western riverside waste authority - wrwa.gov.uk · the lgps is a defined benefit statutory scheme,...

TRANSCRIPT

WESTERN

RIVERSIDE

WASTE

AUTHORITY

STATEMENT OF

ACCOUNTS

2004/05

1

CONTENTS

The Accounts Page

Foreword to the Accounts 2

Statement of Responsibilities for the Accounts 4

Certificate 4

Statement on Internal Control 5

Independent Auditor’s Report 9

Balance Sheet 10

Statement of Total Movement in Reserves 11

Cash Flow Statement and notes to the Cash Flow Statement 11

Revenue Account 13

Statement of Accounting Policies 14

Notes to the Accounts

Balance Sheet (notes 1-11) 15

Revenue Account (notes 12-23) 18

2

FOREWORD TO THE ACCOUNTS Revenue Account The General Reserve at the end of March 2005 stood at £2.585 million, down by £0.2 million over the year, due to the application of this net sum to mitigate the increase in the levy for 2004/05. The call on balances was less than expected due to lower than budgeted disposal costs of abandoned vehicles. The balance comfortably covered the Authority’s £1.5 million requirement to meet contingencies, assessed when setting the budget and levy for 2005/06. Total waste managed by the Authority increased by 1.5%, from 487,000 tonnes in 2003/04 to 494,000 tonnes in 2004/05, below the national trend of around 3% for municipal waste. Net levy borne expenditure rose by 3.3% reflecting inflation on contract costs, a further £1 per tonne increase in landfill tax and higher costs attributable to waste recycling. The net cost per head of resident population for the Authority’s services was £23.92 in 2004/05 compared with £21.67 for the previous year. Balance Sheet The Authority’s assets were revalued at 1st April 2004 from £21.7 million to £27.8 million. The net value at 31st March 2005 was £27 million after allowing for depreciation in the year. In recent years the Authority has had no capital expenditure; the Government’s expectation has been that capital investment in waste management facilities would be undertaken by the private sector. The current Waste Management Services contract provides for a range of capital investments in infrastructure, plant and machinery, in some cases subject to cash “ceilings”. The first of these investments was undertaken in 2003/04: waste transport containers to a value of £1.3 million, as an Authority asset to be written down over 10 years. However, should the contract be terminated in the interim, the Authority will be liable to reimburse the contractor for the written down value, estimated at £1.040 million at 31st March 2005. The Authority’s short term deposits were higher at 31st March 2005 than 2004, because of a later profile for payments under the Waste Management Services contract. This was mirrored by an increase in creditors. However, the Authority’s underlying financial position was strong enough to allow a £0.5 million reduction in long term debt, down to £1.5 million. All permanent staff are eligible for inclusion in the statutory Local Government Pension Scheme (LGPS) administered by the London Pension Fund Authority (LPFA). The LGPS is a defined benefit statutory scheme, administered in accordance with the Local Government Pension Scheme Regulations 1997. The gross assets of the whole of the LPFA Pension Fund as at 31st March 2005 were valued at £1,544 million. The Authority’s deemed share of these assets is £3.68 million, an increase of £0.27 million over the year. The Fund’s actuary estimated that the present value of scheme liabilities also increased over the same period by £0.93 million, from £4.72 million to £5.65 million. The net pension liability therefore increased by £0.66 million from £1.31 million to £1.97 million.

3

As a public body providing statutory services backed by powers of taxation, the Authority can be more relaxed than private firms about including such valuations in its balance sheet. However, the scale of the net liability, compared with total annual employment costs of only £0.4 million, underlines the risk of increased pension contributions that could ultimately be required. The full triennial valuation as at 31st March 2004 showed a deficit of £1.24 million. The Authority has agreed to make this up over fifteen years from 1st April 2005, with annual lump-sum contributions increasing by 4.4% a year. Conclusion Despite increased costs due, in no small measure, to statutory pressures from both landfill taxation and recycling targets, the Authority has been able to maintain a sound financial base.

4

STATEMENT OF RESPONSIBILITIES FOR THE ACCOUNTS The Authority is required to make arrangements for the proper administration of its financial affairs and to secure that one of its officers has the responsibility for the administration of those affairs. That officer is the Treasurer who accordingly is responsible for the preparation of the Authority’s statement of accounts, to present fairly the financial position at the accounting date and its income and expenditure for the year. In preparing this statement of accounts, the Treasurer has: • selected suitable accounting policies and then applied them consistently; • made judgements and estimates that were reasonable and prudent; • stated whether applicable accounting standards, and CIPFA/LASAAC Codes have been followed,

subject to any material departures disclosed and explained in the statement of accounts; • kept proper accounting records which were up to date; • taken reasonable steps for the prevention and detection of fraud and other irregularities. CERTIFICATE I certify that the statement of accounts presents fairly the financial position of Western Riverside Waste Authority at the end of the period to which it relates and its income and expenditure for that period. S HEYWOOD Treasurer T COLERIDGE Councillor Chairman of the Authority Approved by the Authority on 28th June 2005

5

STATEMENT ON INTERNAL CONTROL 2004/05 1. SCOPE OF RESPONSIBILITY Western Riverside Waste Authority is responsible for ensuring that its business is conducted in

accordance with the law and proper standards, and that public money is safeguarded and properly accounted for, and used economically, efficiently and effectively. The Authority also has a duty under the Local Government Act 1999 to make arrangements to secure continuous improvement in the way in which its functions are exercised, having regard to a combination of economy, efficiency and effectiveness. In discharging this overall responsibility, the Authority is also responsible for ensuring that there is a sound system of internal control which facilitates the effective exercise of the Authority’s functions and which includes arrangements for the management of risk.

2. THE PURPOSE OF THE SYSTEM OF INTERNAL CONTROL The system of internal control is designed to manage risk to a reasonable level rather than to eliminate all risk of failure to achieve policies, aims and objectives; it can, therefore, only provide reasonable and not absolute assurance of effectiveness. The system of internal control is based on an ongoing process designed to identify and prioritise the risks to the achievement of the Authority’s policies, aims and objectives, to evaluate the likelihood of those risks being realised and the impact should they be realised, and to manage them efficiently, effectively and economically. The system of internal control as outlined below has been in place at the Authority for the year ended 31st March 2005 and up to the date of approval of the annual report and accounts.

3. THE INTERNAL CONTROL ENVIRONMENT The key elements of the internal control environment operating within the Authority are

detailed below: Establishing and monitoring the achievement of the Authority’s Objectives The Best Value Performance Plans for 2004/05 and 2005/06 set out the Authority’s four key

objectives based upon consultation with its four constituent councils, the London Boroughs of Hammersmith and Fulham, Lambeth and Wandsworth, and the Royal Borough of Kensington and Chelsea, with residents and other stakeholders. There is a hierarchy of sub-objectives with targets and performance indicators. In year progress in implementing outcomes and the outturn position are reported to the Authority.

6

Policy and Decision Making The Authority’s Constitution and Standing Orders set out how the Authority operates, how

decisions are made, and the procedures that are followed to ensure that these are efficient, transparent and accountable to local people. The membership of the Authority comprises two elected Members appointed by each of the four constituent councils. The budget, policy framework and all key decisions are taken at Authority meetings. All meetings of the Authority are open to the press and public, but there are a small number of confidential matters considered in private. Authority officers and the officers servicing the Authority provide appropriate advice at the points of consideration and report to members on progress and the outcome of decisions taken.

Compliance with established policies, procedures, laws and regulations. Ensuring compliance with established policies, procedures, laws and regulations involves a

range of measures:

• Monitoring of compliance by the Clerk to the Authority (as the Authority’s monitoring officer), the General Manager and the Section 151 Officer. Legal advice is available via the Authority’s legal adviser.

• Regular meetings with Constituent Council Chief Executives and Technical Officers • The drawing up and circulation of guidance and advice on key procedures, policies and

practices including Codes of Conduct, Financial Regulations*, Procurement, Whistle Blowing policy and procedures and the Anti-Fraud and Anti-Corruption Policy.

• Notification of changes in the law, regulations and practice.

* Revised Financial Regulations were approved by the Authority on 1st February 2005 (Paper No. WRWA 502).

Economical, effective and efficient use of resources and securing continuous improvement The Authority has established a Best Value Review programme including action plans for

continuous improvement. The programme of reviews is agreed by the Authority and focuses upon improving the levels of efficiency and effectiveness in key areas. The structure of the Authority is such that the eight appointees from the constituent councils can monitor performance on securing the economical, effective and efficient use of resources. A significant proportion of the Authority’s costs relate to the competitively tendered long-term waste management contract which commenced on 5th October 2002 and includes a requirement to support the Authority in meeting its Best Value obligations.

7

Financial management Financial management is based on a framework of a contracts code of practice and a scheme of

delegation to officers and accountability, segregation of duties, management supervision, and administrative procedures. In particular the system includes:

• Comprehensive budgeting systems • An annual budget approved by the Authority, formally revised in the year of account as part

of the annual budget process • A medium term financial planning process • Mid-year forecast outturn reported to the Authority • Financial outturn reported annually to the Authority • Quarterly financial forecast against budget to the Board.

Performance Management The Authority’s Best Value Plan compares actual performance with performance indicators

and also includes future targets. In addition the Plan includes benchmarking comparative performance information with other joint waste disposal authorities on a number of statutory and non-statutory environmental indicators. In-year monitoring reports and year-end reviews are presented to the Authority to monitor progress and action plans for seeking continuous improvement are in place and progress reviewed.

4. REVIEW OF EFFECTIVENESS The Authority has responsibility for conducting, at least annually, a review of the effectiveness

of the system of internal control. The review is informed by the work of the internal auditors, by managers within the Authority, and by comments made by external auditors. The Internal Audit Service works with managers in assessing control environments and enhancing controls where necessary.

For 2004/05, the Authority has produced a Statement on Internal Control (SIC). The Internal

Audit Service for the Authority has coordinated the production of this SIC on behalf of the officers. In reviewing the effectiveness of the system of internal control, the review has also drawn upon the work undertaken by the Authority’s external auditor.

5. SIGNIFICANT INTERNAL CONTROL ISSUES

Internal Audit has carried out reviews of Corporate Governance, Budgetary Control and the Authority’s key financial systems. The significant internal control issues are:-

8

• Corporate Governance.

(a) Risk management is now embedded with an annual review regime. Significant policy decisions are likely to be required during 2005/06 as a result of the review of the Waste Management Service contract, and the review of the Risk Register will need to reflect these changes.

(b) The adoption of a local Code of Corporate Governance needs to be considered within the forthcoming Best Value Review which includes Corporate Governance.

(c) The mid-year report on performance to the December meeting should be comprehensive.

(d) Other priorities did not allow the Authority’s complaints procedure to be reviewed during 2004/05. However, updated procedures were reported to the October meeting of the Authority.

(e) The threats to the continuity of the Authority’s administration, including the roles of the monitoring officer and chief financial officer, were handled during the later part of 2004/05 by the appointment of interim officers. Following the conclusion of the dispute the Clerk and Treasurer were reinstated on 4th July 2005.

• Budgetary Control.

(a) The updating of detailed budget information onto budget system was reinitiated in the early part of 2004/05. This is an annual process.

(b) Officers have always undertaken budget monitoring, however, the process has been

formalised by the re-establishment of quarterly budget monitoring reports to the Management Team with effect from the first quarter 2005/06.

6. CONCLUSION We have been advised on the implications of the results of the review of the effectiveness of

the system of internal control by the Authority, and plans to address the identified weaknesses and provide improvements to the control systems in place. We are satisfied that these plans satisfactorily address the need for improvements that have been identified during the year.

G K Jones Councillor T Coleridge

Clerk Chairman of the Authority 13th October 2005 13th October 2005

9

INDEPENDENT AUDITORS’ REPORT TO WESTERN RIVERSIDE WASTE AUTHORITY We have audited the financial statements on pages 2 to 4 and 10 to 23. This report is made solely to Western Riverside Waste Authority, as a body, in accordance with Section 2 of the Audit Commission Act 1998. Our work has been undertaken so that we might state to Western Riverside Waste Authority, as a body, those matters we are required to state to it in an auditor’s report and for no other purposes. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than Western Riverside Waste Authority, as a body, for our audit work, for this report, or for the opinions we have formed. Respective Responsibilities of the Chief Financial Officer and Auditors As described on page 4, the Treasurer is responsible for preparation of the statement of accounts in accordance with the Code of Practice on Local Authority Accounting in the United Kingdom 2004: A Statement of Recommended Practice. Our responsibilities, as independent Auditors, are established by statute, the Code of Audit Practice issued by the Audit Commission and our profession’s ethical guidance. We report to you our opinion as to whether the statement of accounts presents fairly the financial position of the Authority and its income and expenditure for the year. We review whether the statement on internal control on pages 5 to 8 reflects compliance with CIPFA’s guidance The Statement on Internal Control in Local Government: Meeting the Requirements of the Accounts and Audit Regulations 2004, published on 2nd April 2004. We report if it does not comply with proper practices specified by CIPFA or if the Statement is misleading or inconsistent with other information we are aware of from our audit of the financial statements. We are not required to consider, nor have we considered, whether the statement on internal control covers all risks and controls. We are not required to form an opinion on the effectiveness of the authority’s corporate governance procedures or its risk and control procedures. Our review was not performed for any purpose connected with any specific transaction and should not be relied upon for any such purpose. Basis of Audit Opinion We conducted our audit in accordance with the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission, which requires compliance with relevant auditing standards issued by the Auditing Practices Board. An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statements. It also includes an assessment of the significant estimates and judgements made by the authority in the preparation of the financial statements, and of whether the accounting policies are appropriate to the authority’s circumstances, consistently applied and adequately disclosed. We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order to provide us with sufficient evidence to give reasonable assurance that the statement of accounts is free from material misstatement, whether caused by fraud or other irregularity or error. In forming our opinion, we evaluated the overall adequacy of the presentation of the information in the financial statements. Opinion In our opinion, the statement of accounts presents fairly the financial position of the Western Riverside Waste Authority as at 31st March 2005 and its income and expenditure for the year then ended. Certificate The appointed day for the exercise of rights of electors under the Accounts and Audit Regulations 2003 is 28th November 2005. We cannot certify that we have completed the audit of the accounts in accordance with the requirements of the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission until electors have been given the opportunity to exercise their statutory rights. KPMG LLP Chartered Accountants London 28 October 2005

10

11

BALANCE SHEET

(Note) 31st March 2005 31st March 2004 £000 £000 £000 £000 Fixed Assets Land and buildings 21,905 16,844Fixed plant and equipment 3,543 3,056Vehicles and moveable plant 1,592 1,805 (1) 27,040 21,705 Current Assets VAT repayable 1,590 826 Other debtors and accruals (2) 239 1,063 Stock (3) 100 100 Short term deposit (4) 3,319 1,578 5,248 3,567 Current Liabilities Creditors and provisions (5) 7,121 4,728 Pension deficit (6) 1,967 1,311 9,088 6,039 Net Current Assets/(Liabilities) (3,840) (2,472)Total Assets less Current Liabilities 23,200 19,233 Long term borrowing (7) 1,500 2,000 Other long term liability (8) 1,040 2,540 1,170 3,170 Total Assets less Liabilities 20,660 16,063 Fixed Asset Restatement Reserve (9) 22,810 16,890Capital Financing Reserve (10) (2,768) (2,301)Pension Reserve (1,967) (1,311)General Reserve 2,585 2,785 Total Equity 20,660 16,063

12

STATEMENT OF TOTAL MOVEMENT IN RESERVES

Capital Reserves Revenue Reserves Total

Reserves Fixed Asset

Restatement Reserve

Capital Financing Reserve

Pension Reserve

General Reserve

£000 £000 £000 £000 £000 Balance as at 1st April 16,890 (2,301) (1,311) 2,785 16,063Net surplus - - - (200) (200)Other movements 5,920 (467) (656) - 4,797 Balance at 31st March 22,810 (2,768) (1,967) 2,585 20,660

CASH FLOW STATEMENT

2004/05 2003/04 £000 £000 £000 £000 REVENUE ACTIVITIES Outflows Cash paid to and on behalf of employees 436 400 Other operating costs 22,978 26,810 23,414 27,210 Inflows Levy on constituent Authorities (20,256) (19,078) Income earned (5,327) (6,556) (25,583) (25,634)Net cash (in) flow from revenue activities (2,169) 1,576 SERVICING OF FINANCE Outflows Interest received/paid (72) (23) (72) (23) CAPITAL Outflows Loan repaid 500 500 - - Decrease(Increase) in cash and cash equivalents (1,741)

1,553

13

NOTES TO THE CASH FLOW STATEMENT

MOVEMENT IN CASH AND CASH EQUIVALENTS Balance

31.3.05 Movement

In the Year Balance

31.3.04 Movement

in the Year Balance

31.3.03 £000 £000 £000 £000 £000 Deposits (3,319) (1,741) (1,578) 1,701 (3,279)Overdraft - - - (148) 148 Cash and Cash Equivalents (3,319) (1,741) (1,578) 1,553 (3,131)

RECONCILIATION OF REVENUE ACCOUNT TO CASH FLOW FROM REVENUE ACTIVITIES 2004/05 2003/04 £000 £000 £000 £000 Revenue account (surplus)/deficit 200 (1,096) Non cash transactions Depreciation (715) (736) Revenue provision for debt redemption (248) (258) Provisions set aside 78 (156) Contributions to reserves (1) (12) (886) (1,162) Other items, including those on an accruals basis Increase/(decrease) in debtors (60) (108) Other adjustments 1,048 771 (Increase)/decrease in creditors (2,471) 3,171 (1,483) 3,834 Net cash (in) flow from revenue activities (2,169) 1,576

14

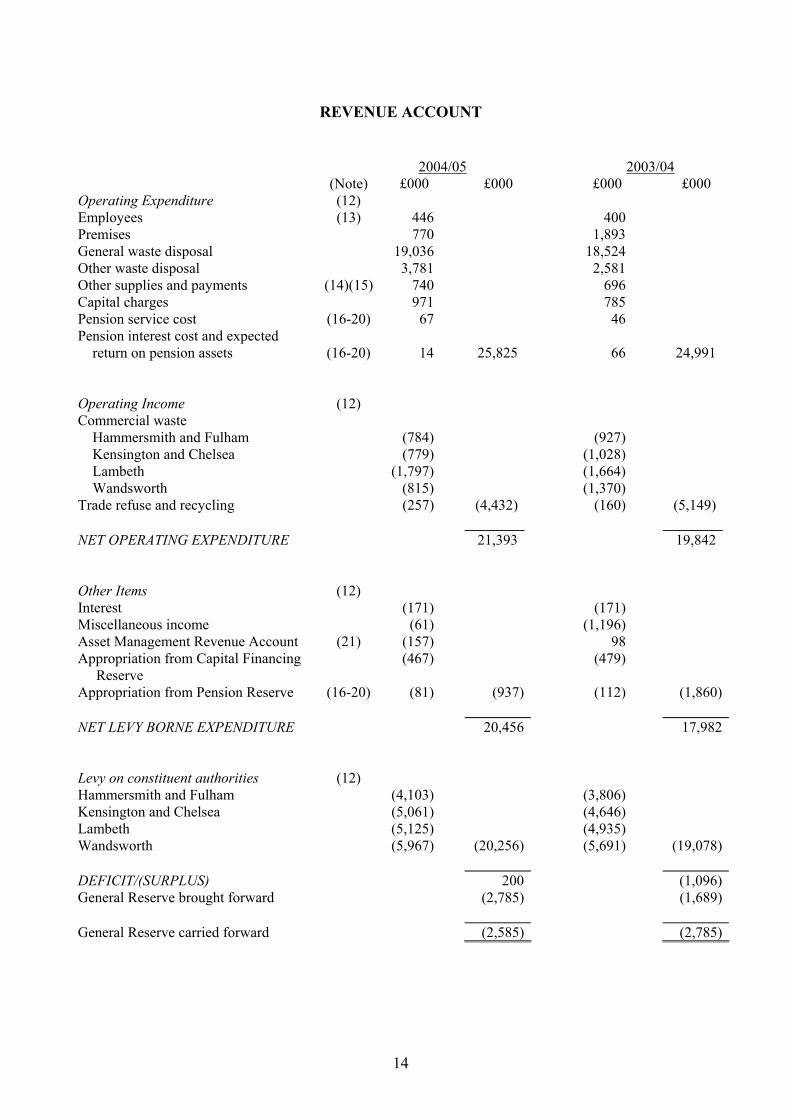

REVENUE ACCOUNT 2004/05 2003/04 (Note) £000 £000 £000 £000 Operating Expenditure (12) Employees (13) 446 400 Premises 770 1,893 General waste disposal 19,036 18,524 Other waste disposal 3,781 2,581 Other supplies and payments (14)(15) 740 696 Capital charges 971 785 Pension service cost (16-20) 67 46 Pension interest cost and expected return on pension assets

(16-20)

14

25,825

66

24,991

Operating Income (12) Commercial waste Hammersmith and Fulham (784) (927) Kensington and Chelsea (779) (1,028) Lambeth (1,797) (1,664) Wandsworth (815) (1,370) Trade refuse and recycling (257) (4,432) (160) (5,149) NET OPERATING EXPENDITURE 21,393 19,842 Other Items (12) Interest (171) (171) Miscellaneous income (61) (1,196) Asset Management Revenue Account (21) (157) 98 Appropriation from Capital Financing Reserve

(467) (479)

Appropriation from Pension Reserve (16-20) (81) (937) (112) (1,860) NET LEVY BORNE EXPENDITURE 20,456 17,982 Levy on constituent authorities (12) Hammersmith and Fulham (4,103) (3,806) Kensington and Chelsea (5,061) (4,646) Lambeth (5,125) (4,935) Wandsworth (5,967) (20,256) (5,691) (19,078) DEFICIT/(SURPLUS) 200 (1,096)General Reserve brought forward (2,785) (1,689) General Reserve carried forward (2,585) (2,785)

15

STATEMENT OF ACCOUNTING POLICIES General Principles The general principles adopted in the compiling and presentation of the accounts are those recommended in the Chartered Institute of Public Finance and Accountancy (CIPFA)/Local Authority (Scotland) Accounts Advisory Committee (LASAAC) Code of Practice on Local Authority Accounting in the United Kingdom, which is recognised by statute as representing proper accounting practice. Debtors and Creditors Revenue transactions are accounted for on the basis of income and expenditure attributable to the year, establishing debtors and creditors amounts on the basis of estimates where necessary, with the exception of charges accruing annually that are not material compared to total income and expenditure. Stocks The value of stock has been progressively written down to £100,000 to take account of potential stock obsolescence under the current waste management contract and this valuation was confirmed by the General Manager on a sample valuation basis in October 2002. Fixed Assets Expenditure on the acquisition, creation or enhancement of fixed assets is included in the accounts on a receipts and payments basis, where accruals are not material. Fixed assets are valued at five yearly intervals in accordance with the Statements of Asset Valuation Principles and Guidance Notes issued by The Royal Institution of Chartered Surveyors (RICS), although material changes to asset valuations would be adjusted in the interim period, as and when they occurred. A valuation was undertaken during 2005/06 to reflect values as at 1st April 2004. Capital Charges All operational assets, other than land, are depreciated on a straight line basis over the expected life of the asset. Operating Expenditure also includes a capital financing charge determined by applying a specified rate of interest to net asset values. The specified rate is currently 3.5%. External interest payable and a statutory provision for debt redemption are charged to the Asset Management Revenue Account, which is credited with capital charges made to Operating Expenditure. Capital charges, therefore, have a neutral impact on the amounts required to be raised from the levy. Amounts set aside from revenue to finance capital expenditure or as transfers to other earmarked reserves are disclosed separately as appropriations.

16

NOTES TO THE ACCOUNTS

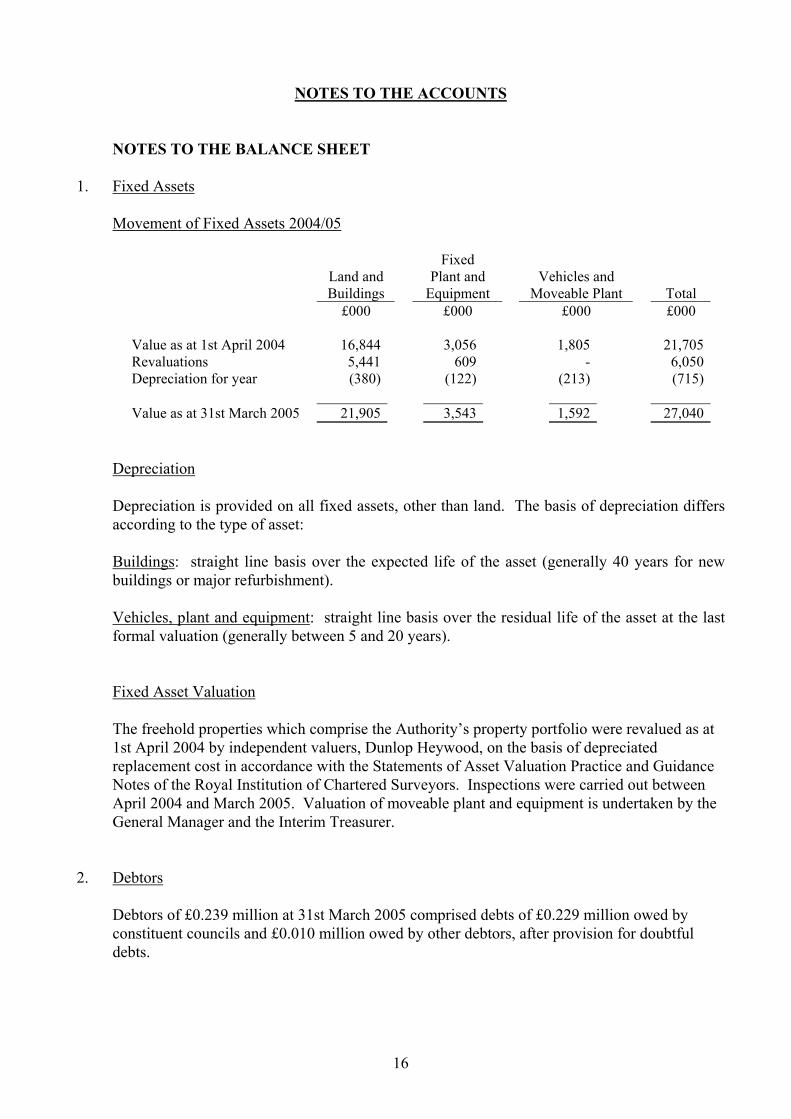

NOTES TO THE BALANCE SHEET 1. Fixed Assets Movement of Fixed Assets 2004/05

Land and Buildings

Fixed Plant and

Equipment

Vehicles and

Moveable Plant

Total £000 £000 £000 £000 Value as at 1st April 2004 16,844 3,056 1,805 21,705Revaluations 5,441 609 - 6,050Depreciation for year (380) (122) (213) (715) Value as at 31st March 2005 21,905 3,543 1,592 27,040

Depreciation Depreciation is provided on all fixed assets, other than land. The basis of depreciation differs

according to the type of asset: Buildings: straight line basis over the expected life of the asset (generally 40 years for new

buildings or major refurbishment). Vehicles, plant and equipment: straight line basis over the residual life of the asset at the last

formal valuation (generally between 5 and 20 years). Fixed Asset Valuation The freehold properties which comprise the Authority’s property portfolio were revalued as at

1st April 2004 by independent valuers, Dunlop Heywood, on the basis of depreciated replacement cost in accordance with the Statements of Asset Valuation Practice and Guidance Notes of the Royal Institution of Chartered Surveyors. Inspections were carried out between April 2004 and March 2005. Valuation of moveable plant and equipment is undertaken by the General Manager and the Interim Treasurer.

2. Debtors Debtors of £0.239 million at 31st March 2005 comprised debts of £0.229 million owed by

constituent councils and £0.010 million owed by other debtors, after provision for doubtful debts.

17

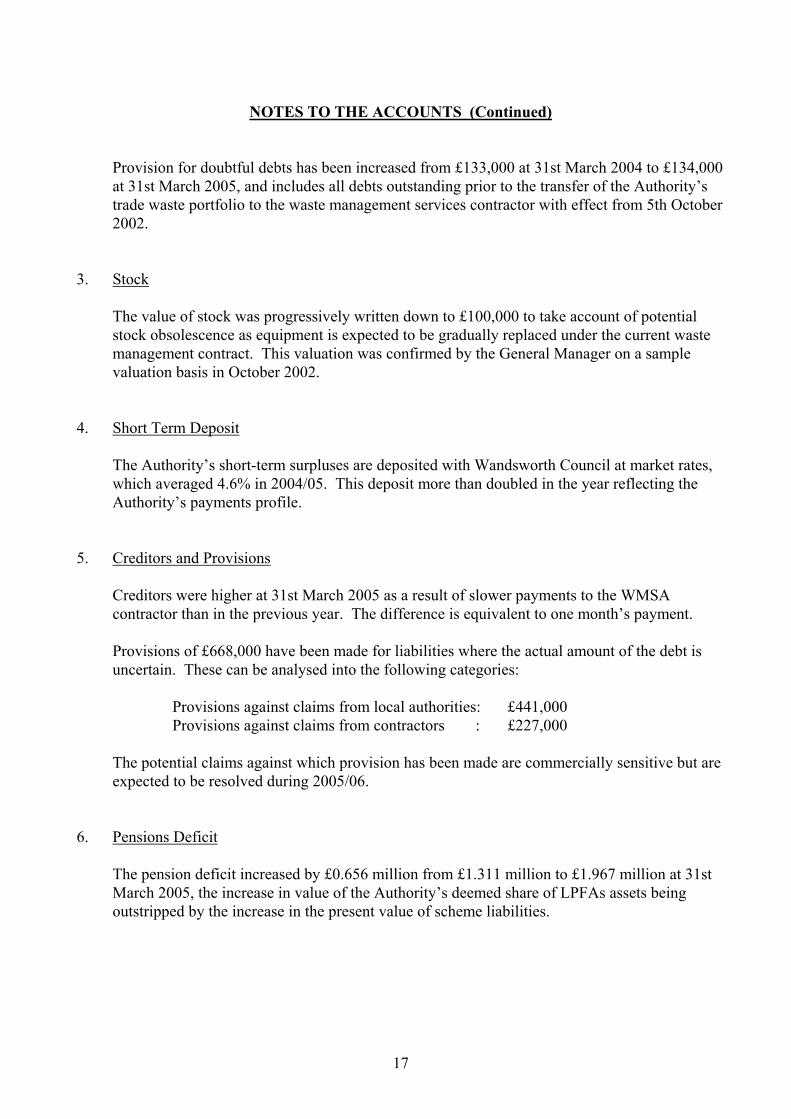

NOTES TO THE ACCOUNTS (Continued) Provision for doubtful debts has been increased from £133,000 at 31st March 2004 to £134,000

at 31st March 2005, and includes all debts outstanding prior to the transfer of the Authority’s trade waste portfolio to the waste management services contractor with effect from 5th October 2002.

3. Stock The value of stock was progressively written down to £100,000 to take account of potential

stock obsolescence as equipment is expected to be gradually replaced under the current waste management contract. This valuation was confirmed by the General Manager on a sample valuation basis in October 2002.

4. Short Term Deposit The Authority’s short-term surpluses are deposited with Wandsworth Council at market rates,

which averaged 4.6% in 2004/05. This deposit more than doubled in the year reflecting the Authority’s payments profile.

5. Creditors and Provisions Creditors were higher at 31st March 2005 as a result of slower payments to the WMSA

contractor than in the previous year. The difference is equivalent to one month’s payment. Provisions of £668,000 have been made for liabilities where the actual amount of the debt is

uncertain. These can be analysed into the following categories: Provisions against claims from local authorities: £441,000

Provisions against claims from contractors : £227,000 The potential claims against which provision has been made are commercially sensitive but are

expected to be resolved during 2005/06. 6. Pensions Deficit The pension deficit increased by £0.656 million from £1.311 million to £1.967 million at 31st

March 2005, the increase in value of the Authority’s deemed share of LPFAs assets being outstripped by the increase in the present value of scheme liabilities.

18

NOTES TO THE ACCOUNTS (Continued) 7. Long Term Borrowing All long term borrowing is from the Public Works Loan Board. An analysis of the debt as at

31st March 2005 is shown below:

Maturity Within: £000 Ave. Rate (%) 2 - 3 years 500 5.625 4 - 5 years 500 4.875 5 - 10 years 500 5.625 1,500 5.375

One loan of £0.5 million was repaid during 2004/05. 8. Other Long Term Liability. The Waste Management Services contract that commenced in

October 2002 provides for a range of capital investments in infrastructure, plant and machinery. The first of these investments was undertaken in 2004/05: containers to a value of £1.3 million as at 1st April 2003. This is an Authority asset to be written down over 10 years. However, should the contract be terminated in the interim, the Authority will be liable to reimburse the contractor for the written down value. The £1.04 million represents the potential liability to the contractor and is matched by an equivalent value of fixed assets.

9. Fixed Asset Restatement Reserve

2004/05 2003/04 £000 £000 Balance brought forward 16,890 16,755 Surplus on revaluation of fixed assets 6,050 5 Other movements ( 130) 130 Balance carried forward 22,810 16,890

The balance represents the difference between the historic cost of assets and their current valuation. The reserve is adjusted for differences arising on revaluations and for disposals.

10. Capital Financing Account The capital financing account contains the amounts contributed from the Revenue Account for

the repayment of external loans, and for meeting capital expenditure. The reserve is reduced by depreciation.

2004/05 2003/04 £000 £000 Balance brought forward (2,301) (1,822)Revenue provision for debt redemption 248 258Depreciation provision (715) (737) Balance carried forward (2,768) (2,301)

19

NOTES TO THE ACCOUNTS (Continued)

11. Capital Financing Account (continued) Provision for Credit Liabilities (memorandum Account)

2004/05 2003/04 £000 £000 Balance brought forward 1,098 840Amount set aside for minimum revenue provision 248 258Amount used to repay debt (500) - Balance carried forward 846 1,098

NOTES TO THE REVENUE ACCOUNT 12. The general principles adopted in compiling the accounts are those recommended by the

CIPFA/LASAAC Code of Practice, however, the presentation reflects features of specific relevance for the statutory waste disposal sector.

13. Staff Remuneration

The following table shows the number of staff whose taxable pay was in the relevant £10,000 range:

Range of Taxable Pay No. of Staff 2004/05 No. of Staff 2003/04

£50,001 - £60,000 1 1 £100,001 - £110,000 1 1

14. Publicity The costs in the Revenue Account include the following amounts spent on publicity:

2004/05 2003/04 £ £

7,550 16,158 15. External Audit Fees. The costs in the Revenue Account include payments of £23,000 to the

Authority’s External Auditors, KPMG.

20

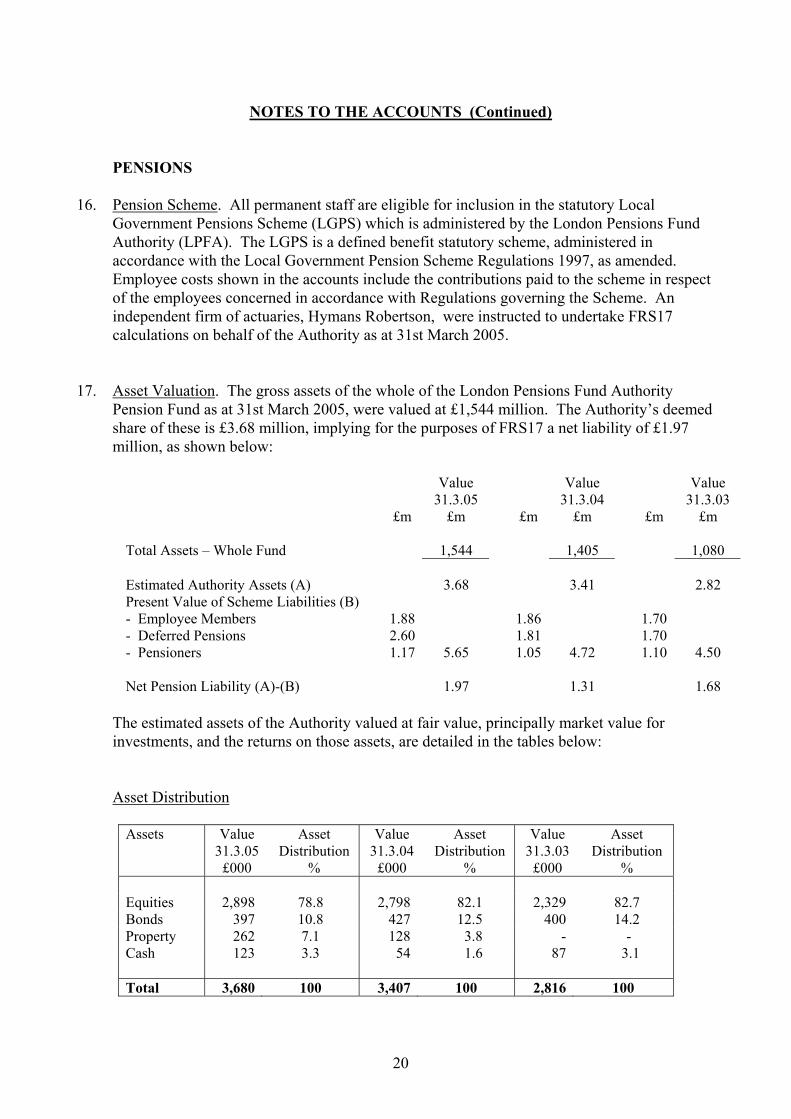

NOTES TO THE ACCOUNTS (Continued) PENSIONS 16. Pension Scheme. All permanent staff are eligible for inclusion in the statutory Local

Government Pensions Scheme (LGPS) which is administered by the London Pensions Fund Authority (LPFA). The LGPS is a defined benefit statutory scheme, administered in accordance with the Local Government Pension Scheme Regulations 1997, as amended. Employee costs shown in the accounts include the contributions paid to the scheme in respect of the employees concerned in accordance with Regulations governing the Scheme. An independent firm of actuaries, Hymans Robertson, were instructed to undertake FRS17 calculations on behalf of the Authority as at 31st March 2005.

17. Asset Valuation. The gross assets of the whole of the London Pensions Fund Authority Pension Fund as at 31st March 2005, were valued at £1,544 million. The Authority’s deemed share of these is £3.68 million, implying for the purposes of FRS17 a net liability of £1.97 million, as shown below:

£m

Value 31.3.05

£m

£m

Value 31.3.04

£m

£m

Value 31.3.03

£m

Total Assets – Whole Fund 1,544 1,405 1,080 Estimated Authority Assets (A) 3.68 3.41 2.82 Present Value of Scheme Liabilities (B) - Employee Members 1.88 1.86 1.70 - Deferred Pensions 2.60 1.81 1.70 - Pensioners 1.17 5.65 1.05 4.72 1.10 4.50 Net Pension Liability (A)-(B) 1.97 1.31 1.68

The estimated assets of the Authority valued at fair value, principally market value for

investments, and the returns on those assets, are detailed in the tables below: Asset Distribution

Assets Value 31.3.05

£000

Asset Distribution

%

Value 31.3.04

£000

Asset Distribution

%

Value 31.3.03

£000

Asset Distribution

% Equities 2,898 78.8 2,798 82.1 2,329 82.7 Bonds 397 10.8 427 12.5 400 14.2 Property 262 7.1 128 3.8 - - Cash 123 3.3 54 1.6 87 3.1 Total 3,680 100 3,407 100 2,816 100

21

NOTES TO THE ACCOUNTS (Continued)

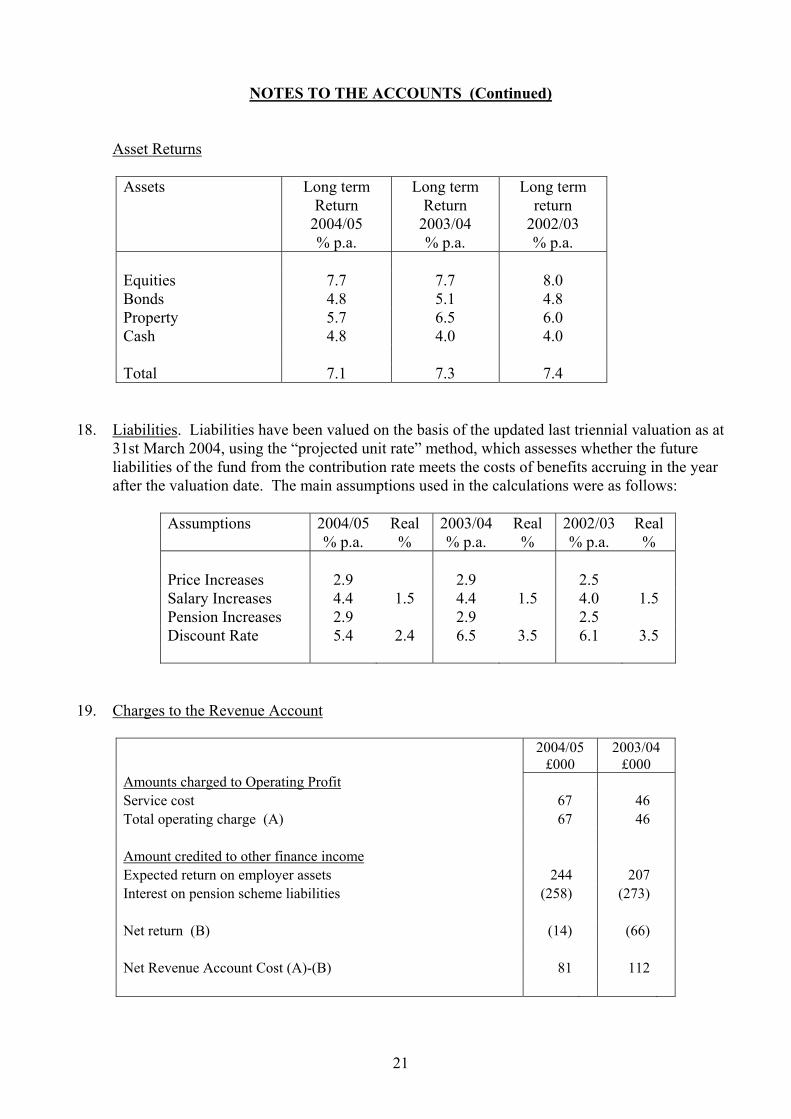

Asset Returns

Assets Long term Return

2004/05 % p.a.

Long term Return

2003/04 % p.a.

Long term return

2002/03 % p.a.

Equities 7.7 7.7 8.0 Bonds 4.8 5.1 4.8 Property 5.7 6.5 6.0 Cash 4.8 4.0 4.0 Total 7.1 7.3 7.4

18. Liabilities. Liabilities have been valued on the basis of the updated last triennial valuation as at

31st March 2004, using the “projected unit rate” method, which assesses whether the future liabilities of the fund from the contribution rate meets the costs of benefits accruing in the year after the valuation date. The main assumptions used in the calculations were as follows:

Assumptions 2004/05

% p.a. Real %

2003/04% p.a.

Real %

2002/03 % p.a.

Real %

Price Increases 2.9 2.9 2.5 Salary Increases 4.4 1.5 4.4 1.5 4.0 1.5 Pension Increases 2.9 2.9 2.5 Discount Rate 5.4 2.4 6.5 3.5 6.1 3.5

19. Charges to the Revenue Account

2004/05

£000 2003/04

£000 Amounts charged to Operating Profit Service cost 67 46 Total operating charge (A) 67 46 Amount credited to other finance income Expected return on employer assets 244 207 Interest on pension scheme liabilities (258) (273) Net return (B) (14) (66) Net Revenue Account Cost (A)-(B) 81 112

22

NOTES TO THE ACCOUNTS (Continued)

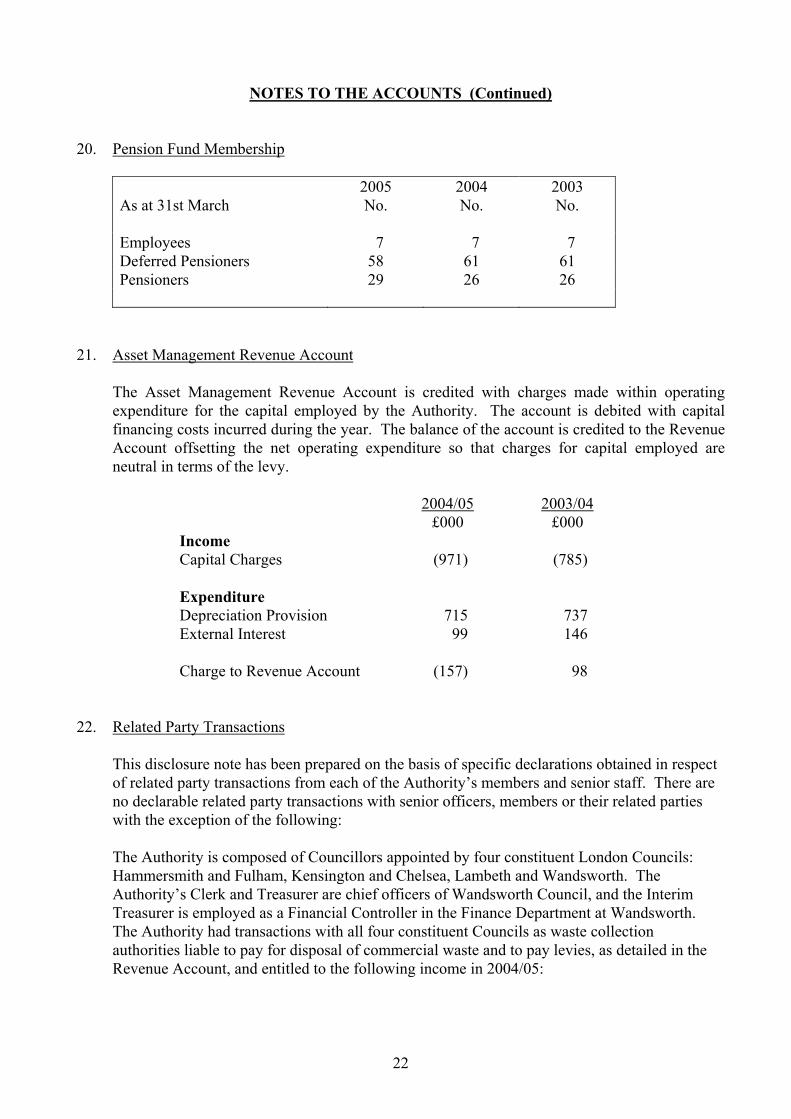

20. Pension Fund Membership

As at 31st March

2005 No.

2004 No.

2003 No.

Employees 7 7 7 Deferred Pensioners 58 61 61 Pensioners 29 26 26

21. Asset Management Revenue Account

The Asset Management Revenue Account is credited with charges made within operating expenditure for the capital employed by the Authority. The account is debited with capital financing costs incurred during the year. The balance of the account is credited to the Revenue Account offsetting the net operating expenditure so that charges for capital employed are neutral in terms of the levy.

2004/05 2003/04 £000 £000 Income Capital Charges (971) (785) Expenditure Depreciation Provision 715 737 External Interest 99 146 Charge to Revenue Account (157) 98

22. Related Party Transactions This disclosure note has been prepared on the basis of specific declarations obtained in respect

of related party transactions from each of the Authority’s members and senior staff. There are no declarable related party transactions with senior officers, members or their related parties with the exception of the following:

The Authority is composed of Councillors appointed by four constituent London Councils:

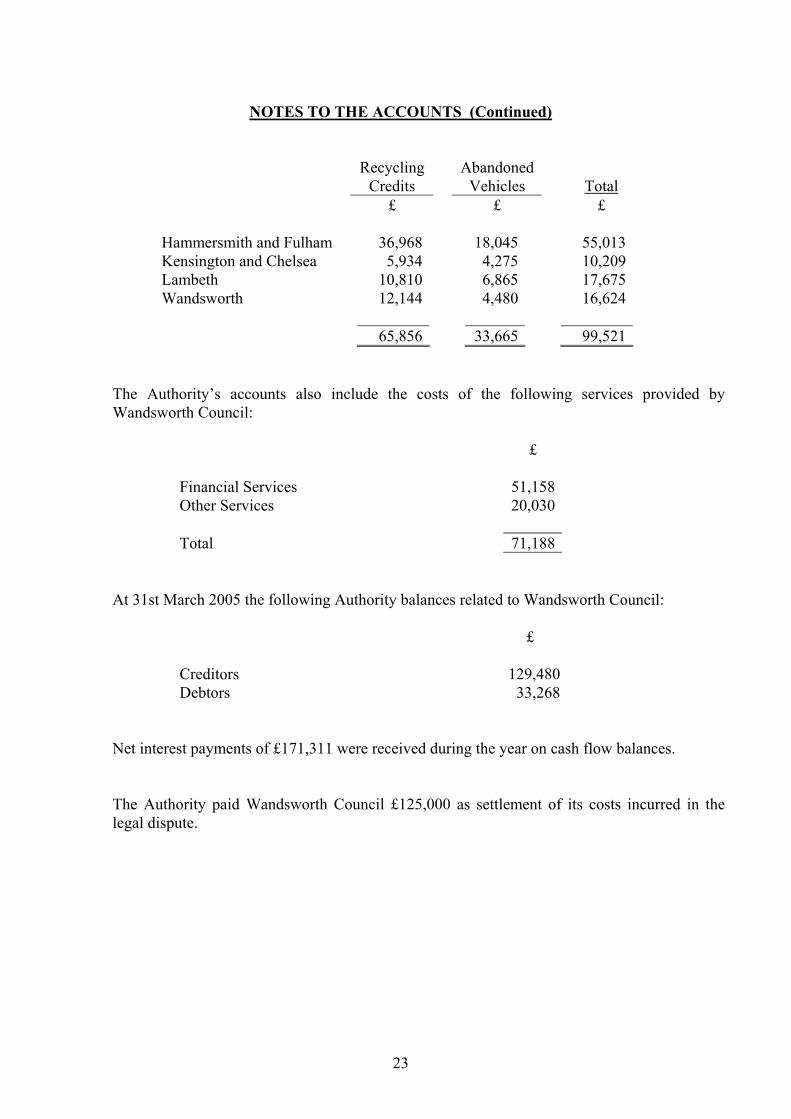

Hammersmith and Fulham, Kensington and Chelsea, Lambeth and Wandsworth. The Authority’s Clerk and Treasurer are chief officers of Wandsworth Council, and the Interim Treasurer is employed as a Financial Controller in the Finance Department at Wandsworth. The Authority had transactions with all four constituent Councils as waste collection authorities liable to pay for disposal of commercial waste and to pay levies, as detailed in the Revenue Account, and entitled to the following income in 2004/05:

23

NOTES TO THE ACCOUNTS (Continued)

Recycling Credits

Abandoned Vehicles

Total

£ £ £

Hammersmith and Fulham 36,968 18,045 55,013 Kensington and Chelsea 5,934 4,275 10,209 Lambeth 10,810 6,865 17,675 Wandsworth 12,144 4,480 16,624 65,856 33,665 99,521

The Authority’s accounts also include the costs of the following services provided by

Wandsworth Council:

£

Financial Services 51,158Other Services 20,030 Total 71,188

At 31st March 2005 the following Authority balances related to Wandsworth Council:

£

Creditors 129,480 Debtors 33,268

Net interest payments of £171,311 were received during the year on cash flow balances. The Authority paid Wandsworth Council £125,000 as settlement of its costs incurred in the

legal dispute.

24

NOTES TO THE ACCOUNTS (Continued) The son of the General Manager, Mr. James, is employed by Packaging Datastore Ltd. (PDL),

a company acquired by Cory Environmental Management Limited (CEML) in October 2003. The principal business of PDL is to provide data collection, analysis, interpretation and presentation services to retailers and wholesalers. Cory Environmental Limited, the company to which the Cory is contracted for its waste management functions, is a subsidiary of CEML. The Authority had the following transactions with Cory Environmental Limited in 2004/05:

Waste Management Contract: £22.7 million 23. During 2004/05 the Authority sought judicial review of a decision by Wandsworth Council,

which the Authority believed undermined its power of direction, and made appropriate arrangements for handling the conflicts of interest of those officers who are both officers of the Authority and Wandsworth Council. This included the appointment of an Interim Clerk and an Interim Treasurer for the period 23rd November 2004 until 3rd July 2005. The Clerk and Treasurer were reinstated on 4th July 2005 following a Judicial Review hearing, which found in Wandsworth’s favour, and after declarations by both the Authority and Wandsworth Council that the dispute was resolved.