world bank documentdocuments.worldbank.org/curated/en/250741468253823… · · 2016-07-14dyoll...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

PROJECT COMPLETION REPORT

JAMAICA

INDUSTRIAL CREDIT PROJECT

(LOAN 2294-JM)

T r a d e , F i n a n c e , I n d u s t r y a n d Energy O p e r a t i o n s Country Department I11 L a t i n America The C a r i b b e a n R e g i o n a l O f f i c e

I This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FISCAL YEAR

National Development Bank of Jamaica Ltd. (NDB)-NDB's financial year covered October 1 through September 30 until 1987 when it was changed to April 1 through March 3 1.

CURRENCY EOUIVALEm

Currency Unit = Jamaican Dollar (J$) Exchange rates used for conversion of J$ values in this report are:

US$l = J$3.00 for 1983; J$5.50 for 1985-87 and FY88-89; J$6.50 for FY90; and J$8.50 for FY91.

GLOSSARY OF ABBREVIATIONS

AFIs - BNS - CDB - CIBC - CNB - m - DFC - DFI - DMB - EIB - ERR - EMB - IDB - IRR - IFMB - JCB - JDB - MSB - NCB - NDB - PCR - PIC - SIFCO WSL -

Approved Financial Intermediaries Bank of Nova Scotia Caribbean Development Bank cmc ~ a m a i ~ a ~ t d . Century National Bank Citibank Development Finance Company Development Financial Institution Dyoll Merchant Bank European Investment Bank Economic Rate of Return Eagle Merchant Bank Inter-American Development Bank Internal Rate of Return Investment & Finance Merchant Bank Jamaica Citizens Bank Jamaica Development Bank Mutual Security Bank National Commercial Bank National Development Bank Project Completion Report Premier Investment Corp. Small Industries Finance Co. Workers Savings & Loan Bank

FOR OFFICIAL USE ONLY THE WORLD BANK

Washington, D.C. 20433 U.S.A.

Office of Director-General Operations Evaluation

June 30, 1993

MEMORANDUM T O THE EXECUTIVE DIRECTORS AND THE PRESIDENT

S U B J E m Project Completion Report on Jamaica - Industrial Credit Project (Loan 2294-JM)

Attached is the Project Completion Report on Jamaica - Industrial Credit Project (Loan 2294-JM) prepared by the Latin America and the Caribbean Regional Office. The Government's contribution (Part 11) closely mirrors the conclusions of Parts I and 111. The report provides excellent coverage of the project's success but it is weak on how and why the project succeeded in a poor, unstable macroeconomic environment.

The Project Completion Report (PCR) suggests that the project has a significant institutional impact and was successful and sustainable. The objectives were to: (a) assist in developing NDB as a strong conduit for credit for financing private investment projects; (b) provide term financing to NDB for onlending through approved financial intermediaries to private investment projects; and (c) induce commercial banks and other financial intermediaries to undertake appraisal, financing and supervision of sound investment projects.

The project may be audited. The focus of the audit would be on issues not well covered in the PCR relating to the targeting of credit in an unstable and uncertain macroeconomic environment.

Attachment

I This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. I

FOR OFFICIAL USE ONLY

JAMAICA

INDUSTRIAL CREDIT PROJECT LOAN 2294-JM

PROJECT COMPLETION REPORT

Preface .............................................................. i ...................................................... Evaluation Summary iii

Part I . PROJECT REVEW FROM BANK'S PERSPECI'IVE

.................................................... 1 . Project Identity 1 2 . Background ....................................................... 1

...................................... 3 . Project Objectives and Description 1 ....................................... 4 . Project Design and Organization 2

.............................................. 5 . Project Implementation 4 6 . ProjectResults ..................................................... 6

................................................ 7 . Project Sustainability 9 .................................................. 8 . Bankperformance 9

9 . BorrowerPerformance ............................................... 10 ............................................... 10 . Project Relationships 11

................................................ 11 . Consulting Services 11 ...................................... 12 . Project Documentation and Data 11

Part I1 . P R O J E n REVlEW FROM BORROWER'S P E R S P E W ............ 12

Part III . STATISTICAL INFORMATION

................................................ 1 . Related Bank Loans 14 .................................................. 2 Project Timetable 15

3 . Cumulative Estimated and Actual Disbursement ........................... 16 4 . StatusofCovenants ................................................ 17

............................................. 5 . Use of Bank Resources 18 6 . Project Implementation

6.1 Characteristics of Subprojects ..................................... 19 6.2 Performance of Subprojects ...................................... 21 6.3 Distniution of Subprojects ....................................... 23

....................................... 6.4 Project Costs and Fmancing 24

7 . NDB's Fmancial Performance ................. 7.1 Audited Balance Sheet (as of December 31). 1985-1991 25

.............................. 7.2 Audited Income Statements . 1985-1991 26

....................... 8 . Projected and Actual Loan Commitments. 1983-1991 27

This document has a restricted distribution and may be used by recipients only in the performance of their official duties . Its contents may not otherwise be disclosed without World Bank authorization .

Table o f Contents (cont'd)

Page N o .

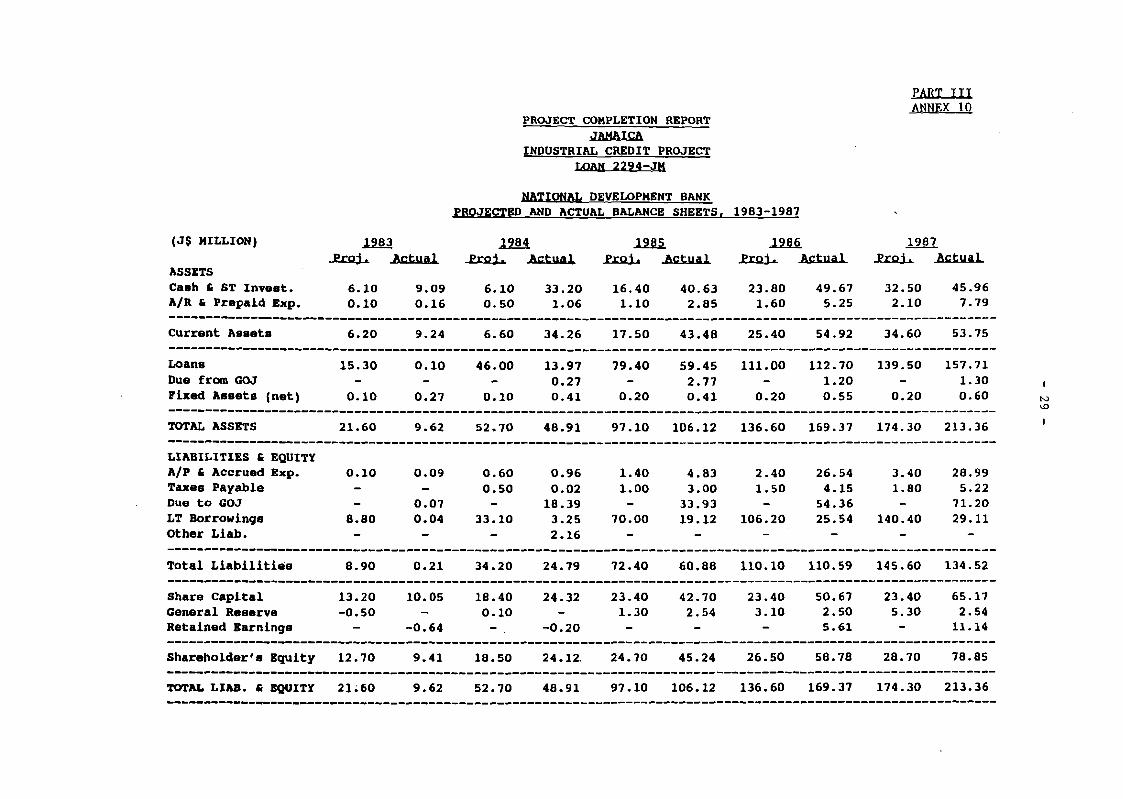

9 . Projected and Actual Income Statements. 1983-1987 . . . . . . . . . . . . . . . . . . . . . . . 28 10 . Projected and Actual Balance Sheets. 1983-1987 . . . . . . . . . . . . . . . . . . . . . . . . . . 29

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Attachment: Copy o f letter from PIOJ 31

JAMAICA

INDUSTRIAL CREDIT PROJECT LOAN 2294-JM

PROJECT COMPLETION REPORT

PREFACE

This Project Completion Report (PCR) reviews the performance of the Industrial Credit Project in Jamaica for which Loan 2294-JM (US$15.1 million) was approved by the Board on May 26, 1983. The Loan had a credit component of US$15.0 million and a technical assistance (TA) component of US$O.1 million. The proceeds of the credit component were channeled through the National Development Bank of Jamaica Limited (NDB). NDB, established in 1981, has operated as an apex (or second-tier) institution, providinfr term finance to business enterprises engaged in manufacturing and tourism and related services through a network of approved financial intermediaries (AFIs). The loan was closed with the cancellation of US$326,796 on July 27, 1990, about 31 months after the original Closing Date.

Parts I and 111 of the PCR were prepared by the Trade, Finance, Industry and Energy Operations Division, Country Department 111, Latin America and the Caribbean Region (LA3TF). Part I1 has been prepared by NDB. The entire draft PCR has been sent to the Borrower and NDB for their review and comments. The Borrower approved Part I1 prepared by NDB without comments on Parts I and II.

The PCR is based on the Staff Appraisal Report (SAR); the Loan and Project Agreements; supervision reports; internal Bank memoranda; correspondence between the Bank and the Borrower1 NDBl AFIs; NDB's audited annual financial statements and periodic progress reports; and data compiled on subprojects and World Bank missions' interviews with selected subborrowers.

INDUSTRIAL CREDTT PROJECT

EVALUATION SUMMARY

1. Obiectives. The principal objectives of the project were to: (a) assist NDB in establishing and testing sound policies, procedures and organizational arrangements for financing private investment projects; (b) provide term financing to NDB for onlending through approved financial intermediaries (AFIs) for sound industrial projects of new and expanding private enterprises and, in the process, to improve the financial position and efficiency of these enterprises; and (c) induce commercial banks and other financial intermediaries to undertake appraisal, financing and supervision of sound investment projects (para. 3.1).

2. Imvlementation Experience. The project's scope and timing were appropriate. The project funds covered all the productive activities in the manufacturing, industrial, agro-industrial, mining, tourism, and related service sectors. The project's two-tier credit system was timely and necessary in view of the planned closure of the public development financial institutions (DFIs) (para. 4.5). The final disbursement took place 3 1 months after the original Closing Date of December 3 1, 1987, due mainly to a clouded investment climate in the early stage of project implementation and partly to NDB's decision not to use IBRD funds for indirect foreign exchange cost and working capital until late 1986 (para. 5.1). The Bank continued to pursue before the emergence of a private DFI that NDB should also be involved in direct lending in order to ensure the access of potentially profitable projects of smaller or new enterprises to development funds. The Government, however, did not allow NDB to lend directly because of understandable concerns that this could lead NDB into the same problems suffered by the previous DFIs. Thus, the issue of potential conflict of interest that could have arisen from NDB's duaI roles (as the Apex institution and as a retail lender) was avoided. However, initial perception of NDB's potential dual roles was reflected in the NDB's Statement of Policies and Operating Criteria, which include elaborate guidelines normally applicable to a typical DFC (para. 4.5). With such guidelines and to satisfy the requirement of international financial institutions, NDB continued to be involved in the preparation of detailed subproject appraisal reports (para. 5.2 and 9.1). Against the background explained in detail in para. 5.3, NDB applied the additional 1% interest charge on loans funded out of foreign borrowing. This provided a basis for an arrangement under which NDB would recover from the Government the foreign exchange losses in excess of accumulated additional interest charges. This arrangement was used with a view to protecting NDB from the exchange losses resulting from its direct borrowing from other international financial institutions with the Government's guarantee. The Bank found the arrangement technically deficient mainly because the arrangement did not provide adequate compensation for the Government's assuming the exchange risk. The Bank proposed in 1985 that NDB introduce a variable interest rate system in order to ensure that onlending rates to the final beneficiaries could generally follow market forces during the life of subloans and to enable the Government to assume the foreign exchange risk without incurring major losses. However, the Bank could not effectively persuade NDB to implement the Bank supervision missions' specific recommendations on onlending rates and simplification of procedures (paras. 5.2 and 5.3). Judging from the generally good performance of subprojects financed, NDB carried out the Industrial Credit project reasonably well in collaboration with AFIs (paras. 6.1-6.6 and 9.1).

3. Results. The project has largely met its specific objectives. First, NDB's Statement of Policies and Strategy and its Operating Criteria introduced under the project have been found, by and large, sound and provisions therein have generally been complied with by NDB and AFIs with a minor exception. NDB has developed into a reasonably effective Apex lending institution and played an important role in the aftermath of closure of the public DFIs (paras. 6.5 and 9.1). Second, the proceeds of Loan 2294-JM were used to finance 37 subprojects with aggregate project costs of about US$80.7 million. For every dollar disbursed by the IBRD, nearly six dollars equivalent of resources were contributed by NDB, AFIs and subborrowers to the subprojects. Most subprojects weathered the liberalization process reasonably well. Third, most of AFIs have built up capability for long-term lending.

4. The performance of the 37 subprojects financed has been generally good in terms of debt servicing, employment creation and operational performance. Twenty four subloans were fully repaid and thirteen subloans remained outstanding with no arrears with AFIs for over three months. These subprojects created approximately 2,600 new jobs as against 1,650 estimated at the time of appraisal. Out of thirty two firms on which information is available, twenty four firms (75%) are currently operating profitably; five firms are currently operating at a loss; two subprojects were burnt down and one subproject was closed down (para. 6.3).

5 . Sustainability. The institutional arrangements for the two-tier credit system proved sustainable as the arrangements had worked reasonably well under the project and the European Investment Bank, Caribbean Development Bank, and the Inter-American Development Bank have subsequently used the same arrangements. However, its current institutional structure and modus operandi should be reviewed and modified as needed to introduce realistic policies and simpler procedures relevant to the liberalized economic environment as well as the AFIs' enhanced capability for long-term lending and to ensure that its related institutional arrangement is cost-effective (para. 7.1). The sustainability of benefits of subprojects financed is difficult to assess precisely. However, almost all tourism subprojects and export oriented subprojects, having benefitted from the liberalization of the exchange control regime, performed very well with few exceptions. Most of the import substitution subprojects were associated with well established business groups and appeared to be well managed with sound financial structure; they should be able to adapt to the new business environment. Some import substitution firms, however, would need to restructure their operations with a view to improving their productivity (para. 7.2).

6. Findings and Lessons Leaned. The project has largely achieved its specific objectives. On the whole, the project was well designed and carried out reasonably well, but specific financial soundness criteria for financial intermediaries to become AFIs (the establishment and enforcement of which are now mandatory in the Bank) should have been established and the respective roles of NDB and AFIs in subloan appraisal, and their documentation could have been more realistically designed (para. 4.5). One lesson that may be learned from the project has to do with the general framework of onlending rates to AFIs and to the final beneficiaries. The onlending rate to AFIs should be linked to a market-based reference rate and adjusted periodically so that onlending rates to the final beneficiaries can follow market forces during the life of the subloan. The bulk of interest differential between rates on foreign borrowing and (market-based) onlending rate to AFIs should accrue to the Government to enable it to assume the foreign exchange risk without incurring major losses (para. 8.2).

PART I. p w

-y

Name : Industrial Credit Project Loan Number : 2294-JM RVP Unit : Latin America and the Caribbean Country : Jamaica Sector : Industrial Finance Subsector : Manufacturing and Tourism and Related Services

2. Backqround

2.1 The key elements of the development objectives and strategy pursued by the Government at the time of project appraisal in November 1982 were: (a) stabilization and economic growth in conjunction with an outward-looking strategy; and (b) freer play of market forces and an expaneion of the private sector. With the support of the IMF and the Bank during the early 1 9 8 0 ~ ~ the Government executed several structural adjustment programs. The Government emphasized a reduction of its role and began to reduce state interventions so as to eliminate distortions in resource allocation. The goal was to foster Jamaica's comparative advantages and attain a balanced, stable and sustained growth in output, income and employment. The Loan was approved in May 1983.

2.2 As part of the institutional and policy reforms, the Government decided in 1981 to phase out three public development financial institutions (DFIs) involved in industrial lending, namely, the Jamaica Development Bank (JDB), the Small Induetries Finance Co. (SIFCO) and Premier Investment Corp. (PIC). The first two institutions and their predeceaeore had not performed well and had a historically poor record of loan collections. The third one, a separate agency of the Bank of Jamaica, had provided credit through commercial banks for small businesses; it was focusing on the collection of outstanding loans and winding up its operations since 1982. Bank assistance was requested in organizing and financing a publicly-owned National Development Bank (NDB), a new second-tier (Apex) inetitution that would be insulated from the credit risk by onlending through commercial banks and other financial intermediaries.

3. Proiect Obiectives and Description

3.1 The Project objectives were to:

(a) assist NDB in establishing and testing sound policies, procedures and organizational arrangement6 for financing private investment pro jects ;

(b) provide term financing to NDB for onlending through approved financial intermediaries (AFIe) for sound industrial projects of

new and expanding p r i v a t e e n t e r p r i s e s and, i n t h e process , t o improve t h e f i n a n c i a l p o s i t i o n and e f f i c i e n c y of t h e s e e n t e r p r i s e s ; and

( c ) induce commercial banks and o t h e r f i n a n c i a l i n t e r m e d i a r i e s t o undertake a p p r a i s a l , f i nanc ing and supe rv i s ion of sound investment p r o j e c t s .

3.2 The p r o j e c t provided USS15.1 m i l l i o n f o r f inancing: ( a ) t h e f o r e i g n exchange component of sub loans extended by NDB f o r s u b p r o j e c t s i n t h e manufacturing, i n d u s t r i a l , a g r o - i n d u s t r i a l , mining, tour i sm, and r e l a t e d s e r v i c e s s e c t o r s . (Large bauxite-alumina e n t e r p r i s e s w e r e not e l i g i b l e f o r funding . ) ; ( b ) t r a i n i n g and t e c h n i c a l a s s i s t a n c e program f o r NDB and p a r t i c i p a t i n g in t e rmed ia r i e s ; and ( c ) acqu i r ing micro-computer equipment and s o f t w e ~ e , and o f f i c e equipment of up t o USS100,OOO equ iva l en t . The loan was t o f i nance cons t ruc t ion and/or renovat ion of i n d u s t r i a l s t r u c t u r e s , purchase of machinery and equipment, permanent working c a p i t a l , and t e c h n i c a l a s s i s t a n c e t o f i n a l b e n e f i c i a r i e s f o r preinvestment and market s t u d i e s , t r a i n i n g and consu l t i ng s e r v i c e s . NDB d i d no t use t h e Loan proceeds f o r f i nanc ing t e c h n i c a l a s s i s t a n c e and t r a i n i n g and a c q u i s i t i o n of microcomputers noted i n i t e m s ( b ) and ( c ) above a s bo th i t e m s w e r e m e t by o t h e r sources of funds . 4. P r o j e c t Desisn and Orqaniza t ion

4.1 NDB was e s t a b l i s h e d i n 1981 and has opera ted a s an apex o r second- t ier i n s t i t u t i o n , p rovid ing t e r m f i nance t o bus ines s e n t e r p r i s e s engaged i n manufacturing and tour i sm and r e l a t e d s e r v i c e s through a network of -1s. The Government of Jamaica, t h e Borrower, passed on t h e Bank l o a n proceeds t o NDB on t h e same terms a s t h e Bank loan bu t i n JS a t t h e o f f i c i a l exchange r a t e a t t h e time of t h e r e s p e c t i v e disbursements. Thus, t h e Government assumed t h e f u l l exchange r i s k . The loan was f o r 17 yea r s , i nc lud ing 4 y e a r s of g race , wi th t h e s t anda rd v a r i a b l e i n t e r e s t r a t e . The e l i g i b i l i t y cond i t i ons f o r AFIs enabled a l l f i n a n c i a l i n s t i t u t i o n s l e g a l l y e s t a b l i s h e d and approved by NDB t o p a r t i c i p a t e i n t h e program provided t h a t t h e y have exper ience i n app ra i s ing and supe rv i s ing term loans and t h a t t h e y des igna t e a t l e a s t one s e n i o r execu t ive a s be ing r e s p o n s i b l e f o r p r o j e c t eva lua t ion and co-ordinat ion wi th NDB. NDB had t h e r i g h t t o withdraw its approval of any AFI a t i t s own d i s c r e t i o n . NDB's Statements of P o l i c i e s and S t r a t e g y and Opera t ing C r i t e r i a , accepted by t h e Bank, d i d no t s p e c i f y f i n a n c i a l soundness c r i t e r i a f o r f i n a n c i a l i n s t i t u t i o n s t o become and remain an AFI. AFIs w e r e t o be r e spons ib l e , i n a d d i t i o n t o assuming t h e c r e d i t r i s k on t h e i r subloans, f o r a p p r a i s a l and supe rv i s ion of subp ro j ec t s t h e y f inanced and semi-annual submission t o NDB of t h e i r f i n a n c i a l s t a t emen t s and subpro j ec t supe rv i s ion r e p o r t s . NDB was expected t o ensu re no t on ly t h e f i n a n c i a l v i a b i l i t y b u t a l s o t h e economic and t e c h n i c a l v i a b i l i t y of each subpro j ec t . Each AFI waa o b l i g a t e d t o repay NDB accord ing t o an agreed schedule , r e g a r d l e s s of whether a subborrower m e t i t s repayment o b l i g a t i o n a o r not . NDB waa t o review annual ly ope ra t i ons of AFIs wi th r e s p e c t t o t h e i r i n t e r f a c e w i th NDB.

4.2 The Bank loan was to finance: (a) 100% of foreign exchange costs for imported iteme; (b) 65% of the coete of locally procured goods; and (c) 30% of expenditures for civil worke required for the eubproject. Final beneficiariee (eubborrowers), AFIe and NDB (out of ite local reeourcee) were expected to contribute for subproject financing. The subborrowere were expected to comply with a maximum debt-equity ratio of 4:l in the case of subprojecte with net fixed aeeete below J$300,000, and 3:l with net fixed assets above thie amount. All eubprojecte would be reviewed and approved by NDB in accordance with the evaluation criteria contained in its project appraieal manual approved by the Bank. AFIe had a free limit with NDB of J$100,000 and NDB had a free limit with the Bank of USS250,OOO equivalent. The internal rate of return (IRR) was to be calculated for all subprojects with net aeeete above J$100,000 and the economic rate of return (ERR) for all eubprojecte whose net fixed aeeet value, including eubloan financing, exceeded J$500,000. Cut-off IRR and ERR ueed by NDB were 12%. The maximum subloan limit of USS2.0 million was establiehed through an amendment to the Loan Agreement. Although the Loan Agreement wae amended to open and thereafter maintain a Special Account to facilitate diebureemente for eligible expenditures, nearly all (about 98%) eubloan diebureemente were made on the baeie of full documentation. The NDB'e onlending rate to AFIe would be at least 12% p.a. plue a 1% one-time front-end fee. AFIe were to onlend the loan proceed8 to final beneficiariee at a minimum of 15% p.a. (retaining a 3% epread) plue a one-time front-end fee not exceeding 2%. Except for the early stage of implementation when both NDB and AFIe charged the minimum ratee, the NDB's onlending rate varied between 13% and 17% during the project implementation; and intereet rate to final beneficiaries, between 16% and 20%. The maturities of eubloane, which were expected to be for 3 to 10 yeare including 3 years of grace, varied according to debt eervice capacity of the individual eubprojecte but were generally ehorter than the maximum allowable eubloan repayment schedule.

4.3 NDB wae expected to endeavor to earn profit and to maintain a debt- equity ratio not exceeding 5:l. NDB'e operations were profitable becauee of a generoue epread and guaranteed loan collections from AFIe. Its financial structure wae doubtleeely sound before the ieeue of the foreign exchange loeees surfaced (para. 5.3). Its maximum financial exposure in a single enterprise (or a group of enterprises with joint capital or management control) was limited to 25% of NDB'e net worth or USS2 million. No subloan under the Bank loan exceeded thie limit. By the time Loan 2294-JM became effective, NDB'e paid-in capital reached JS10.0 million and a USS6.0 million line of credit wae aleo made available by the Caribbean Development Bank (CDB) . 4.4 At the time of project appraisal, NDB'e Board of Directore consisted of eight membere, four of whom were from the private eector including the Board's Chairman. NDB wae expected to have a modeet number of well qualified profeeeional etaff, including economiete, financial analyete and engineers. At the time of appraieal, the NDB'e etaff etrength wae found satisfactory to initiate operations under the Bank loan8. NDB obtained the eervicee of an expatriate advieor for about one year.

4.5 The project's scope and timing were appropriate. The project funds covered all the productive activities in the manufacturing, induetrial, agro- industrial, mining, touriem, and related eervice eectore. The project'e two- tier credit eyetem wae timely and neceeeary in view of the planned closure of the public DFIS (para. 2.2). On the other hand, the Bank agreed with the Government'e initial thought that NDB ehould be engaged, in due couree, in all the function8 of the previoue institutione, including direct lending and equity inveetmente. The Bank continued to pureue thie thought, particularly during project preparation and the initial etage of project implementation, until a private development bank etarted operations in May 1985. However, the Government did not allow NDB to begin direct lending becauee of underetandable feare that thie could lead NDB into the eame probleme euffered by the previous inetitutione. Thue, the ieeue of potential conflict of intereet that could have arieen from NDB'e dual rolee ae the apex institution and ae a retail lender was avoided. However, the Bank'e endorsement of the Government'e initial perception of NDB'e potential dual rolee wae reflected in the NDB'e Statement of Policiee and Operating Criteria, which include elaborate guidelines normally applicable to a typical DFC. On the whole, the project wae well deeigned, but epecific financial eoundneee criteria for financial intermediaries to become AFIe ehould have been eetabliehed, and the reepective rolee of NDB and AFIe in eubloan appraieal and eupervieion, and their documentation could have been more realietically deeigned.

5. Proiect Implementation

5.1 1 The final diebureement took place in July 1990, 31 months after the original Cloeing Date of December 31, 1987. An undiebureed balance of US$326,796 wae canceled on July 27, 1990. Diebureemente were completed in a eeven-year period, elightly elower than the etandard diebureement profile for apex type lending. Three factore were mainly reeponeible for the elower than expected pace of diebureemente: (a) clouded investment climate, particularly in the early etage of project implementation due to a combination of factore including labor unrest; (b) NDB'e decieion not to use IBRD funde for indirect foreign exchange coat and working capital until late 1986; and (c) need for replacing eubprojecte, approved earlier but remained dormant, with new onee.

5.2 Proiect Riske. The project did not involve any unueual rieke. Of the potential rieke identified and diecueeed in the appraieal report, the riek of NDB'e aeeuming a greater reeponeibility for eubproject appraieale had some eignificant implicatione. A number of AFIs readily accepted that, during the period of project implementation, they had built up the capability of (and eometimee undertaken) appraieal of the riek involved in long-term lending; thie is borne out by the fact that most connnercial banks in Jamaica have establiehed either a corporate finance unit or a merchant bank eubeidiary. However, NDB continued to undertake project appraieal and eupervieion and ite modue operandi basically remained unchanged. The underlying rationale for NDB'e continuing involvement in the preparation of detailed project appraieal reporte wae to eatiefy the requirement of international financial inetitutione. Related to thie, it ehould be noted that the Bank'e June 1986 eupervieion miseion recommended (and NDB management agreed) that in caeee

where AFIs' loan e v a l u a t i o n r e p o r t e t o g e t h e r w i th f e a s i b i l i t y s t u d i e e , i n NDB's judgment, cover most important a s p e c t s of a subpro jec t proposa l adequately, NDB send IBRD cop ie s of AFIs' r e p o r t e and f e a s i b i l i t y s t u d i e s t o g e t h e r wi th NDB'e summary r e p o r t s ( 3 t o 5 pages) supplementing MIS' r e p o r t s / s t u d i e s . This recommendation wae not t e e t e d under t h e p r o j e c t . Despi te a l l t h i s , NDB's working r e l a t i o n s h i p wi th AFIs w i th r e s p e c t t o subpro jec t a p p r a i s a l was good, mainly because of NDB's w i l l i n g n e s s t o work wi th AFIs a t t h e e a r l y s t a g e of eubpro jec t a p p r a i s a l .

5.3 Actions o r Decis ions Taken o r not Taken which Affected P r o i e c t I m ~ a t a t i o n . A ques t ion was r a i s e d wi th in t h e Bank dur ing t h e Loan Committee review on t h e 1% p.a. f e e on eubloans r e q u i r i n g f o r e i g n currency f inanc ing s i n c e t h a t f e e d i d no t appear t o be adequate t o cover t h e fo re ign exchange r i s k . I t was c l a r i f i e d t h a t t h e Government had decided t o re lend t h e procef9e of Loan 2294-JM t o NDB on t h e same terms a s t h e Bank loan but i n J $ and t h a t t h e 1% premium on " f o r e i g n exchange loane" would remain wi th NDB. (Under Loan 2294-JM, t h e Government, i n add i t i on , undertook t o prevent NDB from i n c u r r i n g any exchange l o s s e s r e s u l t i n g from i ts borrowing opera t ions . ) Against t h i e background, NDB app l i ed t h e 1% p.a. premium on subloans funded ou t of f o r e i g n borrowing al though subloans w e r e denominated i n J$. This p r a c t i c e had t h e fo l lowing consequences. F i r s t , t h e 1% p.a. onlending r a t e d i f f e r e n t i a l i n f avo r o f l o c a l l y mobilized J$ r e sou rces provided d i s i n c e n t i v e f o r AFIs t o u se IBRD funds f o r f i nanc ing t h e i n d i r e c t f o r e i g n exchange component of subpro jec t c o s t s . Second, t h e a d d i t i o n a l 1% i n t e r e e t charge on loans funded ou t o f f o r e i g n borrowing provided a b a s i s f o r an arrangement between t h e Government and NDB under which NDB would recover from t h e Government t h e f o r e i g n exchange loseea i n exceea of accumulated a d d i t i o n a l i n t e r e s t charges. This arrangement was used wi th a view t o p r o t e c t i n g NDB from exchange l o s s e s r e s u l t i n g from i t s d i r e c t borrowing from o t h e r i n t e r n a t i o n a l f i n a n c i a l i n s t i t u t i o n s wi th t h e Government's guarantee. The June 1985 Bank miseion found t h a t t h i s arrangement ( o u t l i n e d i n t h e Government's letter t o NDB of June 6, 1983) was vague and t e c h n i c a l l y d e f i c i e n t : vague because t h e t iming of t h e Government's indemnifying NDB such l o s s e e was unc lea r , and d e f i c i e n t because t h e arrangement d i d not provide adequate compensation f o r t h e Government's aesuming t h e f o r e i g n exchange r i s k . The same mission recognized t h e need f o r i n t roduc ing a new mechanism under which t h e Government should b e adequate ly compensated f o r assuming t h e f u l l exchange r i s k whi le p r o t e c t i n g NDB from i n c u r r i n g any exchange lose . I n i ts letter t o NDB da t ed August 16, 1985, t h e Bank proposed t h a t NDB in t roduce a v a r i a b l e i n t e r e s t r a t e syetem (i.e., automatic , p e r i o d i c adjustment of onlending r a t e s l i n k e d t o a e e l e c t e d base r a t e du r ing t h e l i f e of subloans) under t h e proposed Second I n d u s t r i a l Cred i t p r o j e c t i n o rde r t h a t onlending r a t e e t o t h e f i n a l b e n e f i c i a r i e s could gene ra l ly fo l low market fo rce8 dur ing t h e l i f e of subloans and, e q u a l l y important , t o e n a b l e t h e Government t o assume t h e f o r e i g n exchange r i s k without i n c u r r i n g major l o s s e s . But, t h e proposed follow-up Bank credit ope ra t ion d i d not m a t e r i a l i z e . A v a r i a b l e i n t e r e s t r a t e system was in t roduced i n 1991, a f t e r p r o j e c t completion. Af t e r t h e f u l l l i b e r a l i z a t i o n of exchange c o n t r o l regime i n September 1991 and t h e subsequent d e p r e c i a t i o n of J $ , NDB has recognized e i g n i f i c a n t f o r e i g n exchange l o s s e s on i ts f o r e i g n cur rency borrowing; NDB is t r y i n g t o recover such l o s s e s from t h e Government under t h e arrangement noted above.

5.4 At the time of appraisal, NDB was required to review with the Bank at least annually NDB'e lending ratee and, if neceeeary, to revise them in a manner satisfactory to the Bank. NDB'e discount rates hovered around 13% to 17% and onlending ratee to financial beneficiaries, around 16% to 20% plus a front end fee not exceeding 2%. NDB's lending ratee were at times below the commercial banke' weighted average deposit rate and onlending ratee to financial beneficiaries were negative in real terms particularly at the early etage of project implementation. NDB, at the repeated urging of the Bank, raised its diecount rate by 3% to 17% on foreign funded resources in March 1985. Since then, intereet rates to final beneficiaries were generally positive in real terms during the project implementation period but lower than market ratee.

Proi ect Reeults

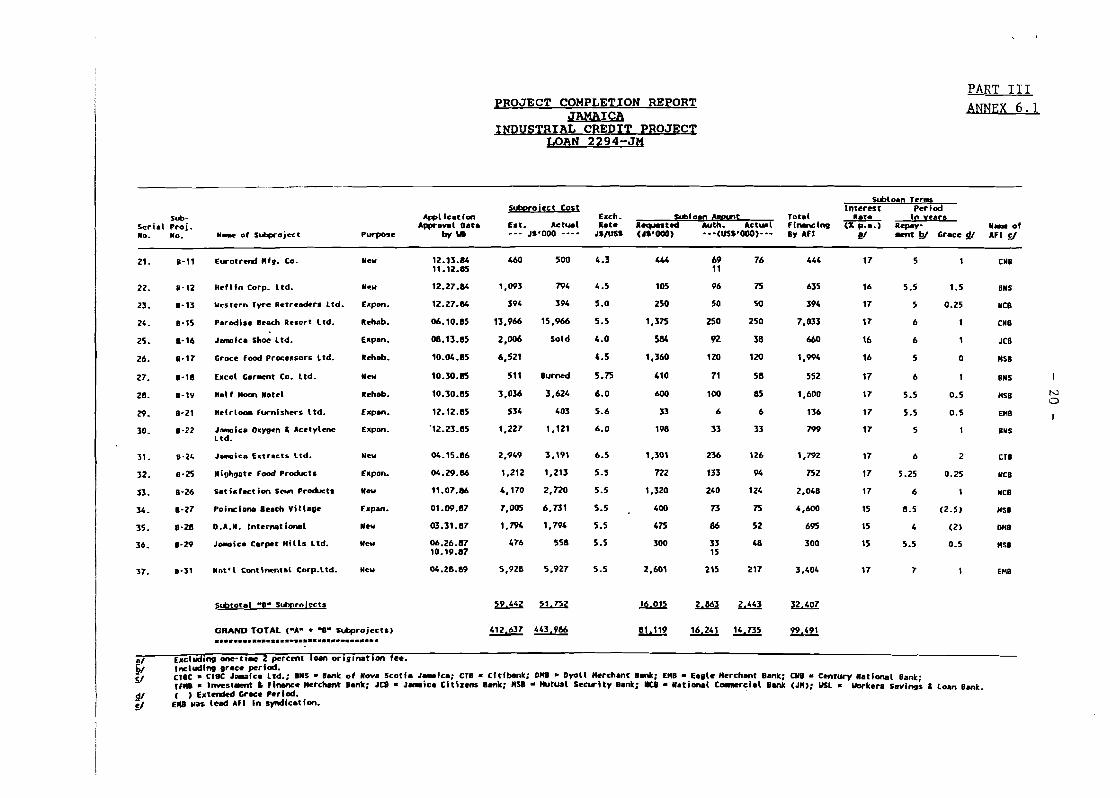

6.1 Achievements of Proiect Obiectivee. The project has largely met its specific objectives noted in paragraph 3. Firet, NDB'e Statement of Policies and Strategy and its Operating Criteria introduced under the project have been found, by and large, sound and provieione therein have generally been complied with by NDB and AFIe with the exception of AFIs' reporting on subproject performance (para. 6.4). Although, its Statement of Policy and Strategy permite it to ieeue guaranteee, enter into cofinancing arrangements, extend direct loans, make underwriting commitments, and participate in equity inveetmente, NDB ha8 been operating only as a second-tier inetitution in order not to repeat a history of the public DFIe for which NDB subetituted. From a modeet start, NDB has developed into a reaeonably effective second-tier lending institution and played an important role in the aftermath of the closure of public DFIe (paras. 6.5 and 9.1). Second, the proceeds of Loan 2294-JM were used to finance 37 eubprojects with aggregate project costs of about USS80.7 million. For every US dollar disbursed by IBRD, nearly six US dollare equivalent of resources were contributed by NDB, AFIe and eubborrowers to subprojects. Moat subprojecte weathered the liberalization process reasonably well. Almost all touriem subprojects and export oriented subprojecte, having benefitted from the full liberalization of the exchange control regime, are currently operating profitably. Moet of the import substitution eubprojecte were aeeociated with well eetablished business groups and appeared to be well managed; some of them were actively exploring the possibility of penetrating CARICOM markets. Actual performance of eubprojects was generally good; most of them fully repaid eubloane to AFIe on t h e and thoee eubborrowere with outstanding eubloan balances had no arreare with AFIe (para. 6.3). In reepect of the third objective, most of AFIs that the PCR preparation mission interviewed explained that they have built up capability for long-term lending (para. 5.2).

6.2 Impact of Proiect. (a) Characteristics of Subprojects financed are ehown in Annex 6.1. A total of 37 eubprojects were financed with an aggregate subproject coet of approximately USS80.7 million, of which IBRD funding amounted to USS14.7 million or about 18.2% of the total, with final beneficiaries (eubborrowers) and AFIe making up the balance. One eubborrower received two eubloane (for two separate eubprojects) totalling US$253,000; and thus 36 subborrowere benefitted from the project. Of the 37 subprojecte, 12

relatively large (involving IBRD funding above the "free limitn of US$250,000) subprojects absorbed USS12.3 million equivalent of IBRD resources, or 83.7% of the credit component. The remaining 25 subprojects were for eubloans of leee than US$250,000 and received a total of USS2.4 million equivalent of IBRD reeourcee. The average eubloan eize for the larger eubprojects was in the order of USS1.0 million and for the smaller, in the order of USS100,OOO. On the whole, the average eubloan size wae USS397,000, the largest being USS2.O million and the smallest being USS6,OOO. Fifteen (15) eubloane were made for new projects; and the remaining 22, for expansion and/or rehabilitation projects. In terme of sectore, eubloane totalling USS5.99 million were channelled for ten food processing projects; USS4.68 million, for seven tourism projects; and USS0.44 million for five garment projecte. The remaining fifteen eubloane totalling USS3.62 million coneieted of: four in packaging (USS2.13 million); nine in various manufacturing (USS0.87 million); one in agro-industry (USS0.57 million); and one in the eervice eector (USS0.05 million).

6.3 (b) Performance of Subloans. The performance of the eubprojects financed has been generally good in terme of debt servicing, operational performance and employment creation. As of February 14, 1992, twenty four subloans were fully repaid and thirteen eubloane remained outetanding with no arrears with AFIs for over three months. Four outstanding eubloans, however, had a history of their grace period extended during the project implementation period. The Bank's PCR preparation miseion visited eighteen eubprojecte and had extensive diacuesions with AFIs and NDB on the performance of moet of eubprojecte financed. According to information obtained from the field vieite, AFIe and NDB (Annex 6.2), nineteen firme are operating profitably and are likely to achieve ratee of return higher than NDB's cut-off rate of 12%; five firme had a hietory of initial difficultiee but are currently operating profitably with the poesibility of ratee of return being in the range of the NDB'e cut-off rate; five firme are currently operating at a lose; two eubprojecte were burnt down and one subproject wae closed down. Information on four companiee, for which subloans totalling USS245,OOO were extended, was not available as theee firme had fully repaid subloane some time ago and eince then their banking relationship with AFIe wae not active. Thue, out of thirty two firme on which information is available, twenty four firme (75%) are currently operating profitably. Subprojects financed created 2,587 new jobs compared with 1,650 estimated at the time of appraisal of Loan 2294-JM.

6.4 (c) Participating Financial Intermediariee. Eleven financial institutions participated in the project. All AFIs are privately owned or controlled by the private eector. Annex 6.3 shows a summary of each AFI'e participation in the project. The moet active, in terme of number of eubprojecte financed, were four commercial banks. Theee banks, taken together, financed 24 eubprojecte while each bank financed five to seven projects. The remaining eeven AFIs (three merchant banks, four commercial banks) financed thirteen projects. In two inetancee, eeveral AFIs cofinanced eubprojecte to avoid concentration of the credit riek. With one exception, the financial performance of AFIs seemed to have been satisfactory throughout the project implementation period. In the caee of one commercial bank, NDB euepended ite eligibility pending its restructuring. Moet of the commercial

banks that participated in the project established a corporate finance unit or a merchant bank subsidiary. Judging from the generally good performance of subborrowera (para. 6.3), AFIs did a good job in selecting creditworthy project sponsors. Representatives of the nine AFIs the PCR preparation mission interviewed indicated that they followed up closely the credit and financial standing of subborrowers until subloans were fully repaid. They exchanged information on subborrowers during semi-annual meetings with NDB officials in lieu of submitting reports on subproject performance required under NDB's Operating Criteria.

6.5 (d) The National Development Bank (NDB). NDB has developed into a reasonably sound second-tier credit institution. It has played an important role in the aftermath of closure of public DFIs by: (a) tapping foreign currency resources (totalling about USS71.0 million equivalent) not only from IBRD but also from the Caribbean Development Bank (CDB), the U.S. Agency for International Development (USAID), the Inter-American Development Bank (IDB) and the European Investment Bank (EIB); and (b) channelling these funds through AFIs to over 340 subprojecte in various sectors. It has four departments (Projects, Finance and Accounts, Administration & Legal, and Special Projects) and the internal audit unit. NDB has a total of 73 staff (including 22 professionals). One of the main reasons for having the large number of staff has been that NDB has managed, at the request of the Government, the liquidation/administration of portfolios of the now defunct Jamaica Developnent Bank, Small Enterprise Developnent Corporation (SEDCO), Small Industries Finance Co. (SIFCO), and Premier Investment Corp. (PIC). The Bank had originally encouraged NDB to build up its project-oriented staff, but it did so in the light of NDB's role perceived by the Bank as a project promoter, evaluator and provider of technical assistance. In 1984 when the total number of NDB staff reached 30 people and, subsequently, as it became clear that NDB would not involve itself in direct lending, a question was raised within the Bank as to whether a rapid increase in NDB staff was necessary. Since then, the number of NDB staff increased further partly for the reason noted above.

6.6 At the time of appraisal, NDB's loan commitments were projected to total about USS109.5 million during the 1983-87 period but the actual loan commitments, according to NDB's data, were about USS56.3 million during the five-year period (Annex 8). Between 1988 and 1990, NDB'e annual loan commitments averaged around USS25 million. Despite the lower-than-anticipated lending volume, NDB'a profits were higher than the levels projected for the FY84-87 period due entirely to a higher spread than projected. NDB's after tax income totalled nearly JS15 million during four and half years ended March 31, 1987 as against JS5.8 million projected for FY83-87 (refer to Annex 9). Its return on equity hovered around 8.3% to 17.8% during the FY86-90 period before it dropped to 2.4% in FY91 due to the large amount of provisions made for the foreign exchange loee. As diecussed in para. 5.3, NDB is, in principle, protected from foreign exchange losaee; nevertheless, given the sharp JS depreciations which took place in FY91 and the potential difficulties in early recovery of the foreign exchange losses from the Government, the NDB's Board decided to make provisions against non-recovery of these losses amounting to JS20.6 million for FY91 ended on March 31, 1991. Further sharp

depreciations took place during FY92 and NDB is attempting to recover these additional foreign exchange losses from the Government. NDB's total assets have grown at an average rate of about 35% annually, during the FY85-91 period. Its liquidity position has been comfortable with guaranteed loan collections and its financial structure has been strong with a debtlequity ratio of below 2.5:1, considerably below the maximum limit of 5:l specified under NDB's Statement of Policy and Strategy, before the issue of the foreign exchange losses has surfaced. Audited balaace sheets and income statements for FY85-91 are shown in Annexes 7.1 and 7.2.

Project Sustainabilitv

7.1 The institutional arrangements for the two-tier credit system, established and tested in Jamaica under this project, proved sustainable for some time as the arrangements had worked reasonably well under the project and the European Investment Bank, Caribbean Development Bank, and Inter-American Development Bank have subsequently used the same arrangement. NDB has played an important role in filling a gap in the aftermath of closure of all public DFIs in Jamaica. However, while the two-tier credit mechanism, in one form or another, would continue to be necessary over the medium and longer term, the current institutional structure and modus operandi should be reviewed carefully and modified as necessary to introduce realistic policies and simpler procedures relevant to the liberalized economic environment as well as the AFIs' enhanced capability for long-term lending and to ensure that the related institutional arrangement is cost-effective.

7.2 The suetainability of benefits of subprojects financed is difficult to aseess precisely. However, the seventeen subborrowere that the Bank PCR preparation mission had visited performed fairly well with the exception of two projects. Needless to say, their output and employment levels will fluctuate over time. But, their generally good performance to date in competing in a liberalized domestic market and regional (and in a limited way in extra regional) markets, apparently well established management, and sound financial structure suggest that most of these seventeen firms, if not already benefitting f r m liberalized economic environment, are capable of adapting to the new business environment. Some small subborrowers went under but the subprojects financed were apparently well run by new owners. Some import subetitution firms are currently struggling to stay afloat and are considering the restructuring of their operations with a view to improving their productivity . 8. Bank Performance

8.1 1 Bank staff contributed to the establishment of policies and procedures of NDB and the smooth working of the two-tier credit system through supportive working relationships and professional advice. However, unlike the Government which abandoned its own idea of letting NDB have dual roles (para. 4 . 5 ) , the Bank continued to pursue, at the initial stage of project implementation and before the emergence of a private sector development bank, that NDB should also be involved in direct lending and equity investments in order to ensure the access of sound and

potentially profitable projecte of emaller or new enterprieea to development funde. For the reaeone etated in para. 4.5, the Government did not allow NDB to lend directly. Ae NDB did not function ae a retail lender in addition to ite apex role, the iaeue of conflict of intereet was avoided. However, potential dual rolee built into the NDB8e Statement of Policy and Strategy may be reeponeible for overly structured reepective rolee of NDB and AFIe in eubloan appraieal and eupervieion and their documentation. Ae the propoeed eecond induetrial credit project, which wae prepared in 1985, did not materialize becauee NDB opted to tap reeourcee of other multilateral financial inetitutione noted in para. 7.1, the Bank could not effectively pereuade NDB to implement the Bank eupervieion mieeione' epecific recomendatione on onlending ratee (para. 5.3) and other aepecte (para. 5.2).

8.2 Leesone Learned. One leeeon that may be learned from the experience in the project hae to do with the general framework of onlending ratee to AFIe and to the final beneficiariee. Ae diecueeed in paragraph 5.3, the onlending rate to AFIe ehould have been linked to a market baaed reference rate and adjueted periodically eo that onlending ratee to the final beneficiariee could generally have followed market force8 during the life of the eubloan. The bulk of intereet differential between ratee on foreign borrowinge and (market-baaed) onlending rate to AFIe ehould have accrued to the Government to enable it to aeeume the foreign exchange riek without incurring major loeeee.

9. Borrower'e Performance

9.1 Mafn. The Borrower (the Government) and the project executing agency (NDB) were efficient in completing the condition6 of effectiveneee. The Borrower reeieted, for the good reaeone noted in para. 4.5, the nudging from the Bank to let NDB move into direct lending. While the Government hae yet to indemnify NDB the foreign exchange loeeee on NDB'e foreign currency liabilitiee (para. 5.3), the Government eupported the emooth functioning of NDB by eneuring that NDB continue8 to have foreign currency reeourcee for onlending to AFIe through facilitating NDB'e mobilization of reeourcee from varioue multilateral financial inetitutione. NDB'e acceee to four different multilateral financial inetitutione, particularly at the early stage of inetitutional developnent, eeemed to have booeted NDB'e confidence in its policiee and proceduree. Aleo, NDB'e high profitability during FY86-89 did not help etimulate eerioue thinking on the evolution of the role of NDB and related policies and proceduree. Nevertheleee, NDB carried out the Induetrial Credit project well due mainly to ite willingneee to work with AFIe from the early etage of eubproject appraieal through subproject completion. NDB'e involvement in eubproject appraieal and eupervieion, however, hae had some implicat.ione for NDB'e high adminietrative coat which hovered around 2.3- 2.5% of average total aeeete. Thie ie on the high aide for a second-tier inetitution. Although NDB'e profitability wae high during 1986-89 before the ieeue of foreign exchange loeeee eurfaced, it wae due to generous intereet spread (or the abeence of adequate annual provieioning for foreign exchange loeeee). During the project implementation period, the Bank worked with the NDB'e Managing Director appointed at the outeet of the project. He wae well reepected within NDB and by AFIe. NDB experienced a turnover of middle

management: departure of a project economiet whoee poeition wae never filled; untimely death of the former Director of the Projecte Department; and departure of Director of Finance. The latter two poeitione were filled through internal promotion. The NDB'e current management team including the new Chief Executive Officer ie addreeeing the ieeue of NDB'e future role in the liberalized economic environment.

10. Proi ect Relationehi~e

10.1 Bank relationehip with the Borrower on the project, while somewhat etrained at the beginning of the project becauee of the Bank'e euggeetione on NDB'e carrying out direct lending, hae been generally good. The Bank relationship with NDB has aleo been good. NDB hae maintained good relationehipe with the AFIe and private eector borrowere.

11.1 The need for technical aeeietance for helping NDB did not arise.

12.1 The Loan Agreement and Project Agreement were appropriate for the project. The etaff appraieal report provided a useful framework for both the Bank and NDB during project implementation. NDB'e file8 on eubprojecte were well maintained and the data on performance of aubprojecta were available ae NDB, in accordance with ite policy, prepared eubproject completion reporte in many caeee, in addition to reporte on follow-up vieite.

PART I1 Pase 1 of 2

INDUSTRIAL CREDIT PROJECT

PROJECT COMPLETION REPORT (PCR) PART I1

LOAN 2294-JM

Introduction

This report (Part I1 of the completion report on Loan 2294-JM) is prepared by the National Development Bank (NDB) of Jamaica Limited as executing agent for the Government of Jamaica (the Borrower). This report is intended to be analytical and selective (rather than descriptive and comprehensive) in commenting on the design and effectiveness of the project and lessons learned.'

Adeauacv and Accuracv of the Factual Information contained in Part I11

Part I11 of the PCR presents fairly the factual information on the project implementation, characteristics and performance of subprojects, and NDBts financial and operational performance.

NDB has no major comments (nor disagreement) on the analysis contained in Part I, which was found thorough and exceedingly candid yet well-balanced. However, the dynamic nature of the financial sector particularly during the period of structural adjustment which coincided with the project implementation period can not be over-emphasized. NDB fully concurs with the assessment as presented in paragraph 6.1 of Part I that the project has largely met its specific objectives. However, with regard to the third objective (i.e:, to induce commercial banks and other financial intermediaries to undertake appraisal, financing and supervision of sound investment projects), NDB, while admitting the significant progress to date, still believes that more can be done in this area.

The loan 2294-JM was secured at a time when NDB in its infancy needed resources in both local and foreign currency to support its lending. The Project was prepared and appraised by IBRD expeditiously, reflecting the high level of understanding and cooperation that existed between officers of NDB and IBRD. NDB is satisfied with the resulting developments/subprojects that were assisted from the proceeds of this loan.

' The Government, by its letter of December 10, 1992, has confirmed its approval of Part XI of the project completilon report (PCR) prepared by the NDB.

PART I1 Page 2 of 2

-E OF IBRD

The performance of IBRD has been very good and its staff have been very cooperative. The NDB is pleased to have collaborated with IBRD on this undertaking. IBRD played a significant role of facilitating and supporting the institutional development of NDB as a J~wholesalef institution.

While there were no major problems experienced in the execution of the programme, the following area is listed for the record and only at the IBRDfs request.

Reassignment of IBRD personnel resulted initially in loss of continuity and personal contact between IBRD and NDB officers. It is noted that the officer currently responsible for NDBfs operation has provided continuity for some time. In any event, officers assigned to NDB s programme were usually cooperative and enthusiastic . NDBfs Performance., Sustainabilitv and Lessons Learned

NDB is proud of the successful results of the Industrial Credit Project as presented in Part I. Also, it should be noted that NDB has played an important role in the aftermath of the closure of some public Development Finance Institutions (DFIs) i.e. Jamaica Development Bank (JDB), Premier Investment Corporation (PIC) and Small Enterprises Development Corporation, etc. The two-tier lending system introduced under the project worked smoothly (due mainly to NDBfs willingness to work with AFIs from the early stage of project appraisal through project completion) and has been used by other multi-lateral lenders. Despite all this, NDB management is keenly aware that NDB is at the crossroad given the liberalized economic environment (which encourages the institution to review the appropriateness of its existing policies and procedures) and the -1s' increased capability for long-term lending (out of their own deposit resources and/or direct external borrowing). NDB has been exploring various options for adapting itself to making further contribution toward development of the financial sector. Toward this end, NDB has recently collaborated with other Government-owned and private sector institutions in establishing the 'Jamaica Venture FundJ (JVF) which is intended to promote and foster the development of new projects by way of equity injection.

One positive lesson that may be learned from the experience is that AFIs and the Apex institution (NDB) can usefully work together from the early stage of subproject appraisal through subproject completion, particularly when AFIs lack necessary expertise and experience in long-term lending. Of course, such an arrangement would entail high administrative cost on the part of the Apex institution. Therefore, this aspect should be carefully assessed and a special effort for containing administrative costs would be needed.

RELATED Brn LOLVS

Loan No. 1 P r o j e c t T i t l e Purpose

Year of Approval Scatue

Ln 1003-JH S i t e e and S e w i c e e

To b r i n g housing, e s s e n c i a l commnity 1974 e e r p i c e s and job oppor tun ic iee t o J a n a i c a ' e l o v e r income groups.

Ln 1609-JH To provide f o r e i g n exchange f o r SSEs; t o 1978 Small-Scale E n t a r p r i e e involve commercial banking system i n landing Deve lopment t o SSEs; t o inc rease f l o v of b a k a b l e SSE

p r o j e c t e ; and co e s t a b l i s h SEDCO f o r ee rp ic ing v e r y smal l - sca le e n t e r p r i s e s .

Ln 1715-Jn To eupport Covernmencle o v e r a l l e f f o r t s t o 1979 Second Program Loan e t i m u l a t e expor t s of nontraditional (EDF-I) manufactured goods by a s s u r i n g continued

a v a i l a b i l i t y of f o r e i g n exchange, by Ln 1978-Jn c i rcumvent ing tho cunbersonie and inadequate 1981 Export Dev. Fund-11 fo re ign exchange a l l o c a t i o n eyetem, by eas ing

accese t o import f inanc ing c r e d i t s and terme, Ln 2320-Jn and by encouraging p r i v a t e investment f o r 1983 Export Dev. Fund-111 expor t s .

Ln 2105-JH SAL-I

Ln 2315-Jn SAL-I1

Ln 2678-Jn SAL-111

To f o s t e r e x p o r t - l e d development and t o 1982 e t r ang then t h e operacion of market fo rcee v i t h an enhanced r o l e f o r t h e p r i v a t e e e c t o r ; t o improve p u b l i c a d m i n i s t r a t i o n ; and t o 1983 develop a n energy program t o reduce petroleum importe and efianced export development programs f o r l a b o r - i n t e n s i v e manufactured and 1984 a g r i c u l t u r a l producte .

Ln 2848-JM To e r t a b l i s h a broad bared and more uniform 1987 Trade & F i n n n c i i L Sec to r t a r i f f s t t u c t u r e v i t h a p p r o p r i a t e incen t ives Adfuetment Operat ion-1 f o r expor t s ; and t o reduce b i a s a g a i n s t

p r i v a t e inveetments .

Ln 3303-Jn To reduce p r o t e c t i o n and make it uniform Trade & F i n a n c i a l Sec to r acroee r e c t o r s and s u b r e c t o r r , and inc rease Ad jusunen t Operat ion-I1 compet i t ion and e f f i c i e n c y of e n t e r p r i s e e ;

and t o improve monetary p o l i c y management and r e g u l a t o r p framevork and supervision of f i n a n c i a l i n s t i c u t i o n s .

Cloeed (1982)

Closed (1983)

Closed (1982)

Closed (1983)

Cancelled (4130185)

Cloeed (1983)

Cloeed (1984)

Closed (1985)

Cloeed (1988)

Ac t ive

ANNEX q

JAMAICA

LOAN 2294-JM

PROJECT TIMETABLE

1tem Date Planned Date Revised Date Actual

Identification (Project Brief)

Preparation

Appraisal Mission

Loan Negotiations

Board Approval

Loan Signature

Loan Effectiveness

Final Date for Subproject g/ Submission

Loan Closing &/

a/ The final date for the submission of subloan authorization requests (presentation of subloan applications) was extended from December 31, 1985 to December 31, 1986 (on December 23, 1985) , to June 30, 1987 (on December 23, 1986) to March 31, 1989 (on January 6, 1989) to June 30, 1989 (on March 8, 1989).

b/ The Loan Closing Date was extended from December 31, 1987 to June 30, 1988 (January 1988) to December 31, 1988 (on July 19, 1988) and finally to December 31,1989 (on March 7, 1989). Further, in accordance with the current practice of the Bank regarding the Closing Date, disbursements were to be made for withdrawal applications received at the Bank by April 30, 1990 (via January 10, 1990 letter).

PART I11 ANNEX 3

PROJECT COMPLETION REPORT JAMAICA

INDUSTRIAL CREDIT PROJECT LOAN 2294

LOAN DISBURSEMENTS Cumulative Estimated and Actual Disbursements

SAR Estimate a/ Actual/ Actual/ Original Revised Actual Original Revised

!2/ E/ Estimate Estimate b/ -------- (US$ millions) -------- % %

December 31, 1983 June 30, 1984

December 31, 1984 June 30, 1985

December 31, 1985 8.5 4.6 June 30, 1986 11.8 7.6

December 31, 1986 14.1 11.6 June 30, 1987 14.9 14.6

December 31, 1987 15.1 15.1 June 30, 1988

December 31, 1988 June 30, 1989

December 31, 1989 June 30, 1990 July 31, 1990

Date of Final Disbursement: July 27, 1990

a/ Subloans committed are assumed to be disbursed 213 within the following year and 113 in the second year.

b/ Revised as of February 24, 1984. c/ Revised as of June 25, 1986. g / A loan amount of US$326,796 was canceled as of July 27, 1990.

PART I I L

STATUS OF COVENANTS

Section Subject Status

loan Aarecmenc

2.03(c) ALL subloan appl icat ions s h a l l be presented t o the Bar* by Decemkr 31, 1985.

F ina l date was extended t o t o March 31, 1989.

Interest and other charges sha l l be payable semi- amual ly on May 15 and Novenber 15 o f each year.

Conplied ( s a n e t i m with delay).

Borrouer sha l l repay the p r i nc ipa l amunt i n accordance wi th the amortization schedule.

Conplied (sometimes with delay).

Borrower sha l l relend the Loan proceeds t o MOB udcr subsidiary Loan agreement, sa t i s fac to ry t o the Bank.

Conpl id.

Borrower sha l l not assign. emend, abrogate or waive the Subsidiary Loan Agreement.

Conplied.

Borrower t o p rwen t MOB from incur r ing any exchange Losses resu l t ing from i t s barrowing oprat ions.

Borrower's indennif i ca t i on o f NOB1s exchange losses i s baing discussed between both part ies.

4.03t i i ) aJ Borrower s h a l l furnish t o the aank w i t h i n s i x m t h s a f t e r the end of each f i s c a l year audited repor t of the Special Account.

C a r p l i e d .

4.03( i i i ) g/ Borrower sha l l furnish t o the Bank monthly c e r t i f i e d statements of the Special Account.

Conplied.

Proiect Aareemenf

WOE t o annually review and rev ise ( i f necessary) the in terest rates i n consul tat ion wi th the Bank.

Conplied (differences betwen WOE and the Bank were reconciled)

Within s i x months fol lowing the Last withdraual frm the Loan Account in respect of the Subloans, NDB t o furn ish t o the Bank a pro jec t carp le t ion report .

Expected by Jme 12, lW2

NDB sha l l enploy management and investment consultants t o assist i t i n the car ry ing out of Part B of the Project.

Need f o r consultants d i d not a r i se dur ing project irrplementation.

NDB sha l l exchange views wi th the Bank p r i o r t o ongaging in any lending o r investment operat iom other than areking NDB loans.

Conpl i ed

NDB sha l l fu rn ish t o the Bank w i t h i n s i x months a f t a r the end o f each f i s c a l year audi ted finmncial statements and w d i t o r 8 s report.

Coaplied (socatimas with delay).

g/ Seetian 4.03 uas addd t o the Loen Agreement i n August/Novcnkr 1984. By ta lex t o NO0 dated February 28, 19L15, the B& srrggested t h a t the special account should ba audited by external auditors, acceptable t o the Bank, in the context of the o v e r r l l aud i t o t NDB8s eccants and statements.

PART I l I ANNEX 5

PROJECT COMPLETION REPORT JAMAICA

INDUSTRIAL CREDIT PROJECT LOAN 2294-JY

USE OF BANK RESOURCES

A. Staff Inputs (Staffweeks)

Stage of. Project Cycle Planned Revised Final Comments

Through appraieal - - 20.3 - Appraisal through Board Agproval

Board Approval through Effectiveneee

Supervieion

Total

a/ Relatee to FY88-FY91. b/ Relates to FY90 and FY91.

B. Missions

Staff Performance Stage of Project Month/ No. of Days Specialization Rating Types of

Cyc 1 l Year Persons i n F ie ld Represented Status g/ Problems bJ

Preparation 10/82 1 6 Dev. Finance

Appraisal 12/82 2 22 Dev. Finance

Appraisal through Board Approval

Board Approval through Effectiveness

8/83 3 1 Dev. Finance 1 None Legal

- . - v. 07i8S

V I . 06/86 V I I . 11/86

V111. 10/87 I X . 02/88

Dev. Finance 5 Dev. Finance

3 g/ n.a. 1 0 d Dev. FiMnce - 10 Dev. Finance 5 f/ DeV. Finance 4 f/ DeV. Finance

g/ K e y t o Status: 1. Problem-free or minor problem; 2. Moderate problems. K e y t o Problem: M - Mmogerial; T - TechnIcaL; P - Pol i t ica l ; 0 - Other. D w t o s u l t i p l e task assignnents, precise Information i s not available f roa TORS, Fom 590, etc.

$/ The raquired Back-to-Office end Fu l l Report are not available. p/ Refers t o Form 590 @tea as of 6/30/80, 6/30/89 a d 6/30/90.

In c o n j m c t i m with missions f o r ident i f icat ion a d preparation of proposed indust r ia l restructur ing project. n.a. - Form 590 o r a full sqerv is ion report i s not available.

. t

PART TI1 ANNEX 6 . 1

EKLJ ECT COHPLETJON REPORT

- -

YAlIOYAL DEVELOPMEYT EWC Of JMAICA LIMITED

s u b r o i c c t cost ~n re re . t - P r r l c d S h - Appl lcml lnn Each. Subloan Anvun~ l o tml Rate I n years

Ser ia l Proj. Approval ~ a t c Est. Actual note n .gas t rd Auth. Actual Flrurrinn (X p.m.) Repay- U * r of Yo. Yo. Y n o f S-ojmct Purpom* b l w - - - J$,OOO -.-- JS/USS (JS.000) ---(USt'WO)--- By Af l , amt w Grace # A f l 9

-Ag SUBPROJEClS

1. 0 ~ . o u i c a f l c x o p r ~ i c Lld. Ycu 03.07.84 2.460 3,321 3.15 1.707 542 461 2.322 16 6 2 l f n e

2. 1-02 E-Mart. Corp. L t d Yeu OI.08.84 4,541 4.762 3.3 2,595 363 529 16 7 (3) YCB 04.16.85 5,245 5.0 156 2.136 17 7 (3)

3. A-04 Mctml Box Co. L t d Rehab. 06.22.84 9,135 1,500 4.0 5,600 1.400 1,406 6,463 16 5 2 El0

4. 1-05 Corlbbcan Prod. Ltd. Rehmb. 10.05.M 11,067 12.500 4.0 6.01% 1.516 1,102 6,244 16 5 1 HSB

5. 1.06 Dalry I d s s t r l e s (JII) Ltd. Expon. 03.06.85 3.634 2,884 4.5 1,467 326 310 1,395 16 6 1 ClEC

6. 1-07 Project Conrul tontr Ltd. Rchab/Acqul. 01.17.86 6,231 4.980 4.0 1,200 300 235 3,762 16 6 (1.5) JCB

7. A-08 Joaalco Hotel Propcr t ic r ~chab. 06.04.86 20,555 60.115 5.1 4.125 17 10 2 YCB 750 683 C4.670

I 8. A-09 But tc rk ls t Lld. Rehab. 06.Ob.M 24,154 24,500 5.5 11.000 2,000 1.988 10.985 17 10 2 ENS

I- 9. 1 Clgmrettc to. of J I Ltd. mchob. 11.13.86 14,754 15,000 5.5 9,401 1.709 1.453 7.997 IS 0.5 1.7 SMS a

10. 8-13 Bloody Emy Dcv. Co. Ltd. Ycu 04.23.87 93.570 154.000 5.5 11,000 2,000 1,910 11.061 19 7 2 MSE~YCE I

11. 1-14 C i h y Yotcl Dev. Ltd. Ycr 12.07.87 70.514 95,000 5.5 6.075 1,725 1.&2 9,719 18 6 1 Em c/

12. 4-16 Ycqo r t n i l l r ~ t d . Eapmn. 09.29.89 6,665 6.665 5.5 4,070 591 573 ~.~ 16 7 2 JCE

-0- swPnoJrcrs

13. 8-02 Coxfullworth Ltd. Rchmb. 03.16.W 313 384 3.3 M - 1 O - M

4 . 1-01 Pa rqu t Spcc io l l s t Ltd. Ycu 03.16.84 1,135 1,342 3.6 720 200 209 1.031 16 7 3 YCE

5 8-05 Plmstlc L Metal l b r k s Ltd. Rehab. D4.26.M 922 1.200 3.6 650 180 179 983 16 6 1 JCE

16. 8-06 leach Vlcu Hotel Expan. 06.21 -64 3 14 253 4.2 17.5 4 1 37 156 16 4 1 CIBC

17. 1-07 Intl. +re1 Ltd. Yeu 07.25.M 1,627 1.650 4.3 686 160 160 954 16 5 1 YCB

18. I CL l u x G a r m t Mf9. CO. Ltd. Yeb~ 08.14.04 110 114 4.0 110 22 22 94 16 5.5 0.5 JCI

19. 1-09 J m l c a oryeen L Rehab. 10.26.84 1.271 1,361 4 .O Be0 220 220 880 16 4 1 BUS Accty lmc Ltd.

0 . 1-10 ~ o l y - r a k (JU) ~ t d . tapm. 12.04.84 468 512 4.5 140 31 32 170 17 5 1 Clnc

PROJECT COMPLETION REPORT ?I;AMAICS

JNDUSTRIAL CREDIT PROJECT LOAN 2 2 9 4 4 4

PART I11 ANNEX 6.1,

.----.

Subloan Te rm svkoroiec t Cost I n t e res t Per iod

s*- rppl i c a t i m Each. S d l o a n Aaant Total mate In years Se r i a l Pro j . Approval Data Est. ~ c t c u t ate ~ c q r r r t c d ~ u t h . ~ c t r u l f i m n c t n p ~ e p a y - W l r o t NO. YO. wmnr o f s w o j e c t Pwposc h m - - - JS.000 - - - - JS/USS (JS.000) - - - ( ~ $ * ~ ) - - - By AFI )I mt Grace d/ AFI CJ

8-12 H e t l f n Corp. Ltd. N e u

s-13 Usstern l y r e metreaders Ltd. Eapon.

0-15 Parodlre Deach Resort Ltd. Rehab.

J m i c a Shot Ltd.

Groce Food Processors Ltd.

Excel E n r m t Co. Ltd.

nn l t noon note l

n e l r l o a r furnishers Ltd.

Jamaica Oxygen Acetylene L td.

J-ica E l t r a c t s Ltd.

Highgate food P r o b c t s

sar is fmet ion SEU~ PrObCts

Poinciono 8each V i l l age

O.A.U. In ternat ial

J m i c a Carpet M i t t s Ltd.

Expan.

Rehab.

W eu

Rehab.

Expan.

Expm.

NCY

Expon.

W e u

Eapn.

Yew

Weu

a-31 Mnt' l C m t l m n t a l Gorp-Ltd. Ncu

GRAND TOTAL ("A" "8" S ~ r o j e c t t ) 1...............~........I.....I.I.

500

794

394

15.966

So ld

Uurned

3,624

403

1,121

3,191

1,213

2, n o

6,731

1,796

558

5,927

2Llzz

443,986

CNB

ENS

YC6

CNB

JCB

HSB

8NS

HSB

EMB

BUS

CT8

YCB

YC8

WS8

one

MS8

EMB

"1 ~ a c l u d i n g one-time 2 p r c m t loen o r i g i n u t i m tee. =. i n c l u d i ~ grace p r l d . C ~ B C C ~ C ~ i u i c a ~ td . ; IIYS lank o f nova sco t f a J u f c a ; cTB = C l t l b n k ; OM0 Oyo l l Merchant Bank; EM8 - Eagle Merchmt Bank; CUB - Century uatl-1 eank;

l n v c s t m t b Finnce Merchant Bank; JCO = Jam ice C i t i z w a Bank: m8 - Mutual S e e U i t v Bank; YCO Yati- l C-rcial Bmnk (JM); U L = Uwkers savings a Loan eurk. ( ) ~ x t m d r d Grace Period.

E m ~n r+ ica t im.

PART I11 ANNEX 6 . 2

MAlIQ1L DEW.LWWl1 #AUK 01 JLIUICA LIMIIID

t s p o r t ~

srb- I r r r r m ~ m In P r o b c t l m 11)

Srrlml p a ) . Do. lo . D n of I ~ o J . c t P r l r r1p . l p r ~ t ( . ) - - - - - - - - ~s.000 ..-..-.... Par lor-

1. 1.01 J u l c s I l * a q r l p l l c Ltd. L ~ l m l r d (Ir*nrpmr.nt) ( 4 R . m Ita) I 1 2 L O H ~ 1 I 0 - 14 Y, l O l M 04 IM 81- P u k l w l l a t r r l a l 1.925

2. A.02 1 . k r t m Corp. L t d

1. A-04 l l r t e l 10s Co. L l d l l e t * I Cans 10,100 I l o h r r 160x1 10.060 l l o h r r n l l n l l 18 60 Y 01/11 11/84 CIS

4. A - M Car l t&m ?rod. l t d . t d l b l a O l l r end la18 144.114 n1ph.r MI1 r l l nl l n l l 60. 60* Y m i a s 1 2 m mm

S. A-06 Dalrv I r d g t r l a * (YO Ltd. Ckrr. L #ut ter (6.846 t am) IICrr Ill lw 34 Y SO* 3 1 V w t a 7 11IBI ClBC 91.410

6. A-07 V r o l u t C a ~ ~ u l t n t . Ltd. r l a m l l c 1 1 1 ~ L (7,140.000 It01 I r r l n l d 1ags 11,011 I l o h r r 2.R1 5l.r 61 67 20 21 @l 0 4 l M l21M JCIlt lm h,

a. A -W 8utl.rklmt ~ td . mlacult* 26.400 Nlghrr to ox^ 26,400 It lohrr 51 41 12 11 Y m j a r WIM nus

9. 1-80 Clmeretta Ca. a1 II Lld. C l p ~ r * l t t a

lo. A-13 81- 81v 0.r. Co. Lad. ' l a u l s m

10,000 b Nlohrr 11.42? I l s h t r n l l n l l 10 12 Y 06/87 1 / 1 7 IUS

51.000 l i o h r r lIOOl)58.WO I lghc r 266 lM 16 24 Y l 2 l M 011W )rS#lrCI

11. 1-11 CI-1 lot.^ h v . ~ t d . IWIU n.sw 12. A- 16 S n g a t (1Ilt1 Lld. Ilv.mtock I r w h lu.110

Mlohrr IlOOX) TI.509 I l g h r r 150 4W l a 44 U 81/88 O l l W tm w nlohrr n l l nl I 14 16 22 44 U OIIW m!vo ~n

14. 8-01 r a r g r b Ipc la l l . 1 Ltd. Yoodn I lwr 111.m

1-r 1581) 2.360 I l ~ h r r 18 150 10 n C I 10184 10184 YCS

1s. 1.B P I m ~ l l c 8 k l m l York* Ltd. C a h w t syrt- 2.179 Iolr 4 I 1T 1w.r 1.400 V WIBI w i n JCI

1 - 8 I e m h VI*r Dotal lwr lu 2.850 L w t r ID Loutr 2.T- 10 10 ..A. 1 V u m/M Cl#C

17. 8-07 Inll. m r - 1 Lld. S.rmt* snm I l p h t r (1001) 1.TVO Il1gh.r IM 210 40 @I 01111 m/ms YCI

1. # a CI1-rn bnmt 111s. L.dler E a r m t s 1.440 C- momtructurd 410 11 101 . c/ 0 3 1 ~ - JCI Cb. Lld.

REPoRr

-%T PROJECT

a&- 5-r la l pro). lo. lo. r.r O( h b p l o j u t

Incramma In am. .I 4-

Capc tcd A c t u l

I - O I J m l r m Oanem I D a m n I 11 t rog rn 0.122 L r * t v l m Ltd. Cmaaa

1-10 Pol*-r.L (m) Ltd. P l a a t l r P u k a q l r r 4.V6

I l e h r r n l l

Y1sh.r n i l

n l I nll n l l 10 - u I t I I S - @US

n l l I I SO - d l 05/64 0(/U CIIC

I - 1 1 E u o t r d llig. Co. I r n l r a a K l t ch rn 2,140 l l@hrr I.6tV l o r 16 50 30. - &/ 12185 09181 CMI CDblnrt*

I - I 2 k l l l n Corp. Ltd. C.rmta 2.016 I 1 2 . 0 I I p h r r 1&t 150 50. - @I t W 5 - I n s

9-15 YIatmrn I v r a l m t r a d r a Ltd. Ietrmmdrd 1vr.a 1 . m ~ L a r n i l rill. 7 7 90 1.1. WI85 I Z I M hC9

0. I r a r d l s r I a u h I w l Ltd. lowla 10.1VI L w r r 11001) 10.197 L a v r I 10 110 41 Y O I I M 02181 CUl

1-16 J m l c a & Ltd. ~PO~IC.~. 5 . m (60x1 3.OW n l I 61 nm 42 1.1. O?IW JC8

1 Cru. load Procas.wa Ltd. Iulcma. Svrqm, 41.W 8.000 n l l n l l nm 30 70 1.1. 4 4 I M *SO Suraa, r t c .

9.18 Iuc * l car-t Co. Ltd. 6.-t. t.V60 Plant 1und D m l l001) 2.960 5s SO - e/ 071U #US

9 I a I f )(eon Yotr l larlu 40,9(4 I I g h r r (901) 56,850 l l g h r r n l l n l l 63 Y 18/81 11185 US9

1-21 I.lrl- I u n l m h r a Ltd. l u n l t u e Z.WO r l a n t m u d O m (121) 551 25 25 32 - e/ O?18? 111M €A

1-22 J m l c m 0 r n m L 0 a v w I I t I t r oe rn 1.024 l l p h r r (1001) t.024 n l l nll n l l 4> 41 0 2 8 O218? INS Awtv1o-m Lld. tmaaa

1-24 J m l c m t a t r r t a Ltd. 6 l r q . r 011 1.512 L w r r (1001) 3.112 lavr M 8 35 27 E/ 07/87 W l M CII

2 ~ l p k w t r food r r o b c t m C m l u t 1-rl ?,W6 Y I C r r (1001) 7.046 llqhrr 14 Y 69 - bl 4Al8? 1218? ICE

1-26 S . t lm iu t lm S m Probc ta -ta 18.240 [email protected] (1001)18.260 Y1sh.r 4W 545 44 9 l018? 06/8? I C I

1-27 ~ o l n c l r r # a r k VIIImer 1 a v l r 2.m I l p h r r Z.WU) 1l1ph.r 21 35 52 . W WI~? t018? RSB

1-28 0.A.I. I n t e r m t l a u l 5ervlcrID.t. Ent rv 2.421 Cloard Doul (1001) 1.421 mr 101 o n - P/ 0?187 9 D I O

3 Imtl- l C m t l m t m l Gorp. Ltd. C m i r c t l o u r y L l r r c k a 28.000 NIphrr (281) 1.640 Mlgher 12 32 42 15 41 OSlW O l l W E l l o

CIBC - CIIC J n l c m Ltd.; WS - Id o f lorm Scot la I r r l c m : CIB C I t I M ; W . O w l l k r c h m t Id; Ilu I Emsir M*rchml @ant : CUI - Crnturv e a t l a u l ld : l i l t@ - fnre.1-t L i lrvnc. )Ierch.#tt P d : Ja - J m l c a C l t l l a M; I(Y - h t u l Sacur l tv Id; 1U . Imtl- l C m r c l a l Id (a): YIL . Uorker. S.wlngs L L m Id. U m Id bt In r p d l c a t l a . At t l r 4 u 4 v e J - t -1mal. A c t w l Par(-@ h w bm bud a tha aaaaa.mt e l IIRD'm ProJrc t C o p l m t l m I l s a l m . Dm'. .tuff ard lor 1111' u r u g m m t . l h r c l m ~ . l i l c a t l m l a ma follar.: A/ C- m r a t l m pral l tmblv. P r o l u t I l b I v l a wh l sva rmt ta o i r a t v n r c h h l * r r Ih ~I's c u t . o i i r a te o i 121. V C u r t l y c- q m r l t l q prm(lt&lv, k t r l t h h la to rv 01 I n l l l a t d l f l l cu l t l " . Irtn a i r e t u r n r* I n rh. r a w * 01 hQI's cut .o i f rat.. g/ c w m t l y c- gall^^ a t a I r a . O a b t l u l rat. o f r a t u n mbwa m1'r c u t - e l l rat. rlll b. uhl.rrd. g l C- . p r a t l m b t r l w l m a w h u bm c l a d dm. l a tea e l rNwn arm ~ a t l v m . m . l n i r r t l a a p r o l l l . b l l l t ~ l a not avallabl*.

PISTRIBUTION BY AFT:

NO. OF SUBPROJ. -

BNS-Bank of Nova Scotia MSB-Mutual Set-Bank EMB-Eagle Merchant Bank NCB-Nat'l Comer.Bank CTB-Citibank JCB--Jamaica Citizena IFMB-1nv.fFin.Merch.Bank CIBC-CIBC Jamaica Ltd. CNB-Century Nat'l Bank WSL-Workera S&L Bank DMB-Dyoll Merchant Bank

TOTAL

PISTRIBUTION BY INDUSTRIAL SECTOR:

MANUFACTURING 2 8 OF WHICH: FOOD PROCESS. 10 GARMENT 5

AGRO-INDUSTRY 1 TOUR1 SM 7 SERVICES 1 --------- TOTAL 3 7

PROJECT COMPLETION REPORT JAMAICA

INDUSTRIAL CREDIT PROJECT LOAN 2294-Ja

DISTRIBUTION OF SUBPROJECTS

PART I11 ANNEX 6.3

TOTAL AVERAGE $ DISTRIBUTION SUBLOAN SUBLOAN NO. OF SUBLOAN &MOUNTS AMOUNTS SUBPROJ. AMOUNTS (US$~OOO) (US$ '000)

Component

p - 0

JBNAICA INDUSTRIAL CREDIT PROJECT

JOAN 2294-JM

PART I I1 AmIULGA

W i e c t Costs and Financinq (US$ Million)

F"nOJECT COSTS FINRNCING PLRN

Appraisal APPRAISAL ESTIMATE ACTUAL Estimates Actual IBRD NDB/AFIs and TOTAL I BRD NDBIAFIs and TOTAL

- Subborrowere Subborrowers

Credit Component 23.1 80.7 1/ 15.0 8.1 23.1 14.7 66.0 80.7 (Subproject Financing)

Technical Assistance 0.1 0.0 0.1 0.0 0.1 0.0 0.0 0.0

TOTAL 23.2 80.7 15.1 2/ 8.1 23.2 14.7 3/ 66.0 80.7

Cement e r The cost of the credit component shown in the Staff Appraisal Report represents an estimate of aggregate cost of subprojects yet to be identified; the actual cost of the credit component is the (estimated) aggregate cost of subprojects actually financed. Thus, the comparison of the two cost figures is not particularly meaningful in the case of thie project. Every U.S. dollar disbursed by IBRD was matched by a nearly six U.S.dollar equivalent of local resources contributed by NDB, AFIs and subborrowers to subprojects, as compared to 54 cents estimated at the time of appraisal. This was largely because three or four of the subprojects financed were large (in the tourism sector) and IBRD funding only represented a small portion of the costs.

1/ Estimated on the baeis of subproject data. J$ value was converted at the exchange rate of 5.5 because the bulk of Loan 2294-JH was disbursed during FY85-89.