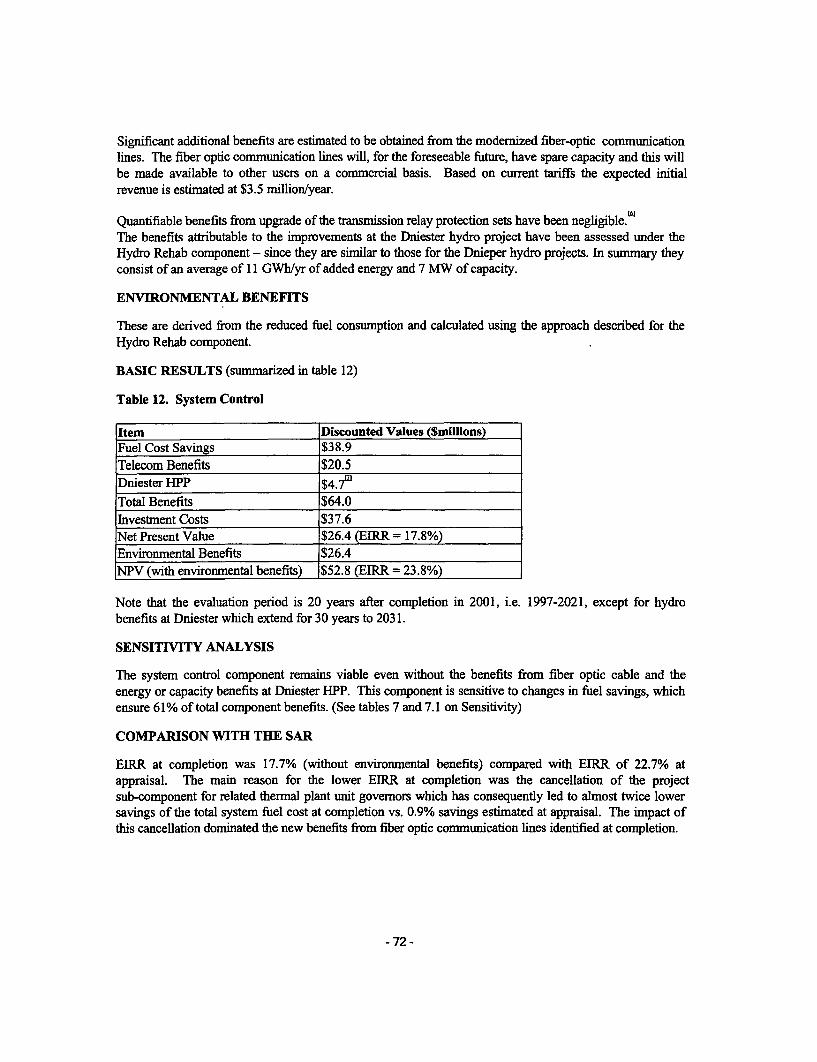

world bank document€¦ · · 2016-07-17hydropower rehabilitation and system control project...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 24947

IMPLEMENTATION COMPLETION REPORT(CPL-38650; TF-20272)

ONA

LOAN

IN THE AMOUNT OF US$ 114 MILLION

TO

UKRAINE

FOR A

HYDROPOWER REHABILITATION AND SYSTEM CONTROL PROJECT

12/24/2002

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of November 1, 2002)

Currency Unit = 1 Hrivnya = 100 kopeksUAH 1 = US$ 0.19US$ 1 = 5.33 UAH

FISCAL YEARJanuary 1 December 31

ABBREVIATIONS AND ACRONYMSCAS Country Assistance StrategyCFP Coal-Fired PlantCHF Swiss FrancCIDA Canadian Agency for International DevelopmentDHE DniprohydroenergoEBRD European Bank for Reconstruction and DevelopmentEIRR Economic Internal Rate of ReturnEU European UnionFSU Former Soviet UnionGDP Gross Domestic ProductGEF Global Environment FacilityGoU Government of UkraineGWh Gigawatt hourHPP Hydropower PlantIAS Intemational Accounting StandardsICR Implementation Completion ReportIDC Interest During ConstructionkWh Kilowatt hourMW Megawatt (I0^6 W)MUV Manufacturing Unit ValueNDC National Dispatch CenterNERC National Electricity Regulatory CommissionNPP Nuclear Power PlantNPV Net Present ValueO&M Operations and MaintenancePPI Producer Price IndexPSP Pump Storage PlantSAR Staff Appraisal ReportSCADA Supervisory Control and Data SystemTA Technical AssistanceTWh Terawatt hour (1012 Wh)UAH Ukrainian Hrivnya (1 Hrivnya = 100 kopeks)UE UkrenergoUPS Ukrainian Power SystemVAT Value-Added Tax

Vice President: Johannes F. LinnCountry Manager/Director: Luca Barbone

Sector Manager/Director: Hossein RazaviTask Team Leader/Task Manager: Nikolay Nikolov

UKRAINEHYDROPOWER REHAB

CONTENTS

Page No.1. Project Data 12. Principal Performance Ratings 13. Assessment of Development Objective and Design, and of Quality at Entry 24. Achievement of Objective and Outputs 95. Major Factors Affecting Implementation and Outcome 166. Sustainability 197. Bank and Borrower Performance 208. Lessons Learned 249. Partner Comments 2610. Additional Information 40Annex 1. Key Performance Indicators/Log Frame Matrix 56Annex 2. Project Costs and Financing 58Annex 3. Economic Costs and Benefits 60Annex 4. Bank Inputs 111Annex 5. Ratings for Achievement of Objectives/Outputs of Components 113Annex 6. Ratings of Bank and Borrower Performance 114Annex 7. List of Supporting Documents 115Annex 8. Summaries of project completion reports from the DHE and UE 116

Map IBRD 32185

Project ID: P038820 Project Name: HYDROPOWER REHAB ANDSYSTEM CONTROL

Team Leader: Nikolay Nikolov TL Unit: ECSIE

ICR Type: Core ICR Report Date: December 24, 2002

1. Project Data

Name: HYDROPOWER REHAB AND SYSTEM L/C/TF Nzmber: CPL-38650; TF-20272CONTROL

Country/Department: UKRAINE Region. Europe and CentralAsia Region

Sector/subsector: Power (100%)

KEY DATESOriginal Revised/Actual

PCD. 06/24/1994 Effective: 12/27/1995 05/24/1996Appraisal: 09/14/1994 MTR: 09/30/1997 11/11/1997Approval: 04/11/1995 Closing: 12/31/2000 06/30/2002

Borrower/Inmplementing Agency: GOVT OF UKRAINE/DNIPROHYDROENERGO & NATL. DISPATCH CTR.Other Partners: Governments of Canada, Norway, Switzerland

STAFF Current At AppraisalVice President: Johanes Linn Wilfried ThalwitzCountry Manager: Luca Barbone Basil KavalskySector Manager: Hossein Razavi Dominique LallementTeam Leader at ICR Nikolay Nikolov Laszlo LoveiICR Primary Author: Nikolay Nikolov with

contributions from DennisCreamer - consultant (economicanalysis); Simos Kamchis -consultant (financial analysis);Yun Miroshnichenko; YolandaL. Gedse; Maria Koreniako

2. Principal Performance Ratings

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HL=Highly Likely, L=Likely, UN=Unlikely, HUN=HighlyUnlikely, HU=Highly Unsatisfactory, H=High, SU=Substantial, M=Modest, N=Negligible)

Outcome: S

Sustarnabilety. L

Institutional Development Impact: M

Bank Performance: S

Borrower Performance: S

QAG (if available) ICRQuality at Entry:

Project at Risk at Any Time: Yes

3. Assessment of Development Objective and Design, and of Quality at Entry

3.1 Original Objective:Background

The Ukrainian Power System (UPS) was developed and operated as a part of the integrated power systemof the FSU. The efficient performance of the system was severely affected by (i) a vertical state-ownedmonopoly structure; (ii) high energy intensity; (iii) limited domestic energy endowments, and (iv) a deepeconomic and institutional crisis which followed the disintegration of the FSU in 1991.

The separation of the Ukrainian Power System from the Russian power system revealed serious structuraland functional weaknesses which affected the overall system operation, security, reliability and quality ofpower supply. These weaknesses concemed the insufficient amount of load-following generation capacity,capable of maintaining flexible production schedule and providing frequency regulation, i.e., the lack ofplants which operate in the mid and peak sections of the load duration curve. This critical function wasprovided by the hydropower plants on the Dnieper and Dniester rivers. Most of the Ukraine's thermalplants were base load, especially the coal-fired ones. Some larger gas units were more flexible, but weresuffering from difficulties in fuel supply as the Ukrainian power sector had difficulties paying for gasimports.

To address these issues, the GoU adopted a two-pronged strategy of institutional reforms and investmentsin priority areas. The development of the Government's energy strategy was supported by the Bank since1992 through technical assistance and an Energy Sector Review (Report No. 11646-UA). During thisprocess, the Bank reached an agreement with the Government and other international donors to enhancesupport to power generation and gas transmission and distribution as sectors in which the Bank could makea significant difference in Ukraine. In this context, the Government, assisted by the Bank and other donors,started the preparation of the Hydropower Rehabilitation and System Control Project. A comprehensivefeasibility study outlined the overall rehabilitation needs of the Dnieper cascade. In view of the large scopeof identified rehabilitation works, the project was designed to include as a first phase a portion of theneeded overall hydropower plants rehabilitation. The remaining rehabilitation works at the Dniepercascade were to be pursued in the context of the outcome of the first rehabilitation phase, the furtheradvancement of the Governments priorities in the power sector and the continuation of a project enablingframework.

The project aimed at addressing some of the important priorities in the Ukrainian power system:rehabilitation of hydropower plants meant maintaining the most flexible generation plants at their maximumproductive levels. The project also provided a moderate leverage for implementation of broader sectorreforms, especially in its preparatory stage. The early stage of the project's implementation was affectedby a severe economic and financial crisis which caused a precipitous decline of electricity payments.Nevertheless, through sustained efforts of the Bank, the GoU, the project beneficiaries Dniprohydroenergoand Ukrenergo, and with support from the governments of Canada, Norway and Switzerland, the projectwas successfully implemented, within an unbundled power sector with much improved financial discipline,advancing privatization of electricity companies and a developed regulatory framework.

Obiectives

The project had the following objectives: (i) improve the efficiency, reliability, safety and environmentalperformance of hydropower plants - this objective included enhancement of the dam safety monitoringsystem, improvement of the water quality of the Dnieper River through reduction of oil leakages into the

- 2-

river to minimal level due to installation of new ecologically safe turbines, and improvement of themanagement of the multi-purpose Dnieper reservoirs, (ii) increase hydropower generation capacity, whichimplied increasing peak capacity and power generation in peak time zone; (iii) improve the quality ofelectricity supply by upgrading load and frequency control; and (iv) reduce fuel costs by facilitating theeconomic dispatch of generating units.

The objectives of the project were clear and important for sector development. They were responsive to thepriorities of the least cost investment plan for the power sector which included the rehabilitation of thehydropower plants. The project objectives were also supportive of the Bank's overall strategy to facilitateUkraine's effort to carry out structural reforms and to promote efficiency investments in high prioritysectors such as energy in order to complete the transition to a market economy and to accelerate economicgrowth. The project was designed to respond to the needs of the power sector in a critical period ofUkraine's history, shortly after the country gained independence and suffered a deep economic crisis at thesame time.

The project was quite demanding on the two implementing agencies (Dniprohydroenergo and NationalDispatch Center/Ukrenergo) because of its broad institutional, geographical and technical scope, the relatedcomplexity and risks, and the beneficiaries' limited experience in dealing with projects financed byinternational institutions. In this context, the good technical expertise of the implementing agencies wasconsidered an important counterbalancing factor.

Complex institutional and organizational aspects

The rehabilitation of the hydropower plants (one of the two main investment components of the project),carried out by Dniprohydroenergo, required coordination of the work of eight large power plants on thereservoirs of the Dnieper cascade with a total capacity of 3,799 MW, 18 design institutes, more than 100equipment manufacturers, over 30 installation and commissioning companies, and about 100 othercontractors. The upgrade of the system control and dispatch (the other investment component of theproject) was carried out by an entity - National Dispatch Center (NDC) - which, during the projectimplementation period, was subject to more institutional changes than any other entity in the electricitysector. NDC has endured a series of major reorganizations, starting up just as a dispatch center, then beinga part of the company providing transmission, dispatch and market operation services, and ending up as apart of the Ukraine's unified transmission and dispatch company (Ukrenergo).

Broad geographical scope

The dams of the Dnieper cascade are some of the world's longest, located in six of the most industrializedand heavily populated regions of Ukraine along the basin of the third largest river in Europe. The upgradeof the system control and dispatch encompassed works throughout the country.

Complex technical aspects.

Rehabilitation on such a large scale was not carried out before in Ulraine. In view of the importance of theDnieper cascade for the power system load and frequency regulation, the turbines and generators had to berehabilitated without discontinuing the operation of the remaining equipment at the power plants.Maintaining normal operational parameters of the power plants even during rehabilitation of individualgeneration units was a pioneering approach in Ukraine.

- 3-

Risks

Low cash collections in the electricity sector represented huge financial risk to the project. The need torehabilitate turbines and generators while continuing to generate posed difficult scheduling requirementsand continuously risked delaying the project. The requirement to operate as many units as possible duringthe spring flood seasons put significant pressure on the rehabilitation works as well.

3.2 Revised Objective:The objectives of the project were not revised.

3.3 Original Components.The achievement of the project objectives was ensured by the adequate design of the original projectcomponents, listed below:

(i) Rehabilitation of hydropower plants on the Dnieper cascade;(ii) Installation of a dam safety monitoring system at the main reservoirs on the Dnieper river;(iii) Upgrade of communications, dispatch, and system control;(iv) Technical assistance.

The first two components, implemented by Dniprohydroenergo, supported the first two project objectives ofimproving the efficiency, reliability, safety and environmental performance of hydropower plants; andincreasing hydropower generation capacity. The third component, implemented by NDC/Ukrenergo,supported the other two project objectives (improving the quality of electricity supply by upgrading loadand frequency control; and reducing fuel costs by facilitating economic dispatch of generating units).

Although demanding, the project design capitalized on the beneficiaries' good technical and engineeringcapabilities.

Key aspects of the project components are presented below:

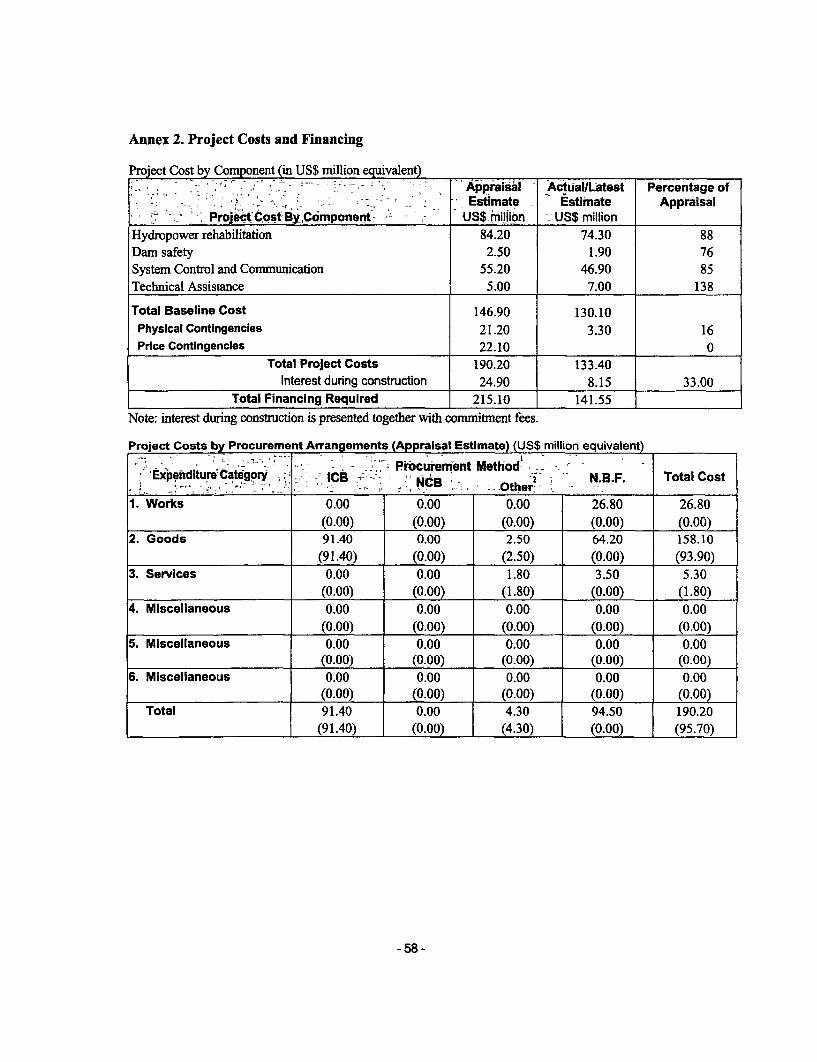

(a) Rehabilitation of hydropower plants on the Dnieper cascade.Cost: US$ 84.2 million.

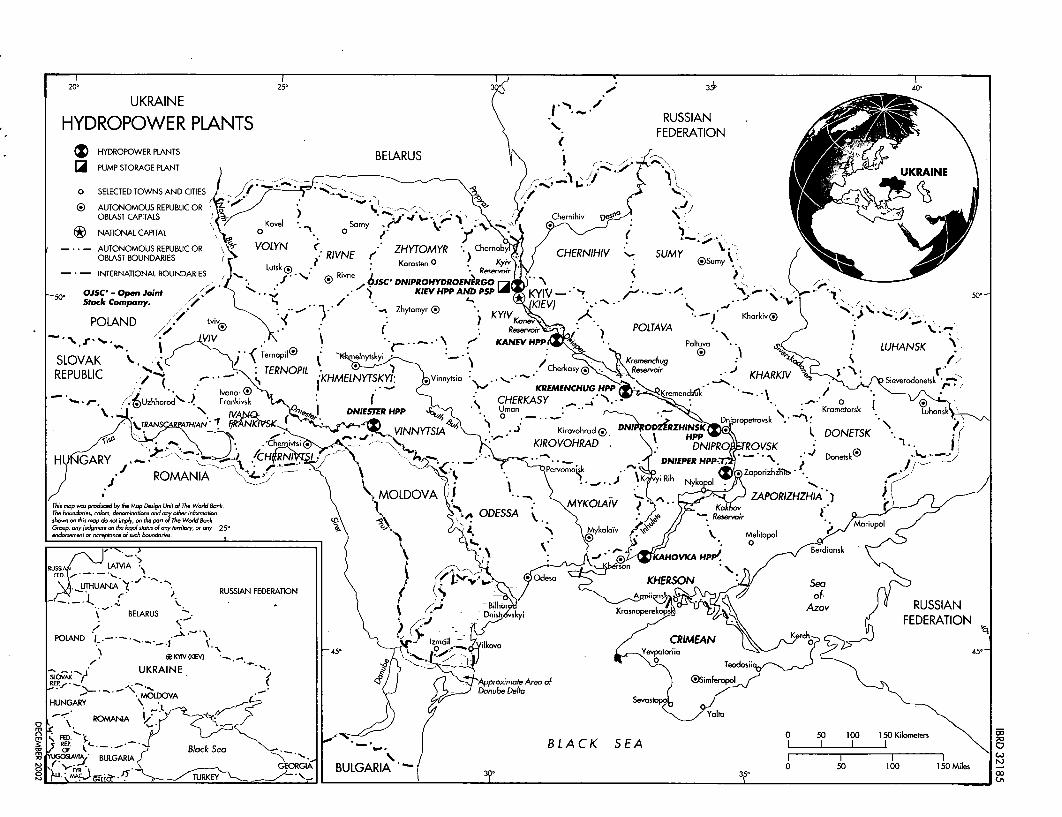

This component included rehabilitation of the eight HPPs on the Dnieper River. (See attached map). Therehabilitation of the system control and monitoring at HPPs on the Dnieper cascade was also included.

The component addressed critical performance aspects of aging HPPs such as derating of the units, lowefficiency and availability. The oldest HPP, Dnieper-l (Dniproges-l) was built in 1932 and reconstructedin 1947, five of the plants were more than 30 years old and the other two were more than 20 years old.

-4-

(b) Installation of a dam safety monitoring system at the main reservoirs of the Dnieper River (Kiev,Kanev, Kremenchug, Dniprodzerzhinsk, Dnieper, Kakhovka).Cost: US$ 2.5 million.

This component aimed at rehabilitating the existing dam monitoring system in order to improve the safetyof about 100 km of dams and dykes for the multipurpose reservoirs on the Dnieper river. The reservoirdams have low heads and long embankmnents with dykes protecting the surrounding land from floods.

(c) Upgrade of communication, dispatch, and system control.Cost: US$ 55.2 million.

This component included an upgrade of the following key elements of the UPS:

(i) communications systems;(ii) frequency regulation, dispatch and control systems;(iii) relay protection devices of the main transmission network.

The rehabilitation of the system control and monitoring at the Dniester HPP was also included.

This component aimed at overcoming the deficiencies across the UPS that compromised the reliability,quality and security of electricity supply. The poor frequency regulation represented an increased risk foroperation of the nuclear power plants, since their protection system would trip them off if the systemfrequency were to go beyond certain range.

(d) Technical assistance.Cost: US$ 5.0 million.

Building on a lesson learned from an earlier World Bank - financed Institution Building Project in Ukraine(Loan 3614-UA), a technical assistance (TA) component was included in the project to compensate for thebeneficiaries' inexperience in implementing projects with donor financing and international procurement.This was to be done through supporting technical services for preliminary engineering design, preparationof technical specifications and tender documents, conducting international tendering, contract negotiationsand administration, and helping in project monitoring and reporting. Training by equipment suppliers wasenvisaged in the tender documents. Training in management and procurement was also provided by Bankstaff.

In addition, in view of the importance of the multi-purpose use of the reservoirs on the Dnieper river, thetechnical assistance component included a review of the procedures in managing the river basin'sreservoirs.

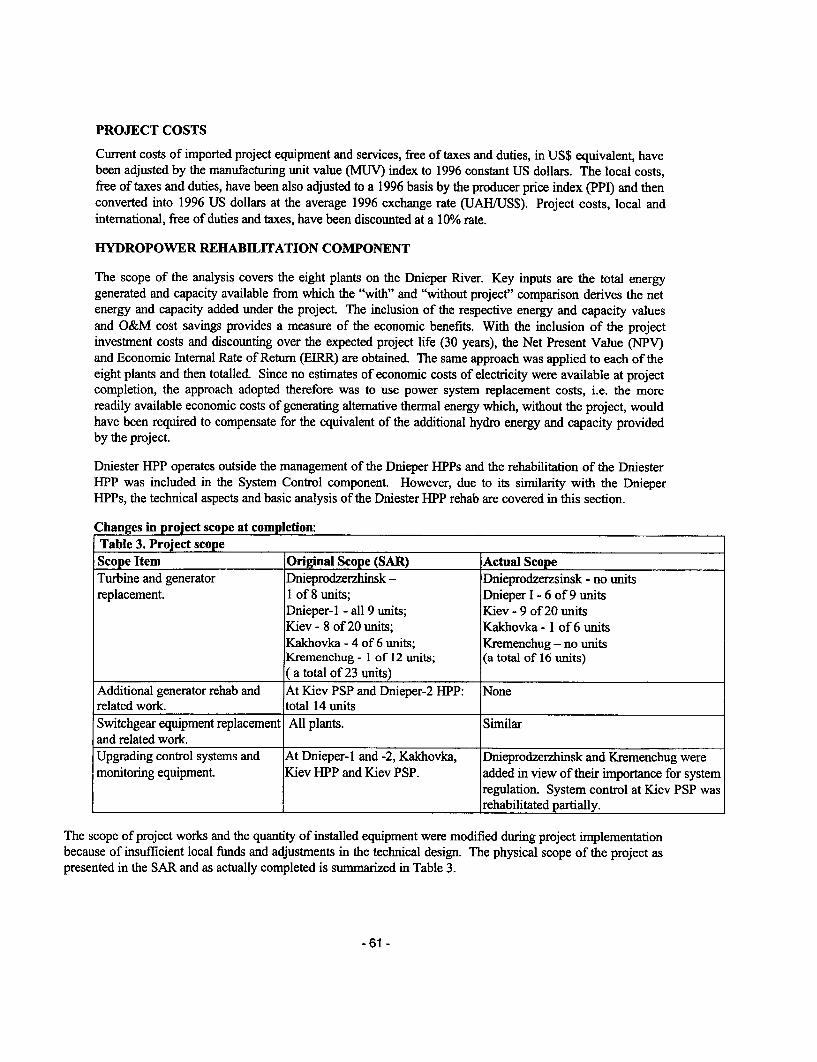

3.4 Revised Components:The number and the type of the components were not revised, but the schedules and physical quantities ofsome of the components were modified. The main revisions concemed the number of turbines andgenerators subject to rehabilitation which was financed from Dniprohydroenergo's revenues rather thanfrom the IBRD loan.

- 5-

The schedule for the installation of dam safety monitoring system experienced major delays as a result ofthe desire by DHE to have this system delivered by a local contractor and financed from internal funds.However, it turned out that the local contractor at the end was not able to deliver the system withsatisfactory technical performance. Consequently, DHE then decided to procure the system internationallyand finance it from the IBRD loan, but much time had been lost in the meantime. As a result, dam safetymonitoring equipment was installed only at the most critical and longest Kiev dam of the cascade.

The length of the fiber optic conmmunications lines was slightly increased together with the scope ofequipment for hydro generators to better respond to the evolving system needs. The scope of systemcontrol and monitoring equipment was significantly increased and installed on two additional plants tofully accommodate the needs of the entire Dnieper cascade. Such equipment was additionally installed atKremenchug and Dneprodzerzhinsk HPPs in view of their importance for regulating operations of theplants in the cascade. A component for installing thermal power plants (TPPs) governors (technicaldevices which regulate the output of the TPPs) was replaced by a relevant study to respond to the reducedincentives in the power market for installing such governors. The scope and timing of the TA wereadjusted to the overall changes in scope and timing of the project works.

Turbine and Generator Rehabilitation

(a) The original project scope foresaw the rehabilitation of 23 turbines and 37 generators. Upon beginningof the project works, larger than expected wear and tear of the generating units called for a greater level oflocal works per each unit. Consequently, the number of turbines to be rehabilitated was reduced from 23 to22 in the early stage of the project

(b) In addition, the deterioration of electricity payments continued from 1998 to early 2000 and affectedlocal project financing. It was therefore agreed to further scale down the turbine/generator rehabilitationworks, which critically depended on local funds. Thus, the number of turbines and generators to berehabilitated was reduced from 22 turbines and 37 generators to 13 and 15 respectively. At the end of theproject, DHE had managed to exceed this target, rehabilitating 16 pairs of turbines and generators.

Dam Safety Monitoring System

(c) In the beginning of the project, locally financed national manufacturers could not ensure the requiredspecifications of the dam monitoring equipment. It was then decided to launch an international competitivetender for a pilot contract for supply and installation of such equipment for only the Kiev HPP. Theexperience gained from this pilot contract was supposed to be used in procuring monitoring equipment forthe other dams of the cascade. The unexpected replacement of the local supplier with an intemational onedelayed the implementation schedule of the dam safety component. Consequently, the scope of installingmonitoring equipment was reduced from 100 km along all HPPs to 50 km at Kiev HPP, which is mostcritically located at the beginning of the cascade. The experience from preparing tender documents forKiev HPP was used for the design and technical specifications of the dam safety upgrade at the remainingplants.

Control and Monitoring System

(d) During the installation of the system control and monitoring equipment at Dnieper HPPs, additionalpossibilities were identified for a better adaptation of the equipment to the needs of the cascade. Therefore,the original scope of equipment was significantly expanded with modified software, electrical protection

-6-

systems, metering equipment and spare parts, and included two more plants -- Kremenchug andDneprodzerzhinsk - in view of the importance of their regulatory capacity for the entire cascade. At thesame time, system controls at Kiev PSP and Dnieper HPP-2 were rehabilitated partially in response to thespecific needs at these plants.

(e) One hundred and sixty km of fiber optic communications line were laid in addition to the original scopeof 1,000 km in order to connect the Central and Western communications networks of the UPS.

Auxiliary Equipment

(f) The quantity of the equipment for hydro generators was also slightly increased.

(g) The Ukrenergo's component for upgrade of frequency regulation, dispatch and system control includedoriginally a sub-component for upgrading the governors of the generation units of the thermal power plants.This activity was designed to improve the capability of the power system to regulate frequency. However,this sub-component was canceled due to (i) lack of financial incentives for the thermal plants to participatein load frequency regulation, since payments for this service were not recognized by the electricity market;(ii) the requirement for the plants to finance local costs associated with insta1ling new governors, while theplants lacked such funds due to non-payments in the electricity market; (iii) the status of the plants asindependent legal entities, which hampered the management of this project sub-component outside thestructure of the implementing agency Ukrenergo; (iv) the unique water technology of the governors, notsupported by mranufacturers outside the former Soviet Union; (v) physical ware-and-tear of the thermalgenerators and the auxiliary TPP equipment together with outdated boiler automation called for muchlarger investments than expected.

(h) The Bank proposed instead, that a study on the automatic frequency regulation by the thermal powerplants be carried out in order to partially compensate for the cancellation of the sub-component forinstalling governors at these plants. The findings were used by the Ministry of Fuel and Energy as a basisfor preparing official guidelines for providing economic incentives to the thermal power plants involved inautomatic frequency regulation.

Audits and Technical Assistance

(i) The scope and timing of the technical assistance were modified to follow the changes in the actual scopeand timing of the project work. In addition, in view of the insufficient local funds, the project beneficiaries,with the Bank's agreement, chose to use more than half of the technical assistance funds from the Bank tocover the cost of. annual audits under the project. Technical assistance from the Canadian and Swissgovernments compensated for the reduction of the Bank's TA funds as a result of the audit fundingarrangements.

3.5 Quality at Entry:Quality at entry is judged to be satisfactory because the project objectives were consistent with (i) thegovernment priorities; (ii) the CAS, and (iii) the Bank's safeguard policies. In addition, the projectcomponents were designed to enable the achievement of the project objectives.

The project was consistent with the Government's strategy of rationalizing energy use throughrehabilitating hydro and thermal power plants, increasing reliance on renewable energy, and improvingsafety of the power system within the context of overall sector restructuring.

-7-

Bank sector work was used in the project preparation. In addition, the project was also responsive to theBank's strategy to promote efficiency improvements and adapt the energy utilities to the requirements of amarket economy. The project objectives were clearly outlined, and although demanding, were achievable inthe context of the counterparts' implementation capacity and commnitment for results. The project wasdesigned to respond to the priorities of the power sector and the funding arrangements were commensuratewith the project scope and needs. Project conditionality focused on ensuring proper structure andoperations of the implementing agencies in terms of consolidation of the Dnieper HPPs into a single jointstock company, transfer of the ownership of the regional dispatch centers to the National Dispatch Center,establishment of Project Implementation Units, signing adequate agreements for electricity sales andcontracts with strategic domestic turbine and generator manufacturers, observance of proper financialreporting and auditing standards.

The Bank ensured that the Ministry of Energy and the implementing agencies were actively involved in therelevant sector work and feasibility studies. The technical, financial, economic and environmental aspectsof the project were thoroughly assessed. Sensitivity of project sustainability to cost overruns, decline ofeconomic value of electricity and fuel savings was assessed as well.

Readiness for implementation was also analyzed in detail: the implementation capacity of the projectbeneficiaries was reviewed along with the manufacturing potential of the local suppliers, critical to theproject. On the basis of this analysis, technical assistance was envisaged to provide support in the areas ofengineering, procurement and project management. The engineering design was based on detailedfeasibility studies. The project performance indicators were designed to ensure adequate monitoring ofprogress towards achieving project objectives in terms of increasing generating capacity, improvingefficiency and frequency, reducing oil leakages and enhancing dam safety. Major risks related to pricingand non-payments were addressed through relevant loan conditions, political risk of reversal of reforms wasalso outlined.

In compliance with the Bank's safeguard policies, an environmental analysis was carried out and noimplications for intemational waterways were identified. Although the former Operational ManualStatement (OMS) 3.80 on dam safety safeguards was applicable only to the construction of new dams, andnot to the already existing dams included in the project at the time of appraisal, relevant safeguardmeasures, required under the current more rigorous safeguard policies, were actually designed andimplemented in an effort to bring more dam safety benefits to the project company Dniprohydroenergo.

Most of the assumptions made during project preparation were reasonable with the notable exception ofthose related to the timely improvement of the payment collections in the sector and the subsequentimprovement of the financial situation of the project implementing agencies. Non-payments persisted untilearly 2000 when the govemment initiated efficient measures to resolve this issue. These measurescoincided with the actual beginning of the economic recovery, which was forecasted at appraisal to beginmuch earlier in 1997.

In addition, the electricity demand forecast and the related least-cost development program were moreoptimistic at appraisal than their revaluation towards the project's end in 2001. Nevertheless, the finaloutcome was overall satisfactory.

-8-

4. Achievement of Objective and Outputs

4.1 Outcome/achievement of objective*Summary assessment of outcome

The overall outcome of the project is rated as satisfactory. As noted in the following sections, allenvisioned objectives were achieved, although with delays, and on occasion, on a reduced scale. Theproject objectives are in line with the current CAS objectives to attain job-creating sustainable economicgrowth, solve enviromnental issues in the energy sector and move Ukraine closer to the European Union'sstandards, fostering environmentally sustainable development. The development impact has been alsosatisfactory since the two project components brought desired quality, efficiency, safety and environmentalbenefits to the entire power system, although within the smaller scope of turbine/generator rehabilitationworks at commensurate lower total costs. The assessment was facilitated by the performance indicators inthe Staff Appraisal Report (SAR).

Achievement of objectives

Achievement of objective (a) improve the efficiency, safety, and environmental performance of thehydropower plants:

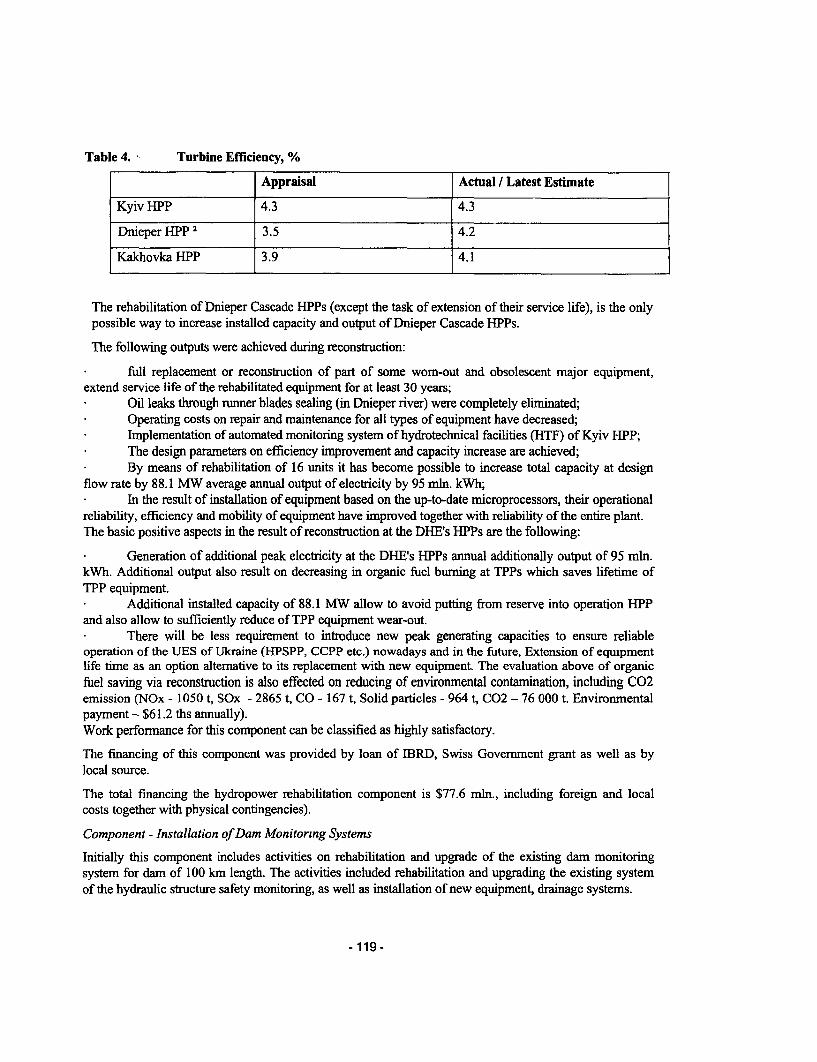

Efficiency of the hydropower plants:The nominal target efficiency parameters have been achieved for all rehabilitated units at the hydropowerplants. (See Annex 1)

Safety of the hydropower plants:The installation of a dam safety monitoring system at the Kiev reservoir dam, situated upstream at the headof the Dnieper cascade, has improved the safety and reliability of the Kiev reservoir and the downstreamreservoirs, all situated along very densely populated and industrialized areas.

In addition, the installation of electrical protection devices and microprocessor-based control systems forturbine/generators units and entire plants has contributed to improved the safety of equipment maintenanceand operation.

Environmental performance of the hydropower plants:Environmental improvements have been also enhanced by upgrading the dam safety instrumentation atKiev HPP. Oil leaks into the Dnieper River have been eliminated by installing new environmentally safeturbines. Environmental risks have been further reduced by improving the water management of theDnieper reservoirs as a result of the installation of modem control and monitoring system equipment andthe follow up on the TA recommnendations of a water management study.

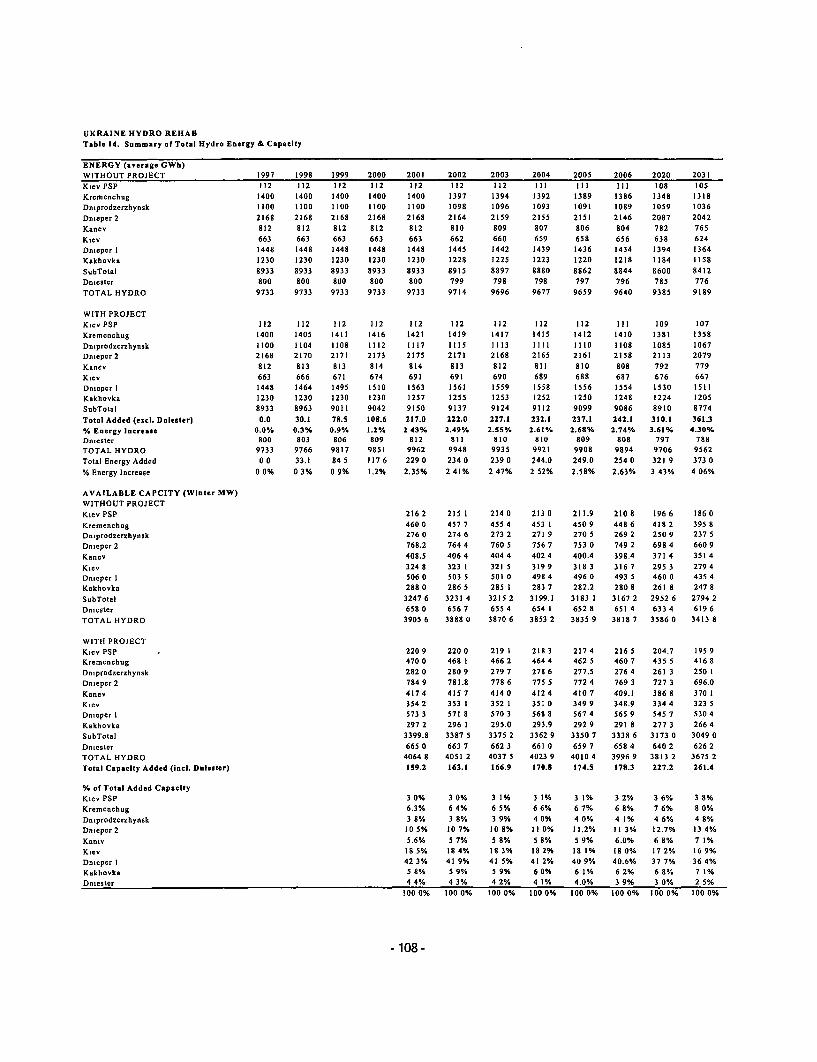

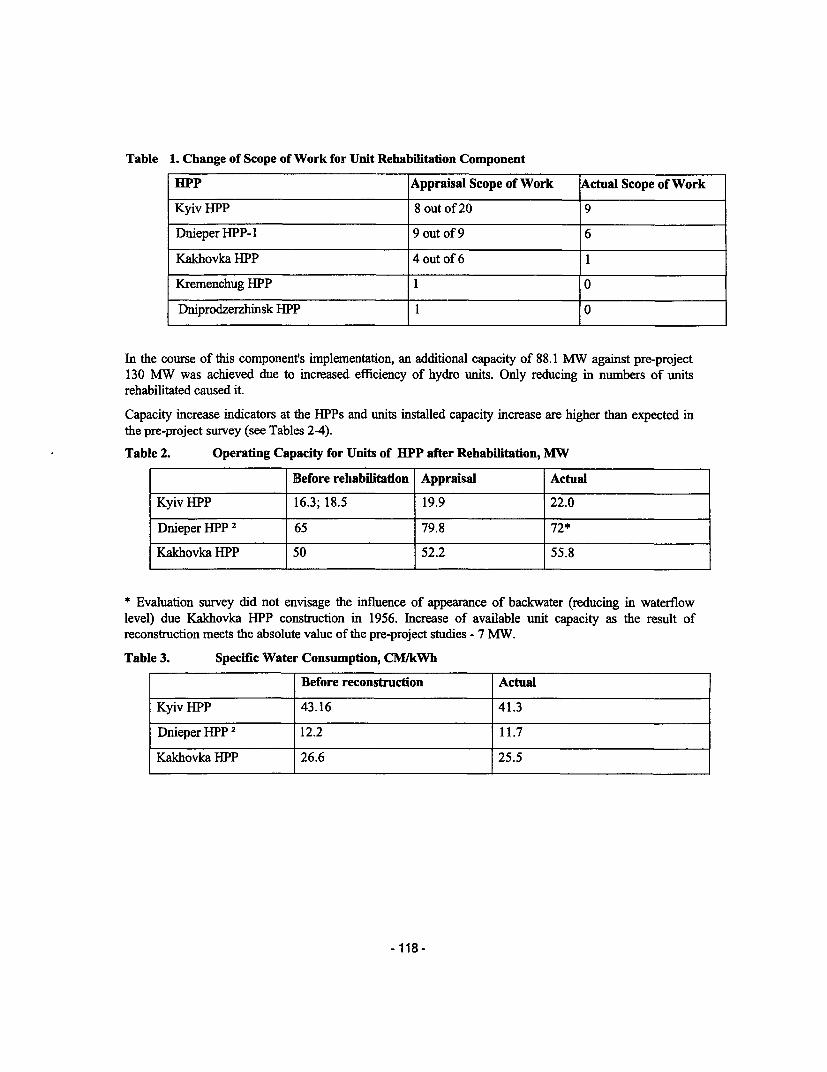

Achievement of objective (b) increase of hydropower generation capacity:

Additional total capacity of 88.1MW (2% increase of total capacity of the Dnieper cascade) was obtainedwithin the reduced project scope vs. 130 MW (3% increase of total capacity of Dnieper cascade) expectedunder the initial full project scope. The lower capacity increase at project completion was commensuratewith the overall reduction of the scope of rehabilitation works under the project.

-9-

Achievement of objective (c) improving the quality of electricity supply by upgrading load and frequencycontrol:

Frequency, a key criterion of the quality of electricity supply, has improved. Deviations of maximum andminimum frequency from the 50 Hz target have been reduced to acceptable ranges. Also, the monthlymaximum accumulated time error has been reduced from minutes to seconds. The number and the amount(MW) of load curtailments per year have been also reduced.

These results have been achieved from the joint effect of (i) the parallel operations of the Ukrainian powersystem with the power system of Russia since August 20, 2001, where Russia regulates frequency based onexchange of power flows with Ukraine; (ii) relatively lower demand and consequently lower system loadwhich allows easier maintenance of adequate frequency; (iii) the further upgrade of load and frequencyregulation under the project which is expected to bring about a substantial improvement of the scheduledinter-state exchange of active power flows.

Achievement of objective (d) reduction of fuel costs by facilitating the economic dispatch of generatingunits:

The project sub-component of upgrading the regulation and management systems of the TPPs wascancelled mainly because of the lack of a friamework for pricing ancillary system services such asfrequency regulation. At project completion, this has contributed to somewhat lower estimates of 0.4%savings of fuel consumption in the UPS, (except nuclear fuel), compared with the original estimates of0.9% of such savings as a result of the upgrade of the communications, dispatch and system control.

4.2 Outputs by components:(a) Rehabilitation of hydropower plants on the Dnieper cascade;Cost: US$ 84.2 million at appraisal, US$ 74.3 million at completion.

The rehabilitation of the hydropower plants on the Dnieper cascade was satisfactory although in reducedscope. Out of 23 turbines and 37 generators, originally planned for rehabilitation, a total of 16 turbinesand generators were rehabilitated at project completion. Hydraulic auxiliary and electric equipment wasreplaced or rehabilitated at all eight HPPs on the Dnieper cascade. The rehabilitation works resulted inincreased efficiency, capacity, reliability, and safety, improved environmental performance and extendedlife of the power plants equipment. Oil leaks into the Dnieper River were eliminated from the rehabilitatedturbines.

In addition, the installation of a new control monitoring and protection system on 5 of the HPPs (Kiev,Kremenchug, Dniprodzerzhinsk Dnieper-l and Kahovka) has optimized the HPPs' output and has furtherenhanced their availability and lifetime due to the system's pre-waming capability in case of abnornaloperation parameters. The ongoing integration of the control, monitoring and protection systems -of thehydropower plants with the SCADA system of the National Dispatch Center will further optimize theperformance of the hydropower plants and will also enhance their load and frequency regulating role inresponse to the needs of the entire power system. Improved frequency regulation also allows to operate thenuclear power plants (NPP) at the right frequency and thus enhances their safety.

- 10-

(b) Installation of the dam safety monitoring system;Cost: US$ 2.5 million at appraisal, US$ 1.9 milhon at completion.

The installation of a computer-aided safety monitoring system at Kiev dam has been rated satisfactory inview of the complexity and umqueness of the component This has been the first such type of equipmentinstalled in Ukraine and the other CIS countries. The uniqueness of this pilot project has been furtherenhanced by the fact that the Kiev 50 km earth dyke is one of the longest in the world, critically situatedupstream at the head of the Dnieper cascade. The upgrade of the control instruments, the automation ofinformation processing, and the reading of the safety meters all have contributed to improving the safety inthe Kiev dam flood zone along with the safety of the downstream HPPs which are all located in denselypopulated and industrialized areas.

As a part of the dam safety works and in compliance with the Bank's new safeguards on dams, (i) a localinstitute has assessed the discharge capacity of the entire Dnieper cascade; (ii) flood assessmentinformation is regularly conveyed to DHE; (iii) inspections of the sediments in water storages in front of theHPPs have been carried out; (iv) drainage devices have been rehabilitated where needed; (v) the emergencyaction plans of the HPPs have been updated; (vi) new guidelines have been developed for the exploitation ofthe reservoirs of the Dnieper cascade; and (vii) the preparation of project designs for installing dam safetyequipment on the remaining HPPs on the Dnieper River is underway.

(c) Upgrade of communication, dispatch, and system control;Cost: US$55.2 million at appraisal, US$46.9 million at completion.

These activities were also rated satisfactory since the initially envisaged equipment was installed. Theintroduction of automated load and frequency control and the enhanced protection of the high voltage (HV)transmission network will improve the quality of electricity supply which will then enhance the system'scapacity to integrate with the neighboring power systems. System efficiency will be also enhanced by thereduced fuel consumption from improved dispatch. The installation of an uninterrupted power supplysystem, including batteries, charging appliances and diesel generators, enhanced the operations of thepower system by counteracting the impact of the emergency outages.

(i) The upgrade of the communications system of the UPS was successfully achieved by laying 1,160 km ofnew fiber optic comrnmunications lines and installing digital automatic telephone stations. The introductionof a modem digital communications system on the basis of fiber optic cable increased considerably the

speed and volume of the transmitted information among the subdivisions of the unified power system ofUkraine. The installation of digital automatic telephone stations at the regional dispatch centers increasedthe reliability of the power dispatch communications.

(ii) The upgrade of the frequency regulation, dispatch and system control has been implementedsatisfactorily by installing:

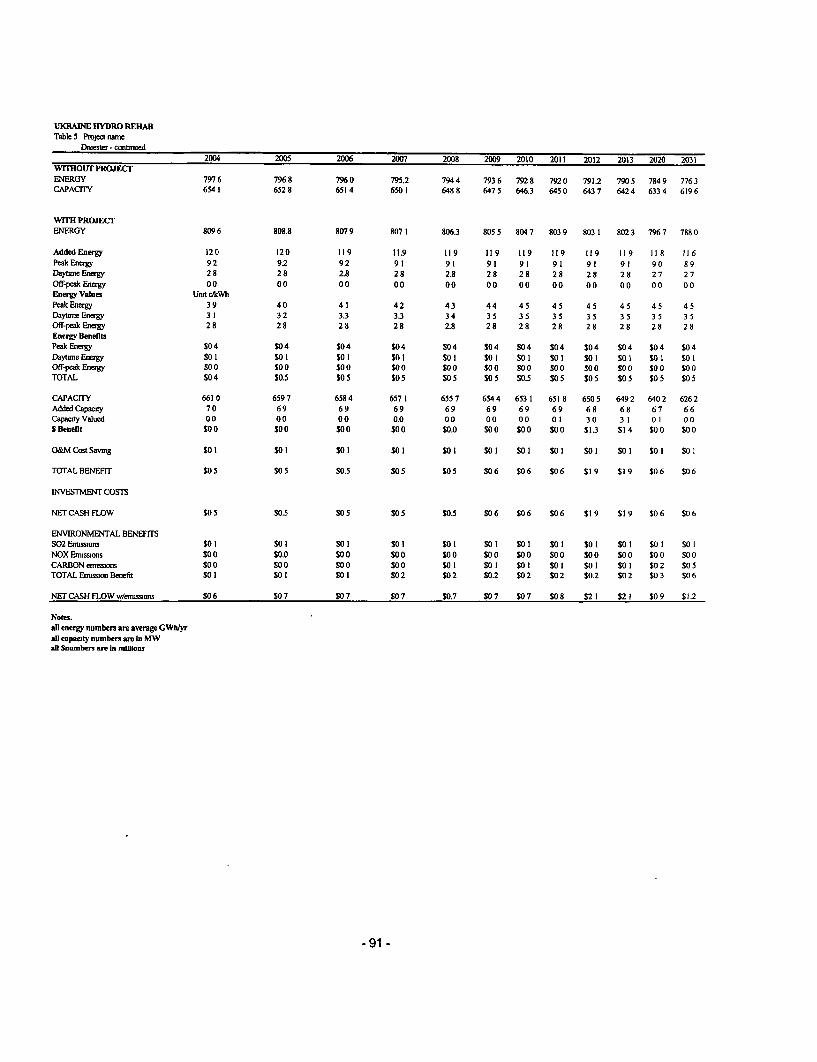

* an integrated package for automated load and frequency control which replaced outdated inefficientmanual control functions;

* a protection, management and control system at the Dniester HPP (702 MW) which enhancedmaneuverability and life of the plant equipment and integrated its regulating ability into the load andfrequency regulation of the entire power system of Ukraine; and

-1 1-

* relay protection devices on the high voltage transmission lines of the UPS main network, includingtransmission lines connected with the nuclear power plants. These devices further enhanced the reliabilityof the system, including the reliability of operations of the nuclear power plants (NPPs).

(d) Technical assistance.Cost: US$5 million at appraisal, US$7.0 million at completion.

Although this component has been completed in an overall satisfactory manner, the level of success ofseparate TA components varied.

The Swiss consulting company Stucky S.A. assisted in a satisfactory manner in the procurement of projectswitchgear equipment financed by the Swiss government with a grant to the Government of Ukraine,on-lent to DHE. (see note I at the end of this section)

The Norwegian Government financed a study on improved water management and hydropower generation.The study's recomnmendations were taken into account for the development of a new version of the Dniepercascade water reservoir exploitation rules.

A study on the automatic frequency regulation of the thennal power plants, financed by local funds, wascompleted as well. The Ministry of Fuel and Energy of Ukraine used the findings of the study as a basis toprepare guidelines for providing economic incentives to the thermal power plants involved in automaticfrequency regulation.

The local research institute Ukrhydroproekt together with DHE participated in developing the dam safetyconcept and preparing technical specifications for the procurement of project equipment.

The Canadian Agency for International Development (CIDA) financed technical assistance services for thefirst 3 years of the implementation of the project. The technical assistance services were provided byHydro Quebec Intemational (HQ]) in the areas of engineering, procurement and project management.These services initially suffered some difficulties related to the extremely limited number of experiencedspecialists available to work in a Russian and Ukrainian languages environment. However, after solvingprogressively this major recruitment problem, the situation notably improved after mid-1996 when moreexperienced consultants joined the project and at the same time a better interaction was reached with thebeneficiaries. The situation was completely normalized in 1998 when the beneficiaries hired HQI withfunds from the World Bank loan to provide further TA services.

DHE's needs for project management assistance declined during the second half of the project period as aresult of the reduction of the physical scope of some project components. In this regard, and in view of theimproved local financing, DHE opted for hiring local consultants with its own funds until the project'scompletion.

Audits by PriceWaterhouse and KPMG were also financed with technical assistance funds.

The project design was appropriate for achieving the project's objectives.

a/ technical aspects: adequate rehabilitation works and modem equipment were included in the projectscope to ensure the envisaged improvements in the power system. Project sites and specificturbine/generator units were selected for rehabilitation in view of ensuring maximum benefits from the

- 12 -

project works. Technical assistance was expected to compensate for the implementing agencies' lack ofprevious experience with Bank-financed projects.

b/ country needs and Bankpriorities: the project provided critical support to the power sector in line withthe government's priorities and the Bank's CAS.

cl sustainability: the project was designed under the enabling famework for sector reforms, envisaged bythe govemment. The benefits from improving the financial discipline in the power sector under the reformprocess, although delayed, trickled down to the project level and restored the financial stability of theproject implementing agencies beginning in 2000, which consequently ensured successful projectcompletion.

dl project monitoring and reporting: the project performance criteria and the loan covenants weredesigned to enable adequate measurement and reporting of project progress and to provide a leverage forcorrective actions, when needed. The performance indicators for minimizing frequency deviations,increasing operating capacity and turbine/generator efficiency were reasonably quantified to enable theassessment of project achievements during supervision and at completion. The logical framework tool didnot exist at project appraisal. Therefore project outcomes and outputs were outlined at completion on thebasis of analysis of the actual project results. The loan covenants related to auditing requirements, debtratio, and self financing ratio facilitated the monitoring of compliance with the Bank's fiduciaryresponsibilities and financial requirements for the project's agencies. The loan covenants related tocompliance with the power purchase agreement between DHE and NDC, and the contracts between NDCand its downstream clients were deleted from the respective project agreements with the Bank. Instead,during each following supervision mission, requirements for specific allocations of funds from the newlyestablished Energomarket (the wholesale electricity market) to DHE and NDC were agreed and closelymonitored thereafter. This change took place as a result of introducing a new mechanism of allocatingpayments for electricity transactions directly through Energomarket to all participants in the power sector,including DHE and NDC, which made irrelevant the earlier bilateral payment arrangements between DHEand NDC, and NDC and its clients.

Note 1: Under the conditions of a Grant Agreement between the Governments of Switzerland and Ukraine, the SwissGovernment extended a CHF 13.7 rnillion grant to Ukraine. The Grant Agreement also stipulated that the Ministry of Financeof Ukraine should then extend the Swiss grant proceeds as a loan to DHE. DHE has already used this loan to finance thesupply and installation of Swiss switchgear equipment under the project. DHE was supposed to repay the loan with interest tothe Mimstry of Finance. The Mmistry of Finance was expected then to use DIE's loan repayments for setting up fiunds tosupport environmentally friendly initiatives in the energy sector. However, DHE has repaid so far only a mmor portion of theloan due to earlier difficulties in payment collections. On November 14, 2002, the parties agreed on revised loan repaymentoptions.

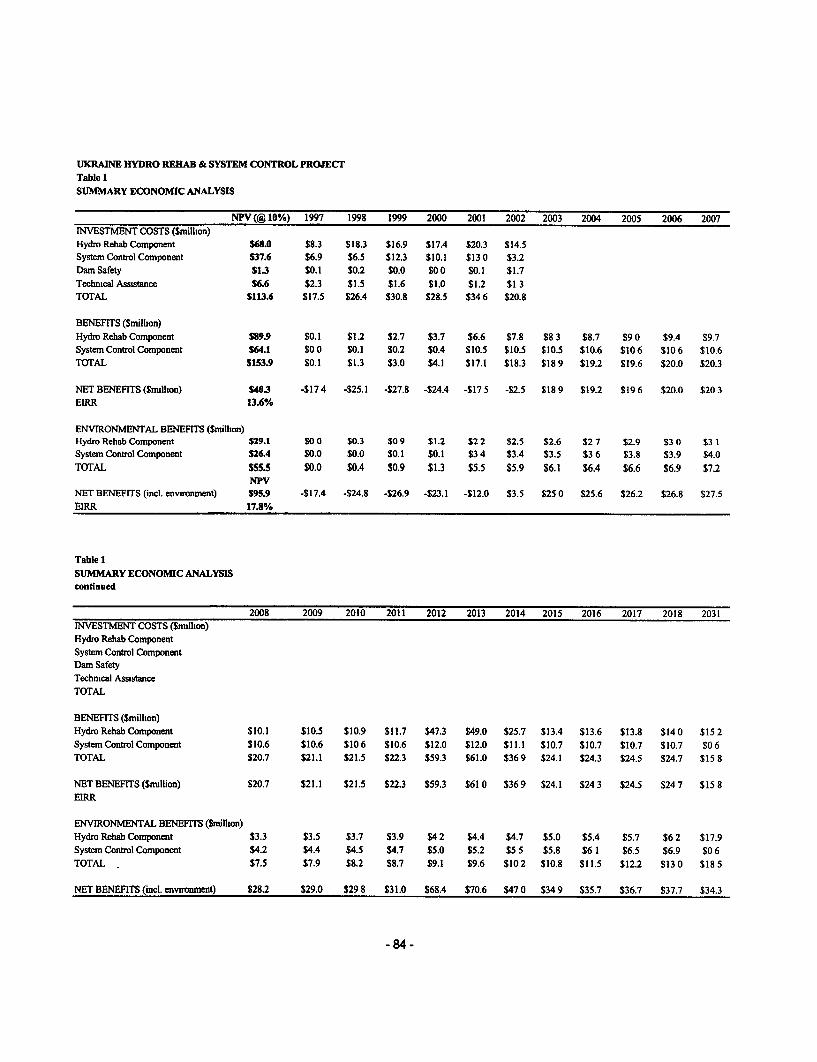

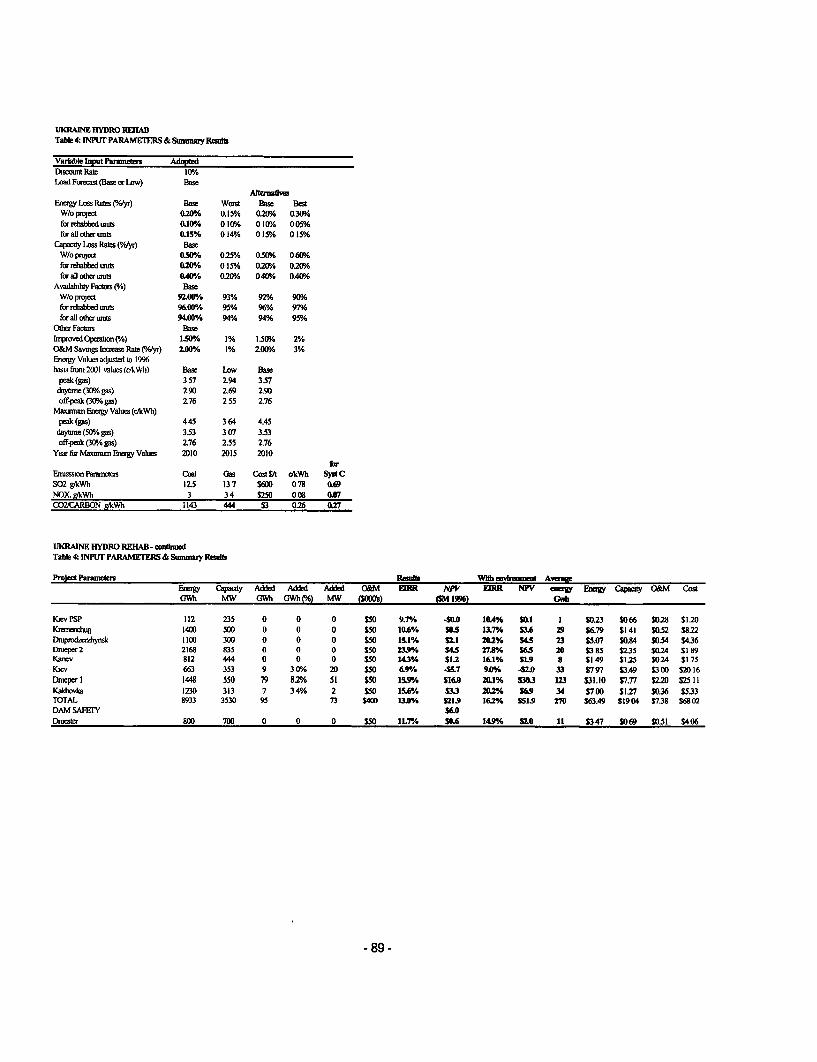

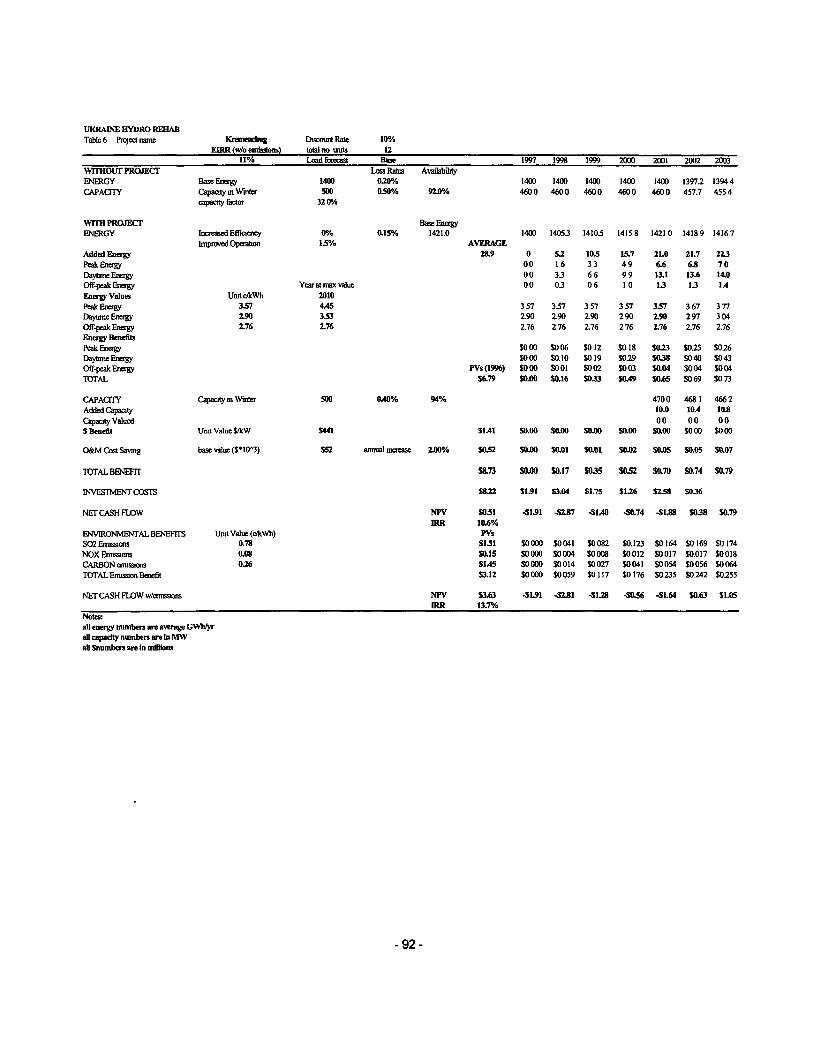

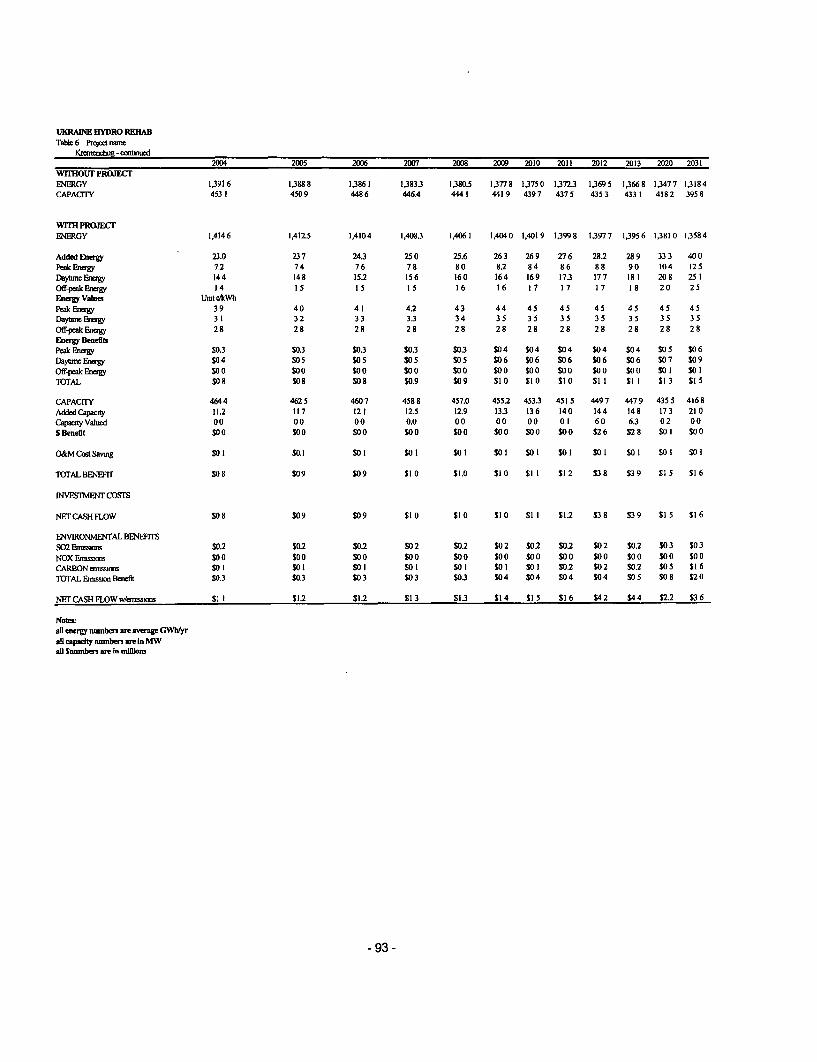

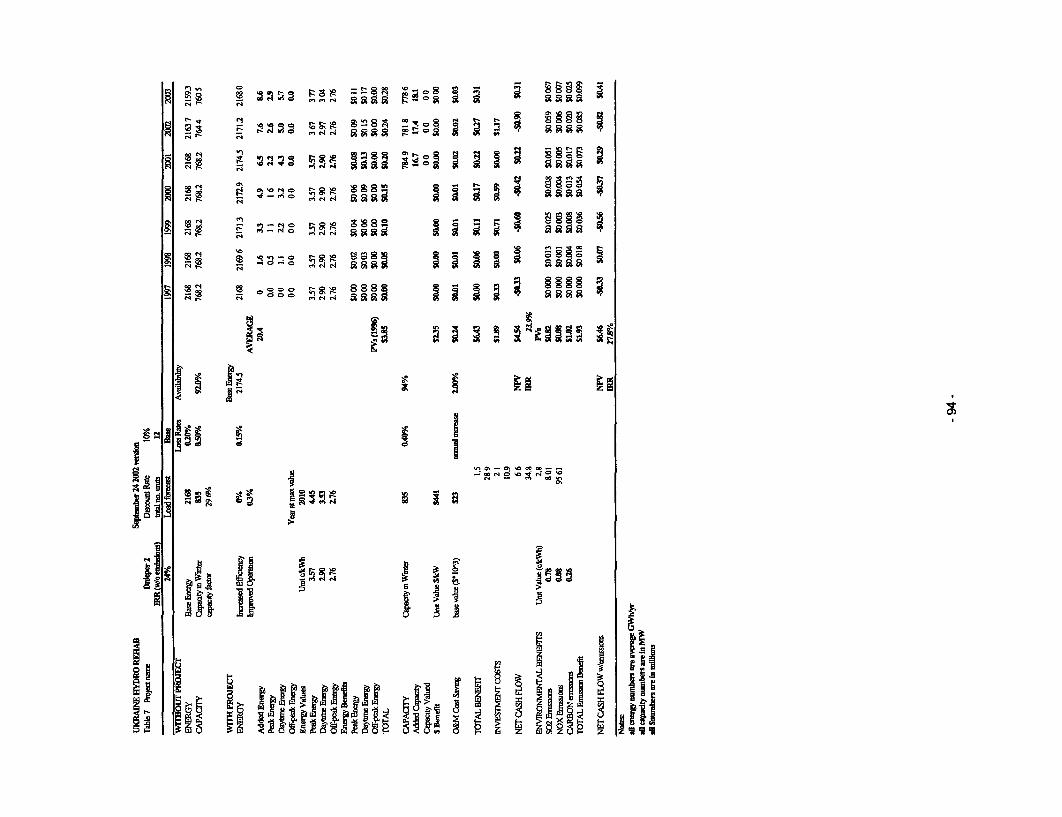

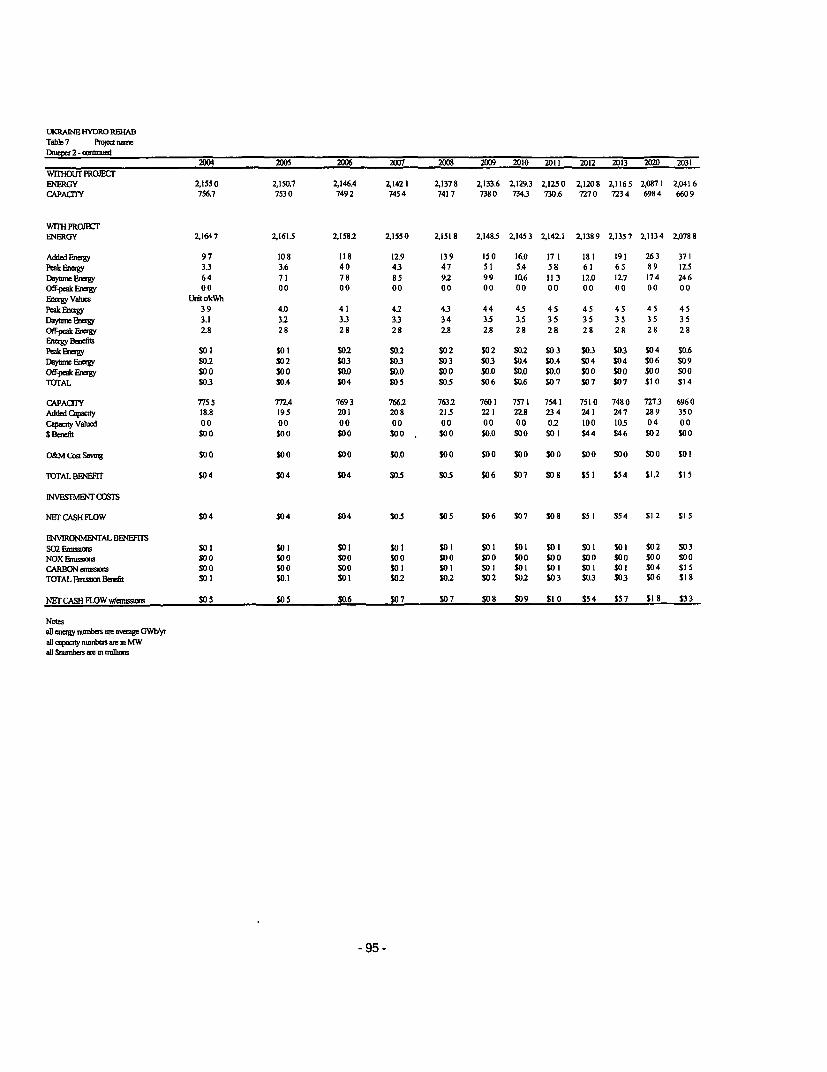

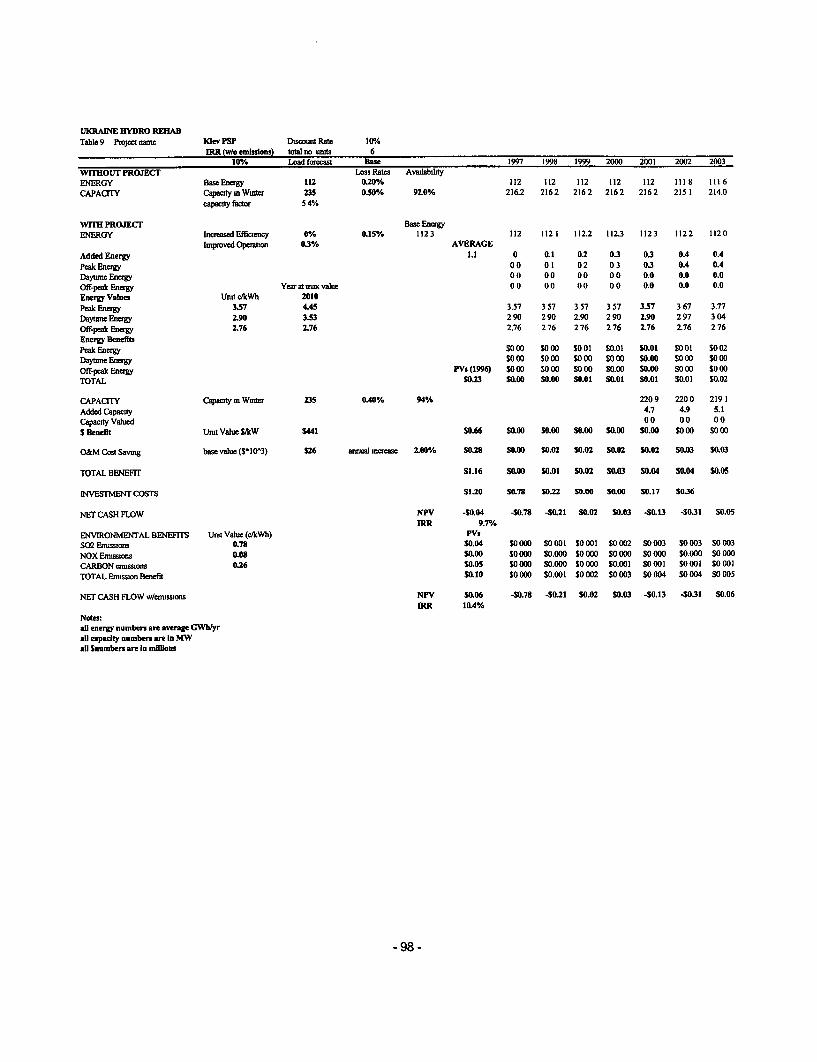

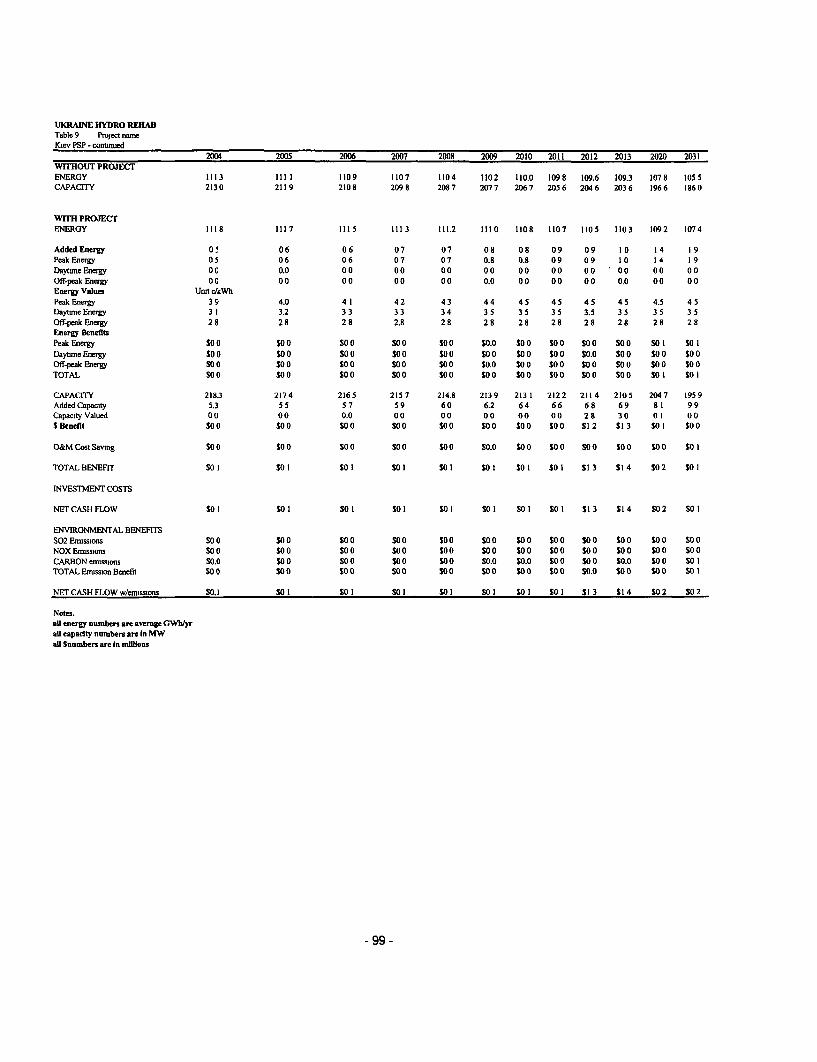

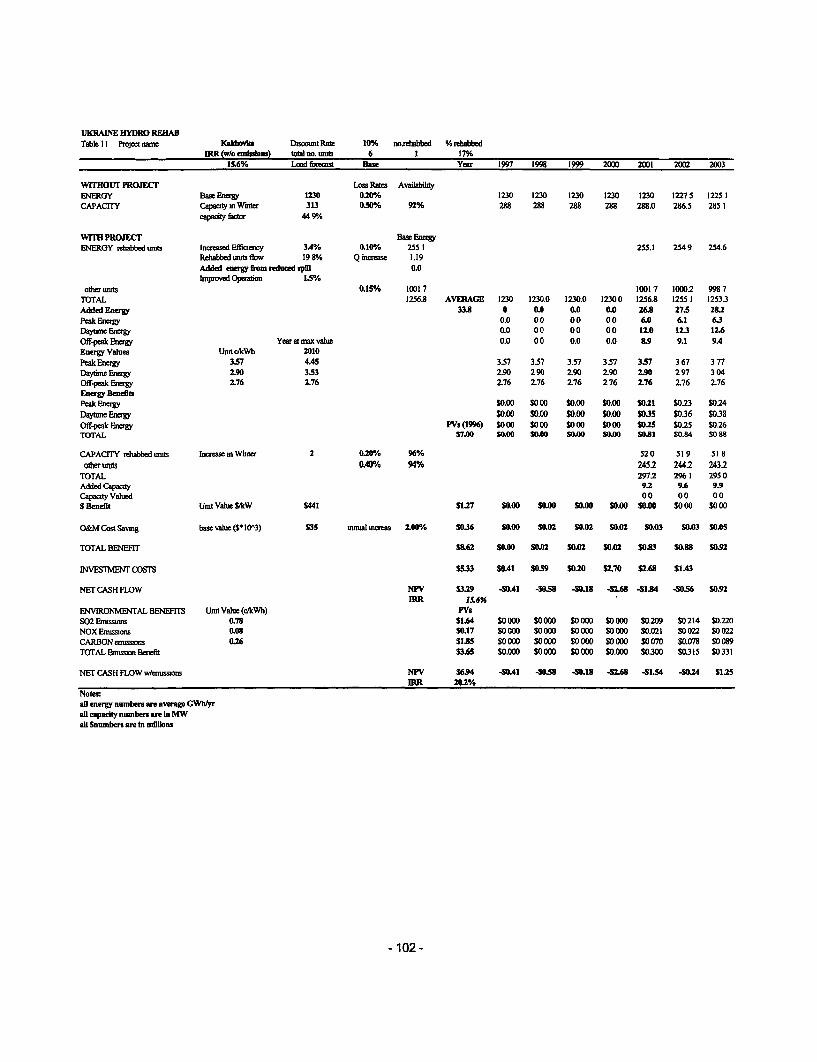

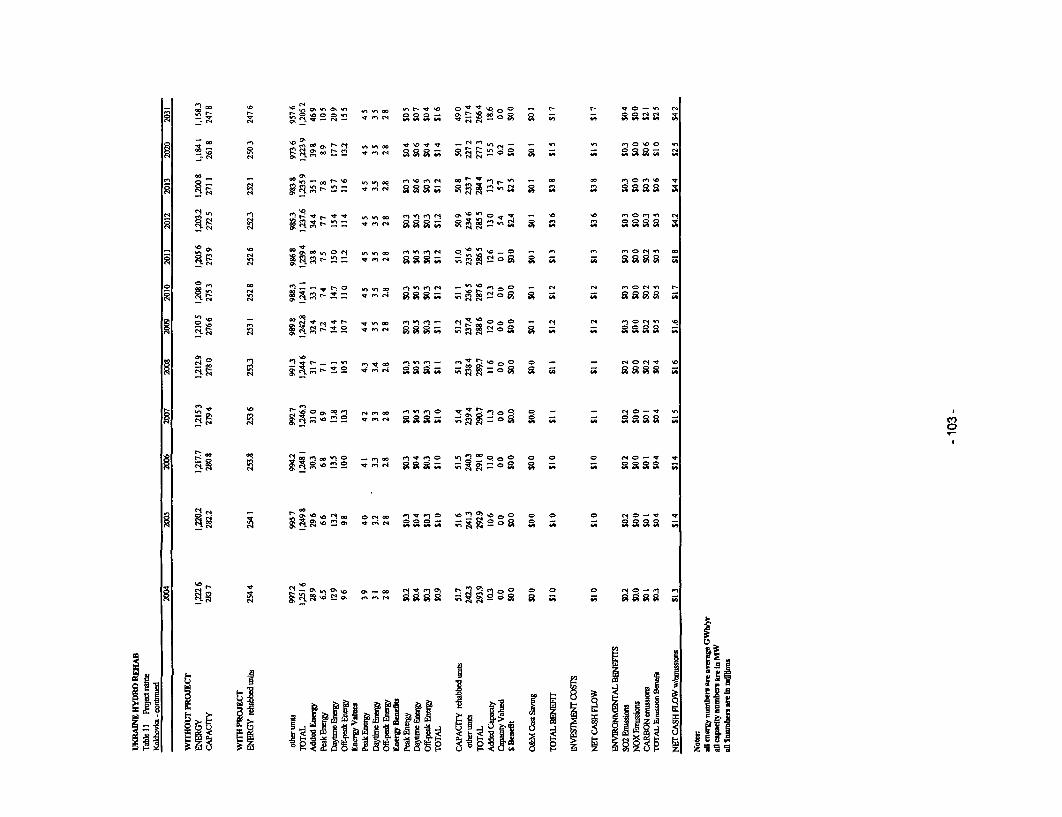

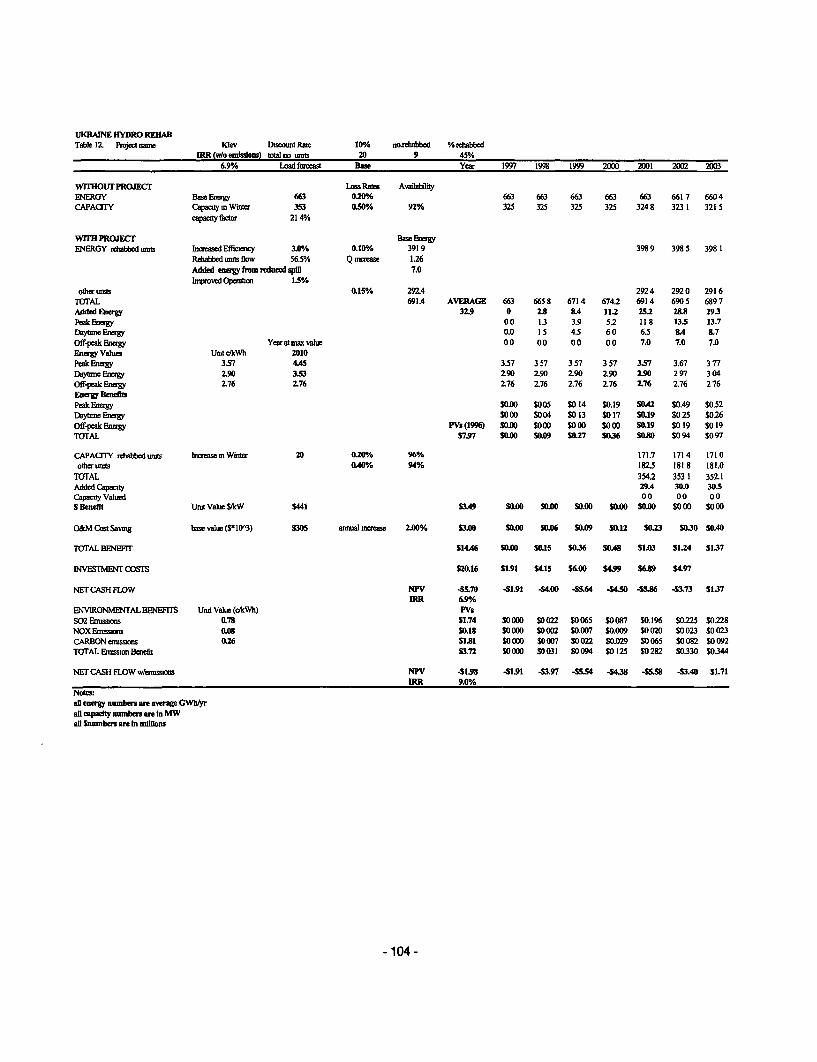

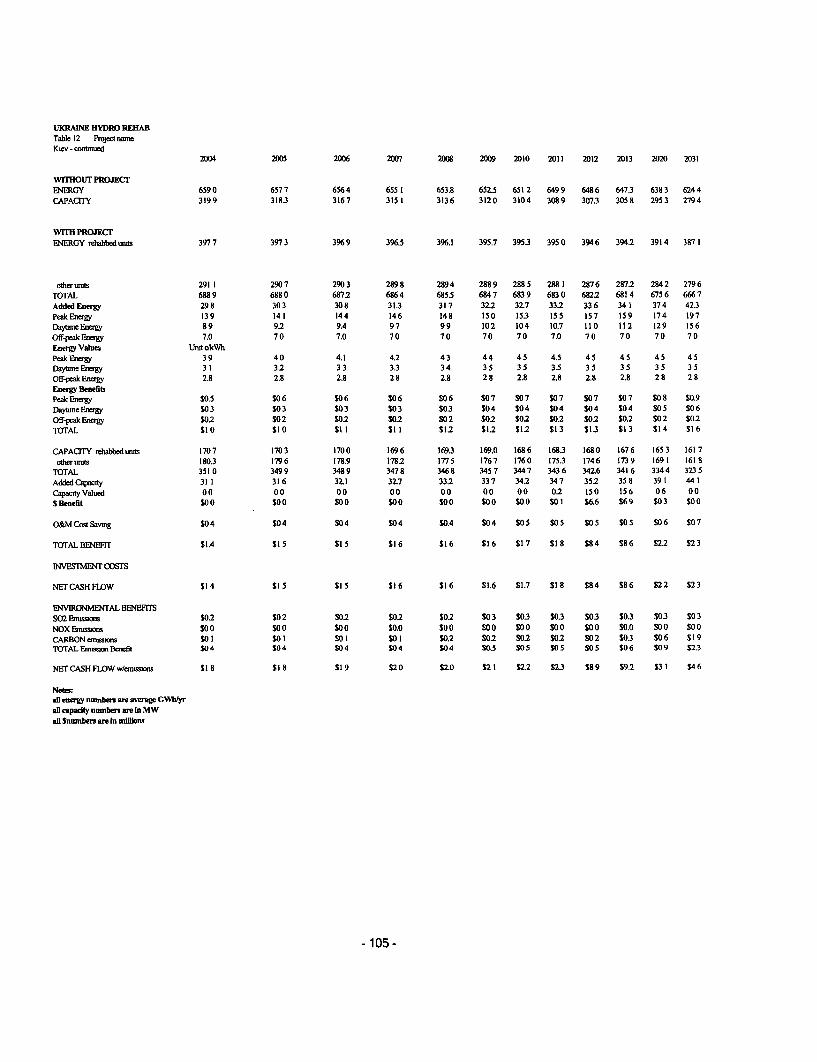

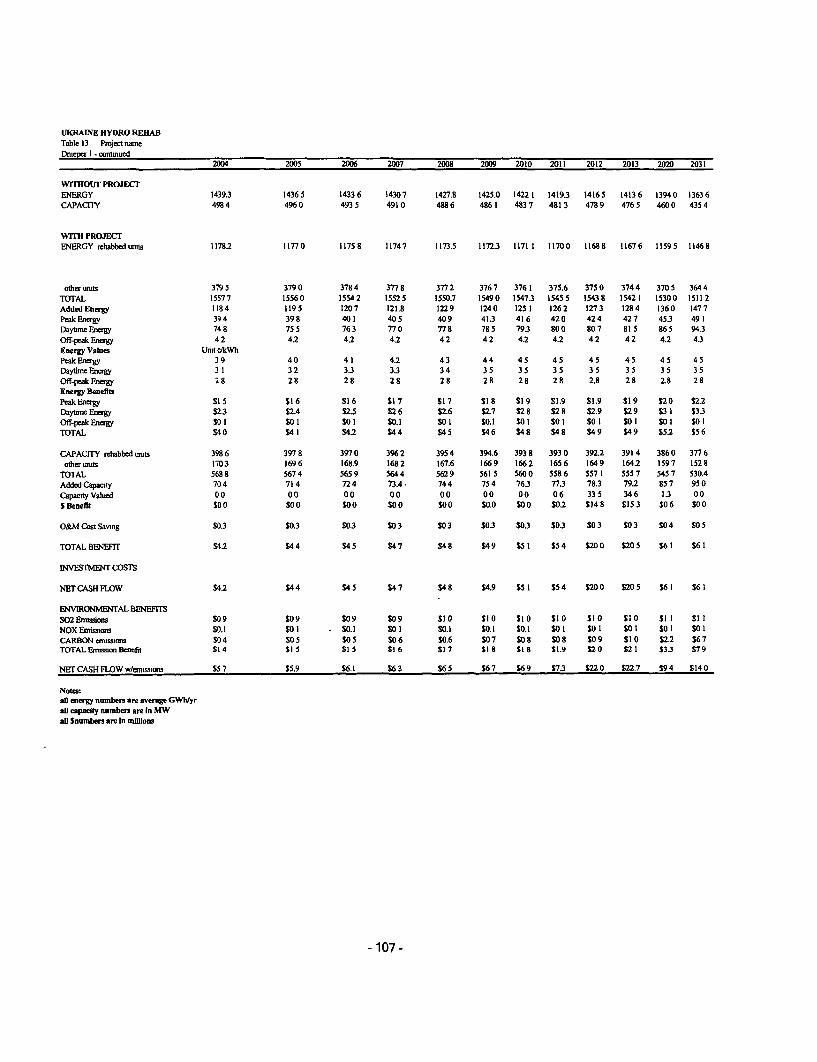

4.3 Net Present Value/Economic rate of return:Economic returns upon project completion were sustainable, although lower than the ones at appraisal duein large part to the lower benefits as a result of reducing the project scope. The SAR showed an estimatedeconomic intemal rate of return (EIRR) for the total project at 18.1%. The re-estimated EIRR for the totalproject at completion was 13.6%. A separate EIRR was estimated for the Hydropower PlantsRehabilitation component: 17% at appraisal and 13% at completion, and for the System Control andCommunications Upgrade component: 22.7% at appraisal and 17.7% at completion.

- 13 -

Hydropower Plants Rehabilitation Component

The lower EIRR of the hydropower plants rehabilitation component at completion was mainly due to lowergains in capacity and energy as a result of the reduction of the project scope, the revised smaller impact ofimproved reliability and availability of the HPPs.

The reduction of the number of the turbines and generators, which were rehabilitated under the project,resulted in lower net benefits from additional energy output under the project. The original scope envisagedthe upgrade of 23 turbines and generators which represented some 33% of the total energy capability of thehydropower plants. Only 16 turbines and generators, were actually rehabilitated representing about 18% ofthe total energy capability. Had the original number of turbines and generators been rehabilitated, EIRRwould have increased by about 1%.

In addition, at completion, gains in capacity and energy from improved reliability and availability of theHPPs were lower than expected - at about 0.15 % per year. Had the larger appraisal estimate of 0.4%annual gains been materialized, EIRR would have increased by about 2%.

System Control and Communications component

The cancellation of the component for govemors of the thermal power plants led to reducing the benefit offuel savings from improved frequency regulation to 0.4% of the thermal fuel cost of the UPS, comparedwith the estimated 0.9% of such fuel saving at appraisal. This reduction in fuel savings was the mainreason for obtaining a lower EIRR at completion for the System Control and Communications Upgradecomponent, despite the effect of new benefits from fiber-optic-based communication services which werenot identified at appraisal.

Environmental benefits from reducing emissions from fossil fuels as a result of additional hydropowergeneration under the project were estimated at completion. This has led to higher EIRRs at completion asfollows: Total project: 17.7%, Hydropower Plants Rehabilitation component: 16.2%, and System Controland Communications Upgrade component: 23.7%.

The original and completion EIRR estimates were based on total project costs. The appraisal andcompletion analysis included the cost of the technical assistance and dam safety components withoutquantifying any relevant benefits.

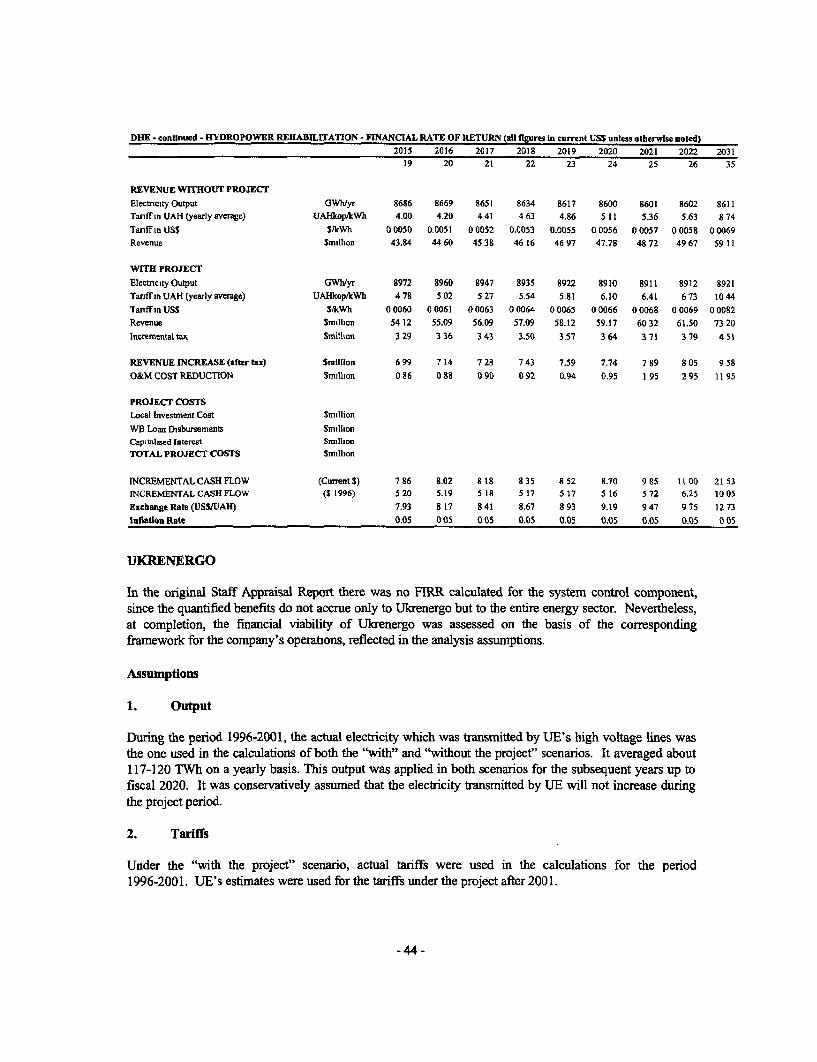

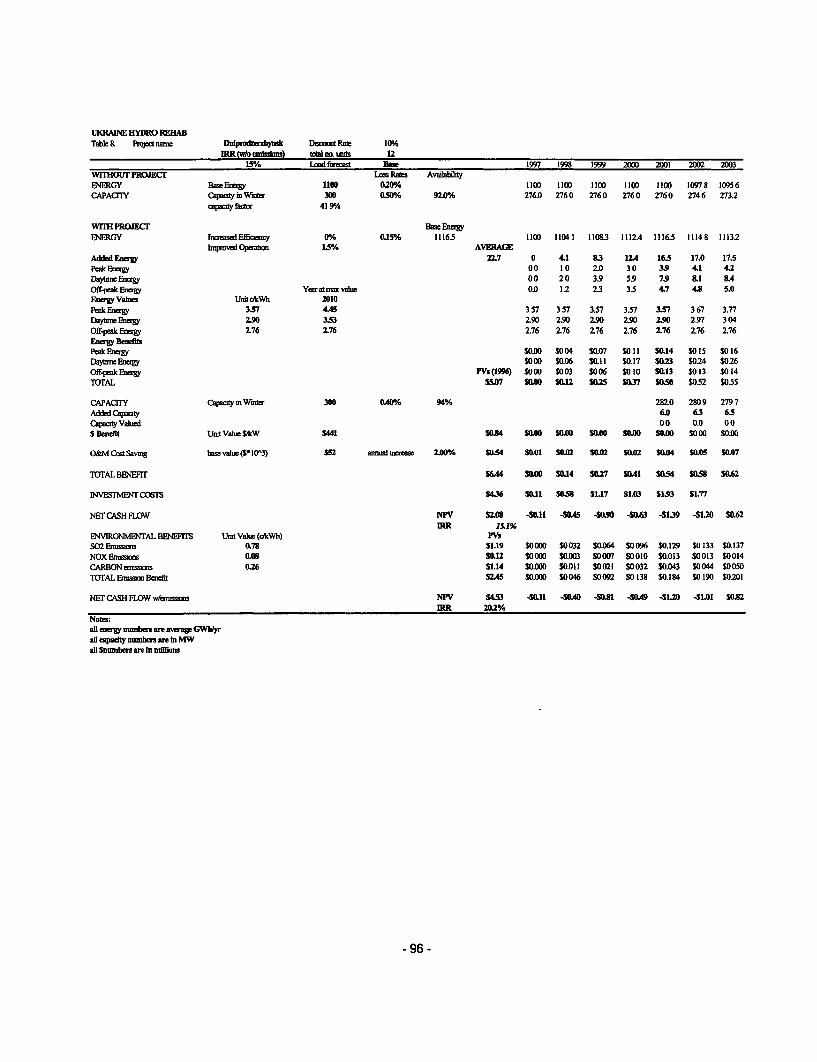

4.4 Financial rate of rehirn:The financial intemal rate of return (FIRR) for DHE's hydropower plants rehabilitation component iscurrently estimated at 9.9% (in real terms) which is lower than the appraisal estimate of 13%.Nevertheless, the FIRR at completion still compares favorably with DHE's cost of capital, 8.5%, reflectingthe cost of borrowing under the project (1.5% on-lending interest rate, plus 7.0% estimated World Bankrate).

As in the case of the EIRR, the lower FIRR of the hydropower plants rehabilitation component atcompletion was also due to lower gains in capacity and energy which altogether resulted in a loweradditional average annual electricity output at completion - 270 GWh/yr, compared with the expected 567GWh/yr appraisal.

- 14-

Key assumptions for the analysis at appraisal and completion do not differ. The same cost-recoveryprinciple in tariff formation and the taxation rules relevant to enterprise income were followed at appraisaland completion. Savings from operation and maintenance costs did not differ significantly.

The FIRR is sensitive to changes in project cost, level of electricity output, and rate of inflation. Thesechanges can be absorbed under the present tariff mechanism based on cost recovery. Adding US$ 8.8million equivalent of the Swiss Grant to the project cost (See footnote 3 in Section 4.2), which is 10% oftotal DHE's project cost) would require at least an additional average tariff increase of 0.4% per yearduring the project life in order to ensure the project's financial sustainability. The estimated level of projectelectricity output can be reduced by no more than 1.7% within financial sustainability limits. Any largerreductions will have to be compensated by commensurate tariff increases. Any changes in rate of inflationcan be also absorbed by corresponding tariff increases.

No FIRR was calculated for NDC (Ukrenergo) at appraisal since the quantified benefits from fuel savingsas a result of more efficient economic dispatch did not accrue to the company, but to the entire powersector. Nevertheless, at completion, the financial viability of Ukrenergo was assessed on the basis of thecorresponding framework for the company's operations, reflected in the assumptions on tariffs for UE'sservices, and the electricity transmitted through UE's high voltage lines. The assumptions regardingtaxation, the expected inflation and exchange rate in subsequent years are the same as those used for DHE.The FIRR for UE was calculated at 15.9% on a current basis and 13.4% on a real basis which alsocompares favorably with UE's cost of capital, 8.5%, the same as the one for DHE. The UE's FIRR iscritically sensitive to even very minor to changes in the tariff for UE's services, and less sensitive tochanges in the amount of electricity transmitted through the UE's lines. (See section 10 for details on FIRRcalculations and sensitivities).

4.5 Institutional development impact:Background

As the first Bank investment operation in the energy sector of Ukraine, the project was successful. Itcomplemented the Bank's Programmatic Adjustment Loan (PAL) and the IMF's Extended Fund Facility(EFF) mainly in the area of improving cash collections in the power sector.

The original project design depended on progress of sector reforms, and coupled with the requirements forfinancial viability of the project implementing agencies, contributed to creating an initial basis for thepursuit of key elements of the current joint Bank/GoU strategy to improve institutions and governancethrough (i) design of a regulatory environment with a level playing field in the energy sector; (ii) creationand protection of property rights, and (iii) improvement of fiscal and financial discipline, publicaccountability and management of social and environmental risks.

- 15 -

Sector level impact

The project was designed and implemented in the context of the first steps to improve management of theelectricity sector through restructuring of the hydropower plants into a joint stock company andconsolidating the regional dispatch centers into a National Dispatch Center, followed by sector unbundling,establishment of a National Electricity Regulatory Commission and a Wholesale Electricity Market andprivatization of electricity distribution companies to strategic investors. The improved quality of electricitysupply and stability of the power system, achieved under the project, improved the safety of the NPPs andenhanced Ukraine's possibility for interconnection with neighboring power systems, thus moving thecountry closer to EU standards.

Since 2000, efficient government measures to improve collections and restructure arrears in the powermarket, in addition to all of the above institutional improvements, further contributed to increasing privateinterest in the sector and enhanced the financial stability of the project companies, a key factor forsuccessful project completion.

Company level impact

The project had a direct beneficial impact on improving corporate govemance of the implementing agenciesby (i) involving them in intemational project management, accounting and procurement practices, (ii)ensuring transfer of advanced technologies and know-how, and (iii) enhancing national key scientificresearch and industrial capacity. In addition, the project covered important social and environmentalaspects of the country's policy priorities by generating additional employrnent and reducing environmentalhazards along the Dnieper basin.

The project helped Dniprohydroenergo and Ukrenergo acquire experience in management andimplementation of projects financed by international financial institutions. The companies' accountingimproved by adopting standards closer to international practices.

Project procurement experience contributed to incorporating sound procurement principles of economy andefficiency, international competition, transparency, equity and fairness in the national procurementlegislation. Intemational competitive bidding enabled DHE and Ukrenergo to acquire at least costequipment which was best suited to the project needs and resulted in transfer of most advanced technology.

Transfer of project know-how was ensured by proper training of Ukrainian experts by suppliers. Thisenabled further transfer of knowledge. Inovative technological experience from the project was sharedwith the programs of two key engineering institutes in Ukraine which train high caliber experts for thehydropower industry.

In support of the joint Bank/GoU strategy to ensure employment-generating growth, 10,000 new jobs werecreated in the course of project implementation. In addition, amid the economic crisis, project design workspreserved the existence of research and design institutes.

5. Major Factors Affecting Implementation and Outcome

5. 1 Factors ou2tside the control of government or implementing agencyLengthy Parliamentary ratification procedures and an international economic crisis were the main factorsoutside the control of the Government, DHE and LJkrenergo which affected project implementation.

-16 -

Inclement weather and spring floods additionally constrained project works on occasion. In this context,close flank supervision and intensive work of local contractors mitigated adverse impacts on the project andfacilitated the completion of physical works under a tight schedule.

Parliamentary ratification, and respectively the date of effectiveness of the project Loan Agreement,approved by the Board of the Bank in April 1995, were delayed by more than a year. This postponedaccordingly the start of project implementation. Lengthy and repetitive internal government proceduresalso contributed to the delayed approval of the Loan Agreement by Parliament

Economic instability: Intensified economic problems in East Asia and Russia in 1998 destabilized debtservice dynamics in Ukraine by causing yields on Ukrainian T-bills, issued to foreign investors to finance alarge budget deficit, to rise to unsustainable levels. In this regard, the effort to pay off or restructure theT-bills debt alnost depleted the country's foreign exchange reserves and triggered a severe financial crisis,which then, among other adverse impacts, brought to a halt payments in the power sector and led to aninterruption of local project financing.

Force-Majeure: On occasion, winter blizzards led to icing and damage of power transmission lines andrelated equipment. The unforeseen need to repair these damages imposed an additional strain on the scarcelocal project funds and related project works. Longer than usual spring flood periods, when as manyturbine/generator units as possible have to operate, occasionally delayed project rehabilitation schedules

5 2 Factors generally subject to government control:The main factors subject to government control that critically affected the project were (i) overallinconsistent economic and reform policies, and (ii) poor payrnent discipline in the electricity sector.

Project implementation was also negatively affected by additional factors subject to government controlsuch as (i) varying profit tax and VAT regulations; (ii) burdensome customs and export-import rules; (iii)lack of clear regulations on contract liabilities; (iii) lack of national standards for new project equipmnentand (iv) the 1998 merger of the of the project implementing agency National Dispatch Center (NDC)together with the National Power Transmission Company into a new National Power Company Ukrenergowhich also encompassed the establishment of the Wholesale Electricity Market within the new company.

Economic policies and non-payments in the electricity sector: Adverse extemal economic developmentsonly aggravated persisting domestic economic imbalances caused by a relaxed fiscal stance and weakfinancial discipline, particularly in the power sector, in the context of the overall reversal in thegovernment's drive for economic reforms between 1996 and 2000. As non-paymnents, coupled with barterand promissory notes (veksels) transactions, continued during this period, scarce collections inEnergomarket were re-allocated primarily to ensure emergency purchase of fuel for the thermal powerplants during the winter, to the detriment of the needs for local project financing. Consequently, the overallproject implementation delay, relative to the initial schedule, rose to about 20 months in early 2000 andaffected primarily turbine/generator rehabilitation and installation of already imported equipment, as theseactivities entirely depended on sufficient local financing.

In 2000 the new reform-oriented government undertook active measures to irnprove electricity payments.The cash collections consequently rose from only 9% in April 2000 to 71% in May 2001 and 90% in May2002. The concerted govemment's effort to improve electricity payments provided grounds for extendingthe loan closing date for another 18 months which allowed for overall achievement of project objectives,although with delay and reduced scope of rehabilitation works.

- 17 -

Tax legislation: Introduction of an accruals form of accounting for tax calculations in 1997 resulted inmuch higher accounting profits and consequently higher profit tax obligations for the power sectorenterprises. This measure was enforced without consideration of the actually low revenues of the powercompanies due to non-payments for their output and lack of tax exemptions for their mandatorycontributions to various state funds, unrelated to the companies' activities. In addition, the availability oflocal project funds was further constrained by the temporary introduction of VAT (1998 and 2002) onimported equipment and electricity sales (1999) under the project.

Customs and import-export regulations: Lengthy and complex procedures for customs clearance ofproject equipment compressed subsequent installation and commissioning schedules. Import-exportregulations did not contain provisions for exporting earlier imported project equipment for repairs at thesupplier's site. This limited the possibility for repairs of project equipment under suppliers' contractguarantees.

Lack of clear stipulations in the national legislation regarding local liabilities of foreign contractors andsuppliers, engaging in project activities in Ukraine, hampered preparation of tenders.

Lack of national standards for project equipment which was new to the country required additional timefor testing and acceptance procedures for such equipment.

Restructuring of the National Dispatch Center and frequent changes of its management. The 1998merger of the original project implementing agency (the National Dispatch Center) with the NationalTransmission Company and the Energomarket (the wholesale electricity market) into a new entityUkrenergo seriously constrained the review of the financial performance of the resulting project entity. Thesituation improved since 2000 when Energomarket was separated from Ukrenergo. However, furtherre-organizations within the sector affected the project implementation schedule. Complex project equipmenthad to be contracted and delivered first to the project implementing agency Ukrenergo which then had tolease it for installation, commissioning and operation to other entities which have remained outsideUkrenergo's structure. In addition, throughout project implementation until 2000, changes of Ukrenergo'sdirectors (there have been four directors of Ukrenergo during project implementation) and staff involved inproject implementation adversely affected the project.

5 3 Factors generally subject to implementing agency control:Slow, burdensome and inaccurate intemal procurement review processes within both project agenciesthroughout the project, particularly at its beginning, along with seriously delayed project status reportingfrom UE during the first half of the project, compounded overall project implementation difficulties. Inaddition, some project works were constrained by UE's intemal difficulties to optimally scheduledisconnections of transmission lines to install project equipment.

Nevertheless, the strong ownership and drive for results of DHE's top management and staff at all powerplants throughout the entire project period, along with improved project ownership at UE since 1999, uponthe advent of the company's present management, have altogether compensated for the initial lack ofknowledge of Bank procedures, have mitigated negative external impacts and have ensured overallsuccessful completion of the project works.

- 18-

5.4 Costs andfinancing:Total project costs, including interest during construction (Il)C), were about US$141.5 million equivalent,or 66% of the appraised estimate of US$215.1 million. The difference of US$73.6 million equivalent inproject costs resulted from:

(i) the reduction of the number of rehabilitated turbine/generator units;(ii) the cancellation of the TPP governors sub-component,(iii) and generally lower than estimated local costs of the System Control component.

In addition, actual interest paid during construction was lower than estimated due to cancellation of unusedBank funds.

The above reductions of costs have outweighed increases in the cost of installing dam safety equipment perkm of dam, the cost of higher volume of local works related to a turbine/generator unit along with theincrease in contract values because of additional project quantities of fiber-optic cable, switchgear, systemcontrol and monitoring equipment and extended technical assistance.

The brunt of the project financing was based on a 17-year IBRD loan with a 5-year grace period and alevel repayment pattern. Seventy two percent -US$ 82 million- of the original amount of US$ 114 millionof the Bank loan was used. The Canadian Government more than doubled the funds for the project-relatedconsulting services which were extended to cover additional needs for such services as a result of thealmost one year delay in the start of project implementation due to late Parliamentary ratification of theLoan Agreement. The grant from the Swiss government in the amount of CBP13.7 million was used forthe supply and installation of high voltage (HW) equipment at the hydropower plants. The US$ 0.6 milliongrant from the Norwegian government was used for a study on the management of the reservoirs on theDnieper River.

6. Sustainability

6.1 Rationalefor sustainability rating:The benefits from the project are sustainable in view of the improvements in the power system's efficiency,stability and safety, the system's enhanced possibility for interconnections with the neighboring systems,achieved in the context of macro-economic improvements, coupled with positive trends in the overallbusiness environment, sector privatization, improving cash collections, debt restructuring and GoU'scontinuing commitment to further sector reforms with active support from donors and internationalfinancial institutions.

Continued adequate financial discipline in the sector remains a critical factor for ensuring projectsustainability. Current competition among thermal generators, their expected privatization and thecontinued process of divesting electricity distribution companies are expected to enhance overallperformance of the power sector through attracting new investments.

6.2 Transition arrangement to regular operations:DHE and UE will continue the work to (i) ensure proper financing of their operations; (ii) integratecompletely the project equipment in their systems; (iii) draft internal regulations for equipment operationsand maintenance and train relevant staff accordingly; (iv) ensure arrangements with suppliers for properservicing of the project equipment beyond the contract guarantee period, and (v) monitor key physical andfinancial performance indicators.

- 19 -

DHE and UE will also pursue improvements in their financial management and accounting practices basedon the auditors' recommendations received during project implementation. Both companies will continuetraining staff to improve preparation of their consolidated financial statements based on NationalAccounting Standards (NAS) format, will work on introducing proper registry and software systems alongwith streamlining their tax records and tax payments forecasts. (See details on transition arrangements inSection 10, paragraph V)

UE has estimated that the project impact on the entire power system will be fully felt in about 5-10 years inview of the large size of the system and the additional time needed to fully integrate the project equipmentinto overall system operations. The project rehabilitation improvements in terns of hydropower plants'efficiency, capacity and oil leakages have been already assessed, although it will take more time tocompletely materialize the benefits of better cascade operations as a result of improved system control andmonitoring.

Dniprohydroenergo and Ukrenergo are satisfied with the results achieved under the project, which inaddition to responding to the needs for upgrading dispatch, communications, and system control, alsocovered about 20% of the rehabilitation needs of the Dnieper cascade equipment. Further support to theremaining rehabilitation works at the hydropower plants will enhance the benefits to the power systemprovided (i) the Government's overall reform efforts remain on track; (ii) proper financial discipline in thesector is consistently maintained, and (iii) completion of the hydropower plants rehabilitation, and furtherdam safety improvement remain a Government's prionty.

7. Bank and Borrower Performance

Bank7.1 Lending:Identification

The Bank's performance in project identification was satisfactory. The project was identified in line withthe Bank's country assistance strategy which responded to a far-reaching reform program advanced by theGovemment in 1994-1996. The Bank carried out an Energy Sector Review to assist the Govermment incrafting its strategy for the energy sector. The Bank also agreed with the Govemment and otherinternational donors that power generation was an area in which the Bank's support could make a notabledifference. In this context, the Hydropower Rehabilitation and System Control Project was proposed inconsideration of the Bank's comparative advantage in the sector. An earlier Power Demand and SupplyOptions study of 1993 (report No.1 1561-UA) indicated that the rehabilitation of thermal and hydropowerplants was likely to result in the most significant net benefits for the power system. The priority ofreforming and upgrading the power sector was clearly outlined in the Government's strategy. The Bankprovided critical investment to the power industry along with donors' co-financing in a crucial period of thecountry's transition from a centrally planned to a market economy. At the same time, the Bank alsoinitiated the coordination of the donors' technical assistance to implement the Government's energy sectorstrategy, which was conducive to a proper enabling environment for this investment operation.

-20-

Preparation assistance

The Bank's performance in project preparation was satisfactory. The Ukrainian counterparts benefitedfrom early Bank involvement in the preparation process soon after project identification. The Bankundertook appropriate coordination with donors and Ukrainian counterparts. Feasibility studies werecarried out to prioritize the Government's hydropower rehabilitation programs and analyze therehabilitation needs of system-wide control and dispatch facilities. The studies were carried out byconsultants financed by trust funds of the governments of the Netherlands and Switzerland under thesupervision of the Ministry of Energy. The project investment activities were linked with specific policymeasures regarding tariffs and arrears in connection with the project entities.

Appraisal

The Bank's performance at appraisal was satisfactory. The Bank's appraisal team included experts with acomprehensive skill mix. The Government's and implementing agencies' commitment to the project wasanalyzed. Major risks related to pricing and non-payments were addressed through relevant conditions ofeffectiveness and loan covenants. The political risk of reversing sector reforms was also outlined.Capitalizing on the lesson learned from the first Bank project in Ukraine about the importance of technicalassistance (TA), technical assistance from the Govemments of Canada, Norway and Switzerland wasincorporated in the project scope to complement rehabilitation and water management activities andcompensate for the Borrower's insufficient experience with procurement and project management. Allrelevant safeguard policies were reviewed and discussed within the Bank and with the Government.

Continuity from identification through appraisal was good. Important project benefits were outlined andthe goal of achieving and preserving them served as a key incentive for the implementing agencies and theGovernment to pursue project sustainability.

The loan amount was commensurate with the project scope.

The performance indicators were designed to ensure adequate monitoring and reporting of projectimplementation progress. The institutional and commercial conditions of installing governors at the TPPscould have been assessed in greater detail in order to ensure that the system is ready for such investmnentand avoid cancellation of this sub-component. On the other hand, the project was brealing new grounds asthe first Bank investment operation in Ukraine.

7.2 Supervision.The Bank's performance during supervision was satisfactory in terms of (i) ensuring regularity ofsupervision missions and adequate skill-mix of Bank staff; (ii) providing timely responses to project issuesand involving management when called for by the complexity of the project matters; (iv) actively involvingthe field office in maintaining close working contacts with the local project counterparts; (v) applyingrealistic project performance ratings.

-21 -

The skill-mix and frequency of missions was aligned with the needs of implementation and responsivenessto the issues as they emerged. Close supervision and interaction with the Ukrainian counterparts facilitatedconstructive agreements on amending contracts, loan covenants and project scope in response to evolvingcompany needs, changes in sector structure and adverse external impacts. This approach prevented projectcancellation, and later allowed the extension of the loan closing date by 18 months to ultimately achieveproject objectives, although with delay and reduced physical scope of some components.

In addition, close and regular supervision enabled the Bank to take a pro-active stance and follow up oncases of serious noncompliance with Bank requirements, and even issue a threat to suspend the UE'scomponent when the company continuously failed to present a mid-term progress report and an updatedimplementation plan. The Bank's proactivity continued throughout the project through regularly followingup on key agreements on project financing, audits and completing project works under a realistic timeschedule.

Performance ratings were realistic and when required, "unsatisfactory" and "high risk" flags alerted sectorand country management about critical problems with project implementation and facilitated constructivediscussion to find solutions.

The Bank went to great lengths to ensure high quality advice to the Borrower. A world class dam safetyexpert assisted DHE in implementing current Bank safeguards on dam safety and solving difficult andunique dam safety issues related to some of the major and the longest dams in the world along the Dniepercascade.

The Bank developed a very good working relationship with the management and staff of the implementingagencies during supervision missions, site visits, and regular follow-up communications. A goodinteraction was also developed with the National Electricity Regulatory Commission, Energomarketadministration and the Ministry of Finance to ensure proper project financing. The Bank also maintainedclose contacts on project-related issues with the Ministry of Fuel and Energy despite frequent changes inthe Ministry's leadership.

The Bank should have been more proactive in guiding DHE about formally closing the process of selectionof project management consultants. Although the changes in project scope and the uncertaintiessurrounding the closing date of the project during the second half of 2000 may have made the intended TAinappropriate and unnecessary after the selection was initiated, the process could have been terminatedearlier.

7.3 Ot'erall Bankperformance:In view of the above assessments, overall Bank performance was satisfactory throughout the project cycle.

Borrower7.4 Preparation:

The Borrower's performance during project preparation is assessed as satisfactory. The Borrowerdemonstrated a high level of commitment and responsibility during project preparation since theGovernment assigned high priority to improving electricity supply as a main prerequisite for modemizingthe country's industry. Rehabilitation of the HPPs on Dnieper cascade was considered a key factor forimproving electricity supply in view of the important role of the HPPs in regulating frequency of the powersystem. In this context, there was close cooperation during preparation between the Government and the

- 22 -

Bank. The earlier work on preparing a comprehensive Government strategy for the energy sector ensuredthat the project was appropriate to Ukraine's needs.

7.5 Government implementation performance:

The Government's implementation performance is assessed as satisfactory since the project objectiveswere ultimately achieved with critical Government support, despite the deep financial crisis suffered duringproject implementation. The low level of payment collections in the power sector -the key constraint toproject implementation-- was overcome as a result of the Government's decisive measures aimed atfinancial recovery through elimination of barter and promissory note transactions, enforcing disconnectionsof delinquent electricity consumers along with other measures conducive to improving cash payments in thesector. In addition, the Government and the National Electricity Regulatory Commission adopted specificmeasures to ensure sufficient allocation of local funds to the project companies through Energomarket'sfunds distribution mechanism. The Government's effort to enhance economic growth and continue energyreforms within a broad program to improve institutions and govemance in the economy, with support fromthe Bank and donors, provided a framework which facilitated satisfactory completion of the project works.

7.6 Implementing Agency:The performance of the implementing agencies is rated as satisfactory because they managed to completethe revised scope of project works agreed with the Bank within the extended loan closing date.

Both DBE and UE suffered the adverse influence of a deep financial crisis in the sector which paralyzedimplementation of the DHE's component for more than six months and delayed for more than 20 monthsthe installation of some equipment under UE's component.

Despite the extemal difficulties, DHE demonstrated strong commitment and ownership with respect to theproject throughout the entire preparation and implementation periods. The company did its best to ensurethat all possible actions within the scope of its capacity and authority were undertaken to enable projectcompletion, including provision of adequate management and staffing. Interaction with Bank andGovernment counterparts on project issues was active and contributed to finding solutions to problems.Project reporting and audit compliance were adequate except for delays at the initial stage due to lack ofknowledge of Bank procedures.

NDC/UE's audits suffered delays due to irreconcilable discrepancies of accounts caused by the temporaryinclusion of Energomarket in the structure of the project agency. . UE's management was less persistent atthe early stage of the project in exploring all possible means to mitigate the impact of the external financialcrisis on project implementation.

UE's project staff had the necessary skills and experience which contributed to the final successful projectcompletion.

- 23 -

DHE and UE managed to comply with the agreed self financing ratio only after 2000 as a result of theimproved cash collections and local financing for the project. The companies did not incur any other majordebts except for the borrowing from the World Bank. This ensured compliance with the relevant projectcovenant not to incur debt unless a reasonable forecast of the beneficiaries' revenues and expendituresindicates an agreed debt service ratio throughout the term of the debt.

Both companies, and especially Dniprohydroenergo, had certain problems in conducting procurementefficiently throughout the project, particularly during the early stages of project implementation. In anumber of cases there were significant delays in concluding procurement due to protracted or improperevaluation of bids, vagueness in technical specifications, etc. Subsequently, these deficiencies werecorrected -- with significant involvement of Bank staff, - and did not result in violation of procurementpolicies and procedures, except the case of not properly closing the consultant selection process at DHE.These deficiencies did adversely impact on the project schedule. Despite this setback, DHE managementand current UE management did not spare efforts to coordinate the complex project works in a largelysuccessful manner.

7.7 Overall Borrowerperformance:In view of the above assessments, overall performance of the Borrower was satisfactory.

8. Lessons Learned

Assessment of the Government's long term commitment and ability to carry out reforms is a key aspect ofanalyzing overall project sustainability. It is important to have a reform-oriented government not onlyduring project preparation, but throughout the entire project cycle as well. The experience in Ukraine hasshown that a reversal of the initially progressive course of economic reforns has adversely affected theimplementation of the Bank's investment project