welcome to taxmama’s place home of the after successful

TRANSCRIPT

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 1Page 1

After SUCCESSFUL Collections or Audits – What Next?

Welcome to TaxMama’s Place Home of the

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 2Page 2

Table of Contents

Meet Your InstructorsThe end of the auditClosing letters – how to read them, and ensuring you get them, and the importance of ensuring you get themAdjustment of tax attributesAmending prior IRS and State returns affected by the settlementPreparing current year returns based on audit resultsGetting liens releasedEvaluations and Thanks!

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 3Page 3

Who is Eva Rosenberg MBA, EA

Eva Rosenberg, EA, Your TaxMama® has been teaching Enrolled Agents Exam review courses off and on since developing the program for UCLA Extension over 15 years ago. These days, she’s teaching her own course online at www.irsexams.com

Eva has a BA in Accounting and an MBA in International business. Your TaxMama® is a TaxWatch columnist for Dow Jones' www.MartketWatch.com and author of the ever-popular book, Small Business Taxes Made Easy, published by McGraw-Hill – new edition – just released!

As a speaker, TaxMama® is popular with both tax professionals and taxpayers. You can find her at www.TaxMama.com and subscribe to her free daily podcast at www.TaxQuips.com

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 4Page 4

Who is Tom Buck, CPA

Tom Buck, CPA is a published author, tax coach, teacher And mentor. He has been a licensed CPA since 1971 and has been in private practice since 1982.

Tom was chairman of the Nevada Society of CPAs Taxation Committee. Tom has been representing taxpayers and solving IRS problems ever since the landmark Casino employee cases in 1982.

The approach Tom takes and that he would like to pass on to you is this:the “science” of the work is the law and how it should be applied. The “art” is being able to counter any and all IRS measures which are not supported by law. Does the IRS always follow the rules? Of course not, so part of the “art” is really in forcing the IRS to obey the law. Of course, having the tenacity of a bulldog is often the critical ingredient. In the final analysis, once you determine what the outcome should be, then you must be ready to take any detours necessary to get your client to the finish line.

Tom is a willing and helpful teacher and looks forward to sharing his hard-gained knowledge.

08/15/11

Page 4

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 5Page 5

Who is Sonya Wilt, EA

Sonya Wilt, BS in Management, EA and entrepreneur. A graduate of Upper Iowa University, Fayette, and former student of Eva Rosenberg’s Enrolled Agent Review Course, Sonya also has an extensive background in management and accounting, small business consulting, and employee training

Sonya’s desire to stay on top of the changes in tax law is two-fold: 1) To make sure her investments and entities are taking advantage of

every legal tax deduction available with adequate documentation, and…

2) 2) To provide our clients with accurate information so they may make solid decisions in both resolving current tax issues and legally protecting their future earnings.

Sonya and her partner, Tom Buck, CPA aggressively represent clients before state and federal taxing authorities through audits, appeals and collections.

08/15/11

Page 5

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 6The End of and Audit

A perfect audit = No Change …Whatsoever

A good audit = No Change – to the tax due, but there are underlying changes that affect carryovers

An acceptable audit = Additional tax up to $500 - $1,000A bearable audit = There’s a balance due, but you expected it

from the beginning – and prepared your client for it.

A bad audit = Results you didn’t prepare your client for!We won’t be talking about this.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 7IRS Letters you might get

A. Form 886-A, Explanation of Items;B. Form 1273, Report of Estate Tax Examination Changes;C. Form 2504, Agreement to Assessment and Collection of Additional Tax and Acceptance of

Overassessment. - NEVER SIGN THIS!D. Form 4549, Income Tax Examination Changes—for agreed cases for individuals and

corporations; E. Form 4549–A, Income Tax Examination Changes—for unagreed and accepted agreed cases

for individuals, corporations, taxable fiduciaries, and taxable small business corporations; F. Form 4605, Examination Changes—Partnerships, Fiduciaries, Small Business Corporations,

and Domestic International Sales Corporations—used to report audit changes made to partnership, fiduciary, and small business corporation returns;

G. Form 4605–A, Examination Changes—Partnerships, Fiduciaries, Small Business Corporations, and Domestic International Sales Corporations—for unagreed and excepted agreed cases for partnerships, fiduciaries, and small business corporations;

H. Form 4665, Report Transmittal—never send the taxpayer or power of attorney copies of Form 4665;

I. Form 4666, Summary of Employment Tax Examination.J. Form 4667, Examination Changes—Federal Unemployment TaxK. Form 4668, Employment Tax Examination changes Report and,L. Form 5385, Excise Tax Examination Changes.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 8Form 2504

Form 2504, Agreement to Assessment and Collection of Additional Tax and Acceptance of Overassessment. - NEVER SIGN THIS!

Sometimes IRS assesses additional tax and you can’t do anything to prevent it.

Instruct the client to pay, if there’s no other choice.

Do NOT sign this form!Why?

If you find additional information later to prove your client’s case, you can’t use it. The taxpayer has agreed to the tax.

If client doesn’t sign – you can amend that tax return within 2 years of the payment of the additional tax.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 9Page 9Adjustments & Closing Letters

The importance of closing letters – why you need them…CYA

These letters are your proof.

Making sure the revenue officer actually made the changes as agreed.

There are often adjustments to NOL or depreciation schedules that will affect other years.

If the IRS as agreed with your position on certain issues the closing letter can provide protection against future audits of the same items. Audit results usually impact future tax preparation.

Removal of tax liens, proving tax liability has been paid, etc. If you’ve dealt much with the IRS, it is not uncommon to have to provide them with information they already have.

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 10Page 10Closing Letters

Ensure you get a copy – IRS is required to send out copies to both taxpayer and POA on file, we have our clients fax us a copy of all correspondence received from IRS

08/15/11

Reading them – unless it is a no change audit you should receive a 4549 Income Tax Examination form (or similar form depending on type of audit) that explains the changes that were discussed, and the penalties that were assessed.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 11No Need to Amend Future Returns

Very few audits result in absolutely no change at all.Changes – affecting only the year of audit

Schedule A MedicalSchedule A Property TaxSchedule A Mortgage InterestSchedule A MiscellaneousSchedule B Dividends and InterestSchedule C profitSchedule D profit Schedule E profit

Check to see if changes affect that year’s State tax return(s) or future returns.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 12Need to Amend for

Some typical changes that may require 1040X:Schedule A – Charitable Contributions carryoverSchedule B – May affect Foreign Tax Credit Form 1116Schedule C losses

NOL carryforward or backOffice in Home carryforwardDepreciation schedule (Sec 179 recaptured)Vehicle worksheet

Schedule D loss carryforwardsBasis adjustments of any kinds – especially cancellation of debt attribute reductions picked up in auditSchedule E passive lossesForm 3468 – Investment Credit CarryoversForm 4952 – Investment Interest carryforwardsForm 6251 – AMT carryforwardsForm 6252 – Installment agreement

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

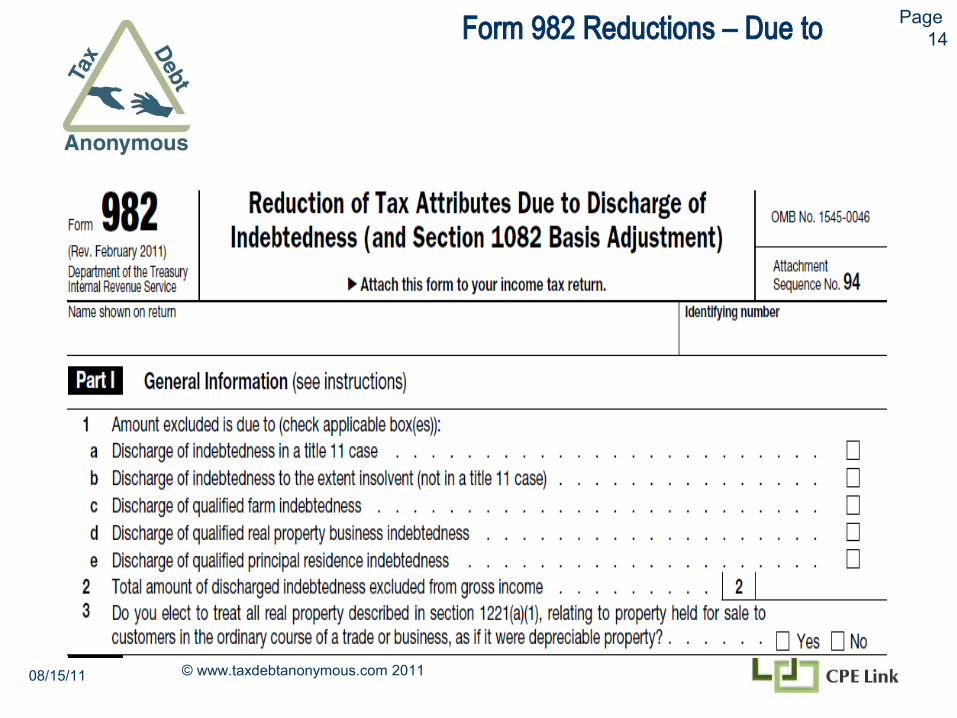

Page 13Attribute Reductions

The audit may have generated issues, like a surprise cancellation of debt.

You helped client avoid tax using insolvency. The insolvency caused a reduction in tax attributes.You and the examiner prepared a Form 982 for the year of

the audit. You must pick up attribute reductions in subsequent years.Attributes that get reduced – see Form 982

Note: After a bankruptcy, you may have to reduce tax attributes and amend carryforwards, too.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 14Form 982 Reductions – Due to

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 15Form 982 – Attributes to Reduce

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 16Some Attributes Only Partially Reduced

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 17Amending Prior Year Returns

What amendments are possible or needed?

Audits take place 18 months – 30 months after filingBy end of audit, statutes of limitations on years before audit are often closedYears after the audit, before the current year, are still open.NOL carrybacks may be possibleAlways remember state amendments, too

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 18Form 1040X - Top

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 19Form 1040X-Center

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

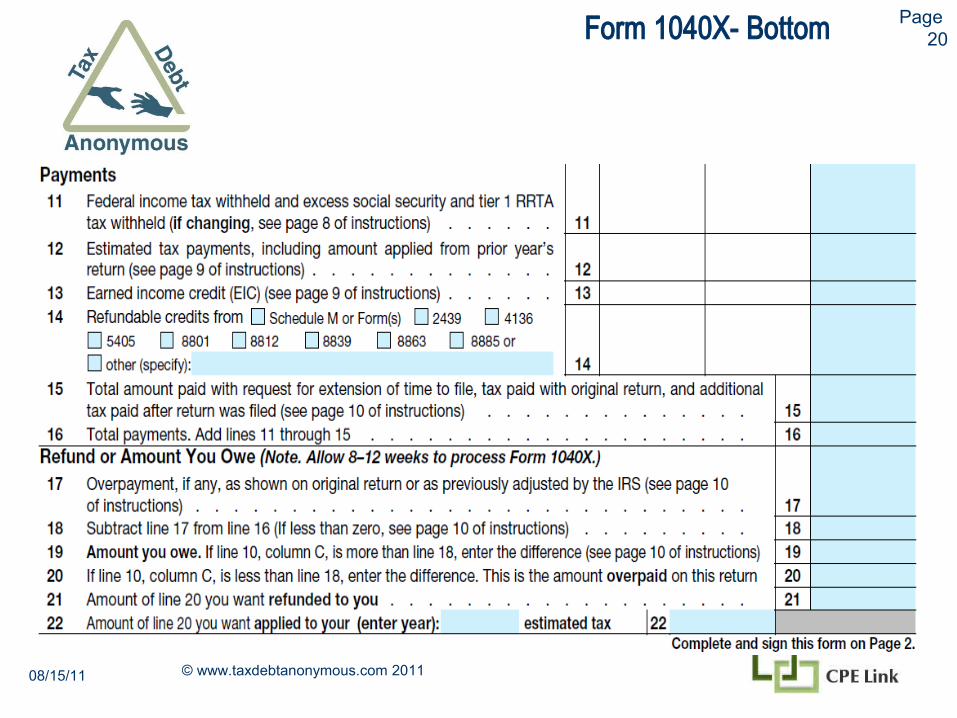

Page 20Form 1040X- Bottom

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

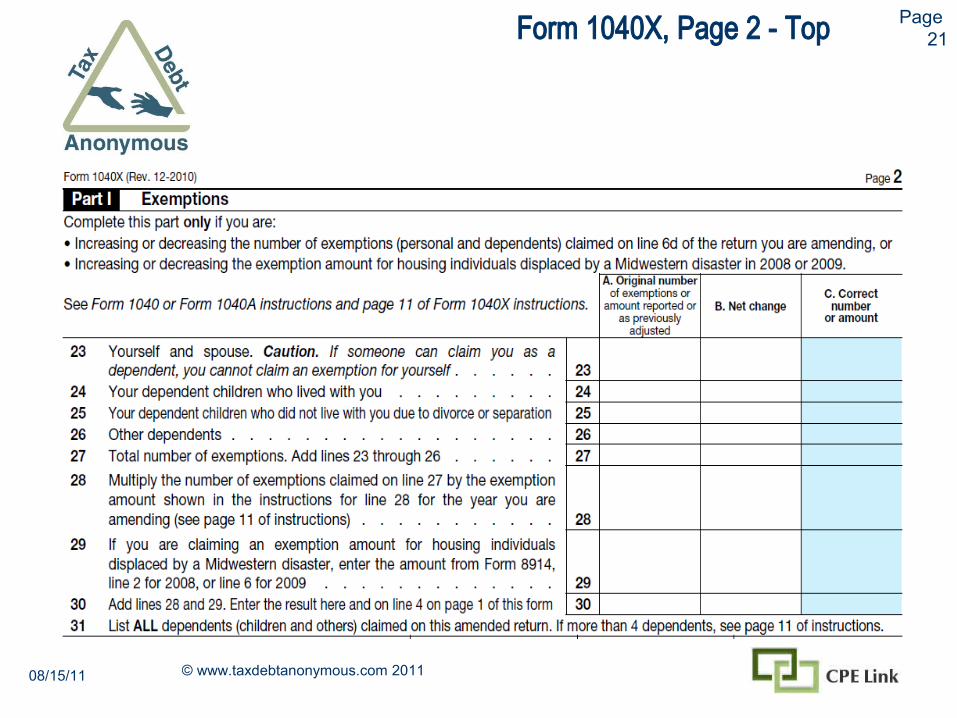

Page 21Form 1040X, Page 2 - Top

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 22Form 1040X, Page 2- Bottom

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 23Amending Open Statute Years

Use the Form 1040X – Revised Dec 2010Open old tax return file• Print out copy of the original tax return - Stamp it AS ORIGINALLY

FILED.• Save the file with a new name – filenameX• Make your revisions in the new file.

Make revisions based on the auditReview the tax return for any improvements you can make based on law changes, Presidential disaster areas, new information about dependents, deductions, expenses, etc. Theft Loss – deduct in year of discovery – up to 7 years after the theftIf you know of any significant errors not in the client’s favor that need to be corrected, advise the client those should be made, too

• Print out the revised tax return - Stamp it AS AMENDED

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 24Significant Changes and Worksheets

In addition to the revised forms, include detailed worksheets or spreadsheets

Changes in capital gains (basis) or capital loss carryovers DepreciationOffice in Home carryforwardAdjusted home basis due to Rental of part of home

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 25NOL Carrybacks – Special 5 Year Carryback

Audit of 2008 or 2009 tax year or fiscal year

American Recovery and Reinvestment Act of 2009, enables small businesses with a net operating loss (NOL) in 2008 to elect to offset this loss against income earned in up to five prior years. Typically, an NOL can be carried back for only two years. http://www.irs.gov/newsroom/article/0,,id=205329,00.html

The Worker, Homeownership, and Business Assistance Act of 2009 (WHBAA) expanded the carryback for 2008 and 2009. http://www.irs.gov/newsroom/article/0,,id=215657,00.html

The IRS released legal guidance in Revenue Procedure 2009-19 (Update: please see superceding Revenue Procedure 2009-26) outlining specific details.

If a small business previously elected to waive the carryback of 2008 NOL but now wants to elect this special carryback, the small business may revoke its previous election to waive the carryback. The election revocation must be made on or before April 17, 2009.

In other words, if the NOL carryback was originally waived, the 5-year option for 2008 NOLs is not available.

However, many taxpayers, even preparers, neglect to elect the NOL carryback waiver. So it may be obligatory to carryback any NOLs before carrying them forward. The 5-year option may still be in effect.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 26Waiving NOL Carryback

To waive the carryback when filing an original tax return, or an amended tax return that creates an NOL, include the following statement with the tax return:

Taxpayer elects to waive the net operating loss carryback under section 172(b)(3) of the Internal Revenue Code

If you filed your return timely but did not file the statement with it, you must file the statement with an amended return for the NOL year within 6 months of the due date of your original return (excluding extensions).

Enter “Filed pursuant to section 301.9100-2” at the top of the statement.

Note: This election is irrevocable.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 27NOL Carryback Options

Two options:

Form 1040X – one year at a time

Form 1045 – the quick way – several years

Note 1: After carryback is used up, NOL is carried forward up to 20 years

Note 2: States may have different rules about both carrybacks and carryforwards.

PDF version of IRS Publication 536 includes an illustrated Form 1045 http://www.irs.gov/pub/irs-pdf/p536.pdf

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 28Quick NOL

Form 1045. You can apply for a quick refund by filing Form 1045. This form results in a tentative adjustment of tax in the carryback year. See the Form 1045 illustrated at the end of this discussion.

If the IRS refunds or credits an amount to you from Form 1045 and later determines that the refund or credit is too much, the IRS may assess and collect the excess immediately.

Generally, you must file Form 1045 on or after the date you file your tax return for the NOL year, but not later than one year after the end of the NOL year. If the last day of the NOL year falls on a Saturday, Sunday, or holiday, the form will be considered timely if postmarked on the next business day.

For example, if you are a calendar year taxpayer with a carryback from 2010 to 2008, you must file Form 1045 on or after the date you file your tax return for 2010, but no later than January 2, 2012.

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 29Page 29Amending State Returns

Often forgotten after an audit, Remember to amending the client’s state tax returns to conform to IRS results. States will get the IRS adjustments automatically – and will

issue their own assessments. However, some states (like California) assess penalties when

the amended return isn’t filed within 6 months after the audit. Sometimes, IRS will send the revisions to the states while you

are still in the Appeals or Tax Court process.Alert your client to watch for thisPut this assessment on hold until the IRS case is resolved

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 30Page 30Current & Future Prep

Preparing current year returns based on audit results

The best wayWhen rolling over clients from prior-year software, roll over the amended file.

• If you have already rolled over clients, delete the current year file and roll over the amended file.

• If you already have entries in the current file (probably), roll over the amended file and move the entries to the new client file.

This will keep all the carryovers intactMake sure all the carryovers are correct

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 31Page 31Dealing with Tax Liens

Federal Tax Liens hurt your clients! They are damaging to your client’s credit score. They often prevent the sale or refinance of your

clients property. They often prevent clients from obtaining credit for

other purchases. They can impact your clients credit for 10+ years.

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 32Page 32Dealing with Tax Liens

Resolving Federal Tax Liens

A Notice of Federal Tax Lien (NFTL) gives the IRS legal claim to your client’s property as security or payment for their tax debt. There are several ways to deal with Federal Tax Liens: Release (Paid in Full or Beyond Statute of Limitations) Discharge (Balance Remaining) Subordination (Balance Remaining) Withdrawal (Balance Remaining)

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 33Page 33Dealing with Tax Liens – full pay

Lien Release A Certificate of Lien Release Form 668Z – sent within 30 days Section 6325(a) directs IRS to issue Certificate of Lien Release

within 30 days of full payment or the lien becoming legally unenforceable…or if they accept a bond for payment of tax. Copy request 1-800-913-6050 Address for submitting written request or additional info see

http://www.irs.gov/pub/irs-pdf/p1450.pdf Send Certificate of Lien Release to all reporting Credit Bureaus

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 34Page 34Dealing with Tax Liens – debt remains

Lien Discharge - A Certificate of Discharge from Federal Tax Lien removes the lien from the property named in the Notice ofFederal Tax Lien (NFTL): Form 14135 6325(b)(1) – remaining property is equal to 2x (the federal tax liability +

mortgages, taxes, and other liens) 6325(b)(2)(A) – partial satisfaction when property is being sold and

proceeds above mortgages and settlement costs are paid to IRS 6325(b)(2)(B) – property being sold for less than combination of

mortgage(s) and settlement costs, no value in IRS lien 6325(b)(3) – sale of property will pay off lien, funds put in escrow to pay IRS

at closing 6325(b)(4) – bond issued to protect government interest in property

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 35Page 35Dealing with Tax Liens – debt remains

Lien SubordinationConvincing the IRS to take a second position. Form 14134 6325(d)(1) – refinance of existing mortgage, loan proceeds after

closing costs paid to IRS 6325(d)(2) – subordination would increase or improve collectability

of tax liability; i.e.. Lower interest rate – a written statement (signed & dated) explaining benefit to IRS

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 36Page 36Dealing with Tax Liens

Lien WithdrawalIRS Office of Chief Counsel concluded: “In the absence of a definition of

‘best interests’ in the Code or regulations, we believe that this term can be

broadly defined so as to permit withdrawal where the NFTL has been

released but the taxpayer nevertheless needs the NFTL withdrawn to

improve his credit. In the general sense, withdrawal can be said to be in the

United States’ best interests insofar as the improvement in the taxpayer’s

credit history assists him with future tax compliance.”

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 37Page 37Dealing with Tax Liens

Lien Withdrawal Form 12277 - Help your client improve their credit by requesting

a tax lien withdrawal Paid In Full, Client Received Certificate of Lien Release, take it

one step further, request withdrawal Balance due <$25,000 with Direct Debit Installment Agreement

(DDIA)…Feb 2011, IRS announced it will now allow withdrawal of NFTL in client enters or converts to DDIA. Taxpayers with existing DDIAs can also request Lien Withdrawal.

08/15/11

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 38The Taxpayers Advocate and Liens

Nina Olson is passionate about IRS’s slowness in dealing with liens. She feels that, just as IRS has automated the lien generation process, they should be able to automate the lien release process for liens that have expired.

http://www.irs.gov/pub/irs-utl/2006_arc_vol_1_cover__section_1.pdf These are just some of the problems she has identified in her annual report to

Congress IRS had not addressed the following recommendations regarding management reviews of

lien processing information controls:• Implement procedures to closely monitor the release of tax liens to ensure that theyare released within 30 days of the date the related tax liability is fully satisfied. Aspart of these procedures, IRS should carefully analyze the causes of the delays inreleasing tax liens identified by GAO’s work and prior work by IRS’s former internalaudit function and ensure that such procedures effectively address these issues.• Research and resolve the current backlog of unresolved manual interest or penalties

reports. • Improve the current unmatched exception report by including a cumulative list ofall unmatched taxpayer accounts that have not been resolved to date

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 39Page 39Resources

Special 5-year NOL Carryback for 2008http://www.irs.gov/newsroom/article/0,,id=205329,00.html The Worker, Homeownership, and Business Assistance Act of 2009 (WHBAA) expanded the carryback for 2008 and 2009. http://www.irs.gov/newsroom/article/0,,id=215657,00.html Form 1040 X – Amended Returns http://www.irs.gov/pub/irs-pdf/f1040x.pdf Form 982 – Reduction of Attributes Due to Discharge of Indebtednesshttp://www.irs.gov/pub/irs-pdf/f982.pdf Lien Discharge Form - http://www.irs.gov/pub/irs-pdf/f14135.pdfLien Subordination Form - http://www.irs.gov/pub/irs-pdf/f14134.pdfLien Withdrawal Form- http://www.irs.gov/pub/irs-pdf/f12277.pdfNFTL Guidelines - http://www.irs.gov/pub/irs-pdf/p1468.pdfInternal Revenue Manual – Closing Letters - http://www.irs.gov/irm/part4/irm_04-075-015.html

08/15/11

Page 39

08/15/11 © www.taxdebtanonymous.com 2011 After Successful Audits & Collections

Page 40Page 40CPE Link

Thanks for coming.

Remember to give CPE Link your evaluations.

Drop by to sign up for other TaxMama classes – http://www.cpelink.com/teamtaxmama

The next class in the series is – Computing Or Recalculating IRS Assessments For Interest And Penalties– And Ways To Reduce Or Eliminate Both, if Possible

Series are available as Self-Study or Resources: • The Tax Practice Series - Taxpayer representation – Collections,

Offers In Compromise, other payment alternatives• TaxMama’s Courses

08/15/11

Page 40