what can we learn from the financial flows of the 2008 ... · what can we learn from the financial...

TRANSCRIPT

What can we Learn from theFinancial Flows of the 2008-2009 Crisis?

Juliane Begenau Saki Bigio Jeremy Majerovitz

HBS UCLA Stanford

Barcelona GSE Summer Forum

June 9, 2015

1 / 77

Introduction

I Financial Crisis ⇒ Crisis in macro theory

I Quick Response ⇒ Army of macro models now

I ...but are shocks and frictions consistent w/ financial flows?

I Here use financial flows to learn about:

1. shocks affecting bank activities2. frictions on banks

2 / 77

Introduction

I Financial Crisis ⇒ Crisis in macro theory

I Quick Response ⇒ Army of macro models now

I ...but are shocks and frictions consistent w/ financial flows?

I Here use financial flows to learn about:

1. shocks affecting bank activities2. frictions on banks

3 / 77

Introduction

I Financial Crisis ⇒ Crisis in macro theory

I Quick Response ⇒ Army of macro models now

I ...but are shocks and frictions consistent w/ financial flows?

I Here use financial flows to learn about:

1. shocks affecting bank activities2. frictions on banks

4 / 77

Frictions in Macro-Finance

I Constraints on external financing

I Market value constraints: banks can divert assetsI Agency conflicts or asymmetric informationI Gertler & Kiyotaki 2010, Jerman & Quadrini 2012, Christiano &

Ikeda 2013, Bigio 2014, Martinez-Miera & Suarez 2014

I Regulatory book value constraintsI Adrian & Shin 2011, Begenau 2015

I Costly asset/balance sheet adjustment

I Fire sales: e.g. Brunnermeier & Sannikov 2014I Debt overhang: e.g. Admati, DeMarzo, Hellwig & Pfleiderer 2014

5 / 77

Frictions in Macro-Finance

I Constraints on external financing

I Market value constraints: banks can divert assetsI Agency conflicts or asymmetric informationI Gertler & Kiyotaki 2010, Jerman & Quadrini 2012, Christiano &

Ikeda 2013, Bigio 2014, Martinez-Miera & Suarez 2014

I Regulatory book value constraintsI Adrian & Shin 2011, Begenau 2015

I Costly asset/balance sheet adjustment

I Fire sales: e.g. Brunnermeier & Sannikov 2014I Debt overhang: e.g. Admati, DeMarzo, Hellwig & Pfleiderer 2014

6 / 77

Frictions in Macro-Finance

I Constraints on external financing

I Market value constraints: banks can divert assetsI Agency conflicts or asymmetric informationI Gertler & Kiyotaki 2010, Jerman & Quadrini 2012, Christiano &

Ikeda 2013, Bigio 2014, Martinez-Miera & Suarez 2014

I Regulatory book value constraintsI Adrian & Shin 2011, Begenau 2015

I Costly asset/balance sheet adjustment

I Fire sales: e.g. Brunnermeier & Sannikov 2014I Debt overhang: e.g. Admati, DeMarzo, Hellwig & Pfleiderer 2014

7 / 77

Frictions in Macro-Finance

I Constraints on external financing

I Market value constraints: banks can divert assetsI Agency conflicts or asymmetric informationI Gertler & Kiyotaki 2010, Jerman & Quadrini 2012, Christiano &

Ikeda 2013, Bigio 2014, Martinez-Miera & Suarez 2014

I Regulatory book value constraintsI Adrian & Shin 2011, Begenau 2015

I Costly asset/balance sheet adjustment

I Fire sales: e.g. Brunnermeier & Sannikov 2014I Debt overhang: e.g. Admati, DeMarzo, Hellwig & Pfleiderer 2014

8 / 77

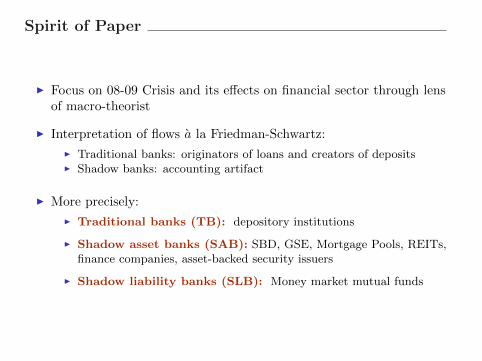

Spirit of Paper

I Focus on 08-09 Crisis and its effects on financial sector through lensof macro-theorist

I Interpretation of flows a la Friedman-Schwartz:

I Traditional banks: originators of loans and creators of depositsI Shadow banks: accounting artifact

I More precisely:

I Traditional banks (TB): depository institutions

I Shadow asset banks (SAB): SBD, GSE, Mortgage Pools, REITs,finance companies, asset-backed security issuers

I Shadow liability banks (SLB): Money market mutual funds

9 / 77

View

I Two key events (shocks):

1. Implosion of shadow banks & absorption by traditional banksI fire-sale shock

2. Equity losses on traditional banksI wealth shock

I Did events impair ability to issue loans and deposits?

I Question fundamental for macro-finance models

10 / 77

Answers depend on

1. Magnitude of shocks:I Magnitude of shadow-bank implosion?

I Magnitude of bank losses?

2. Frictions affecting traditional banking activities:

I Constraints on banks?

I Lessons: How to setup and calibrate models?

11 / 77

This paper

I (Tedious) accounting with theory in mind

I Steps:

1. Quantify flows from shadow to traditional banks (shock 1)2. Quantify traditional bank losses (shock 2)3. Analyze cross-sectional responses (constraints)

12 / 77

Step 1: Aggregate Financial Flows to QuantifyImplosion of Shadow Banks

13 / 77

Traditional Financial System

Reserves

Loans

Deposits

Equity

Bank

Goods

Equity

Borrower

Deposits

Loans

Equity

Saver

14 / 77

Modern Financial System: SB grew to 150% of TB

Reserves

Loans

Deposits

Equity

Bank

Goods

Equity

Borrower

Deposits

Loans

Equity

Saver

CP/Repo

ABS etc

Shadow liability

Shadow assetMMMF

MMMF

CP/RepoABS, MBS and Co

15 / 77

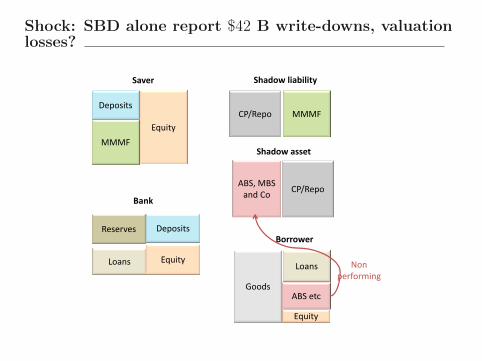

Shock: SBD alone report $42 B write-downs, valuationlosses?

Reserves

Loans

Deposits

Equity

Bank

Goods

Equity

Borrower

Deposits

Loans

Equity

Saver

CP/Repo

ABS etc

Shadow liability

Shadow assetMMMF

MMMF

CP/RepoABS, MBS and Co

Non performing

16 / 77

Unraveling between 2007q3-2009q2

Reserves

Loans

Deposits

Equity

Bank

Goods

Equity

Borrower

Deposits

Loans

Equity

Saver

CP/Repo

ABS etc

Shadow liability

Shadow asset

MMMF

MMMF

CP/RepoABS etc

Run on the REPOCollapse in ABCP

Run on MMMF

ABS etc

Repurchase of MBS by Banks

+Deposits

+Deposits

Shadow Banks: $541 billion net outflow$499 billion increase in traditional banking assets

17 / 77

Accounting Principles

I Where are these numbers coming from?

I Obviously, not-trivial

I Consolidate shadow bank balance sheets...

I Balance sheets shrinking, (by t-accounts) either:I Sales of assets and payout of liabilitiesI Write-down of assets, equity losses

I Assets sold, someone has to buy them...

I Assets lost, someone else has to lose also...

18 / 77

Data

I Most of the time focus on 2007-2011 quarterly

I Flow of Funds

I Bank level data on commercial banks and bank holding companies

I Data on security broker and dealers (FOCUS) filed by SEC

I Annual reports

19 / 77

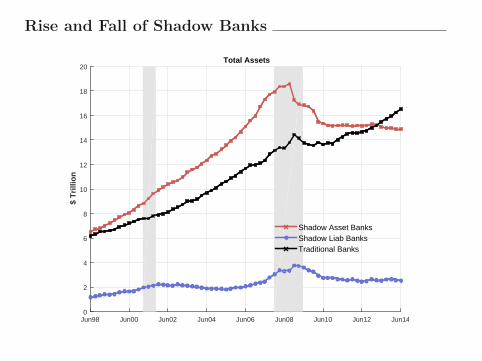

Rise and Fall of Shadow Banks

Jun98 Jun00 Jun02 Jun04 Jun06 Jun08 Jun10 Jun12 Jun14

$ T

rilli

on

0

2

4

6

8

10

12

14

16

18

20 Total Assets

Shadow Asset BanksShadow Liab BanksTraditional Banks

20 / 77

Assets

Total Assets

Mar07 Sep07 Mar08 Sep08 Mar09 Sep09 Mar10 Sep10 Mar11 Sep11

$ T

rilli

on

Ch

ang

e

-1.5

-1

-0.5

0

0.5

1

Shadow Asset BanksShadow Liab BanksTraditional Banks

21 / 77

Asset Flows: Diff 2007 Q3 and 2009 Q2

I SAB: −$879 billion

I SLB: $805 billion / Caveat: mixes prime with gov funds

I TB: $912 billion

I TARP: $426.4 billion of which $157.28 billion at least benefited TB

I What about redefinitions?

I Goldman Sachs and Morgan Stanley now traditional banks

I Holding companies with few deposits

I Broker dealer subsidiaries stay in SBD section of the FoF

I But GS and MS ∆ in SBD assets absorbed within holding company→adjust SAB asset for GS and MS

I Effect of Adjustment: SAB outflow −$1346 billion

I Shadow sector: net outflow of $541 billion

22 / 77

Upper bound of what TB did absorb?

I 2007q3-2009q2

I Adjusting TB inflows by CB in GS or MS holdings

I $912 billion increase in TB assets of which $413 GS and MS

I TB: absorbed at most $499 billion from SB

I What securities needed to be absorbed and from whom?

I SBD, borrowed securities Detail

I GSE & Mortgage-pools, mortgages Detail

I Asset-backed security issuers Detail

23 / 77

SBD Gains and Losses

I Annual reports from large SBD

I Reported writedowns $46.1 Billion

24 / 77

Back of the Envelope

I Shadow banking institution: net outflow of $541 billion

I Write-downs: $46.1B

I TB assets increased by $499B , only $495B could come from theshadow

I Puzzle $-4.1 billion?I ”Natural growth” in TB activity (TBD compute detrended flows)

I Gross ammounts (double counting)?

I Central bank

I Institutional Investors

I Realization of losses

I Book versus market value accounting

25 / 77

Step 2: Traditional Sector Equity Losses

26 / 77

Data

I This section...

I BHC level data from FR Y-9C and CRSP

I Aggregate series corrected by dropping new entrants (e.g. MS, GS,AXP, etc.)

27 / 77

Major Drivers of Losses and Profits

−60

−40

−20

020

40

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Net Income (−) Provision for Loan LossesNet Gains from Securities Trading Revenue

US

D B

illio

n

Major Drivers of Losses and Profits

28 / 77

Trading Revenue Components

−30

−20

−10

010

20

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Trading Revenue Interest Rate ExposuresCredit Exposures

US

D B

illio

n

Total, Interest Rate Exposures, and Credit ExposuresTrading Revenue:

29 / 77

Decomposition of Charge-Offs

010

2030

40

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Other IndividualLoansCandI RELoans

US

D B

illio

n

Net Charge−Offs

30 / 77

Within Real-Estate Charge-Offs

05

1015

20

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Farm+Foreign CommercialResidential Construction

US

D B

illio

n

Real Estate Net Charge−Offs

31 / 77

How did the losses show up in equity?

32 / 77

Book Equity vs. Market Capitalization

400

600

800

1000

1200

1400

US

D B

illio

n

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Equity Equity (Public BHCs)Market Capitalization

Book Equity and Market Capitalization of BHCs

33 / 77

Book vs. Market Equity of Big Four

010

020

030

00

100

200

300

2000q1 2004q1 2008q1 2012q1 2000q1 2004q1 2008q1 2012q1

Bank of America Citigroup

J.P. Morgan Wells Fargo

Equity Market Capitalization

US

D B

illio

n

34 / 77

Facts

I Two Notions...

I Losses Accumulated Over Recession:

1. Book Value Gains of 173 Billion

2. Market Value Losses of 656 Billion

3. Equity Issuances of 147 Billion

I Very little action in books...

35 / 77

Differences in Book and Market?

I From cross-section...more than only price of risk

I Bank incentives to delay acknowledging losses

I Regulation: better capital ratioI Corporate Control: better numbers to shareholders

I + flexibility to delay losses (Laux and Leuz JEP 2010)

36 / 77

Differences in Book and Market?

I From cross-section...more than only price of risk

I Bank incentives to delay acknowledging losses

I Regulation: better capital ratioI Corporate Control: better numbers to shareholders

I + flexibility to delay losses (Laux and Leuz JEP 2010)

37 / 77

Are books missing something?

I Test whether market cap is picking up important information

I log(MarketCap/BookEquity) = α+ βX + ε

I β reflects effect on market cap beyond effect on book equity

I Test regressors that should provide information about bank’s valueI Return on Book EquityI Return on Book Equity One Year LaterI Delinquent Loans to Book EquityI Total Dividends to Book Equity

I Compare results before (2006 Q1) and after crisis (2009 Q1)

38 / 77

Tobin’s Q and RoE (Cross-Sectional)

−3

−2

−1

01

2T

obin

’s Q

(Lo

gged

)

−.1 −.05 0 .05 .1Return on Book Equity (Trimmed)

2006 Q1 Fitted values2009 Q1 Fitted values

Tobin’s Q and Return on Book Equity

39 / 77

Tobin’s Q and RoE Next Year

−3

−2

−1

01

2T

obin

’s Q

(Lo

gged

)

−.1 −.05 0 .05 .1Return on Book Equity Next Year (Trimmed)

2006 Q1 Fitted values2009 Q1 Fitted values

Tobin’s Q and Return on Book Equity Next Year

40 / 77

Tobin’s Q and Delinquency Rates (Cross-Section)

−3

−2

−1

01

2T

obin

’s Q

(Lo

gged

)

0 .2 .4 .6 .8 1Delinquent Loans to Equity (Trimmed)

2006 Q1 Fitted values2009 Q1 Fitted values

Tobin’s Q and Delinquent Loans to Equity

41 / 77

Tobin’s Q and Dividend Rate (Cross-Section)

−3

−2

−1

01

2T

obin

’s Q

(Lo

gged

)

0 .01 .02 .03 .04 .05Total Dividend Rate (Trimmed)

2006 Q1 Fitted values2009 Q1 Fitted values

Tobin’s Q and Total Dividend Rate

42 / 77

Market data seems better

I Market data driven by:

I Profits & Future ProfitsI Loan DelinquencyI Dividends

I Oaxaca Decomposition: 43% to 45% of Drop in Logged Tobin’s Qcan be explained by these four regressors

I Takeaway: info in market cap not in books

43 / 77

Why are book/market values relevant?

I Market Cross-section: tells us who lost wealth

I Book Cross-section: who acknowledged losses

I ...relevant to learn bank constraints

44 / 77

Step 3: Constraints on Bank Activities

45 / 77

Traditional Sector

I ”Fire-Sale Shock” Outflow from shadow banking system totraditional banks: $495B

I ”Wealth Shock” Market value losses of 656 Billion (803 Billion Lostand 147 Billion New Equity)

I Effects on bank activities?

I Answer depends on constraints...(this section)

46 / 77

Illustrate different constraints

I Two period bank optimization model

I Prices and demands exogenous

I Choose flow: equity e, dividend div, riskless assets c, loans l, whetherto acknowledge losses

I Net-worth Nt, deposits Dt, loans Lt, riskless assets Ct

I Constraints:

I Regulatory

I Market value

I Assets: e.g. fire sale

I Liabilities: e.g. debt overhang

47 / 77

Bank Problem

Normalized by stock of loans L0

W(D0, ε0;F0, p, R

L)

= max{div,c,l,e}∈R+

4Q (e) + U (div) + . . .

+βE[max

(0, (1− ε1)

(RLl + 1

)+ C1 −D1

)]subject to

λ (l) l + pC1 −D1 = W1

and

W1 = pe− div −D0

48 / 77

Frictions

I Regulatory constraints (can choose to acknowledge losses)

L1 ≤κ

(1− κ)((C1 −D1) + max {ε0, 0})

I Liability constraints (downward stickiness)

D1 ≥ δD0

I Market-based constraints:

E[V

(NM

1

L1− ε1

)]≥ V

(ξλ (l)

RL

).

I Fire-sale function: λ (l)

I Equity adjustment costs: Q (e)

49 / 77

This Section

I Book-based constraints irrelevant:I Banks can “slow down” accounting

I Sticky assets and liabilities?

I Wealth shocks and “market-based” constraints:I Induce decrease in leverage

I Shocks ⇒ Wealth ⇓, Market-Leverage ⇑

50 / 77

Leverage

510

1520

2530

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Book Leverage Market Leverage

Leverage Ratios

51 / 77

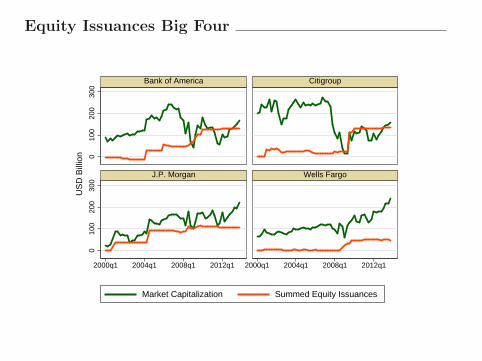

Frictions in Equity Issuance?

I Banks issued lots of equity, but not enough to undo the losses

I Anecdotal: hard to issue enough equity after hit by losses

52 / 77

Equity Issuances (Levels Since 2000 Q1)

050

010

0015

00U

SD

Bill

ion

2000q1 2002q1 2004q1 2006q1 2008q1 2010q1 2012q1 2014q1

Market Capitalization Summed Equity Issuances

Levels of Market Capitalization and Equity Issuances

53 / 77

Equity Issuances Big Four

010

020

030

00

100

200

300

2000q1 2004q1 2008q1 2012q1 2000q1 2004q1 2008q1 2012q1

Bank of America Citigroup

J.P. Morgan Wells Fargo

Market Capitalization Summed Equity Issuances

US

D B

illio

n

54 / 77

Irreversibility of Leverage in the Cross-Section

I Can banks de-lever in the cross-section?

I Estimate a dynamic market-equity elasticity of liabilities

I Idea:I Market-equity describes wealthI Poorer, more market-constrained banks should reduce liabilitiesI Did we see this?I Similarly: did we see a reduction in loans, liquid assets such as cash

and liquid liabilities such as repos?

55 / 77

Liabilities vs. Market Capitalization (Log Differences)

−1

01

2Li

abili

ties

(Log

Diff

eren

ces)

−4 −2 0 2Market Capitalization (Log Differences)

2006 Q1 Fitted values2009 Q1 Fitted values

Change in Logs Over Past Three YearsLiabilities and Market Capitalization

56 / 77

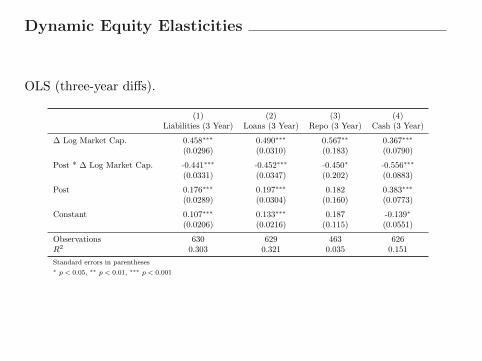

Dynamic Equity Elasticities

OLS (three-year diffs).

(1) (2) (3) (4)Liabilities (3 Year) Loans (3 Year) Repo (3 Year) Cash (3 Year)

∆ Log Market Cap. 0.458∗∗∗ 0.490∗∗∗ 0.567∗∗ 0.367∗∗∗

(0.0296) (0.0310) (0.183) (0.0790)

Post * ∆ Log Market Cap. -0.441∗∗∗ -0.452∗∗∗ -0.450∗ -0.556∗∗∗

(0.0331) (0.0347) (0.202) (0.0883)

Post 0.176∗∗∗ 0.197∗∗∗ 0.182 0.383∗∗∗

(0.0289) (0.0304) (0.160) (0.0773)

Constant 0.107∗∗∗ 0.133∗∗∗ 0.187 -0.139∗

(0.0206) (0.0216) (0.115) (0.0551)

Observations 630 629 463 626R2 0.303 0.321 0.035 0.151

Standard errors in parentheses∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

57 / 77

Discussion: illiquid liabilities a constraint?

I Illiquid liabilities: (can’t turn away depositors)

I Some highly liquid (e.g. Repo)

I If illiquid liabilities constraint:I Repo elasticity should be higher than non-Repo during the crisis

I Result: Repo elasticity also zeroI Constrained banks should be picking a corner solution

I But: Most banks have some liquid liabilities during the crisis

58 / 77

Composition of Liabilities

2000 2002 2004 2006 2008 2010 20120

20

40

60

80

100P

erce

ntBHC Liabilities Composition

DepositsFed Funds PurchasedTrading LiabilitiesOther

2000 2002 2004 2006 2008 2010 2012

6

7

8

9

10

Tril

lion

$

Liabilities

59 / 77

Deposits as a Share of Liabilities

01

23

45

Den

sity

0 .2 .4 .6 .8 1Deposits as a Share of Liabilities

2006 Q1 2009 Q1

Deposits as a Share of Liabilities

60 / 77

Deposits / Liabilities (Weighted by Liabilities)

01

23

4D

ensi

ty

0 .2 .4 .6 .8 1Deposits as a Share of Liabilities

2006 Q1 2009 Q1

Deposits as a Share of Liabilities (Weighted by Total Liabilities)

61 / 77

Repo as a Share of Liabilities

05

1015

20D

ensi

ty

0 .05 .1 .15 .2Repo as a Share of Liabilities (Trimmed)

2006 Q1 2009 Q1

Repo as a Share of Liabilities

62 / 77

Repo / Liabilities (Weighted by Liabilities)

02

46

8D

ensi

ty

0 .05 .1 .15 .2Repo as a Share of Liabilities (Trimmed)

2006 Q1 2009 Q1

Repo as a Share of Liabilities (Weighted by Total Liabilities)

63 / 77

Discussion: Sticky Leverage

I Hard to sell assets or unwillingness to sell assets?

I If illiquid assets constraint:I Poorer banks should have:I sold off liquid assets, reduce liquid liabilities

I Data: Dynamic equity elasticity of cashI negative: poorer banks increased reserves

I Caveats:I Bigger losses ⇒ liquidity demand (omitted variable bias)

I Alternative: dynamic debt-overhangI Shareholders: prefer maintain high leverage

64 / 77

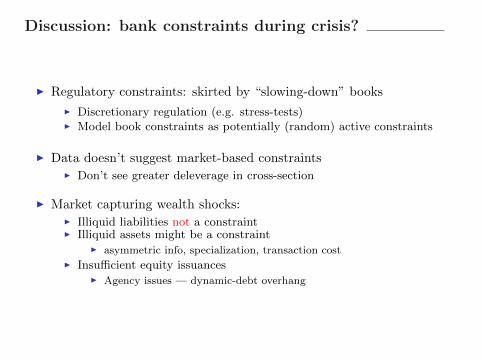

Discussion: bank constraints during crisis?

I Regulatory constraints: skirted by “slowing-down” books

I Discretionary regulation (e.g. stress-tests)I Model book constraints as potentially (random) active constraints

I Data doesn’t suggest market-based constraintsI Don’t see greater deleverage in cross-section

I Market capturing wealth shocks:I Illiquid liabilities not a constraintI Illiquid assets might be a constraint

I asymmetric info, specialization, transaction costI Insufficient equity issuances

I Agency issues — dynamic-debt overhang

65 / 77

Conclusion - Takeaway Insights

I Two numbers: measure size of implosion of shadow-banks and lossesto traditional banks.

I Modeling Constraints:

I Different class of constraints than pop in macro literatureI Wealth shocks: illiquid assets (+deposits) + agency frictions

66 / 77

End

67 / 77

Drivers of Market LossesDep variable: log market cap growth (2006 Q1 to 2009 Q1)Regressors: (2006 Q1).

(1) (2) (3) (4) (5) (6)

MBSMarketCap. 0.261∗∗

(0.0841)

LoansMarketCap. -0.0837∗ 0.158∗

(0.0323) (0.0751)

RELoansMarketCap. -0.137∗∗∗ -0.296∗∗∗

(0.0355) (0.0836)

CDSSoldMarketCap. 0.0196

(0.0856)

CDSNetMarketCap. 2.652

(2.789)

Constant -1.229∗∗∗ -0.740∗∗∗ -0.657∗∗∗ -0.810∗∗∗ -1.082∗∗∗ -1.078∗∗∗

(0.0677) (0.140) (0.120) (0.139) (0.0491) (0.0490)

Observations 306 306 306 306 306 306R2 0.031 0.022 0.047 0.061 0.000 0.003

Standard errors in parentheses∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

68 / 77

Security Brokers & Dealers: Total Assets

Jun90 Jun94 Jun98 Jun02 Jun06 Jun10 Jun13

US

$ T

rillio

n

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5 Total Financial Assets

69 / 77

Lion Share: Other Securities

Jun90 Jun94 Jun98 Jun02 Jun06 Jun10 Jun13

US

$ T

rillio

n

0

0.5

1

1.5

2

2.5

3

REPOTotal Government SecuritiesTotal Private SecuritiesOther Securities

70 / 77

Other Securities: Mostly Borrowed Securities

Jun90 Jun94 Jun98 Jun02 Jun06 Jun10 Jun13

US

$ T

rillio

n

0

0.5

1

1.5

Borrow SecuritiesUnidentified Misc

Net of receivables due and payables owed to other SBD, largely cashcollateral associated with securities lending transactions

71 / 77

Security Brokers & Dealers: Liabilities

Jun90 Jun94 Jun98 Jun02 Jun06 Jun10 Jun13

US

$ T

rillio

n

0

0.5

1

1.5

2

2.5

3

3.5

REPOCredit Market InstrumentsOther LiabilitySecurity Credit

back

72 / 77

Asset-backed Security Issuers: Assets

Jun91 Jun94 Jun97 Jun00 Jun03 Jun06 Jun09 Jun12

US

$ T

rillio

n

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5 Asset-backed Security Issuers - Assets

Government Sec. MortgagesConsumer CreditSec. Business Loans

73 / 77

Asset-backed Security Issuers: Liabilities

Jun91 Jun94 Jun97 Jun00 Jun03 Jun06 Jun09 Jun12

US

$ T

rillio

n

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5 Asset-backed Security Issuers - CP Liabilities

Commercial PaperCorporate Bonds

back

74 / 77

Agency-and GSE-backed mortgage pools: Assets

Jun99 Jun02 Jun05 Jun08 Jun11

US

$ T

rillio

n

0

1

2

3

4

5

6 #Mortgages

Home Multifamily residentialCommercialFarm

75 / 77

Government-Sponsored Enterprises (GSEs): Assets

Jun99 Jun02 Jun05 Jun08 Jun11

US

$ T

rillio

n

0

1

2

3

4

5

6

7 #Mortgages

ShortMortgagesCredit Mkt Instrument other than Mortgages

76 / 77

back

77 / 77