welcome to the “national pension system” nps – pension nahi yeh pran hai 1 ‘nps’ - pension...

TRANSCRIPT

1

Welcome to the

“National Pension System”NPS – Pension nahi yeh Pran Hai

‘NPS’ - Pension nahi yeh Pran hai

2

Agenda

Understanding NPS…. What is NPS ? How does it work ?

Why should I invest in NPS ?

How is it superior to other Retirement Plans ?

Tax treatment on Contribution, Accretion & Maturity under NPS.

NPS Report Card – 1. Assets Under Management

2. Fund Performance as on 31/03/2015

NPS‘NPS’ - Pension nahi yeh Pran hai

3

About NPS

NPS is a ‘Government of India’ initiative with an objective of Development of a sustainable and efficient voluntary defined contribution Pension System in India. It is regulated by PFRDA.

NPS provides a platform for savings through three baskets of Investment Equity (E), Corporate Bonds (C) and Govt. Securities (G) to create a Retirement Corpus (Pension Wealth), to enable subscriber for purchasing Annuity post retirement.

It also allows for withdrawal of up to 60% of the Retirement Corpus post retirement. The withdrawal can be spread over 10 Years post Retirement age.

It is open for all citizens of India (Resident/Non Resident) who are between 18-60 years of age.

‘NPS’ - Pension nahi yeh Pran hai

4

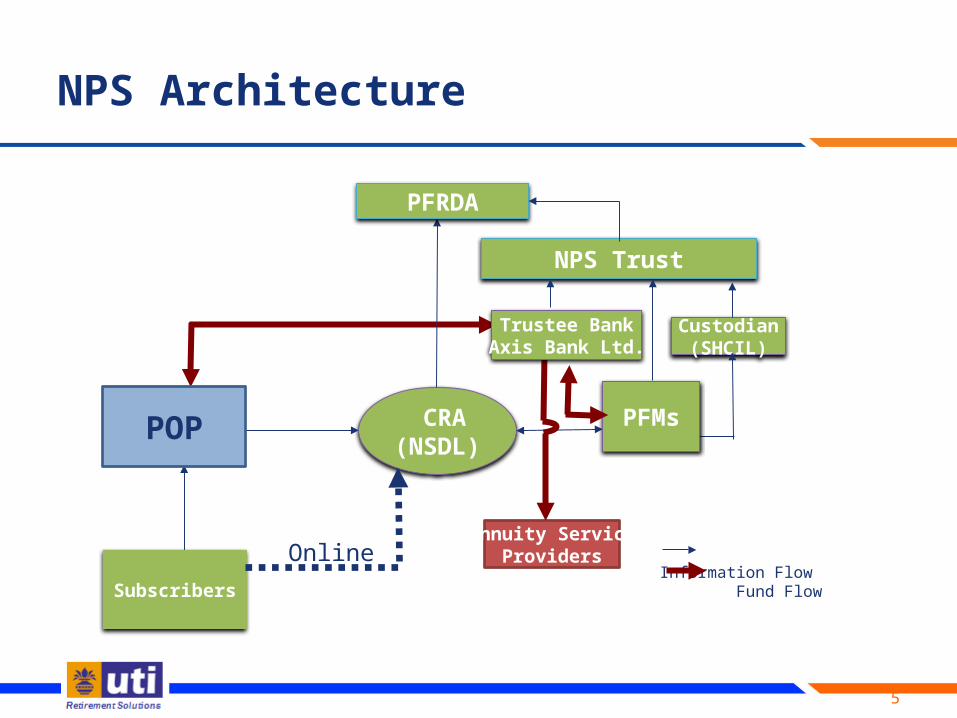

NPS - Architecture

Main Components of the NPS Architecture are :

1. Points of Presence (PoPs) – The first single contact point. It is the interface

between the subscribers and the NPS Architecture. Responsible for

disseminating all the information about NPS.

2. Central Recordkeeping Agency (CRA) -( at present NSDL)

3. Pension Fund Managers – ( at present 8 PFMs)

4. Custodian (SHCIL)

5. Trustee Banker (Axis Bank Ltd.)

6. Annuity Service Providers - (at present 7 annuity providers)

It has an unbundled Architecture. Ownership of the Product does not lie with any single entity

5

NPS Architecture

CRA(NSDL)

Subscribers

Custodian(SHCIL)

NPS Trust

Annuity ServiceProviders

PFMs

PFRDA

Online

POP

Information Flow Fund Flow

Trustee BankAxis Bank Ltd.

6

Why should I invest in NPS?

Additional Tax Deduction: Opportunity of Extra Tax Savings under Sec 80 CCD (1B) up to

Rs.50000/- ( This is applicable for investments in NPS only) and is over and above the Sec 80C limit.

Lower Expense Ratio : NPS is perhaps the world’s lowest cost pension scheme. The total recurring expenses inclusive of the Fund Management fee and all other handling and administrative charges would work out to be around 0.05% to 0.21% p.a. The Lower Expense ratio would lead to HIGHER RETIREMENT CORPUS.

Ensures Complete Portability: NPS account can be operated from anywhere in the country

irrespective of employment and geography.

Tax Efficient : The Retirement Corpus used for buying Annuity will be totally Taxfree.

No liquidity before Retirement: Under Normal circumstances, No withdrawal is allowed before

Retirement i.e. 60 Years of age. In a true sense this investment will prove to be the "REAL BUDHAPE

KI LATHI".

Flexibility: Subscribers have - i) Choice of Pension Fund managers (PFMs)

ii) Choice of Investment mix

iii) Choice of Life Cycle Fund is also availableI have a freedom to change the PFM or the Investment Mix once a year without any exit load.

7

Public Provident Fund (PPF)

Mutual Fund Pension Schemes

Pension Plans from Insurance Companies

Small Savings Scheme (Post Office Investments)

Other customized Individual Products

Is there any other good option available?

Popular Retirement Tools……

‘NPS’ - Pension nahi yeh Pran hai

8

How is it superior to other perceived Retirement Plans ?

Parametres

<=== Products ===>

NPS MF Pension Products

Insurance Pension Products PPF Postal

Savings

Tax RebateAdditional Tax Savings under

Sec 80 CCD (1B) which is beyond the Sec 80 C Limit

Only under Sec 80 C Limit

Only under Sec 80 C Limit

Only under Sec 80 C Limit

Only under Sec 80 C Limit

Expense Ratio Ranges between 0.15% to 0.25%

Ranges between 2% to 2.50%

Ranges over 2.50%Government Administered

Government Administered

Returns Market Linked Market Linked Market LinkedAssured (Depends

upon 10 Year G SEC current yield)

Assured

Asset Allocation

Subscribers can customize based on their Risk appetite. Also

change once a Year without any exit load

Based on Inestment Objective of the Scheme.

Investors can not customize it.

Based on Inestment Objective of the

Scheme. Investors can not customize it.

Government Administered

Government Administered

Liquidity No liquidity before Retirement Age

Liquidity available subject to exit load

Liquidity available subject to huge exit

load

Liquidity not before 7th Year

Not Available

Tax Treatment on Maturity

The amount used for purchasing Annuity - TAXFREE

The Amount withdrawn as lumpsum - TAXABLE

LTCG on Schemes where Equity Component < 65%

Taxfree where Equity Component >65%

Maturity Amount TAXFREE

Maturity Amount TAXFREE

Maturity Amount TAXABLE

Fund Managers Can be Changed once a Year without any exit load

Can not be Changed Can not be Changed N/A N/A

9

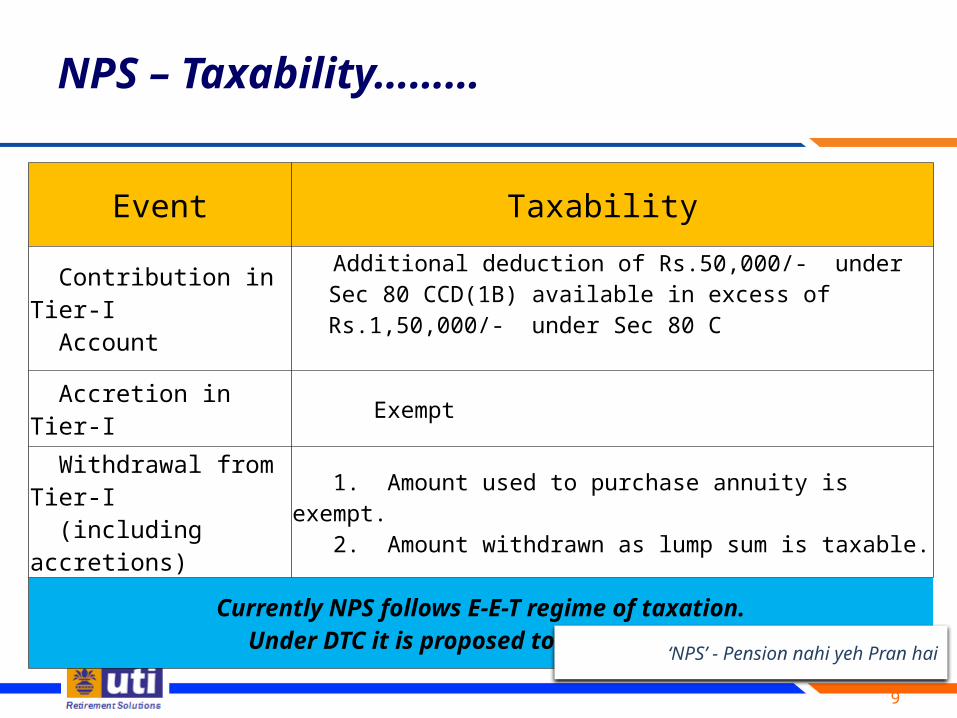

NPS – Taxability………

Event Taxability

Contribution in Tier-I Account

Additional deduction of Rs.50,000/- under Sec 80 CCD(1B) available in excess of Rs.1,50,000/- under Sec 80 C

Accretion in Tier-I Exempt

Withdrawal from Tier-I (including accretions)

1. Amount used to purchase annuity is exempt. 2. Amount withdrawn as lump sum is taxable.

Currently NPS follows E-E-T regime of taxation.Under DTC it is proposed to be under EEE.

‘NPS’ - Pension nahi yeh Pran hai

10

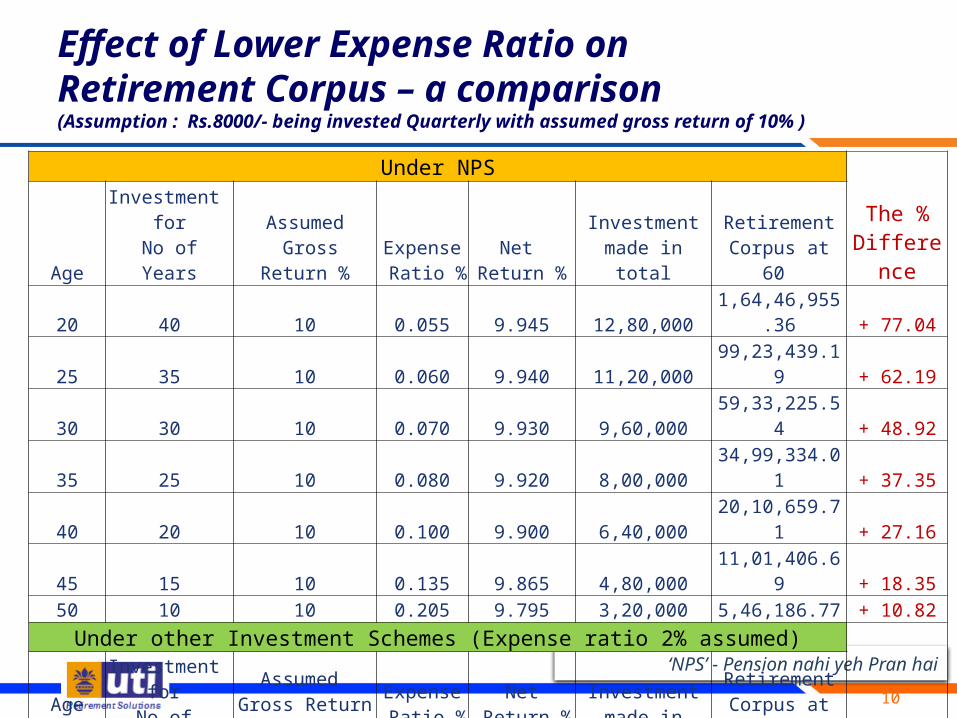

Effect of Lower Expense Ratio onRetirement Corpus – a comparison(Assumption : Rs.8000/- being invested Quarterly with assumed gross return of 10% )

‘NPS’ - Pension nahi yeh Pran hai

Under NPS

The % DifferenceAge

Investment for No of Years

Assumed Gross Return %

Expense Ratio %

Net Return %

Investment made in total

Retirement Corpus at 60

20 40 10 0.055 9.945 12,80,000 1,64,46,955.36 + 77.0425 35 10 0.060 9.940 11,20,000 99,23,439.19 + 62.1930 30 10 0.070 9.930 9,60,000 59,33,225.54 + 48.9235 25 10 0.080 9.920 8,00,000 34,99,334.01 + 37.3540 20 10 0.100 9.900 6,40,000 20,10,659.71 + 27.1645 15 10 0.135 9.865 4,80,000 11,01,406.69 + 18.3550 10 10 0.205 9.795 3,20,000 5,46,186.77 + 10.82

Under other Investment Schemes (Expense ratio 2% assumed)

AgeInvestment for

No of YearsAssumed

Gross Return %Expense Ratio %

Net Return %

Investment made in total

Retirement Corpus at 60

20 40 10 2.000 8.000 12,80,000 92,90,122.0425 35 10 2.000 8.000 11,20,000 61,18,558.1130 30 10 2.000 8.000 9,60,000 39,84,186.5135 25 10 2.000 8.000 8,00,000 25,47,815.6140 20 10 2.000 8.000 6,40,000 15,81,179.1745 15 10 2.000 8.000 4,80,000 9,30,660.5650 10 10 2.000 8.000 3,20,000 4,92,880.18

11

Effect of Lower Expense Ratio onRetirement Corpus – a comparison(Assumption : Rs.8000/- being invested monthly with assumed gross return of 10% )

‘NPS’ - Pension nahi yeh Pran hai

Under NPS

The % Difference

Age Investment for No of Years

Assumed Gross Return

%Expense Ratio %

Net Return %

Investment made in total

Retirement Corpus at 60

20 40 10 0.055 9.945 38,40,000 4,40,80,760 +69.9725 35 10 0.060 9.940 33,60,000 2,70,23,703 + 56.6530 30 10 0.070 9.930 28,80,000 1,64,09,728 + 44.7035 25 10 0.080 9.920 24,00,000 98,22,480 + 34.2140 20 10 0.100 9.900 19,20,000 57,23,667 + 24.9445 15 10 0.135 9.865 14,40,000 31,76,640 + 16.8650 10 10 0.205 9.795 9,60,000 15,94,268 + 9.92

Under Other Investment Schemes (Expense ratio 2% assumed)

AgeInvestment for

No of YearsAssumed

Gross Return %Expense Ratio %

Net Return %

Investment made in total

Retirement Corpus at 60

20 40 10 2.000 8.000 38,40,000 2,59,34,43125 35 10 2.000 8.000 33,60,000 1,72,50,82330 30 10 2.000 8.000 28,80,000 1,13,40,90635 25 10 2.000 8.000 24,00,000 73,18,71540 20 10 2.000 8.000 19,20,000 45,81,28045 15 10 2.000 8.000 14,40,000 27,18,22850 10 10 2.000 8.000 9,60,000 14,50,266

12

Starting Age

Total Amount Invested

Assumed Rate of Return

Retirement Corpus at Age 60

Assumed Rate of Return

Retirement Corpus at

Age 60

Assumed Rate of Return

Retirement Corpus at Age 60

18 346000 10% 8696192 11% 12316624 12% 17452471

19 340000 10% 7899629 11% 11090058 12% 15576563

20 334000 10% 7175481 11% 9985043 12% 13901646

21 328000 10% 6517164 11% 8989534 12% 12406184

22 322000 10% 5918694 11% 8092680 12% 11070950

23 316000 10% 5374632 11% 7284702 12% 9878776

24 310000 10% 4880029 11% 6556795 12% 8814336

25 304000 10% 4430390 11% 5901022 12% 7863943

Starting Age

Total Amount Invested

Assumed Rate of Return

Retirement Corpus at

Age 60

Assumed Rate of Return

Retirement Corpus at Age 60

Assumed Rate of Return

Retirement Corpus at Age 60

18 4200000 10% 59140070 11% 79806547 12% 108008262

19 4100000 10% 53663699 11% 71797790 12% 96335948

20 4000000 10% 48685181 11% 64582693 12% 85914239

21 3900000 10% 44159256 11% 58082607 12% 76609142

22 3800000 10% 40044778 11% 52226673 12% 68301020

23 3700000 10% 36304343 11% 46951056 12% 60883053

24 3600000 10% 32903949 11% 42198249 12% 54259869

25 3500000 10% 29812681 11% 37916441 12% 48346312

13

NPS Report Card

1. Assets Under Management

2. Fund Performance as on 31/03/2015

14

Where do we Stand now in terms of AUM?

Total AUM Details as on 31/03/2015

Pension Fund Manager AUM% of Total Industry

SBI PENSION FUNDS PRIVATE LIMITED 31407.09 38.84 UTI RETIREMENT SOLUTIONS LIMITED 24831.45 30.71 LIC PENSION FUND LIMITED 24010.13 29.70 ICICI PRUDENTIAL PENSION FUNDS MGMENT COMPANY LTD 369.00 0.46 KOTAK MAHINDRA PENSION FUND LIMITED 107.47 0.13 RELIANCE CAPITAL PENSION FUND LIMITED 76.97 0.10 HDFC PENSION MANAGEMENT COMPANY LIMITED 53.08 0.07 Grand Total 80855.19 100.00

15

Incentive Scenario for IFAs…….

Rs.75/- per Application

Up front commission of 0.15% of the amount mobilised i.e. on each instalment

16

Annuity Service Providers

Subscribers of the National Pension System (NPS) would have a choice to select Annuity Service Providers, and annuity schemes offered by them at the time of exit from NPS.

Pension Fund Regulatory and Development Authority (PFRDA) has at present empaneled the following Seven IRDA approved life insurance companies for providing annuity services to the subscribers of National Pension System (NPS).

1. Life Insurance Corporation of India 4. Bajaj Allianz Life Insurance Co. Ltd

2. SBI Life Insurance Co. Ltd. 5. Star Union Dai-ichi Life Insurance Co. Ltd.

3. ICICI Prudential Life Insurance Co. Ltd. 6. Reliance Life Insurance Co. Ltd.

4.

7. HDFC Standard Life Insurance Co. Ltd.

17

Types of Annuity available:

• Pension (Annuity) payable for life at a uniform rate to the annuitant only.

• Pension (Annuity) payable for 5, 10, 15 or 20 years certain and thereafter as long as you are alive.

• Pension (Annuity) for life with return of purchase price on death of the annuitant (Policyholder).

• Pension (Annuity) payable for life increasing at a simple rate of 3% p.a.

• Pension (Annuity) for life with a provision of 50% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

• Pension (Annuity) for life with a provision of 100% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

18

Low Expense Ratio

‘NPS’ - Pension nahi yeh Pran hai

Charges under NPSIntermediary Charge Head Service Charge

Method of Deduction

PoP

Initial Subscriber Registration (One Time) Rs. 100/-

To be collected upfront

Initial Contribution 0.25% of the amount mobilised

All Subsequent Contributions Minimum: Rs.20/- & Maximum: Rs.25000/-

Any Non Financial Transaction Rs.20/- per Transaction

CRA

PRA Opening (One Time) Rs.50/-

Through NAV Cancellation/

Deduction

PRA Maintanance (Per Annum) Rs.190/-

Per Transaction (Financial/Non Financial) Rs.4/-

Custodian Asset Servicing (Per Annum) 0.0075%

PFM Investment Management Fee 0.01 % per Annum

The overall expense ratio (PoP Charges + CRA Charges+ PFM Charges+ Custodian Charges) will range from 0.05% to 0.21% depending on the subscriber’s entry age from 18 to 50 Years

19

Important ….

Any person above the age of 18 irrespective of nature of employment or profession can open an NPS account.

NPS is flexible and portable i.e the NPS account opened once can be used anywhere across India even when you change your job, profession, Location etc.

NPS is independent of other retirement plans/investments. Any person with or without existing retirement plans/investments like EPF/PF, PPF, Insurance Policies, Mutual Funds, Bank Deposits etc can open NPS account and plan the retirement better.

NPS investments can be customised (within the specified asset class and limits) as per individual need and can be changed once a year.

NPS also provides an Auto Choice Option for investment where investments in asset classes of Equity, Corporate debt and Gsec gets realigned based on persons age.

Opening an account in NPS is the first step for securing ones Sunset Years

20

Disclaimer : The Illustration and figures given in the presentation are only for understanding

purpose and based on assumptions mentioned in each illustration. Investments in the scheme are subject to the risk involved with various asset

class. Past performance may or may not be sustained in future. Nothing contained

herein shall amount to the PFM having assured any minimum rate of return on the investment.

All investment in Pension Funds and securities are subject to market risks and the NAV of the funds may go up or down depending on the factors and forces affecting the securities market.

For complete information of NPS please refer to the Offer document and/or log on to PFRDA website www.pfrda.org.

Details of Tax Deductions as per Budget Memorandum 2015

Deduction u/s 80C Rs. 1,50,000 Deduction u/s 80CCD (1B) - (Only NPS) Rs. 50,000 Deduction on account of interest

on house property loan (Self occupied property) Rs. 2,00,000 Deduction u/s 80D on health

insurance premium Rs. 25,000 Exemption of transport allowance Rs. 19,200

Total Rs. 4,44,200

23

THANK YOU