what is value-at-risk, and is it appropriate for property/liability insurers? neil d. pearson...

TRANSCRIPT

What is Value-at-Risk, and Is It Appropriate for Property/Liability

Insurers?Neil D. Pearson

Associate Professor of Finance

University of Illinois at Urbana-Champaign

12-13 April 1999

What is Value-at-Risk?

0

5

10

15

20

25

P/L

< -

130

-11

0 <

P/L

<-9

0

-70

< P

/L <

-50

-30

< P

/L <

-10

10

< P

/L <

30

50

< P

/L <

70

90

< P

/L <

110

P/L

> 1

30

Hypothetical Daily Mark-to-Market Profit/Loss on Forward Contract (in $thousands)

Fre

quen

cy

value at risk(using x=5%)

If You Like the Normal Distribution

0.0

-150,000 -75,000 0 75,000 150,000

Mark-to-Market Portfolio Profit/Loss

Freq

uenc

y

5% 1.65 std. dev.

Value at risk: $86,625

What is Value-at-Risk?• Notation:

V change in portfolio value

f(V) density of V

x specified probability, e.g. 0.05

• Value-at-risk (VaR) satisfies

orx f V d V

( )

VaR

VaR

1

x f V d V( )

What is Value-at-Risk?

• Value-at-risk (for a probability of x percent) is the x percent critical value

• If you like the normal distribution, it is proportional to the portfolio standard deviation

What is Value-at-Risk?

• Value-at-risk is something you already understand• Value-at-risk is a particular way of summarizing

the probability distribution of changes in portfolio value

• The language of Value-at-Risk eases communication

If Value-at-Risk Isn’t New, Why Is It So Fashionable?

• It provides some information about a firm’s risks• It is a simple, aggregate measure of risk• It is easy to understand• “Value” and “risk” are business words

Basic Value-at-Risk Methodologies

• 3 methodologies:– Historical simulation

– Variance-covariance/Delta-Normal/Analytic

– Monte Carlo simulation

• Illustrate these using a forward contract– current date is 20 May 1996

– in 91 days (19 August)• receive 10 million

• pay $15 million

First step: Identify market factors

USD mark - to - market value =GBP million

1 +

USD million

1 +GBP USD

Sr r

10

91 360

15

91 360( / ) ( / )

Market factors: S, rGBP, and rUSD

PositionCurrent $ Value ofPosition

Cash Flow onDelivery Date

Long position in 91 day denominatedzero coupon bond with face value of 10million

S+r ( / )

GBP million

GBP

10

1 91360

Receive 10million

Short position in 91 day $ denominatedzero coupon bond with face value of $15million

USD 15 million

USD1 91360+r ( / )

Pay $15 million

Historical Simulation

• Start with current situation:– date: 20 May 1996– portfolio: 1 forward contract

– market factors: S=1.54, rGBP=6.06%, and rUSD=5.47%

• Obtain values of market factors over last N days• Use changes in market factors to:

– simulate values of market factors on 21 May– compute mark-to-market values of forward contract on 21

May– compute hypothetical profit/loss

Historical simulation: P/LTable 1: Calculation of Hypothetical 5/21/96 Mark-to-Market Profit/Loss on aForward Contract Using Market Factors from 5/20/96 and Changes in Market Factorsfrom the First Business Day of 1996

Market FactorsMark-to-Market Value

$ Interest Rate(% per year)

Interest Rate(% per year)

ExchangeRate($/ )

of ForwardContract($)

Start with actual values ofmarket factors and forwardcontract as of close of businesson 5/20/96:

(1) Actual values on 5/20/96 5.469 6.063 1.536 327,771

Compute actual past changesin market factors:

(2) Actual values on 12/29/95 5.688 6.500 1.553

(3) Actual values on 1/2/96 5.688 6.563 1.557

(4) Percentage change from12/29/95 to 1/2/96

0.000 0.962 0.243

Use these to computehypothetical future values ofthe market factors and themark-to-market value of theforward contract:

(5) Actual values on 5/20/96 5.469 6.063 1.536 327,771

(6) Hypothetical future valuescalculated using rates from5/20/96 and percentage changesfrom 12/29/95 to 1/2/96

5.469 6.121 1.539 362,713

(7) Hypothetical mark-to-marketprofit/loss on forward contract

34,942

Repeat N timesTable 2: Historical Simulation of 100 Hypothetical Daily Mark-to-Market Profits andLosses on a Forward Contract

Market FactorsHypothetical

Mark-to-MarketChange in Mark-

to-Market

Number

$ Interest Rate(% per year)

InterestRate

(% per year)ExchangeRate($/ )

Value ofForward

Contract ($)

Value of ForwardContract ($)

1 5.469 6.121 1.539 362,713 34,942

2 5.379 6.063 1.531 278,216 -49,555

3 5.469 6.005 1.529 270,141 -57,630

4 5.469 6.063 1.542 392,571 64,800

5 5.469 6.063 1.534 312,796 -14,975

6 5.469 6.063 1.532 294,836 -32,935

7 5.469 6.063 1.534 309,795 -17,976

8 5.469 6.063 1.534 311,056 -16,715

9 5.469 6.063 1.541 379,357 51,586

10 5.438 6.063 1.533 297,755 -30,016.

.

.

91 5.469 6.063 1.541 378,442 50,671

92 5.469 6.063 1.545 425,982 98,211

93 5.469 6.063 1.535 327,439 -332

94 5.500 6.063 1.536 331,727 3,956

95 5.469 6.063 1.528 249,295 -78,476

96 5.438 6.063 1.536 332,140 4,369

97 5.438 6.063 1.534 310,766 -17,005

98 5.469 6.125 1.536 325,914 -1,857

99 5.469 6.001 1.536 338,368 10,597

100 5.469 6.063 1.557 539,821 212,050

SortTable 3: Historical Simulation of 100 Hypothetical Daily Mark-to-Market Profits andLosses on a Forward Contract, Ordered From Largest Profit to Largest Loss

Market FactorsHypothetical

Mark-to-MarketChange in Mark-

to-Market

Number

$ Interest Rate(% per year)

Interest Rate(% per year) Exchange

Rate($/ )

Value of ForwardContract ($)

Value of ForwardContract ($)

1 5.469 6.063 1.557 539,821 212,050

2 5.469 6.063 1.551 480,897 153,126

3 5.469 6.063 1.546 434,228 106,457

4 5.469 6.063 1.545 425,982 98,211

5 5.532 6.063 1.544 413,263 85,492

6 5.532 6.126 1.543 398,996 71,225

7 5.469 6.063 1.542 396,685 68,914

8 5.469 6.063 1.542 392,978 65,207

9 5.469 6.063 1.542 392,571 64,800

10 5.469 6.063 1.541 385,563 57,792...

91 5.469 6.005 1.529 270,141 -57,630

92 5.500 6.063 1.529 269,264 -58,507

93 5.531 6.063 1.529 267,692 -60,079

94 5.469 6.004 1.528 255,632 -72,139

95 5.469 6.063 1.528 249,295 -78,476

96 5.469 6.063 1.526 230,541 -97,230

97 5.438 6.063 1.526 230,319 -97,452

98 5.438 6.063 1.523 203,798 -123,973

99 5.438 6.063 1.522 196,208 -131,563

100 5.407 6.063 1.521 184,564 -143,207

Variance-covariance method

value at risk standard deviation of

change in portfolio value

165.

0.0

-150,000 -75,000 0 75,000 150,000

Mark-to-Market Portfolio Profit/Loss

Freq

uenc

y

5% 1.65 std. dev.

Value at risk: $86,625

Portfolio standard deviation

• Portfolio standard deviation

• Portfolio variance

Xi = dollar investment in i-th instrument

i = standard deviation of returns of i-th instrument

ij = correlation coefficient

portfolio portfolio 2

21

21

22

22

23

23

21 2 12 1 2

1 3 13 1 3 2 3 23 2 3

2

2 2

portfolio

X X X X X

X X X X

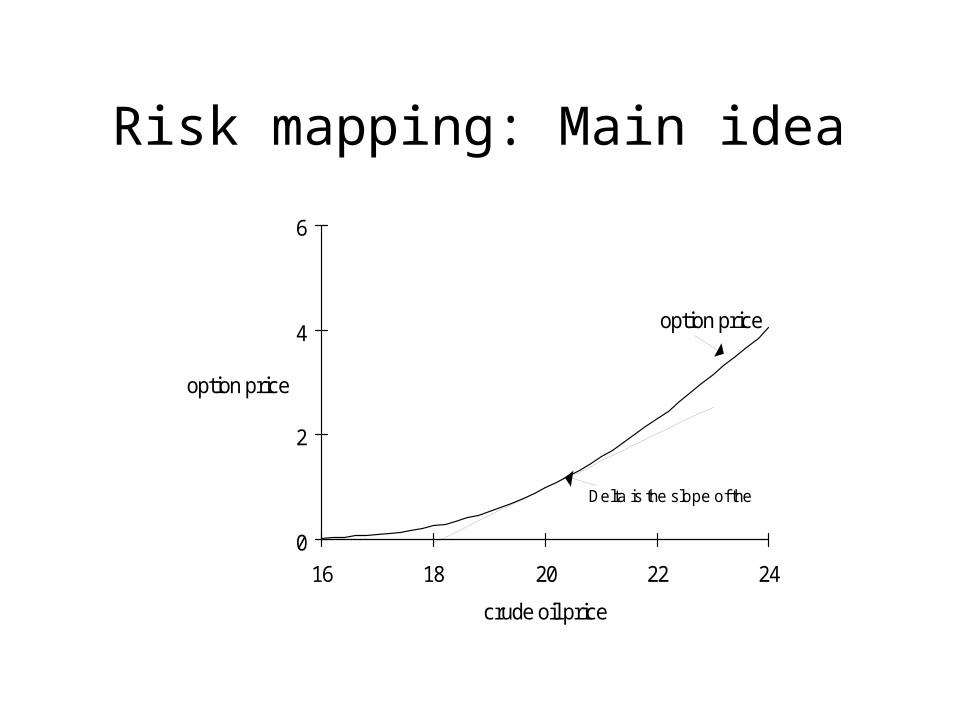

Risk mapping: Main idea

0

2

4

6

16 18 20 22 24

crude oil price

option price

option price

Delta is the slope of thetangent, approximately .5

Risk mapping: Main idea

• The option price change resulting from a change in the oil price is:

• In this sense the option “acts like” barrels of oil• The option is “mapped” to barrels of oil

option price change change in oil price

Risk mapping: Interpret forward as portfolio of standardized positions

• Change in m-t-m value of forward:

• Find a portfolio of simpler (“standardized”) instruments that has same risk as the forward contract

• “Same risk” means same factor sensitivities

etc.

VV

rr

V

rr

V

SSF

F F F

USD

USDGBP

GBP

Vr

F

USD

,

Risk mapping: Interpret forward as portfolio of standardized positions

• Let V = X1 + X2 + X3 denote value of portfolio of standardized instruments– each standardized instrument depends on only 1 factor

• Change in V is

• Choose X1, X2, X3 so that:

VX

rr

X

rr

X

SS

1 2 3

USDUSD

GBPGBP

X

r

V

rF1

USD USD

,

X

r

V

rF2

GBP GBP

and ,

X

S

V

SF3

Choice of X1, X2, X3

• Recall that the m-t-m value of the forward is

• This implies

VF

Sr r

GBP million

1 +

USD million

1 +GBP USD

10

91 360

15

91 360( / ) ( / )

Xr

Xr

X S

1

2

3

15

1 91 360

15355 10

1 91 360

10

1 06063 91 360

USD million

USD / GBP GBP million

USD / GBPGBP million

USD

GBP

( / ),

( . )

( / ),

( ). ( / )

.

Compute variance of portfolio of standardized instruments

• Variance of portfolio of standardized instruments:

where

and USD is the standard deviation of % changes in the $ interest rate.

21

21

22

22

23

23

21 2 12 1 2

1 3 13 1 3 2 3 23 2 3

2

2 2

portfolio

X X X X X

X X X X

11

1

Xr

rXUSD

USDUSD

Compute value-at-risk

• Portfolio standard deviation

• Value-at-risk

portfolio portfolio 2

Value - at - risk = portfoliok

Variance-covariance method

value at risk standard deviation of

change in portfolio value

165.

0.0

-150,000 -75,000 0 75,000 150,000

Mark-to-Market Portfolio Profit/Loss

Freq

uenc

y

5% 1.65 std. dev.

Value at risk: $86,625

Monte Carlo simulation

• Like historical simulation• Use psuedo-random changes in the factors rather

than actual past changes• Psuedo-random changes in the factors are drawn

from an assumed multivariate distribution

What Is VaR, Again

• One need not focus on change in portfolio value over the next day, month, or quarter

• Instead, one could estimate the distribution of:– cash flow

– net income

– surplus

– or almost anything else one cares about

• VaR (broadly defined) DFA

Is VaR Appropriate for Property/Liability Insurers?

• Do property/liability insurers have investment portfolios?

• Do they care about the possible future values of things like:– Cash flow?

– Net income?

– Surplus?

What is Value-at-Risk?

0

5

10

15

20

25

P/L

< -

130

-11

0 <

P/L

<-9

0

-70

< P

/L <

-50

-30

< P

/L <

-10

10

< P

/L <

30

50

< P

/L <

70

90

< P

/L <

110

P/L

> 1

30

Hypothetical Daily Mark-to-Market Profit/Loss on Forward Contract (in $thousands)

Fre

quen

cy

value at risk(using x=5%)

Limitations of VaR

• VaR DFA– it is a particular, limited summary of the distribution

• VaR is an estimate of the x percent critical value– based on various assumptions

– sampling variation

• VaR doesn’t indicate what circumstances will lead to the loss– 2 portfolios with opposite interest rate exposure could

have same VaR