world bank document - documents &...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 10625-TA

STAFF APPRAISAL REPORT

TANZANIA

FINANCIAL AND LEGAL MANAGEMENT UPGRADING (FILMUP)PROJECT

JUNE 1, 1992

!Mi &;i.'A,,.-i ';'^

.- ep, rt N>i . 1:t;L h IA Yy' xs¢ AS-:1/B.ANEF^^'<. l' X7L:5u.l v'1 17, AIt',1

Southern Africa DepartmentIndustry and Energy Operations Division

This document has a restricted distribution and may be used by recipients only in the performance oftheir offici'al duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CUJRRENCY EQUIVALENT

Currency Unit = Tanzania Shillings (T.Sh)

US$1 = T.Sh 245 (at time )f appraisal)US$1 = T.Sh 291 (April 1992)

FISCAL YEARJuly 1 to June 30

MEASURESMetric System

ACRONYMS

Acc.G - Accountant-GeneralAGD Administrator-General's DivisionCAG - Controller and Auditor-GeneralCID - Civil and International DivisionCPA - Certified Public AccountantCPE - Continuing Professional EducationDPP - Director of Public ProsecutionsDSA - Dar es Salaam School of AccountancyFMCC - Financial Management Component CoordinatorIAA - Institute of Accountancy, ArushaIDLI - International Development Law InstituteIDM - Institute of Development Management, MzumbeIFM - Institute for Finance ManagementILC - International Legal CenterLD - Legislative DivisionLLM - Master of LawsLSCC - Legal Sector Component CoordinatorNBAA - National Board of Accountants and AuditorsNGOs - Non-Governmental OrganizationsNIC - National Investment CorporationNORAD - Norwegian Agency for Development CooperationOCAG - Office of the Controller and Auditor-GeneralODA - Overseas Development AdministrationRIPA - Royal Institute of Public AdministrationSIDA - Swedish International Development AuthorityTAA - Tanzania Association of AccountantsTAC - Tanzania Audit CorporationUSAID - United States Agency for International Development

FOR OFFICIAL USE ONLY

UNITED REPUBLIC OF TANZANIAFINANCIAL AND LEGAL MANAGEMENT UPGRADING (FILMUP) PROJECT

STAFF APPRAISAL REPORT

Table of ContentsPages

CREDIT AND PROJECT SUMMARY ............................... I iii

I. BACKGROUND

A. Introduction ................... 1..................B. The Accountancy and Auditing Prefessions .......................... 1C. Public Sector Financial Management & Institutions ...... .............. 3

The Accountant-General ........... ......................... 3The Controller and Auditor-General ............................ 3The Office of the Controller and Auditor-General ..... ............ 3The Tanzania Audit Corporation ........ ...................... 3Accountancy Education ........... .......................... 4The Institute of Finance Management .......................... 4The Institute of Accountancy, Arusha ........................... 4

D. The Legal System .............................................. 5Tlhe Judiciary .............................................. SAttorney-General's Office ........... ......................... 5Law Reform Commission ........... ......................... 6Department of Registration, Commercial Law

and Industrial Licensing ........ ....................... 7Training for the Legal Profession .............................. 7Commercial Laws and Related Legislation ...... ................. 7

H. SECTOR ISSUES .................................................. 8

A. Accounting and Auditing Issues .......... ......................... 8NBAA role regarding pre- and post - qualification Training .... ...... 8NBAA's issuing of Tanzanian Accounting & Auditing

Standards ............. ............................. 9NBAA's lack of capacity for enforcement ........................ 9Increasing the Number of Qualified Accountants ..... ............. 9The Shortage of accountants in the Public Service ..... ............ 9A special Accountancy Qualification for the Civil Service ..... ....... 9

B. Legal Sector Issues ................ .......................... .9

This report is based on the findings of an appraisal mission which visited Tanzania in March 1992.The mission consisted of Messrs. Uche Mbanefo (Mission Leader and Financial Analyst), andBernard Abeille (Sr. Architect/Procurement Specialist), Ms. Elizabeth Adu (Senior Counsel), andMs. Sonia Johnsen (Consultant). The lead adviser for the operation was John Graves and thepeer reviewer for the legal component was Mr. Hans Gruss. Ms. Dotilda Sidibe typed thereports. Mr. David Cook is the managing Division Chief, and Mr. Stephen Denning is theDepartment Director for the operation.

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

The proper limits of Bank involvement ........ ................. 10Lack of Knowledge of Modem Commercial Law ...... ........... 10The Overloading and Inefficiency of the Judiciary ...... ........... 10Lack of Relevant, Up-to-date Legal Materi.' ..... ..... .......... 10

C. Sector Development Strategies .... ............................ 10Accounting and Auditing .............................. 10The Legal Sector ............................. 11Past Role of the Bank and Lessons of Experience ................ 12

D. Rationale -`r Project Components ................................ 12II. THCE PROJECT ................................................. 13

A. Rationale and Objectives ....................................... 13Objectives . ................................................ 13

B. Project Components ............. ............................. 14Financial Management Upgrading ................................. 14

National Board of Accountants and Auditors .................... 14Office of the Controller and Auditor-General ................... 16Institute of Accountancy, Arusha ............................. 17Institute for Finance Management ............................ 18

Upgrading of the Legal Sector ................................... 19Attorney-General's Office ................................... 19Judiciary ................................................ 20Law Reform Commission ................................... 21Registrar of Companies .................................... 21

Studies ................................................. 21Legal Sector Study ............ ............................ 21Cost Recovery Study ....................................... 22TAC Study . ............................................. 22

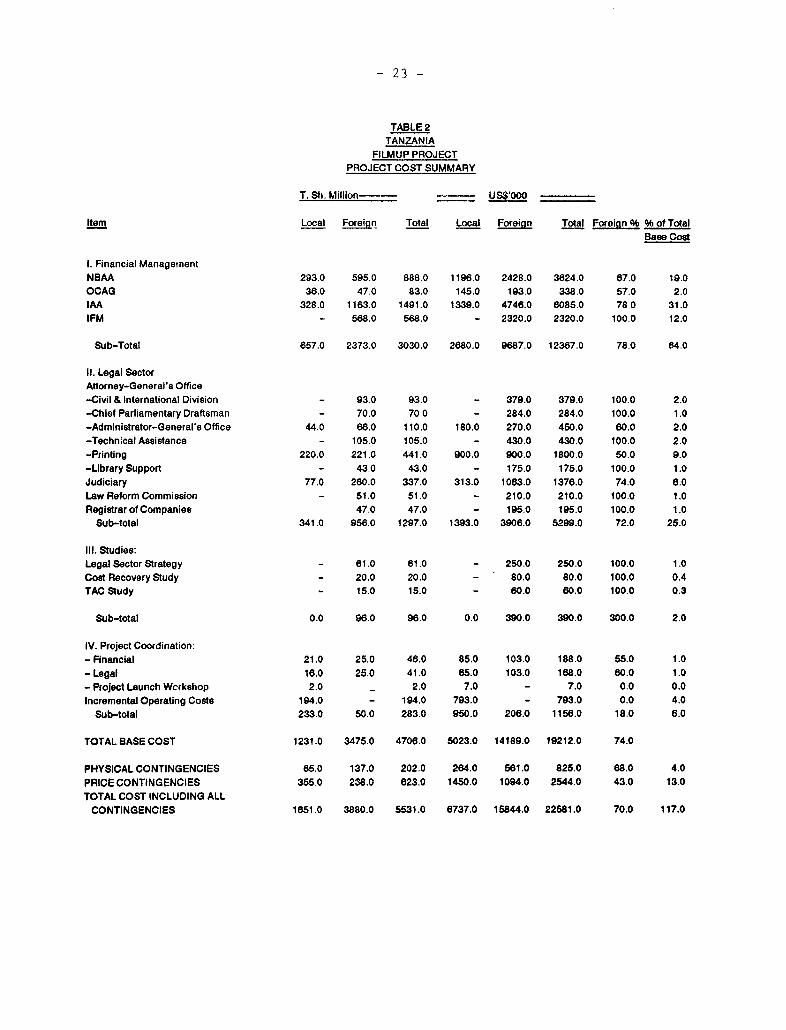

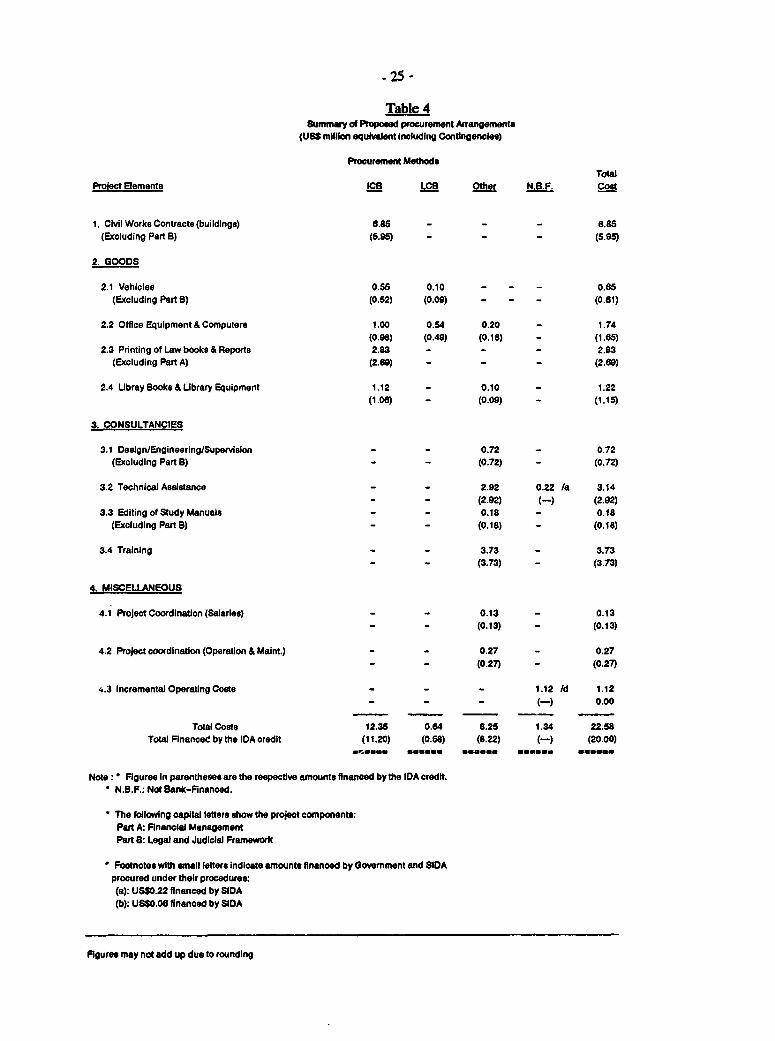

Project Coordination .............. ............................. 22C. Cost Estimates . .............................................. 22D. Financing . ................................................. 24E. Procurement . ............................................... 24F. Disbursement . ............................................... 28G. Accounting and Audit ............. ............................ 29

rV. PROJECT IMPLEMENTATION ...................................... 30A. Organization and Management .................................. 30B. Monitoring, Evaluation and Reporting ............................. 31C. Mid-term Review . ............................................. 31

V. BENEFITS, RISKS AND SUSTAINABILITY .... ........ .. ................. . 32A. Benefits ................................................. 32B. Impact on the Economic Reform Program and the Environment .... ..... 32

Environmental Aspects ..................................... 33C. Sustainability .................. ............................. 33D. Risks and Uncertainties ...................................... 33

VI ASSURANCES AND RECOMMENDATIONS .................... ....... 33

LIST OF TEXT TABLES

Table 1: Project Components SummaryTable 2: Prcject Costs SummaryTable 3: Project Financing PlanTable 4: Summary of Proposed Procurement Arrangements

LIST OF ANNEXES

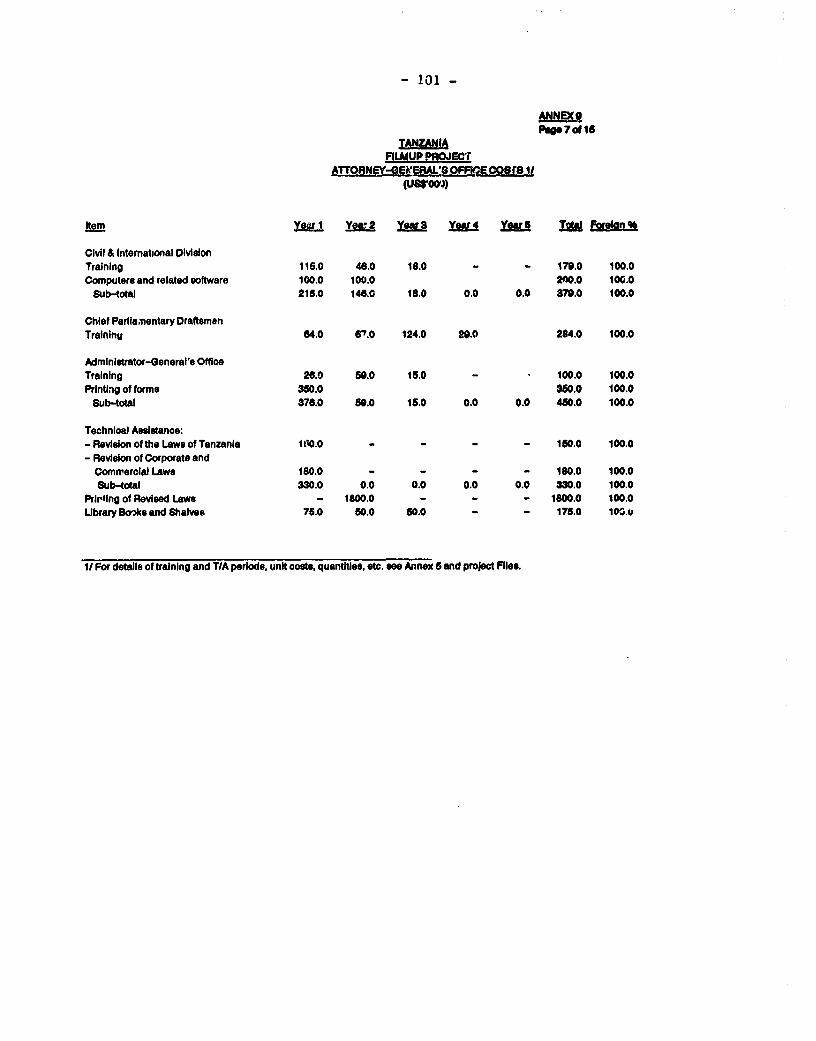

Annex 1: National Board of Accountants and Auditors (NBAA)Annex 2: O)ffice of Controller and Auditor-General (OCAG)Annex 3: Institute of Accountancy, Arusha (IAA)Annex 4: Institute for Finance Management (IFM)Annex 5: Direct Assistance to the Legal frameworkAnnex 6: Terms of Reference for the Legal Sector StudyAnnex 7: Terms of Reference for the Cost Recovery StudyAnnex 8: Terms of Reference for the TAC StudyAnnex 9: Project Cost Tables:

Page 1: Project Cost SummaryPage 2: Project Cost Summary Year by YearPage 3: NBAA CostsPage 4: OCAG CostsPage 5: IAA CostsPage 6: IFM CostsPage 7: Attomey General's Office CostsPage 8: Judiciary CostsPage 9: Law Reform Commission CostsPage 10: Studies CostsPage 11: Financial Component CoordinationPage 12: Legal Component CoordinationPage 13: Calculation of Contingencies - Foreign CostsPage 14: Calculation of Contingencies - Local CostsPage 15: Registrar of Companies

Annex 10: Estimated Schedule for DisbursementsAnnex 11: Project Implementation ScheduleAnnex 12: Supervision PlanAnnex 13: Selected Documents in the Project FileAnnex 14: Planning For Project Launch Workshop

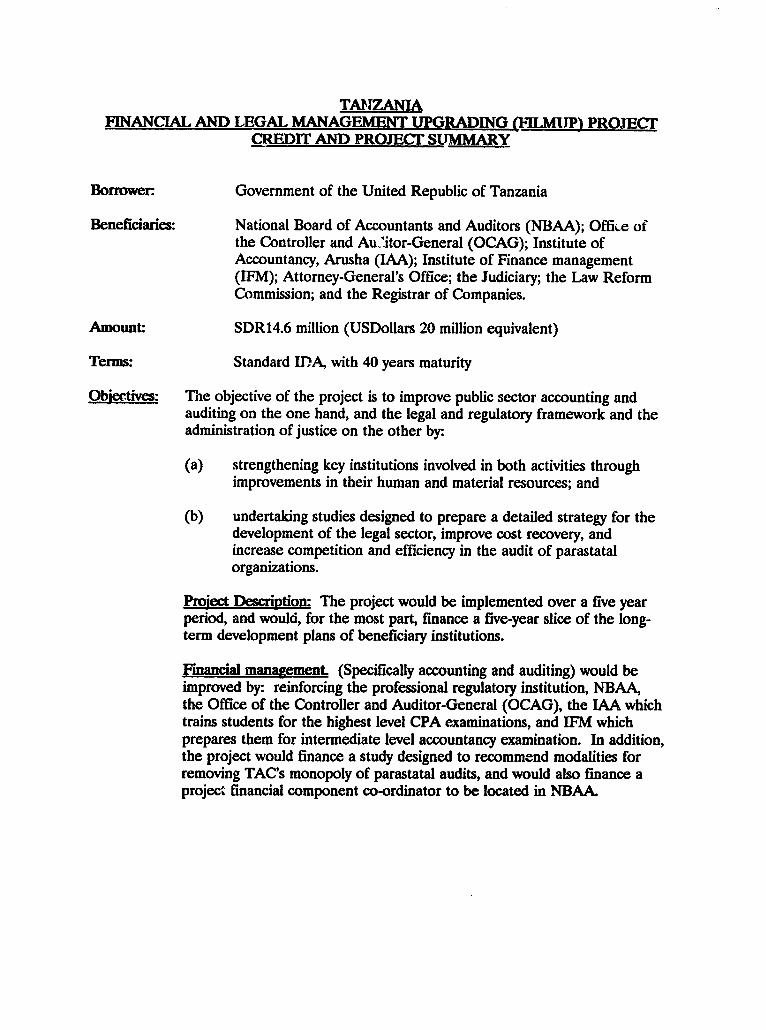

TAIZANIAFINANCIAL AND LEGAL MANAGEMENT UPGRADING (lILMIP) PROJECT

CRED1T AND PROJECT SUMMARY

Borrower. Government of the United Republic of Tanzania

Beneficiaries: National Board of Accountants and Auditors (NBAA); Offi.e ofthe Controller and Au,'itor-General (OCAG); Institute ofAccountancy, Arusha (LAA); Institute of Finance management(IFM); Attorney-General's Office; the Judiciary; the Law ReformCommission; and the Registrar of Companies.

Amount: SDR14.6 million (USDollars 20 million equivalent)

Terms: Standard IDA, with 40 years maturity

Objectives: The objective of the project is to improve public sector accounting andauditing on the one hand, and the legal and regulatory framework and theadministration of justice on the other by:

(a) strengthening key institutions involved in both activities throughimprovements in their human and material resources; and

(b) undertaking studies designed to prepare a detailed strategy for thedevelopment of the legal sector, improve cost recovery, andincrease competition and efficiency in the audit of parastatalorganizations.

Project Description The project would be implemented over a five yearperiod, and would, for the most part, finance a five-year slice of the long-term development plans of beneficiary institutions.

Fmancial management. (Specifically accounting and auditing) would beimproved by: reinforcing the professional regulatory institution, NBAA,the Office of the Controller and Auditor-General (OCAG), the IAA whichtrains students for the highest level CPA examinations, and IFM whichprepares them for intermediate level accountancy examination. In addition,the project would finance a study designed to recommend modalities forremoving TAC's monopoly of parastatal audits, and would also finance aproject financial component co-ordinator to be located in NBAA.

- ii -

Dge.!awA and regulatory framework would be improved by:

- development of a long-term strategy and implementation programfor the legal sector;

- strengthening the Attorney-General's Department, the Judiciary,the Registrar of Companies and the Law Reform Commission,through the provision of staff training, management informationsyste.ns, basic office equipment and publications for law libraries;

- (i) revision and publication of the Laws of Tanzania, and (ii) reviewof laws relevant to private sector development, the parastatalreform program and privatization; and

- a project legal component co-ordinator to be located in the officeof the Attorney-General.

The Cost-recovery study would explore ways of recovering more of theoperating costs of all the beneficiary institutions (see above) involved inboth the financial and the legal components of the project.

Benefits: The project is expected to result in both quantitative andqualitative improvements in the services provided by beneficiaryinstitutions. The pass rates achieved by IAA and IFM students in nationalaccountancy examinations are expected to increase. The quality ofaccounting practice would improve through the issue and enforcement ofaccounting and auditing standards. Many of the country's out-of-date lawswould be revised and made more accessible. Through its impact onaccountability and the legal framework, the project would provide thepractical under pinnings for the policy changes being introduced throughthe structural adjustment program.

Risl The only foreseen risk lies in possible inability of the beneficiaryagencies to absorb and put to good use the resources and improvementsbeing introduced through the project. However, built-in measures, such as,raining, technical assistance, highly de-centralized yet well-coordinatedproject management, and gradual phasing of implementation are alldesigned to minimize that risk.

- iii -

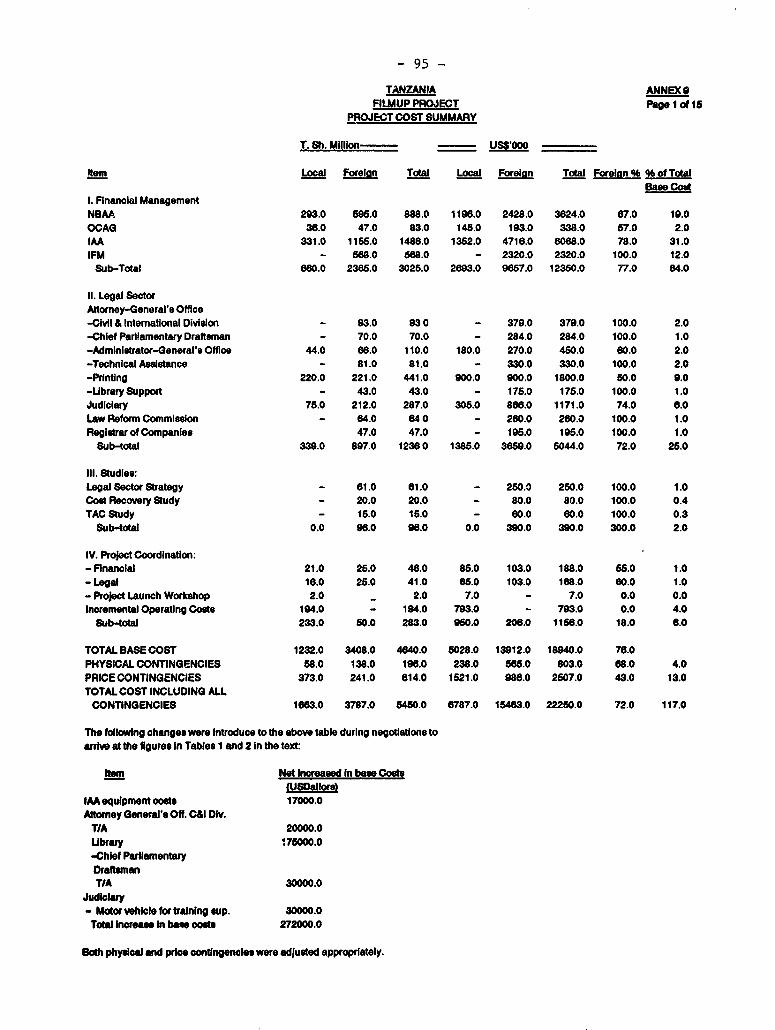

L ESTIMATED COSIS AND FNANCING

Project Cost SummaryUSS Mfllion

Local Forljo Total Of Total

Improvement of Financial Management 2.7 9.6 12.3 64

Improvement of the Legal Framework 1.4 3.9 5.3 28

Studies - 0.4 0.4 2

Project Coordination 0.2 0.2 0.4 2

Incremental Operating Cost 0.8 - 0.8 4

Total Base Cost 5.1 14.1 19.2 100

Physical Contingencies 0.2 0.6 0.8 4

Price Contingencies 1.4 1.1 2.5 13

Total Project Costs 6.7 15.8 22.5 117

Flnancing Plan USS Milion

Local Foreign Total

IDA 4.3 15.7 20.0Government of Tanzania 2.3 0.0 2.3SIDA 0.1 0.1 0.2

TOTAL 6.7 15.8 22.5

2. ESTMA-TED IDA DISBURSEMENT SCHEDULE(USS Million)

1DA Fscal Year 1993 1994 1995 1996 1997 1998

Annual 0.8 4.6 7.0 6.4 0.7 0.4

Cumulative 0.8 5.4 12.4 18.9 19.6 20.0

Economic Rate of Return: Not Applicable

1. BACKGROUND

A. Introduction

1.01 This report describes the first attempt by the World Bank to provide direct financialassistance to two key areas critical to the efficiency of the public service, to the rule of law, and inparticular, to the success of Tanzania's current economic reform program. These two areas are publicsector financial management (specifically accounting and auditing) on the one hand, and the legal andregulatory framework on the otht!;.

1.02 Public sector financial accoun.ability has been a subject of continuing concern for manyyears, not only with the Government, which has created numerous institutions, and issued Presidentialproclamations on the subject, but also with bilateral donors and private organizations, which havecarried out studies, and created or supported several training and other institutions in an effort toimprove it.

1.03 The legal f.amework, dlthough it has not received as much public or doncr attention aspublic sector accountability, is nevertheless, equipped with the usual institttions for the legalframework and administration of justice found in most former British colonies and protectorates.Like the financial institutions, the legal institutions were designed to serve an economic system basedon extensive public ownership of the means of production. Now that Tanzania is moving away fromthat system, there is a need to adapt the institutions to service a libera!ized economy. A successfuleconomic reform program and the development of an active private sector depend on goodaccounting and auditing systems, as well as a system of laws, regulations and administration of justicewhich is transparent, easilv accessible, consistently applied but at the same time dynamic and sensitiveto the changing needs of the society. The Economic Recovery program has been underway foralmost six years and has dramatically changed the business orientation of the country. As theprogram is proceeding it has become increasingly clear that there are serious weaknesses that needto be addressed in the financial, legal and judicial systems. In order to increase investor confidence,it is essential that these reforms be undertaken.

1.04 Government, Bank, and donor interests in public financial accountability are similar andnon-controversial: good accounting and auditing systems are essential for good economicmanagement. With regard to the legal framework, however, the Bank approaches issues of legalreform from the stand-point of economic efficiency, but many bilateral donors, now keenly interestedin the legal framework, approach it from the point of view of human rights and good governance.The two interests converge in practice, not only because good "economic" laws governing, forexample, rights to personal property, serve as a logical starting point for good governance, but alsobecause the same legal institutions (e.g. the Ministry of Justice) administer the legal framework forbotb economic and political rights. Nevertheless, as will be discussed further in Chapter II, thisdifference of approach has to be taken into account in deciding specific areas of intervention by theBank and bilateral donors.

B. The Accountancy and Auditing Professions

1.05 The accountancy and auditing professions in Tanzania have developed along a patternwhich, although it is not unique, is certainly unusual in some important respects. As in most otherAfrican countries, T&_ania's first accountants and auditors were trained abroad, mostly in the UnitedKingdom, Canada, the United States, and other English-speaking countries. In most other countries

-2 -

these foreign-trained professionals formed a national Institute of Accountants - a member-owned self-regulatory body - which later sought and icceived official 'ancticn, generally by being incorporatedthrough a special Act of Parliament.

1.06 In Tanzania the typical professional evolution descrined above was pre-empted by theAccountants and Auditors (Registration) Act of 1972, which created ti;e National Board ofAccountants and Auditors (NBAA) as a statutory body, with which all accountants and auditorspractising in Tanzania have to be registered. Its main functions are to conduct examinations, approveand register accountants and auditors, and generally regulate the activities and conduct of accountantsand auditors. Due to inadequate resources, it is far behind in its program of introducing accoundingand auditing standards in Tanzania. In addition, it has no means of enforcing the few internationalstandards it has adopted. The NBAA offers an accounting technician qualification as well as aprofessional Certified Public Accountant (CPA) qualification. In addition to its student educationprogram, the NBAA organizes short seminars for practicing accountants. Despite its manyachievements, the NBAA is constrained in the activities it can undertake by both staff capacity andfinance. Its offices are also scattered in three different buildings and locatio.ns a source ofconsiderable administrative cost and inefficiency which this project would address.

1.07 About a decade after NBAA was established, Tanzania's accountants and auditors,frustrated by the problems of having their interests represented by a parastatal body over which theyhad no control, formed the Tanzania Association of Accountants (TAA) to represent the interestsof the profession. However, since NBAA, through its enabling legislation, had been endowed withthe power and functions nL mally belonging to a member-owned institute, TAA has had to contentitself with the role of a more informal organization providing the framework for social contacts,lectures, and other events.

1.08 Despite the situation described in the above paragraph, ar.1 a certain amount ofduplication (e.g. in the area of continued professional education for practicing accountants andauditors), there is no serious conflict between NBAA and TAA. This is largely because everymember of TAA is also a registered member of NBAA, and practically every Board member ofNBAA is also a member of TAA

1.09 Currently, Government budgetary allocations pay for ab out one-half of NBAA's recurrentexpenditure. The other half is recovered from members. Government also provides TAA with afixed annual subvention of TSh2 million. With Tanzanian salaries as low as they are, the fact thatmost Certified Public Accountants (CPAs) pay annual subscriptions to both NBAA and TAA meansthat neither organization can raise enough money from members to (ully cover its operating costs.

1.10 For all the reasons discussed above, the roles of the 14BAA and TAA need to be moreclearly defined in the future. Eventually, a situation more akin to that in most other countries couldbe envisaged, in which TAA would take over all the self-regulatory and professional control andpromotional activities normally carried out by Institutes of CPAs in other countries, and be the solerecipient of members' subscriptions, while NBAA would limit itself to the issue and enforcement ofaccounting standards, and would be financed entirely out of the Government budget. However, thepace of this evolution cannot be forced, because it will depend on TAA's demonstrated and declaredreadiness to take on more responsibilities.

1.11 Pass rates in NBAA examination are around 20%, and the throughput of qualified peopleis very slow, leaving considerable gaps in the market place. A 1989 study estimated that Tanzania

-3.

was short of about 2,000 fully-qualified and about 5600 semi-qualified accountants, as well as ovcr15,000 accounting technicians.

r. Public Sector Fmancial Management and Institutions

1.12 The Accountant-General (AG) of Tanzania ad his staff are responsible for themaintenance of all Government accounts. The staff are posted to all the Ministries, where theyprepare the accounts of all Government units, which they later consolidate at the Treasury, wherethe Accountant-General's office is located. The Acc-G has had difficulty in attracting and keepingstaff, partly as a result of the overall shortage of accountants noted above, and partly because of pooisalary levels (despite re-classification of accountancy as a rare skill . >-w years ago). The Acc-G'soffice has been receiving assistance from several bilateral donors.

1.13 The Controller and Auditor-General (CAG) is the single most important watch-Jog ofpublic finances in Tanzania. He is required by Section 143 of the Constitution of Tanzania amongother things:

(a) to grant to the Treasury credits on the Exchequer Account and satisfy himselfthat all monies appropriated by Act of Parliament and disbursed have beenapplied to the purpose for which they were appropriated and that theexpenditure conforms to the authority which governs it; and

(b) at least once in every year to audit and report upon the public accounts of theUnited Republic, the accounts of all officers and authorities of the Governmentof the United Republic, the accounts of all the courts of the United Republic andthe accounts of the Clerk of the National Assembly.

1.14 The Office of the Controller and Auditor-General (OCAG) has twenty branch offices -one in each Region. It has on its staff some 100 auditors with different levels of accountancy

qualifications. It shares the Acc-G's problems of recruiting and retaining qualified staff, and for thesame reasons. For several years, the OCAG has received the assistance of the British OverseasDwvelopment Administration (ODA), and it is currently negotiating a second phase of that assistancewl ich is expected to include assistance with the management of audits, training in the audit ofco nputerized audit systems, and the training of trainers. In addition to inadequate staff resources,the OCAG also lacks office equipment, and enough transportation to cover the entire territo,y ofTar. zania.

1.15 The Tanzaia Audit Corporation (TAC) is a pa-'statal institution which, until recently,enjoyed a virtual monopoly of auditing the accounts of I, 400 or so parastatal institutions inTanzania. Following the Arusha Declaration in February 1967, the Treasury tried to get theController and Auditor-General to take on the audit of all the parastatals, in exercise of his statutoryduties (para. 1.13 above). The CAG, however, pointed out that his staff of civil service auditors didnot possess the requisite commercial audit experience to audit the accounts of revenue-earningparastatal entities. This prompted the Goverment to set up TAC under the Tanzania AuditCorporation Act of February 1, 1968. Although TAC's chairman submits his annual report to thePresident of Tanzania, TAC's accounts are submitted to, and audited by, the Controller and Auditor-General, who stil has the statutory power to appoint any auditor to audit any parastatal.

4 -

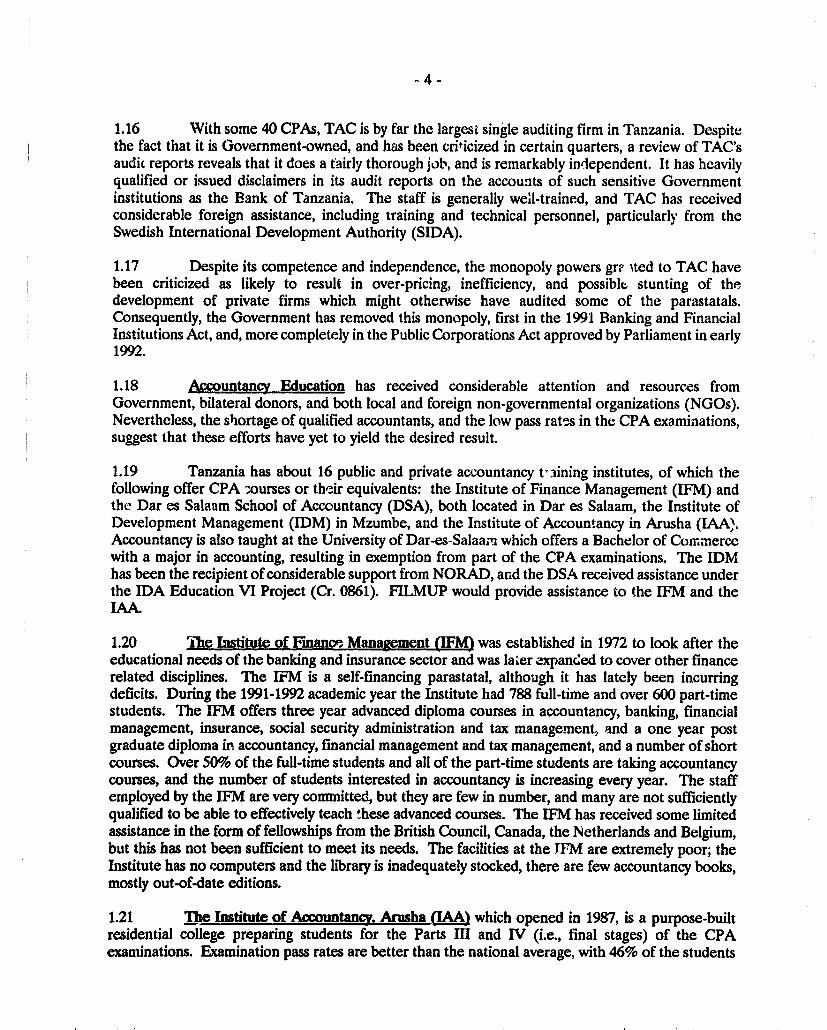

1.16 With some 40 CPAs, TAC is by far the largest single auditing firm in Tanzania. Despitethe fact that it is Government-owned, and has been criticized in certain quarters, a review of TAC'saudit reports reveals that it does a tairly thorough job, and is remarkably independent. It has heavilyqualified or issued disclaimers in its audit reports on the accounts of such sensitive Governmentinstitutions as the Bank of Tanzania. The staff is generally well-trained, and TAC has receivedconsiderable foreign assistance, including training and technical personnel, particularly from theSwedish International Development Authority (SIDA).

1.17 Despite its competence and independence, the monopoly powers gr? ited to TAC havebeen criticized as likely to result in over-pricing, inefficiency, and possible stunting of thedevelopment of private firms which might otherwise have audited some of the parastatals.Consequently, the Government has removed this monopoly, first in the 1991 Banking and FinancialInstitutions Act, and, more completely in the Public Corporations Act approved by Parliament in early1992.

1.18 Accountancy Education has received considerable attention and resources fromGovernment, bilateral donors, and both local and foreign non-governmental organizations (NGOs).Nevertheless, the shortage of qualified accountants, and the low pass rates in the CPA examinations,suggest that these efforts have yet to yield the desired result.

1.19 Tanzania has about 16 public and private accountancy t'3ining institutes, of which thefollowing offer CPA mourses or their equivalents: the Institute of Finance Management (IFM) andthe Dar es Salaam School of Accountancy (DSA), both located in Dar es Salaam, the Institute ofDevelopment Management (IDM) in Mzumbe, and the Institute of Accountancy in Arusha (LAA).Accountancy is also taught at the University of Dar-es-Salaam which offers a Bachelor of Commercewith a major in accounting, resulting in exemption from part of the CPA examinations. The IDMhas been the recipient of considerable support from NORAD, and the DSA received assistance underthe IDA Education VI Project (Cr. 0861). FILMUP would provide assistance to the IFM and the

1.20 The Institute of Fmanoe Management (FM) was established in 1972 to look after theeducational needs of the banking and insurance sector and was laier -xpanded to cover other financerelated disciplines. The IEM is a self-financing parastatal, although it has lately been incurringdeficits. During the 1991-1992 academic year the Institute had 788 full-time and over 600 part-timestudents. The IFM offers three year advanced diploma courses in accountancy, banking, financialmanagement, insurance, social security administration and tax management, and a one year postgraduate diploma in accountancy, financial management and tax management, and a number of shortcourses. Over 50% of the full-time students and all of the part-time students are taking accountancycourses, and the number of students interested in accountancy is increasing every year. The staffemployed by the IFM are very conmitted, but they are few in number, and many are not sufficientlyqualified to be able to effectively teach these advanced courses. The IFM has received some limitedassistance in the form of fellowships from the British Council, Canada, the Netherlands and Belgium,but this has not been sufficient to meet its needs. The facilities at the JFM are extremely poor; theInstitute has no computers and the library is inadequately stocked, there are few accountancy books,mostly out-of-date editions.

1.21 'he Institute of Acoauntancy. Arusha (af) which opened in 1987, is a purpose-builtresidential college preparing students for the Parts III and IV (i.e., final stages) of the CPAexaminations. Examination pass rates are better than the national average, with 46% of the students

-5 -

passing the dinal examinations at the May 1991 examination sitting. In addit;on, the Institute runsshort courses in accounting and related subjects, and revision courses for the CPA examination. TheInstitute is able to accommodate 180 students, and has plans for an additional hostel which willincrease its capacity to 300. The current hostel capacity greatly restricts the numbers of students thatcan attend the courses. The Institute has recently built a new lecture theater, but it does not havesufficient funds to furnish it. Lack of funds has also resulted in an inadequately-equipped kitchenand dining room and a poorly resourced library. Staffing is a major problem, and for many subjectsthe LAA has difficulty in attracting and retaining lecturers. As with the IFM, the IAA has receivedlittle donor support.

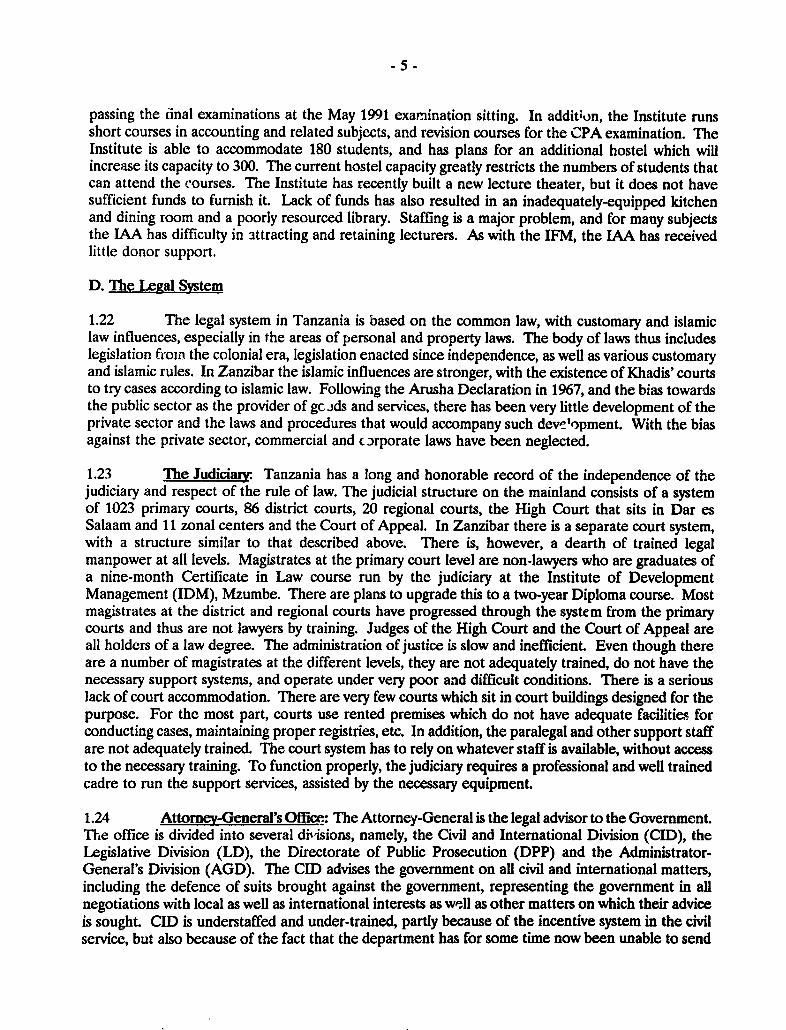

D. The Legal System

1.22 The legal system in Tanzania is based on the common law, with customary and islamiclaw influences, especially in the areas of personal and property laws. The body of laws thus includeslegislation from the colonial era, legislation enacted since independence, as well as various customaryand islamic rules. In Zanzibar the islamic influences are stronger, with the existence of Khadis' courtsto try cases according to islamic law. Following the Arusha Declaration in 1967, and the bias towardsthe public sector as the provider of gcids and services, there has been very little development of theprivate sector and the laws and procedures that would accompany such development. With the biasagainst the private sector, commercial and corporate laws have been neglected.

1.23 The Judicily. Tanzania has a long and honorable record of the independence of thejudiciary and respect of the rule of law. The judicial structure on the mainland consists of a systemof 1023 primary courts, 86 district courts, 20 regional courts, the High Court that sits in Dar esSalaam and 11 zonal centers and the Court of Appeal. In Zanzibar there is a separate court system,with a structure similar to that described above. There is, however, a dearth of trained legalmanpower at all levels. Magistrates at the primary court level are non-lawyers who are graduates ofa nine-month Certificate in Law course run by the judiciary at the Institute of DevelopmentManagement (IDM), Mzumbe. There are plans to upgrade this to a two-year Diploma course. Mostmagistrates at the district and regional courts have progressed through the system from the primarycourts and thus are not lawyers by training. Judges of the High Court and the Court of Appeal areall holders of a law degree. The administration of justice is slow and inefficient. Even though thereare a number of magistrates at the different levels, they are not adequately trained, do not have thenecessary support systems, and operate under very poor and difficult conditions. There is a seriouslack of court accommodation. There are very few courts which sit in court buildings designed for thepurpose. For the most part, courts use rented premises which do not have adequate facilities forconducting cases, maintaining proper registries, etc. In addition, the paralegal and other support staffare not adequately trained. The court system has to rely on whatever staff is available, without accessto the necessary training. To function properly, the judiciary requires a professional and well trainedcadre to run the support services, assisted by the necessary equipment.

1.24 Attorney General's Offlce: The Attorney-General is the legal advisor to the Government.The office is divided into several dirisions, namely, the Civil and International Division (CII)), theLegislative Division (LD), the Directorate of Public Prosecution (DPP) and the Administrator-General's Division (AGD). The CID advises the government on all civil and international matters,including the defence of suits brought against the government, representing the government in allnegotiations with local as well as international interests as well as other matters on which their adviceis sought. CID is understaffed and under-trained, partly because of the incentive system in the civilservice, but also because of the fact that the department has for some time now been unable to send

- 6-

its staff abroad for further training and exposure. LD comprises the office of the Chief ParliamentaryDraftsman who is responsible for the drafting of all legislation in Tanzania. In addition, the officeis entrusted with the task of publishing regular revised Laws of Tanzania as well as annualsupplements. Again, the office is Hi-equipped to do this, and there are not enough trained legislativedraftsmen to keep up with the regular workload. There has not been a revision of the Laws ofTanzania since 1965. This makes it impossible for practitioners and judges alike to know at any pointin time what the law on any give subject is. It makes relying on precedent difficult, especially as theTanzania Law Reports have not been printed since 1982. AGD is responsible for the registrationof births, marriages and deaths. It is also responsible for administering estates of persons who dieintestate. DPP is in charge of all prosecutions at the senior courts namely the High Court andregional courts. Again most the counsel are fresh out of law school, with very little experience, andnormally do not stay long in the department.

1.25 Law Reform Commission: The Law Reform Commission (LRC), which was establishedpursuant to the Law Reform Commission of Tanzania Act, No. 3 of 1980, is charged with thefunction of taking and keeping under review all the laws of Tanzania with a view to their systematicdevelopment and reform. The functions are set out in more detail in Section 4(2) of the Act, namelyto:

(a) review any law or branch of the law and propose measures necessary for:

(i) bringing the law or branch of the law into accord with currentcircumstances of Tanzania;

(ii) eliminating anomalies or other defects in the law, repealing obsoleteor unnecessary laws and reducing the number of separate enactments;and

(iii) the proper codification and simplification of that law or branch of law;

(b) consider and advise on proposals for the adoption of new or more effectivemethods for the administration of the law and the dispensation of justice;

(c) from time to time, prepare and submit to the Attorney-General programs for theexamination of different branches of law with a view to reforming those laws,including recommendations as to the agency, whether the commission or anotherbody, by which any such examination should be carried out;

(d) at the request of the Attomey-General, prepare comprehensive programs for theconsolidation and revision of laws, and undertake the preparation of any draftbills pursuant to an such program approved by the Attorney-General; and

(e) at the instance of the Attomey-General provide advice and assistance to anyministry or department or any public authority or institution by undertaking theexamination of any particular branch of the law and making recommendations forreform so as to bring it into accord with current circumstances.

1.26 The LRC thus has a major role to play in the legal reform process. In this regard its role,particularly at this time, is crucial, in order to put in motion a review of laws which impact, inter alia,

- 7 -

on the private sector and its activities. The LRC is however currently ill-equipped to undertake thistask. It has neither the staff, equipment nor resources. Since its establishment LRC has carried outor is in the process of carrying out reviews in several areas, e.g. Private legal practice, delays in thedisposal of civil suits, personal laws etc. As with the other agencies the needs of the LRC are in theareas of training, access to reference and research materials, equipment, and the establishment of anappropriate data storage and retrieval system.

1.27 Registrar of Companies. This is the law department of the Ministry of Industries andTrade. The Department is responsible for the following:

(a) Commercial and Industrial Laws, registration of companies, business names,industrial licenses and hire purchases;

.q Intellectual Property Laws, registration of patents, trade marks, industrial designs,etc.; and

(c) Administration of Copyright Laws.The department is also responsible for giving legal advice to government, parastatals and the privatesector on commercial and intellectual property matters. The office is operating under very difficultconditions with very little office space, poor filing space, poorly trained staff, and poor equipment.The department has about four hundred thousand files, but has no computers. The informationretrieval system is manual and inefficient. There is no library. This office should be efficiently runwith an information management system which makes it easy for companies to obtain information thatthey need in a timely fashion.

1.28 Training for the Legal Profession: Tanzania has a long record of training of lawyers.The Law Faculty at the University of Dar es Salaam (UDS) is the only institution in Tanzaniaoffering formal legal education at the degree level. It has been training lawyers for decades. Anumber of East African lawyers trained in the 1960s and 1970s were trained there. The Law Facultyoffers LLB and LLM courses. The UrS generally and the Law Faculty in particular were in theforefront of the activism following the Arusha Declaration, consequently the content of the lawtaught was biased. For example, company law was not taught as a subject for a long time, but as partof a course on public enterprise law. In addition, the training unit in the judiciary and the Instituteof Development Management (IDM), Mzumbe, run a nine month certificate of law course forPrimary Court Magistrates. Further training for the legal profession is undertaken outside thecountry on an ad hoc basis, as and when there is money available, usually from donors.

1.29 Commercial Laws and Related Legislation: For some of the reasons which have beenmentioned above, the existing laws dealing with commercial matters have been neglected. Apart fromvery few changes, the Companies Ordinance, bankruptcy and other commercial laws date from thecolonial era. The Companies Ordinance is based on the 1938 English companies legislation and isthus totally outdated. This and other legislation have to be revised and consolidated where necessary.It is also necessary to ensure the legislation meets the needs of modem commercial transactions.There is the recognition of the need to update the laws governing the entry, governance and exit ofcompanies. In addition, there are various other laws dealing with tax, foreign exchange, licensing,bankruptcy, land tenure etc., which need to be reviewed by the Government. Some steps havealready been taken in this regard. A Banking and Financial Institutions Act was enacted in 1991, anda new Public Corporations Act and Foreign Exchange Act have already been enacted. What is now

- 8 -

needed is a thorough review of existing commercial and related legislation starting with theCompanies Ordinance and associated regulations, which would be undertaken under the Project.

IL SECTOR ISSUES

A Accounting and Auditing Issues

2.01 In addition to the problems discussed in Chapter 1, the main issues in accounting andauditing have to do with:

(a) the proper role of the National Board of Accountants and Auditors (NBAA),particularly with regard to its training of candidates for its own examinations, andits relation with the Tanzania Association of Accountants (TAA);

(b) how best to increase the number of qualified accountants in the country;

(c) the extent to which staff shortages in the public sector are more the result ofpoor renumeration than of the inadequate numbers of accountants in theeconomy as a whole;

(d) the need for NBAA to rapidly issue accounting and auditing standardsconforming to international standards;

(e) NBAA's capacity to enforce the standards it issues;

(f) the development of continuing professional education (CPE) for practicingaccountants and auditors;

(g) the desirability of introducing a special accountancy syllabus and qualification forpublic sector accountants; and

(h) other measures for strengthening NBAA and improving its effectiveness.

2.02 Most, but not all, of the above issues relate to the NBAA, its role, capacity andeffectiveness. Given the pivotal role of that institution in the sector, those issues are discussed firstbelow, followed by discussion of the other issues.

2.03 NBAA's role reigarding prequalification and postqualification training has beendiscussed in a number of reports. Many observers see a possible conflict of interests in NBAA'straining of students for its own pre-qualification examinations. NBAA is therefore withdrawingcompletely from this activity. IAA has become an independent state-owned institution instead of oneowned and directed by NBAA There are numerous training institutions in the country and NBAAis encouraging the creation of more, particularly privately-owned, and in areas not adequately servedby state-owned schools. NBAA continues to provide continuing professional education along sidethe TAA, but this is an activity from which NBAA should probably withdraw as soon as the TAAdemonstrates its capacity to provide it adequately.

-9-

2.04 NBAA's issuing of Tanzanian accounting and auditing standards has lagged well behindthe publication of international standards which NBAA is trying to adopt after adapting them toTanzanian laws and conditions. This is largely a result of inadequate staff and financial resources -one of the main problems this project is designed to address. Even for those standards it has issued,NBAA lacks the capacity for enforcement again largely because it does not have enough staff withthe requisite qualifications and experience. Other inadequacies hindering NBAA's effectivenessinclude its difficulties in organizing and moderating examinations and maintaining a members' register,and the fact that it operates from three different offices in Dar-es-Salaam, and needs to move intoone location. All these issues are being addressed through a broad-based sector development strategyin which several donors are now participating with the Government, and of which this project formsan integral part (see Section C below).

2.05 Increasine the number of qualified accountants in the country has been a primaryconcem. NBAA has so far successfully resisted suggestions that it should lower its examinationstandards in order to improve the pass rates in its examinations (currently about 20% nationwide).There is now a consensus that the right way to increase the number of accountants is to improvetraining quality, not to reduce examination requirements. NBAA (in common with most Tanzanians)is concemed to ensure that a Tanzanian-qualified Certified Public Accountant (CPA) should be seento be in every way as well-qualified professionally as a CPA from any other country.

2.06 The shortage of accountants in the public sector is seen by many as resulting, not justfrom the national shortage, but also from the poor salaries paid in the civil service. As of March 1992the most highly-paid accountants in the civil service were eaming less than TSh25,000 (aboutUS$100) a month. This is after a decision by the Govemment a few years ago to pay a salarypremiumn to accountants by classifying their skill (along with medicine and engineering, for example)as rare. Although free housing sometimes adds ten times the cash salary to the total remuneration,the cash part of the package is still too low to attract and keep CPAs in the civil service. A policybased on eliminating free housing but paying a much higher cash salary would save money for theGovernment while providing the employee with a much larger discretionary income to spend oneither private housing or something else. This issue needs to be tackled in the context of the overallcivil service reform, as it goes beyond the accounting, auditing and legal professions. It is, in fact,being addressed by the Public Sector Adjustment Credit currently rinder preparation.

2.07 The question of a special accountancy qualification for the civil service is related to thatdiscussed in the preceding paragraph. Tanzania's CPA training (as with such training in mostcountries world wide) although commendable efforts have been made to broaden it, is still heavilybiased in favor of commercial or private sector accounting. Part of the 'iew strategy on which NBAAis currently embarking, therefore, involves the introduction of a new qualification: the AdvancedDiploma in Government Accounting and Auditing. NBAA has approved a detailed plan forintroducing this qualification, and has applied to the ODA for financing to implement it. Apart fromthe hope of making this qualification more relevant to the needs of the civil service, it is also hopedthat it will result in Government being able to retain more qualified accountants in its service.

B. Legal Sector Issues

2.08 The major issues include:

(a) the proper limits of Bank involvement;

- 10-

(b) the legal profession's lack of knowledge of commercial and corporate matters;

(c) the inadequate capacity of the judiciary to cope with its workload; and

(d) lack of relevant up-to-date legal material in Tanzania.

2.09 'he proper limits of Bank involvement constitutes an issue. The Bank's mandate has todo primarily with economic development, rather than with human rights, the police force, or prisonservices. It will be necessary, therefore, in designing assistance to this sector, to clearly define wherethe Bank's mandate ends, but that of its bilateral partners continues. Already there is clear evidencethat many donors are keenly interested in pursuing human rights aspects of the rule of law andrelated matters in which the Bank would not normally be involved. This crucial issue would be dealtwith in the proposed study.

2.10 Lack of knowledge of modem commercial law and practioe poses some danger for theeconomic liberalization program now underway in Tanzania. There is a shortage of lawyersconversant with commercial and corporate matters in the various government agencies (including thejudiciary), as well as in private practice. This problem would be directly addressed through thisproject.

2.11 The overloading and inefficiency of the judiciarg constitute a much bigger problem whichcan be addressed directly by this project only in part, but would be examined in depth during thesector study. Skill levels are generally poor. Lower level personnel (primary court magistrates andcourt registry staff) in particular are inadequately trained. The project would begin to address thesetraining needs.

2.12 There is a lack of relevant. uv-to-date legal material to enable lawyers and judges toundertake their tasks. The Tanzanian Law Reports have not been printed since 1982, and there hasnot been a revision of the Laws of Tanzania (as required by statute) since 1965. This should be doneat least every ten years. In addition, the law libraries are totally inadequate. This issue would alsobe directly addressed by the project.

C. Sector Development Strateces

2.13 Accounting and Auditing. During the last ten years numerous inquiries have beenconducted into the state of the accountancy and auditing professions and many recommnrldations putforward for their development. In 1991, under the auspices of the IDA-financeL FinancialAdjustment Credit, ODA financed the latest and one of the most comprehensive of these studies,which came up with proposals for a strategy for the developmeLt of the sector. Most of theserecommendations have been accepted by the NBAA and the donor community, and many are alreadybeing implemented.

2.14 Following is a summary of the main elements of this strategy:

- NBAA is to withdraw from training students for its own examinations;- NBAA should take on the new function of accounting and audit review -

monitoring the performance of practising accountants and auditors to ensure thatit is up to acceptable standards, and disseminating best practises;

- 11 -

- NBAA should intensify its program of issuing accounting and auditing standards,and take on the new responsibility of enforcing those standards;

- NBAA should introduce continuing professional education (CPE) to keeppractising accountants up to date with the latest best practice;

- NBAA should be strengthened with training, technical assistance, and its ownoffice building, to enable it to carry out the responsibilities described above;

- TAC's monopoly of the audits of parastatal companies should be removed;

- A new syllabus and qualification should be introduced to deal with the accountingneeds of the civil service;

- The roles of NBAA and TAA should be more clearly defined with NBAAfocussing more on the setting and enforcement of standards, and TAA onmember-related services and professional promotion; and

* The Accountant-General, the Controller and Auditor-General, and TAC shouldall be assisted with staff training and technical assistance.

2.15 Actions to implement the above strategy have been taken, not only by the Govermnentof Tanzania and NBAA, but also by the donor community. Most of NBAA's actions in pursuit ofthe strategy have been described in Section A above. Proposed donor activities fitting into thestrategy include the ODA-financed training and technical assistance project to the Accountant-General's office, the OCAG, and the Institute of Development Management (IDM), Mzumbe. Theyalso include continuing SIDA assistance to TAC, and NORAD assistance to IDM.

2.16 This project would represent the single most comprehensive attempt to date to implementthe new sector strategy. It would include not only provision of material assistance to key sectorinstitutions targeted by the strategy, but also policy actions, such as NBAA Schedules for introducingaccountinc and auditing standards, action plans for removing TAC's monopoly, a cost recovery study,and othei measures detailed in the next chapter.

2.17 The Legal Sector. Government, the Bank, and bilateral donors have agreed on a two-part strategy for assisting the development of the legal sector in Tanzania, namely:

- a limited direct assistance to alleviate some of the more pressing needs identifiedin Section B above under 'Issues"; and

- a major sector study with Government, Bank, and bilateral donors' participationdesigned to diagnose the sector problems, and prepare an action plan (includingindicative project briefs) for its development.

2.18 There is at present no clearly articulated Government strategy for the development ofthe sector. There is, nevertheless, a recognition that there are major problem areas within the legalprofession, the judiciary, and the support services. Some of these needs are so obvious and non-controversial that they can be immediately addressed. However, it is important that a strategy for thesector be developed, which takes into account the various needs and expectations of the sector.

- 12 -

Under the Project, assistance would be provided to the Government to enable it to develop such astrategy and a program for the implementation of the strategy.

2.19 There is intense interest, on the part of donors active in Tanzania, in supporting activitiesin this area, in pursuance of the good governance theme. The Nordic Governments (particularlyDANIDA and SIDA), ODA, the Canadian Government, and USAID have shown interest. However,this is an area where there is very little expertise, and all bilateral donors are looking to the Bank toplay a coordinating role. The donors are interested in participating in the development of thestrategy for the sector, and have indicated that they have the necessary resources to support thevarious studies that will go into developing the strategy.

2.20 Past Role of the Bank and Lessons of Experience The Bank has never financed aproject to assist either accounting and auditing or the legal sector. However, the Bank has had directexperience of the inadequacies of accounting and auditing in the public sector. This has taken theform of poor compliance with the auditing covenant on many IDA-financed projects in Tanzania.It was largely this experience that alerted the Bank to the existence of a problem in that area. It ishoped that the successful implementation of this project would improve public sector accounting andauditing in the medium to long term, while more intensive supervision and focus on this specific issueshould improve the situation in the short term.

D. Rationale for Project Components

2.21 The main factors responsible for low accounting and auditing standards in Tanzania havebeen identified in many studies, as well as in Chapter I and this chapter, and may be summarized as:

(a) inadequate dissemination and enforcement of acceptable accounting and auditingstandards; and

(b) inadequate numbers of qualified accountants and auditors in the country ingeneral, and in the public service particular.

2.22 The problem in 2.21 (a) (inadequate dissemination and enforcement of accounting andauditing standards) above has been funher diagnosed as due primarily to (i) inadequate staff skiDls,inexperience, inadequate and fragmented office accommodations and poor equipment at the NBAA--the sole institution in Tanzania responsible for setting and upholding accounting and auditingstandards; (ii) the inadequate supply of accountancy text-books; and (iii) the inadequate human andmaterial resources available to key public sector institutions, such as the office of the Controller andAuditor-General, which is responsible for auditing all civil service accounts.

2.23 The inadequate supply of accountants to the country as a whole is largely a result of poorpass rates in professional accountancy examinations due to problems in key accountancy traininginstitutions, particularly the institute of accountancy, Arusha (IAA) and the Institute for FinanceManagement (IFM) which are currently receiving no foreign assistance. These problems include:

(i) inadequate skills of trainers, particularly in such subjects as advanced financialmanagement, quantitative analysis and computer science;

(ii) difficulty of attracting and retaining staff due to poor salaries and inadequate staffhousing;

- 13 -

(iii) poor library facilities everywhere;

(iv) the incomplete development of the LAA's administrative and training facilities;and

(v) poor office and training equipment, e.g., computers.

2.24 In the legal sector the most pressing problems have also been identified in Chapter I andthis chapter as:

(i) the absence of a long term strategy for the development of the sector;

(ii) the inadequacy of skills throughout the sector, especially in such areas ascommercial and company law;

(iii) the absence of up-to-date laws, due to the long neglect of law revision and long-delayed publication for the laws of Tanzania;

(iv) inadequate library facilities for judges and legal practitioners who need access toup-to-date legal decisions and precedents;

(v) poor office equipment and informatioan systems; and

(vi) inadequate post-qualification training facilities.

IIL THE PROJECT

A. Rationale and Objectives

3.01 Implementation of the Economic and Social Reform Program in Tanzania is placingheavy demands on public sector accounting, auditing, financial management, legal management, andadministration of justice in Tanzania which are outstripping the laudable efforts the Government hasbeen making to meet them. The reasons for this state of affairs are manifold, but underlying theinadequate level of services is a number of problems cutting across several other public sector servicesand activities, including, for example, an inadequate supply of trained staff, poor equipment, andinadequate performance incentives. This capacity building project is designed to address theseproblems.

3.02 The issues in public sector accounting and auditing have been reasonably well-analyzedin many studies over the years, and a strategy for developing the sector has recently evolved. In thelegal sector, however, the issues require considerable further analysis and a detailed strategy for fulldevelopment still has to be prepared. For these reasons, a cautions two-pronged approach is adoptedof providing limited and obviously-needed assistance, while financing a study designed to remove, orat least reduce, the uncertainties described above.

- 14 -

Objectives

3.03 The objectives of the project are to improve accounting and auditing standards on theone hand, and the legal regulatory framework and the administration of justice on the other.

B. Project Components

3.04 Table 1 shows the five p3roject components, the beneficiary institutions, and the type ofassistance each institution would receive under the project. Unless where specified otherwise, allcosts (both in Table 1 and the rest of this Section) are base cost (i.e., without provision for physicalor price contingencies). Project incremental costs (Component V in Table 1) represent estimatedmaintenance costs of buildings, additional rental for NBAA staff housing, vehicle operating costs andother incremental expenses which project institutions would incur, as a result of project investments.Government would be expected to finance these as well as any part of local procurement notfinanced 100% by IDA, as explained in Section E below.

Fiancial Manai-ement Unpirading USS12 million)

3.05 The problems highlighted in paragraphs 2.21 to 2.23, would be addressed through (a)better dissemination and enforcement of acceptable accounting and auditing s.andards by the NationalBoard of Accountants and Auditors (NBAA) and the Office of the Controller and Auditor-General(OCAG); and (b) increasing the national output of CPAs by strengthening the two most relevanttraining institutions, IAA and IFM.

3.06 The National board of Accountants and Auditors (NBAA) would be assisted under theproject through training, technical assistance, the preparation of study manuals, office equipment,vehicles, and office accommodation. In-service traiing would be provided to upgrade technical andprofessional skills of the NBAA staff. Staff need to be trained in modern accounting and auditingtechniques to enable NBAA to complete its program of issuing accounting and auditing standards,and to expand its activities to include computer training for students and members, and to introducepractice review. The subcomponent would provide for NBAA staff to take masters degree coursesin accounting, business, and public administration as well as short term courses relevant to their work.Details of the training program are in Annex 1 and the Project File.

3.07 Technical assistance for NBAA would be provided to help to introduce a practice re"iewsystem whereby NBAA would review whether an auditor is complying with relevant standards. Thissubcomponent would provide the NBAA with an expert for four weeks in the first year, and twoweeks each in the second and third years of the project to assist in drawing up guidelines for practicereview, and monitoring the work of the NBAA reviewers, and an expert for similar periods to assistthe NBAA in reviewing and updating its examination syllabus. In addition, the project would financeshort-term consultancy to teach information technology and the latest techniques in accounting,auditing and costing in NBAA's program of continuing professional education (CPE) aimed atpracticing accountants and auditors. NBAA brought to negotiations a schedule of accounting andauditing standards it plans to issue, with target issue dates, and assurances were obtained atnegotiations that NBAA would implement that schedule.

3.08 In addition, the project would finance NBAA's preparation of studv manuals. Pass ratesin the NBAA examinations are very poor. Textbooks in Tanzania are in very scarce supply, and thereare no books covering Tanzanian accounting, auditing and taxation. To improve examination pass

- 15 -

rates and increase the number of accountants and auditors in the country, the NBAA has recruitedauthors to write 30 study manuals over the next two years. These manuals would be sold to studentsat prices designed to recover fuli production costs. The project would finance initial production andprinting expenses. Thereafter manual production is expected to be self-financing.

TABLE IPROJECT COMPONENTS SUtMMAU

Compnuter& Office&t ohnbal Study Ofc Reidential

h rn Training Astnoe Manuab j Equlpment Printing Vehice, Accommod. Total

1. Flnianl MsnagemmntNBAA 487 108 168 - 174 - 146 2661 3e24OCAG 163 - - - 74 - 111 - 338IAA 69 1260 - 614 79 - 78 3466 6085IFM 668 720 - 166 626 - 160 - 2320

StJB-TOTAL 1997 2088 168 680 963 0 486 6008 12387

11. LSee10

Attorney-General's Offie-Clvll&lntematinalDivision 179 200 - 176 200 - - - 764- Chief Parimntary Draftsman 284 180 - - - 1800 - - 2264- Administrator-General's Offloe 100 - - - - 360 - - 460

Judciary 801 _ _ 176 200 370 30 - 1376Law Feform Coimlmalon 180 60 - - 60 - - - 260Regletr rofCompane 111i - - 84 _ _ _ 196

SUB-TOTAL 1436 430 0 360 634 2620 30 6299

Ill. STUDIESLegal etor Strategy - - - - - - - - 260oCt Roo-eyStudy -SI1

TAC Study - - - - - - - - so

SUB-TOTAL _90

IV. PROJWECt OOOROINATION:-Financel - - - - - - - _ 18e

-Lagal - - - - - - -~~~ ~ - 188

- Prjeot Launch Workshop _ _ _ _ _ _ 7SUB-TOTAL - - - - - - - - 3603

V. ICNtEMENTAL OPERATION COSTS - - - - - - - - 793TOTAL BASE COST 3432 2618 168 1030 1487 2620 615 6006 19212

- 16 -

3.09 The project would also finance computers and office equipment for the NBAA whoseequipment is heavily over-utilized and does not meet the demands of running a growing professionalbody. The NBAA currently has a manual system for members and students records, and anaccounting system which is time consuming to use and does not enable the NBAA to easily analyzedata. A computerized database for members and students and a computerized accounting systemwould help alleviate these problems. There is an urgent need to train accountants in computer skills,so that they can effectively use and help design the computer systems currently being installed inTanzania. This includes not just familiarization with basic computer programs, but also training inthe use of accounting software. The NBAA can play a very useful role in enabling members andworking students, who do not have access to college facilities, to gain hands-on computer experience.This subcomponent would provide the NBAA with computers, peripheral equipment and software,as well as other office equipment detailed in Annex 1 and the Project files.

3.10 The project also provides for five vehicles to enable NBAA to meet its transportationneeds, particularly for conducting its professional oversight role and for arranging and conductingexaminations simultaneously in different parts of the country.

3.11 NBAA offices are currently scattered in three different locations in Dar-es-Salaam: NICHouse, which is its headquarters and main office; Mavuno House which houses its Education,Research and Training, and Examinations Division; and Mhasibu House where three temporaryclassrooms have been built for training and to house the printing unit. This attempt to operate outof three locations is not only an administrative nightmare, but also a great waste of managerial timeand fuel, especially given telephone and other communication problems, as NBAA managerscommute between these three sites in an effort to co-ordinate NBAA activities. To make mattersworse, none of the three offices is really adequate for the purpose for which it is intended.

3.12 NBAA's efforts to rent consolidated offices in Dar have proved futile, not only becauseof the shortage of office accommodation in the city, but also because NBAA is not in a financialposition to compete with businesses for commercial space. A recent ODA-financed study hastherefore recommended that NBAA be provided with a grant to enable it to construct its own officebuilding.

3.13 The NBAA holds the title to the Mhasibu House plot of land. The plot covering 1.614acres, is large enough to accommodate all NBAA's office requirements. The project would financethe construction of the NBAA headquarters in Dar Es Salaam which would include: (i) civil worksand external works (estimated at US$4.4 million equivalent) comprising about 900 m2 for office space,and 1,900 m2 for training, library, and other facilities; (ii) related equipment and furniture (estimatedat US$1.1 million); and (iii) technical fees (estimated at US$0.4 millions equivalent) fordesign/supervision of civil works and procurement of goods. Construction is expected to becompleted in Project Year 2. Details of space areas in square meters, room occupancy and costs aregiven in Annex 1. To promote close collaboration and eventual integration of NBAA and TAA (theCPA member organization), assurances were obtained at negotiations that NBAA would providethree offices for TAA in the new building. Government also brought to negotiations a statement ofits future policy for the development of the accountancy profession, with particular reference to thefuture relationship between NBAA and TAA

3.14 The project would also finance for the Office of the Controller and Auditor-General(OCAG) (Annex 2) training, computers and office equipment and vehicles. The OCAG needs to

- 17 -

train its staff in three new areas crucial for the propoi exercise of its audits of all civil serviceaccounts, namely, contract audit, value for money audit, and computer accounting and auditing. Theproject would provide financing for these courses. The project would also finance the local trainigof already-identified OCAG staff for the CPA examination. In addition, the project would financecomputers, typewriters, and vehicles foi OCAG's twenty offices located in all the twenty provincesof Tanzania.

3.15 As explained in paragraph 3.06 above, cfforts to increase the national output of CPAswould center on strengthening IAA and IFM, two key institutions responsible for training studentsfor CPA examinations. The IAA, located on the outskirts of Arusha, is a residential campus for full-time students, producing better examination results than the national average. IFM is in Dar-es-Salaam, and has a large number of part-time anoi day students.

3.16 For the Institute of Accountancy. Arusha (IAA) (Annex 3) the project would financestaff training, technical assistance, library support, computers and office equipment, vehicles, andoffice and residential accommodation. Training of trainers is necessary because, although theexamination pass rates at the IAA are over twicc the national average, there is still considerable roomfor improvement. To improve student performance, the lecturing staff at the LAA need to be betterinformed in modern accounting and auditing techniques. The subcomponent would provide for a fewmasters degree courses, and several short update courses in financial accounting, cost andmanagement accounting. Technical assistance would consist mostly of two substitute lecturers, eachfor 2 years, to temporarily replace staff who would be going away on training, plus short-termconsultancy to provide seminars for LAA staff, particularly in computer literacy. Details of trainingcourses and consultancy arrangements are in Annex 3 and the Project Files.

3.17 The poor condition of most libraries in the count±y has been noted earlier in this report.In both MAA and IFM - two important training institutions for the CPA examinations - there are veryfew text books, and what exists is mostly out-of-date. Accordingly, the project would finance librazvsupport for IAA in the form of already-identified and necessary text-books, periodicals and libraryequipment.

3.18 The equipment and vehicles that IAA has are insufficient to meet the needs of a growingteaching establishment. Although it plans to teach computer applications, it is now completely devoidof computers. Therefore, in addition to some basic library equipment, this subcomponent wouldprovide LAA with a limited number of computers, photocopiers, duplicating machines, overheadprojectors, electric typewriters, power bank, audio-visual equipment, and a public address system. TheIAA would cover the costs of installation. In addition, given that the LAA is located a considerabledistance from a town which has little public transportation, and most of the administrative personnellive in town, the project would finance one car and two mini-buses to transport staff and students.

3.19 All the buildings on LkA's campus have been fmianced by the Government of Tanzania -one of the many practical examples of the importance the Government attaches to the developmentof competent accountancy skills at the highest level. The buildings already completed and currentlyin use include classrooms, two students' hostels, 18 staff houses, a kitchen/cafeteria attached to oneof the residential blocks, a theater, and part of an administrative block housing all the offices as wvellas the library.

3.20 Construction of the administrative block was not completed due to lack of funds. LAAclearly will not have enough offices or library space unless the administrative block is completed.

- 18 -

Moreover, the half-completed structure, not properly roofed, is deteriorating fast. So the alreadyconsidcrable investment in it would bc lost il the building was left uncompleted. Also the cafeteriais so poorly-designed as to constitute both a health and a fire hazard. In addition, there is notenough housing for staff or for the expected future student expansion. During project preparation,both the administrative block and the proposed new cafeteria were re-designed to more modest (andless costly) standards than the original buildings. The project proposes to finance these specific worksdesigned to complete the development of the institute to a more modest design than was originallyintended.

3.21 Accordingly, the project would finance the extension and remodeling of the LAA whichwould include: (i) civil works and external works (estimated at US$3.4 million) comprising anadministration block with a library for students and teachers, a board room and offices (2,000 m2 ),boarding facilities (1,100 m2), a cafeteria (910 m2), and 12 additional staff houses (1,740 m2); (ii)related equipment and furniture (estimated at US$0.6 million equivalent); and (iii) technical fees fordesign/supervision of civil works and procurement of goods (estimated at US$0.4 million equivalent).Construction is expected to be completed in Project Year 2, with the exception of civil works for thestaff housing and extension of boarding facilities. The signing of the contract and disbursement ofIDA funds for staff housing and boarding facilities will be subject to confirmation that the studentpopulation has increased to 150 and is likely to increase to 300 within 2 years thereafter. Details ofspace areas in square meters, room occupancy and costs are given in Annex 3.

3.22 In a further effort to increase the output of CPAs by improving the quality of training,the project would provide the Institute for Finance Management (IFM) with financing (US$2.3million) for staff training, technical assistance, librarv support, computers and office equipment, andvehicles. As regards staff training, the IFM wishes to expand its curriculum to introduce computingcourses and extend the coverage of its finance and business courses, but for the purpose will haveto upgrade skills of faculty members. Under its training budget the IFM will be able to finance some40 man-years of training in Tanzania over the coming five years. The IFM however, does not havesufficient money within its recurrent budget to finance external training. The project would providefinancing for IFM staff to participate in degree and non-degree courses in accountancy,banking/insurance, taxation, financial management and busir.ess administration/computing. Thesecourses are for both academic and administrative staff. The project would also finance 3 consultant-years of technical assistance: two for a Professor in Finance and/or Accounting, to teach advancedcourses in accounting, and one for a Lecturer in Computer Science, to help set up facilities and theteaching of computer courses. Library support would include identified text-books and periodicals,as well as essential library equipment listed in Annex 4. There is a growing need for accountants tobe able to use computers. In addition there are no diploma courses in computing in Tanzania. T:heIFM wishes to introduce computer courses not only for accountants, but also for students who wishto specialize in computing. This subcomponent would provide IFM with a computer lab consistingof a mini computer networked to 20 PCs with appropriate software, five heavy duty printers, simpleair conditioning and wiring, as well as visual aids and equipment for desk-top publishing.

3.23 Through sponsorship by the Tanzania banking and insurance community, IFM has beenable to construct a six story building comprising hostel accommodation and six classrooms. TheInstitute's sponsors who had pledged financial support to furnish the classrooms are now unable toprovide the funding. The classrooms are needed if the IFM is to cope with the ever increasingdemand for its courses and IFM is to provide the right learning environment. The project wouldtherefore provide the IFM with classroom equipment and fittings, the replacemen: of a central

- 19-

cooling system in the lecture theater, library and function room, and other essential equipment andvehicles.

Upgrading the Legal Sector (USS5.0 million)

3.24 As explained in Chapter II, project assistance to the legal sector would be in two parts:(i) immediate direct assistance to alleviate some of the pressing needs of the sector; and (ii) a studydesigned to produce a long-term development strategy for the sector. Project direct assistance wouldbe provided to the Attorney-General's office, and, more specifically, to three divisions in that office,namely, the Civil and International Division, the Office of the Chief Parliamentary Draftsman, andthe Administrator-General's office; the Judiciary; the Law Reform Commission and RegistrarCompanies. The Attorney General's office would also oversee the formulation of the developmentstrategy for the legal sector.

3.25 At the Attomey-General's office. the project would finance training, technical assistance,library support, and the first stage of a management information and legal database system. Staffahiinr would include participation by staff members of the Civil and International Division in

courses offered by the International Development Law Institute (IDLI) and the International LawCenter (ILC). These involve development lawyers courses, courses on negotiation skills, privatization,procurement, capital markets, etc. One or two masters level courses would also be included. Thetraining for the office of the Chief Parliamentary Draftsman concentrates on legislative drafting, avery specialized skill. The training for this involves a combination of short - and longer-term trainingcourses spread over three years. This includes the diploma in legislative drafting run for BritishCommonwealth countries in Barbados, as well as shorter curses run in India, and by the RoyalInstitute of Public Administration in England. About three of the more senior staff members wouldpursue LLM courses in legislative drafting. In addition, law revisers would undertake two monthattachments with the legislative departments of neighboring Commonwealth countries where thelegislative departments function well. As the new laws being drafted are increasingly in thecommercial and corporate law areas, there is included in the project the opportunity for some of thedraftsmen to attend some of the short courses on relevant areas being offered by IDLI and ILC. Thetraining needs of the Administrator-General's Office are somewhat different, involving mostly studytours to other Commonwealth countries which have good registration programs, e.g., the U.K, Kenya,Pakistan, etc. In addition there would be some short-term training in demographic data collection.

3.26 The project would also finance for the Attorney-General's Office some technicalassistance to develop a management information and legal database system, revise the laws ofTanzania (a general and continuing exercise), and undertake a review of laws dealing with commercialmatters, starting with the Companies Ordinance. Government brought to negotiations a statementof areas of law to be reviewed, with indications of approximate completion dates and assurances wereobtained from Government that it would adhere to that schedule during project implementation.Other project support to the Attorney- General's Office would involve the acquisition of legal books,legal journals, shelving, equipment and other materials. The project would als. finance the printingof forms for the Office of the Administrator-General. Assurances were obtained at negotiatioais lh itthe Administrator-General would be allowed to charge realistic fees for services rendered and thatGovermment would provide that office with a minimum annual budget equivalent to US$300,000adjusted for inflation.

3.27 For the JudiciaI the project would finance training, library support, typewriters, andcomputers and other office equipment needed for a first-stage management information system.

- 20 -