why did shareholder value gain influence? ciaran driver © imperial college business school

TRANSCRIPT

Why did shareholder value gain influence?

Ciaran Driver

• www.imperial.ac.uk/people/c.driver

© Imperial College Business School

Introduction 1

• Forward commitments, such as innovative search, are affected by modes of governance. On the one hand, transparency and oversight may create a stable climate for innovation. But equally, it is difficult to offer adequate incentives using a reward system that is contractual, since much of the required inputs to innovation are difficult to set out in formal contracts. Furthermore, excessive control of slack resources may dampen motivation and deter engagement by employees. Sometimes these latter arguments are used to support stakeholder involvement, where incentives are strengthened by shared bargaining rights over the distribution of returns to innovation.

•

© Imperial College Business School

Introduction 2

• The paper examines whether it is possible to rationalise the current dominance of shareholder orientation. One view is that organizational reforms have pushed power lower in corporations, motivating workers in a way that makes employee control unnecessary. Opponents of this “new foundations” view argue that organizational effects have been different to those envisaged and do not explain tendencies in corporate governance. A distinct argument is that the observed increase in shareholder orientation may be explained by a need to substitute external for internal capital allocation The paper questions the generality of such arguments, leaving open the ultimate reason for shareholder primacy.

© Imperial College Business School

Increasing dominance of shareholder value orientation

• CEO tenure down and performance-related turnover up, in all regions (Kaplan & Minton 2006; Booz Allen 2009).

• Shift to external directors (Higgs 2003)

• Shift to metrics such as EVA (Rebérioux 2007)

• More active shareholders (ICR 2006)

• Buy-backs (Hill and Taylor 2000;Lazonick 2008;Perraudin et al 2008)

• Greater legal protection for shareholders (Conway et al 2008)

© Imperial College Business School

A balance of theories

Knowledge Agency Incentives

• Agency perspective supports a shareholder value orientation

• But the need for knowledge incentives undermines a pure shareholder value orientation, particularly from the property rights perspective

© Imperial College Business School

A balance of theory but imbalance in policy: why?

Knowledge Agency Hold-up

• Has opportunism increased in importance - why?

• Have non-contractible investments of skills and resources become less important – why?

© Imperial College Business School

Hard to argue that agency problems increased in importance

“How could productivity … be so great at a time [1960s] when managers supposedly wasted large amounts of money?” (Holmstrom & Kaplan 2001)

Restructuring in the US raised capital utilisation only in the resource industries

© Imperial College Business SchoolSource: Driver & Shepherd 2005

US manufacturing Capacity Utilisation H-P filter

Knowledge Economy? How does it feature?

• Is the Knowledge Based Economy important enough to influence forms of governance ?

• Ratio of business R&D to sales have not increased much in most major economies over the last quarter century (Bulli 2008)

© Imperial College Business School

© Imperial College Business School

Caveats: failure to count intangibles?

• Intangibles have grown faster than tangibles and now match them (Corrado, Hulten & Sichel 2006)

• But 35% of US intangibles series include organizational capital such as Wall-Mart supply chain technology and Dell’s Business Model (Oliner et al 2008)

• Business consultancy & advertising included

• So … are intangibles source of rent or profit?

© Imperial College Business School

www.imperial.ac.uk/business-school © Imperial College Business School

“Declining importance of firms’ physical assets …starkly illustrated by the

soaring share prices of Microsoft, Netscape, Yahoo…” (Burton-Jones 1999)

Source: Andrew Smithers: http://www.smithers.co.uk/files/UKSIP_7th_March_2007.pdf

Provisional conclusion

© Imperial College Business School

• Formal knowledge inputs are not as important as thought in the 1990s

• Non-contractable knowledge activities include search, cooperation, and organizational commitment

• It seems reasonable to suppose that these increase as the complexity of work increases

• The question then is how to encourage these processes if they cannot be contracted on

• Property rights view implies a stakeholder model for knowledge–workers (Blair 1995; Hart 1996;Roberts & Van den Steen 2001)

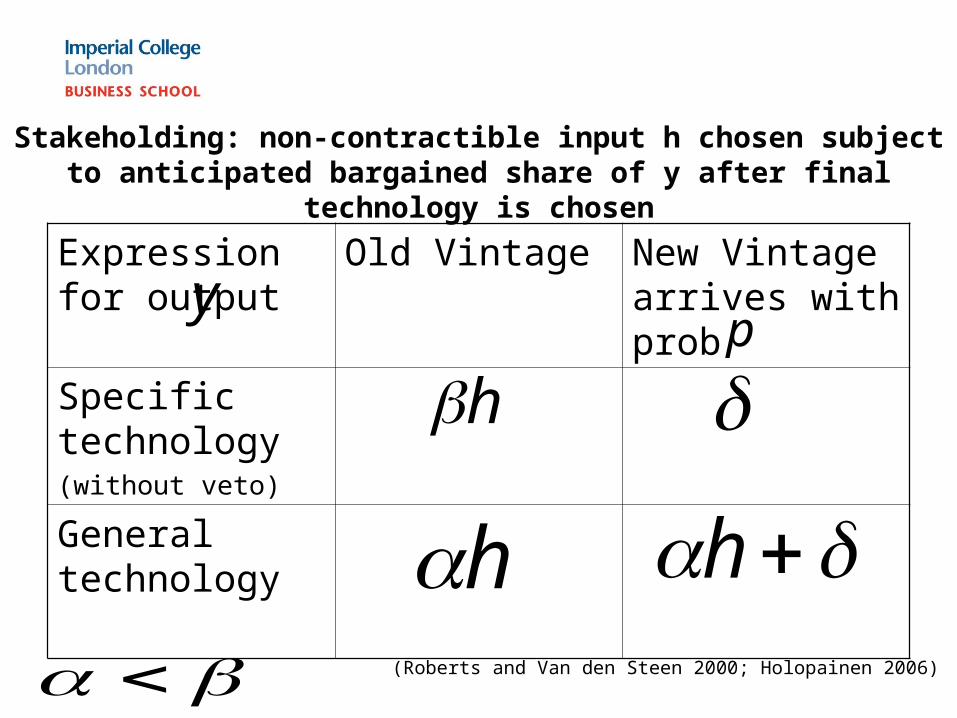

Stakeholding: non-contractible input h chosen subject to anticipated bargained share of y after final technology is chosen

Expression for output

Old Vintage New Vintage arrives with prob

Specific technology (without veto)

General technology

h

h h

py

(Roberts and Van den Steen 2000; Holopainen 2006)

Full shareholder control not pareto optimal?

• With the specific technology shareholders optimally give away bargaining power over surplus

• Granting a stakeholder tradable veto for specific technology would increase h but decrease profit except in restricted conditions

• Stakeholder veto raises probability of general technology being introduced

• Shareholder choice between specific and general technology does not always maximise total surplus

© Imperial College Business School

Alternative to property rights approach?

• Fama (1980) originally suggested that reputation concerns of managers could be an alternative to direct oversight and thus could also substitute for stakeholder control

• However, this depends on the managerial productivity signal not being too noisy

• Subsequently other theories have emerged to suggest how non-contractable effort could be encouraged –

• Granting “access” to managers (Rajan & Zingales)• Granting informal authority to managers (Aghion & Tirole)

© Imperial College Business School

Internal theories of governance

© Imperial College Business School

Real Authority: CEO & Manager Reaction Functions for Effort (E.e)

CEO

Manager

E

e

1

)()1(

eE

eEMANAGER

rr

esearcherEErU

Aghion and Tirole 1997

Implication – both models seen as explaining delegation

• “As the importance of human capital has grown, power has moved away from the top and is much more widely dispersed through the firm” (Rajan & Zingales 2000, p.202)

• “Within corporations, there has been de facto a recent trend in management towards “empowerment” and “team-work” , which by and large amount to a reassignment of some decision rights to lower tiers of the hierarchy” (Aghion & Tirole 1997, p.8)

© Imperial College Business School

The Flattening Firm has empirical support

Delayering introduced in 1980s and 1990s: changes responsibilities and reporting in a way that shortens the hierarchical chain of command.

© Imperial College Business SchoolSource: Rajan & Wulf 2006

Delegation without empowerment• Delayering has robust empirical support but some work has confused

delayering with empowerment as the OB literature shows

• …insecurity has risen and trust has fallen (Di Maggio 1997)

• “Little evidence of middle managers autonomy” (Morris et al 2008).

• “The proportions reporting a great deal of influence over how to do tasks at work fell from 57 percent in 1992 to 43% in 2001 , where it remained in 2006” (Felstead et al 2009)

• Managers may take steps to motivate employees, but they are less willing to give them a voice in the way work is organized (Conway et al 2008)

• “…middle managers are eliminated and the firm bifurcates into top managers …and worker/managers…” (Rajan & Wulf 2006)

© Imperial College Business School

Internal Governance Theories

• The internal governance theories do not explain trend towards shareholder orientation

• Access plus high powered incentives do not resolve problems of non-contractible commitment

• Any trade-off between authority and delegation within the firm is hard to relate to forms of external governance because it requires CEO autonomy

© Imperial College Business School

Why has the balance shifted to shareholder value?

• Have agency concerns become more important? – Probably not

• Have firm specific investments of skills and resources become less important – Probably not

• Have non-contractible investments been facilitated by organisational change? – Probably not

Shareholder value – alternative view

• Incentives for knowledge workers must be set against need for new external capital

• Control rights for knowledge workers may imply lower shareholder protection

• “Optimal split of rights [should] account …for its impact on pledgeable income” (Tirole 2001)

• Importance of external finance related to problems with internal capital allocation (Holmstrom & Kaplan 2001)

© Imperial College Business School

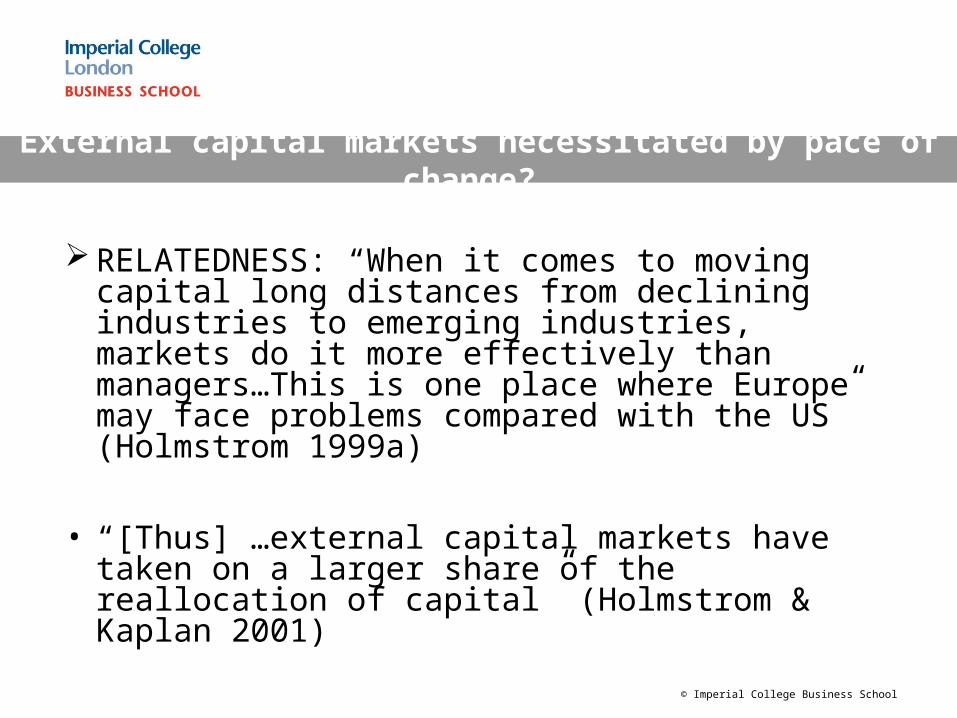

External capital markets necessitated by pace of change?

RELATEDNESS: “When it comes to moving capital long distances from declining industries to emerging industries, markets do it more effectively than managers…This is one place where Europe may face problems compared with the US” (Holmstrom 1999a)

• “[Thus] …external capital markets have taken on a larger share of the reallocation of capital” (Holmstrom & Kaplan 2001)

© Imperial College Business School

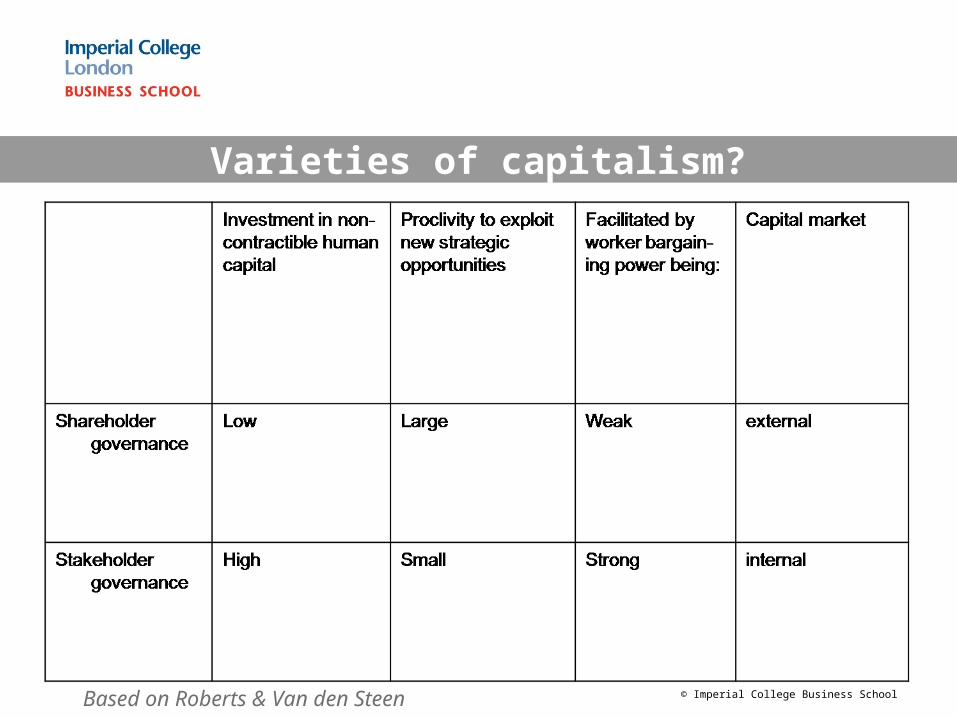

Varieties of capitalism?

© Imperial College Business SchoolBased on Roberts & Van den Steen

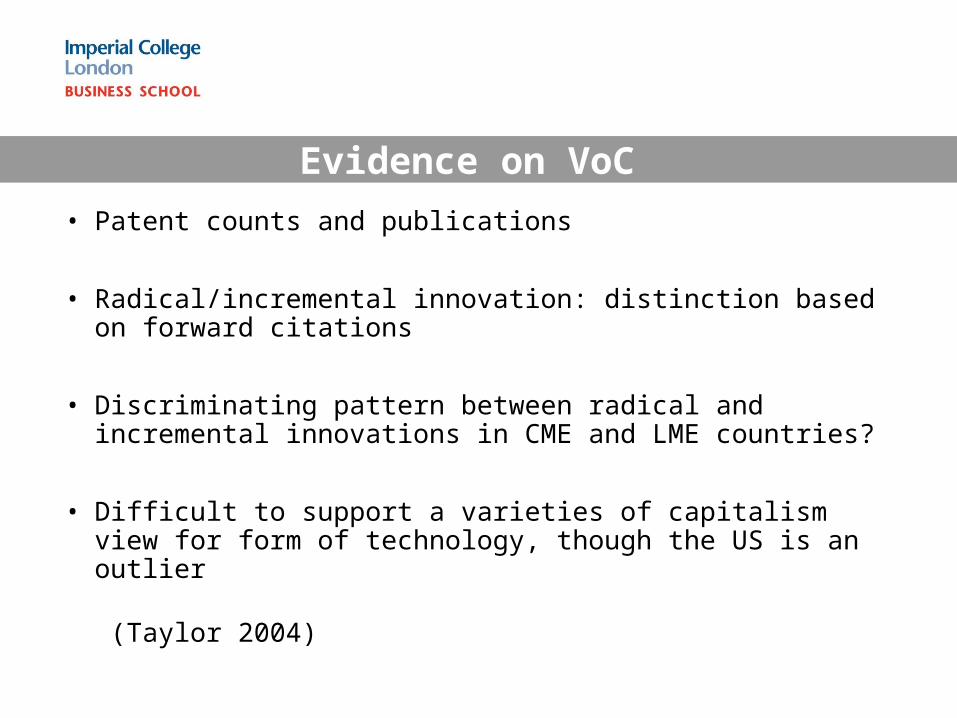

Evidence on VoC

• Patent counts and publications

• Radical/incremental innovation: distinction based on forward citations

• Discriminating pattern between radical and incremental innovations in CME and LME countries?

• Difficult to support a varieties of capitalism view for form of technology, though the US is an outlier

(Taylor 2004)

Importance of External Allocation for Sectoral Transfer

• Transfer of resources across (heterogeneous) sectors explains US – Europe gap?

• Testable using shift-share analysis of productivity

• The data do not show this (Maudos et al 2008). US hourly labour productivity advantage over Europe lies within sectors (47-sector decomposition) and relates to whatever starting composition it had before the 1990s.

Conclusions

• We are left with a paradox in search of an explanation. Why has shareholder value gained ground? One answer is loss of trust by employees. The absence of trust makes managerial autonomy potentially unfeasible under current governance arrangements so that internal allocation becomes problematic. In its place there is more top-level control, high-powered incentives and siphoning off of free cash flow for external allocation.

© Imperial College Business School