western hvdc final funding review - pöyry · 7 western hvdc final funding review a report to ofgem...

TRANSCRIPT

7

WESTERN HVDC FINAL FUNDING REVIEW

A report to Ofgem April 2012

WE

ST

ER

N H

VD

C F

INA

L F

UN

DIN

G R

EV

IEW

Commercially sensitive content has been removed for the public version of the report.

WESTERN HVDC FINAL FUNDING REVIEW

April2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

PÖYRY MANAGEMENT CONSULTING

Contact details

Name Email Telephone

Mike Wilks [email protected] 01865 812 251

Pöyry is a global consulting and engineering firm. Our in-depth expertise extends across the fields of energy, industry, urban & mobility and water & environment.

Pöyry plc has 7000 experts operating in 50 countries and net sales of EUR 682 million (2010). The company‟s shares are quoted on NASDAQ OMX Helsinki (Pöyry PLC: POY1V).

Pöyry Management Consulting provides leading-edge consulting and advisory services covering the whole value chain in energy, forest and other process industries. Our energy practice is the leading provider of strategic, commercial, regulatory and policy advice to Europe's energy markets. Our energy team of 200 specialists, located across 14 European offices in 12 countries, offers unparalleled expertise in the rapidly changing energy sector.

Copyright © 2012 Pöyry Management Consulting (UK) Ltd

All rights reserved

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without the prior written permission of Pöyry Management Consulting (UK) Ltd (“Pöyry”).

This report is provided to the legal entity identified on the front cover for its internal use only. This report may not be provided, in whole or in part, to any other party without the prior written permission of an authorised representative of Pöyry. In such circumstances additional fees may be applicable and the other party may

-

Important

This document contains confidential and commercially sensitive information. Should any requests for disclosure of information contained in this document be received (whether pursuant to; the Freedom of Information Act 2000, the Freedom of Information Act 2003 (Ireland), the Freedom of Information Act 2000 (Northern Ireland), or otherwise), we request that we be notified in writing of the details of such request and that we be consulted and our comments taken into account before any action is taken.

Disclaimer

While Pöyry considers that the information and opinions given in this work are sound, all parties must rely upon their own skill and judgement when making use of it. Pöyry does not make any representation or warranty, expressed or implied, as to the accuracy or completeness of the information contained in this report and assumes no responsibility for the accuracy or completeness of such information. Pöyry will not assume any liability to anyone for any loss or damage arising out of the provision of this report.

WESTERN HVDC FINAL FUNDING REVIEW

April2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

PÖYRY MANAGEMENT CONSULTING

TABLE OF CONTENTS

EXECUTIVE SUMMARY 1

1. INTRODUCTION 7

1.1 Overview of the Review 7

1.2 Overview of requirements 9

1.3 Project deliverables and associated tasks 10

2. OUTPUT 1 – SUMMARY OF FINAL PLANS 13

2.1 Overview of approach 13

2.2 Consolidation of details of final contract and non-contract costs: 13

2.3 Evolution of Project Risks from Aug 11 to Jan 12 Position 24

2.4 Evolution of Project Risk from Jan 12 to Feb 12 Position 28

2.5 Consolidating information on key risks from risk register 31

2.6 Highlighting key changes in the above since SKM‟s review 33

2.7 Conclusions 34

3. OUTPUT 2 – REVIEW OF FINAL STAGES OF PROCESS TOWARDS CONTRACT AWARD 37

3.1 Overview of approach 37

3.2 High level review of tender evaluation process 37

3.3 Review of approach to managing outstanding delivery risks 44

4. OUTPUT 3 – RECOMMENDATIONS ON RISK SHARING ARRANGEMENTS 47

4.1 Assessing risk profile of the project 47

4.2 Developing a risk methodology 49

4.3 Applying this risk methodology to key risks 52

4.4 Summary 55

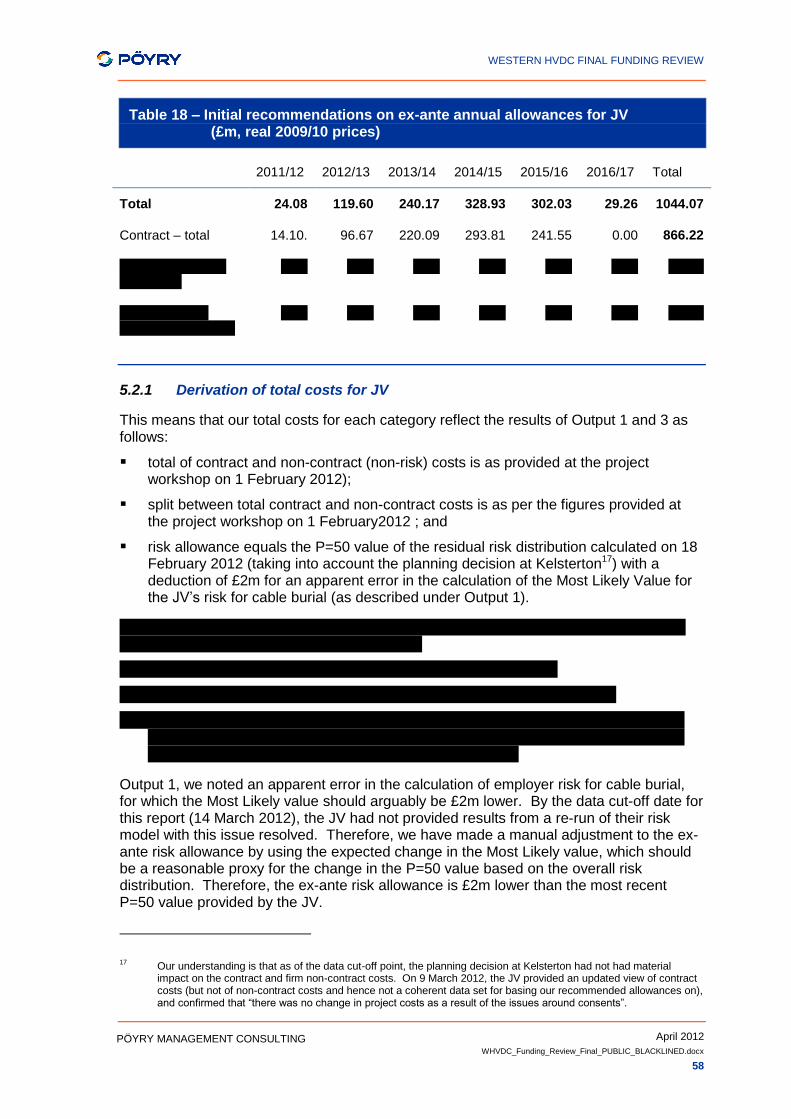

5. OUTPUT 4 – RECOMMENDATIONS ON ANNUAL EX-ANTE FUNDING ALLOWANCES 57

5.1 Overview of approach 57

5.2 Recommended ex-ante allowances 57

6. OUTPUT 5 – RECOMMENDATIONS ON DELIVERABLES TO BE ASSOCIATED WITH FUNDING ALLOWANCES 61

6.1 Overview of approach 61

6.2 Key project milestones 61

6.3 Technical output measures 65

6.4 Additional technology risks 67

7. OUTPUT 6 – RECOMMENDATIONS ON BENCHMARKING OF HVDC COSTS 69

7.1 Overview of approach 69

WESTERN HVDC FINAL FUNDING REVIEW

April2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

PÖYRY MANAGEMENT CONSULTING

8. OUTPUT 7 – IDENTIFICATION OF ANY LIMITATIONS IN THE RECOMMENDATIONS 75

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

1

PÖYRY MANAGEMENT CONSULTING

EXECUTIVE SUMMARY

Introduction

The Western HVDC Link as proposed by NGET and SPT would be an undersea cable, running from Hunterston in Scotland to Deeside in England, providing c.2GW of additional transfer capability across the B6, B7 and B7a boundaries. The project is being funded under the Transmission Investment Incentives (TII) framework.

The project is currently being funded under the Transmission Investment Incentives (TII) framework until the end of March 2013. Thereafter, it will be subject to ongoing funding arrangements under the RIIO-T1 price control.

The objectives of this assessment are to support Ofgem in regard to the following three objectives:

the final stage of Ofgem‟s assessment of funding request in relation to construction works on the HVDC component of the Western HVDC Link,

the determination of appropriate funding provisions under TII and RIIO-T1 including any specific risk sharing arrangements to apply

establishing unit cost benchmarks for wider application to similar projects under RIIO-T1.

Table 1 lists the specific outputs and deliverables requested by Ofgem, and is reflected in the structure of this report, which addresses each of the „key outputs‟ in turn.

Table 1 – Project outputs and associated tasks

Key outputs Key tasks in delivery of key outputs

1: Summary of final plans of the TOs which are used as the basis for determination of funding arrangements under TII and RIIO-T1

1. Consolidating detailed information on preferred solution / final contract:

final costs (with detailed breakdown by cost item and TO), design (including technical specification) and programme (with key milestones and dates);

treatment of project risks within contract and assumptions underpinning these; and

any additional risk allowances proposed by the TOs for factors not reflected in the contract costs.

2. Consolidating information on key risks from risk register and identifying any outstanding delivery risks with a bearing on the terms of the contract including any cancellation provisions

3. Highlighting key changes in the above since SKM‟s review 2: Review of final stages of TOs‟ process towards contract award

4. High level review of the final stages of the TOs‟ tender evaluation process against the planned process reviewed by SKM, and giving a view on extent to which the planned contracting strategy has been followed.

5. Reviewing the TOs‟ approach to managing outstanding delivery risks, and giving a view on the appropriateness of how this is reflected in terms of contract award as summarised in item 1.

3: Recommendations on risk sharing arrangements between TOs and consumers under TII and RIIO-T1

6. Assessing the risk profile of the project, identifying any material differences in characteristics compared to works funded under TII to date, and giving a view on implications for risk sharing arrangements under TII and RIIO-T1

7. Developing a risk methodology, using appropriate criteria, for identifying which risks should be: reflected in ex ante allowances; dealt with ex post; or borne by the TOs

8. Applying this risk methodology to key risks, and giving a view on the reasonableness of the costs assigned to those risks in item 1, taking into account expected likelihood and impact and TO methodology for developing risk-normalised costs

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

2

PÖYRY MANAGEMENT CONSULTING

Key outputs Key tasks in delivery of key outputs

4: Recommendations on annual ex ante funding allowances under TII and RIIO-T1

9. Proposing annual ex ante funding allowances for each TO under TII and RIIO-T1, with reference to the final costs identified in item 1 above and any specific adjustments to those costs, e.g. in line with recommendations under item 3 or to take account of overlaps with any existing funding

5: Recommendations on deliverables to be associated with funding allowances under TII and RIIO-T1

10. Proposing annual key project milestones which are consistent with the planned programme

11. Proposing technical output measures which are consistent with the final design and reflect the expected benefits (thermal, voltage and/or stability) across relevant system boundaries on completion of construction works

6: Recommendations on benchmarking of HVDC costs for wider application

12. Consolidating high level information on costs and design of all viable bids/combinations, and applying this and own data sources in proposing unit cost benchmarks at component level (convertor stations, DC cables, harmonic filters etc.), onshore civil work, undersea cable laying and by applied technology (e.g. Voltage Source Converter, Current Source Converter)

7: Identification of any limitations in the recommendations

13. Where applicable, identifying extent to which the depth of the review and resulting recommendations are limited by gaps or delays in provision of relevant information by the TOs

Recommendations

Our final recommendations on the methodology for risk-sharing arrangements are:

cost allocation ratio of 70% (NGET) and 30% (SPT);

RIIO-T1 sharing factors to be used for TII period;

for both NGET and SPT, a sharing factor of 50% to be used, consistent with the treatment of the project as a single entity in the rest of the funding arrangements; and

P=50 value from the residual risk distribution to be used in the calculation of ex-ante residual risk allowance, given existence of reopener provisions.

Our provisional recommended annual ex-ante allowances for each TO are shown in Table 2 – they reflect our findings for each Output and the data available to us as of the agreed data cut-off point for this report of 14 March 2012.

Table 2 – Provisional recommendations on ex-ante allowances by TO and by cost pot (£m, real 2009/10 money)

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 Total

Contract

NGET 9.87 67.67 154.06 205.67 169.09 0.00 606.35

SPT 4.23 29.00 66.03 88.14 72.47 0.00 259.87

XXXXXXXXXXXXXX

XXXX XXX XXX XXX XXX XXX XXX XXXX

XXX XXX XXX XXX XXX XXX XXX XXXX

XXXXXXXXX

XXXX XXX XXX XXX XXX XXX XXX XXXX

XXX XXX XXX XXX XXX XXX XXX XXXX

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

3

PÖYRY MANAGEMENT CONSULTING

We note (under Output 7) as some data issues remained unresolved at that point, we have described our recommendations on the allowances themselves as provisional. This is because they are based on the information available as of the data cut-off point for this report, and may be updated by Ofgem, in line with the methodology set out above. This will allow Ofgem to take account of updated data available at the final data freeze date (to be set by Ofgem) for determining the final annual ex-ante funding allowances.

We now discuss the supporting evidence for these recommendations.

Output 1

In our view, NGET/SPT overall provided a thorough and well justified explanation of:

how final contract costs have been arrived at, relative to the August 2011 position;

how project risks have been passed to the contractor, and the demonstrably positive impact of this on the overall project cost;

how their understanding of risks not covered by the contract has evolved, with reduction in the „best view but increase in the „maximum‟ assumption driven by cable burial risks.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXX

Output 2

NGET/SPT clearly faced a complex procurement in a constrained market with limited capacity. The procurement process appears to have been followed as designed and it is hard to conceive of an alternative process which would have been any significant improvement.

Overall it is our view that the process has led, ultimately, to an efficient outcome, based on the proviso that the 600 kV solution can be delivered at its full stated rating. Even were this not to be the case ultimately, the value of this as a potential option is such that it can be argued that it was worth the JV taking this path and taking on the technology risk in view of the potential benefits. We therefore consider that the JV took a reasonable and balanced approach to the costs and risks of the solution finally selected.

Our conclusion is that the principles applied to the approach of passing risk to the contractor during negotiations were appropriate, and that the JV have arguably negotiated as effectively as their position permits.

Output 3

Our recommendations on the areas of risk-sharing arrangements highlighted by Ofgem are described above.

Ofgem provided guidance that the capex efficiency incentive sharing factors to apply under RIIO-T1 are determined separately and could potentially differ between the TOs. It is Poyry‟s view that an alternative solution may better meet the principle to treat the

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

4

PÖYRY MANAGEMENT CONSULTING

project as whole. Different capex efficiency incentive sharing factors would mean that each TO has a different exposure to risk from this JV, although they do not necessarily differ in their ability to manage the risk faced by the JV. . Therefore, we would support a sharing factor of 50% for this project, in line with the Initial Proposals for SPT for RIIO-T11. This would be consistent with the treatment of the project as a single entity in the rest of the funding arrangements.

The choice of the sharing factor for the Western Link project should not fetter Ofgem‟s ability to set a different sharing factor for NGET in RIIO-T1 as a whole. We acknowledge that it would not be ideal to have a separate sharing factor for Western HVDC Link as for other projects. However, the regulatory attention on the Western HVDC Link project means that there should be little risk of this distorting behaviour (e.g. through the TO being able to move costs between this project and general RIIO-T1 spend).

Output 4

Our provisional recommended annual ex-ante allowances for each TO are shown in Table 2 – they reflect the findings of the other Outputs of this project, and the data available to us at the data-cut off point for the purposes of this report (14 March 2012). The annual allowances are determined by the total cost figures for each cost category (contract, firm non-contract and ex-ante risk) and the assumed annual profile of each cost category.

We have based our provisional recommended allowances on the most recent appropriate costs provided by the JV before 14 March 2012, the cut-off date for data to be considered in this report. Therefore, these allowances are provisional as they will need to be updated based on the cost and risk position as of the data freeze point to be determined by Ofgem.

The annual profiles for the allowance for the JV in each funding category have been based on data provided by the JV on 16 February 2012 for non-risk costs, and 12 March 2012 for risk costs (although applying to risk totals provided on 18 February 2012).

Output 5

The programme proposed by NGET and SPT (“Western Link Construction Phase High Level Overview”, “Project Development Plan update 2011 12 20” and “WHVDC Contract Prog 09032012”) has been reviewed and appears reasonable to meet the contract completion date. NGET/SPT have indicated that they will review the project programme if required following the submission of a full planning application for the Kelsterton converter station site in May, following a planning rejection for this site. The following tasks are identified by NGET and SPT as being on the critical path:

Civil construction of converter station at Hunterston

Cable and converter station commissioning

We would also recommend that cable type testing, cable manufacture and deep water cable laying activities are included on the critical path.

We have proposed a set of annual project milestones based on the completion date for the link and the proposed programme provided by NGET and SPT, by financial year. These are supported by proposed technical output measures based on the boundary transfer requirements, the contracted link design and requirements of the AC transmission system.

1 No Initial Proposals for RIIO-T1 are available for NGET as they are not going through the fast-track process.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

5

PÖYRY MANAGEMENT CONSULTING

Output 6

We have benchmarked unit costs at component level and for the overall project. Comparing costs across projects can be challenging (for example, the applicability of the cable materials unit cost will be influenced to an extent by the volatility of the price of copper and steel etc.), but we do provide a comparison of project costs for recent subsea transmission projects using HVDC LCC technology in Table 3, based on publically available information.

Table 3 – HVDC LCC Offshore Transmission Projects - Examples

Project Name Capacity

(GW)

Offshore Cable

Length (km)

HVDC Cable

Contract

HVDC Converter

Contract

Contract Price Base

Total Cost

Year of Completion

Cometa bipole 0.4 250 €267m €100m 07/08 €375m† Est. 2012

Sapei bipole 1 420 €400m US$180m 06/07 €750m‡ 2011

Britned bipole 1 244 US$350m €220m 07/08 €600m‡ 2011

Fenno-Skan 2* 0.8 200 €150m US$170m 08/09 €315m

‡ 2011

WHVDC Link bipole

2.25 386 XXXXXXXXXXXXXXXXX 11/12 XXXX‡ Est. 2015

† Total contract price (in 2007/08 price base) ‡ Total outturn price (forecast outturn for WHVDC Link in 2009/10 price base) * single cable

This provides a useful comparison to costs for the Western HVDC Link although there will be a dependence on seabed conditions and cable metal costs. For example, both COMETA and SAPEI involved subsea cable laying at water depths greater than 1000m. Also, the transmission links are less than half the capacity of the Western HVDC Link. The cable contract price also includes a small proportion of onshore cable costs.

Output 7

Whilst we have endeavoured to ensure we capture all relevant information and data required to provide Ofgem with a comprehensive and robust assessment covering all aspects of this work; in the timeframes for this project we were reliant on the nature of cooperation and information provision provided by the relevant TOs (NGET and SPT). We proactively worked with Ofgem and NGET/SPT to address any gaps identified.

By the time of the 14 March cut-off date the outstanding information gap and the impact it had on our assessment and resulting recommendations for the relevant affected Outputs can be summarised follows:

We had not received requested set of self-consistent risk profile information based on updated/best knowledge as of early March, including accounting for Kelsterton and Hunterston planning application decisions.

Consequently our assessment of the contracting position is based on the complete self-consistent set of information and data provided on 18 February 2012.

Our recommendations for ex-ante funding allowances in Section 5 are also undertaken on this basis but also including a further adjustment that we have made to

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

6

PÖYRY MANAGEMENT CONSULTING

correct an apparent error in the calculation of employer risk for cable burial, which we believe should be £2m lower.

Our understanding is that the materiality of difference between risk related costs as presented 18 February 2012 versus that which might be expected as at March 2012 in the light of updated information will be very low. Specifically it suggests <£2m in absolute magnitude as measured at the P=50 point on the risk related cost distribution. This is <0.2% of overall cost of delivery of HVDC component of WHVDC link costs material provided; and barely measurable in the context of combined SPT and NGET RIIO-T1 capex programmes.

Thus we believe this information “gap” and our use of information as at 18 February does not have any impact on our assessment of the procurement process (Output 2), determination of funding approach (Output 3), assessment of milestones (Output 5) or benchmarking of costs (Output 6).

As indicated above we also believe it does not have a material impact on our assessment of costs (Output 2), our recommendations on the methodology to be adopted for determining funding and risk sharing arrangements (Output 3) or the (provisional) ex ante funding allowances derived from application of that methodology to the data available as of 14 March 2012 (Output 4)especially if viewed from the perspective of setting an annual funding profile for each of the two TOs within the WHVDC link joint venture across the full project timeframe. Consequently we believe our recommendations within this report including those for annual funding are robust to a reasonable level of accuracy, with the following conditions:

If Ofgem wishes to pursue accuracy to the £10k level (or tighter) of risk-related costs at the P=50 point in ex-ante setting of agreed funding arrangements for the WHVDC link it will need to make minor adjustments to our provisional recommendations for annual funding figures.

Also we are aware the contract NGET/SPT have put in place had a limited number of variable elements due to be locked down in early March; and it may be possible these change the contract cost from that we have used based on 18 February information and that Ofgem may need to adjust accordingly in determining final funding allowances2.

Where Ofgem chooses to apply a determination based on an updated set of information/data on final contract cost and view of risk-related costs we advise this is done based on a designated data freeze date; and any subsequent variations are captured by the agreed risk sharing mechanism (and if required) relevant reopener conditions.

2 We note that on 9 March 2012, the JV provided an updated view of contract costs (but not of non-contract costs and

thus not a coherent data set for basing our recommended allowances on), and these were subject to further change.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

7

PÖYRY MANAGEMENT CONSULTING

1. INTRODUCTION

1.1 Overview of the Review

The Western HVDC Link as proposed by NGET and SPT would be an undersea cable, running from Hunterston in Scotland to Deeside in England, providing c.2GW of additional transfer capability across the B6, B7 and B7a boundaries. The project is currently being funded under the Transmission Investment Incentives (TII) framework until the end of March 2013. Thereafter, it will be subject to ongoing funding arrangements under the RIIO-T1 price control.

The purpose of this assessment is to support Ofgem in regard to the delivering following three objectives:

the final stage of Ofgem‟s assessment of funding request in relation to construction works on the HVDC component of the Western HVDC Link,

the determination of appropriate funding provisions under TII and RIIO-T1 including any specific risk sharing arrangements to apply

establishing unit cost benchmarks for wider application to similar projects under RIIO-T1.

1.1.1 Overview of the Western HVDC link project

The Western HVDC link project comprises three components:

an HVDC cable, of capacity circa 2GW and about 400km in length, together with converter stations at each end;

onshore works around the northern connection point, near Hunterston 400kV substation in SPT‟s transmission area, and

onshore works around the southern connection point, near Deeside 400kV substation in NGET‟s transmission area.

However it is the intention of this project to focus on the aspect of the project highlighted in the first bullet highlighted above, namely the Western HVDC cable and convertors, subsequently referred to as “the HVDC component” of the overall Western HVDC link scheme.

1.1.2 Overview of the TII framework

In April 2010, Ofgem introduced the TII framework for providing interim funding , within the current transmission price control period (TPCR4, running to the end of 2011-12), for critical large-scale investments that the Transmission Owners (TOs) identify are required to support achievement of the Government‟s 2020 renewable energy targets. TII funding is provided on a capex basis via ex ante allowances specified for each year which are linked to defined deliverables.

The TII framework has been extended into 2012-13 under the one year adapted rollover of TPCR4. For all projects considered under TII, funding arrangements beyond March 2013 will be addressed as part of work on the next full transmission price control review, RIIO-T1.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

8

PÖYRY MANAGEMENT CONSULTING

1.1.2.1 Funding requests and previous consultancy reviews

The large-scale investments put forward for funding consideration under TII typically take the form of an overall project comprising a number of discrete components being developed over different timescales which, when taken together, are designed to achieve an overall aim of increasing transmission boundary capability in a given part of the network in response to anticipated future demands from network users.

In line with the “funding in stages” approach adopted under TII, the Transmission Owners (TOs) can submit TII funding requests for individual components of works they expect to take forward within the next year. Ofgem assesses such requests against criteria including the need for those works to proceed in the identified timescales and the readiness of the TOs to take forward those works. The funding decision is also subject to receipt of sufficient information from the TOs for Ofgem to determine appropriate ex ante funding allowances and deliverables with reference to the specific plans of the TOs over the period of TII funding.

Previous consultancy reviews under TII of the Western HVDC Link project3,4,5 have considered the overall project (the Western HVDC Link) and the discrete components (the HVDC component, the associated onshore substation works at Deeside/Connah‟s Quay, and the associated onshore substation works at Hunterston East).

This review focuses on the HVDC component in particular. Following previous consultancy reviews of the HVDC component of the project, in its August 2011 consultation6 Ofgem had concluded that there was a case for proceeding with this component in line with the TOs‟ planned programme towards delivery of the link in 2015. As such, for the purposes of this review, Ofgem did not require further assessment against the criteria adopted in previous consultancy reviews under TII. Rather, Ofgem required specific support relevant to the determination of the specifics of funding, i.e. the cost allowances to apply in each year for each TO and deliverables associated with those allowances, and the risk sharing arrangements to apply between the TOs and consumers.

1.1.2.2 Specific issues in relation to projects with materially different characteristics

A key point to note for this review is that the TII framework, as applied to all works funded under TII to date, reflects the treatment of capex in the prevailing price control, including the capex efficiency incentive, on the basis that their characteristics are similar. However, Ofgem has retained flexibility to vary the TII framework when funding projects of materially different characteristics to those funded to date.

For example, depending on the risk profile, and how this is reflected in the TOs‟ cost submission, this may involve varying the risk sharing arrangements by:

applying different level of incentivisation (the efficiency incentive rate, 25% under the price control arrangements that currently apply) in the capex efficiency incentive,

3 http://www.ofgem.gov.uk/Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives/

Documents1/KEMA%20Final%20Report.pdf 4 http://www.ofgem.gov.uk/Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives/

Documents1/WesternHVDCLinkSKMStage1ReviewReportmFinalPublic.pdf 5, http://www.ofgem.gov.uk/Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives/

Documents1/SKM_Stage2_Public.pdf 6 Transmission Investment Incentives: consultation on minded-to position for Western HVDC link (“Western

Bootstrap”), 1 Aug‟11:

http://www.ofgem.gov.uk/Pages/MoreInformation.aspx?docid=10&refer=Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

9

PÖYRY MANAGEMENT CONSULTING

excluding or adjusting for certain risks when setting ex ante allowances,

and/or introducing specific adjusting event provisions to deal with certain risks ex post.

With this in mind, Ofgem have indicated in their November 2011 update document7 that the specific characteristics of the Western HVDC Link (and the HVDC component in particular) meant that it could be appropriate to adopt a different treatment to that used for works funded under TII to date.

Therefore the particular focus of this review is on the specific risk characteristics of the HVDC component. This issue is also relevant to consideration of ongoing funding arrangements in RIIO-T1.

1.2 Overview of requirements

As noted above, following previous consultancy reviews of the HVDC component of the Western HVDC Link project, Ofgem had concluded that there is a case for proceeding with this component in line with the TOs‟ planned programme towards delivery of the link in 2015.

Ofgem‟s November 2011 update6 confirmed that, taking into account progress of the project and findings of a further consultancy review (SKM Stage 25), Ofgem had maintained its minded-to position, while also reaching a positive conclusion on the case for delivery in 2015. It also stated that the minded-to position remained subject to no material escalation of expected costs and that the remaining aspects of Ofgem‟s project assessment would require further review as the TOs firm up their plans, and this would be an input to consideration of the specifics of funding with reference to those plans.

This review therefore seeks to inform Ofgem‟s ongoing work to determine the specifics of funding both under TII and RIIO-T1. Thus, it provides specific assessment relevant to the determination of the details of funding, i.e. the cost allowances to apply in each year for each TO and deliverables associated with those allowances, and the risk sharing arrangements to apply between the TOs and consumers. This will take into account the contractual arrangements put in place for the delivery of the project – namely that NGET and SPT have set up a joint venture (JV) which signed one contract with a consortium of Prysmian and Siemens to deliver a 600kV/2.25GW HVDC link. This followed four rounds of design iterations, negotiations and bid re-submissions.

A key aspect of this review is on the specific risk characteristics of the HVDC component to understand whether it is appropriate to use the same treatment of capex as under the prevailing price control, as has been done for the award of funding for all projects to date under the TII framework.

In addition, the TII framework will be superseded on 1 April 2013 by the arrangements for wider works under RIIO-T1. Therefore, this review also provides information to inform Ofgem‟s decisions on appropriate funding arrangements for the Western HVDC link under both frameworks, in terms of the risk sharing arrangements to apply under each frameworks and the annual ex ante funding allowances and associated deliverables.

7 “Transmission Investment Incentives: update on Western HVDC link (“Western Bootstrap”), 10 Nov‟11:

http://www.ofgem.gov.uk/Pages/MoreInformation.aspx?docid=20&refer=Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

10

PÖYRY MANAGEMENT CONSULTING

Under RIIO-T1 funding allowances will be specified on a totex basis8 and linked to deliverables and the same risk sharing arrangements, including efficiency incentive rate and uncertainty mechanisms, are expected to be used for all capex including that funded under the arrangements for wider works.

Therefore specific points for the RIIO-T1 assessment that are additional to the TII assessment are also addressed - including recommendations relating to the costs and deliverables for the RIIO-T1 years, and about unit cost benchmarks for use in future assessments of similar projects under RIIO-T1.

1.3 Project deliverables and associated tasks

Our proposed project approach and associated tasks are presented in Table 4 below (sourced from the Ofgem ITT for this review).

We have used this approach as the structure for this report, addressing each of the „key outputs‟ in turn.

Table 4 – Project outputs and associated tasks

Key outputs Key tasks in delivery of key outputs

1: Summary of final plans of the TOs which are used as the basis for determination of funding arrangements under TII and RIIO-T1

1. Consolidating detailed information on preferred solution / final contract:

final costs (with detailed breakdown by cost item and TO), design (including technical specification) and programme (with key milestones and dates);

treatment of project risks within contract and assumptions underpinning these; and

any additional risk allowances proposed by the TOs for factors not reflected in the contract costs.

2. Consolidating information on key risks from risk register and identifying any outstanding delivery risks with a bearing on the terms of the contract including any cancellation provisions

3. Highlighting key changes in the above since SKM‟s review 2: Review of final stages of TOs‟ process towards contract award

4. High level review of the final stages of the TOs‟ tender evaluation process against the planned process reviewed by SKM, and giving a view on extent to which the planned contracting strategy has been followed.

5. Reviewing the TOs‟ approach to managing outstanding delivery risks, and giving a view on the appropriateness of how this is reflected in terms of contract award as summarised in item 1.

3: Recommendations on risk sharing arrangements between TOs and consumers under TII and RIIO-T1

6. Assessing the risk profile of the project, identifying any material differences in characteristics compared to works funded under TII to date, and giving a view on implications for risk sharing arrangements under TII and RIIO-T1

7. Developing a risk methodology, using appropriate criteria, for identifying which risks should be: reflected in ex ante allowances; dealt with ex post; or borne by the TOs

8. Applying this risk methodology to key risks, and giving a view on the reasonableness of the costs assigned to those risks in item 1, taking into account expected likelihood and impact and TO methodology for developing risk-normalised costs*

4: Recommendations on annual ex ante funding allowances under TII and RIIO-T1

9. Proposing annual ex ante funding allowances for each TO under TII and RIIO-T1, with reference to the final costs identified in item 1 above and any specific adjustments to those costs, e.g. in line with recommendations under item 3 or to take account of overlaps with any existing funding

5: Recommendations 10. Proposing annual key project milestones which are consistent with the

8 In practice, for the HVDC component of the Western Link Project, all spending would be counted as capex, and

therefore, totex and capex allowances are equivalent.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

11

PÖYRY MANAGEMENT CONSULTING

Key outputs Key tasks in delivery of key outputs

on deliverables to be associated with funding allowances under TII and RIIO-T1

planned programme 11. Proposing technical output measures which are consistent with the final

design and reflect the expected benefits (thermal, voltage and/or stability) across relevant system boundaries on completion of construction works

6: Recommendations on benchmarking of HVDC costs for wider application

12. Consolidating high level information on costs and design of all viable bids/combinations, and applying this and own data sources in proposing unit cost benchmarks at component level (convertor stations, DC cables, harmonic filters etc.), onshore civil work, undersea cable laying and by applied technology (e.g. Voltage Source Converter, Current Source Converter)

7: Identification of any limitations in the recommendations

13. Where applicable, identifying extent to which the depth of the review and resulting recommendations are limited by gaps or delays in provision of relevant information by the TOs

* See Section 1.3.1 below

1.3.1 Additional Ofgem Guidance

Subsequent clarifications from Ofgem provided guidance that recommendations should be made on the following basis (and hence compatible with RIIO-T1 policy and Ofgem‟s Initial RIIO-T1 Proposals for SPT):

for both TOs the re-openers applicable to this project are as set out in the Initial Proposals for SPT under RIIO-T1;

SPT‟s capex efficiency incentive sharing factor for the HVDC component of the Western Link HVDC project should be the same as for other SPT projects, e.g. as set out in SPT‟s Initial Proposals under RIIO-T1;

NGET‟s capex efficiency incentive sharing factor for the HVDC component of the Western Link HVDC project should be the same as for other NGET projects, with no initial proposals for this sharing factor under RIIO-T1 currently available as NGET is not going through the fast-track process.; and

the Western Link HVDC project will be treated as a whole both ex ante and ex post, with pre-defined cost allocation ratios between the two TOs.

Ofgem noted that where Pöyry wanted to propose a different approach (e.g. on having different ratios for different component), there should be a discussion of the pros and cons of this approach versus the default position.

1.3.2 Sources

Unless otherwise attributed the source for all tables, figures and charts is Pöyry Management Consulting.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

12

PÖYRY MANAGEMENT CONSULTING

[This page is intentionally blank]

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

13

PÖYRY MANAGEMENT CONSULTING

2. OUTPUT 1 – SUMMARY OF FINAL PLANS

2.1 Overview of approach

This chapter provides a summary assessment of the final plans of the TOs which are used as the basis for determination of funding arrangements under TII and RIIO-T1. In this chapter we present:

final costs (with detailed breakdown by cost item and TO), design (including technical specification) and programme (with key milestones and dates);

treatment of project risks within contract, with underpinning assumptions;

any additional risk allowances proposed by the TOs for factors not reflected in the contract costs;

consolidating information on key risks from risk register and identifying any outstanding delivery risks with a bearing on the terms of the contract including any cancellation provisions; and

highlighting key changes in the above since SKM‟s Stage 2 review9.

SKM previously identified several key project risks in their Stage 2 report, notably: (i) cable supply and manufacture availability; and (ii) issues relating to consents and land purchase. This review addresses the extent to which NGET/SPT have managed to mitigate these risks, and explores the whole range of project risks more widely.

In addition, having reached this stage of the procurement process, we have reviewed the risk register in a more quantitative manner than was possible in previous stages, and assessed whether the specific risk items and their magnitudes are appropriate at this stage of the project.

2.2 Consolidation of details of final contract and non-contract costs:

The preferred contract option selected by NGET/SPT was the combined Prysmian/Siemens submission for a 600kV/2.25GW HVDC link, following four rounds of design iterations, negotiations and bid re-submissions. The proposed link has an overall length of 420km connecting convertor stations located in North Ayrshire (South-East Scotland) and Flintshire (North Wales) utilising 600kV Mass Impregnated Polypropylene Laminate (PPL) paper insulated cable, with a nominal rating of 2.25GW with a 6 hour overload capacity of 2.4GW – the first of its kind.

2.2.1 Final costs – High level breakdown of contract costs

Table 5 provides (as presented at the National Grid workshop on 01 February 2012) a high level breakdown of the cost submission for this project. The table compares data based on a January 2012 position to the previous submission on this project to Ofgem in August 2011. The risk cost category is based on a P=80 value from the risk distribution.

9 http://www.ofgem.gov.uk/Networks/Trans/ElecTransPolicy/CriticalInvestments/InvestmentIncentives/

Documents1/SKM_Stage2_Public.pdf

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

14

PÖYRY MANAGEMENT CONSULTING

Table 5 – Overview of project cost (£m, real 2009/10 prices)

Project Costs Category (09/10 prices) – (£m) 2.25GW Option (August 2011)

2.25GW Option (January 12)

Cable & Convertor Contracted* XXX 866

XXXXXXXXXXXXX XXX XXX

XXXXXXXXXXXXXXXXXXXXX XXX XXX

Total 1094 1072

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

We note that the JV supplemented this with further information on 16 February 2012 which included an annual profile and cost breakdown between NGET and SPT for various cost categories. The total project cost of XXXXX and total risk cost of XXXX (P=80) were equal to the figures presented in Table 5 for the January 2012 data. However the remaining items were categorised differently compared to the Janaury 2012 data and this had to be taken into account when comparing the data from 16 February with previous iterations. Further, on 18 February the JV provided updated risk analysis based on updated input assumptions in response to Poyry questions (giving XXXX at P=80 and XXXX at P=50) . For the purposes of our recommendations set out in Output 4 we have adjusted these figures downwards by £2m to correct an error. This is discussed in more detail below and in Output 4.

The specific project costs for the Prysmian/Siemens bid are summarised in Table 6 below. The dominant cost item is the prime contract, the majority of which relates to the procurement and manufacture of plant (further detailed in Table 8).

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

15

PÖYRY MANAGEMENT CONSULTING

At the start of the tender evaluation process, NGET/SPT stated that because of the relatively broad way the project scope had been designed they needed to undertake a „levelling‟ analysis to ensure all bidders were compared on the same basis. This means that, for example, if one tenderer is priced in a specific risk and another left this risk to the employer, the second tenderer would have their offer adjusted by an amount judged by NGET/SPT to be their cost of mitigation, so that both were compared on the same basis.

In order to understand how NGET/SPT had approached this „levelling‟ analysis, we tracked the evolution of the ultimately winning bid from initial offer (the initial tender returns in May 2011) to the final offer at standstill (in January 2012) of £866m (£1,012m in nominal prices).

NGET/SPT stated that as a result of these negotiations the contractors agreed to take on greater risk, which is reflected with an increment in the main contract price but, they argue, has in effect lowered the overall cost by decreasing the size of the anticipated risk allowance required.

As this is a turnkey contract the contractor was not obliged to provide cost breakdown information in any level of detail below this, therefore they had some flexibility to move margins between activity areas. Nevertheless some clear messages emerge overall, and the movements in the contract costs are driven by a combination of the following main factors:

Contractor sharing weather risk – The contractor has agreed to take responsibility for up to 60 days of weather-related delays. For weather related delays between 60 and 120 days the costs are shared between contractor and employer. Beyond 120 days NGET/SPT are financially responsible in entirety.

Results of geophysical and geotechnical surveys – The cable route has evolved following numerous surveys to avoid difficult ground conditions as far as reasonably possible. The final route corridor has subsequently improved but some potentially difficult areas remain. NGET/SPT identified 160km of potentially difficult terrain and agreed that the contractor will allow for 25km of rock dumping and trenching. There was some confusion about this figure in their modelling of residual risk which is discussed in Section 2.3 below.

Type registration – NGET/SPT have proposed a period of sea trials shortly after manufacturing of the deep-sea cable has commenced. Should the cable not satisfy these tests i.e if the contractor delivers a link that is above 1.8 GW but below 2.25GW/600kV then the JV may accept the link and recover liquidated damages for the reduced performance.

Commodity price changes – specifically a decrease in metal prices since initial offer.

Identification of new/missing risks from original bid.

Insurance – NGET/SPT insurance costs have decreased as substantial risks passed to contractor. We did query whether there was any overlap between risks covered by the insurance and other items in the risk model and was told verbally that there were not, as insurance covers general liabilities etc., which are not project risks as such.

2.2.2 Final Costs – Breakdown of other Costs

Aside from the main contract costs, a number of other individual cost items have also been identified. („non-contract costs‟) outside of the risk modelling. The movement in these figures between the August 2011 position and the January 2012 position is shown

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

16

PÖYRY MANAGEMENT CONSULTING

in Table 7. No revised breakdown was provided by NGET/SPT for the February figures and so a breakdown cannot be presented for the latest cost figures.

Key issues to note are as follows:

The Kelsterton land purchase figure had been double counted, with a figure of XXX for this item also remained in the risk/contingency calculation. NGET/SPT have adjusted their risk model to remove this double-count.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

The non-contract project management budget has risen from XXX to XXX, apparently due to a revised view by NGET/SPT as to the level of internal resource required.

A new line item has been added for New Technology Development – this is an allowance for further testing of the 600 kV solution; notably further work on the voltage control scheme, tests on the impact of the cable cooling cycle on joints and terminations, increased levels of witness testing and quality assurance. This issue was not raised in the August 2011 submission and NGT/SPT admitted that this was effectively an oversight, in that the project team subsequently identified this as being

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

17

PÖYRY MANAGEMENT CONSULTING

necessary for the 600 kV option. This set of activities is distinct from the type testing which would have to be carried out in any case.

2.2.3 Final Costs – Split by TO

At the workshop on 9 February 2012 the TOs presented us and Ofgem with a breakdown of the costs (split by TO). Clarification was sought as to how this split was derived and the following explanation was provided on 16 February 2012.

“Whilst the EPC Contract costs are relatively high level, they are sufficiently defined to allow a split of costs between the Stakeholders. For those costs that have not been defined in the required level of detail we are able to apply logical assumptions and methodology into the evaluation of the costs to provide a fair and reasonable estimation of the split between the Stakeholders”.:

EPC Contract

“The Contractor has provided a detailed cashflow split into the generic tender milestones provided in the Invitation to Tender. These costs have been split notionally into either SPT or NGET costs for the purpose of allocation. Most costs were easily identifiable as occurring either at Hunterston or Kelsterton/Wirral (i.e. Converter, land cables) and could be fully apportioned in this manner, however certain costs were either occurring across boundaries (i.e. some marine campaigns, marine surveys, etc) or were generic cross project costs (Management costs, advance payment, etc.)”

The process for calculating the splits was therefore as follows:

100% attributable milestones were first allocated to either SPT or NGET.

For cable laying activities milestones split between stakeholders were split on a pro-rata basis based upon length of cable under SPT and NGET control. This made no allowance whatsoever for particular site conditions/anomalies encountered in this area (i.e. Campaign 2 splits into 96km cable/48km route (86%) for SPT and 16km cable/8km route (14%) for NGET. Where costs relate generically to Converter Stations (i.e. Converter commissioning costs) a pro-rata split in line with capex costs was adopted.

At this stage totals were taken for each stakeholder and a percentage split was calculated. The figures arrived at were 67.6% for NGET and 32.4% for SPT.

Finally, all other milestone costs not able to be split in this manner (i.e. Project Management) were allocated on a 67.6%/32.4% split.

Project Fixed Costs

Other Project costs were considered in isolation and split logically between the stakeholders wherever possible. If a split was not easily derived then the 67.6%/32.4% split was adopted. Specific splits used in the calculation were as follows:

Provisional sums – were clearly identifiable as being either for works at Hunterston or Kelsterton and were split accurately.

Asbestos Removal – was for works at Kelsterton converter station site only and was fully allocated as such.

Insurance costs – were split on a 67.6%/32.4% basis.

Bonds – were split on a 67.6%/32.4% basis.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

18

PÖYRY MANAGEMENT CONSULTING

Project costs – were split on a 67.6%/32.4% basis.

New Technology Development – were split on a 67.6%/32.4% basis.

Land purchase Kelsterton and Hunterston – Costs allocated to the appropriate Shareholder.

Sea bed & crown estate leases – costs split on accordance with ratios of total cable (i.e. 76.67% NGET and 23.33% SPT).

Risk Costs

Due to the nature of the simulation it is not possible to split risk outputs into each and every risk on the register as the output is a function of the many inputs. In addition it is not correct to simulate each and every input and add together. As a result a three stage operation was utilised to calculate the risk allocation.

The entire cost register is run through the simulator to get a risk allowance at P=80.

Risks were split between SPT and NGET and then 2 further simulations were run in isolation in order to get a percentage split between the Shareholders. In this case the split was 73%/27%. It should be noted that the sum of the individual P=80‟s is extremely unlikely to be equal to the earlier combined simulations but can be used for apportioning a risk pot.

The combined simulation is multiplied by the Stakeholders percentages to get a risk sum for both SPT and NGET.”

In order to assess whether this appeared reasonable an attempt was made to replicate this split using the „nominal‟ costs presented by NGET/SPT in their budget breakdown.

It was our view that broadly the assumptions seemed reasonable, notably that:

converter stations and associated costs, along with onshore cabling, would form part of the costs of the respective TO responsible;

remaining cable costs would be split in proportion to the length of route lying in Scots/other waters;

combining these gives the ratio of prime costs per TO.

other generic overheads would be likely to be split by the same proportion; and

risks might be expected to split slightly differently, as the greater magnitude of risk lies with offshore cable related issues, and NGET has the greater proportion of the cable route.

NGET/SPT provided a table summarising the split of costs on the basis of the above, but there were some inconsistencies with the project fixed costs relative to other information provided. We therefore attempted to reconstruct this calculation using NGET/SPT‟s January 2012 standstill position as the starting point. Table 9 summarises the basis of our calculation of the split of contract costs, based on the final budget breakdown for the Best and Final Offer. The final budget breakdown is based on the movement in detailed procurement and construction costs described in Table 8, which was provided by NGET/SPT, and provides a breakdown of two of the cost categories shown in Table 6.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

19

PÖYRY MANAGEMENT CONSULTING

NGET/SPT have not directly provided data on the TO share of the submarine cable (the greatest single element of cost). However, NGET/SPT advised us during discussions about the split of costs, that they had split cable laying costs approximately 75%/25% between NGET/SPT. We have examined the information contained in the above tables to estimate the TO share of the submarine cable in Table 10 (based on the overall cost for submarine cable shown in Table 9).

The TO share of the contract element, in real 2009/10 prices, has been used to estimate the TO share in nominal prices by applying the same percentage split. The nominal values set out in Table 8 have been compared to the contracted costs and explained in Table 9, where the procurement and installation of the submarine cable itself is calculated to cost a total of XXXX. NGET‟s share of the submarine cable can be deduced by subtracting the defined costs associated to NGET from the NGET share of the contract element, as illustrated in Table 10. Note that the data for Table 9 and Table 10 was provided by NGET/SPT in nominal prices.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

20

PÖYRY MANAGEMENT CONSULTING

The above calculations assume the same percentage split in 2009/10 prices and in nominal prices. Alternatively, using the approximate percentage suggested in discussions with NGET/SPT, the XXXX of cable laying costs in this proportion gives the following overall split:

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

This gives a split approximately 67% to NGET and 33% to SPT.

In conclusion, the approach to splitting the contract costs is clear with NGET accounting for 75% of the submarine cable. The largest item of project fixed costs is project management, the remainder being comprised of the new technology development costs, plus a number of things such as land purchase which relate to specific converter station

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

21

PÖYRY MANAGEMENT CONSULTING

sites – we have therefore assumed that the NGET/SPT as JV partners have arrived at a split between them which they consider to be equitable. The split of risks was derived from the Monte Carlo model so it is not possible to replicate this exactly without re-running the model.

2.2.4 Design (including technical specification)

The proposed link has an overall length of 420km (386km offshore) connecting convertor stations located in North Ayrshire (Kelsterton) and Flintshire (Hunterston) utilising 2 x 2400mm2 Mass Impregnated Polypropylene Laminate (PPL) paper insulated cables, designed to operate at 600kV with a nominal rating of 2.25GW with a 6 hour overload capacity of 2.4GW.

In many respects the design is similar to other HVDC schemes of this scale; the key innovations are the cable composition using PPL insulation, and the operation at 600 kV. The latter requires that the HVDC system has a voltage control system when de-loading the circuits from high levels of loading, in order to manage the electrical stresses on the insulation.

The cable will be first-of-a-kind in terms of the voltage it will be operated at (600kV). One impact of this includes the additional budget item for testing over and above normal type testing, another impact is the risk that if serious issues are brought to light during testing, the cable may need to be derated to some level between 600 and 500kV if type testing at 600kV is not successful.

The design may change if type testing at 600kV is not successful, to the lower rated voltage (500kV) which would also reduce the capacity to c.1.875GW. The cost impact of a lower rated capacity is borne by the manufacturer (as described below) as additional costs for reinforcement elsewhere in the system may be required in this case.

We asked NGET/SPT the impact such a situation would have commercially and contractually and NGET stated (on behalf of the JV) that:

"If the contractor does not deliver to specification and the link has a rating of less than 1.8 GW then the employer may ultimately terminate the Contract and reject the link if it so wishes and get his monies and certain costs refunded, subject to any relevant caps on liability.

If the contractor delivers a link that is above 1.8 GW but below 2.25GW/600kV then the Employer may accept the link and recover liquidated damages for the reduced performance or may ultimately terminate the Contract following a prolonged delay to completion for Contractor default and appoint a third party contractor to complete the Works.

In practice this commercial pressure is most likely to result in the payment of performance liquidated damages where the rating is above 1.8 GW or, where the rating is below 1.8 GW a negotiated settlement i.e. a reduced payment for the link if you assume the resulting system still has value to all parties including crucially consumers. If the system has no value or a value could not be agreed then rejection without payment is the ultimate sanction."

Other design issues still to be finalised include:

filter design at the converter stations – this is because design would be optimised for the system configuration prevalent when the link is installed, which may change between now and 2014;

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

22

PÖYRY MANAGEMENT CONSULTING

exact circuit length, particularly if a new converter station site is chosen; and

some localised design issues about converter station auxiliary supplies etc., and issues related to consenting (e.g. the physical appearance of buildings etc.).

Cost impacts for the first two issues are included as „design‟ risks in the risk model; other consenting related issues are also included under the classification of „consent‟ risks.

A summary of the project design costs is shown below in Table 11 – these costs were shown under a single category heading in Table 6.

From a technical perspective, there are no restrictions preventing pairing the 600kV operation of the PPL cable with a convertor available from other manufacturers included in the tender process. However, as this 600kV option was not submitted standalone in Lot 2, NGET/SPT were contractually unable to split the Lot 3 bid. NGET/SPT did invite Lot 2 bidders to submit higher voltage operation but they declined – this issue is explained in more detail in Chapter 3.

The new PPL cable technology would be the first of its kind by operating at 600kV and will subsequently require operational verification of the cable, joints and terminations for which NGET/SPT have allocated approximately 9 months of Type Registration, starting September 2012. As this is the first HVDC link to be built by NGET/SPT as a TO (and such cable systems are bespoke and therefore a „first of a kind‟ anyway) we assume that type registration would take a similar timescale regardless of whether the 600 kV or 500 kV solution were chosen. Through discussions NGET/SPT were confident that should the Type Registration of 600kV prove unsatisfactory the fall-back plan of operating nearer 500kV would be implemented. The management of this new technology risk is discussed in Section 2.3.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

23

PÖYRY MANAGEMENT CONSULTING

2.2.5 Programme (with key milestones and dates)

The critical path and principal deliverables of the project are summarised in Figure 1.

Figure 1 – Key programme areas (approximate timings)

Based on our analysis we highlighted three key issues with the programme:

Firstly, it has become apparent that the most significant areas of project risk (by value) relate to the offshore cable installation (weather and seabed burial risks). This would therefore tend to load the bulk of the risk into the latter part of the programme.

Secondly, the commissioning process relies on hitting a specific time window. Commissioning the link fully requires testing the link under some relatively extreme system conditions, and National Grid SO have stated to the project that this will only be likely to be possible in periods when other plant is not out for summer maintenance outages, and when the load on the system is not too great – i.e. either in Autumn before the clocks change or in the subsequent spring. A delay, therefore, of two months at the end of the project may result in an effective 6 month delay to full commissioning. Whilst the NGET/SPT project team have costed the impact on them (in terms of contractor downtime) they have not quantified the (indirect) cost of system constraints, as these lie with the SO. These issues are on the critical path regardless as the constraint on commencing the cable laying, and hence the commissioning, is the time to manufacture the offshore cable. In the event of a significant delay it may therefore occur quite late in the programme, and the SO would have to choose between waiting for the next commissioning window, or accepting the link into partial service with not all tests completed.

Thirdly, during February the planning application for the converter station at Kelsterton was refused. The impact of this was discussed with NGET and they stated

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

24

PÖYRY MANAGEMENT CONSULTING

that the planning process would have to slip by over 9 months before it puts the project end date at risk. It appears that enabling works at Kelsterton are not scheduled to start for 6 months, and that there is around 3 month float in the Kelsterton programme, so this statement aligns with the programme.

2.3 Evolution of Project Risks from Aug 11 to Jan 12 Position

In order to assess project risk, NGT/SPT conducted risk workshops at each stage of the procurement process, and undertook comparative risk modelling of all the tenders using a common approach.

The approach adopted involved listing all the identified risks and assigning each a least likely, most likely and worst case value, along with a percentage probability of that risk materialising. All the risks were fed into a Monte Carlo simulation which them produced a probability distribution curve. The Monte Carlo simulation used three-point probability distributions for each risk, the points being named „minimum, most likely and maximum.‟ As each tenderer offered to take on different risks and had made different assumptions, this analysis was carried out separately for all tender offers as part of the evolving risk assessment and tender evaluation.

The risk allowance requested by NGET/SPT in August 2011 was split into XXXX representing the P=80 (i.e. probability of being less than or equal to this level is 80%) point on this curve, plus an additional XXX for weather/seabed risk which TOs calculated separately and excluded from requested risk allowance on basis that is should be covered by a re-opener rather than ex ante allowance. The version presented to us at the commencement of this analysis indicated that once weather/seabed risk had been rolled into the Monte Carlo model the P=80 point had reduced to XXXX (all numbers quoted based on 2009/10 figures).

NGET/SPT stated that the total risk allowance has been reduced as an outcome of negotiations whereby the contractors agreed to take a greater proportion of the project risk – i.e. simplistically an increase in contract value of XXX (2009/10 value) had been offset by a reduction of XXX of risk. At first sight this does not appear to be a reduction but the contractor has also taken on insurance (previously cost at XXX) so overall NGET/SPT appear to have driven a real cost reduction overall.

In addition to moving some risks into the contract, and therefore removing them from the risk register, the project team had stated that in other cases the cost of a risk had been calculated precisely – so, for example, if an additional piece of land needs to be purchased but the purchase price was known, this would have one single value. A fourth column (in addition to the „minimum, most likely and maximum) was therefore added entitled „base cost‟ which captured these items with a single value. This column was intended to cover risk items whose cost was known, but which had not moved into contract price.

The NGET/SPT project team had also changed a number of assumptions through the period August 2011 to January 2012 as their understanding of the issues improved (for example, as better survey data was made available and new delivery team members joined with relevant experience of previous projects). The major impact of this was in the weather and burial risks, where some risk had been absorbed into the contract price, but where the project team modified their assumptions as to the „worst case‟ risk, such that the „best view‟ number reduced but the „maximum‟ number increased, making the risk curve more asymmetric.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

25

PÖYRY MANAGEMENT CONSULTING

We undertook a detailed audit of the evolution of risks for the winning tender, looking in detail at key risks and how they had evolved. For the most part NGET/SPT were able to give detailed account of the risk definitions, their underlying assumptions/calculations for the values, and how/why a given risk had evolved. They also demonstrated that periodic reviews had been carried out to remove any double counting. We were able to therefore form an independent view of where the key areas of risk lay in the project. The evolution of the „best view‟ risks from August 2011 to the January 2012 version is summarised in Figure 2, with the magnitude of each column being the sum of the „best view‟ risks (each having first been multiplied by its probability factor). Note however that where new risks were added NGET/SPT had not classified all risks, we did not have a firm definition of each risk category, so some level of interpretation had to be applied to the more recent (January) figures.

Notable movements were as follows:

the „best view‟ value for cable laying dropped significantly, as some of this risk was passed to the contractor (note however that the „maximum‟ value went up, so care should be taken interpreting this movement);

design risks were issues relating to uncertainty about the length of cable routes, which appear to have been resolved through re-surveying;

a large element of the „converter‟ risk in August 2011 related to risks of spend due to contaminated land, this risk has been better quantified and effectively passed to the contractor; hence the increase in „contractor‟ risk in January 2012 to compensate; and

some items were classed as „converter risk‟ which were really related to land purchase and consenting, the risks in the January 12 figures have been reorganised somewhat compared to August 11 so that the „consenting‟ risks have risen as a result.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

26

PÖYRY MANAGEMENT CONSULTING

Whilst the overall view was that this approach appeared thorough and well documented, the outcome of this audit produced several apparent issues:

Land purchase at Kelsterton appeared in the risk modelling at XXX where it has been itemised separately as a non-contract project cost of XXXX. NGET/SPT stated that the XXX was a double count and in the subsequent February submission corrected this.

Results of geophysical and geotechnical surveys – The cable route has evolved following numerous surveys to avoid difficult ground conditions as far as reasonably possible. The final route corridor has subsequently improved but some potentially difficult areas remain. NGET identified 160km of potentially difficult terrain and agreed that the contractor will allow for 25km of rock dumping and trenching. Of the remaining 135km, NGET have stated that a further 10% is considered most likely in the risk register at XXXXXXX (deduced from Prysmian figures) with XXX for demobilisation, totalling XXXXX. The figure in the risk register is, however, XXXXX best view as the calculation is based on 15km of difficult terrain – which implies an arithmetic mistake has been made in this calculation.

The impact of multiple delays has not been explicitly quantified – other than through addition of small risk contingency items to cover contractual basis for claims where more than one risk occurs. There has been no systemic assessment of the consequential risk of, say, cable burial delay triggering commissioning delay.

The nature of the Monte Carlo approach is such that it is not possible to add the risk items together simplistically to reproduce the risks. We therefore asked NGET/SPT to undertake the following analysis:

“We wish to understand the relationship between the overall project risk profile (covering all identified risks) and the residual project risk profile (i.e. that remaining given risk transfer to contract) and how that would compare at August 11 versus January 12. Please provide (a) a chart showing (i) the overall risk profile for the project as at August 11, (ii) the residual risk profile if you assumed "zeroing" of relevant August 11 risks since adopted by the contractor; and (iii) the overall risk profile if you added new items of risk (NOT changes of assumption for risks identified as at August 11) and deleted items of risks removed by January 11. (b) a chart showing (i) the residual risk profile as at January 12 derived from "zeroing" of relevant January 12 risk items adopted by the contractor, (ii) the overall risk profile for the project as at January 12 if you reinserted "zeroed" risk items with the latest assumptions at the time they were zeroed out; and (iii) the overall risk profile if you deleted new items of risk which were added after August 11 (NOT changes of assumption for risks identified as at August 11) and re- added items of risks removed by January 11 Please provide in both tabular and graphical format in Excel. Please also provide discussion of the key drivers of difference between the three curves within each of the two charts.”

The results of the response to this request are shown in Figure 3 and Figure 4.

Figure 3 uses the August 2011 risk profile as a starting point and overlays the Monte Carlo plots for:

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

27

PÖYRY MANAGEMENT CONSULTING

the original August 2011 risk profile (solid red plot):

the above with risks subsequently passed to the contractor between August 2011 and January 2012 removed, but no other changes of assumptions (solid blue plot);

the original August 2011 profile, with no risk passed to the contractor, but all changes in assumptions made by the project team between then and January 2012 added in (solid green plot); and

the January 2012 profile (purple line).

Figure 4 works back from the January 2012 plot as follows:

the red curve is the same line as the purple line above (January 2012 profile);

the blue curve adds back risks which were passed to the contractor between August 2011 and January 2012;

the green curve assumes that any new assumptions added since August 2011 are zeroed out.

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

28

PÖYRY MANAGEMENT CONSULTING

Considering these two graphs in figures 3 and 4 together the following observations can be made.

The response to Qn. 1a tells an overall story of the P=80 value of risk being reduced as well quantified risks are reduced, at the same time as the maximum value of risk is increased due to the project team‟s changes of assumptions. Together with the NGET/SPT technical team we spent time analysing this data and concluded that this increased asymmetry was almost entirely accounted for by the change of assumptions of seabed burial risk – a point which becomes clear on inspection of the response to Qn. 1b. We believe that this increased asymmetry is driven by:

improved survey data, which the JV argue has indicated that their initial risk assessments were conservative; and

the presence of new expertise in the team with substantial offshore installation experience, and consequently a change of perspective on the part of the delivery team in the light of this experience.

2.4 Evolution of Project Risk from Jan 12 to Feb 12 Position

Following our review of the risk registers, the double counting of numbers for land purchase at Kelsterton was corrected by NGET/SPT. In addition, the issues around planning consent at Kelsterton resulted in the risks related to converter station delivery being updated/revised by NGET/SPT. Monte Carlo plots for this revision were not provided to us, but a summary of the changes made was provided on a line-by-line basis. The tables below provide details of the changes made which are reflected in the updated risk analysis provided on 18 February referred to above in Figure 4. The further adjustment of £2m we made to correct an error is discussed in Output 4. Table 12 provides a summary of how the risk numbers have moved for the specific risk categories,

WESTERN HVDC FINAL FUNDING REVIEW

April 2012

WHVDC_Funding_Review_Final_PUBLIC_BLACKLINED.docx

29

PÖYRY MANAGEMENT CONSULTING

and Table 13 provides a narrative explanation (this is NGET‟s own narrative from their risk register).

WESTERN HVDC FINAL FUNDING REVIEW

April 2012