working capital management report · in this context, the theme of our annual working capital...

TRANSCRIPT

Are you leaving cash on the table?Working capital management report

2018

Contents

Foreword ...................................................04

Executive summary ..................................06

Need for a focus on working capital .............08

Working capital overview for India ................10

Sector insights ............................................18

Impact of the Goods and Services Tax (GST) ..22

Working capital financing .............................24

Delivering working capital excellence.........26

Industry views ...........................................28

How we can help? .......................................30

Foreword

fficient working capital management is one of the fundamental elements for the financial and operational success of any business. Transformational value can be created by effectively combining the strengths of people, process and technology to improve the balance

between profitability and liquidity.

In current times, managing cash and liquidity effectively is imperative given the significant increase in non-performing assets and ballooning corporate balance sheets. Further, the recent implementation of the Goods and Service Tax (GST), technological advancements and alternative sources of debt-funding are providing companies and opportunity to rethink their approach towards resourcefully and most effectively managing their working capital.

In this context, the theme of our annual working capital management report this year is “Are you leaving cash on the table?” In this edition, we have analyzed the working capital performance of leading companies in India for FY17 and Q18. Based on our research, we have discovered and analyzed some of the key trends across industries and the potential opportunities for corporate India to release trapped cash from their working capital.

As per our findings, the overall cash-to-cash (C2C) deteriorated by 4% in FY17 vis-a-vis FY16 and payables are being stretched to fund working capital requirements. Also, Indian companies continue to have a longer C2C cycle compared to their global peers across a number of sectors. This presents corporate India with significant opportunities for working capital optimization. Our analysis shows that by adopting better working capital practices, India Inc. can release INR1.8 trillion of cash trapped in the corporate balance sheets.

We believe this report can benefit both industries and practitioners in their analysis and decision-making processes by providing the requisite insights into managing capital better. It is our endeavor to help contribute to Indian corporates release cash and support investments in growth.

Naveen TiwariPartner and Leader, Working Capital Advisory Services, EY India

E

There is a considerable need for Indian companies to focus on working capital optimization

Payables are being stretched in order to manage working capital

Timely payment to vendors can have a positive impact on margins due to improved supplier relationship (from discounts, rebates etc.)

Large firms have significantly more efficient working capital management as compared to the smaller firms

Sufficient cash on the table improves return on capital employed and credit profile, and increases cash availability for all stakeholders

In addition to better negotiating leverage, larger companies adopt better operating practices, which drive improved working capital

4 pp*Increase in C2C days in FY17 compared to FY16

5 daysIncrease in payables in FY16 as compared to FY14

54 daysDifference between the C2C of large and small firms

1.1 pp*Increase in short-term debt as a percentage of sales in FY17 as compared to FY16

Executive SummaryDeteriorated

Improved

*percentage point

Top 3 sectors with the highest C2C in FY17

GST can prove to be both a challenge and an opportunity to effectively manage working capital

Compared to other regions, there appears to be a significant scope of optimizing working capital for India Inc. by adopting efficient working capital practices

Managing the complexities and extracting maximum benefits from the working capital opportunities presented by the GST regime would be a key area of focus in the short-term

Executive Summary

Pharmaceuticals ChemicalsEngineering and

Engineering, Procurement, and Construction

(EPC) companies

Impact of GST on working capital performance:

Supply chain efficiencies

Timing of tax payments

Utilization of input credits

Difference in tax rates

Refund of export claims

Restriction on utilization of duty credit scrips

INR1.8trillion

Cash on the table!

The overall cash opportunity for India Inc.

Are you leaving cash on the table?

Need for a focus on working capital

1There is a considerable need for Indian companies to focus on working capital optimization.

9Working capital management report - 2017

While the overall free cash flow (FCF) has improved since 2014, it declined by about 20% (0.7ppts) between 2016 and 2017. This was combined with an increase in the C2C cycle over the same period.

In order to fund the increased cash needs, there has been a significant increase in short-term borrowings.

However, the ability of the firms to service the debt (interest coverage) has been steadily declining over the years.

There is a great need for the top management teams to focus on optimizing working capital. Having sufficient cash on the table provides numerous advantages:

• Better return on capital employed

• Reduce interest expense, thus increasing cash flow to shareholders

• Better credit profile

• Positive impact on margins due to improved supplier relationships (i.e. discounts from timely payments)

• Increased cash availability to fund growth initiatives (e.g. capex and acquisitions)

11.0%

9.6%

11.3%

12.4%

2014 2015 2016 2017

Short-term debt(% of sales)

3.6

3.1 3.1 3.1

2014 2015 2016 2017

Interest coverage ratio(EBIT/Interest expense)

-0.5%

2.2%

3.4%

2.7%

2014 2015 2016 2017

FCF(% of sales)

45

44

43

44

2014 2015 2016 2017

C2C (days)

Need to focus on working capital optimization

Are you leaving cash on the table?

Working capital overview for IndiaCash-to-cash (C2C) cycles for India inc. has deteriorated by 4% in FY17 cycle as compared to FY16.

2

11Working capital management report - 2017

India Working capital metrics

47

45

44

47

2014 2015 2016 2017

DIO DPO

4849

5453

2014 2015 2016 2017

DSO

46

48

53

51

2014 2015 2016 2017

45

44

43

44

2014 2015 2016 2017

C2C

Payables are being stretched in order to manage working capital While there have been year-on-year variations, the overall C2C cycle broadly remained stable between 2014 and 2017. However, on closer inspection, there was a significant deterioration in receivables, which was countered by an almost equivalent increase in payables.

It appears that companies in India find it easier to manage their cash needs by stretching payables rather than bringing in operational efficiencies across the board. In FY17, an increase in DPO (days payable outstanding) was observed in 14 out of

the top 25 sectors analyzed. Companies miss out not only on immediate opportunities such as early payment discounts but also on the opportunity to get further discounts from suppliers by using credit terms effectively.

Inventory levels have also increased in FY17 as compared to FY16. In addition to inefficiencies in the supply chain, inventory levels appear to have been impacted by the recent increase in underlying input prices (e.g. oil, steel, coal etc.).

Our analysis estimates that about INR1.8 trillion of cash is on the table for India Inc., to be released if companies were to adopt efficient working capital practices.

Are you leaving cash on the table?

38

47 44

53

77 75

57 55

92

80

67

55

0

10

20

30

40

50

60

70

80

90

100

C2C DSO DIO DPO

Day

s Top

Mid

Low

Note: Top: Top 166 companies by revenue in FY17

Mid: Top 167—332 companies by revenue in FY17

Low: Top 333—500 companies by revenue in FY17

Large firms have significantly more efficient working capital management as compared to smaller firmsOur analysis shows that the C2C for larger companies (top one-third by revenue) is significantly lower than for smaller companies (bottom one-third by revenue). Larger companies have better negotiating leverage and operating efficiencies, thus driving improved collections and relatively lower inventory levels.

The larger firms appear to be relatively well managed which means that in addition to having a better working capital performance, they also have better profitability and higher return on capital.

Performance comparison between large, mid-sized and small Indian companies

Top Mid Low

EBITDA margin 16% 14% 14%

PAT margin 7% 3% 2%

Interest coverage 3.6 1.8 1.5

ROCE 6% 3% 2%

WC comparison between large, mid-sized and small companies

13Working capital management report - 2017

There is a significant scope of optimizing working capital for India Inc. across certain sectors when compared with other regions

WC performance across geographies

India US Europe China Brazil

C2C 44 31 41 98 42

DSO 51 37 40 56 46

DIO 47 31 38 124 37

DPO 53 37 37 82 41

Working capital performance across geographies for top sectors

Compared to developed economies, Indian companies appear to have a longer C2C cycle, signifying opportunities to adapt better working capital practices, thus releasing trapped cash.

Specifically, significant working capital improvement potential exists across sectors including the engineering and EPC services, technology, chemicals and auto parts as compared to some of the other regions like the US, Europe etc.

Receivables for Indian engineering and EPC services companies were more than two times those of companies in the US, Europe and China. Delays in project execution combined with inadequate documentation have led to stretched receivables for Indian companies.

High DSO days for technology companies in India predominantly drive a longer C2C cycle compared to other developed regions.

Outstanding Government subsidies for fertilizer and agro-chemical manufacturers in India contribute to high DSO days for the chemicals sector.

Similarly, higher levels of inventory and faster vendor payments by Indian auto parts companies have driven higher working capital needs as compared to the US, Europe and China.

India

Europe

US

China

Brazil

Oil and gasMetals and

miningAutomobile

manufacturers Technology

C2C 19 49 -7 75 20 48 137 89 48 102

DSO 12 38 25 89 27 91 192 82 51 76

DIO 49 69 38 2 27 23 50 65 50 80

DPO 43 57 70 17 34 66 105 57 53 55

C2C 23 64 -2 48 69 33 54 62 41 81

DSO 37 33 24 61 35 49 86 49 55 63

DIO 23 60 28 5 58 26 3 53 42 43

DPO 37 30 54 17 25 43 35 40 56 25

C2C 38 68 15 67 81 23 57 56 32 119

DSO 35 30 22 88 29 52 71 30 61 94

DIO 31 70 47 23 88 13 40 50 36 64

DPO 28 31 54 44 36 41 54 24 64 39

C2C 17 16 -1 25 76 31 109 22 27 189

DSO 13 38 67 48 36 52 88 42 80 76

DIO 31 51 27 27 100 29 157 47 42 162

DPO 27 73 95 50 60 50 136 66 96 49

C2C 29 62 - 249 165 20 413 9 75 170

DSO 22 41 - 270 144 60 559 18 45 135

DIO 32 57 - 1 57 2 34 43 59 50

DPO 24 37 - 22 35 42 180 52 29 16

WC comparison across sectors and geographies

C2C 19 49 -7 75 20 48 137 89 48 102

DSO 12 38 25 89 27 91 192 82 51 76

DIO 49 69 38 2 27 23 50 65 50 80

DPO 43 57 70 17 34 66 105 57 53 55

C2C 23 64 -2 48 69 33 54 62 41 81

DSO 37 33 24 61 35 49 86 49 55 63

DIO 23 60 28 5 58 26 3 53 42 43

DPO 37 30 54 17 25 43 35 40 56 25

C2C 38 68 15 67 81 23 57 56 32 119

DSO 35 30 22 88 29 52 71 30 61 94

DIO 31 70 47 23 88 13 40 50 36 64

DPO 28 31 54 44 36 41 54 24 64 39

C2C 17 16 -1 25 76 31 109 22 27 189

DSO 13 38 67 48 36 52 88 42 80 76

DIO 31 51 27 27 100 29 157 47 42 162

DPO 27 73 95 50 60 50 136 66 96 49

C2C 29 62 - 249 165 20 413 9 75 170

DSO 22 41 - 270 144 60 559 18 45 135

DIO 32 57 - 1 57 2 34 43 59 50

DPO 24 37 - 22 35 42 180 52 29 16

Accessories and luxury

goodsUtilities

Engineering and EPC services

Auto partsChemicals Pharma-ceuticals

Are you leaving cash on the table?

31

49

41

58

27

49

41

63

C2C DSO DIO DPO

H1 FY17 H1 FY18

An analysis of the working capital metrics of the available data set in India (219 firms of the top 500 firms) as at 1H18 shows marginal improvement in working capital performance as compared to H1 FY17.

The C2C movement of the top companies between H1 FY17 and H1 FY18:

YTD working capital overview

Most of the sectors showed an improvement in C2C in H1 FY18

17Working capital management report - 2017

WC performance, H1-FY18

Sectors C2C H1 FY18 C2C change (vs. H1 FY17)

Metals and mining 27 -36%

Oil and gas (19) 75%

Automobile manufacturers 2 -588%

Technology 68 2%

Accessories and luxury goods 23 80%

Pharmaceuticals 109 6%

Engineering and EPC services 31 -19%

Telecommunications (78) 40%

Chemicals 69 -17%

Utilities (15) 147%

Auto parts 38 4%

Cement and building products 43 -9%

Distributors 36 -23%

Food producers 45 -14%

Textiles 92 0%

Electrical components and equipment 111 5%

Diversified industrial products 89 -6%

Media and entertainment 63 49%

Logistics and transportation 47 0%

Consumer products (non durable) 19 -44%

Retail 24 -24%

Consumer products (durable) 32 -8%

DeterioratedImproved

Are you leaving cash on the table?

Sector insightsC2C performance varies across sectors and is impacted by changes in government regulations, commodity price fluctuations and the changing business environment, in addition to the inherent inefficiencies in the system.

3

19Working capital management report - 2017

Working capital performance varied significantly across sectors in FY17. Many sectors recorded an improvement in working capital performance as compared to FY16 but many sectors operated at higher working capital levels as compared to FY14.

-7

19

20

48

48

49

75

89

102

137

-20 0 20 40 60 80 100 120 140

Automobile manufacturers

Oil and gas

Accessories and luxury goods

Auto parts

Utilities

Metals and mining

Technology

Chemicals

Pharmaceuticals

Engineering and EPC services

C2C (days)

There is a significant correlation between a change in working capital and a change in short-term debt used by companies. For instance, sectors such as oil and gas and metals and mining display a significant increase in C2C days with a corresponding increase in the short-term debt, signifying increased funding needs.

Working capital performance across sectors, FY17

Are you leaving cash on the table?

Change in C2C and short-term debt (FY17 vs. FY16), and free cash flow (% of FY17 sales)

Oil and gas

Metals and mining

Automobile manufacturers

Technology

Accessories and luxury Goods

Utilities

Engineering and EPC services

ChemicalsAuto parts

Pharmaceuticals

-15

-10

-5

0

5

10

15

20

-4% -2% 0% 2% 4% 6% 8%

Cha

nge

in C

2C d

ays

(vs.

FY1

6)

Change in short-term debt as a % sales (vs. FY16)

Oil and gas

Engineering and EPC service

Auto components

Metals and mining

Pharmaceuticals

Chemicals

Number of companies with improved/deteriorated WC w.r.t. FY16

Number of companies with improved/deteriorated working capital w.r.t. FY16

Number of companies with improved/deteriorated WC w.r.t. FY16

Number of companies with improved/deteriorated WC w.r.t. FY16

Number of companies with improved/deteriorated WC w.r.t. FY16

Number of companies with improved/deteriorated WC w.r.t. FY16

There was significant deterioration in C2C days between FY16 and FY17. This was mainly driven by an increase in DIO by 10 days, which appears to be due to the increase in underlying oil prices, thus impacting both inventory value and volume.

The overall C2C reduced in FY17 across the construction and engineering sector primarily due to improvement in inventory days. While the receivables days also decreased, receivables management continues to be a significant challenge for the sector. This sector continues to be troubled by project delays, liquidity crunch and inherent inefficiencies in the system, leading to a C2C cycle of over four months.

The auto components sector experienced a marginal improvement in C2C days in FY17 mainly due to an increase in payable days, which was partially offset by an increase in inventory days. A significant increase in key input commodity prices (steel, rubber, copper etc.) along with an increase in imports impacted the payables.

The metals and mining sector saw a deterioration in C2C in FY17 mainly due to an increase in the working capital of steel companies. This appears to have been driven by disruption in coke/coal imports impacting inventory values and payables.

The pharmaceuticals sector witnessed a large improvement in C2C days in FY17 as compared to FY16. While this is an improvement over FY16, the overall working capital performance is broadly in line with the average performance across FY14 and FY15. Some of the improvements in FY17 over FY16 were driven by companies engaging in factoring and bill discounting to reduce receivables.

The overall C2C days across the chemicals sector reduced in FY17 largely driven by a significant decrease in receivables. The fertilizers and agrochemicals and diversified chemical sectors demonstrated a reduction in DSO, which was partly driven by a reduction in outstanding subsidies.

2 10

15 19

17

19

23

17

17 12

25 28

310

3946

1912

4943

C2C DSO DIO DPO

4641

6458

4938

6957

C2C DSO DIO DPO

145

194

56

105137

192

50

105

C2C DSO DIO DPO

111

84 80

53

102

76 80

55

C2C DSO DIO DPO

50

52

48

50

48

5150

53

C2C DSO DIO DPO

95 88

62 55

89 8265

57

C2C DSO DIO DPO

DeterioratedImproved

Are you leaving cash on the table?

Impact of the Goods and Services TaxGST can prove to be both a challenge and an opportunity to effectively manage working capital.

4

23Working capital management report - 2017

Managing the complexities and extracting the maximum benefits from the working capital opportunities presented by the GST regime would be key areas of focus for businesses in the short-term.

The transition from the old tax structure to GST initially impacted the working capital cycle of companies.

Impact on supply chainThe implementation of a nationwide tax structure is expected to bring supply chain efficiencies such as network consolidation and manufacturing footprint rationalization, and enable free flow of goods across states. GST will present firms with an opportunity to not only optimize costs but to also have a lean supply chain with lower required inventory levels.

However, taxing stock transfers, though credit is available, has added extra working capital requirement considering the disposal cycle of the goods received via the stock transfer mode.

Impact on receivables and payablesWith the credit eligibility restricted to making payments within 180 days, firms would be required to optimize their procure-to-pay processes to optimally utilize the available input credit. On the other hand, firms’ suppliers would have to bring in process efficiencies to optimize invoicing processes and to take maximum advantage of this favorable regulation.

Impact due to refund of export claimsDue to system-related issues, there has been a delay in disbursement of export refund claims for exporters. This has caused a strain on working capital in the initial months of the GST implementation for firms with substantial exports.

Impact due to restriction on utilization of duty scripsDuty credit scrips issued under the Foreign Trade Policy are not allowed to be used for payment of GST in the current regime. This could also have an impact on working capital where there has been a reliance on duty scrips for the payment of the applicable taxes/duties in the earlier regime.

GST is a game-changing reform for the Indian economy. For businesses, GST has opened up avenues for efficiencies, reducing the cascading of taxes across the supply chain. A study of the working capital scenario could help the industry optimize the benefits of GST by undertaking relevant changes to mitigate negative impacts, if any.

—Suresh Nair Partner, Indirect Tax, EY India

In India, transitional credit in some cases has been delayed due to system-related glitches and lack of data readiness. Firms with strong working capital management are expected to tackle the short-term disruption better than firms with lesser focus on cash management.

GST impact

Impact on the timeline of tax paymentEarlier, there were different dates of cash outflow for various taxes levied such as excise duty, service tax and VAT. Under GST, the consolidated tax will have to be paid at once. On the one hand, firms will need to manage the cash flow to support the increased outflow at one go, while on the other hand, firms would be able to enjoy additional float for the amounts that they would have paid at multiple points in time in the earlier regime.

Impact of difference in tax ratesUnder the erstwhile tax regime, firms were required to pay a service tax of 15% on the procurement of services as against GST of 18% thereof under the current regime. The additional tax component would also contribute to an increased cash flow requirements of firms where there is a substantive procurement of services.

Similarly, where the effective rate on goods is higher under the GST regime as compared to the erstwhile regime, there could be a cash flow impact to the extent

Are you leaving cash on the table?

Working capital financingIn addition to operational efficiencies, CFOs are continuously exploring new ways of financing working capital needs.

5

25Working capital management report - 2017

All businesses need funds to run their operations. Traditionally, working capital funding has been arranged through banks using instruments such as overdrafts, cash credit and line of credit. Over the years, firms and banks have come up with new ways of working capital financing that are attractive and accessible to a wider set of companies.

There has been a significant increase in stressed assets(NPAs and restructured assets), which has led to a decline innew lending. Lending from banks to Indian corporationsdeclined by 5.2% in FY17 as compared to a growth of 2.8%in FY16, which has had an impact on both short and long-term financing*.

Alternative funding solutions such as corporate bonds andcommercial papers have emerged as short-term fundinginstruments. Consequently, as per RBI's annual report,the share of banks in credit decreased from 50% to 38% in FY17. Commercial papers are generally bought by mutual funds and as these are unsecured, funding through commercial papers is largely available to companies with a healthy credit rating. However, due to the impact of the recent monetary policy announcements, companies may have to pay a higher rate of interest for short-term borrowing through commercial papers.

*Source: 'We need a bank just for long-term credit” - C Rangarajanand S Sridhar, Published in the Business Line

Channel financing has been employed in India for quite some time as an alternate means of raising working capital finance for dealers and suppliers of firms. This provides the dealers and suppliers with a line of credit through their relationships with corporates (based on the corporate credit rating), which, on a standalone basis, would be difficult to obtain. For corporates, this helps mitigate the risk of short supplies or loss of sales due to a lack of funds in its supply chain.

The traditional approach to channel financing is changing. Fintech firms are developing technology platforms that are intended to help MSMEs sell their receivables at a discount, thus freeing up cash for operational needs. Such platforms and technologies are already well established in developed markets. Further, RBI has come up with Trade Receivables Discounting Systems (TReDS) which acts as an exchange for MSMEs to discount their invoices.

A few businesses are also currently experimenting with disruptive technologies such as blockchain to streamline the vendor payment processes.

Debt capital markets Supply chain financing

Are you leaving cash on the table?

Delivering workingcapital excellenceIncreasing use of analytics and technological advancesare assisting to drive working capital excellence.

6

27Working capital management report - 2017

Digitization:Implement an end-to-end integration application to eliminate manual processes

Automation in supply chain:Leverage upcoming advances such as drone technology in warehousing and logistics

A working capital optimization drive requires strategic and disciplined efforts from the leadership team and needs to be communicated to all work streams and business units. Technology plays a key role in driving working capital optimization in several ways, such as by providing real-time and clearer insights on the working capital position, enabling

better decision-making. Process improvements aimed at the lead time reduction, better customer engagement and improved vendor relations have a direct impact on reducing working capital. Last, but most importantly, when an organization decides to implement a working capital improvement program, people across functions should be pulling in the same direction with a strong internal leadership.

Customer engagement:Facilitate greater collaboration with customers, resulting in better payment terms and collection efficiencies.

Agile supply chain:Conduct robust sales and operations planning combined with flexible supply chain to meet dynamic demand requirements

Supplier management:Leverage “timely payments” as a tool to develop better supplier relationship and reduce sourcing costs

Enhanced role of finance:Move from a “transactional” approach to business partnering to help functions manage trade-offs between cost and cash

Cash culture:Embed a “cash culture” in the organization across functions

Organization structure:Establish adequate role definitions and clearly defined RACI

Management focus:Strike a balance between competing priorities and appropriate incentives for “cash” focus

Governance:Establish a robust governance structure, metrics and regular reporting

Robotic process automation(RPA):Use emerging technologies such as RPA for automating repetitive transactional processing

Analytics:Use big data to enhance control through improved visibility, and decision support

Process

System People

Selection of a funding mechanism for working capital may also have negative tax effects. In a multinational corporate environment, generally the infusion of working capital is done through a related party arrangement. This should be evaluated for the recent changes in the tax regime from the transfer pricing perspective regarding deduction of interest expense from the taxable income and consequently the higher effective tax rate.

Recent regulatory changes have made working capital management highly vulnerable. Another important aspect for working capital management within organizations is the efficient management of some hidden elements in working capital, for example, timely utilization of available input tax credits (indirect taxes) and MAT credits (direct tax). If not managed efficiently, at times these elements are large enough to make a dent in the profitability via higher interest costs on borrowed funds/loss of opportunity cost on own funds.

Indu

stry

in

sigh

ts

Sanjeev AgarwalHead of Finance of a major auto company

Working capital management is critical to any organization, whether in the past, current or future, since it has a direct impact on fund management, policies, discipline, interest cost and the overall profitability of the company.

Working capital management is a controllable factor and is the lifeline for any organization. It requires complete focus by all in the organization. The key factors in our sector (electronics retail) are inventory and receivables. As we are growing, we are trying to ensure that our trade partners also focus on efficient working capital management to achieve higher turnover and rotation of funds.

We try to arrange funds at competitive rates under the ‘channel finance’ program of banks and NBFCs for our trade partners to match our growth. For efficient working capital management, many controls are centralized in spite of decentralized branch operations. We continue to focus on our credit rating to ensure adequate facilities at competitive rates.

Post GST implementation, there was some initial impact on cash flow due to IGST on imports and stock transfer, but it should streamline in a few months.

Working capital management has become more critical than ever before for us. The telecom sector has seen more than its fair share of turmoil and consolidation resulting in cash becoming king more than ever before. Debtors and inventory of fixed assets are the critical components in our sector (telecom tower) that impact working capital within any telecom firm. The key strategies employed by management to optimize working capital are mainly around engaging with customers to ensure prompt payments, having a hard look at inventory norms, aging of inventory and pulling back of the same.

In the future, working capital requirements will influence many decisions, including new projects. To get working capital financing, it is easy for well-rated firms as there is more money chasing fewer good assets. Things have become more difficult for corporates/firms which may not have good ratings. Working capital management has become more challenging than ever. Demonetization did have an impact on working capital of many firms and the jury is still out if all of the impact is behind us or not. However, GST will have a permanent impact as corporates/firms will not be able to take credit of taxes if matching has failed. They will also then need to engage with their partners to ensure that the GSTN portal is corrected before the corporate/firm can take credit.Sanjay Bhargava

Director, CFO and Company Secretary, Sony India

Hemant Kumar RuiaCFO, Indus Towers

EY’s India team of dedicated working capital professionals can help you identify, evaluate and prioritize realizable improvements to liberate significant cash tied up in working capital.

We assist organizations in their transition to a cash-focused culture and help implement the relevant metrics to prioritize focus on working capital. We also identify areas for improvement in cash flow forecasting practices and assist in implementing processes to improve forecasting and frameworks to sustain those improvements. In addition to increased levels of cash, implementation of working capital improvement initiatives results in significant economic benefits from productivity improvements, reduced transactional and operational costs, lower levels of bad and doubtful debts, and reduced inventory obsolescence.

How we can

help

Order to cash (OTC)

Forecast to fulfil (FTF)

Procure to pay (PTP)

People and organization

Systems and tools

Process and practice

Sales mgmt.

Contractual terms

Supplier rationalization

Demand forecasting

Order processing

Goods and invoice receipt

Supplier mgmt.

Collections strategies

Supplier terms

Credit risk mgmt.

Purchase request and order fulfilment

Planning, purchasing and replenishment

Invoice processing

Invoice processing

Order processing and distribution

Dispute resolution

Sourcing and contracting

Customer service and inventory levels

Cash application

Payment processing

Product range mgmt.

Procure -ment planning

Cash flow management

• 13-week rolling cash forecast

• Cash flow budgeting and planning

• ►Managing day-to-day cash flow operations

• ►Finance function effectiveness

EY’s working capital optimization framework

MethodologyThe report contains findings of an analysis of the working capital performance of the leading 500 companies (by sales of FY17) headquartered in India. All the data points have been sourced from S&P Capital IQ. This analysis excludes sectors such as financial institutions, infrastructure and real estate corporations, and companies that were listed after FY14 (as their data for historical comparison was not available).

Our overall analysis draws on companies’ latest fiscal 2017 reports and compares performance in 2017 with that in 2016 and in some instances with that of a further three previous years.

The analysis is segmented by country, sector and company. It uses metrics to provide a clear picture of overall working capital management and to identify resultant levels of cash opportunity. The analyzed numbers have been calculated on a sales-weighted basis. Each of the companies analyzed in this research has been allocated to an industry.

The opportunity of cash release through working capital optimization has been computed by comparing the C2C days of a company with the average C2C days for its sector. The total cash release opportunity highlighted in this report is the sum of potential cash release opportunities for companies were they to operate at their respective sector C2C averages.

Glossary• Days sales outstanding (DSO): year-end trade receivables divided by full-year sales

and multiplied by 365 (expressed as the number of days of sales, unless stated otherwise)

• Days inventory outstanding (DIO): year-end inventories divided by full-year sales and multiplied by 365 (expressed as the number of days of sales, unless stated otherwise)

• Days payable outstanding (DPO): year-end trade payables divided by full-year sales and multiplied by 365 (expressed as the number of days of sales, unless stated otherwise)

• Cash-to-cash (C2C): equals DSO plus DIO minus DPO (expressed as the number of days of sales, unless stated otherwise)

• Percentage of EBITDA/sales: EBITDA (earnings before interest, tax, depreciation and amortization) divided by full-year sales (expressed in percentage)

• Return on capital employed (ROCE): full year PAT (Profit after tax), divided by year-end capital employed (sum of total equity and debt), expressed in percentage

• O&G: oil and gas

• M&M: metal and mining

• IT: information technology

• WC: working capital

• TWC: trade working capital

C2C DSO DIO DPO

Sector Q1 Median Q3 Q1 Median Q3 Q1 Median Q3 Q1 Median Q3

Oil and gas 11 21 37 9 19 24 35 40 54 21 28 59

Metals and mining

32 61 114 29 42 73 43 70 95 29 44 78

Automobile manufacturers

-12 -8 -4 16 20 27 13 26 37 42 51 65

Technology 57 72 87 72 88 106 0 0 5 7 16 32

Accessories and luxury goods

64 112 151 7 33 72 72 115 143 23 38 83

Utilities 18 71 111 52 88 136 5 15 26 21 26 88

Engineering and EPC services

73 120 179 81 144 244 16 52 112 64 104 139

Chemicals 52 74 105 47 61 86 41 61 75 35 45 66

Auto parts 28 45 68 38 51 68 34 48 61 42 53 60

Pharmaceuticals 72 101 113 59 77 91 63 77 91 37 51 62

Tele- communications

-41 -24 -14 26 42 59 0 1 2 56 75 86

Cement and building products

17 42 66 21 37 69 35 41 53 31 41 52

Food producers 17 50 113 13 28 38 31 50 154 23 31 43

Distributors 32 36 67 45 68 113 10 21 30 29 42 71

Diversified industrial products

33 62 137 56 66 107 35 54 77 44 59 80

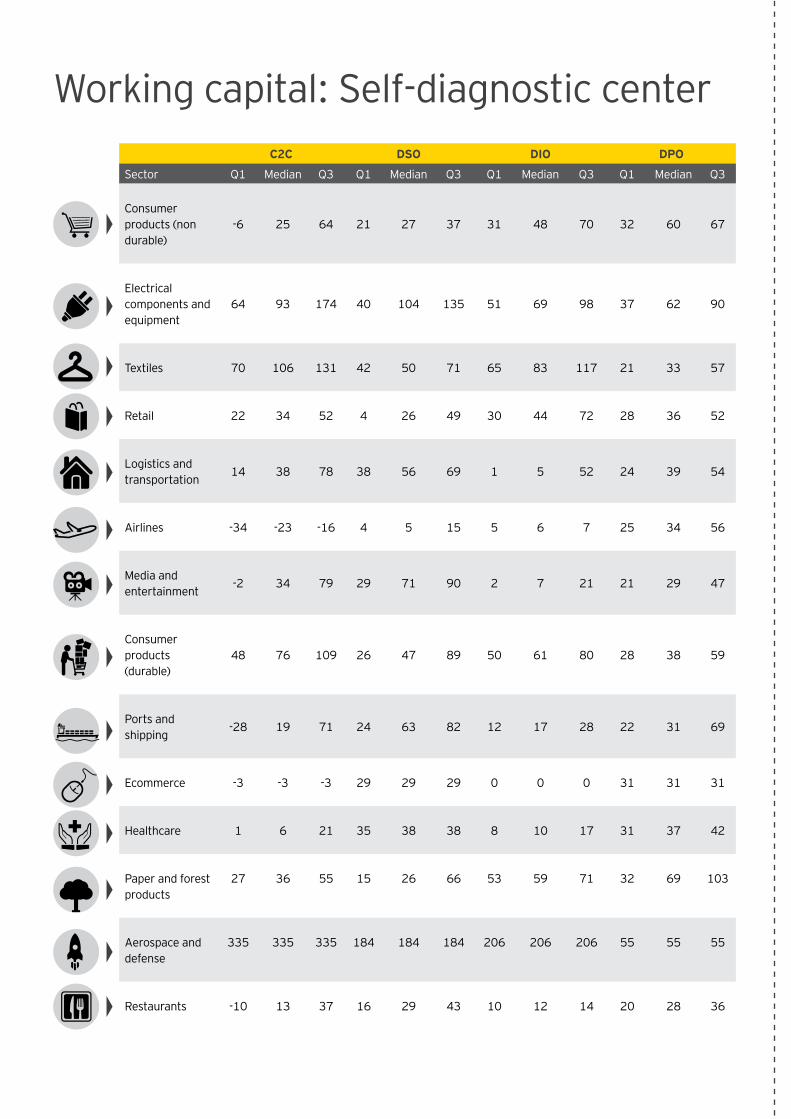

Working capital: Self-diagnostic center

C2C DSO DIO DPO

Sector Q1 Median Q3 Q1 Median Q3 Q1 Median Q3 Q1 Median Q3

Consumer products (non durable)

-6 25 64 21 27 37 31 48 70 32 60 67

Electrical components and equipment

64 93 174 40 104 135 51 69 98 37 62 90

Textiles 70 106 131 42 50 71 65 83 117 21 33 57

Retail 22 34 52 4 26 49 30 44 72 28 36 52

Logistics and transportation

14 38 78 38 56 69 1 5 52 24 39 54

Airlines -34 -23 -16 4 5 15 5 6 7 25 34 56

Media and entertainment

-2 34 79 29 71 90 2 7 21 21 29 47

Consumer products (durable)

48 76 109 26 47 89 50 61 80 28 38 59

Ports and shipping

-28 19 71 24 63 82 12 17 28 22 31 69

Ecommerce -3 -3 -3 29 29 29 0 0 0 31 31 31

Healthcare 1 6 21 35 38 38 8 10 17 31 37 42

Paper and forest products

27 36 55 15 26 66 53 59 71 32 69 103

Aerospace and defense

335 335 335 184 184 184 206 206 206 55 55 55

Restaurants -10 13 37 16 29 43 10 12 14 20 28 36

Working capital: Self-diagnostic center

EY officesAhmedabad

2nd floor, Shivalik IshaanNear C.N. VidhyalayaAmbawadiAhmedabad - 380 015Tel: + 91 79 6608 3800Fax: + 91 79 6608 3900

Bengaluru

6th, 12th & 13th floor“UB City”, Canberra BlockNo.24 Vittal Mallya RoadBengaluru - 560 001Tel: + 91 80 4027 5000 + 91 80 6727 5000 + 91 80 2224 0696Fax: + 91 80 2210 6000

Ground Floor, ‘A’ wingDivyasree Chambers# 11, O’Shaughnessy RoadLangford GardensBengaluru - 560 025Tel: +91 80 6727 5000Fax: +91 80 2222 9914

Chandigarh

1st Floor, SCO: 166-167Sector 9-C, Madhya MargChandigarh - 160 009 Tel. +91 172 331 7800Fax: +91 172 331 7888

Chennai

Tidel Park, 6th & 7th Floor A Block (Module 601,701-702)No.4, Rajiv Gandhi Salai Taramani, Chennai - 600 113Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120

Delhi NCR

Golf View Corporate Tower BSector 42, Sector RoadGurgaon - 122 002Tel: + 91 124 464 4000Fax: + 91 124 464 4050

3rd & 6th Floor, Worldmark-1IGI Airport Hospitality DistrictAerocity, New Delhi - 110 037Tel: + 91 11 6671 8000Fax + 91 11 6671 9999

4th & 5th Floor, Plot No 2B Tower 2, Sector 126 NOIDA - 201 304Gautam Budh Nagar, U.P.Tel: + 91 120 671 7000Fax: + 91 120 671 7171

Hyderabad

Oval Office, 18, iLabs CentreHitech City, MadhapurHyderabad - 500 081Tel: + 91 40 6736 2000Fax: + 91 40 6736 2200

Jamshedpur

1st Floor, Shantiniketan BuildingHolding No. 1, SB Shop AreaBistupur, Jamshedpur – 831 001Tel: +91 657 663 1000BSNL: +91 657 223 0441

Kochi

9th Floor, ABAD NucleusNH-49, Maradu POKochi - 682 304Tel: + 91 484 304 4000Fax: + 91 484 270 5393

Kolkata

22 Camac Street3rd Floor, Block ‘C’Kolkata - 700 016Tel: + 91 33 6615 3400Fax: + 91 33 2281 7750

Mumbai

14th Floor, The Ruby29 Senapati Bapat MargDadar (W), Mumbai - 400 028Tel: + 91 22 6192 0000Fax: + 91 22 6192 1000

5th Floor, Block B-2Nirlon Knowledge ParkOff. Western Express HighwayGoregaon (E)Mumbai - 400 063Tel: + 91 22 6192 0000Fax: + 91 22 6192 3000

Pune

C-401, 4th floorPanchshil Tech ParkYerwada (Near Don Bosco School)Pune - 411 006Tel: + 91 20 6603 6000Fax: + 91 20 6601 5900

For further information, please contact

Naveen Tiwari Partner Working Capital Advisory Services, EY T: + 91 22 6192 0550 E: [email protected]

Bhavin Shah Senior Manager Working Capital Advisory Services, EY T: + 91 22 61923595 E: [email protected]

Sushant Chaturvedi Manager Working Capital Advisory Services, EY T: +91 22 6192 2423 E: [email protected]

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

© 2018 Ernst & Young LLP. Published in India. All Rights Reserved.

EYIN1802-015 ED None

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

VN

Ernst & Young LLPEY | Assurance | Tax | Transactions | Advisory

ey_indiacareers

ey.com/in

EY India@EY_India EY|LinkedIn EY India careers