witholding tax to vat notes

TRANSCRIPT

Description-Withholding Tax on Compensation is the tax withheld from income payments to individuals arising from an employer-employee relationship.

- Expanded Withholding Tax is a kind of withholding tax which is prescribed on certain income payments and is creditable against the income tax due of the payee for the taxable quarter/year in which the particular income was earned.

- Final Withholding Tax is a kind of withholding tax which is prescribed on certain income payments and is not creditable against the income tax due of the payee on other income subject to regular rates of tax for the taxable year. Income Tax withheld constitutes the full and final payment of the Income Tax due from the payee on the particular income subjected to final withholding tax.

-Withholding Tax on Government Money Payments (GMP) - Percentage Taxes - is the tax withheld by National Government Agencies (NGAs) and instrumentalities, including government-owned and controlled corporations (GOCCs) and local government units (LGUs), before making any payments to non-VAT registered taxpayers/suppliers/payees

-Withholding Tax on GMP - Value Added Taxes (GVAT) - is the tax withheld by NationalGovernment Agencies (NGAs) and instrumentalities, including government-owned and controlled corporations (GOCCs) and local government units (LGUs), before making any payments to VAT registered taxpayers/suppliers/payees on account of their purchases of goods and services.

Codal ReferenceRepublic Act Nos. 8424, 9337, 9442, 9504Sections 57 to 58 and 78 to 83 of the National Internal Revenue Code (NIRC)

Frequently Asked Questions

1) What are the types of Withholding Taxes?

There are two main classifications or types of withholding tax. These are:

a) Creditable Withholding Tax - Withholding Tax on Compensation - Expanded Withholding Tax - Withholding of Business Tax (VAT and Percentage)b) Final Withholding Taxc. Withholding Tax on Government Money Payments

- Withholding Tax on Vat- Withholding Tax on Percentage Taxes

2) What is compensation?

It means any remuneration received for services performed by an employee from his employer under an employee-employer relationship.

3) What are the different kinds of compensation?

a) Regular compensation - includes basic salary, fixed allowances for representation, transportation and others paid to an employeeb) Supplemental compensation - includes payments to an employee in addition to the regular compensation such as but not limited to the following:- Overtime Pay- Fees, including director's fees- Commission- Profit Sharing- Monetized Vacation and Sick Leave- Fringe benefits received by rank & file employees- Hazard Pay- Taxable 13th month pay and other benefits- Other remunerations received from an employee-employer relationship

4) What are exempted from Withholding Tax on Compensation?

1. Remuneration as an incident of employment, such as follows: a. Retirement benefits received under RA 7641 b. Any amount received by an official or employee or by his heirs from the employer due to death, sickness or other physical disability or for any cause beyond the control of the said official or employee such as retrenchment, redundancy or cessation of business c. Social security benefits, retirement gratuities, pensions and other similar benefits d. Payment of benefits due or to become due to any person residing in the Philippines under the law of the US administered US Veterans Administration e. Payment of benefits made under the SSS Act of 1954, as amended f. Benefits received from the GSIS Act of 1937, as amended, and the retirement gratuity received by the government employee2. Remuneration paid for agricultural labor3. Remuneration for domestic services4. Remuneration for casual labor not in the course of an employer's trade or business5. Compensation for services by a citizen or resident of the Philippines for a foreign government or an international organization6. Payment for damages7. Proceeds of Life Insurance8. Amount received by the insured as a return of premium

9. Compensation for injuries or sickness10. Income exempt under Treaty11. Thirteenth (13th) month pay and other benefits (not to exceed P 30,000)12. GSIS, SSS, Medicare and other contributions

13. Compensation Income of Minimum Wage Earners (MWEs) with respect to their Statutory Minimum Wage (SMW) as fixed by Regional Tripartite Wage and Productivity Board (RTWPB)/National Wage and Productivity Commission (NWPC), including overtime pay, holiday pay, night shift differential and hazard pay, applicable to the place where he/she is assigned.

14. Compensation Income of employees in the public sector if the same is equivalent to or not more than the SMW in the non-agricultural sector, as fixed by RTWPB/NWPC, including overtime pay, holiday pay, night shift differential and hazard pay, applicable to the place where he/she is assigned.

5) What are De Minimis Benefits?

-These are facilities and privileges of relatively small value and are offered or furnished by the employer to his employees merely as means of promoting their health, goodwill, contentment or efficiency. The following shall be considered "De Minimis" benefits not subject to income tax, hence not subject to withholding tax on compensation income of both managerial and rank and file employees:

v Monetized unused vacation leave credits of private employees not exceeding ten (10) days during the year;

v Monetized value of vacation and sick leave credits paid to government officials and employees.

v Medical cash allowance to dependents of employees, not exceeding P750.00 per employee per semester or P125.00 per month;

v Rice subsidy of P1,500 or one (1) sack of 50 kg. rice per month amounting to not more than P1,500;

v Uniform and clothing allowance not exceeding P4,000 per annum;

v Actual medical assistance, e.g. medical allowance to cover medical and healthcare needs, annual medical/executive check-up, maternity assistance, and routine consultations, not exceeding P10,000 per annum;

v Laundry allowance not exceeding P300.00 per month;

v Employees achievement awards, e.g., for lenght of service or safety achievement, which must be in the form of a tangible personal property other than cash or gift certificate, with an annual monetary value not exceeding P10,000 received by the employee under an established written plan which does not discriminate in favor of highly paid employees;

v Gifts given during Christmas and major anniversary celebration not exceeding P5,000.00 per employee per annum;

v Daily meal allowance for overtime work and night/graveyard shift not exceeding twenty-five percent (25%) of the basic minimum wage on a per region basis;

6) What is substituted Filing of income tax returns (ITR)?

Substituted Filing of ITR is the manner by which declaration of income of individuals receiving purely compensation income which have been withheld by their employers the correct tax due, is no longer required.Instead of the filing of Individual Income Tax Return (BIF Form 1700) , the employer’s annual information return (BIR Form No. 1604-CF) duly stamped received by the BIR may be considered as the “substitute” Income Tax Return (ITR) of the employee, inasmuch as the information provided therein are exactly the same information required to be provided in his income tax return (BIR Form No. 1700).

7) Who are qualified to avail the substituted filing?

Employees who satisfies all of the following conditions:a. Receiving purely compensation income regardless of amount;b. Working for only one employer in the Philippines for the calendar year;c. Withholding tax has been withheld correctly by the employer (tax due equals tax withheld);d. The employee’s spouse also complies with all three (3) conditions stated above.e. The employer files the annual information return (BIR Form No. 1604-CF)f. The employer issues BIR Form 2316 to each employee.

8) What income payments are subject to Expanded Withholding Tax?

a) Professional fees / talent fees for services rendered by the following:

- Those individually engaged in the practice of profession or callings such as lawyers,certified public accountants, doctors of medicine, architecs, engineers and all other professionals who have undergone licensure examinations regulated by the Professional Regulations Commission, Supreme Court, etc. - Professional entertainers such as but not limited to actors and actresses, singers, lyricist, composers and emcees- Professional athletes including basketball players, pelotaris and jockeys- Directors and producers involved in movies, stage, radio, television and musical

productions- Insurance agents and insurance adjusters- Management and technical consultants- Bookkeeping agents and agencies- Other recipient of talent fees- Fees of directors who are not employees of the company paying such fees whose duties are confined to attendance at and participation in the meetings of the Board of Directorsb) Professional fees, talent fees, etc for services of taxable juridical personsc) Rentals: -Rental of real property used in business -Rental of personal properties in excess of P 10,000 annually -Rental of poles, satellites and transmission facilities -Rental of billboardsd) Cinematographic film rentals and other paymentse) Income payments to certain contractors- General engineering contractors- General building contractors- Specialty contractors- Other contractors like: 1. Filling, demolition and salvage work contractors and operators of mine drilling apparatus 2. Operators of dockyards 3. Persons engaged in the installation of water system, and gas or electric light, heat or power 4. Operators of stevedoring, warehousing or forwarding establishments 5. Transportation Contractors 6. Printers, bookbinders, lithographers and publishers, except those principally engaged in the publication or printing of any newspaper, magazine, review or bulletin which appears at regular intervals, with fixed prices for subscription and sale 7. Advertising agencies, exclusive of payments to media 8. Messengerial, janitorial, security, private detective, credit and/or collection agencies and other business agencies 9. Independent producers of television, radio and stage performances or shows 10. Independent producers of "jingles" 11. Labor recruiting agencies and/or “labor-only” contractors 12. Persons engaged in the installation of elevators, central air conditioning units, computer machines and other equipment and machineries and the maintenance services thereon 13. Persons engaged in the sale of computer services, computer programmers, software developer/designer, etc. 14. Persons engaged in landscaping services 15. Persons engaged in the collection and disposal of garbage 16. TV and radio station operators on sale of TV and radio airtime, and 17. TV and radio blocktimers on sale of TV and radio commercial spotsf) Income distribution to the beneficiaries of estates and trustsg) Gross commission or service fees of customs, insurance, stock, real estate, immigration and commercial brokers and fees of agents of professional entertainers

h) Income payments to partners of general professional partnershipsi) Payments made to medical practitioners j) Gross selling price or total amount of consideration or its equivalent paid to the seller/owner for the sale, exchange or transfer of real property classified as ordinary assetk) Additional income payments to government personnel from importers, shipping and airline companies or their agents l) Certain income payments made by credit card companies m) Income payments made by the top 20,000 private corporations to their purchase of goods and services from their local/resident suppliers other than those covered by other rates of withholding n) Income payments by government offices on their purchase of goods and services, from local/resident suppliers other than those covered by other rates of withholding o) Commission, rebates, discounts and other similar considerations paid/granted to independent and exclusive distributors, medical/technical and sales representatives and marketing agents and sub-agents of multi level marketing companies. p) Tolling fees paid to refineriesq) Payments made by pre-need companies to funeral parlorsr) Payments made to embalmers by funeral parlorss) Income payments made to suppliers of agricultural products (suspension not yet lifted)t) Income payments on purchases of mineral, mineral products and quarry resourcesu) On gross amount of refund given by MERALCO to customers with active contracts as classified by MERALCO;v) Interest income on the refund paid through direct payment or application against customers' billing by other electric Distribution Utilities in accordance with the rules embodied in ERC Resolution No. 8 series of 2008 dated June 4, 2008 governing the refund of meter deposits which was approved and adopted by ERC in compliance with the mandate of Article 8 of the Magna Carta for Residential Electricity Consumers and Article 3.4.2 of DSOAR exempting all electricity consumers, whether residential or non-residential from the payment of meter deposit.w) Income payments made by the top 5,000 individual taxpayers to their purchase of goods and services from their local/resident suppliers other than those covered by other rates of withholdingx) Income payments made by political parties and candidates of local and national elections of all their campaign expenditures, and income payments made by individuals or juridical persons for their purchases of goods and services intended to be given as campaign contribution to political parties and candidates

9) What income payments are subject to Final Withholding Tax?

a) Income Payments to a Citizen or to a Resident Alien Individual:- Interest on any peso bank deposit- Royalties - Prizes [except prizes amounting to P10,000 or less which is subject to tax under Sec. 24(A)(1) of the Tax Code]- Winnings (except winnings from Philippine Charity Sweepstake Office and Lotto)

- Interest income on foreign currency deposit- Interest income from long term deposit (except those with term of five years or more)- Cash and/or property dividends- Capital Gains presumed to have been realized from the sale, exchange or other disposition of real property

b) Income Payments to a Non-Resident Alien Engaged in Trade or Business in the Philippines- On Certain Passive Income - cash and/or property dividend - Share in the distributable net income of a partnership- Interest on any bank deposits- Royalties- Prizes (except prizes amounting to P10,000 or less which is subject to tax under Sec. 25(A)(1) of the Tax Code.- Winnings (except from Philippine Charity Sweepstake Office and Lotto)- Interest on Long Term Deposits (except those with term of five years or more)- Capital Gains presumed to have been realized from the sale, exchange or other disposition of real property

c) Income Derived from All Sources Within the Philippines by a Non-Resident Alien Individual Not Engaged in Trade or Business - On gross amount of income derived from all sources within the Philippines- On Capital Gains presumed to have been realized from the sale, exchange or disposition of real property located in the Philippines

d) Income Derived by Alien Individual Employed by a Regional or Area Headquarters and Regional Operating Headquarters of Multinational Companies, Income Derived by Alien Individual Employed by Offshore Banking Units and Income of Aliens Employed by Foreign Petroleum Service Contractors and Subcontractors

e) Income Payment to a Domestic Corporation- Interest from any currency bank deposits and yield or any other monetary benefit from deposit substitutes and from trust fund and similar arrangements derived from sources within the Philippines- Royalties derived from sources within the Philippines- Interest income derived from a depository bank under the Expanded Foreign Currency Deposit (FCDU) System- Income derived by a depository bank under the FCDU from foreign transactions with local commercial banks- On capital gains presumed to have been realized from the sale, exchange or other disposition of real property located in the Philippines classified as capital assets, including pacto de retro sales and other forms of conditional sales based on the gross selling price or fair market value as determined in accordance with Sec. 6(E) of the NIRC, whichever is higher

f) Income Payments to a Resident Foreign Corporation- Offshore Banking Units- Tax on branch Profit Remittances- Interest on any currency bank deposits and yield or any other monetary benefit from deposit substitute and from trust funds and similar arrangements and royalties derived from sources within the Philippines- Interest income on FCDU- Income derived by a depository bank under the expanded foreign currency deposits system from foreign currency transactions with local commercial banks

g) Income Derived from all Sources Within the Philippines by a Non-Resident Foreign Corporation- Gross income from all sources within the Philippines such as interest, dividends, rents, royalties, salaries, premiums (except re-insurance premiums), annuities, emoluments or other fixed determinable annual, periodic or casual gains, profits and income or capital gains;- Gross income from all sources within the Philippines derived by a non-resident cinematographic film owner, lessor and distributor- On the gross rentals, lease and charter fees derived by a non-resident owner or lessor of vessels from leases or charters to Filipino citizens or corporations as approved by the Maritime Industry Authority- On the gross rentals, charter and other fees derived by a non-resident lessor of aircraft, machineries and other equipment- Interest on foreign loans contracted on or after August 1, 1986

h) Fringe Benefits Granted to the Employee (except Rank and File)- Goods, services or other benefits furnished or granted in cash or in kind by an employer to an individual employee (except rank and file) such as but not limited to the following:- Housing- Vehicle of any kind- Interest on loans- Expenses for foreign travel- Holiday and vacation expenses- Educational assistance to employees or his dependents- Membership fees, dues and other expense in social and athletic clubs or other - similar organizations- Health insurance

i) Informers Reward

10) Aside from the required withholding of income tax by government agencies and instrumentalities on their payments to their suppliers of goods and services, what other tax types must be withheld by them?

a) Value Added Tax – on all payments subject to VAT - On gross payments for the purchase of goods - On gross payments for the purchase of services

b) VAT – on payments for lease or use of properties or property rights to non-resident owners; and other services rendered in the Philippines by non-residents.

c) Percentage Tax – on all payments subject to percentage tax such as payments to the following: - Any person engaged in business whose gross sales or receipts do not exceed P1,500,000 and who are not VAT-registered persons. (Persons exempt from VAT under Sec. 109V of the Tax Code) - Domestic carriers and keepers of garages, except owners of bancas and owners of animal drawn two wheeled vehicle - Operators of international carriers doing business in the Philippines. - Franchise grantees of electric, gas or water utilities - Franchise grantees of radio and/or television broadcasting companies whose gross annual receipts of the preceding year do not exceed Ten Million (P10,000,000.00) Pesos and did not opt to register as VAT Taxpayers - Banks and non-bank financial intermediaries and finance companies - Life insurance companies - Agents of foreign insurance companies - Proprietor, lessee, or operator of cockpits, cabarets, night or day clubs,videoke/karaoke bars, karaoke television, karaoke boxes, music lounges and other similar establishments, boxing exhibitions, professional basketball games, jai-alai and race tracks - Every stock broker who effected a sale, barter, exchange or other disposition of shares of stock listed and traded through the Local Stock Exchange (LSE) other than the sale by a dealer in securities - A corporate issuer/stock broker, whether domestic or foreign, engaged in the sale, barter, exchange or other disposition through Initial Public Offering (IPO) /secondary public offering of shares of stock in closely held corporations

11) Who is a withholding agent?

A withholding agent is any person or entity who is required to deduct and remit the taxes withheld to the government.

12) What are the duties and obligations of the withholding agent?

The following are the duties and obligations of the withholding agent:a) To Register - withholding agent is required to register within ten (10) days after acquiring such status with the Revenue District office having jurisdiction over the place where the business is located

b) To Deduct and Withhold - withholding agent is required to deduct tax from all money payments subject to withholding tax

c) To Remit the Tax Withheld - withholding agent is required to remit tax withheld at the time prescribed by law and regulations

d) To File Annual Return - withholding agent is required to file the corresponding Annual Information Return at the time prescribed by law and regulations

e) To Issue Withholding Tax Certificates - withholding agent shall furnish Withholding Tax Certificates to recipient of income payments subject to withholding

13) Who are considered TOP 20,000 Corporate Taxpayers?

Top twenty thousand (20,000) private corporations shall include a corporate taxpayer who has been determined and notified by the Bureau of Internal Revenue (BIR) as having satisfied any of the following criteria:

a) Classified and duly notified by the Commissioner as a large taxpayer under Revenue Regulation No. 1-98, as amended, or belonging to the top five thousand (5,000) private corporations under RR12-94, or to the top ten thousand (10,000) private corporations under RR 17-2003, unless previously de-classified as such or had already ceased business operations (automatic inclusion);

b) VAT payment or payable whichever is higher, of at least P100,000 for the preceding year;

c) Annual income tax due of at least P200,000 for the preceding year;

d) Total percentage tax paid of at least P100,000 for the preceding year;

e) Gross sales of P10,000,000 and above for the preceding year;

f) Gross purchases of P5,000,000 and above for the preceding year;

g) Total excise tax payment of at least P100,000 for the preceding year.

14. What are the obligations of Top 20,000 Corporate Taxpayers?

a) In addition to the above responsibilities of a withholding agent, Top 20,000 private corporations shall withhold the one percent (1%) creditable expanded withholding tax on the purchase of goods and two percent (2%) on the purchase of services (other than those covered by other withholding tax rates) from local suppliers where it regularly makes purchases. However, casual purchase of goods shall not be subject to withholding tax unless the amount of purchase at any one time involves P10,000 or more, in which case, it shall then be required to withhold the tax. The same rule apply to local/resident supplier of services other than those covered by separate rates of withholding tax.Provided, however, that for purchases involving agricultural products in their original state, the tax required to be withheld shall only apply to purchases in excess of the cumulative amount of P300,000 within the same taxable year. For this purpose, agricultural products in their original state shall only include corn, coconut, copra, palay, rice cassava, sugar cane, coffee, fruits, vegetables, marine food products, poultry and livestocks.

b) Taxes withheld shall be remitted using BIR Form 1601-E on a monthly basis thru the use of the Electronic Filing and Payment System (EFPS) on the dates prescribed for e-filers. Filing shall be done on a staggered basis provided under RR 26-2002 and payment shall be made every 15th day following the end of the month for Jan-Nov and Jan. 20 of the following year for the month of December.

c) Certificate of Creditable Tax Withheld at Source (BIR Form No. 2307) shall be issued to the payees within twenty (20) days following the close of such payees’ taxable quarter or upon demand of the payees;

d) A list of regular supplier of goods and/or services shall be submitted on a semestral basis to the RDO/LTS/LTDO having jurisdiction over the principal place of business in hard copy if below ten payees or soft-copy for those with ten (10) or more payees per semester while e-submission regardless of the number of payees for those under Electronic Filing and Payment System (EFPS). Deadline for submission of the list is not later than July 31 and January 31 of each year. However, initial list of regular suppliers should be submitted within fifteen (15) days from actual receipt hereof.

15. Who are considered TOP 5,000 Individual Taxpayers?

Top 5,000 Individual Taxpayers shall refer to individual taxpayers engaged in trade or business or exercise of profession who have been determined and notified by the Bureau of Internal Revenue (BIR) as having satisfied any of the following criteria:

a) VAT payment or payable whichever is higher, of at least P100,000 for the preceding year;

b) Annual income tax due of at least P200,000 for the preceding year;

c) Total percentage tax paid of at least P100,000 for the preceding year;

d) Gross sales of P10,000,000 and above for the preceding year;

e) Gross purchases of P5,000,000 and above for the preceding year;

f) Total excise tax payment of at least P100,000 for the preceding year.

16. What are the obligations of Top 5,000 Individual Taxpayers?

a) In addition to the obligations of a withholding agent, Top 5,000 Individual Taxpayers shall withhold the one percent (1%) creditable expanded withholding on the purchase of goods and two percent (2%) on the purchase of services (other than those covered by other withholding tax rates) from local suppliers where it regularly makes purchases. However, casual purchase of goods shall not be subject to withholding tax unless the amount of purchase at any one time involves P10,000 or more, in which case, it shall then be required to withhold the tax. The same rule apply to local/resident supplier of services other than those covered by separate rates of withholding tax. Provided, however, that for purchases involving agricultural products

in their original state, the tax required to be withheld shall only apply to purchases in excess of the cumulative amount of P300,000 within the same taxable year. For this purpose, agricultural products in their original state shall only include corn, coconut, copra, palay, rice cassava, sugar cane, coffee, fruits, vegetables, marine food products, poultry and livestocks.

b) Taxes withheld shall be remitted under BIR Form 1601-E on a monthly basis thru the Electronic Filing and Payment System (EFPS) facility within the prescribed period.

c) Certificate of Creditable Tax Withheld at Source (BIR Form No. 2307) shall be issued to the payees within twenty (20) days following the close of such payees’ taxable quarter or upon demand of the payees;

d) A list of regular supplier of goods and/or services shall be submitted on a semestral basis to the RDO/LTS/LTDO having jurisdiction over the principal place of business in hard copy if below ten payees or soft-copy for those with ten (10) or more payees per semester while e-submission regardless of the number of payees for those under Electronic Filing and Payment System (EFPS). Deadline for submission of the list is not later than July 31 and January 31 of each year. However, initial list of regular suppliers should be submitted within fifteen (15) days from actual receipt hereof.

15. WHO ARE THE RESPONSIBLE OFFICIALS IN THE GOVERNMENT OFFICES CHARGED WITH THE DUTY TO DEDUCT, WITHHOLD AND REMIT WITHHOLDING TAXES?

The following officials are duty bound to deduct, withhold and remit taxes:a) For Office of the Provincial Government-province- the Chief Accountant, Provincial Treasurer and the Governor;

b) For Office of the City Government-cities- the Chief Accountant, City Treasurer and the City Mayor;

c) For Office of the Municipal Government-municipalities- the Chief Accountant, Municipal Treasurer and the Mayor;

d) Office of the Barangay-Barangay Treasurer and Barangay Captaine) For NGAs, GOCCs and other Government Offices, the Chief Accountant and the Head of Office or the Official holding the highest position.

16. Who are not subject to Withholding Tax on Compensation?

Any employee whose total compensation income does not exceed the statutory minimum wage of Five Thousand (P 5,000.00) Pesos a month or Sixty Thousand (P 60,000.00) Pesos a year is not subject to Withholding Tax on Compensation.

NOTE: Employee whose total annual compensation does not exceed P 60,000 shall be given two options with which to pay his income tax due as follows:

· His compensation income shall be subjected to withholding tax, but he shall not be required to file the income return prescribed in Section 51 of the Code (filing of an individual return) except when covered by any of the situations enumerated in Sec. 2.83.4 of Revenue Regulations No. 2-98, or

· His compensation income shall not be subject to withholding tax but he shall file his annual income tax return and pay the tax due thereon, annually.

When the employee has opted to have his compensation income subjected to Withholding tax so as to be relieved of the obligation of filing an annual Income Tax return and paying his tax due on a lump sum basis, he shall execute a waiver in a prescribed BIR Form of his exemption(s) from withholding, which shall constitute the authority for the employers to apply the withholding tax table provided under Revenue Regulations No. 2-98.

17. What income payments are subject to Final Withholding Tax?

a) Income Payments to a Citizen or to a Resident Alien Individual:· Interest on any peso bank deposit· Royalties · Prizes (except prizes amounting to P10,000 or less which is subject to tax under Sec. 25(A)(1) of the Tax Code· Winnings (except from Philippine Charity Sweepstake Office and Lotto)· Interest income on foreign currency deposit· Interest income from long term deposit· Cash and/or property dividends· Capital Gains presumed to have been realized from the sale, exchange or other disposition of real property

b) Income Payments to a Non-Resident Alien Engaged in Trade or Business in the Philippines· On Certain Passive Income - cash and/or property dividend - Share in the distributable net income of a partnership- Interest on any bank deposits- Royalties- Prizes (except prizes amounting to P10,000 or less which is subject to tax under Sec.

25(A)(1) of the Tax Code.- Winnings (except from Philippine Charity Sweepstake Office and Lotto)· Interest on Long Term Deposits· Capital Gains presumed to have been realized from the sale, exchange or other disposition of real property

c) Income Derived from All Sources Within the Philippines by a Non-Resident Alien Individual Not Engaged in Trade or Business · On gross amount of income derived from all sources within the Philippines· On Capital Gains presumed to have been realized from the sale, exchange or disposition of real property located in the Philippines

d) Income Derived by Alien Individual Employed by a Regional or Area Headquarters and Regional Operating Headquarters of Multinational Companies

e) Income Derived by Alien Individual Employed by Offshore Banking Units

f) Income of Aliens Employed by Foreign Petroleum Service Contractors and Subcontractors

g) Income Payment to a Domestic Corporation· Interest from any currency bank deposits and yield or any other monetary benefit from deposit substitutes and from trust fund and similar arrangements derived from sources within the Philippines· Royalties derived from sources within the Philippines· Interest income derived from a depository bank under the Expanded Foreign Currency Deposit (FCDU) System· Income derived by a depository bank under the FCDU from foreign transactions with local commercial banks· On capital gains presumed to have been realized from the sale, exchange or other disposition of real property located in the Philippines classified as capital assets, including pacto de retro sales and other forms of conditional sales based on the gross selling price or fair market value as determined in accordance with Sec. 6(E) of the NIRC, whichever is higher

h) Income Payments to a Resident Foreign Corporation· Offshore Banking Units· Tax on branch Profit Remittances· Interest on any currency bank deposits and yield or any other monetary benefit from deposit substitute and from trust funds and similar arrangements and royalties derived from sources within the Philippines· Interest income on FCDU· Income derived by a depository bank under the expanded foreign currency deposits system from foreign currency transactions with local commercial banks

i) Income Derived from all Sources Within the Philippines by a Non-Resident Foreign Corporation· Gross income from all sources within the Philippines such as interest, dividends,

rents, royalties, salaries, premiums (except re-insurance premiums), annuities, emoluments or other fixed determinable annual, periodic or casual gains, profits and income or capital gains;· Gross income from all sources within the Philippines derived by a non-resident cinematographic film owner, lessor and distributor· On the gross rentals, lease and charter fees derived by a non-resident owner or lessor of vessels from leases or charters to Filipino citizens or corporations as approved by the Maritime Industry Authority· On the gross rentals, charter and other fees derived by a non-resident lessor of aircraft, machineries and other equipment· Interest on foreign loans contracted on or after August 1, 1986

j) Fringe Benefits Granted to the Employee (except Rank and File)· Goods, services or other benefits furnished or granted in cash or in kind by an employer to an individual employee (except rank and file) such as but not limited to the following:- Housing- Vehicle of any kind- Interest on loans- Expenses for foreign travel- Holiday and vacation expenses- Educational assistance to employees or his dependents- Membership fees, dues and other expense in social and athletic clubs or other - similar organizations- Health insurance- Informers Reward

18. What are the types of withholding tax on government money payments?

a) Withholding of Creditable Value Added Tax · On gross payments for the purchase of goods · On gross payments for the purchase of services· Payments made to government public works contractors· Payments for lease or use of property or property rights to non-resident owners

b) Withholding of Percentage Tax Ø Payments to the following: · Any person engaged in business whose gross sales or receipts do not exceed P 550,000 and who are not VAT-registered persons. (Persons exempt from VAT under Sec. 109z of the Tax Code) · Domestic carriers and keepers of garages, except owners of bancas and owners of animal drawn two wheeled vehicle · Operators of international carriers doing business in the Philippines. · Franchise grantees of electric, gas or water utilities · Franchise grantees of radio and/or television broadcasting companies whose gross annual receipts of the preceding year do not exceed Ten Million (P10,000,000.00) Pesos and did not opt to register as VAT Taxpayers · Banks and non-bank financial intermediaries and finance companies

· Life insurance companies · Agents of foreign insurance companies · Proprietor, lessee, or operator of cockpits, cabarets, night or day clubs, boxing exhibitions, professional basketball games, jai-alai and race tracks · Every stock broker who effected a sale, barter, exchange or other disposition of shares of stock listed and traded through the Local Stock Exchange (LSE) other than the sale by a dealer in securities · A corporate issuer/stock broker, whether domestic of foreign, engaged in the sale, barter, exchange or other disposition through Initial Public Offering (IPO) /secondary public offering of shares of stock in closely held corporations.

DESCRIPTIONValue-Added Tax is a form of sales tax. It is a tax on consumption levied on the sale of goods and services and on the imports of goods into the Philippines. It is an indirect tax, which can be passed on to the buyer.

WHO ARE REQUIRED TO FILE VAT RETURNS? Every person or entity who in the course of his trade or business, sells or leases

goods, properties and services subject to VAT, if the aggregate amount of actual gross sales or receipts exceed Five Hundred Fifty Thousand Pesos (P 550,000.00) for any twelve month period;

A person required to register as VAT taxpayer but failed to register; A person who imports goods Professional practitioners

Professional Practitioners (PPs) are formerly classified as non-VAT taxpayers and were exempt from the Value-Added Tax and Percentage taxes under Section 109 of the National Internal Revenue Code (hereinafter referred to as the Code), until December 31, 2002. Prior to this date, they were subject only to Income Tax under Section 24 of the Code.Effective January 1, 2003, however, by virtue of Republic Act Nos. 7716 and 9010, which were implemented by Revenue Regulation Nos. 1-2003 and 3-2003, services of PPs are also subject to either VAT (if gross professional fees exceed P 550,000.00 for a 12-month period) or 3% Percentage Tax (if gross professional fees totals P 550,000 and below for a 12-month period), depending on their gross professional fee for a twelve (12) - month period."Professional Practitioners" include the following:· Certified Public Accountants· Lawyers· Doctors· Insurance Agents (Life & Non-life)· Other Professional Practitioners required to pass the government examination· Others

FREQUENTLY ASKED QUESTIONS

I. General VAT Queries

1) Who are required to file VAT returns and/or pay VAT?· Every person or entity who in the course of his trade or business, sells or leases goods, properties and services subject to VAT, if the aggregate amount of actual gross sales or receipts exceed Five Hundred Fifty Thousand Pesos (P 550,000.00) for any twelve month period;· A person required to register as VAT taxpayer but failed to register; and· A person who imports goods.

2) Where are VAT returns filed?The Monthly VAT Declaration (BIR Form 2550M) and Quarterly VAT Return (BIR Form 2550Q) shall be filed with any Authorized Agent Bank (AAB) in the place where the taxpayer is registered or required to be registered.In cases of no-payment, the return shall be filed with the Revenue District Office (RDO)/LTDO and LTAD where the taxpayer is registered or required to be registered.

In places where there are no AABs, it shall be filed with and the tax paid to the Revenue Collection Officer or duly Authorized City or Municipal Treasurer of the place where the RDO is located.

3) What is "output tax"?Output tax means the VAT due on the sale, lease or exchange of taxable goods or properties or services by any person registered or required to register under section 236 of the Tax Code.

4) What is "input tax"?Input tax means the VAT paid by a VAT-registered person in the course of his trade or business on importation of goods or local purchase of goods or services, including lease or use of property, from a VAT-registered person. It shall also include the transitional input tax determined in accordance with Section 111 of the Tax Code.

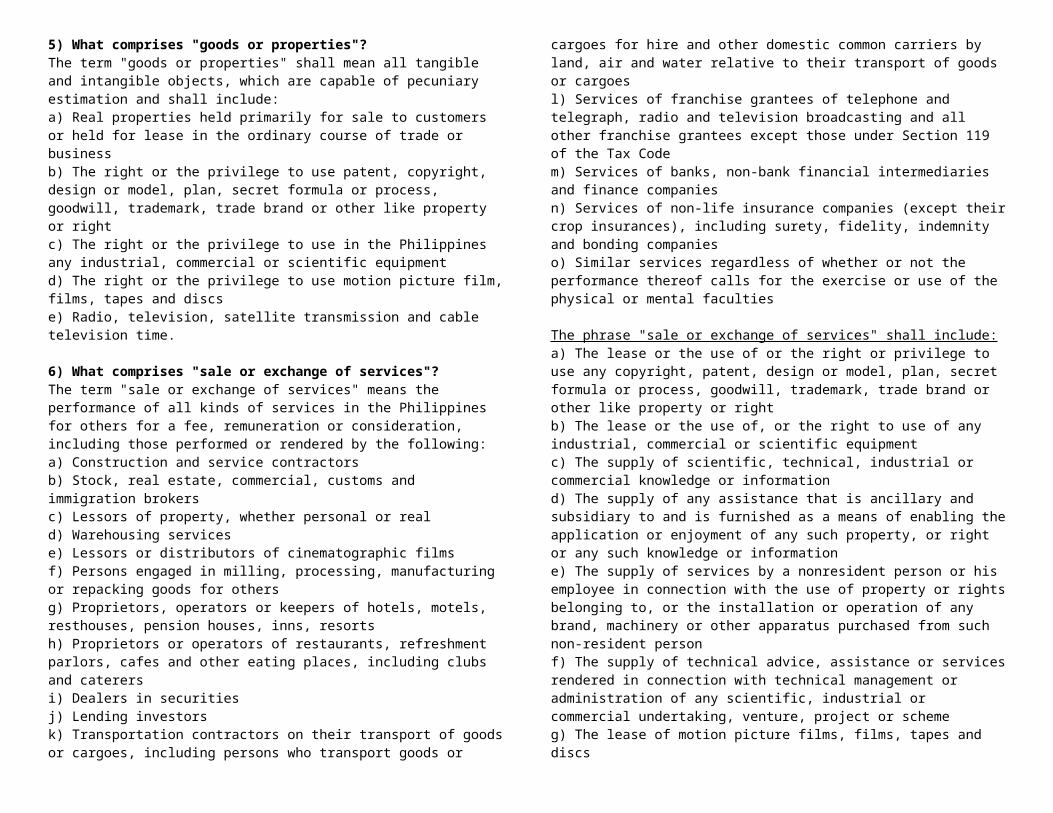

5) What comprises "goods or properties"?The term "goods or properties" shall mean all tangible and intangible objects, which are capable of pecuniary estimation and shall include:a) Real properties held primarily for sale to customers or held for lease in the ordinary course of trade or business b) The right or the privilege to use patent, copyright, design or model, plan, secret formula or process, goodwill, trademark, trade brand or other like property or right c) The right or the privilege to use in the Philippines any industrial, commercial or scientific equipment d) The right or the privilege to use motion picture film, films, tapes and discs e) Radio, television, satellite transmission and cable television time.

6) What comprises "sale or exchange of services"?The term "sale or exchange of services" means the performance of all kinds of services in the Philippines for others for a fee, remuneration or consideration, including those performed or rendered by the following:a) Construction and service contractors b) Stock, real estate, commercial, customs and immigration brokers c) Lessors of property, whether personal or real d) Warehousing services e) Lessors or distributors of cinematographic films f) Persons engaged in milling, processing, manufacturing or repacking goods for others g) Proprietors, operators or keepers of hotels, motels, resthouses, pension houses, inns, resorts h) Proprietors or operators of restaurants, refreshment parlors, cafes and other eating places, including clubs and caterers i) Dealers in securities j) Lending investors k) Transportation contractors on their transport of goods or cargoes, including persons who transport goods or cargoes for hire and other domestic common carriers by land, air and water relative to their transport of goods or cargoes l) Services of franchise grantees of telephone and telegraph, radio and television

broadcasting and all other franchise grantees except those under Section 119 of the Tax Code m) Services of banks, non-bank financial intermediaries and finance companies n) Services of non-life insurance companies (except their crop insurances), including surety, fidelity, indemnity and bonding companies o) Similar services regardless of whether or not the performance thereof calls for the exercise or use of the physical or mental faculties

The phrase "sale or exchange of services" shall include:a) The lease or the use of or the right or privilege to use any copyright, patent, design or model, plan, secret formula or process, goodwill, trademark, trade brand or other like property or right b) The lease or the use of, or the right to use of any industrial, commercial or scientific equipmentc) The supply of scientific, technical, industrial or commercial knowledge or information d) The supply of any assistance that is ancillary and subsidiary to and is furnished as a means of enabling the application or enjoyment of any such property, or right or any such knowledge or information e) The supply of services by a nonresident person or his employee in connection with the use of property or rights belonging to, or the installation or operation of any brand, machinery or other apparatus purchased from such non-resident person f) The supply of technical advice, assistance or services rendered in connection with technical management or administration of any scientific, industrial or commercial undertaking, venture, project or scheme g) The lease of motion picture films, films, tapes and discs h) The lease or the use of or the right to use radio, television, satellite transmission and cable television time.

7) What is a zero-rated sale?It is a sale, barter or exchange of goods, properties and/or services subject to 0% VAT pursuant to Sections 106 (A) (2) and 108 (B) of the Tax Code.

8) What transactions are considered as zero-rated sales?The following services performed in the Philippines by VAT-registered persons shall be subject to zero percent (0%) rate:a) Processing, manufacturing or repacking goods for other persons doing business outside the Philippines which goods are subsequently exported where the services are paid for in acceptable foreign currency and accounted for in accordance with the rules and regulations of the Bangko Sentral ng Pilipinas (BSP)b) Services other than those mentioned in the preceding paragraph, the consideration for which is paid for in acceptable foreign currency and accounted for in accordance with the rules and regulations of the Bangko Sentral ng Pilipinas (BSP)c) Services rendered to persons or entities whose exemption under special laws or international agreements to which the Philippines is a signatory effectively subjects the supply of such services to zero percent (0%) rated) Services rendered to vessels engaged exclusively in international shipping e) Services performed by subcontractors and/or contractors in processing, converting,

or manufacturing goods for an enterprise whose export sales exceeds seventy percent (70%) of total annual production.· The following sales shall be subject to zero percent (0%) rate:a) Sale of goods which are directly shipped by a VAT-registered resident to a place outside the Philippinesb) Sale of goods which are considered as "deemed" export sales by a VAT-registered person to certain entities who are also residents of the Philippines:· Sales to export-oriented enterprises which the Code considers as export sales at the level of the supplier of raw materials· Sales to entities, the exemption of which, under a special law or an international agreement with the Government of the Philippines, effectively zero rates such sales· Sales of gold to the Bangko Sentral ng Pilipinas· Foreign currency denominated sales of goodsc) Sales considered as exportation of goods under a special law such as Executive Order No. 226 (Omnibus Investments Code of 1987) and Republic Act No. 7916 (PEZA Law)

9) Where will taxpayers file their applications for VAT zero-rating?Taxpayers may file their application with the Audit Information, Tax Exemption and Incentives Division (AITEID) at the BIR National Office.

10) What is a Contractor's Final Payment Release Certificate and where should taxpayers file their application for this?The Contractor's Final Payment Release Certificate is issued by the BIR before a government contractor is fully paid for his contract with the government. Taxpayers may file their application at the BIR National Office at the Audit Information, Tax Exemption and Incentives Division (AITEID)

11) What transactions are considered as deemed sales?

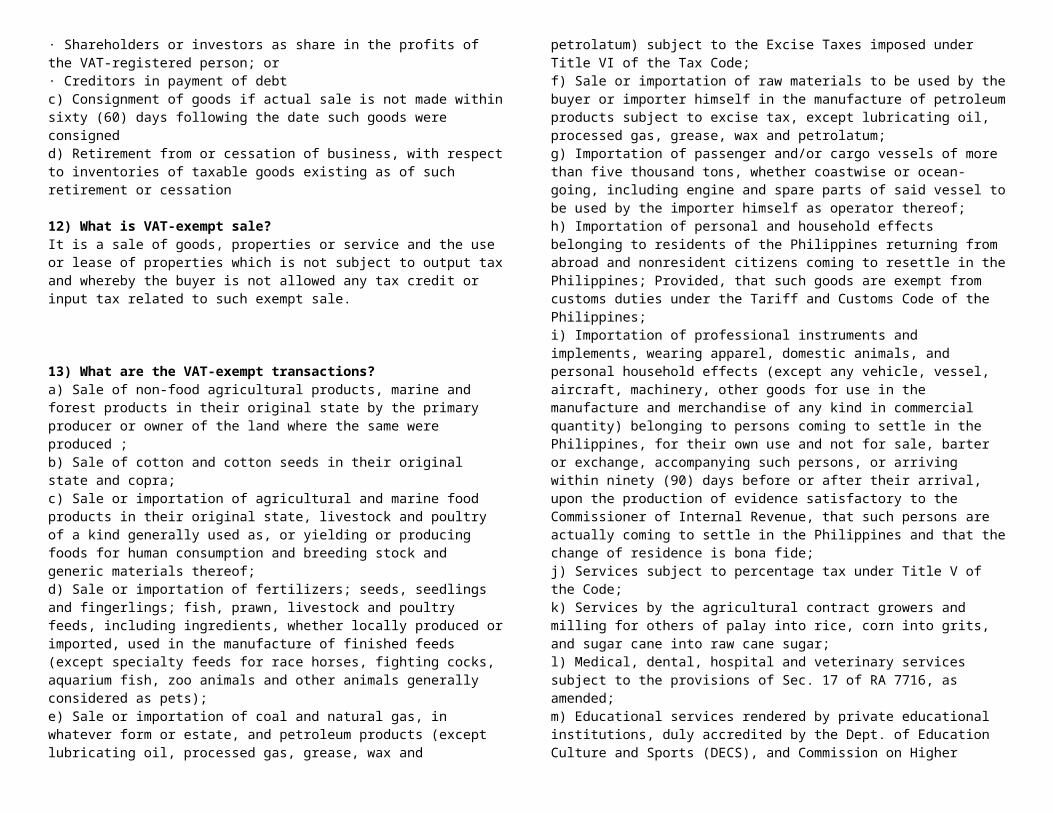

The following transactions are considered as deemed sales:a) Transfer, use or consumption, not in the course of business, of goods or properties originally intended for sale or for use in the course of business b) Distribution or transfer to:· Shareholders or investors as share in the profits of the VAT-registered person; or· Creditors in payment of debtc) Consignment of goods if actual sale is not made within sixty (60) days following the date such goods were consignedd) Retirement from or cessation of business, with respect to inventories of taxable goods existing as of such retirement or cessation

12) What is VAT-exempt sale?It is a sale of goods, properties or service and the use or lease of properties which is not subject to output tax and whereby the buyer is not allowed any tax credit or input tax related to such exempt sale.

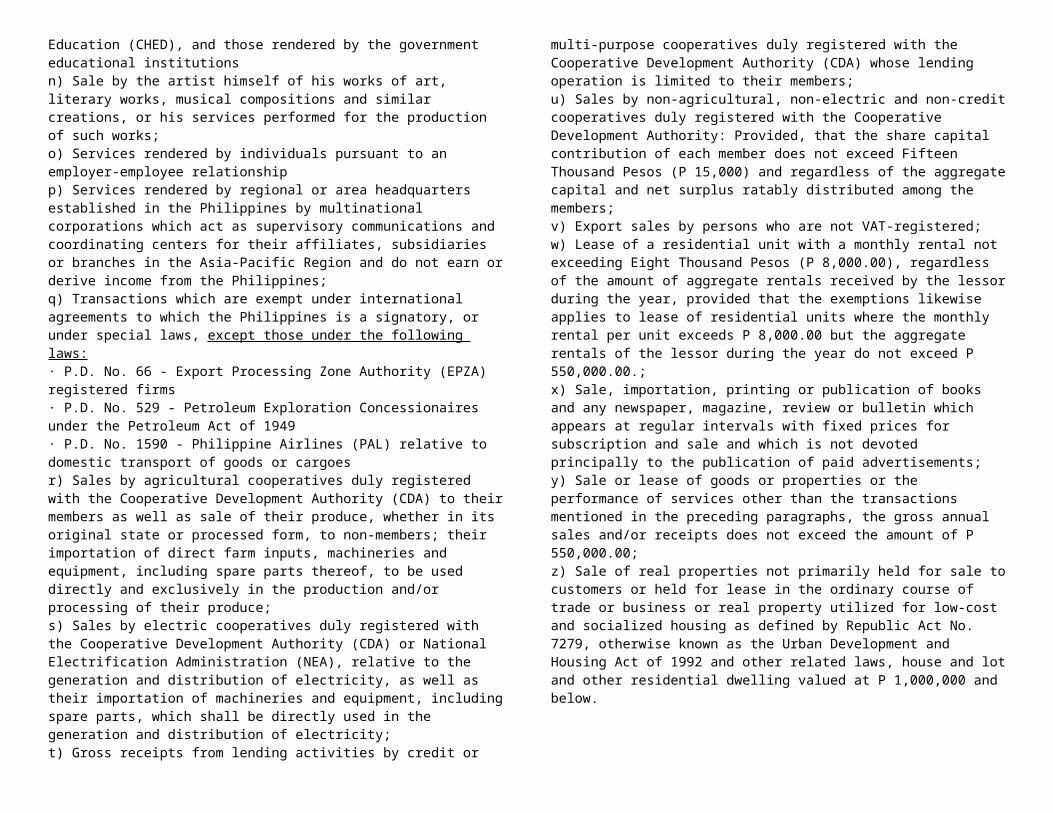

13) What are the VAT-exempt transactions?a) Sale of non-food agricultural products, marine and forest products in their original state by the primary producer or owner of the land where the same were produced ;b) Sale of cotton and cotton seeds in their original state and copra;c) Sale or importation of agricultural and marine food products in their original state, livestock and poultry of a kind generally used as, or yielding or producing foods for human consumption and breeding stock and generic materials thereof;d) Sale or importation of fertilizers; seeds, seedlings and fingerlings; fish, prawn, livestock and poultry feeds, including ingredients, whether locally produced or imported, used in the manufacture of finished feeds (except specialty feeds for race horses, fighting cocks, aquarium fish, zoo animals and other animals generally considered as pets);e) Sale or importation of coal and natural gas, in whatever form or estate, and petroleum products (except lubricating oil, processed gas, grease, wax and petrolatum) subject to the Excise Taxes imposed under Title VI of the Tax Code; f) Sale or importation of raw materials to be used by the buyer or importer himself in the manufacture of petroleum products subject to excise tax, except lubricating oil, processed gas, grease, wax and petrolatum;g) Importation of passenger and/or cargo vessels of more than five thousand tons, whether coastwise or ocean-going, including engine and spare parts of said vessel to be used by the importer himself as operator thereof; h) Importation of personal and household effects belonging to residents of the Philippines returning from abroad and nonresident citizens coming to resettle in the Philippines; Provided, that such goods are exempt from customs duties under the Tariff and Customs Code of the Philippines; i) Importation of professional instruments and implements, wearing apparel, domestic animals, and personal household effects (except any vehicle, vessel, aircraft, machinery, other goods for use in the manufacture and merchandise of any kind in commercial quantity) belonging to persons coming to settle in the Philippines, for their own use and not for sale, barter or exchange, accompanying such persons, or arriving within ninety (90) days before or after their arrival, upon the production of evidence satisfactory to the Commissioner of Internal Revenue, that such persons are actually coming to settle in the Philippines and that the change of residence is bona fide;j) Services subject to percentage tax under Title V of the Code; k) Services by the agricultural contract growers and milling for others of palay into rice, corn into grits, and sugar cane into raw cane sugar; l) Medical, dental, hospital and veterinary services subject to the provisions of Sec. 17 of RA 7716, as amended; m) Educational services rendered by private educational institutions, duly accredited by the Dept. of Education Culture and Sports (DECS), and Commission on Higher Education (CHED), and those rendered by the government educational institutions n) Sale by the artist himself of his works of art, literary works, musical compositions and similar creations, or his services performed for the production of such works; o) Services rendered by individuals pursuant to an employer-employee relationship p) Services rendered by regional or area headquarters established in the Philippines by multinational corporations which act as supervisory communications and coordinating centers for their affiliates, subsidiaries or branches in the Asia-Pacific Region and do

not earn or derive income from the Philippines; q) Transactions which are exempt under international agreements to which the Philippines is a signatory, or under special laws, except those under the following laws:· P.D. No. 66 - Export Processing Zone Authority (EPZA) registered firms· P.D. No. 529 - Petroleum Exploration Concessionaires under the Petroleum Act of 1949· P.D. No. 1590 - Philippine Airlines (PAL) relative to domestic transport of goods or cargoes r) Sales by agricultural cooperatives duly registered with the Cooperative Development Authority (CDA) to their members as well as sale of their produce, whether in its original state or processed form, to non-members; their importation of direct farm inputs, machineries and equipment, including spare parts thereof, to be used directly and exclusively in the production and/or processing of their produce; s) Sales by electric cooperatives duly registered with the Cooperative Development Authority (CDA) or National Electrification Administration (NEA), relative to the generation and distribution of electricity, as well as their importation of machineries and equipment, including spare parts, which shall be directly used in the generation and distribution of electricity; t) Gross receipts from lending activities by credit or multi-purpose cooperatives duly registered with the Cooperative Development Authority (CDA) whose lending operation is limited to their members; u) Sales by non-agricultural, non-electric and non-credit cooperatives duly registered with the Cooperative Development Authority: Provided, that the share capital contribution of each member does not exceed Fifteen Thousand Pesos (P 15,000) and regardless of the aggregate capital and net surplus ratably distributed among the members; v) Export sales by persons who are not VAT-registered; w) Lease of a residential unit with a monthly rental not exceeding Eight Thousand Pesos (P 8,000.00), regardless of the amount of aggregate rentals received by the lessor during the year, provided that the exemptions likewise applies to lease of residential units where the monthly rental per unit exceeds P 8,000.00 but the aggregate rentals of the lessor during the year do not exceed P 550,000.00.; x) Sale, importation, printing or publication of books and any newspaper, magazine, review or bulletin which appears at regular intervals with fixed prices for subscription and sale and which is not devoted principally to the publication of paid advertisements; y) Sale or lease of goods or properties or the performance of services other than the transactions mentioned in the preceding paragraphs, the gross annual sales and/or receipts does not exceed the amount of P 550,000.00; z) Sale of real properties not primarily held for sale to customers or held for lease in the ordinary course of trade or business or real property utilized for low-cost and socialized housing as defined by Republic Act No. 7279, otherwise known as the Urban Development and Housing Act of 1992 and other related laws, house and lot and other residential dwelling valued at P 1,000,000 and below.

II. RELIEF-Related Queries

1) What is 'RELIEF"?RELIEF means Reconciliation of Listings for Enforcement. It supports the third party information program of the Bureau through the cross referencing of third party information from the taxpayers' Summary Lists of Sales and Purchases prescribed to be submitted on a quarterly basis.

2) Who are required to submit Summary List of Sales?VAT taxpayers with quarterly total sales/receipts (net of VAT) exceeding Two Million Five Hundred Thousand Pesos (P 2,500,000) are required to submit a Summary List of Sales.

3) Who are required to submit Summary List of Purchases?VAT taxpayers with quarterly total purchases (net of VAT) exceeding One Million Pesos (P 1,000,000) are required to submit Summary List of Purchases.

4) What are the Summary Lists required to be submitted?a) Quarterly Summary List of Sales to Regular Buyers/Customers and Casual Buyers/Customers and Output Tax;b) Quarterly Summary List of Local Purchases and Input tax; andc) Quarterly Summary List of Importation

5) Who are "Casual Buyers/Customers?"Casual Buyers/Customers refer to buyers/customers who are engaged in business/ exercise of profession but did not qualify as regular buyers/customers, the amount of individual transaction is P 100,000 or more but did not qualify as regular buyers/customers.

6) Who are "Regular Buyers/Customers"?They shall refer to buyers/customers who are engaged in business or exercise of profession with whom the taxpayer has transacted at least six (6) transactions in the previous year or current year, regardless of the amount of sale per transaction.

7) What are the contents of the Quarterly Summary List of Sales to Regular Buyers/Customers and Casual Buyers/Customers and Output Tax?The Quarterly Summary List of Sales to regular buyers/customers and casual buyers/customers and output tax shall indicate the following:a) BIR Registered Name of the Buyer who is engaged in business/exercise of professionb) TIN of the Buyer for sales subject to VATc) Exempt Salesd) Zero-Rated Salese) Sales Subject to VAT (exclusive of VAT)f) Output Tax (VAT on Sales)

8) What are the contents of the Quarterly Summary List of Local Purchases and Input Tax?The Quarterly Summary List of Local Purchases and Input Tax shall indicate the following:a) BIR Registered Name of the Seller/Supplier/Service Providerb) Address of Seller/Supplier/Service Providerc) Taxpayer Identification Number (TIN) of the Sellerd) Exempt Purchasese) Zero-Rated Purchasesf) Purchases Subject to VAT (Exclusive of VAT) - · On Services· On Capital Goods· On Goods and Other than Capital Goodsg) Creditable Input Taxh) Non-Creditable Input Tax

9) What are the contents of the Quarterly Summary List of Importations?The Quarterly Summary List of Importations shall indicate the following:a) Import Entry Declaration Numberb) Assessment /Release Datec) Date of importationd) Name of Sellere) Country of Originf) Dutiable Valueg) All Charges Before release from the Customs' Custodyh) Landed Cost:· Exempt· Taxable (Subject to VAT) i) VAT Paidj) Official Receipt (OR) No. of the Official Receipt Evidencing Payment of the Taxk) Date of VAT Payment

10) When and where will taxpayers file/submit the Quarterly Summary List of Sales and Purchases?The quarterly summary list of sales or purchases whichever is applicable shall be submitted to the RDO or LTDO or LTAD having jurisdiction over the taxpayer on or before the twenty-fifth (25th) day of the month following the close of each taxable quarter.

11) Can the VAT withheld and paid for the non-resident recipient, which VAT is passed on to the resident withholding agent by the non-resident recipient of the income, be claimed as an input tax?Yes. It can be claimed as an input tax by the said VAT registered Withholding Agent upon filing his own VAT return, subject to the rules on allocation of input tax among taxable, zero-rated and exempt sales.

12) Are all Value Added Taxpayers required to mandatorily file the summary list in magnetic form using 3.5 inch floppy diskette?Yes. Submission of the summary list in diskette form shall be required for the taxable quarter where the total sales (taxable net of VAT, zero-rated, exempt) exceed P 2,500,000 or total purchases (taxable net of VAT, zero-rated, exempt) exceed P 1,000,000.

13) What is the clear-cut rule on the mandatory submission of summary lists in diskette form?The following are the rules in the submission of the said summary lists:a) They are required to submit the said summary lists in diskette form for the taxable quarter where the total sales (taxable net of VAT, zero-rated, exempt) exceed P 2,500,000 or total purchases (taxable net of VAT, zero-rated, exempt) exceed P 1,000,000.b) Those who did not meet the threshold need not file summary lists; however, if there is a taxable quarter where aforesaid VAT taxpayers meet or exceed the threshold, they will be required to submit the prescribed electronic format on such taxable quarter and on the next three (3) succeeding taxable quarters, regardless of whether or NOT such succeeding taxable quarter sales and/or purchases meet/exceed the threshold.

14) What is the penalty for failure to submit the quarterly summary list in the prescribed manner?Administrative Penalty

P 1,000 - For each failure to file, keep or supply the required documentsAggregate amount not to exceed P 25,000 for the taxable yearCriminal PenaltyWillful failure to keep any record or to supply the information at the time or times required shall be subject to the criminal penalty under the Tax Code of 1997. *Compromise on such violation SHALL NOT relieve the violating taxpayer from the obligation to submit the required documents.

IV. VAT on Professionals1) How to compute the VAT on professionals?The general formula is:Output Taxes - Input Taxes = VAT Payable

Fees and Expenses including VAT: (a)Professional Fee with VAT x 1/11 Output TaxLess: Profession-related Expenses x 1/11 (with VAT Receipts) Input TaxDifference VAT PayableFees and Expenses excluding VAT: (b)Professional Fee x 10% Output TaxLess: Profession-related Expenses x 10% (with VAT Receipts) Input TaxDifference VAT PayableNOTE:(a) Computation is in accordance with Secs. 106D and 108C of the Code.

(b) Computation per VAT Return presentation.VAT Payable in (a) and (b) computations should be the same.

2) What are the allowable Input VAT?· 10% of purchase price, exclusive of VAT or 1/11 of total VAT invoice/OR amount on:· Office Supplies / Equipment· Rental of office· Accountant's fees· Other purchases of Goods and Services related to professional fees earnedNote: 1) Supplier of goods/services must be VAT registered 2) Substantiated with VAT OR/invoice 3) Illustrations of VAT ComputationAssumption 1: PP absorbs the VAT

In CY 2002, Professional Fee for Services was P 1,000,000In CY 2003, Professional Fee for Services is P 1,000,000Treatment:CY 2002: Income is P 1,000,000.00CY 2003:Income is 10/11 of P 1,000,000 P 909,091.00Output VAT is 1/11 of P 1,000,000 90,909.00Gross Receipt from Clients/Px + VAT P 1,000,000.00Assumption 2: Payor absorbs the VATIn CY 2002, Professional Fee for Services was P 1,000,000In CY 2003, Professional Fee for Services is P 1,000,000, plus 10% VAT of P 100,000Treatment:CY 2002: Income is P 1,000,000.00CY 2003: Income P 1,000,000.00Income P1M x 10% Output tax 100,000.00Gross Receipt from Clients/ Px + VAT P1,100,000.000

4) How can I compute the 20% Withholding Tax using Assumptions 1 and 2?CY 2002:Income P 1,000,000.0020% Withholding Tax 200,000.00Net Amount Received from Payor P 800,000.00

CY 2003: (PP absorbs the VAT)Income P 909,091.00Add: 10% VAT 90,909.00Gross Amount Rec'd. from Payor P 1,000,000.00 Less: 20% of P 909,091.00 181,818.00Net Amount Received from Payor P 818,182.00CY 2003: (Payor Absorbs the VAT)Income P 1,000,000.00

Add: 10% VAT 100,000.00Gross Amount Rec'd. from Payor P 1,100,000.00 Less: 20% of P 1,000,000 200,000.00Net Amount Received from Payor P 900,000.00

5) How to record the professional fee in the Books of Accounts of the Professional Practitioner?Debit: Cash 900,000Debit: Creditable W/Tax 200,000Credit: Professional Fees 1,000,000Credit: Output VAT Payable 100,0006) How to record the professional fee in the Books of Accounts of the Clients/PatientsDebit: Expenses 1,000,000Debit: Input VAT Credit 100,000Credit: Cash 900,000Credit: Withholding Tax Payable 200,0007) How to issue a VAT Official Receipt by the Professional Practitioner?The invoice or official receipt of a VAT-registered PP must show his name, address, TIN, and professional fee, with VAT and other particulars.

8) Compliance Requirements for PPs· Payment of P 500 annual registration fee, and every year thereafter, on or before January 31.· Printing and registration of VAT Official Receipts· Registration and keeping of Books of Accounts· Filing of monthly VAT declarations and quarterly VAT returns· If applicable, submission of the Summary List of Sales and Purchases in softcopies (diskettes). Please use the BIR data entry module.

Registration as a VAT Taxpayer· File Form 1901 (Application for Registration) and Form 1925 (TIN Capture Form) for new taxpayers with the RDO having jurisdiction over PP's registered address. (By April 2003, TIN application was made available through the Internet, via the BIR Website at www.bir.gov.ph.)· For old taxpayers registered as Non-VAT, file Form 1905 (Update Form) to change registration to VAT, or from NV-Exempt to NV-3%.· Each registrant (for new or for change of registration) must indicate their specific profession (i.e., doctor, lawyer, CPA, etc.) in the appropriate registration form.Registration of Official Receipts· Submit Inventory of Non-VAT unused receipts (as of December 31, 2002) - number of booklets and serial numbers not later than March 19, 2003.· Stamp unused receipts with "VAT-registered as of ________" on ALL copies, and use only until June 30, 2003· For new Official Receipts, secure BIR Permit to PrintRegistration and Keeping of Books of Accounts· Journal · Ledger

· Subsidiary Professional Income Book· Subsidiary Purchases / Expenses BookFiling and Payment of VATForms to be used:· Form 2550M (Monthly VAT Declaration)· Form 2550Q (Quarterly VAT Return)Period/Form1st Month of the Quarter (Form 2550M) Due dates20th day of the next month2nd Month of the Quarter (Form 2550M) 20th day of the next month3rd Month, con-solidated for the Quarter (Form 2550Q) 25th day of the next monthWhere to File and Pay the VATPay to the Accredited Agent Bank (AAB) within the Revenue District Office (RDO) where the PP is registered. In areas where there are no AABs, pay to the Collection Agent in the municipality of the RDO where registered. If without VAT payment, file return with the RDO.Other Transitional Requirements· Submit Billings for Uncollected Professional fee for Sale of Services Rendered on or before December 31, 2002, not later than March 19, 2003.· Submit Inventory of Goods (other than Capital Goods), Materials, and Supplies, as of December 31, 2002, not later than March 19, 2003, to claim transitional (presumptive) input VAT.

V. VAT on Doctors1) If a doctor has several clinics located in different districts, should he register and pay the corresponding fee for each of the clinics?Yes, the doctor should register and pay the corresponding fee for each of the clinic located in different districts, as each clinic is considered a separate and distinct establishment.

2) What is the tax treatment for a doctor who has no clinic but is affiliated with several hospitals?The doctor is considered a professional, subject to 10% VAT provided the gross professional fees is more than P= 550,000.00 and 3% Percentage Tax if P= 550,000.00 and below. He should register his clinic but not his affiliations.

3) A doctor operates a clinic and at the same time hires (as employees) several doctors as part of his staff. For the services provided to patients, the clinic issues the official receipt of the clinic. How will the VAT be charged when the clinic later gives to the individual doctors their professional fees?If the hired doctors are employees receiving compensation income, they are not subject to VAT. If, however, they share in the professional fees, then there exists a professional partnership and their income/fee is subject to VAT. Any amount they receive from the clinic shall be considered as inclusive of VAT. But the clinic is exempt from VAT as far as medical services are concerned, but the professional fee received is subject to VAT.

4) Can a professional doctor claim input VAT? What are the sources of input taxes?Yes, he can claim input VAT on his purchases that are related to the practice of profession and supported with a VAT invoice/official receipts issued in his name.

5) Is a doctor with a maximum of 10 consultations a year required to have his own receipts printed? Is this not too costly for him?Yes, the determining factor is his practice of profession and not the number of transactions in a year. Section 237 of the Tax Code provides that all persons subject to internal revenue tax shall for each sale/transfer of merchandise or for services rendered valued at P= 25.00 or more must issue a duly registered receipt or sales invoice.

6) Are the fees of physical therapists, not a GPP, subject to VAT?Yes, they are subject to 10% VAT if their gross receipt is more than P= 550,000.00. If their gross receipt is P= 550,000.00 or less they are subject to 3% Percentage Tax, unless they opt to register as VAT taxpayer.

VI. VAT on Lawyers

1) What constitute gross receipts of lawyers that is subject to VAT?The gross receipts of lawyers may constitute of, but not limited to the following: retainers' fees, acceptance fees, appearance fees, consultation fees, notarial fees and the like

2) If a lawyer, employed in the government, provides/operates a notarial service, is he required to register as VAT taxpayer with regard to his notarial fees?Yes, because his notarial fees is part of his professional income and not earned under an employee-employer relationship.

VII. VAT on Insurance Agents

1) An agent of a life insurance company has been registered as a Non- VAT Taxpayer, is it necessary for him to register as VAT Taxpayer?An agent is required to register as VAT taxpayer if he is earning more than P= 550,000.00 in any twelve-month period. If his expected income for the 12-month period is P= 550,000.00 or less, he is subject to 3% Percentage Tax, unless he opts to register as a VAT taxpayer.

2) Is the P= 500.00 registration fee a one-time payment only? Will it apply to the succeeding years?The P= 500.00 is a registration fee payable annually on or before January 31 of each year.

3) What particular books of accounts are necessary for taxation purposes?Generally, the books of accounts necessary for taxation purposes are Journals and Ledgers. Professional taxpayers however, are required to keep Subsidiary Professional

Income Book and Subsidiary Purchases/Expense Book for their gross sales/gross receipts and purchases/expenses.

4) Are they required to issue Official Receipts?Yes, Section 237 of the Tax Code provides that all persons subject to internal revenue tax shall for each sale/transfer of merchandise or for services rendered valued at P= 25.00 or more must issue a duly registered receipt or sales invoice. In addition, in order to claim Input VAT, the name, address and TIN of the purchaser/client must be indicated in the receipt/invoice.

VIII. Other Professional Practitioners1) What about other individuals who practice certain calling but need not undergo government exam?Said individuals are subject to VAT if their gross receipts/income is more than P= 550,000.00. They are subject to 3% Percentage Tax if their gross receipts/income is P= 550,000.00 or less, unless they opt to register as VAT taxpayer. However, if their service is rendered under an employee-employer relationship, then they are not subject to VAT nor to Percentage Tax.Examples of individuals who practice certain calling are tourist guides, trainers, masseurs, brokers and other individuals who are paying occupational tax in the local or municipal government, and there exist No employer-employee relationship.

How do we determine the main or principal business of a taxpayer who is engaged in mixed business activities?

In determining the main or principal business of a taxpayer, we apply the predominance test. Under this test, if more than fifty (50%) of its gross sales and/or gross receipts comes from its business/es subject to VAT, its main/principal business falls within the VAT system making its status as a VAT person. Otherwise, he can not be considered as a VAT person eligible for the election provided for under Section 109(2) of the Tax Code.

What is the liability of a taxpayer becoming liable to VAT and did not register as such?

Any person who becomes liable to VAT and fails to register as such shall be liable to pay the output tax as if he is a VAT-registered person, but without the benefit of input tax credits for the period in which he was not properly registered.

Who may opt to register as VAT and what will be his liability?

1. Any person who is VAT-exempt under Sec. 4.109-1 (B) (1) (V) not required to register for VAT may, in relation to Sec. 4.109-2, elect to be VAT-registered by registering with the RDO that has jurisdiction over the head office of that person, and pay the annual registration fee of P500.00 for every separate and distinct establishment.

2. Any person who is VAT-registered but enters into transactions which are exempt from VAT (mixed transactions) may opt that the VAT apply to his transactions which would have been exempt under Section 109(1) of the Tax Code, as amended [Sec. 109(2)].

3. Franchise grantees of radio and/or television broadcasting whose annual gross receipts of the preceding year do not exceed ten million pesos (P10,000,000.00) derived from the business covered by the law granting the franchise may opt for VAT registration. This option, once exercised, shall be irrevocable. (Sec. 119, Tax Code).

4. Any person who elects to register under optional registration shall not be allowed to cancel his registration for the next three (3) years.

The above-stated taxpayers may apply for VAT registration not later than ten (10) days before the beginning of the calendar quarter and shall pay the registration fee unless they have already paid at the beginning of the year. In any case, the Commissioner of Internal Revenue may, for administrative reason deny any application for registration. Once registered as a VAT person, the taxpayer shall be liable to output tax and be entitled to input tax credit beginning on the first day of the month following registration.

What are the instances when a VAT-registered person may cancel his VAT registration?

1. If he makes a written application and can demonstrate to the commissioner's satisfaction that his gross sales or receipts for the following twelve (12) months, other than those that are exempt under Section 109 (A) to (U), will not exceed one million five hundred thousand pesos (P1,500,000.00); or

2. If he has ceased to carry on his trade or business, and does not expect to recommence any trade or business within the next twelve (12) months.

When will the cancellation for registration be effective?

The cancellation for registration will be effective from the first day of the following month the cancellation was approved.

What is the invoicing/ receipt requirement of a VAT-registered person?

A VAT registered person shall issue :

1. A VAT invoice for every sale, barter or exchange of goods or properties; and

2. A VAT official receipt for every lease of goods or properties and for every sale, barter or exchange of services.

May a VAT-registered person issue a single invoice/ receipt involving VAT and Non-VAT transactions?

Yes. He may issue a single invoice/ receipt involving VAT and non-VAT transactions provided that the invoice or receipt shall clearly indicate the break-down of the sales price between its taxable, exempt and zero-rated components and the calculation of the Value-Added Tax on each portion of the sale shall be shown on the invoice or receipt.

May a VAT- registered person issue separate invoices/ receipts involving VAT and Non-VAT transactions?

Yes. A VAT registered person may issue separate invoices/ receipts for the taxable, exempt, and zero-rated component of its sales provided that if the sales is exempt from value-added tax, the term "VAT-EXEMPT SALE" shall be written or printed prominently on the invoice or receipt and if the sale is subject to zero percent (0%) VAT, the term "ZERO-RATED SALE" shall be written or printed prominently on the invoice or receipt.

How is the Value-Added Tax presented in the receipt/ invoice?

The amount of the tax shall be shown as a separate item in the invoice or receipt.

Sample:

Sales Price P100,000.00VAT 12,000.00Invoice Amount P112,000.00

What is the information that must be contained in the VAT invoice or VAT official receipt?

1. Name of Seller

2. Business Style of the Seller

3. Business Address of the Seller

4. Statement that the seller is a VAT-registered person, followed by his TIN

5. Name of Buyer

6. Business Style of Buyer

7. Address of Buyer

8. TIN of buyer, if VAT- registered and amount exceed P1,000.00

9. Date of transaction

10. Quantity

11. Unit cost

12. Description of the goods or properties or nature of the service

13. Purchase price plus the VAT, provided that:

Who are liable to register as VAT taxpayers?Any person who, in the course of trade or business, sells, barters or exchanges goods or properties or engages in the sale or exchange of services shall be liable to register if:

a. His gross sales or receipts for the past twelve (12) months, other than those that are exempt under Section 109 (A) to (U), have exceeded One Million Five Hundred Thousand Pesos (P1,500,000.00): or

b. There are reasonable grounds to believe that his gross sales or receipts for the next twelve (12) months, other than those that are exempt under Section 109 (A) to (U), will exceed One Million Five Hundred Thousand Pesos (P1,500,000.00).

When is a new VAT taxpayer required to apply for registration and pay the registration fee?New VAT taxpayers shall apply for registration as VAT Taxpayers and pay the corresponding registration fee of five hundred pesos (P500.00) using BIR Form No. 0605 for every separate or distinct establishment or place of business before the start of their business following existing issuances on registration.

Thereafter, taxpayers are required to pay the annual registration fee of five hundred pesos (P500.00) not later than January 31, every year.What compliance activities should a VAT taxpayer, after registration as such, do promptly or periodically?The following compliance activities must be performed by a VAT-registered taxpayer:

a. Pay the annual registration fee of P500.00 for every place of business or establishment that generates sales;

b. Register the books of accounts of the business/occupation/calling, including practice of profession, before using the same;

c. Register the sales invoices and official receipts as VAT-invoices or VAT official receipts for use on transactions subject to VAT. (If there are other transaction not subject to VAT, a separate set of non-VAT invoices or non-VAT official receipts need to be registered for use on transactions not subject to VAT);

d. Filing of the Monthly Value-added Tax Declaration on or before the 20th day following the end of the taxable month (for manual filers)/on or before the prescribed due dates enunciated in RR No. 16-2005 (for e-filers) using BIR Form No. 2550M and of the Quarterly VAT Return on or before the 25th day following the end of the taxable quarter using BIR Form No. 2550Q, reflecting therein gross receipts (for seller of service)/ gross sales (for seller of goods) and output tax (VAT on sales); purchases of goods and services made in the course of trade or business/exercise of profession and input tax (VAT on purchases), other allowable tax credits as in the case of advance VAT payment and VAT withheld by government payors, and VAT payable or excess input VAT, whichever is applicable, with the accredited agent banks (AABs) of the BIR or Revenue Collection Officers (RCOs) of the BIR (in areas without AAB), for returns with payment, or with the RDO/LTDO having jurisdiction over the taxpayer (home RDO/LTDO), for returns without payment. (The monthly VAT Declaration and the Quarterly VAT Return shall reflect the consolidated total for all the taxable lines of activity and all the establishments - head office and branches);