished corporate procurement guidelines, they rely onmore than one vendor for price competitiveness.Proprietary spare parts and components for existing equipment.

4 Including contingencies.' Consultancy Guidelines

- 26 -

Schedule aPage 2 of 2

DISBURSEMENTS

I of expend.(US$ million) to be financed

Equipment and Materials

Rehabilitation of facilities (a) 18.8 10OZ of foreignexpend.

Tanga petroleum terminal (b) 4.5 10OZ of foreignexpend.

Spare parts & consumables 7.3 1002 of foreignexpend.

Studies and project management 3.8 10O of foreignexpend.

Office Equipment 0.7 MWEH: 1002 of expen.TIB: 1002 of foreign,802 of local expend.

Training 0.5 1002 of expend.

Unallocated 8.4

TOTAL: 44.0

(a) Rehabilitation of all facilities (excluding Tanga PetroleumTerminal and including new depot at Mpanda).

(b) Tanga offshore facilities and new terminal.

Estimated IDA Disbursementes

IDA Fiscal Year<------------------US$ million------------->FY9M FY92 FY93 FY94 FY95 FY9C6 Y97

Annual 1.3 3.2 9.0 10.5 11.0 7.8 1.2Cumulative 1.3 4.5 13.5 24.0 35.0 42.8 44.0

- 27 -

Schedule C

TANZLAMPEITRILKU SECTOX REA TILIThUON PROJNCT

Timetable for Key Processing Events:

a. Time taken to prepare 20 months

b. Project prepared by MWEHIPWG/ConsultantsIIDA

c. First IDA mission November 1987

d. Departure of AppraisalMission May 1989

e. Negotiations May 1990

f. Planned Date of Effectiveness April 1991

- 28 -Schedule D

Status Of Bank Sroue Ocerations In TANZANIA Page 1 of 3PFO8R2S - Susmary Statement Of Loins and IDA Credits(LOA data as of 10130/90 - NIS data as of 11/lOf901

Auaunt in US1 Billion(less cancellationsl

Lzan or Fiscil -Undis- Closinocredit No. Year SorroNer Purcose ank IdA buried Date

---- __- ------ ---- - --

Credits

*Z Creditsfsl closed 781.57

C Ol50-TAN Vs90 TANZANIA GRAIN STORAGE & IIL. 43.00: 20.52 12/31/90(fi C10560-TAN 1981 TANZANIA EDUCATION VII 25.00 1.67 12/31/90(R)C 12290-TAN 1982 TANZANIA FORESTRM -II 12.00 4.08 12131190f1iC13700-TAN 1963 TANZANIA NIUF!NDI PULP&PAPER 18.00 2.&0 12/31/901R1C137;10-TAN 1983 TANZANIA COAL BNS.CREDIT 6.30 .17 0630/90iRC10S0-TAN 1984 TANtiANIA POWER IV 35.00 2.07 12/31/901R)C1536O-TAN 1985 TANZANIA PORTS R8AH. 27.00 2.82 06130190C16040-TAN 1985 TANZANIA PETROSECTOR.T.A 8.00 4.08 0630t911R)CL6870-TAN 1986 TANZANIA POWER REHABJ.ENERY 40.00 5.77 12/31/90C16980-TAN 1186 TANZANIA SIXTH inY. (RENAl) 50.00 38.27 06/30192C18100-TAN 1987 TANZANIA TELEC.I1 23.00 8.10 06/30191C18?10-TAN 1988 TANZANIA AMLXPORTS RV. I 30.00 29.29 06/30196C9690-TANlS 1989 TANZANIA IND.&TRADE ADJUS.CR. 135.00 76.20 12/31/90Cl0700-TAN 1989 TANZANIA NATL.A6.& LIY.R£S 8.30 7.91 03/31197C19?40-TAN 1989 TANZANIA AGRIC. EXT. 18.40 16.92 03/31/97C20500-TAN 1989 TANZANIA TR2E CROPS 25.10 25.50 @6/30/96CI9j92-TANMSI 190 TANZANIA IND.&TRACE ADJUS.CR. 10.30 11.94 11106/91fR)