what is driving recent increases in prices paid s zehle coleago 16 june 15

TRANSCRIPT

What is driving prices for spectrum at auction, and what effect could this be having on network investment?

Stefan Zehle, CEO, Coleago [email protected] www.coleago.com

The 10th Annual European Spectrum Management ConferenceBrussels, 16 June 2015

Agenda

What is the evidence that spectrum prices are increasing?

What factors drive prices paid for spectrum at auction?

What effect does this have network investment?

© copyright Coleago 2015What is driving prices for spectrum at auctions

1

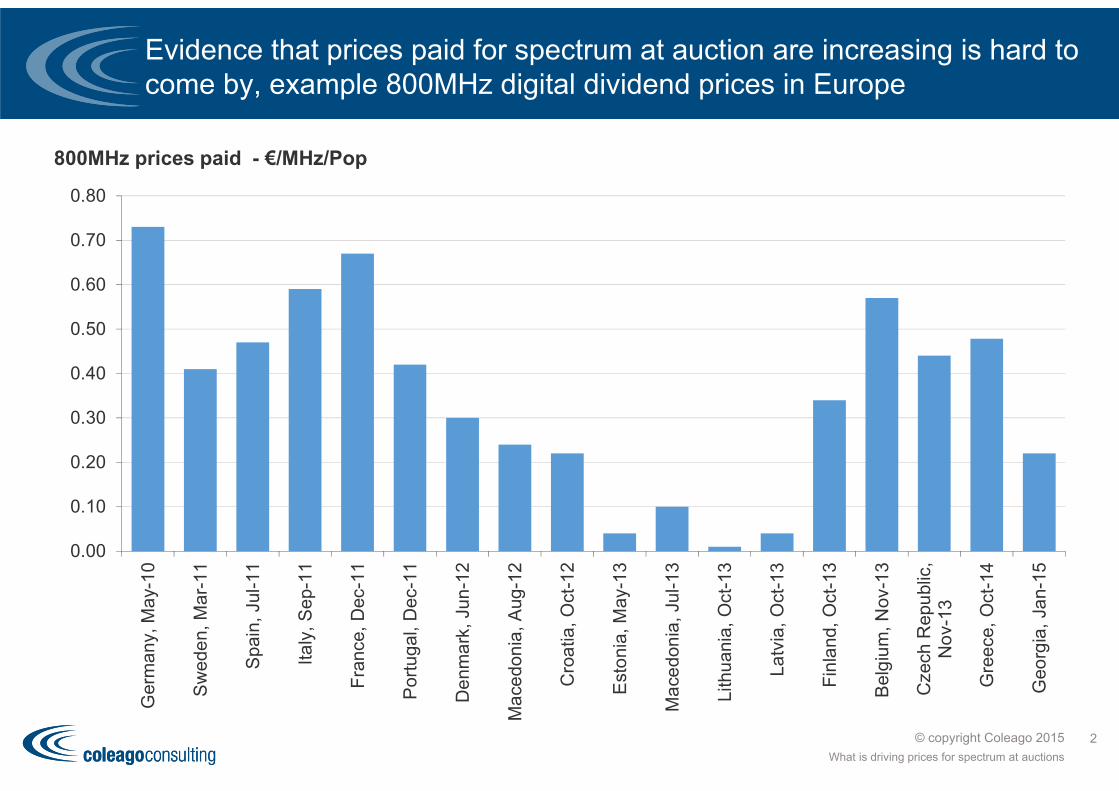

Evidence that prices paid for spectrum at auction are increasing is hard to come by, example 800MHz digital dividend prices in Europe

© copyright Coleago 2015What is driving prices for spectrum at auctions

2

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Ger

man

y, M

ay-1

0

Swed

en, M

ar-1

1

Spai

n, J

ul-1

1

Italy

, Sep

-11

Fran

ce, D

ec-1

1

Portu

gal,

Dec

-11

Den

mar

k, J

un-1

2

Mac

edon

ia, A

ug-1

2

Cro

atia

, Oct

-12

Esto

nia,

May

-13

Mac

edon

ia, J

ul-1

3

Lith

uani

a, O

ct-1

3

Latv

ia, O

ct-1

3

Finl

and,

Oct

-13

Belg

ium

, Nov

-13

Cze

ch R

epub

lic,

Nov

-13

Gre

ece,

Oct

-14

Geo

rgia

, Jan

-15

800MHz prices paid - €/MHz/Pop

But prices paid in the recent US and Canadian AWS-3 auctions are worrying

Conventional wisdom states that spectrum below 1GHz is more valuable than above 1GHz

Prices paid in Canada (2.45 $/MHz/pop) and the US (2.71 $/MHz/pop) for spectrum that is only useful from 2017 are worrying.

© copyright Coleago 2015What is driving prices for spectrum at auctions

3

0.00 0.50 1.00 1.50 2.00 2.50 3.00

Canada AWS-3 (2GHz) 2015

US AWS-3 (2GHz) 2015

Canada AWS-1 (2GHz) Feb 2008

US AWS-1 (2GHz) Feb 2007

EU 800MHz average 2010-15

US$/MHz/Pop

Prices Paid

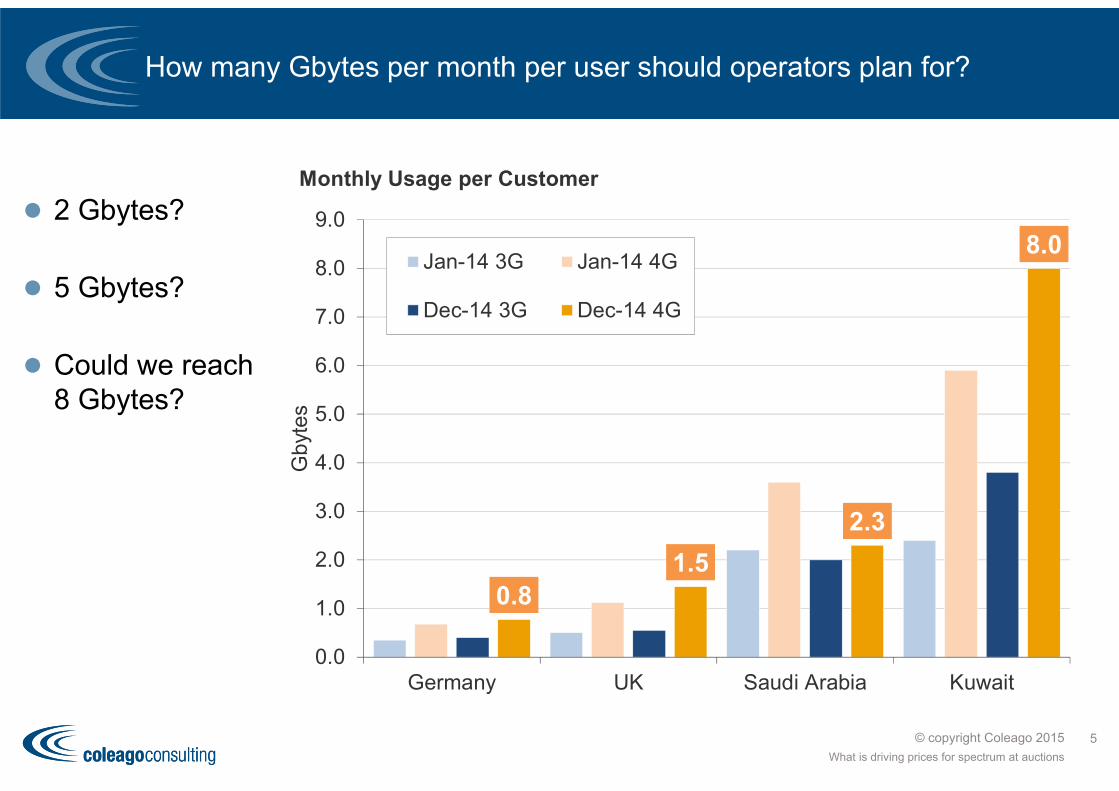

The data Tsunami: 4G users consume more data than 3G users and existing 4G customers increase their usage, month after month

© copyright Coleago 2015What is driving prices for spectrum at auctions

4

3.2 3.3

2.4

1.3

0.8

1.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Japan South Korea US Canada Germany UK

Gby

tes

Monthly Usage per Customer

Jan-14 3G Jan-14 4G

Dec-14 3G Dec-14 4G

How many Gbytes per month per user should operators plan for?

2 Gbytes?

5 Gbytes?

Could we reach 8 Gbytes?

© copyright Coleago 2015What is driving prices for spectrum at auctions

5

0.81.5

2.3

8.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Germany UK Saudi Arabia Kuwait

Gby

tes

Monthly Usage per Customer

Jan-14 3G Jan-14 4G

Dec-14 3G Dec-14 4G

How many Gbytes per month per user should operators plan for?

How about 1 Gbyte per user per day?

What if TV Anywhere Apps really take hold?

© copyright Coleago 2015What is driving prices for spectrum at auctions

6

How many hours does the average American watch TV per day?

– Answer: 2.8 hours

How much data volume does this represent per month, assuming HDTV?

– Answer: 0.7 Terabyte (700 Gigabytes)

If just 4-5% of viewing is via LTE, that’s 1 Gbyte / user / day

How many Gbytes per month per user should operators plan for?

Samsung Galaxy S6 Quad HD screen, i.e. twice normal HD 4K will be next

© copyright Coleago 2015What is driving prices for spectrum at auctions

7

YouTube 4K (Ultra HD) video content is

available now

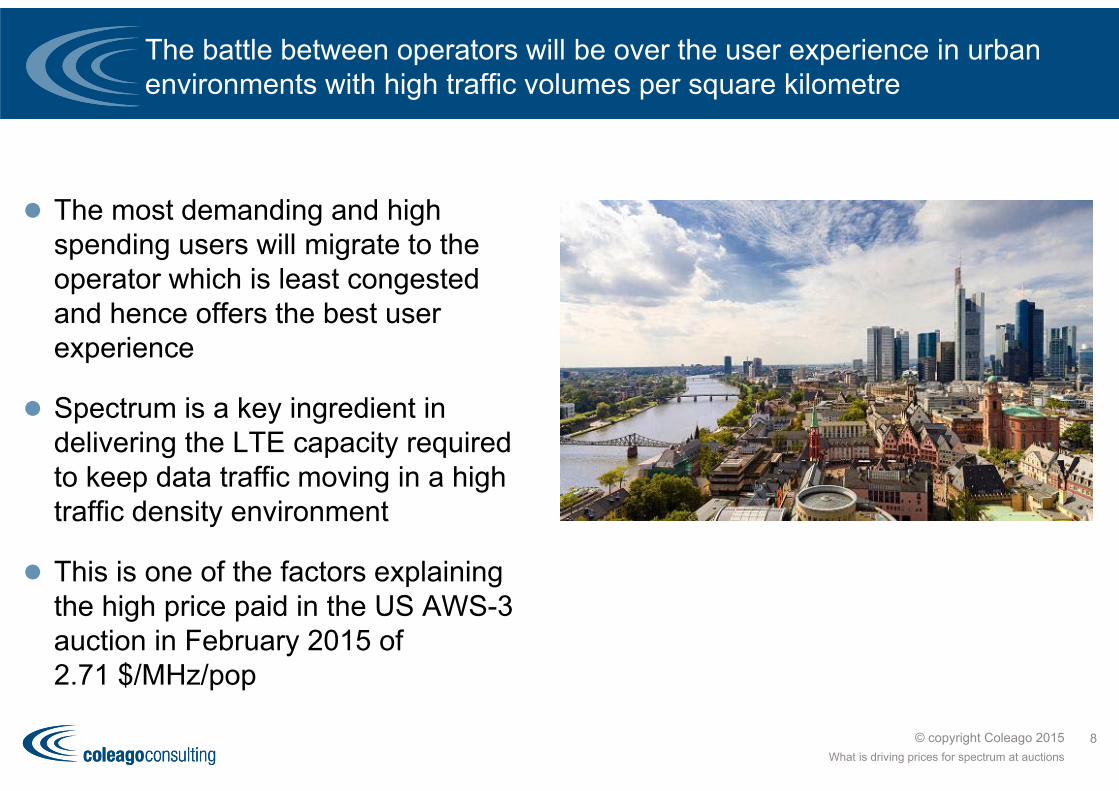

The battle between operators will be over the user experience in urban environments with high traffic volumes per square kilometre

The most demanding and high spending users will migrate to the operator which is least congested and hence offers the best user experience

Spectrum is a key ingredient in delivering the LTE capacity required to keep data traffic moving in a high traffic density environment

This is one of the factors explaining the high price paid in the US AWS-3 auction in February 2015 of 2.71 $/MHz/pop

© copyright Coleago 2015What is driving prices for spectrum at auctions

8

In many markets ever higher reserve prices determine prices paid by operators

© copyright Coleago 2015What is driving prices for spectrum at auctions

9

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Gre

ece

Belg

ium

Den

mar

k

Fran

ce

Portu

gal

Italy

Spai

n

Swed

en

Ger

man

y

€/M

Hz/

pop

800MHz reserve prices and prices paid - €/MHz/PopPaid Reserve

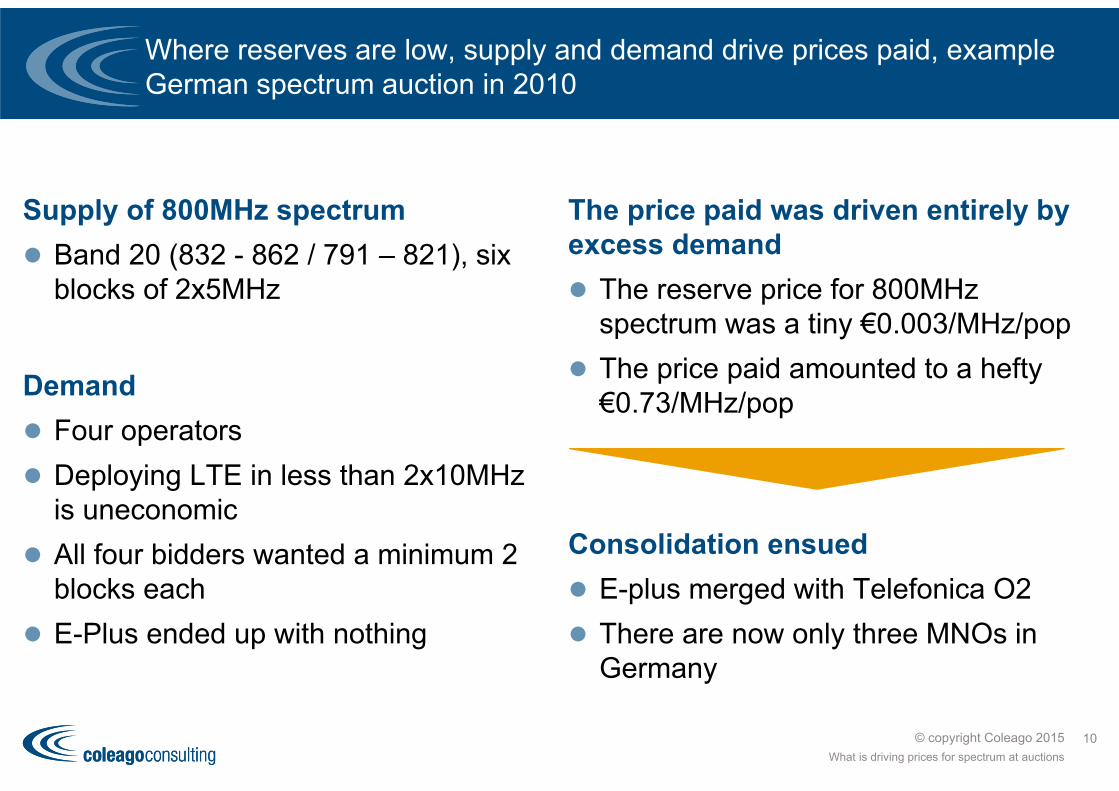

Where reserves are low, supply and demand drive prices paid, example German spectrum auction in 2010

Supply of 800MHz spectrum Band 20 (832 - 862 / 791 – 821), six

blocks of 2x5MHz

Demand Four operators Deploying LTE in less than 2x10MHz

is uneconomic All four bidders wanted a minimum 2

blocks each E-Plus ended up with nothing

The price paid was driven entirely by excess demand The reserve price for 800MHz

spectrum was a tiny €0.003/MHz/pop The price paid amounted to a hefty

€0.73/MHz/pop

Consolidation ensued E-plus merged with Telefonica O2 There are now only three MNOs in

Germany

© copyright Coleago 2015What is driving prices for spectrum at auctions

10

As consolidation sets it, spectrum auctions will be less competitive and hence the reserve price may matter more, German auction, June 2015

Policy objectives in German SMRA spectrum auction, May 2015 Deliver wide area mobile broadband

coverage Provide incumbent operators with

planning certainty Maintain network based competition

Conditions for 700MHz DD2 spectrum Relatively low reserve at

0.09€/MHz/pop Coverage obligation of 98% of

population

Supply of spectrum 6 blocks of DD2 700MHz spectrum 7 blocks of 900MHz renewal 10 blocks of 1800MHz renewal 8 blocks of 1500MHz TDD

Demand for spectrum from three bidders Deutsche Telekom Vodafone Telefonica (O2)

© copyright Coleago 2015What is driving prices for spectrum at auctions

11

German SMRA auction, June 2015 – multiple factors explain bidding behaviour

© copyright Coleago 2015What is driving prices for spectrum at auctions

12

0

50

100

150

200

250

1 9 17 25 33 41 49 57 65 73 81 89 97 105113121129137

€M

illion

Round #

Germany spectrum auction average per block prices

700MHz 900MHz1800MHz 1500MHz

As of round 143

The German multi-band SMRA produced surprising results, such as higher prices for 1800MHz compared to 900MHz and 700MHz spectrum

© copyright Coleago 2015What is driving prices for spectrum at auctions

13

Result 700MHz sold at reserve Others bands sold above

reserve Factor that impacted on price

paid are:– Reserve price– coverage rules – economics of LTE deployment– renewal or new spectrum, – existing holdings – the SMRA auction format– bidder behaviour

as of round 143

0.00

0.05

0.10

0.15

0.20

0.25

0.30

700M

Hz

900M

Hz

1800

MH

z

1500

MH

z

€/M

Hz/

pop

German auction June '15, reserve and prices paid - €/MHz/pop

Paid Reserve

What is your policy objective?

700MHz auction in Chile in 2014 The 700MHz spectrum award process focussed on connectivity and competition policy objectives … cover 1,281 rural towns and 500

schools obligation to build fibre mandated MVNO access and roaming

… rather than extracting money from the mobile industry. Auction proceeds amounted to a

relatively small 0.017 $/MHz/pop

© copyright Coleago 2015What is driving prices for spectrum at auctions

14

© copyright Coleago 2015What is driving prices for spectrum at auctions

15

Is there a linkage between high spectrum prices and investment in mobile broadband?

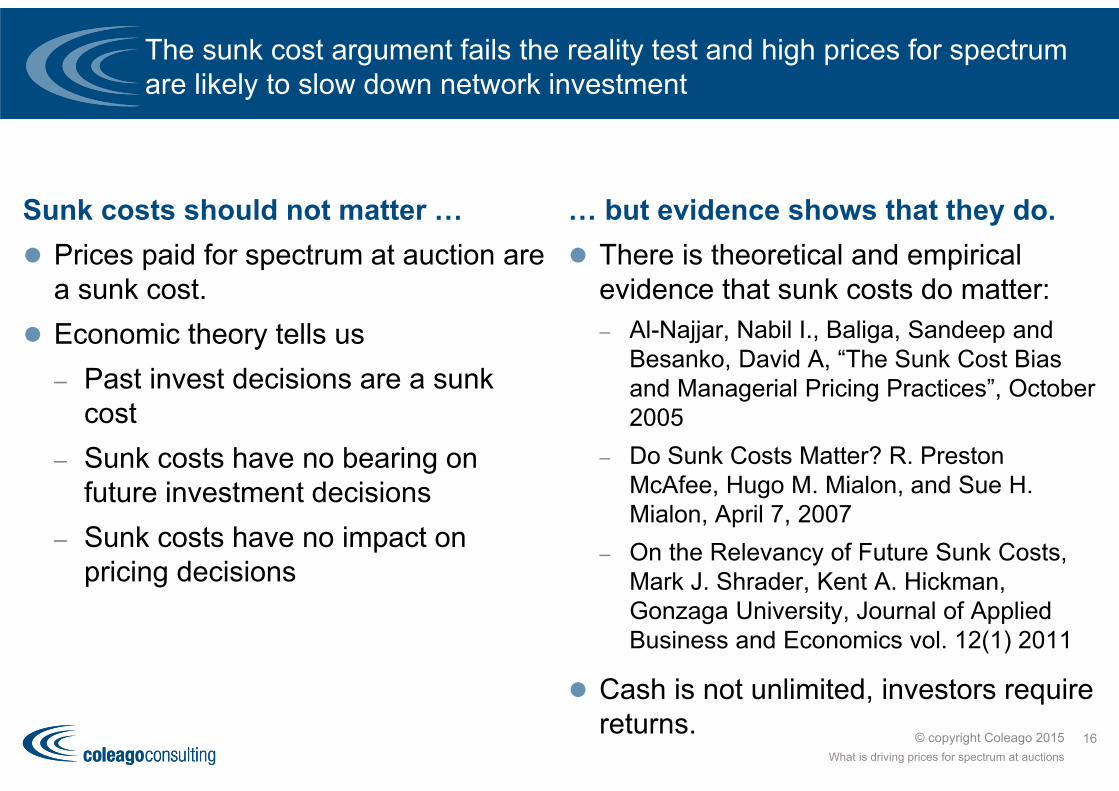

The sunk cost argument fails the reality test and high prices for spectrum are likely to slow down network investment

Sunk costs should not matter … Prices paid for spectrum at auction are

a sunk cost. Economic theory tells us

– Past invest decisions are a sunk cost

– Sunk costs have no bearing on future investment decisions

– Sunk costs have no impact on pricing decisions

… but evidence shows that they do. There is theoretical and empirical

evidence that sunk costs do matter: – Al-Najjar, Nabil I., Baliga, Sandeep and

Besanko, David A, “The Sunk Cost Bias and Managerial Pricing Practices”, October 2005

– Do Sunk Costs Matter? R. Preston McAfee, Hugo M. Mialon, and Sue H. Mialon, April 7, 2007

– On the Relevancy of Future Sunk Costs, Mark J. Shrader, Kent A. Hickman, Gonzaga University, Journal of Applied Business and Economics vol. 12(1) 2011

Cash is not unlimited, investors require returns. © copyright Coleago 2015

What is driving prices for spectrum at auctions16

High spectrum prices are likely to reduce to flow of capital to the industry

Other economists have focused on the impact that excessive auction fees might have on the cost of capital.

The higher the cost of capital, the lower the business case for investment, e.g. in marginal (rural) coverage

This relies on empirical observations that capital markets are not 100% efficient, and that investors may have budget constraints which limit investment.

These budget constraints may be worsened by excessively high auction fees. – For example, after the 3G auctions

many of Europe’s largest mobile operators became heavily indebted, share prices fell and their ability to raise funds for future investment was undoubtedly restricted.

© copyright Coleago 2015What is driving prices for spectrum at auctions

17

In the light of future spectrum requirements current spectrum price levels are not sustainable

The amount of spectrum per user is increasing.

Revenues are flat, so the cost of spectrum – capex and opex – as a proportion of revenues increases.

With the several 100’s of MHz required for LTE and 5G current prices for spectrum are not sustainable.

In future, the cost of spectrum in terms of €/MHz/pop needs to decline.

© copyright Coleago 2015What is driving prices for spectrum at auctions

18

Revenue

Qua

ntity

of s

pect

rum

Spec

trum

cap

ex a

nd

opex

A specialist Telecoms Management Consulting Firm

About Coleago Consulting

© copyright Coleago 2015What is driving prices for spectrum at auctions

19

Since 2001, Coleago has offered a wide range of advisory services to the telecom industry

© copyright Coleago 2015What is driving prices for spectrum at auctions

20

Strategy & Business Planning Strategy Development, Marketing Strategy MVNO and Multi-Brand Wholesale Strategy Business Planning and Business Modelling

Telecoms Regulation & Interconnect Accounting Separation, Regulatory Price

Control Interconnect Cost Modelling, RIO Regulatory Consultations

Business Transformation & Cost Reduction Cost Reduction Mobile Network Sharing Restructuring and Turnaround

Transaction Services Commercial Due Diligence Tower Due Diligence Preparation of Information Memorandum

Spectrum Valuations and Auctions Running Auctions for Regulators Spectrum Strategy and Valuation for Auctions Spectrum Auction Bid Strategy and Execution Beauty Contest Bid Books

Mobile Network Sharing Mobile Network Sharing Managed Services and Outsourcing Tower Due Diligence Network Audit

Coleago has delivered over 70 spectrum related projects across a wide variety of markets

© copyright Coleago 2015What is driving prices for spectrum at auctions

21

Markets in which Coleago has conducted spectrum related projects

Coleago has carried out over 70 spectrum consultation, valuation, auction and beauty contest licence projects

Completed in 2015 Argentina - 900/1800 and 700/AWS Canada - AWS-3 and 2.5GHz

Completed in 2013-14 Canada – 700MHz Paraguay - multi-band Oman - 800MHz & 2.6GHz Belgium - 800MHz New Zealand - 700MHz Myanmar - greenfield Australia - 700MHz & 2.6GHz UK - 800MHz & 2.6GHz Sri-Lanka - 1800MHz

Completed in 2012 Belgium - 2.6GHz Netherlands - multi-band New Zealand -1800MHz spectrum

trading Switzerland - multi-band Russia - 700MHz & 2.6GHz Pakistan - 2.1GHz valuation Bangladesh - 2.1GHz valuation

© copyright Coleago 2015What is driving prices for spectrum at auctions

22

Further information: www.coleago.com

Contact

Stefan Zehle, MBA

Tel: +44 7974 356 [email protected]

CEO, Coleago Consulting Ltd

© copyright Coleago 2015What is driving prices for spectrum at auctions

23