welcome personal payments training 2008. agenda personal payments new personal payment process...

TRANSCRIPT

Welcome

Personal Payments Training

2008

Agenda Personal Payments New Personal

Payment Process Signature

Delegation Form PC Form RCS Glacier Software Non-Resident Alien

Payments

Living Allowances Scholarships &

Fellowships Prizes & Awards Receipt Guidelines Independent

Contractor vs. Employee

Contacts & Reference Materials

Personal Payments Consulting, Honoraria, Fees, etc. Form PC Required

SSN Home Address Period Covered Brief Explanation of Services Fees and expense reimbursements must be on separate

lines on the Invoice Voucher for IRS reporting Form 52A – request for electronic funds transfer

Preferable payment method for payment going outside the US

Route Form 52A & all backup through Cheryl Byers, Taxes

Name & SSN must be on Form 52A

Personal Payments Additional Instructions for Non-Residents Glacier Software has replaced the 2nd page

of the Form 1&2 Attach copies of supporting documentation

Passport Visa Page I-94 Card I-20(F1) DS-2019(J1) I797(H1B)

8233 Form (if applicable) W-7 Form (if applicable)

Personal Payments Lives and Works Outside the US

If a Non-Resident Alien lives and works outside of the US, Purdue has no tax withholding or reporting responsibilities.

Notate in the description box on the Invoice Voucher that the individual lives and works outside of the US.

Retain documentation in the business office that supports the work was done outside of the US.

Personal Payments One-Stop Shop for Personal

Service Payments Reduce processing time Prevent duplication of effort Document review will occur one

time All questions answered in one

department

Personal Payments-Flowchart

Signature Delegation Authority to sign for the procurement

of goods and services – except for payments to individuals

Comptroller/SPS Review Allowability

Conformity to restrictions imposed by state regulations

Meet restrictions imposed by donor, external provider and the University

Meet restrictions imposed by the federal government, OMB Circulars A-21, A-110

Meet restrictions placed on specific grants or contracts

Signature Delegation

Comptroller/SPS Review (cont.) Allocable

Authority to commit funds Benefit the funding sources Funds are available

Reasonable & Necessary Quantity and Price are considered

appropriate by a prudent person Necessary to conduct the work of the

office or department

Signature Delegation

Departmental Review Account number is valid Funds are available Correct object code & DREF (if

applicable) Visa issues for personal travel payments

checked Appropriate documentation is attached Academic approvals Comptroller review – allocable,

allowable, reasonable, signature Route to Tax Department

Signature Delegation Payments to Individuals

Honorariums, Consulting Fees, Reimbursements, etc

Reviewed by Business Office for allowability, allocability & reasonableness

Sign under ‘Recommended’ (based on limit)

If a Form PC is needed, review with scrutiny, any questions contact the Tax Department

Forward to the Tax Department

Form PC-Payee Certification

Start using 07/05 version immediately Replaces Form 1&2 Available on the Taxes Website Non-Residents, who are receiving

compensation and are not current employees, need to complete Glacier

The tax department will use this information to accurately withhold and report taxes

Form 21 (Revised 06/05)

A. Payee Information For Calendar Year

1. Name: 2. Home Address:(Please enter name as shown on your Social Security Card)

3. Social Security Number:

4. Email Address: (Please Include 4-Digit Zip Code Extension)

5. Are you a student? No Yes If yes, Name of Institution

6. Are you an employee or former employee of Purdue University? No * Yes**

*If no, name of Employer **If yes, dates of employment at Purdue

7. Do you have immediate relatives employed at Purdue? No YesIf yes, please list name(s) and department(s).

8. Citizenship and Residency - Used to determine appropriate tax withholding and reportingH1B, F2, TN, and O1 visa holders are not eligible for compensation for independent personal services.Residency Status: US Citizen Permanent Resident

Non-Resident Alien Visa Type:

Non-Resident Aliens, please complete your Glacier file

B. Payment Information

Description of Services/Reason for Payment:

Was the work performed outside the United States? No Yes Is this a progress payment? No Yes*

Period Covered by Payment: *If yes, is this a final payment? No Yes

Itemized Payment:Honorarium/Fees for Service $ X = $Expenses Airfare = $

Ground Transportation $ X = $Subsistence: Food $ X = $

Lodging $ X = $Other $ X = $

-

C. Payee Certification

Signature of Payee: Date:

Signature: Date:

Title/Position:

Foreign Curr.Type

(To by signed by Payee EACH TIME a payment is requested)

Payee CertificationUse when making participant payments, paying non-Purdue student or non-staff awards,reimbursement of fees/expenses to speakers, honoraria,

artists/entertainers, or consultants. Attach to Invoice Voucher, Form 56. Go to www.purdue.edu/ taxes for more information.

(To be completed by Payee)

(To be completed by department business office)

Permanent Resident (Green) Card #

No. of hours,days,etc.

STOP! If this arrangement is long-term consulting (more than 20 calendar days or multiple payments), DO NOT COMPLETE Sections B., C., and D. at this time. Complete Form 22, Request for Approval for Consulting Services, obtain approvals & forward to the Tax Department, FREH, with a copy of this Form 21.

To authorize payment for services rendered, complete Sections B, C, and D, and forward with Invoice Voucher (Form 56) and appropriate documentation to the Tax Department, FREH.

Under penalities of perjury, I certify that: e) The number shown on this form is my correct taxpayer identification number, f) I am not subject to backup withholding, and

g) the information regarding citizenship in A.8. above is correct.

(Project) (Dref)

Fee/ rate per hour,day,etc.

Account Number(Fund) (Dept)

Total

$Total Invoice

Amount

By signing below, I certify that the services described in Section B. are essential to the project, that internal resources are not available to perform the work, and the consultant's fees are appropriate. I also certify that the services have been received, including any report(s) due.

Note: The Internal Revenue Service does not require your consent to any provision of this document other than the certification required to avoid backup withholding.

By Signing this invoice I a) Certify that this invoice is correct and just, the amount claimed is legally due, after allowing for all just credits, no part of the same has been

paid, no part will be paid by another entity, nor will any expenses claimed here be used as a deduction for tax purposes; b) Certify that I am not a Federal employee; c)

Agree that all inventions and materials first developed or produced as a result of the above described consulting activities will be reported to Purdue and all rights, both

domestic and foreign, to inventions and materials first developed or produced as a result of the above described consulting activities shall be retained by Purdue

University, and d) Agree not to disclose any information furnished by Purdue University that was identified as proprietary information.

(Required for all payments except participant payments and award payments.)D. Verification of receipt of deliverables and/or services by individual with first-hand knowledge

Form RCS-Consulting Agreements

Consultant Payments Duration of Service is greater than

20 days Multiple payments paid to

consultant Complete and forward to the Tax

Department

Form RCS-Long Term Consulting Agreement

Form 22 (Revised 06/05)

Name:

(Please enter name as shown on Form 21)

B. Documentation Required for Long Term Consulting Arrangement

Statement of Work:

Describe Consultant's Credentials, including why he/she meets project needs:

Describe required deliverables, if any:

Identify Any Special Conditions Related to the Consulting Arrangement:

Term of Project : Expected Completion Date:

If project will be done in segments, please describe detailed schedule for each segment, including dates and deliverables:

Total Estimated Costs for ProjectFees for Service $ X = $

Expenses to be paid

Transportation Airfare $ X = $

Ground $ X = $

Subsistence Food $ X = $

Lodging $ X = $

Other Expenses $ X = $

-

If progress payments will be made, please describe detailed payment schedule:

Requested by:

Signature: Date:

Title/Position:

Approved by:

Date:

Head of Department/College (Required)Approved by:

Date:

Dean/Director (Follow guidelines for individual College/Area)

Request for Approval for Consulting ServicesDocumentation and Prior Approval(s) Required to Pay Long-Term Consultants

Must be accompanied by a Form 21 with only Section A completed

(Dref)(Dept) (Project)

Complete this section if consulting meets criteria for long-term consulting. Call the Tax Department for more information. Provide enough information to clearly define the work and terms of the agreement. Documentation may be attached to this form in place of filling in the form itself.

A. Payee Information (Required)

C. Request and Approval Signatures

Total FeesFee/ rate per hour,day,etc.

Account Number

No. of hours,days,etc.

(Fund)$

Total Estimated Cost

Form PC & RCS Business Office Guidelines can be

found on the Taxes website as part of the consultant payments tab

A Quick Reference Guide for Form PC & RCS is also available on the Taxes website as part of the consultant payments tab

http://www.purdue.edu/taxes/Consultant_Payments/Welcome.html

GLACIER Glacier is a web based

International tax compliance system.

Instead of handing out tax forms to international visitors, you will be issuing them passwords.

GLACIER Business office procedure to receive access

to issue passwords; e-mail the Tax Department the following information:

Name Title Campus address Campus phone and fax number E-mail address

You will receive an e-mail with your password and instructions on how to login. The e-mail will come from [email protected] and not Purdue.

GLACIER When you issue a password, an e-mail is

sent to the visitor asking them to enter their information into the Glacier system. The e-mail will come from [email protected] and not Purdue. Please advise them to look for this e-mail and others in the future.

Advise them to keep the password and instructions for future use of the Glacier system.

GLACIER

After the visitor enters their information, a Tax Summary Report, and any other required IRS forms will be available to print. Ex) 8233, W-8BEN, or W-7. The Tax Summary Report will replace the NRA-100.

If the visitor does not have a social security number or an ITIN, Glacier will put a hold on printing the forms for that visitor. The Tax Department can override the hold and print the forms when the employee is in our office. The business office needs to contact the Tax Department to override the hold which enable the visitor to print the forms.

The Tax Department will process the ITIN application upon receipt of the payment request.

GLACIER We will use Glacier to generate the

tax forms required for payments to individuals receiving personal service payments, scholarships, awards, royalty payments, or reimbursement of travel expenses via invoice vouchers. The Tax Summary Report printed from Glacier will replace the NRA-100.

GLACIER Fellowship recipients will also be using

this system. For the payments above, check the

Non-Employee box for Pay Period type when you are issuing a password.

If you have an incoming visitor having difficulties printing, offer to print the forms for them when they arrive in your office.

Non Resident Alien Visas Not all Visas are the same Try to choose the

appropriate visa for an individual before they come to the US

There are different restrictions for paying compensation and for reimbursing travel expenses

Refer to the visa payment reference sheets

Visa Types B-1 - Visitor

Business B-2 - Visitor

Tourist WB - Visa

Waiver Business WT - Visa Waiver

Tourist

F – Student J – Exchange Visitor H-1B – Specialty

Worker TN – NAFTA

Professional (Canada or Mexico)

EAD – Employment Authorization Card

Additional Non-Resident Alien Instructions There are IRS and USCIS regulations we must follow for Non-Resident Aliens. Purdue University uses a web-based tax compliance system, called Glacier, to assist us in complying with these regulations. Any time you receive some form of income from Purdue, such as a payment for services, an award, or a fellowship, you will need to create or update you record in Glacier. Current employees or if you have been paid by Purdue this year:

You should have an e-mail with your password and login instructions to the Glacier system. You can request a copy of your password and login instructions by sending an e-mail to [email protected].

You will need to update the Glacier system with your current information and add the type of payment you are receiving.

Print the Tax Summary and any other forms as directed. Sign the forms and send them with copies of the documents listed on the Tax

Summary to your contact in the business office. If you have not been paid by Purdue before:

The business office will send you an e-mail giving you login instructions and your password to create your record in the Glacier system.

Print the Tax Summary and any other forms as directed. Sign the forms and send them with copies of the documents listed on the Tax

Summary to your contact in the business office.

Honorarium / Fee Payments to Non-Resident Short-Term Visitors

- Please attach a copy of the individual's passport, I-94 card and when applicable visa, EAD card, I-20, DS-2019, or approval from sponsor

- Attach a copy of IRS Form 8233 if eligible for a treaty (exemption from taxes)- Attach a copy of IRS Form W-7 if the individual does not have a social security number or ITIN

Can we pay an Honorarium/Fee? Stipulations and Exceptions

B-1 Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

B-2 Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

WB Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

WT Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

F-1 No Human Subject payments to Purdue students are allowableAllowable with approval from sponsor for Curricular Practical Training on the I-20

F-2 No

J -1 Student No Human Subject payments to Purdue students are allowable

J -1 Scholar/ Yes Need written authorization from sponsor or Researcher/ If Purdue is sponsor for activity being compensated, DS-2019 is authorization Teacher

J -2 Yes Must have Employment Authorization Card

H-1B No We may pay the sponsoring institution directly and they can pay the individual

O-1 No We may pay the sponsoring institution directly and they can pay the individual

TN No We may pay the sponsoring institution directly and they can pay the individual

EAD Card Yes(Employment Authorization Card)

* 9-5-6 StatementVisitors in business or tourist status (B1, B2, WB, WT) may be paid honoraria and/or reimbursed for travel expensesif the visitor is engaged in the activity being compensated for any portion of 9 days or less and the visitor hasnot been paid or reimbursed by more than 5 other US institutions or organizations during the past 6 months.

- Please attach a copy of the individual's I-94 card and when applicable authorization from sponsor on F-1s and J -1s

StipulationsB-1 - no honorarium Yes Can reimburse for length of stay ** Must have B1 on I-94 card - with honorarium Yes Limited to 9 days and must sign 9-5-6 statement

B-2 Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

WB - no honorarium Yes Can reimburse for length of stay ** Must have WB on I-94 card - with honorarium Yes Limited to 9 days and must sign 9-5-6 statement

WT Yes * Must have 9-5-6 statement from Glacier signed9 DAY LIMIT

F-1 No Allowable with approval from sponsor for Curricular Practical Training on the I-20F-2 No

J-1 Student No

J-1 Scholar/ Yes Need written authorization from sponsor or Researcher/ If Purdue is sponsor for activity being compensated, DS-2019 is authorization Teacher

J-2 Yes Must have Employment Authorization Card

H-1B Yes Occasional and incidental to alien's employment ** 7 day limit **Greater than 7 days, need written authorization from sponsor or pay sponsor directly

O-1 No We may pay the sponsoring institution directly and they can pay the individualTN No We may pay the sponsoring institution directly and they can pay the individual

EAD Card Yes(Employment Authorization Card)

Travel expenses for business purposes are reimbursed under the accountable plan rules used by the travel department - receipts required

* 9-5-6 StatementVisitors in business or tourist status (B1, B2, WB, WT) may be paid honoraria and/or reimbursed for travel expenses if the visitor is engagedin the activity being compensated for any portion of 9 days or less and the visitor has not been paid or reimbursed by more than 5 other USinstitutions or organizations during the past 6 months.

Note: We can reimburse travel only for F-1 & J-1 if they are not receiving honorarium/fee payments for services w/o sponsors approval.This payment type is taxable to the individual and taxes will be withheld.

Reimbursement of Travel Expenses for a Non-Resident Short-Term Visitors Receiveing Honorarium/Fee Payments

Noteworthy Restrictions B-1 / B-2 and WB / WT Limited to 9 days of service at

Purdue and cannot have been paid or reimbursed expenses at more than 5 institutions in the past 6 months (9-5-6 Statement)

Must sign 9-5-6 statement printed from Glacier

Noteworthy Restrictions Exception: B-1 and WB can be reimbursed

expenses for greater than 9 days if they are not receiving an honorarium. In this case they do not have to sign the 9-5-6 statement.

Must have I-94 card with B-1 or WB indicated The visitor must stop at the border or point of

entry and request the I-94 card be marked B-1 or WB

If B-1 or WB is not marked on the I-94 card, the 9 day limit applies

Noteworthy Restrictions H-1B, F-2, TN, and O-1 visas cannot

be paid honorarium/fee for services H-1B, TN, and O-1 are employment

visas that are employer specific, job specific, and site specific.

If Purdue is not the sponsor of the individual, then approval from the sponsor may be needed before the payment can be made.

Paying an Institution Directly

If you want to pay an H-1B, TN, or O-1 a fee or reimburse expenses, you can pay their sponsoring institution directly.

Ask the sponsor to send an invoice to Purdue and pay it on a direct Invoice Voucher through A/P.

Contact SPS for guidance on their accounts. The sponsor then passes along the fee to

the individual and they are responsible for tax withholding and reporting.

I-94 card

F-1, D/S = Duration of Stay (J-1 also D/S)

TN - Date specific (H-1 also date specific)

DS-2019

What is a Tax Treaty? Treaties between the US and other

countries are negotiated. They allow for certain types of income to be exempt from tax.

There are many articles (categories) in a tax treaty. Some of the common articles we use are an exemption from tax for employee compensation, scholarship and fellowship payments, independent contractor payments, prizes and awards, and royalty payments

What is a Tax Treaty? Some countries have an exemption from

tax withholding for all categories of income and some may only have negotiated an exemption for independent contractor payments for example.

Please check the tax treaty charts on our website for a current listing of countries exempt from tax under each income type.

Glacier will indicate the allowability of the Canadian treaty, however, Purdue University does not honor the Canadian tax treaty; the individual can collect the treaty on their annual return.

IRS Form 8233 This form will print from Glacier if

applicable We must have an original signature to

grant exemption Must have a Social Security Number or

Individual Taxpayer Identification Number

Listing of countries with tax treaties is on the taxes website (http://www.purdue.edu/taxes/pdf/treatlim.pdf)

IRS Form W-7 Used to apply for ITIN (Individual

Taxpayer Identification Number) The IRS will issue an ITIN to anyone not

eligible to receive a SSN Copies, of supporting documentation

will be listed on the Tax Summary printed from Glacier, should be forwarded with the invoice voucher or wire transfer request to Cheryl Byers.

IRS Form W-7 The tax dept. will send the W-7 into the IRS

and follow for the issuance of a number Anyone receiving any type of payment

should have a SSN or ITIN If an individual does not have an ITIN, the

maximum tax withholding of 30% will be withheld

Until an ITIN or an SSN is received by the tax department, no tax treaty will be honored and the maximum tax withholding of 30% will be withheld from all payments

Travel Reimbursement Form PC

NRA (Glacier) Copy of I-94 Card Refer to reimbursement

of travel expense for NRA

Original Receipts CONUS Subsistence Rate

http://www. purdue.edu/travel/subsistence/welcome.html

Sales Tax is Reimbursable to Consultants/Visitors

WT and B-2 visa holders are limited to 9 days reimbursement and must sign the 9-5-6 statement.

Prospective Employees

We can reimburse expenses for trips to interview for any visa type on non-resident aliens.

Follow the travel department’s reimbursement policy.

Form 17C is required.

Living AllowancesKey Question to ask: Is the person

PERFORMING SERVICES(Whether paid fee or not)

versusFELLOWSHIP

(For the benefit of the individual, to further their education or

training)

Living AllowancesPERFORMING SERVICES Reimburse expenses using the Travel

Department’s policies. Paying subsistence is allowable

Payments of rent for temporary assignments (less than one year) should be paid directly to the vendor, but still need to be processed through the tax department

Any amount above allowable expenses is included in income.

Living AllowancesFELLOWSHIP – No Services Provided - US Citizens, Resident Aliens, and

Resident for Tax Purposes Receipts are not needed No tax withholding by Purdue Individual includes payment in

taxable income on their tax return No tax document issued by Purdue

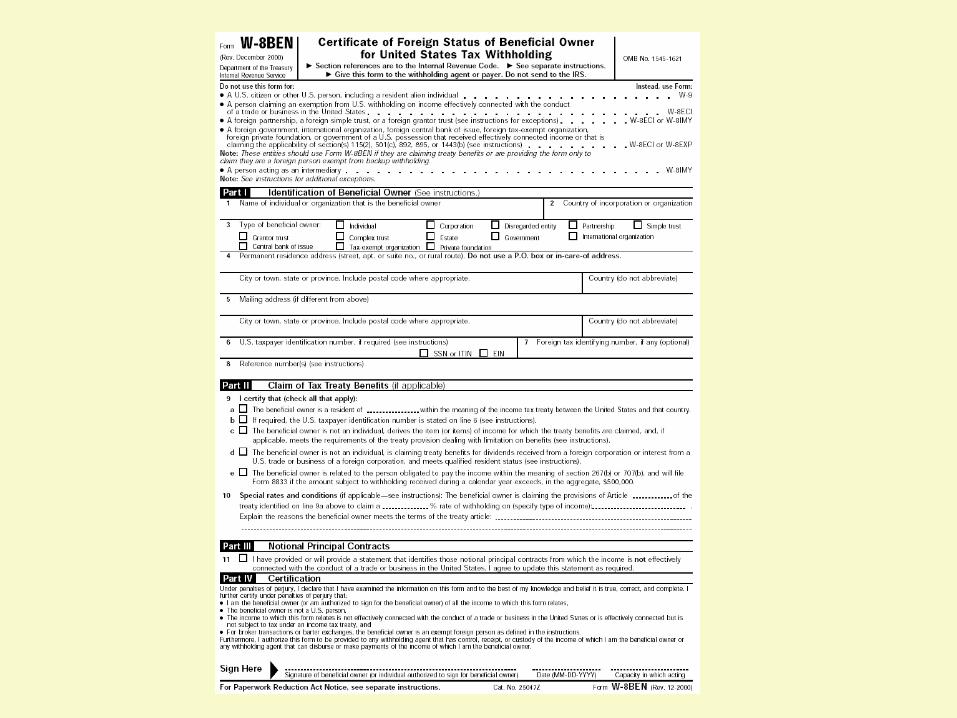

Living AllowanceFELLOWSHIP – No Service Provided - Non-Resident for Tax Purposes Individual needs to be in Glacier Receipts are not needed SSN or ITIN required Signed IRS Form W-8BEN needed (printed

from Glacier) Attach a Copy of I-94 card, visa page, and I-

20 (for F-1) or DS-2019 (for J-1) Reported to the IRS on a 1042-S Form Glacier will indicate the availability of a

treaty

Scholarships and Fellowships An amount given to an individual to aid

in the pursuit of study, training, or research

Cannot be a payment for services Grantor specifically intends money be

spent to defray costs of study, training, or research

Processed through the Division of Financial Aid (DFA) for currently enrolled students

Scholarships and Fellowships Scholarships, Fellowships, and

Training Grants for students not currently enrolled US Citizens, Resident Aliens, and

Resident for Tax Purposes Need SSN Not Reportable to the IRS by Purdue Individual will receive scholarship letter

with payment

Scholarships and Fellowships

Non Resident for Tax Purposes Glacier will determine taxability and forms

required SSN or ITIN required Form PC W-8BEN Form Required (print from Glacier) Attach copies required by the Glacier Tax

Summary; These could include a copy of the I-94 card, visa page, and I-20(F1) or DS-2019(J1)

Reported to the IRS on a 1042-S Form

Scholarships and Fellowships If eligible for a treaty

0% tax withheld If not eligible for a treaty

F-1 or J-1 visa holder – 14% tax withheld Other visa type – 30% tax withheld

Countries with treaties (tax withholding exemptions) can be found on our website (http://www.purdue.edu/taxes/pdf/treatlim.pdf)

Prizes and Awards Currently enrolled students must go

through DFA All others paid through Accounts

Payable An amount received primarily in

recognition of a special achievement or is the result of entering a contest.

Ex.) Poster contest Grantor does not specifically state

how the money should be spent.

Prizes and Awards US Citizens

Need SSN & Home Address Form PC Required Report to IRS on a 1099-MISC

Note: If award is directly related to job performance, must be processed through Payroll.

Prizes and Awards Non Resident Aliens

SSN or ITIN Required Form PC Use Glacier to determine forms required W-8BEN Form Required Attach copies of supporting documentation

I-94 card Visa page I-20 (F1) DS-2019 (J1)

Report to the IRS on a 1042-S Form Tax withheld at 30% without regard to a tax

treaty

Checklist for payments to Non-Resident Aliens

Is visa type eligible for payment of compensation? Is visa type eligible for reimbursement of expenses? Refer to visa payment reference sheets.

Obtain authorization from sponsor if needed (J-1 and H-1B.)

Attach a copy of immigration documents: If Receiving Reimbursement Compensation of Expenses o Passport I-94 Card o I-94 Card Authorization from sponsor, o Visa (except visa waiver) if needed o I-20 for F-1 o DS-2019 for J-1 o Employment Authorization Card, if has one o Authorization from sponsor, if needed

Attach IRS Form 8233, if eligible for a treaty (exemption

from taxes) for an honorarium or fee. Attach IRS Form W8-BEN for payment of scholarships,

fellowships, awards, or royalties. Attach IRS Form W-7 if the individual does not have a

social security number or individual taxpayers identification number (ITIN) - not needed for reimbursement of expenses only.

NOTE: If the visa type is unusual or the circumstances are unique – contact the tax department for guidance.

CASH ADVANCES Common uses for Cash Advances

Human Subject payments (under $50) Business or Consultant expenses in country

outside U.S. (Use credit card when possible) PRF handles cash advances for

employee travel Call the Tax Group for assistance

Cheryl Byers, phone 49-41165

Human Subjects A separate Invoice Voucher is required

for each payment to a non-resident. We have tax withholding and reporting requirements.

If the non-resident is not a current employee, please have them complete Glacier

Copy of the Human Subject procedures is on the Taxes website under the Human Subjects heading. (http://www.purdue.edu/taxes/Human_Subjects/)

Receipt Guidelines Original itemized receipt required Receipt must show paid in full or

proof of payment is needed Cannot reimburse for alcohol Receipts for travel reimbursement

under $75 not required, except hotel Airline receipt must be the

‘Passenger Receipt’ with the fare amounts noted

Receipt Guidelines Any international receipt must be

converted to US dollars, unless being reimbursed in foreign dollars

If receipt is unavailable from vendor, use the missing receipts form (on an exception basis only) Travel Form 17MR (http://www.purdue.edu/travel/xls/missingreceipt.xls)

Worker Classification Determination

“High Profile” Audit Issue

Employee and Independent Contractor defined

Application of facts and circumstances – Right to Control

Behavioral Control – How the Work is Done

Instructions How, when, where to do the work What equipment or tools to use What assistants to hire Where to purchase supplies and

services Training

Required procedures and methods Work needs to be done a certain way

Financial Control – Business Aspects of the

Work

Significant Investment

Reimbursement of Business Expenses

Opportunity for Profit or Loss

Relationship of the Parties

Employee benefits

Essential to daily operations

Continuing relationship

Written contracts

Employee vs. Independent Contractor

Withholding Requirements Employee: FIT, FICA, Medicare Independent Contractor: None

Reporting Requirements Employee: W-2 Independent Contractor: 1099-

MISC

_________________________________________________________________________

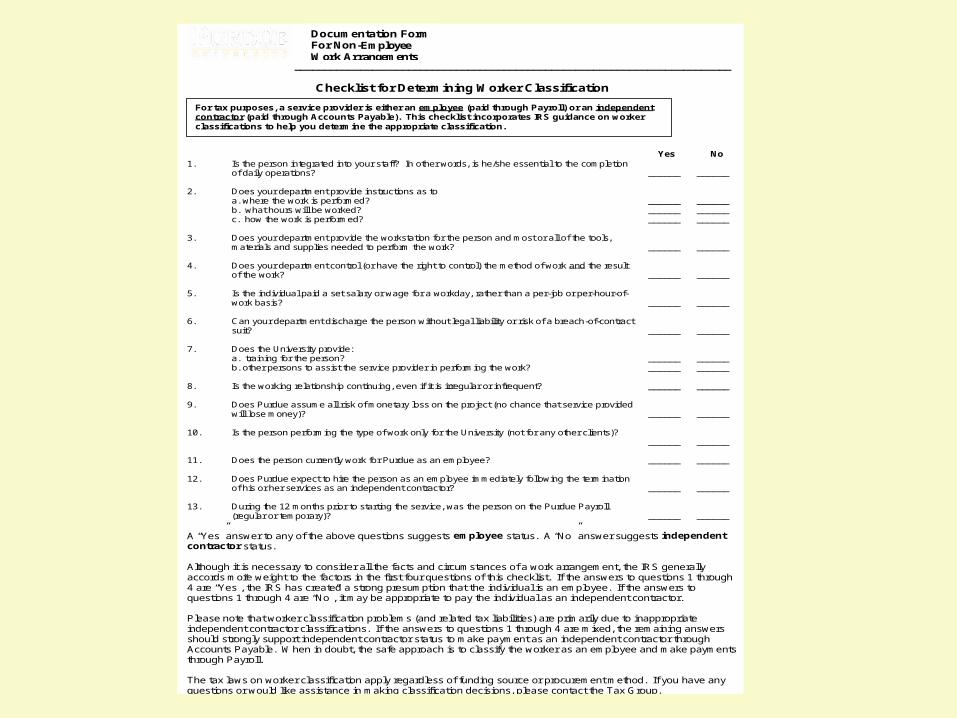

Checklist for Determining Worker Classification

Yes No 1. Is the person integrated into your staff? In other words, is he/she essential to the completion

of daily operations? ______

______

2. Does your department provide instructions as to a. where the work is performed? ______ ______ b. what hours will be worked? ______ ______ c. how the work is performed? ______ ______ 3. Does your department provide the workstation for the person and most or all of the tools,

materials and supplies needed to perform the work? ______

______

4. Does your department control (or have the right to control) the method of work and the result

of the work? ______

______

5. Is the individual paid a set salary or wage for a workday, rather than a per-job or per-hour-of-

work basis? ______

______

6. Can your department discharge the person without legal liability or risk of a breach-of-contract

suit? ______

______

7. Does the University provide: a. training for the person? ______ ______ b. other persons to assist the service provider in performing the work? ______ ______ 8. Is the working relationship continuing, even if it is irregular or infrequent? ______ ______ 9. Does Purdue assume all risk of monetary loss on the project (no chance that service provided

will lose money)? ______

______

10. Is the person performing the type of work only for the University (not for any other clients)?

______ ______

11. Does the person currently work for Purdue as an employee? ______ ______ 12. Does Purdue expect to hire the person as an employee immediately following the termination

of his or her services as an independent contractor? ______

______

13. During the 12 months prior to starting the service, was the person on the Purdue Payroll

(regular or temporary)? ______

______

A “Yes” answer to any of the above questions suggests employee status. A “No” answer suggests independent contractor status. Although it is necessary to consider all the facts and circumstances of a work arrangement, the IRS generally accords more weight to the factors in the first four questions of this checklist. If the answers to questions 1 through 4 are “Yes”, the IRS has created a strong presumption that the individual is an employee. If the answers to questions 1 through 4 are “No”, it may be appropriate to pay the individual as an independent contractor. Please note that worker classification problems (and related tax liabilities) are primarily due to inappropriate independent contractor classifications. If the answers to questions 1 through 4 are mixed, the remaining answers should strongly support independent contractor status to make payment as an independent contractor through Accounts Payable. When in doubt, the safe approach is to classify the worker as an employee and make payments through Payroll. The tax laws on worker classification apply regardless of funding source or procurement method. If you have any questions or would like assistance in making classification decisions, please contact the Tax Group.

Documentation Form For Non-Employee Work Arrangements

For tax purposes, a service provider is either an employee (paid through Payroll) or an independent contractor (paid through Accounts Payable). This checklist incorporates IRS guidance on worker classifications to help you determine the appropriate classification.

Contacts Cheryl Byers – Personal Service

Payments 41165 [email protected]

Pam Hartman – Non-Payroll Tax Accountant 47921 [email protected]

Linda Mundy – Tax Manager 40521 [email protected]

References All of the forms discussed today

can be found on the Taxes Website

www.purdue.edu/Taxes/