willow lakes appraisal 4-1-10

TRANSCRIPT

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 1/86

All of the appraisers at EHA are designated or

associate members of the Appraisal Institute.

EHAEVERSON,

HUBER &

ASSOCIATES, LC

Commercial Real Estate

Services

SELF-CONTAINED APPRAISAL REPORT

OF THE EXISTING

WILLOW LAKES APARTMENTS7703 HARE AVENUE

JACKSONVILLE, DUVAL COUNTY, FLORIDA

EHA File 10-139

DATE OF VALUE

March 3, 2010

PREPARED FOR

Ms. Jill KnightJohnson Capital

2603 Main Street, Suite 200Irvine, California 92614

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 2/86

All of the appraisers at EHA are designated or

associate members of the Appraisal Institute.

EHAEVERSON,

HUBER &

ASSOCIATES, LC

Commercial Real Estate

Services

3535 Roswell Road, Suite 55

Marietta, Georgia 30062

Phone: (770) 977-3000

Fax: (770) 977-3490

Web Site: www.ehalc.com

PRINCIPALS

Larry A. Everson, MAI, CCIM

Stephen M. Huber

ASSOCIATES

Timothy P. Huber

Douglas M. Rivers

Ingrid N. Ott

Jon A. Reiss

Tobin B. JorgensenGeorge H. Corry III

A. Mason Carter

Quentin J. Thomas

ADMINISTRATIVE

Pauline J. Hines

March 8, 2010

Ms. Jill KnightJohnson Capital

2603 Main Street, Suite 200Irvine, California 92614

RE: Self-Contained Appraisal Report Of The ExistingWillow Lakes Apartments7703 Hare AvenueJacksonville, Duval County, Florida 32211-7786

EHA File 10-139

Dear Ms. Knight:

At your request and authorization, we conducted the inspections,

investigations, and analyses necessary to appraise the above referenced real

property. We have prepared a self contained appraisal report. The purpose

of this appraisal is to estimate the “as is” market value of the fee simple

interest in the subject property. The values reported are predicated upon

market conditions prevailing as of the date of appraisal, March 3, 2010. This

appraisal is intended for use by Johnson Capital as an aid in loan underwriting

decisions.

The subject is a 350-unit apartment complex on 10.83 acres. It is

located along Hare, India, and Jasper Avenues just east of Arlington Road inthe city of Jacksonville, Duval County, Florida. This location is less than 0.50

mile south of the Arlington Expressway and about four miles east of downtown

Jacksonville and I-95. The complex consists of 27 one- and two-story

apartment buildings and was reportedly constructed between 1963 and 1969.

The unit mix includes studio, efficiency, and one- and two-bedroom units

ranging from 320 to 1,000 square feet. Property amenities include onsite

management, pool, fitness center, laundry facility, and a pool. The buildings

feature traditional design with painted stucco over concrete block exterior

walls and built-up roofs. The property is in overall fair to average condition.

According to the provided rent roll, there are 23 vacant units.

The property is more fully described, legally and physically, within the

attached report. Additional data, information and calculations leading to the

value conclusions are incorporated in the report following this letter. This

document in its entirety, including all assumptions and limiting conditions, is

an integral part of and is inseparable from this letter.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 3/86

Ms. Jill KnightMarch 8, 2010

Page 2 EHAEVERSON,

HUBER &

ASSOCIATES, LC

Commercial Real Estate

Services

The following narrative appraisal contains the most pertinent data and

analyses upon which our opinions are based. The appraisal was prepared in

accordance with the requirements of the Code of Professional Ethics and

Standards of Professional Conduct of the Appraisal Institute. In addition, this

appraisal was prepared in conformance with our interpretation of the

guidelines and recommendations set forth in the Uniform Standards of

Professional Appraisal Practice (USPAP) of the Appraisal Foundation,

FIRREA, as well as the appraisal requirements of Johnson Capital.

Our opinion of value is formed based on our experience in the field of

real property valuation, as well as the research and analysis set forth in this

appraisal. Our concluded opinion of value, subject to the attached

assumptions and limiting conditions and certification, is:

Estimate of “As Is” Market Value of the Fee Simple Interest in the WillowLakes Apartments, as of March 3, 2010

NINE MILLION DOLLARS$9,000,000

It was a pleasure assisting you in this matter. If you have any

questions concerning the analysis, or if we can be of further service, please

call.

Respectfully submitted,

EVERSON, HUBER & ASSOCIATES, LC

By:

Timothy P. HuberCertified General AppraiserFlorida Certificate No. RZ3001

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 4/86

CERTIFICATION OF THE APPRAISERS

We certify that to the best of our knowledge and belief:

1. The statements of fact contained in this report are true and correct.

2. The reported analyses, opinions, and conclusions are limited only by the reportedassumptions and limiting conditions and are our personal, unbiased professional analyses,

opinions, and conclusions.

3. We have no present or prospective interest in the property that is the subject of this reportand have no personal interest or bias with respect to the parties involved.

4. Our compensation is not contingent upon the reporting of a predetermined value ordirection in value that favors the cause of the client, the amount of the value estimate, theattainment of a stipulated result, or the occurrence of a subsequent event, such as theapproval of a loan.

5. This appraisal assignment was not based on a requested minimum valuation, a specificvaluation, or approval of a loan.

6. Our analyses, opinions, and conclusions were developed, and this report was prepared, inconformity with the Uniform Standards of Professional Appraisal Practice of The AppraisalFoundation and the requirements of the Code of Professional Ethics and the Standards ofProfessional Appraisal Practice of the Appraisal Institute.

7. The use of this report is subject to the requirements of the Appraisal Institute relating toreview by its duly authorized representatives.

8. We have not performed any services regarding the subject property within the prior threeyears, as an appraiser or in any other capacity.

9. Timothy P. Huber inspected the subject property and prepared this report.

10. We have extensive experience in the appraisal of apartment complexes and Timothy P.Huber is appropriately certified by the State of Florida to appraise properties of this type.

Timothy P. HuberCertified General Real Property AppraiserFlorida Certificate No. RZ3001

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 5/86

SUMMARY OF SALIENT FACTS

i

Property Name/Address’ Willow Lakes of Arlington7703 Hare AvenueJacksonville, Duval County, Florida 32211-7786

Appraisal Identification: EHA File 10-139

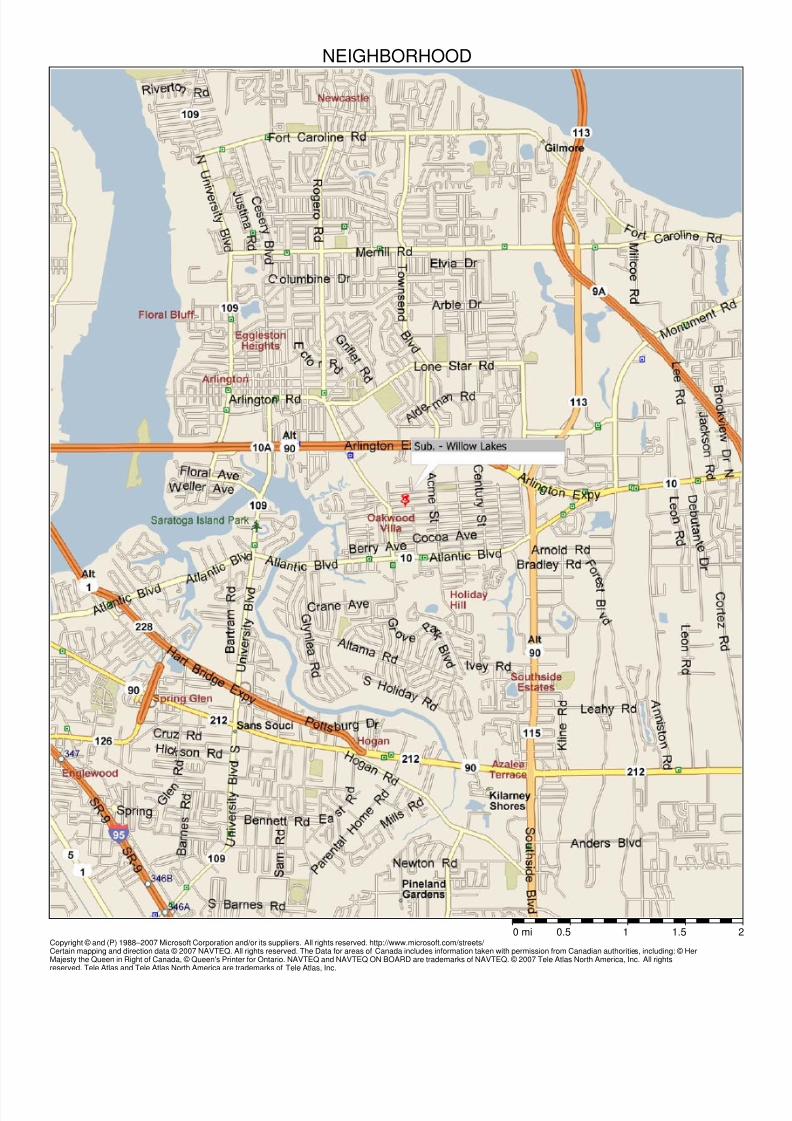

Location: It is located along Hare, India, and Jasper Avenues just eastof Arlington Road in the city of Jacksonville, Duval County,Florida. This location is less than 0.50 mile south of theArlington Expressway and about four miles east of downtownJacksonville and I-95.

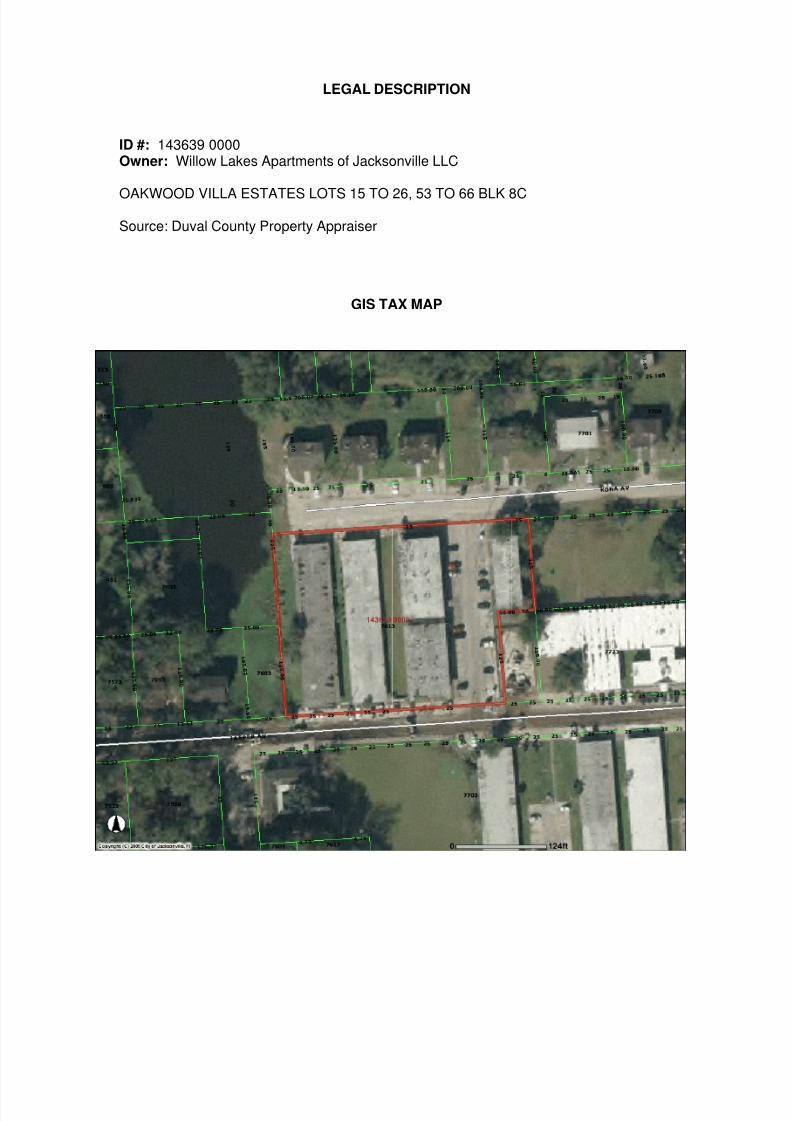

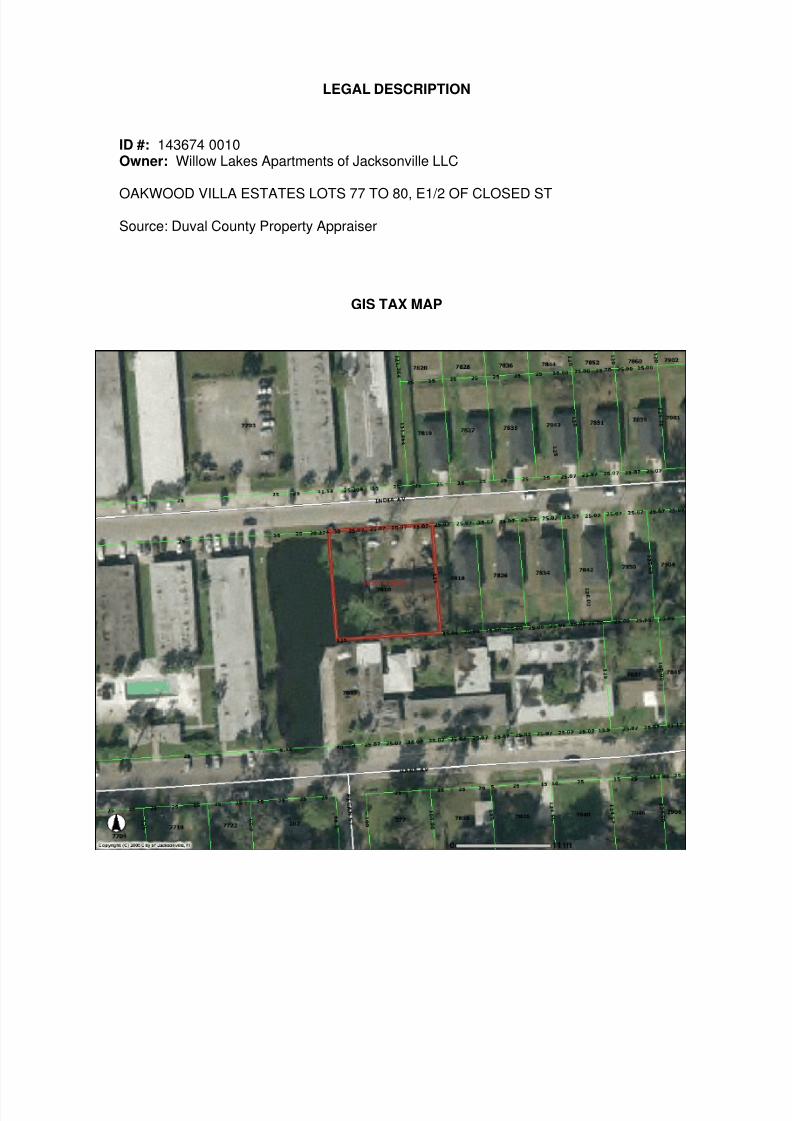

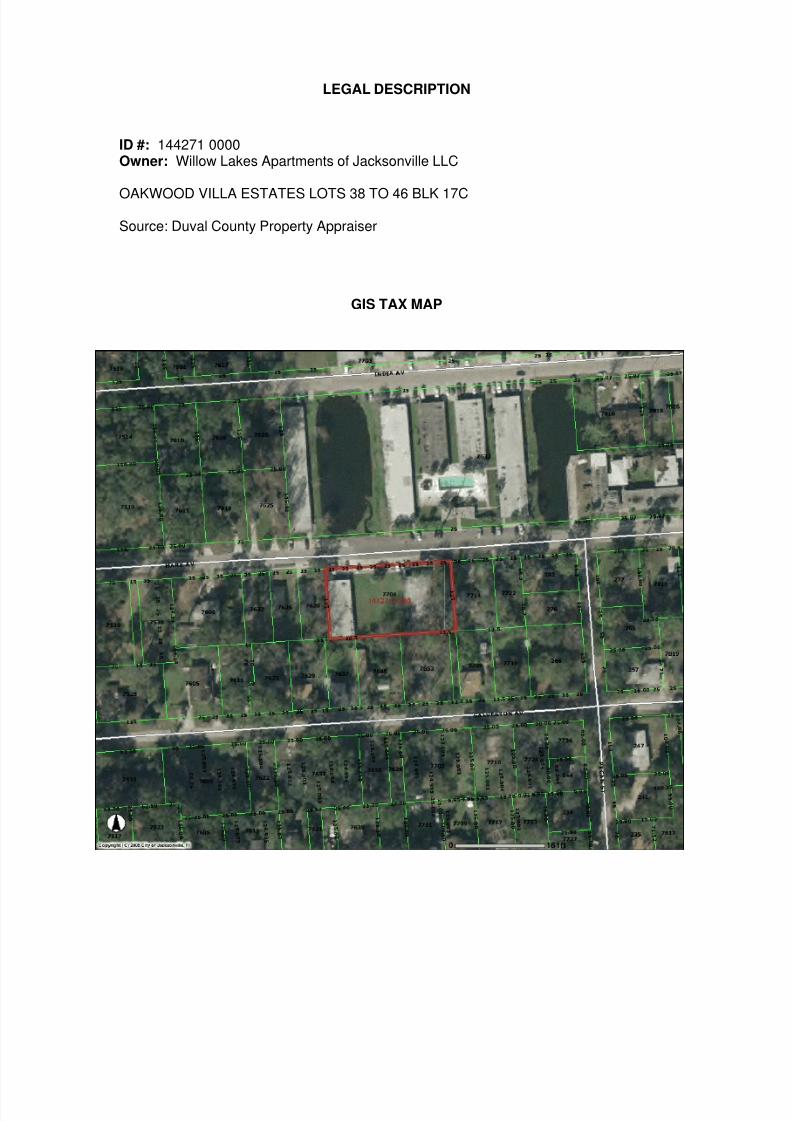

Assessor’s Parcel Nos.: 143499 0010, 143505 0010, 143626 0000, 143633 0000,143639 0000, 143674 0010, and 144271 0000

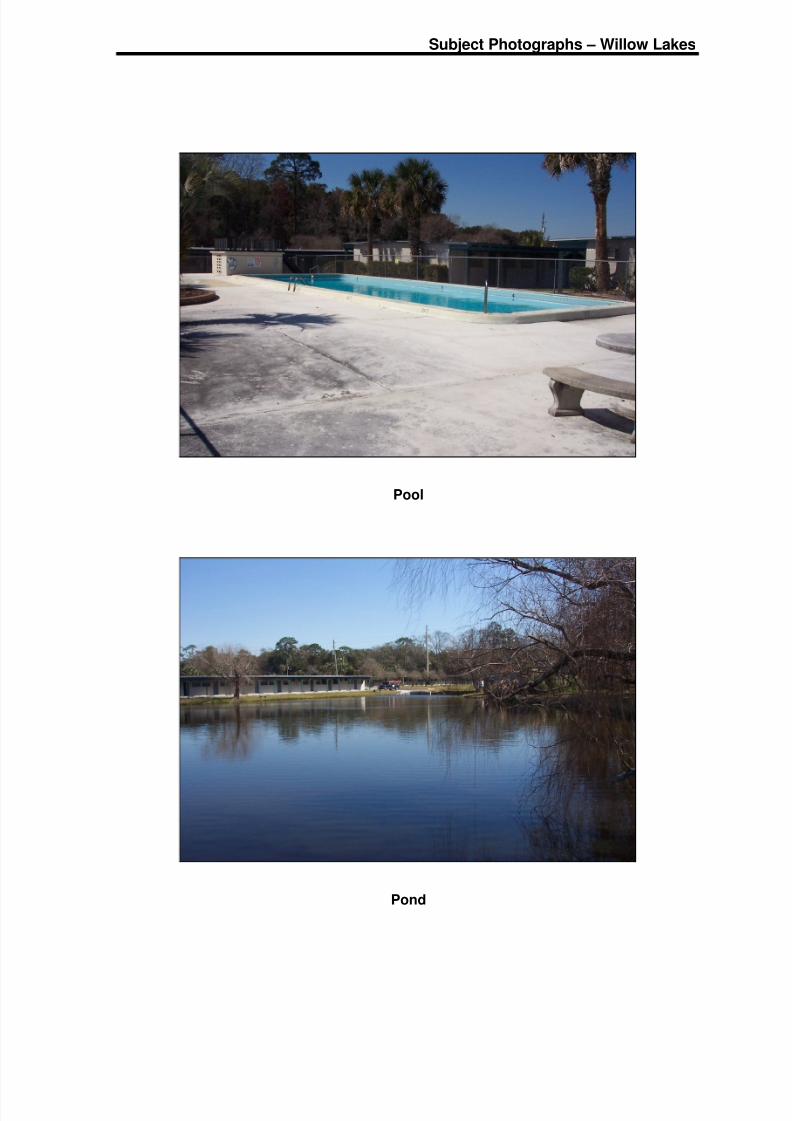

Property Description: The subject is a 350-unit apartment complex on 10.83 acres.The complex consists of 27 one- and two-story apartmentbuildings and was reportedly constructed between 1963 and1969. The unit mix includes studio, efficiency, and one- andtwo-bedroom units ranging from 320 to 1,000 square feet.Property amenities include onsite management, pool, fitnesscenter, laundry facility, and a pool. The buildings featuretraditional design with painted stucco over concrete blockexterior walls and built-up roofs. The property is in overall fairto average condition. According to the provided rent roll,there are 23 vacant units

Highest and Best Use As though vacant: Development of multi-familyimprovements. As improved: Continued operation of anapartment complex.

Purpose of the Appraisal: To estimate the “as is” market value of the fee simple interestin the subject property.

Intended Use of Report: For use by Johnson Capital as an aid in loan underwritingdecisions.

Property Rights Appraised: Fee simple interest

Date of Value / Inspection: March 3, 2010

Estimated Marketing Time: Twelve months or less

Valuation

Estimate of “As Is” Market Value of the Fee Simple Interest in the SubjectWillow Lakes Apartments, as of March 3, 2010: $9,000,000

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 6/86

TABLE OF CONTENTS

ii

INTRODUCTION..........................................................................................................................1

LOCATION ANALYSIS ................................................................................................................ 4

PROPERTY ANALYSIS............................................................................................................. 12

MARKET ANALYSIS ................................................................................................................. 18

HIGHEST AND BEST USE ....................................................................................................... 24

APPRAISAL METHODOLOGY ................................................................................................. 25

INCOME CAPITALIZATION APPROACH................................................................................. 26

SALES COMPARISON APPROACH ........................................................................................35

RECONCILIATION OF VALUE .................................................................................................39

ADDENDAA SUBJECT PHOTOGRAPHS

B SITE PLAN, TAX PLATS, SURVEY, AND LEGAL DESCRIPTIONC LOCATION AND FLOOD MAPSD UNIT FLOOR PLANSE RENT COMPARABLES AND MAPF IMPROVED SALE COMPARABLES AND MAPG ASSUMPTIONS AND LIMITING CONDITIONSH ENGAGEMENT LETTERI QUALIFICATIONS

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 7/86

INTRODUCTION

1

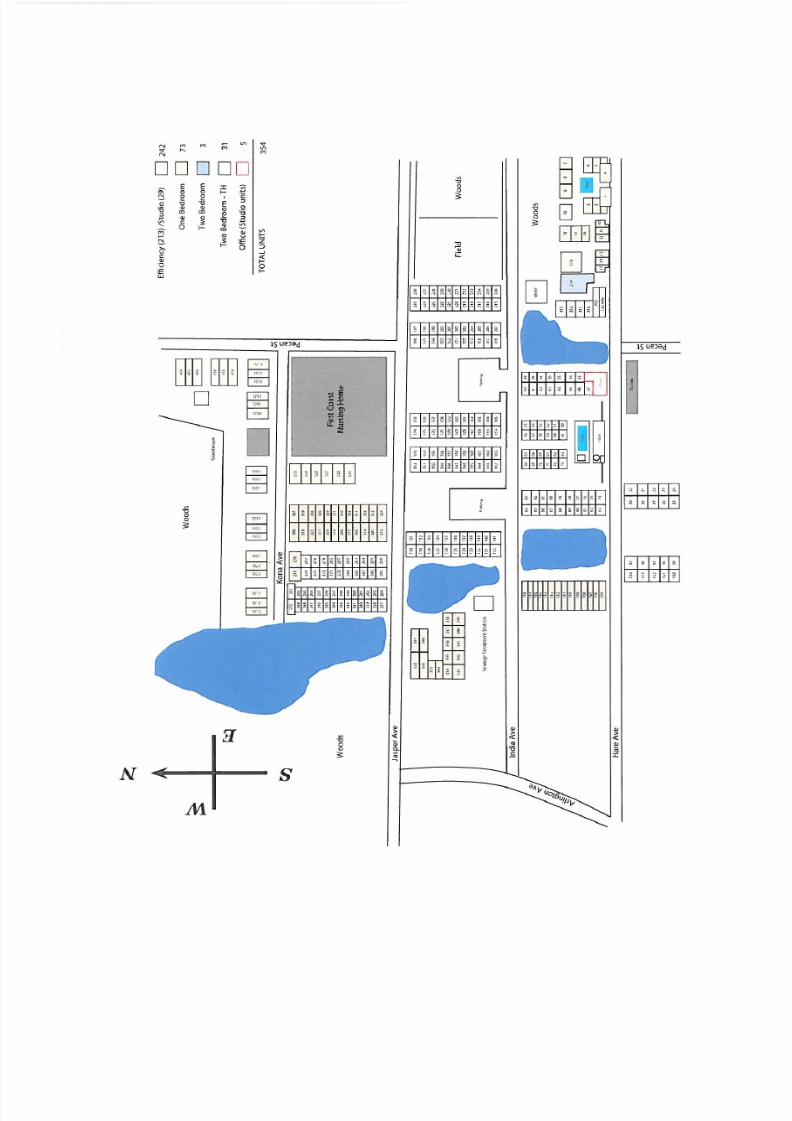

PROPERTY IDENTIFICATION

The subject is a 350-unit apartment complex on 10.83 acres. It is located along Hare,

India, and Jasper Avenues just east of Arlington Road in the city of Jacksonville, Duval

County, Florida. This location is less than 0.50 mile south of the Arlington Expressway and

about four miles east of downtown Jacksonville and I-95. The complex consists of 27 one-

and two-story apartment buildings and was reportedly constructed between 1963 and 1969.

The unit mix includes studio, efficiency, and one- and two-bedroom units ranging from 320 to

1,000 square feet. Property amenities include onsite management, pool, fitness center,

laundry facility, and a pool. The buildings feature traditional design with painted stucco over

concrete block exterior walls and built-up roofs. The property is in overall fair to average

condition. According to the provided rent roll, there are 23 vacant units. The property’s street

address is 7703 Hare Avenue and it is identified as tax parcels 143499 0010, 143505 0010,

143626 0000, 143633 0000, 143639 0000, 143674 0010, and 144271 0000.

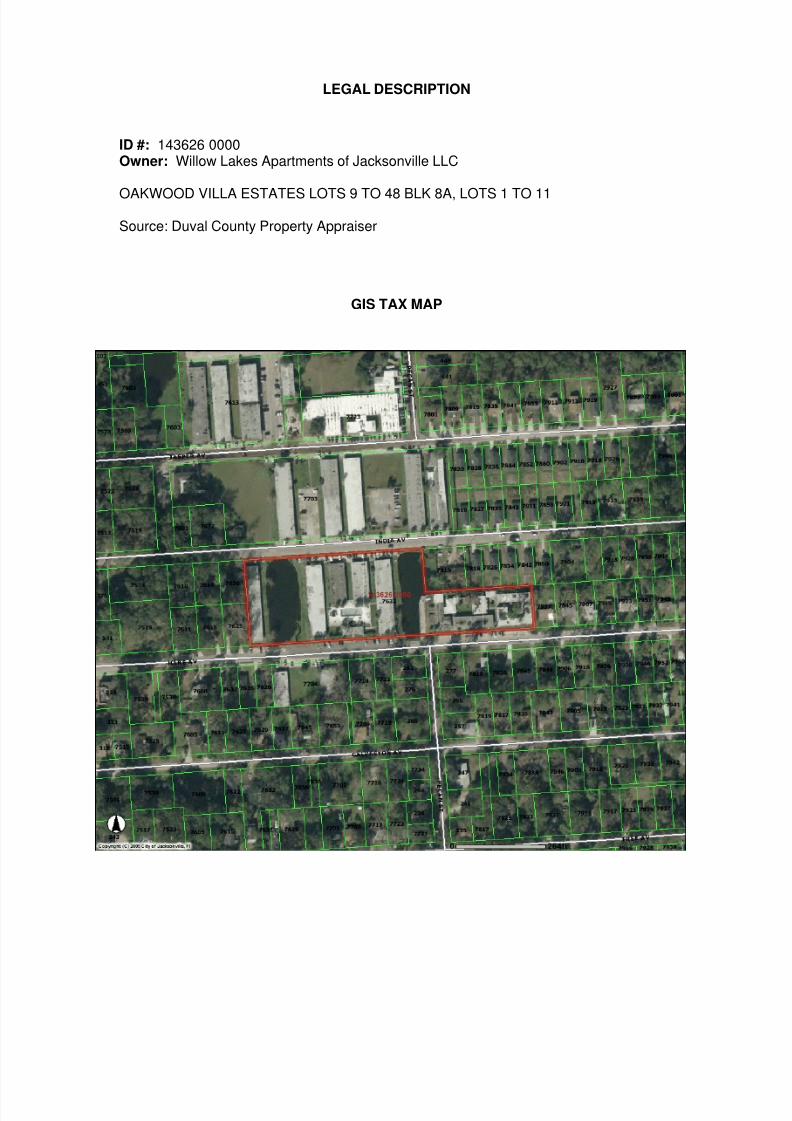

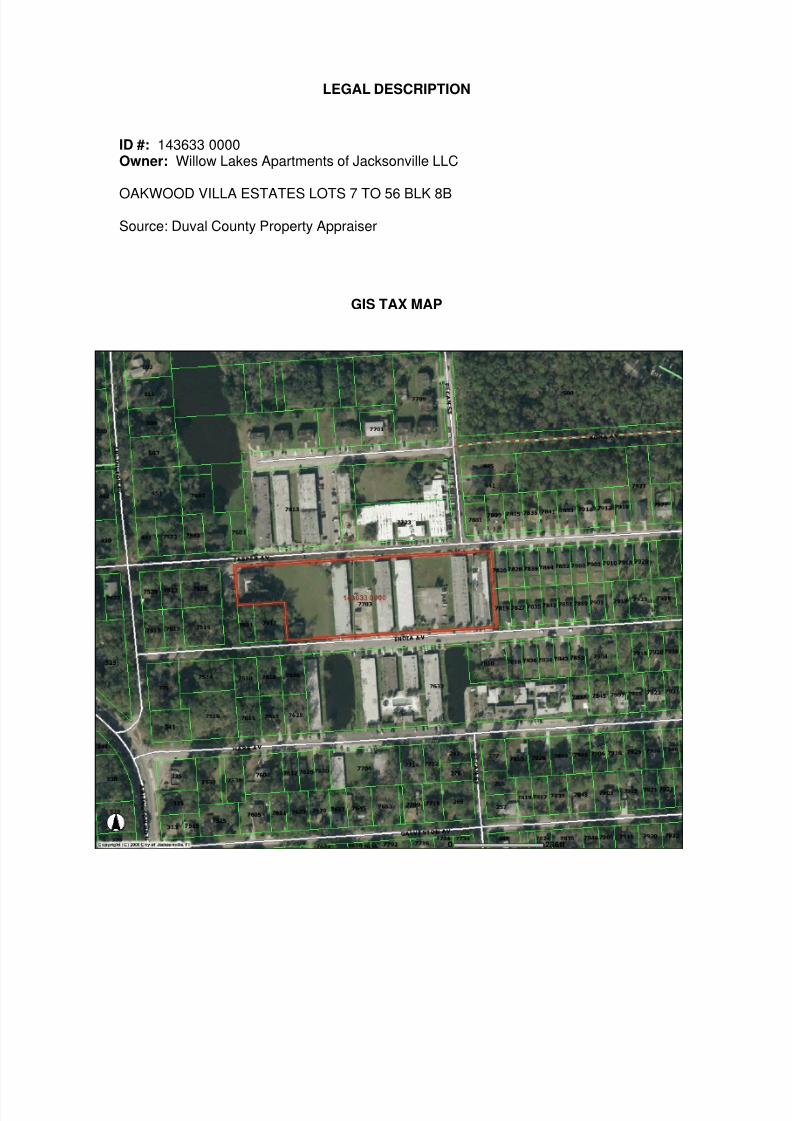

OWNERSHIP AND PROPERTY HISTORY

According to Duval County tax records the property is owned by Willow Lakes

Apartments of Jacksonville, LLC. This entity acquired the property from Rivermont Properties,

Inc. on May 11, 2009 through a special warranty deed for $6.5 million. We were provided a

copy of a purchase and sale contract that was first signed on November 18, 2009 by Alan

Jones, grantee. The grantor is identified as Willow Lakes Apartments of Jacksonville, LLC

and the indicated purchase price is $9.5 million. We are aware of no transactions, offers, or

contracts involving the subject within the last three years.

PURPOSE AND INTENDED USE OF THE APPRAISAL

The purpose of this appraisal is to estimate the "as is" market value of the fee simple

interest in the subject property. This appraisal is intended for use by Johnson Capital as an

aid in loan underwriting decisions.

DATES OF INSPECTION AND VALUATION

Timothy P. Huber inspected the subject properties and prepared this report. The date

of inspection and valuation is March 3, 2010. The value reported is predicated upon market

conditions prevailing as of this date.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 8/86

Introduction

2

DEFINITION OF MARKET VALUE

Market value means the most probable price a property should bring in a competitive

and open market under all conditions requisite to a fair sale, the buyer and seller each acting

prudently and knowledgeably, and assuming the price is not affected by undue stimulus.

Implicit in this definition is the consummation of a sale as of a specified date and the passingof title from seller to buyer under conditions whereby:

1. buyer and seller are typically motivated;

2. both parties are well informed or well advised, and acting in what they considertheir own best interests;

3. a reasonable time is allowed for exposure in the open market;

4. payment is made in terms of cash in U.S. dollars or in terms of financialarrangements comparable thereto; and,

5. the price represents the normal consideration for the property sold unaffected by

special or creative financing or sales concessions granted by anyone associatedwith the sale.1

PROPERTY RIGHTS APPRAISED

We have appraised the fee simple estate, or interest, in the subject property. Real

properties have multiple rights inherent with ownership. These include the right to sell, to

lease, to give away, or to occupy, among other rights. Often referred to as the “bundle of

rights”, an owner who enjoys all the rights in this bundle owns the fee simple title.

“Fee title” is the greatest right and title an individual can hold in real property. Itis “free and clear” ownership subject only to the governmental rights of policepower, taxation, eminent domain and escheat reserved to federal, state, andlocal governments2.

APPRAISAL DEVELOPMENT AND REPORTING PROCESS

We completed the following steps for this assignment:

1. Analyzed regional, city, neighborhood, site, and improvement data.

2. Inspected the subject site and the neighborhood.

1The Office of the Comptroller of the Currency under 12 CFR, Part 34, Subpart C-Appraisals, ♣34.42(f), August 24,

1990. This definition is compatible with the definition of market value contained in The Dictionary of Real Estate Appraisal , Third Edition, and the Uniform Standards of Professional Appraisal Practice adopted by the AppraisalStandards Board of The Appraisal Foundation, 1995 edition. This definition is also compatible with the OTS, FDIC,NCUA, and the Board of Governors of the Federal Reserve System definition of market value.2 The Dictionary of Real Estate Appraisal , Appraisal Institute, Third Edition, 1993

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 9/86

Introduction

3

3. Reviewed data regarding taxes, zoning, utilities, easements, and services.

4. Considered improved sales, as well as comparable rentals. Confirmed data withprincipals, managers, or real estate agents representing principals, unlessotherwise noted.

5. Analyzed the data to arrive at concluded estimates of value via each applicable

approach.

6. Reconciled the results of each approach to value employed into a probable rangeof market data and finally an estimate of value for the subject, as defined herein.

7. Estimated reasonable exposure and marketing times associated with the valueestimate.

The site and improvement descriptions included in this report are based on a personal

inspection of the subject property, information provided by the owner (survey and phase I

ESA), property management, selling broker (financing package), Duval County tax records,

and our knowledge of similar type properties. Not available were building plans, property

condition studies, geotechnical reports. While the available information is adequate forvaluation purposes, our investigations are not a substitute for formal engineering studies.

This is a self-contained report, which is intended to comply with the reporting

requirements set forth under Standards Rule 2-2(a) of the Standards of Professional Appraisal

Practice. The value estimates reflect all known information about the subject, market

conditions, and available data. The self-contained report incorporates to the fullest extent

possible, a practical explanation of the data, reasoning and analysis used to develop the

opinions of value. It also includes thorough descriptions of the subject and the market for the

property type.

SPECIAL APPRAISAL INSTRUCTIONS

As mentioned above, we were asked to appraise the subject “as is”. The following

definition pertains to the value estimate provided in this report.

Market Value “As Is” on Appraisal Date

An estimate of the market value of a property in the condition observed upon inspection

and as it physically and legally exists without hypothetical conditions, assumptions, orqualifications as of the date the appraisal is prepared.

Market value “as is” assumes a typical marketing period, which we have estimated at12 months or less.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 10/86

LOCATION ANALYSIS

4

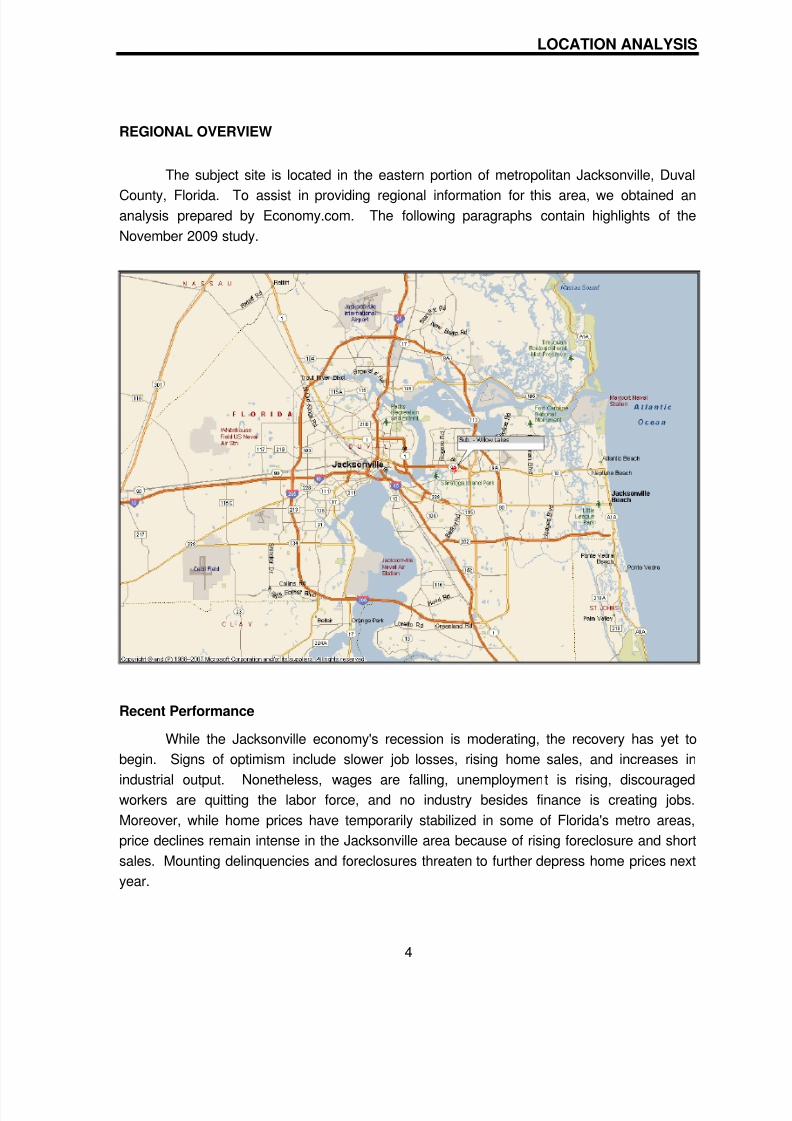

REGIONAL OVERVIEW

The subject site is located in the eastern portion of metropolitan Jacksonville, Duval

County, Florida. To assist in providing regional information for this area, we obtained ananalysis prepared by Economy.com. The following paragraphs contain highlights of the

November 2009 study.

Recent Performance

While the Jacksonville economy's recession is moderating, the recovery has yet to

begin. Signs of optimism include slower job losses, rising home sales, and increases in

industrial output. Nonetheless, wages are falling, unemployment is rising, discouragedworkers are quitting the labor force, and no industry besides finance is creating jobs.

Moreover, while home prices have temporarily stabilized in some of Florida's metro areas,

price declines remain intense in the Jacksonville area because of rising foreclosure and short

sales. Mounting delinquencies and foreclosures threaten to further depress home prices next

year.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 11/86

Location Analysis

5

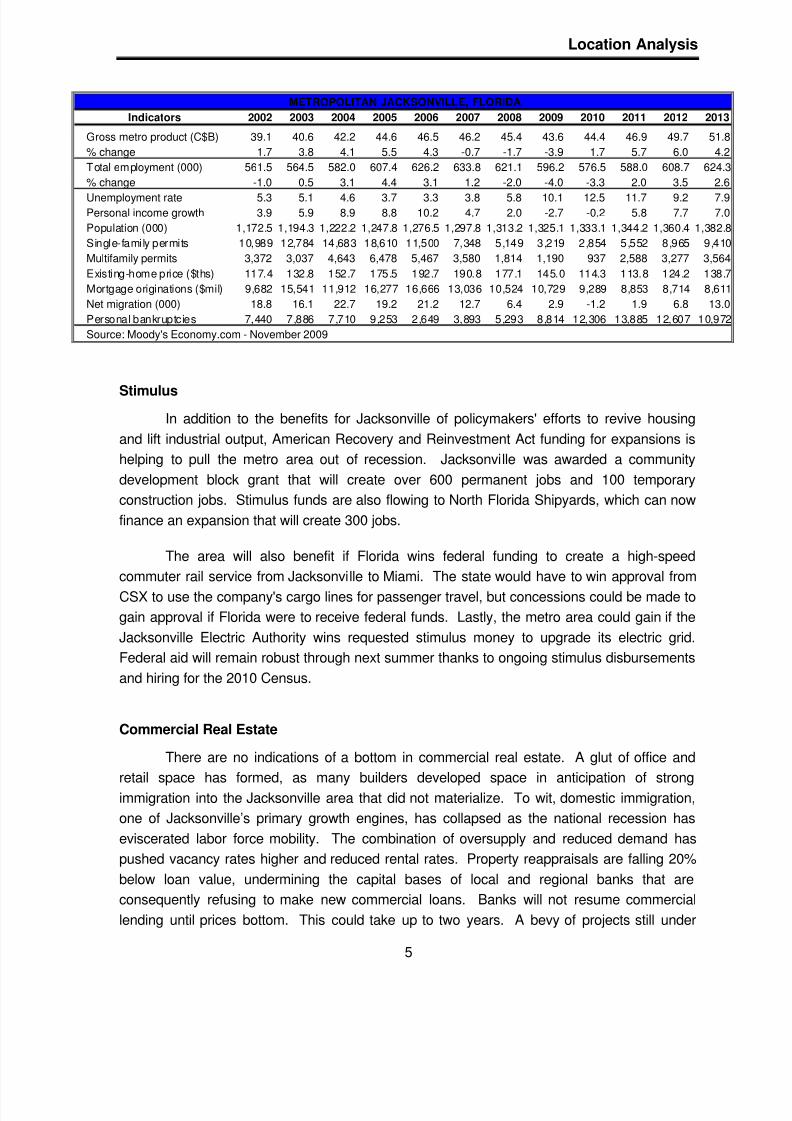

Indicators 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gross metro product (C$B) 39.1 40.6 42.2 44.6 46.5 46.2 45.4 43.6 44.4 46.9 49.7 51.8

% change 1.7 3.8 4.1 5.5 4.3 -0.7 -1.7 -3.9 1.7 5.7 6.0 4.2

Total employment (000) 561.5 564.5 582.0 607.4 626.2 633.8 621.1 596.2 576.5 588.0 608.7 624.3

% change -1.0 0.5 3.1 4.4 3.1 1.2 -2.0 -4.0 -3.3 2.0 3.5 2.6

Unemployment rate 5.3 5.1 4.6 3.7 3.3 3.8 5.8 10.1 12.5 11.7 9.2 7.9Personal income growth 3.9 5.9 8.9 8.8 10.2 4.7 2.0 -2.7 -0.2 5.8 7.7 7.0

Population (000) 1,172.5 1,194.3 1,222.2 1,247.8 1,276.5 1,297.8 1,313.2 1,325.1 1,333.1 1,344.2 1,360.4 1,382.8

Single-family permits 10,989 12,784 14,683 18,610 11,500 7,348 5,149 3,219 2,854 5,552 8,965 9,410

Multifamily permits 3,372 3,037 4,643 6,478 5,467 3,580 1,814 1,190 937 2,588 3,277 3,564

Existing-home price ($ths) 117.4 132.8 152.7 175.5 192.7 190.8 177.1 145.0 114.3 113.8 124.2 138.7

Mortgage originations ($mil) 9,682 15,541 11,912 16,277 16,666 13,036 10,524 10,729 9,289 8,853 8,714 8,611

Net migration (000) 18.8 16.1 22.7 19.2 21.2 12.7 6.4 2.9 -1.2 1.9 6.8 13.0

Personal bankruptcies 7,440 7,886 7,710 9,253 2,649 3,893 5,293 8,814 12,306 13,885 12,607 10,972

Source: Moody's Economy.com - November 2009

METROPOLITAN JACKSONVILLE, FLORIDA

Stimulus

In addition to the benefits for Jacksonville of policymakers' efforts to revive housing

and lift industrial output, American Recovery and Reinvestment Act funding for expansions is

helping to pull the metro area out of recession. Jacksonville was awarded a community

development block grant that will create over 600 permanent jobs and 100 temporary

construction jobs. Stimulus funds are also flowing to North Florida Shipyards, which can now

finance an expansion that will create 300 jobs.

The area will also benefit if Florida wins federal funding to create a high-speed

commuter rail service from Jacksonville to Miami. The state would have to win approval from

CSX to use the company's cargo lines for passenger travel, but concessions could be made to

gain approval if Florida were to receive federal funds. Lastly, the metro area could gain if the

Jacksonville Electric Authority wins requested stimulus money to upgrade its electric grid.

Federal aid will remain robust through next summer thanks to ongoing stimulus disbursements

and hiring for the 2010 Census.

Commercial Real Estate

There are no indications of a bottom in commercial real estate. A glut of office and

retail space has formed, as many builders developed space in anticipation of strong

immigration into the Jacksonville area that did not materialize. To wit, domestic immigration,

one of Jacksonville’s primary growth engines, has collapsed as the national recession has

eviscerated labor force mobility. The combination of oversupply and reduced demand has

pushed vacancy rates higher and reduced rental rates. Property reappraisals are falling 20%

below loan value, undermining the capital bases of local and regional banks that are

consequently refusing to make new commercial loans. Banks will not resume commercial

lending until prices bottom. This could take up to two years. A bevy of projects still under

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 12/86

Location Analysis

6

construction such as The Urbana in Jacksonville Beach and Doctor's Village in northwest St.

Johns County threaten to forestall the recovery in the local commercial real estate market.

International Trade

Jacksonville’s trade industry has strong long-term prospects. To be sure, the global

recession has slowed investment in JAXPORT. The port authority will do more maintenance

than expansion next year, and Hanjin Shipping has delayed the completion of its container

terminal, which will triple the port's handling capacity, until 2013. Nonetheless, the expansion

of the Panama Canal in 2014 has the potential of making Jacksonville one of the largest ports

on the East Coast. To realize its potential, the metro area must soon begin widening its river

channel to handle post-Panamax mega cargo ships. A better business climate, rail

infrastructure, and its location in the fast-growing South make Jacksonville a very attractive

shipping port.

Summary and Conclusions

Despite the efforts of the federal government, weak population growth and woeful

commercial and residential real estate markets will prevent the Jacksonville economy from

stabilizing before next summer. In the long term, a strong military presence, growing

prominence as an international trade port, and robust demographic trends ensure that

metropolitan Jacksonville will be an above average performer.

NEIGHBORHOOD OVERVIEW

Location and Boundaries

The subject is located along Hare, India, and Jasper Avenues just east of Arlington

Road in the city of Jacksonville, Duval County, Florida. This location is less than 0.50 mile

south of the Arlington Expressway and about four miles east of downtown Jacksonville and I-

95.

The subject’s neighborhood can be generally defined as being bound by the St. Johns

River to the north, J. Turner Butler Boulevard/FL Hwy. 202 to the south, SouthsideBoulevard/FL Hwy. 115 to the east, and San Jose Boulevard/Hendricks Avenue/FL Hwy 13 to

the west. The subject's immediate neighborhood is a mature mix of single- and multi-family

mixed with commercial uses along the primary traffic corridors.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 13/86

Location Analysis

7

Accessibility and Availability of Utilities

Interstate 95 extends along the eastern seaboard through Jacksonville. It is a multi-

lane right-of-way with limited access that traverses the western portion of the neighborhood in

a generally north/south direction. Phillips Highway/U.S. Highway 1 more or less parallels I-95

in the western portion of the neighborhood. This roadway extends along the easternseaboard through Jacksonville. It is a four-lane asphalt-paved right-of-way with center turn

lane that serves as a neighborhood thoroughfare. Properties along the road include privately

owned motels, offices, a neighborhood shopping center, retail business and restaurants.

University Boulevard extends north from San Jose Boulevard across Beach Boulevard

and Atlantic Boulevard to the Redi Point area. It is a four-lane asphalt-paved roadway that

traverses the west central portion of the neighborhood. Hendricks Avenue is a four-lane

asphalt-paved right-of-way with median and center turn lane. It extends north from the

southern portion of the neighborhood to the St. Johns River area in the northern portion of the

neighborhood. Properties along the thoroughfare include neighborhood shopping centers,offices, restaurants, and residential communities.

Emerson Street bisects the neighborhood as a major east/west thoroughfare. Also

extending East/West is J. Turner Butler Boulevard, which is a connector road from Interstate

95 in the west to S.R. A1A in the east. Atlantic Boulevard leads east from the San Marco area

of the neighborhood and extends to the Atlantic Ocean. It is a four-lane asphalt surfaced

roadway with several residential developments off of this road, which is developed with retail

and service establishments. Beach Boulevard serves the same purpose as Atlantic Boulevard.

However, it is located about three miles south of Atlantic Boulevard serving another area of

the neighborhood. It is a four-lane asphalt-paved road.

As shown in the neighborhood map in the addenda, there are numerous roads within

the neighborhood, and they were more or less designed in a grid system. Most of these

streets are two-laned, but have high traffic volumes. All have relatively easy access to

Interstate 95.

Utilities available in this neighborhood include public water, sewer, electricity, and

telephone. All standard municipal services are also provided, including police and fire

protection.

Land Use

The neighborhood is approximately 95% developed. The neighborhood is primarily

residential with mixed residential and commercial located along major thoroughfares. The

majority of the industry is in the south and the east portion of the neighborhood, and the

neighborhood is mostly residential nearer to the St. Johns River. There is a full array of

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 14/86

Location Analysis

8

community services, including churches, schools, hospitals, and recreational facilities within

the neighborhood.

Most of the newer construction and redevelopment is in the San Marco area and the

area along U.S. Highway 1 near its intersection with Emerson Street. State Road 13 is mostly

developed, and Emerson Street continues to transition from residential to commercial use.The portion of the neighborhood near and along U. S. Highway 1 is improved with commercial

properties, flex space, and office/warehouse/distribution facilities. A business park is located

north of University Boulevard, west of U. S. Highway 1.

The northern portion of the neighborhood, known as the San Marco area, has recently

undergone renovation and redevelopment. The area along the south-bank of the St. Johns

River is developed with commercial properties including Baptist Medical Center, high-rise and

single-story office buildings, restaurants, and hotels. This area was once home to several light

industrial and warehousing facilities, many of which have been renovated to retain their

original style of architecture with their use changed to office or commercial facilities. South ofthe riverfront, land uses are primarily commercial along the corridors of San Marco Boulevard,

Hendricks Avenue, and Kings Avenue. At the juncture of San Marco Boulevard, Hendricks

Avenue, and Atlantic Boulevard is the San Marco shopping area that centers on a park

concept with green space and a gazebo. What began as a residential area for those working

across the river in downtown Jacksonville in the early 1900’s has evolved into a desirable

cosmopolitan area of Jacksonville. The City of Jacksonville has targeted San Marco for

infrastructure improvement as part of the Better Jacksonville Plan, and efforts for road and

drainage improvements are underway. As the San Marco area continues to improve,

gentrification of adjacent areas has increased the desirability of areas like Miramar and St.

Nicholas.

Multi-family developments in the subject neighborhood are primarily in proximity to the

main corridors including University Boulevard, Arlington Expressway, Merrill Road, Ft.

Caroline Road, Townsend Boulevard and Monument Road. The University Boulevard to

Merrill Road area was developed with apartment communities during the 1950’s and 1960’s.

Apartment growth moved east during the 1970’s and 1980’s.

There are several neighborhood shopping centers located along Beach Boulevard,

Atlantic Boulevard, University Boulevard, Merrill Road and Ft. Caroline Road. The Regency

Square Mall is located at the northwest corner of Atlantic Boulevard and Monument Road. It

was developed during the mid 1960’s and has had several subsequent additions. It serves

residents in Greater Arlington, Northside and parts of Southside. The Avenues Regional Mall

is the newest mall in the Greater Jacksonville Area. It opened in 1991 and the tenants include

several national retailers. The mall coupled with several auto dealerships, restaurants and

neighborhood shopping centers are major area employers. It is located on the west side of

the west boundary of the neighborhood, Southside Boulevard.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 15/86

Location Analysis

9

The Jacksonville beaches are located within a 15-minute drive from the neighborhood.

Ft. Caroline 53 National Park is located off Ft. Caroline Road along the St. Johns River. The

park includes a museum, lookout bluff (St. Johns River) and a replica of a 17 th century fort

located near the original fort’s site. There are several public parks throughout the

neighborhood to accommodate out-door sports. Also, the St. Johns River is nearby for water

related activities. Craig Airport is located in the northeast quadrant of St. Johns Bluff Road and

Atlantic Boulevard. The airport is city owned and serves small private aircraft.

Uses immediately surrounding the subject mostly include single-family, duplexes or

vacant residential lots. The First Coast Health & Rehabilitation Center is located at the

northwest Corner of Jasper Avenue and Pecan Street.

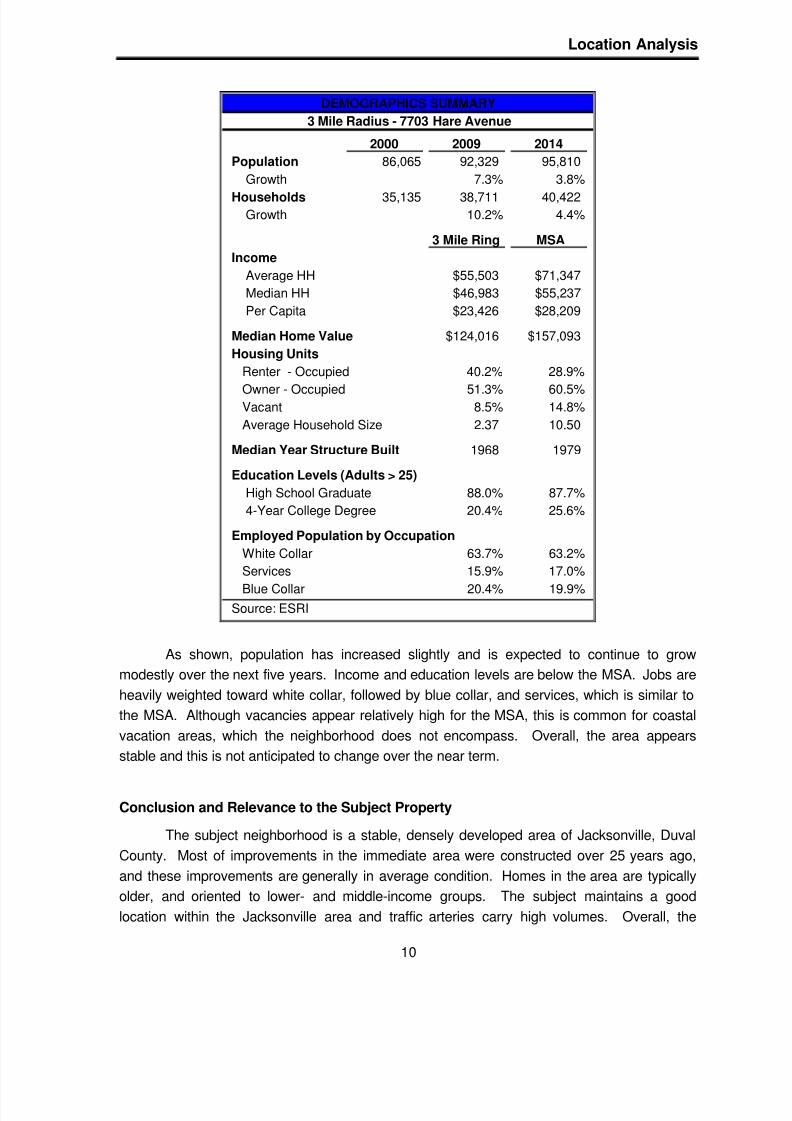

Demographics

To gain additional insight into the characteristics of the subject’s neighborhood, we

reviewed a demographic study prepared by ESRI through STDBonline. The following

information primarily pertains to a three-mile radius around the subject. The full demographic

study is retained in our files.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 16/86

Location Analysis

10

2000 2009 2014

Population 86,065 92,329 95,810

Growth 7.3% 3.8%

Households 35,135 38,711 40,422Growth 10.2% 4.4%

3 Mile Ring MSA

Income

Average HH $55,503 $71,347

Median HH $46,983 $55,237

Per Capita $23,426 $28,209

Median Home Value $124,016 $157,093

Housing Units

Renter - Occupied 40.2% 28.9%

Owner - Occupied 51.3% 60.5%Vacant 8.5% 14.8%

Average Household Size 2.37 10.50

Median Year Structure Built 1968 1979

Education Levels (Adults > 25)

High School Graduate 88.0% 87.7%

4-Year College Degree 20.4% 25.6%

Employed Population by Occupation

White Collar 63.7% 63.2%

Services 15.9% 17.0%

Blue Collar 20.4% 19.9%Source: ESRI

DEMOGRAPHICS SUMMARY

3 Mile Radius - 7703 Hare Avenue

As shown, population has increased slightly and is expected to continue to grow

modestly over the next five years. Income and education levels are below the MSA. Jobs are

heavily weighted toward white collar, followed by blue collar, and services, which is similar to

the MSA. Although vacancies appear relatively high for the MSA, this is common for coastal

vacation areas, which the neighborhood does not encompass. Overall, the area appears

stable and this is not anticipated to change over the near term.

Conclusion and Relevance to the Subject Property

The subject neighborhood is a stable, densely developed area of Jacksonville, Duval

County. Most of improvements in the immediate area were constructed over 25 years ago,

and these improvements are generally in average condition. Homes in the area are typically

older, and oriented to lower- and middle-income groups. The subject maintains a good

location within the Jacksonville area and traffic arteries carry high volumes. Overall, the

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 17/86

Location Analysis

11

neighborhood is a fairly desirable location for apartment developments. The subject is a

complementary use for the area, and we are aware of no negative factors associated with the

area that should have an impact on the property now or in the foreseeable future.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 18/86

PROPERTY ANALYSIS

12

The site and improvement descriptions included in this section are based on a

personal inspection of the subject property, information provided by the owner (survey and

phase I ESA), property management, selling broker (financing package), Duval County tax

records, and our knowledge of similar type properties. Not available were building plans,

property condition studies, geotechnical reports. While the available information is adequate

for valuation purposes, our investigations are not a substitute for formal engineering studies.

SITE DESCRIPTION

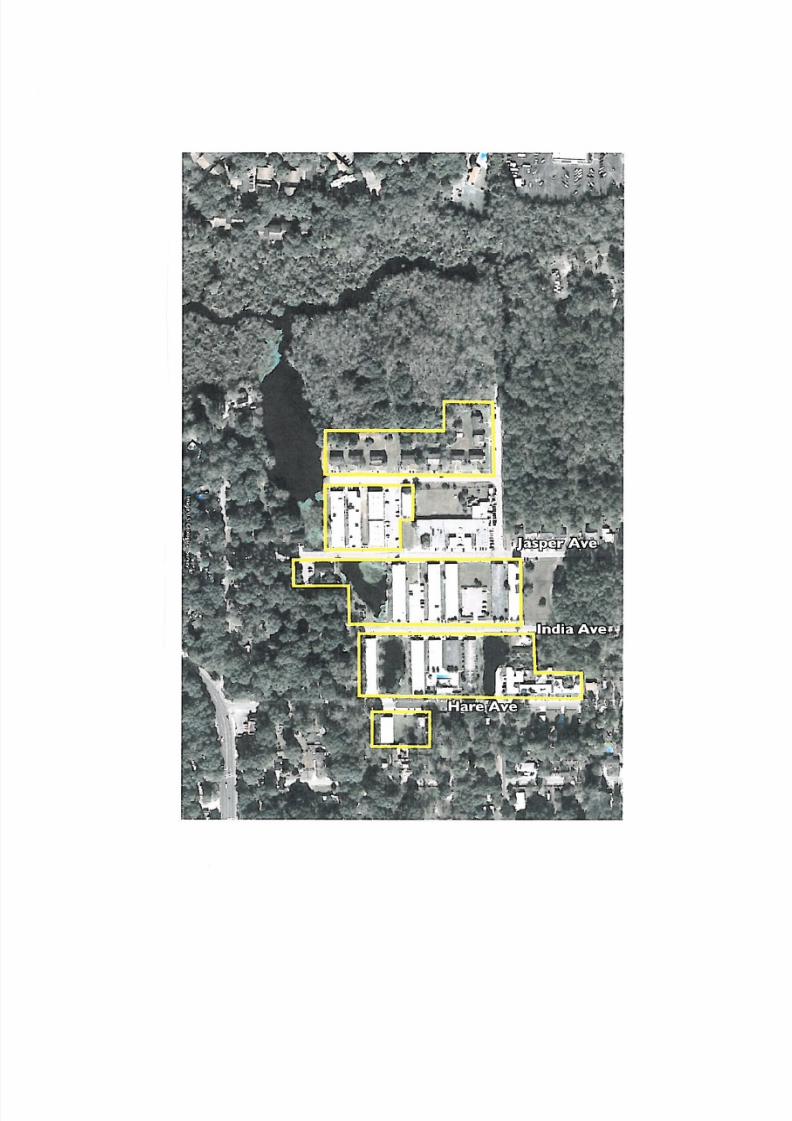

Location: The property consists of seven noncontiguous parcels withfrontage along Hare, India, Jasper and Knox Avenues within thecity limits of Jacksonville, Duval County, Florida.

Assessor’s Parcel Nos. 143499 0010, 143505 0010, 143626 0000, 143633 0000, 1436390000, 143674 0010, and 144271 0000

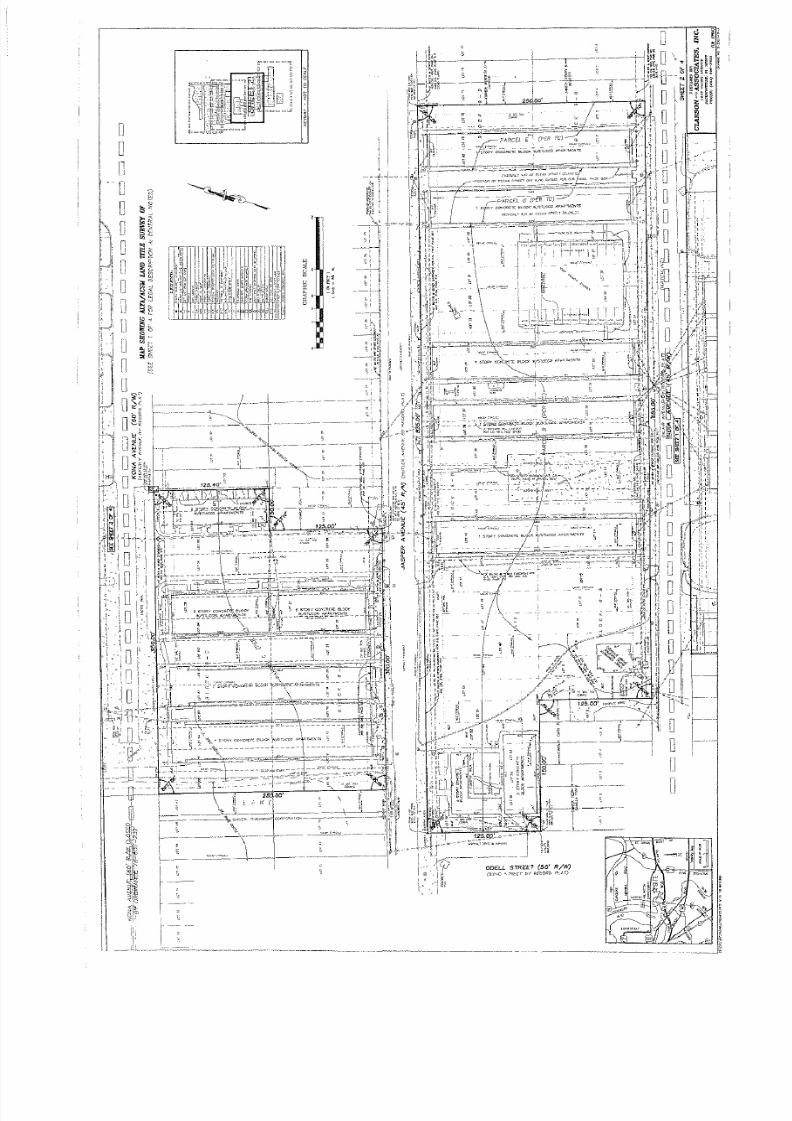

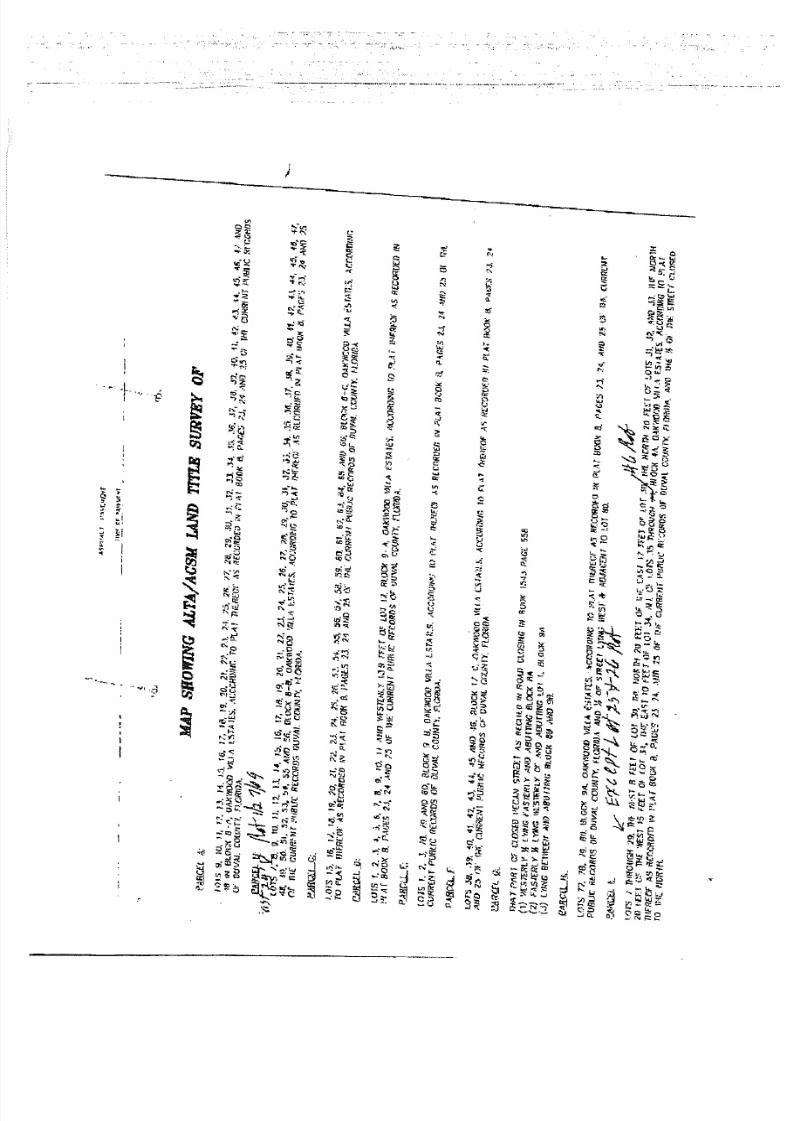

Land Area: According to the owner, the total land area is 10.83 acres(471,737.5 SF). Duval County tax records indicate 10.76 acres.The provided survey, which is included in the addenda,encompasses 24.18 acres, but includes vacant land areas that arenot part of the subject of this appraisal.

Property Status: The site is improved with a 350-unit apartment complex consistingof 27 one- and two-story apartment buildings.

Shape and Frontage: The property consists of seven noncontiguous parcels withfrontage along Hare, India, Jasper and Knox Avenues.

Ingress and Egress: There are no interior roadways within the development, all theparcels front on public streets that are city maintained. Parking islocated along the frontage roads.

Topography andDrainage:

The parcels feature generally level topographies, and they are atgrade with their frontage roads. Overall, the development has agentle downward northerly slope. The parking areas appear tohave been prepared in such a manner as to facilitate drainagealong the frontage roads toward three onsite ponds..

Soils: We were not provided a geotechnical report. We assume that thesites can support the existing improvements both now and into the

future. We have no expertise in this area.

Easements: We were provided an ALTA/ACSM survey prepared by Carsonand Associates, Inc. and dated December 19, 2006. Easementsindicated appear to be only for utilities that serve the subjectimprovements and do not appear to be detrimental. During ourinspection of the site we noted no other easements. This analysisassumes that there are no detrimental easements.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 19/86

Property Analysis

13

Covenants, Conditions,and Restrictions:

We are not aware of any deed restrictions, or restrictingcovenants, other than zoning.

Utilities/Services: Utilities available to the subject include water, sanitary and stormsewer, electricity, and telephone. Services include police and fire

protection.

Flood Zone: According to FEMA, the subject is on Flood Insurance Rate MapNumber 120077 0164 E which was revised August 15, 1989.Most of the site appears to be in Zone X, which is described asareas determined to be outside the 500-year flood. However, aportion of the site appears to be in Zone AE, which his describedas a flood plain where base flood elevations are provided. Basedon a review of the the provided ALTA/ACSM survey prepared byCarson and Associates, Inc. and dated December 19, 2006 theimprovements appear to be in Zone X.

Environmental Issues: We were provided a Phase I Environmental Site AssessmentUpdate prepared by Environmental Services, Inc. dated July 16,2008. Although the report identifies offsite “suspect environmentalcondition”, but goes on to state that they “are not contaminationthreats to the property”. In addition, laboratory analysis of on sitegroundwater samples collected from monitoring wells yieldedresults that were below detection limits and/or regulatory agencylimits. Therefore, the report states that ESI “does not recommendadditional environmental assessment of the property at this time”.

The value estimate rendered in this report is predicated on theassumption that there is no hazardous material on or in theproperty, including land and improvements, which would cause a

loss in value.

Conclusion: The subject site is considered to have adequate overall physicalutility for its current use. This is based on its size, shape,topography, accessibility, and availability of all utilities andservices. Additionally, it is our opinion that the improvementsreflect good utilization of the sites physical characteristics.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 20/86

Property Analysis

14

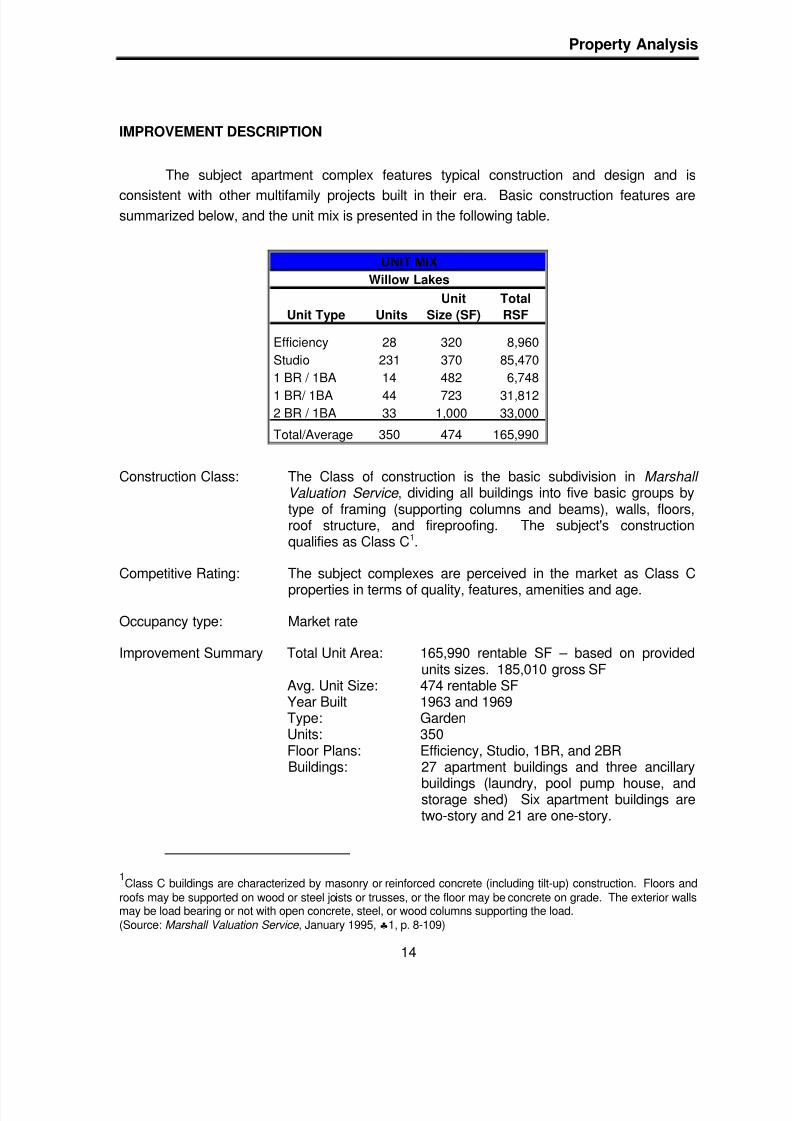

IMPROVEMENT DESCRIPTION

The subject apartment complex features typical construction and design and is

consistent with other multifamily projects built in their era. Basic construction features aresummarized below, and the unit mix is presented in the following table.

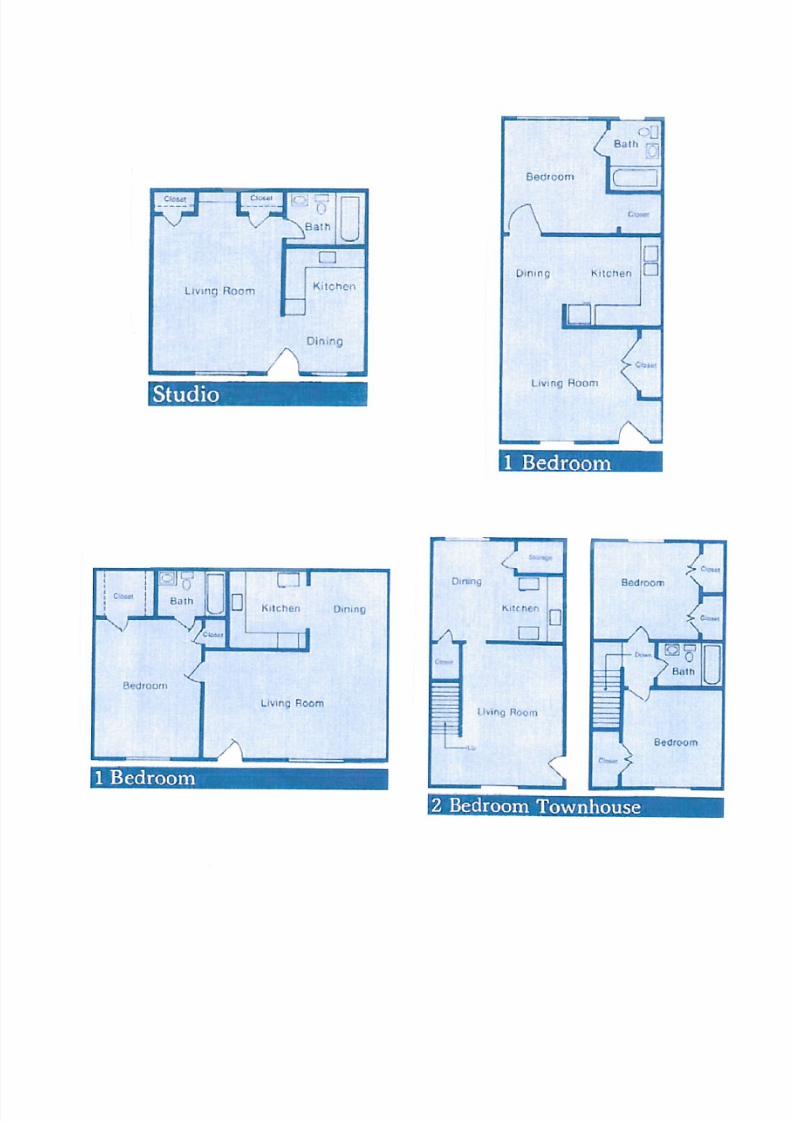

Unit Total

Unit Type Units Size (SF) RSF

Efficiency 28 320 8,960

Studio 231 370 85,470

1 BR / 1BA 14 482 6,748

1 BR/ 1BA 44 723 31,8122 BR / 1BA 33 1,000 33,000

Total/Average 350 474 165,990

UNIT MIX

Willow Lakes

Construction Class: The Class of construction is the basic subdivision in Marshall Valuation Service , dividing all buildings into five basic groups bytype of framing (supporting columns and beams), walls, floors,roof structure, and fireproofing. The subject's constructionqualifies as Class C1.

Competitive Rating: The subject complexes are perceived in the market as Class C

properties in terms of quality, features, amenities and age.

Occupancy type: Market rate

Improvement Summary Total Unit Area:

Avg. Unit Size:Year BuiltType:Units:Floor Plans:Buildings:

165,990 rentable SF – based on providedunits sizes. 185,010 gross SF474 rentable SF1963 and 1969Garden350Efficiency, Studio, 1BR, and 2BR27 apartment buildings and three ancillary

buildings (laundry, pool pump house, andstorage shed) Six apartment buildings aretwo-story and 21 are one-story.

1Class C buildings are characterized by masonry or reinforced concrete (including tilt-up) construction. Floors and

roofs may be supported on wood or steel joists or trusses, or the floor may be concrete on grade. The exterior wallsmay be load bearing or not with open concrete, steel, or wood columns supporting the load.(Source: Marshall Valuation Service , January 1995, ♣1, p. 8-109)

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 21/86

Property Analysis

15

Exterior Description Foundation:Frame:Exterior Walls:Roof Cover:Other Exterior:

Stairs:

Poured, reinforced concrete slab, on gradeConcrete blockPainted stucco over concrete blockBuilt-up, wood framed and sheathedPainted wood soffit, fascia and trim. Many

buildings are connected by a commonbreezeway.Metal railings with concrete risers.

Interior Living Areas Walls:

Windows:Doors:

Ceiling:Lighting:

Flooring:Appliances:Kitchen:

Bathrooms:

Painted sheetrock. Some interior partitionsare wood studs.Double-hung in aluminum frameExterior: solid core wood Interior: hollow corewoodTextured gypsum, 8' height all floorsIncandescent and some fluorescent inkitchens.Vinyl tile and carpetRange/oven and refrigeratorWood cabinetry, laminate counters, andstainless-steel sink.Enameled tub w/tile surround, laminatecounter w/inset bowl on wood base.

Other HVAC:

Electrical/plumbing:

Fire/Safety:Utilities:

Roof mounted condensers and closetmounted furnaces (64 units) and through-wall AC and radiant electric heat.All electric w/individual water heaters. 100 to150 amp single phase breaker panels.Electrical wiring was reportedly updated in1999.Smoke alarms.Water/sewer is included in the rentalstructure. All other utilities at the subject areseparately metered.

Site Improvements: Parking:

Landscaping:

Asphalt or concrete paved, many spaces are“90 degree angle” parking along the frontageroads (340). The largest parking area is theformer tennis court near the center of thedevelopment. There are 80 interior spaces.Parking appears adequate.

Basic with mature trees and shrubs. Thereare extensive sidewalks between streets andbuildings.

Property Amenities: Property amenities include onsite management, pool, fitnesscenter, laundry facility, and a pool.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 22/86

Property Analysis

16

Overall Condition: Overall fair to average condition. Reportedly no units are downand there are no major items of deferred maintenance.

Economic Age and Life: According to Marshall Valuation Service cost guide, buildings ofthis type and quality have an expected life of 55 years. The

subject complex was built in 1963 and 1969. Assuming propermaintenance, we estimate the remaining useful live to exceed 30years.

Conclusion/Comments: Overall, the subject is typical of average quality garden apartmentcomplexes built in its era throughout Florida. It has interiorfeatures that are demanded by tenants in the market, and averagequality construction and exterior appeal. In comparison to thepresent apartment inventory in Jacksonville the subject propertywould comparatively rate as fair to average quality.

ZONING ANALYSIS

The property is subject to the zoning regulations of the City of Jacksonville. It is zoned

Residential Medium Density E (RMD-E) which permits multi-family houses to a density of 20

units per acre or 216 units. Please note that there could be 216 two- and three-bedroom

apartments and not studios, efficiencies or 1-bedroom units so that income generation would

be similar. Subject project currently has 350 units. In addition, there are setbacks of 20 feet

for front, side or rear yards which are not met. Also on site parking requirements are 1.5

spaces for efficiency apartments and studios. 1.75 spaces for one bedroom apartments and 2

spaces for two bedroom units for a minimum of 405 parking spaces. It is our understanding

that the subject is a legal non-conforming use. However, we recommend a letter be obtained

from the City of Jacksonville for further questions regarding this matter.

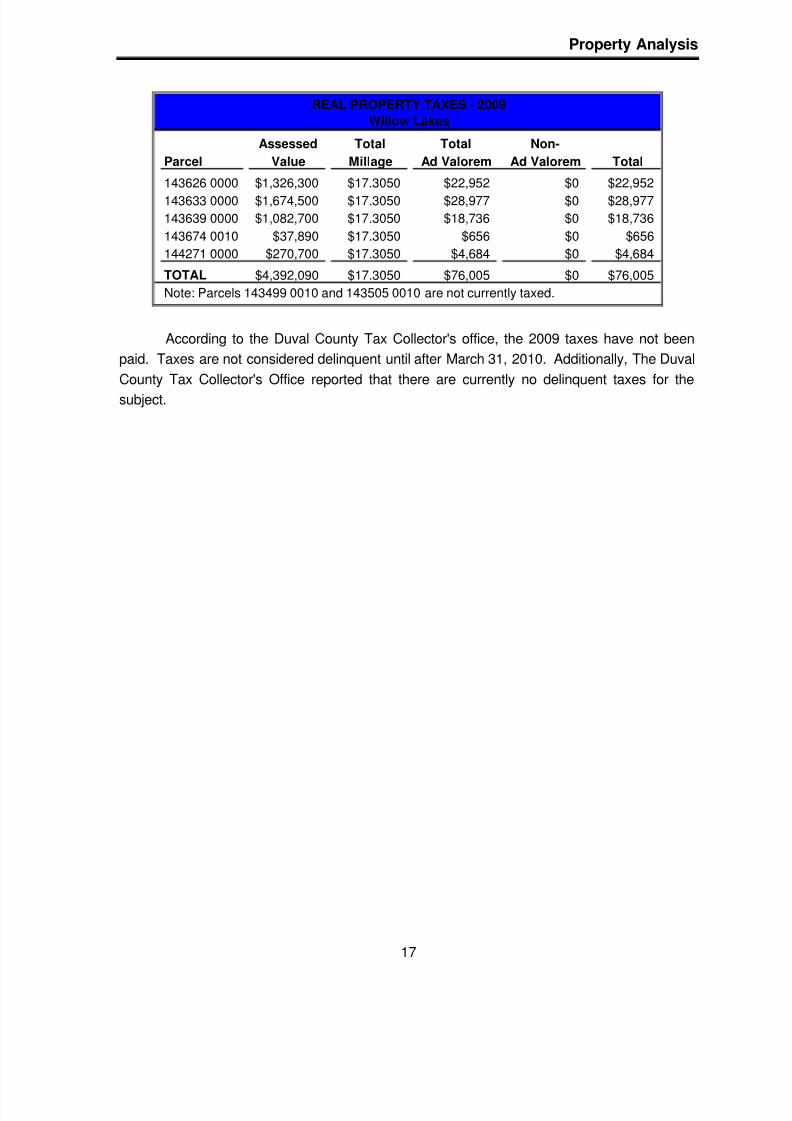

TAX ANALYSIS

Willow Lakes Apartments is subject to taxation by Duval County and the City of

Jacksonville. Real Estate in Florida IS assessed at 100% of the county assessor's estimated

market value. Taxes are determined based upon application of the local millage rate. The

2009 combined tax rate for applicable to the subject was $17.3050 per $1,000 of assessment.Real estate taxes in Florida are discounted for early payment. If taxes are paid in November,

a 4% break is permitted, and a 3% break is permitted if taxes are paid in December.

Additionally, a 2% break is permitted for taxes paid in January, and a 1% break is permitted

for taxes paid in February.

The tax amount for 2009 is indicated in the following table.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 23/86

Property Analysis

17

Assessed Total Total Non-

Parcel Value Millage Ad Valorem Ad Valorem Total

143626 0000 $1,326,300 $17.3050 $22,952 $0 $22,952

143633 0000 $1,674,500 $17.3050 $28,977 $0 $28,977

143639 0000 $1,082,700 $17.3050 $18,736 $0 $18,736

143674 0010 $37,890 $17.3050 $656 $0 $656

144271 0000 $270,700 $17.3050 $4,684 $0 $4,684

TOTAL $4,392,090 $17.3050 $76,005 $0 $76,005

REAL PROPERTY TAXES - 2009

Willow Lakes

Note: Parcels 143499 0010 and 143505 0010 are not currently taxed.

According to the Duval County Tax Collector's office, the 2009 taxes have not been

paid. Taxes are not considered delinquent until after March 31, 2010. Additionally, The Duval

County Tax Collector's Office reported that there are currently no delinquent taxes for the

subject.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 24/86

MARKET ANALYSIS

18

NATIONAL APARTMENT MARKET

The Emerging Trends in R Estate 2010 report, prepared by Price-Waterhouse-

Coopers LLC and ULI – Urban Land Institute, there are numerous reasons why apartmentsare considered to be a good investment. Pent-up demand grows for apartments. Twenty-

something’s who moved back home out of necessity, want out of parents’ homes as soon as

their employment prospects improve. The roommate thing also gets stale for people who had

their own space until the recession struck. A huge generation Y cohort of young adults should

be avid renters. They delay marriage and kids to build careers and many won’t think about

buying suburban houses until they have families. Further, the lack of available mortgage

financing and requirements for larger cash down payments make house buying more difficult.

Demand for apartments should ramp up with the first signs of increased hiring, particularly in

underserved markets. On the supply side, the apartment development has come to a

standstill.

However, the negative aspects of apartments as an investment are also very real. The

jobs outlook hardly looks bright, delaying a pickup in renter demand. Shadow condos flood

some multifamily markets with new supply, hurting occupancies and dropping rents, especially

for upper-income apartments. National vacancy rates climb to record highs. With softer rents

and a 150-basis-point rise in cap rates the impact and values can be significant.

Multifamily investments historically provide the best risk-adjusted returns among real

estate property types and current market experience reinforces investor views of the

apartment sector’s relative resiliency. The expected early rebound in demand trends, supplyconstraints in many markets, and institutional investor appetite for income-producing

properties add up to a solid, albeit not immediate, recovery track.

According to the 1st Quarter 2010 Korpacz Real Estate Investor Survey , prepared by

Price-Waterhouse-Coopers LLC, apartment vacancy rates remain perched at record levels as

owners wait for economic stability, a decline in single-family housing construction, and the full

impact of the echo-boomer generation to boost apartment demand. ver the past year, overall

vacancy escalated 130 basis points, ending 2009 at 8.0%, based on data by Reis. his "all-

time high" in Reis' 30-year history of tracking the U.S. apartment sector compares to the

previous high of 7.8% in 1986. Many investors believe that the apartment market will "bump

along the bottom" through 2010, showing little improvement in its fundamentals.

With a smaller pool of renters, competition among landlords has resulted in declining

rental rates and liberal concession packages to entice tenants. This quarter, free rent ranges

up to nine months and averages just under three months, according to Survey participants. In

addition, some owners are reducing or eliminating deposits and fees and/or offering

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 25/86

Market Analysis

19

merchandise giveaways. Due to concessions, average effective rental rates were down 2.9%

at year-end 2009 over the prior year.

As landlords struggle to preserve revenue, cost-cutting measures remain paramount.

Amid this challenging ownership environment, sales activity has fallen to a record low in this

sector. According to Real Capital Analytics, annual sales of apartment properties dropped63.0% in 2009 and were primarily single-asset deals. While an increase in sales velocity

occurred during the fourth quarter of 2009, it was partially due to an increase in distressed

ownership and forced sales. Similar to other property sectors, equity investors are seeking

well-located, high-quality apartment assets.

The 1st Quarter 2010 Korpacz Real Estate Investor Survey prepared by Price-

Waterhouse Coopers indicates that overall capitalization rates for apartments range from

5.00% to 11.00%, with an average of 7.85%. This is a decrease in the overall average rate of

18 basis points from 4th quarter 2009 and 66 basis points higher than the same period one

year ago. The investors indicated inflation assumptions for market rent generally rangingbetween -10.00% and 3.00%, with an average of -0.91%. Additionally, these investors quoted

an expense inflation rate between 0.00% and 4.00%, with an average of 2.55%. Internal rate

of return requirements for the investors ranged from 6.50% to 14.00%, with an average of

10.18%. The average marketing time reported ranged from 1 to 18 months, with an average

of 8.06 months.

JACKSONVILLE APARTMENT MARKET

According to an article in the Jacksonville Business Journal dated January 29, 2010,

Jacksonville’s apartment market is standing out from the rest of the nation for the worst of

reasons, it has the highest vacancy rate. There are a number of reasons why Northeast

Florida has a 14.4 percent vacancy rate, but multifamily experts said the root of the problem is

another serious issue facing Jacksonville, the rising unemployment rate.

Jacksonville lost more than 22,000 jobs last year and local workers are facing another

3,000 to 4,000 job cuts in 2010, according to Torto Wheaton Research. One of the main

drivers in the apartment market is job growth. Every four to five new jobs is estimated to

create a demand for one rental unit. In addition, while construction of new apartmentcommunities slowed or even stopped for most U.S. markets in the past two years, in

Jacksonville, 1,200 apartment units were completed in 2008 and 2,600 units were completed

in 2009. So the combination of the rising unemployment rate, which was at 11.3 percent in

Northeast Florida as of December 2009, coupled with an over supply of inventory took its toll

on the market.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 26/86

Market Analysis

20

But there were even more factors in the run up to Jacksonville earning the title of

having the highest vacancy rate in the nation. Jacksonville’s 62,000 apartment units is a very

small apartment inventory compared with other cities, so even a minor change in any of the

supply or demand drivers will tend to have a significant impact on the market. During the first

half of the past decade, interest rates were low and Jacksonville had cheap raw land, making

it more affordable for people in lower income brackets who would ordinarily rent to become

homeowners. When the foreclosure rate started to soar, developers ramped up construction

to replace communities that had been converted to condominiums and to prepare for an

expected mass exodus back to the rental market by those who had been foreclosed on. But

that didn’t happen. Instead, people moved into the shadow rental market where condos and

single-family homes are rented instead of sold, often at a less expensive rate than apartment

communities. Other people doubled up with other family members, friends or roommates.

The rising vacancy rate at some apartment communities has been enough to send

them into foreclosure, and more are on the verge, particularly those acquired at the height of

the real estate market with adjustable rate loans. But those bank-owned communities could

be an incentive for investors to move back into the market, because they can buy foreclosed

apartment communities for 30 percent of their earlier value and can bring them up to the

market rate standard for about $10,000 to $20,000 per unit. Developers buying foreclosed

apartment communities, along with the much more narrow development pipeline for new

communities, which includes 520 units in 2010 and none in 2011, will help Jacksonville’s

market correct itself, experts said. However, because of the reputation Jacksonville’s

apartment market has now as a higher risk city for lenders to invest in, it will likely take it

longer to recover.

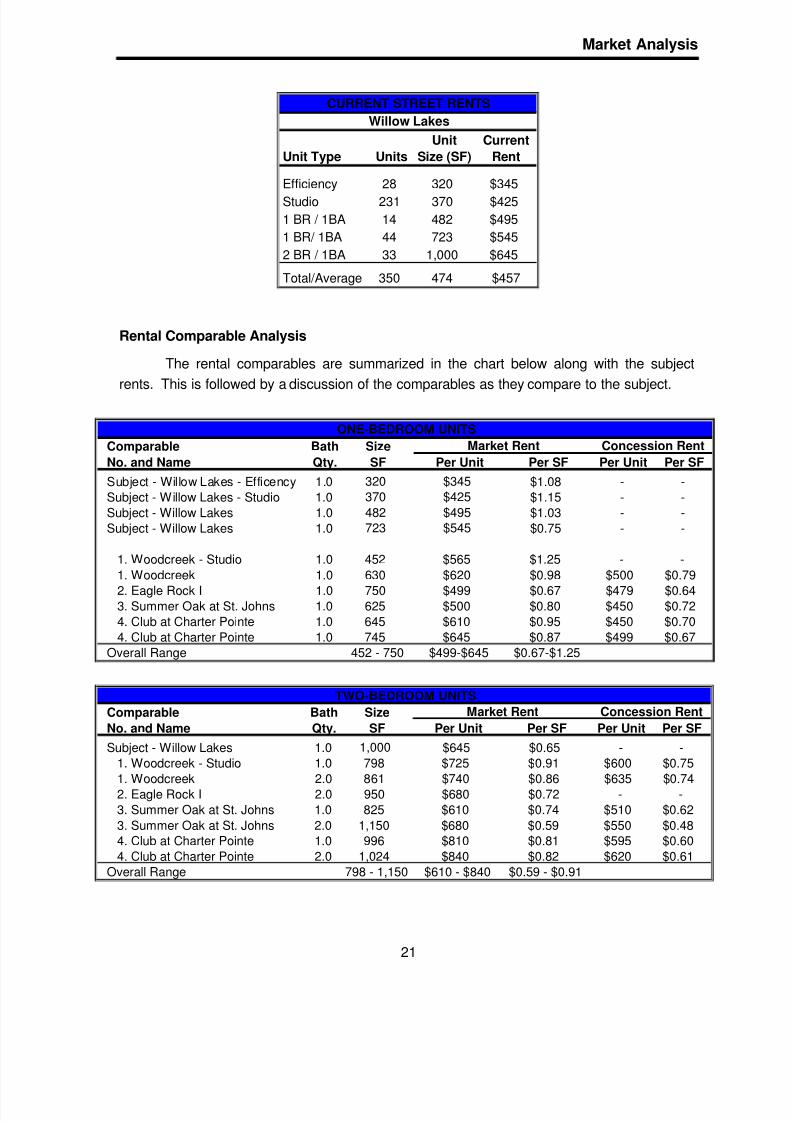

RENTAL INCOME ANALYSIS

Subject Rental Income

The charts below present the current quoted rental rates being offered at the subject

property. It is important to note that the property is not currently offering any concessions.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 27/86

Market Analysis

21

Unit Current

Unit Type Units Size (SF) Rent

Efficiency 28 320 $345

Studio 231 370 $425

1 BR / 1BA 14 482 $495

1 BR/ 1BA 44 723 $545

2 BR / 1BA 33 1,000 $645

Total/Average 350 474 $457

CURRENT STREET RENTS

Willow Lakes

Rental Comparable Analysis

The rental comparables are summarized in the chart below along with the subject

rents. This is followed by a discussion of the comparables as they compare to the subject.

Comparable Bath Size

No. and Name Qty. SF Per Unit Per SF Per Unit Per SF

Subject - Willow Lakes - Efficency 1.0 320 $345 $1.08 - -

Subject - Willow Lakes - Studio 1.0 370 $425 $1.15 - -

Subject - Willow Lakes 1.0 482 $495 $1.03 - -

Subject - Willow Lakes 1.0 723 $545 $0.75 - -

1. Woodcreek - Studio 1.0 452 $565 $1.25 - -

1. Woodcreek 1.0 630 $620 $0.98 $500 $0.79

2. Eagle Rock I 1.0 750 $499 $0.67 $479 $0.643. Summer Oak at St. Johns 1.0 625 $500 $0.80 $450 $0.72

4. Club at Charter Pointe 1.0 645 $610 $0.95 $450 $0.70

4. Club at Charter Pointe 1.0 745 $645 $0.87 $499 $0.67

Overall Range 452 - 750 $499-$645 $0.67-$1.25

ONE-BEDROOM UNITS

Market Rent Concession Rent

Comparable Bath Size

No. and Name Qty. SF Per Unit Per SF Per Unit Per SF

Subject - Willow Lakes 1.0 1,000 $645 $0.65 - -

1. Woodcreek - Studio 1.0 798 $725 $0.91 $600 $0.75

1. Woodcreek 2.0 861 $740 $0.86 $635 $0.74

2. Eagle Rock I 2.0 950 $680 $0.72 - -

3. Summer Oak at St. Johns 1.0 825 $610 $0.74 $510 $0.62

3. Summer Oak at St. Johns 2.0 1,150 $680 $0.59 $550 $0.484. Club at Charter Pointe 1.0 996 $810 $0.81 $595 $0.60

4. Club at Charter Pointe 2.0 1,024 $840 $0.82 $620 $0.61

Overall Range 798 - 1,150 $610 - $840 $0.59 - $0.91

Market Rent Concession Rent

TWO-BEDROOM UNITS

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 28/86

Market Analysis

22

Although the subject’s one- and two-bedroom units are within the size range of the

comparables and are competitively priced in comparison to the comparables. However, the

efficiency and studio units are well below the size range. Although these units have per

square foot rents toward the high end of the market, the monthly rents are well below the

comparables. Based on our analysis of the comparables and the rent roll, it appears that the

current quoted rents for the subject are well supported. Therefore, we used the quoted rents

in our valuation.

Rental Income Conclusion

Based on our analysis of the comparables, the current quoted rents appear generally

reasonable. These rents are also supported within the provided rent roll.

OCCUPANCY

As shown in the chart below, physical occupancy at the subject is 93%. Historically

the property has experienced occupancies in the low to mid 90’s. Occupancy at the

comparables ranges from 36% to 92% and the weighted average occupancy is 76%.

However, the low comparable is undergoing renovations and is still in lease-up. If excluding

this comparable the weighted average is 90%. The subject offers the smallest units in the

market and has corresponding lower rents, which is why it is able to outperform the market in

terms of occupancy.

In our analysis we used stabilized physical occupancy of 92%. This is a largely based

on their current and recent historical occupancies.

No. Units Occupancy

Subject - Willow Lakes 350 93%

1. Woodcreek 260 87%

2. Eagle Rock I 96 90%

3. Summer Oak at St Johns 400 92%

4. Club at Charter Pointe* 258 36%

Total / Weighted Avg. 1014 76%

*Under renovation still in lease

OCCUPANCY

SUBJECT CHARACTERISTICS AND MARKETABILITY

The subject is a 350-unit apartment complex on 10.83 acres. It is located along Hare,

India, and Jasper Avenues just east of Arlington Road in the city of Jacksonville, Duval

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 29/86

Market Analysis

23

County, Florida. This location is less than 0.50 mile south of the Arlington Expressway and

about four miles east of downtown Jacksonville and I-95. The complex consists of 27 one-

and two-story apartment buildings and was reportedly constructed between 1963 and 1969.

The unit mix includes studio, efficiency, and one- and two-bedroom units ranging from 320 to

1,000 square feet. Property amenities include onsite management, pool, fitness center,

laundry facility, and a pool. The buildings feature traditional design with painted stucco over

concrete block exterior walls and built-up roofs. The property is in overall fair to average

condition. According to the provided rent roll, there are 23 vacant units. The subject property

is perceived as ‘Class C’ apartment complex. Overall it is in fair to average condition and

suffers some deferred maintenance.

The metro area's long-term outlook remains good, which will only be bolstered by its

growing prominence as port city. Given all of these factors, it seems that there would be

moderate interest in the investor market for the subject if it were to be placed on the market.

Given the overall value of the asset, it would likely appeal to local or regional investors, but its

size could attract some institutional players.

REASONABLE EXPOSURE AND MARKETING TIMES

Exposure time is always presumed to precede the effective date of appraisal. It is the

estimated length of time the property would have been offered prior to a hypothetical market

value sale on the effective date of appraisal. It assumes not only adequate, sufficient, and

reasonable time but also adequate, sufficient, and reasonable marketing effort. To arrive at

an estimate of exposure time for the subject, we considered direct and indirect market datagathered during the market analysis, the amount of time required for marketing the

comparable sales included in this report, broker surveys, as well as information provided by

national investor surveys that we regularly review. This information indicated typical exposure

periods of twelve months or less for properties similar to the subject. Given this information,

we estimate that an exposure period of twelve months or less, if it was aggressively marketed.

A reasonable marketing time is the period a prospective investor would forecast to sell

the subject immediately after the date of value, at the value estimated. The sources for this

information include those used in estimating reasonable exposure time, but also an analysis of

the anticipated changes in market conditions following the date of appraisal. Based on thepremise that present market conditions are the best indicators of future performance, a

prudent investor will forecast that, under the conditions described above, the subject property

would require a marketing time of twelve months or less. This seems like a reasonable

projection, given the current and projected market conditions.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 30/86

HIGHEST AND BEST USE

24

In appraisal practice, the concept of highest and best use is the premise upon which

value is based. The four criteria that the highest and best use must meet are: legal

permissibility; physical possibility; financial feasibility; and maximum profitability.

Highest and best use is applied specifically to the use of a site as vacant. In cases

where a site has existing improvements, the concluded highest and best use as if vacant may

be different from the highest and best use as improved. The existing use will continue,

however, until land value, at its highest and best use, exceeds that total value of the property

under its existing use plus the cost of removing or altering the existing structure.

HIGHEST AND BEST USE AS THOUGH VACANT

The subject zoning district is primarily intended for medium density residential. The

existing use is a permitted use and given the surrounding current uses a zoning change to amore intense use would be unlikely. The site is generally suitable for virtually all permitted

uses, with the only significant limitation being site area. Due to the sites’ location it is ideally

suited for multifamily development. While some other uses such as single-family residential

might also be financially feasible, it seems likely that an apartment complex would produce the

highest land value. The existing apartment complex is a form of the highest and best use of

the site as if vacant. However, maximum density permitted for the subject site if it were vacant

would be 20 units per acre, which is well below the density of the existing improvements.

HIGHEST AND BEST USE AS IMPROVED

The subject is used in the operation of an apartment complex, which is permitted

under the subject’s current zoning by the City of Jacksonville, however the subject it is

nonconforming in terms of density and parking. The improvements are well suited for their

intended use. It is possible the improvements could be converted to another use entirely, if

the costs were justified. This seems highly unlikely, however. Our investigation indicates that

there is fairly strong demand in the market for apartments. Given that use of the subject

improvements is basically limited to the current or a similar use physically, and the fact that the

improvements are financially feasible, we conclude that the existing apartment use is

consistent with the maximally profitable use. We conclude that the highest and best use of the

property is for continued use as an apartment complex.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 31/86

APPRAISAL METHODOLOGY

25

Three basic approaches to value are typically considered. The cost, sales

comparison, and income capitalization methodologies are described below.

• The cost approach is based on the premise that an informed purchaser will pay nomore for the subject than the cost to produce an equivalent substitute. This approach

is particularly applicable when the subject property is relatively new and represents thehighest and best use of the land, or when relatively unique or specializedimprovements are located on the site for which there exist few sales or leasecomparables. The first step in the cost approach is to estimate land value (at itshighest and best use). The second step is to estimate cost of all improvements.Improvement costs are then depreciated to reflect value loss from physical, functionaland external causes. Land value and depreciated improvement costs are then addedto indicate a total value.

• In the sales comparison approach, sales of comparable properties, adjusted fordifferences, are used to indicate a value for the subject. Valuation is typicallyaccomplished using physical units of comparison such as price per square foot, price

per square foot excluding land, price per unit, etc., or economic units of comparisonsuch as a net operating income (NOI) or gross rent multiplier (GRM). Adjustments areapplied to the physical units of comparison. Economic units of comparison are notadjusted, but rather are analyzed as to relevant differences, with the final estimatederived based on the general comparisons. The reliability of this approach isdependent upon: (a) availability of comparable sales data; (b) verification of the data;(c) degree of comparability; and (d) absence of atypical conditions affecting the saleprice.

• The income approach involves an analysis of the income-producing capacity of theproperty on a stabilized basis. The steps involved are: analyzing contract rent andcomparing it to comparable rentals for reasonableness; estimating gross rent; making

deductions for vacancy and collection losses as well as building expenses; and thencapitalizing net income at a market-derived rate to yield an indication of value. Thecapitalization rate represents the relationship between net income and value.

Related to the direct capitalization method is discounted cash flow (DCF). Inthis method of capitalizing future income to a present value, periodic cash flows (whichconsist of net income less capital costs, per period) and a reversion (if any) areestimated and discounted to present value. The discount rate is determined byanalyzing current investor yield requirements for similar investments.

Since investors are active in the marketplace for properties similar to the subject, the

income approach is particularly applicable to the appraisal. We performed direct

capitalization. The sales comparison method of analysis simulates investigations of a typical

buyer for properties like the subject. Therefore, this approach was employed for this

assignment. We did not employ the cost approach, as the age of the improvements suggests

physical depreciation, which is difficult to quantify. It should also be noted that investors of

income producing properties typically do not perform a cost approach, as they are most

concerned with the income characteristics of the asset.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 32/86

INCOME CAPITALIZATION APPROACH

26

The income capitalization approach to value is based upon an analysis of the

economic benefits to be received from ownership of the subject. These economic benefits

typically consist of the net operating income projected to be generated by the improvements.

There are several methods by which the present value of the income stream may be

measured, including direct capitalization and a discounted cash flow analysis. In this section,we used the direct capitalization method. We initially estimated potential rental income,

followed by projections of vacancy and collection loss and operating expenses. The resultant

net operating income is then capitalized into a value indication based on application of an

appropriate overall capitalization rate.

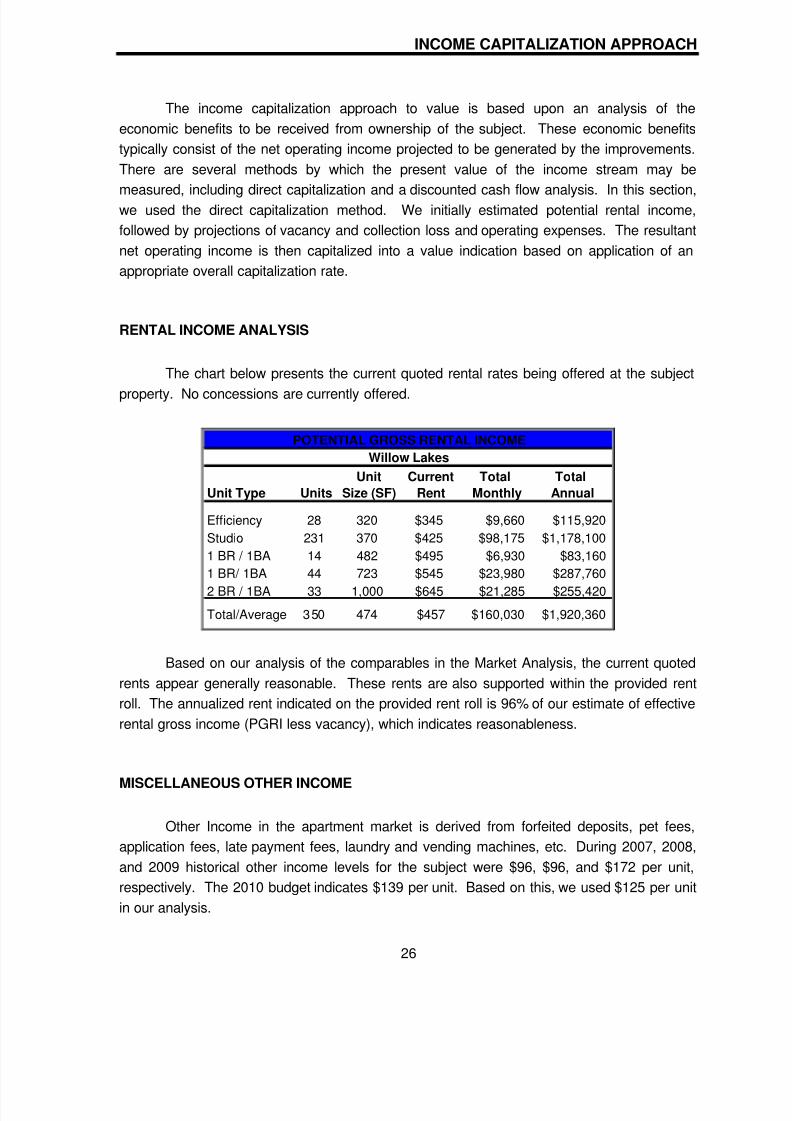

RENTAL INCOME ANALYSIS

The chart below presents the current quoted rental rates being offered at the subject

property. No concessions are currently offered.

Unit Current Total Total

Unit Type Units Size (SF) Rent Monthly Annual

Efficiency 28 320 $345 $9,660 $115,920

Studio 231 370 $425 $98,175 $1,178,100

1 BR / 1BA 14 482 $495 $6,930 $83,160

1 BR/ 1BA 44 723 $545 $23,980 $287,760

2 BR / 1BA 33 1,000 $645 $21,285 $255,420

Total/Average 350 474 $457 $160,030 $1,920,360

POTENTIAL GROSS RENTAL INCOME

Willow Lakes

Based on our analysis of the comparables in the Market Analysis, the current quoted

rents appear generally reasonable. These rents are also supported within the provided rent

roll. The annualized rent indicated on the provided rent roll is 96% of our estimate of effective

rental gross income (PGRI less vacancy), which indicates reasonableness.

MISCELLANEOUS OTHER INCOME

Other Income in the apartment market is derived from forfeited deposits, pet fees,

application fees, late payment fees, laundry and vending machines, etc. During 2007, 2008,

and 2009 historical other income levels for the subject were $96, $96, and $172 per unit,

respectively. The 2010 budget indicates $139 per unit. Based on this, we used $125 per unit

in our analysis.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 33/86

Income Capitalization Approach

27

VACANCY AND COLLECTION LOSS

As noted previously, the subject currently has 23 vacant units indicating an occupancy

level of 93%. Historically, the property has maintained occupancies in the low to mid 90’s and

the comparables are mostly experiencing occupancies ranging from the mid 80’s to mid 90’s.

The subject is able to outperform the market as it has smaller units and corresponding lower

rents relative to the market. We used a combined physical vacancy and collection loss of 8%

in our analysis. This is discussed in more detail in the market analysis section of this report.

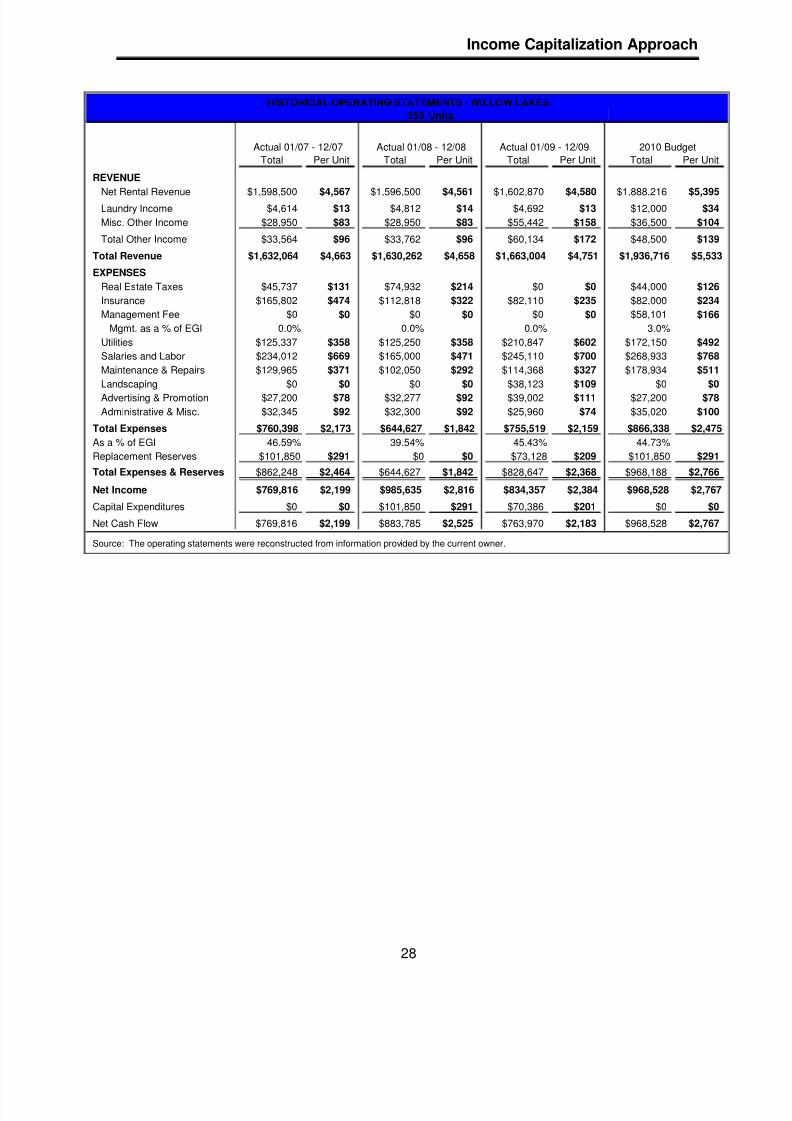

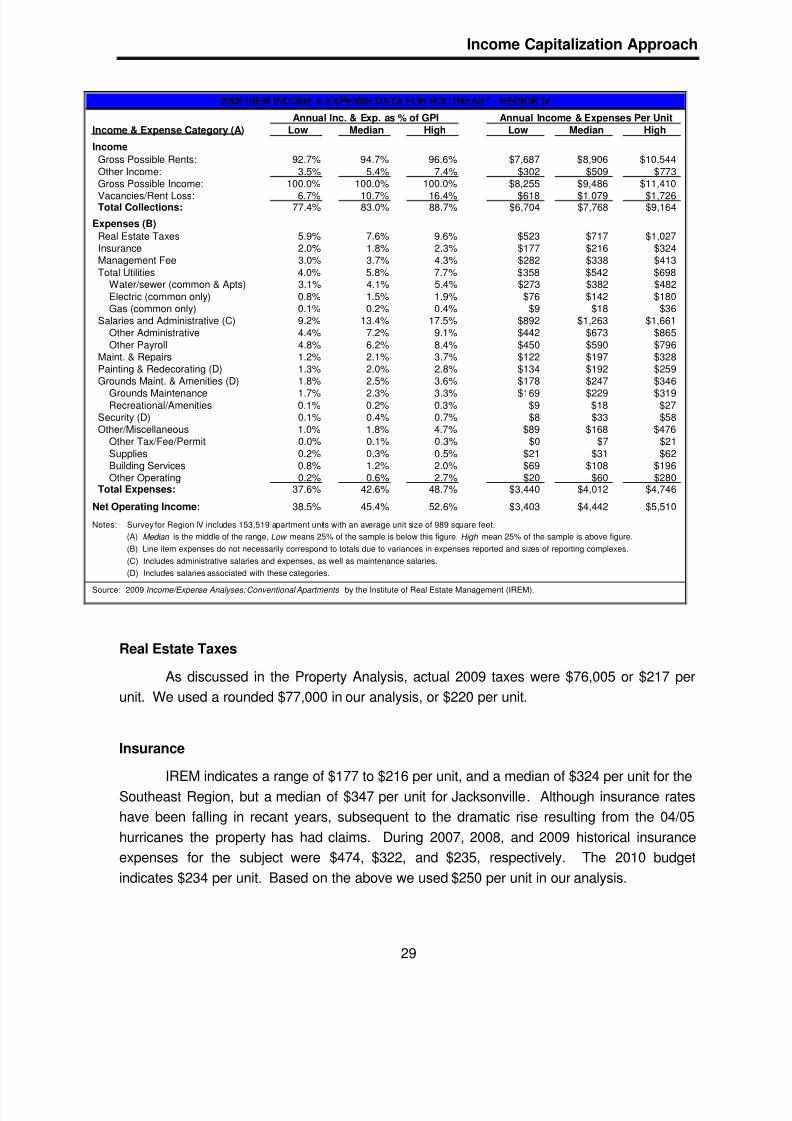

EXPENSE ANALYSIS

In deriving an estimate of net income, it is necessary to consider various expenses and

allowances ascribable to the operation of a property of this type. Operating statements for the

2007, 2008, and 2009 were provided and are summarized on the following page. In addition,we were provided a 2010 operating budget prepared by the selling broker. In estimating

expenses and allowances, we gave primary consideration to the actual operating expenses of

the subject. In addition, we also reviewed industry standard expenses as published in the

2009 edition of the Income/Expense Analysis – Conventional Apartments published by IREM

(Institute of Real Estate Management).

The subjects consolidated historical operating data and IREM data are summarized in

the following charts. Historical operating data for each property is presented in the addenda.

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 34/86

Income Capitalization Approach

28

350 Units

Total Per Unit Total Per Unit Total Per Unit Total Per Unit

REVENUE

Net Rental Revenue $1,598,500 $4,567 $1,596,500 $4,561 $1,602,870 $4,580 $1,888,216 $5,395Laundry Income $4,614 $13 $4,812 $14 $4,692 $13 $12,000 $34

Misc. Other Income $28,950 $83 $28,950 $83 $55,442 $158 $36,500 $104

Total Other Income $33,564 $96 $33,762 $96 $60,134 $172 $48,500 $139

Total Revenue $1,632,064 $4,663 $1,630,262 $4,658 $1,663,004 $4,751 $1,936,716 $5,533

EXPENSES

Real Estate Taxes $45,737 $131 $74,932 $214 $0 $0 $44,000 $126

Insurance $165,802 $474 $112,818 $322 $82,110 $235 $82,000 $234

Management Fee $0 $0 $0 $0 $0 $0 $58,101 $166

Mgmt. as a % of EGI 0.0% 0.0% 0.0% 3.0%

Utilities $125,337 $358 $125,250 $358 $210,847 $602 $172,150 $492

Salaries and Labor $234,012 $669 $165,000 $471 $245,110 $700 $268,933 $768

Maintenance & Repairs $129,965 $371 $102,050 $292 $114,368 $327 $178,934 $511

Landscaping $0 $0 $0 $0 $38,123 $109 $0 $0

Advertising & Promotion $27,200 $78 $32,277 $92 $39,002 $111 $27,200 $78

Administrative & Misc. $32,345 $92 $32,300 $92 $25,960 $74 $35,020 $100

Total Expenses $760,398 $2,173 $644,627 $1,842 $755,519 $2,159 $866,338 $2,475

As a % of EGI 46.59% 39.54% 45.43% 44.73%

Replacement Reserves $101,850 $291 $0 $0 $73,128 $209 $101,850 $291

Total Expenses & Reserves $862,248 $2,464 $644,627 $1,842 $828,647 $2,368 $968,188 $2,766

Net Income $769,816 $2,199 $985,635 $2,816 $834,357 $2,384 $968,528 $2,767

Capital Expenditures $0 $0 $101,850 $291 $70,386 $201 $0 $0

Net Cash Flow $769,816 $2,199 $883,785 $2,525 $763,970 $2,183 $968,528 $2,767

Source: The operating statements were reconstructed from information provided by the current owner.

HISTORICAL OPERATING STATEMENTS - WILLOW LAKES

Actual 01/07 - 12/07 Actual 01/08 - 12/08 Actual 01/09 - 12/09 2010 Budget

8/8/2019 Willow Lakes Appraisal 4-1-10

http://slidepdf.com/reader/full/willow-lakes-appraisal-4-1-10 35/86

Income Capitalization Approach

29

2009 IREM INCOME & EXPENSE DATA FOR SOUTHEAST - REGION IV

Income & Expense Category (A) Low Median High Low Median High

Income

Gross Possible Rents: 92.7% 94.7% 96.6% $7,687 $8,906 $10,544Other Income: 3.5% 5.4% 7.4% $302 $509 $773Gross Possible Income: 100.0% 100.0% 100.0% $8,255 $9,486 $11,410

Vacancies/Rent Loss: 6.7% 10.7% 16.4% $618 $1,079 $1,726Total Collections: 77.4% 83.0% 88.7% $6,704 $7,768 $9,164

Expenses (B)

Real Estate Taxes 5.9% 7.6% 9.6% $523 $717 $1,027Insurance 2.0% 1.8% 2.3% $177 $216 $324Management Fee 3.0% 3.7% 4.3% $282 $338 $413Total Utilities 4.0% 5.8% 7.7% $358 $542 $698

Water/sewer (common & Apts) 3.1% 4.1% 5.4% $273 $382 $482Electric (common only) 0.8% 1.5% 1.9% $76 $142 $180Gas (common only) 0.1% 0.2% 0.4% $9 $18 $36

Salaries and Administrative (C) 9.2% 13.4% 17.5% $892 $1,263 $1,661Other Administrative 4.4% 7.2% 9.1% $442 $673 $865Other Payroll 4.8% 6.2% 8.4% $450 $590 $796

Maint. & Repairs 1.2% 2.1% 3.7% $122 $197 $328Painting & Redecorating (D) 1.3% 2.0% 2.8% $134 $192 $259Grounds Maint. & Amenities (D) 1.8% 2.5% 3.6% $178 $247 $346

Grounds Maintenance 1.7% 2.3% 3.3% $169 $229 $319Recreational/Amenities 0.1% 0.2% 0.3% $9 $18 $27

Security (D) 0.1% 0.4% 0.7% $8 $33 $58Other/Miscellaneous 1.0% 1.8% 4.7% $89 $168 $476

Other Tax/Fee/Permit 0.0% 0.1% 0.3% $0 $7 $21Supplies 0.2% 0.3% 0.5% $21 $31 $62Building Services 0.8% 1.2% 2.0% $69 $108 $196Other Operating 0.2% 0.6% 2.7% $20 $60 $280

Total Expenses: 37.6% 42.6% 48.7% $3,440 $4,012 $4,746

Net Operating Income: 38.5% 45.4% 52.6% $3,403 $4,442 $5,510