witan investment trust plc 2009 annual general meeting 28 april 2009

DESCRIPTION

Witan Investment Trust plc 2009 Annual General Meeting 28 April 2009. Witan Investment Trust plc Harry Henderson Chairman. 2008: An Eventful Year for Witan. 100 th Anniversary global financial crisis new management team fourth anniversary of move to multi-manager. - PowerPoint PPT PresentationTRANSCRIPT

Witan Investment Trust plc

2009 Annual General Meeting

28 April 2009

Witan Investment Trust plc

Harry HendersonChairman

3

2008: An Eventful Year for Witan

100th Anniversary

global financial crisis

new management team

fourth anniversary of move to multi-manager

4

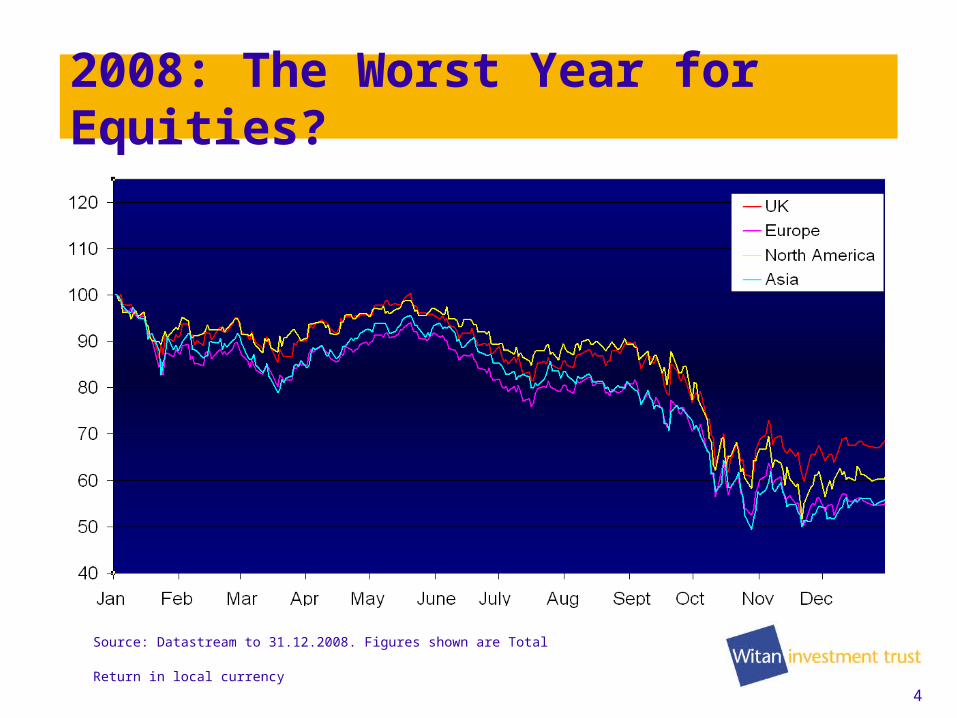

2008: The Worst Year for Equities?

Source: Datastream to 31.12.2008. Figures shown are Total Return in local currency

5

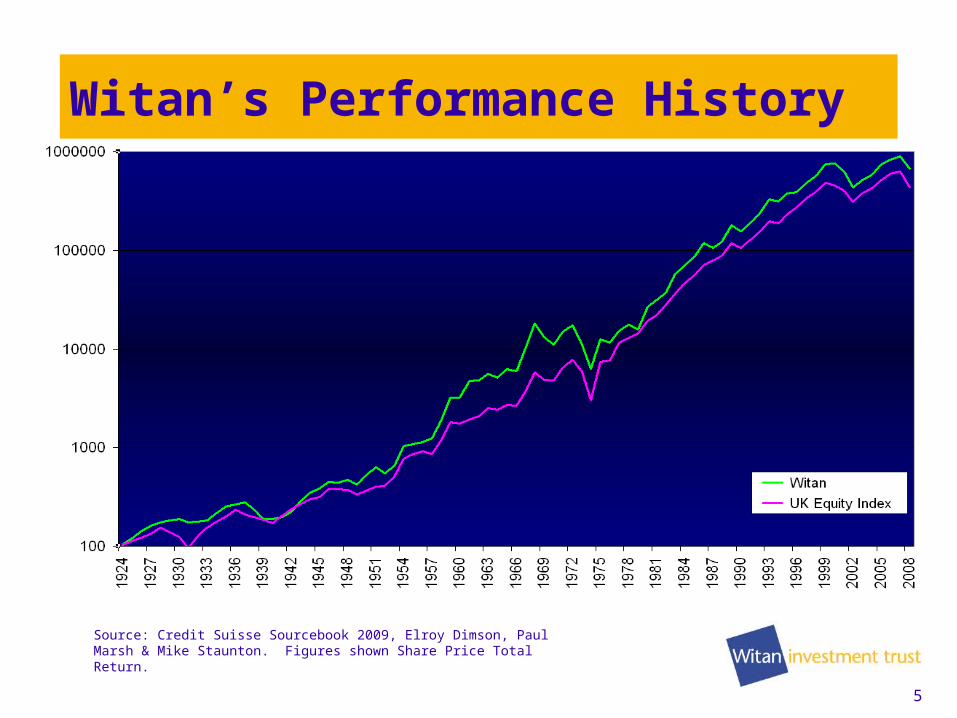

Witan’s Performance History

Source: Credit Suisse Sourcebook 2009, Elroy Dimson, Paul Marsh & Mike Staunton. Figures shown Share Price Total Return.

6

Witan since start of Multi-Manager

Source: Datastream to 31.12.08. Figures shown Share Price Total Return

7

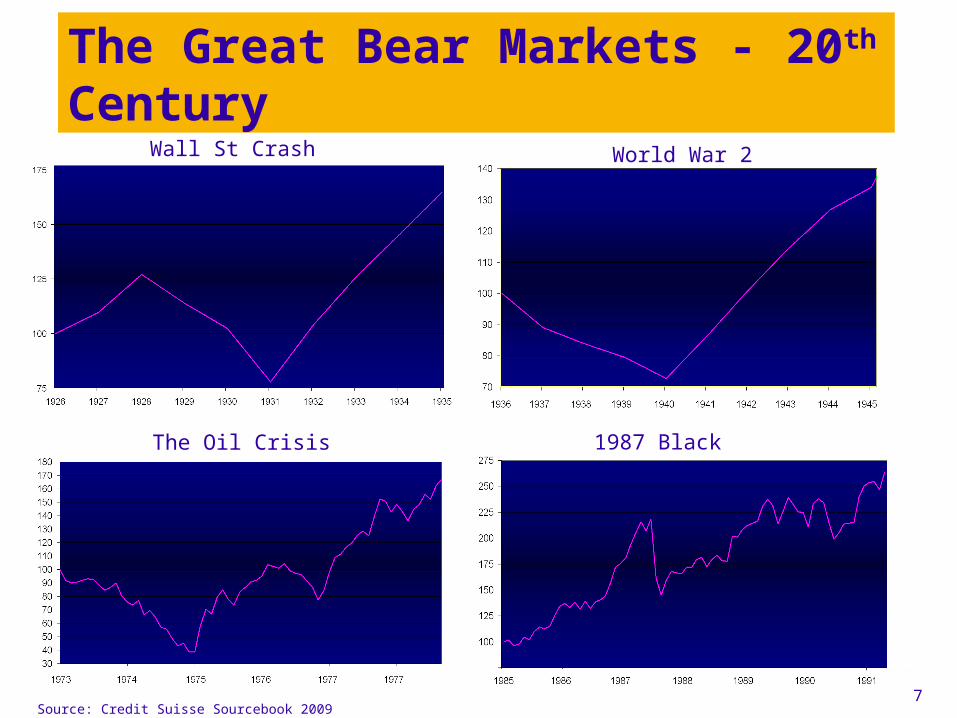

The Great Bear Markets - 20th Century

Source:

Wall St Crash World War 2

The Oil Crisis 1987 Black Thursday

Source: Credit Suisse Sourcebook 2009

8

£1 Invested in 1924

Source: Credit Suisse Sourcebook 2009

9

Reasons for (some) optimism

banking system saved

world working together

global stimulus yet to be felt

easier to deflate than inflate

Witan Investment Trust plc

Robert ClarkeChief Executive Officer

11

First Impressions

Financials– Performance– Dividend– Discount– Debt Repurchase– Total Expense Ratio

Business Development– Witan Investment Services– New Business Development

2009 AGM

12

First Impressions

innovation: 1st multi-manager investment trust

strong brands:

opportunity: portfolio & business development

13

First Impressions

Financials– Performance– Dividend– Discount– Debt Repurchase– Total Expense Ratio

Business Development– Witan Investment Services– New Business Development

2009 AGM

14

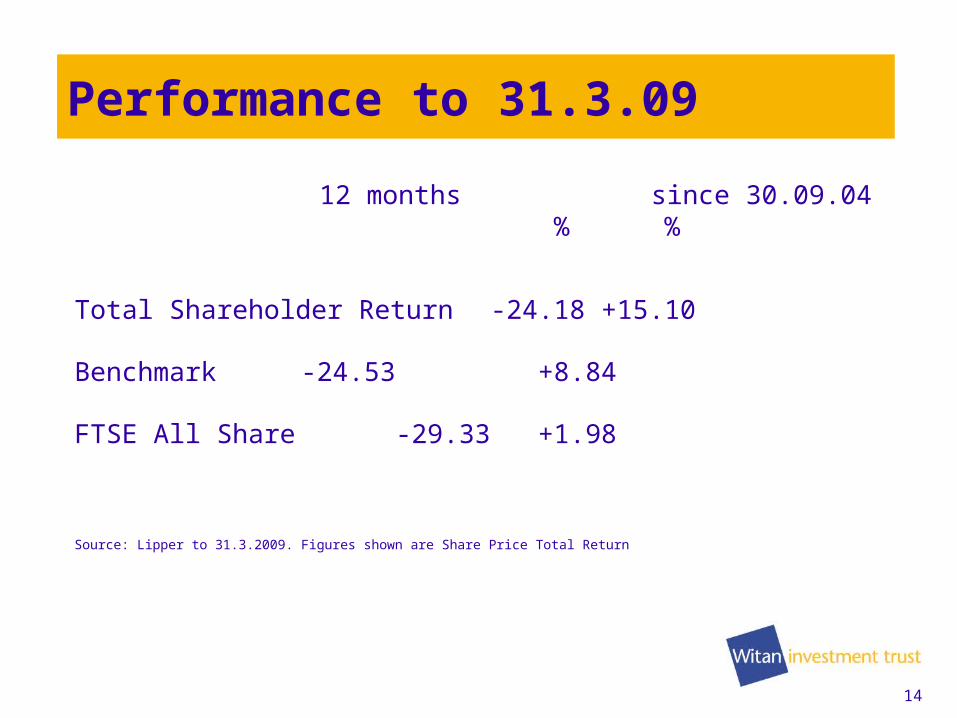

Performance to 31.3.09

12 months since 30.09.04 % %

Total Shareholder Return -24.18 +15.10

Benchmark -24.53 +8.84

FTSE All Share -29.33 +1.98

Source: Lipper to 31.3.2009. Figures shown are Share Price Total Return

15

Dividend

revenue reserves of £52.3m

2.4x covered

34th successive year of increase

Source: Witan to 31.12.2008. Rebased to 7.4p (Witan’s dividend in 1998)

16

Discount to Net Assets

volatile markets

continuing to add value through share buy backs

9m shares (4%): NAV +0.5%

average discount during 2008: 10.1% (2007: 10.5%)

17

Debt Repurchase

repurchased £30m of debt at a cost / premium to par: £2.0m

attractive price level

Impact on NAV: -0.29%

current annual net interest saving of ~ £1.8m (6.2% - 0.2%)

18

Total Expense Ratio

2008

2007

TER 0.71%

0.53%

Performance Fees £1.4m £0.5m

Other Costs £6.0m

£6.3m

Av. Shareholders’ Funds £1.05bn £1.28bn

19

First Impressions

Financials

Business Development– Witan Investment Services– New Business Development

2009 AGM

20

Witan Investment Services

100% owned subsidiary; FSA regulated

i. savings plan administration

ii. marketing services

iii. Executive Manager for Witan Pacific

£200K profit

Jump Child Trust Fund launched

21

Business Development: Why?

to generate additional value:

– income stream

– capital value

– discount

to enhance core business resources

to increase demand for shares

22

Business Development: How?

capitalise on key skills and abilities:

1. manager selection & multi-manager portfolio

construction

2. investment trust administration

new executive management mandates

seek relevant investment opportunities

23

First Impressions

Financials

Business Development

2009 AGM

Witan Investment Trust plc

Mark LynamChief Investment Officer

25

Investment Managers

Multi-manager process

Manager changes in 2008

Update on 2009

26

Witan Manager Selection Process

Questionnaire

Witan database

Qualitative

Appointment

Ongoing Monitoring

Extensive universe of managers

Face to face interviews

Basis to enable comparisons

Agree mandate and negotiate fees

Written reports, performance analysis

27

Manager Changes – Why?

Investment driven increase / decrease a new region

diversification

Manager driven

poor performance

style drift

corporate / manager change

28

Managers in 2008

currency fund redeemed

three new managers:

- Artemis

- Marathon

- Varenne

UK Enhanced Index reduced to 16% from 32%

9 out of 13 managers outperformed their benchmarks in

2008

29

Manager Quartile Rankings 2008 Manager 2008 Since Inception

Quartile Quartile

Thomas White 1st 1st

MFS 1st 1st

Southeastern 2nd 4th

Artemis 1st 1st

Marathon 1st 1st

Henderson UK Enhanced 2nd 1st

Henderson Small Cap 3rd 2nd

Wellington Management 2nd 4th

Varenne 3 rd 3rd

Henderson North America 1st 1st

Brandes 1st 1st

Comgest 1st 1st

Orbis 4th 4th

Source: Witan / Lipper as at 31.12.08

30

– overvaluation comes to an endBOK BOO\KER ORD GBX

Apr-08May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-0916

18

20

22

24

26

28

30

32

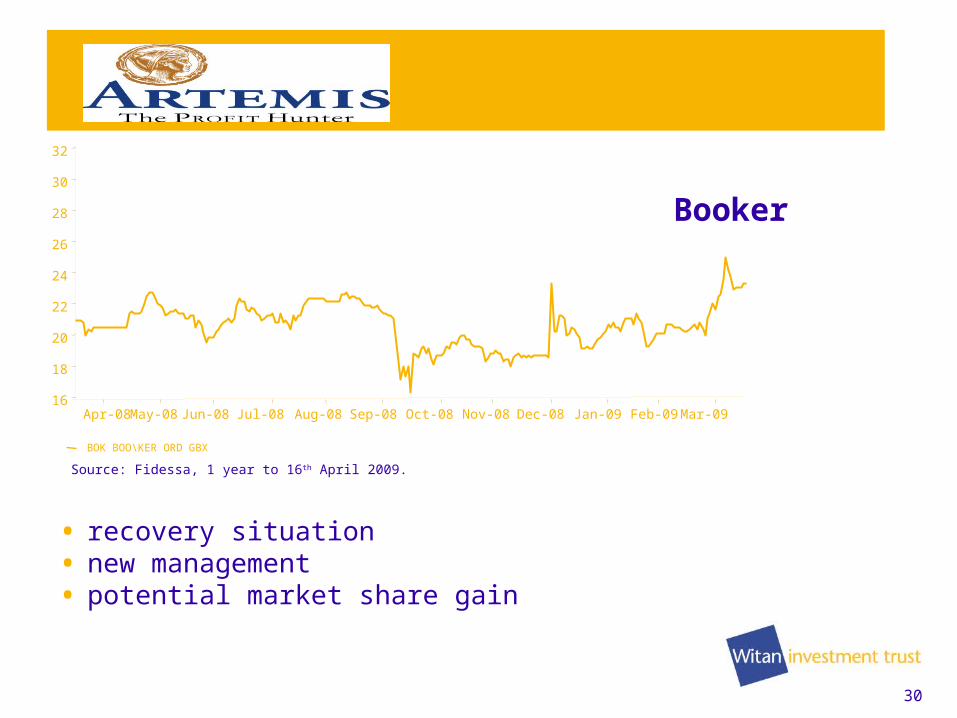

Source: Fidessa, 1 year to 16th April 2009.

• recovery situation • new management • potential market share gain

Booker

31

0

150

300

450

600

750

Dec-99 Apr-01 Aug-02 Dec-03 Apr-05 J ul-06 Nov-07 Mar-09

● dynamic management● double number of new

products● consistently outperformed

Share price relative to MSCI Europe

Reckitt Benckiser

32

.

40

50

60

70

80

90

100

110

120

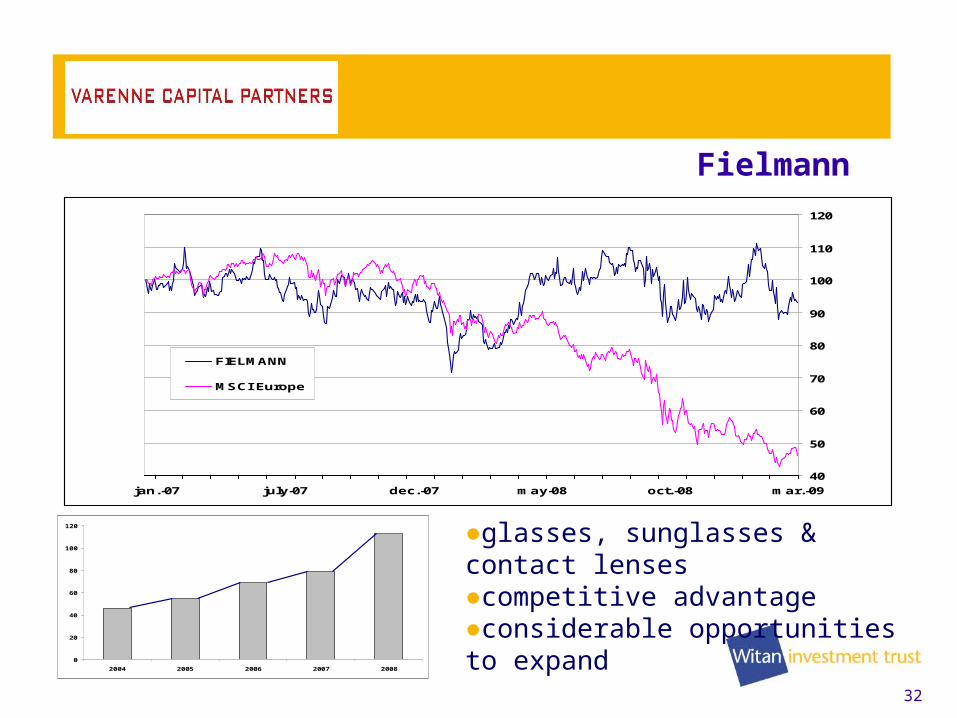

mar.-09oct.-08may-08dec.-07july-07jan.-07

FIELMANN

MSCI Europe

0

20

40

60

80

100

120

2004 2005 2006 2007 2008

+18.80%

+25.45%

+14.51%

+42.89%

●glasses, sunglasses & contact lenses●competitive advantage●considerable opportunities to expand

Fielmann

33

Progress in Q1 2009

8 out of 13 managers outperformed their benchmarks

prudent use of gearing

● added to Artemis and Marathon

● tactical investment in corporate bonds

● PIMCO

34

Witan Investment Services 201 Bishopsgate

London EC2M 3AE Tel: 020 7227 9770

Fax: 020 7227 9771

This document may not be reproduced in any form without the express permission of Witan Investment Services Limited and to the extent that it is passed on care must be taken to ensure that this reproduction is in a form which accurately reflects the information presented here. Whilst Witan Investment Services Limited believe that the information is correct at the date of production, no representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions in this document by any of Witan Investment Services Limited or their respective directors and no responsibility or liability is accepted by such persons for the accuracy or completeness of any such information or opinions or for any action taken on the basis of the contents of this document. No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness.

This document has been produced based on Witan Investment Services’ research and analysis and represents our house view. The information is made available to clients only incidentally. Unless otherwise indicated, the source for all data is Witan Investment Services. Any reference to individual companies is purely for the purpose of illustration and should not be construed as a recommendation to buy or sell or advice in relation to investment, legal or tax matters. Witan Investment Services (201 Bishopsgate, London EC2M 3AE) is authorised and regulated by the Financial Services Authority to provide investment products and services. We may record telephone calls for our mutual protection and to improve customer service.

This document does not constitute or form part of any offer or solicitation to issue, sell, subscribe or purchase any investment, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract for the same.

Please remember that past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Tax assumptions may change if the law changes and the value of tax relief will depend on individual circumstances.