where to next for residential security - parks associates · where to next for residential security...

TRANSCRIPT

A Parks Associates WhitepaperA Parks Associates WhitepaperA Parks Associates Whitepaper

Where to Next for Residential SecurityWhere to Next for Residential SecurityWhere to Next for Residential Security

When viewed from a topline perspective, 2014 reports on the adoption of security systems in the

home seem little changed from the previous two years.

In 1Q 2012, 25% of U.S. broadband households reported having any security system in use; in 2013 and 2014, that

percentage increased to 26%. Given the margin of error, the presence of any active security system in U.S. broadband

households remains roughly the same over those years. However, each year, both the number of U.S. households and

the percentage with broadband increase, so there is a bit of a double-count increase.

Status of Residential Security in U.S. Broadband Households

Where to Next for Residential Security

O F 118.9 million O F 120.6 million U . S . H O U S E H O L D S

had adopted broadband.U . S . H O U S E H O L D S

had adopted broadband.

I N 2012 I N 2014

75% 78%

T H E N E T R E S U LT O F T H E S E S MA L L B U T I M P O R TA N T A D D I T I O N S I S T H AT E V E N AT T H E S AM E P E R C E N TAG E R E P O R T E D, G R O W T H E X I S TS .

I N 2014, that number has increased by

~1.6 million T O 31.3 million T O TA L H O U S E H O L D S

with an active security system.

I N 2012 , approximately

29.7 million U . S . H O U S E H O L D S

had an active security system.

3

Wh

ere to N

ext for Resid

ential Secu

rity

201420132012

© Parks Associates

Electronic Security Systems in U.S. Broadband Households 2012-2014

Professional Monitoring, Self-Monitoring, & Local Alarm Only

$0

10%

20%

Professionally Monitored Security

System

Self-Monitored Fee-based

Security System

Local Alarm-Only Security System

Security Systems in use in U.S. Broadband Households:2012 25%2013 26%2014 26%

FIGURE 1 MONITORING SERVICES IN U.S.

Figure 1 provides Parks Associates’ findings of services in security households from

surveys completed in the 1Q of 2012, 2013, and 2014. Even with limited increases,

there is a trend line for increased adoption of professional monitoring by households

with security systems, as well as a corollary decline, at least by percentage of

households, for fee-based self-monitored security systems.

Those fee-based self-monitored systems are created by adding security system-

level sensors (motion, window, door, etc.) to home controllers or, in a few cases,

a continuing presence in a home of a security system sold with the intent of self-

monitoring. Local alarm-only systems are in households that either never contracted

for professional monitoring services or cancelled service when their contract ended

but continue to use the system for its local alarm and chime value.

Security: Patterns of Acquisition & Attrition

Acquisition of Home Security SystemU.S. Broadband Households with Security System

© Parks Associates

Already had had one but I replaced it with a new system

Did not have one but purchased one within 6 months of moving in

Did not have one but purchased one more than 6 months after I moved in

Already had one and I have not upgraded it since moving in

Already had one but I upgraded components of it

Traditionally, consumers have adopted security at the time of a move.

Timing of Security System Acquisition • 75% acquired their current system at the time of a move

• 25% report that the system was already in the home when they moved in and they have not upgraded or replaced it yet

• 50% acquired a security system or upgraded or replaced their security system within six months of their move

• Only 27% of households report acquiring a system that wasn’t there at the time of the move after living in the home for more than six months

As long as these patterns hold, the security industry is limiting its own market potential.

Several providers, including AT&T Digital Life, ADT, and Comcast, aim at changing this pattern. They are expanding their

sales campaigns to home dwellers who haven’t recently moved and do not yet have a security system, but significant

results are not yet visible. The pattern of security system adoption varies only a few points from Parks Associates’ surveys

completed five or more years ago.

The challenge to lower attrition also remains. In its most recent report, ADT finds that attrition remains at 14%. That is

one piece of unwelcome news among some of the company’s good news: sales are up and so is the attachment rate for

Pulse additions, which raise both the average up-front price of a system and its RMR.

FIGURE 2 TIMING OF SECURITY SYSTEM ACQUISITION

While the introduction of smart devices as value additions to traditional security systems

are transforming the industry, some classic characteristics of the security industry persist—

and beg for change.

Lower attrition rates—that is, rates of 8% or better—are critical to the entire industry.

The task of meeting and beating sales results of past

years is hard, but having to replace cancelled contracts

at near or above 10% as well as gain new subscribers

is daunting.

Parks Associates believes that attrition will decline but

that it will decline as people adopt, become accustomed

to, and learn to value the extra functions available with

smart home devices and “connectedness” to their secu-

rity systems. A year or so more is probably necessary to

begin seeing measurably lower attrition rates.

5

Wh

ere to N

ext for Resid

ential Secu

rity

Emerging smart home and Internet of Things (IoT)

trends represent powerful changes in benefits for all

product types in the home, regardless of specific category.

Current products are first or second generation; they will

become smarter, more open, and more beneficial over

time. Just remember: 10 years ago, there were no iPhone

or Android smartphones, and laptops were well above

$2,000. Five years ago, tablets didn’t exist. Technology

advances reduce cost and improve products and systems.

The “cloud” allows some software functions to remain outside of the home.

It creates easier upgrade potential to products and systems than has been previously available.

Smart Home and IoT Trends Benefit the Security Industry

While some patterns for the industry have not changed and require the industry’s

constant attention for advances, there are real and meaningful changes that bode

well for the industry.

The security industry is at the heart of this transfor-

mation. Its actions and activities over the next few

years can cement its position for the smart home, and

that is what the traditional players along with new par-

ticipants (broadband providers) intend to accomplish.

Perhaps the most important shift in the market is that dealers are selling to a changed consumer public.

A

ll rig

hts

rese

rved

| w

ww

.par

ksas

soci

ates

.com

| ©

Par

ks A

ssoc

iate

s

6

All of these products create familiarity with the concept of con-

nectedness, making the educational and marketing tasks for secu-

rity and smart home device providers easier than would have been

true even five years ago. Security dealers in turn are adding the ca-

pability to access, control, and receive alerts from their security sys-

tems at a quick pace; anytime access is valuable, even when it isn’t

used on a daily basis.

SEVENTY-SIX PERCENT of broadband households have at least one smartphone (the average is 1.57). With ownership of a smartphone comes familiarity with apps and the expectation of access to just about everything when desired.

IP CAMERAS are diffusing into households: 17% of U.S. broadband households report the presence of network security cameras in 2014.

While not all households yet stream video—

MORE THAN 60% do from one or more devices.

CONNECTED GAMING consoles are the leading devices at this time, but smart TVs and streaming media players are joining them.

Figure 3 provides the percentage of households with at least one

of the specified CE products as of 1Q 2014. Highlighted are products

particularly important to smart security and the smart home.

FIGURE 3 1Q 2014 OWNERSHIP OF AT LEAST ONE OF SPECIFIED CE PRODUCTS

Consumer Electronics OwnershipU.S. Broadband Households

Smart watch

Google Chromecast

Motion controller

e-book reader

Blu-ray player

MP3 player

Headphones

Tablet

Gaming console

Earbuds

Desktop computer

Flat panel TV

Home network router

Laptop, notebook,or netbook

0% 30% 60% 90%

© Parks Associates

Streaming media player

7

Wh

ere to N

ext for Resid

ential Secu

rity

THIS YEAR, MORE SURVEY RESPONDENTS ARE from small

dealerships than in 2013; one-third report revenues for 2013 at $500K or

below, compared with only 14% in 2012. This is not bad news; it points

to more dealers finding the marketplace recovering enough to resume

business or enter the business.

65% OF RESPONDING DEALERS REPORT REVENUES for 2013 as

higher than those for 2012, and 66% reported higher revenues for 2012

than for 2011. These are signs of a recovering, but not yet fully recovered,

industry. Eighty percent expect that 2014 revenues will exceed those of

2013.

68% OF SECURITY DEALERS EXPECT SALES for remote control and

monitoring equipment to be higher in 2014 than 2013, while only 3%

expect them to be lower.

SECURITY DEALERS REPORT that about one-quarter of their installs

are in new starts, while 44% are in existing homes acquiring security for

the first time.

INTERESTINGLY, ONE CLEAR DIFFERENCE among respondents in

2014 vs. 2013 is the percentage offering professional monitoring. In 2013,

83% reported offering professional monitoring services while only 61%

report this for 2014. This finding is one more indicator that more small

dealers responded to the SSI/Parks Associates survey in 2014 vs. 2013.

SMALL DEALERS ARE, OF COURSE, MORE LIKELY to use third-party

monitoring providers and less likely to use broadband as a primary com-

munications path for alerts than large dealers or broadband providers

themselves. However, the use of broadband as a communications path

will inevitably increase. It will offer lower cost to the industry over time.

DEALERS REPORT, on average, that 50% of their installations include

the ability for consumers to access and control their systems through a

smartphone, tablet, or computer. There are big swings when viewing per-

centages by tier: 40% percent of dealers report that 70% or more of their

installations include this capability, while 25% report that less than 10%

of their customers receive this.

THE TOP SMART DEVICES DESIRED by dealers include smart door

locks (77%), IP cameras (70%), and smart smoke detectors (60%). Since

these smart devices are close adjacencies to the primary mission of

security systems—safety and well-being—this early attachment is logical.

However, security dealers must expand their categories of desired and

offered smart devices over the next two years to compete effectively.

Security Sales and Integration

(SSI) and Parks Associates

complete a security dealer

survey each spring in order to

assess activities and changes

within the marketplace.

Security dealers do not like

answering surveys; as a result,

there is always a good deal of

margin of error within responses.

That reality notwithstanding, these

survey results provide a good

sense of how dealers are doing

and any changes in activities.

Security Dealer Activity

A

ll rig

hts

rese

rved

| w

ww

.par

ksas

soci

ates

.com

| ©

Par

ks A

ssoc

iate

s

8

Advanced Features O�ered, Beyond Intrusion Alerts, with Security SystemsU.S. Security Dealers

Two-way voice veri�cation frommonitoring station

Ability to set up scripts such as'All Away' across categories

Outdoor or all lights on by control orautomatic in case of alert

Wireless control of door locks fromwithin the house

Energy management

Speci�c access to status of some lightsor their control via the Internet

Connected access control

Pet neutralizing sensor

Panic buttons for sirens

IP network security camera

Chimes when the doors orwindows open

Ability to receive alerts and checkhome status remotely

Ability to check the status of system when away from home

Ability to arm from a remotekey chain (key fob)

0% 50% 100%

© Parks Associates

2014

2013

Figure 4 compares services offered by dealers in 2013 and 2014.

There is a significant increase in most features enabling connectivity.

Given that many small dealers responded to this survey, the real increase

is even more dramatic than it may first appear. The large providers,

new or traditional, all offer full connectivity or “smart home” feature

sets. Smaller dealers are usually somewhat later adopters. Now the

challenge for small and large dealers alike is to learn how to sell

the benefits of these features efficiently and effectively.

FIGURE 4 OFFERINGS BEYOND INTRUSION ALERTS

9

Wh

ere to N

ext for Resid

ential Secu

rity

The second reason, more revenue potential, is also critical.

As security dealers learn through interaction with their

would-be and current customers why they want these

capabilities, they will have ever greater selling confidence,

and more revenues will arrive.

Top Reasons to O�er Remote Monitoring & Control Capabilities (2013 vs. 2014)

U.S. Security Dealers That Currently O�er or Intend to O�er Security Systems with Self-Monitoring & Control Services

0% 50%25% 75% 100%

% Ranked Among Top 3 Reasons

2014

2013

© Parks Associates

Manufacturers are o�ering us better margins on IP security system

equipment

We see our competitors doing this and must keep up

New entrants are entering our territory; we want to be sure we

compete well

The extra services from additional capabilities can provide extra

revenue

Our customers are learning about this and asking us if our company

o�ers these features

We are a dealer for a manufacturer o�ering IP security systems and are

preparing for training

Our housing market is weak; IP security systems give us extra

bene�ts for existing housing

Even better news for the security industry overall is WHY more dealers are adopting remote monitoring and control capabilities.

CUSTOMERS ARE ASKING FOR THESE CAPABILITIES.

That means the giant providers’ marketing messages are resonating and creating awareness—which is good news for all.

FIGURE 5 TOP REASONS TO OFFER REMOTE MONITORING AND CONTROL CAPABILITIES

A

ll rig

hts

rese

rved

| w

ww

.par

ksas

soci

ates

.com

| ©

Par

ks A

ssoc

iate

s

10

Respondent numbers are small because, even with 10,000 broadband households surveyed by Parks Associates,

the number of households that acquired a security system in the previous 12 months is a low percentage of all

households. Nonetheless, the message is clear, and as 2014 unrolls, the number of households with these systems

will increase.

More smart devices and systems are hitting the market from manufacturers and channels that are not security

dealers or professional monitoring providers. Revolv, now at Amazon and soon to be elsewhere, is new. Staples has

Staples CONNECT. Sears has announced a set of “connected home” stores. Lowe’s sells IRIS. Single smart devices

are also gaining attention with devices ranging from Philips’ Hue to Chamberlain’s smart garage remotes to Sonos’

streaming music system.

Momentum is growing; consumers are learning. The front cover of Consumer Reports for June 14

features Smart Home; the June Angie’s List pamphlet does the same.

F I G U R E 6 O F F E R S

P R O O F O F T H I S

S T R AT E G Y.

Forward Momentum & Potential

Types of Security Features Behind Up-Front CostsU.S. Broadband Households that Purchased Security System

in the Last 12 Months and have Speci�ed Service

© Parks Associates

$0

$400

$200

$600

$800

Aver

age

up-fr

ont c

osts

($)

Professional monitoring and PERS

Professional monitoring, interactive services and smart home controls

Professional monitoring only

Professional monitoring and interactive services

Professional monitoring, interactive services and networked camera

FIGURE 6 TYPES OF SECURITY FEATURES BEHIND UP-FRONT SECURITY SYSTEMS COSTS

Selling remote monitoring and smart home services with a security system brings higher up-front revenues.

It also provides an average of $14 more RMR.

11

Wh

ere to N

ext for Resid

ential Secu

rity

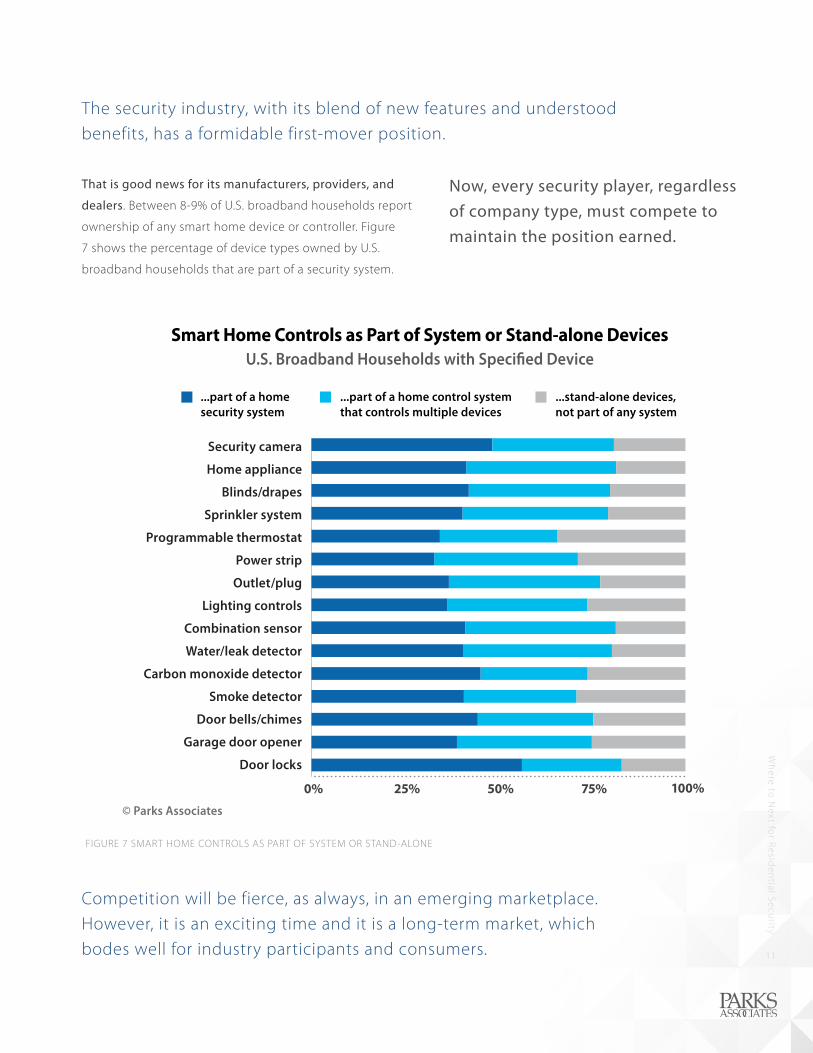

That is good news for its manufacturers, providers, and

dealers. Between 8-9% of U.S. broadband households report

ownership of any smart home device or controller. Figure

7 shows the percentage of device types owned by U.S.

broadband households that are part of a security system.

Smart Home Controls as Part of System or Stand-alone DevicesU.S. Broadband Households with Speci�ed Device

Carbon monoxide detector

Smoke detector

Door bells/chimes

Door locks

Garage door opener

Water/leak detector

Combination sensor

Lighting controls

Outlet/plug

Power strip

Programmable thermostat

Sprinkler system

Blinds/drapes

Home appliance

Security camera

0% 50%25% 75% 100%

© Parks Associates

...part of a home control system that controls multiple devices

...stand-alone devices, not part of any system

...part of a home security system

The security industry, with its blend of new features and understood benefits, has a formidable first-mover position.

Now, every security player, regardless of company type, must compete to maintain the position earned.

Competition will be fierce, as always, in an emerging marketplace. However, it is an exciting time and it is a long-term market, which bodes well for industry participants and consumers.

FIGURE 7 SMART HOME CONTROLS AS PART OF SYSTEM OR STAND-ALONE

About The Author

Tricia Parks, Chairman, Founder, and CEO, Parks Associates

Tricia Parks is the founder, chairman, and CEO of Parks Associates, a market analyst and research company dedicated to providing meaningful information and counsel to companies offering technology-based products aimed at improving people’s lives.

She presents worldwide on consumer trends, market requirements, and industry structure, with

an eye to meshing visionary and progressive ideas to consumer needs and wants.

Parks Associates hosts CONNECTIONS™, an international conference and showcase for the

digital home hosted in the U.S., and CONNECTIONS™ Europe, hosted in Europe and focusing

on market opportunities for digital products and services in the many nations of Europe. Tricia

Parks also developed the Relevancy Theory, a forecasting model for sales across a broad range

of digital electronic products and services.

Tricia has served on a variety of industry boards including CEA’s Home Networking and Informa-

tion Technology division, the National Research Council’s Committee for a Partnership to Assess

Technology for Housing (PATH), the AMD Board of Global Consumer Advocacy, and CABA. Tricia

Parks has a BA from Sweet Briar College and graduate studies from the University of Texas.

About Parks Associates

Parks Associates is an internationally recognized market research and consulting company specializing in emerging consumer technology products and services.

Founded in 1986, Parks Associates creates research capital for companies ranging from Fortune

500 to small start-ups through market reports, primary studies, consumer research, custom

research, workshops, executive conferences, and annual service subscriptions.

The company’s expertise includes new media, digital entertainment and gaming, home net-

works, Internet and television services, digital health, mobile applications and services, con-

sumer electronics, energy management, and home control systems and security.

For more information, visit www.parksassociates.com or contact us at 972.490.1113

ATTRIBUTION—Authored by Tricia Parks. Published by Parks Associates. © Parks Associates, Dallas, Texas 75248.

All rights reserved. No part of this book may be reproduced, in any form or by any means, without permission in

writing from the publisher. Printed in theUnited States of America.

DISCLAIMER—Parks Associates has made every reasonable effort to ensure that all information in this report is

correct. We assume no responsibility for any inadvertent errors.

Research & Analysis Research & Analysis Research & Analysis Research & Analysis Research & Analysis

Discover Parks Associates Today.

Back your venture with accurate consumer data and strategic analysis.

INTERNATIONAL RESEARCH FIRM

for Digital Living Technologiesfor Digital Living Technologies

www.ParksAssociates.comwww.ParksAssociates.com

Access and Entertainment Services

Advertising

Connected CE and Platforms

Connected Home Systems and Services

Digital Gaming

Digital Health

Digital Home Support Services

Digital Living Overview

Digital Media

Home Energy Management

Internet of Things

Mobile and Portable

App Ecosystem

Smart Home

SMB Market

European and Worldwide Consumer Research

ParksAssociates

Research & Analysis