welcome tax-exempt bodies fbt 2006 20 years on 2 recent developments dual cabs – update of...

TRANSCRIPT

WelcomeWelcome

TAX-EXEMPT TAX-EXEMPT BODIESBODIES

FBT 2006FBT 200620 years on20 years on

2

Recent developmentsRecent developments

Dual cabs – update of exempt vehicles – full list Apportioning entertainment between employees

and non-employees – clarification Car benefits – effect of contribution by employee

to purchase price Retention of electronic records – what satisfies the ATO? Meal Entertainment Fringe Benefit: 50/50 split

method - reimbursement of employer’s expenditure by a third party

Laptops - expense payment made earlier inthe FBT year

3

Recent DevelopmentsRecent Developments

Remote area housing - non-arm’s length

arrangements Remote area housing and water – how much is

taxable? Employee contributions -can excess contributions

be used in a later FBT year? New interest and penalties to be applied Employees in foreign service now subject to FBT ATO’s view on what constitutes a LAFHA – update

4

Recent DevelopmentsRecent Developments

Personal credit card payments – exempt or not? When to use 365 days or 366 days in formulae

– surprising ATO change Extended application of relocation concessions ANAO audit report on the administration of FBT Cancellation fees – FBT treatment The provision of food and drink in dining facilities

– when exempt Employer contributions to social clubs and

benefitsprovided by social clubs to members

5

Recent DevelopmentsRecent Developments

Payments on dwelling after employee terminates employment

Work related counselling – what can you provide as exempt benefit?

Charitable institutions and charitable funds – FBT differences

Laptop and loans – one benefit or two? Long service awards – exemption increased Exemption for work-related tools – more

laptop accessories included

6

Recent DevelopmentsRecent Developments

Remote area housing – more employers entitled to provide exemption

FBT rebate eligibility - Commonwealth, State and Territory institutions – latest

Entertainment – employees attending a function as a an employment duty

Relocation exemption – does it include transporting a car?

Employee discounts from third parties – sometimes taxable, sometimes not

7

WHAT IS A FRINGE WHAT IS A FRINGE BENEFITBENEFIT

A ‘payment’ to an employee, but in a different form to A ‘payment’ to an employee, but in a different form to salary or wages.salary or wages.

Employer, associate, third partyEmployer, associate, third party Employee, associateEmployee, associate in respect of employment. in respect of employment. right, privilege, service or facility.right, privilege, service or facility. former or future employee.former or future employee. by another person on behalf of the employer.by another person on behalf of the employer. to another person on behalf of the employee to another person on behalf of the employee

8

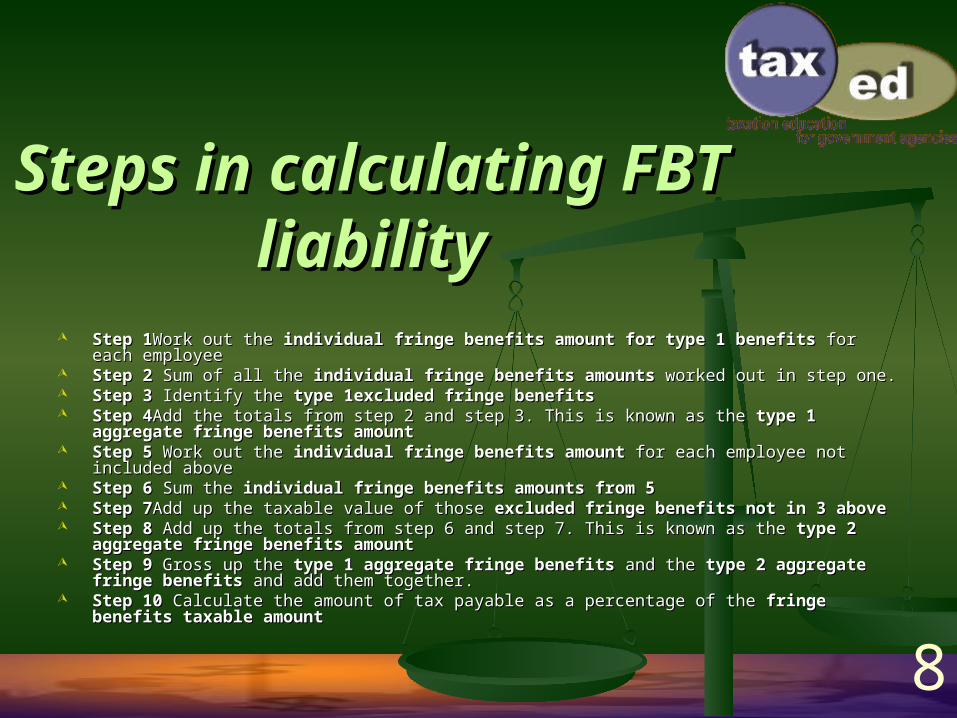

Steps in calculating Steps in calculating FBT liabilityFBT liability

Step 1Step 1Work out the Work out the individual fringe benefits amount for type 1 benefitsindividual fringe benefits amount for type 1 benefits for each for each employeeemployee

Step 2 Step 2 Sum of all the Sum of all the individual fringe benefits amountsindividual fringe benefits amounts worked out in step one. worked out in step one. Step 3 Step 3 Identify theIdentify the type 1excluded fringe benefits type 1excluded fringe benefits Step 4Step 4Add the totals from step 2 and step 3. This is known as the Add the totals from step 2 and step 3. This is known as the type 1 aggregate type 1 aggregate

fringe benefits amountfringe benefits amount Step 5 Step 5 Work out the Work out the individual fringe benefits amountindividual fringe benefits amount for each employee not included for each employee not included

aboveabove Step 6 Step 6 Sum the Sum the individual fringe benefits amounts from 5individual fringe benefits amounts from 5 Step 7Step 7Add up the taxable value of those Add up the taxable value of those excluded fringe benefits not in 3 aboveexcluded fringe benefits not in 3 above Step 8 Step 8 Add up the totals from step 6 and step 7. This is known as the Add up the totals from step 6 and step 7. This is known as the type 2 aggregate type 2 aggregate

fringe benefits amountfringe benefits amount Step 9 Step 9 Gross up the Gross up the type 1 aggregate fringe benefitstype 1 aggregate fringe benefits and the and the type 2 aggregate type 2 aggregate

fringe benefitsfringe benefits and add them together. and add them together. Step 10 Step 10 Calculate the amount of tax payable as a percentage of the Calculate the amount of tax payable as a percentage of the fringe benefits fringe benefits

taxable amounttaxable amount

9

Rebatable employersRebatable employers

Certain non-government, non-profit Certain non-government, non-profit organisations that are eligible for a rebate of organisations that are eligible for a rebate of 48 per cent of the amount of FBT that would 48 per cent of the amount of FBT that would otherwise be payable. 0.48 x (gross tax - otherwise be payable. 0.48 x (gross tax - aggregate non-rebatable amount) x rebatable aggregate non-rebatable amount) x rebatable days in year / total days in yeardays in year / total days in year

10

Compliance issuesCompliance issues

Rate of tax 48.5%. Rate of tax 48.5%. Registration As soon as you begin providing fringe Registration As soon as you begin providing fringe

benefits..benefits.. Annual return 21 MayAnnual return 21 May Fringe benefits tax assessmentsFringe benefits tax assessments Payment of FBT Instalments if previous year’s FBT Payment of FBT Instalments if previous year’s FBT

liability exceeded $3 000.liability exceeded $3 000. Record-keeping requirementsRecord-keeping requirements

11

Reportable fringe benefitsReportable fringe benefits

Grossed-up taxable value on payment summary benefits total taxable value exceeding Grossed-up taxable value on payment summary benefits total taxable value exceeding $1 000.$1 000.

'Reportable Fringe Benefits Amount'Reportable Fringe Benefits Amount RFBAs used in income tests for the following:RFBAs used in income tests for the following: superannuation surcharge superannuation surcharge termination payments surcharge termination payments surcharge Medicare levy surcharge Medicare levy surcharge deduction for non-employer sponsored superannuation contributions deduction for non-employer sponsored superannuation contributions tax offset for personal superannuation contributions tax offset for personal superannuation contributions tax offset for contributions to spouse’s superannuation tax offset for contributions to spouse’s superannuation HECS repayments HECS repayments child-support obligations child-support obligations entitlement to Family Tax Benefits, Child Care Benefit and Youth Allowance administered by entitlement to Family Tax Benefits, Child Care Benefit and Youth Allowance administered by

Centrelink and the Family Assistance Office.Centrelink and the Family Assistance Office.

12

Car fringe benefits Car fringe benefits

13

DefinitionDefinition

motor cars, station wagons, panel vans and utilitiesmotor cars, station wagons, panel vans and utilities all other goods-carrying vehicles with a designed all other goods-carrying vehicles with a designed

carrying capacity of less than one tonne, and carrying capacity of less than one tonne, and all other passenger-carrying vehicles with a all other passenger-carrying vehicles with a

designed carrying capacity of fewer than nine designed carrying capacity of fewer than nine occupants. occupants.

14

Requirements for car benefitRequirements for car benefit

Car held by an employer Car held by an employer Made available for the private use of an employeeMade available for the private use of an employee Taken to be made available for private use by an employee on any Taken to be made available for private use by an employee on any

day that: day that: it is actually used for private purposes by the employee, or it is actually used for private purposes by the employee, or the car is not at the employer's premises, and the employee is allowed the car is not at the employer's premises, and the employee is allowed

to use it for private purposes. to use it for private purposes. Garaged at an employee's home is available for the private use Garaged at an employee's home is available for the private use Private use of a motor vehicle that is not a car may give rise to a Private use of a motor vehicle that is not a car may give rise to a

residual fringe benefit. residual fringe benefit.

15

Home to work travelHome to work travel

Generally private Generally private Exceptions :Exceptions :

where the home constitutes a place of employment and travel is between two places of where the home constitutes a place of employment and travel is between two places of employment or business; employment or business;

where the taxpayer's employment can be construed as having commenced before or at where the taxpayer's employment can be construed as having commenced before or at the time of leaving home the time of leaving home

where the taxpayer transports bulky equipment necessary for employment; where the taxpayer transports bulky equipment necessary for employment; where the taxpayer's employment is inherently of an itinerant nature; and where the taxpayer's employment is inherently of an itinerant nature; and where the taxpayer is required to break his or her normal journey to perform where the taxpayer is required to break his or her normal journey to perform

employment dutiesemployment duties

16

Itinerant TravelItinerant Travel

inherently itinerant; inherently itinerant; fundamental part of the employee's work; fundamental part of the employee's work; impractical to perform the duties without the use of a impractical to perform the duties without the use of a

car; car; employee performs duties at more than one place of employee performs duties at more than one place of

employment; employment; the nature of the job makes travel in the performance of the nature of the job makes travel in the performance of

duties essential; and duties essential; and travelling in the performance of the employment duties travelling in the performance of the employment duties

from the time of leaving home.from the time of leaving home.

17

Statutory formula methodStatutory formula method

Taxable valueTaxable value = = (A x B x(A x B x C/D C/D) -E ) -E

A = the base value of the car A = the base value of the car B = the statutory percentage B = the statutory percentage C= the number of days in the FBT year when the car was used or C= the number of days in the FBT year when the car was used or available for private use of employees available for private use of employees D= the number of days in the FBT year D= the number of days in the FBT year E = the employee contributionE = the employee contribution

18

Annualised kilometresAnnualised kilometres

A x C / BA x C / BA = the number of kilometres travelled in the A = the number of kilometres travelled in the period during the year when the car was period during the year when the car was owned or leased by the employer owned or leased by the employer B = the number of days in that period B = the number of days in that period

C= the number of days in the FBT yearC= the number of days in the FBT year

19

Operating cost methodOperating cost method

Taxable valueTaxable value = (A × B) - C = (A × B) - C

A = the total operating costsA = the total operating costs

B = the percentage of private useB = the percentage of private use

C= the employee contribution C= the employee contribution

20

Operating costsOperating costs

Actual costs and some deemed costs Actual costs and some deemed costs GST inclusive as appropriate.GST inclusive as appropriate. Deemed depreciationDeemed depreciation ApportionedApportioned Year acquired - cost of the carYear acquired - cost of the car Subsequent year - depreciated value Subsequent year - depreciated value Depreciation cost limitDepreciation cost limit Car purchased before 1 July 2002:22.5%Car purchased before 1 July 2002:22.5% Car purchased on or after 1 July 2002:18.75%Car purchased on or after 1 July 2002:18.75% Deemed interestDeemed interest Actual operating costsActual operating costs repairsrepairs maintenance maintenance fuel fuel registration and insurance), and registration and insurance), and leasing costs.leasing costs.

21

Percentage of private Percentage of private useuse

Difference between 100 and the percentage of Difference between 100 and the percentage of business usebusiness use. .

Keeping of log book records and odometer Keeping of log book records and odometer records records

22

Exempt car fringe Exempt car fringe benefitsbenefits

taxi, panel van, utility, other commercial taxi, panel van, utility, other commercial vehicle vehicle

private use of such a vehicle is limited to: private use of such a vehicle is limited to: travel between home and work travel between home and work travel which is incidental to travel in the travel which is incidental to travel in the

course of duties of employment, and course of duties of employment, and non-work-related use that is minor, infrequent non-work-related use that is minor, infrequent

and irregular and irregular

23

Emergency vehicles Emergency vehicles ambulance, police or firefighting serviceambulance, police or firefighting service exterior markings exterior markings fitted with a flashing warning light and horn, fitted with a flashing warning light and horn,

bell or alarm bell or alarm

24

Record keepingRecord keeping Log book yearLog book year Not a logbook yearNot a logbook year Replacement carsReplacement cars

25

EntertainmentEntertainment IntroductionIntroduction

EntertainmentEntertainment Meal entertainmentMeal entertainment Categories of benefitsCategories of benefits Tax exempt body entertainment FBTax exempt body entertainment FB Income tax deductibilityIncome tax deductibility GST creditsGST credits

26

EntertainmentEntertainment IntroductionIntroduction

ExemptionsExemptions Reduction in taxable valueReduction in taxable value 50/50 split method50/50 split method 12 week register method12 week register method Entertainment leasing facility expenseEntertainment leasing facility expense Taxation ruling TR 97/17Taxation ruling TR 97/17

27

EntertainmentEntertainment Categories of BenefitsCategories of Benefits

Property FBProperty FB Expense payment FBExpense payment FB Residual FBResidual FB Meal entertainment FBMeal entertainment FB Tax exempt body entertainment FBTax exempt body entertainment FB Board FBBoard FB Airline transport FBAirline transport FB

28

EntertainmentEntertainment MeaningMeaning

Entertainment by way ofEntertainment by way of FoodFood DrinkDrink RecreationRecreation

Accommodation and travel iro aboveAccommodation and travel iro above Recreation includesRecreation includes

AmusementAmusement SportSport Similar leisure time pursuitsSimilar leisure time pursuits

29

EntertainmentEntertainment MeaningMeaning

Entertainment (32 -10 ITAA 97)Entertainment (32 -10 ITAA 97) The provision of propertyThe provision of property

Entertainment at time of Entertainment at time of provision?provision?

Direct connection with Direct connection with entertainment?entertainment?

ExampleExample Bottled spirits, TV sets etc.Bottled spirits, TV sets etc.

ExampleExample Glasses of champagne, hot Glasses of champagne, hot

meals, holiday accommodation meals, holiday accommodation etc.etc.

30

EntertainmentEntertainment Meal entertainmentMeal entertainment

Distinction between “entertainment” Distinction between “entertainment” and “meal entertainment” importantand “meal entertainment” important Can elect to be a distinct categoryCan elect to be a distinct category

~ 50/50 method of valuation50/50 method of valuation~ 12 week register method of valuation12 week register method of valuation~ If no election actual value of benefitIf no election actual value of benefit

Meal entertainment is excluded benefitMeal entertainment is excluded benefit

31

EntertainmentEntertainment Meal entertainmentMeal entertainment

Definition of “meal entertainment” Definition of “meal entertainment”

Entertainment bwo food or drinkEntertainment bwo food or drink Accommodation or travel iro aboveAccommodation or travel iro above Payment or reimbursementPayment or reimbursement Irrespective of:Irrespective of:

~ Business discussions/ transactionsBusiness discussions/ transactions~ Working overtime or performance of dutiesWorking overtime or performance of duties~ Promotion or advertisingPromotion or advertising~ At or connection with seminarAt or connection with seminar

32

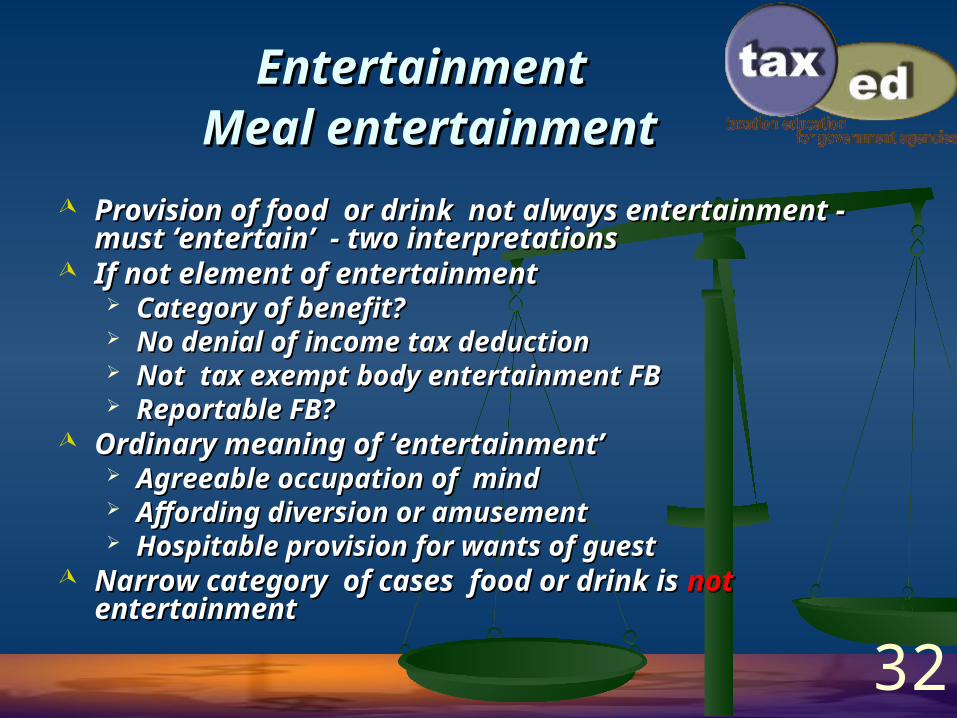

EntertainmentEntertainment Meal entertainmentMeal entertainment

Provision of food or drink not always Provision of food or drink not always entertainment - must ‘entertain’ - two entertainment - must ‘entertain’ - two interpretationsinterpretations

If not element of entertainmentIf not element of entertainment Category of benefit?Category of benefit? No denial of income tax deductionNo denial of income tax deduction Not tax exempt body entertainment FBNot tax exempt body entertainment FB Reportable FB?Reportable FB?

Ordinary meaning of ‘entertainment’Ordinary meaning of ‘entertainment’ Agreeable occupation of mindAgreeable occupation of mind Affording diversion or amusementAffording diversion or amusement Hospitable provision for wants of guestHospitable provision for wants of guest

Narrow category of cases food or drink is Narrow category of cases food or drink is not not entertainmententertainment

33

EntertainmentEntertainment Meal entertainmentMeal entertainment

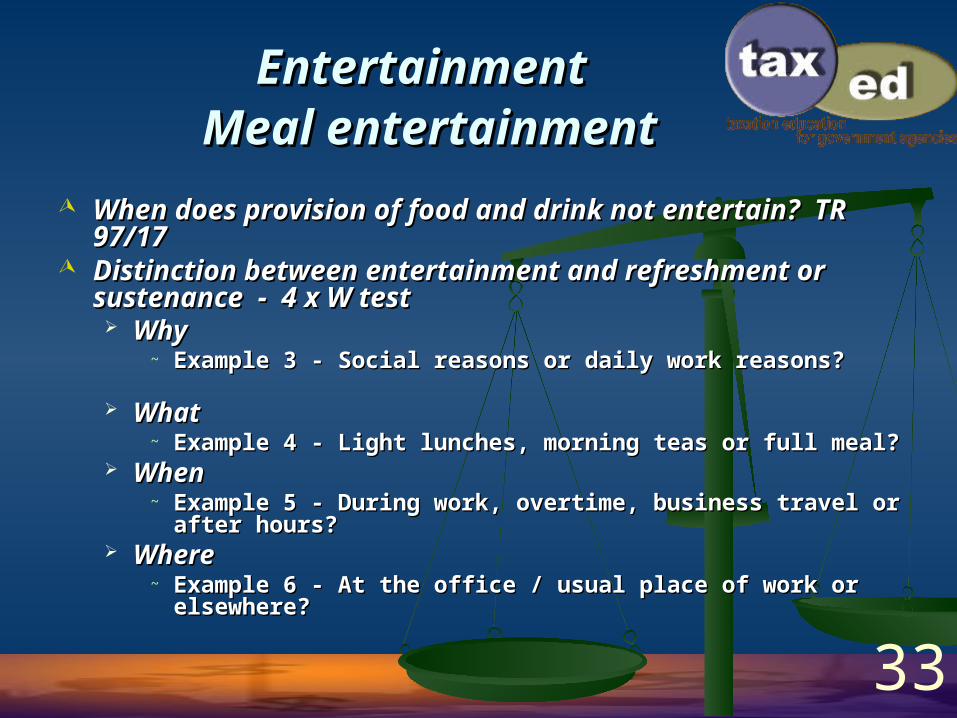

When does provision of food and drink not When does provision of food and drink not entertain? TR 97/17entertain? TR 97/17

Distinction between entertainment and Distinction between entertainment and refreshment or sustenance - 4 x W testrefreshment or sustenance - 4 x W test Why Why

~ Example 3 - Social reasons or daily work reasons?Example 3 - Social reasons or daily work reasons?

What What ~ Example 4 - Light lunches, morning teas or full meal?Example 4 - Light lunches, morning teas or full meal?

When When ~ Example 5 - During work, overtime, business travel Example 5 - During work, overtime, business travel

or after hours?or after hours? Where Where

~ Example 6 - At the office / usual place of work or Example 6 - At the office / usual place of work or elsewhere?elsewhere?

34

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

TEBEFB TEBEFB Provider incurs non deductible exempt Provider incurs non deductible exempt

entertainment expenditureentertainment expenditure Non-deductible entertainment expenditure Non-deductible entertainment expenditure

not incurred for assessable incomenot incurred for assessable income As result of Div 32 of ITAAAs result of Div 32 of ITAA

TEBEFB or other benefitTEBEFB or other benefit

35

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Implications of TEBFBE Implications of TEBFBE No exempt property benefits (s 41)No exempt property benefits (s 41) Limitation on minor exempt benefit (s 58P)Limitation on minor exempt benefit (s 58P) Taxable value – extent of expenditureTaxable value – extent of expenditure No reduction in value under otherwise No reduction in value under otherwise

deductible rule – (property FB, expense deductible rule – (property FB, expense payment FB, residual FB, loan FB, airline payment FB, residual FB, loan FB, airline transport FB)transport FB)

Still have choice of 50/50 or 12 week Still have choice of 50/50 or 12 week register for any meal entertainmentregister for any meal entertainment

36

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Income tax deductibilityIncome tax deductibility s 8 ITAA general deductions 8 ITAA general deduction s 32 - 5 ITAA no deduction for entertainments 32 - 5 ITAA no deduction for entertainment Exceptions to s32 - 5 other than s 32 -20Exceptions to s32 - 5 other than s 32 -20

Relevant income tax exceptions Relevant income tax exceptions Food & drink to employees @ in-house dining Food & drink to employees @ in-house dining

facilityfacility ( no party, reception or like) ( no party, reception or like)~ In-house dining facilityIn-house dining facility

On employer propertyOn employer property Mainly for food & drink to employeesMainly for food & drink to employees Not open to publicNot open to public

37

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Relevant income tax exceptions ctd.Relevant income tax exceptions ctd. Food or drink to non-employees @ in-house Food or drink to non-employees @ in-house

dining facility ( no party, reception or like)dining facility ( no party, reception or like) Food or drink to employees working in Food or drink to employees working in

dining facility (no party etc.)dining facility (no party etc.)~ Dining facilityDining facility

Canteen, dining room or likeCanteen, dining room or like Café, restaurant or likeCafé, restaurant or like On employer propertyOn employer property

38

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Relevant income tax exceptions ctd.Relevant income tax exceptions ctd. Food or drink to employee under industrial Food or drink to employee under industrial

instrument iro overtimeinstrument iro overtime~ Industrial instrumentIndustrial instrument

Award or industrial agreement under Australian Award or industrial agreement under Australian lawlaw

Recreation facility mainly for employeeRecreation facility mainly for employee~ Not for accommodationNot for accommodation~ Not for dining or drinking unlessNot for dining or drinking unless

Vending machineVending machine

Assessable allowance to employeeAssessable allowance to employee

39

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Relevant income tax exceptions ctd.Relevant income tax exceptions ctd. Food, drink, accommodation reasonably Food, drink, accommodation reasonably

incidental to 4 hour or longer seminar, unlessincidental to 4 hour or longer seminar, unless~ Business meeting, other thanBusiness meeting, other than

TrainingTraining General policy and management issuesGeneral policy and management issues

~ Main purpose to promote the businessMain purpose to promote the business~ Main purpose to provide entertainmentMain purpose to provide entertainment

4 hour seminar4 hour seminar~ Conference, convention, lecture, speechConference, convention, lecture, speech~ Q & A, training, educationQ & A, training, education~ Ignore lunch and refreshment time, even if seminar Ignore lunch and refreshment time, even if seminar

continues through lunchcontinues through lunch

40

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Relevant income tax exceptions ctd.Relevant income tax exceptions ctd. Entertainment businessEntertainment business Entertainment part of advertising business Entertainment part of advertising business

to general publicto general public Food or drink for overtime under industrial Food or drink for overtime under industrial

instrumentinstrument Free entertainment to public who are sick, Free entertainment to public who are sick,

disabled, poor or otherwise disadvantageddisabled, poor or otherwise disadvantaged

41

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Exempt property benefitExempt property benefit To current employee iro employmentTo current employee iro employment Consumed on working dayConsumed on working day At business premises of employerAt business premises of employer

Would include provision of any food and Would include provision of any food and drinkdrink other than for TEBEFB (eg food to other than for TEBEFB (eg food to

employee at in-house dining facility which employee at in-house dining facility which is tax deductible)is tax deductible)

42

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Exempt minor benefit (not TEBEFB)Exempt minor benefit (not TEBEFB) Less than $100 taxable value before gross-upLess than $100 taxable value before gross-up Unreasonable to treat as fringe benefitUnreasonable to treat as fringe benefit

~ Infrequency and irregularityInfrequency and irregularity~ Taxable value of other minor benefitsTaxable value of other minor benefits~ Difficulty in determining taxable valueDifficulty in determining taxable value

Stationary for private use, Christmas gifts Stationary for private use, Christmas gifts (MT 2042) , could include food and drinks to (MT 2042) , could include food and drinks to non employees or entertainment other than non employees or entertainment other than food (ie not covered by property exemption)food (ie not covered by property exemption)

43

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Exempt minor benefit (TABEFB)Exempt minor benefit (TABEFB) Provision of entertainment to employee or Provision of entertainment to employee or

assass~ Incidental to provision of ent. to outsiders; andIncidental to provision of ent. to outsiders; and

Not a meal to employee or assNot a meal to employee or ass~ To recognise special achievement of employeeTo recognise special achievement of employee

Otherwise deductible rule does not Otherwise deductible rule does not applyapply Why?Why?

44

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Example Example Food and drinks to employees, spouses Food and drinks to employees, spouses

and others at social function and others at social function Example Example

Hot lunch to employees at canteen on Hot lunch to employees at canteen on premisespremises

Same to spousesSame to spouses

45

EntertainmentEntertainment Tax exempt body entertainment Tax exempt body entertainment

FB (TEBEFB)FB (TEBEFB)

Example Example Employee reimbursed for meal and wine on Employee reimbursed for meal and wine on

business tripbusiness trip Also reimbursed for meal of spouseAlso reimbursed for meal of spouse

Example Example Employee sent to day seminar at which hot Employee sent to day seminar at which hot

food and wine is providedfood and wine is provided The seminar is only 2 hours longThe seminar is only 2 hours long 2 hour seminar and only snacks provided2 hour seminar and only snacks provided

46

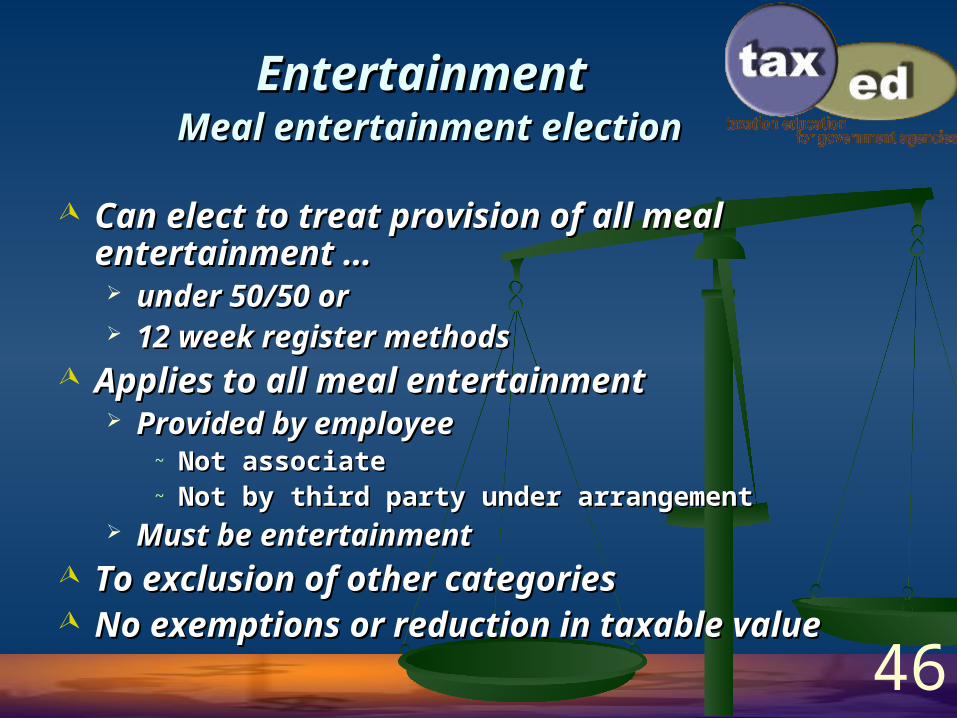

EntertainmentEntertainment Meal entertainment electionMeal entertainment election

Can elect to treat provision of all meal Can elect to treat provision of all meal entertainment …entertainment … under 50/50 or under 50/50 or 12 week register methods12 week register methods

Applies to all meal entertainmentApplies to all meal entertainment Provided by employeeProvided by employee

~ Not associateNot associate~ Not by third party under arrangementNot by third party under arrangement

Must be entertainmentMust be entertainment To exclusion of other categoriesTo exclusion of other categories No exemptions or reduction in taxable No exemptions or reduction in taxable

valuevalue

47

EntertainmentEntertainment 50/5050/50

Taxable value = 50% of all meal Taxable value = 50% of all meal entertainment expenseentertainment expense Provided to employeesProvided to employees AssociatesAssociates OthersOthers

Example 11Example 11 Planning hintPlanning hint

Does more than 50% of meal ent relate to Does more than 50% of meal ent relate to staff?staff?

Does more than 50% of meal ent relate to Does more than 50% of meal ent relate to others?others?

48

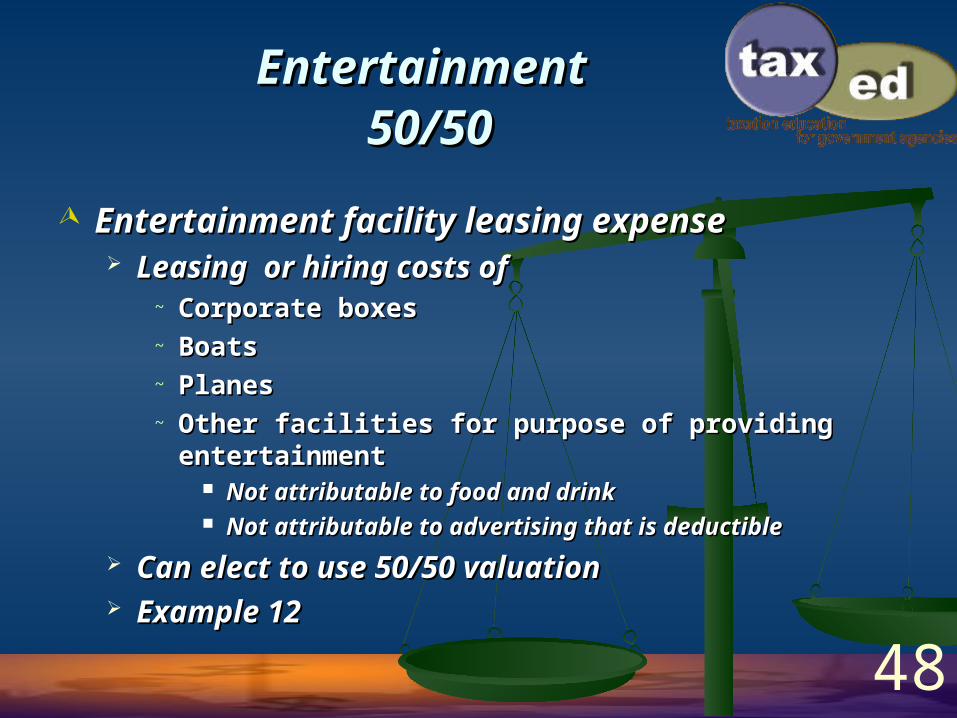

EntertainmentEntertainment 50/5050/50

Entertainment facility leasing expenseEntertainment facility leasing expense Leasing or hiring costs ofLeasing or hiring costs of

~ Corporate boxesCorporate boxes~ BoatsBoats~ PlanesPlanes~ Other facilities for purpose of providing Other facilities for purpose of providing

entertainmententertainment Not attributable to food and drinkNot attributable to food and drink Not attributable to advertising that is deductibleNot attributable to advertising that is deductible

Can elect to use 50/50 valuationCan elect to use 50/50 valuation Example 12Example 12

49

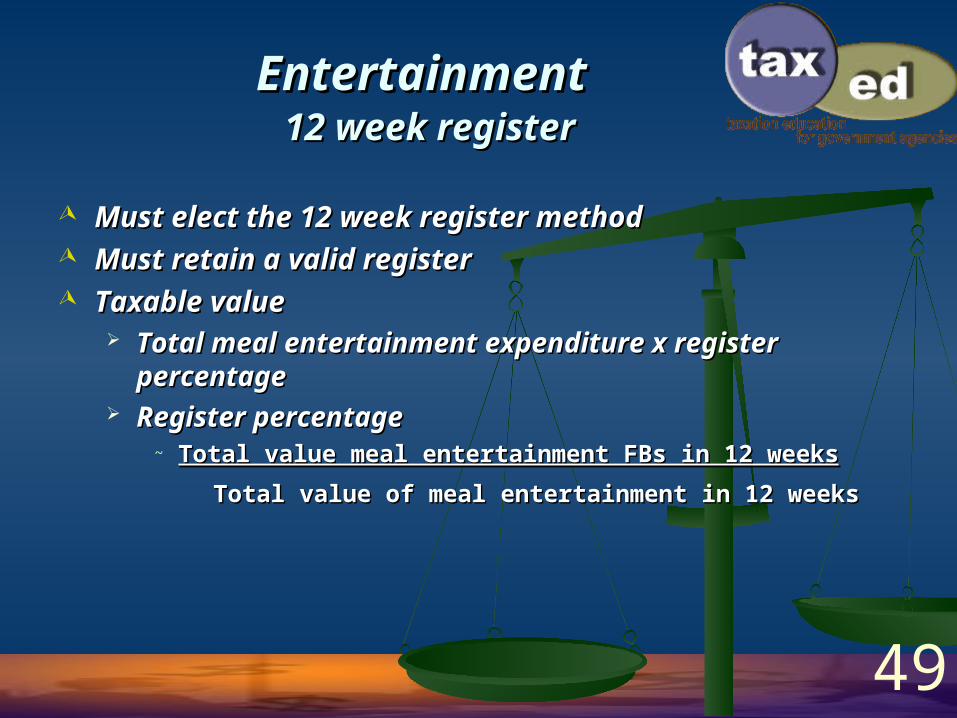

EntertainmentEntertainment 12 week register12 week register

Must elect the 12 week register methodMust elect the 12 week register method Must retain a valid registerMust retain a valid register Taxable valueTaxable value

Total meal entertainment expenditure x Total meal entertainment expenditure x register percentageregister percentage

Register percentageRegister percentage~ Total value meal entertainment FBs in 12 weeksTotal value meal entertainment FBs in 12 weeks

Total value of meal entertainment in 12 weeksTotal value of meal entertainment in 12 weeks

50

EntertainmentEntertainment 12 week register12 week register

Requirements of a valid registerRequirements of a valid register Kept for 12 weeksKept for 12 weeks Valid for year 12 weeks end plus another 4Valid for year 12 weeks end plus another 4 Register starts 1 year ends next, valid for Register starts 1 year ends next, valid for

next plus 4next plus 4 If meal entertainment expense in year > If meal entertainment expense in year >

20% of first year, valid only for that year20% of first year, valid only for that year Two registers in 1 year, first invalidTwo registers in 1 year, first invalid 12 week period must be representative of 12 week period must be representative of

first FBT yearfirst FBT year

51

EntertainmentEntertainment 12 week register12 week register

Information required in registerInformation required in register Date meal providedDate meal provided If recipient is employee or associateIf recipient is employee or associate Cost of meal entertainmentCost of meal entertainment Kind of meal providedKind of meal provided Where meal providedWhere meal provided If provided on employer’s premises, If provided on employer’s premises,

whether at in-house dining facilitywhether at in-house dining facility

52

EntertainmentEntertainment GST creditsGST credits

To extent for a creditable purposeTo extent for a creditable purpose No creditable acquisition if no income tax No creditable acquisition if no income tax

deduction for entertainment expenditurededuction for entertainment expenditure Credit to extent entertainment deductibleCredit to extent entertainment deductible

Actual methodActual method 50/5050/50 12 week register12 week register

TEBEFB = not deductible for income tax TEBEFB = not deductible for income tax other than 32-20, but may still be other than 32-20, but may still be creditable as result of 32-20creditable as result of 32-20

53

EntertainmentEntertainment

Comparison of valuationsComparison of valuations~ ActualActual~ 50/5050/50~ 12 week register12 week register

54

Other CategoriesOther CategoriesIntroductionIntroduction

PropertyProperty Expense paymentExpense payment ResidualResidual Debt waiverDebt waiver Loan Loan Car parkingCar parking BoardBoard Remote housingRemote housing Living away from home allowanceLiving away from home allowance

55

Other CategoriesOther CategoriesPropertyProperty

Property provided for free or at discount Property provided for free or at discount Paid for my employerPaid for my employer PropertyProperty

Tangible – goods including gas, electricity, Tangible – goods including gas, electricity, animals and fishanimals and fish

Intangible – includes real property, chose in Intangible – includes real property, chose in action, but not contract of insurance or action, but not contract of insurance or licence or lease over real property or licence or lease over real property or tangibletangible

TV depends on TV depends on In-house property FBIn-house property FB External property FBExternal property FB

56

Other CategoriesOther CategoriesPropertyProperty

Property provided for free or at discount Property provided for free or at discount Paid for my employerPaid for my employer PropertyProperty

Tangible – goods including gas, electricity, Tangible – goods including gas, electricity, animals and fishanimals and fish

Intangible – includes real property, chose in Intangible – includes real property, chose in action, but notaction, but not

~ contract of insurance contract of insurance ~ licence or lease over real property or tangiblelicence or lease over real property or tangible

TV depends on TV depends on In-house property FBIn-house property FB External property FBExternal property FB

57

Other CategoriesOther CategoriesPropertyProperty

In-house property FB In-house property FB Only tangible propertyOnly tangible property Provided by employer or assProvided by employer or ass

~ Identical or similar to that ordinarily sold Identical or similar to that ordinarily sold Provided by 3Provided by 3rdrd party party

~ Acquired from employer or associateAcquired from employer or associate~ Identical or similar to that ordinarily sold y Identical or similar to that ordinarily sold y

employer and 3employer and 3rdrd party provider party provider

External property FBExternal property FB Any property FB that is not an in-house Any property FB that is not an in-house

prop FBprop FB

58

Other CategoriesOther CategoriesPropertyProperty

Taxable Value - In-house property FB Taxable Value - In-house property FB Goods manufactured for retail saleGoods manufactured for retail sale

~ 75% lowest price to public75% lowest price to public Goods manufactured for wholesale saleGoods manufactured for wholesale sale

~ Lowest arm’s length selling priceLowest arm’s length selling price Goods manufactured, similar but not identical Goods manufactured, similar but not identical

to those sold ( for example seconds)to those sold ( for example seconds)~ 75% market value75% market value

Goods purchased for sale in businessGoods purchased for sale in business~ Arm’s length purchase priceArm’s length purchase price

All otherAll other~ 75% of market value75% of market value

59

Other CategoriesOther CategoriesPropertyProperty

Taxable Value – external property FB Taxable Value – external property FB Provider is employer or ass and prop Provider is employer or ass and prop

purchased at arm’s lengthpurchased at arm’s length~ Cost priceCost price

Provider not employer or associate but Provider not employer or associate but incurred the expense under arm’s length incurred the expense under arm’s length transactiontransaction

~ Amount of expenditureAmount of expenditure All otherAll other

~ Amount employee could reasonably be Amount employee could reasonably be expected to payexpected to pay

60

Other CategoriesOther CategoriesPropertyProperty

Reduction in Taxable ValueReduction in Taxable Value Amount of the employee’s contributionAmount of the employee’s contribution Amount that would be otherwise deductibleAmount that would be otherwise deductible

~ Had the employee purchasedHad the employee purchased~ Only for one off deductions, not depreciable Only for one off deductions, not depreciable ~ Can agree that contribution relates to non-deductible Can agree that contribution relates to non-deductible

portion so as to reduce TV to nilportion so as to reduce TV to nil~ Require employee declaration as to what is otherwise Require employee declaration as to what is otherwise

deductibledeductible~ Does not apply to associatesDoes not apply to associates

In-house FB reduced by $500In-house FB reduced by $500 Exempt property benefitsExempt property benefits

Provided to employee for consumption at work on Provided to employee for consumption at work on a working daya working day

Minor benefitMinor benefit

61

Other CategoriesOther CategoriesExpense paymentExpense payment

Discharge recipients obligation to 3Discharge recipients obligation to 3rdrd partyparty

Reimburse recipients expenditureReimburse recipients expenditure In-house expense payment FBIn-house expense payment FB

Relates to good or services employer or Relates to good or services employer or associate sells to publicassociate sells to public

External expense payment FBExternal expense payment FB Everything other than in-houseEverything other than in-house

62

Other CategoriesOther CategoriesExpense paymentExpense payment

Taxable valueTaxable value In-houseIn-house

~ As per in-house property FBAs per in-house property FB ExternalExternal

~ Amount of expenditureAmount of expenditure ExemptionsExemptions

““no-private use” declaration, only work no-private use” declaration, only work expensesexpenses

In respect of accommodationIn respect of accommodation~ Recipient living away from homeRecipient living away from home~ Not travelling for workNot travelling for work~ Recipient declarationRecipient declaration

63

Other CategoriesOther CategoriesExpense paymentExpense payment

Exemptions continuedExemptions continued ‘‘cents per kilometre’ motor vehiclecents per kilometre’ motor vehicle

~ Not for holidayNot for holiday~ Not for relocation, employment interview, work Not for relocation, employment interview, work

medical etcmedical etc~ Not to former employeeNot to former employee

Minor benefitMinor benefit Reduction in taxable valueReduction in taxable value

Recipient contributionRecipient contribution To expense were otherwise deductibleTo expense were otherwise deductible

~ Only if recipient is employeeOnly if recipient is employee~ Once only deductionOnce only deduction~ An employee declaration requiredAn employee declaration required

$500 for in-house$500 for in-house

64

Other CategoriesOther CategoriesResidualResidual

Catch-all, not falling in other benefit Catch-all, not falling in other benefit categoriescategories

Usually servicesUsually services In-houseIn-house

Provider is employer or associateProvider is employer or associate Similar to that provided to publicSimilar to that provided to public

ExternalExternal Anything not in-houseAnything not in-house

65

Other CategoriesOther CategoriesResidualResidual

Taxable valueTaxable value In-houseIn-house

~ Identical benefitsIdentical benefits 75% of lowest arm’s length price to public75% of lowest arm’s length price to public

~ No identical to publicNo identical to public 75% of lowest price employee expected to pay in 75% of lowest price employee expected to pay in

arm’s length transactionarm’s length transaction ExternalExternal

~ Purchased by providerPurchased by provider Cost priceCost price

~ Any other caseAny other case Amount employee reasonably expected to pay in Amount employee reasonably expected to pay in

arm’s length transactionarm’s length transaction

66

Other CategoriesOther CategoriesResidualResidual

Taxable value continuedTaxable value continued Motor vehicle other than carMotor vehicle other than car

~ Calculated under operating cost orCalculated under operating cost or~ Cents/kilometreCents/kilometre

Reduction in taxable valueReduction in taxable value Recipient contributionRecipient contribution Otherwise deductibleOtherwise deductible

~ Only employeeOnly employee~ One-off deductionOne-off deduction~ Employee declarationEmployee declaration

$500 for in-house$500 for in-house

67

Other CategoriesOther CategoriesDebt waiverDebt waiver

Employer forgives or waives an employeesEmployer forgives or waives an employees~ Not if written of as genuine bad debtNot if written of as genuine bad debt

Taxable valueTaxable value~ Amount of debt waivedAmount of debt waived

Include interest accrued Include interest accrued

No reduction in taxable value availableNo reduction in taxable value available

68

Other CategoriesOther CategoriesLoanLoan

Employer makes loan to employeeEmployer makes loan to employee~ Provided in respect of each year that an Provided in respect of each year that an

obligation to repay existsobligation to repay exists~ Benefit also arises if amount owed and Benefit also arises if amount owed and

payment not enforcedpayment not enforced~ Repayments not require before 6 monthsRepayments not require before 6 months

Accrued interest = separate loanAccrued interest = separate loan

Taxable valueTaxable value~ Difference between actual interest and Difference between actual interest and

‘notional amount of interest’ accrued at ‘notional amount of interest’ accrued at statutory ratestatutory rate

Current statutory rate = 6.55%Current statutory rate = 6.55%

69

Other CategoriesOther CategoriesLoanLoan

Exempt loanExempt loan~ On same terms and conditions as ordinary On same terms and conditions as ordinary

customercustomer~ Advance for sole purpose of expenses in course Advance for sole purpose of expenses in course

of employment dutiesof employment duties Not exceed reasonable expenseNot exceed reasonable expense Employee to vouch for expenseEmployee to vouch for expense Expense incurred within 6 months of advanceExpense incurred within 6 months of advance

~ Advance to employee for rental bond or utilitiesAdvance to employee for rental bond or utilities Repaid in 12 monthsRepaid in 12 months Employee in receipt of one of following:Employee in receipt of one of following:

Expense payment iro accommodationExpense payment iro accommodation Housing benefitHousing benefit Residual benefit iro accommodationResidual benefit iro accommodation

70

Other CategoriesOther CategoriesLoanLoan

Reduction in taxable valueReduction in taxable value~ Otherwise deductible ruleOtherwise deductible rule

Recipient an employeeRecipient an employee Once-only deductionOnce-only deduction Interest rate less than statutory rateInterest rate less than statutory rate Employee declaration necessaryEmployee declaration necessary

71

Other CategoriesOther CategoriesCar parkingCar parking

Provided by employer for use of employee or Provided by employer for use of employee or ass.ass.

~ Car parked at premises owned, leased or controlled Car parked at premises owned, leased or controlled by providerby provider

~ Within 1 km radius = commercial parking stationWithin 1 km radius = commercial parking station Charging fee for all day parkingCharging fee for all day parking In excess of car parking threshold (currently $5.96)In excess of car parking threshold (currently $5.96)

~ Parked > 4 hrs between 7.00am and 7.00pmParked > 4 hrs between 7.00am and 7.00pm~ Car provided by employer or leased, owned or Car provided by employer or leased, owned or

controlled by employeecontrolled by employee~ Provided iro employmentProvided iro employment~ Parked at or near primary place of employmentParked at or near primary place of employment~ Travel between work and home once a dayTravel between work and home once a day

72

Other CategoriesOther CategoriesCar parkingCar parking

Taxable value – 3 methodsTaxable value – 3 methods~ Commercial parking station methodCommercial parking station method~ Market value methodMarket value method~ Average cost methodAverage cost method

Commercial parking station methodCommercial parking station method~ Lowest fee chargedLowest fee charged~ By commercial parking stationBy commercial parking station~ Within 1 km radiusWithin 1 km radius~ Reduced by employees payment towards costReduced by employees payment towards cost

73

Other CategoriesOther CategoriesCar parkingCar parking

Commercial parking station method ctd.Commercial parking station method ctd.~ Employer to keep records of actual number of Employer to keep records of actual number of

benefits providedbenefits provided Number spaces availableNumber spaces available Number business days in yearNumber business days in year Method of valuation chosenMethod of valuation chosen Daily value of spacesDaily value of spaces Number of employees parked on premises each Number of employees parked on premises each

dayday

Market value methodMarket value method~ Valuation of space by valuerValuation of space by valuer~ Reduced by employee paymentReduced by employee payment~ Same record requirements as aboveSame record requirements as above

74

Other CategoriesOther CategoriesCar parkingCar parking

Average cost methodAverage cost method~ Average of lowest fee for first and last day of Average of lowest fee for first and last day of

FBT yearFBT year~ Reduced by recipient paymentReduced by recipient payment~ Same record keeping requirements as aboveSame record keeping requirements as above

Number of benefits provided – 3 methodsNumber of benefits provided – 3 methods~ ActualActual~ 12 week register12 week register~ Statutory formulaStatutory formula

75

Other CategoriesOther CategoriesCar parkingCar parking

12 week register12 week register~ Parking FBs valued for 12 weeksParking FBs valued for 12 weeks~ Yearly value calculatedYearly value calculated

$A x 52/12 x B/365$A x 52/12 x B/365 A = total TV over 12 weeks (any of 3 A = total TV over 12 weeks (any of 3

methods)methods) B = number of days in period from first day B = number of days in period from first day

provided to employee covered by election and provided to employee covered by election and ends on last day FBT year benefit proved to ends on last day FBT year benefit proved to same employeesame employee

76

Other CategoriesOther CategoriesCar parkingCar parking

Statutory formulaStatutory formula~ Assumes 228 FBs arise from each space in FBT Assumes 228 FBs arise from each space in FBT

yearyear~ Reduced proportionately if number employees Reduced proportionately if number employees

is less than number of car parksis less than number of car parks~ ValueValue

$A x B/365 x 228$A x B/365 x 228 A and B = same as aboveA and B = same as above

~ Must make electionMust make election Specify if covers all employees orSpecify if covers all employees or Class of employees orClass of employees or Specific employeesSpecific employees

77

Other CategoriesOther CategoriesCar parkingCar parking

Exempt benefitsExempt benefits~ Not meet requirements for car parking FBNot meet requirements for car parking FB~ Expense payments that are not car parking Expense payments that are not car parking

expense payment FBsexpense payment FBs~ Disabled employeesDisabled employees~ Parking provided by various exempt employersParking provided by various exempt employers~ Small businessSmall business

78

Other CategoriesOther CategoriesCar parking expense paymentCar parking expense payment

Reimbursement of parking expensesReimbursement of parking expenses~ Parking > 7 hoursParking > 7 hours~ Between 7.00am and 7.pmBetween 7.00am and 7.pm~ No requirement regardingNo requirement regarding

Availability of car parkingAvailability of car parking Lowest fee chargedLowest fee charged

79

Other CategoriesOther CategoriesBoardBoard

Provision of meal to employee or ass. where Provision of meal to employee or ass. where also entitled to provision of accommodation also entitled to provision of accommodation and:and:

~ entitlement to 2 meals a dayentitlement to 2 meals a day Under industrial award orUnder industrial award or Under employment arrangement ordinarily providedUnder employment arrangement ordinarily provided

~ Supplied by employerSupplied by employer~ Cooked or prepared on employers premises or Cooked or prepared on employers premises or

worksite or place adjacentworksite or place adjacent~ Meal supplied on employees premisesMeal supplied on employees premises~ ExampleExample

meals in dining facility on remote construction site, meals in dining facility on remote construction site, oil rig or shipoil rig or ship

80

Other CategoriesOther CategoriesBoardBoard

Taxable valueTaxable value~ $2 per meal per person$2 per meal per person~ $1 per meal if person under 12$1 per meal if person under 12

ReductionReduction~ Reduced by any recipient paymentReduced by any recipient payment~ To extent otherwise deductibleTo extent otherwise deductible

81

Other CategoriesOther CategoriesRemote housingRemote housing

HousingHousing~ Employee provided with accommodationEmployee provided with accommodation

House, flat, hotel, motel, caravan, ship, etcHouse, flat, hotel, motel, caravan, ship, etc~ Usual place of residence of employeeUsual place of residence of employee

Taxable valueTaxable value~ Market valueMarket value~ Reduced by recipient rentReduced by recipient rent~ Employee of hotel etc.Employee of hotel etc.

75% market rental75% market rental Reduced by recipient rentReduced by recipient rent

82

Other CategoriesOther CategoriesRemote housingRemote housing

ExemptExempt~ Remote housing benefitRemote housing benefit~ RemoteRemote

40km from town with population 14,000 -130,00040km from town with population 14,000 -130,000 100km from town with population > 130,000100km from town with population > 130,000

Reduction in TV of related benefitsReduction in TV of related benefits~ 50% reduction in TV of residential fuel to recipient 50% reduction in TV of residential fuel to recipient

of:of: Exempt remote area housing benefitExempt remote area housing benefit Remote area housing loan FBRemote area housing loan FB Remote area housing rent FBRemote area housing rent FB

~ Remote housing loanRemote housing loan Loan FB iro housing loan provided iro usual place of Loan FB iro housing loan provided iro usual place of

resres Instead of remote housing would be exempt benefitInstead of remote housing would be exempt benefit

83

Other CategoriesOther CategoriesRemote housingRemote housing

Reduction in TV of related benefits, ctd.Reduction in TV of related benefits, ctd.~ Remote area housing rent Remote area housing rent

Expense payment arises from rent iro usual residenceExpense payment arises from rent iro usual residence Instead of remote housing would be exempt benefitInstead of remote housing would be exempt benefit

~ 50% reduction in TV remote area housing assistance50% reduction in TV remote area housing assistance If provided as housing benefit would be exemptIf provided as housing benefit would be exempt Housing assistance that is not housing benefitHousing assistance that is not housing benefit

Reimbursement /payment of rentReimbursement /payment of rent Making housing loanMaking housing loan Reimbursement/payment interest on housing loanReimbursement/payment interest on housing loan Provision of land or house and landProvision of land or house and land Reimburse/payment cost of acquiring land/houseReimburse/payment cost of acquiring land/house Payment to employee iro granting to employer Payment to employee iro granting to employer

purchase option or payment iro purchase optionpurchase option or payment iro purchase option

84

Other CategoriesOther CategoriesLiving away from home Living away from home

allowanceallowance

Allowance paid to employee by employer Allowance paid to employee by employer for for

~ Additional expenses incurredAdditional expenses incurred~ Disadvantages sufferedDisadvantages suffered~ Because required to live away from homeBecause required to live away from home~ To perform employment dutiesTo perform employment duties

Distinction between travel and living away Distinction between travel and living away from homefrom home

Separately identified allowance in additionSeparately identified allowance in addition

85

Other CategoriesOther CategoriesLiving away from home Living away from home

allowanceallowance

Taxable value Taxable value ~ Allowance reduced byAllowance reduced by

Reasonable cost of accommodationReasonable cost of accommodation Reasonable compensation for increased food Reasonable compensation for increased food

expense, equal to difference betweenexpense, equal to difference between Sum of $42 per adult in household and $21 Sum of $42 per adult in household and $21

for every child under 12; andfor every child under 12; and Lesser of food component of allowance or Lesser of food component of allowance or

maximum reasonable amount notified by maximum reasonable amount notified by commissioner commissioner

86

The EndThe End