what can australia teach us about tax reform? by jon forman professor in residence irs office of...

TRANSCRIPT

What Can Australia Teach Us about Tax Reform?

by Jon FormanProfessor in Residence

IRS Office of Chief Counsel(Room 3501; 622-7639)

&Alfred P. Murrah Professor of Law

University of OklahomaNorman, Oklahoma

2

Overview

• In 2008, the Australian Government established Australia’s Future Tax System Review panel to examine Australia’s tax and transfer system and make recommendations to position Australia to deal with its demographic, social, economic and environmental challenges.– The Review Panel prepared detailed background reports,

received more than 1,500 formal submissions, and held a two-day conference in June 2009.

– In December 2009, the Review Panel delivered its final report to the Australian Government.

– In May 2010, the Government released the report, along with an initial response.

• Will Australia’s Parliament soon enact comprehensive tax reform?

Source: http://www.taxreview.treasury.gov.au/Content/Content.aspx?doc=html/home.htm

3

Australia’s Future Tax System Review

• Almost accidental birth– Not on the agenda when the Labor

Government was elected in 2008– At a 2008 summit on Australia’s future,

business leaders nominated tax reform as a priority area

• Government appointed the Secretary of the Treasury Ken Henry + four advisors– The Henry Review

4

5

Geography

• Area: 7.7 million sq. km. (3 million sq. mi.); about the size of the 48 contiguous United States.

• Cities (2008): Capital--Canberra (pop. 345,000). Other cities--Sydney (4.4 million), Melbourne (3.9 million), Brisbane (1.95 million), Perth (1.6 million), Adelaide (1.2 million), Darwin (120,000), Hobart (209,000).

• Terrain: Varied, but generally low-lying.• Climate: Relatively dry and subject to drought,

ranging from temperate in the south to tropical in the far north.

Source: U.S. Department of State, Background Note: Australia (2009),

http://www.state.gov/r/pa/ei/bgn/2698.htm.

6

People• Population (2009 est.): 21.8 million.• Annual population growth rate: 1.7%.• Ethnic groups: European 92%, Asian 6%, Aboriginal 2%.• Religions (2006): Catholic 26%, Anglican 19%, other Christian

19%, other non-Christian 1%, Buddhist 2.1%, Islam 1.7%, no religion 19%, and not stated 12%.

• Languages: English.• Education: Years compulsory--to age 16 in all states and

territories except New South Wales and the Northern Territory where it is 15, and Western Australia where it is 17. Literacy--over 99%.

• Health: Infant mortality rate--4.7/1,000. Life expectancy--males 78 yrs., females 83 yrs.

• Work force (10.8 million): Agriculture--3.3%; mining--1.5%; manufacturing--9.8%; retail trade--11.3%; public administration, defense, and safety--6%; construction--9.2%

8

Government

• Type: Constitutional monarchy: democratic, federal-state system.

• Constitution: Passed by the British Parliament on July 9, 1900.

• Independence (federation): January 1, 1901.• Branches:

– Executive--Queen Elizabeth II (head of state, represented by a governor general); the monarch appoints the governor general on the advice of the prime minister.

– Legislative--bicameral Parliament (76-member Senate, 150-member House of Representatives). The governor general appoints the prime minister (generally the leader of the party which holds the majority in the House of Representatives) and appoints ministers on the advice of the prime minister.

– Judicial--independent judiciary.

9

Government, cont.

• Administrative subdivisions: Six states and two territories.

• Political parties: Australian Labor, Liberal, the Greens, the Nationals, and Family First. The Australian Labor Party currently forms the government.

• Suffrage: Universal and compulsory 18 and over.• Central government budget (revenue): FY 2008-2009

A$295.9 billion (U.S. $236.7 billion); FY 2009-2010 A$290.6 billion (U.S. $232.5 billion).

• Defense: A$25 billion (U.S. $20 billion) or 2.20% of GDP for FY 2009-2010.

10

Principal Government Officials

• Governor General--Quentin BrycePrime Minister--Kevin RuddDeputy Prime Minister--Julia GillardTreasurer--Wayne SwanForeign Minister--Stephen SmithDefense Minister--John FaulknerTrade Minister--Simon CreanAmbassador to the United States--Dennis RichardsonAmbassador to the United Nations--Gary Quinlan

• Australia maintains an embassy in the United States at 1601 Massachusetts Avenue NW, Washington, DC 20036.

Australia's national gemstone is the opal.

11

Economy

• GDP (2009-2010 estimate): A$1.17 trillion (U.S. $893.6 billion).

• Inflation rate (year to March 2009): 2.5% per annum.• Reserve Bank official interest rate (May 2009): 3.00%.• Trade:

– Exports ($178.9 billion, 2008 estimate)--coal, iron ore, gold, meat, wool, alumina, wheat, machinery and transport equipment. Major markets--Japan, China, South Korea, U.S. ($10.7 billion), and New Zealand.

– Imports ($187.2 billion, 2008 estimate)--machinery and transport equipment, computers and office machines, telecommunication equipment and parts; crude oil and petroleum products. Major suppliers--China, United States ($23.96 billion), Japan, Singapore, and Germany.

• Exchange rate (2009): U.S. $1 = A$1.25

12

Economy, cont.

• Australia's economy is dominated by its services sector, yet it is the agricultural and mining sectors that account for the bulk of Australia's exports.

• Australia's comparative advantage in the export of primary products is a reflection of the natural wealth of the Australian continent and its small domestic market; 21 million people occupy a continent the size of the contiguous United States.

• Since the 1980s, Australia has undertaken significant structural reform of its economy and has transformed itself from an inward-looking, highly protected, and regulated marketplace to an open, internationally competitive, export-oriented economy.

13

Key economic reforms

• unilaterally reducing high tariffs and other protective barriers to free trade

• floating the Australian dollar• deregulating the financial services sector• reducing duplication and increasing efficiency between

the federal and state branches of government• privatizing many government-owned monopolies• reforming the taxation system, including introducing a

broad-based Goods and Services Tax (GST) and large reductions in income tax rates.

Echidna

14

Economy, cont.

• Australia enjoys a higher standard of living than any G7 country other than the United States.

• Australia's economic standing in the world is a result of a commitment to best-practice macroeconomic policy settings, including the delegation of the conduct of monetary policy to the independent Reserve Bank of Australia, and a broad acceptance of prudent fiscal policy where the government aims for fiscal balance over the economic cycle.

15Source: Congressional Budget Office, Fiscal Policy Choices, http://www.cbo.gov/ftpdocs/112xx/doc11277/CBOPresentation-NABE_3-8-10.pdf

16

Economy, cont.

• Over the last year, unemployment has risen to around 5.5% from 4.2%, and the labor market participation has remained at around 65%.

• Both the federal and state governments have recognized the need to invest heavily in water, transport, ports, telecommunications, and education infrastructure to expand Australia's supply capacity.

• A second significant issue is climate change. Prime Minister Kevin Rudd plans to introduce a domestic carbon trading system by 2011.

Source: U.S. Department of State, Background Note: Australia (2009),

http://www.state.gov/r/pa/ei/bgn/2698.htm.

Platypus

17

Political Conditions

• A written Constitution

• Parliamentary Government

• Voting– In 1855, Victoria introduced the secret ballot.– For all citizens over the age of 18 it is

compulsory to vote in the election of both federal and state governments, and failure to do so may result in a fine or prosecution.

Australian Government, Australia’s System of Government, http://www.dfat.gov.au/facts/sys_gov.html

18

Political Conditions• Three political parties

– The Liberal Party nominally representing urban business interests, and its smaller coalition partner

– The Nationals nominally representing rural interests are more conservative

– The Labor Party nominally represents workers, trade unions, and left-of-center groups – really social democrats

• Labor, under the leadership of Kevin Rudd, defeated the Liberal/National coalition, led by then-Prime Minister John Howard, in the November 24, 2007 election.– House: Labor holds 83 seats, against 64 for the Liberal/National

coalition, and 3 independents.– Senate: Liberal/National Coalition holds 37 seats, against 32

seats for Labor, 5 seats for the Greens, 1 for Family First, and 1 independent.

Source: U.S. Department of State, Background Note: Australia (2009),

http://www.state.gov/r/pa/ei/bgn/2698.htm.

19

Past Political “Achievements”

• A Universal Pension System

• Goods and Services Taxation

Australia's national floral emblem is the golden wattle.

20

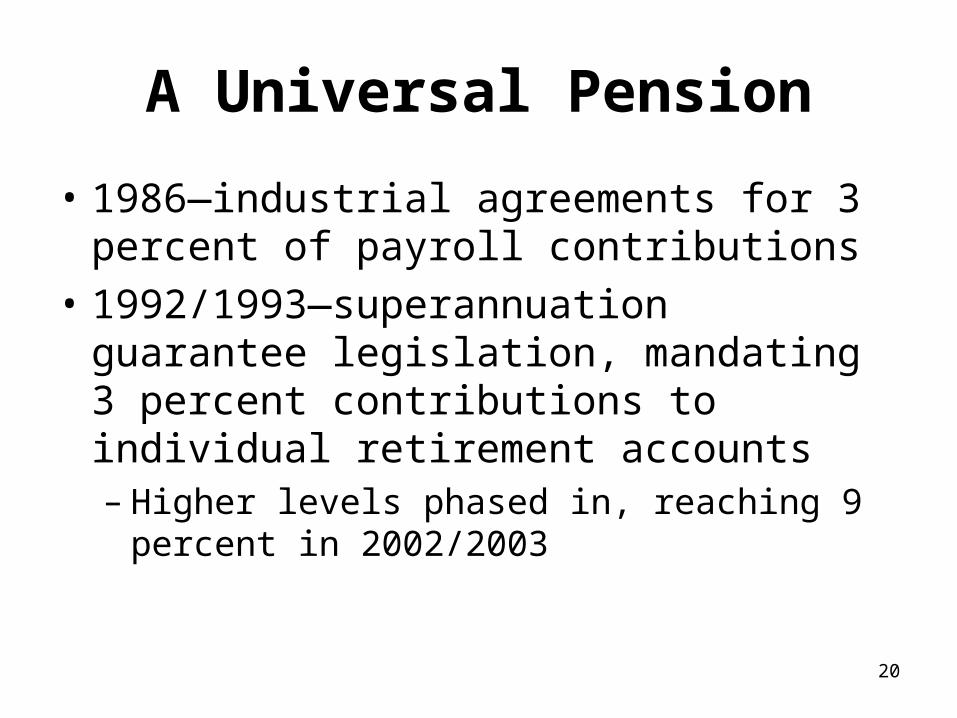

A Universal Pension

• 1986—industrial agreements for 3 percent of payroll contributions

• 1992/1993—superannuation guarantee legislation, mandating 3 percent contributions to individual retirement accounts– Higher levels phased in, reaching 9 percent in

2002/2003

21

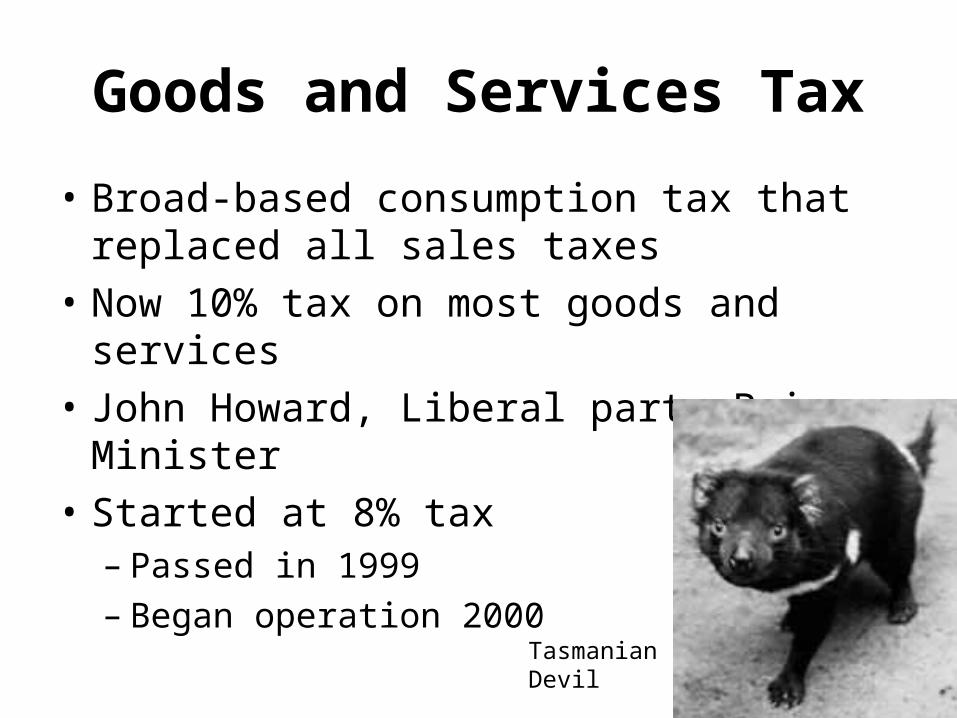

Goods and Services Tax

• Broad-based consumption tax that replaced all sales taxes

• Now 10% tax on most goods and services

• John Howard, Liberal party Prime Minister

• Started at 8% tax– Passed in 1999– Began operation 2000

Tasmanian Devil

22

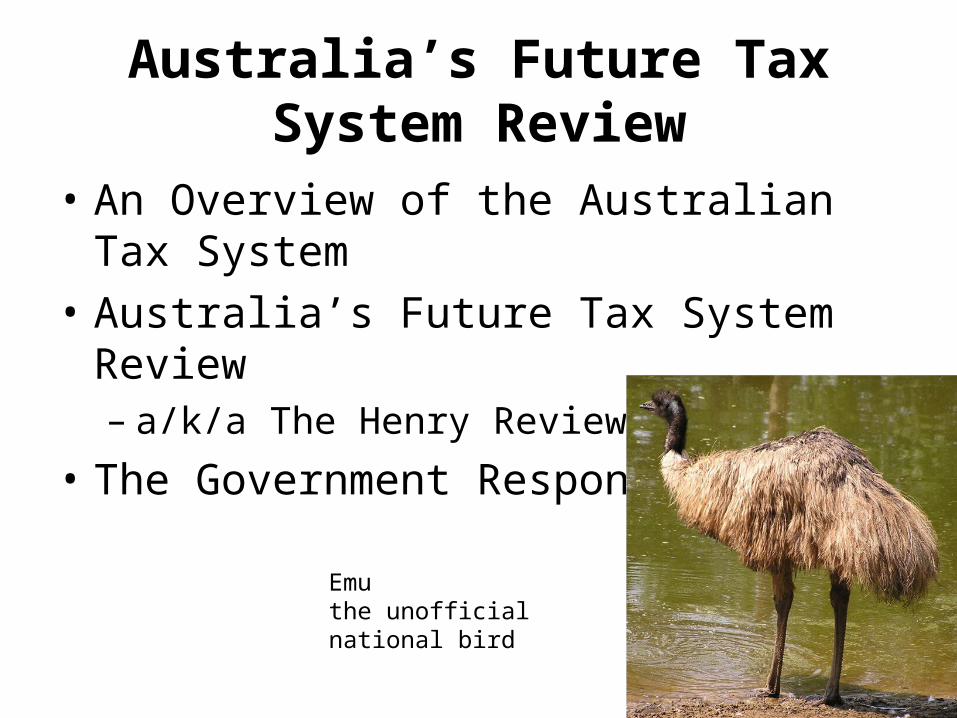

Australia’s Future Tax System Review

• An Overview of the Australian Tax System

• Australia’s Future Tax System Review– a/k/a The Henry Review

• The Government Response

Emuthe unofficial national bird

23

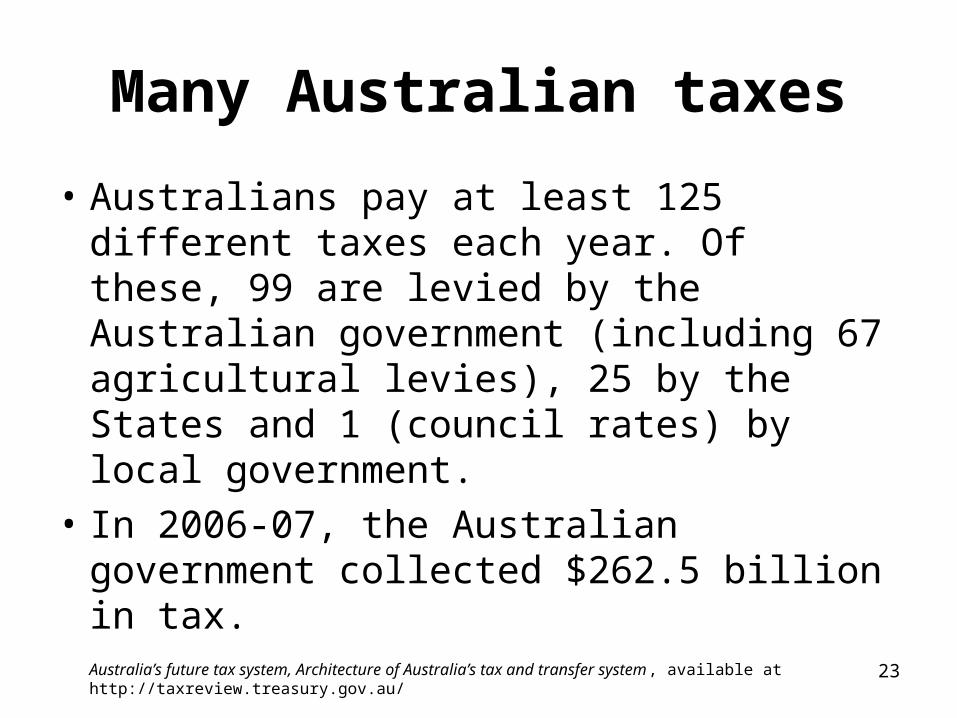

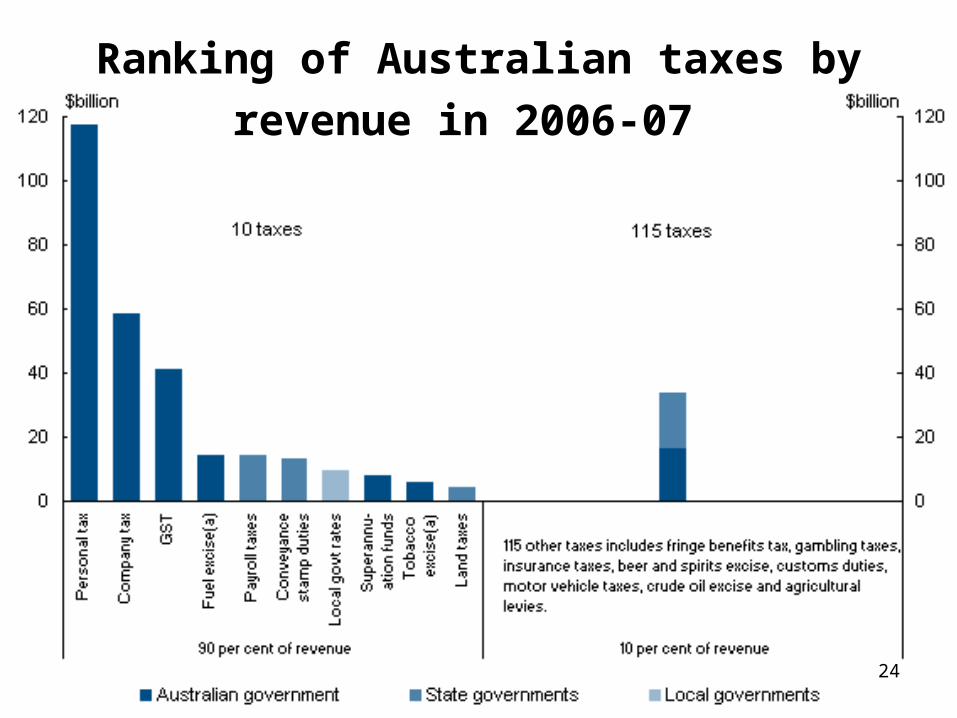

Many Australian taxes

• Australians pay at least 125 different taxes each year. Of these, 99 are levied by the Australian government (including 67 agricultural levies), 25 by the States and 1 (council rates) by local government.

• In 2006‑07, the Australian government collected $262.5 billion in tax.

Australia’s future tax system, Architecture of Australia’s tax and transfer system, available at http://taxreview.treasury.gov.au/

24

Ranking of Australian taxes by revenue

in 2006‑07

25

The Australian Tax System

• Taxes on labor provided 39% of total tax revenue– personal income tax on labour income – 31%– payroll tax – 5%– taxes on fringe benefits and superannuation contributions –3%

• Taxes on capital provided 34%– 20% from corporate tax (including petroleum resource rent tax, crude oil

excise and taxes on the earnings of superannuation funds)– 9% from annual taxes on real property and conveyancing and other

stamp duties, in roughly equal proportions– taxes on individuals' capital income, such as interest, net rental and

business income, capital gains and dividends, and some state government taxes on financial and capital transactions – 5%

• Taxes on consumption contributed 27%.– GST contributing around half of total consumption tax revenue– excises contributed around 7%– while a range of state taxes – including on motor vehicles, gambling,

and insurance – 7%Australia’s future tax system Consultation Paper, available at http://taxreview.treasury.gov.au/

26

Composition of Tax Revenue, 2007-2008

27

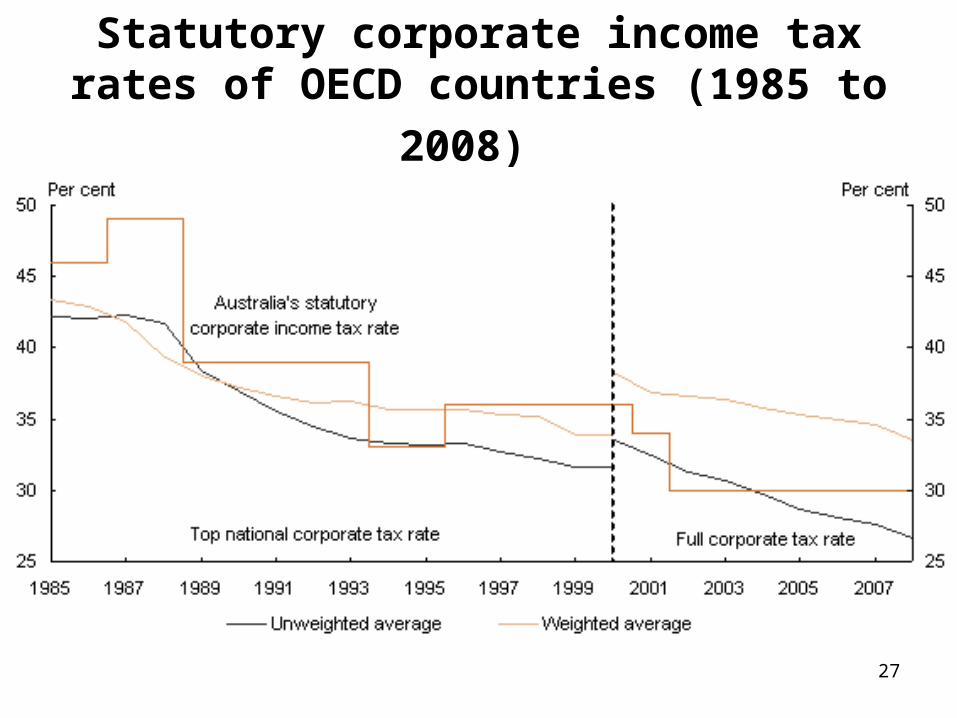

Statutory corporate income tax rates of

OECD countries (1985 to 2008)

28

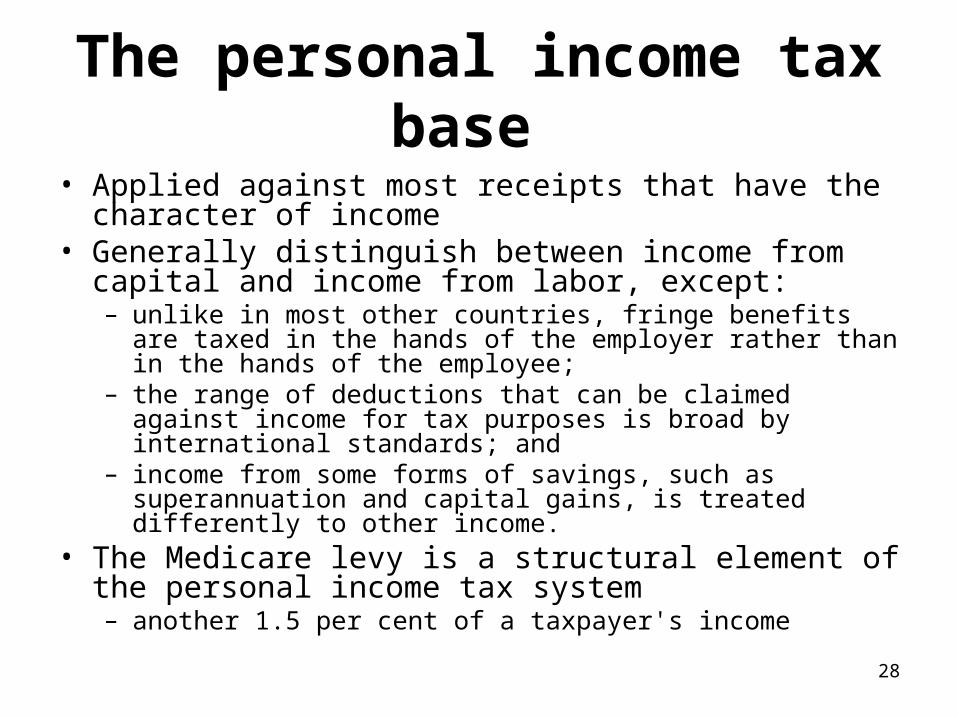

The personal income tax base

• Applied against most receipts that have the character of income

• Generally distinguish between income from capital and income from labor, except:– unlike in most other countries, fringe benefits are taxed in the

hands of the employer rather than in the hands of the employee; – the range of deductions that can be claimed against income for

tax purposes is broad by international standards; and – income from some forms of savings, such as superannuation

and capital gains, is treated differently to other income.• The Medicare levy is a structural element of the personal

income tax system– another 1.5 per cent of a taxpayer's income

29

Personal tax rates and progressivity

• Australia has a progressive personal income tax system.

• The personal rate scale has 4 personal income tax rates, as well as a zero rate of tax below the tax-free threshold.

• In addition, other elements such as the low income tax offset (LITO) alter the effective rate of taxation.

30

Marginal rates including the low income tax offset, by taxable income (2008-09)

31

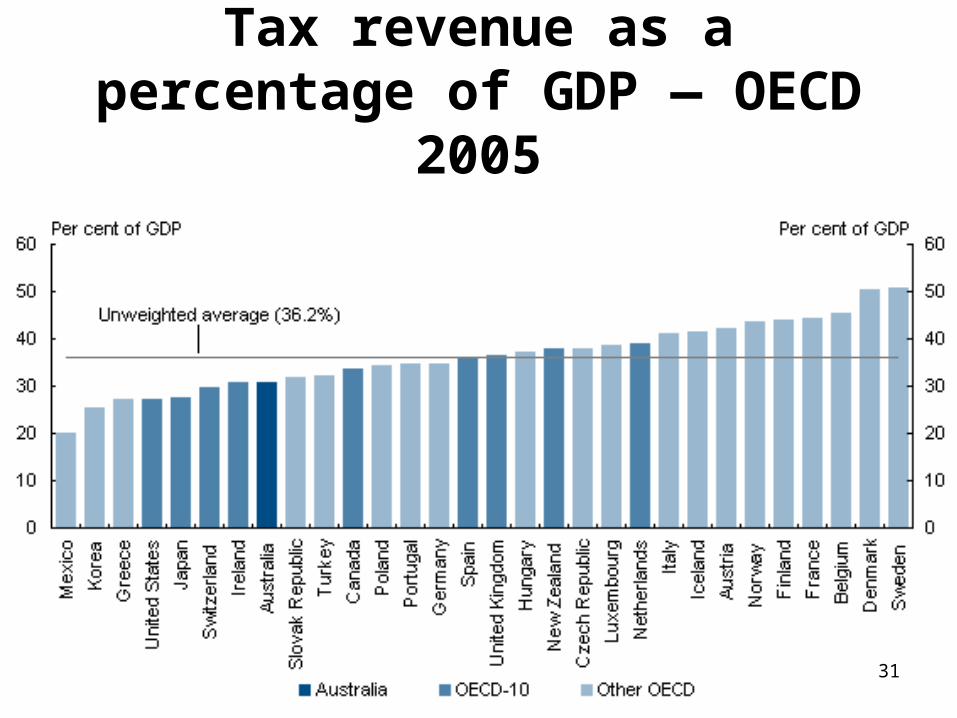

Tax revenue as a percentage of GDP — OECD 2005

32

Australia’s transfer system

• The transfer system is the means by which the Australian Government redistributes around $70 billion of income each year. While much of this redistribution is targeted to those on low incomes, some transfers assist middle and higher income individuals and families. The transfer system has evolved over time, with a range of provisions that are complex for recipients.

• Key ongoing forms of family assistance include Family Tax Benefit (FTB) Parts A and B, Child Care Benefit and the Child Care Tax Rebate.

33

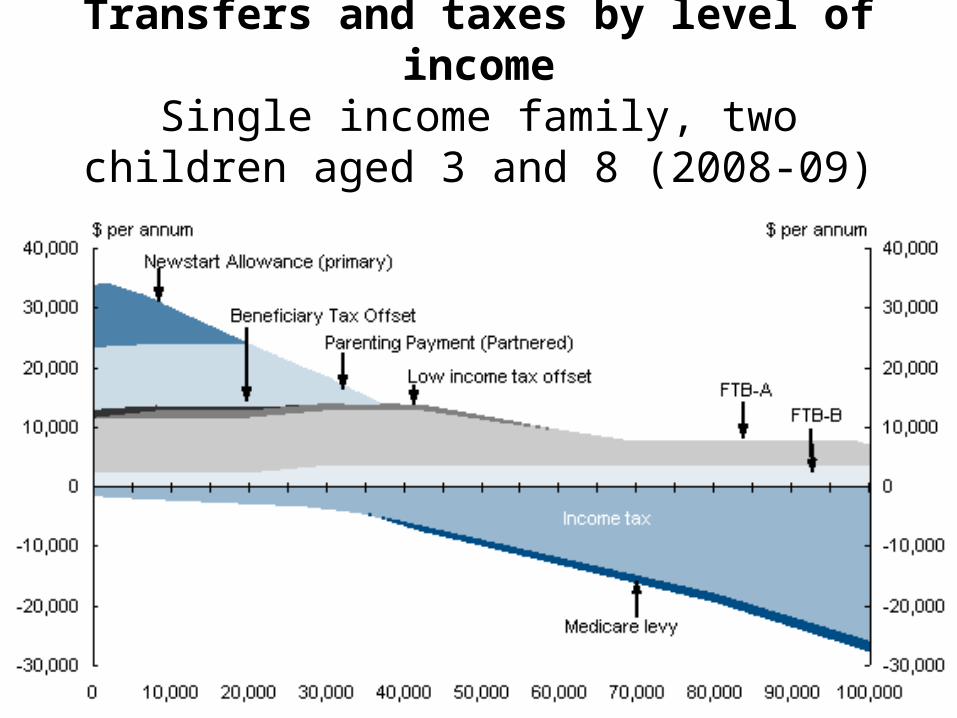

Transfers and taxes by level of incomeSingle income family, two children aged 3

and 8 (2008-09)

34

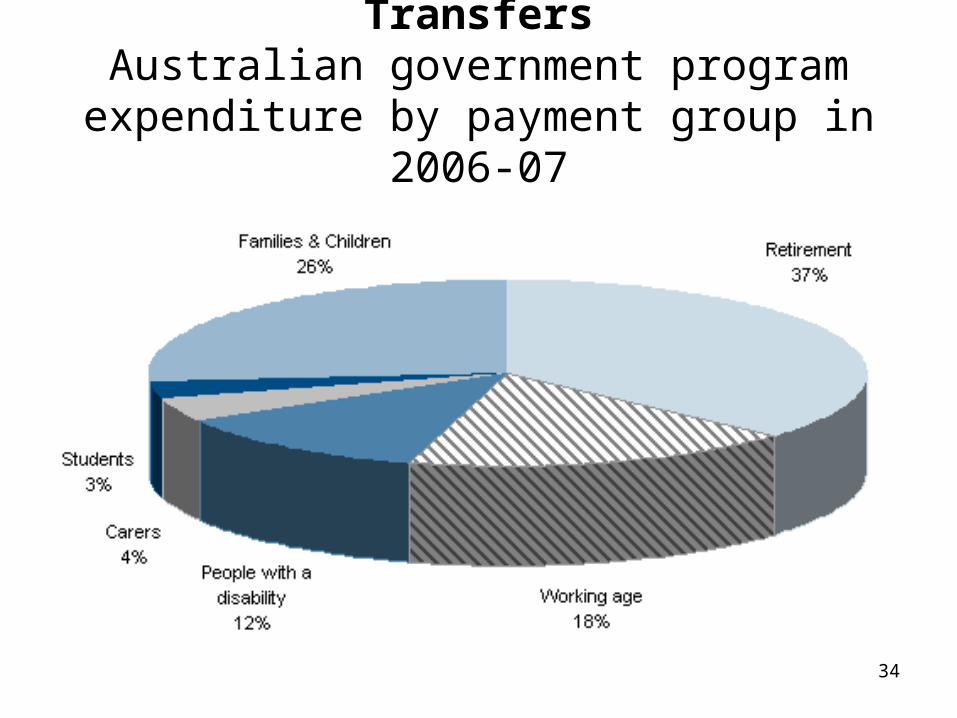

TransfersAustralian government program expenditure

by payment group in 2006‑07

35

The Henry Review

• The Australia's Future Tax System Review was established by the Rudd Government in 2008 to examine Australia's tax and transfer system, including state taxes, and make recommendations to position Australia to deal with the demographic, social, economic and environmental challenges of the 21st century.

• The review panel comprised:– Dr Ken Henry AC, Chair (Secretary to the Treasury)– Dr Jeff Harmer (Secretary of FaHCSIA)– Professor John Piggott (University of New South Wales)– Mrs Heather Ridout (Australian Industry Group), and– Mr Greg Smith (Adjunct Professor, Australian Catholic

University)

36Major Mitchell's Cockatoo

Blue Winged Kookaburra

Sulphur-crested Cockatoo

37

The Henry Review, cont.

• In December 2010, the panel delivered its final report to the Government.

• On Sunday, May 2, 2010, at 2:30 p.m.– The Government released the Henry Review– And the Government’s Initial Response

SydneyOperaHouse

38

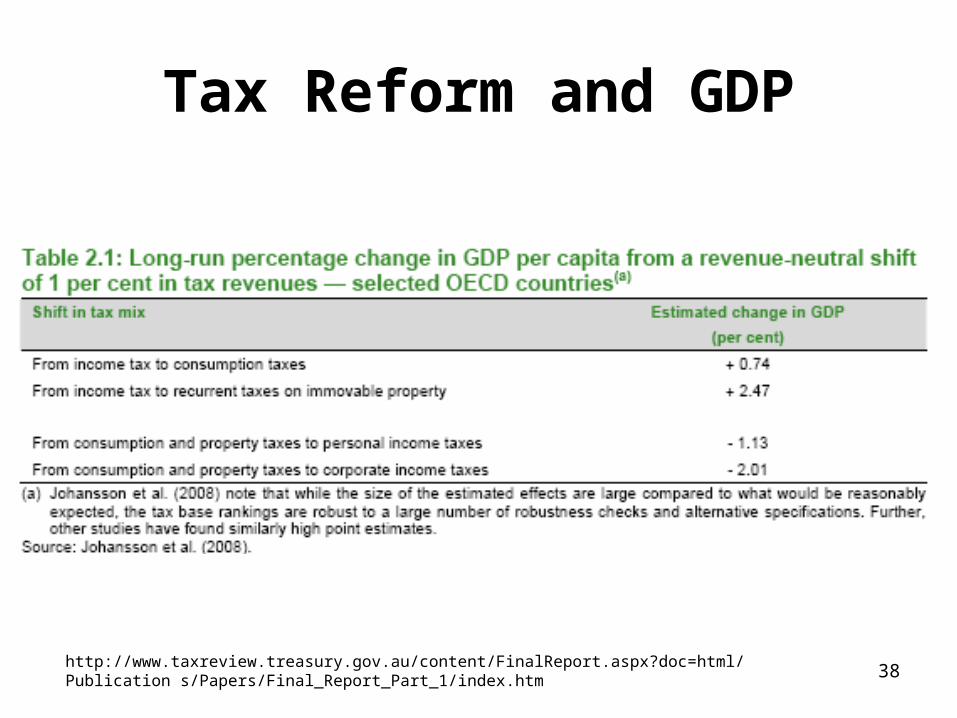

Tax Reform and GDP

http://www.taxreview.treasury.gov.au/content/FinalReport.aspx?doc=html/Publication s/Papers/Final_Report_Part_1/index.htm

39

Henry Review Recommendations

• Recommendation 1: Revenue raising should be concentrated on four robust and efficient broad-based taxes:– personal income, assessed on a more comprehensive

basis;– business income, designed to support economic

growth;– rents on natural resources and land; and– private consumption.

• Additional specific taxes should exist only where they improve social outcomes or market efficiency through better price signals.

40

Personal Taxation

• Recommendation 2: Progressivity in the tax and transfer system should be delivered through the personal income tax rates scale and transfer payments. A high tax-free threshold with a constant marginal rate for most people should be introduced to provide greater transparency and simplicity.

• Recommendation 6: To remove complexity and ensure government assistance is properly targeted, concessional offsets should be removed, rationalised, or replaced by outlays.

41

Company and other investment taxes

• Recommendation 26: The structure of the company income tax system should be retained in its present form, at least in the short to medium term. – A business level expenditure tax could suit Australia in the future

and is worthy of further consideration and public debate. It is possible that other economies will move towards such systems over coming years and it could be in Australia’s interest to join this trend at an early stage.

• Recommendation 27: The company income tax rate should be reduced to 25 per cent over the short to medium term with the timing subject to economic and fiscal circumstances. Improved arrangements for charging for the use of non-renewable resources should be introduced at the same time.

42

43

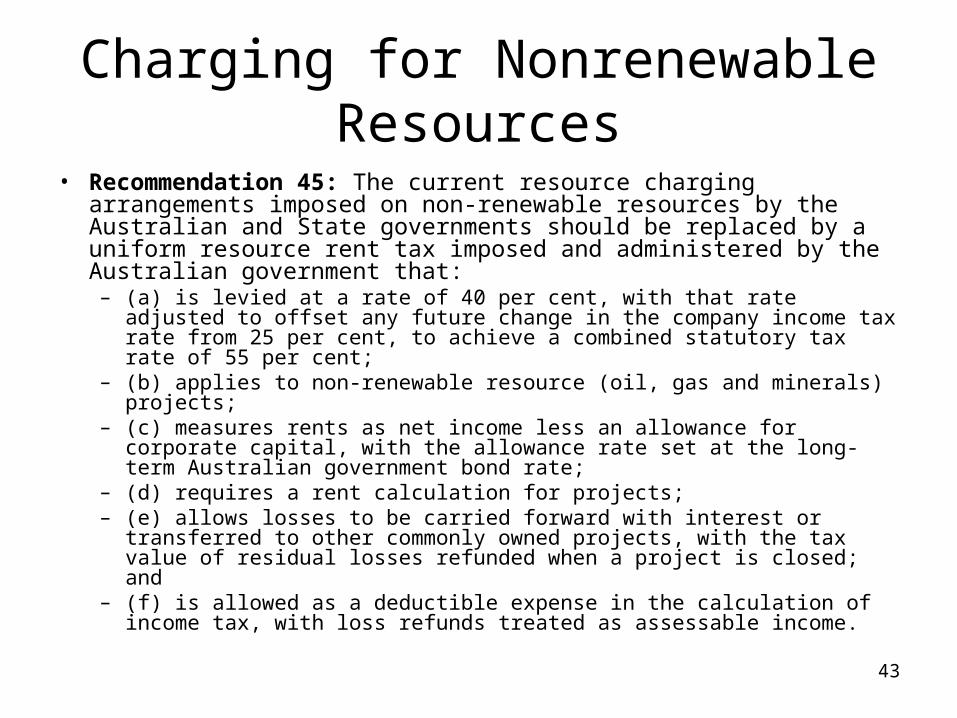

Charging for Nonrenewable Resources

• Recommendation 45: The current resource charging arrangements imposed on non-renewable resources by the Australian and State governments should be replaced by a uniform resource rent tax imposed and administered by the Australian government that:– (a) is levied at a rate of 40 per cent, with that rate adjusted to offset any

future change in the company income tax rate from 25 per cent, to achieve a combined statutory tax rate of 55 per cent;

– (b) applies to non-renewable resource (oil, gas and minerals) projects;– (c) measures rents as net income less an allowance for corporate

capital, with the allowance rate set at the long-term Australian government bond rate;

– (d) requires a rent calculation for projects;– (e) allows losses to be carried forward with interest or transferred to

other commonly owned projects, with the tax value of residual losses refunded when a project is closed; and

– (f) is allowed as a deductible expense in the calculation of income tax, with loss refunds treated as assessable income.

44

Taxing consumption

• Recommendation 55: Over time, a broad-based cash flow tax — applied on a destination basis — could be used to finance the abolition of other taxes, including payroll tax and inefficient State consumption taxes, such as insurance taxes. Such a tax would also provide a sustainable revenue base to finance future spending needs.

45

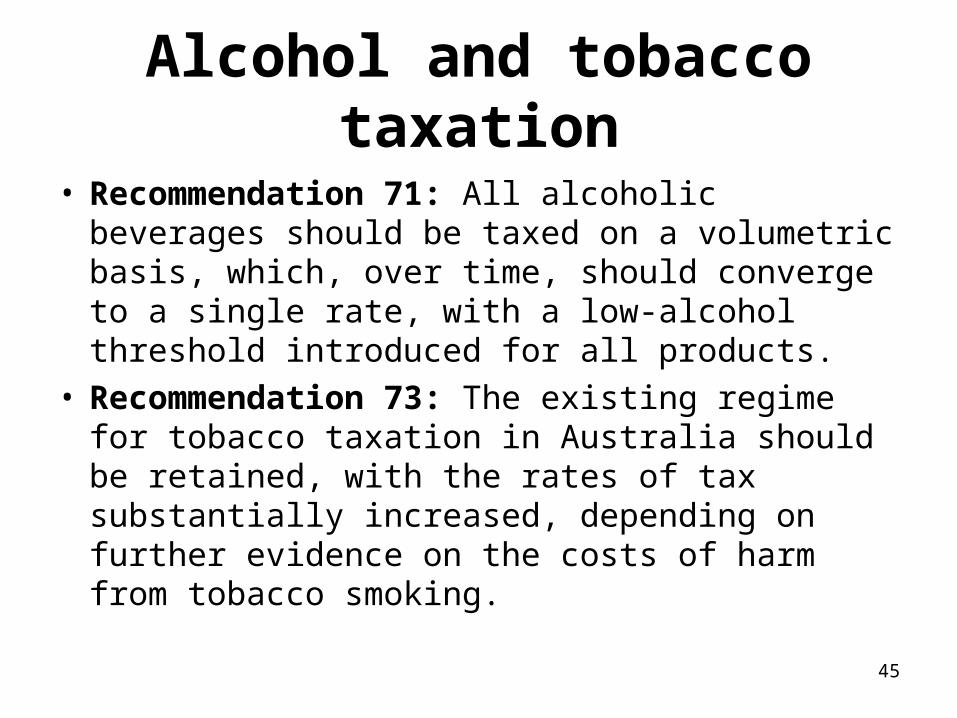

Alcohol and tobacco taxation

• Recommendation 71: All alcoholic beverages should be taxed on a volumetric basis, which, over time, should converge to a single rate, with a low-alcohol threshold introduced for all products.

• Recommendation 73: The existing regime for tobacco taxation in Australia should be retained, with the rates of tax substantially increased, depending on further evidence on the costs of harm from tobacco smoking.

46

47

Rationalising other taxes

• Recommendation 79: All specific taxes on insurance products, including the fire services levy, should be abolished. Insurance products should be treated like most other services consumed within Australia and be subject to only one broad-based tax on consumption.

• Recommendation 80: The luxury car tax should be abolished.

• Recommendation 81: Governments should undertake a systematic review of existing and potential user charges and minor taxes against the principles set out in this report. This should be coordinated with the introduction of the system wide Tax and Transfer Analysis Statement proposed in Recommendation 132.

48

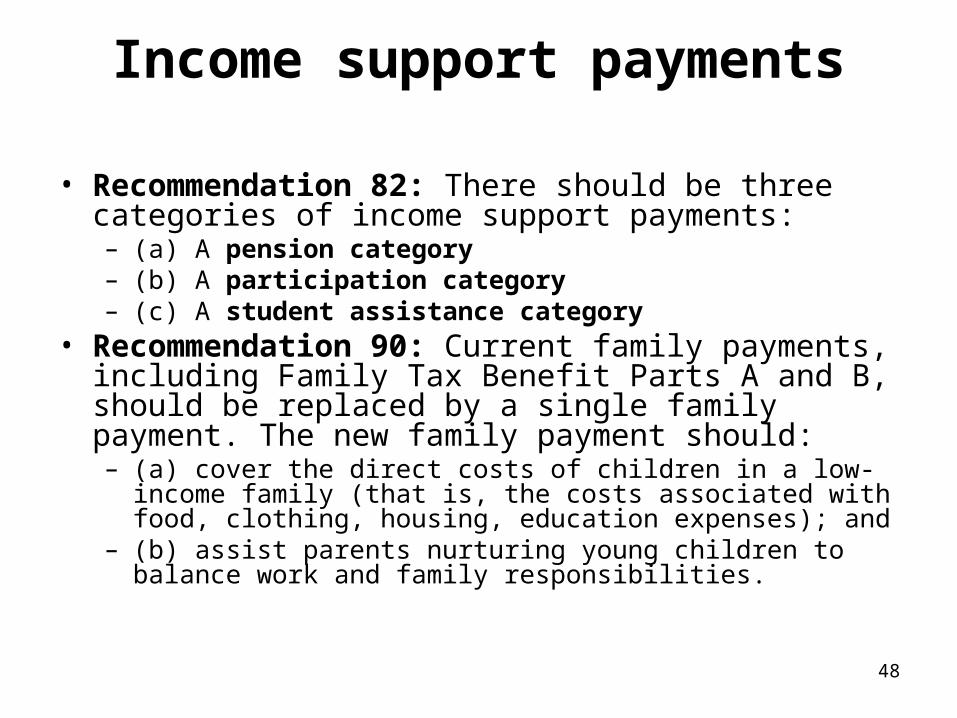

Income support payments

• Recommendation 82: There should be three categories of income support payments:– (a) A pension category– (b) A participation category – (c) A student assistance category

• Recommendation 90: Current family payments, including Family Tax Benefit Parts A and B, should be replaced by a single family payment. The new family payment should:– (a) cover the direct costs of children in a low-income family (that

is, the costs associated with food, clothing, housing, education expenses); and

– (b) assist parents nurturing young children to balance work and family responsibilities.

49

State tax reform

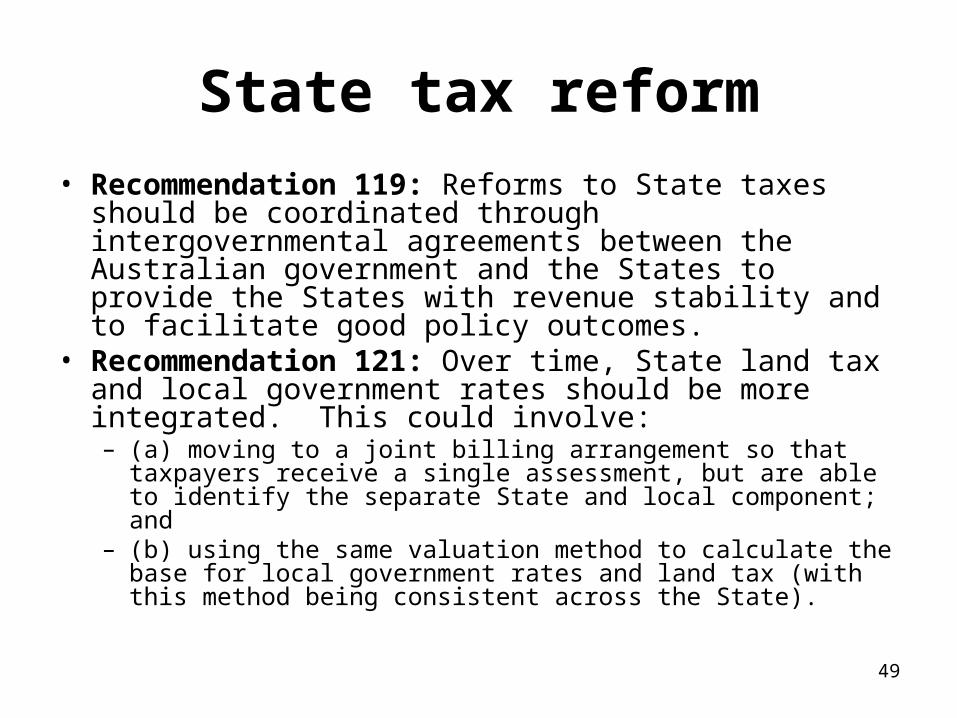

• Recommendation 119: Reforms to State taxes should be coordinated through intergovernmental agreements between the Australian government and the States to provide the States with revenue stability and to facilitate good policy outcomes.

• Recommendation 121: Over time, State land tax and local government rates should be more integrated. This could involve:– (a) moving to a joint billing arrangement so that taxpayers

receive a single assessment, but are able to identify the separate State and local component; and

– (b) using the same valuation method to calculate the base for local government rates and land tax (with this method being consistent across the State).

50

The Government Response

• Released on Sunday, May 2, 2010, at 2:30 p.m.• This is a long term plan to apply a Resource Super

Profits tax to the profits earned from resources that are owned by all Australians, and use it to:– generate more superannuation savings for working families;– lower tax for all companies, especially small businesses; and– invest in our future infrastructure needs, particularly for mining

states.

• The Government’s tax reform agenda is fiscally responsible.

http://www.futuretax.gov.au/pages/default.aspx#newsDocs-factSheets; http://www.deewr.gov.au/Department/Documents/Files/Final%20Tax%20policy%20Statement.pdf; http://www.deewr.gov.au/Department/Documents/Files/100502%20stronger%20fairer%20simpler%20a%20tax%20plan%20for%20our%20future.pdf

51

FISCALLY RESPONSIBLE TAX REFORM

• This package is fully funded over the forward estimates and in the medium term.

• The reform agenda fully meets the Government’s fiscal strategy, including the commitment to keep the tax to GDP ratio on average below the 2007‑08 level of 23.6 per cent.– And it strengthens the economy, generating a growth

dividend that will be returned back to the budget to strengthen the fiscal position.

http://www.deewr.gov.au/Department/Documents/Files/11_Fact_sheet_Fiscally_responsible_tax_reform.pdf

52

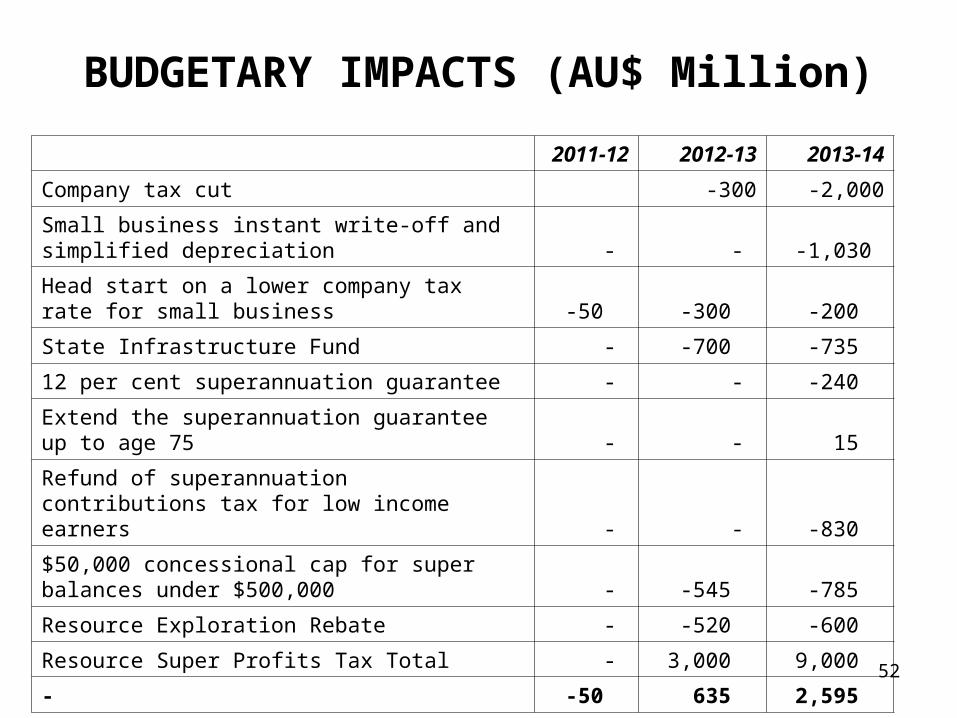

BUDGETARY IMPACTS (AU$ Million)

2011-12 2012-13 2013-14

Company tax cut ‑300 ‑2,000

Small business instant write‑off and simplified depreciation ‑ ‑ ‑1,030

Head start on a lower company tax rate for small business ‑50 ‑300 ‑200

State Infrastructure Fund ‑ ‑700 ‑735

12 per cent superannuation guarantee ‑ ‑ ‑240

Extend the superannuation guarantee up to age 75 ‑ ‑ 15

Refund of superannuation contributions tax for low income earners ‑ ‑ ‑830

$50,000 concessional cap for super balances under $500,000 ‑ ‑545 ‑785

Resource Exploration Rebate ‑ ‑520 ‑600

Resource Super Profits Tax Total ‑ 3,000 9,000

‑ ‑50 635 2,595

53

A 28% Corporate Tax Rate

• A LOWER COMPANY TAX RATE– The Government will cut the company tax rate to 29 per cent

from the 2013-14 income year and then to 28 per cent from the 2014-15 income year.

– will move Australia towards achieving an internationally competitive tax rate.

– Australia will become an even more attractive place to invest.– is expected to increase long run GDP by 0.4 per cent (excluding

the gains from refunding royalties).

• A HEAD START FOR SMALL BUSINESS– This measure reduces the company tax rate to 28 per cent for

eligible small business companies from the 2012-13 income year, one year earlier than the start of the general reduction in the company tax rate.

54

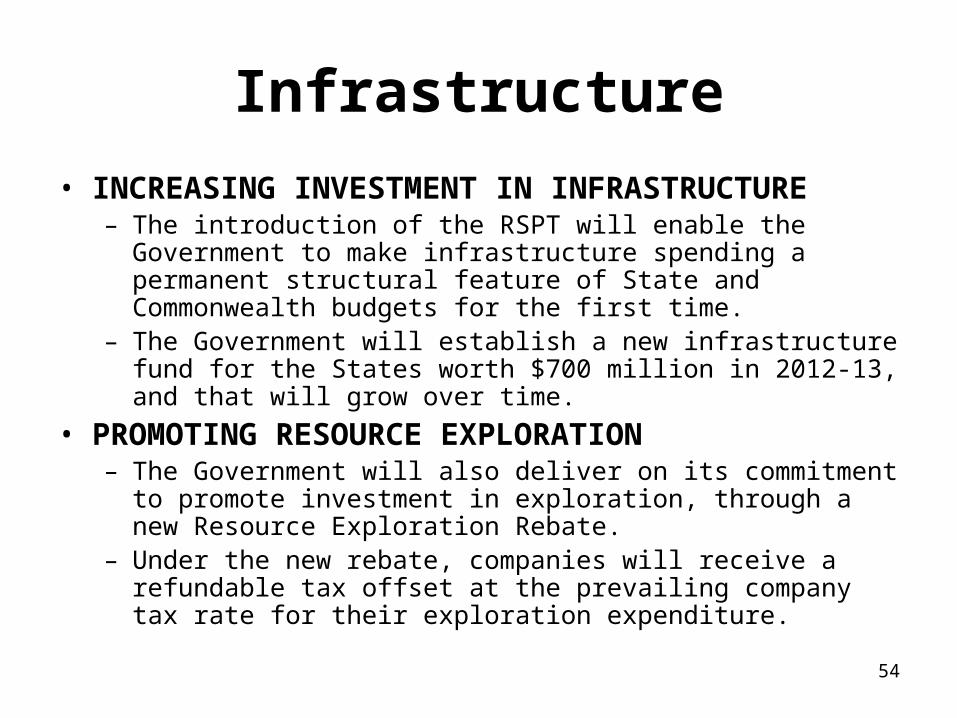

Infrastructure

• INCREASING INVESTMENT IN INFRASTRUCTURE– The introduction of the RSPT will enable the Government to

make infrastructure spending a permanent structural feature of State and Commonwealth budgets for the first time.

– The Government will establish a new infrastructure fund for the States worth $700 million in 2012-13, and that will grow over time.

• PROMOTING RESOURCE EXPLORATION– The Government will also deliver on its commitment to promote

investment in exploration, through a new Resource Exploration Rebate.

– Under the new rebate, companies will receive a refundable tax offset at the prevailing company tax rate for their exploration expenditure.

55

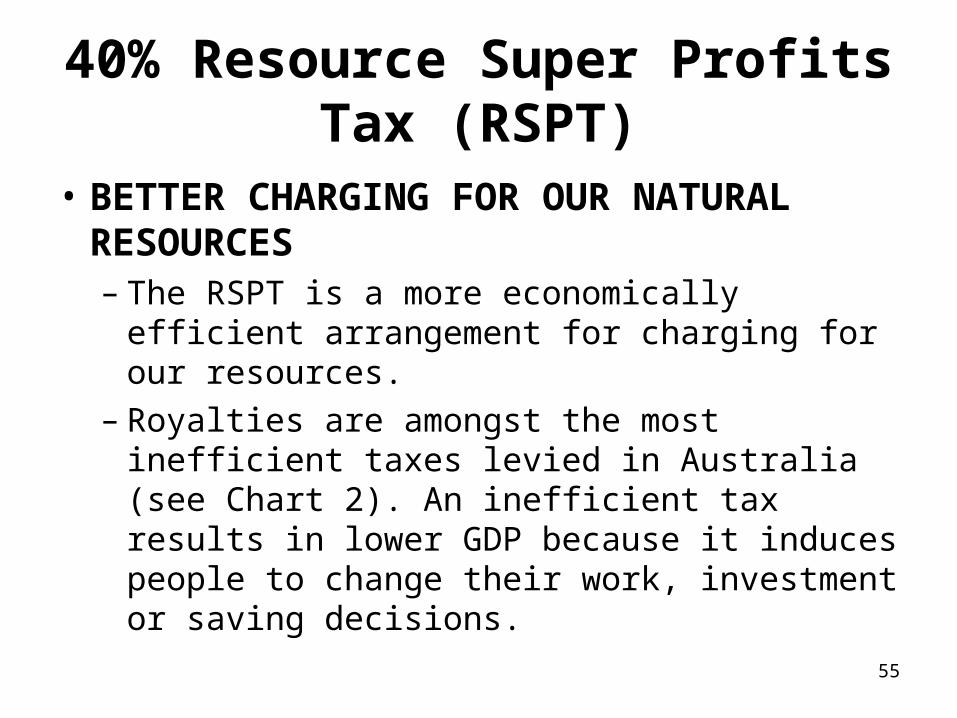

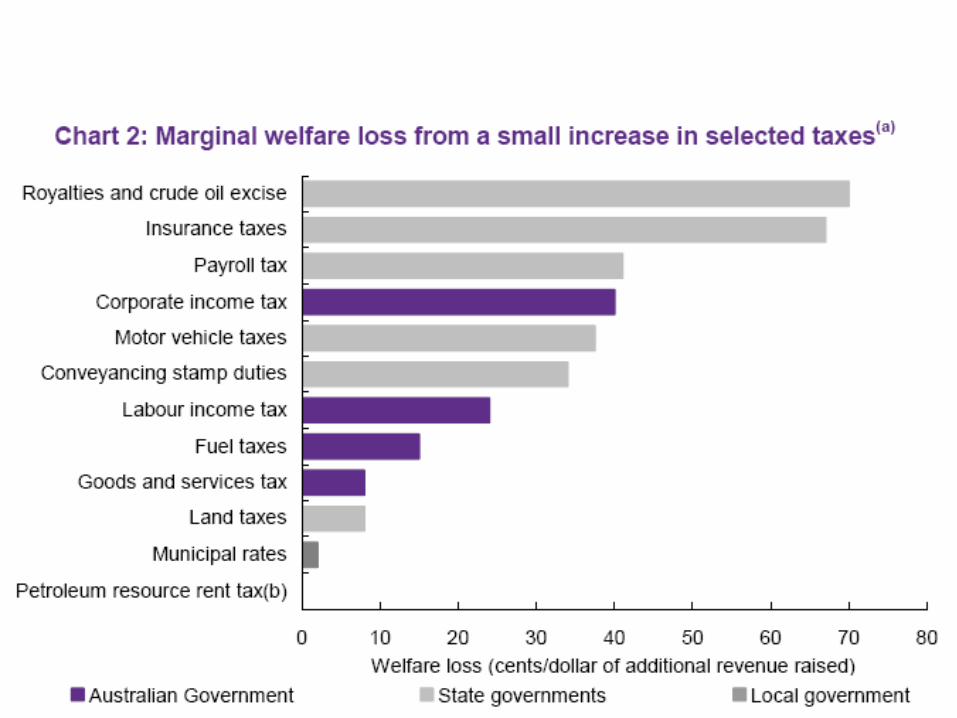

40% Resource Super Profits Tax (RSPT)

• BETTER CHARGING FOR OUR NATURAL RESOURCES– The RSPT is a more economically efficient

arrangement for charging for our resources.– Royalties are amongst the most inefficient

taxes levied in Australia (see Chart 2). An inefficient tax results in lower GDP because it induces people to change their work, investment or saving decisions.

56

57

40% Resource Super Profits Tax

• The RSPT is at the centre of the Government’s tax reform agenda. This tax is designed to tax resource projects on the basis of profits rather than production, but also to ensure that Australia gets a fair return from our natural resource wealth.

• The effective resource charge (charges as a percentage of super profits earned) has almost halved from an average of around 34 per cent over the first half of this decade to less than 14 per cent in 2008-09.– Existing resource taxes and royalties have only captured a small

share of the increased value of the nation’s resource deposits. Resource profits were over $80 billion higher in 2008-09 than in 1999-00, but governments only collected an additional $9 billion through resource charges (see Chart 3).

http://www.deewr.gov.au/Department/Documents/Files/100502%20stronger%20fairer%20simpler%20a%20tax%20plan%20for%20our%20future.pdf

58

59

40% Resource Super Profits Tax

• The Australian Government will introduce a 40 per cent resource super profits tax (RSPT) from 1 July 2012. Under the RSPT the Government will provide a refundable credit to resource entities for state royalties and will guarantee to contribute 40 per cent of the investment cost of a resource project. In effect, the Australian community will share in the costs of, and returns from, realising the value of resource deposits.

• There will be a staged consultation process over the course of this year to work through detailed design issues, particularly the transition for existing projects. This is a major reform and the Australian Government is committed to a genuine and open consultation process to make sure we get it right.

http://www.deewr.gov.au/Department/Documents/Files/FERGUSON%20MEDIA%20RELEASE%20(4).pdf

60

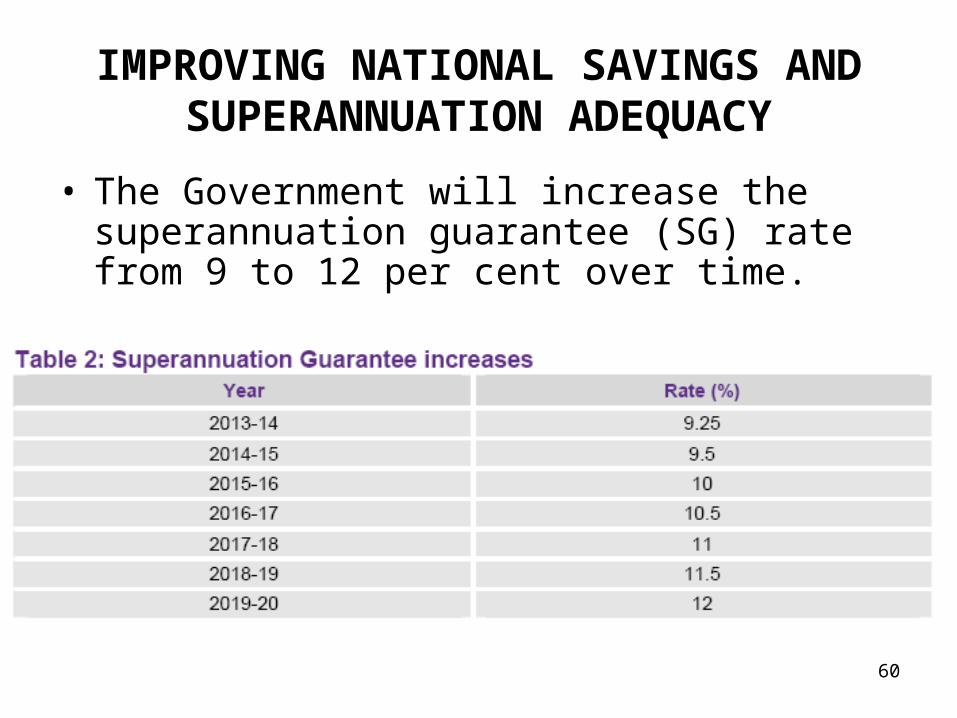

IMPROVING NATIONAL SAVINGS AND SUPERANNUATION ADEQUACY

• The Government will increase the superannuation guarantee (SG) rate from 9 to 12 per cent over time.

61

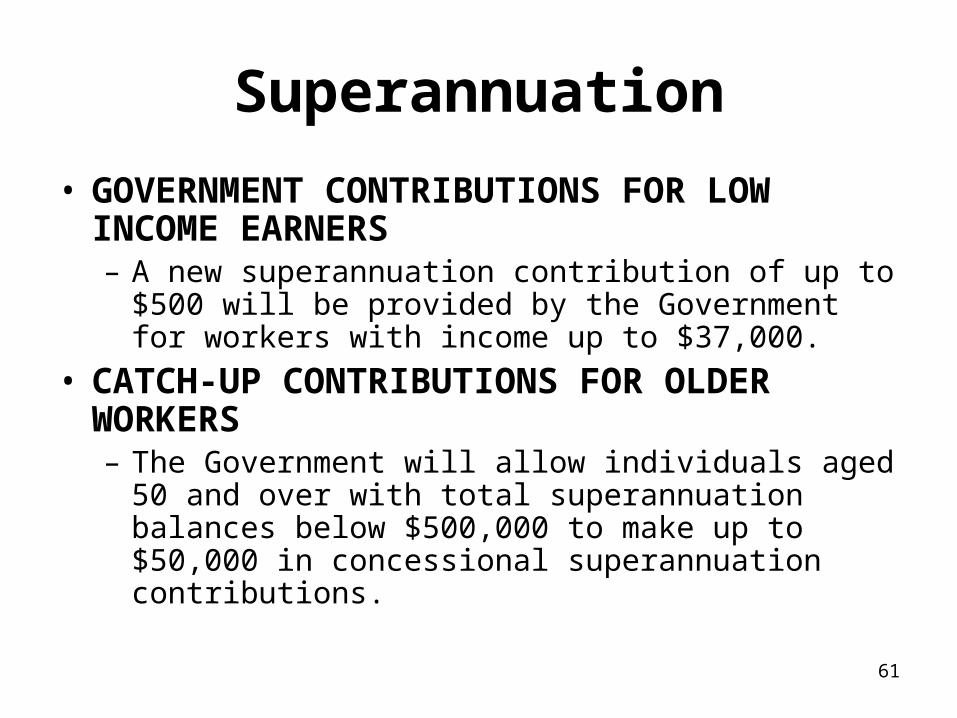

Superannuation

• GOVERNMENT CONTRIBUTIONS FOR LOW INCOME EARNERS– A new superannuation contribution of up to $500 will

be provided by the Government for workers with income up to $37,000.

• CATCH-UP CONTRIBUTIONS FOR OLDER WORKERS– The Government will allow individuals aged 50 and

over with total superannuation balances below $500,000 to make up to $50,000 in concessional superannuation contributions.

62

STRONGER.FAIRER.SIMPLER - A tax plan for our future

• STRONGER.FAIRER.SIMPLER - A tax plan for our future - Overview PDF (850KB)

• STRONGER.FAIRER.SIMPLER - A tax plan for our future - Tax Policy Statement PDF (231KB)

• The Resource Super Profits Tax: a fair return to the nation PDF (373KB)

http://www.futuretax.gov.au/pages/default.aspx#newsDocs-factSheets

63

Conclusion• “Experience suggests that tax reviews rarely

lead to successful tax reform.” . . . But “Tax Reform in Australia is necessary and overdue.”– Chris Evans and Richard Krevor (2009).

• Let’s see if we can do better in the US:– Delayed: Tax report from the President's

Economic Recovery Advisory Board (PERAB)– Forthcoming: National Commission on Fiscal

Responsibility and Reform, http://www.fiscalcommission.gov/

64

About the Author• Jonathan Barry Forman (“Jon”) is

– The Professor in Residence at the Internal Revenue Service Office of Chief Counsel for the 2009-2010 academic year;

– the Alfred P. Murrah Professor of Law at the University of Oklahoma College of Law, teaching tax and pension law; and

– the author of Making America Work (Washington, DC: Urban Institute Press, 2006).

• Prior to entering academia, Professor Forman served in all three branches of the federal government. He has a law degree from the University of Michigan and master’s degrees in both economics and psychology.

• Jon can be reached at (202) 622-7639; [email protected]; www.law.ou.edu/faculty/forman.shtml

64