what every attorney should know - nacle.com · hummel consultation services the ... this is sample...

TRANSCRIPT

MASTERING MSA’S:

WHAT EVERY ATTORNEY

SHOULD KNOW

Robert F. Brogan, CELA Certified Elder Law Attorney

BROGAN LAW GROUP 3728 River Road

Point Pleasant, NJ 08742 732-701-9999 732-701-1492 (fax)

www.broganelderlaw.com [email protected]

Most of the MS A slides were taken, in significant part, from: Recovering for Personal Injury: Successful End or Just the Beginning

Medicare’s Interest in a Personal Injury Settlement?

Many thanks are given to the original authors, Brad Frigon and Patty Sitchler who, as fellow members of the Special Needs Alliance, were gracious enough to have given their permission to its reproduction for this audience. Additionally, I have included an article by Special Needs Alliance Member, Dennis Vorhees, who was kind enough to permit his materials to be included and who provides a n interesting commentary on the internal conflict most counsel face in deciding whether an MSA is necessary in a given case. The articles and commentary by Christine Hummel, Esq., are from someone whose opinions, insights, and experience I find invaluable in this area of the law. I thank her for her permission to include her articles for your benefit. Lastly, I want to thank my friend and colleague, Carl Price, Esq., for his research into Qualified Settlement Funds under IRC Section 468B. In several situations, MSAs are required when a person is duly eligible for Medicaid and Medicare, and because I have found that personal injury attorneys have varying levels of knowledge about Medicaid, I am including an additional Power Point presentation addressing What every Attorney needs to know about Public Benefits, which I hope you will find helpful in understanding how both programs effect MSAs and future benefits.

Bradley J. Frigon, JD, LLM (Tax), CELA Patricia F. Sitchler, JD, CELA Certified Elder Law Attorney Certified Elder Law Attorney 6500 S. Quebec St., Suite 330 112 E. Pecan Street, Suite 3000 Englewood, CO 80111 San Antonio, Texas 78205 (720)-200-4025 (210) 224-4491 (720)-200-4026 fax (210) 224-7983 fax [email protected] [email protected] www.bjflaw.com www.scs-law.com Christine Hummel, Esq. Dennis Vorhees, Esq. Hummel Consultation Services The Voorhees Law Firm Post Office Box 180 Key Bank Center Portsmouth, NH 03802-0180 Twin Falls, ID 83301 (603) 758-1411 Tel: (208) 736-6000 Fax: (603) 758-1411 Fax: (208) 736-6001 [email protected] [email protected] http://hummelcs.com www.idahocounsel.com

For their kind permission, I am including the contact information of the contributors

Tips for Practitioners

Develop a specific check list for cases that have a MSP/MSA issue.

Keep updated. CMS does not have a policy. Currently, each regional office is making up their own submission requirements. Most regional offices want you to follow WC guidelines.

Likely, Medicare beneficiary will be denied coverage by Medicare for medical services completed after settlement that are related to the injury.

Incorporate specific language that addresses these issues in your release and settlement documents.

Verify that plaintiff’s counsel has contacted COB office early in the case to ascertain MSP claim.

Know how you are going to address the MSA/MSP issue at the time of settlement, not as an after thought when you are ready to write the settlement check. See Tomilson v. Landers, 2009 WL 1117399 (M.D.Fla.)

Be careful of a claimant that is not represented by counsel.

Request a review or opinion by outside counsel or have outside counsel available at the mediation to advise you on public benefit, MSA/MSP issues.

Sample Release and Settlement COMPLIANCE WITH OBLIGATION TO PROTECT MEDICARE’S INTEREST

The parties acknowledge that Claimant currently receives Title II (Social Security Disability Income) monthly disability benefits from the Social Security Administration. The parties agree that this Settlement and Release Agreement is not intended to shift to the Center for Medicare and Medicaid Services (CMS) the responsibility for payment of the Claimant’s future medical expenses related to the alleged occurrence describe herein. To that end, Claimant shall establish, fund and administer a Medicare Set-Aside Arrangement pursuant to the requirements of the Section 1917(d)(4)(A) of the Social Security Act Section 42 USC 1395y(b)(2) and the regulations and policy memoranda issued by CMS applicable to and interpreting Medicare Set-Aside allocations, being 42 C.F.R. 411.20 et seq. These efforts have been undertaken by Claimant without the participation or consultation of Defendant or Insurers. Claimant agrees to indemnify, defend and hold harmless Defendant, Insurers and all persons or entities released by name or description in this Settlement Agreement from any loss, damage or claim, including attorney fees that occurs to Defendant or it’s Insurers by reason of Claimant’s failure to consider Medicare’s past or future interest in this settlement, and all matters related to the creation and administration of the Medicare Set-Aside Arrangement.

THIS IS SAMPLE LANGUAGE AND SHALL NOT CONSTITUTE LEGAL ADVICE.

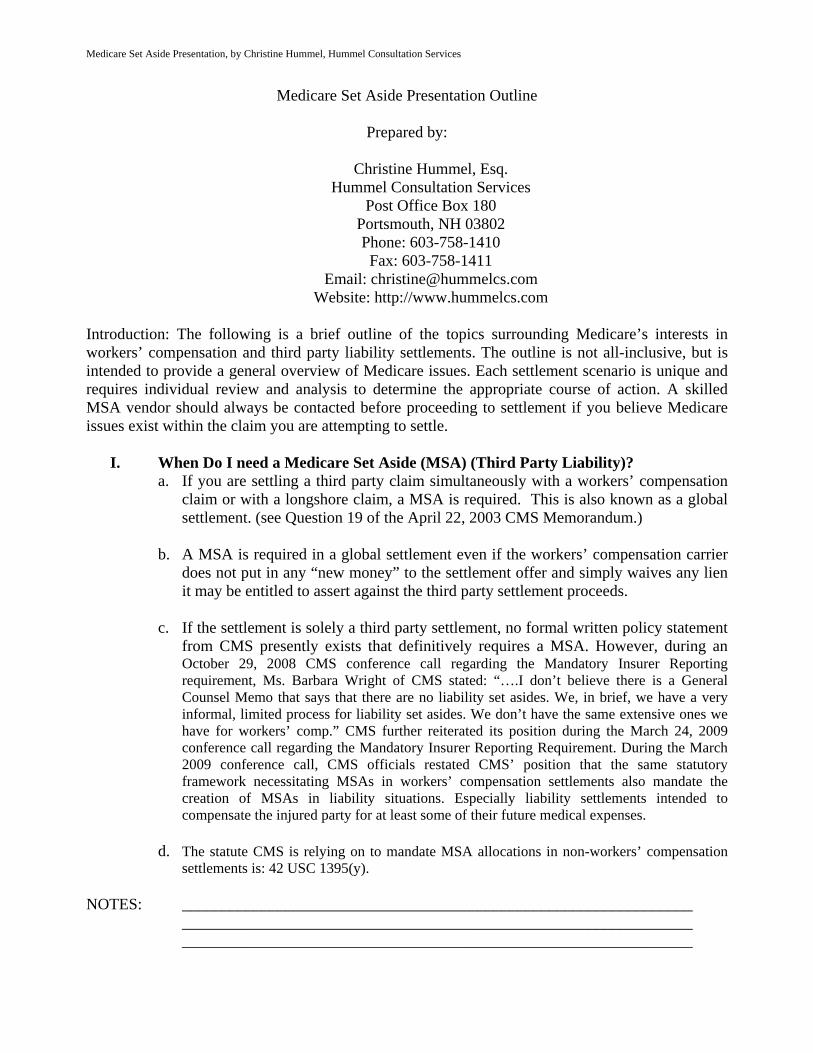

Medicare Set Aside Presentation, by Christine Hummel, Hummel Consultation Services

Medicare Set Aside Presentation Outline

Prepared by:

Christine Hummel, Esq. Hummel Consultation Services

Post Office Box 180 Portsmouth, NH 03802 Phone: 603-758-1410 Fax: 603-758-1411

Email: [email protected] Website: http://www.hummelcs.com

Introduction: The following is a brief outline of the topics surrounding Medicare’s interests in workers’ compensation and third party liability settlements. The outline is not all-inclusive, but is intended to provide a general overview of Medicare issues. Each settlement scenario is unique and requires individual review and analysis to determine the appropriate course of action. A skilled MSA vendor should always be contacted before proceeding to settlement if you believe Medicare issues exist within the claim you are attempting to settle.

I. When Do I need a Medicare Set Aside (MSA) (Third Party Liability)?

a. If you are settling a third party claim simultaneously with a workers’ compensation claim or with a longshore claim, a MSA is required. This is also known as a global settlement. (see Question 19 of the April 22, 2003 CMS Memorandum.)

b. A MSA is required in a global settlement even if the workers’ compensation carrier

does not put in any “new money” to the settlement offer and simply waives any lien it may be entitled to assert against the third party settlement proceeds.

c. If the settlement is solely a third party settlement, no formal written policy statement

from CMS presently exists that definitively requires a MSA. However, during an October 29, 2008 CMS conference call regarding the Mandatory Insurer Reporting requirement, Ms. Barbara Wright of CMS stated: “….I don’t believe there is a General Counsel Memo that says that there are no liability set asides. We, in brief, we have a very informal, limited process for liability set asides. We don’t have the same extensive ones we have for workers’ comp.” CMS further reiterated its position during the March 24, 2009 conference call regarding the Mandatory Insurer Reporting Requirement. During the March 2009 conference call, CMS officials restated CMS’ position that the same statutory framework necessitating MSAs in workers’ compensation settlements also mandate the creation of MSAs in liability situations. Especially liability settlements intended to compensate the injured party for at least some of their future medical expenses.

d. The statute CMS is relying on to mandate MSA allocations in non-workers’ compensation

settlements is: 42 USC 1395(y). NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

Medicare Set Aside Presentation, by Christine Hummel, Hummel Consultation Services

II. When Do I Need a Medicare Set Aside (MSA) (Workers’ Compensation and

Longshore)? a. You need a Medicare Set Aside every time you settle the medical portion of a

workers’ compensation claim or a longshore claim and the injured claimant is anticipated to require future medical care for the work injury.

b. If future medical care is anticipated for the work injury, the MSA should be done

even if the injured claimant is not eligible for Medicare at the time of settlement (see Question 1 of the July 11, 2005 CMS Memorandum.)

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

III. When Can I Get CMS Approval of the Proposed MSA Figure and How Long Does

it Take? a. CMS approval of a proposed MSA figure is always optional for every settlement; no

CMS regulation requires approval. b. CMS Workers’ Compensation review thresholds: CMS will only review proposed

MSA figures for the following situations:

i. For Medicare eligible persons: CMS approval can only be obtained if the total settlement value exceeds $25,000.00.

ii. For non-Medicare eligible persons: CMS approval can only be obtained if

both of the following criteria are met: 1) there is a reasonable expectation that the injured person will be Medicare eligible within 30 months of the date of settlement, and 2) the total settlement value exceeds $250,000.00.

c. CMS approval generally takes 2 to 4 months. CMS decisions may be appealed, but

will require additional approval time. d. It is believed CMS will use the same review thresholds for third party MSA

submissions, but this has not been confirmed in writing by CMS. e. An MSA should still be done even if the CMS review thresholds are not met.

f. NOTE: Third Party Liability MSA proposals are being reviewed by the CMS

Regional Offices on a case-by-case basis. Each Regional Office is establishing its own set of review criteria for Liability MSA submissions.

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

Medicare Set Aside Presentation, by Christine Hummel, Hummel Consultation Services

IV. What Types of Medical Care Must be Included in the MSA?

a. All regular and ongoing medical care to the injured party, including, but not limited to: physician office visits, prescribed medications, diagnostic testing, physical therapy, and durable medical equipment.

b. All medical care anticipated to take place in the future and as necessitated by the

work injury, including, but not limited to: all recommended surgeries, pain management injections, and the purchase or replacement of durable medical equipment.

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

V. Will CMS Approve a $0.00 MSA Allocation? a. CMS will approve a $0.00 MSA allocation only if the injured person has been fully

discharged from all treatment for the work injury by the treating physician, and no settlement funds are allocated for future medical needs (see question 20 of the April 22, 2003 CMS Memorandum.)

b. CMS may approve a $0.00 MSA allocation in a workers’ compensation settlement if

the claim has been fully denied or disputed. Obtaining CMS approval in disputed cases is always recommended as CMS may demand an increase to the proposed MSA allocation.

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

VI. What May Help to Decrease an MSA? a. Rated ages. b. Statements from the treating physician that the injured party is no longer a candidate

for certain medical procedures, such as surgeries, intrathecal pain pumps, and spinal cord stimulators.

c. Statements from the injured party that they do not wish to proceed with a

recommended surgery or treatment now or in the future. (Note: CMS is not necessarily bound by these statements and may still request an increase to the proposed MSA even if they are obtained.)

d. A statement from the treating physician that the party can be switched from brand

name to generic prescription medications.

Medicare Set Aside Presentation, by Christine Hummel, Hummel Consultation Services

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

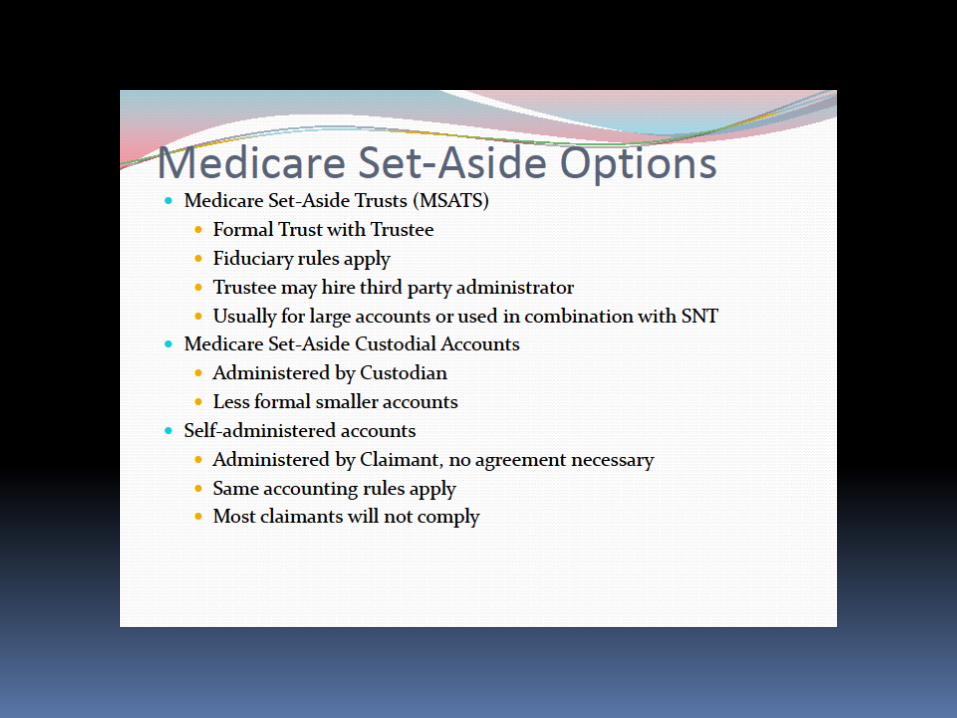

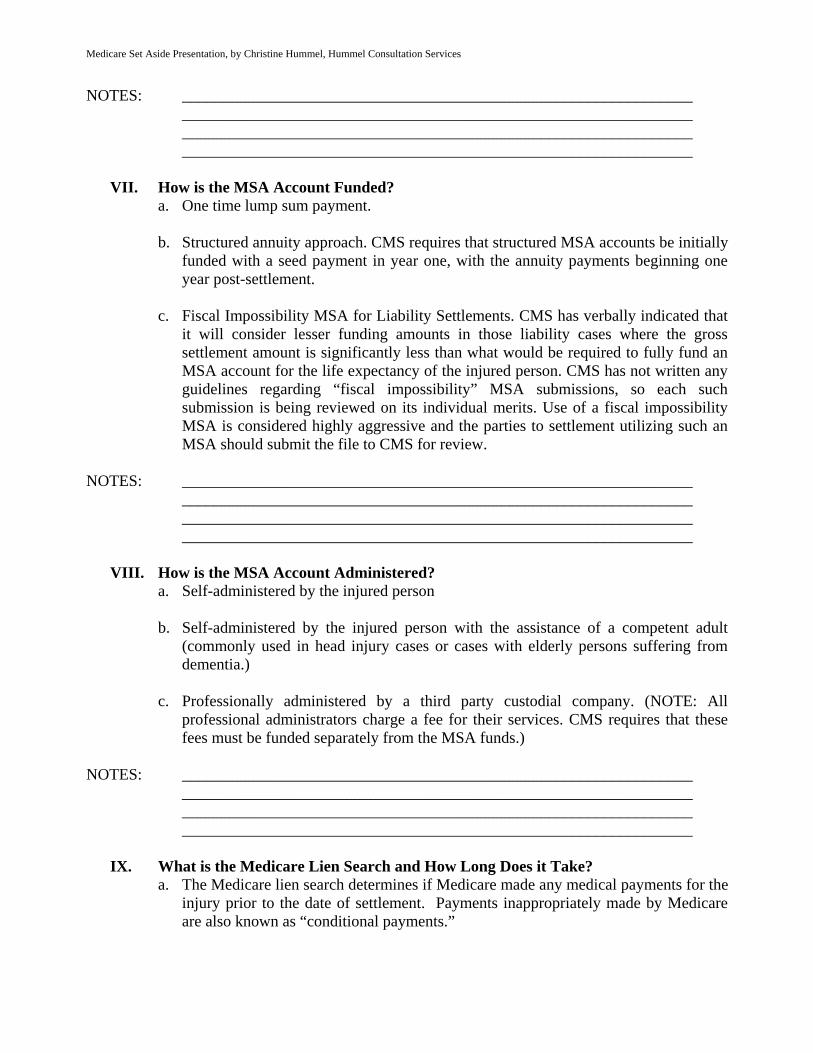

VII. How is the MSA Account Funded? a. One time lump sum payment. b. Structured annuity approach. CMS requires that structured MSA accounts be initially

funded with a seed payment in year one, with the annuity payments beginning one year post-settlement.

c. Fiscal Impossibility MSA for Liability Settlements. CMS has verbally indicated that

it will consider lesser funding amounts in those liability cases where the gross settlement amount is significantly less than what would be required to fully fund an MSA account for the life expectancy of the injured person. CMS has not written any guidelines regarding “fiscal impossibility” MSA submissions, so each such submission is being reviewed on its individual merits. Use of a fiscal impossibility MSA is considered highly aggressive and the parties to settlement utilizing such an MSA should submit the file to CMS for review.

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

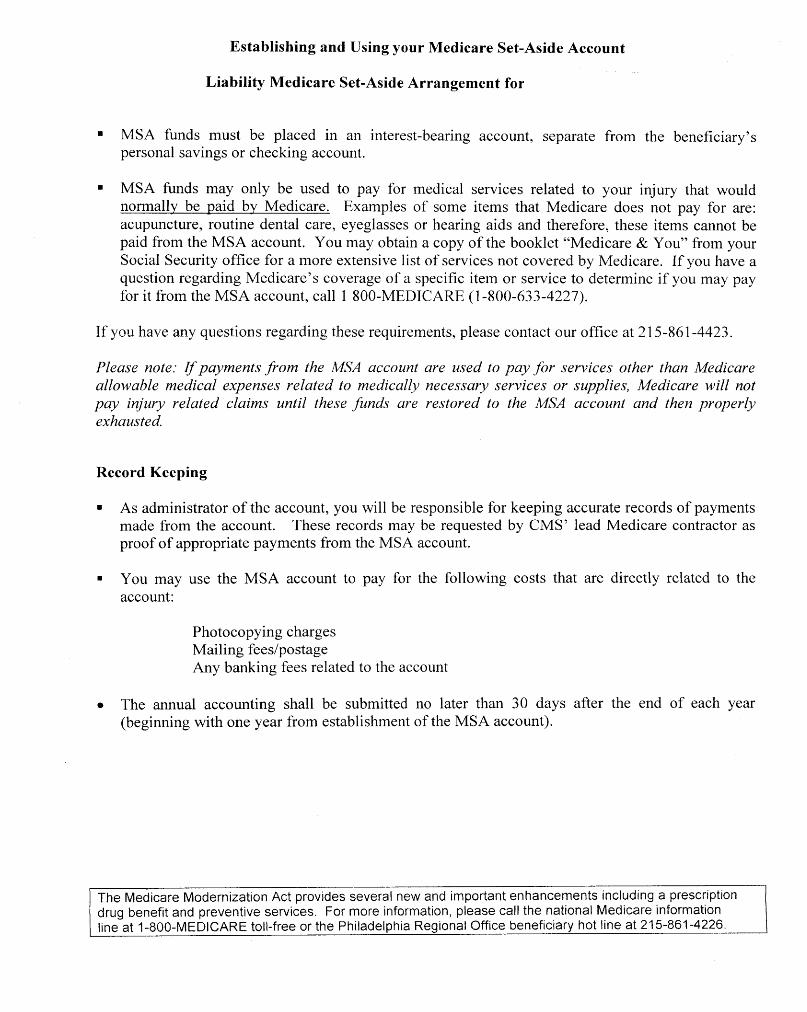

VIII. How is the MSA Account Administered? a. Self-administered by the injured person b. Self-administered by the injured person with the assistance of a competent adult

(commonly used in head injury cases or cases with elderly persons suffering from dementia.)

c. Professionally administered by a third party custodial company. (NOTE: All

professional administrators charge a fee for their services. CMS requires that these fees must be funded separately from the MSA funds.)

NOTES: ________________________________________________________________ ________________________________________________________________

________________________________________________________________ ________________________________________________________________

IX. What is the Medicare Lien Search and How Long Does it Take?

a. The Medicare lien search determines if Medicare made any medical payments for the injury prior to the date of settlement. Payments inappropriately made by Medicare are also known as “conditional payments.”

Medicare Set Aside Presentation, by Christine Hummel, Hummel Consultation Services

b. Medicare must be provided with a copy of the fully executed settlement documents before the final lien amount will be issued. Prior to receipt of the settlement documents, Medicare will only issue the tentative lien amount.

c. The final lien amount must be reimbursed to Medicare within 60 days of notice. d. The lien search takes, at a minimum, from 3 to 8 months. Lien totals returned by

Medicare may be appealed, but require much more additional review time. e. The Medicare lien search must always be conducted in every settlement involving a

Medicare beneficiary, regardless if CMS approval is obtained of the proposed MSA. In third party claims, the lien search is required even if the parties to settlement elect not to do a MSA.

NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

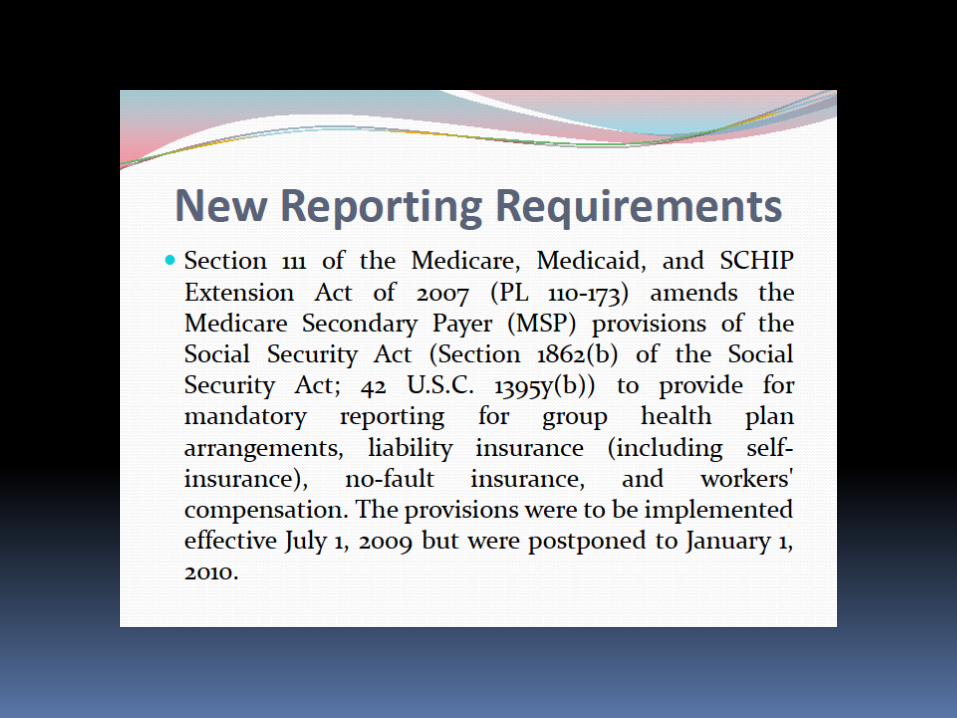

X. The Mandatory Insurer Reporting Requirement

a. On December 29, 2007 President Bush signed into law the Medicare, Medicaid and

SCHIP Extension Act (MMSEA). Section 111 of the MMSEA required that all workers’ compensation and third party liability insurers and benefit providers (i.e. self-insured entities) report to CMS any time they accept responsibility for payment of a Medicare beneficiary’s medical treatment and when that responsibility for payment terminates (i.e. there is a settlement, judgment, or other award that terminates or closes the claim for benefits).

b. Workers’ compensation claims settled on or after October 1, 2010 are now being

reported to the federal government through a secure website.

c. Liability claims/settlements will begin reporting settlements on January 1, 2012. Reporting will be back dated to all claims settled on or after October 1, 2011.

d. Additional information regarding the new reporting requirements can be found at the

official CMS website: http://www.cms.hhs.gov/mandatoryinsrep NOTES: ________________________________________________________________ ________________________________________________________________ ________________________________________________________________ ________________________________________________________________

________________________________________________________________ ________________________________________________________________

CHRISTINE L. HUMMEL, ESQ. President [email protected]

JOSEPH A. HUMMEL, IV Vice President of Operatijo

Please use the Hampton address for delivery services only. http://www.hummelcs.com

HUMMEL CONSULTATION SERVICES POST OFFICE BOX 180

PORTSMOUTH, NEW HAMPSHIRE 03802-0180

600 STATE STREET, UNIT 4 PORTSMOUTH, NEW HAMPSHIRE 03801

Telephone: (603) 758-1410 Facsimile: (603) 758-1411

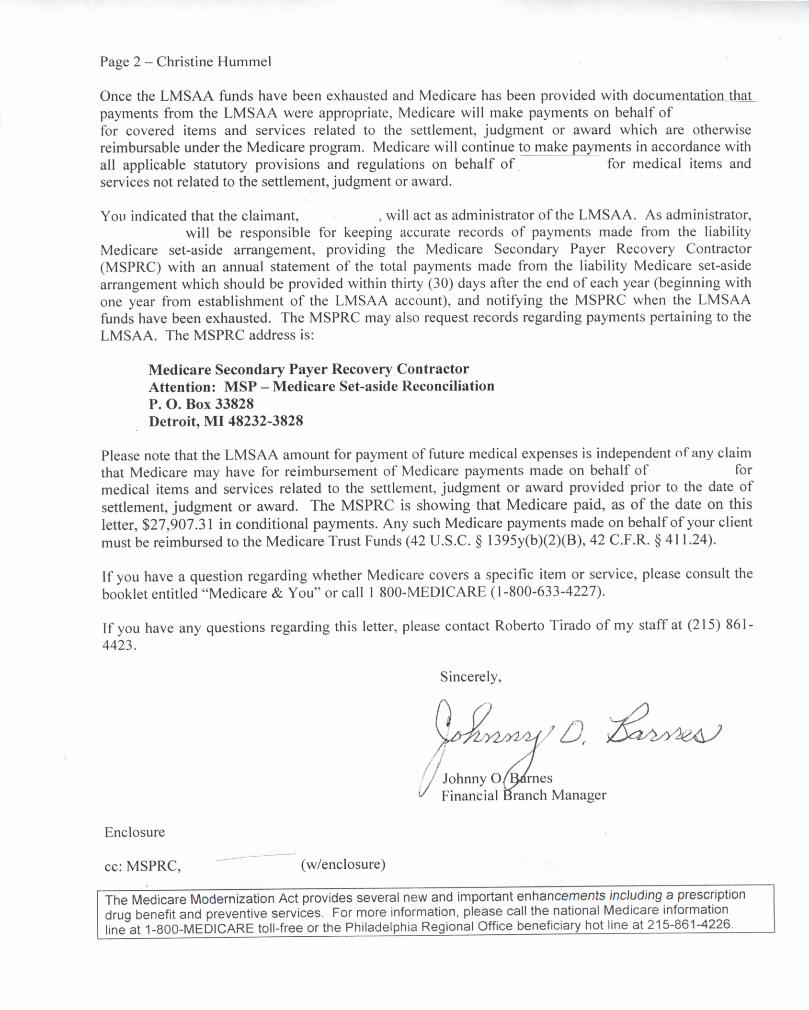

Third Party Liability Reference Sheet The main reference sources for CMS’ current policy position that third party liability settlements must also include Medicare set aside allocations to protect the Medicare trust fund are a series of Town Hall Conference Calls held by CMS to discuss the implementation of the Section 111 reporting requirement. It is important to remember that the transcripts of the conference calls are not necessarily legally binding and it is questionable if they would even be admissible in some courts. However, until there is an actual legal challenge regarding CMS’ current position regarding liability MSAs, HCS advises all of its clients to give great weight to the language of the Town Hall Transcripts. Statutory Sources for Workers’ Compensation:

42 USCA Section 1395y. This statute creates the statutory framework for the Medicare Secondary Payor Act. The key congressional intent behind passage of the Act was to ensure that Medicare would always be the secondary payor any time a third party payor could be found responsible for an injury or illness. Third party payments include workers’ compensation benefits, private health insurance benefits, and third party settlements, judgments, or awards. NOTE: This statute is applicable to all Third Party Situations.

42 CRF section 411.46: Lump Sum settlements of future medical benefits in workers’ compensation cases. This regulation states that a lump sum settlement of the medical benefits in a workers’ compensation case must not shift the burden of payment for that work injury to the federal Medicare program. If CMS feels the settlement does attempt to shift the burden of payment, the settlement will not be recognized. (42 CFR section 411.46(b)(2) ). 42 CFR section 411.47: This section outlines how Medicare’s interest in a settlement is to be allocated for in a compromise settlement of a workers’ compensation medical claim. There are no similar corresponding third party liability regulations. However, as will be detailed below, CMS has indicated that the same statutory framework outlining MSAs in workers’ compensation can be applied in Liability circumstances.

Town Hall Transcripts:

October 29, 2008 Transcript: on page 18 of the transcript of the October 29, 2008 CMS conference call regarding the Mandatory Insurer Reporting requirement, Ms. Barbara Wright of CMS stated: “….I don’t believe there is a General Counsel Memo that says that there are no liability set asides. We, in brief, we have a very informal, limited process for liability set asides. We don’t have the same extensive ones we have for workers’ comp.” March 24, 2009 Transcript: on page 23: Ms. Barbara Wright of CMS: “CMS for liability set-asides does not have the same formal review process [as CMS does for workers’ compensation MSA proposals] although our regional offices will consider review of proposed liability set-aside

Third Party Reference Sheet Prepared by: Hummel Consultation Services March 1, 2011 Page 2

amounts depending on their particular work load and whether or not they believe significant dollars are at issue.” Page 61: Ms Barbara Wright of CMS: “Liability set-aside and workers’ comp neither one has ever been required to participate in a CMS review process. Nonetheless they’re based on the same underlying statutory language which is that Medicare is not supposed to pay if payment has been made. And to the extent a settlement, judgment award, or other payment takes into consideration future medical then that settlement, judgment, or award should be appropriately expended for those future medicals. The fact that we don’t have a formal review process never did and does not create any type of safe harbor if its not reviewed by CMS.” (emphasis added by HCS) October 22, 2009 Transcript: Page 64: Ms Barbara Wright of CMS: “And all it is [Section 111] is a reporting requirement but we also said Section 111 doesn’t change any preexisting obligation. The idea of a set aside is based on the fact that Medicare is prohibited from making payment where payment has already been made. So that if you have a settlement or other payment that takes into account in any way future medicals that settlement judgement award or other payment should be exhausted or appropriately before Medicare is billed for the associated services. We do not have the same formal process for liability set aside that we have for workers’ comp set aside.” Page 65: Ms Barbara Wright “For Liability we don’t have the staffing or resources right now to [review every settlement] what we’ve told our regional offices is if they believe there are significant dollars at issue in a particular case and the workload of that particular regional office permits [they should review the proposal]. They may review a proposed set aside amount for liability. The fact that they declined to review in a particular case does not create any type of safe harbor. So you’re back to an obligation that has existed essentially since 1980.” (emphasis added by HCS). March 16, 2010 Transcript: page 41: Ms Barbara Wright of CMS: “As we’ve said on many calls, CMS has formalized process to review proposals for worker’ compensation, Medicare set aside amounts. It does not have the same formalized process for liability Medicare set aside arrangements. The process for workers’ compensation is voluntary. …. But regardless of whether CMS has a formalized process, or regardless of whether or not you’re participating in the formalized process for workers’ compensation Medicare set aside, the statue has the same language in either situation. It’s not parallel language. It’s not similar language. It’s literally the same physical sentence that we’re not to make payment where payment has already been made.” Continuing on Page 42: “so where future medicals are a consideration in arriving at the settlement et cetera, then appropriate arrangements should be made for appropriate exhaustion of the settlement before Medicare is billed for related services.”

September 22, 2010 Transcript: page 41: Ms. Barbara Wright of CMS: “…we will repeat what little we talked about these[Medicare set asides] in prior calls, is that Medicare beneficiaries and insurers have an obligation to protect Medicare’s interests but Medicare does not mandate the specific mechanism they use to do that. So can we say a set aside is required? No. But Medicare’s interests do need to be protected and any TPOC or settlement should be exhausted appropriately before Medicare is billed for related services.” Further down on Page 41: Ms. Barbara Wright of CMS: “Yes, again, as I said, that we can’t mandate the set aside, the settlement should be exhausted appropriately and as we said on other calls, we are not bound by the allocations of the parties to any settlement judgment or award.”

A review of the transcript data shows a clear and consistent interpretation from the CMS officials of the pertinent statutes. CMS clearly believes the Medicare Secondary Payor Act and its implementing

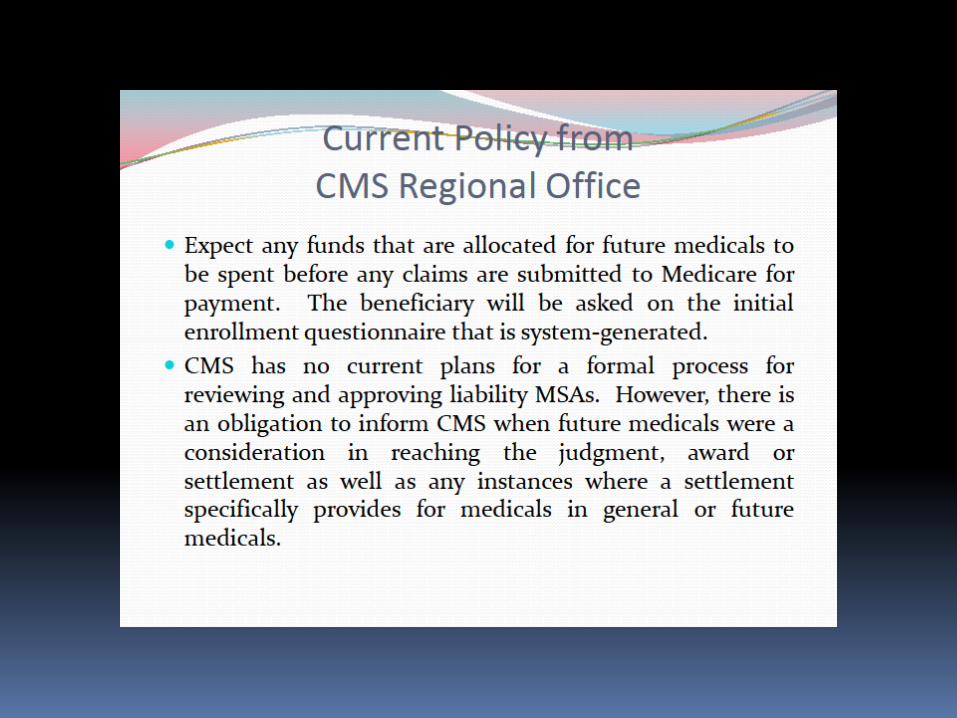

Third Party Reference Sheet Prepared by: Hummel Consultation Services March 1, 2011 Page 3 regulations give it the statutory framework necessary to mandate Medicare set-aside allocations in liability settlements. As discussed above, from a congressional intent perspective, CMS is completely correct. Congress clearly never intended for Medicare to be making payments on injuries or illnesses where a third party payment (remember third party payment can include a settlement or award from a judge or jury) has been made. That third party payment should be primary to Medicare. Medicare has the right to expect that third party payment to be appropriately exhausted prior to Medicare making any payments; thus, preserving Medicare’s secondary payer status. While some attorneys will argue that the key workers’ compensation regulations (outlined on page one of this memorandum) are narrowly tailored to only apply to workers’ compensation, CMS will argue that the statutory authority goes beyond those two regulations. Both sides have valid arguments; however, the congressional intent argument by CMS is likely to be very persuasive should the issue ever be formally litigated. All ten CMS Regional Offices have the authority to review Liability MSAs; however, this review is at the discretion of each individual office. Each office can set its own internal review thresholds and criteria for determining if it will or will not review a proposed MSA. Further the Regional Offices are free to modify their review criteria as frequently as they wish and without any warning to the MSA community. Therefore, a liability proposal reviewed today may not be reviewed by the same Regional Office in six months. As far as HCS can determine, the only Regional Office to issue a policy memo on the topic of Liability MSAs is San Francisco. The memo is not dated, but HCS received a copy in February 2010. The San Francisco CMS Policy statement regarding Liability MSAs reads as follows:

The Centers for Medicare & Medicaid Services (CMS) has no current plans for a formal process for reviewing and approving Liability Medicare set-aside arrangements. However, even though no formal process exists, there is an obligation to inform CMS when future medicals were a consideration in reaching the Liability settlement, judgment, or award as well as any instances where a Liability settlement, judgment, or award specifically provides for medicals in general or future medicals.

This San Francisco Policy memo appears to be in agreement with the CMS policy statements made by Ms. Wright during the Section 111 Town Hall Conference Calls. In September 2010, the Dallas Regional Office sent an email correspondence which contained the following data:

From: Stalcup, Sally J. (CMS/SC) Sent: Thursday, September 16, 2010 9:45 AM

The law does not require a “set-aside” in any situation. The law requires that the Medicare Trust Fund be protected from payment for future services whether it is a Workers’ Comp or liability case. There is no distinction in the law.

Set-aside is our method of choice and the agency feels it provides the best protection for the program and the Medicare beneficiary.

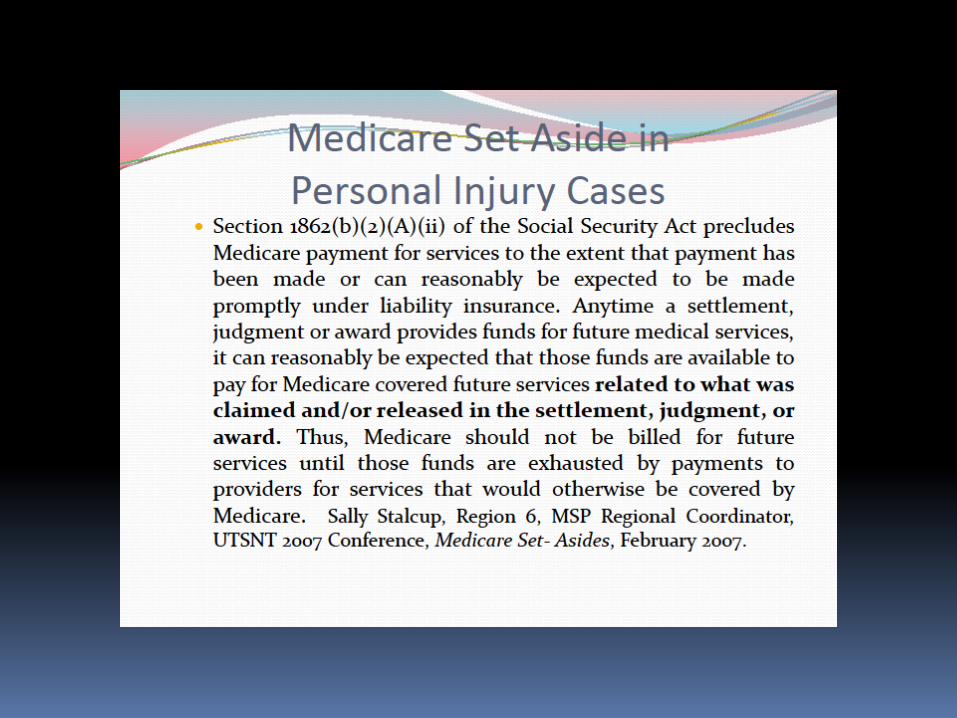

Section 1862(b)(2)(A)(ii) of the Social Security Act precludes Medicare payment for services to the extent that payment has been made or can reasonably be expected to be made promptly under liability insurance. This also governs Workers’ Compensation. 42 CFR 411.50 defines liability

Third Party Reference Sheet Prepared by: Hummel Consultation Services March 1, 2011 Page 4

insurance. Anytime a settlement, judgment or award provides funds for future medical services, it can reasonably be expected that those funds are available to pay for future services related to what was claimed and/or released in the settlement, judgment, or award. Thus, Medicare should not be billed for future services until those funds are exhausted by payments to providers for services that would otherwise be covered by Medicare. If they are not funded there is no reasonable expectation that third party funds area available to pay for those services.

There is no formal CMS review process in the liability arena as there is for Worker’ Compensation. However, CMS does expect the funds to be exhausted on otherwise Medicare covered services related to what was claimed/released before Medicare is ever billed. CMS review is decided on a case by case basis.

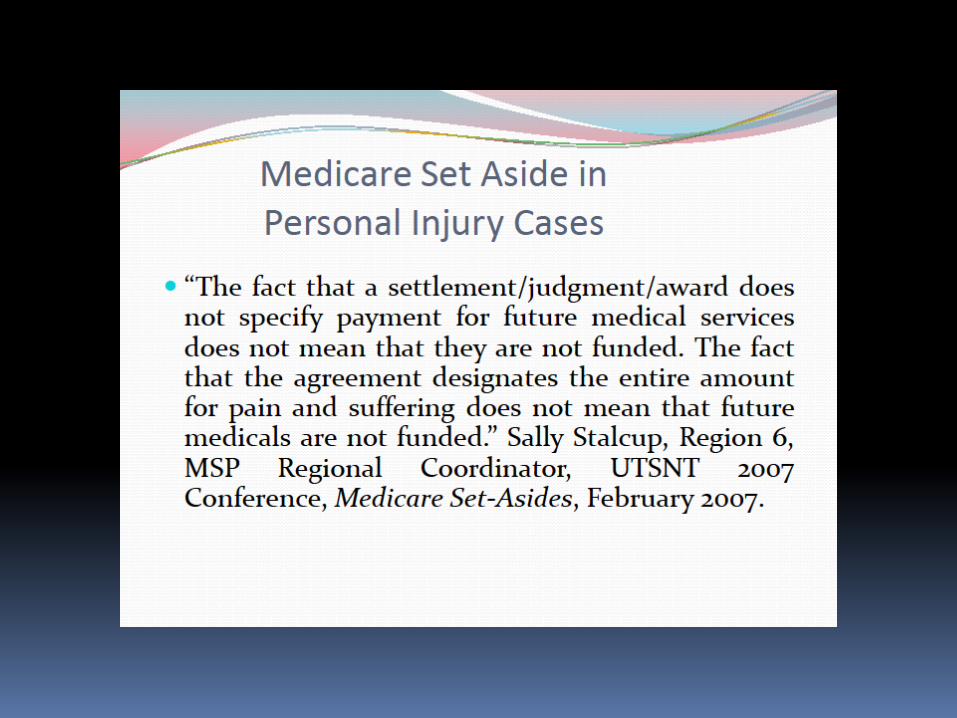

The fact that a settlement/judgment/award does not specify payment for future medical services does not mean that they are not funded. The fact that the agreement designates the entire amount for pain and suffering does not mean that future medicals are not funded.

The above summarizes the Liability MSA policy statements made by CMS officials as of February 2011. It is probable that CMS will continue to address Liability MSA issues and eventually issue formal policy memorandums. These future CMS policy statements may significantly alter or modify the policy positions outlined in this memorandum.

Office of Financial Management/Financial Services Group October 11, 2011 Note: this document revises the September 30, 2011 document issued on this subject. The revised language appears in the right-hand column of the “Examples” chart.

Liability Insurance (Including Self-Insurance): Exposure, Ingestion, and Implantation Issues and December 5, 1980 (12/5/1980)

The Centers for Medicare & Medicaid Services has consistently applied the Medicare Secondary Payer (MSP) provision for liability insurance (including self-insurance) effective 12/5/1980. As a matter of policy, Medicare does not assert a MSP liability insurance based recovery claim against settlements, judgments, awards, or other payments, where the date of incident (DOI) occurred before 12/5/1980. When a case involves continued exposure to an environmental hazard, or continued ingestion of a particular substance, Medicare focuses on the date of last exposure or ingestion for purposes of determining whether the exposure or ingestion occurred on or after 12/5/1980. Similarly, in cases involving ruptured implants that allegedly led to a toxic exposure, the exposure guidance or date of last exposure is used. For non-ruptured implanted medical devices, Medicare focuses on the date the implant was removed. (Note: The term “exposure” refers to the claimant’s actual physical exposure to the alleged environmental toxin, not the defendant’s legal exposure to liability.) In the following situations, Medicare will assert a recovery claim against settlements, judgments, awards, or other payments, and the Medicare, Medicaid, and SCHIP Extension Act of 2007 (MMSEA) Section 111 MSP mandatory reporting rules must be followed:

• Exposure, ingestion, or the alleged effects of an implant on or after 12/5/1980 is claimed,

released, or effectively released.

• A specified length of exposure or ingestion is required in order for the claimant to obtain the settlement, judgment, award, or other payment, and the claimant’s date of first exposure plus the specified length of time in the settlement, judgment, award or other payment equals a date on or after 12/5/1980. This also applies to implanted medical devices.

• A requirement of the settlement, judgment, award, or other payment is that the claimant was exposed to, or ingested, a substance on or after 12/5/1980. This rule also applies if

the settlement, judgment, award, or other payment depends on an implant that was never removed or was removed on or after 12/5/1980.

When ALL of the following criteria are met, Medicare will not assert a recovery claim against a liability insurance (including self-insurance) settlement, judgment, award, or other payment; and MMSEA Section 111 MSP reporting is not required. (Note: Where multiple defendants are involved, the claimant must meet all of these criteria for each individual defendant in order for a settlement, judgment, award, or other payment from that defendant to be exempt from a potential MSP recovery claim and MMSEA Section 111 reporting):

• All exposure or ingestion ended, or the implant was removed before 12/5/1980; and

• Exposure, ingestion, or an implant on or after 12/5/1980 has not been claimed and/or specifically released; and,

• There is either no release for the exposure, ingestion, or an implant on or after 12/5/1980; or where there is such a release, it is a broad general release (rather than a specific release), which effectively releases exposure or ingestion on or after 12/5/1980. The rule also applies if the broad general release involves an implant.

EXAMPLES: Below are some illustrative examples of how the policy related to December 5, 1980, should be applied to situations involving exposure, ingestion, and implantation. These examples are illustrative, as each situation must be evaluated individually on its merits. (Note: It is the parties’ responsibility to make a determination regarding this policy).

Situation Application of 12/5/80 Policy The claimant was exposed to a toxic substance in his house. He moved on 12/4/1980. The claimant did not return to the house.

Exposure ended before 12/5/1980.

The claimant was exposed to a toxic substance in his house. He moved on 12/4/1980. The claimant makes monthly visits to the house because his mother continues to live in the house.

Exposure did not end before 12/5/1980.

The claimant was exposed to a toxic substance while he worked in Building A. He was transferred to Building B on 12/4/1980, and did not return to Building A.

Exposure ended before 12/5/1980.

The claimant was exposed to a toxic substance while he worked in Building A. He was transferred to Building B on 12/4/1980, but routinely goes to Building A for meetings.

Exposure did not end before 12/5/1980.

The claimant had a defective implant removed on 12/4/1980. The implant had not ruptured.

Exposure ended before 12/5/1980.

The claimant had a defective implant that was never removed.

Exposure did not end before 12/5/1980.

REPORTING REMINDER: Information related to the MMSEA Section 111 MSP reporting requirements can be found at www.cms.hhs.gov/MandatoryInsRep. When reporting a potential settlement, judgment, award, or other payment related to exposure, ingestion, or implantation, the date of first exposure/date of first ingestion/date of implantation is the date that MUST be reported as the DOI. This is true for purposes of individual self-identification of a pending claim to the Centers for Medicare & Medicaid Services’ Coordination of Benefits Contractor, as well as for MMSEA Section 111 reporting.

Resolving the MSA in Liability Case Debate:

tougher than a cowboy stuffing feathers

into a pillow case during a dust storm . . .1

Author: Dennis S. Voorhees

The Voorhees Law Firm

Twin Falls, Idaho

208.736.6000

Reprinted with Permission

* * * * *

One of the most contentious issues confronting trial lawyers today is whether

Medicare set aside (MSA) arrangements must be established in third-party liability cases.

Around the nation listservs share accounts on how defense counsel are demanding that

MSAs be established in liability cases. These materials address this issue and provide

guidance on how to effectively evaluate and address the issues surrounding the

controversy.

A. Background on the MSA issue . . . a continuum of refinements . . .

A thumbnail sketch of Medicare and the government’s attempts to make Medicare

a secondary payer to all other sources of health care insurance coverage:

1965 – Congress enacts Title XVII of the Social Security Act, establishing

the Medicare program. 42 U.S.C. §1395y establishes Medicare as

secondary payer to workers compensation and group health plans under

Medicare Secondary Payer (MSP) provisions.

1980 – The MSP statute is broadened to include automobile, liability and

no-fault insurance (including self-insurance) as third-party payers.

1 Credit to Matt Garretson of the Garretson Lien Resolution Group for this observation.

- 2 -

2001 – Center for Medicare and Medicaid Services (CMS) issues what has

been called “the Patel memo” directing Regional CMS offices to take an

active role in assuring that Medicare’s interests were considered in

commutations of carriers’ liability for future medical expenses in workers

compensation (WC) settlements. MSAs were the recommended

mechanisms for protecting Medicare’s interests in such settlements.

2003 – Medicare Prescription Drug, Improvement and Modernization Act

(MMA) enacted. Revised the MSP statute to create greater certainty that

insurance carriers and self-insureds had primary coverage

responsibilities for third party claims. Previously, carriers were

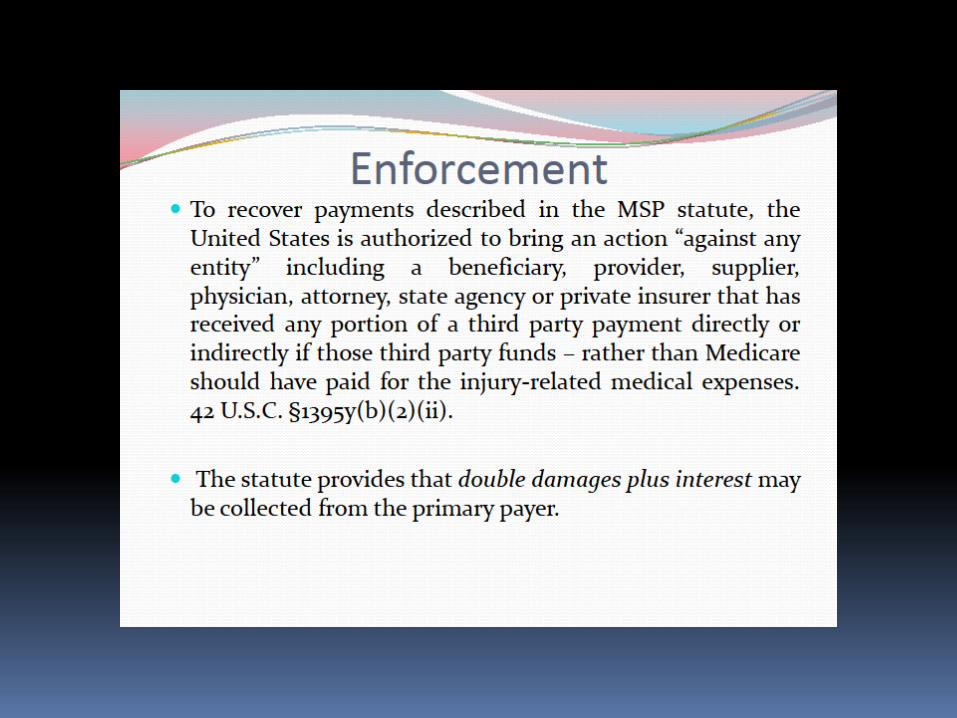

successfully able to argue that Medicare was primary if the carriers were

unable to pay a third party claim reasonably promptly. CMS was granted a

right to seek recovery "against any entity, including a beneficiary,

provider, supplier, physician, attorney, state agency, or private insurer

that has received any portion of a third party payment directly or

indirectly" if those third-party funds--rather than Medicare--should have

covered injury-related medical expenses. This right of reimbursement

exists regardless of whether the settlement acknowledges liability and how

the settlement agreement stipulates disbursement should be made. This

includes situations in which the settlement does not expressly include

damages for medical expenses. The plaintiff attorney and defendant can be

held responsible for twice the amount owed to the agency. See 42 U.S.C.

§1395y(b)(2)(B)(iii). 2 The MMA also made clear a plaintiff’s lawyer’s

duty to verify and resolve conditional Medicare payments made from the

date of injury to the date of settlement. See Attachments 1 and 2 for the

MSP statute and (some) applicable regulations.

2003-2004 – CMS publishes a series of memoranda (in the form of FAQs)

detailing WC carrier responsibilities in the creation of MSAs to protect

2 Garretson and Von Sauken, Act II: Reporting Obligations for Settling Insurers where Medicare is a

Secondary Payer: The Medicare, Medicaid and SCHIP Extension Act of 2007

- 3 -

Medicare’s interests when WC settlements conclude a carrier’s

responsibility for future medical expenses.

2007 – former President Bush signs the Medicare, Medicaid and SCHIP

Extension Act of 2007 (MMSEA), which required providers of liability

insurance (including self-insurance), no-fault insurance, and workers

compensation insurance (insurers) to determine whether a claimant is a

Medicare beneficiary and report this and other information (containing

more than 100 data points) to CMS for the purpose of better assuring

coordination of benefits and identifying sources of Medicare

reimbursement. Severe monetary penalties attached for non-compliance

($1,000 per beneficiary for each day an insurer is out of compliance).

These rules will apply to settlements taking effect on or after January 1,

2010.

B. Questions the personal injury lawyer must confront . . .

1. What is the current standard of care owed to Medicare-entitled clients in

considering and protecting Medicare’s interest with unallocated, third-party liability

settlements?

2. Are MSAs or similar protections required in all such cases? Some cases?

3. What factors should be considered in discharging these seemingly dual duties

to Medicare and client?

4. How should the personal injury lawyer document the file regarding duties to

Medicare and client?

5. How does the personal injury lawyer respond to a carrier’s demand that

Medicare’s name be placed on the check or that an MSA be established?

- 4 -

C. What the experts are saying . . .

There is any number of seasoned professionals expressing opinions on the

questions raised above. Industry professionals differ in their approach and

recommendations. Some, not surprisingly, sound self-serving with their

recommendations for techniques and services, but most have some basis in fact or law for

their perspectives. What follows is a sampling of perspectives from industry

professionals, accompanied by the author’s observations.

1. CMS officials. There is a diversity of views from within CMS. Sally Stalcup,

CMS’s MSP regional coordinator (Dallas – Region 6) is the most outspoken CMS

official for the proposition that a Medicare-entitled client’s unallocated, post-settlement

recovery be fairly allocated to estimated future medical expenses and spent before

seeking Medicare payment for any accident-related medical care. Her position is:

The Social Security Act (42 U.S.C. 1395y(b)(2)(A))

precludes Medicare payment for services to the extent that

payment has been made or can reasonably be expected to be

made promptly under liability insurance. Any time a

settlement, judgment or award provides funds for future

medical services, it can reasonably be expected that those

funds are available to pay for Medicare-covered future

services related to what was claimed and/or released in the

settlement, judgment, or award. Thus, Medicare should not

be billed for future services until those funds are exhausted

by payments to providers for services that would otherwise

be covered by Medicare. 3

In contrast, Thomas Bosserman, a CMS official from Region 9 (San Francisco)

was adamant in his remarks to Arizona workers compensation attorneys in June 2009 that

it was not current CMS policy to sanction Medicare beneficiaries for using their

unallocated post-settlement recoveries for purposes other than accident-related, future

medical care.4 See Attachment 3 for a copy of a letter stating his position in July 2002

(the “Bosserman letter” as it is referred to by practitioners). Note that Bosserman

3 Comments appearing in a PowerPoint presentation given to special needs trust attorneys in Dallas, April

2009. Lien Resolution Boot Camp, presented by the Special Needs Alliance, LLC. 4 Related by Tucson, AZ elder law attorney Robert Fleming who addressed Bosserman directly at the

seminar.

- 5 -

confines his statement to “unallocated” settlement monies, i.e., that no part of the

settlement was allocated to accident-related, future medical care.

Observation. Stalcup provides a correct statement of the law as enacted by

Congress in 1980. She does not acknowledge the practical – and perhaps legal – effect of

CMS policy not requiring that unallocated, post-settlement monies be used, in part, for

accident-related medical care. CMS has articulated the meaning and effect of the MSP

statute through regulations and policy, but no such requirements have ever been

announced by CMS for unallocated, post-settlement dollars received in third-party

liability cases.

The mechanics for fairly allocating a tort settlement are categorically different

than a workers compensation settlement. Comparative fault, damages caps, multiple

defendants, carrier policy limits, and complex recovery theories call for a sophisticated

resolution system that has not yet been articulated by CMS. Workers compensation-type

MSA rules are not responsive or equitable to rights and interests at stake in tort

recoveries.

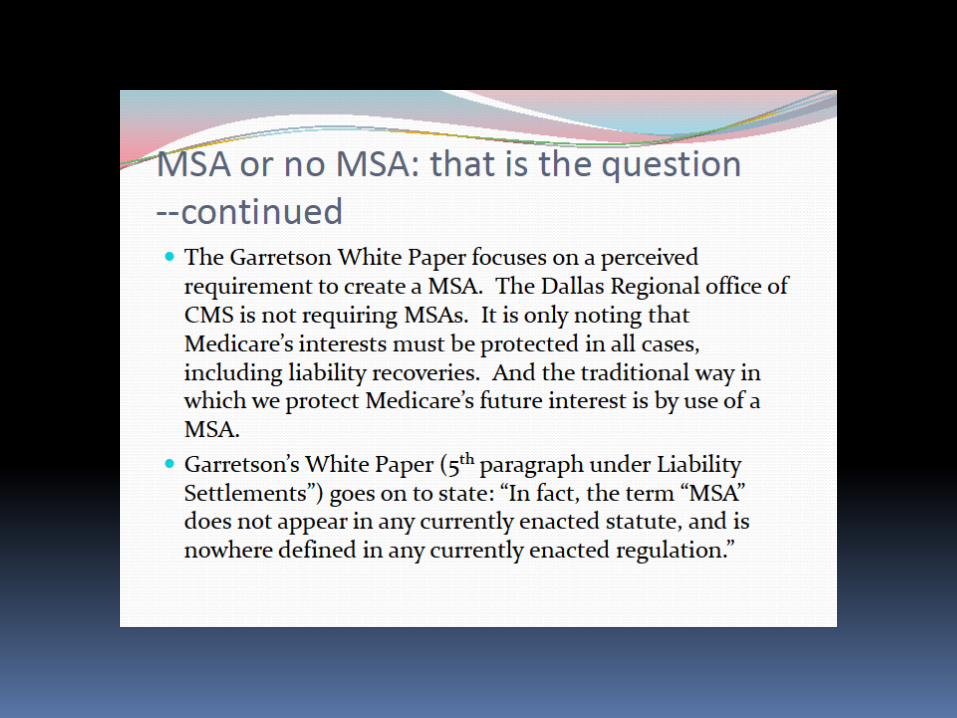

2. Settlement specialists. Matt Garretson of the Garretson Firm Resolution

Group has written extensively on the subject. Garretson concludes that MMSEA is a

reporting statute and adds nothing to longstanding CMS policy against requiring that

unallocated post-settlement monies be used for accident-related, future medical care.5 He

also argues that CMS has reiterated in its various 2009 Town Hall meetings that MMSEA

did not change existing CMS recovery practices. Garretson attributes “industry

misinformation” as injecting liability MSAs into a national debate.6 See Attachment 4. In

his earlier (May 2006) article on the topic (appearing in TRIAL magazine) Garretson

argued for taking a more nuanced approach: facts-and-circumstances, rule of reason.7

See Attachment 5. This more nuanced approach now appears in Garretson’s latest White

Paper on the topic. The paper “covers the waterfront” on the history of the controversy,

5 Act II: Reporting Obligations for Settling Insurers where Medicare is a Secondary Payer: The Medicare, Medicaid

and SCHIP Extension Act of 2007 http://www.garretsonfirm.com/garretson/news/index.cfm?newsID=13 (last visited

081809). 6 Dealing with Misinformation regarding Medicare Set Asides in Liability Settlements, Feb. 16, 2009.

http://garretsonfirm.com/garretson/pdf/Dealing_with_Misinformation_re_MSAs_in_Liability%20Settleme

nts_021609.pdf (last visited 081809). See Attachment 4. 7 Making Sense of Medicare Set-Asides, TRIAL May 2006.

http://garretsonfirm.com/garretson/pdf/MakingSenseofMedicareSetAsides.pdf

- 6 -

agency pronouncements, and recommended practices. This paper is “must” reading.8 See

Schedule 8 for the material.

Observation: For reasons discussed below, a facts-and-circumstances approach to

dealing with the duty of considering Medicare’s interest appears to be prudent.

3. MSA allocation and cost projection professionals. Mark Popolizio is a well-

respected professional in the MSA allocation industry, and employed by NuQuest/Bridge

Pointe, an MSA allocation company. He has analyzed the issue9 and concluded:

From the author’s review, the MSP does not contain

any specific provisions directly addressing future medicals in

liability cases. Specifically, the liability equivalent of 42

C.F.R. § 411.46 does not seem to exist under the liability

provisions of the MSP. The author is unaware of any judicial

decisions or other administrative proclamation requiring the

establishment of a MSA in the liability context. Furthermore,

CMS has not released any memoranda or other written policy

proclamation directly on point.

Popolizio concludes that notwithstanding the absence of CMS guidance, practitioners

should monitor the debate and announcements and create their own protocols for dealing

with the issue.

4. Insurers and defense counsel. Increasingly, MSP law and regulation has

focused upon insurers as a target for recovery responsibility and compliance. Roy A.

Franco, Director of Risk Management Strategies for Safeway Inc., has written a

compelling account of the predicament insurers are in balancing their duties to Medicare

and their insureds as they attempt to work through a dysfunctional set of laws,

regulations, and policy mandates.10

Quite apart from costly and onerous compliance

regulations with attendant fines and penalties, are the potential risks from contingent

liabilities arising out of Medicare’s interest in the handling of post-settlement medical

8 MSA White Paper: The Use and Propriety of Medicare Set Asides in Liability Settlements. 081909.

http://www.garretsonfirm.com/garretson/news/index.cfm?newsID=92

9 Liability Cases & Medicare Compliance Understanding How The Medicare Secondary Payer Statute Applies to

Liability/Primary Payers.

http://www.nuquestbridgepointe.com/services/med_res/liability_cases_and_medicare_compliance__june_08_.pdf

10

Resolution of a Case with a Medicare Claimant - For the Defense - May 2009.

http://forthedefense.org/CD/Public/FTD/2009/May/2009%20May%20FTD%20-

%20Mission%20Impossible%20-

%20Resolution%20of%20a%20Case%20with%20a%20Medicare%20Claimant.pdf

(last visited 081809) See Attachment 6

- 7 -

costs and a private right of action under the MSP act for the agency, the beneficiary and

others. See Attachment 6.

Observation. It is important for claimant’s counsel to appreciate the challenges

confronting insurers and their counsel so that effective collaborations can ensue. See

Attachment 6, Mission Impossible: Resolution of a Case with a Medicare Claimant?

Study it. You’ll be a better advocate for your clients on the MSA issue.

5. AAJ Position paper on MMSEA and MSAs in liability cases. The

Association for American Justice recently issued a position paper addressing the defense

bar’s increasing request for MSAs in third-party liability cases involving Medicare

beneficiaries. The AAJ paper makes the point – quite unequivocally – that section 111 of

MMSEA does not require MSAs in third-party liability cases. See Attachment 7.

Observation: The AAJ advisory is true as far as it goes, but it does not answer the

larger questions of whether – apart from section 111 of MMSEA – a Medicare

beneficiary’s counsel (and the beneficiary) has particular duties to Medicare, as appear

evident under 42 U.S.C. 1395y(b)(2)(A) and how each should go about discharging those

duties. So the larger questions go unanswered by the AAJ advisory.

C. Points on which there appears to be consensus . . .

1. Medicare cannot pay for a service or item that has already been paid for. 42

U.S.C. 1395y(b)2)(A). This law has been applicable to liability settlements since 1980.

2. Medicare’s policy, since 1980, has been to permit beneficiaries to apply non-

allocated, post-settlement monies toward their accident-related medical care any way

they wish, with no loss of Medicare eligibility.

3. CMS has proceeded incrementally to enhance its enforcement of the MSP.

4. CMS has promulgated regulations providing for consideration and protection

of Medicare’s interest in post-settlement use of commutated workers compensation

payments of future medical expenses. CMS has not done so with respect to liability

settlements, although CMS could do so.

5. Fair and equitable allocation of future medical expense settlements in tort

cases presents a categorically different and more complex system of analysis and

adjustment than do workers compensation settlements.

- 8 -

6. Current caseload burdens presented by WCMSA reviews are currently

overwhelming CMS staffing levels. MMSEA will further inundate the tasks of CMS

personnel with no commensurate increase in staffing levels.

7. Delay in MSP recovery activity and case resolutions have placed an unfair

burden on Medicare beneficiaries.

8. There are differences in the approaches being taken by the ten CMS regions

regarding requests to review and approve MSA proposals in liability cases. There are also

differences among regional offices regarding informal policy statements on the MSA in

liability case issue.

9. There is no consensus among MSP industry professionals regarding how to

consider and protect Medicare’s interests in liability cases resulting in unallocated, post-

settlement recoveries for Medicare beneficiaries.

10. Over the last four years CMS has not responded to numerous requests by

industry professionals for the agency to articulate how parties should fulfill their duty to

consider and protect Medicare’s interests in non-allocated, post-settlement monies arising

out of liability cases involving Medicare beneficiaries.

E. Recommendations to personal injury counsel . . .

1. Read about and come to a clear understanding of what the issues are in

unallocated, third-party liability settlements involving Medicare beneficiaries.

2. Talk to your clients about the issue. The level of discussion will vary with such

factors as age of client; likelihood of need for accident-related, post-settlement medical

care; amount of net settlement; presence of comparative fault and other elements of

recovery; client tolerance for risk; absence of settlement trust or vehicle to minimize

dissipation of recovery; and other considerations.

3. Reasonableness, good faith, and judgment. These are the special talents legal

counsel brings to this deliberation. Be able to give a nuanced articulation of the factors

that were considered in the approach taken.

- 9 -

4. Take into account what appears in settlement demand letters and life-care

planning documents. These are the instruments against which your reasonableness, good

faith, and judgment will be tested.

5. Triage. Divide your cases into three categories

a. The first group will be “business as usual”; little will be done in the way of

“considering and protecting Medicare’s interests” because of the absence of factors

identified in paragraph 2 above. However, even then, a brief memo to the file – perhaps a

completed checklist – will serve to document the file.

b. The second group will be where the factors outlined above are sufficiently

present and the client’s appetite for risk sufficiently low that an “informal arrangement”

(even a client-administered MSA account, not submitted to CMS) is developed.

c. The third group would be the once- (or ten-times) in-a-lifetime case that results

in a substantial settlement for a young claimant (and Medicare beneficiary) who sustained

catastrophic injuries and will need extensive and ongoing medical care. In that group of

cases you will want to (i) thoroughly discuss the issues with your client and interested

parties and (ii) find a strategy, perhaps submission of a liability MSA to CMS, that all are

comfortable with.

6. In the final analysis the decision regarding what to do with a Medicare

beneficiary’s third-party liability settlement belongs to the client (or client representative

if capacity is an issue). The duty to advise belongs to counsel.

7. In this author’s opinion there will be no adverse consequences to the attorney

and client who disregard these recommendations unless and until CMS articulates a

mechanism to rationally take Medicare’s interest into account. That day may come, but it

is not here yet. Nonetheless, prudence dictates that a demonstrable effort be undertaken to

consider and protect Medicare’s interest. Client and counsel must document the analysis.

8. The protocols recommended here will serve claimant’s counsel well in dealing

with defense counsel demanding formal MSA arrangements. Claimant’s counsel must

know the issues better than defense counsel and must be sensitive to the insurer’s risks,

concerns, and need for finality. The insurer cannot be expected to “bet the farm” on how

- 10 -

this issue will shake out. The draconian fines and penalties imposed by MMSEA and the

crazy quilt of counterproductive regulations applied against carriers, as expressed by

Safeway’s Roy Franco, illustrate the understandably paranoid environment the insurer is

currently operating in. Counsel must seek ways to work collaboratively with the insurer

to maximize gain to the client.

9. Monitor developments. There are sure to be some. The MSA in third party

liability cases won’t go away, and it won’t stand still. Follow the action and revise

protocols accordingly. You do not have to be the Lone Ranger. Consider an Association

working group to develop strategies and guidelines.

10. Opinion of counsel. In a difficult case the involvement and written legal

opinion of a legal specialist in this area of law may be warranted. It’s one way to off-load

potential liability, meet standard of care, educate the client and litigation parties, and

achieve a better outcome for all.

Conclusion

The “good old days” (if that’s what they were) of liability and damages are now

often dwarfed by lien resolution and benefits protection challenges. Governments,

insurers, ERISA plan administrators, and health care providers are all looking for ways to

recoup dollars spent on health care. The “recovery” system has gone so far into overdrive

that claimants and their counsel are increasingly inclined to walk away from litigation

because there is just simply nothing in the game for the injured party. A better system

must emerge Secondary payers are dependent upon the skill and resolve of counsel to

recover money for injured parties. Medicare and others are increasingly killing the goose

that lays the golden egg.

Presented by

Robert F. Brogan Certified Elder Law Attorney

Law Office of Robert F. Brogan, P.C.3728 River Road

Point Pleasant, NJ 08742732-701-9999

WWW.BROGANELDERLAW.COM

Guiding Families Through Life’s Storms

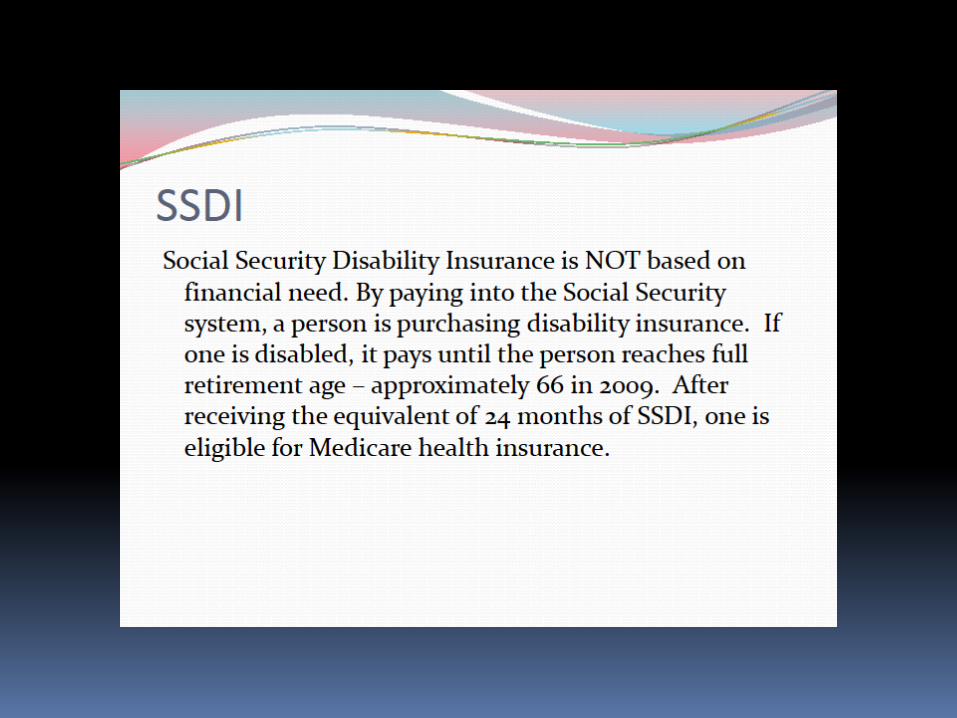

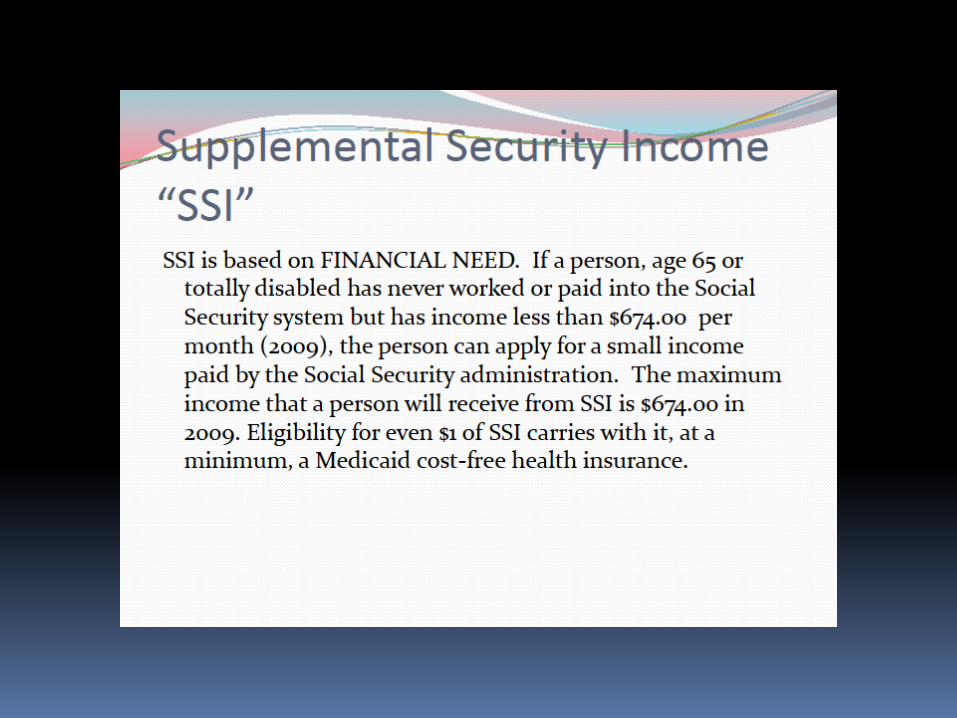

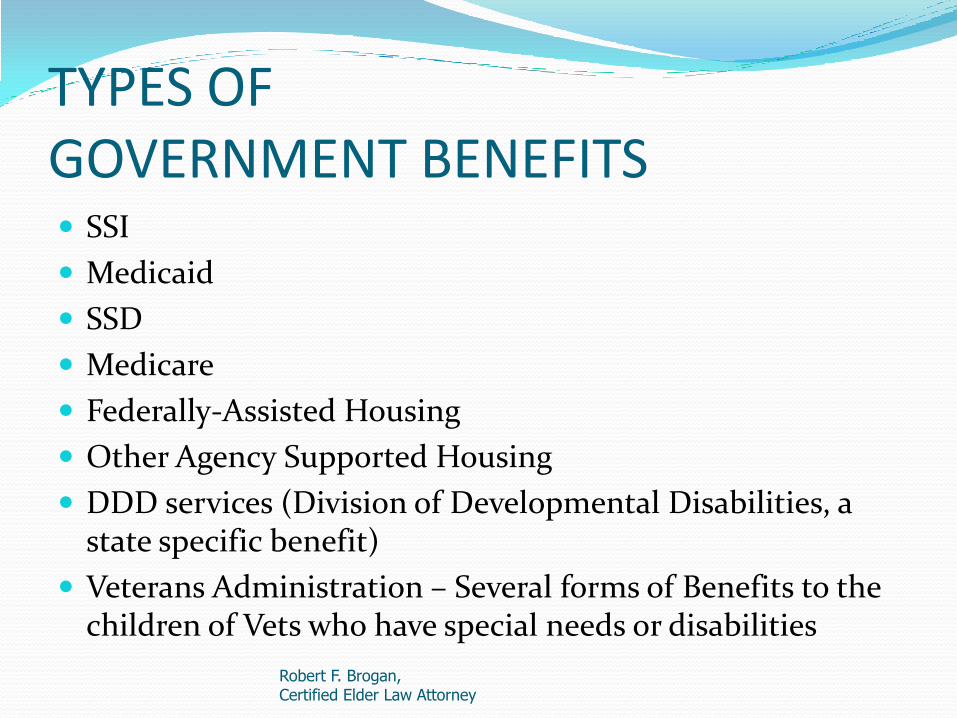

TYPES OF GOVERNMENT BENEFITS SSI

Medicaid

SSD

Medicare

Federally-Assisted Housing

Other Agency Supported Housing

DDD services (Division of Developmental Disabilities, a state specific benefit)

Veterans Administration – Several forms of Benefits to the children of Vets who have special needs or disabilities

Robert F. Brogan, Certified Elder Law Attorney

Special Needs Trusts and

Supplemental Benefits Trusts

TRUSTS FOR THE BENEFIT OF A DISABLED BENEFICIARY Special Needs “Payback” Trust

U.S.C. §1396p(d)(4)(A) A/K/A a self-settled trust

U.S.C. §1396p(d(d)(4)(C) trust or “pooled” trust;

Third Party Special Needs Trust

Also known as Supplemental Benefits Trust

Most are more advantageous plan to the self-settled trusts requiring “Payback”

Sole Benefit Trust – When Parent needs SNF, requires Payback, but makes Parent eligible.

Robert F. Brogan, Certified Elder Law Attorney

SOCIAL SECURITY ACT DEFINITION OF “DISABLED”

Pursuant to the Social Security Administration you are disabled if you are “unable to engage in any substantial, gainful activity by reason of any medically determinable physical or mental impairment which can be expected to result in death or which has lasted or can be expected to last for a continuous period of not less than twelve months”

Robert F. Brogan, Certified Elder Law Attorney

Special Needs “Payback” Trust Established with assets of disabled individual

Individual must be under 65 at time of the establishment and funding

Individual must be disabled as defined in Social Security Act

Robert F. Brogan, Certified Elder Law Attorney

Court-created Special Needs Trusts If trust is created or authorized by court, the court may

retain oversight in following areas:

Accountings

Trustee’s commissions

Investments

Limitations on Purchases of Major Assets

A good and convenient practice is to bring the application before the Judge who oversaw the 3rd Party liability action, particularly if there will be a friendly on behalf of a minor. Two birds – One Judge.

Robert F. Brogan, Certified Elder Law Attorney

PAYBACK REQUIREMENTS Medicaid agency entitled to reimbursement from any

assets remaining in trust upon death of beneficiary or trust termination for other reasons.

Reimbursement to the state “dollar for dollar” up to amount paid by Medicaid on behalf of individual.

Unless payback trust is very small, discourage additional funding by third parties.

Robert F. Brogan, Certified Elder Law Attorney

CHECK STATE REQUIREMENTS! New Jersey has some of the most stringent trust

requirements of the 50 states.

Limitation for distributions greater than $5,000.

Annual accounting requirements for minor’s trusts and those over 18 but who have a Court Appointed Guardian.

Get expert guidance on distribution issues, as an improper structure could result in a client losing government benefits they are validly entitled to otherwise receive.

Robert F. Brogan, Certified Elder Law Attorney

GENERAL TRUST REQUIREMENTS

Supplement, not supplant, government benefits

Definition of “special need” or “supplemental benefit”?

No definitive explanation.

There is guidance in the POMS.

The POMS have persuasive authority for New Jersey Medicaid, per the 3rd. Cir.

Robert F. Brogan, Certified Elder Law Attorney

What is NOT a Special Need Basic necessities of life

i.e., food, clothing, shelter, utilities

Incidental spending money (unearned income)

Gifts

Insurance on life of disabled beneficiary

Robert F. Brogan, Certified Elder Law Attorney

CHECKLIST FOR ASELF-SETTLED SPECIAL NEEDS TRUST

Check for compliance with federal law. Is the beneficiary under age 65?

Is the beneficiary “disabled?”

Is the trust created by the beneficiary’s parent, grandparent, guardian or by the court?

Does the trust contain a provision requiring repayment of the state Medicaid program upon termination of the trust?

Check for compliance with state law.

Verify that statutory liens have been paid prior to the funding of the trust.

Robert F. Brogan, Certified Elder Law Attorney

FUNDING ISSUES Structured Settlements Payments made directly to disabled beneficiary may

render beneficiary ineligible to receive means-tested government benefits

Trust should be payee.

Payments should “pour over” into trust.

Robert F. Brogan, Certified Elder Law Attorney

SUPPLENTAL BENEFITS TRUSTBetter known as THIRD PARTY TRUSTS Living trust or

Testamentary trust created by will

Often created as a Living Trust, which remains unfunded until the parents’ death and the Will pours over into the Living Trust

These are funds from a parent, grandparent, friend, e.g., rather than payments owed to the Medicaid recipient. That’s why no pay back to the State is required, except in rare circumstances between spouses.

Robert F. Brogan, Certified Elder Law Attorney

THIRD PARTY TRUSTS (Cont.) Periodic additions can be made through lifetime

giving or inheritances. Other family members may contribute to the Trust.

Additions of beneficiary’s assets to third party trust may result in ineligibility for certain government benefits

Robert F. Brogan, Certified Elder Law Attorney

NO PAYBACK CLAUSE? Generally, no payback provision required BUT

Check state regulations to make sure no payback is required. Spousal funds may still require payback in some states. SOB trusts require Payback clause.

Include specific dispositive provisions for final disposition of trust assets. Legacy planning for the whole family.

Robert F. Brogan, Certified Elder Law Attorney

ADDITIONS TO 3rdParty TRUST

Additions of beneficiary’s assets to third party trust may result in ineligibility for certain government benefits.

When drafted properly, most third party trusts can be designed specifically in anticipation of receipt of funds from third parties without sacrificing the eligibility of the Medicaid recipient third-party.

Robert F. Brogan, Certified Elder Law Attorney

LIEN ISSUES FOR CONSIDERATION Medicaid

Arkansas HHS v. Ahlborn, 2006 U.S. Supreme Court decision

Medicare

State Department of Human Services

Workers Compensation

ERISA

Robert F. Brogan, Certified Elder Law Attorney

Home Ownership Options Options include:

Trust owns house, rent is not charged.

Trust owns house, rent is charged.

Trust buys house and transfers house to beneficiary

Trust buys fractional interest in house, such as life estate.

The purchase of a home is often the most frequently raised desire when a significant sum is obtained, the next two considerations are often automobiles (including handicap accessible vans) and Disney trips.

Robert F. Brogan, Certified Elder Law Attorney

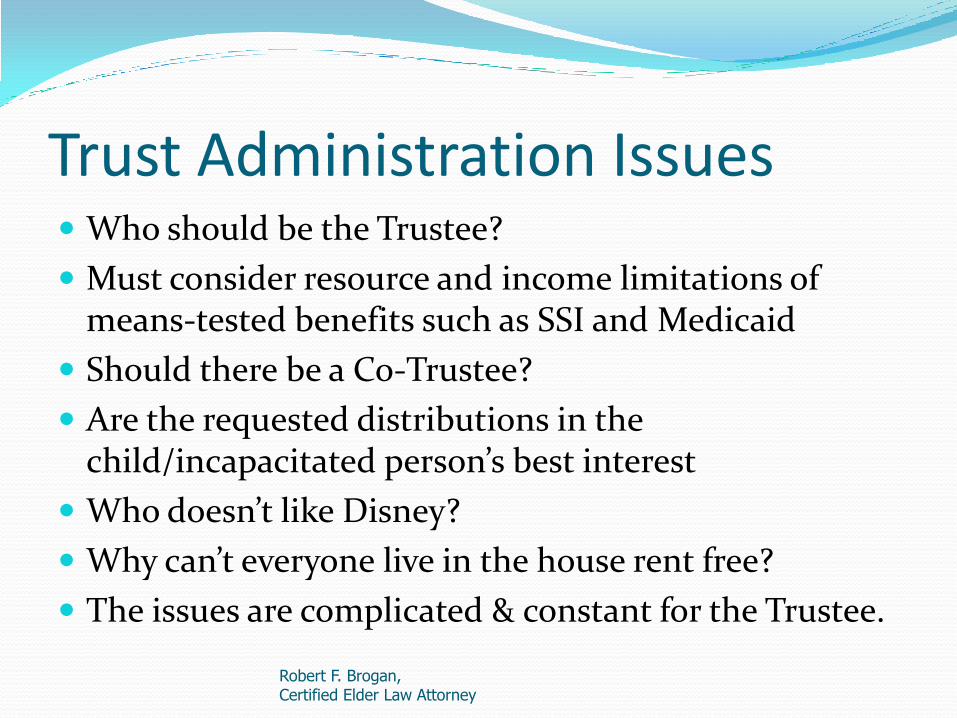

Trust Administration Issues Who should be the Trustee?

Must consider resource and income limitations of means-tested benefits such as SSI and Medicaid

Should there be a Co-Trustee?

Are the requested distributions in the child/incapacitated person’s best interest

Who doesn’t like Disney?

Why can’t everyone live in the house rent free?

The issues are complicated & constant for the Trustee.

Robert F. Brogan, Certified Elder Law Attorney

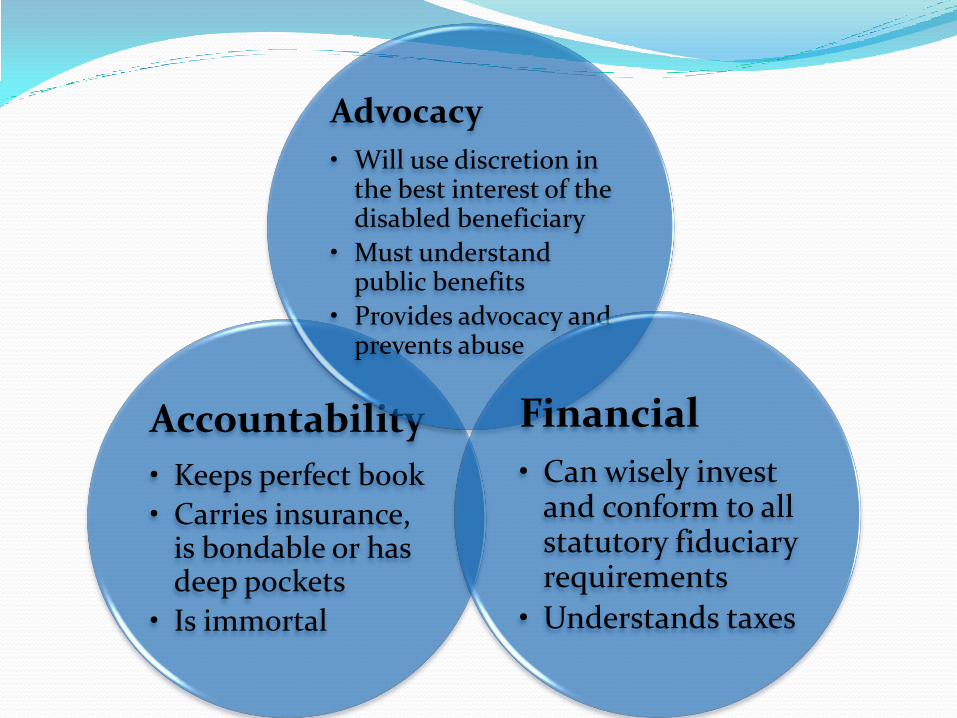

What Does the Corporate Trustee Do for the Special Needs Attorney & clients? My first line of defense is my trustee.

Keeps in contact with my clients and their beneficiaries.

Gives me piece of mind that my trust will do what it is intended to do.

Reduces the risk of an accidental distribution which terminates benefits.

Can assist me in educating the public

THE IDEAL TRUSTEEWill use discretion in the best interest of the disabled beneficiary

Must understand public benefits and keep up with changes in the law

Can wisely invest and conform to all statutory fiduciary requirements

Understands taxes

Keeps perfect books

Carries insurance, is bondable or has deep pockets

Provides advocacy and prevents abuse

Is immortal

Accountability

• Keeps perfect book

• Carries insurance, is bondable or has deep pockets

• Is immortal

Advocacy

• Will use discretion in the best interest of the disabled beneficiary

• Must understand public benefits

• Provides advocacy and prevents abuse

Financial

• Can wisely invest and conform to all statutory fiduciary requirements

• Understands taxes

MODIFYING IMPROPERLY ORPOORLY DRAFTED SNT

May be able to modify or reform trust by Court intervention or by terms of the Trust instrument itself

Trustee may be able to transfer assets into another SNT without court approval

An outright distribution in a Will cannot normally be modified into an SNT, so do not leave it to the Courts to do your planning for you.

Robert F. Brogan, Certified Elder Law Attorney

Quicksand The difficulty in concentrating in public benefits law is

that it is constantly changing in significant ways.

The future of Medicaid as the provider of Medical care for the impoverished is uncertain.

Efforts are constantly made to limit eligibility and cut federal and state budget costs.

DRA of 2005 is an example.

New Jersey’s unique requirements for Self-Settled d(4)(a) Trusts are another example.

Robert F. Brogan, Certified Elder Law Attorney

Deficit Reduction Act of 2005 Extends Medicaid's "look-back" period for all asset

transfers from three to five years.

Changes the start of the penalty period for transferred assets from the date of transfer to the date when the individual transferring the assets enters a long-term care facility and would otherwise be eligible for Medicaid coverage.

Robert F. Brogan, Certified Elder Law Attorney

Deficit Reduction Act of 2005 Prohibits States from "rounding down" fractional

periods of ineligibility when determining ineligibility periods resulting from asset transfers.

Permits States to treat multiple transfers of assets as a single transfer and begin any penalty period on the earliest date that would apply to such transfers.

Robert F. Brogan, Certified Elder Law Attorney

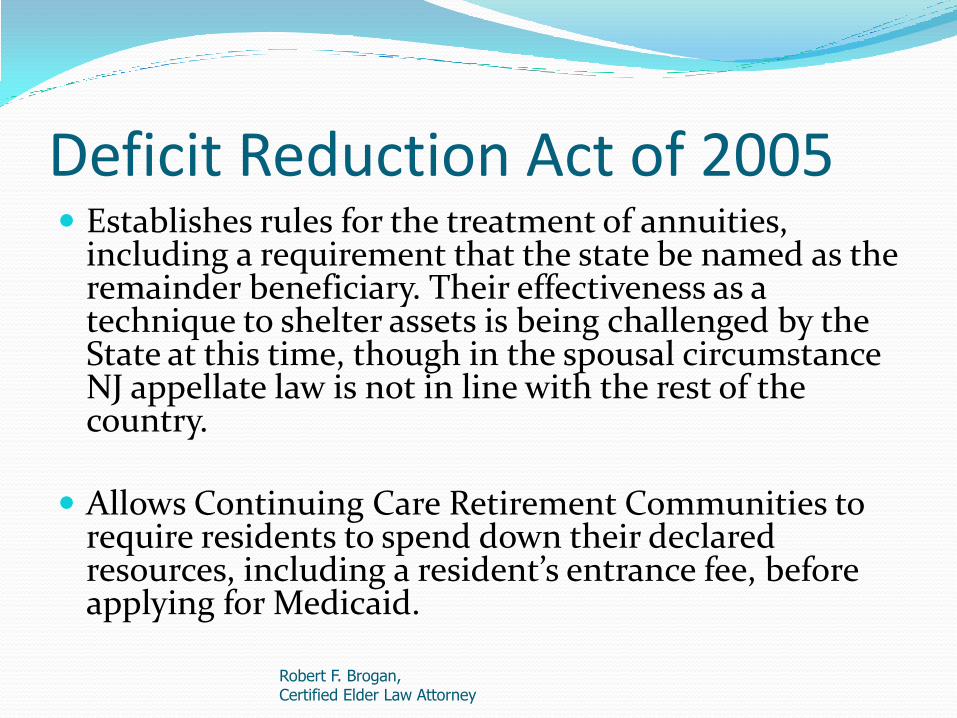

Deficit Reduction Act of 2005 Establishes rules for the treatment of annuities,

including a requirement that the state be named as the remainder beneficiary. Their effectiveness as a technique to shelter assets is being challenged by the State at this time, though in the spousal circumstance NJ appellate law is not in line with the rest of the country.

Allows Continuing Care Retirement Communities to require residents to spend down their declared resources, including a resident’s entrance fee, before applying for Medicaid.

Robert F. Brogan, Certified Elder Law Attorney

Deficit Reduction Act 0f 2005 Requires all states to apply the so-called “income-

first” rule to community spouses who appeal for an increased resource allowance based on their need for more funds invested to meet their minimum income requirements.

Requires the purchase of a life estate to be included in the definition of "assets" unless the purchaser resides in the home for at least one year after the date of purchase.

Robert F. Brogan, Certified Elder Law Attorney

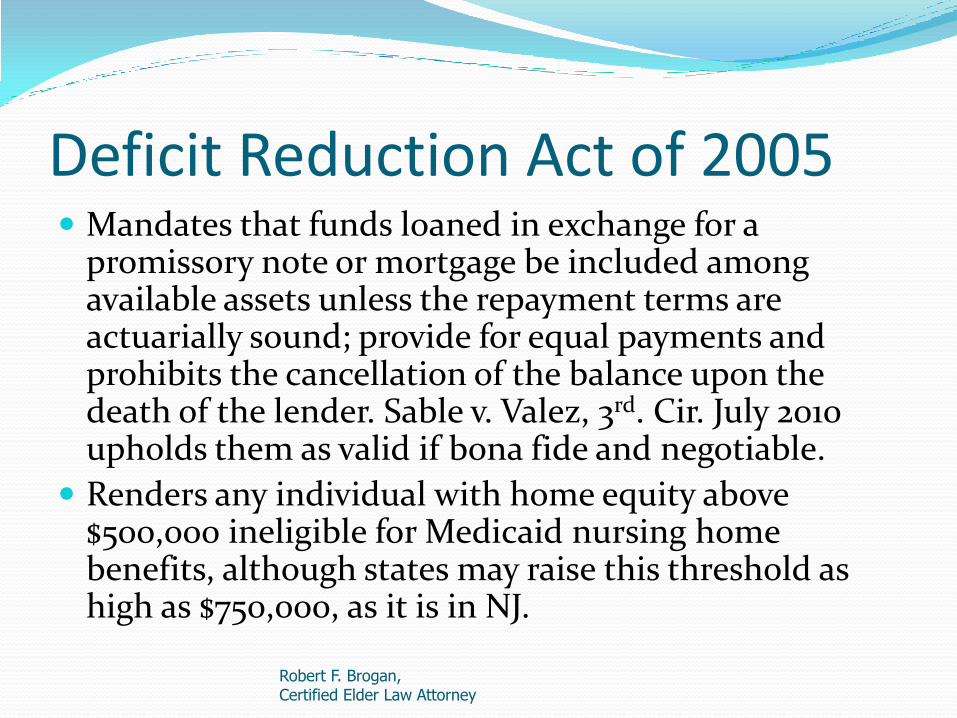

Deficit Reduction Act of 2005 Mandates that funds loaned in exchange for a

promissory note or mortgage be included among available assets unless the repayment terms are actuarially sound; provide for equal payments and prohibits the cancellation of the balance upon the death of the lender. Sable v. Valez, 3rd. Cir. July 2010 upholds them as valid if bona fide and negotiable.

Renders any individual with home equity above $500,000 ineligible for Medicaid nursing home benefits, although states may raise this threshold as high as $750,000, as it is in NJ.

Robert F. Brogan, Certified Elder Law Attorney

Common Pitfalls Causing Medicaid Eligibility

Gift to Minor Act Accounts

Unstructured Beneficiary Designations

Disinheritance

No planning at all

RECEIVING PROCEEDS FROM A THIRD-PARTY LIABILITY ACTION OR OTHER LAW SUIT

Finding a Special Needs Attorney

Special Needs Alliance

Network of disability and public benefits attorneys.

www.specialneedsalliance.org

1.877.572.8472

Robert F. Brogan, Certified Elder Law Attorney

Presented by

Robert F. Brogan Certified Elder Law Attorney

Law Office of Robert F. Brogan, P.C.3728 River Road

Point Pleasant, NJ 08742732-701-9999

WWW.BROGANELDERLAW.COM

Guiding Families Through Life’s Storms

Division of Developmental Disabilities

DDD serves more than 40,000 people.

About 3,000 are in group homes.

Underfunded to meet the demands of the families it is designed to serve.

Case Management and residential support services dominates its activity.

Discouragingly long Wait-lists and difficulty in responding to clients’ needs are the experiences of many.

It can take years to actually be eligible for crucial services such as housing.

Notably, there are opportunities in certain tragic circumstances to move up the wait lists, particularly if the disabled individual’s lost both parents and is potentially going to be homeless.

Robert F. Brogan, Certified Elder Law Attorney

DDD Services

Case Management

Residential Services (various levels and types of services from group homes to caretaker training to remain in family home)

Adult Day Care and Employment Training

Guardianship Services (though because it only addresses Guardian of the Person, it is insufficient for authority to apply for government benefits, such as Medicaid or VA)

Family Support and Developmental Centers

Robert F. Brogan, Certified Elder Law Attorney

CONCLUSION

Maintaining eligibility for government programs for disabled family members often contradicts the efforts of family members to provide support and care for their loved ones. Supplemental Benefits Trusts and Special Needs Trusts provide the mechanism for sheltering resources to benefit disabled family members so that these contradictory efforts can be harmonized. A well managed support system, using Special Needs Trusts, can maximize the use of government-provided services while supporting the family’s care and enhancing the comfort and enjoyment of life for the disabled beneficiary. Coordination by the special needs attorney, the special needs planner and the corporate trustee increase the likelihood of the family’s plans and objectives being met, while preserving the much needed government benefits for their loved one.

Robert F. Brogan, Certified Elder Law Attorney

DDD services To apply for DDD services contact

1-800-832-9173

Or get additional information online at:

http://www.state.nj.us/humanservices/ddd/help.html

Robert F. Brogan, Certified Elder Law Attorney