william m. burns, ceo roche pharmaceuticalsfbb4c0ca-2406-4018-b922-3343f0b57360/...william m. burns,...

TRANSCRIPT

1

Roche: Committed to InnovationWilliam M. Burns, CEO Roche Pharmaceuticals

2

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as ‘believes’, ‘expects’, ‘anticipates’, ‘projects’, ‘intends’, ‘should’, ‘seeks’, ‘estimates’, ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation, among others:

1 pricing and product initiatives of competitors;2 legislative and regulatory developments and economic conditions;3 delay or inability in obtaining regulatory approvals or bringing products to market; 4 fluctuations in currency exchange rates and general financial market conditions; 5 uncertainties in the discovery, development or marketing of new products or new uses of existing products, including without

limitation negative results of clinical trials or research projects, unexpected side-effects of pipeline or marketed products; 6 increased government pricing pressures; 7 interruptions in production 8 loss of or inability to obtain adequate protection for intellectual property rights; 9 litigation;10 loss of key executives or other employees; and11 adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted to mean that Roche’s earnings or earnings per share for this year or any subsequent period will necessarily match or exceed the historical published earnings or earnings per share of Roche.

For marketed products discussed in this presentation, please see full prescribing information on our website – www.roche.com

All mentioned trademarks are legally protected

2

3

Roche: Committed to innovation

Growth opportunities

Summary

4

Roche Pharma 5,702 5,498 -4 1 11

excl. Tamiflu pandemic 5,151 5,455 6 11 22

Genentech 2,547 2,399 -6 9 9

Chugai 893 671 -25 -23 -13

excl. Tamiflu pandemic 698 669 -4 -2 11

Pharmaceuticals 9,142 8,568 -6 1 8

excl. Tamiflu pandemic 8,396 8,523 2 9 17

Pharma Q1 `08: strong underlying momentum

USDQ1’07 Q1’08 CHF local growth

% change inSales CHF m

3

5

Pharma: Strong growth at well balanced risk profile Based on multiple products

0

5

10

15

20

25

30

35

40

1997

1999

2001

2003

2005

2007

Pharma sales1 (CHF billion)

CAGR 13 %

2007 Blockbuster Sales Pyramid (CHF billion)

Continuing to focus on our core assets

XelodaCHF 1.2 bn

MabThera/Rituxan CHF 5.5 bn

Pegasys CHF 1.6 bn

TarcevaCHF 1.1 bn

Cellcept CHF 2.0 bn

NeoRecormon/EpoginCHF 2.1 bn

Avastin CHF 4.1 bn

Herceptin CHF 4.9 bn

1 Continuing businesses

6

Major growth opportunities outside the US

76 68 6253 51 48

33

24 32 3847 49 52

67

0

20

40

60

80

100

PEGASY

S

HERCEP

TIN

XELODA

TARCEV

A

CELLC

EPT

MABTH

ERA

AVASTIN

% o

f Tot

al 2

007

Sal

es

USEU / ROW (incl. Japan)

4

7

Roche: Committed to innovation

Growth opportunities

Summary

8

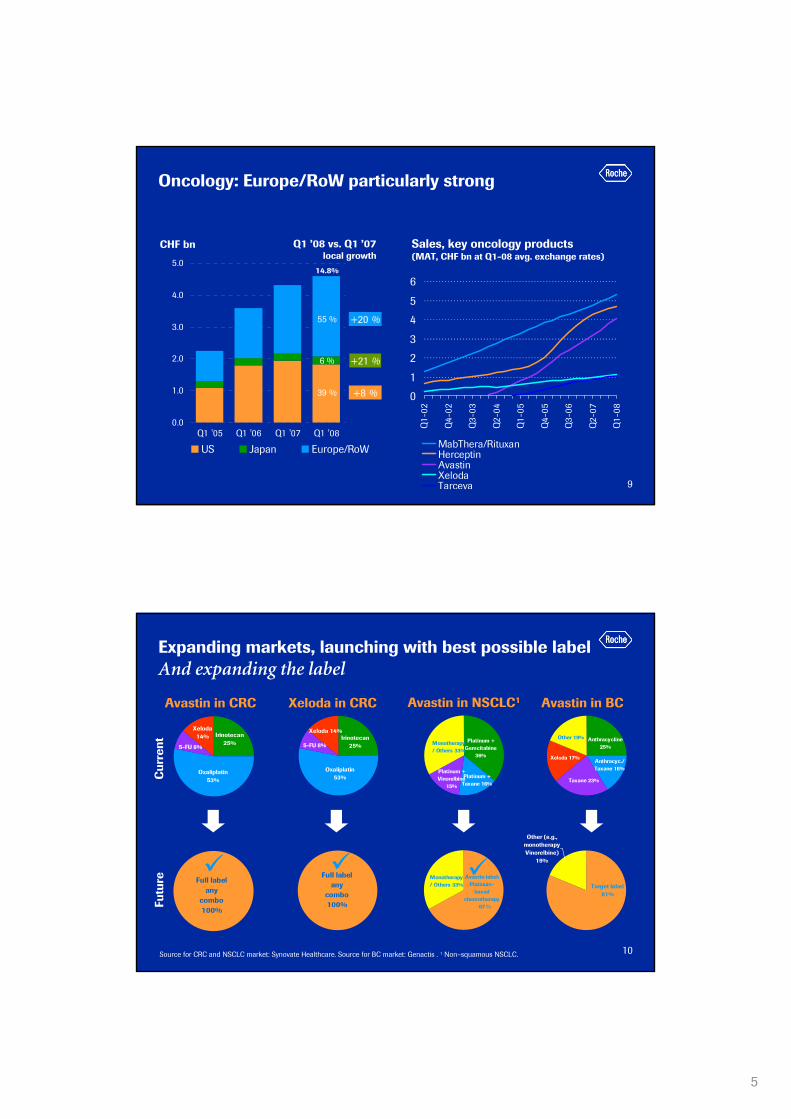

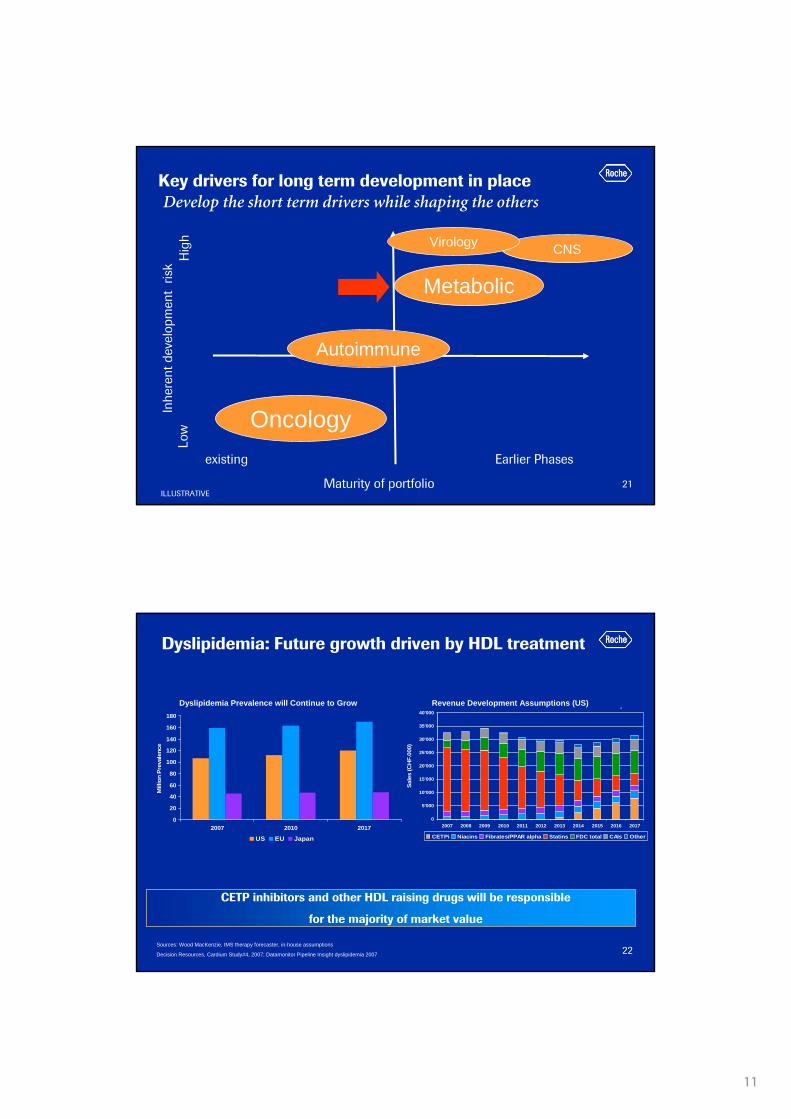

Existing Earlier Phases

ILLUSTRATIVE

Inhe

rent

dev

elop

men

t ris

k

Maturity of portfolio

Low

Hig

h

Oncology

Autoimmune

Metabolic

CNSVirology

Key drivers for long term development in placeDevelop the short term drivers while shaping the others

5

9

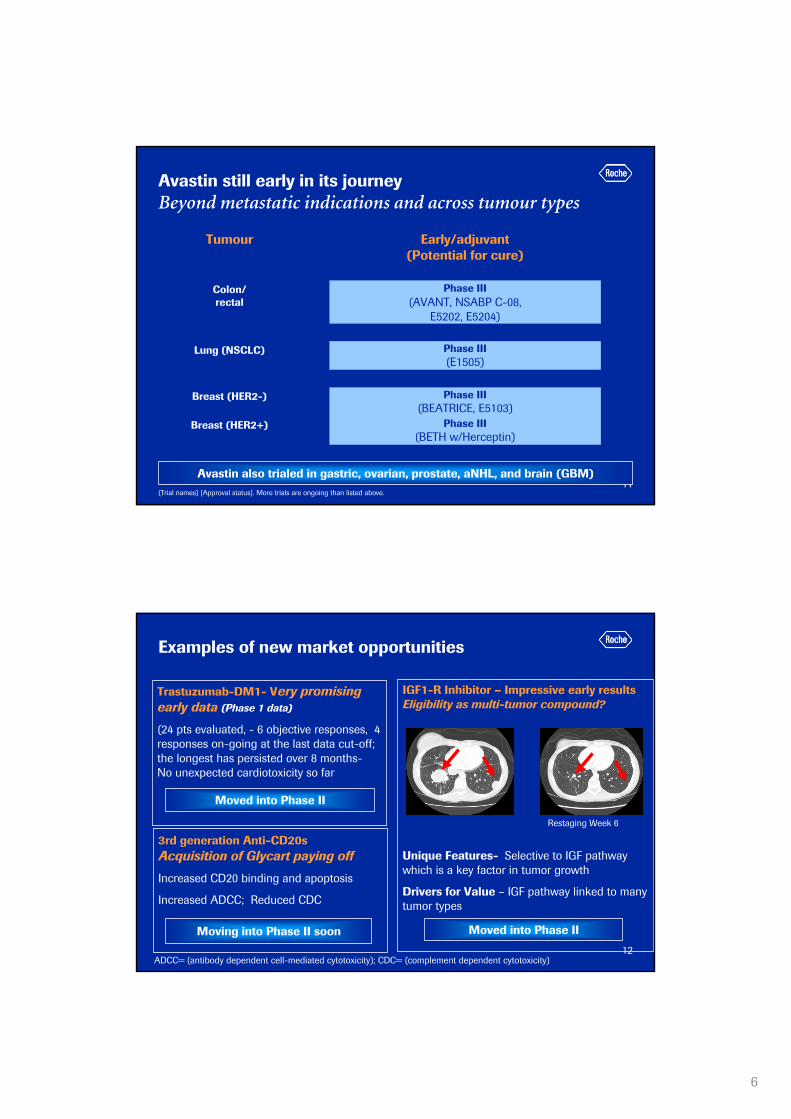

Oncology: Europe/RoW particularly strong

xx %

x %

CHF bn Q1 ’08 vs. Q1 ’07local growth

0.0

1.0

2.0

3.0

4.0

5.0

Q1 '05 Q1 '06 Q1 '07 Q1 '08

US Japan Europe/RoW

55 %

6 %

39 %

+20 %

+21 %

+8 % 0

1

2

3

4

5

6

Q1-

02

Q4-

02

Q3-

03

Q2-

04

Q1-

05

Q4-

05

Q3-

06

Q2-

07

Q1-

08

MabThera/RituxanHerceptinAvastinXelodaTarceva

Sales, key oncology products(MAT, CHF bn at Q1-08 avg. exchange rates)

14.8%

10

Expanding markets, launching with best possible labelAnd expanding the label

Xeloda 14% Irinotecan

25%

Oxaliplatin 53%

5-FU 8%

Avastin in CRC Xeloda in CRC

Oxaliplatin 53%

Irinotecan 25%5-FU 8%

Xeloda 14%

Avastin in NSCLC1

Monotherapy / Others 33%

Platinum + Gemcitabine

36%

Platinum + Vinorelbine

15%

Platinum + Taxane 16%

Avastin in BC

Anthracycline 25%

Anthracyc./ Taxane 16%

Taxane 23%

Xeloda 17%

Other 19%

Full label any

combo 100%

Full label any

combo 100%

Other (e.g., monotherapy Vinorelbine)

19%

Target label 81%

v

Cur

rent

Futu

re

Source for CRC and NSCLC market: Synovate Healthcare. Source for BC market: Genactis . 1 Non–squamous NSCLC.

Avastin label: Platinum-

based chemotherapy

67

Monotherapy / Others 33%

%

6

11

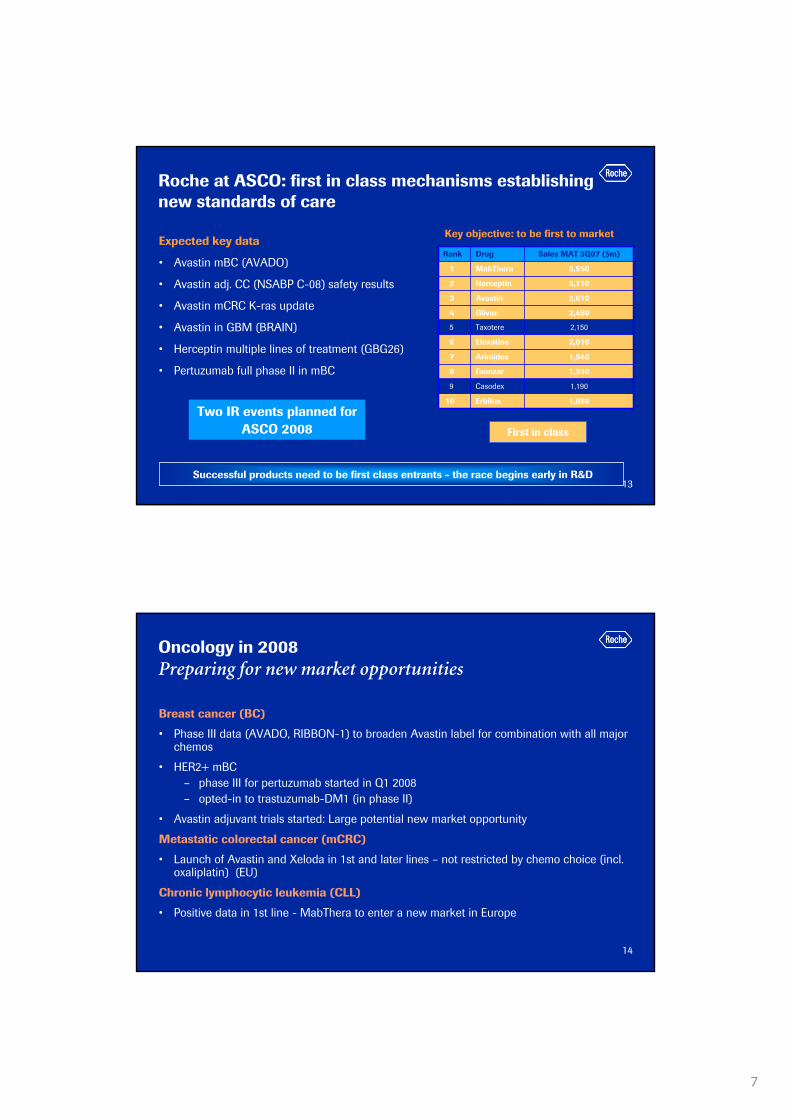

Avastin still early in its journey Beyond metastatic indications and across tumour types

Avastin also trialed in gastric, ovarian, prostate, aNHL, and brain (GBM)(Trial names) [Approval status]. More trials are ongoing than listed above.

Phase III(BETH w/Herceptin)

Breast (HER2+)

Phase III(BEATRICE, E5103)

Breast (HER2-)

Phase III(E1505)

Lung (NSCLC)

Phase III(AVANT, NSABP C-08,

E5202, E5204)

Colon/ rectal

Early/adjuvant (Potential for cure)

Tumour

12

Examples of new market opportunities

Trastuzumab-DM1- Very promising early data (Phase 1 data)

(24 pts evaluated, - 6 objective responses, 4 responses on-going at the last data cut-off; the longest has persisted over 8 months-No unexpected cardiotoxicity so far

Moved into Phase II

3rd generation Anti-CD20sAcquisition of Glycart paying off

Increased CD20 binding and apoptosis

Increased ADCC; Reduced CDC

ADCC= (antibody dependent cell-mediated cytotoxicity); CDC= (complement dependent cytotoxicity)

Moving into Phase II soon

IGF1-R Inhibitor – Impressive early resultsEligibility as multi-tumor compound?

Unique Features- Selective to IGF pathway which is a key factor in tumor growth

Drivers for Value – IGF pathway linked to many tumor types

Restaging Week 6

Moved into Phase II

7

13

Roche at ASCO: first in class mechanisms establishing new standards of care

Expected key data

• Avastin mBC (AVADO)

• Avastin adj. CC (NSABP C-08) safety results

• Avastin mCRC K-ras update

• Avastin in GBM (BRAIN)

• Herceptin multiple lines of treatment (GBG26)

• Pertuzumab full phase II in mBC

Rank Drug Sales MAT 3Q07 ($m)

1 MabThera 3,550

2 Herceptin 3,110

3 Avastin 2,610

4 Glivec 2,450

5 Taxotere 2,150

6 Eloxatine 2,010

7 Arimidex 1,540

8 Gemzar 1,330

9 Casodex 1,190

10 Erbitux 1,080

First in class

Successful products need to be first class entrants - the race begins early in R&D

Key objective: to be first to market

Two IR events planned for ASCO 2008

14

Oncology in 2008Preparing for new market opportunities

Breast cancer (BC)

• Phase III data (AVADO, RIBBON-1) to broaden Avastin label for combination with all major chemos

• HER2+ mBC– phase III for pertuzumab started in Q1 2008– opted-in to trastuzumab-DM1 (in phase II)

• Avastin adjuvant trials started: Large potential new market opportunity

Metastatic colorectal cancer (mCRC)

• Launch of Avastin and Xeloda in 1st and later lines – not restricted by chemo choice (incl. oxaliplatin) (EU)

Chronic lymphocytic leukemia (CLL)

• Positive data in 1st line - MabThera to enter a new market in Europe

8

15

existing Earlier Phases

ILLUSTRATIVE

Inhe

rent

dev

elop

men

t ris

k

Maturity of portfolio

Low

Hig

h

Oncology

Autoimmune

Metabolic

CNSVirology

Key drivers for long term development in placeDevelop the short term drivers while shaping the others

16

332

1'522

429

0

200

400

600

800

1'000

1'200

1'400

1'600

Treated forMod/Sev

Treated with Bio Adherence

Mid to Long-Term Opportunities• Low biologic penetration Mod/Sev RA• Future growth drivers:

• Novel orals: Potent & convenient• PHC defined differentiation = premium pricing• New brand Rx combination regimens

2007 US Patient Treatment

0

200

400

600

800

1000

1200

1400

1600

2008 2010 2012 2014 2016 2018 2020

Num

ber o

f Bio

logi

c Tr

eate

d pa

tient

s in

000

s

5EUUSA

Short to mid-term growth driverBiologic treated population projected to grow 6.7% CAGR (2008-2020)

Rheumatoid Arthritis: Continued Market GrowthDriven by increased Biologic use, novel oral DMARDs & PHC

9

17

Actemra: Significant clinical benefitStrong improvement also at higher ACR scores

Source: Roche´s OPTION trial. All comparisons are to placebo + MTXCochran-Mantel-Haenszel analysis was used to calculate p-values

Δ=20.0

ACR20 ACR50 ACR70

Patie

nts

(%)

***p<0.000143.9%***

22.0%***

58.5%***

26.5%

10.8%

2.0%

12.2%***

***47.9%

31.5%***

Δ=32.0

Δ=33.1

0

10

20

30

40

50

60

70 PlaceboTCZ 4 mg/kg + MTXTCZ 8 mg/kg + MTX

18

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

0 12 24 36 48 60 72 84

DA

S28

< 2

.6 (

%)

AMBITION RADIATE OPTION, TOWARD, LITHE

AMBITION (n) 564 546 502 438 369 262 168 87

RADIATE (n) 398 384 377 344 308 237 175 117

Pooled DMARD-IR (n)

1587 1541 1504 1380 1287 1143 963 690

Weeks

Actemra: Impressive Long-term extension data DAS28 (ESR) < 2.6 (ITT)

10

19

Next generation anti-CD20s (MabThera follow-ons)Opportunities for improvement

2nd gen. anti-CD20 (ocrelizumab)

Fully humanized

Potential clinical benefits

• Less immunogenicity

• Better tolerability

• Shorter infusion time

3rd gen. anti-CD20 (R7159)

Fc engineered (glycosylations)

• Increased CD20 binding and apoptosis

• Increased ADCC (antibody dependent cell-mediated toxicity)

• Reduced CDC (complement dependent cell toxicity)

Potential clinical benefits

• Improved efficacy/ Less infusion reactions

In phase III in RA, Phase II in RRMS to start 2008

In phase I for oncology / hematology

20

Inflammation PortfolioA rich pipeline in multiple AI indications

nn

nn nn RARγ

nn

nn

nn

nn

hMAb OX40L

Rheumatology

Respiratory

nn

P2P2P1P1P0P0LOLOLILI P3P3 MktMkt

nn

MabTheraDMARD inad resp

Actemra RA

MabTheraRA MTX naive

Actemra sJIA

Ocrelizumab RA

nn

Group OriginTPIProject origin: External Origin Line Extensions

nn

nn

nn

nn

nn

nn

nn

nn

MabThera RA

nnTransplant nn CellCept

Pain nnnn

ocrelizumabANCA vasculitis

nn

nn

Other

Ocrelizumab SLE

nn

nn nn

S1P1 Psoriasis

11

21

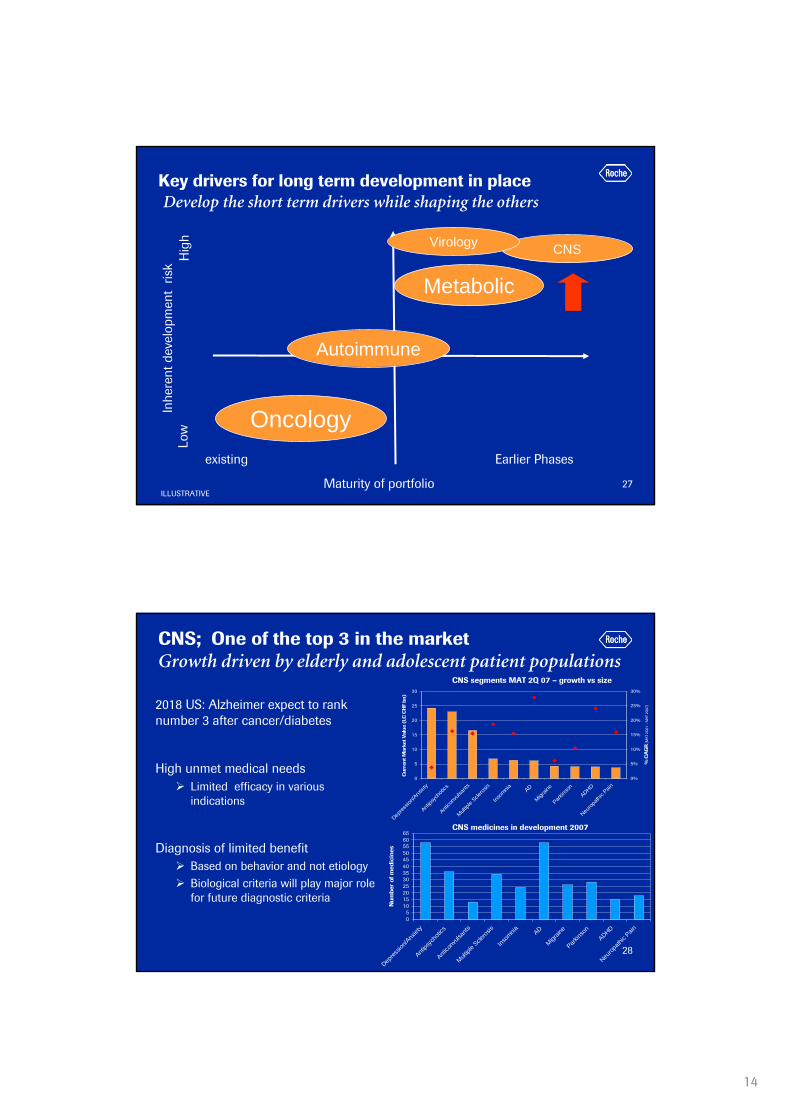

Key drivers for long term development in placeDevelop the short term drivers while shaping the others

existing Earlier Phases

ILLUSTRATIVE

Inhe

rent

dev

elop

men

t ris

k

Maturity of portfolio

Low

Hig

h

Oncology

Autoimmune

Metabolic

CNSVirology

22

Revenue Development Assumption in Dyslipidemia (US)

0

5'000

10'000

15'000

20'000

25'000

30'000

35'000

40'000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sale

s (C

HF.

000)

CETPi Niacins Fibrates/PPAR alpha Statins FDC total CAIs Other

Sources: Wood MacKenzie, IMS therapy forecaster, in-house assumptions

Decision Resources, Cardium Study#4, 2007; Datamonitor Pipeline Insight dyslipidemia 2007

CETP inhibitors and other HDL raising drugs will be responsible

for the majority of market value

Dyslipidemia Population Development

0

20

40

60

80

100

120

140

160

180

2007 2010 2017

Mill

ion

Prev

alen

ce

US EU Japan

Dyslipidemia prevalence will continue to grow Revenue Development Assumptions in (US)Dyslipidemia Prevalence will Continue to Grow Revenue Development Assumptions (US)

Dyslipidemia: Future growth driven by HDL treatment

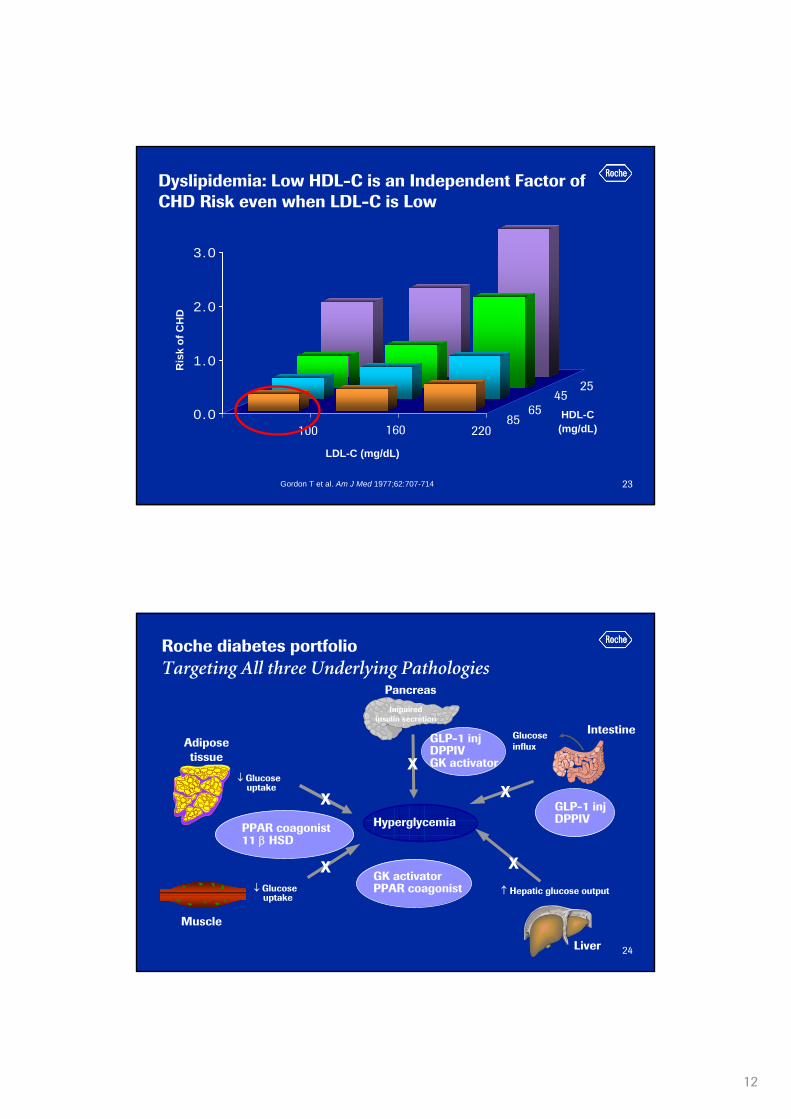

12

23Gordon T et al. Am J Med 1977;62:707-714.

0.0

1.0

2.0

3.0

Ris

k of

CH

D

HDL-C(mg/dL)

LDL-C (mg/dL)

100 160 220

2545

6585

Dyslipidemia: Low HDL-C is an Independent Factor of CHD Risk even when LDL-C is Low

24

Hyperglycemia

↑ Hepatic glucose output

Impairedinsulin secretion

GlucoseinfluxAdipose

tissue

↓ Glucoseuptake

GLP-1 injDPPIVGK activator

PPAR coagonist11 β HSD

GLP-1 injDPPIV

GK activatorPPAR coagonist

Muscle

↓ Glucoseuptake

X

X

X

X

X

Liver

Intestine

Pancreas

Roche diabetes portfolio Targeting All three Underlying Pathologies

13

25

Our metabolic pipeline: maturing quicklyCommitted to become a major player

PPAR-CO

nn

nn

nn

DPP-IV (3)

nnnn

nn

GLP-1

nn

nn

nn

nn

nn

nn

nn

nn

nnnn

nn

P2P2P1P1P0P0LOLOLILINMP/TANMP/TA P3P3CETP

nn

nn

nn

nn

nn

nn

nn

nnnn

nnnn

nn

RegReg

nn

nn

nn

nn

nn

nn

nn

February 04, 2008

nn

nn

nnRoche

Chugainn

nn

nn

nn

nn

nn

nn

nn

nn

nn

nn

nn

nn

SGLT2

Shanghai nn

SGLT2

26

Metabolism/Diabetes in 2008Committed to become a major player

CETP Inhibitor to move into phase III

• Safety data to be presented at major medical meetings

GLP-1 phase II data available

• Decision for phase III to be taken in H1 2008

• Publication planned for ADA

Phase II data for DPP-IV (3) and PPARαγ expected

• Looking for a differentiated profile (e.g. weight reduction for DPP-IV)

• Go/no-go decisions for phase III trials to be taken this year

SGLT2 just moved into Phase II

Investor science event

14

27

existing Earlier Phases

ILLUSTRATIVE

Inhe

rent

dev

elop

men

t ris

k

Maturity of portfolio

Low

Hig

h

Oncology

Autoimmune

Metabolic

CNSVirology

Key drivers for long term development in placeDevelop the short term drivers while shaping the others

28

CNS; One of the top 3 in the marketGrowth driven by elderly and adolescent patient populations

2018 US: Alzheimer expect to rank number 3 after cancer/diabetes

High unmet medical needsLimited efficacy in various indications

Diagnosis of limited benefitBased on behavior and not etiologyBiological criteria will play major role for future diagnostic criteria

05

101520253035404550556065

Depres

sion/A

nxiet

y

Antips

ycho

tics

Antico

nvuls

ants

Multipl

e Scle

rosis

Insom

nia AD

Migrain

e

Parkins

onADHD

Neurop

athic

Pain

Num

ber

of m

edic

ines

CNS medicines in development 2007

CNS segments MAT 2Q 07 – growth vs size

0

5

10

15

20

25

30

Depres

sion/A

nxiet

y

Antips

ycho

tics

Antico

nvuls

ants

Multipl

e Scle

rosis

Insom

nia AD

Migrain

e

Parkins

onADHD

Neurop

athic

Pain

Cu

rren

t Mar

ket V

alue

(LC

CH

F bn

)

0%

5%

10%

15%

20%

25%

30%

% C

AG

R (

MA

T 2Q

01 -

MA

T 2Q

07)

15

29

CNS Portfolio 2008- A clear commitment

nn

GLYT1

nn

nnnn

nn

nn

nn

nn

nn

nnnn

nn

nn

nn

nn

nn nn

Development Phase

P2P2P1P1P0P0LOLOLILITATA P3P3

Neurology

Psychiatry

nn

nn

nn

S1P1

Nic-a7 mem3454

nn

nn

nn

Ocrelizumab

Rituximab

nn

nn

nn

GLYT1(2)

30

Roche: Committed to innovation

Growth opportunities

Summary

16

31

Key drivers in place for sustainable growthCurrent and projected sources of value creation (phase IIb and III)

2007 2011 2015

AvastinmCRC,NSCLC

Herceptinadjuvant BC

MabTheraNHL

HCVPolymerase

Inhibitor

ILLUSTRATIVE

ActemraRA

Avastinadjuvant

Colon cancer CETPinhibitor

OcrelizumabRA, lupus

PertuzumabmBC

Avastinadjuvant

Breast cancerAvastinadjuvant

Lungcancer

OcrelizumabMS

GLP-1T2 diabetes

MabTheraRA

AvastinmBC

extensions

MabTheraCLL

HPV16therapeutic

vaccine

Tarceva1st line maint.

Tarceva+Avastin

combo 2nd line

Xelodaadj. BC

32

17

33

Our objectives for 2008

Sales

• High single-digit local currency sales increase for Roche Group (excl. Tamiflu pandemic1)

• Above-market sales growth1 in both divisions

Core EPS

• Core earnings per share target2 at least at record 2007 level despite significant increase in R&D investment and considerably lower Tamiflu pandemic sales

Shareholder return

• Continuous increase in dividend pay-out ratio over the next 3 years

1 Excluding government and corporate stockpiling orders of Tamiflu for pandemic use2 At constant exchange rates Barring unforeseen events

34

Major growth opportunities outside the USHerceptin leading the way

0

20

40

60

80

100

MabThera/Rituxan

Herceptin

48 %

33 %

53 %

Tarceva Avastin

68 %

% o

f Tot

al 2

007

Sale

s

USEU / ROW (incl. Japan)

62 %

Xeloda