who leaves, where to, and why worry? employee mobility ...terpconnect.umd.edu/~rajshree/research/38...

TRANSCRIPT

Strategic Management JournalStrat. Mgmt. J., 33: 65–87 (2012)

Published online EarlyView in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.943

Received 26 January 2010; Final revision received 1 June 2011

WHO LEAVES, WHERE TO, AND WHY WORRY?EMPLOYEE MOBILITY, ENTREPRENEURSHIP

AND EFFECTS ON SOURCE FIRM PERFORMANCE†

BENJAMIN A. CAMPBELL,1 MARTIN GANCO,2 APRIL M. FRANCO,3

and RAJSHREE AGARWAL4*1 Fisher College of Business, Ohio State University, Columbus, Ohio, U.S.A.2 Carlson School of Management, University of Minnesota, Minneapolis, Minnesota,U.S.A.3 Rotman School of Management, University of Toronto, and Department ofManagement, University of Toronto at Scarborough, Toronto, Ontario, Canada4 Robert H. Smith School of Business, University of Maryland, College Park, Maryland,U.S.A.

We theorize that the value provided by the firm’s complementary assets has important implica-tions for the exit decisions of employees and their subsequent effects on the firm’s performance.Using linked employee-employer data from the U.S. Census Bureau on legal services, we findthat employees with higher earnings are less likely to leave relative to employees with lowerearnings, but if they do, are more likely to create a new venture than join another firm. Employeeentrepreneurship has a larger adverse impact on source firm performance than moves to estab-lished firms, even controlling for observable employee quality. Our findings suggest that inknowledge intensive settings, managers should focus on tailoring compensation packages to helpminimize the adverse impact of employee entrepreneurship, particularly among high performingindividuals. Copyright 2011 John Wiley & Sons, Ltd.

INTRODUCTION

Human assets often represent an organization’s keycompetency and source of competitive advantage(Coff, 1997; Lippman and Rumelt, 1982), thusstrategic management of human assets is criticalparticularly in knowledge-intensive industries. AsCoff eloquently argued, translating human assetsto sustainable competitive advantage is fraught

Keywords: entrepreneurship; strategic human capital;employee mobility; complementary assets; professionalservice firms

† All authors contributed equally.*Correspondence to: Rajshree Agarwal, Robert H. Smith Schoolof Business, Department of Management and Organization, Uni-versity of Maryland, 4512 Van Munching Hall, College Park,MD 20742, U.S.A. E-mail: [email protected]

with management dilemmas, given the obviousfact that employees ‘walk out the door eachday, leaving some question about whether theywill return’ (1997: 375). Employee mobility putsfirms in the precarious position of not only los-ing their competitive advantage but also enablingtheir competition, given the transfer of the humanassets to either established competitors or to ‘spin-outs’ (i.e., entrepreneurial ventures created by ex-employees).1 In addition, the firm’s disadvantagemay be amplified by the ability of the exiting

1 A spin-out is defined as a start-up founded by a formeremployee of an established firm within the same industry (Agar-wal et al., 2004). Employee movement between organizationsthat have ownership affiliations are typically not consideredemployee entrepreneurship or mobility events (e.g., Agarwal,Ganco, and Ziedonis, 2009).

Copyright 2011 John Wiley & Sons, Ltd.

66 B. A. Campbell et al.

employee to transfer or recreate the complemen-tary assets that were important in value creation.

Because employee mobility may lead to firmdisadvantage, the following research questions arecritical in the strategic management of human cap-ital: what types of employees are most likely toleave, what types of firms are they most likely tojoin, and what are the competitive ramificationsfor the focal firm’s performance? To answer thesequestions, we develop our theoretical rationale foremployee mobility and entrepreneurship decisionsby drawing on Teece (1986) and the importanceof complementary assets to value created by thecore assets. In our context, the core asset refers tothe human capital embodied in the focal employeewho is at risk of exit, while the complementaryassets relate to the other human and nonhumanresources and capabilities (e.g., other employees,routines, opportunities, physical assets, intellectualproperty, etc.) that are provided by the firm for thecreation of value. We posit that the relative bar-gaining power of the firm with the focal employeewill be determined by the employee’s ability torecreate or transfer the complementary assets. Thisaffects employees’ decisions to stay, create a newventure, or join another established firm. Further,we posit that each of these three employee-leveldecisions lead to differential performance ramifica-tions for the focal firm and are, thus, an importantsource of performance heterogeneity.

We examine our research questions in the empir-ical context of the legal services industry—aprofessional services sector where human assetsare critical for the creation and appropriation ofvalue. Using data derived from a custom extractof the Longitudinal Employer-Household Dynam-ics (LEHD) Project2 used at the U.S. CensusResearch Data Center in Chicago, we test our pre-dictions about who leaves, where they go, and theimpact of the mobility events on source firm per-formance. At the individual employee level, wefind support for our hypotheses that higher incomeearners are less likely to be mobile, but if theydo leave, they are more likely to be involved infounding a spin-out firm. At the firm level, wefind that employee moves to a spin-out have alarger adverse impact on source firm performancethan employee moves to established firms, evenafter controlling for observable employee quality

2 For details, see http://lehd.did.census.gov/led/library/tech userguides/overview master zero obs 103008.pdf

differences. We also find that the adverse impactof employee entrepreneurship on source firm per-formance increases with employee earnings.

In addressing these questions, we contribute tothe literature on strategic human capital manage-ment and entrepreneurship. We connect humancapital and strategy by extending Teece’s (1986)framework of complementary assets to the micro-level mobility decisions of individual employeesand the impact of these decisions on macro-levelfirm outcomes. Through this framework, we aug-ment the understanding of how employees andemployers generate and appropriate value andthe extent to which complementary assets mayaffect each party’s bargaining power vis-a-vis theother. Our research also contributes to the con-nection between strategy’s knowledge-based viewand research on knowledge spillovers throughemployee mobility and employee entrepreneur-ship by simultaneously examining both the deter-minants and the effects of knowledge transferthrough employee moves to established firms ver-sus employee entrepreneurship. Thus, our researchsuggests that strategic management of complemen-tary assets may help mitigate the potentially neg-ative performance consequences of moves, andalso enable firms to assess the differential likeli-hood of moves to rivals versus to spin-outs. Fur-ther, in keeping with Schumpeter’s (1934) conceptof creative destruction, we explicitly capture thedestruction of source firm value wrought by thecreation of spin-outs. There are greater pressureson source firms due to employee movement tospin-outs rather than to established firms. As aresult, new venture creation may be more harmfulto the source firm than employee mobility amongalready existing firms.

THEORETICAL FRAMEWORK ANDHYPOTHESES

Human assets have been recognized as an integralpart of value creation, and their value increaseswith the knowledge intensity of an industry (Coff,1997; Lippman and Rumelt, 1982). Since employ-ees can quit at will, Coff (1997) highlightedthe uncertain ‘ownership’ by firms of valuablehuman assets. Coff questioned whether competi-tive advantage based on human assets is truly sus-tainable, absent systems to cope with the associatedmanagement dilemmas. In doing so, Coff’s work

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 67

underscored the need for research that integratesmicro-level human resource management (HRM)and macro-level strategic management to helpidentify factors that impact not only value creationbut also the extent of value appropriation by eachof the co-creators: the focal individual and the firm.From a macro perspective, greater appropriationof value by the employees as stakeholders in thefirm implies that common measures of firm per-formance such as profitability may understate thetrue extent of value creation of the firm. Further,by undertaking such an integration, we can informmicro-level HRM strategies regarding compensa-tion of heterogeneous employees based on theirrelative bargaining power by explicitly accountingfor the macro strategic implications of employeemobility and entrepreneurship, given the rich liter-ature stream that underscores the competitive rami-fications of employee exit (Phillips, 2002; Somaya,Williamson, and Lorinkova, 2008; Wezel, Cattani,and Pennings, 2006; Aime et al., 2010).

We integrate these perspectives by beginningwith a framework that models differences in orga-nizational and employee bargaining power as afunction of two dimensions: the importance of afirm’s complementary assets to value creation, andthe ability of an employee to transfer or recre-ate the complementary assets outside the firm’sboundaries.

Complementary assets, relative bargainingpower, and value appropriation in theemployee-employer relationship

In his seminal article, Teece (1986) identifiedthe importance of complementary assets to coretechnological know-how in both the creation andappropriation of value. While largely used toexplain value appropriation by innovating firms(Franco et al., 2009; Gans and Stern, 2003; Trip-sas, 1997), by linking it to the classic articles byAlchian and Demsetz (1972) and Klein, Craw-ford, and Alchian (1978), this framework can alsoshed light on human resource management issues.Alchian and Demsetz (1972) discuss the impor-tance of the firm to an employee for creatingvalue, since it facilitates the contractual relation-ships between the various owners of the comple-mentary inputs that are required jointly for pro-duction. Further, Klein et al. (1978) discuss howfirms’ ownership of specialized assets (e.g., brandname and reputation) increases the value that can

be created by the employee in conjunction, ratherthan in isolation.

The complementarities in this employee-employer value-creating relationship led to Hart’sinsightful observation: ‘Control over non-humanassets leads to control over human assets’ (1995:58, italics in original). Thus, we can enhanceTeece’s (1986) depiction of the interaction betweencore and complementary assets to include the casewherein a firm’s complementary assets are impor-tant to the ‘core’ knowledge possessed by theemployee at risk of exit (the focal employee). Thecomplementary assets may consist of organiza-tional knowledge (e.g., codified routines, knowl-edge embodied in products and processes, andintellectual property rights), nonhuman comple-mentary assets (e.g., physical capital, contractualrelationships with buyers/suppliers, brand equity,and reputation), and human complementary assets(e.g., tacit knowledge embodied in other employ-ees). Firms can appropriate ‘quasi-rents’ based onthat portion of value that employees are unable tocreate absent these complementary assets, (Klein,et al., 1978). However, the ‘portability’ of thesecomplementary assets, or the extent to which anemployee is able to transfer or recreate comple-mentary assets, will in turn limit the firm’s abilityto appropriate these quasi-rents.

We depict the relationship between relative bar-gaining power and resultant value appropriationbetween the firm and the employee in Figure 1.The x-axis in Figure 1 represents the relativeimportance of a firm’s complementary assets tothe focal employee’s human assets for value cre-ation, and the y-axis represents that employee’sability to recreate or transfer these complementaryassets outside the firm’s boundaries. The relativebargaining power of the firm and the employeeis a function of whether the firm’s complemen-tary assets are important for value creation, and ofwhether the employee can walk away with thesecomplementary assets or recreate them at low costafter exit. Accordingly, we differentiate three areasin Figure 1.

If complementary assets are important to valuecreation and not easily reproducible by theemployee outside a firm (e.g., intellectual prop-erty rights on complementary knowledge or spe-cialized physical assets), the firm can prevent anemployee from competing with it, thus limiting theemployee’s outside options. As a result, the firmwill possess greater bargaining power—allowing it

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

68 B. A. Campbell et al.

Importance of firm’s complementary assets in valuecreation relative to the focal employee’s human assets

Abi

lity

of th

e fo

cal e

mpl

oyee

to r

ecre

ate

ortr

ansf

er c

ompl

emen

tary

ass

ets

afte

r ex

itfr

om f

irm

Employeeadvantage

Bilateralbargainingpower

Firmadvantage

Figure 1. Complementary assets and relative bargainingpower of employee

to appropriate a higher share of the value created(the area labeled ‘Firm advantage’ in Figure 1). Onthe other hand, even when the firm possesses thenecessary complementary assets, an employee whois able to recreate or transfer these to a recipientfirm will have higher bargaining power and mayappropriate much of the value created (‘Employeeadvantage’ in Figure 1). As a result, the employeehas a bargaining advantage over the employer.The middle area represents a situation of bilat-eral bargaining power: the firm’s complementaryassets are important for value creation, and thefocal employee has limited ability to recreate thesecomplementary assets. Thus, the ability of eitherthe employee or the firm to appropriate value islimited.

Who leaves? Types of human assets andpropensity for exit

In examining questions related to employeepropensity to exit, our key underlying constructis the ability of an employee to generate valuefor the employer. The construct is highly corre-lated with employee earnings and related to manyfactors, including the employee’s innate ability,education, and experience; motivation to work;social network (Shaw et al., 2005); and positionand responsibilities in the firm (Elfenbein, Hamil-ton, and Zenger, 2010; Castanias and Helfat, 2001;Williams and Livingstone, 1994; Zenger, 1992).Variation in the above factors among individualsalso results in heterogeneity in their generationof value within a firm. Since the human assets

embodied in a focal employee (core knowledge)determine what is complementary for value cre-ation, both dimensions represented in Figure 1vary with the focal employee’s human assets.Employees with low human capital are likely tocontribute less to total created value than thosewith high human capital. Further, they are lesslikely to recreate or transfer complementary assets,thus diminishing their bargaining power and abil-ity to appropriate value. Accordingly, they fall intothe ‘Firm advantage’ area of Figure 1. In con-trast, strong skills, education, experience, and workethic imply higher levels of knowledge embod-ied in employees. Further, these factors are corre-lated with promotions, which increase individuals’control and authority within the firm (Castaniasand Helfat, 2001; Huselid, 1995; Phillips, 2002;Zenger, 1992). These employees have higher bar-gaining power because of their ability to replicatenecessary complementary assets. They can cred-ibly threaten to exit and transfer complementaryresources and opportunities from a firm. Trans-ferred resources may include technologies identi-fied while working within the firm (Agarwal et al.,2004; Bhide, 1994; Klepper and Sleeper, 2005),supporting team members (Groysberg, Nanda, andPrats, 2009), and social networks (Burton,Sørensen, and Beckman, 2002). Transferred oppor-tunities may include attracting clients (i.e., a firm’s‘book’) to a new firm (Stull, 2009; Taylor, 2000,2005), a focus on niche industry segments (Agar-wal et al., 2004), and creation of new products andpractices (Mondics, 2009; Taylor, 2000). Conse-quently, high value generators have high bargain-ing power vis-a-vis their firms and capture mostof the value they create. Thus, they are likely tobe in either the ‘Bilateral bargaining power’ or‘Employee advantage’ area of Figure 1.

We posit that, although the exit of employeeswith high human capital diminishes firm valuemore than does the exit of those with low humancapital, the former are less likely to actually exit,given their increased ability to appropriate value.This view is consistent with evidence from theHRM literature that firms provide both pecuniaryand nonpecuniary benefits to such employees toreduce turnover (Williams and Livingstone, 1994;Zenger, 1992). Firms’ sharing ‘rents’ with high-performing employees in the form of higher wagesnot only increases employees’ perceptions of dis-tributive and procedural justice (McFarlin and

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 69

Sweeney, 1992) but also creates a penalty for exit-ing (Coff, 1997; Weiss, 1990; Zenger, 1992). Inaddition, since employees with higher levels ofknowledge value the intrinsic satisfaction of theirwork, autonomy, and input (Raelin, 1991), firmscan optimize the fit of their complementary assetsto employees’ core knowledge, and create stronginternal ties (Dess and Shaw, 2001; Lee et al.,2004) to better motivate these people to stay andperform well (Hackman and Oldham, 1980).

The above human capital management strategiestranslate into high-performing employees havingenhanced ability to appropriate value and thus gainhigh earnings, reducing their desire to leave andincur the costs and risks of mobility. Thus, eventhough high earners are more able to transfer orrecreate a firm’s complementary assets, they areless likely to do so. Coff (1997) provided casestudy evidence that although high-producing secu-rity brokers could leave their current firms with 95percent of their clients and business, their turnoverrate was less than 10 percent, given their firms’‘rent-sharing’ in the form of pay, performance-based incentives, and high participation in criti-cal management-related decisions. This argumentleads us to our first baseline hypothesis:

Hypothesis 1: The relationship between earn-ings and the likelihood of employee mobility isnegative.

Where to? Employee moves to spin-outs vs.established firms

There are important differences between anemployee moving to an established firm andemployee entrepreneurship. While moving toanother established firm does entail adjustmentcosts, the risks and challenges of engaging inentrepreneurship are different. Starting a newenterprise implies undertaking the risk of operat-ing a new business, given the daunting statisticthat over a third of new firms do not survivefor five years (Agarwal and Audretsch, 2001).Drucker (1985) attributed the high failure rateof entrepreneurial enterprises not to the qual-ity of their underlying ideas or innovations, butto the lack of business and management skillsamong their founders. Anecdotally, Gordon Mooreattributed spin-out Shockley Semiconductor’s fail-ure to its lack of management experience (Moore

and Davis, 2001). Thus, when contemplating spin-ning out, the challenges facing an employee relateto the creation of an organizational structure thatcan generate synergies between their knowledgeand the necessary complementary assets.

We posit that higher performers/earners are morelikely to found start-ups than other employees.3

First, while the literature in HRM and entre-preneurship have developed in parallel, ourintegration reveals that many of the same individ-ual characteristics positively associated with jobperformance and, thus, individual earnings (Par-sons, 1977; Castanias and Helfat, 2001), are alsopositively associated with entrepreneurship. In theHRM literature for instance, meta-analyses of therelationship between personality traits and job per-formance find that conscientiousness, emotionalstability, and extraversion are strong positive pre-dictors of job performance (Barrick and Mount,1991; Hurtz and Donovan, 2000; Salgado, 1997).Entrepreneurship researchers have also found thatthese same traits are meta-analytically associ-ated with individuals’ intentions of forming theirown firms (Zhao and Seibert, 2006; Zhao, Seib-ert and Lumpkin, 2010). Braguinsky, Klepper, andOhyama (2009) connect employees’ entrepreneur-ship ability to their ability to create value for theiremployer. In addition, intelligence is a strong pre-dictor of job performance in the HRM literature(Schmidt and Hunter, 1992; Ree and Earles, 1992),and for new venture formation because it increasesan individual’s absorptive capacity (Cohen andLevinthal, 1990; Shane, 2005) and thus the abil-ity to recognize new opportunities (Knight, 1921;Shane and Venkataraman, 2000) and exploit them(Hebert and Link, 1989).

Second, unlike joining an established firm, start-ing a new venture requires an individual to addressissues related to optimal organization. In this con-text, the individual’s ability to transfer or recreatecomplementary assets (the y-axis of Figure 1) iskey. Since earnings are typically correlated withability, experience, and status, high earners are bet-ter than low earners at replicating complementaryassets and transferring resources and opportuni-ties from the source firm (Agarwal et al., 2004;Bhide, 1994; Burton, Sørensen, and Beckman,2002; Klepper and Sleeper, 2005; Mondics, 2009;

3 Groysberg et al. (2009) and Elfenbein et al. (2010) provideempirical evidence of this relationship, but do not offer anytheoretical explanation of their empirical findings.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

70 B. A. Campbell et al.

Taylor, 2005; Stull, 2009). Accordingly, high earn-ers founding new firms have higher value creationpotential and lower set-up costs and risks. In con-trast, mobile employees with lower earnings maybe limited in their ability to replicate complemen-tary assets effectively, and they may be more likelyto move to established firms rather than to foundstart-ups.

Third, it is easier to transfer or replicate theresources and opportunities to ‘new soil’ thantrying to graft them onto an existing organiza-tion. Existing organizations may be characterizedby complex internal networks, and the existingbureaucratic structure may retard the employee’sability to recreate or transfer the complementaryassets. Further, since high earners typically accu-mulate more firm-specific skills, resources, andidiosyncratic knowledge (Coff, 1997; Williamson,1975) relative to low earners, they will experi-ence greater challenges in integration and recon-figuration of their resources and knowledge in anexisting organization. The lack of a bureaucraticstructure in a new firm allows greater ability totransfer and replicate the necessary complementaryassets. For example, Ganco (2010) found that teammobility (i.e., transfer of complementary humanassets) is higher to a start-up rather than an existingfirm. Similarly, while the link between knowledgefrom one established firm to another after mobil-ity events is neither direct nor clear, Agarwal et al.(2004) showed that spin-outs do inherit knowledgefrom their parents through their founders.

While the above reasons relate to the ability ofhigh earners to transfer core and complementaryassets to a new venture relative to an establishedfirm, differences in motives may be salient to thechoice of where employees go. Since high earnerscan appropriate most of the value they create, theirmotivation for exit could be twofold. First, theymay believe they could generate or appropriateeven more value outside their current firm becausethey see underexploited opportunities, poor fit withtheir skills, and other constraints at that firm. Theseinertial tendencies are likely to exist at other estab-lished firms, and a move might even exacerbatethem to the extent that differences in corporate cul-ture create a difficult match (Coff, 1997). Thus, ifmotivated by frustration with parental inertia andperception of underexploited opportunities (Agar-wal et al., 2004; Klepper and Thompson, 2010),employees are more likely to move to spin-outsthan to existing firms. Second, high earners are

likely to have diminishing marginal returns topecuniary gain and may value nonpecuniary fac-tors such as job satisfaction and autonomy morethan low earners (Blanchflower and Oswald, 1998;Gompers, Lerner, and Scharfstein, 2005; Hamil-ton, 2000; Puri and Robinson, 2007; Teece, 2003).Starting a new firm enables them to fulfill nonpecu-niary aspirations better than moving to an existingfirm with constraining norms.

In sum, we expect employees with high earningsto be less likely to move, but if they do move, theyare more likely to start new firms. Accordingly,

Hypothesis 2: Conditional on mobility, employ-ees with greater earnings are more likely to joinspin-outs than established firms.

Why worry? Impact on source firmperformance

How do the micro-level mobility choices ofemployees affect macro-level firm performance?We turn to the analysis of the impact of moves toestablished firms and to spin-outs on source firmperformance. Regardless of where an employeegoes, the mobility event represents the sourcefirm’s loss of the focal human asset as a criticalresource (Phillips, 2002). The competitive impacton the source firm of this loss is a function of therecipient firm’s ability to capitalize on the focalhuman asset and is greater for employee movementto a spin-out than to an established firm becauseit is harder to assimilate the employee’s accumu-lated firm-specific skills, resources, and idiosyn-cratic knowledge at an established firm (Coff,1997; Williamson, 1975).

Moreover, moving to a spin-out also results ina greater replication and transfer of complemen-tary assets, thus impacting the source firm moreadversely than a move to an established firm.Employees who start a firm are more motivatedto transfer the necessary resources and capabil-ities given the high risk and uncertainty associ-ated with starting a new venture (Agarwal andAudretsch, 2001; Drucker, 1985, Khessina andCarroll, 2008). While employees who move toestablished firms have the relative luxury of lever-aging the latter’s existing complementary assets,employee entrepreneurs need to recreate comple-mentary assets. Wezel et al. (2006) hypothesizethat the replication of a source firm’s organiza-tional knowledge and routines in a spin-out is

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 71

a likely cause of the greater adverse impact ofemployee moves to spin-outs versus those to estab-lished firms. More importantly, employees are bet-ter able to transfer both human and nonhumancomplementary assets to spin-outs than to estab-lished firms (Agarwal et al., 2004). In particular,supporting team members are important comple-mentary assets (Groysberg et al., 2009) that aremore susceptible to transfer to a start-up than toan existing firm (Ganco, 2009). Such transfers willhave a larger negative impact on the source firm’sperformance than transfers to established firms.

The transfer of nonhuman complementary assetsalso increases the impact of employee entre-preneurs on their parent firms. Research in rela-tionship marketing highlights the importance ofemployees as the ‘face of the firm,’ even in firm-firm interactions (e.g., business-to-business sales),and the importance of employees in both firm cus-tomer relationships (e.g., end-consumer sales) andprofessional services (provider-customer) relation-ships (Berling, 1993; Crosby, Evans, and Cowles,1990; Iacobucci and Ostrom 1996; Solomon et al.,1985). Similarly, employees starting new firms cancapitalize on their relationships with customers andcash in on their parent firm’s reputation, sincebrand loyalty is connected to the employees ratherthan to the firms (Beatty and Lee, 1996), and cus-tomers are more willing to follow the employeesthan to stay with the parent (Beatty and Lee, 1996;Stull, 2009; Taylor, 2000, 2005).

The transfer of complementary assets and oppor-tunities is damaging to a source firm. Since com-plementary assets are more likely to be transferredto start-ups than to existing firms, we theorizethat employee moves to spin-outs have a largernegative impact than moves to established firms.Consequently, we propose:

Hypothesis 3: The adverse impact on source firmperformance of employee mobility is greater formoves to spin-outs than moves to establishedfirms.

Our final hypothesis on the impact of mobilityon source firm performance directly flows fromthe linkages among the previous hypotheses. Theloss of high value generating employees has ahigher detrimental effect on a firm’s performancethan the loss of low value generating employ-ees, since in the former case the parent firm losesemployees who are core to its creation of value

(Phillips, 2002). This is supported by research thatpoints to the impact of inadequate chief executiveofficer succession planning on firm value (David-son, Nemec, and Worrell, 2001; Harris and Helfat,1998). At the micro-level, we reasoned in Hypoth-esis 1 that employees with higher ability to gen-erate value have greater ability to transfer and/orrecreate complementary assets; and, in Hypothe-sis 2 we argued that they are more likely to joinspin-outs than established firms. Further, employeemobility adversely impacts parent firm perfor-mance through the transfer/replication of comple-mentary assets, and exiting employees moving to aspin-out have greater ability and incentive to trans-fer/replicate complementary assets than movers toestablished firms.

If higher ability employees are more likely tocreate spin-outs and more able to transfer or recre-ate complementary assets, it follows that the dif-ference in the impact on source firm performanceassociated with an exit to an established firm ver-sus one to a spin-out increases with the exitingemployee’s ability. Employees with low value-generating ability also have low ability to replicatecomplementary assets. As the ability to generatevalue increases, employees are also able to transfera larger pool of complementary assets and oppor-tunities. Given higher absolute differences in boththe core and complementary assets that may betransferred to a spin-out relative to an establishedfirm, the difference in the impact of a move to spin-out and a move to an established firm increaseswith the mobile employee’s earnings. This reason-ing leads to the following:

Hypothesis 4: The adverse impact on source firmperformance of employee moves to spin-outsrelative to moves to established firms increaseswith the earnings of the mobile individuals.

DATA AND METHODOLOGY

Context: the U.S. legal services industry

We tested our hypotheses using data from the legalservices industry. We focus on a professional ser-vice context due to its knowledge intensivenessand the critical role of human assets. Professionalservices, which include legal, financial, manage-ment, consulting, education, and health care, are alarge and growing portion of the economy (Buera

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

72 B. A. Campbell et al.

and Kaboski, 2008). Services constituted 68 per-cent of the U.S. gross domestic product (GDP) in2007 (relative to 19 percent for manufacturing),and within the services sector, professional ser-vices contributed to 49 percent of GDP in 2009(Bureau of Economic Analysis, 2010).4 Since pro-fessional services are human capital intensive,portability of complementary assets is relativelyeasier than in manufacturing industries. In legalservices, as in other professional service industries,complementary assets are likely to be embodiedin people and human assets are more importantthan physical assets (Teece, 2003). Since comple-mentary human assets are more easily transferablethan complementary physical assets (Coff, 1997),mobility and spin-out generation is common in theprofessional services sector (Teece, 2003). Further,employment contracts in legal services excludenon-compete clauses and, for lawyers who havepassed relevant bar exams—key players in theindustry—the barriers to mobility and entry arelow. As a result, the costs associated with mobil-ity are relatively low for employees (within theborders of a state) and new firm creation rates arehigh.5 Thus, the legal services industry representsan active environment in which to study issuesrelated to the strategic management of talent.

The dominant organizational design in legal ser-vices is partnership, wherein partners own firmsand almost all revenues are returned to employees,including partners, as taxable earnings. The major-ity of these firms’ employees fall into the followingcategories: equity partner lawyers; associate andsalaried lawyers; assistants, secretaries, and parale-gals (staff). Lawyers typically account for approx-imately 80 percent of employees (Wymer, 2009).Lawyers are typically promoted to partners withinsix or seven years of joining their firms, at whichpoint they can earn a share of revenues. Theseare divided either evenly or on the basis of indi-vidual contribution (Gilson and Mnookin, 1985).Notably, an important driver of mobility is the‘tournament’ employment system, in which asso-ciates who are not promoted are typically forced toleave. To rule out alternative explanations related

4 See http://www.bea.gov/industry/xls/GDPbyInd VA NAICS1998-2010.xls. The shift from manufacturing to services indeveloped nations has been rising since the mid-20th century(Baumol, 1967).5 State-specific bar exams cause low transferability of lawyers’credentials across state borders but high transferability withinstate borders.

to tournament-driven mobility for Hypotheses 1and 2, we conduct robustness checks by examiningsub-samples of employees that are not likely to beat risk of involuntary turnover (Please see Table 4Panels 3–6 in the Results section, and discussionbelow).

Data source

The data for the study are derived from theLEHD Project. Our custom extract includes linkedemployer-employee data drawn from state-levelunemployment insurance (UI) records and sev-eral data products from the U.S. Census Bureau.Every quarter, organizations that pay into theirstate’s UI fund submit form ES-202, which lists allemployees covered by the UI program, their tax-able earnings, and firm characteristics. From thesemandatory submissions, the LEHD project con-structs both employer characteristics files, whichinclude longitudinal records of firm-level char-acteristics,6 and employment history files, whichinclude longitudinal records of all employment‘spells’ (periods), including employer name andtaxable earnings, for all employees covered byUI. Individual characteristics files, containing indi-cators like gender, date of birth, race, ethnicity,and education, are drawn or imputed from theSocial Security Administration’s ‘Personal Char-acteristics Files,’ the decennial census, the CurrentPopulation Survey, and the Survey of Income andProgram Participation. Together, the longitudinaldata is rich with individual-, firm-, and dyad-levelcharacteristics.

Our data identify all individuals employed inU.S. legal services in the following states: Califor-nia, Florida, Illinois, New Jersey, North Carolina,Oregon, Pennsylvania, Texas, Virginia, and Wis-consin. The time frame depends on when the indi-vidual participating state chose to enter the LEHDprogram; the earliest states entered the program in1990, and other states entered across subsequentyears up to 1994. Since the data are drawn frommandatory filings, they cover the entire universe of

6 Because the data were collected at the state level, the firmidentifier is actually a firm-state identifier. As a result, ourdefinition of firm includes only the activities of a given firmlocated within a given state’s borders. Data limitations precludedlinking firms across state borders, so a firm that operated in statesx and y was disaggregated into two records: the firm’s activitieslocated in state x and the firm’s activities located in state y. Thehigh cost of crossing state borders in the legal services industryminimizes the impact of this issue on our empirical results.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 73

legal services firms in the 10 states. This universal-ity permits us to track interfirm employee mobilityand to identify new firms. Because the data arerestricted to legal service firms, the analysis is lim-ited to focusing only on employee mobility andemployee entrepreneurship where both the sourceand the target firm are legal service firms. As manylawyers are employed in the public sector or aremembers of an in-house legal staff, this restrictionleads to under-measurement of employee mobilityevents because we do not include employee mobil-ity where the employee moves from or moves toa different industry.7 This under-measurement ulti-mately provides conservative tests of our hypothe-ses. All results have been cleared for disclosure bythe U.S. Census Bureau to ensure that no individ-ual respondent or firm could be identified.

We draw a random 25 percent sample of theemployees in the data for our tests of Hypothe-ses 1 and 2. We restrict that sample to employeeswho earned more than $25,000 per year, and wereemployed at a firm that both contained more thanfive people and did not exit the data in that orthe subsequent year. The first restriction excludesemployees with a weak attachment to the labormarket; the second restriction excludes employ-ees of very small firms that contribute a smallpercentage of total industry revenues (Gilson andMnookin, 1985), and the third restriction excludesemployees of firms that die within two years of theindividual moving. This last restriction is particu-larly important to understanding employee mobil-ity from healthy firms, given that employees leav-ing dying firms may be systematically differentfrom employees who leave a healthy firm.

For our tests of Hypotheses 3 and 4, we aggre-gated all the employee-level data to the firm level.As in the sample used to test Hypotheses 1 and2, we exclude employees of very small firms(less than five people) and of dying firms (firmsthat exit within the next two years) to eliminatetheir effects on the measured impact of mobil-ity on firm performance. We also exclude firmobservations with revenues per employee of lessthan $10,000 or more than $1,000,000. Exclu-sion of firms with more than $1,000,000 revenueper employee eliminates a handful of observations

7 This under-measurement is likely to be small. Sauer (1998)shows that lawyers in the legal services industry tend to remainin the same industry (only 11% of the mobility events are fromlegal services to business sector [in-house counsel] and 6% topublic sector).

where firm revenues have a dramatic temporaryspike. Because firms with such a dramatic spike inearnings may be the firms that rely most heavily onthe ability of their human assets to generate value,excluding these observations provides a conserva-tive test of our hypotheses. Finally, we excludefirm observations that lost more than 20 employ-ees in any payroll class to an established firm orto a spin-out in a given year. This last restrictionallowed us to exclude mergers, acquisitions, andadministrative recoding of organizational identi-fiers.8

Estimation methodology

For the mobility analysis, we estimated a series oflinear probability models with dependent variablesthat were dummies indicating general mobilityand mobility to a spin-out. Firm-year fixed effectswere included to absorb any variation owing tounobserved characteristics, and use of robust stan-dard errors accounted for inherent heteroskedastic-ity. Computing constraints drove our choice of alinear probability model over a conditional logitmodel, since the large sample sizes made con-ditional logit computationally infeasible.9 Out-of-sample predictions were extremely rare in ourdata, which suggests that the model performedacceptably. Robustness checks confirmed consis-tency of the linear probability results with panellogit model results for a random 2.5 percent sam-ple of the data.

For the source firm performance analysis, weestimate a series of fixed-effects linear regressionequations of firm performance as a function of theintensity of different types of employee mobilityand firm characteristics. These allow us to assessthe impact of the quantity and quality of exitingemployees on source firm performance one yearafter a mobility event. Our explanatory variablesinclude number of exiting employees, their com-bined pay, and the number in different pay classes.We include firm fixed effects to absorb any vari-ation caused by unobserved firm characteristics.In each firm performance specification, we com-pare the effect of employees lost to spin-outs to

8 An administrative recode, or changes in a firm’s identificationnumber, are infrequent appearances in the data as large mobilityevents where all of a firm’s employees move from an existingfirm to a new firm.9 All analyses were limited by the time and computing poweravailable onsite at a Census Research Data Center.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

74 B. A. Campbell et al.

the effect of employees lost to established firms.The coefficients on these mobility measures cap-ture the impact on firm performance of each type ofevent relative to the baseline of no mobility. As aresult, comparing the two coefficients represents adifference-in-differences approach. The differencein coefficients captures the effect on firm perfor-mance of losing an employee to a start-up (relativeto no mobility) minus the effect on firm perfor-mance of losing an employee to an established firm(relative to no mobility). As we discuss the results,we focus on the comparison of the two mobilitymeasures to emphasize the differential effect onfirm performance of mobility to start-up relativeto mobility to established firm.

Variables

Employee mobility

The dependent variable for tests of Hypothesis 1,employee mobility, is a dummy variable coded 1 ifan employee’s dominant employer changed sincethe previous year and 0 otherwise. A dominantemployer is the one at which the employee earnedthe most during the year.

Employee exit to spin-out

This dependent variable for testing Hypothesis 2is a dummy coded 1 if an employee’s dominantemployer changed since the previous year and thenew employer appeared in the data for the firsttime in that year. This measure of exit to spin-outis broader than the typical definition of a spin-outfounder. To the extent that nonfounding employ-ees who join spin-outs are similar to employeeswho move to established firms, our results differ-entiating between moves to established firms andmoves to spin-outs should be seen as conserva-tive. That is, the presence of employee exits toestablished firms should bias our analysis againstfinding significant differences between the twocategories. Alternatively, nonfounding employeeswho join a spin-out during the first year of itsexistence (especially at higher levels of earnings)may be driven by motives and preferences similarto those of founder(s)—which may translate intosimilar characteristics and impact on the parentfirm. If that is the case, in the context of our theo-retical questions, the difference between foundingand nonfounding employees who join early is lesscrucial.

Firm performance

The dependent variable for testing Hypotheses 3and 4, firm performance, is measured as revenuesper employee. In the partnership model, almost allrevenues are returned to employees, which includepartners, as taxable earnings. By aggregating theearnings of all employees inside a firm, we couldconstruct its total revenues (less noncompensationcosts and set-asides for future years). To com-pare firms of different sizes, we divide revenuesby number of employees to obtain the averagefirm revenue generated per employee (includingpartners, associates, and staff). The firm perfor-mance measures are calculated at least one yearafter the measured mobility events, thus the firmperformance measures are based on the earnings ofthe retained workforce and any individuals hired toreplace the moving employees. Because this allowsfor replacement of individuals who left, this is aconservative measure of the impact of mobility.

Employee earnings

Our key explanatory variable for Hypotheses 1 and2, employee earnings, is measured as all forms oftaxable compensation that an employee received ina given calendar year; including salary, bonuses,and other reported income.

Firm-level mobility

The key explanatory variables for Hypotheses 3and 4 are measures of firm-level mobility. Weaggregate our exit measures over five years to cap-ture the lagged effect of employee mobility onfirm performance and also to facilitate disclosurereview at the Bureau of the Census. We constructtwo different variables to capture firm-level mobil-ity. First, we count the number of unique individ-uals who leave a firm to join another establishedfirm in each measurement year and the four yearsprior to it. We do the same for employees wholeave to join a spin-out. As a result, for every firm-year in the data, our measure captures the humanassets that exited to established firms and to spin-outs. Our second measure is based on employeemobility at different levels of employee earnings.We sort exiting employees into these earningsclasses: $25,000–$100,000, $100,000–$300,000,$300,000–$5,000,000, and $5,000,000+ and countthe number of movers to established firms andspin-outs in each class over the past five years.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 75

Control variables

Demographic characteristics and observable humanassets have been shown to play an important rolein the employee mobility decision. Specifically,employee mobility is impacted by age and tenure(Topel and Ward, 1992), and varies by gender(Loprest, 1992), race (Raphael and Riker, 1999),and education (Buchinsky et al., 2010). To con-trol for these underlying effects, we include mea-sures for the quadratic effects of age and tenure,and linear effects of gender, race, and years ofeducation. Years of education is a continuousvariable imputed by the Census Bureau. Genderand race are dummy variables (male/female andwhite/nonwhite, respectively). Age and tenure arecontinuous variables measuring time since birthand first year of employment at current firm,respectively. We include a dummy for individu-als with less than one year of tenure to capture theeffect of employees who do not have strong tiesto the labor market. Since our data begins in themiddle of the careers of some employees, tenureis ‘left-censored’ and under-measured for employ-ees who began working in the industry before thedata begins. To address this issue, we construct adummy indicating potentially left-censored tenurespells.

Similarly, the human assets possessed by thefirm have been shown to be an important predictorof firm performance (Hitt et al., 2001). Firm-levelcontrols for human assets include both measuresfor demographic composition and variables asso-ciated with human capital. We proxy for demo-graphic characteristics with gender and race andfor human capital differences with age and edu-cation (Becker, 1964). We control for the meansof the observed demographic and human capitalvariables measured over all of a firm’s employees.Specifically, we measure mean age, education, andpercentages of whites and men in each firm in thefourth quarter of each year. Because workforceschange over time as firms hire and lose employ-ees, year averages would have been biased, over-counting employees at firms with high employmentfluidity. Calculating within just one quarter min-imized the impact of fluidity on our measures,but we could still have overcounted employees,because the total number employed over a quartermight exceed a firm’s steady-state employment. Toaccount for the effect of unobserved characteristicsof the firm on firm performance, we also include

a firm fixed effect that controls for time-invariantunobserved differences across firms.

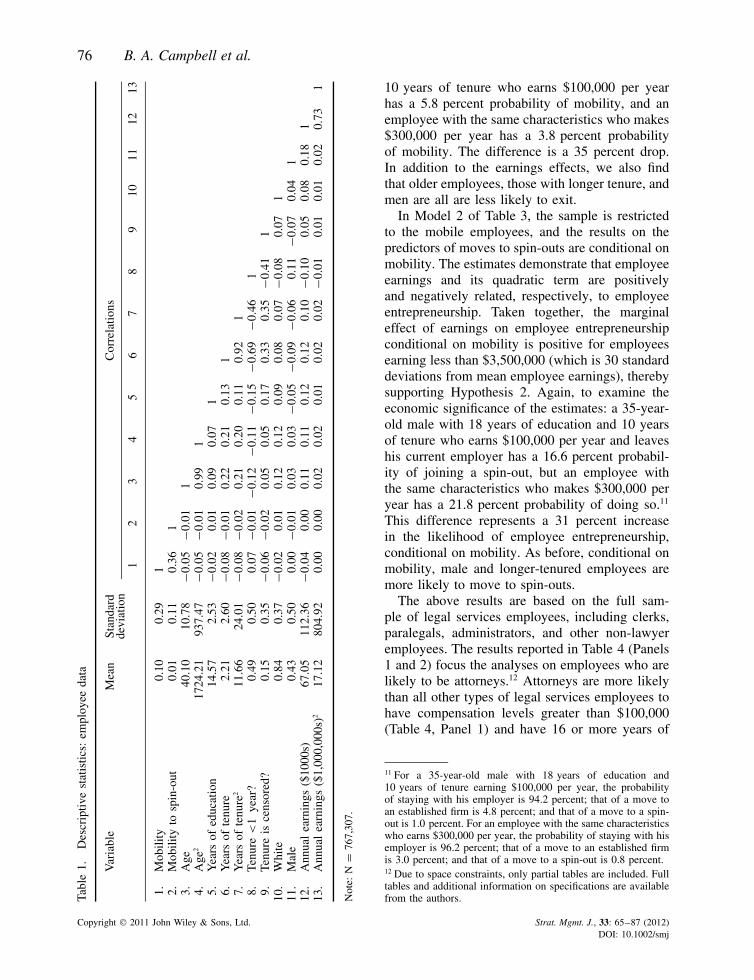

Tables 1 and 2 give descriptive statistics andcorrelations for the individual-level mobility dataand the firm-level performance data, respectively.There is no evidence of high correlations (exceptfor variables with their squared terms). As shownin Table 1, 10 percent of employees changed theirdominant employer in a given year, and 1 percentleft to go to spin-outs in any given year. The tworates imply that 10 percent of those exiting go tospin-outs. Our sample was largely white (84%) andfemale (56%), and it included many short-tenuredemployees. The average age was 40 years; averageeducation was 14 years of schooling; and averageearnings were $67,047 per year. Per Table 2, theaverage revenues per employee for firms were$63,007.10 The workforce had an average age of38 years, average education of 13.85 years, andaverage composition of 83 percent white, and 30percent male. Every year, the firms lost an average8.13 employees with total pay of $301,705 to otherestablished firms and lost 0.77 employees withtotal pay of $36,838 to spin-outs. On average,those exiting to established firms earned $37,089,and those exiting to spin-outs earned $47,704.

RESULTS

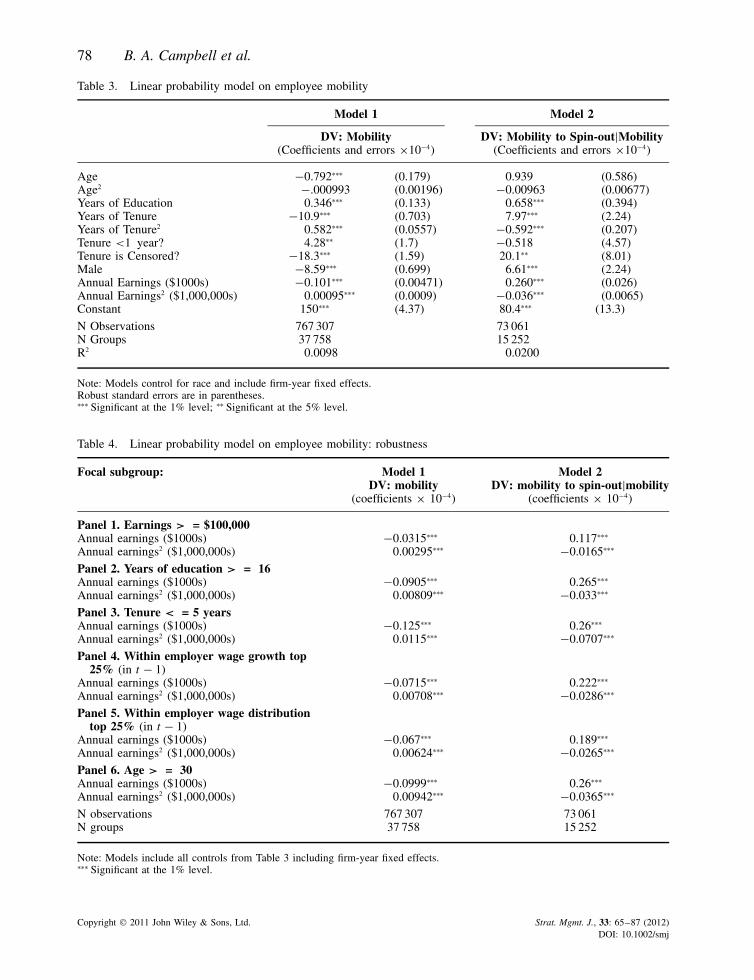

Table 3 contains our results on employee mobil-ity decisions. Model 1 in Table 3 provides esti-mates of the impact of employee characteristics onemployee mobility. Model 2 captures the impact ofemployee characteristics on the decision to go toa spin-out, conditional on mobility. Model 1 indi-cates that employee earnings are negatively relatedto employee mobility, and the square of earnings ispositively related to mobility. Combining both sta-tistically significant quadratic effects, the marginaleffect of earnings on mobility is negative foremployees earning between $0 and $5,200,000.Since $5,200,000 is over 45 standard deviationsaway from the mean of employee earnings($67,047), this finding thus suggests strong sup-port for Hypothesis 1. In terms of economic sig-nificance, the marginal effects reveal that a 35-year-old male with 18 years of education and

10 Individual-level measures and firm-level measures differ dueto the different sampling frames for the individual data and thefirm-level data and due to the churning concerns raised earlier.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

76 B. A. Campbell et al.

Tabl

e1.

Des

crip

tive

stat

istic

s:em

ploy

eeda

ta

Var

iabl

eM

ean

Stan

dard

Cor

rela

tions

devi

atio

n1

23

45

67

89

1011

1213

1.M

obili

ty0.

100.

291

2.M

obili

tyto

spin

-out

0.01

0.11

0.36

13.

Age

40.1

010

.78

−0.0

5−0

.01

14.

Age

217

24.2

193

7.47

−0.0

5−0

.01

0.99

15.

Yea

rsof

educ

atio

n14

.57

2.53

−0.0

20.

010.

090.

071

6.Y

ears

ofte

nure

2.21

2.60

−0.0

8−0

.01

0.22

0.21

0.13

17.

Yea

rsof

tenu

re2

11.6

624

.01

−0.0

8−0

.02

0.21

0.20

0.11

0.92

18.

Tenu

re<

1ye

ar?

0.49

0.50

0.07

−0.0

1−0

.12

−0.1

1−0

.15

−0.6

9−0

.46

19.

Tenu

reis

cens

ored

?0.

150.

35−0

.06

−0.0

20.

050.

050.

170.

330.

35−0

.41

110

.W

hite

0.84

0.37

−0.0

20.

010.

120.

120.

090.

080.

07−0

.08

0.07

111

.M

ale

0.43

0.50

0.00

−0.0

10.

030.

03−0

.05

−0.0

9−0

.06

0.11

−0.0

70.

041

12.

Ann

ual

earn

ings

($10

00s)

67.0

511

2.36

−0.0

40.

000.

110.

110.

120.

120.

10−0

.10

0.05

0.08

0.18

113

.A

nnua

lea

rnin

gs($

1,00

0,00

0s)2

17.1

280

4.92

0.00

0.00

0.02

0.02

0.01

0.02

0.02

−0.0

10.

010.

010.

020.

731

Not

e:N

=76

7,30

7.

10 years of tenure who earns $100,000 per yearhas a 5.8 percent probability of mobility, and anemployee with the same characteristics who makes$300,000 per year has a 3.8 percent probabilityof mobility. The difference is a 35 percent drop.In addition to the earnings effects, we also findthat older employees, those with longer tenure, andmen are all are less likely to exit.

In Model 2 of Table 3, the sample is restrictedto the mobile employees, and the results on thepredictors of moves to spin-outs are conditional onmobility. The estimates demonstrate that employeeearnings and its quadratic term are positivelyand negatively related, respectively, to employeeentrepreneurship. Taken together, the marginaleffect of earnings on employee entrepreneurshipconditional on mobility is positive for employeesearning less than $3,500,000 (which is 30 standarddeviations from mean employee earnings), therebysupporting Hypothesis 2. Again, to examine theeconomic significance of the estimates: a 35-year-old male with 18 years of education and 10 yearsof tenure who earns $100,000 per year and leaveshis current employer has a 16.6 percent probabil-ity of joining a spin-out, but an employee withthe same characteristics who makes $300,000 peryear has a 21.8 percent probability of doing so.11

This difference represents a 31 percent increasein the likelihood of employee entrepreneurship,conditional on mobility. As before, conditional onmobility, male and longer-tenured employees aremore likely to move to spin-outs.

The above results are based on the full sam-ple of legal services employees, including clerks,paralegals, administrators, and other non-lawyeremployees. The results reported in Table 4 (Panels1 and 2) focus the analyses on employees who arelikely to be attorneys.12 Attorneys are more likelythan all other types of legal services employees tohave compensation levels greater than $100,000(Table 4, Panel 1) and have 16 or more years of

11 For a 35-year-old male with 18 years of education and10 years of tenure earning $100,000 per year, the probabilityof staying with his employer is 94.2 percent; that of a move toan established firm is 4.8 percent; and that of a move to a spin-out is 1.0 percent. For an employee with the same characteristicswho earns $300,000 per year, the probability of staying with hisemployer is 96.2 percent; that of a move to an established firmis 3.0 percent; and that of a move to a spin-out is 0.8 percent.12 Due to space constraints, only partial tables are included. Fulltables and additional information on specifications are availablefrom the authors.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 77

Tabl

e2.

Des

crip

tive

stat

istic

s:fir

mda

ta

Var

iabl

eM

eans

Stan

dard

Cor

rela

tions

devi

atio

n1

23

45

67

89

1011

1213

14

1.C

umul

ativ

epa

yrol

lpe

rem

ploy

eein

t−1

63.0

147

.87

1.00

2.C

umul

ativ

epa

yrol

lof

leav

ers

toes

tabl

ishe

dfir

ms

301.

7159

2.97

0.22

1.00

3.C

umul

ativ

epa

yrol

lof

leav

ers

tosp

in-o

uts

36.8

415

5.50

0.12

0.27

1.00

4.C

umul

ativ

e#

ofem

psle

avin

gto

esta

blis

hed

firm

s8.

1311

.00

0.18

0.87

0.29

1.00

5.C

umul

ativ

e#

ofem

psle

avin

gto

spin

-out

s0.

771.

660.

090.

380.

630.

471.

00

6.C

umul

ativ

e#

ofem

psle

avin

gto

esta

blis

hed

firm

s(0

-$10

0k)

7.79

10.2

10.

170.

830.

280.

990.

471.

00

7.C

umul

ativ

e#

ofem

psle

avin

gto

esta

blis

hed

firm

s($

100k

-$30

0k)

0.33

1.37

0.18

0.77

0.18

0.60

0.22

0.51

1.00

8.C

umul

ativ

e#

ofem

psle

avin

gto

esta

blis

hed

firm

s($

300k

-$5M

)0.

012

0.13

60.

140.

290.

100.

170.

090.

140.

211.

00

9.C

umul

ativ

e#

ofem

psle

avin

gto

spin

-out

s(0

-$10

0k)

0.70

1.47

0.08

0.36

0.54

0.46

0.98

0.47

0.19

0.07

1.00

10.

Cum

ulat

ive

#of

emps

leav

ing

tosp

in-o

uts

($10

0k-$

300k

)0.

060.

350.

100.

270.

560.

270.

570.

260.

230.

090.

401.

00

11.

Cum

ulat

ive

#of

emps

leav

ing

tosp

in-o

uts

($30

0k-$

5M)

0.00

20.

050

0.09

0.10

0.45

0.08

0.26

0.08

0.05

0.08

0.18

0.20

1.00

12.

Ave

rage

age

38.0

16.

870.

00−0

.09

−0.0

2−0

.13

−0.0

4−0

.13

−0.0

5−0

.01

−0.0

50.

000.

001.

0013

.A

vera

geed

ucat

ion

13.8

51.

380.

130.

030.

040.

020.

040.

020.

030.

030.

030.

030.

020.

331.

0014

.Pe

rcen

tw

hite

0.83

0.25

0.00

−0.0

7−0

.01

−0.0

9−0

.01

−0.0

9−0

.05

−0.0

1−0

.01

0.00

0.00

0.29

0.14

1.00

15.

Perc

ent

mal

e0.

300.

220.

170.

090.

040.

090.

040.

080.

070.

030.

040.

040.

030.

000.

040.

04

Not

e:N

=70

130.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

78 B. A. Campbell et al.

Table 3. Linear probability model on employee mobility

Model 1 Model 2

DV: Mobility(Coefficients and errors ×10−4)

DV: Mobility to Spin-out|Mobility(Coefficients and errors ×10−4)

Age −0.792∗∗∗ (0.179) 0.939 (0.586)Age2 −.000993 (0.00196) −0.00963 (0.00677)Years of Education 0.346∗∗∗ (0.133) 0.658∗∗∗ (0.394)Years of Tenure −10.9∗∗∗ (0.703) 7.97∗∗∗ (2.24)Years of Tenure2 0.582∗∗∗ (0.0557) −0.592∗∗∗ (0.207)Tenure <1 year? 4.28∗∗ (1.7) −0.518 (4.57)Tenure is Censored? −18.3∗∗∗ (1.59) 20.1∗∗ (8.01)Male −8.59∗∗∗ (0.699) 6.61∗∗∗ (2.24)Annual Earnings ($1000s) −0.101∗∗∗ (0.00471) 0.260∗∗∗ (0.026)Annual Earnings2 ($1,000,000s) 0.00095∗∗∗ (0.0009) −0.036∗∗∗ (0.0065)Constant 150∗∗∗ (4.37) 80.4∗∗∗ (13.3)

N Observations 767 307 73 061N Groups 37 758 15 252R2 0.0098 0.0200

Note: Models control for race and include firm-year fixed effects.Robust standard errors are in parentheses.∗∗∗ Significant at the 1% level; ∗∗ Significant at the 5% level.

Table 4. Linear probability model on employee mobility: robustness

Focal subgroup: Model 1 Model 2DV: mobility

(coefficients × 10−4)DV: mobility to spin-out|mobility

(coefficients × 10−4)

Panel 1. Earnings > = $100,000Annual earnings ($1000s) −0.0315∗∗∗ 0.117∗∗∗

Annual earnings2 ($1,000,000s) 0.00295∗∗∗ −0.0165∗∗∗

Panel 2. Years of education > = 16Annual earnings ($1000s) −0.0905∗∗∗ 0.265∗∗∗

Annual earnings2 ($1,000,000s) 0.00809∗∗∗ −0.033∗∗∗

Panel 3. Tenure < = 5 yearsAnnual earnings ($1000s) −0.125∗∗∗ 0.26∗∗∗

Annual earnings2 ($1,000,000s) 0.0115∗∗∗ −0.0707∗∗∗

Panel 4. Within employer wage growth top25% (in t − 1)

Annual earnings ($1000s) −0.0715∗∗∗ 0.222∗∗∗

Annual earnings2 ($1,000,000s) 0.00708∗∗∗ −0.0286∗∗∗

Panel 5. Within employer wage distributiontop 25% (in t − 1)

Annual earnings ($1000s) −0.067∗∗∗ 0.189∗∗∗

Annual earnings2 ($1,000,000s) 0.00624∗∗∗ −0.0265∗∗∗

Panel 6. Age > = 30Annual earnings ($1000s) −0.0999∗∗∗ 0.26∗∗∗

Annual earnings2 ($1,000,000s) 0.00942∗∗∗ −0.0365∗∗∗

N observations 767 307 73 061N groups 37 758 15 252

Note: Models include all controls from Table 3 including firm-year fixed effects.∗∗∗ Significant at the 1% level.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 79

Table 5. Source firm performance and number of mobileemployees

DV: revenue/worker

Payroll per employee int − 1

−0.0015 (0.0018)

Cumulative # ofemployees leaving toestablished firms

−0.0187 (0.0334)

Cumulative # ofemployees leaving tospin-outs

−0.2691∗∗ (0.1056)

Total # employees inquarter 1

−0.0771∗∗∗ (0.0074)

Average age 0.1018∗∗∗ (0.0330)Average education 0.5341∗∗∗ (0.1251)Average tenure −1.6794∗∗∗ (0.1624)Percent white 1.3539 (0.8398)Percent male 4.9576∗∗∗ (0.8239)Constant 50.6183∗∗∗ (2.0519)N Observations 70 130N Groups 18 454R2 0.0004

Note: Model includes firm and year fixed effects.Robust standard errors are in parentheses.∗∗∗ Significant at the 1% level; ∗∗ Significant at the 5% level.

education (Table 4, Panel 2). In both the high earn-ings sample and the high education sample, theprobability of mobility decreases with earnings,while the probability of mobility to a spin-out con-ditional on mobility increases with earnings. Thus,the results provide consistent support for Hypothe-ses 1 and 2 even when limiting the analyses toemployees who are likely to be attorneys.

Table 5 reports the estimates of the relationshipbetween source firm performance and employeemoves to established firms and to spin-outs. Theresults in Table 5 demonstrate that the impact ofexits to spin-outs is significant and negative, andthe impact of exits to established firms is not sig-nificant. The difference in the two coefficients isstrongly statistically significant (at the 0.1% level).These findings support Hypothesis 3. Given thelarge sample size in the estimates, it is surprisingthat some coefficients are not significant; this isstrong evidence that there is not an economicallysignificant relationship between these explanatoryvariables and the dependent variable. Specifically,although employee exit to an established firm isnot associated with a change in source firm per-formance, an exit to a spin-out adversely impactsthe source firm’s revenue per employee by $269,

Table 6. Source firm performance and compensation ofmobile employees

DV: revenue/worker

Cumulative payroll peremployee in t − 1

−0.0012 (0.0018)

Cumulative # ofemployees leaving toestablished firms(0-$100k)

0.0661∗∗∗ (0.0360)

Cumulative # ofemployees leaving toestablished firms($100k-$300k)

0.1334 (0.1873)

Cumulative # ofemployees leaving toestablished firms($300k-$5M)

0.8336 (1.2414)

Cumulative # ofemployees leaving tospin-outs (0-$100k)

0.1984 (0.1283)

Cumulative # ofemployees leaving tospin-outs($100k-$300k)

−2.2708∗∗∗ (0.4889)

Cumulative # ofemployees leaving tospin-outs ($300k-$5M)

−11.7648∗∗∗ (1.4966)

Average age 0.1805∗∗∗ (0.0305)Average education 0.0907 (0.1222)Percent white 0.3364 (0.8401)Percent male 5.0674∗∗∗ (0.8258)Constant 52.6925∗∗∗ (1.9369)

N Observations 70 130N Groups 18 454R2 0.0038

Note: Model includes firm and year fixed effects.Robust standard errors are in parentheses.∗∗∗ Significant at the 1% level.

which translates to a $22,865 loss for an average-sized firm (which is 85 employees).

Table 6 provides results on the relationship bet-ween exiting employee ability and source firmperformance. The coefficients on the number ofemployees exiting in each earnings class measurethe impact of each type of exit on source firmperformance through revenues, after accountingfor the replacement of exited workers. For movesto established ventures, exits of employees earn-ing less than $100,000 actually positively impactsource firm performance and exits of those in thehigher pay classes have no significant impact. Wenote that given the large sample size in the esti-mates, non-significant results provide strong evi-dence that there is not an economically significant

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

80 B. A. Campbell et al.

relationship between these explanatory variablesand the dependent variable. However, the esti-mates for employees moving to spin-outs tell adifferent story. Exits to new ventures of employ-ees who earn less than $100,000 do not have asignificant impact on parent firm performance, butexits of those in higher pay classes have a signif-icant and negative impact that increases with payclass. Further, the coefficient differences betweenemployee entrepreneurship and mobility to estab-lished firms are strongly statistically significant forthe two higher pay classes. Specifically, losing anemployee to a spin-out who is represented in thesecond pay class in Table 6 (average earnings of$147,000) results in a net loss, above and beyondthe loss of the employee’s earnings, of $193,015in revenue in the following year for an average-sized firm relative to a firm without a mobilityevent to a spin-out. The loss is far greater for anemployee exit to spin-out from the highest payclass (average earnings of $481,000): the sourcefirm suffers a net loss in revenue of $1,000,007dollars relative to a similar firm without a mobil-ity event. These results, which suggest that theadverse impact on firm performance of employeeentrepreneurship relative to mobility to establishedfirms increases with the compensation of the exit-ing employee, support Hypothesis 4.

The effects of the control variables are consis-tent throughout the firm performance regressions.The average education of its workforce is pos-itively related to a firm’s performance. Gendercomposition is significantly related to revenue peremployee within firms; those with a greater per-centage of male employees have more revenueper employee. Occupational differences by gen-der within law firms likely drive this result. Racialcomposition is not a significant factor, and averageworkforce age is not consistently significant.

Additional analysis and robustness checks

Our analysis connects micro- and macro-levelanalysis by examining the determinants of mobilityat the individual-level and connecting these indi-vidual decisions with firm-level outcomes. How-ever, alternative micro- and macro-processes mayexplain our findings. To probe our analyses further,we examine whether our results persist after weaccount for involuntary turnover, aggregate qual-ity of mobility events and alternative measures offirm performance.

An assumption in our theoretical section isthat all mobility decisions are voluntary; how-ever, employee mobility may also be involuntary.Notwithstanding that involuntary exits may be gen-erally related to underlying individual characteris-tics for value creation, we examine the robustnessof our results after accounting for three primarysources of involuntary turnover. First, we con-trol for turnover driven by the up-or-out tourna-ment model of promotion (Rebitzer and Taylor,2007). Second, we control for turnover precededby poor performance. Third, we exclude turnoverthat was likely driven by the temporary nature ofinternships.

Results of the coefficients of interest are demon-strated in Table 4. In Panels 3–6, the coefficientscapture the impact of earnings on individuals’mobility decisions for the group of individuals thatis less likely to be moving involuntarily. Becauseinvoluntary exit due to the tournament model typ-ically occurs after six or seven years at a firm, inthe first set of coefficients we focus on employeeswith five or fewer years of tenure at the firm (Panel3).13 Second, to exclude employees who may havelost their jobs due to poor individual performance,we focus on employees whose wage growth is inthe top quartile of similar employees in the prioryear (Panel 4) and we focus on employees whoare in the top quartile of their employer’s earn-ings distribution (Panel 5). Third, we control forthe mobility of interns who are likely to be youngand work for fixed terms, by focusing on employ-ees who are at least 30 years old (Panel 6). In allspecifications, the results are consistent with thebaseline model. Hypotheses 1 and 2 are supportedeven when focusing only on employees who arevery unlikely to face involuntarily mobility.

At the macro level, we extend the analysis toexamine the effect of the aggregate quality ofmovers on firm performance. Table 7 contains esti-mates of the impact of the aggregate quality ofexiting employees (as measured by the cumula-tive pre-mobility earnings of all movers) on firmperformance. Again, the estimates demonstrate anadverse impact on parent firm performance of

13 Turnover driven by the up-or-out system is also unlikelyto occur for workers with more than seven years tenure. Weperform similar analysis focusing only on employees with tenuregreater than seven years, and again obtain results consistentwith Table 3. Given left-censoring and truncation of the tenurevariable at ten years, sample size related disclosure concernsprevent us from reporting the estimates.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

Who Leaves, Where to, and Why Worry? 81

employee moves to spin-outs, but moves to estab-lished firms do not have a significant effect onsource firm performance with the difference incoefficients being strongly statistically significant.

Finally, in unreported regressions, we exam-ine the sensitivity of our results to firm perfor-mance measures other than revenue per employee.Because they are the ultimate decision makersin most law firms, partners may seek to maxi-mize revenue per partner instead of revenue peremployee. Under the assumption that partners arethe highest earners in their firms, we reestimatedthe results for Hypotheses 3 and 4 using revenueper high-earning employee as our dependent vari-able, first defining high-earning employees as indi-viduals earning $100,000 or more, and second asindividuals earning $300,000 or more. Results arerobust to both specifications.

DISCUSSION AND CONCLUSION

We connect micro-level decisions and their macro-level outcomes by examining both the determi-nants of employee mobility and the effects of thatmobility on firm performance. We focus on movesfrom non-dying firms both to established firms and

Table 7. Source firm performance and total payroll ofmobile employees

DV: revenue/worker

Payroll per employee int − 1

−0.0016 (0.0018)

Cumulative payroll ofemployees leaving toestablished firms

0.0002 (0.0006)

Cumulative payroll ofemployees leaving tospin-outs

−0.0062∗∗∗ (0.0012)

Average age 0.0399 (0.0324)Average education 0.4500∗∗∗ (0.1250)Percent white 1.1353 (0.8409)Percent male 4.7760∗∗∗ (0.8250)Constant 49.8202∗∗∗ (2.0383)

N Observations 70 130N Groups 18 454R2 0.0053

Note: Model includes firm and year fixed effects.Robust standard errors are in parentheses.∗∗∗ Significant at the 1% level.

to spin-outs. Differences in the observable qual-ity of exiting employees, in the importance ofappropriating new opportunities and complemen-tary assets, and in the unobservable quality ofexiting employees may differentiate the impactsof these two types of mobility. Understanding therelative impacts of employee exits to establishedfirms and employee entrepreneurship on sourcefirm performance provides insights for the strategicmanagement of human capital based on the valueof human capital in different contexts, the value ofknowledge transfer, and the nature of the creativedestruction process.

At the micro-level, we predict and find supportfor a negative relationship between an employee’sability to generate value (as proxied by earn-ings) and mobility (Hypothesis 1). Further, wetheorize and show that conditional on mobility,the likelihood of spin-out formation relative tomobility to an established firm increases withearnings (Hypothesis 2). At the macro level, wedevelop hypotheses relating the effect of bothquantity (Hypothesis 3) and quality (Hypothesis4) of employees exiting to established firms andspin-outs on source firm performance relative tono employee mobility. We find that employeeentrepreneurship events have a larger negativeeffect on parent firm performance than employeemoves to established firms (Hypothesis 3), andthe difference in the effects of the two types ofmobility events is positively related to the exitingemployees’ ability to generate value (Hypothesis4). Importantly, our findings suggest that the largeradverse impact on source firm performance ofemployee entrepreneurship over mobility to estab-lished firms is driven not only by the observablefactors of exiting employee quantity and qual-ity. The empirical support for Hypothesis 4 sug-gests that the (per person) effect of moves tospin-outs relative to moves to established firmsincreases with observable employee quality. Thatis, if two observably equivalent employees exit afirm, one to an established firm and one to a spin-out, the source firm is more adversely impactedby the spin-out event; and further, the differencein impact on source firm performance increaseswith employee quality. This pattern suggests thatmuch of the adverse effect can be attributed tothe importance of complementary assets, given thattheir transfer or recreation is more likely to occurin spin-outs rather than in established firms.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 65–87 (2012)DOI: 10.1002/smj

82 B. A. Campbell et al.

Theoretically and taken together, these resultspoint to fundamental differences in the causes andconsequences of employee mobility and employeeentrepreneurship: when labor markets among exist-ing firms are unable to correctly assess either thequality of the human capital embodied in employ-ees, or incorporate their nonpecuniary motives,they may choose to venture out on their own.Further, the differential ability to replicate or trans-fer complementary assets when moving to anestablished firm relative to moving to a spin-outalso relates to the market opportunities that arebeing exploited. It may be that general oppor-tunities (e.g., better career development, highercompensation) trigger moves to established firms,but specific opportunities (e.g., ability to transferclient accounts or capitalize on underutilized tech-nologies or enter new markets) trigger employeeentrepreneurship. The results also highlight thatsuch entrepreneurial decisions are more likelyto unleash the Schumpeterian forces of creativedestruction (Schumpeter, 1934). Since higher per-forming employees seem to have more entre-preneurial abilities and aspirations, their loss andthe concomitant loss of complementary assets andspecific opportunities have a greater detrimentaleffect on source firm performance.

Finally, it is important to note that in our empir-ical context, high earnings correlate strongly withage and gender. In particular, most partners in lawfirms are older males. While law schools haverecently made great strides toward gender balancein their student bodies, these trends in the popula-tion of law students are not yet represented at thehighest levels of law firms. In the current empiricalcontext, the most senior lawyers are drawn froma pool of lawyers who entered the field during aperiod of substantial gender imbalance. However,in our empirical analysis we control for differ-ences attributable to age and gender of mobileemployees, so the effect that is measured is themobility effect after controlling for the older maleeffect. One additional correlation is that partnersare more likely to stay with their firms, but if theydo leave, they are more likely to go to spin-outs. Inlight of the theoretical construct we develop, thisresult is not surprising. Partners are more likely tohave a bargaining advantage, since the importanceof complementary assets to their ability to createvalue is low, and they are more able to recreatethese complementary assets should they move.

Limitations and future research