world bank document · document of the world bank report no: icr0000710 implementation completion...

TRANSCRIPT

Document of The World Bank

Report No: ICR0000710

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IBRD-73910)

ON A

LOAN

IN THE AMOUNT OF US$ 500.0 MILLION

TO THE

ARAB REPUBLIC OF EGYPT

FOR A

FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

February 21, 2007

Finance and Private Sector Group Social and Economic Development Department Middle East and North Africa Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective October 31, 2007)

Currency Unit = EGP 1.00 = US$ 0.18 US$ 1.00 = EGP 5.52

FISCAL YEAR July 1st – June 30th

ACRONYMS AND ABBREVIATIONS

AfDB African Development Bank CAS Country Assistance Strategy CASE Cairo and Alexandria Stock Exchange CBE Central Bank of Egypt CFAA Country Financial Accountability Assessment CMA Capital Market Authority ECB European Central Bank EISA Egyptian Insurance Supervisory Authority EMRC Egypt Mortgage Refinancing Company EU European Union FIRST Financial Sector Strengthening Program FSAP Financial Sector Assessment Program FSRP Financial Sector Reform Program GDP Gross Domestic Product GOE Government of Egypt GSF Guarantee and Subsidy Fund IBRD International Bank for Reconstruction and Development IFC International Finance Corporation IHC Insurance Holding Company IMF International Monetary Fund MFA Mortgage Finance Authority MTPL Motor Third Party Liability SIF Social Insurance Fund

Vice President: Daniela Gressani

Country Director: Emmanuel Mbi

Sector Manager: Zoubida Allaoua

Task Team Leader: Sahar Nasr

ICR Team Leader Sahar Nasr

EGYPT Financial Sector Development Policy Loan

CONTENTS

DATA SHEET A. Basic Information .................................................................................................................... i B. Key Dates ................................................................................................................................ i C. Ratings Summary .................................................................................................................... i D. Sector and Theme Codes ........................................................................................................ ii E. Bank Staff ............................................................................................................................... ii F. Results Framework Analysis................................................................................................... ii G. Ratings of Program Performance in ISRs............................................................................... ii H. Restructuring .......................................................................................................................... ii

1. PROGRAM CONTEXT, DEVELOPMENT OBJECTIVES AND DESIGN........................................... 1 2. KEY FACTORS AFFECTING IMPLEMENTATION AND OUTCOMES............................................. 3 3. ASSESSMENT OF OUTCOMES................................................................................................... 9 4. ASSESSMENT OF RISK TO DEVELOPMENT OUTCOME............................................................ 14 5. ASSESSMENT OF BANK AND BORROWER PERFORMANCE..................................................... 15 6. LESSONS LEARNED................................................................................................................ 17 7. COMMENTS ON ISSUES RAISED BY BORROWER/IMPLEMENTING AGENCIES/PARTNERS...... 19 Annex 1: Bank Lending and Implementation Support/Supervision Processes ......................... 20 Annex 2: Summary of Borrower’s ICR and/or Comments on Draft ICR.................................. 20 Annex 3: Comments of Cofinanciers and Other Partners/Stakeholders.................................... 25 Annex 4: Operational Policy Matrix ......................................................................................... 25 Annex 5: Achievements of Project Development Objectives................................................ 32 Annex 6: List of Supporting Documents................................................................................... 38

MAP .......................................................................................................................................... 39

i

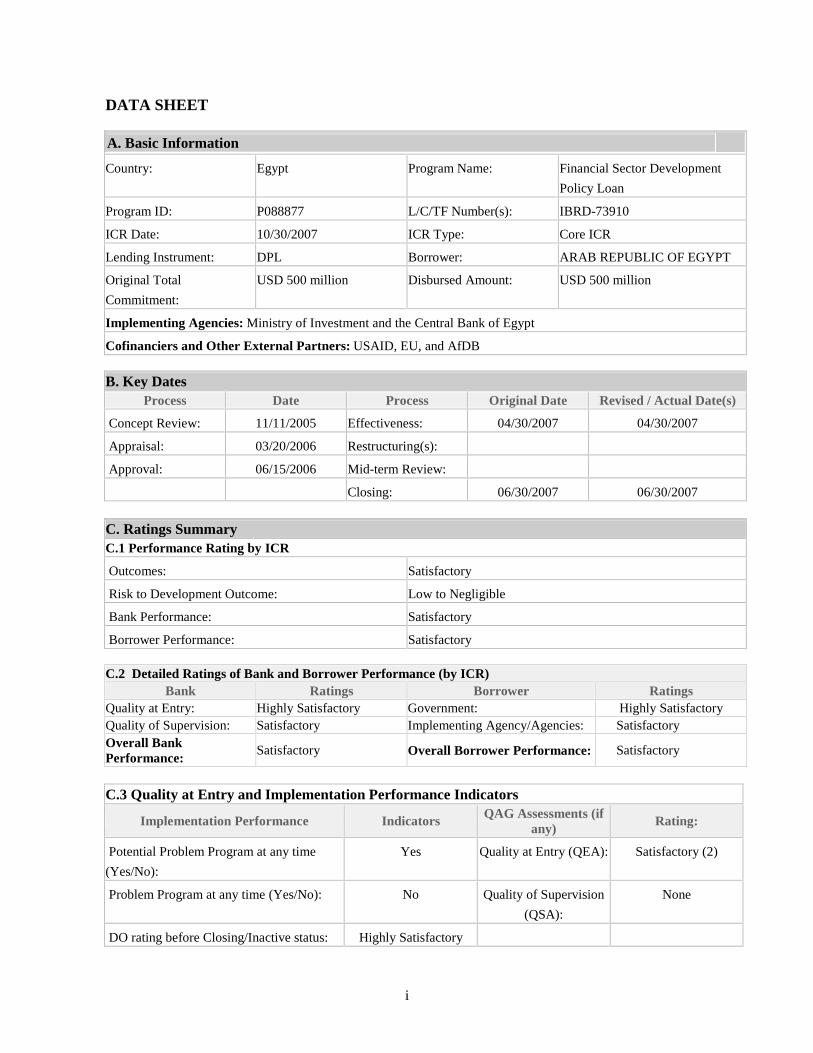

DATA SHEET

A. Basic Information

Country: Egypt Program Name: Financial Sector Development

Policy Loan

Program ID: P088877 L/C/TF Number(s): IBRD-73910

ICR Date: 10/30/2007 ICR Type: Core ICR

Lending Instrument: DPL Borrower: ARAB REPUBLIC OF EGYPT

Original Total

Commitment:

USD 500 million Disbursed Amount: USD 500 million

Implementing Agencies: Ministry of Investment and the Central Bank of Egypt

Cofinanciers and Other External Partners: USAID, EU, and AfDB

B. Key Dates Process Date Process Original Date Revised / Actual Date(s)

Concept Review: 11/11/2005 Effectiveness: 04/30/2007 04/30/2007

Appraisal: 03/20/2006 Restructuring(s):

Approval: 06/15/2006 Mid-term Review:

Closing: 06/30/2007 06/30/2007

C. Ratings Summary C.1 Performance Rating by ICR

Outcomes: Satisfactory

Risk to Development Outcome: Low to Negligible

Bank Performance: Satisfactory

Borrower Performance: Satisfactory

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR) Bank Ratings Borrower Ratings

Quality at Entry: Highly Satisfactory Government: Highly Satisfactory Quality of Supervision: Satisfactory Implementing Agency/Agencies: Satisfactory Overall Bank Performance:

Satisfactory Overall Borrower Performance: Satisfactory

C.3 Quality at Entry and Implementation Performance Indicators

Implementation Performance Indicators QAG Assessments (if any)

Rating:

Potential Problem Program at any time

(Yes/No):

Yes Quality at Entry (QEA): Satisfactory (2)

Problem Program at any time (Yes/No): No Quality of Supervision

(QSA):

None

DO rating before Closing/Inactive status: Highly Satisfactory

ii

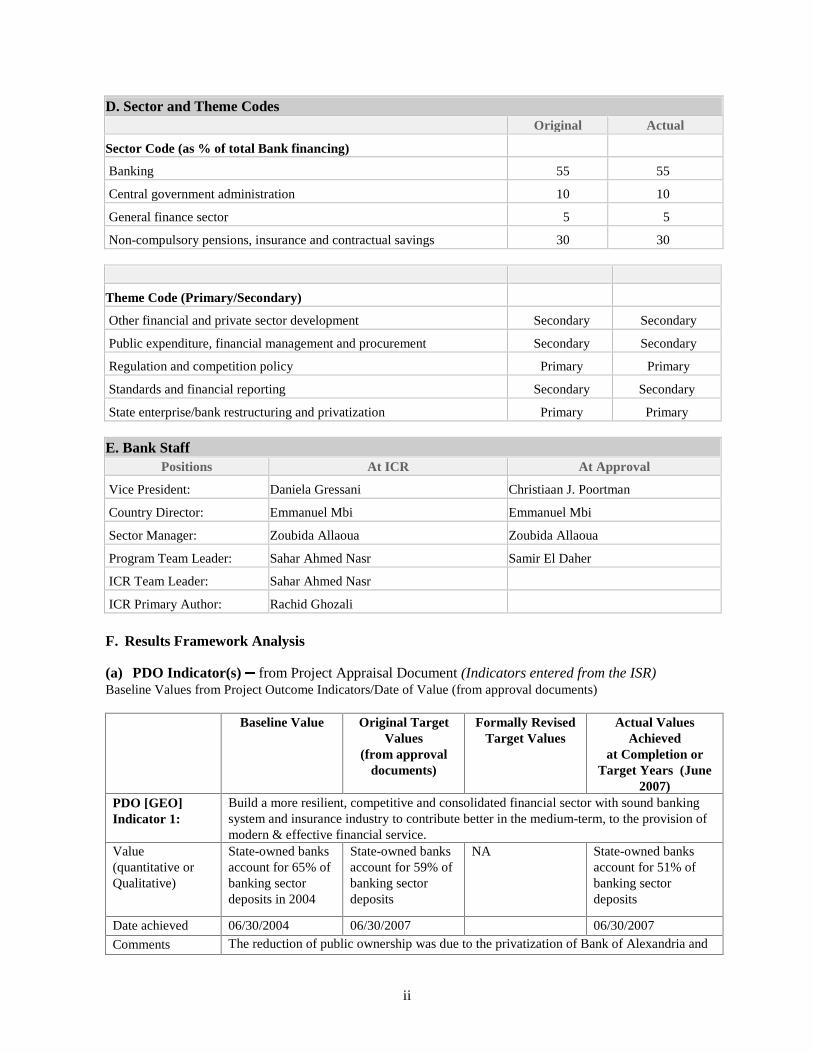

D. Sector and Theme Codes Original Actual

Sector Code (as % of total Bank financing)

Banking 55 55

Central government administration 10 10

General finance sector 5 5

Non-compulsory pensions, insurance and contractual savings 30 30

Theme Code (Primary/Secondary)

Other financial and private sector development Secondary Secondary

Public expenditure, financial management and procurement Secondary Secondary

Regulation and competition policy Primary Primary

Standards and financial reporting Secondary Secondary

State enterprise/bank restructuring and privatization Primary Primary

E. Bank Staff Positions At ICR At Approval

Vice President: Daniela Gressani Christiaan J. Poortman

Country Director: Emmanuel Mbi Emmanuel Mbi

Sector Manager: Zoubida Allaoua Zoubida Allaoua

Program Team Leader: Sahar Ahmed Nasr Samir El Daher

ICR Team Leader: Sahar Ahmed Nasr

ICR Primary Author: Rachid Ghozali

F. Results Framework Analysis (a) PDO Indicator(s) from Project Appraisal Document (Indicators entered from the ISR) Baseline Values from Project Outcome Indicators/Date of Value (from approval documents)

Baseline Value Original Target Values

(from approval documents)

Formally Revised Target Values

Actual Values Achieved

at Completion or Target Years (June

2007) PDO [GEO] Indicator 1:

Build a more resilient, competitive and consolidated financial sector with sound banking system and insurance industry to contribute better in the medium-term, to the provision of modern & effective financial service.

Value (quantitative or Qualitative)

State-owned banks account for 65% of banking sector deposits in 2004

State-owned banks account for 59% of banking sector deposits

NA State-owned banks account for 51% of banking sector deposits

Date achieved 06/30/2004 06/30/2007 06/30/2007

Comments The reduction of public ownership was due to the privatization of Bank of Alexandria and

iii

(incl. % achievement)

the divesture of public sector bank shares in joint venture banks.

Value (quantitative or Qualitative)

NPLs of SOEs outstanding in state-owned commercial banks is LE 26 billion in June 2004

NPLs drop to 19.1 billion

LE 10 billion in December 2006

Date achieved 07/15/2004 02/15/2006 02/15/2006

Comments (incl. % achievement)

The government has achieved beyond the agreed on target on settlement of NPLs, as follows: (i) all of Bank of Alexandria public enterprise NPLs, in an amount of LE6.9 billion (US$ 1.2 billion equivalent) were settled by the Ministry of Finance in cash in February 2006; (ii) an additional L.E 9.1 billion (the allocation of sales proceeds of Bank of Alexandria) was paid in cash by the Ministry of Finance in December 2006 partially settling SOEs’ NPLs owed to National Bank of Egypt, Bank Misr and Banque du Caire; and (iii) SOEs’ NPLs of state-owned commercial banks declined from LE 26 billion in June 2005 to LE 10 billion in December 2006 (reduction of around 60 percent).

(b) Intermediate Outcome Indicator(s) - from Project Appraisal Document Baseline Values from Project Outcome Indicators/Date of Value (from approval documents)

Baseline Value

Original Target Values

(from approval documents)

Formally Revised Target Values

Actual Values Achieved at Completion or Target Years

IO Indicator 1: Strengthening legal, regulatory and supervisory framework in banking and insurance.

Value (quantitative or Qualitative) � Capacity

building of the supervisory and regulatory authority of banks and insurance

� The need to develop the supervisory and regulatory framework for banks and insurance

� Implementation of phase I of the capacity building program of the supervisory authority of banks.

� Strengthening the supervisory capacity of the insurance sector

NA � Successful implementation of phase I of the capacity building program for banking regulation and supervision has been approved by CBE to be implemented over 2006-2007 with substantial staff upgrading already taking place at the CBE Banking Supervision Department.

� Supervisory development plan in the

insurance sector is progressing and the new Chairman of EISA appointed in mid- 2006 is driving the change

Date achieved 06/15/2006 06/30/2007 06/30/2007

Comments (incl. % achievement)

� Implementation of capacity building measures is on track in banking regulation and supervision as per agreed program.

� Egypt has strengthened the effectiveness of its supervisory apparatus in banking, with better adherence to international codes and standards

� Egypt has strengthened insurance and private pension supervisory IO Indicator 2: Institutional and operational restructuring of state-owned banks

Value (quantitative or Qualitative) � State-owned

commercial

� The state-owned commercial banks suffer from poor

� State-owned commercial banks under restructuring show

NA � The operational restructuring of the two state-owned commercial banks is underway in 3 critical areas (human resource development, risk management and information technology) as part of a

iv

banks under restructuring show improvement in: (i) human resources build-up; and (ii) operational and financial performance

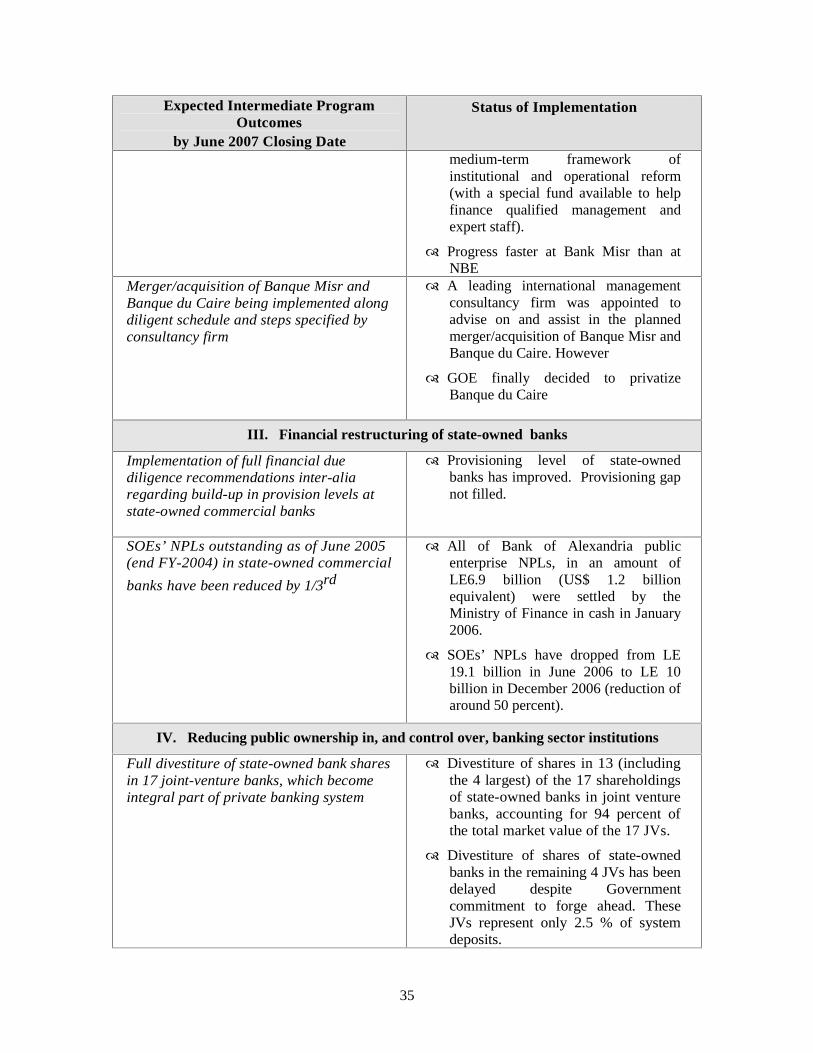

� Merger of Banque Misr and Banque du Caire being implemented along diligent schedule and steps specified by consultancy firm

performance, week governance structure, and inadequate IT.

improvement in: (i) human resources build-up; and (ii) operational and financial performance.

broader medium-term framework of institutional and operational reform.

Date achieved 06/30/2006 06/30/2007 06/30/2007

Comments (incl. % achievement)

The three state-owned commercial banks have undergone institutional and operational restructuring

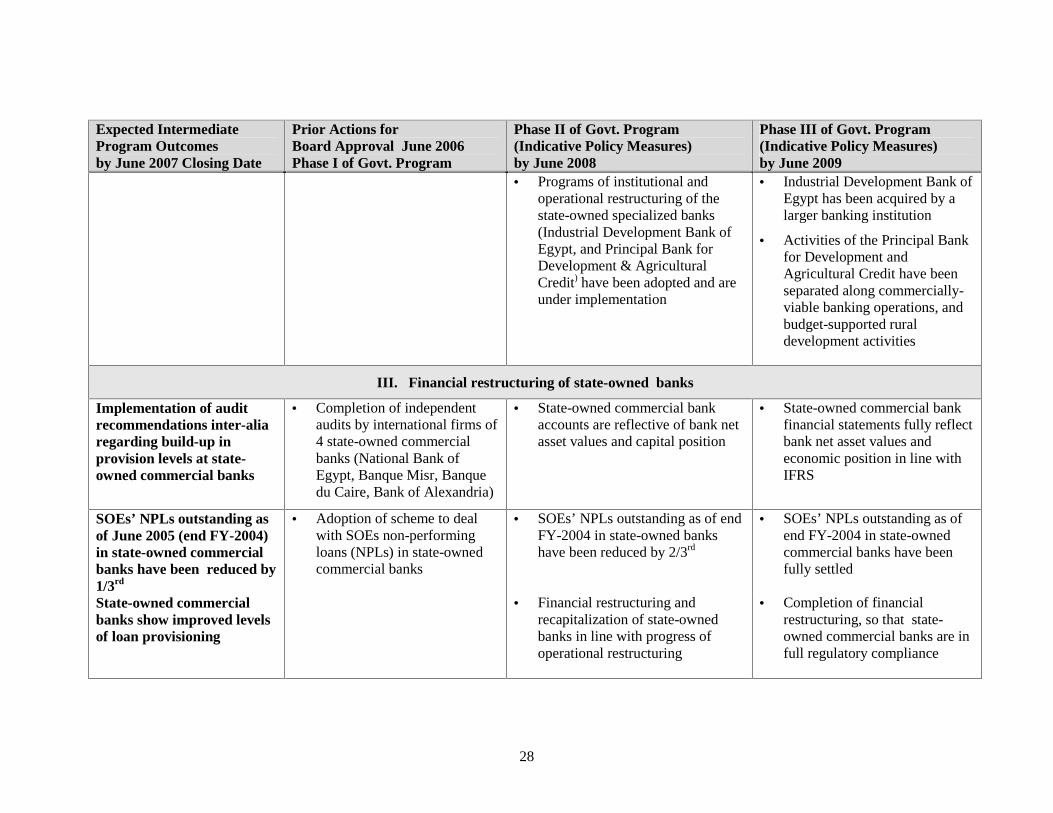

IO Indicator 3: Financial and operational restructuring of state-owned banks.

Value (quantitative or Qualitative)

� Implementation of financial due diligence recommendations inter-alia regarding build-up in provision levels at state-owned commercial banks

� SOEs’ NPLs outstanding as of June 2004 in state-owned commercial banks have been reduced by 1/3rd

� State-owned commercial banks show

� State-owned banks were never subject to independent financial due-diligence.

� State-owned commercial banks were burdened by huge NPLs of SOEs, amounting to LE 19.1 billion

� State-owned commercial banks are inadequately provisioned for

� Implementation of the full financial due diligence’s recommendations.

� Build-up in provision levels at state-owned commercial banks

� Reduction of SOEs NPLs by 1/3rd

NA � Completion of independent full due diligence of state owned commercial banks.

� Provisioning level of state-owned banks has improved.

� NPLs of SOEs dropped from LE 19.1 billion to LE 10 billion.

v

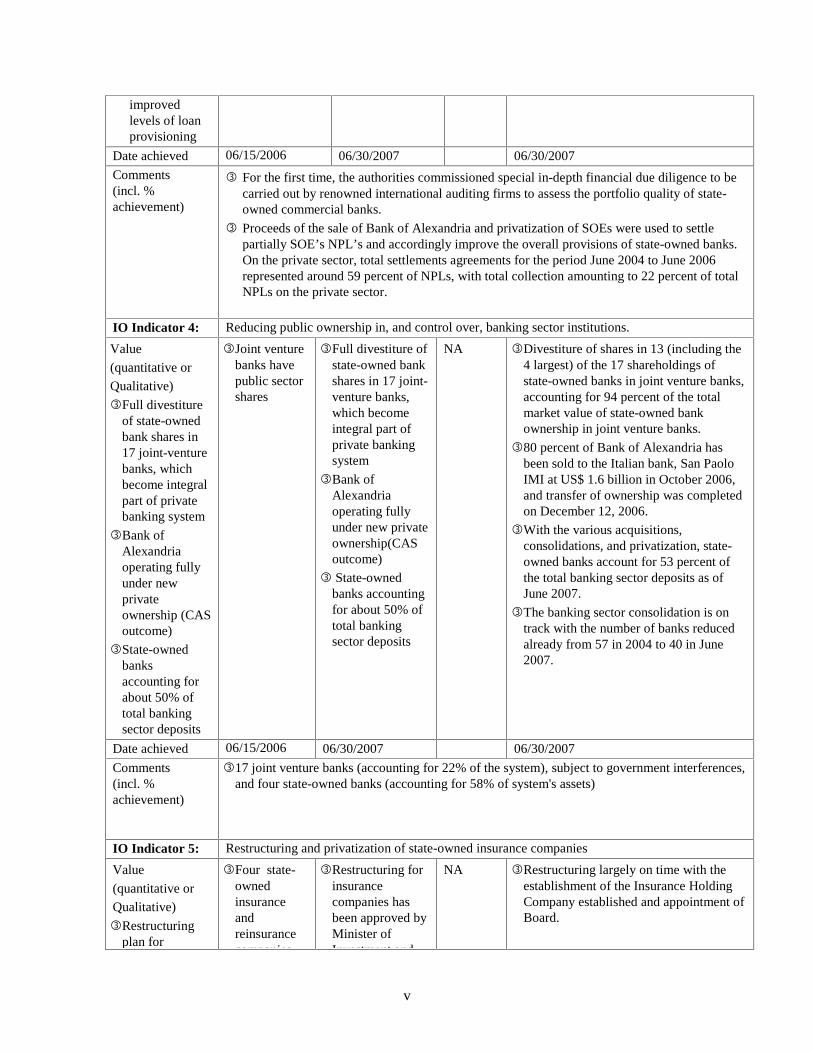

improved levels of loan provisioning

Date achieved 06/15/2006 06/30/2007 06/30/2007 Comments (incl. % achievement)

� For the first time, the authorities commissioned special in-depth financial due diligence to be carried out by renowned international auditing firms to assess the portfolio quality of state-owned commercial banks.

� Proceeds of the sale of Bank of Alexandria and privatization of SOEs were used to settle partially SOE’s NPL’s and accordingly improve the overall provisions of state-owned banks. On the private sector, total settlements agreements for the period June 2004 to June 2006 represented around 59 percent of NPLs, with total collection amounting to 22 percent of total NPLs on the private sector.

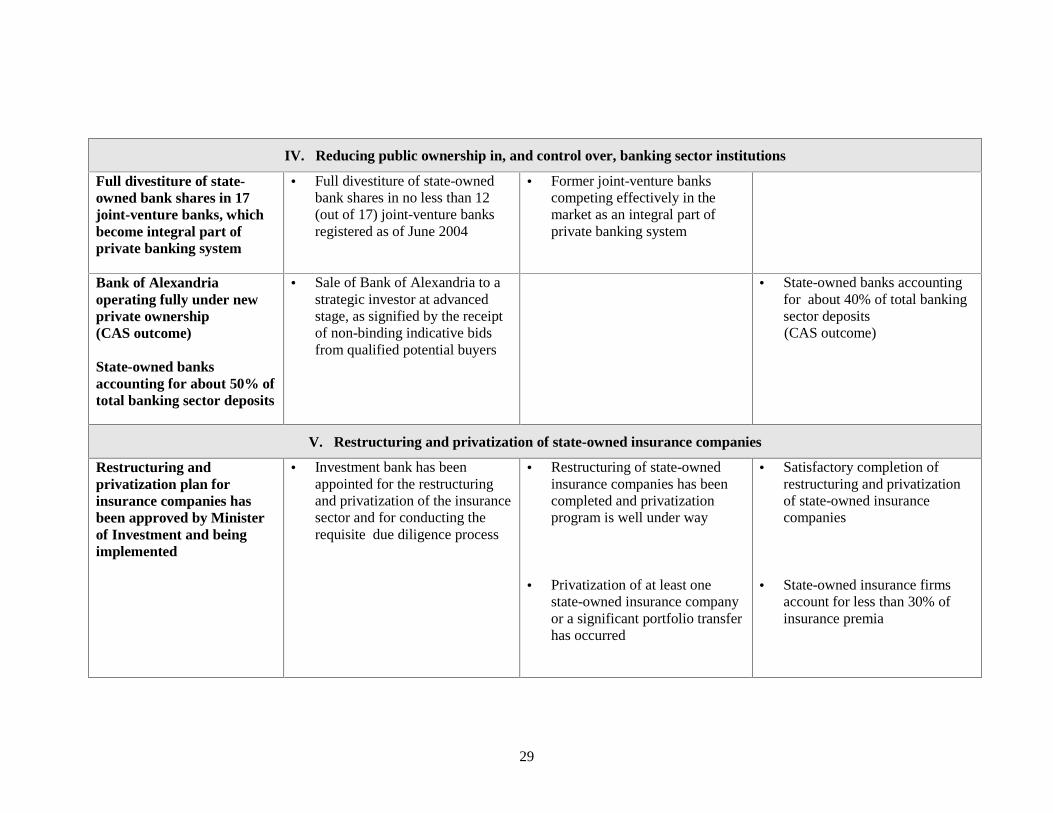

IO Indicator 4: Reducing public ownership in, and control over, banking sector institutions.

Value

(quantitative or

Qualitative)

� Full divestiture of state-owned bank shares in 17 joint-venture banks, which become integral part of private banking system

� Bank of Alexandria operating fully under new private ownership (CAS outcome)

� State-owned banks accounting for about 50% of total banking sector deposits

� Joint venture banks have public sector shares

� Full divestiture of state-owned bank shares in 17 joint-venture banks, which become integral part of private banking system

� Bank of Alexandria operating fully under new private ownership(CAS outcome)

� State-owned banks accounting for about 50% of total banking sector deposits

NA � Divestiture of shares in 13 (including the 4 largest) of the 17 shareholdings of state-owned banks in joint venture banks, accounting for 94 percent of the total market value of state-owned bank ownership in joint venture banks.

� 80 percent of Bank of Alexandria has been sold to the Italian bank, San Paolo IMI at US$ 1.6 billion in October 2006, and transfer of ownership was completed on December 12, 2006.

� With the various acquisitions, consolidations, and privatization, state-owned banks account for 53 percent of the total banking sector deposits as of June 2007.

� The banking sector consolidation is on track with the number of banks reduced already from 57 in 2004 to 40 in June 2007.

Date achieved 06/15/2006 06/30/2007 06/30/2007

Comments (incl. % achievement)

� 17 joint venture banks (accounting for 22% of the system), subject to government interferences, and four state-owned banks (accounting for 58% of system's assets)

IO Indicator 5: Restructuring and privatization of state-owned insurance companies

Value

(quantitative or

Qualitative)

� Restructuring plan for

� Four state-owned insurance and reinsurance companies

� Restructuring for insurance companies has been approved by Minister of Investment and

NA � Restructuring largely on time with the establishment of the Insurance Holding Company established and appointment of Board.

vi

insurance companies has been approved by Minister of Investment and being implemented

� Time bound MTPL reform strategy has been agreed at Cabinet level

� Non own use real estate of state owned insurers has been transferred to a specialist assets management company under the holding company, and the liquidation program has begun

companies were operating fully by the Government

Investment and being implemented

Date achieved 06/15/2006 06/30/2007 06/30/2007 Comments (incl. % achievement)

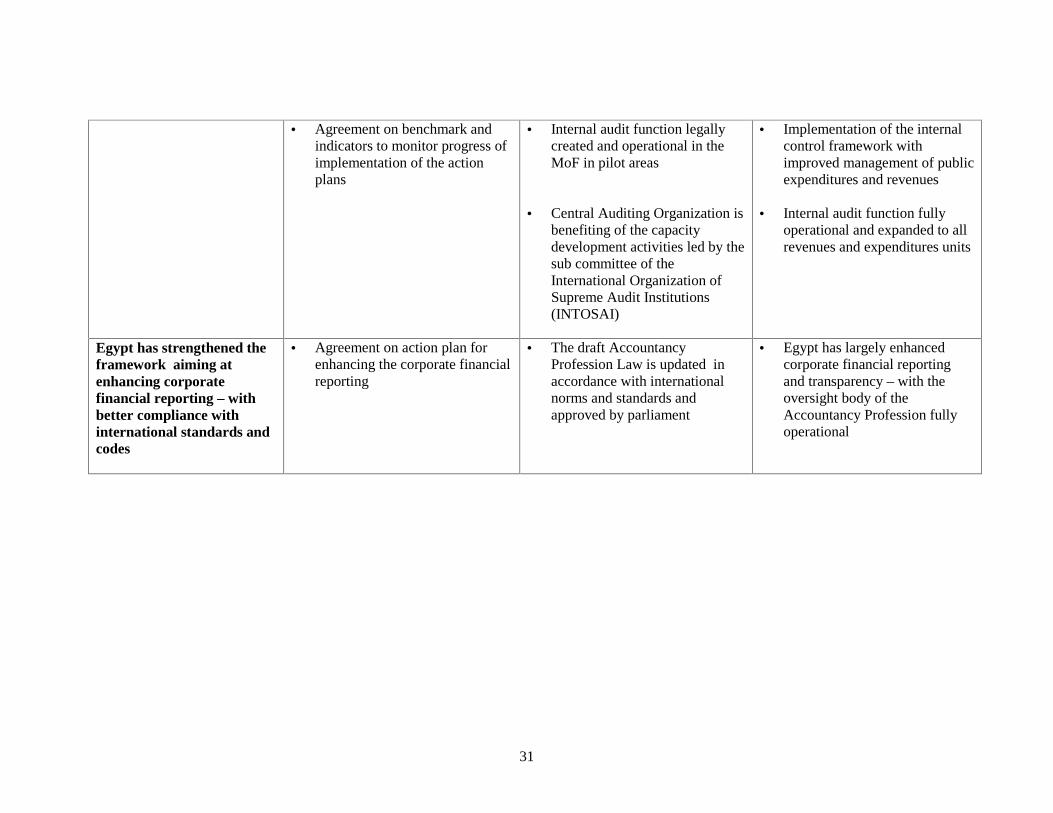

IO Indicator 6: Strengthening the fiduciary framework for public financial management & corporate financial reporting.

Value (quantitative or Qualitative) � Egypt has

strengthened the key areas of public financial management and has strengthened the framework aiming at enhancing corporate financial reporting

� The need to enhance the framework for public financial management & corporate financial reporting.

� Egypt has strengthened the key areas of public financial management—with better controls over revenues and expenditures and availability of accurate and consolidated financial information.

� Egypt has strengthened the framework aiming at enhancing

NA � Ministry of Finance established a single treasury account, which addressed the issue of cash management. In terms of control over revenues, the new tax law and its Executive Regulations addressed the collection of tax income that led to a significant increase in tax revenues.

� Action plan was developed and agreed by the Ministry of Investment and the Capital Market authority (CMA) to enhance corporate financial reporting; and on July 2006, a Ministerial Decree was issued to improve financial reporting.

vii

corporate financial reporting–-with better compliance with international standards and codes.

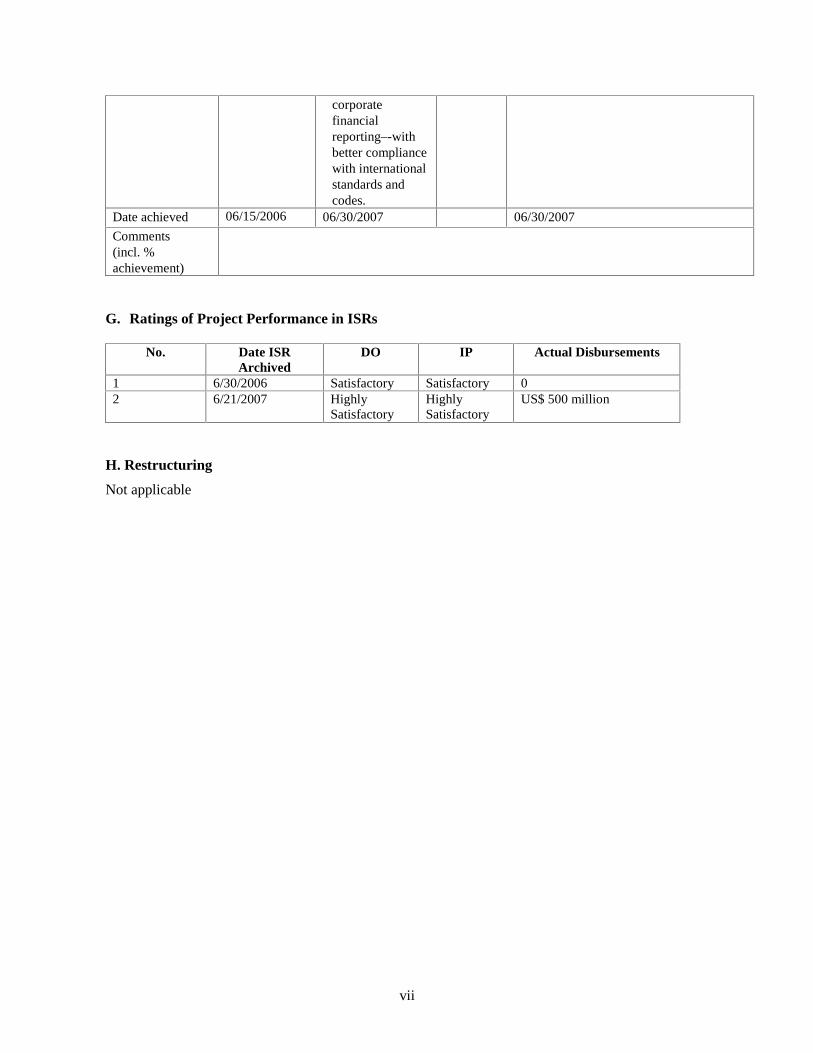

Date achieved 06/15/2006 06/30/2007 06/30/2007

Comments (incl. % achievement)

G. Ratings of Project Performance in ISRs

No. Date ISR Archived

DO IP Actual Disbursements

1 6/30/2006 Satisfactory Satisfactory 0 2 6/21/2007 Highly

Satisfactory Highly Satisfactory

US$ 500 million

H. Restructuring

Not applicable

1

1. Program Context, Development Objectives and Design

1.1. Context at Appraisal

Macroeconomic Framework

The overall performance of the Egyptian economy—a necessary condition to developing a sound financial sector—has continued to improve in 2005. Results are reflected in an accelerating economic growth rate, improved market confidence, strong capital inflows, stability in the foreign exchange market, significant increase in international reserves, decreases in inflation rates, and expansion in the stock market. Since 2004, the government has undertaken various and wide-ranging measures, including tariff cuts, reduction in tax rates, floatation of the exchange rate, privatization of state-owned enterprises, and reforming the financial sector. The restored confidence associated with recent reforms, along with favorable external conditions, has led to improved economic performance. Growth has been reviving since 2004, and real GDP grew by 5.1 percent in fiscal year 2005 compared to 4.2 percent in 2004, after a low growth rate of 3 percent during 2001–03. The large current-account surplus and low international indebtedness help insulate the economy from external shocks. The current account surplus was US$2.9 billion in 2005, accounting for 3.3 percent of GDP. Inflation fell from 18.2 percent in October 2004 to 3.7 percent in March 2006. However, the government budget deficit, though declining, remains relatively high, about 8 percent of GDP. The Bank team found that the overall performance of the Egyptian economy—a necessary condition to restore a sound financial sector—was underpinned by a satisfactory macroeconomic policy framework, but with lingering concerns about long-term fiscal sustainability, which would fade away only if the annual growth rate was sustained at 5 percent at least. The outlook for growth in Egypt was better than it was during the past few years, partly because of high expectations from anticipated reforms and improvements in the investment climate associated with the new government. Overall, the macroeconomic framework was supportive to financial sector reforms.

Sector Background

The financial sector in Egypt has been, over the past decade and a half, the subject of reform efforts. These reforms aimed at financial liberalization to develop more effective financial instruments, strengthen the system infrastructure, and enhance competitiveness through increased private participation. The sector was subject to various legal and regulatory reforms. However, despite these positive steps, the financial system in the late 1990s continued to face significant challenges given the low levels of competition, large non-performing loans (NPLs), relatively high intermediation costs, limited innovation and dominance of state ownership. Non-bank segment was characterized by underdeveloped bond market, insurance,, thin trading in equities, and underdeveloped mortgage markets. The political and economic context at appraisal of this operation was conducive. The reformist cabinet that took office in July 2004 set a major agenda of macroeconomic and structural reforms. An integral component of this comprehensive reform program was the Financial Sector Reform Program that was endorsed by the President in September 2004 for implementation over 2005–2008. This endorsement set the stage for the Ministry of Investment and the Central Bank of Egypt (CBE) to embark on implementing this reform program aimed at addressing the identified vulnerabilities, enhance the performance of the banking sector, as well as developmental non-

2

bank financial institutions, including the insurance sector, the capital market, and the mortgage industry. Underpinning the whole program was also a major effort at strengthening the regulatory capacity and supervisory framework. In this regard, lending further credence to the authorities’ determination to see the reforms through, sweeping executive measures—uncharacteristic of the consensus-driven Egyptian establishment—were taken with the appointment of a new CBE’s Governor, new management at all supervisory and regulatory bodies, including Egyptian Insurance Supervisory Authority (EISA), Capital Market Authority (CMA), Mortgage Finance Authority (MFA), and the Cairo and Alexandria Stock Exchange (CASE). The newly established Ministry of Investment was given oversight for all non-bank financial institutions. In parallel, new management was appointed for the state-owned banks and insurance companies.

Rationale for Bank Involvement

The World Bank Financial Sector Development Policy Loan (DPL) was the ideal instrument to support the government’s financial sector reform agenda. The DPL was consistent with the objectives agreed in the Country Assistance Strategy (CAS) endorsed by the Board on June 16, 2005, in particular under its first strategic objective to strengthen the capacity of the financial system to facilitate private sector development. A high case lending scenario was also envisaged, which included two quick-disbursing loans to support financial sector reforms, considered central to improving the climate for private sector development. The Egyptian authorities valued the Bank’s expertise in financial sector reforms and requested the Bank’s support of the program. Bank involvement built upon years of earlier policy dialogue with the Egyptian authorities particularly in the context of the 2002 joint IMF-World Bank Financial Sector Assessment Program (FSAP) as well as through four “FIRST Initiative” projects sponsored by the World Bank.1 In parallel to DPL, the World Bank was also supporting the housing sector policy reforms through a Mortgage Market Development Project, which helped reinforce the objectives of the proposed financial sector operation.

1.2. Original Program Development Objectives (PDO) and Key Indicators

The main development objective of the operation was to build a more resilient and competitive financial sector with a sound banking system and insurance industry that could contribute better, in the medium-term, to the provision of modern and effective financial services. The operation would support the government in implementing the first phase of the Finance Sector Reform Program. The operation would help achieve this objective in particular by locking in a set of irreversible policy measures. To this effect, World Bank operations seeked to:(i) strengthen the domestic banking system inter-alia by divesting fully state-owned banks shares in joint venture banks, privatizing one of the large state-owned commercial banks, defining a framework to implement institutional, operational and financial restructuring of the remaining public banks, and consolidating and merging small banks in an over banked market; (ii) develop the contractual savings system and restructure the insurance industry so it can play an effective role in the management and transfer of risk and mobilization of long-term savings; and (iii) strengthen the regulatory and supervisory

1 The FIRST Initiatives are: (i) strengthening the capacity of the banking supervision department at CBE; .(ii) strengthening the existing credit information department at CBE; (iii) establishing the private credit bureau and making the necessary regulatory, legal and institutional changes; and (iv) modernizing the payments system at CBE.

3

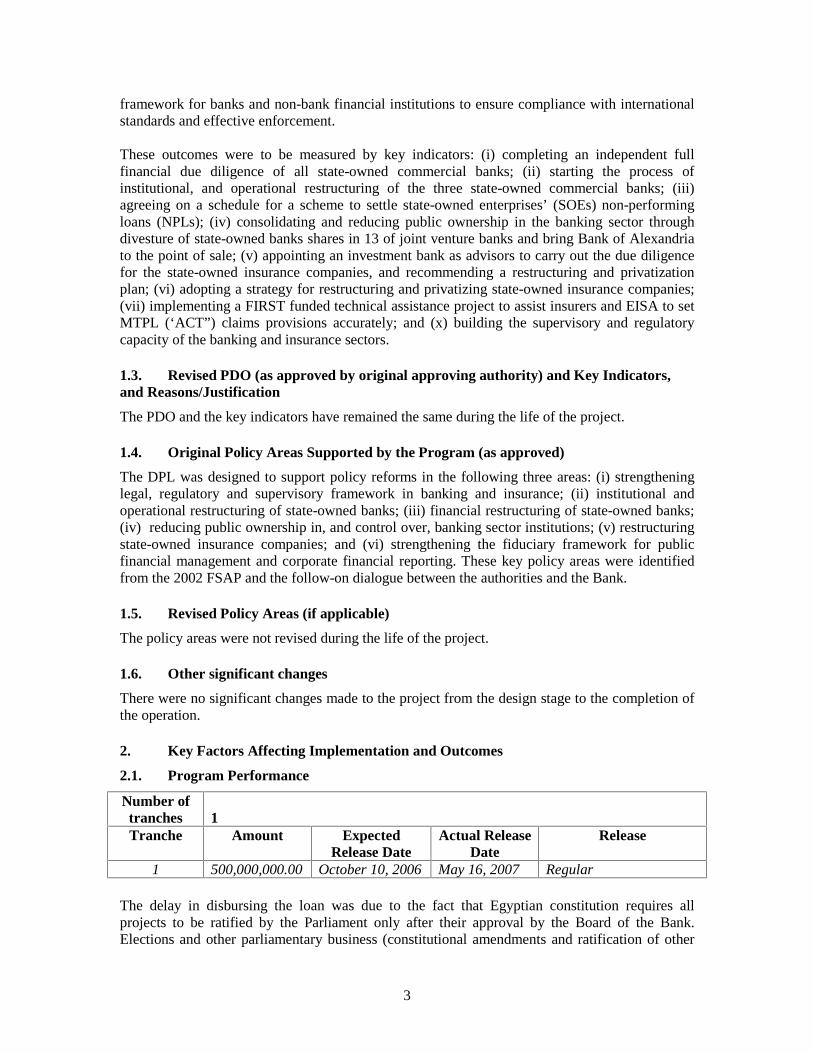

framework for banks and non-bank financial institutions to ensure compliance with international standards and effective enforcement. These outcomes were to be measured by key indicators: (i) completing an independent full financial due diligence of all state-owned commercial banks; (ii) starting the process of institutional, and operational restructuring of the three state-owned commercial banks; (iii) agreeing on a schedule for a scheme to settle state-owned enterprises’ (SOEs) non-performing loans (NPLs); (iv) consolidating and reducing public ownership in the banking sector through divesture of state-owned banks shares in 13 of joint venture banks and bring Bank of Alexandria to the point of sale; (v) appointing an investment bank as advisors to carry out the due diligence for the state-owned insurance companies, and recommending a restructuring and privatization plan; (vi) adopting a strategy for restructuring and privatizing state-owned insurance companies; (vii) implementing a FIRST funded technical assistance project to assist insurers and EISA to set MTPL (‘ACT”) claims provisions accurately; and (x) building the supervisory and regulatory capacity of the banking and insurance sectors.

1.3. Revised PDO (as approved by original approving authority) and Key Indicators, and Reasons/Justification

The PDO and the key indicators have remained the same during the life of the project.

1.4. Original Policy Areas Supported by the Program (as approved)

The DPL was designed to support policy reforms in the following three areas: (i) strengthening legal, regulatory and supervisory framework in banking and insurance; (ii) institutional and operational restructuring of state-owned banks; (iii) financial restructuring of state-owned banks; (iv) reducing public ownership in, and control over, banking sector institutions; (v) restructuring state-owned insurance companies; and (vi) strengthening the fiduciary framework for public financial management and corporate financial reporting. These key policy areas were identified from the 2002 FSAP and the follow-on dialogue between the authorities and the Bank.

1.5. Revised Policy Areas (if applicable)

The policy areas were not revised during the life of the project.

1.6. Other significant changes

There were no significant changes made to the project from the design stage to the completion of the operation.

2. Key Factors Affecting Implementation and Outcomes

2.1. Program Performance

Number of tranches

1

Tranche Amount Expected Release Date

Actual Release Date

Release

1 500,000,000.00 October 10, 2006 May 16, 2007 Regular

The delay in disbursing the loan was due to the fact that Egyptian constitution requires all projects to be ratified by the Parliament only after their approval by the Board of the Bank. Elections and other parliamentary business (constitutional amendments and ratification of other

4

laws concerning approval of economic reforms) lengthened the queue for Parliamentary approvalIn addition given the comprehensiveness of the financial sector reform agenda, Parliamentarians spent far more time than usual discussing the reforms supported under the DPL before finally approving the loan on April 15, 2007. A legal opinion was submitted to the Bank on April 30, 2007 and the loan was declared effective on May 3, 2007.

Tranche 1 List conditions from Legal Agreement/ Program Document Status

A The Borrower has maintained a sound macro-economic framework consistent with the objectives of the Program

Met

B The Borrower has completed the audit of the records and accounts of all state-owned banks, such audit having been carried out by independent auditors in accordance with consistently applied auditing standards satisfactory to the Bank

Met

C. The Borrower has adopted an operational scheme, satisfactory to the Bank, for the settlement of non-performing loans owed by public enterprises to state-owned banks

Met

D. The Borrower has developed and put into effect a program, satisfactory to the Bank, of divestiture of public shareholding in joint-venture banks consisting, inter alia, of the sale of the public sector’s holdings in twelve joint-venture banks.

Met

E The Borrower has received non-binding indicative bids from reputable potential purchasers of Bank of Alexandria.

Met

F. The Borrower has adopted and put into effect a framework, satisfactory to the Bank, for institutional and operational restructuring of the National Bank of Egypt and Banque Misr-Banque du Caire.

Met

G. The Borrower has appointed an investment bank, with terms of reference satisfactory to the Bank, to advise on, and assist in, the implementation of the merger of Banque Misr and Banque du Caire.

Met

H The Central Bank of Egypt has adopted and put into effect a detailed program, satisfactory to the Bank, for capacity building in the areas of banking regulation and supervision.

Met

I. The Borrower has adopted and put into effect a time bound supervisory development plan, satisfactory to the Bank, to enhance the supervisory capacity of the Egyptian Insurance Supervisory Agency as a prelude to a risk-based supervisory regime.

Met

J. The Borrower has completed the preparation of draft insurance sector reform laws regulating premium taxes, brokers and motor third party liability.

Met

K. The Borrower has appointed an investment bank, whose qualifications and terms of reference are satisfactory to the Bank, responsible for the restructuring and privatization of the insurance sector and for conducting the requisite due diligence process.

Met

L. The Borrower has adopted and put into effect a detailed proposal to set up a state-owned insurer holding company.

Met

M. The Borrower has developed a time bound action plan, including monitoring indicators for the ongoing public financial management reform agenda.

Met

N. The Borrower has adopted an action plan for the enhancement of corporate financial reporting

Met

5

2.2. Major Factors Affecting Implementation

Adequacy of Government’s Commitment

Strong government’s commitment to the reform program was key to the success of the operation. The presence in the new cabinet of a core group of credible reformers, including the Ministers of Investment, and the Governor of CBE sent an unequivocal signal to investors and the donors’ community that Egypt is seriously committed to move towards a private-led economy. They designed a comprehensive program of reforms, moved swiftly to recruit highly qualified and experienced professionals in the market specially for the purpose of implementing the banking and non-banking sector reforms. The successful implementation also benefited from an enhanced communications and consultation process through the new strategic partnership between the Egyptian authorities and the Bank during the formulation of the CAS. This involved a constructive dialogue with the authorities based on the principle of mutual commitment between the Egyptian authorities and the Bank, through a policy compact, whereby the Bank commits to support the reform process (not just specific ad hoc measures) in Egypt and the government commits to continuing along an agreed upon reform path.

Soundness of Background Analysis

The design and implementation of the Financial Sector Reform Program and DPL was significantly enhanced by the analytical work carried out in 2002 in the context of the FSAP, the follow-on policy dialogue, and the successive FIRST Initiatives which helped greatly clarify the capacity building needs. The experience that the World Bank has gathered in development policy lending in the financial sector was used by the authorities to guide the design and implementation of the program. USAID and the European Union (EU) have also supported analytical work on reforming and restructuring the financial sector.

Assessment of the Operation’s Design

The design of the operation was well thought out. The operation was a one-tranche operation to support the government in implementing phase I of the Financial Sector Reform Program. At the preparation stage there is the option of having a programmatic operation amounting US$ 1 billion or a two operations amounting to US$ 500 million each, aiming at implementing the reform program. At the Operational Committee (OC) meeting, a decision was taken to proceed with two operations, aiming at supporting the government in implementing the two phases of the government program, which was consistent with the CAS which envisioned two financial sector operations (FY 2006 and FY 2008). Two separate operations were considered more underpinning to irreversible policy measures, as disbursement will occur upon the realizations of up front specific actions under each phase. This would in turn ensure stringer government’s commitment to the comprehensive implementation of the reform program. Despite the complexity of the reform program and the number of organizations involved both domestically as well as outside donors, the policy areas were well identified and narrowly focused; and reforms were sliced into two stages according to their degrees of priority. The Egyptian government has repeatedly indicated its appreciation of the Bank’s integrated delivery of assistance, and has requested the operation as a mean to improve program design and to enhance discipline in reform implementation. The perception that the Bank is prepared to remain engaged in the reform effort helped the dialogue and made the Bank a privileged partner. Given the multifaceted nature of the financial sector reform effort, donors’ contributions were needed. In this context, the authorities sought assistance from other donors to complement that of

6

the Bank to help them implement this comprehensive and substantive reform program. Given the World Bank’s experience, it chose to address banking sector reform while the worked on the supervision and regulatory framework. A large assistance and training program for banking supervision was put in place by the European Central Bank (ECB). USAID provided assistance to the financial sector reforms under a Memorandum of Understanding (MOU) with the Government of Egypt in mortgage finance and the insurance sector, and the IMF was concerned with exchange rate and monetary policy management. Having the presence of many donors itself posed a challenge which led the Egyptian government to put in place an innovative approach to donors support by making it clear that it wanted the Bank to lead the coordination of donors’ support to financial sector reform to avoid overlap and address key issues on a timely and priority basis. To this end, a Financial Sector Donors Sub-group was formed to coordinate efforts related to both technical and financial support provided to the government. Furthermore, the innovative approach followed by the Bank and other donors gave the authorities the flexibility needed to decide on how best to manage the privatization of the Bank of Alexandria and reduce state ownership in the joint venture banks without unduly imposing conditionality that could have undermined their bargaining power. The benchmarking approach helped implementation by focusing on results. In the end, the privatization of Bank of Alexandria transferred seven percent of the banking deposits while the divestiture of state-owned banks shares in joint venture banks, which is more than 95 percent complete, transferred about 20 percent of system deposits to private hands.

Relevance of Risks Identified

Risks identified at appraisal (political, social, fiscal, and governance) were relevant and have been well managed as mitigating factors were embedded in the design of DPL. To mitigate the risk that social, political and stakeholder opposition would weaken government resolve as had happened in the previous efforts to reform the financial sector, the government decided to communicate regularly and in a transparent way the objectives of the reform program, its expected outcomes, to show that consumers will in the end gain from such reforms. There was also a much better communication of the government’s financial sector reform program to the various stakeholders—parliamentarians, media, and political parties. Contingency financing in terms of voluntary early retirement and compensation schemes were planned to alleviate the resulting social burden. In addition, the program included staff training and skills upgrading for employees whose current profile did not readily fit in the organization chart of the restructured financial institutions. The risk to fiscal sustainability from the added burden of bank restructuring (fiscal cost of the settlement of NPLs, tax settlements, and the cost of compensation packages) on an already tight fiscal position was correctly identified and adequately managed. Indeed, the government was able to mobilize significant privatization proceeds of the sale of state-owned bank shares in joint venture banks, the sale of state owned enterprises (law 203 companies) and other public entities, which were then used as planned to partially offset the cost and reduce its potential negative impact on the fiscal position. The risks associated with governance were also correctly identified. To minimize the likelihood that state-owned banks may revert to the old lax management and lending practices that are at the root of their current problems, recapitalization by the government was made conditional on the state banks agreeing upon a plan of operational, institutional and financial restructuring which in

7

turn was made contingent upon, and was to be implemented in step with the progress of the capacity building program and restructuring plan designed to strengthen the banks governance, and overhaul their lending and risk control practices, within a timeframe agreed with the Bank. Full implementation of the institutional and operational restructuring was to remain under close CBE supervision (acting on the owner’s behalf) throughout the restructuring period.

Risks related to the implementation of the program of reforms were rightly judged low because of the strong dialogue and broad agreement on the substance and design of the operation, the continuous dialogue with official counterparts and thorough adequate supervision of the DPL, as well as the Bank’s recognition for the need to proceed diligently with the reform program. The financial sector dialogue conducted in Egypt between the 2002 FSAP and the preparation of this operation allowed for differences between the authorities and the World Bank to be narrowed down, and for a common view to emerge on a number of priority sector policy issues and orientations with clear objectives and a transition process to reach them. These were largely embodied in the government Financial Sector Reform Program. There has been a broad agreement on the substance and design of the operation components, the scope of World Bank assistance, and the need to proceed diligently with the reform program.

2.3. Monitoring and Evaluation (M&E) Design, Implementation and Utilization

(i) M&E design

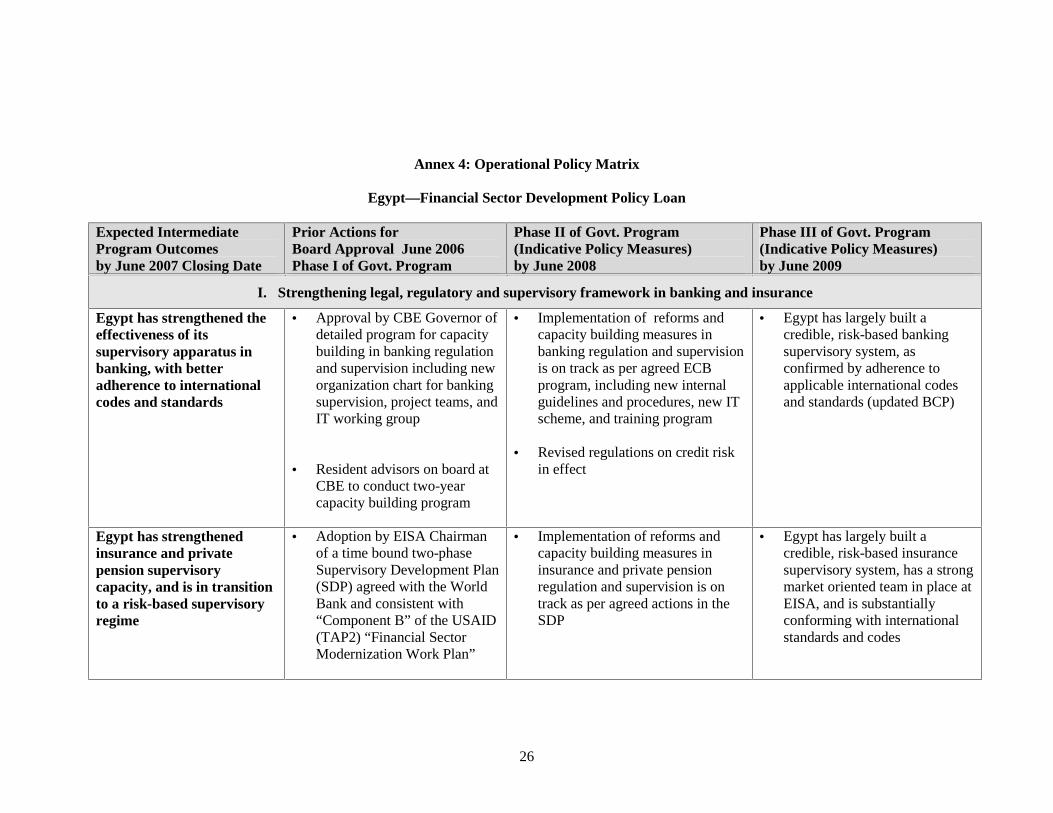

A set of qualitative and quantitative intermediate outcome indicators were defined to monitor progress towards the achievement of the Program Development Objectives (PDO). The M&E framework was established during the design of the DPL for the clear purpose of monitoring progress against the agreed upon benchmarks as outlined in DPL the Operational Policy Matrix (see Annex 4) but also to help design the second stage of reforms to be supported by the forthcoming DPL II. These indicators were selected in agreement with government counterparts, taking into account the availability of data, their relevance and feasibility.

Qualitative operational expected policy outcomes were selected to monitor the progress in the execution of the Financial Sector Reform Program, and the operation, including: (i) implementation of the strengthening of the supervisory and regulatory authorities of banks and insurance industry; (ii) progress in the operational, institutional and financial restructuring of state-owned banks and insurers; and (iii) strengthening the fiduciary framework for public and financial management, and corporate financial reporting. Quantitative indicators were selected in areas where data was available, such as: (i) reduction in NPLs of state-owned enterprises in state-owned banks as of June 2004 by 1/3rd by June 2007; (ii) reduction in public ownership of banks from 65 percent in June 2004 of banking sector deposits to 51 percent by June 2007; and (iii) consolidation of the banking sector, evident in the reduction in the number of operating banks from 57 in June 2004 to 40 in June 2007.

(ii) M&E Implementation

Apart from some difficulties in obtaining up-to-date data on the NPLs, data availability was adequate to follow up on the policy dialogue initiated during preparation of the operation. The program was jointly implemented by the Ministry of Investment and CBE. The Ministry had the overall responsibility for implementing the measures related to the non-bank financial sector, while CBE was the Executing Agency for the aspects of the program dealing with the banking sector. Within the CBE, a Bank Reform Unit (BRU) was set up as the focal point for implementation of banking reforms. The BRU, headed by a Sub-Governor, a former international

8

banker, is staffed with highly qualified and experienced professionals, many of whom were specially recruited for the purpose of implementing the banking reform program. The overall status of the government’s program was well monitored during the supervision missions to ensure that the reform program was on track, and highlighting pending issues to the authorities throughout the process to ensure that all expected and agreed on outcomes are met. In addition, the supervision missions also provided the Bank with the opportunity to continue the policy dialogue with the institutions involved in the program implementation, and to ensure the deployment of staff and consultants able to advise the government in all of the policy and technical areas pertaining to the reforms.

(iii) M&E Utilization

Armed with the information collected from the first ever independent financial due diligence, of the state owned banks, the Bank in coordination with the BRU was able to follow up on the implementation of the plans to restructure the state-owned bank and enhance their governance structure. Specific indicators were designed and monitored through meetings with the state-owned banks’ management to monitor progress in cleaning up the balance sheets, upgrading their IT systems to prepare them for the new competitive, and risk management environment. The Bank’s supervision mission’s discussions with the BRU and the state-owned banks also helped the Bank’s supervision mission staff also monitor progress in implementing these restructuring plans and discuss the next reforms which are going to be supported by the forthcoming DPL II. Similarly, at the Ministry of Investment, sub-units were established to ensure the effective implementation of the various reforms related to the non-bank financial sector. A Steering Committee on Insurance Reform was established by Ministerial decree and included the Chairman of EISA, the resident Technical Advisor to EISA, and one senior executive each from the four public sector insurance companies. The Steering Committee, in turn, set up small restructuring units within each of the public sector insurance companies, whose mandate included ensuring proper communication of the envisaged reform measures to the companies’ staff in order to ensure their commitment and effective participation in the program implementation process. Measures related to the capital market and the mortgage sectors were implemented by the regulatory authorities, the CMA and the MFA respectively, under the overall supervision of the Ministry of Investment.

2.4. Expected Next Phase/Follow-up Operation (if any)

The government’s achievements under DPL I are sufficiently encouraging for the Bank to prepare a follow-up operation in response to the government’s request of December 2, 2006. In this context, the second DPL of US$500 million would support the authorities’ implementation and partial funding of the costs of the second phase of the reform program. Reforms envisioned include strengthening the domestic banking system inter-alia by further reducing public ownership through divesting public sector in joint venture banks, continuing the institutional, operational, and financial restructuring of the state-owned banks, settling the remaining non-performing loans (NPLs) of the state enterprises and the private sector, encouraging further consolidation and merger of small and weak private banks through stronger capital requirements, and adequate provisioning.

Phase II of the reform program would also include a comprehensive agenda for the development of non-bank financial institutions and securities markets, with the objective of building a more diversified and balanced financial system, capable of providing the broader range of financial services to a wide range of clients while managing risks effectively. This would include the

9

restructuring and privatization of the insurance industry, the promotion of investment and pension funds, the strengthening of securities regulation, and improvements of the institutional infrastructure for the financial sector, focusing on information infrastructure (credit bureau, and credit registry), payments system, and the establishment of specialized commercial courts.

The follow up DPL is expected to be presented to the Bank’s Board by May 2008.

3. Assessment of Outcomes

3.1. Relevance of Objectives, Design and Implementation

The DPL objectives were to “The main development objective of the government financial sector reform program, and of the proposed World Bank operation, is to build a more resilient and competitive financial sector with a sound banking system and insurance industry that could contribute better, in the medium-term, to the provision of modern and effective financial services” (DPL PAD, para.39). These objectives were adopted considering that the country had undertaken important measures to build a more resilient and competitive banking system, through consolidation and reduction of public ownership. Numerous foreign banks entered the market which enhances competition. The merger of the three state-owned insurance companies led to the evolvement of a stronger and better performing company. However, credit to GDP declined in this period of reform—from 68 percent in 2003 to 52 percent in 2006, as banks contained lending and increased their holdings of government securities, but this is a typical development in a period of large-scale restructuring and privatization. This ratio is expected to recover, as the reforms implemented under DPL and those to be supported under the forthcoming DPL II, as well those related to improving the investment climate, encourage private investment and a more competitive financial system to finance it.

The design of the DPL was highly aligned with the country’s priorities and CAS. They continue to be relevant at ICR preparation as;

� The 2005 CAS’s first strategic objective was to “strengthen the capacity of the financial system to facilitate private sector development”.

� The DPL fits well within the mandate given to the new cabinet to reduce poverty and improve living standards.

� Financial sector reforms are demonstrably linked to growth and poverty reduction. They are fundamental to reforms in other sectors, including private sector development, infrastructure, housing and social policies.

� Strengthening financial infrastructure acts as a steady promoter of growth and reduces the frequency and cost of financial crises.

� Prevention of financial crises is essential to poverty reduction.

� The DPL objectives remain those that will be pursued under the forthcoming DPL II; this was foreseen at the start of the design of the DPL in 2004 as building a competitive financial system is a medium term endeavor which needs years of reforms and implementation to fulfill the objectives fully.

Thus, the relevance of objectives, design and implementation is considered satisfactory,based on: (i) the consistency of the program with government and Bank priorities; (ii) quality of the design, with a clear focus in the resolution of the deleterious problem of NPLs and strengthening of the legal, regulatory and supervisory capacity of the banking and insurance

10

sectors; and (iii) adequate implementation, that resulted in increased sustainability of supported reforms as evidenced by the continuation of the reform program which will be supported by another DPL; by increased private sector interest in Egypt (FDI doubled to US$6 billion between 2003-2004 and 2005-06 and again to US$11 billion in 2006-07) suggesting favorable market perceptions about Egypt’s overall macroeconomic and structural reform program, including the financial sector reform program.

3.2. Achievement of Program Development Objectives

Achievement of Development Program Objectives is considered satisfactory

Key achievements in the banking sector that are the direct result of the reforms implemented under the DPL included: (i) preparation of the fourth largest state-owned bank, Bank of Alexandria, for privatization and selection of an international sales advisor; (ii) divestiture of state bank shares in 13 of the 17 joint venture banks; (iii) consolidation of the banking sector—the enforcement of stricter prudential rules resulted in the exit of small and weak banks through a series of mergers, and acquisitions, and reduced the overall number of banks from 57 in 2004 to 40 in 2007; (iv) completion of independent financial due diligence of all state-owned commercial banks in line with International Financial Reporting Standards (IFRS), showing the extent of the poor quality of the state-owned commercial bank portfolio; (v) development of a strategy for the resolution of NPLs of state-owned enterprises (SOEs) vis-à-vis state-owned commercial banks, with defined resources from privatization proceeds; (vi) settlement of more than 30 percent of NPLs of SOEs,2 and settlement of 46 percent of the non-SOE’s NPLs in state-owned banks with total collection accounting for 12 percent of those NPLs; (vii) inception of the operational restructuring of the state-owned commercial banks in three critical areas (human resource development, risk management, and information technology); and (viii) adoption of a detailed program for capacity building in banking regulation and supervision. On the divestiture of state-owned bank shares in joint venture banks only 13 out of the 17 joint venture banks have been sold.3 However these 13 banks included the four largest, and accounted for 94 percent of the total market value of state-owned banks ownership in joint venture banks, and for more than 22 percent of deposit market share. It is worth noting that in three of the remaining joint venture banks the state-owned banks have negligible share holdings, namely, Egyptian Saudi Finance Bank (5.3 percent), Egyptian Workers Bank (9.8 percent), and Cairo BNPP (4.8 percent). State-owned banks holding in the fourth bank namely the Export Development Bank of Egypt amounts to 34.5 percent yet its divesture would require amendments

2 In this context, all of Bank of Alexandria public enterprise NPLs, in an amount of US$ 1.2 billion equivalent were settled in cash in February 2006. 3 State-owned banks shares in joint venture banks were sold to private interests in 13 banks, namely: the Egyptian American Bank (33.8 percent public ownership), National Société Générale Bank (18.7 percent), Cairo Barclays Bank (40 percent), Misr America International Bank (48.9 percent), Misr Romania Bank (33.3 percent), Egyptian Commercial Bank (9.8 percent), Suez Canal Bank (5 percent), Misr International Bank (25.9 percent), Commercial International Bank (CIB) (18.9 percent), Misr Iran Development Bank (30 percent), Delta International Bank (10.2 percent), Cairo Far East Bank (19.6 percent), and Alexandria Commercial & Maritime Bank (5 percent). The sale process is underway in the remaining 4 joint-venture banks, namely: Egyptian Saudi Finance Bank (5.3 percent), Egyptian Workers Bank (9.8 percent), Cairo BNP Paribas Bank (4.8 percent), and Export Development Bank of Egypt (34.5 percent).

11

to its by laws that is taking some time4, the Banking Reform Unit at CBE is currently working on the divestiture of those four remaining joint venture banks.

Main achievements in the non-banking sector that are the direct result of the reforms implemented under DPL included: (i) initial progress in restructuring the state-owned insurance companies. The authorities are working on developing restructuring and privatization plans for the insurance companies with the support of BNPP—the consortium leader. The process has been facilitated by the establishment of the Insurance Holding Company in July 15, 2006 by Presidential Decree 246 of 2006, and the appointment of its chairman and board in September 6, 2006; (ii) preparation of a development plan to enhance the supervisory capacity of insurance and private pensions in transition to a risk-based supervisory regime at the EISA with funding from USAID, as a result of which the capacity of the insurance and private pension supervisor has been strengthened, and is in transition to a market based system incorporating a risk-based supervisory regime; (iii) excellent progress was made in the Motor Third party Liability (MTPL) reforms through the endorsement of a time-bound MTPL reform strategy by the Cabinet in December 2006, the establishment of a MTPL working committee, and actuarial assessments have been carried out by Milliman; (iv) the Insurance Law 10 of 1981 was reviewed to suit a market-based rather than a state-owned sector, and new draft law was prepared and reviewed by the Bank team.; and (v) Stamp Law of 2006, with stamp duty dropping overall by 50 percent and being removed altogether for life insurance—one of the key recommendations put forward by the 2002 FSAP. Inter ministerial agreement has been reached on increasing MTPL premium rates by decree. Progress has been evident regarding strengthening the insurance and private pension supervisory capacity. Capacity building at EISA is underway, and it initiated the Supervisory Development Plan (SDP), which has progressed well. EISA completed a Supervision Manual and a Letter of Intervention, and has also conducted a supervision test of their risk based supervision model at AIG and Allianz—two foreign insurance companies operating in Egypt and worldwide, with well established experience in the risk based approach to supervision. The Insurance Holding Company (IHC) has been established and a Chairman has been appointed, which has enabled EISA to focus on regulatory and supervisory reform. EISA has put in place a new IT environment that will ultimately establish online connection with the insurance companies it supervises and regulates so as to minimize reaction time. Notable progress has been made in the SDP. SDP has been updated and improved. The implementation team has been formed (with support from USAID funded project). Stamp duty reduction amendment issued and implemented in July 2006 (reduced by 50 percent from 20 percent to 10 percent for general insurance). For life insurance the duty was reduced from 4 percent to 1 percent for the company share and from 3 percent to 0 percent for the policyholder. In addition, the law concerning MPTL was passed in June 2007 and an executive regulation was issued in August 2007. Rates on MPTL were increased and a new rate list was issued and was effective as of September 2007. These new measures will take the MPTL business to a break-even situation. There will an annual rate review based on the technical results. Non own use real estate of state-owned insurers has been transferred to a specialist assets management company under the holding company, and the liquidation program has begun. Misr Real Estate Asset Management (MREAM) was established in February 2007 and held

4 Selling state-owned banks shares in the Export Development Bank would require an amendment of its bylaw, to be approved and decreed by parliament as the law governing its establishment was enacted by parliament and stipulates state-ownership of 75 percent.

12

its first General assembly in July 2007. The Board of Directors has been formed and the company’s bylaws have been approved. The general assembly of each State-owned Insurer (SOI) met on November 13, 2007 and approved the full transfer of real estate from the SOIs to MREAM. MREAM is currently working to liquidate assets according to a predetermined time frame. On the insurance sector, although major progress has been made in identifying the financial status of the MTPL system and underlying causes of deficiencies, amending MTPL law was delayed. While all the relevant Ministers accept the urgent need for MTPL reform, the quantum of any price increased needed to put the system back into balance (up to 6 times current prices) raises serious transition issues, including the likelihood that permanent cross subsidies will be required and that price increases will have to be phased in over a number of years. In addition, there is not universal agreement that unlimited cover should be removed. During supervision the Bank provided considerable background on coverage and premium setting systems in other countries, and in particular pointed to an international trend to require minimum rather than unlimited coverage for both physical damage and injury claims. Although a number of achievements in the insurance sector have been made, some intermediate outcomes in DPL are still behind schedule. A draft Corporate Brokers Law was prepared but given that it needed strengthening, it was agreed with the Bank that it would be reviewed for further amendments before it is presented to the Parliament. EISA is reviewing Insurance law 10 of 1981 to this effect. The amendments will also include an increase in minimum capital for insurance companies from LE 30 million to LE 100 million. Ministry of Investment expects to submit this law to Parliament during December 2007 –January 2008. On strengthening the Fiduciary Framework for Public Financial Management and Corporate Financial Reporting, achievements directly related to DPL, include: (i) strengthening the public financial management—with better controls over revenues and expenditures and availability of aggregated financial information. The Ministry of Finance established a single treasury account, which addressed the issue of cash management through the issuance of Law 139 of 2006. This will lead to better cash management, which has implications for enhanced controls over expenditures. In addition, Egypt has strengthened the framework aiming at enhancing corporate financial reporting—with better compliance with international standards and codes. An action plan was developed and agreed on with the Ministry of Investment and the CMA to enhance corporate financial reporting; and on July 2006, a Ministerial Decree was issued to adopt, effective January 2007, translated International Financial Reporting Standards (IFRS). Finally, while in some cases the impact of the actions taken might take time to be felt, in others it is clear that actions supported by the DPL resulted in appreciable improvements as shown by the medium term outcome indicators.

� State control of the banking sector was reduced as indicated by the share of the banking system deposit under state control or influence which declined from 65 percent in 2004 to 51 percent in June 2007. This was due to the privatization of Bank of Alexandria, the fourth largest state-owned commercial bank, and the divestiture of the state-owned banks shares in 13 of the joint venture banks.

� The stock of NPLs by state-owned enterprises at the state-owned commercial banks was curtailed by over 60 percent falling from L.E 26 billion to L.E. 10 billion. The stock of private sector NPLs was also significantly reduced through the work out unit created at the state-owned banks with a recovery rate of 22 percent, of which 85 percent in cash.

13

� Provisioning of state-owned banks was improved as shown in the ratio of provisions to NPLs which increased from 42 percent and 32 percent in 2005 for National Bank of Egypt and Bank Misr respectively to 55.9 percent and 57.6 percent in 2006.

� The increase in capital requirements and stricter compliance enforcement rules have led to a vast consolidation in the banking sector that led to a fall in the number of banks operating in the sector from 57 in June 2004 to 40 in June 2007.

3.3. Justification of Overall Outcome Rating

Rating: Satisfactory

The overall outcome rating for DPL is “satisfactory”. Planned reforms were implemented, some (such as the privatization of Bank of Alexandria) ahead of time and are achieving their key objectives of restoring soundness in the banking sector. Significant institutional and operational strengthening has been carried out in the state-owned commercial banks and insurance companies. While the government is pursuing its reform agenda, the impact of the measures taken under DPL is perceptible: (i) state control in the banking sector has been appreciably reduced through privatization and divestiture; (ii) the supervisory and regulatory framework is more robust than it was before the reforms were launched; (iii) the large stock of NPLs has been significantly reduced and provisioning boosted resulting in sounder state-banks balance sheets; (iv) state-owned banks are undergoing a comprehensive restructuring that will enhance their operations and profitability, will enable them to operate as pure commercial entities, and will reduce drastically the likelihood of future claims on the government budget; and (v) new laws have been introduced and others amended to remove significant constraints on the development of the insurance sector (Stamp Duty Law and MTPL Law).

3.4. Overarching Themes, Other Outcomes and Impacts

(a) Poverty Impacts and Social Development

Though the DPL did not have explicit social development outcomes as objectives, clearly the shift from public to a more market-oriented financial system is expected to have a direct and positive impact on growth, employment, and crisis prevention, while also increasing access of various social groups, including the poor to financial services. The privatized Bank of Alexandria has already increased its outreach in rural areas through mobile banking services outputs, increased ATMs, and is moving into the SME finance market. Restoring the soundness of the state-owned insurance companies and increased competition in the sector will enable the industry to provide better quality products at a more reasonable cost. This combined with the sharp reduction in stamp duty levied on insurance premia will lower the cost of insurance for Egyptians and ease access to insurance in a country where penetration is very low. The measures aimed at addressing the soundness of the private pension funds and strengthening of the supervisory function of the pension system will ensure that the interest of retirees are protected in the future and that their savings are well managed.

(b) Institutional Change/Strengthening

The DPL had, and will continue to have, a substantial institutional development impact in the financial sector even though it was a single-tranche project. The policies supported by the program are fast transforming the Egyptian financial sector. Substantial capacity building provided to CBE, and EISA are modernizing these institutions while introducing state of the art risk management tools and IT systems and will lead to the emergence of a robust supervisory and

14

regulatory capacity in the country. The comprehensive operational and institutional restructuring of the two largest state-owned commercial banks is modernizing these banks and enhancing their operating environment thereby contributing to enhancing their capacity to increase intermediation and improve savings mobilization. Substantial staff training sector wide, in and outside Egypt, will have a long lasting impact and will develop a pool of financial skills hitherto not readily available in Egypt thereby contributing to the sustainability of the reforms.

(c) Other Unintended Outcomes and Impacts (positive or negative, if any)

Not applicable

3.5. Summary of Findings of Beneficiary Survey and/or Stakeholder Workshops

Not applicable

4. Assessment of Risk to Development Outcome

Rating: Low to Negligible

The risks to development outcomes which were well identified at appraisal remain low to negligible. Three sources of risks were identified at that point: (i) political feasibility and macroeconomic framework; (ii) building credible and independent regulators; and (iii) state banks reverting to old lax management practices after recapitalization. After closing the operation, the risk to the Development Outcome is considered Negligible to Low since the mitigating measures envisaged in the Program Document are still in place.

(i) Political feasibility and macroeconomic framework: Nearly two years after appraisal, commitment of the government towards the reform program continues to be strong and focused on implementation as evidenced by their request for a second operation to support the second phase of reforms. In addition, despite some criticism of the privatization of Bank of Alexandria by the media, most agree that the privatization was a success, brought in more revenues than expected, with the privatized bank leading change in modernizing access to financial services. The labor layoffs were also well managed through the implementation of early and retirement programs. (ii) Building credible and independent regulatory authorities. The credibility and independence of the regulator is the base upon which a resilient financial system may emerge and prosper. This risk relates to the authorities’ ability, within the program timeframe, to build the capacity and implement the strengthened regulatory and supervisory framework. These risks are being adequately managed through the strong donor driven capacity building initiatives discussed earlier and the Government’s commitment to continuing to benefit from ECB’s existing technical assistance. The protocol agreement for a two year technical assistance program will end in December 2007. ECB was asked to submit a draft report on a successor assistance program to be discussed between CBE, EU and Ministry of International Cooperation in Egypt. (iii) Recapitalization without privatization is considered a serious risk for fiscal waste at best, such unconditional financial support may provide bank management with the wrong signal to pursue their past and costly lending practices. To reduce such a risk, the Government is still committed to proceed with the recapitalization of these banks only

15

upon the satisfactory implementation of their operational and restructuring plan. Full compliance is being closely monitored by CBE (acting on the owner’s behalf) and the Bank.

5. Assessment of Bank and Borrower Performance

5.1. Bank Performance

(a) Bank Performance in Ensuring Quality at Entry

Rating: Highly Satisfactory

Bank performance is rated as highly satisfactory at entry. The project team paid particular attention to ensuring high quality at entry for this operation. The Loan identification and design were consistent with the CAS, and the recommendations put forward by the 2002 FSAP. In terms of design, a single-tranche operation was chosen to support the government in implementing Phase I of the Financial Sector Reform Program. This ensures comprehensive completion of all reform measures envisioned at the first phase. Main components of the operation were developed from the recommendations of 2002 FSAP.

� The Bank was instrumental in taking full advantage of a window of opportunity presented by the reformist government that led to this major progress on financial sector reforms outcomes.

� Sound preparatory and analytical work, strong policy dialogue and good working relationships with government counterparts, high level of consultation with market participants, and Bank expertise led to the design of an operation which took into account the need to build regulatory capacity, and manage the key risks (political, social, fiscal, and governance) that could derail implementation.

� Close coordination with the active donors in the financial sector work, namely USAID, the EU, AfDB and the IMF to help the government build the necessary capacity to implement the program.

� The Bank set a clear results based framework which included reaching an irreversibility step in the privatization process of the Bank of Alexandria, and agreeing to subjecting recapitalization of restructured state owned banks to implementation of the financial, institutional, and operational plans before taking the operation to the Board.

� The insurance sector witnessed significant reforms through the adoption of a comprehensive restructuring strategy for the insurance sector, the establishment of the Insurance Holding Company, the issuance of the Stamp Duty Law and MTPL Law.

In addition, the Bank rightly identified the principal risks to which the financial sector was exposed and ensured that the FS DPL Program would address those risks which were related to the most vulnerable areas of the financial sector, the banking and insurance sectors.

(b) Quality of Supervision

Rating: Satisfactory

Bank supervisory performance is rated as satisfactory. The Bank conducted two supervision missions, in addition to the regular monitoring of the progress in the field. The policy dialogue continued with official counterparts on both the implementation of the reforms under DPL but also on new areas of reforms which the government wanted to seek advice on. Period monitoring

16

of the implementation of the reform program and the operation was done regularly from the field by the task manager, in addition to the periodic supervision missions. These missions provided sound technical advice to the authorities. For example, the team was strengthened with experts that provided substantive comments and input in the drafting of some laws and amendments to existing ones before their presentation to parliament. The missions followed up on progress on the agreed monitoring indicators and discussed results with the Ministry of Investment and CBE as well as other counterparts in the sector. These supervision missions had their terms of reference extended to the preparation of the follow up operation DPL II.

(c) Justification of Rating for Overall Bank Performance

Rating: Satisfactory

The rating of satisfactory is based on the following considerations: (i) the project was very well designed, its PDO was in line with the CAS and the Bank’s priorities, the intermediate indicators were relevant, helped focus the supervision, and helped inform the design of the second stage of reforms; (ii) the Bank was aware of the challenges involved in seeking the reduction of the state’s ownership of financial sector assets and addressing the restructuring of major financial institutions so it adopted a flexible results based framework and a risk mitigating strategy, in consultation with the authorities, who remained committed to the implementing the reforms; (iii) from identification to closing, the team was extensively involved in a policy dialogue with the authorities and independent counterparts, collaborating to ensure that the ultimate goal of this operation - to assist Egypt in strengthening the enabling environment for financial intermediation, resource mobilization and risk management, and increasing private sector role and participation in the provision of financial services- would be achieved; and; (iv) the project team and the country office developed an optimal level of cooperation that played a key role in the success of the operation.

The combination of clear and focused policy actions supported in PL with sustained dialogue before and after the loan was approved and disbursed, during supervision and preparation of other operations, resulted in a constructive interaction with counterparts, strengthening sustainability of the policies supported by DPL in the process. QAG rated the DPL satisfactory (2) overall. Strategic, relevance and approach was rated as highlight satisfactory (1). QAG Panel praised the “sound preparatory work, drawing effectively on prior studies, and the country team's good working relationships with government counterparts and linkages to other donors enabled the Bank to take advantage of a window of opportunity for progress on financial reform.” It also acknowledged that the work was fully in line with the recommendations of the 2002 FSAP and the current CAS (approved in 2005). The Bank chose to work on banking sector reform, given its experience in this field. QAG congratulated the Bank Team for its ability to take full advantage of a window of opportunity presented by a reformist government and on actually being associated with a concrete result.

5.2. Borrower Performance

(a) Government Performance

Rating: Highly Satisfactory

From the design to implementation stage, the government was in the “driver seat” seeking advice from the Bank where needed to implement its strategic reform agenda. The authorities remained focused on the success of the Development Objective as they saw its importance in fulfilling ultimately through the financing of a private sector let investment strategy, their growth and

17

improvement of Egyptians living standards. In this context, the Government took the initiative to seek support from other donors according to their respective comparative advantage, and was keen on ensuring good coordination between the various partners. The decision to request the Bank to play a lead role succeeded in getting the best out of each donor’s support and avoided waste that comes from unclear donors mandate and overlap. The donors coordinating committee, chaired by the Bank, also helped the Government address key financial sector issues on a timely and priority basis.

(b) Implementing Agency or Agencies Performance

Rating: Satisfactory

Implementing agencies Ministry of Investment (MOI) Satisfactory Central bank of Egypt (CBE) Satisfactory The Ministry of Investment and CBE are the two agencies responsible for the design and overall implementation of the operation. The Minister of Investment and the Governor of CBE, his two deputies, and the CBE Banking Reform Unit staff in charge of the implementation of the reforms, were instrumental to the success of this operation. They were systematic in the way they went about the design of the blueprint for the reforms, and seeking advice from the Bank and other donors, at judicial junctures to keep the implementation moving and get support and advice when they encountered major challenges. The reporting and coordination of actions between the concerned agencies was efficient and timely throughout the life of the project resulting in a successful operation that went far beyond compliance with identified intermediate outcomes as one can see during the follow on operation that is under preparation. Their availability and knowledge of all the program benchmarks allowed for a timely presentation to the Board of the operation and for an effective implementation of the FSDPL reform agenda before project closing.

(c) Justification of Rating for Overall Borrower Performance

Rating: Satisfactory

The rating of satisfactory is justified by the following:

� The GOE demonstrated a clear ownership of the project. The respective responsibilities of the MOI and the CBE where clearly defined reducing to a minimum the opportunities for overlapping or misunderstanding.