world bank document...1999/08/15 · annex ii government of malawi's letter of development...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: P 7273 MAI

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL DEVELOPMENT ASSOCIATION

TO THE

EXECUTIVE DIRECTORS

ON

A PROPOSED CREDIT AND TECHNICAL ASSISTANCE PROJECT

iN THE A\MOUNT EQUIVALENT TO SDR 65.7 MILLION AND SDR 1.5 MILLION

TO

THE REPUBLIC OF MALAWI

FOR

THE SECOND FISCAL RESTRUCTURING AND DEREGULATION PROGRAM

AND THE

'.ECO\D FISCAL RESTRUCTURING AND DEREGULATION PROGRAM TECHNICALASSISTANCE PROJECT

NOVEMBER 10, 1998

Tlhis document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWVorld Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

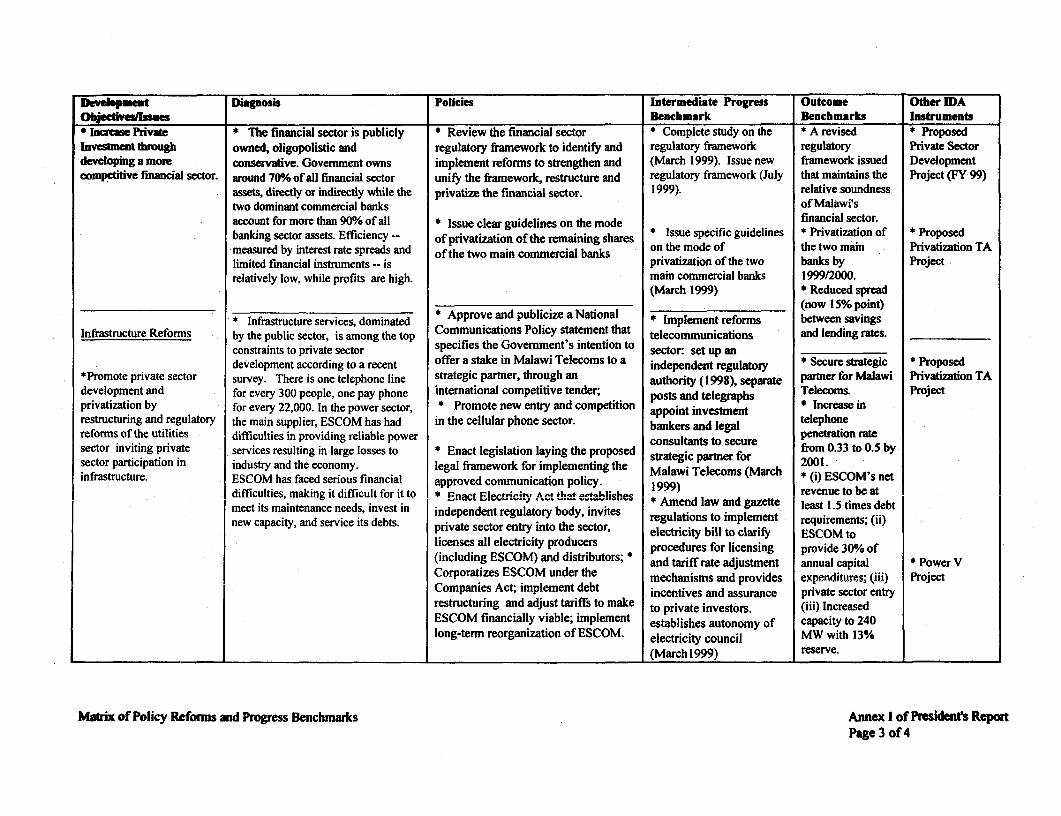

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective October 1, 1998)

Currency Unit = Malawi Kwacha (MK)US$ I = MK42.875MK I = US$0.0233

SDR I US$1.369863

MEASURES

Metric System

FISCAL YEAR

July I to June 30(as of July 1998)

Vice President :C allisto E. MadavoCountry Director :Barbara KafkaSector Manager :Ataman Aksoy

Task Team Leader : Ahmad Ahsan

FOR OFFICIAL USE ONLY

GLOSSARY OF ACRONYMS

ADMARC Agricultural Development and MIarketing CorporationBOP Balance of PaymentsCAS Country Assistance StrategyCBM : Commercial Bank of MalawiCOMESA Common Market for Eastern and Southem AfricaESAF Enhanced Structural Adjustment FacilityESCOM Electricity Supply Corporation i(previously, Commission).GDP Gross Domestic ProductGOM Government of MalawiHIAL High Impact Adjustment LendingIBRD International Bank for Reconstruction and DevelopmentIDA International Development AgencyIDF Institutional Development FundlIMF International Monetary FundLDP Letter of Development PolicyMDC Malawi Development CorporationMK . Malawi KwachaMPTC Malawi Posts and Telecommunications CorporationMT : Metric TonsMTEF Medium-Term Expenditure FrameworkOED Operations Evaluation DepartmentPAR Project Audit ReportPCR Project Completion ReportPFP : Policy Framework PaperPRP . Permanent Residence PermitPSD Private Sector DevelopmentRBM Reserve Bank of MalawiSPA Special Program of Assistance to Low-income Debt Distressed

Countries in Sub-Saharan AfricaTA : Technical AssistanceTEP Temporary Employment PermiitTOR Terms of ReferenceVAT Value Added Tax

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may nol: otherwise be disclosed withoutWorld Ban}c authorization.

MALAWI

SECOND FISCAL RESTRUCTURING AND DEREGULATION PROGRAM (FRDP)AND FRDP II TECHNICAL ASSISTANCE

Table of Contents

I. INTRODUCTION ....................................................... 1

II. ECONOMIC DEVELOPMENTS AND PROSPECTS ........................................2Box 1: Policy Reforms Undertaken by the Government Since 1994 .................. 3

III. THE REFORM PROGRAM ...................................................... 6

A. Improving Public Sector Efficiency ....................................................... 6Improving Public Expenditures ....................................................... 6Rationalizing Government Functions ....................................................... 8Tax Policy Reforms ....................................................... 9

B. Supporting Growth Through Private Sector Development .............................. 9.... 9Box 2: Policy Reforms Supported by FRDP II ......................................... 10Privatization ...................................................... 11Infrastructure Policy Reforms ...................................................... 12Agriculture Markets and Storage ...................................................... 13Maize Price and Marketing Reforms ...................................................... 14Facilitating Temporary Employment Permits ...................................................... 14

IV. IMPACT OF REFORMS ...................................................... 5 SBox 3: Overview of FRDP II: Instruments, Intermediate Targetsand Outcomes ...................................................... 16

V. DESIGN OF CREDIT, IMPLEMENTATION AND DISBURSEMENT ....... 17Lessons from Operations Evaluation Department Reports andthe High Impact Adjustment Lending ........................................... 17Relationship with the Country Assistance Strategy .......................... 18Disbursement Procedures and Implementation Arrangements ............. 18

VI. BENEFITS, RISKS AND GOVERNMENT OWNERSIHIP ........................... 19

VII. CONCLUSION ...................................................... 20

Annexes

Annex I Matrix of Policy Reforms

Annex II Government of Malawi's Letter of Development Policy

Annex 1I- I Expenditure Prioritization Targets in the 1998/99 BudgetAnnex II-2 Expenditure Prioritization/Medium Term Expenditure Framework

Preparation Plan for 1998/99Annex II-3 Expenditure Monitoring and Control ProceduresAnnex 11-4 Rationalization of Government FunctionsAnnex 11-5 Divestiture Sequence PlanAnnex II-6 Implementation Plan for Telecommunication Sector Reforms

Annex III Previous IDA Adjustment Operations in Malawi

Annex IV : Status of Bank Group Operations in Malawi: IBRD Loans and IDACredits in the Operations Portfolio

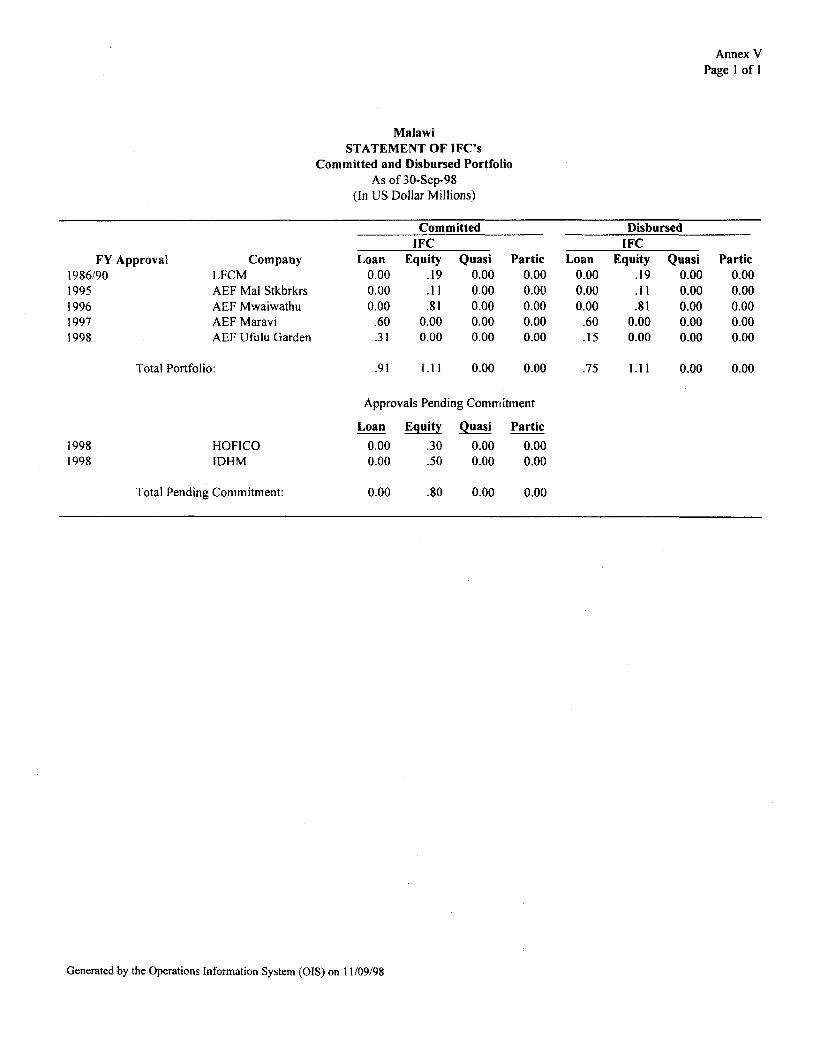

Annex V Statement of IFC's Committed and Disbursed Portfolio

Annex VI : Malawi at a Glance

Annex VII : Malawi Social Indicators

Annex VIII : Key Economic Indicators and Key Exposure Indicators

Annex IX Balance of Payments

Annex X : Procurement and Disbursement Procedures for the FRDP II TAProject

Map IBRD No. 29374

The FRDP II credit and the FRDP II TA Project were prepared by an IDA team consisting ofAhmad Ahsan (Senior Country Economist and Task Team Leader, AFTMI), Peter Moll (CountryEconomist, AFTM 1), Tejaswi Raparla (Research Analyst, AFTM 1), Rose Thunyani (Senior TaskAssistant, AFTM1), Elizabeth Adu (Principal Counsel, LEGAL), Steve Gaginis (DisbursementOfficer, LOAAF), Jim Smith, Deputy Resident Representative (AFMMW), MaxwellMkwezalamba (Economist, AFMMW),. Stanley Hiwa (Agricultural Economist, AFMMW),Ahmet Soylemezoglu (PSD Specialist, AFTPI), Arnold Sowa (PSD Specialist, AFTPI), PaulBermingham (Principal Financial Analyst, IEN), Anna Bjerde (Economist) and Paivi Koljonen(Economist, AFTGI). Peter Miovic (Sector Manager, AFTM2), Gene Tidrick (Lead Specialist,AFTMI), and Shahid Yusuf (Economic Advisor, DECVP) were reviewers. Overall supervisionand guidance were provided by Robert Liebenthal (Resident Representative), Ataman Aksoy(Sector Manager) and Barbara Kafka (Country Director).

MALAWI

THE SECOND FISCAL RESTRUCTURING AND DEREGULATION PROGRAM CREDIT(FRDP II) AND THE SECOND FISCAL RESTRUCTURING AND DEREGULATION

PROGRAM TECHNICAL ASSISTANCE PROJECT (FRDP II TA)

SUMMARY

Borrower: Government of the Republic of Malawi

Guarantor: Not applicable

Beneficiary: Republic of Malawi

Amounts: SDR 65.7 Million (US$90 Million equivalent) and SDR 1.5Million (US$ 2 Million equivalent).

Terms andCommitment Charge: Standard IDA Terms, with 40 years maturity and I 0-year

grace period.

Co-financing: Co-financing discussions are taking place with the AfricanDevelopment Bank and the Overseas Economic CooperationFund of the Government of Japan. Staff from theseorganizations participated in the IDA Appraisal mission for thecredit.

Disbursement: The FRDP II Credit will follow the Bank's new simplifieddisbursement procedures for structural adjustment credits.Under the revised procedures the Credit will be disbursedagainst satisfactory implementation of the adjustment programand not tied to any specific purchases. Once the Credit isapproved by the Board, and becomes effective the proceeds ofthe first tranche of SDR 43.8 million will be deposited by IDA inan account at the Reserve Bank of Malawi at the request of theBorrower. The second tranche of SDR 21.9 million will bedisbursed after the second tranche conditions on expenditureprioritization, rationalization of Government functions andprivatization have been met. The disbursement and procurementprocedures for the FRDP II TA project are laid out in detail inAnnex X of the text.

Objectives: The proposed programs will support policy reforms to accelerateeconomic growth and poverty reduction and technical assistanceto help implement policy reforms. The adjustment credit aims tomaintain the momentum of policy reforms launched byGovernment of Malawi since 1994 by improving public

expenditure management and promoting private sectordevelopment. The credit will help to meet the balance ofpayments financing requirements that Malawi faces this year thathave increased due to a sharp fall in export earnings, and toimplement policy reforms by maintaining economic stability andmitigating the transitional costs of adjustment.

Objectives FRDP IITA Project: FRDP II Technical Assistance Project has been designed to

provide necessary technical support, training and equipment tomeet three objectives: (i) implement policy reforms, includingthe medium term expenditure framework, auditing andreviewing the development budget, reforrning expenditurecontrol procedures and systems, and implementing civil servicereforms; (ii) evaluate the impact of structural reforms onMalawi's economy, in particular by examining the effects ofliberalizing trade and exchange rate policy on manufacturing,and liberalizing agriculture production and trade on theagriculture sector; and (iii) develop the agenda for the next oundof macroeconomic and sectoral policy reforms through researchinto further constraints to growth. A separate proposedPrivatization Technical Assistance Project (US $ 10 million) willprovide assistance to implement the privatization program.

Government Commitment: The Government of Malawi has a credible track record ofimplementing policy reforms (see Box 1, pp. 3 of President'sReport). The FRDP II credit is primarily based on detailedreforms programs prepared by the Government in the areas ofexpenditure management, rationalization of Governmentfunctions and privatization. Following this, the basis of the legaldocuments, the Development Credit Agreements has been theGovernment's Letter of Development Policy which details, inthe text and in Annexes all these reforms. This ownership of thedesign of the program will be publicly affirmed by theGovernment issuing and disseminating a White Paper (inNovember 1998) presenting this reform program to the people ofMalawi. The Cabinet Committee on the Economy will overseethe implementation of the FRDP II as a key part of its overalleconomic reform program. This committee will be assisted by aTask Force of officials led by the Ministry of Finance tosupervise and to coordinate the implementation of the program.

Benefits: The reform program, supported by this credit, will benefit thepeople of Malawi by leading to accelerated reduction in povertyin two ways: (i) helping to create conditions -- macroeconomicstabilization, improvement in infrastructure and major advancesin privatization --for a broad based GDP growth of between 5% -6% p.a. in the 1999 - 2001 period; this high case scenario

ii

should, ceteris paribus, lead to a decline in the poverty headcount ratio from 43% to roughly 38% of the population in thenext five years; and (ii) by improving the targeting of publicexpenditures and Government s:rvices towards the poor.

Risks: The key risk arises from the possibility that the commitment topolicy reforms may be unsteady, especially in the face ofapproaching elections in May 11999. However, in early 1998, thepolitical economy changed mairkedly as a reconstructed cabinetcommittee on the economy has now the authority to make andimplement key decisions on the economy. Nevertheless, in therun up to the elections these ris:ks will persist: there will be, interalia, pressures to relax expendliture controls, provide subsidieson inputs and on credits to farmers, avoid difficult decisions inareas such as retrenchment of unqualified civil servants, and selllarge assets to non-indigenous persons.

However, these political risks are moderated by the GOM'sappreciation of the gains that can be obtained throughimplementing these reforms and by making the people aware ofthe benefits of these reforms. Government can get credit forwelfare improvements from directing public expenditures togoods and services that benelit the poor, and lead to a moreequitable distribution of income and opportunities, generatinggrowth and employment through deregulation and private sectordevelopment, implementing safety net programs to help the poorsuch as the starter packs program of 1998/99 that will distribute0.3% of GDP in input packages to smallholder households,expanding the public works program and the smallholder credit,and providing a temporary subsidy to Government sales ofmaize to ease the burden of a sharp increase in prices.

The second risk arises from the lack of capacity to implementthis multi-pronged operation. This risk is being addressed byproviding technical assistance and by setting up a high levelGovernment body to oversee the implementation of thesereforms and mobilize necessary resources for doing so.

The final set of risks are posecl by exogenous shocks such as theeffects of drought or large terms of trade losses, such as thosebetween 1992 and 1994, and 1998, on savings, investment andgrowth. The risks posed by these exogenous shocks are bestaddressed in the long run by economic growth, employment anddiversification through implenmenting structural reforms that aresupported by this credit. In the short run the disbursements fromthis credit will provide the economy a buffer against theseshocks and thereby help the Government maintain the course ofreforms.

...

REPORT AND RECOMMENDATION OF TH[E PRESIDENT OFTHE INTERNATIONAL DEVELOPMENT ASSOCIATION

TO THE EXECUTIVE DIRECTORS ON A PROPOSED CREDIT OF SDR 65.7 MILLION(US$ 90 MILLION EQUIVALENT) TO THE REPUBLIC OF MALAWI FOR

THE SECOND FISCAL RESTRUCTURING AND DEREGULATION PROGRAM (FRDPII) AND SDR 1.5 MILLION (US$ 2 MILLION E]QUIVALENT) FOR

THE SECOND FISCAL RESTRUCTURING AND DEREGULATION PROGRAMTECHNICAL ASSISTANCE PROJECT (FRDP II TA)

I. Introduction

1. This memorandum seeks approval to extend a SDR 65.7 million (US$ 90 millionequivalent) structural adjustment credit to Malawi in support of policy reforms to accelerateeconomic growth and poverty reduction, and a Technical Assistance Project of SDR 1.5million (US$ 2 million equivalent) to help implement poliicy reforms.' The credit aims tomaintain the momentum of policy reforms launched by the (Government of Malawi since 1994by improving public expenditure management and promoting private sector development.The credit will help to meet the balance of payments financing requirements that Malawi facesthis year that have increased due to a large fall in export earnings, and to implement policyreforms by maintaining economic stability and mitigating the transitional costs of adjustmnent.

2. The proposed credit will support Government's policies to reduce poverty in threeways. First, by creating the policy environment for higher private sector investment andefficiency, leading to a sustained and diversified growth of GDP of around 5 to 6 % per annum-- without which there may be no reduction in poverty in Malawi.2 Second, by supportingGovernment policies to redirect expenditures into social sectors and programs that benefit thepoor. The targeted growth rate combined with a better targeting of public expenditures to thepoor -- i.e. a more equitable distribution -- should lead to an accelerated reduction of poverty.Third, the financing of the credit will help Government to maintain macroeconomic stability ina year affected by a large terms of trade shock (a 28% drop in tobacco prices) and a US$ 60million (over 3% of GDP) cut in export earnings.

3. This credit comes at a critical period, when Malawi is at a crossroads: it can deepenreforms launched in 1994 which led to economic stabil:ity, and liberalized the economy,especially in agriculture, with impressive results (see Box 1, pp. 3). Or Malawi can slip into acostly period of instability and lost growth, as it did in the second half of 1997 and early 1998.A broad range of key policy reforms undertaken by the Government in recent months (see Box2, pp. 10) underscores the Government's renewed commitment to deepen structural reformsand sustain growth and poverty reduction.

' The implementation of these policy reforms will also be supported by technical assistance provided from othersources such as the Institutional Development II credit ($22 million), and the proposed Privatization TA credit(US$ 10 million).2 The study, "Accelerating Malawi's Growth" (September 1997) showed that, with unchanged incomedistribution and population growth, Malawi needs an annual growth rate of GDP of 5.3% to reduce the absolutenumber of people living below the poverty level.

4. Malawi went off-track its macroeconomic program in December 1997, during a periodof uncertainty and large expenditure overruns. In March 1998, Government appointed a neweconomic management team with wide authority to design and implement stabilization andstructural reforms. Subsequently, in May 1998, the Government and the IMF agreed on a StaffMonitored macroeconomic program that, after satisfactory implementation, will now lead tothe renewal of the third year arrangement of the current Extended Structural AdjustmentFacility (ESAF). The staff papers recommending approval of this arrangement will be issuedto the IMF Board in early December 1998 for their Board meeting in mid-December 1998.Given that Malawi is implementing a satisfactory medium term macroeconomic frameworkand has started implementation of wide ranging structural reforms, and that there is a seriousforeign exchange shortage that can destabilize the economy over the medium term unlessquick balance of payments support is provided, this adjustment credit is being submitted forconsideration by the Bank's Board of Directors two weeks ahead of the Fund Board'sconsideration of the third year ESAF Arrangement.

II. Economic Developments and Prospects

5. In the first 15 years after independence in 1964, Malawi's GDP grew at an averageannual rate of nearly 6%. But the fruits of this growth were poorly distributed3, and growthitself was narrowly based on estate ownedagriculture, and large public and private Table 1: Some Economic and Social Indicatorsconglomerates protected by pervasive barriers Economic Indicators Malawi SSA

to entry. As a result, at the end of this period Per capita income (USS) 220 490

Malawi emerged with one of the worst sets of Population (millions) 10.3 583human welfare indicators in the world [See of which urban % 13 31

Table 1 and Annex VII for datal. Then, Agriculture as % of GDP 32 24

starting in the late 1970s, Malawi suffered from Social Indicators 13 30

a series of exogenous shocks -- high import Life expectancy (years) 43 52costs due to disruptions in trade routes, oil Adult illiteracy (%) 43 44

price shocks, the influx of refugees from Infant mortality rate (per 000) 133 91Mozambique, and droughts -- that disrupted Child mortality rate (per 000) 225 157

Access to safe water (%) 54 47even this pattern of growth. Since 1981, Primary enrollment (%) 81 75Malawi has been implementing policy reforms, Male 84 82supported by successive adjustment credits, to Female 77 67stabilize and restructure its economy, but with HIV prevalencelittle sustained success. These policy reforms among sexually active adults(%) 13 na

and .Iwomen in urban antenatal 3 1 namainly aimed to stabilize the economy, and care clinics(%)liberalize international trade, investmentlicensing and financial markets, whileneglecting important structural regulatory constraints and entry barriers in product and factormarkets. The results were poor, and the growth rate of GDP during the 1981 -1994 period was2.4% per annum, well below the annual population growth rate of 3 %.

3 Malawi's Gini coefficient of 0.62 makes its income distribution among the worst in the world

2

Box 1: Policy Reforms Undertaken by Government Since 1994

Fiscal, External Sector and Financial Policy Reforms* Implementation of stabilization policies that have brought down fiscal deficits (before grants) from 28 % of

GDP (1994/95) to 8% of GDP (1996/97), before increasing it again to 12% in 1997/98.* Reforms in tariff and surtax policies, that have reduced average weighted statutory tariffs from 19% 1994 to

around 14 % currently. Surtax refonns extended the base and rationalized rates.* In expenditures the share of education and health sectors increased lFrom around 14% of expenditures to 26%

in 1997/98. A medium term expenditure framework was introduced to manage expenditures.* The exchange rate was floated in 1994 and Malawi attained current account convertibility in 1995.* A treasury bill market was successfully launched avoiding inflationary borrowing from the Reserve Bank.* The stock exchange was opened in 1996.* Export processing zone (s) were introduced, while the processing oiF export duty drawbacks was improved to

increase incentives for exporters. There is now a fledgling export oriented manufacturing sector in garmentsand cut flowers.

Civil Service Reforms* The ci-il service structure has undergone significant changes as 20,1300 new teachers were appointed in place

of 20,000 other temporary employees who were laid off.* A Civil Service Reform Action Plan was adopted and is now being implemented. Under this, the common

services cadre was abolished enabling better accountability and management in professional services.- The completion of the first phase of the Functional Reviews of the Government and rationalization of

Government ministries was completed in 1996. Based on that the number of Ministries have been reducedfrom 27 (June 1997) to 19 (March 1998).

Agriculture- Restrictions on smallholder production of tobacco were removed by amending the Special Crops Act* Restrictions on private trading in fertilizer, seeds and burley tobacco were removed.- Subsidies on fertilizer were removed.* The agriculture financing system was revamped by introducing the Malawi Rural Finance Company on a

sound financial basis in place of the Smallholder Agriculture Credit Authority that went bankrupt.

Transport, and Private Sector Development* The Malawi Railways a parastatal, previously a big drain on Government finances, was restructured. A new

company was formed, and will be transferred to private management as a concession by end- 1998.* The minimum freight charges on domestic transport were eliminated (1996), and imports of second hand

transport and equipment were deregulated, leading to more competjition and services.* A Privatization Law was passed (1996) laying the legal foundations and the institutional framework for

privatization. Some 25 companies have been privatized.

Social Sectors* Primary education was made free in 1994. In response, enrollment increased by nearly a million.* Government has also launched a secondary education expansion program to accommodate the rising number

of primary school graduates (1997).* A Social Action Fund (MASAF) is being used to help organize and finance 988 (as of June 1998)

community demanded projects and support public works. The communities play a critical role in designingand funding these projects in building classroom, boreholes, clinics, roads and irrigation.

* A Poverty monitoring system has been launched to measure changes in the welfare of the people throughregular household surveys.

3

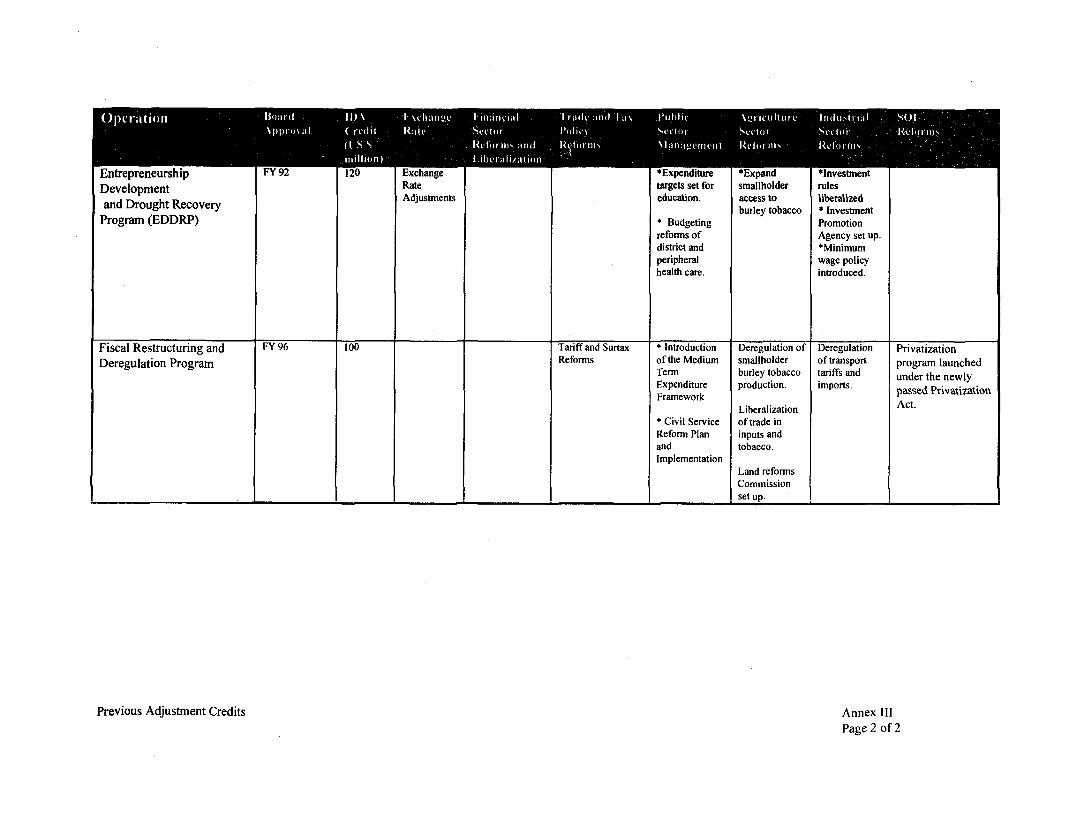

6. Since 1994, however, with the advent of new political leadership, the pace of reformsaccelerated significantly (See Box 1, previous, for details). Supported by IDA adjustment --the Fiscal Restructuring and Deregulation Credit approved in April 1996 -- and investmentcredits, the Government removed restrictions on small-holder production of burley tobacco andother cash crops, liberalized the trading of agriculture outputs and inputs, launched majorprograms of privatization, civil service reforms and expenditure prioritization, implementedsubstantial tariff and surtax reforms, and attained current account convertibility. At the sametime, large investments in education, health and community development took place.

7. The economy responded well to these reforms. Macroeconomic balances werestabilized as fiscal deficits (before grants) were reduced from 28% in 1994/95 and 15% in1995/96 to around 8% in 1996/97, mainly through expenditure adjustments. The averageannual inflation rate4 fell from 83% in 1995 to 9 % in 1997, interest rates declined and theexchange rate, floated in 1994, was stable as foreign exchange reserves rose to more than fourmonths of imports by end 1996. Growth averaged more than 10 % p.a. in the last three year(1995 - 1997), although around a third of this growth was based on recovery from the 1994drought. Equally significant, this recent growth has been more broad based and diversifiedthan anytime in the past, and is being led by the small-holder economy and the service sector.Smallholder production of burley tobacco -- the most valuable cash crop produced by Malawi -- has increased threefold since 1993. This has injected US$ 185 million in earnings in the lasttwo years into the smallholder economy, and generated growth of trading, markets and othersecondary activities in the countryside. A non-traditional exports sector has emerged,exporting garments and cut flowers and has grown by 80% in US Dollar terms between 1995and 1997, albeit starting from a small base.

8. But macroeconomic performance slipped again in the second half of 1997 mainly as aresult of loss in expenditure control. A higher than budgeted wage bill, excessive travelrelated expenditures, and a shortfall in income tax collections resulted in an increase in the1997/98 fiscal deficit to 12 % of GDP, while the primary deficit' -- targeted to be zero -- was4.6% of GDP. At the same time gross official foreign exchange reserves declined to 2.1months of imports of goods and non-factor services at end-1997 and the exchange ratedepreciated by nearly 60% in 1998. This large depreciation reflected the correction of thepreviously misaligned rate, terms of trade losses, depreciation in the currencies of majortrading partners as well as lack of confidence in the private sector on the Government'scommitment to stabilization and reforms.

9. In addition to continuing problems in expenditure management, Malawi's growthprospects confront deep-rooted structural problems, vulnerability to shocks and an overallinhospitable climate for the private sector. This is reflected in low private fixed investmentand gross domestic savings rates which have averaged around 4 % (gross private investmentincluding inventories was more than 3% of GDP) and 1.5% of GDP6 respectively, in the last

4 The change in the average annual CPI index over the previous year's average CPI index.5 Primary deficit is defined as overall deficit less interest payments and foreign financed developmentexpenditure: (All Expenditure - Revenues) - (Interest Payments + Foreign Financed Development Expenditures).6 This refers to only the measured investrnent which probably underestimates investment in smallholderdwellings, the purchase of transport (e.g. the large sale of bicycles in the countryside) and other such activities.

4

two years.' Crowding out by high Government consumption and domestic borrowing (5% ofGDP in 1997/98), a shallow and oligopolistic financial sector, deteriorating infrastructure, thedominance of inter-locking public sector ownership in production, trade and finance, andbureaucratic red tape all deter private investment and savings. Malawi's economy also remainshighly vulnerable to shocks: as in 1998, there were also large income losses between 1992-1994 (cumulatively 10% of GDP) due to deterioration in terms of trade. Poor rainfall in 1997led to a 23 % drop in maize production -- the main staple. Hence a key task clearly is toaccelerate the diversification of the economy to make it less vulnerable to such shocks.

10. As noted, Government launched wide ranging reforms in 1995 and 1996 supported bythe last IDA adjustment credit, the Fiscal Restructuring and Deregulation Program. This newcredit will complement the previous adjustment credit by focusing more on reforns to promoteprivate sector led growth in the non-agriculture sector, through accelerating privatization andinfrastructure development thereby diversifying the economy and making it less vulnerable toshocks. Alongside, public sector management reforms will increase the focus of Governmentfunctions and expenditures on public goods and services, and strengthen expendituremonitoring and control systems.

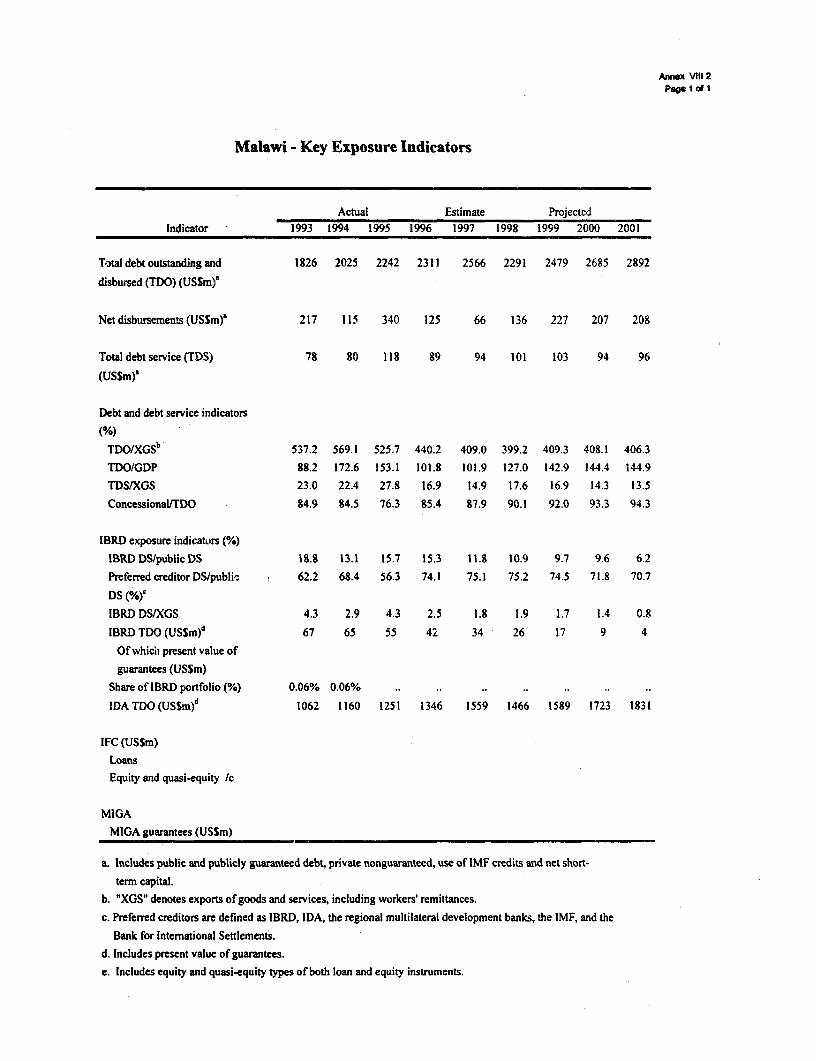

11. This program of policy reforms is also underpinned by a strong stabilization program thatis expected to be supported by the renewal of the IMF ESAkF program. Under this programGDP growth, expected to decline to 4% in 1998, is projected to increase to around 5% in 1999and even higher thereafter as the economy adjusts to exchange rate depreciation and the exportprice shock of 1998. The primary fiscal balance in 1998/99 is expected to improve by around4.5 % points of GDP, compared to 1997/98, even though the budget accommodatesGovernment expenditure for the May 1999 elections, an increase in development expendituresand provision for a temporary subsidy on maize sold from Government stocks as a socialsafety net measure 8. The program includes a large repayment of domestic Government debt(by over 6% of GDP in 1998/99), which will ease pressure on interest rates and the exchangerate, an increase of external reserves to more than 3 months of imports of goods and non factorservices by end of 1998 and to around 4 months by end-1999, and a tight monetary policy --with declining net domestic assets in 1998 -- which still accommodates a real increase of creditto the private sector. Inflation is expected to average around 30% in 1998 and then decline toaround 25% in 1999 as the effects of the 1998 exchange rate depreciation is expected to causehigh inflation in the first half of 1999. The program is also expected to supported through1999 by an increase of external assistance to around US $ 340 million in 1999 both throughlending and grants. Malawi's external debt burden is high vhich makes it a severely indebtedlow income country. However, debt sustainability anal,ysis carried out for the last CAS(August 1998) have confirmed previous findings that M:alawi's external debt position isexpected to improve over the medium term, thereby making it ineligible for the HIPCinitiative. Given Malawi's borderline situation, Malawi's debt position will be continuouslymonitored. The next debt sustainability analysis will be undertaken before end-1998.

7Private total investment has averaged around 8% in the past three years. However, this includes nearly 3% ofinventory changes.' The landed price of maize imports has increased by nearly 100% in 1998/99 mainly because of depreciation.The maize subsidy thus cushions maize buyers by allowing more graduail increase in the price of maize in oneyear.

5

III. The Reform Program

12. The proposed credit supports structural reforms in two main areas: (a) public sectorreforms to improve the quality and management of public expenditures, restructureGovernment functions and the civil service in line with priorities; and (b) private sectordevelopment reforms through privatization and improving infrastructure policies (Box 2, p. 10provides a full list of the policy reforms undertaken under this credit). A complementarypackage of investment operations and technical assistance is designed to help implement thesemeasures and longer term institutional reforms [See Annex I]. These reforms are based onconsultations with stakeholders during the preparation missions and discussions on the August1998 Country Assistance Strategy.

13. The main analytical underpinning of the credit has been provided by the study,"Accelerating Malawi's Growth" (September 1997). This study concluded, inter alia, that awide range of policy reforms was needed to promote high investment and growth ratesincluding (i) good fiscal management, i.e. keeping budget deficits low, avoiding domesticfinancing of deficits, and prioritizing expenditures to ensure adequate funding of key socialsector items; (ii) improving land policies to encourage higher utilization of estate lands throughfacilitating sale and sub-lease arrangements, streamlining land transfer and titlingrequirements; (iii) improving infrastructure services and inviting private sector participation ininfrastructure; and (iv) increasing the supply of industrial land sites and streamliningprocedures for the approval of employment of skilled expatriate workers. The proposedreform program focuses on some of these key recommendations: improving expendituremanagement, accelerating privatization and private sector development, and improvinginfrastructure.

A. Improving Public Sector Efficiency: Expenditure Policy Reforms,Rationalization of Government Functions and Tax Reforms.

14. Improving Public Expenditures: Improving the quality and management of publicexpenditures is among the most important challenges facing Malawi. A significant positiveshift in public expenditures has taken place in favor of the social sectors in Malawi as the shareof education and health increased from 14% of all aggregate expenditures in 1993/94 to aplanned 29% in 1998/99. As a result, the share of Malawi's expenditures in social sectorscompares favorably with many other countries. Hiowever, public expenditures have continuedto be a problem in three respects.

15. First, public expenditures and functions have been thinly spread over too manyactivities. Given existing trends, recurrent expenditures are expected to be 20% less thanrequirements in 2005 even after assuming that non-essential areas are excluded. Criticalexpenditures on public goods (such as road maintenance, which received only 40% of itsrequired expenditure in recent years) and key social sector programs where there are strongexternalities -- such as primary education, and primary health care programs -- have beeninadequately funded. The full implementation of the Government's secondary school

6

expansion program would require that education's share of the recurrent budget rise from 23%at present to nearly 40% in the next three years, if cost recovery is not improved.

16. Second, as there will be probably be a cut in the goods and service budget in real terms inthe 1998/99 fiscal year, compared to 1997/98, it becomes even more important to prioritizeexpenditures.9 Without prioritization, such expenditure cuts can become unsustainable anddamaging. Third, weaknesses in prioritizing the budget have been compounded by poorexpenditure monitoring and control procedures. As a result, actual expenditures deviatedsharply from budgets, as in 1997/98 when travel and travel related expenditures were 50%higher than budgeted in the first nine months of the fiscal year, while expenditures on teachingand learning materials were only 40% of what had been budgeted.

17. Government has used the Medium Term Expenditure Framework (MTEF) -- introducedunder the FRDP credit, to prioritize expenditures in the last three years. First introduced in theplanning for recurrent expenditures only in four ministries in 1996 and then gradually extendedto other Ministries, the MTEF introduced a process of strategic thinking under which key goalsof the Ministries were defined and mapped to programs and sub-programs. The costs of theseprograms were to be estimated and prioritized within the overall resource envelope dependingon their relevance to the objectives. This exercise was to provide the basis for activity basedbudgeting and prioritization of expenditures based on the importance of these activities. Allthese steps represent important advances.

18. However, the MTEF process was undermined in the past by some serious weaknesses inimplementation including: (i) lack of involvement of senior managers -- both Ministers andcivil servants; (ii) lack of clear decisions on inter-sectoral and intra-sectoral allocations basedon explicit choices and trade-offs under which expenditures in non-essential items are reducedsharply or completely cut providing room for more expenditures in priority areas; (iii) lack ofclearly defined and prioritized strategies, programs and outputs of Ministries and the costing ofsuch programs and outputs; (iv) delays in preparing and forecasting the sectoral allocations andindicative ceilings in a timely manner; and (v) failure to effectively integrate the developmentbudget and the programming of aid resources into the MTE,F budget. As a result, the MTEFturned into more of a pro forma accounting exercise than a strategic resource allocation plan.

19. The Government is now addressing these problems. The MTEF has been madecomprehensive and integrated with the budget process. Two rounds of expenditureprioritization for the 1998/99 budget increased allocations of expenditures on current non-wage expenditures for agriculture (by 22% over previows year), health (24%), education(49%), and police services (23%) sectors. The expenditure on road maintenance has beenincreased sharply by over 100% and is expected to meet around 75% of road maintenancerequirements. At the sub-sectoral level, allocations have been increased or maintained in realterms for high priority items such as provision of teaching and learning materials in primaryand secondary education, drugs, preventive medicine progrems, water and sanitation, and roadmaintenance; [Annex II. 1 of Letter of Development Policy (LDP) shows details of expenditure

This large cut arises from the need to accommodate expenditures on the national and local Governmentelections that will take place in May 1999, and an increase in the wage bill of more than 20%.

7

prioritization]. At the same time, non-essential public expenditures in all other sectors, andespecially in foreign affairs, works,. office of the Vice President, and other administrativedepartments have been reduced or eliminated. In addition, the Government has introducedclear procedures that engage both the Cabinet and senior civil servants in preparing the1999/2000 MTEF through prioritizing programs, costing them and allocating resources in linewith priorities and within indicative ceilings that are provided early, and integratingdevelopment and recurrent budgets in a consistent manner [See Annex 11.3 of LDP for detailsof the medium term expenditure framework implementation plan].

20. Alongside expenditure prioritization, new expenditure monitoring and controlprocedures have been introduced to ensure that actual expenditures are allocated as budgetedunless explicitly sanctioned by approved virement procedures [See Annex II.2 of Letter ofDevelopment Policy for details of new expenditure monitoring and control procedures].Under the new system, monthly expenditure data from Ministries, especially on core programsand major areas of deviation, are received and distributed to the Special Cabinet Committee onthe budget and the Finance and Audit Committee of Principal Secretaries by the 25th of thefollowing month to identify, correct or approve deviations (if expenditures are more than 10%above or 25% below pro-rated budgeted levels). There has also been agreement on reportingarrangements between the Government and the World Bank on key targets. In the area ofexpenditure controls, Government has issued clear instructions to enforce virement rules andpunitive measures against violators. Alongside, a circular has also been issued notifying thatall Government procurement will be done on a cash basis. Lastly, and most significantly, theSpecial Cabinet Committee on the Budget has been made responsible for reviewing allrequests for extra-budgetary expenditures -- the source of most expenditure overruns in the lastyear -- and approving them only after financing from expenditure cuts elsewhere or additionalresources have been explicitly identified.

21. Rationalizing Government Functions: Rationalizing government and civil servicefunctions in line with the new more focused definition of the role of the Government is anotherkey area in need of reform, and one directly related to expenditure prioritization andgovernment efficiency. The problem in Malawi is not so much with the size of the civilservice, but more with the breadth of its functions and its composition. There are 120,000civil servants in Malawi (population: 10.6 million) of which some 55,000 are teachers, healthworkers and police personnel. However, lack of focus in Government functions results inunderstaffing in priority areas (e.g. nurses, teachers and police), but overstaffing and wagecompression in general. Lack of clear job descriptions and accountability, inadequate linkagebetween performance and career path, inadequate salary levels and a compressed salarystructure, and the lack of adequate training of the civil service all lead to deterioratingefficiency and morale.

22. The Government has been undertaking civil service reforms since 1995, under whichthe composition of the civil service has changed significantly as 20,000 temporary employeesand industrial class workers were retrenched and replaced by school teachers. Under thepreceding adjustment program, the FRDP I, the Government prepared a Civil Service ReformAction Plan that is now being implemented. Accountability of civil servants has beenincreased by eliminating the common service cadre, and establishing clearer, specialized career

8

paths within Ministries. Some 3,300 civil servants have been discharged in the past two yearsas a part of the rationalization of the civil servants. A civil service salary and a job evaluationstudy is to be completed by December 1998 to prepare for clearer job definitions and civilservice salary reforms and wage decompression. The number of Ministries has beenconsolidated from 27 to 19, though without significantly adjiusting the size or composition ofthe civil service. Consequently, the effectiveness of this reduction has been limited.

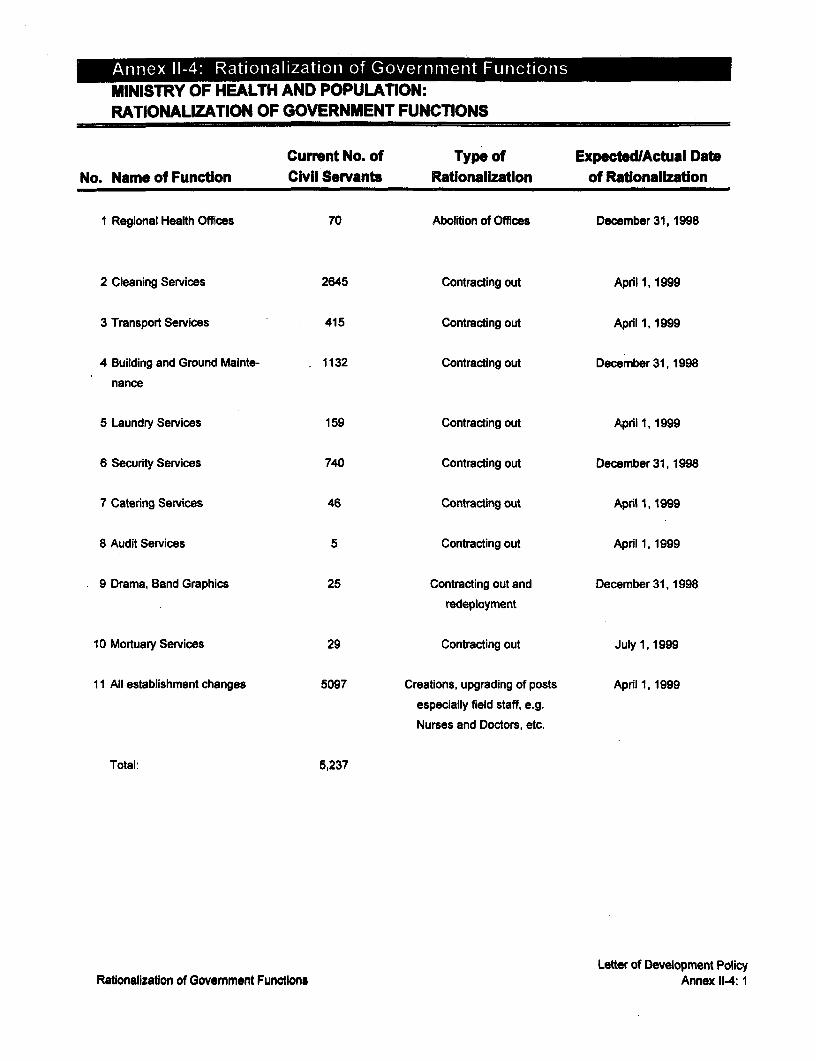

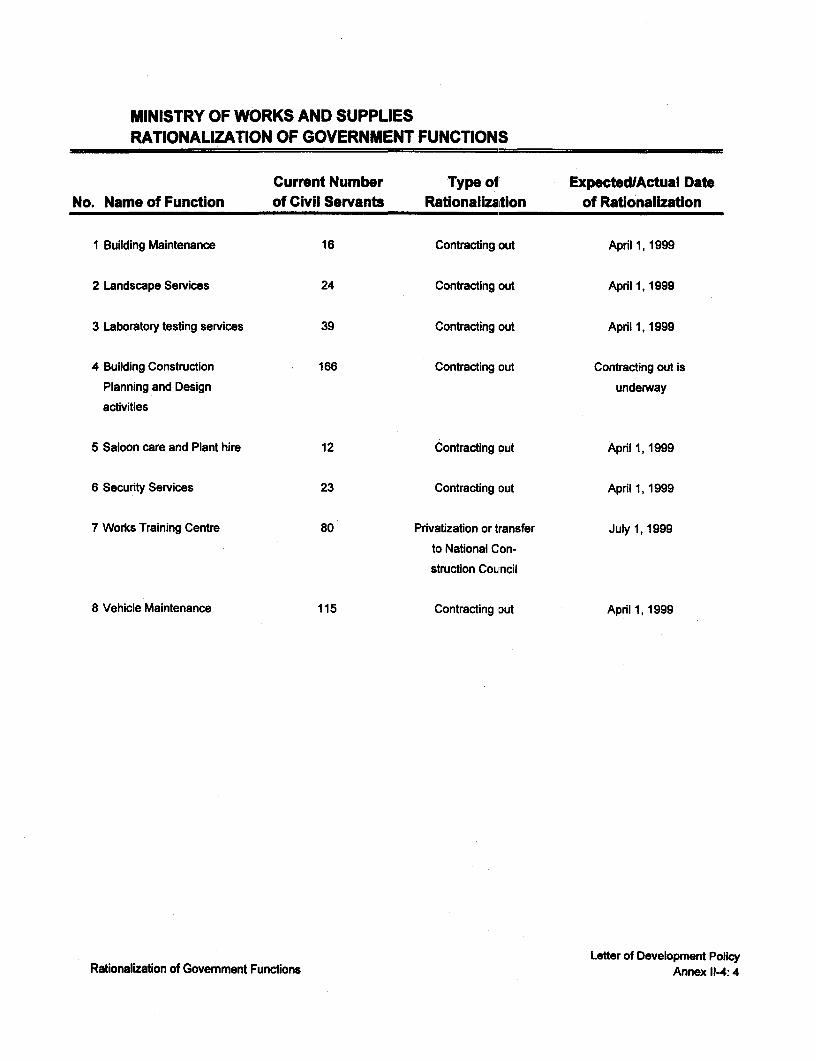

23. Government is now undertaking a program of eliminating, privatizing and outsourcingfunctions, agencies and departments. Progress in this area has been held up by delays incompleting detailed functional reviews of Ministries (a condition of rationalizing fourGovernment services was waived before disbursing the second tranche of the previousadjustment credit). But now, based on recommendations from the detailed functional reviewsof five major ministries and the overall strategic review of all ministries undertaken in1996/97, the Government has taken the decision to eliminate, outsource or privatize 47functions [See Annex 11.4 of Letter of Development Policy] in five major ministries that nowemploy more than 60% of the civil service. The rationalization of 30 of these functions isexpected to be carried out by end-March 1999. The civil service composition and deploymentwill also change through a program for the separation and recruitment of civil servants in linewith priority functions. The budget includes provisions for separation benefits.

24. Tax Policy Reforms: Government has continued tariff and surtax policy reforms toincrease efficiency of the tax system while protecting revenues. Tax policy -- especially hightaxes on raw materials, intermediate and capital goods comb:ined with low taxes on final goodsfrom COMESA countries and other countries with which Malawi has bilateral agreements -- isroutinely cited by the private sector as among its top constraints. There has been steadyprogress in this area as average weighted tariffs have decreased from 19% to 14% while surtax(which credits taxes paid on inputs, like a VAT) rates halve been rationalized and the baseextended. In April 1998 the Government eliminated all taxes on exports which it firstintroduced in 1994 as a temporary fiscal measure.

25. In the 1998/99 budget, the maximum tariff rate on consumer goods was reduced from35% to 30%, while those on selected intermediate goods, raw materials and capital goods wasreduced from 10% to 5 %. Combined with the removal of the export taxes, this tariff reductionamounts to major gains in promoting Malawi's internationa]b trade. The revenue shortfall willbe partly offset by another extension of the base of the surtax that presently covers onlymanufacturing and imports. The planned introduction of a well staffed, properly funded andmotivated Malawi Revenue Authority is also expected to, improve revenue collection andefficiency of the tax system.

B. Supporting Growth through Private Sector Development

26. The 1997 study, "Accelerating Malawi's Growth" concluded that raising private fixedinvestment would be a decisive condition for increasing GDP growth rates to the targeted 5-6% range. Second, it also concluded, that while agriculture (:35% of GDP) would be the main

9

Box 2: Policy Reforms Supported by FRDP IIImplemented Before Board (December 1998, US$ 60 million equivalent)

A. Fiscal Restructuring and Public Sector Management* Established expenditure level targets (specified in amounts and shares of expenditures that have been increased) on

key sub-sectoral items in education, health, roads and agriculture sectors in the 1998/99 budget. Identifiedexpenditure cuts to finance expenditures on priority sectors.

* Introduced agreed system to monitor (wage, and current expenditure targets on a monthly basis) and controlexpenditures, including monitoring of priority expenditures by IDA.

* Established agreed procedures and timetable for expenditure prioritization under the MTEF in 1999.* Started implementing policy to eliminate, outsource and privatize 47 specifically identified functions (30 by end

March 1999) activities, and agencies in the 5 major Ministries, and re-deploy civil service based on the detailedfunctional reviews.

* Reduced tariffs on final goods from 35% to 30%, on selected intermediate goods, raw materials and capital goodsfrom 10% to 5%. Changed all zero rated surtaxes (except on exports) to exempt (in the case of unprocessedagriculture sector goods, and merit goods) or to 20%.

B. Privatization and Deregulation* Approved and publicized a National Communications Policy statement. This policy, among other things, specifies

the Govemment's intention to offer a stake in Malawi Telecoms to a strategic partner, through an internationalcompetitive tender; licensed a second cellular operator introducing competition.

* Published the bill laying the proposed legal framework for implementing the approved communication policy, inparticular, to create a separate telecommunications regulatory body, to split posts and telecommunications intoseparate legal entities, and to facilitate further liberalization and private participation in the sector.

* Approved a detailed time-bound program, and implementation plan, to bring to point of sale a list of assets (the"divestiture sequence list") including banks, held by MDC, ADMARC, ADMARC Investment Holdings andimplementation of the communications policy, in particular finding a strategic partner for Malawi telecoms;

* Enacted Electricity Act that establishes independent regulatory body, invites private sector entry into the sector,licenses all electricity producers (including ESCOM) and distributors; corporatized ESCOM under the CompaniesAct.

* Initiated debt restructuring and adjusted tariffs to make ESCOM viable; started reorganization of ESCOM.* Gazetted a clear temporary employment permit (TEP) policy for expatriates such that all TEP applications are

responded to within 40 working days.* Announced policies to widen the maize price band for 1998/99 and reforms of maize marketing arrangement.

Before Second Tranche (April 1999, $ 30 million equivalent)

A. Fiscal Restructuring and Public Sector Management* Implement agreements of the first tranche on meeting agreed public expenditure targets in the first two quarters of

the 1998/1999 fiscal year, on public expenditure monitoring and control procedures, and preparing the MTEF.* Implement the rationalization of 30 Government functions as per agreed timetable.

B. Privatization and Deregulation* Implement agreed action plan for bringing to the point of sale government's interests in at least 15 enterprises.* Prepare privatization/commercialization program for ADMARC.* Implement agreed plan to reform telecommunications sector, as per first tranche (i.e. enact communications law,

appoint investment bankers/consultants to secure strategic partner for Malawi Telecoms).* Review Electricity law, in line with agreement with IDA, to establish clear procedures for licensing, tariff rate

adjustment mechanisms that provides adequate incentives to private investors and establishes autonomy ofelectricity council from the Government.

* Finish review of financial sector regulatory framework to identify reforms to strengthen and unify regulatoryframework, restructure and privatize the financial sector, and issue guidelines for the privatization of the two maincommercial banks - on the basis of the study agreed to in the first tranche.

10

source of growth in the near term, growth would have to be driven by manufacturing and othernon-agricultural activities in the medium term and beyond.

27. Achieving these objectives will be a significant challenge, as private sectorperformance, especially in the industrial sector, has been weak, and measured private sectorfixed investment has been virtually stagnant since 1992 due lo several factors, as noted earlier:(i) the continued macroeconomic instability of the last few years that has crowded out privateinvestment, created price and exchange rate instability and generally signaled an unstableeconomic management; (ii) the continued presence and dominance of public or semi-publicparastatals that control most of the economy through their size, inter-locking ownership inproduction, trade and financial sectors; (iii) inadequate and deteriorating public sectorinfrastructure, especially in telecommurnlcations and power; (iv) regulatory obstacles to thesupply of key factors of production such as skilled labor and serviced industrial land sites;(v)the inefficient utilization of land in estates and inadequate land husbandry due to inequitableand unclear landholding rights, and (vi) interventions in the maize markets through large scalepublic sales at below market prices, taxing producers and maize traders.

28. The reform program supported by this credit addresses some of these areas through: (i)reducing fiscal deficits and eliminating domestic deficit financing, such that it can "crowd in"the private sector; (ii) implementing a privatization program including the shares of majorcommercial banks; (iii) preparing reforms in the financial sector regulatory framework that canmeet the needs of a more diversified and privatized financial sector; (iv) improvinginfrastructure services through commercializing and corporatizing operations and invitingprivate sector investment; and (v) promoting agricultural production and trade through a moreliberalized maize pricing policy. Problems on the supply of industrial land sites and landreforms will be addressed separately by the proposed private sector development project andreforms currently being prepared by the Presidential Commission on Land Reforms.

29. Privatization: Private sector development in Malawi has been constrained in thegeneration of new markets, capital, technology, and management partly because of thedominance of parastatal companies. While public sector parastatals account for around 20%of GDP, their influence is greater because of the oligopolistic nature of the formal sector inMalawi and the integration of these firms in inter-lockiing ownership of other firms inmanufacturing, agriculture, trade, transport and finance. At present, some 100 wholly orpartly public sector owned banks, transport companies, utilities and industries (in grainprocessing, textiles, chemicals, tobacco, tea, leather, building, and packaging) maintain adominating presence in non-agriculture economic activity in Malawi. In the case of thefinancial sector, Government owns around 70% of all assets, directly or indirectly through itsownership of public holding companies such as ADMARC Holdings and MalawiDevelopment Corporation (MDC). Interlocking ownership structures have resulted in the twodominant commercial banks, the National Bank and the Commercial Bank, which account formore than 90% of all banking sector assets, being controlled by Government, ADMARC, theMDC and the quasi-private PRESS corporation. Predictably, the level of efficiency of thefinancial sector -- measured by interest rate spreads and the limited range of financialinstruments -- is relatively low, while profit margins are high.

II

30. In 1996, the Government embarked upon an ambitious privatization program, executedby a Privatization Commission, but with modest success so far. Some 25 companies havebeen partially or fully privatized in the last two years. Nevertheless, compared to some othercountries in the region -- such as Ghana, Uganda, and Mozambique -- the pace of privatizationhas been slow and halting. While the Privatization Act has laid a clear legal basis, there isneed to accelerate the implementation of the privatization program. Moreover, until recently,the utilities, agriculture and financial sectors activities have been excluded. In the case of thefinancial sector, privatization is further complicated by the need to review and reform, asrequired, the regulatory framework in order to ensure that prudential standards meet the needsof the changing landscape where four new private banks have entered and the two main banksare being wholly privatized.

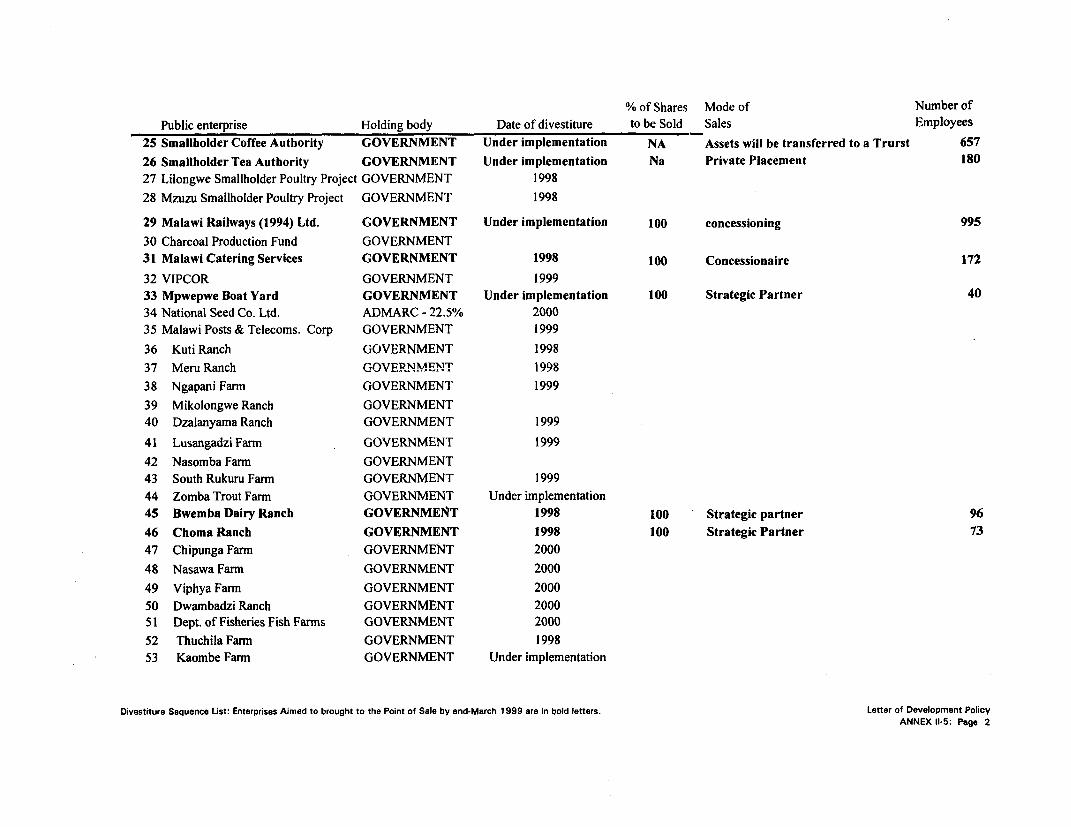

31. Under the FRDP II program the Government has accelerated the pace of privatizationby approving (in August 1998) and starting to implement a privatization plan, the "DivestitureSequence List" of assets, held by Government directly and indirectly through MDC andADMARC HoIdings'°(See Annex 11.4 of LDP for the list of firms and the timetable forprivatization). Under this plan, another 15 to 20 firms (including the concessioning of MalawiRailways, the sale of shares of Banks) will be offered for sale between October 1998 andMarch 1999. In the financial sector the Government has sold 12 % of the total shares in theCommercial Bank of Malawi (CBM) through the stock exchange and is expected to sellanother 14% of public sector shares in the National Bank of Malawi through the stockexchange before March 1998. Government subsequently plans to offer for sale all remainingpublic shares (24% in the Commercial Bank and 40% in the National Bank) in both banks tostrategic partners or through the stock exchange. The specific guidelines for privatizing theseremaining shares will be finalized by March 1999. Government will also complete a study byMarch 1999 on the financial sector regulatory framework to undertake needed reforms. Theaim will be to issue, by June 1999, regulatory reforms that meet the needs of the new postprivatized financial sector where four private banks and the further privatization of the twomain commercial banks will have brought new demands on the regulatory framework.

32. Infrastructure Policy Reforms: A survey of the private sector, conducted for the 1997World Development Report, identified the deterioration of Malawi's infrastructure to be theprincipal constraint to private business. There is one telephone line for every 300 people, onepay phone for every 22,000, virtually no service in the rural areas, and the waiting time for atelephone connection can be as long as ten years. The sector is dominated by the Governmentowned Malawi Posts and Telecommunications Corporation (MPTC), which acts as regulatorand sole provider of basic voice telephony services. It suffers chronic operational and financialproblems. It relies entirely on public sources of financing, and has little commercialautonomy. These poor telecommunication indicators severely undercut Malawi'scompetitiveness in today's global economy. In the power sector, the main supplier, ESCOMhas had difficulties in providing reliable power services resulting in large losses to industryand the economy. ESCOM has faced serious financial difficulties, making it difficult for it tomeet its maintenance needs, invest in new capacity, and service its debts.

'° ADMARC Holdings is a subsidiary of ADMARC which focuses on activities in the agriculture sector.

12

33. Resolving financial and institutional problems such as the presence of a large foreignexchange denominated debt (in the case of ESCOM), and the lack of managerial and pricingautonomy that results in weak commercial orientation requires fundamental restructuring ofthese utilities. At the same time, the interest of foreign capital to invest in utilities indeveloping countries also presents an opportunity to increase investment and productivity,while freeing valuable public resources for other important public goods. However, enablingthis to happen will require clear Government policy and legislation to commercialize and, asappropriate, privatize whole or parts of these utilities, and allow private sector entry andcompetition in these sectors.

34. To achieve this in the telecommunications sector, the Government has approved aCommunications policy which provides for opening up all non-basic telecommunicationsservices (mobile, data, internet, paging) to new private service providers; the splitting of postsand telecommunications into separate businesses; securing an established internationaltelecommunications operator as a strategic partner for Malawi Telecom through aninternational competitive tender; improving access to conmmunications in the rural areas,through a combination of Malawi Telecom's service obligations once the strategic partner hasbeen' secured, licensing small local operators, more effective use of the postal infrastructure,increased deployment of pay phones, and other mechanisnms yet to be developed; and thecreation of an independent regulatory body. A bill has been published, and expected to beapproved by March 1999, that will lay out the legal framework for the implementation of theapproved policy. Simultaneously the Government will use the proposed PrivatizationTechnical Assistance Project to assist the Government in implementing these policies.

35. In the power sector the Electricity Act has been enacted, establishing an independentregulatory body (the Electricity Council) that will license alil electricity producers (includingESCOM) on equal terms. In the next stage of reforms Government will review the electricitylaw by end-March 1998 further clarifying licensing and tariff' setting procedures to increase thetransparency of licensing and tariff setting rules so that they give investors necessaryincentives and assurance. These revisions will also establish the autonomy of the ElectricityCouncil. The Government has taken steps to corporatize and commercialize ESCOM (nowcalled the Electricity Supply Corporation instead of the Electricity Supply Commission) byincorporating it under the Companies Act to establish commercial and managerial autonomy.The Government has also initiated financial restructuring of' ESCOM by converting a sectionof ESCOM's debt to Government to equity, adjusting ESCOM's tariffs (by 35% in July 1,1998) and another 35% (due in November 1, 1998) all of which will enable ESCOM to makeits financial position viable. ESCOM is also implementing an organizational restructuringunder which seven distinct cost centers have been set up to cover generation, transmission anddistribution.

36. Agriculture Markets and Storage: At present ADMARC is dominant in most ofmarketing and storage capacity in agriculture. It operates 344 markets and depots, and has astorage capacity of 468,000 tons, much of which is currently unutilized. In the 1996/97season, the agency used only 132,000 tons of space, of which 54,000 tons of space was rented

13

out. In addition, ADMARC's crop operations include profitable activities such as tobacco andcotton, which can provide a good base for private sector ownership. Historically, ADMARChas used its profits from these activities to support its development-oriented role. However,the significance of this latter role has lessened sharply over recent years; in the last yearADMARC acted mainly as a channel for Government's maize procurement, imports and saleswhere the costs were borne by the budget. At the same time as ADMARC's development roleis becoming ambiguous, its dominance in marketing and storage, deters the growth ofcompetitive, private trading.

37. To address these issues Government is now preparing a program by March 1999 for theprivatization and commercialization of ADMARC that will clearly identify ADMARC's assets-- markets, depots and marketing activities, such as tobacco, cotton and fertilizer -- forprivatization and their recommended mode of privatization. This program will seek toidentify 20 to 30 markets that are profitable and which could be immediately offered forprivatization through the privatization commission. The program will also recommendmodalities for privatizing and commercializing the rest of ADMARC in a time bound planwhile giving consideration to Government's objectives of using ADMARC, with necessarybudgetary subventions, to serve outlying markets and vulnerable areas.

38. Maize Price and Marketing Reforms: Government will continue the process ofgradually reducing its interventions in the maize market. It currently intervenes in the maizemarket through the wholesaling operations of the Strategic Grain Reserve (SGR), sales throughADMARC and by implementing a maize price band. The principle is that maize fromGovernment stocks and imports will be sold at the ceiling price of the band to containexcessive increases in consumer prices and purchased at the lower price band to supportproducer prices. In practice maize market interventions in the past year have suffered from thelow ceiling price of the band that discourages the supply of maize, as it deters imports byprivate traders and taxes producers. Partly as a result of these adverse incentives, lowersupplies of maize resulted in very high open market prices at the end of the season. TheGovernment has addressed this problem in two ways by increasing the selling price ofGovernment maize from MK3.95 per kg. to MK 6.50 per kg. for sale of small quantities inrural areas and to MK. 8.50 for sale in larger quantities in urban areas. While it is clear that theMK 6.50 price is below import parity price, the Bank has supported this subsidized price as atransitional social safety net measure to cushion the shock of the doubling of the landed costprice of this basic staple. For the next season, 1999/00 the Government has decided to replacethe SGR with the National Food Reserve Agency and to make it the principal instrument formaize market interventions that will take place on clearly established price based rules insteadof discretionary practice. The trigger prices for intervention will be the floor and ceiling pricesof the band which will be based on the export parity price and the import parity pricesrespectively, and which will be adjusted periodically.

39. Facilitating Temporary Employment Permits. Difficulties and uncertainties inemploying skilled expatriate labor are another major constraint to private sector activity inMalawi, where the secondary school enrollment ratio is only 1 1%, and expertise andexperience are scarce. Obtaining employment permits (called temporary employment permits

14

or TEPs) for skilled expatriate workers in Malawi has taken as long as two years and can act asa critical constraint for private sector activity, especially foreign investment. The difficultiesin obtaining TEPs are evident in that as of late 1996 there were only 54 TEPs issued to firms inthe manufacturing sector.

40. To address this constraint Government has undertaken the following measures tosimplify and liberalize the TEP approval process: (i) gazetting a clear, well publicized liberalTEP policy; (ii) making the approval of the "key posts" automatic through a separateapplication process; (iii) making the number of "key posts" to be determined not only by themagnitude of the investment but also by its level of exports; (iv) allowing existing companies,both Malawian and foreign owned, to have the same rights to, acquire TEPs as new firms; (v)restoring the rights of Permanent Residence Permit (PRP) holders to work in Malawi; and (vi)making the approval process time-bound such that all TEP applicants are responded to within40 working days of application. Government has also introduced a monthly monitoringsystem to enforce the implementation of this newly liberalizecl policy.

IV. Impact of Reforms

41. The reform program, supported by this credit, should lead to an accelerated reductionin poverty in two ways: (i) helping to create conditions -- macroeconomic stabilization,infrastructure improvements and privatization -- for a broad based GDP growth of between 5% - 6 % p.a. in the 1999 - 2001 period; this high case scenario should, ceteris paribus, lead to adecline in the poverty head count ratio from roughly 43% to 38% of the population in the nextfive years; (ii) by improving the targeting of public expenditures and Government servicestowards the poor. A GDP growth target of between 5 % to 6 % represents a pragmaticmedium term target in that it reduces the number of poor living in poverty, and also representsan attainable and reasonably ambitious target, in the light of recent experience. An overviewof the design of the credit and its expected impact is presented in the flow chart in Box 3 in thenext page. However attaining such a target will depend on the continuation of normalweather. Furthermore, given increasing prospects of slowdown of the global economy and itsdeleterious effects on demand for Malawi's exports, it is possible that actual growth rates inthe medium term will be lower than targeted. Nevertheless lthe reform program supported bythis credit will lay the foundations for sustained, higher rates of growth and poverty reductionin the longer term.

42. The key question is, of course, how can the Governmeint create the environment for thenecessary rate of private investment to support such a growth performance ? Here again pastexperience shows that proper fiscal management -- running low fiscal deficits and avoidingdomestic financing of deficits -- will be critical, along with a functional public sector that canenforce law, security and contracts, provide priorities such as proper maintenance ofinfrastructure and investments in human capital. A private fixed investment rate of more 7%of GDP, one that could support the targeted growth rate, was attained between 1988 and 1991.In addition to providing the macroeconomic stabilization policies to reattain this investmentrate, the reform program supported by this credit will also help to attain this target byproviding a more hospitable and competitive climate for the private sector to operate throughimproving infrastructure services (which itself will lead to increase in investment rates),

15

BOX 3: OVERVIEW OF POLICY REFORMS UNDER THE SECOND FISCAL RESTRUCTURING ANDDEREGULATION PROGRAM: INSTRUMENTS AND TARGETS

PoliCY Instmments Intermediate Tareets Outcome Tarsets

Private Sector Development* PrivatizinglOOparastatals(15-20,byMarch 1999) l privaeF1 xCd

h/Investment Rtsfo\/Broad based * Financial sector regulatory reform and privatization 4% of GDP (1997) to 7% GDP Growth of

* Liberalizing employment of skilled expatriates improving efficiency of a to 6% p.a\1~~~~~~~~~ investment/\/

Improving Ifmstnwcture Efficienc>* Reforming regulatory framework to promote private sector

entry into power and telecom sectors

* Commercializing power and telecommunications utilities

* Securing a strategic partner for Malawi telecoms Macroeconomic

t / / ~~~~~~~~~~~ ~ ~ ~ ~ ~~Stabilization Reuto .o. f* Low inflation and Reducton of

interest rates in second poverty ratesFical Restruduring halfof 1999 from 43% of* Maintaining primary fiscal balance * Stability in real population to at

effective exchange rate least 38% in 5. Reducing domestic financing of deficits and retiring \ Increase in real credit /ars.

domestic debt flows to the puivate /\sector/

* ImFroving budgeting, monitoring and control of\/expenditures, and financial control over pars-statals

Implement na the Medium Tenn Expenditure Greaterefficiency in ImprovedFramework and Functional Rationalization public spending and distribution of. Costing and prioritizing sector programs and outputs services: more public goods

expenditure goods and pbi od* Preparing three year expenditure frameworks services for priorities and and services

\ the poor(SeeAnnex Il- and income* Auditing, evaluatimg and integrating the Development \ .fordetails)

Budget with the recurrent budget and sector programs

16

creating opportunities for the private sector through privati2ation, and finally by facilitatingavailability of skilled expatriate labor.

43. The program supported by this credit will also support poverty reduction by making thepattern of growth more broad based and equitable. In the short run growth will continue to bedriven by the smillholder sector (which now produces burley tobacco and thereby enjoys thebenefits of exchange rate adjustments),. the growth of small scale trading and services in therural economy and creating more scope for the private sector through the plannedprivatization of government trading and cropping activities. These measures will benefit thesmallholder sector and improve income distribution as indicaled by the evidence from the pastfew years. Containing inflation will help to maintain food security of the bottom one-third ofsmallholders who are net buyers of maize. Lastly, improvements in the business climate alongwith trade reforms should encourage the private sectcor to develop labor intensivemanufacturing, strengthening the recent trend of garments and other exports. The share oflaborin income should increase from this development. Directing public expenditures to goods andservices that benefit the poor -- teaching and learning mateaials in primary schools, a moreexpanded secondary education program that is less costly and elitist but includes greaternumbers of primary school leavers, preventive medicine, and immunization should also lead toa more equitable distribution of income. Lastly Government programs will help the poor byexpanding targeted poverty and food security programs such as the starter packs program of1998/99, that will distribute 0.3% of GDP in input packages to smallholder households. Theresult of all this will be to lead to a faster reduction in poverty, than could be achieved throughan increase of incomes alone.

V. Design of Credits, Disbursement Procedures and Implementation Arrangements

44. The FRDP II credit has been designed to focus on two main critical areas: publicexpenditure and civil service reforms and reforms to generate private sector development. Thecredit will be disbursed in two tranches of $ 60 million in (December 1998) and $ 30 million(April 1999). The first tranche (see Box 2 in page 10) supports the implementation of publicexpenditure management reforms and civil service reforms, wrhile at the same time it initiatesprivate sector and infrastructure reforms through key policy decisions. The second tranchewill follow implementation of policies in public expendilture management, civil servicereforms and private sector development reforms against specified benchmarks. This designwas adopted after consideration of an alternative: simultaneously processing two adjustmentcredits, one focusing on public sector and expenditure management and the other on privatesector development issues. However, processing two operations simultaneously would haveover-stretched capacity in a year when the Government was engaged in restoringmacroeconomic stability and responding to a large terms of trade shock. At the same time,leaving out any one part of the reform agenda, expenditure management or the private sectordevelopment reform, would have significantly undermined the beneficial impact of theprogram.

45. The FRDP II Technical Assistance Project has been designed to provide necessarytechnical support, training and equipment to meet three olbjectives: (i) implement policy

17

reforms, including the medium term expenditure framework, auditing and reviewing thedevelopment budget, reforming expenditure control procedures and systems, andimplementing civil service reforms; (ii) evaluate the impact of structural reforms on Malawi'seconomy, in particular by examining the effects of liberalizing trade and exchange rate policyon manufacturing, and liberalizing agriculture production and trade on the agriculture sector;and (iii) develop the agenda for the next round of macroeconomic and sectoral policy reformsthrough research into further constraints to growth.

46. Lessons from OED and Review of High Impact Adjustment Lending (HIAL): Thecredit's design draws on important lessons from OED's Performance Audit Report on the lastcompleted adjustment credit (the Entrepreneurship Development and Drought RecoveryProgram closed in 1997) and its recent Country Assistance Note. These lessons include: (i)stabilization without structural adjustment is unlikely to be sustained; (ii) coordinated andsustained implementation of a broad range of policy interventions is a prerequisite to a relevantinvestment response; (iii) deficiencies in the financial sector, competitive environment, andprovision of infrastructure and services can forestall investment response; (iv) protection ofsocial expenditures and ensuring quality of expenditures is critical; and (v) using relevantmonitorable indicators is important for ensuring progress and success. The credit also drawson recommendations from the review of high impact adjustment lending and other OEDreports " in (i) being grounded in a multi-sector economic work, "Accelerating Malawi'sGrowth, and other sector work; (ii) obtaining Government commitment and ownership (seeparas. 50-51 below); (iii) arranging for broad consultations with civil society; and (iv) beingwell embedded in the country assistance strategy and supported by complementary credits inthe areas of infrastructure investment and private sector development.

47. Relationship with the Country Assistance Strategy and Supporting Credits: Theobjectives of this operation are the central objectives of IDA's Country Assistance Strategy.The policy reforms supported by this credit are supported by several ongoing and plannedBank investment and technical assistance credits. Expenditure prioritization and therationalization of Government functions are supported by technical assistance provided underthe Institutional Development II credit, and sector work under projects such as SecondaryEducation, Population Health and Nutrition, Agricultural Services, and the proposed RoadsRehabilitation Project. Tax policy reforms are being supported by assistance provided by IDA,IMF and the U.K. Privatization and private sector development are being supported byinvestment and technical assistance under an IDF grant for privatization, and by a plannedPrivatization Technical Assistance Project, and a proposed Private Sector Development projectcurrently under preparation. An IDF grant and the Environmental Support Project aresupporting land policy reforms. In addition the Malawi Social Action Fund credit, whichincludes a public works program, will serve as a safety net for people adversely affected bymarket liberalization -- such as through fertilizer and food price increases.

"World Bank Structural and Sectoral Adjustment Operations, The Second OED Overview, 1992.

I8

48. Disbursement Procedures and Implementation Arrangements: The FRDP IICredit will follow the Bank's new simplified disbursement procedures for structuraladjustment credits. Under the revised procedures the Credit will be disbursed againstsatisfactory implementation of the adjustment program and not tied to any specific purchasesand no procur,ment requirements will be needed. Once the Credit is approved by the Board,and becomes effective the proceeds of the first tranche (and in due course, the second tranche)will be deposited by IDA in an account at the Reserve Bank of Malawi at the request of theBorrower. If, after deposit in this account, the proceeds of the Credit are used for ineligiblepurposes as defined in the Development Credit Agreement, IDA will require the Borrower toeither: (a) return the amount to the account for use for eligible purposes; or (b) refund theamount directly to IDA. The administration of this Credit will be the responsibility of theMinistry of Finance. Although an audit of the deposit account will not be required, the Bankreserves the right to require audits at any time. The disbursement procedures under the SecondFRDP Technical Assistance Project are described in detail in Annex X.

49. Implementation of the policy and actions under the program will be monitored by theCabinet Committee on the Economy, supported by an inter-ministerial committee of officialscoordinated by the Ministry of Finance. The impact of this program in implementation will bemonitored by tracking the indicators mentioned in Annex I (Policy and Processing Matrix).

VI. Benefits, Risks and Government Ownership