what is a multilateral development bank? s. samuel tumiwa deputy representative north america...

TRANSCRIPT

What is a Multilateral Development Bank?

S. Samuel TumiwaDeputy Representative

North America Representative Office

Canada Business Opportunities SeminarHalifax – Montreal – Calgary – Saskatoon

September 20151

Multilateral Development Banks

2

Multilateral Development Banks

3

The Asian Development Bank

4

How We are Different• Infrastructure – 85% of investments are in energy,

water, transport, urban• Regional Cooperation – Central Asia, Greater Mekong

Subregion, South Asia, etc.• Specific Focus on the Pacific Islands

Our Challenge• Rapidly Changing Region – By 2030, all of the region will

be middle income, except for AFG, NEP, and • Not just about financing – Also about knowledge and

Partnership

Why Asia?

S. Samuel TumiwaDeputy Representative

North America Representative Office

Canada Business Opportunities SeminarHalifax – Montreal – Calgary – Saskatoon

September 2015

5

Why Asia?

6

Economic Outlook: DevelopingAsia extends steady growth…

7

f: forecast

2010 2011 2012 2013 2014 2015f 2016f0

2

4

6

8

10

9.37.3 6.2 6.5 6.3 6.3 6.3

GDP growth (%)

5-year average: 7.110-year average: 7.6

Asian Development Outlook 2015

…contributing the most to global growth

PRC India ASEAN US Japan Euro area0

10203040 31.2

11.8 7.9 9.61.8 1.6

Global cumulative GDP growth, 2009–2014 = 21.4%, annual growth=4.0%

8

Þ Asia accounts for about 60% of global growth; still fastest-growing region

PRC India ASEAN US Japan Euro area0

20

40 31.9

15.28.0

14.4

1.4 3.7

Global GDP growth, 2015 = 3.6%

Percentage contributions to global GDP growth

Asian Development Outlook 2015

High overall growth, but divergence across countries

East Asia South Asia Southeast Asia

Central Asia

The Pacific0

2

4

6

8

10

12 2014 2015f 2016f5-year ave. 10-year ave.

9

f: forecast Asian Development Outlook 2015

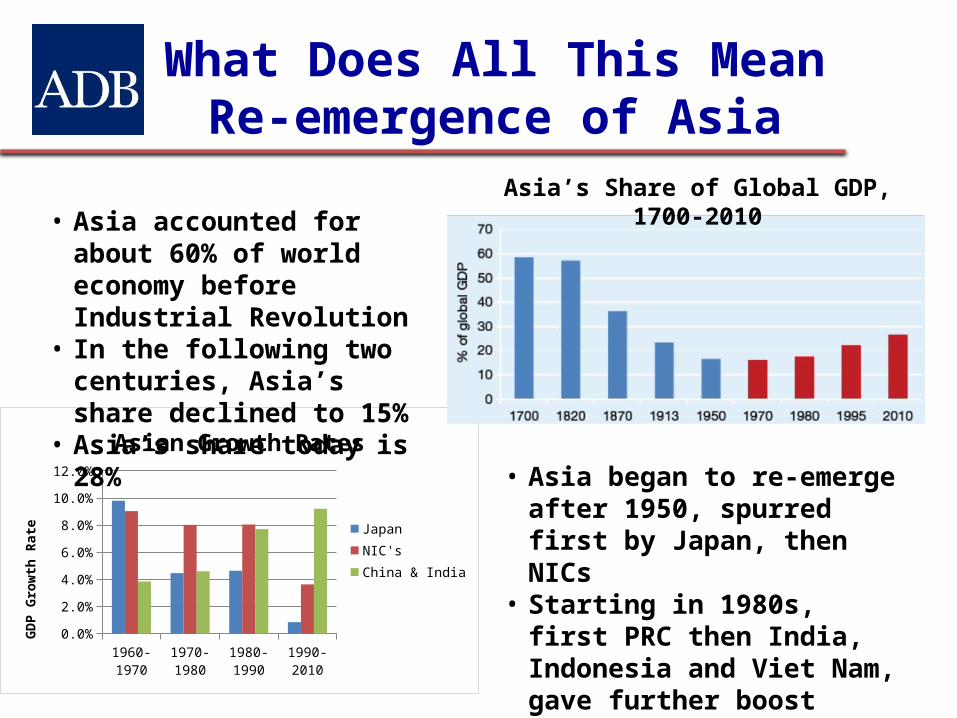

What Does All This MeanRe-emergence of Asia

1960-1970 1970-1980 1980-1990 1990-20100.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Asian Growth Rates

JapanNIC'sChina & India

GDP

Grow

th R

ate

• Asia began to re-emerge after 1950, spurred first by Japan, then NICs

• Starting in 1980s, first PRC then India, Indonesia and Viet Nam, gave further boost

• Asia accounted for about 60% of world economy before Industrial Revolution

• In the following two centuries, Asia’s share declined to 15%

• Asia’s share today is 28%

Asia’s Share of Global GDP, 1700-2010

The Asian Century

Asia; 52%

North America; 13%

Latin America & Caribbean; 10%

Europe, 18%

Sub Saharan Africa, 2%

Middle East & North Africa, 3%

Rest of World, 2%

Asian Century Scenario

Asia; 31%

North Amer-ica; 21%

Latin America & Car-ibbean, 9%

Europe, 28%

Sub Saharan Africa, 4%

Middle East & North Africa, 5%

Rest of World, 2%

Middle Income Trap Scenario

Asian GDP: $65 trillionAsian GDP per capita: $20,600

Asian GDP: $174 trillionAsian GDP per capita: $40,800

Asian century driven by Asia 7: India, Indonesia, Japan, Malaysia, PRC, Republic of Korea, and Thailand - projected to account for 90% of

Asia’s growth between 2010 and 2050

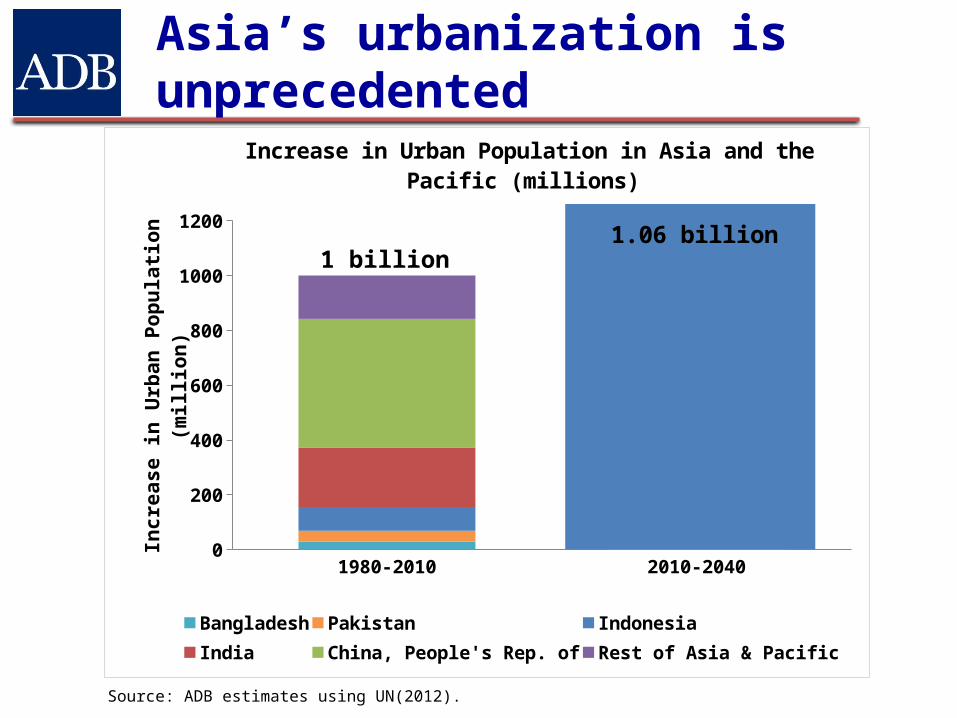

1980-2010 2010-20400

200

400

600

800

1000

1200

Increase in Urban Population in Asia and the Pacific (millions)

Bangladesh Pakistan Indonesia India China, People's Rep. ofRest of Asia & Pacific

Incr

ease

in U

rban

Pop

ulati

on (m

illio

n) 1.06 billion1 billion

Asia’s urbanization is unprecedented

Source: ADB estimates using UN(2012).

China, People's Rep. of

Bhutan

Lao PDR

Indonesia

Viet Nam

Asia and the Pacific

Europe

North America

Latin America and Car-ibbean

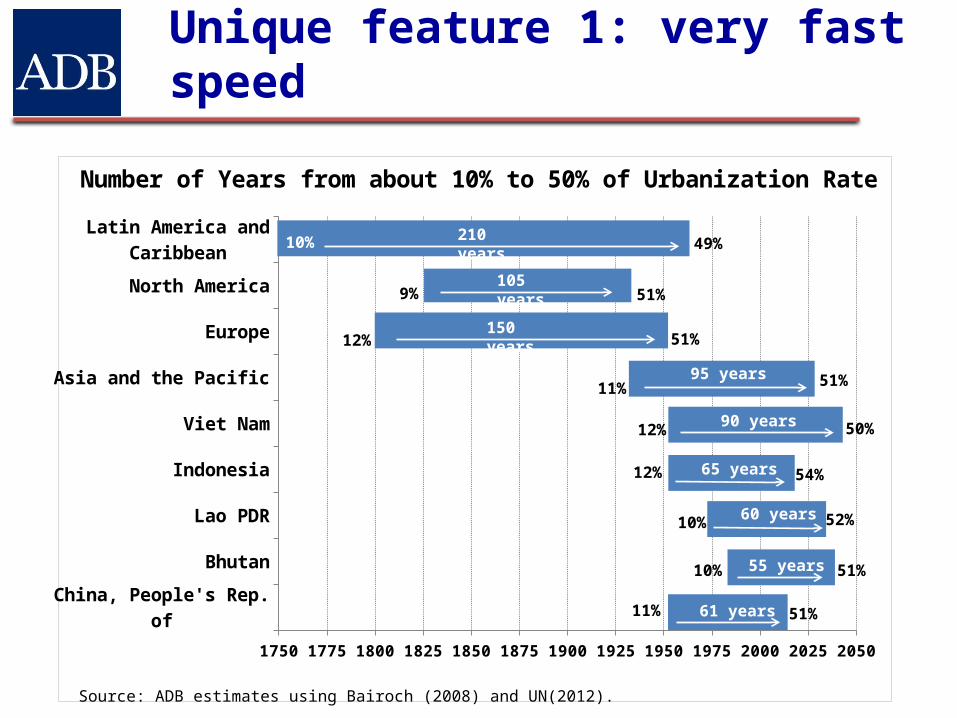

1750 1775 1800 1825 1850 1875 1900 1925 1950 1975 2000 2025 2050

Number of Years from about 10% to 50% of Urbanization Rate

10% 49%210 years

9% 51%105 years

12% 51%150 years

11% 51%95 years

12% 50%90 years

12% 54%65 years

10% 52%60 years

10% 51%55 years

11% 51%61 years

Unique feature 1: very fast speed

Source: ADB estimates using Bairoch (2008) and UN(2012).

Unique feature 2: highest densities in the world…

Mumbai

Kolkata

KarachiLa

gos

Shenzhen

Seoul/Inch

eon

Taipei,China

Chennai

Bogota

ShanghaiLim

a

BeijingDelhi

Kinshasa

Manila

Tehran

Jakarta

Tianjin

Bangalore

Ho Chi Minh City

Cairo

Baghdad

Shenyang

Hyderabad

São Paulo0

5000

10000

15000

20000

25000

30000

35000

Top 25 World's Cities Ranked by Density, 2007

Den

sity

(per

son/

m2)

Asia & the Pacific (17/25)AfricaEurope Latin America & CaribbeanMiddle East & North Africa

Source: www.citymayors.com

Unique feature 3: many megacities

Megacities, 2010

ASIA: 12/23

Note: The circles indicate population sizes ranging from (10 million) to (39 million). The circles do not reflect the physical extents of the cities and any overlap between them merely reflects their relative population sizes and not any official acceptance or endorsement of any geographical sovereignty.

Source: UN (2012).

Unique feature 4: low starting base

19501955

19601965

19701975

19801985

19901995

20002005

20102015

20202025

20302035

20402045

20500

10

20

30

40

50

60

70

80

90

100Level of Urbanization by Region (%)

Leve

l of U

rban

izati

on (%

)

52%

43%

67%

63%

Northern America

Europe

Latin Americ

a & Caribbean

WORLD

ASIA & PACIFIC

Africa

Source: ADB estimates using Bairoch (2008) and UN(2012).

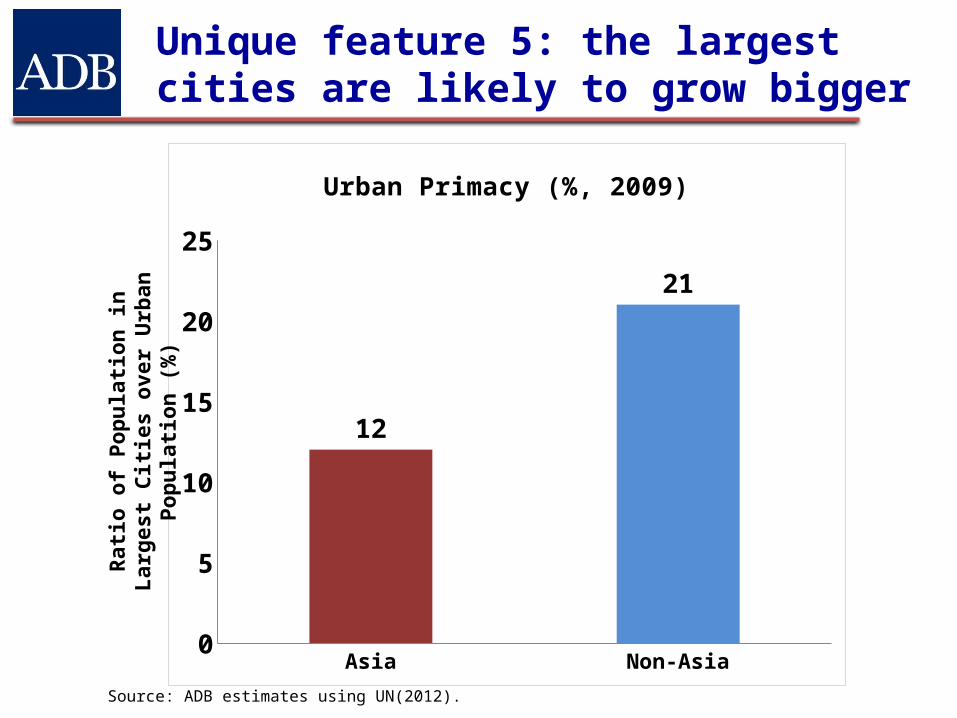

Asia Non-Asia0

5

10

15

20

25

12

21

Urban Primacy (%, 2009)

Rat

io o

f P

op

ula

tio

n in

Lar

ges

t C

itie

s o

ver

Urb

an P

op

ula

tio

n (

%)

Unique feature 5: the largest cities are likely to grow bigger

Source: ADB estimates using UN(2012).

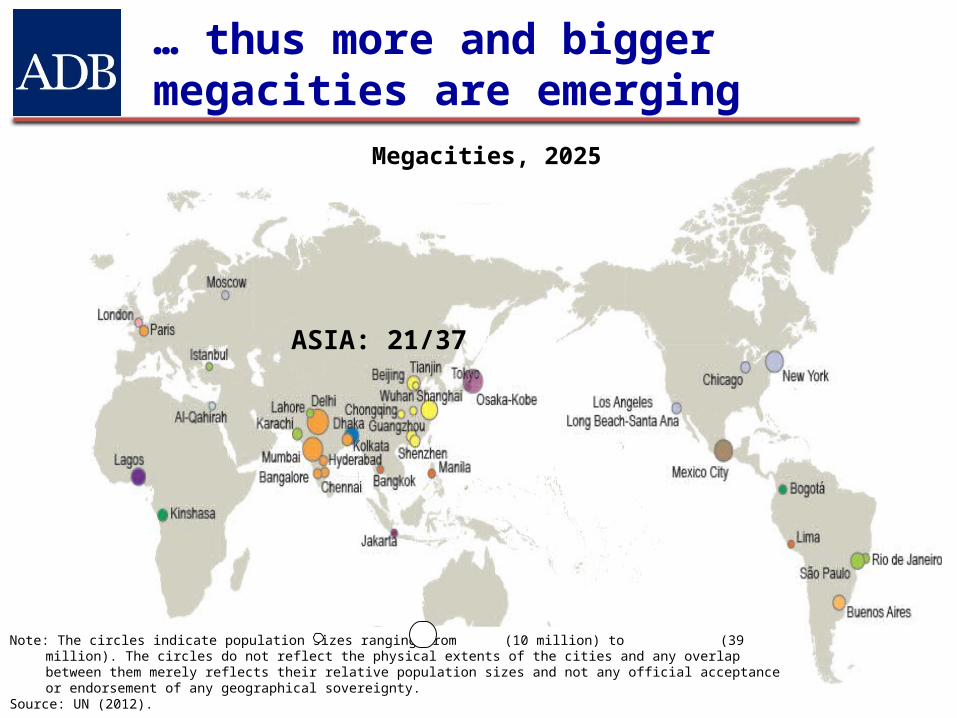

… thus more and bigger megacities are emerging

Megacities, 2025

ASIA: 21/37

Note: The circles indicate population sizes ranging from (10 million) to (39 million). The circles do not reflect the physical extents of the cities and any overlap between them merely reflects their relative population sizes and not any official acceptance or endorsement of any geographical sovereignty.

Source: UN (2012).

Asia’s financing requirements are huge

19

Source: ADB, 2009. Infrastructure for a Seamless Asia. Manila

Total of $8.3 trillion (2010–2020) or $750 billion/year

Source: Various reports compiled by ADB

In Asia the infrastructure gap means

People without Access to:

Water and Sanitation 900 million people

Electricity 800 million people

Roads 1.2 billion people

Internet 80% of Asia

20

Deep DiveSustainable Infrastructure

S. Samuel TumiwaDeputy Representative

North America Representative Office

Canada Business Opportunities SeminarHalifax – Montreal – Calgary – Saskatoon

September 2015 21

Asia’s Urban Challenge

• Globally, 6.2 billion people in urban areas and 53% in Asia by 2050

(World Urban Prospects, 2011 Revision)

• By 2050, 64.4% of population of Asia is in urban areas

• 23 megacities, 13 of which are in Asia

• Approximately 75% of GDP today comes from the urban areas- urban areas of engines of growth in Asia

• 44 million people are added to city populations in Asia every yearo equivalent to 120,000 people each day who require construction of

more than 20,000 new dwellings, 250 km of new roads and additional infrastructure to supply more than 6000 liters of potable water

23

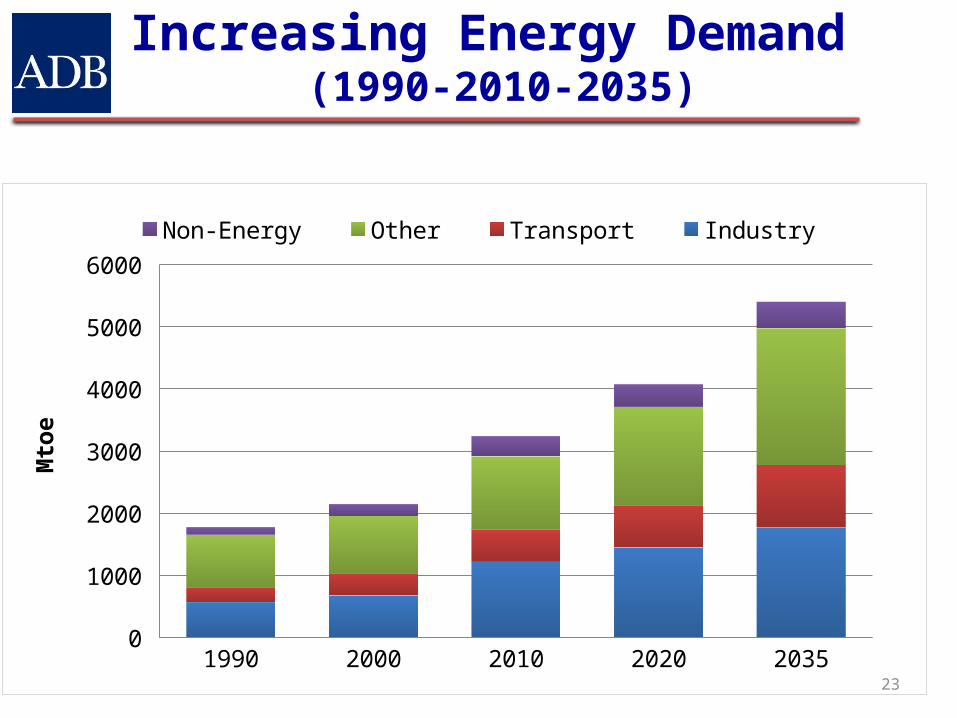

1990 2000 2010 2020 20350

1000

2000

3000

4000

5000

6000 Non-Energy Other Transport Industry

Mto

eIncreasing Energy Demand

(1990-2010-2035)

Road to Nowhere

24

Beijing, 2010

ADB’s Water Financing Program 2006-2020

Urban WaterRural Water Basin Water

• Rural water – rural water supply and sanitation; irrigation and drainage

• Urban water – urban water supply, sanitation and wastewater management

• Basin water – water resources development and management, flood management, wetlands and watershed protection, hydropower

How Does it Really Work?

S. Samuel TumiwaDeputy Representative

North America Representative Office

Canada Business Opportunities SeminarHalifax – Montreal – Calgary – Saskatoon

September 2015

26

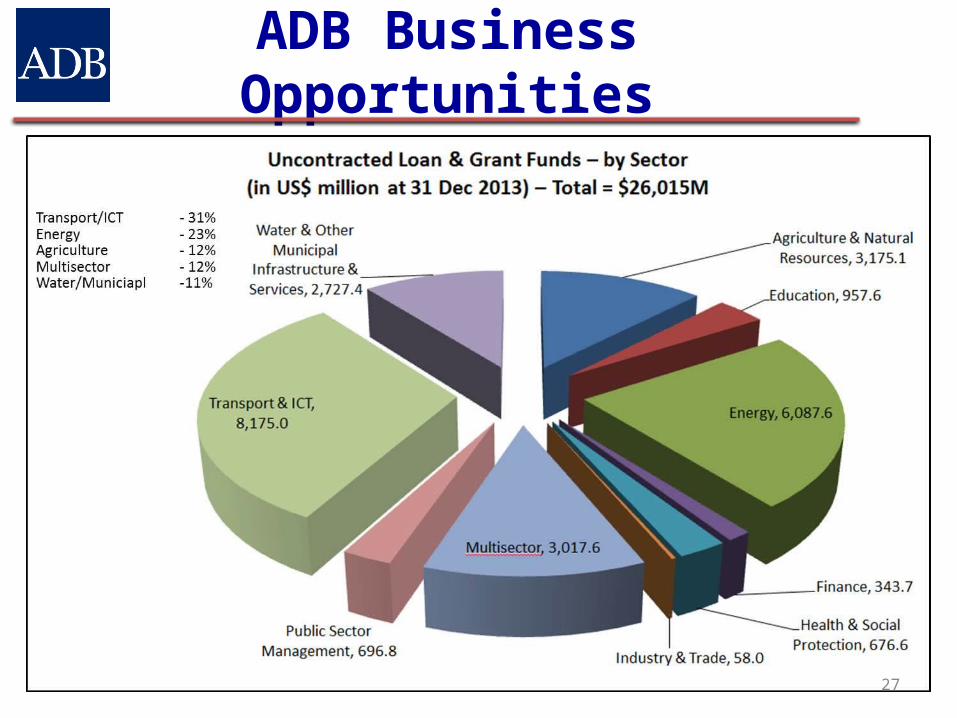

ADB Business Opportunities

27

ADB Business Opportunities

28

Almost all ADB

projects rely on

Consultants and

Contractors

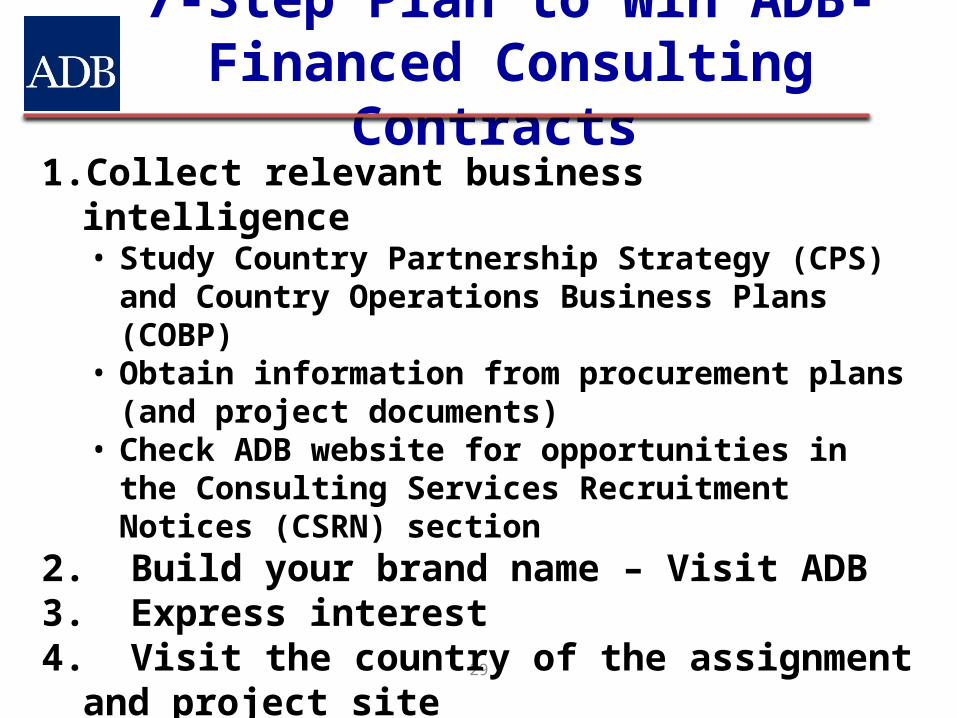

7-Step Plan to Win ADB-Financed Consulting Contracts

29

1. Collect relevant business intelligence • Study Country Partnership Strategy (CPS) and Country

Operations Business Plans (COBP) • Obtain information from procurement plans (and project

documents) • Check ADB website for opportunities in the Consulting

Services Recruitment Notices (CSRN) section 2. Build your brand name – Visit ADB3. Express interest 4. Visit the country of the assignment and project site 5. Offer partnership to firms likely to be shortlisted 6. Prepare a responsive and strong technical proposal 7. Do good work

Business Opportunities Fair and ADB’s Project Pipeline

30

ADB’s yearly Business Opportunities Fair - How to register

http://www.adb.org/news/events/6th-adb-business-opportunities-fair-2015

Background on the 2015 Business Opportunities Fair including Project Pipelines across countries and sectors

http://adbprocurementforum.net/?page_id=2362

Supplemental Slides

S. Samuel TumiwaDeputy Representative

North America Representative Office

Canada Business Opportunities SeminarHalifax – Montreal – Calgary – Saskatoon

September 2015

31

Vision An Asia and Pacific

region free of poverty

Strategic Agenda1. Inclusive Economic Growth2. Environmentally Sustainable3. Regional Integration

Core Areas of Operations

1. Infrastructure2. Environment3. Regional Cooperation and Integration4. Finance Sector Development5. Education

Other Areas of Operations

1. Health2. Agriculture3. Disaster and Emergency Assistance

Technical Assistance and Knowledge Sharing• Project preparatory feasibility studies• Research and analytical work• Policy dialogue and advisory activities• Training and capacity building programs• Dissemination of best practices

ADB’s Services to Foster Development Impacts

Program and Project Financing• Grants• Low interest loan • LIBOR based loan

Samuel TumiwaDeputy Representative

North America Representative Office

900 17th Street, N.W. Suite 900Washington, DC 2006

202 728 [email protected]

35