west alabama real estate summit tuscaloosa, alabamaaugust 24, 2012 ahmad ijaz center for business...

TRANSCRIPT

Tuscaloosa Economic Outlook

Tuscaloosa Economic Outlook

West Alabama Real Estate Summit

Tuscaloosa, Alabama August 24, 2012

Ahmad Ijaz

Center for Business and Economic Research

Culverhouse College of Commerce and Business Administration

The University of Alabama

http://cber.cba.ua.edu (205) 348-6191

Overview: U.S. Economic Conditions Overview: U.S. Economic Conditions

Economic recovery has lost momentum, but has not come to a halt

Inventory cycle caused relatively strong growth in late 2011 and early 2012

2.1 percent economic growth expected for U.S. in 2012 and 1.8 percent for 2013, chance of another recession is currently at 25 percent

Commercial and industrial loan market is gradually reviving

Center for Business and Economic Research, The University of Alabama 2

Downside RisksDownside Risks

State and local governments continue to lay off workers

Relatively tight credit and loan markets

Housing markets remain weak and distressed

Rising gasoline and food prices

External risks (Eurozone and China)

Lack of income growth

Economy will require much faster job growth for a sustained recovery

Center for Business and Economic Research, The University of Alabama 3

Center for Business and Economic Research, The University of Alabama 4

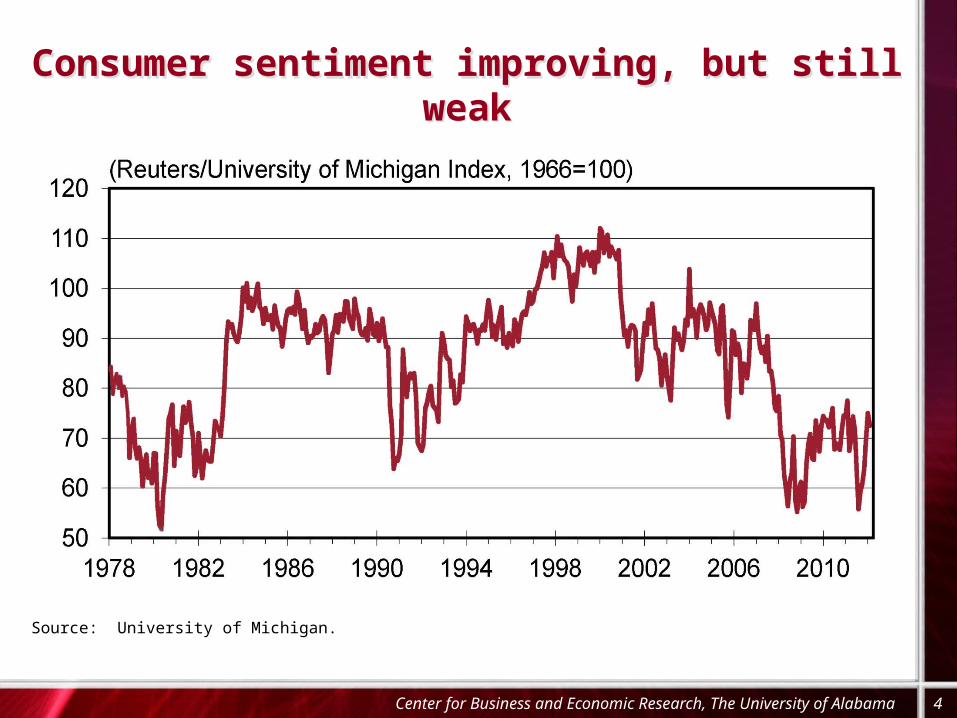

Consumer sentiment improving, but still weakConsumer sentiment improving, but still weak

Source: University of Michigan.

Center for Business and Economic Research, The University of Alabama 5

Productivity growth has run out of steamProductivity growth has run out of steam

Source: Federal Reserve Board.

Commercial and industrial loan market reviving gradually

Commercial and industrial loan market reviving gradually

Center for Business and Economic Research, The University of Alabama 6

Source:

U.S. Economic OutlookU.S. Economic Outlook

Source: IHS Global Insight, August 2012.

(Percent change unless otherwise noted) 2009 2010 2011 2012 2013

Real GDP -3.5 3.0 1.7 2.1 1.8

Consumption -1.9 1.8 2.5 1.9 2.1

Residential Investment -22.2 -3.7 -1.4 11.6 11.2

Commercial, Healthcare Structures -30.7 -25.0 -2.3 6.5 4.9

Nonresidential Fixed Investment -18.1 0.7 8.6 8.6 4.8

Federal Government 6.1 4.5 -2.8 -2.8 -3.1

State & Local Government 2.2 -1.8 -3.4 -1.7 -0.9

Exports -9.1 11.1 6.7 4.0 4.3

Imports -13.5 12.5 4.8 3.7 3.8

Payroll Employment -4.4 -0.7 1.2 1.4 1.4

Unemployment Rate 9.3 9.6 9.0 8.2 8.0

CPI Inflation -0.3 1.6 3.1 2.0 1.6

Light Vehicle Sales (Millions) 10.40 11.55 12.73 14.13 14.81

Center for Business and Economic Research, The University of Alabama 7

Monthly Employment Indicators (July 2012) Monthly Employment Indicators (July 2012)

Center for Business and Economic Research, The University of Alabama 8

Not Seasonally Adjusted

Seasonally Adjusted

Civilian Labor Force 2,175,298 2,157,890 Percent Change from Year Ago Level -1.2% -1.5% Absolute Change from Year Ago Level -25,726 -31,920

Employed 1,980,599 1,978,355 Percent Change from Year Ago Level -0.5% -0.5% Absolute Change from Year Ago Level -9,390 -9,144

Unemployed 194,699 179,535 Percent Change from Year Ago Level -7.7% -11.3% Absolute Change from Year Ago Level -16,336 -22,776

Alabama Unemployment Rate 9.0% 8.3%Alabama Unemployment Rate (July 2011) 9.6% 9.2%U.S. Unemployment Rate 8.6% 8.3%U.S. Unemployment Rate (July 2011) 9.3% 9.1%

Source: Alabama Department of Industrial Relations, Labor Market Information Division.

Alabama Nonagricultural EmploymentChange in Number of Jobs

Alabama Nonagricultural EmploymentChange in Number of Jobs

Center for Business and Economic Research, The University of Alabama 9

Source: Alabama Department of Industrial Relations, Labor Market Information Division.

July 2010 to July 2011

July 2011 to July 2012

Total Nonagricultural -6,700 5,700 Natural Resources and Mining 400 -200 Construction -8,800 -6,300 Manufacturing 1,500 3,400 Durable Goods Manufacturing 2,300 3,900 Nondurable Goods Manufacturing -800 -500 Trade, Transportation and Utilities 6,400 3,400 Wholesale Trade 700 -500 Retail Trade 3,600 5,900 Transportation, Warehousing and Utilities 2,100 -2,000 Information -800 -700 Financial Activities 700 900 Professional and Business Services -1,900 4,100 Educational and Health Services -400 1,500 Leisure and Hospitality 3,300 7,300 Other Services -300 1,300 Government -6,800 -9,000 Federal Government -3,000 -1,300 State Government -3,000 -8,000 Local Government -800 300

Share of Total Nonfarm Employment (2011) andShare of Alabama Gross Domestic Product (2010)

Share of Total Nonfarm Employment (2011) andShare of Alabama Gross Domestic Product (2010)

Source: Alabama Department of Industrial Relations. Source: U.S. Bureau of Economic Analysis.

Center for Business and Economic Research, The University of Alabama 10

1 20%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rest of Sectors22.72

Rest of Sectors38.71

Education and Health Services11.52

Leisure and Hospitality8.85

Professional and Business Services

11.60

Government20.18

Retail Trade12.44

Manufacturing12.71

Education and Health Services8.12

Leisure and Hospitality 2.77Professional and

Business Services 9.78

Government17.12

Retail Trade 7.20

Manufacturing16.31

Share of Total Nonfarm Employment Share of Alabama Gross Domestic Product

Tax Revenues (Fiscal Year to Date, July) Tax Revenues (Fiscal Year to Date, July)

Center for Business and Economic Research, The University of Alabama 11

Percent Change

From Year Ago

Change in Revenue

from Year Ago LevelTax Total Collection

Total $7,479,875,896 4.0% $290,488,033

Income (Individual) $2,880,218,386 4.9% $134,778,934

Sales $1,670,289,091 4.7% $75,106,878

Source: Alabama Department of Revenue.

Total Monthly Nonfarm Employmentand Unemployment Rate

Total Monthly Nonfarm Employmentand Unemployment Rate

Center for Business and Economic Research, The University of Alabama 12

Source: Alabama Department of Industrial Relations.

Employment (Thousands), Unemployment Rate (Percent)January 1990 – July 2012

Non

farm

Em

ploy

men

t

Une

mpl

oym

ent

Rat

e

JAN APR JUL OCT JAN APR JUL OCT JAN APR JUL OCT JAN APR JUL OCT JAN APR July1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

2,000

2,050

2

3

4

5

6

7

8

9

10

11

1990 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2012

Employment

Unemployment Rate

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

1,500

1,600

1,700

1,800

1,900

2,000

2,100

0

2

4

6

8

10

12

Center for Business and Economic Research, The University of Alabama 13

Total Annual Nonfarm Employmentand Unemployment Rate

Total Annual Nonfarm Employmentand Unemployment Rate

Employment (Thousands), Unemployment Rate (Percent)1990-2012

Source: Alabama Department of Industrial Relations.

Non

farm

Em

ploy

men

t

Une

mpl

oym

ent

Rat

e

Employment

Unemployment Rate

84

86

88

90

92

94

96

98

100

102

104

19801981199020012007

Change in Employment From the Beginning of the Recession

Change in Employment From the Beginning of the Recession

Center for Business and Economic Research, The University of Alabama 14

Number of months

(Number of Months)

ABCI™ History ABCI™ History

Center for Business and Economic Research, The University of Alabama 15

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q330

35

40

45

50

55

60

65

70

31.5

50.2Inde

x

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Business Environment ExpectationsBusiness Environment Expectations

Much Worse

Somewhat Worse

Remain the Same

Somewhat Better

Much Better

0 5 10 15 20 25 30 35 40 45 50 55

6.6

32.6

40.3

19.4

1.1

1.1

23.8

44.7

29.3

1.1 Alabama National

Q3 2012 compared to Q2 2012

Center for Business and Economic Research, The University of Alabama 16

Industry Performance ExpectationsSales and Profits

Industry Performance ExpectationsSales and Profits

Center for Business and Economic Research, The University of Alabama 17

Q3 2012 compared to Q2 2012

Strong Decrease

Moderate Decrease

No Change

Moderate Increase

Strong Increase

0 5 10 15 20 25 30 35 40 45

1.1

18.7

40.7

39.2

0.4

1.5

27.1

38.5

33.0

0.0 Sales Profits

Industry Performance ExpectationsHiring Plans and Capital Expenditures

Industry Performance ExpectationsHiring Plans and Capital Expenditures

Center for Business and Economic Research, The University of Alabama 18

Q3 2012 compared to Q2 2012

Strong Decrease

Moderate Decrease

No Change

Moderate Increase

Strong Increase

0 10 20 30 40 50 60

2.9

16.5

59.7

20.5

0.4

3.3

16.9

54.5

24.2

1.1 Hiring Plans Capital Expenditures

ABCI™ ABCI™

Center for Business and Economic Research, The University of Alabama 19

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q30

10

20

30

40

50

60

70

80

90

100

51.6 47.955.0 55.8

51.445.5

50.856.8

50.2

Inde

x

2010 2011 2012

This Alabama GDP and employment forecast summary is the CBER July 2012 preliminary forecast

Preliminary 2013 forecast included below

Alabama Forecast Summary Alabama Forecast Summary

Probability: Forecast (60 Percent) and Range (90 percent)

CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 20

(Percent change) 2010 2011 2012 2013

Real GDP 2.3 1.5 2.0 2.1

range 0.5 to 2.5 1.5 to 3.0 1.8 to 3.5

Employment -0.8 -0.2 0.5 1.5

range 0.1 to 1.5 0.7 to 2.3

Total Tax Receipts, FY -2.5 5.0 4.0 4.1

range 3.5 to 4.5 3.0 to 7.0

Alabama Gross Domestic Product andEmployment by Metro Areas

Alabama Gross Domestic Product andEmployment by Metro Areas

Center for Business and Economic Research, The University of Alabama 21

Source: Alabama Department of Industrial Relations, U.S. Bureau for Economic Analysis.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2.582.87

26.10

2.853.003.001.88

11.04

9.36

8.72

4.94

23.65

Non-metro areas

Tuscaloosa

Montgomery

Mobile

Huntsville

Gadsden

Florence-Muscle Shoals

Dothan

Decatur

Birmingham-Hoover

Auburn-Opelika

Anniston-Oxford

Alabama Employment by Metro Area0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2.162.11

31.20

2.832.672.381.53

12.11

9.18

8.65

5.13

20.05

Alabama GDP by Metro Area

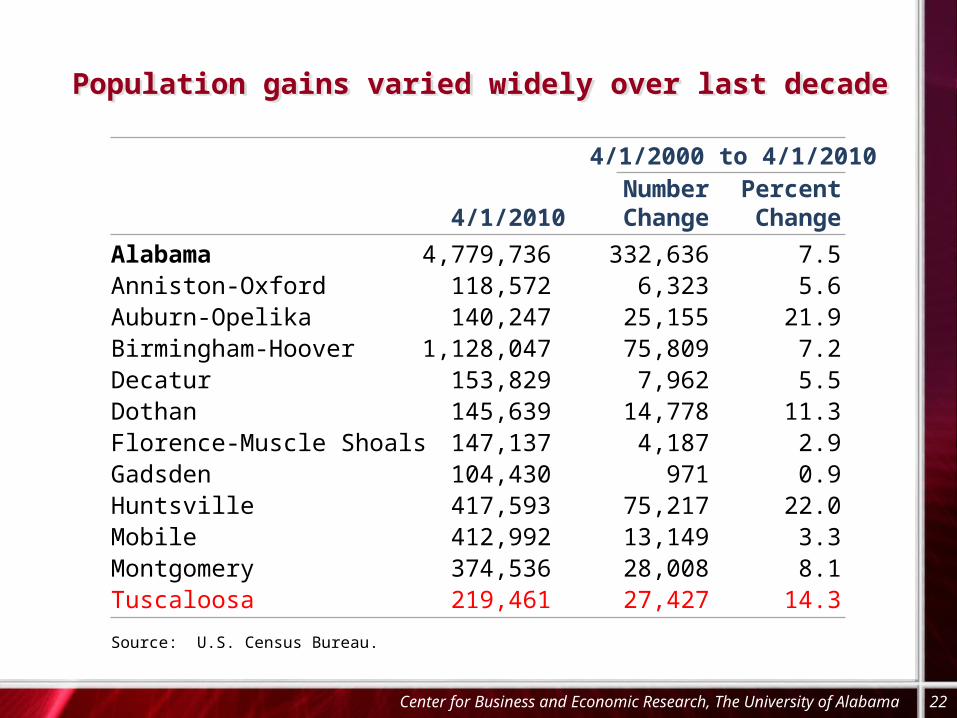

Population gains varied widely over last decadePopulation gains varied widely over last decade

4/1/2000 to 4/1/2010 Number Percent

4/1/2010 Change Change

Alabama 4,779,736 332,636 7.5Anniston-Oxford 118,572 6,323 5.6Auburn-Opelika 140,247 25,155 21.9Birmingham-Hoover 1,128,047 75,809 7.2Decatur 153,829 7,962 5.5Dothan 145,639 14,778 11.3Florence-Muscle Shoals 147,137 4,187 2.9Gadsden 104,430 971 0.9Huntsville 417,593 75,217 22.0Mobile 412,992 13,149 3.3Montgomery 374,536 28,008 8.1Tuscaloosa 219,461 27,427 14.3

Source: U.S. Census Bureau.

Center for Business and Economic Research, The University of Alabama 22

Center for Business and Economic Research, The University of Alabama 23

Median Family Income FY2011

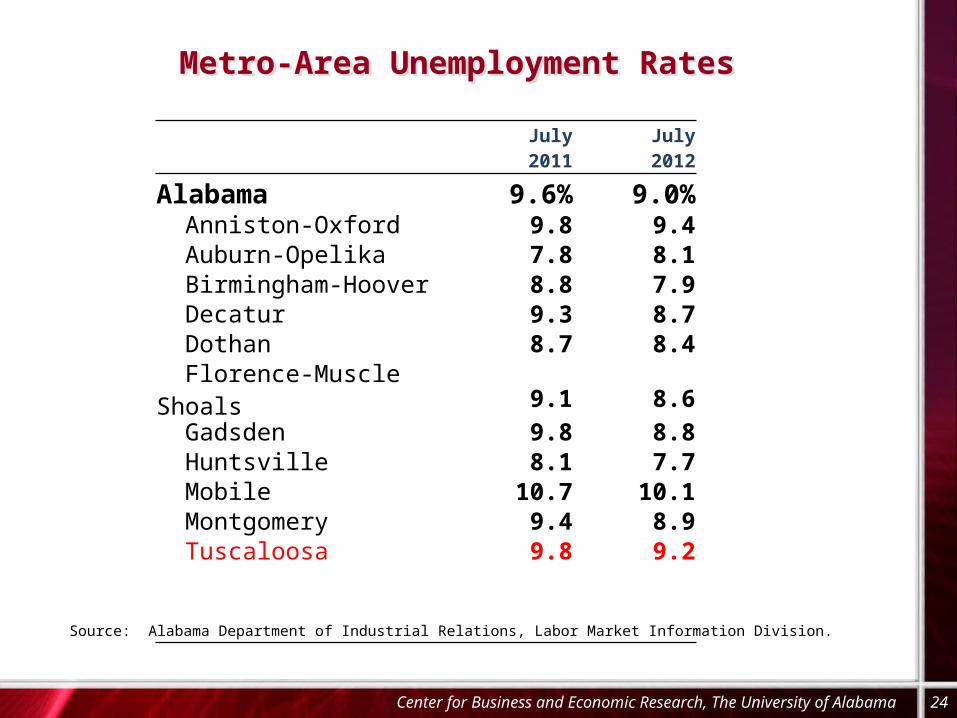

Metro-Area Unemployment RatesMetro-Area Unemployment Rates

Center for Business and Economic Research, The University of Alabama 24

Source: Alabama Department of Industrial Relations, Labor Market Information Division.

July 2011 July 2012

Alabama 9.6% 9.0% Anniston-Oxford 9.8 9.4 Auburn-Opelika 7.8 8.1 Birmingham-Hoover 8.8 7.9 Decatur 9.3 8.7 Dothan 8.7 8.4 Florence-Muscle Shoals 9.1 8.6 Gadsden 9.8 8.8 Huntsville 8.1 7.7 Mobile 10.7 10.1 Montgomery 9.4 8.9 Tuscaloosa 9.8 9.2

No metro back to 2007/2008 annual peak in 2011No metro back to 2007/2008 annual peak in 2011

2007 or 2008 Job Loss to 2011

Nonfarm Employment Peak Year Number PercentAlabama 2,003,800 -134,800-6.7Anniston-Oxford 53,500 -4,800 -9.0Auburn-Opelika 54,800 -2,200 -4.0Birmingham-Hoover 531,300 -43,200 -8.1Decatur 58,500 -5,100 -8.7Dothan 63,100 -7,000 -11.1Florence-Muscle Shoals 57,300 -1,800 -3.1Gadsden* 38,100 -2,900 -7.6Huntsville* 214,300 -6,600 -3.1Mobile* 184,700 -9,800 -5.3Montgomery 179,200 -13,200 -7.4Tuscaloosa* 98,500 -5,800 -5.9Net Jobs in Metropolitan Areas -102,400

Net Jobs in Nonmetro Counties -32,400* Gadsden, Huntsville, Mobile, and Tuscaloosa employment peaked in 2008; all others saw peaks in 2007.

Note: Nonfarm employment (jobs) is by place of work. Data are January to November averages.

Source: Alabama Department of Industrial Relations and U.S. Bureau of Labor Statistics.

Center for Business and Economic Research, The University of Alabama 25

ABCI by Metro Area Q3 2012(Tuscaloosa – 51.0)

ABCI by Metro Area Q3 2012(Tuscaloosa – 51.0)

Center for Business and Economic Research, The University of Alabama 26

Montgomery

Mobile

Huntsville

Birmingham-Hoover

Alabama

0 10 20 30 40 50 60

53.1

48.9

48.3

52.8

50.2

Tuscaloosa Metro Area Nonfarm EmploymentTuscaloosa Metro Area Nonfarm Employment

Center for Business and Economic Research, The University of Alabama 27

IndustryJuly 2012

employmentNet change since

July 2011Total Nonfarm 87,300 -2,400Goods Producing 20,300 -300Natural Resources, Mining, and Construction 7,300 -400Manufacturing 13,000 100Service Providing 67,000 -2,100Trade, Transportation, Warehousing, and Utilities 14,500 200 -Wholesale Trade 2,000 200 -Retail Trade 10,200 0 -Transportation, Warehousing, and Utilities 2,300 0Information 900 0Financial Activity 3,400 -100Professional and Business Services 7,800 100Education and Health Services 7,200 -200Leisure and Hospitality 8,500 100Other Services 3,300 0Government 21,400 -2,200 -Federal 1,600 -100 -State and Local 19,800 -2,100

Source: Alabama Department of Industrial Relations

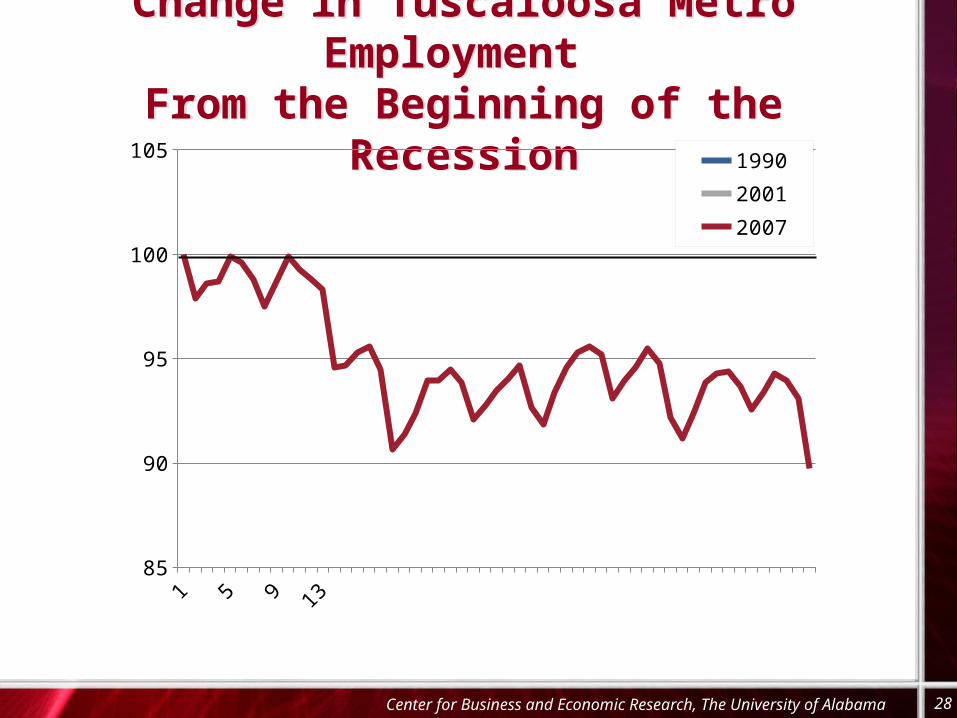

Change in Tuscaloosa Metro Employment From the Beginning of the Recession

Change in Tuscaloosa Metro Employment From the Beginning of the Recession

28Center for Business and Economic Research, The University of Alabama

85

90

95

100

105 1990

2001

2007

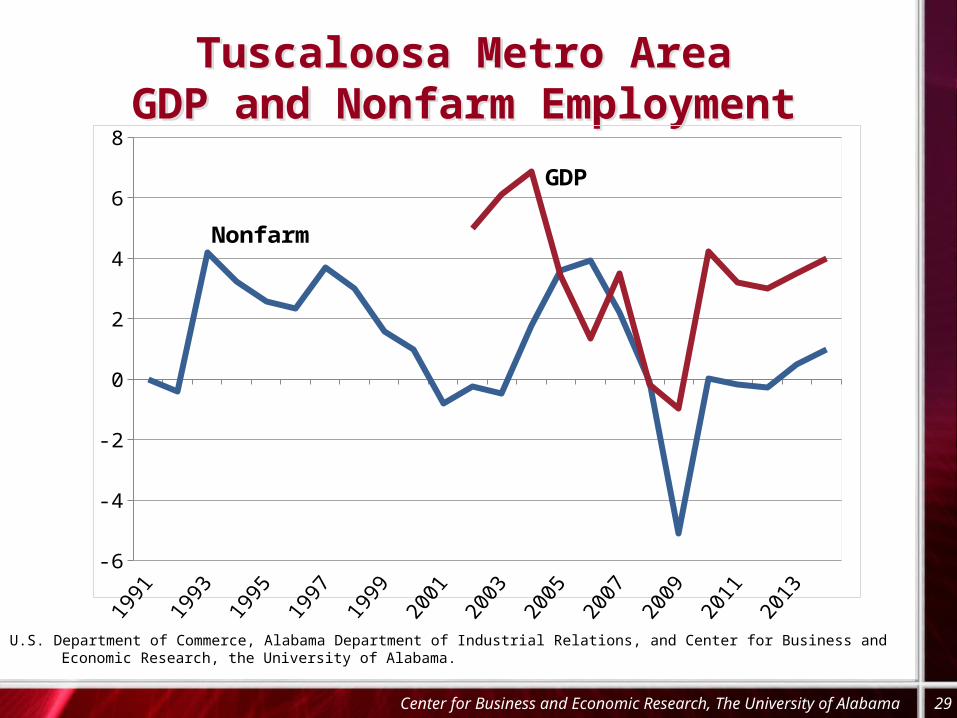

Tuscaloosa Metro AreaGDP and Nonfarm Employment

Tuscaloosa Metro AreaGDP and Nonfarm Employment

Center for Business and Economic Research, The University of Alabama 29

-6

-4

-2

0

2

4

6

8

Nonfarm

GDP

Source: U.S. Department of Commerce, Alabama Department of Industrial Relations, and Center for Business and Economic Research, the University of Alabama.

Ahmad Ijaz

Center for Business and Economic Research

Culverhouse College of Commerce and Business Administration

The University of Alabama

http://cber.cba.ua.edu (205) 348-6191

Questions, comments, suggestions, discussion,…

Thank You

Center for Business and Economic Research, The University of Alabama 30