wfe 2004 - bib.kuleuven.be · jakarta stock exchange erry firmansyah, president director jse...

TRANSCRIPT

ANNUAL REPORT AND STATISTICS 2004

2004 WO

RLD

FE

DE

RAT

ION

OF

EX

CH

AN

GE

S

WO

RL

DF

ED

ER

AT

ION

OF

EX

CH

AN

GE

S

WORLD FEDERATION OF EXCHANGES

American Stock ExchangeAthens ExchangeAustralian Stock ExchangeBermuda Stock ExchangeBME Spanish ExchangesBolsa de Comercio de Buenos AiresBolsa de Comercio de SantiagoBolsa de Valores de ColombiaBolsa de Valores de LimaBolsa de Valores do São PauloBolsa Mexicana de ValoresBorsa Italiana SpABourse de LuxembourgBourse de MontréalBSE The Stock Exchange, MumbaiBudapest Stock Exchange Ltd.Bursa MalaysiaChicago Board Options ExchangeColombo Stock ExchangeCopenhagen Stock ExchangeDeutsche Börse AGEuronext AmsterdamEuronext BrusselsEuronext LisbonEuronext ParisHong Kong Exchanges and ClearingIrish Stock Exchange

Istanbul Stock ExchangeJakarta Stock ExchangeJSE Securities Exchange, South AfricaKorea ExchangeLjubljana Stock ExchangeLondon Stock ExchangeMalta Stock ExchangeNASDNational Stock Exchange of India New York Stock ExchangeNew Zealand ExchangeOMX Exchanges Ltd.Osaka Securities ExchangeOslo BørsPhilippine Stock ExchangeShanghai Stock ExchangeShenzhen Stock ExchangeSingapore ExchangeStock Exchange of TehranStock Exchange of ThailandSWX Swiss ExchangeTaiwan Stock Exchange Corp.Tel-Aviv Stock ExchangeTokyo Stock ExchangeTSX GroupWarsaw Stock ExchangeWiener Börse AG

MEMBER EXCHANGES

The World Federation of Exchanges is an international association comprised of the world’s leading bourses. Its membership includes:

World Federation of Exchanges - Telephone: 33 (0)1.58.62.54.00 - Fax: 33 (0)1.58.62.50.48Home Page: www.world-exchanges.org E-mail: [email protected]

TABLE OF CONTENTS

Every effort has been made to ensure that the information in this publication is accurate at the time of printing. The Secretariat cannot accept responsibility for errors or omissions.

Address by his Imperial Highness the Crown Prince of Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Letter from the Secretary General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

The Working Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2004 General Assembly and Annual Meeting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

IOMA/IOCA Annual Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Workshop on Financial Management of Exchanges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Workshop on Corporate Communications and Investor Relations . . . . . . . . . . . . . . . . . . . . . . . . 12

Survey: 2003 Cost and Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Survey: Regulation of Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

IOMA 2003 Market Survey. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Publications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

IOMA / IOCA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Affiliates and Correspondents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Representation of the Exchange Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

2004 Market Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Statistics Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

2004 Foreign Exchange Rates against the US Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Equity Markets Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Fixed Income Markets Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Derivative Markets Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

Indicators of Market Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Small and Medium Business (SMB) Markets Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Other Markets Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

WFE Audited Financial Statements 2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

WORLD FEDERATION OF EXCHANGES 3

ADDRESS BY HIS IMPERIAL HIGHNESSTHE CROWN PRINCE OF JAPAN

Address by His Imperial HighnessThe Crown Prince of Japanat the Gala Dinner of the WorldFederation of Exchanges 44th General Assembly 13 October 2004 in Tokyo

Reprinted with the kind permission of the Tokyo Stock Exchange

Distinguished guests, ladies and gentlemen,

I am very pleased that the World Federation of Exchanges44th General Assembly was brought to a successful con-clusion with the participation of representatives fromexchanges around the world.

Three centuries have passed since the first securities market was established in the 17th century. With the modernization of national economies, securities marketshave now developed to the point that they are regarded asnational assets which are indispensable to the social andeconomic activities of individual countries.

Exchanges have several important tasks as the centers ofsecurities markets, which directly connect securitiesissuers with investors who offer funds. These tasksinclude encouraging the active and accurate disclosure ofinformation by companies, as well as deepening the public’s understanding of securities investment. I myself have long had great interest in water transporta-tion. Hubs of water transportation are centers of trade, and

it is there that commerce flourishes and securities mar-kets, which support economic activities in the field offinance, exist there. In fact, adjacent to the place wherethe Tokyo Stock Exchange stands are commercial areaswhich have prospered through the ages, and canals stillexist there. Nearby, there was also a landmark bridgecalled Kaiun-bashi, or “Marine Transportation Bridge.” Thisis where the residence of the naval magistrate was locatedduring the Edo Period. I find this link fascinating.

In our world of today, where the operations of securitiesmarkets cross borders and oceans and continue tobroaden, I believe it is very meaningful that representa-tives of the leading exchanges in the world have convenedto deepen mutual understanding. I hope that all gatheredhere today will make even further efforts toward develop-ing securities markets from "national assets" into “globalassets.”

Thank you.

His Imperial Highness the Crown Prince of Japan

LETTER FROMTHE SECRETARY GENERAL

4

The state of the exchange industry in 2004 was heart-ening for several reasons. First, the gains in nearly all

the equity indices world-wide confirmed the trend towardmore vigorous global economic growth, and followed theadvances made in every member market in 2003.Enterprises were participating in that growth and enablingit to happen. For details, please see “2004 MarketHighlights”.

Second, the gains in valuation in 2004 were accompaniedby higher trading volumes. This took place in nearly everyFederation member market. Given that the financial services industry was hit by several storms over the pastfew years, the volume figures reflect a return of investorconfidence.

Enhancing trust in public capital markets has been thecentral work of many exchanges. The Federation’s keyreport in 2004 was on market quality issues tied to the regulatory work that exchanges perform in conjunctionwith public authorities. The themes of this survey are notedin this Annual Report.

Last year, high level contacts with IOSCO (the InternationalOrganization of Securities Commissions) were designed togive national regulators insight into the market operators’concerns on policy, as well as on efficiency as regulatorycosts rise. In addition to these and other ongoing ties withfinancial policy leaders world-wide, in 2004 several memberexchanges and WFE were invited to become directly involvedin the work of the United Nations Global Compact initiativefor socially responsible investment. Further information isfound in the External Relations section of this report.

Under the chairmanship of Russell Loubser, CEO of the JSE Securities Exchange, South Africa, last year theFederation’s Working Committee explored the handling ofconflicts of interest in the financial services sector, andreported on the trends in extending exchange businessservices more widely.

The Committee also guided the program development fortwo workshops, the first for exchange chief financial officers hosted by Deutsche Boerse, and the second on corporate communications hosted by Bolsa Mexicana deValores. Vice Chairman Takuo Tsurushima hosted theindustry’s leaders at the WFE General Assembly and AnnualMeeting in Tokyo in October. Outlines of these activities arefound in the “Events” section of this report.

The majority of WFE members run diversified operations,including markets for futures and options, where year-on-year growth was again strong in 2004. Most also providepost-trade services. In this report, highlights are givenfrom the IOMA/IOCA Annual Meeting (International OptionsMarkets Association/International Options ClearingAssociation), which was organized by the Osaka SecuritiesExchange in collaboration with WFE. Data from the IOMAAnnual Survey indicate that these markets remain on ahigh-growth trajectory.

In a time of rapidly changing technology and shifting regulation, the exchanges of WFE have been leaders inanticipating demand and adapting to new commercial con-ditions. The WFE Cost and Revenue Survey, carried out inassociation with Duke University, bears out that these keyactors in financial services continue to develop their coreresponsibilities while innovating commercially. The keyfindings from that survey are included in this AnnualReport, too.

None of these accomplishments would have been possi-ble without the commitment of exchanges, the carefulguidance given by the Board of Directors, and the leader-ship of the NYSE and its Chief Executive Officer, John A. Thain, who served as WFE Chairman in 2004.

My colleagues at the WFE office enabled this work to bewell executed.

Thomas KrantzSecretary General

March 2005

Thomas Krantz, Secretary General of the World Federation of Exchanges

WORLD FEDERATION OF EXCHANGES

Officers

ChairmanTokyo Stock Exchange Takuo Tsurushima, President & Chief Executive Office

Vice ChairmanBorsa Italiana Massimo Capuano, President & Chief Executive Officer

Working Committee ChairmanBolsa de Valores do São Paulo Gilberto Mifano, Chief Executive Officer

Directors

AmericasBolsa Mexicana de Valores Guillermo Prieto-Treviño, Chairman of the Board

Chicago Board Options Exchange William J. Brodsky, Chairman & Chief Executive OfficerNASD Douglas Shulman, President, Markets, Services and Information

New York Stock Exchange John A. Thain, Chief Executive Officer

Asia-PacificAustralian Stock Exchange Tony D'Aloisio, Managing Director & Chief Executive Officer

Hong Kong Exchanges and Clearing Paul Chow, Chief ExecutiveKorea Exchange Young-Tak Lee, Chairman & Chief Executive Officer

Singapore Exchange Hsieh Fu Hua, Chief Executive Officer

EuropeBME Spanish Exchanges Antonio J. Zoido, Chairman

Copenhagen Stock Exchange Hans-Ole Jochumsen, President & Chief Executive OfficerEuronext Paris Jean-François Théodore, Chairman & Chief Executive Officer*

JSE Securities Exchange, South Africa Russell M. Loubser, Chief Executive Officer

*Serves as Federation Treasurer

Members of the Board are elected to two-year renewable terms by the General Assembly. The Board meets three times per year, in accordance with the WFE Statutes.

BOARD OF DIRECTORS

31 January 2005

5

6

ChairmanBolsa de Valores do São Paulo Gilberto Mifano, Chief Executive Officer

MembersAmerican Stock Exchange Peter Quick, President

Athens Exchange Socrates G. Lazaridis, General Director, Market Supervision

& Listed Securities Sector

Australian Stock Exchange Colin R. Scully, Chief Operating Officer

Bermuda Stock Exchange Gregory A. Wojciechowski, President & Chief Executive Officer

BME Spanish Exchanges Ramon Adarraga, Director of International Affairs

Bolsa de Comercio de Buenos Aires Gabriela Bindi, Head of International Affairs

Bolsa de Comercio de Santiago Gonzalo Ugarte Encinas, Planning & Development Manager

Bolsa de Valores de Colombia Juan Camilo Ramirez Ruiz, Director Juridico

Bolsa de Valores de Lima Federico Oviedo, General Manager

Bolsa Mexicana de Valores Pedro Zorrilla Velasco, Chief Operating Officer

Borsa Italiana SpA Antonella Amadei, Advisor to the President & C.E.O.

for Global Relationship Development

Bourse de Luxembourg Michel Maquil, President & Chief Executive Officer

Bourse de Montréal Luc Bertrand, President and Chief Executive Officer

BSE The Stock Exchange, Mumbai Rajnikant Patel, Executive Director and Chief Executive Officer

Budapest Stock Exchange Ltd. Zsolt Horvath, General Manager

Bursa Malaysia Li Lee Ong, Head, Research & External Affairs,

Finance & Strategy

Chicago Board Options Exchange Richard G. DuFour, Executive Vice President

Colombo Stock Exchange Hiran Mendis, Director General

Copenhagen Stock Exchange Poul Erik Skaanning-Jørgensen, Senior Vice President

Deutsche Börse AG Dirk Schlochtermeyer, Head of Market Policy

Euronext Amsterdam André Went, Group Policy Director

Euronext Brussels Vincent van Dessel, Markets Director

Euronext Lisbon Abel Sequeira Ferreira, Administrator

Euronext Paris Robert Thys, Director International Affairs

Hong Kong Exchanges and Clearing Henry Law, Head, Corporate Communications

THE WORKING COMMITTEE

March 2005

WORLD FEDERATION OF EXCHANGES 7

Irish Stock Exchange Tom Healy, Chief Executive

Istanbul Stock Exchange Aril Seren, Senior Vice-Chairman

Jakarta Stock Exchange Erry Firmansyah, President Director

JSE Securities Exchange, South Africa Nicky Newton-King, Deputy Chief Executive Officer

Korea Exchange Hong-sik Choi, Senior Vice President, International Relations

Ljubljana Stock Exchange Andrej Sketa, Vice-President & Chief Operating Officer

London Stock Exchange Ed Wells, Principal Policy Adviser

Malta Stock Exchange Alfred Mallia, Chairman

NASD Steven Polansky, Director, International Affairs and Services

National Stock Exchange of India Chitra Ramkrishna, Deputy Managing Director

New York Stock Exchange Alain Y. Morvan, Senior Vice-President, International Relations

New Zealand Exchange Mark Weldon, Chief Executive Officer

OMX Exchanges Ltd. Pekka Peiponen, Senior Vice President, Cash Market

Osaka Securities Exchange Mikio Hinoide, Executive Officer of Strategy & Product Planning

Oslo Børs Anders Brodin, Deputy CEO

Philippine Stock Exchange Atty. Francisco Ed. Lim, President

Shanghai Stock Exchange Chian Q. Li, Head of International Affairs,

Global Business Development

Shenzhen Stock Exchange Li Ran, International Cooperation

Singapore Exchange Seck Wai Kwong, Chief Financial Officer, and Head of Strategy

and Business Development

Stock Exchange of Tehran Hossein Abdoh Tabrizi, Secretary General

Stock Exchange of Thailand Kittiratt Na-Ranong, President

SWX Swiss Exchange Richard T. Meier, Delegate for International Affairs

Taiwan Stock Exchange Corp. Nai-Kuan Huang, Executive Vice President, Research &

Development, International Affairs

Tel-Aviv Stock Exchange Saul Bronfeld, Managing Director

Tokyo Stock Exchange Yoshitaka Muranushi, Director, International Affairs,

Corporate Planning Dept.

TSX Group David Ablett, Director, Policy Development and Planning

Warsaw Stock Exchange Wieslaw Rozlucki, President and CEO

Wiener Börse AG Stefan Zapotocky, Joint Chief Executive Officer

The General Assembly and Annual Meeting were con-ducted by the WFE Chairman, John A. Thain, the Chief

Executive Officer of the New York Stock Exchange.

The General Assembly of members reviewed the affairs of the Federation. In particular:

- the Board of Directors was elected. Notably, Mr. Takuo Tsurushima, WFE Vice Chairman and President and ChiefExecutive Officer of the Tokyo Stock Exchange, will serveas Chairman for 2005-2006, and Mr. Massimo Capuano,President and Chief Executive Officer of the BorsaItaliana will serve as Vice Chairman;

- great attention was paid to the business standards ofmembers adhering to WFE, as they assure the operationof a superior, transparent market for the listing and trading of securities and derivatives instruments. Thosehigh standards distinguish exchanges from competingfinancial actors;

- the Bolsa de Colombia in Bogota was admitted to mem-bership.

The Annual Meeting opened for a series of business policy roundtables. The topics addressed were of signifi-cance to the financial services industry world-wide, andinvestigation of these questions was best conducted bythe leaders of this industry together. Exchanges are adjust-ing their commercial strategies to meet the decade’s capital markets environment, and to assure their partici-pation in defining its development.

• Sir David Tweedie, Chairman of the Board, InternationalAccounting Standards Committee Foundation spoke onthe implementation of international financial reporting

standards (IFRS), the new accounting norms; currentquestions in their definition; and possible implicationsof these changes in financial information for exchanges.

• Hiroshi Koshida, Chairman of the Japan SecuritiesDealers Association, updated delegates on issues in theJapanese market, and on the business outlook for theintermediary community.

• Tatsuya Itoh, Japanese Minister for Financial Services,spoke of the government’s plans for this sector follow-ing the recent reshuffling of portfolios in Prime MinisterKoizumi’s cabinet.

• Professor Roberta Karmel of the Brooklyn Law School, aformer US SEC Securities Commissioner and Director ofthe NYSE, presented a study on members’ current workand planning in the field of regulation of the exchangesthey operate. Comments were made by Douglas Shulman,President, Market Activities, Services and Operations atNASD, who emphasized the role technology can play; andHans-Ole Jochumsen, President and Chief ExecutiveOfficer, Copenhagen Stock Exchange, who added infor-mation on changes underway in European Union coun-tries in the structuring of capital markets.

As the business model shifts, important questions arise asto the quality of market operations, historically assured bya mix of work done by the exchange and its regulatoryauthority, and how the work of regulation is to be paid for.

• Professor Kunio Itoh of Hitotsubashi University and Headof the Listed Companies Awards Committee at the TokyoStock Exchange, and Masao Morita, Senior Vice President,Executive Officer, Sony Corporation described their workin the field of branding and corporate/product branddevelopment. Exchange remarks were made by TonyD’Aloisio, Managing Director and Chief Executive Officer,Australian Stock Exchange.

Lessons from Sony and the country’s leading businessschool author on the subject of corporate brand develop-ment were shared with delegates eager to grow their busi-nesses and improve yet more the standing of exchanges’reputations. Client relationship management in this contextwere also reviewed. The integrity of the brand of regulatedfinancial markets, and the benefits of good regulation, wereamong the topics for comment by Mr. D’Aloisio.

8

2004 GENERAL ASSEMBLYAND ANNUAL MEETING

Hosted by the Tokyo Stock Exchange,11-13 October 2004

WFE Annual Meeting, October 2004 in Tokyo

WORLD FEDERATION OF EXCHANGES 9

• Jean-François Théodore, Chairman and Chief ExecutiveOfficer of Euronext, pronounced an address on exchangestrategy, in order to open a full morning’s work on thetopic of “new business models of exchanges.” Followinghis speech, discussion among delegates was led byTakuo Tsurushima, President and CEO, Tokyo StockExchange.

There has been much change in the last five years for theleaders of WFE to evaluate. In response to Mr. Théodore’saddress, Chairman Thain invited delegates to consider constructing a business model for exchanges operating incompetitive environments, allowing as well for variations onthat theme. In particular, demutualized exchanges mustenhance shareholder returns by diversifying incomesources. It proved to be instructive for delegates to shareviews on possible future business models for their industry.

• Junichi Ujiie, Chairman, Nomura Holdings; Hsieh Fu Hua,Chief Executive Officer from Singapore Exchange; andRuben Lee, Adjunct Professor, ISMA Center, ReadingUniversity, all shared their thoughts on the changestransforming this industry.

• Paul Chow, Chief Executive, Hong Kong Exchanges andClearing, moderated a round table on the topic of finan-cial analysts’ observations of the exchange business.The speakers were Robert Luciano, Investment Managerof Caledonia Investments in Sydney; and YasuoKuramoto, Vice Chairman, Fidelity Investment Japan Ltd.WFE’s guests shared their insights into the businesspotential for listed and unlisted exchanges.

• Mr. Hiroshi Okuda, Chairman of Toyota Motor Corporation,and Chairman of the Japanese Business Federation,spoke to delegates about the business outlook as theyear 2004 comes to a close.

• Toshitsugu Shimizu, Executive Officer, Tokyo StockExchange, led a session on the “Exchange industry worldreport: regional news and current questions.” This briefing by members for members included remarks by:

- Yung-Joo Kang, Chairman & CEO, Korea StockExchange

- Osman Birsen, Chairman & CEO, Istanbul StockExchange

- Massimo Capuano, President and Chief ExecutiveOfficer, Borsa Italiana

- Russell Loubser, Chief Executive Officer, JSE SecuritiesExchange, South Africa

- Guillermo Prieto-Trevino, Chairman of the Board, BolsaMexicana de Valores

- And for derivatives, Craig Donohue, Chief ExecutiveOfficer, Chicago Mercantile Exchange

The purpose of this briefing was to update delegates onthe world’s capital markets’ regions by business themes,such as market growth, trading volumes, new products andmarket design. Remarks covered recent events, and futureplans or expectations.

• Toshihiko Fukui, Governor of the Bank of Japan, closedthe WFE Annual Meeting with a special session on monetary policy.

WFE Annual Meeting, October 2004 in Tokyo

WFE Annual Meeting, October 2004 in Tokyo

10

IOMA/IOCA ANNUAL MEETING

IOMA/IOCA stand for the International Options MarketAssociation/International Options Clearing Association,which work in affiliation with WFE.

IOMA Opening Session• Welcoming Remarks – Yair Orgler, Chairman, Tel-Aviv

Stock Exchange• Welcoming Remarks – Michio Yoneda, President & CEO,

Osaka Securities Exchange • President’s Report – Yair Orgler, Chairman, Tel-Aviv Stock

Exchange• Installation of New President - Yair Orgler/Colin Scully,

Chief Operating Officer, Australian Stock Exchange• Financial Report – Ted Westerterp, IOMA Treasurer

IOMA World Report• Moderator: Yair Orgler, Chairman, Tel-Aviv Stock Exchange• Zaha Rina Zahari, Head, Exchanges Business Unit,

Malaysia Securities Exchange Berhad• Chitra Ramkrishna, Deputy Managing Director, National

Stock Exchange India• William J. Brodsky, Chairman & Chief Executive Officer,

CBOE • Toshihiro Oritate, Advisor, Osaka Securities Exchange

Internalization - Developments in the Debate • Meyer S. Frucher, Chairman & CEO, Philadelphia Stock

Exchange• Luc Bertrand, President & CEO, Bourse de Montreal and

Chairman, BOX

Cross-Border Issues and Business Development• Nicholas Weinreb, Head of Regulation, Euronext.Liffe• Jorge Alegria Formoso, Chief Executive Officer, Mercado

Mexicano de Derivados (Mexder)

Strategic Role of Clearing / Clearing OTC Products• Andrew Lamb, Managing Director, Risk and Deputy Chief

Executive, LCH.Clearnet• Kim Taylor, President, Clearing House, CME• Dennis Dutterer, President & CEO, The Clearing Corporation• Orlando Chiesa, Head of Clearing Strategy, Eurex

Demutualization Roundtable• Kim Taylor, President, Clearing House, CME• Ivers Riley, Chairman, International Securities Exchange• Colin Scully, Chief Operating Officer, ASX• Mikio Hinoide, Executive Officer, Osaka Securities

Exchange

Developments for the WFE and IOMA/ IOCA• Thomas Krantz, Secretary General, WFE

Market Design• Richard DuFour, Executive Vice President, CBOE• Sung Hee Hong, Senior Vice President, Option Market

Dept., Korea Stock Exchange

Product Development• Patrick Conroy, Chief Operating Officer, Hong Kong

Exchanges and Clearing• André Cappon, President, The CBM Group

IOMA Closing session• Speech – Michio Yoneda, President & CEO, Osaka

Securities Exchange • IOMA 2005 Information – Richard DuFour, Executive Vice

President, Chicago Board Options Exchange

Program for IOMA/IOCA Annual MeetingHosted by the Osaka Securities Exchange

5 – 8 May 2004

WORLD FEDERATION OF EXCHANGES

The 2003 WFE Exchange Cost and RevenueSurvey• Thomas Krantz, WFE Secretary General

Outside investment analysis of exchanges• Mamoun Tazi, Bear Stearns in London• Robert Luciano, Investment Manager, Caledonia Invest-

ments in Sydney

Standard & Poor’s methodology for ratingsused for counter-parties, issuers, and exchanges’ public debt issues – both quantitative and qualitative• Diane Hinton, Director of Financial Services at Standard

and Poor’s in Paris• Miguel Pintado, Associate Director of Financial Institutions

at Standard and Poor’s in Stockholm

Appropriate capital reserves and cash levels for exchanges, and their management• Saul Bronfeld, Managing Director, Tel Aviv Stock Exchange

Current Treasury issues from the creation of OMX out of the merger of several marketsand a strong high-tech business. • Teuvo Rossi, Senior Vice President, Finance and Business

Control, OMX Exchanges

Current treasury issues from: The change inownership structure of the Budapest StockExchange, and how valuations were made by those bidding. How might the informationgenerated in this ownership transformationmodify the future treasury management of theExchange ?• György Mohai, Deputy General Manager, Budapest Stock

Exchange

Balance sheet management• Marcus Thompson, Head of Finance, Deutsche Börse• Freda Evans, CFO of the JSE Securities Exchange, South

Africa• Khairussaleh Ramli, CFO of Bursa Malaysia

Accounting and audit questions for exchanges• Bernhard Stamm, Head of Finance, Wiener Börse

International Accounting Standards now beingadopted by numerous WFE members• Kurt Ramin, Director, IASCF• Manfred Hannich, Partner, Global Conversion Services,

KPMG

Business liability management and mitigatingthe risk of potential claims against exchanges.What insurance coverage is appropriate, andwhat kinds of reserves in cash or other invest-ments should the exchange keep on hand?• David Higgins, Partner at Freshfields London

Investment planning: exchange decision-making on the appropriate cost of capital forprojects with different risk-return ratios andtime horizons. How are risks spread, and whichproposals are accepted in order to diversifyrisk while using capital sparingly ? Is this awell defined process at exchanges ?• Ulrich Becker, Managing Director at Deutsche Börse AG• Javier Hernani, Chief Financial Officer, BME Spanish

Exchanges

The case for exchanges as a growth industry• John Hayes, Chief Financial Officer of the Australian

Stock Exchange• Paul Malcolmson, Head of Investor Relations, TSX Group• William Megginson, University of Oklahoma

WORKSHOP ON FINANCIALMANAGEMENT OF EXCHANGES

11

Program for Workshop on Financial Management of Exchanges Hosted by Deutsche Börse

15 – 17 September 2004

Care was taken with regard to market-sensitive information by applying the “Chatham House Rule”, assuring effective discussion and discretion for delegates and their institutions.

12

WORKSHOP ON CORPORATECOMMUNICATIONS

AND INVESTOR RELATIONS

Welcome and Introduction to Workshop• Guillermo Prieto Trevino, Chairman of the Board, Bolsa

Mexicana de Valores• Thomas Krantz, WFE Secretary General

World report on Corporate Communications• Eduardo Trigueros, BMV Issuers and Information Director• Yoshitaka Muranushi, Director, International Affairs and

Corporate Planning, Tokyo Stock Exchange• Henry Law, Head, Corporate Communications, Hong Kong

Exchanges and Clearing• John Parry, Director, Rostron Parry• Iwona Pawlina, Director of Market and Promotion,

Warsaw Stock Exchange

Branding• David Ablett, Director, Public Affairs, Research and

Communications, TSX Group• Elsie Maio, President, Maio and Co• Jeremy Sampson, Chief Executive, Interbrand Sampson

Change management among Europeanexchanges• John Parry, Director, Rostron Parry

Crisis management• James T. MacGregor, President, The Abernathy MacGregor

Group• Melissa Jenner, Marketing Manager, New Zealand

Exchange

Retail Investor Services Offered by a Commercial Exchange• Anthony B. Hunter, National Manager, Investor Services,

Australian Stock Exchange

Socially Responsible Investing• Geoff Rothschild, Director, Corporate Marketing and

Communications, JSE Securities Exchange, South Africa• Jerry Moskowitz, Managing Director, FTSE Americas

The Annual Report – Marketing Tool or PublicRecord?• Stuart Z. Goldstein, Managing Director Corporate

Communications, Depositary Trust and ClearingCorporation

Internet• Ted Szu-Che Peng, Senior Vice President, Administrative

Department, Taiwan Stock Exchange Corp.• Cynthia H. Elsener, Director of Internet, Chicago Board

Options Exchange

Public Trust and Confidence - The Exchangeas Industry Spokesperson and Standard Setter• Geraldine M. Walsh, Deputy Director, Office of Investor

Education and Assistance, United States Securities andExchange Commission

• Gavin Power, Project Manager, United Nations GlobalCompact

• Stephen Davis, President, Davis Global Advisors • Cristiana Pereira, Advisor for Development and

International Relations, Sao Paulo Stock Exchange

Program for Workshop on Corporate Communications & Investor Relations

Hosted by Bolsa Mexicana de Valores29 – 30 November 2004

1. Otherwise expressed, $15.4 billion means $15 400 million.

WORLD FEDERATION OF EXCHANGES

Summary

The World Federation of Exchanges’ annual memberCost and Revenue Survey, begun in 1991, provides an

overview of member expenses and revenues while analyz-ing data to discover larger trends. Information is collectedand organized according to exchange legal status, geog-raphy, and size. Comparison of 2003 to 2002 data exhibitseffects of changes in the economic, legal, and accountingcontext in which the exchanges operate.

Unlike both demutualized exchanges and listed exchanges,not all member-owned exchanges are run for profit.Consequently, review of WFE member data necessitates firsta breakdown by exchange legal status. Overall, this annualreport analyzes data in three ways: by legal status, geo-graphic region, and 10 largest exchanges versus all others.

Some key observations that are included in the report:

• Member-owned, limited company exchanges was thefastest growing of the five categories over the past year.

• Total equity capital across all exchanges increased from$15.4 billion1 in 2002 to $16.2 billion in 2003, a 5% changeafter correcting for US dollar depreciation over the period.

• Profitability varies considerably among exchanges,whether sorted by legal or geographic categorization,indicating that both local (idiosyncratic) and global factors have an impact on ROE.

• Most exchanges showed increases in both earnings and net income.

• The industry overall shows evidence of considerablepolarization, so that a small number of the largerexchanges account for the lion’s share of both equitycapital and revenues among all WFE member exchanges.

- Two European exchanges alone account for approxi-mately 30% of the equity capital across all WFE mem-ber exchanges.

- For equity and derivatives trading, the 10 largestexchanges dominate, accounting for 71% and 60% ofall product revenues, respectively.

- The 10 largest exchanges also account for approxi-mately 50% of transaction-related revenues across allWFE member exchanges.

• Total revenues in 2003 were $6.41 billion, a 4% increasefrom 2002. The most important source of revenue for allexchanges is from trading, accounting for 38% of totalrevenues. Services (including information dissemination,clearing and IT sales) comes a close second, at 35%.

• Trading revenues in derivatives grew sharply by volumein 2003, while trading revenues in equities was slightlyreduced, which might have been expected to coincidewith lower trading volumes and fees. Trading in equities is the historical basis for this industry, and ofmembership.

• The most important products traded across allexchanges are equities, accounting for just over 50%of all exchanges’ trading revenues. Derivatives accountfor about 35% of trading revenues. The European andAsian exchanges both show nearly as much revenuefrom derivatives as from equities, while in theAmericas, almost all of the revenue comes from equitytrading.

• Total trading revenues across all products and exchangesin 2003, at $2.36 billion, was almost unchanged from2002 at $2.39 billion.

• The vast majority (about 80%) of trading revenue feesare generated by transaction fees, while membership/access fees account for about 15%, and IT fees theremaining 5%.

• The largest portion of costs across exchanges is compensation (salaries and benefits), accounting forapproximately 35% of costs. Costs have remained relatively stable across the industry between 2002 and 2003.

SURVEY: 2003 COST AND REVENUE

13

SURVEY: 2003 COSTAND REVENUE (CONTINUED)

While this report endeavors to exhibit a broad and com-prehensive survey of the relative costs and revenues ofmember exchanges, certain limitations must be noted. Tobegin, the survey does not include financial informationfrom the American Stock Exchange, The Chicago Board OfTrade (CBOT) or the Chicago Mercantile Exchange Holdings(CME) and therefore underestimates the relative size ofthe “Americas” exchanges and may additionally misstatecertain relative profitability data between different geographic areas.

Additionally, comparison of financial figures amongexchanges may be influenced by the use of differentaccounting systems. Some members adhere to IAS stan-dards, while others follow national GAAP standards.

Further, the financial data reported in this presentation aregiven in US dollars. When comparing between 2002 and2003 data, we take account of the impact of significantdollar depreciation over the period by using 2003 exchangerates throughout. Where relevant, we also consider howthese numbers differ when using dollar exchange ratesthat applied in each year.

14

2003 2002$(billion) member demut listed assoc other Total member demut listed assoc other Total

Revenues

Listing: Initial & Annual 0,358 0,266 0,295 0,050 0,018 0,987 0,345 0,272 0,271 0,060 0,016 0,963

Trading 0,327 0,556 1,063 0,408 0,077 2,431 0,312 0,495 1,023 0,375 0,064 2,268

Services 0,516 0,430 1,118 0,182 0,028 2,274 0,524 0,347 1,100 0,213 0,025 2,209

Financial Income 0,085 0,075 0,277 0,238 0,039 0,715 0,097 0,096 0,205 0,233 0,099 0,731

Total 1,287 1,327 2,753 0,878 0,162 6,407 1,277 1,210 2,599 0,881 0,203 6,171

Costs

Compensation 0,667 0,710 0,653 0,150 0,051 2,231 0,671 0,687 0,677 0,151 0,048 2,234

IT 0,270 0,372 0,313 0,113 0,005 1,072 0,217 0,339 0,304 0,119 0,005 0,984

Admin 0,125 0,381 0,313 0,057 0,020 0,895 0,134 0,518 0,339 0,046 0,023 1,060

Dep/amort 0,127 0,272 0,232 0,074 0,014 0,719 0,126 0,275 0,231 0,089 0,013 0,735

Reg. costs 0,176 0,044 0,060 0,003 0,011 0,294 0,174 0,049 0,050 0,002 0,007 0,281

Fixed costs 0,211 0,234 0,045 0,019 0,031 0,539 0,256 0,240 0,043 0,025 0,024 0,588

Total 1,576 2,013 1,615 0,415 0,132 5,751 1,578 2,108 1,643 0,433 0,120 5,881

Equity Capital 2,251 3,979 7,410 1,933 0,628 16,201 2,159 3,800 6,983 1,902 0,555 15,398

This survey was conducted for the World Federation of Exchanges with the assistance of Professor Stephen Wallensteinof the Duke University Global Capital Markets Center.

WORLD FEDERATION OF EXCHANGES

This survey was conducted for the World Federation ofExchanges by Professor Roberta S. Karmel of the

Brooklyn Law School.

Summary

Most exchanges believe that regulation is a part of theirbrand, and most exchanges are engaged in market regula-tion. Many continue to license trading members and super-vise clearing and settlement activities. Many continue toregulate listed company disclosure and corporate gover-nance. The costs of regulation are a significant portion ofexchange operating expenses, although the answers toquestions about costs in this survey were somewhat dis-appointing in terms of genuine comparability for the group.Some exchanges did not respond to these questions, andsome answers seemed somewhat arbitrary, and perhapseven erroneous due to diverse costing measures.

A majority of exchanges wished their answers to remainconfidential. Whether they wished all or only someanswers to be confidential was unclear, so this report givesall exchanges anonymity.

Most, if not all, exchanges expressed the view that theirregulatory responsibilities would not change in the nextyear, but that response seemed more of a hope than a real-ity. Exchange regulation is clearly in a state of flux. Perhapsan inability by exchanges to fully understand or controlwhat is happening to the exchange markets and to theirregulation explains some of the difficulties exchanges hadin answering the questions. Perhaps that is an importantconclusion in itself.

Another possible impediment to clearer responses is thatas exchanges become commercial enterprises in a globalcapital market, they are all competitors on some level. Thatalso makes giving quantitative information a sensitive matter. But if most exchanges become public companiesin the future, they will have to learn how to disclose finan-cial information in an accurate and fulsome manner. A goodexercise for any exchange contemplating a public offeringwould be to look at the U.S. SEC requirements for aManagement Discussion and Analysis in an annual reportand see if it is willing or able to make such a presentation.

Conclusion

Regulation by exchanges is changing rapidly due to newlaws, new trading platforms, technology, demutualizationand globalization. Public confidence in the securitiesindustry generally and exchange regulation has beenshaken by the numerous scandals in the U.S. and else-where since the bursting of the technology bubble in 2000.There is a risk that exchanges will lose their power to regulate their markets, market participants and listedcompanies. Both exchanges and investors would be poorlyserved if such an eventuality occurs. Virtually allexchanges believe that regulation is a part of their brand,and that they should make every effort to maintain theirregulatory authority by adapting to changing market conditions and changing laws by the creative use of technology and creative solutions to the new conflicts ofinterest which are emerging from new markets and neworganizational forms.

SURVEY: REGULATION OF MARKETS

15

On behalf of IOMA/IOCA, WFE conducted this surveywith the assistance of Stephen Wells. Excerpts follow.

Introduction

It is a strange industry where a 31% annual growth can bedescribed as slowing down, but that is the fact for the deriv-atives exchanges. 2003 saw contract volumes rising to anew record high just short of 8 billion contracts, from 6 bnin the previous year. The rebound of equity markets during2003 no doubt contributed to the buoyant growth, but it isinteresting that volumes actually rose by 39% in 2002 whenequity markets were falling. This suggests instead a matur-ing of derivatives investment as users exploit the risk trans-ference function as well as speculative uses.

The 31% growth of overall contract volumes showed dif-ferential movements in options and futures. The growth infutures was almost identical to that of the previous year,28%. Options volumes increased more rapidly at 33%, butthe rate of growth was significantly reduced from the previous year.

The differential growth in options and, indeed, much of thegrowth generally reflects the effect of the KOSPI IndexOption on the Korea Stock Exchange. This contract alonerepresented some 55% of all options volumes in 2003.Stripping out the effect of the KSE index options the annualgrowth in 2003 was 17% - almost exactly equal to the figure for 2002.

The mention of the KSE index option marks a good pointat which to discuss volume measurement. It is clear thatthe enormous success of the KSE contract, which is a relatively low value contract targeted at retail investors,raises a question about how best to measure derivativemarkets. A similar debate in cash markets was resolvedin favour of measuring value of assets traded. This is nota perfect solution but, to quote Churchill on democracy, “ itis the worst possible system apart from all the others”.

Derivatives markets have traditionally measured theirturnover in contracts traded. Exchanges defined contractsizes to suit their users. For a single exchange comparingactivity in terms of contracts traded over time, this is fine– and makes business sense, since the contract is usuallythe basis for charging.

The difficulty arises when looking at volumes across dif-ferent exchanges, since there is no reason why contractson one exchange should be comparable with contracts onanother exchange, even in similar products.

The desire for comparable data has led to a number of sug-gestions to solve this problem, but the most widelyaccepted has been the underlying value of the assets rep-resented by the derivative. Other possibilities have beendiscussed – the FIA in its annual review makes an eloquentcase for a risk-based measure. But pragmatism – usingwhat is available - has won the day, and underlying valuehas been adopted by the WFE after consulting with IOMA.

IOMA 2003 MARKET SURVEY

16

5 193

2 730OptionsFutures

Million contracts

28%28%

47%

33%

39%

31%

200320022001

Million contracts

TotalOptions

Year on year %

Futures0

9 000

8 000

7 000

6 000

5 000

4 000

3 000

2 000

1 000

2003 Derivatives Volume Growth

2003 Worldwide Derivatives Volume7.9 Billion Contracts Traded

WORLD FEDERATION OF EXCHANGES 17

Focus on economic impact

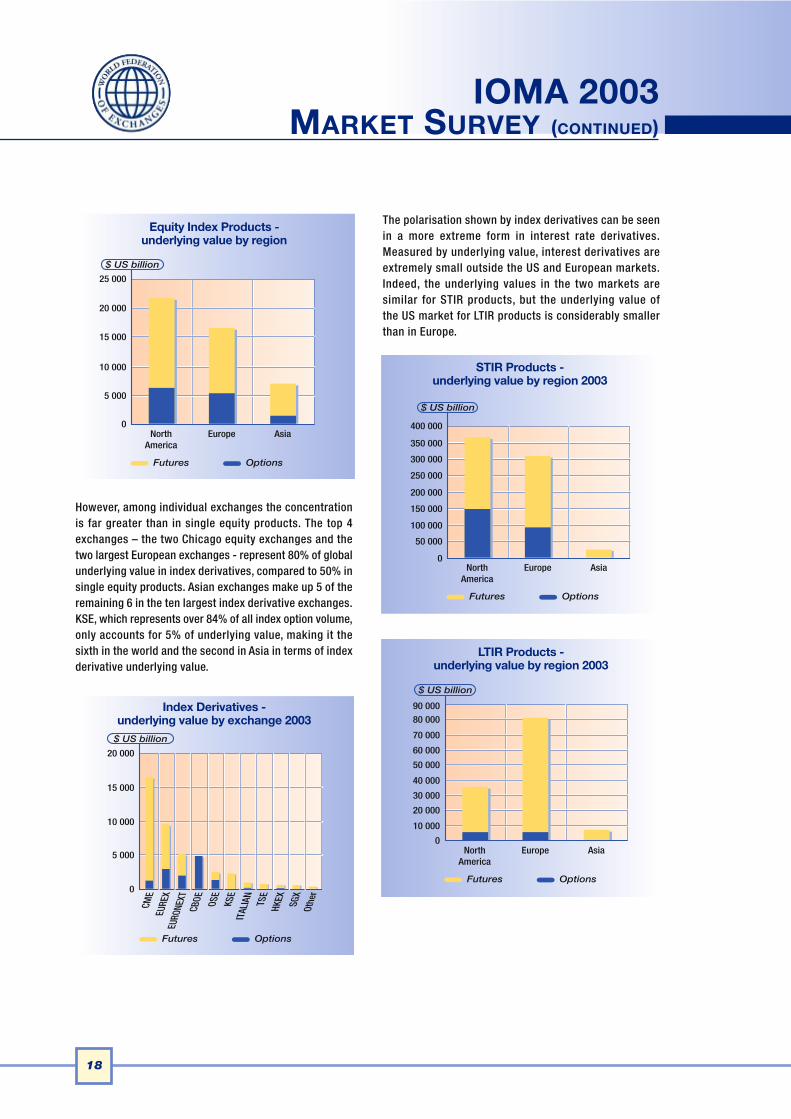

We have discussed the use of underlying value as a meas-ure of exchange activity and concluded that for many pur-poses, such as looking at year-to-year growth, contractvolumes are generally adequate. However, the underlyingvalue figures are important, since for a user they do repre-sent the economic interest or potential economic impact ofa derivative position. With this in mind, it is interesting tolook at comparative underlying values to see where theconcentration of economic interest lies. In this section, welook at the underlying value figures for equity and interestrate products, for regions and for individual exchanges.

We should add a slight word of caution at this point. Thecalculation/estimation of underlying value is not entirelyconsistent across exchanges, and for some exchanges wehave had to estimate values where none were availablefrom the institutions themselves. That said, we have a gooddegree of confidence that the calculations and estimatesare adequate for the analysis given here, and that we candraw broad conclusions.

In terms of underlying value, the US market remains thedominant region for single stock derivatives, representingnearly twice the value of Europe and four times that ofAsia. The development of single stock futures has so farby-passed the US, with the Asian region having significantunderlying value in single stock futures – actually NSEIwith an underlying value in stock futures of $ 198 billion.

Looking at individual exchanges, the 10 exchanges withthe largest underlying value in single equity productsaccount for 96% of the total for all exchanges. As onewould expect, US exchanges make up half of the top 10,with the two major cross-border European exchanges alsopresent. BOVESPA saw more than a tripling of its underly-ing value in single equity products in 2003. NSEI has beenmentioned and is the only exchange apart from Euronextand Spanish Exchanges and RTS (both in the “Other”column on the graph) with significant underlying value insingle equity futures.

In index products, the dominance of the US market is lesspronounced than in single equity derivatives. Note that thegraph scales are approximately 10 times the scale for sin-gle equity derivatives. The European markets have beengrowing rapidly and approach the size of the US market.Some Asian markets have also been growing rapidly –indeed index derivatives have enjoyed more widespreadacceptance in Asia that any other type of derivative.

OptionsFutures

$ US billion

AsiaEuropeSouthAmerica

NorthAmerica

0

1 800

1 600

1 400

1 200

1 000

800

600

400

200

Futures Options

ISE

EURE

XCB

OEAM

EXEU

RONE

XTNS

EIPH

LXBO

VESP

APC

XAS

XOt

her0

100 000

200 000

300 000

400 000

500 000

600 000

$ US million

Individual Equity Products -underlying value by region 2003

Single Equity Derivatives - underlying value by exchange 2003

IOMA 2003 MARKET SURVEY (CONTINUED)

However, among individual exchanges the concentrationis far greater than in single equity products. The top 4exchanges – the two Chicago equity exchanges and thetwo largest European exchanges - represent 80% of globalunderlying value in index derivatives, compared to 50% insingle equity products. Asian exchanges make up 5 of theremaining 6 in the ten largest index derivative exchanges.KSE, which represents over 84% of all index option volume,only accounts for 5% of underlying value, making it thesixth in the world and the second in Asia in terms of indexderivative underlying value.

The polarisation shown by index derivatives can be seenin a more extreme form in interest rate derivatives.Measured by underlying value, interest derivatives areextremely small outside the US and European markets.Indeed, the underlying values in the two markets are similar for STIR products, but the underlying value of the US market for LTIR products is considerably smaller than in Europe.

18

Futures Options

CME

EURE

XEU

RONE

XTCB

OE OSE

KSE

ITAL

IAN

TSE

HKEX SGX

Othe

r0

5 000

10 000

15 000

20 000

$ US billion

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

0North

AmericaEurope Asia

Futures Options

$ US billion

Index Derivatives - underlying value by exchange 2003

350 000

400 000

300 000

250 000

200 000

NorthAmerica

Europe Asia

150 000

100 000

50 000

0

Futures Options

$ US billion

STIR Products - underlying value by region 2003

LTIR Products - underlying value by region 2003

5 000

10 000

15 000

20 000

25 000

0North

AmericaEurope

Futures Options

Asia

$ US billion

Equity Index Products -underlying value by region

Singapore and Tokyo trading in interest derivatives repre-sent the only significant underlying values in Asian markets. The dominance of futures over options confirmsthat interest rate derivatives tend to be institutional prod-ucts rather than retail, and the strongest growth in Asianmarkets has continued to be in retail-oriented products.

Looking at individual exchanges, the polarisation is yetmore extreme. The two Chicago exchanges and the twolarger European exchanges account for 95% of the globalunderlying value.

Within different underlying product maturities the resultsshow a segmentation in Europe, with Eurex dominating theunderlying value in LTIR derivatives and Euronext dominat-ing in STIR derivatives. Euronext and CME represent 90%

of exchange 2003 global underlying value in STIR deriva-tives. EUREX alone represents 63% of underlying value inLTIR derivatives.

These results on economic impact in both equity and interest rate derivatives show a surprising degree of continuing concentration, given the opening and growth ofother derivative markets. It confirms what is obvious,namely that bigger economies mean bigger exchanges. Butbeyond that, it may also suggest something more. It is easier for derivative exchanges to offer exposure to non-domestic underlying assets than it is for cash marketexchanges, and this is for two reasons:

• the settlement issues that exercise cash markets areless of a problem, especially where derivatives can becash-settled

• the asymmetric information issues that tend to holdunderlying stock trading to the home market are lessapparent in index products, which are the staple ofequity derivative trading

This means that derivative positions are more fungible thancash market positions. It is possible that the concentrationthat has often been predicted for underlying trading, espe-cially in equities, but which has been thwarted by the tworeasons given above, may become a fact in derivativestrading, at least for some of the broader asset classes. Theidea of a major dominant exchange in each time zone ispossibly feasible in derivatives, where it has not provedpossible in cash products. In time, we shall see how thisplays out, and what other factors may be at work.

WORLD FEDERATION OF EXCHANGES 19

CME

CBOT

EURE

X

EURO

NEXT

Othe

r

100

0

200

300

400

$ US trillion

Futures Options

STIR and LTIR - underlying value by exchange

PUBLICATIONS

20

Federation's Annual Reports Annual Report 2004Annual Report 2003 Annual Report 2002 Annual Report 2001

Earlier annual reports are available on request

Market Information WFE Market Principles

Market Holidays of members and other markets Market Information on members and other markets

Studies - Federation Surveys and External Analysis Regulation of Markets Survey – January 2005

Equity derivatives and cash equity trading: analysis of figures for 1995-2003 – December 2004Cost & Revenue Survey 2003, and earlier years available on requestThe Significance of the Exchange Industry – 5th edition, July 2004

Disclosure Survey 2003 Trading Survey – March 2003

Property of Information in the Networked Economy – October 2002 Central Counter-Parties and the Stock Exchange Industry – November 2001

Price Discovery and the Competitiveness of Trading Systems – 2000 Value Chain in Financial Markets – 2000

Statistics WFE market data since 1991 are posted on the Federation website and available on request

2004 IOMA Market Survey2003 IOMA Market Survey 2002 IOMA Market Survey

Workshop reports Corporate Communications and Investor Relations – November 2004

Financial Management of Exchanges – September 2004Executive Briefing on Exchange Technology, MIT – December 2003

Forum on Managing Exchanges in Emerging Economies – December 2002 Surveillance Workshop – April 2002

Data Management and Vending – September 2001 Investor Education – November 2000

Focus “Focus”, is the Federation’s monthly news and statistical review.

The entire series since 1991 is available on request

WORLD FEDERATION OF EXCHANGES

IOMA / IOCA

21

IOMA / IOCA bring together derivative exchanges and clearing houses. Since 2002, this association has been affiliatedwith the World Federation of Exchanges, which provide the services of the Secretariat. The purpose is to make sure the

members of both organizations benefit from the cross-workings of cash and derivatives markets. This is achieved by crossinvitations to one another meetings, and finding synergies in work.

The current President is Colin Scully of the Australian Stock Exchange.

The members of IOMA / IOCA are:

IOMA / IOCA International Options Market Association /

International Options Clearing House Association

• American Stock Exchange

• Athens Derivatives Exchanges, S.A. (ADX)

• Australian Stock Exchange

• Bolsa de Valores do São Paulo

• Borsa Italiana SpA

• Bourse de Montréal

• Bursa Malaysia Derivatives

• Bursa Malaysia Derivatives Clearing Berhad

• Canadian Derivatives Clearing Corp.

• Chicago Board of Trade (CBOT)

• Chicago Board Options Exchange

• Chicago Mercantile Exchange (CME)

• China Zhengzhou Commodity Exchange

• Copenhagen Stock Exchange

• Eurex Frankfurt AG

• Eurex Zürich AG

• Euronext Amsterdam

• Euronext Brussels

• Euronext Paris

• Euronext.Liffe

• Hong Kong Exchanges and Clearing

• International Petroleum Exchange (IPE)

• International Securities Exchange (ISE)

• Korea Exchange

• LCH.Clearnet Limited

• LCH.Clearnet SA

• London Metal Exchange Ltd. (LME)

• MEFF

• MEFF Financial Futures and Options Exchange

• Mercado Mexicano de Derivados (MEXDER)

• New York Board of Trade (NYBOT)

• New York Mercantile Exchange (NYMEX)

• NOS Clearing ASA

• OM London Exchange Limited (OMLX)

• OMX Exchanges Ltd.

• OMX Exchanges Stockholm Stock Exchange

• Osaka Securities Exchange

• Oslo Børs

• Pacific Exchange (PCX)

• Philadelphia Stock Exchange (PHLX)

• Shenzhen Stock Exchange

• Singapore Exchange

• Sydney Futures Exchange (SFE)

• Taiwan Futures Exchange (TAIFEX)

• Tel-Aviv Stock Exchange

• The Clearing Corporation

• The Options Clearing Corporation, Inc.

• Tokyo Stock Exchange

• Wiener Börse AG

AFFILIATES ANDCORRESPONDENTS

22

Affiliates

Affiliates are candidates for membership, exchangesthat wish to attend the annual meeting, and since

October 2002 the IOMA/IOCA group.

• Amman Stock Exchange

• Bourse de Casablanca

• Cairo & Alexandria Stock Exchanges

• Chicago Board of Trade (CBOT)

• Chicago Mercantile Exchange (CME)

• China Zhengzhou Commodity Exchange

• The Clearing Corporation

• The Cyprus Stock Exchange

• Iceland Stock Exchange

• International Petroleum Exchange (IPE)

• International Securities Exchange (ISE)

• LCH.Clearnet Limited

• London Metal Exchange Ltd. (LME)

• New York Board of Trade (NYBOT)

• New York Mercantile Exchange (NYMEX)

• The Nigerian Stock Exchange

• NOS Clearing ASA

• The Options Clearing Corporation, Inc.

• Pacific Exchange (PCX)

• Philadelphia Stock Exchange (PHLX)

• Stock Exchange of Mauritius

• Sydney Futures Exchange (SFE)

• Taiwan Futures Exchange (TAIFEX)

Correspondents

Correspondents are newer markets in both wealthy andemerging economies. They receive all WFE documents

and can attend workshops.

• Abu Dhabi Securities Market

• Bahrain Stock Exchange

• Baku Interbank Currency Exchange

• Beirut Stock Exchange

• Belgrade Stock Exchange

• Bolsa de Comercio de Rosario

• Bolsa de Valores de Panama S.A.

• Bolsa Nacional de Valores de Costa Rica

• Bourse Régionale des Valeurs Mobilières S.A.

• Bratislava Stock Exchange

• Bucharest Stock Exchange

• Bulgarian Stock Exchange

• Cayman Islands Stock Exchange

• Channel Islands Stock Exchange, LBG

• Chittagong Stock Exchange Ltd.

• Ghana Stock Exchange

• GreTai Securities Market

• Karachi Stock Exchange Ltd

• Kazakhstan Stock Exchange

• Kuwait Stock Exchange

• Lusaka Stock Exchange Ltd

• Moscow Interbank Currency Exchange

• Muscat Securities Market

• Nairobi Stock Exchange Ltd

• Namibian Stock Exchange

• Palestine Securities Exchange, Ltd.

• Port Moresby Stock Exchange Ltd.

• Prague Stock Exchange Ltd.

• RTS Stock Exchange

• Surabaya Stock Exchange

• Swaziland Stock Exchange

• Tadawul - Saudi Arabian Monetary Agency

• Virt-x Exchange Limited

• The Zagreb Stock Exchange

WORLD FEDERATION OF EXCHANGES

The World Federation of Exchanges maintains workingrelations with public policy and private sector profes-

sional bodies of importance to the capital markets. In 2004,this representation of the member exchanges’ businessinterests was keyed to:

Global policy making forums

IOSCO (International Organisation of Securities Commissions)

Regular exchanges of information are organized betweenthe WFE and IOSCO Board of Directors and TechnicalCommittee, and the two secretariats. The focus of discus-sion remained market structure issues, fairness, and theeconomic trade-off between the burdens of increasing regulation in recent years and benefits accrued to users ofpublic markets over that period.

OECD (Organisation of Economic Cooperation and Development)

In 2004, WFE’s work with OECD centered on the revisedversion of its Principles of Corporate Governance. TheOECD introduced fresh investor powers and board dutiesin an update of principles ordered by G-7 leaders five yearsago. The WFE Secretariat took part in, and commented on,the Steering Group’s review of the new draft benchmarks.

Concerning capital market development, the WFE shares itsongoing work on business standards, the Federation’sMarket Principles. Also, the Secretariat has offered its com-ments and made suggestions on OECD documentation inthis field. In addition, the OECD’s leaders speak regularly atWFE events. The OECD’s Director for Financial, Fiscal andEnterprise Affairs will be addressing delegates in June 2005at the WFE Forum on Developing Exchanges in Beijing. Suchinteraction enables OECD leaders to interact with managersof exchanges, to the benefit of all parties.

IFAC (International Federation of Accountants)

WFE represents exchanges on the International Federationof Accountants’ external advisory group. The group’s pur-pose is to express the viewpoint of users of financialreporting on the standards being developed for audit andassurance work. The review work can become verydetailed, as the interaction between auditors and corpora-tions is evolving in today’s business environment. The goal

pursued by WFE and IFAC is better financial reporting forthe users of the capital markets.

IBA (International Bar Association)

In 2004, WFE focused on interacting with the Capital MarketsForum of the IBA. WFE materials on regulatory issues havebeen circulated within the legal community, as a matter ofpublic information sent to the legal community on businessissues specific to the regulated financial exchanges industry.

United Nations Global Compact

Founded by the U. N. in 2000, the Global Compact is a vol-untary international corporate citizenship network initiatedto support the participation of both the private sector andother social actors to advance responsible corporate citi-zenship and universal social and environmental principlesto meet the challenges of globalization. The interests of cap-ital markets actors are involved here, and in 2004 the GlobalCompact and WFE held their first joint meetings.

Regional exchange federations

As a matter of efficiency in the task of promoting finan-cial exchanges, WFE shares its materials with regional

exchange federations. Several of these have been foundedover the years to suit business purposes specific to certainparts of the world. The following texts introduce them briefly.

AOSEF (Asian and Oceanian StockExchanges Federation)

The Asian and Oceanian Stock Exchanges Federation cur-rently comprises 15 stock exchanges. It originated in 1982as an informal organization called the East Asian StockExchanges Conference. Its objectives were to promotefriendship and to facilitate an information dialogue amongmember exchanges.

Facilitating communications among member exchangesand the management of day-to-day AOSEF affairs is theresponsibility of the standing Secretariat. The services ofthe Secretariat have been provided by the Tokyo StockExchange since the beginning.

The 2004 General Assembly was held in Singapore. The keyreports given were on “Market Information Sharing” and“Liquidity of Small Cap Stocks.”

REPRESENTATION OF THEEXCHANGE INDUSTRY

23

REPRESENTATION OF THEEXCHANGE INDUSTRY (CONTINUED)

FEAS (Federation of Euro-Asian Stock Exchanges)

FEAS was established in May 1995, and currently there are 25 bourses which participate. Membership in theFederation is open to stock exchanges in Europe and Asia. The mission of FEAS is to create fair, efficient and trans-parent market environments, with little or no barriers totrade, between the FEAS members and in their operatingregions. Harmonization of rules and regulations and adop-tion of new technology for trading and settlement by mem-ber securities markets will facilitate the objectives of FEASby promoting the development of the member markets andproviding cross-border trading opportunities for securitiesissued within FEAS member countries.The founding members selected Istanbul as the head-quarters for the Federation's Secretariat.

FESE (Federation of European Securities Exchanges)

In recent years, European securities exchanges have risento the challenges of an evolving business in a number ofways, such as increasing the number of hours during whichtrading can take place to increase access, introducing market-making and block-trading to increase liquidity,refining order handling and execution systems to increaseefficiency and to reduce settlement times, improving infor-mation systems to increase transparency and access, anddeveloping new and imaginative investment instrumentsto enhance investment options.

In this time of change and increasing international com-petition, the Federation of European Securities Exchanges(FESE) exists to represent the collective interests ofEuropean exchanges as they seek to improve their individ-ual and collective efficiency and effectiveness.

The Federation focuses on the European institutions: theCommission, Parliament and Council, as well as theCommittee of European Securities Regulators (CESR)and other regulators such as the United States SEC andCFTC.

FIAB (Federation of Ibero-AmericanExchanges)

The 19 exchange members of FIAB cover the Spanish andPortuguese language jurisdictions. The FIAB mission is to:

• foster cooperation among its members, in order to promote the development and advancement of theirsecurities markets, in the best interests of all marketparticipants

• cooperate with national and international entities having legislative, regulatory, or other functions inrespect of financial and securities markets with a viewto ensuring homogeneous standards and regulations asto securities issuance, circulation, distribution, and registration; trading; issuers; brokers; securities mar-kets; securities depositories and custodians; as well asin connection with any fiscal and other issues deemedto be relevant to market development

• promote integration of the Federation's stock markets,stimulating inter-activity among market participants aswell as the free circulation, within their respective juris-dictions, of securities issued in any of its members'home countries

• encourage the establishment of rules and proceduresensuring solvency, competence, legitimacy, and fairinformation disclosure to all savers investing throughMember Exchanges.

SAFE (South Asian Federation of Exchanges)

SAFE has 11 members in the Indian Ocean region. It is aforum launched by bourses to promote the development ofsecurities markets in the area. The inception of SAFEmarked an important milestone in the march of South Asiancapital markets towards regional and global integration.

The imperatives of globalization necessitate increasinginterdependence among nations in terms of inter-dependence among nations in terms of business, politicsand cross-cultural activities. The members of SAFE haveagreed to work towards common standards, includinginternational accounting standards and best businesspractices in capital markets. SAFE will represent its mem-bers in related international forums, encourage cross-border listing, co-operate in human resource development,facilitate technology transfer among members, andaddress other issues of common interest.

Finally, the African Stock Exchange Federation constitutesan informal, useful network of contacts in that region, too.

24