Webinar Slides: The 2016 Election – Key Races and the Expected Impact on the Construction Industry

93

#cbizmhmwebinar 1 CBIZ & MHM Executive Education Series™ The 2016 Election – Key Races and the Expected Impact on the Construction Industry Brian Lenihan, Associated General Contractors Chris Singerling, Associated Builders and Contractors October 25, 2016

The 2016 Election ndash Key Races and the Expected Impact on the Construction Industry Brian Lenihan Associated General Contractors Chris Singerling Associated Builders and Contractors October 25 2016

cbizmhmwebinar 2

About CBIZ amp MHM

bull Together CBIZ amp MHM are a Top Ten accounting provider bull Offices in most major markets bull Tax audit and attest and advisory services bull Over 2900 professionals nationwide

A member of Kreston International A global network of independent

accounting firms

MHM (Mayer Hoffman McCann PC) is an independent CPA firm that provides audit review and attest services and works closely with CBIZ a business consulting tax and financial services provider CBIZ and MHM are members of Kreston International Limited a global network of independent accounting firms

cbizmhmwebinar 3

About AGC of America

The Associated General Contractors of America (AGC) is the leading association for the construction industry

AGC represents more than 26000 firms including over 6500 of Americarsquos leading general contractors and over 9000 specialty-contracting firms

More than 10500 service providers and suppliers are also associated with AGC all through a nationwide network of chapters

cbizmhmwebinar 4

About ABC

Associated Builders and Contractors (ABC) is a national construction industry trade association representing nearly 21000 chapter members

Founded on the merit shop philosophy ABC and its 70 chapters help members develop people win work and deliver that work safely ethically profitably and for the betterment of the communities in which ABC and its members work

ABCs membership represents all specialties within the US construction industry and is comprised primarily of firms that perform work in the industrial and commercial sectors

cbizmhmwebinar 5

Before We Get Startedhellip

bull To view this webinar in full screen mode click on view options in the upper right hand corner

bull Click the Support tab for technical assistance

bull If you have a question during the presentation please use the QampA feature at the bottom of your screen

cbizmhmwebinar 6

CPE Credit

This webinar is eligible for CPE credit To receive credit you will need to answer periodic participation markers throughout the webinar External participants will receive their CPE certificate via email immediately following the webinar

cbizmhmwebinar 7

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation

Please contact your service provider to further discuss the impact on your business

cbizmhmwebinar 8

Presenter ndash Brian Lenihan

Brian is a government affairs professional with over 13 years of experience As AGCrsquos Director

of Tax amp Fiscal Affairs he oversees the development and advocacy of the industryrsquos positions

on tax and accounting issues in consultation with AGCrsquos CFO and CPA membership owners

and other AGC subject matter experts

Previously as a senior aide for a member of the House Ways amp Means Committee Brian

formulated and executed a legislative agenda focusing on tax and health issues In previous

positions he represented a number of clients before Congress including top publically-traded

companies municipalities defense contractors development authorities small businesses and

non-profit organizations

Brian has worked on over 30 House and Senate campaigns since 2004 A core team member

recruiting managing and coordinating over 150 volunteers each cycle he has fundraised and

implemented six-figure campaign budgets for get-out-the-vote ground operations in the

perennial battleground state of Ohio

Brian is involved with over 15 business coalitions focused on tax health pension and employer

issues Brian is a frequent speaker and panelist for tax meetings and briefings in DC and

around the country Brian earned a Political Science degree from the

University of Central Florida and resides with his wife amp children in

Virginia

cbizmhmwebinar 9

Presenter ndash Chris Singerling

Chris is senior director of political affairs at Associated Builders and

Contractors Inc in Washington DC In this capacity he supervises plans

and directs ABCrsquos political action committee (ABC PAC) its issue

advocacy arm the Free Enterprise Alliance and all other national political

efforts

Mr Singerling brings to ABC more than 12 years of experience on Capitol

Hill

Prior to joining ABC he served in a variety of positions for five different

Members of Congress most recently as political director for former

Congressman John Boehner (R-Ohio)

cbizmhmwebinar 10

Moderators

ANTHONY HAKES National Construction Industry

Practice Group Leader CBIZ amp MHM

TONY STAGLIANO National Construction Industry Practice

Group Member CBIZ amp MHM

cbizmhmwebinar 11

Agenda

Year to Date

02

01

03

04

Players in 2016

Candidates

POTUS and Veep

05 Timetable

06 Content

07 Strategy

08 Outlook

cbizmhmwebinar 12

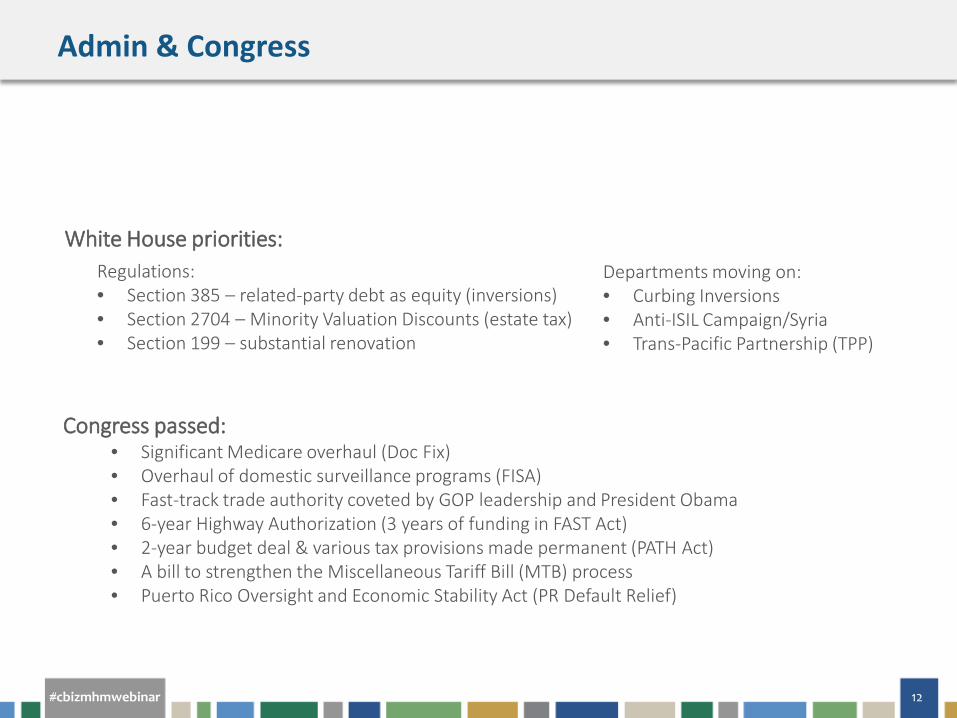

White House priorities Regulations bull Section 385 ndash related-party debt as equity (inversions) bull Section 2704 ndash Minority Valuation Discounts (estate tax) bull Section 199 ndash substantial renovation

Congress passed bull Significant Medicare overhaul (Doc Fix) bull Overhaul of domestic surveillance programs (FISA) bull Fast-track trade authority coveted by GOP leadership and President Obama bull 6-year Highway Authorization (3 years of funding in FAST Act) bull 2-year budget deal amp various tax provisions made permanent (PATH Act) bull A bill to strengthen the Miscellaneous Tariff Bill (MTB) process bull Puerto Rico Oversight and Economic Stability Act (PR Default Relief)

Admin amp Congress

cbizmhmwebinar 13

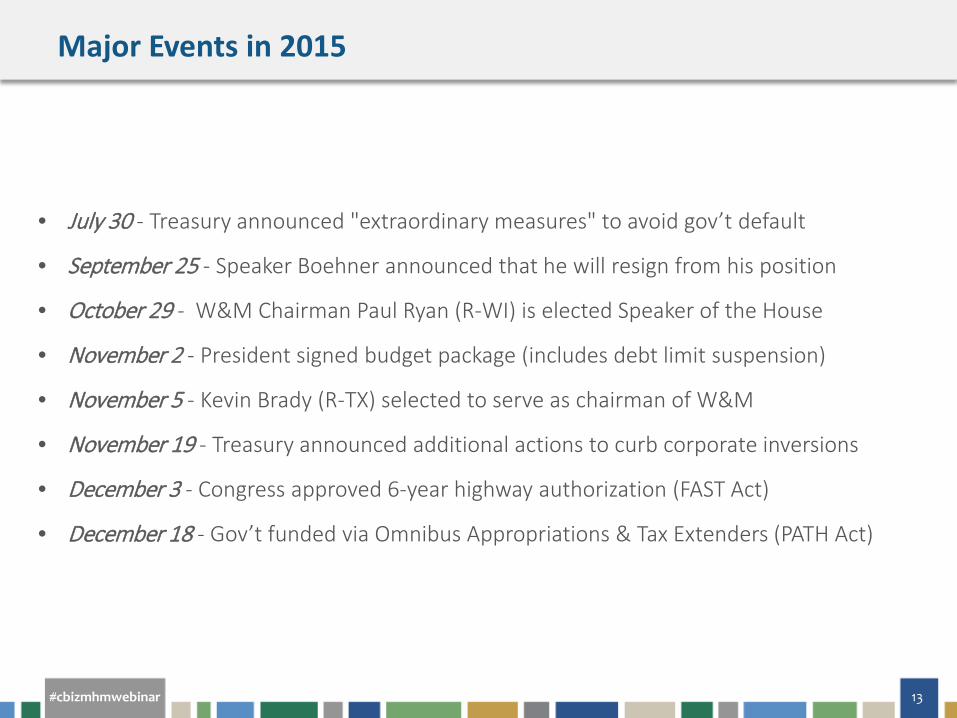

bull July 30 - Treasury announced extraordinary measures to avoid govrsquot default

bull September 25 - Speaker Boehner announced that he will resign from his position

bull October 29 - WampM Chairman Paul Ryan (R-WI) is elected Speaker of the House

bull November 2 - President signed budget package (includes debt limit suspension)

bull November 5 - Kevin Brady (R-TX) selected to serve as chairman of WampM

bull November 19 - Treasury announced additional actions to curb corporate inversions

bull December 3 - Congress approved 6-year highway authorization (FAST Act)

bull December 18 - Govrsquot funded via Omnibus Appropriations amp Tax Extenders (PATH Act)

Major Events in 2015

cbizmhmwebinar 14

bull January 12 - President Obamarsquos 8th amp final State of the Union Address

bull January 14 amp 17 - First debates of 2016 for Republicans (6th) and Democrats (4th)

bull February 9 - President released FY17 budget

bull March 1 - Super Tuesday Clinton amp Trump both won 7 of 11 states

bull March 10 - 12th and final GOP debate (Foxrsquos debate canceled Trump and Kasich back out)

bull March 16 - Obama nominated Merrick Garland to fill the Supreme Court (Scalia passed 213)

bull April 4 - Treasury released updated tax reform framework amp issued 385 regulations

bull April 14 - 10th and final Democratic primary debate

Major Events in 2016

cbizmhmwebinar 15

bull May 3 - Indiana GOP Primary solidifies Trump as presumptive GOP presidential nominee

bull May 17 amp 24 - Finance hearings on chairmanrsquos Corporate Integration proposal

bull May 25 - WampM hearing on need for tax reform

bull May 26 - Trump officially surpassed the 1237 delegates required to secure nomination

bull June 7 - Clinton secured the nomination during final Democratic primaries

bull June 24 - House Speaker released tax blueprint (sixth plank of GOP platform)

bull July 15 - Congressional Summer Recess and Major Party Conventions held (OH amp PA)

bull August 2 - Treasury released NPRM Section 2704 on valuation discounts

bull November 8 - Election day

Major Events in 2016 - YTD

cbizmhmwebinar 16

Players

cbizmhmwebinar 17

bull Republicans won their largest majority since 1928 when the party won 270 bull Vacancies ndash Rep Mark Takai (HI) passed away resigned Reps Chaka Fattah (IL) amp Ed Whitfield (KY) bull Republicans have a 4 seat majority in the Senate

2

3

US Congress

cbizmhmwebinar 18

The Chairmen

Kevin Brady (R-TX) Elected 1996 10th term

Secretary Jack Lew Assumed 2013

Asst Secretary Mark Mazur Assumed 2010

The Administration

Orrin Hatch (R-UT) Elected 1977 6th term

Players - Key Decision-Makers

cbizmhmwebinar 19

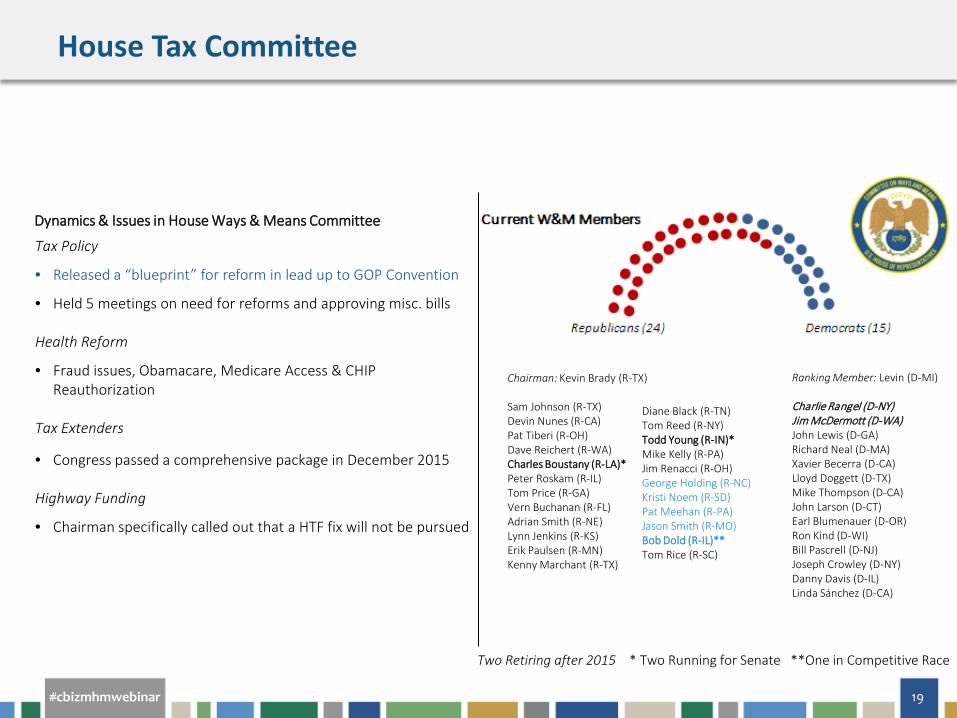

Current WampM Members

Ranking Member Levin (D-MI) Charlie Rangel (D-NY) Jim McDermott (D-WA) John Lewis (D-GA) Richard Neal (D-MA) Xavier Becerra (D-CA) Lloyd Doggett (D-TX) Mike Thompson (D-CA) John Larson (D-CT) Earl Blumenauer (D-OR) Ron Kind (D-WI) Bill Pascrell (D-NJ) Joseph Crowley (D-NY) Danny Davis (D-IL) Linda Saacutenchez (D-CA)

Dynamics amp Issues in House Ways amp Means Committee Tax Policy

bull Released a ldquoblueprintrdquo for reform in lead up to GOP Convention

bull Held 5 meetings on need for reforms and approving misc bills Health Reform

bull Congress passed a comprehensive package in December 2015 Highway Funding

bull Chairman specifically called out that a HTF fix will not be pursued

Diane Black (R-TN) Tom Reed (R-NY) Todd Young (R-IN) Mike Kelly (R-PA) Jim Renacci (R-OH) George Holding (R-NC) Kristi Noem (R-SD) Pat Meehan (R-PA) Jason Smith (R-MO) Bob Dold (R-IL) Tom Rice (R-SC)

Chairman Kevin Brady (R-TX) Sam Johnson (R-TX) Devin Nunes (R-CA) Pat Tiberi (R-OH) Dave Reichert (R-WA) Charles Boustany (R-LA) Peter Roskam (R-IL) Tom Price (R-GA) Vern Buchanan (R-FL) Adrian Smith (R-NE) Lynn Jenkins (R-KS) Erik Paulsen (R-MN) Kenny Marchant (R-TX)

Two Retiring after 2015 Two Running for Senate One in Competitive Race

House Tax Committee

cbizmhmwebinar 20

Politically Endangered ndash eked out a victory in March primary but he is likely to have a target on his back for years to come Opponent held Brady to 53 of the vote one of the lowest re-election totals in his 18 year career

Seventh Texan as Chairman ndash Won out over Pat Tiberi (OH) in 2015 to become 7th Texan with a gavel

Ch a i r m a n K ev in Br a d y

cbizmhmwebinar 21

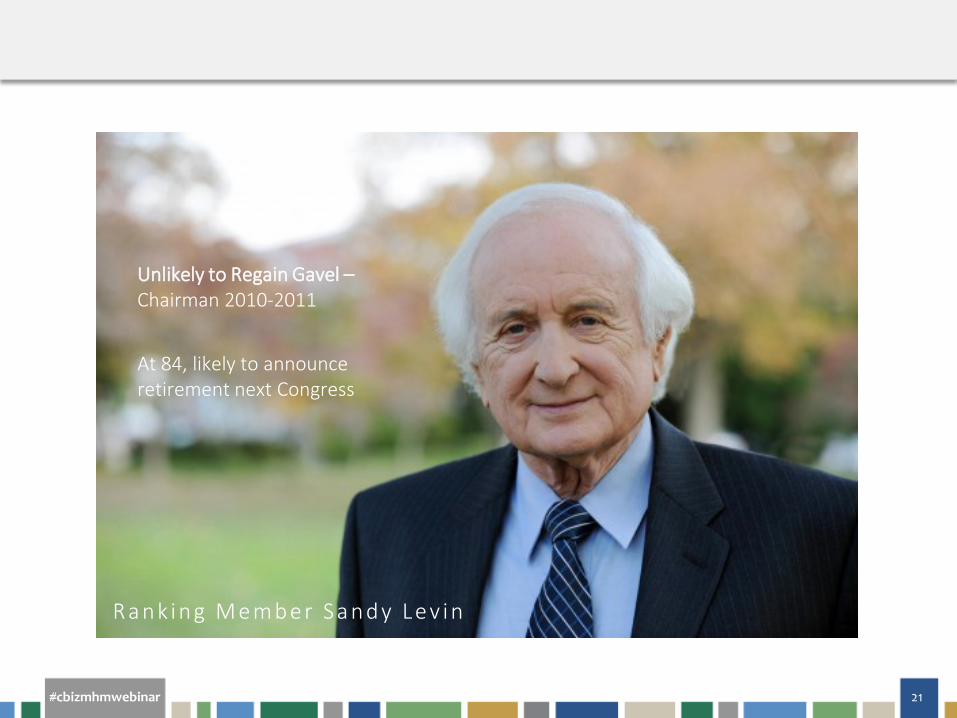

Unlikely to Regain Gavel ndash Chairman 2010-2011

At 84 likely to announce retirement next Congress

R a n k in g M em b er S a n d y L ev in

cbizmhmwebinar 22

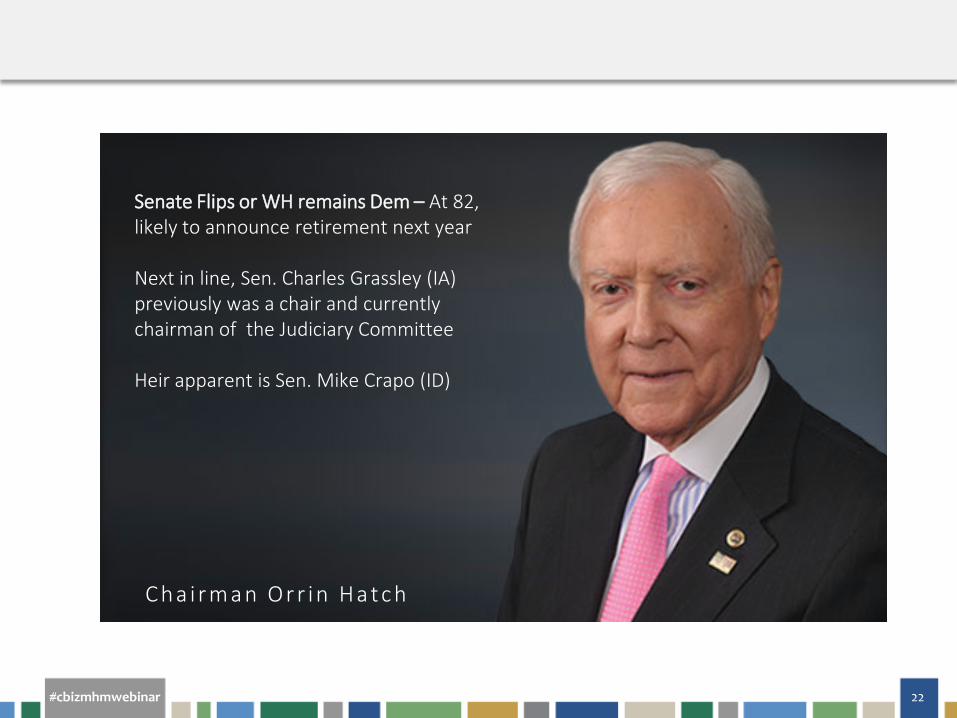

Senate Flips or WH remains Dem ndash At 82 likely to announce retirement next year Next in line Sen Charles Grassley (IA) previously was a chair and currently chairman of the Judiciary Committee Heir apparent is Sen Mike Crapo (ID)

Ch a i r m a n Or r in H a tc h

cbizmhmwebinar 23

Senate Flips ndash regains gavel lost in 2015 Has a moderate record with construction industry and businesses groups Next in line Sen Charles Schumer will be Democratic Leader in next Congress (an Ex officio member and thus a vacancy will be filled on the committee)

R a n k in g M em b er R on Wyd en

cbizmhmwebinar 24

Tax Reform and Inversions

bull Continue to address inversions comprehensive reform remains unlikely in the short term due to brevity of calendar

bull Working Groups formed in 2015 to propose recommendations (eg 2013 WampM groups)

bull Dividends Received Deduction ndash Integration proposal

Highway Trust Fund bull No plans to address funding shortfall

IRS Oversight

bull Advancing proposals to protect taxpayers from fraud and identity theft

Obamacare

bull CMS ldquo Part B Drug Payment Modelrdquo

Trade amp Trans-Pacific Partnership

bull Administration must submit a description of changes in law

bull Chairman Orrin Hatch (R-UT) dagger bull Chuck Grassley (R-IA) bull Mike Crapo (R-ID) bull Pat Roberts (R-KS) bull Mike Enzi (R-WY) bull John Cornyn (R-TX) bull John Thune (R-SD) bull Richard Burr (R-NC) bull Johnny Isakson (R-GA) bull Rob Portman (R-OH) bull Pat Toomey (R-PA) bull Dan Coats (R-IN) bull Dean Heller (R-NV) dagger bull Tim Scott (R-SC)

bull Ranking Member Ron Wyden (R-OR) bull Chuck Schumer (D-NY) bull Debbie Stabenow (R-MI) dagger bull Maria Cantwell (D-WA) dagger bull Bill Nelson (D-FL) dagger bull Bob Menendez (D-NJ) dagger bull Tom Carper (D-DE) dagger bull Ben Cardin (D-MD) dagger bull Sherrod Brown (D-OH) dagger bull Michael Bennet (D-CO) bull Bob Casey (D-PA) dagger bull Mark Warner (D-VA)

One Retiring after 2015 11 2016 re-election dagger 2017 re-elect

Dynamics amp Issues in Senate Finance Committee

Senate Tax Committee

cbizmhmwebinar 25

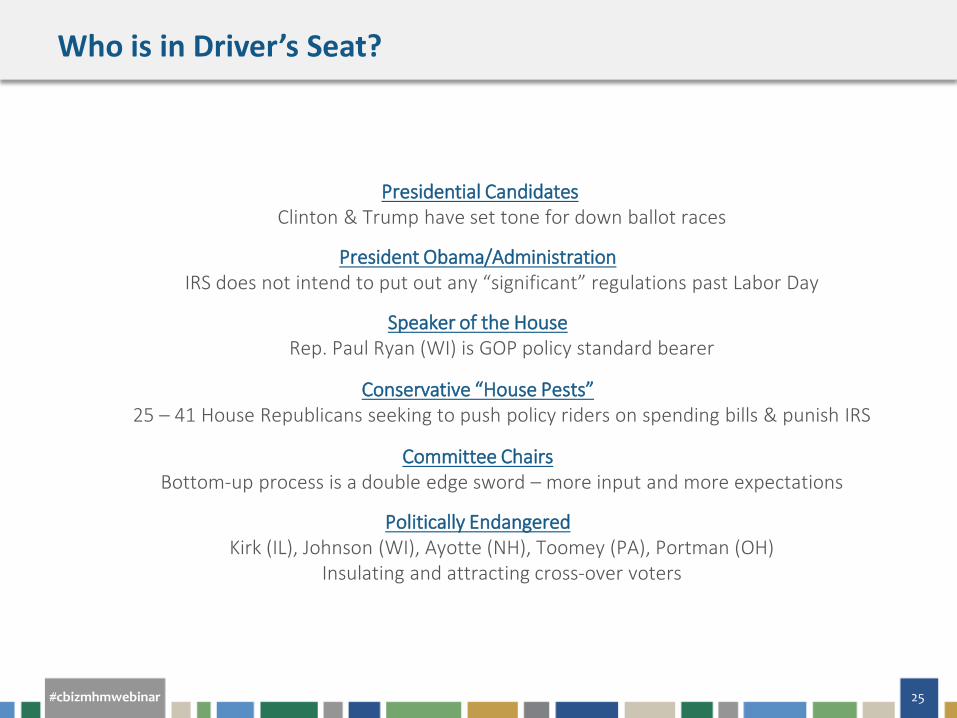

Presidential Candidates Clinton amp Trump have set tone for down ballot races

President ObamaAdministration IRS does not intend to put out any ldquosignificantrdquo regulations past Labor Day

Speaker of the House Rep Paul Ryan (WI) is GOP policy standard bearer

Conservative ldquoHouse Pestsrdquo 25 ndash 41 House Republicans seeking to push policy riders on spending bills amp punish IRS

Committee Chairs Bottom-up process is a double edge sword ndash more input and more expectations

Summary bull 12 seats are up for election in 2016 bull 3 incumbent Democrats and

2incumbent Republicans are running for re-election

bull There are seven open seats ndash bull 5 formerly Democrat bull 2 formerly Republican

Open Democrat Seat Incumbent Democrat Seeking Re-election Open Republican Seat Incumbent Republican Seeking Re-election

OH

WV VA

PA

NY

ME

NC

SC

GA

TN

KY

IN

MI

WI

MN

IL

LA

TX

OK

ID

NV

OR

WA

CA

AZ NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS

AL

NE

KS

AK

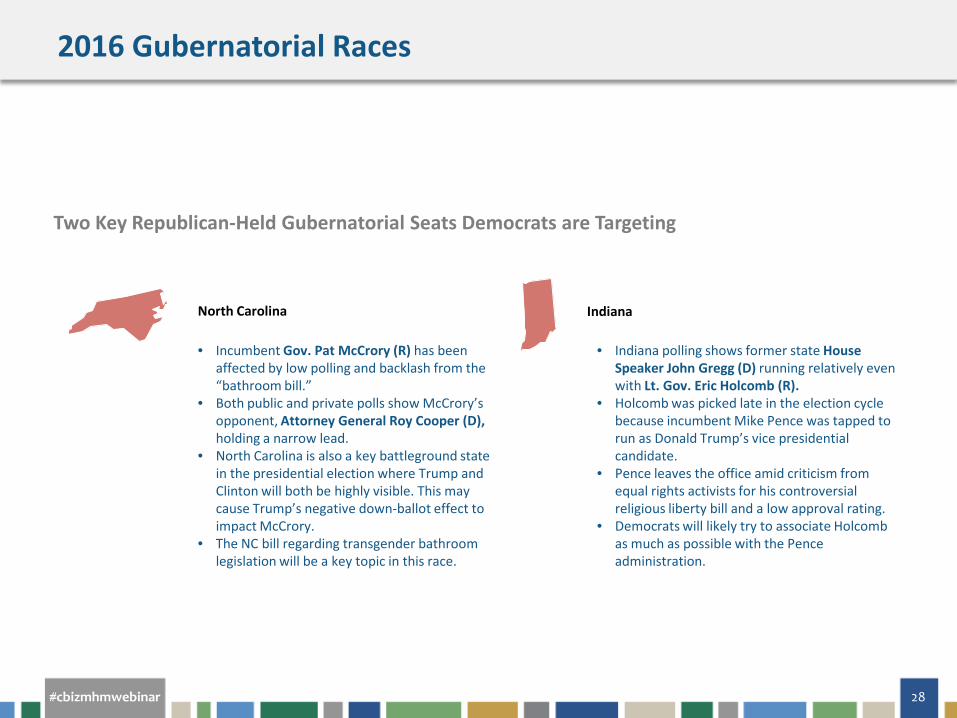

2016 Gubernatorial Races

cbizmhmwebinar 28

Two Key Republican-Held Gubernatorial Seats Democrats are Targeting

North Carolina

bull Incumbent Gov Pat McCrory (R) has been affected by low polling and backlash from the ldquobathroom billrdquo

bull Both public and private polls show McCroryrsquos opponent Attorney General Roy Cooper (D) holding a narrow lead

bull North Carolina is also a key battleground state in the presidential election where Trump and Clinton will both be highly visible This may cause Trumprsquos negative down-ballot effect to impact McCrory

bull The NC bill regarding transgender bathroom legislation will be a key topic in this race

Indiana

bull Indiana polling shows former state House Speaker John Gregg (D) running relatively even with Lt Gov Eric Holcomb (R)

bull Holcomb was picked late in the election cycle because incumbent Mike Pence was tapped to run as Donald Trumprsquos vice presidential candidate

bull Pence leaves the office amid criticism from equal rights activists for his controversial religious liberty bill and a low approval rating

bull Democrats will likely try to associate Holcomb as much as possible with the Pence administration

2016 Gubernatorial Races

cbizmhmwebinar 29

Two Key Democrat-Held Gubernatorial Seats Republicans are Targeting

Missouri

bull Gov Jay Nixon (D) is retiring from his position and the GOP sees his seat as the primary pick-up opportunity among gubernatorial races

bull Polls show a tight race between Attorney General Chris Koster (D) and Eric Grietens (R) a veteran of the wars in Iraq and Afganistan

bull Koster is a Republican-turned-Democrat campaigning with $11 million in the bank

bull Grietens is a newcomer to politics but beat three more experienced candidates in his run for the Republican nomination

West Virginia

bull West Virginia was initially a likely pick-up opportunity for the GOP but state Senate President Bill Colersquos (R) chances have been hurt by a fight over state budget problems

bull Meanwhile billionaire Jim Justice (D) has a slight lead in the polls

bull Republicans seem to be moving their focus to other races as Colersquos outlook looks grim in this election

2016 Gubernatorial Races

cbizmhmwebinar 30

Dynamics of the 2016 Senate

bull Republicans took control in 2014 and have more seats at risk from the 2010 class

bull Senate Democrats are defending 10 seats vs 24 for Republicans

bull 7 Republican Senate seats and only 2 Democratic Seats in play

bull Democrats need to net 4 (w VP Kaine) or 5 seats (w VP Pence) to retake the Senate

bull During Presidential years demographics of ldquolikely votersrdquo heavily favors Democrats

bull The opposite is true during mid-term elections when Republicans tend to be favored

bull 2018 fares better for GOP Senate Races ndash when Dems have 23 seats up vs 10 GOP

2016 Senate Races

cbizmhmwebinar 31

Since the 1970s the share of voters who split their tickets mdashsupporting one party for president and the other in Senate racesmdash has steadily declined to 23 on average during the 1980s 16 across Clintonrsquos two races 13 in 2008 and just 10 in 2012 The goal is no longer to identify and persuade those in the squishy middle of the ideological spectrum to split their tickets Instead campaigns try to find sporadic voters who if they could be persuaded to go to the polls would vote straight down the ticket ndash GET OUT THE VOTE Overall just 8 of voters in the 34 states with Senate races say they will vote for either Clinton or Trump for president and a Senate candidate from the opposing party 4 will vote for a Democrat or Republican for president and a House candidate from other party

Source Pew Research Center Survey 927- 1010 National Election Studies analyzed by Emory Univ Prof Abramowitz

Straight vs Split Tickets

cbizmhmwebinar 32

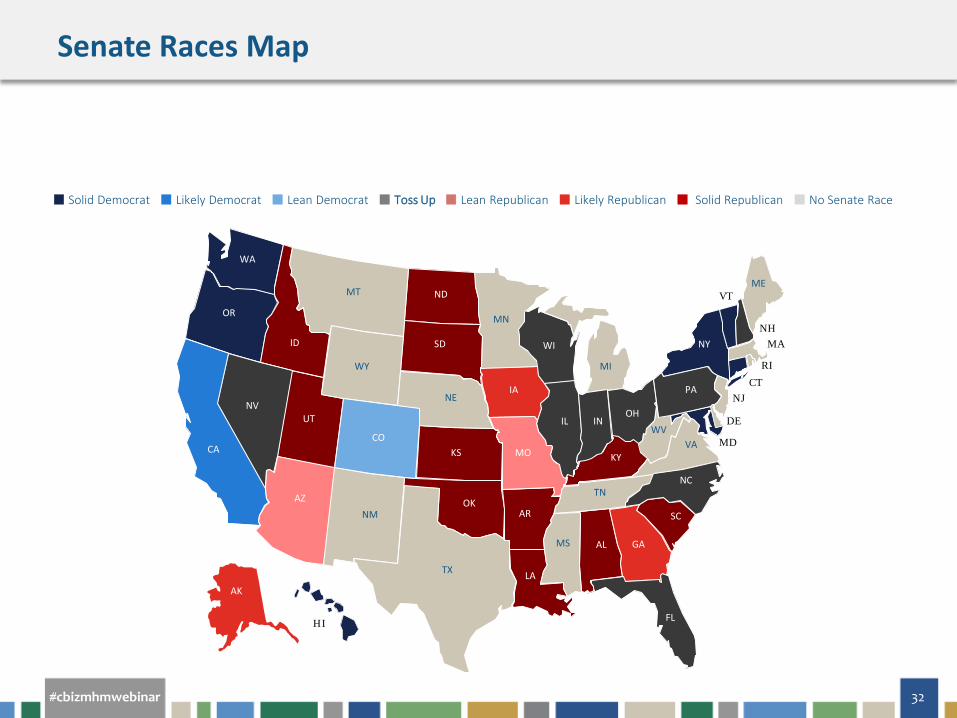

Solid Democrat Likely Democrat Lean Democrat Toss Up Lean Republican Likely Republican Solid Republican No Senate Race

NY

SC

KY

LA

OK

ID

OR

WA

ND

SD

UT

AR

AL

KS

HI

VT

MD

CT

GA

CA

IA

AK

MI

MN

TX

NM

WY

MT

NE

WV VA

TN

MS

ME

RI

MA

NJ

DE OH

PA

IN

WI

IL NV

FL

NH

NC

MO

AZ

CO

Senate Races Map

cbizmhmwebinar 33

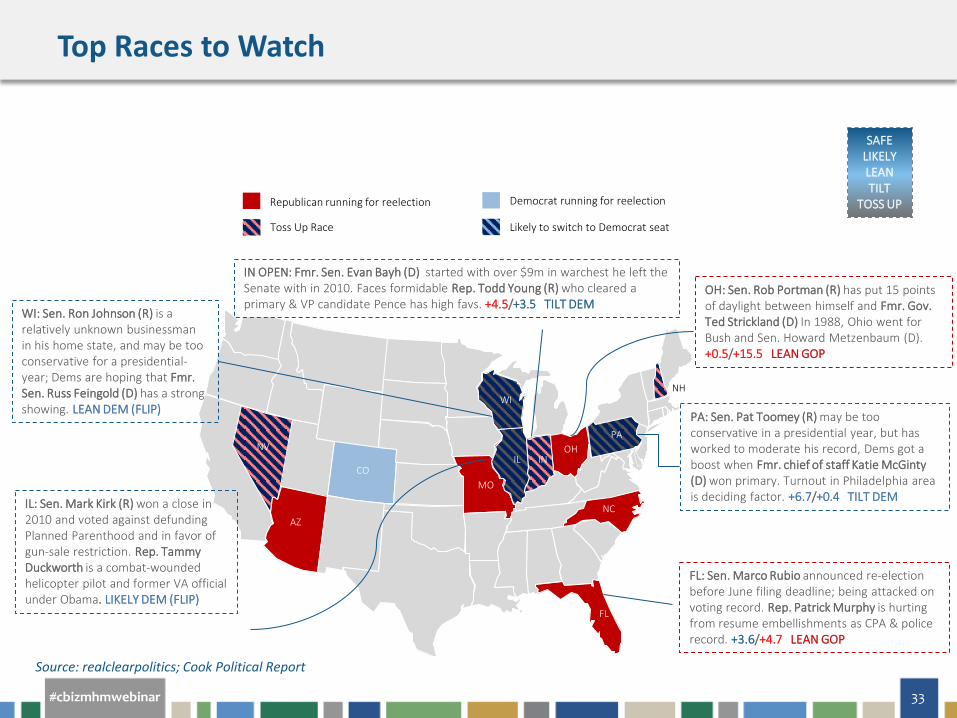

Top Races to Watch

Republican running for reelection

Toss Up Race

Democrat running for reelection

Likely to switch to Democrat seat

OH NV

CO

FL

NH

FL Sen Marco Rubio announced re-election before June filing deadline being attacked on voting record Rep Patrick Murphy is hurting from resume embellishments as CPA amp police record +36+47 LEAN GOP

PA Sen Pat Toomey (R) may be too conservative in a presidential year but has worked to moderate his record Dems got a boost when Fmr chief of staff Katie McGinty (D) won primary Turnout in Philadelphia area is deciding factor +67+04 TILT DEM

WI Sen Ron Johnson (R) is a relatively unknown businessman in his home state and may be too conservative for a presidential-year Dems are hoping that Fmr Sen Russ Feingold (D) has a strong showing LEAN DEM (FLIP)

IL Sen Mark Kirk (R) won a close in 2010 and voted against defunding Planned Parenthood and in favor of gun-sale restriction Rep Tammy Duckworth is a combat-wounded helicopter pilot and former VA official under Obama LIKELY DEM (FLIP)

AZ

SAFE LIKELY LEAN TILT

TOSS UP

MO

NC

WI

IL

PA

IN

IN OPEN Fmr Sen Evan Bayh (D) started with over $9m in warchest he left the Senate with in 2010 Faces formidable Rep Todd Young (R) who cleared a primary amp VP candidate Pence has high favs +45+35 TILT DEM

OH Sen Rob Portman (R) has put 15 points of daylight between himself and Fmr Gov Ted Strickland (D) In 1988 Ohio went for Bush and Sen Howard Metzenbaum (D) +05+155 LEAN GOP

WI

IL

PA

IN

Source realclearpolitics Cook Political Report

cbizmhmwebinar 34

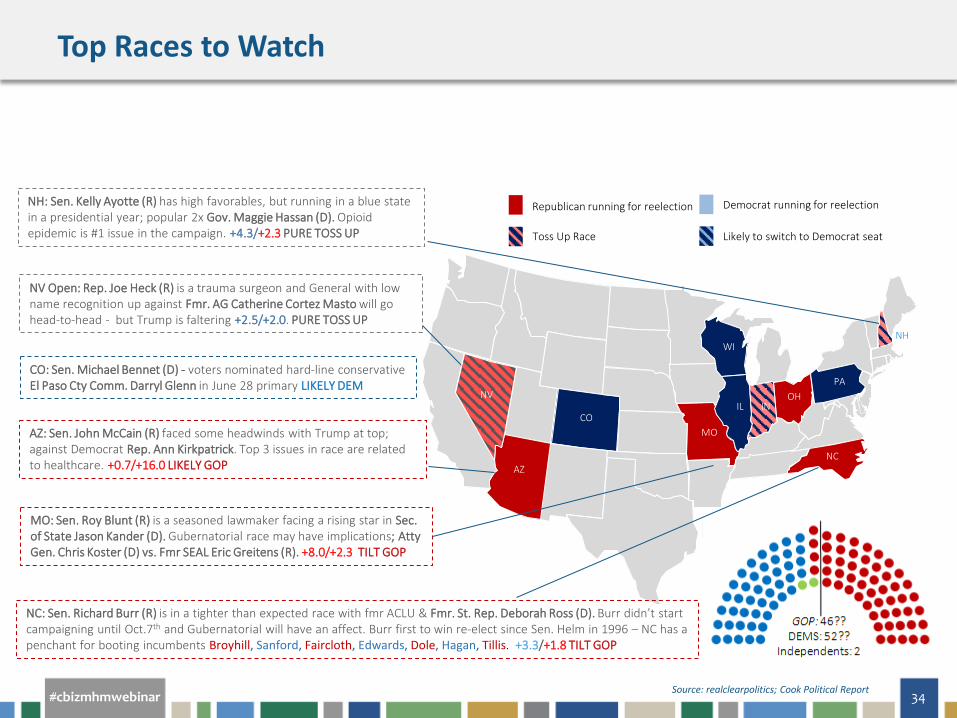

Top Races to Watch

OH NV

CO

NH

NV Open Rep Joe Heck (R) is a trauma surgeon and General with low name recognition up against Fmr AG Catherine Cortez Masto will go head-to-head - but Trump is faltering +25+20 PURE TOSS UP

CO Sen Michael Bennet (D) - voters nominated hard-line conservative El Paso Cty Comm Darryl Glenn in June 28 primary LIKELY DEM

AZ Sen John McCain (R) faced some headwinds with Trump at top against Democrat Rep Ann Kirkpatrick Top 3 issues in race are related to healthcare +07+160 LIKELY GOP AZ

MO

NC

MO Sen Roy Blunt (R) is a seasoned lawmaker facing a rising star in Sec of State Jason Kander (D) Gubernatorial race may have implications Atty Gen Chris Koster (D) vs Fmr SEAL Eric Greitens (R) +80+23 TILT GOP

WI

IL

PA

IN

NH Sen Kelly Ayotte (R) has high favorables but running in a blue state in a presidential year popular 2x Gov Maggie Hassan (D) Opioid epidemic is 1 issue in the campaign +43+23 PURE TOSS UP

NC Sen Richard Burr (R) is in a tighter than expected race with fmr ACLU amp Fmr St Rep Deborah Ross (D) Burr didnrsquot start campaigning until Oct7th and Gubernatorial will have an affect Burr first to win re-elect since Sen Helm in 1996 ndash NC has a penchant for booting incumbents Broyhill Sanford Faircloth Edwards Dole Hagan Tillis +33+18 TILT GOP

Democrats have 23 seats up with 10 competitive races (FL IN MO NM ND OH PA VA WV WI) Republicans expected to have 8 seats up in fairly safe territory

2018 Senate Races

cbizmhmwebinar 36

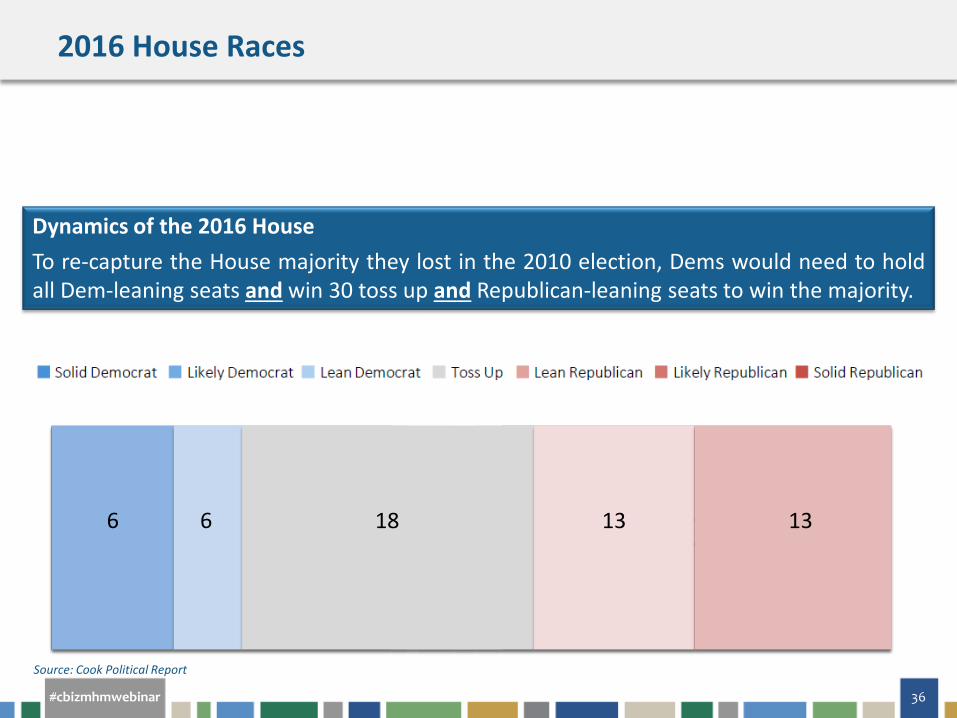

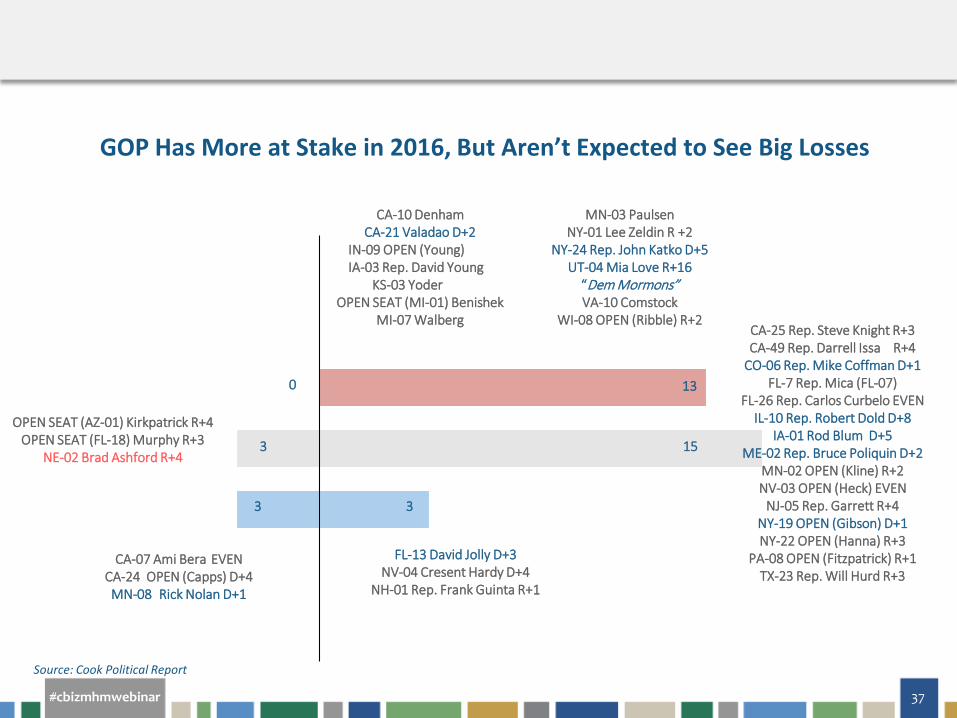

177 202 6 13 6 13 18

Dynamics of the 2016 House To re-capture the House majority they lost in the 2010 election Dems would need to hold all Dem-leaning seats and win 30 toss up and Republican-leaning seats to win the majority

Source Cook Political Report

2016 House Races

cbizmhmwebinar 37

Lean Democrat

Toss-Up

Lean Republican

15 3

0 13

3 3

OPEN SEAT (AZ-01) Kirkpatrick R+4 OPEN SEAT (FL-18) Murphy R+3

NE-02 Brad Ashford R+4

CA-07 Ami Bera EVEN CA-24 OPEN (Capps) D+4 MN-08 Rick Nolan D+1

FL-13 David Jolly D+3 NV-04 Cresent Hardy D+4

NH-01 Rep Frank Guinta R+1

CA-25 Rep Steve Knight R+3 CA-49 Rep Darrell Issa R+4

CO-06 Rep Mike Coffman D+1 FL-7 Rep Mica (FL-07)

FL-26 Rep Carlos Curbelo EVEN IL-10 Rep Robert Dold D+8

IA-01 Rod Blum D+5 ME-02 Rep Bruce Poliquin D+2

MN-02 OPEN (Kline) R+2 NV-03 OPEN (Heck) EVEN

NJ-05 Rep Garrett R+4 NY-19 OPEN (Gibson) D+1 NY-22 OPEN (Hanna) R+3

PA-08 OPEN (Fitzpatrick) R+1 TX-23 Rep Will Hurd R+3

CA-10 Denham CA-21 Valadao D+2

IN-09 OPEN (Young) IA-03 Rep David Young

KS-03 Yoder OPEN SEAT (MI-01) Benishek

MI-07 Walberg

MN-03 Paulsen NY-01 Lee Zeldin R +2

NY-24 Rep John Katko D+5 UT-04 Mia Love R+16

ldquoDem Mormonsrdquo VA-10 Comstock

WI-08 OPEN (Ribble) R+2

GOP Has More at Stake in 2016 But Arenrsquot Expected to See Big Losses

Source Cook Political Report

Chart1

Democrats

Republicans

-3

4

-3

16

0

14

Sheet1

cbizmhmwebinar 38

Source Nielsen

0

20

40

60

80

100

120

LOYALISTS PERSUADABLES ANTAGONISTS

85 96

22

28 15

(members)

At Risk

Safe Seat

NEXT CONGRESS LESS FRIENDLY Votes with House Leadership

Loyalists at least 9 of 11 Persuables 5-8 times Antagonists 4 of 11 or fewer

Sour

ce ldquo

At R

iskrdquo

base

d on

Sab

ato

Crys

tal B

all r

atin

gs (n

ot ldquo

safe

rdquo) v

otes

with

Lea

ders

hip

com

pile

d by

Fisc

alN

ote

cbizmhmwebinar 39

POTUS

cbizmhmwebinar 40

cbizmhmwebinar 41

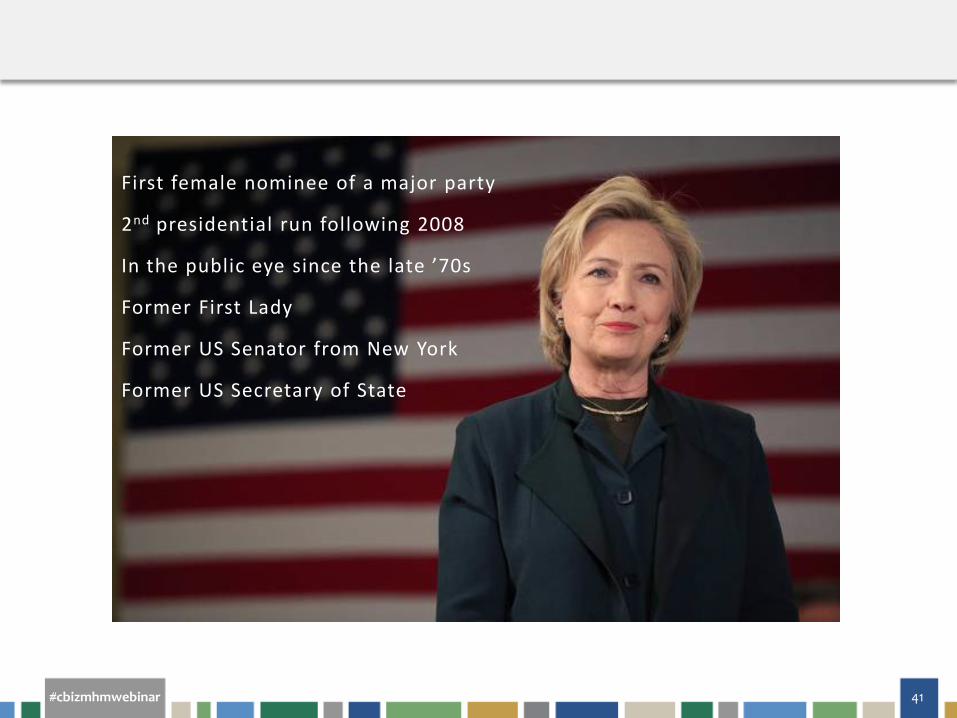

First female nominee of a major party

2nd presidential run following 2008

In the public eye since the late rsquo70s

Former First Lady

Former US Senator from New York

Former US Secretary of State

cbizmhmwebinar 42

Businessman amp TV personality

Chairman of Trump Organization

Explored 2008 run as Reform Party candidate

First candidacy as a Republican

Defeated 16 Republicans to secure nomination

cbizmhmwebinar 43

bull Ticket became the first ticket of any party to consist of two governors since the 1948 election cycle

bull Platform is socially liberal and fiscally conservative a political ideology that currently resonates well in the Mountain West and the Northeast

bull Nationally he has hovered around 7

Name Gary Johnson

Party Libertarian

Last Political Position Held

Governor of New Mexico (1995-2003)

Vice President

William Weld Former Gov of Massachusetts

Name Jill Stein

Party Green

Last Political Position Held

Lexington MA Town Meeting Member (1995-2011)

Vice President

scholar and activist Ajamu Baraka

Committed to running on a platform that very much resembles Bernie Sandersrsquo policy goals but Steinrsquos approach has been called slightly ldquomore pacifistrdquo and ldquomore ambitiousrdquo Polling nationally around 5 but has failed to show a promising regional appeal from which she could make an impact on the electoral college vote

Major 3rd Party Candidates

cbizmhmwebinar 44

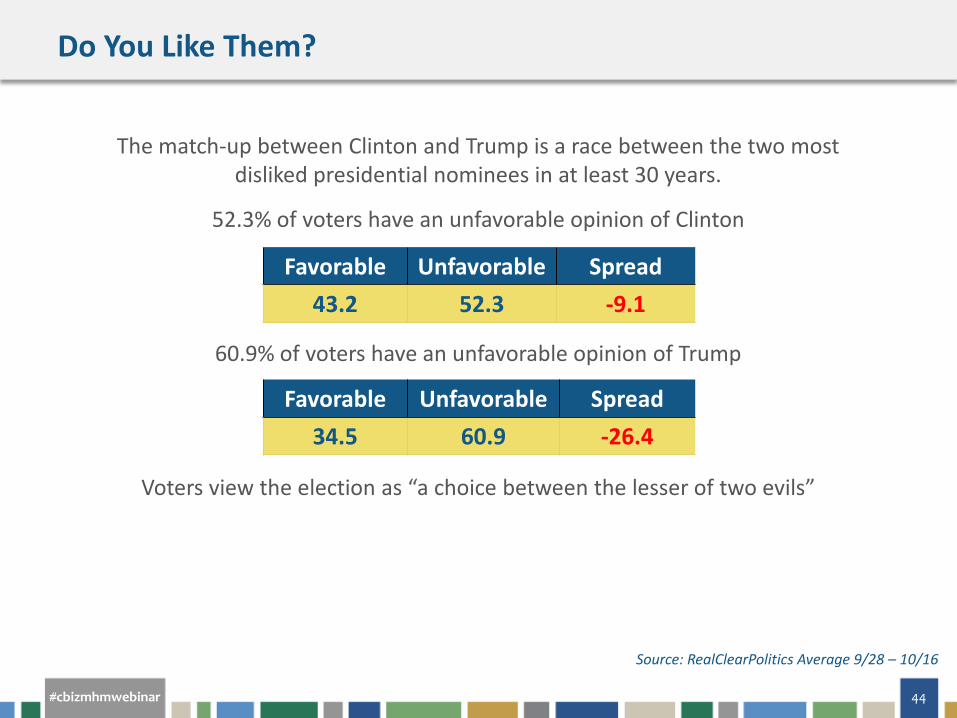

Do You Like Them

The match-up between Clinton and Trump is a race between the two most disliked presidential nominees in at least 30 years

523 of voters have an unfavorable opinion of Clinton

609 of voters have an unfavorable opinion of Trump

Voters view the election as ldquoa choice between the lesser of two evilsrdquo

Source RealClearPolitics Average 928 ndash 1016

Favorable Unfavorable Spread 432 523 -91

Favorable Unfavorable Spread 345 609 -264

cbizmhmwebinar 45

Source Quinnipiac University Poll August 2015

Use One Word

cbizmhmwebinar 46

Use One Word

Source Quinnipiac University Poll August 2015

cbizmhmwebinar 47

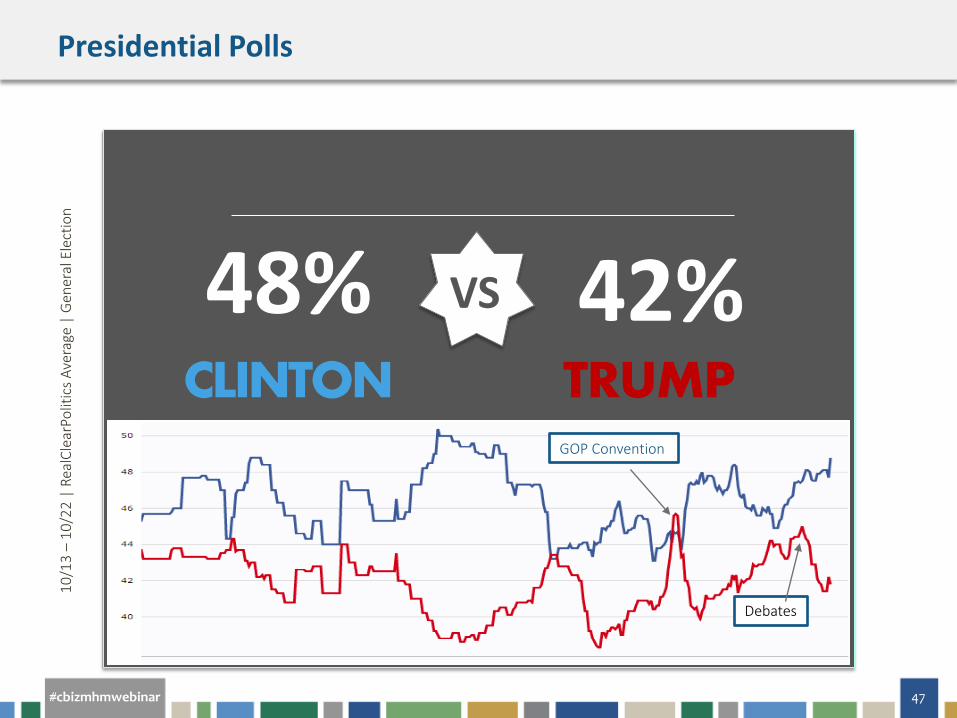

48 42 CLINTON TRUMP

VS

GOP Convention

Debates

101

3 ndash

102

2 |

Real

Clea

rPol

itics

Ave

rage

| G

ener

al E

lect

ion

Presidential Polls

cbizmhmwebinar 48

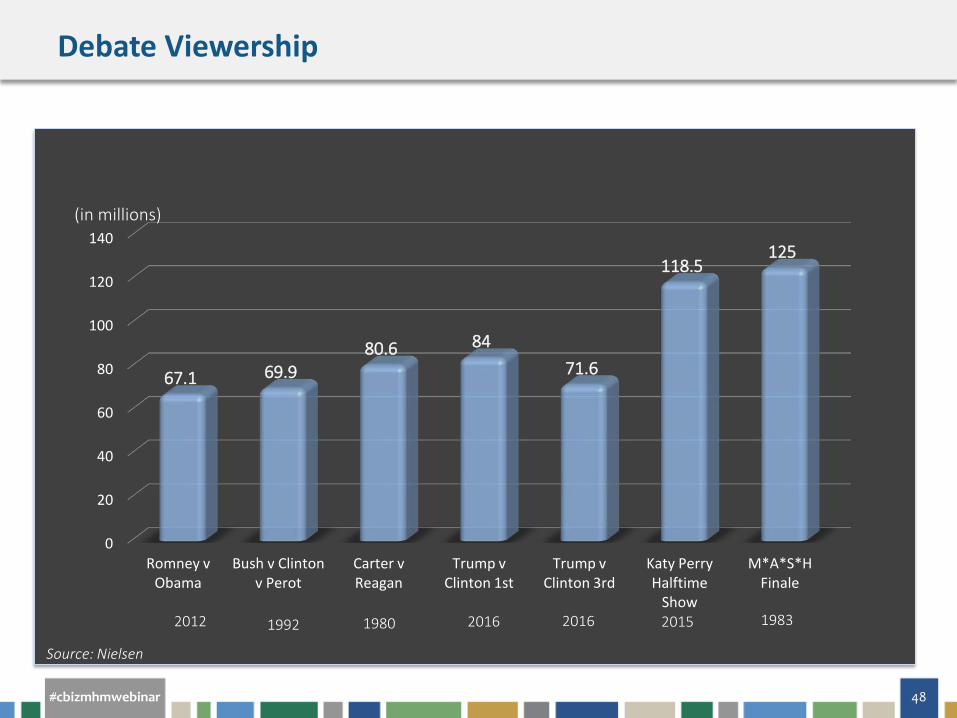

Source Nielsen

0

20

40

60

80

100

120

140

Romney v Obama

Bush v Clinton v Perot

Carter v Reagan

Trump v Clinton 1st

Trump v Clinton 3rd

Katy Perry Halftime

Show

MASH Finale

671 699 806 84

716

1185 125

(in millions)

1992 1980 2012 2016 2016 2015 1983

Debate Viewership

cbizmhmwebinar 49

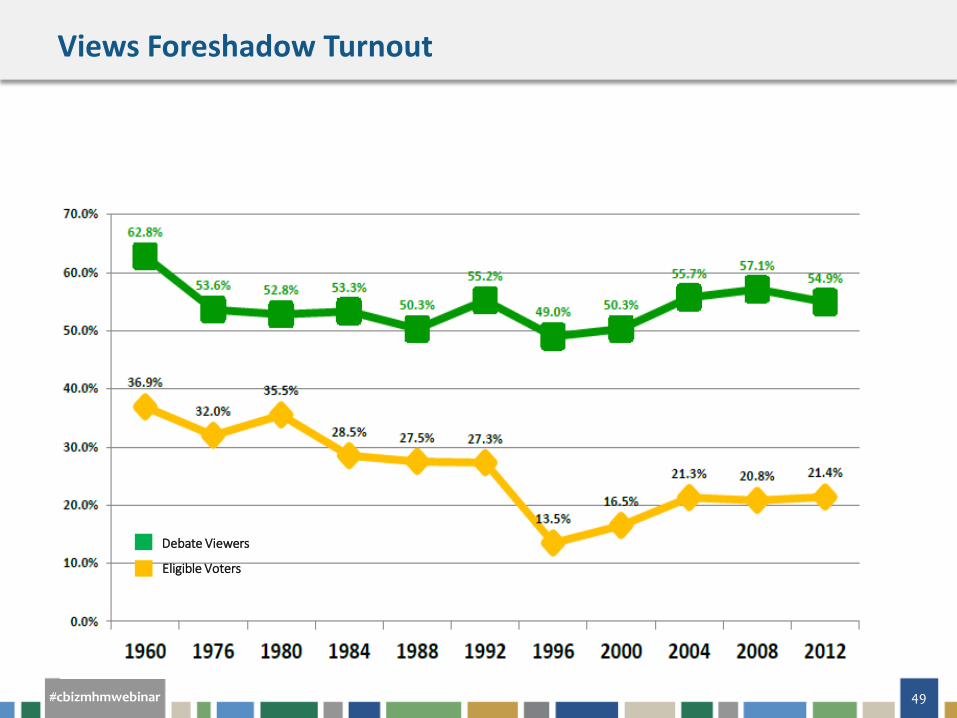

Debate Viewers

Eligible Voters

Views Foreshadow Turnout

cbizmhmwebinar 50

200 million now registered to vote for 1st time in US history Milestone is due to aggressive voter registration efforts and a symptom of the fast-growing and demographically shifting electorate 426 of new voters lean Democratic while only 29 lean Republican Only 1463 million were registered as recently as 2008 mdash a remarkable 33 surge The last time a Clinton ballot 20 years ago the electorate was 1276 million

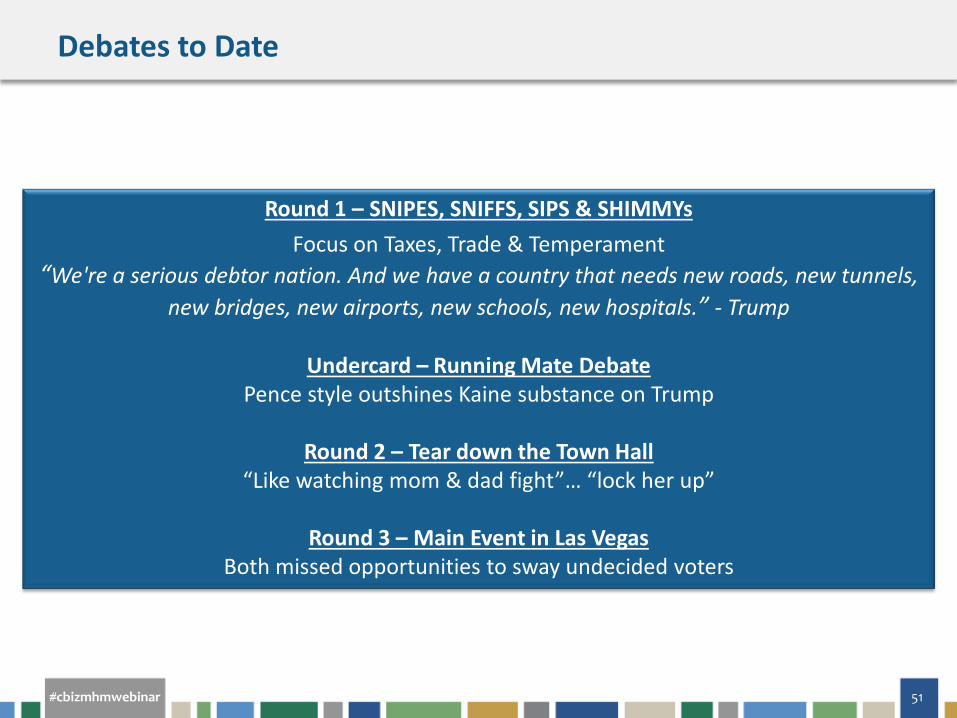

ldquoWere a serious debtor nation And we have a country that needs new roads new tunnels new bridges new airports new schools new hospitalsrdquo - Trump

Undercard ndash Running Mate Debate

Pence style outshines Kaine substance on Trump

Round 2 ndash Tear down the Town Hall ldquoLike watching mom amp dad fightrdquohellip ldquolock her uprdquo

Round 3 ndash Main Event in Las Vegas

Both missed opportunities to sway undecided voters

Debates to Date

cbizmhmwebinar 52

OH 20

WV 5

VA 13

PA 21

NY 31

ME 4

NC 15

SC 8

GA 15

TN 11

KY 8

IN 11

MI 17

WI 10

MN 10

IL 21

LA 9

TX 34

OK 7

ID 4

NV 5

OR 7

WA

CA 55

AZ 10 NM

5

CO 9

WY 3

MT 3 ND

3

SD 3

IA 7

UT 5

FL 27

AR 6

MO 11

MS 6

AL 9

NE 4

KS 6

AK 3

11

HI 4

NH 4

VT 3

1

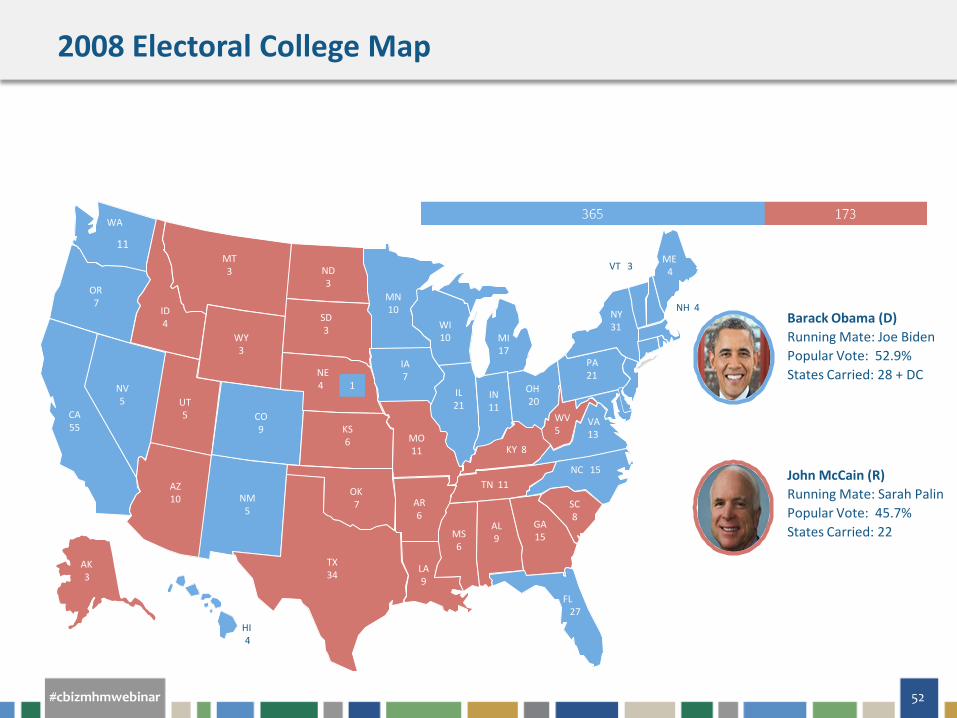

Barack Obama (D) Running Mate Joe Biden Popular Vote 529 States Carried 28 + DC

John McCain (R) Running Mate Sarah Palin Popular Vote 457 States Carried 22

2008 Electoral College Map

Chart1

Obama

McCain

Sheet1

cbizmhmwebinar 53

OH 18

WV 5 VA

13

PA 20

NY 29

ME 4

NC 15

SC 9

GA 16

TN 11

KY 8

IN 11

MI 16

WI 10

MN 10

IL 20

LA 8

TX 38

OK 7

ID 6

NV 6

OR 7

WA

CA 55

AZ 11 NM

5

CO 9

WY 3

MT 3

ND 3

SD 3

IA 6

UT 6

FL 29

AR 6

MO 10

MS 6

AL 9

NE 5

KS 6

AK 3

12

HI 4

NH 4

VT 3

Barack Obama (D) Running Mate Joe Biden Popular Vote 511 States Carried 26 + DC

Mitt Romney (R) Running Mate Paul Ryan Popular Vote 472 States Carried 24

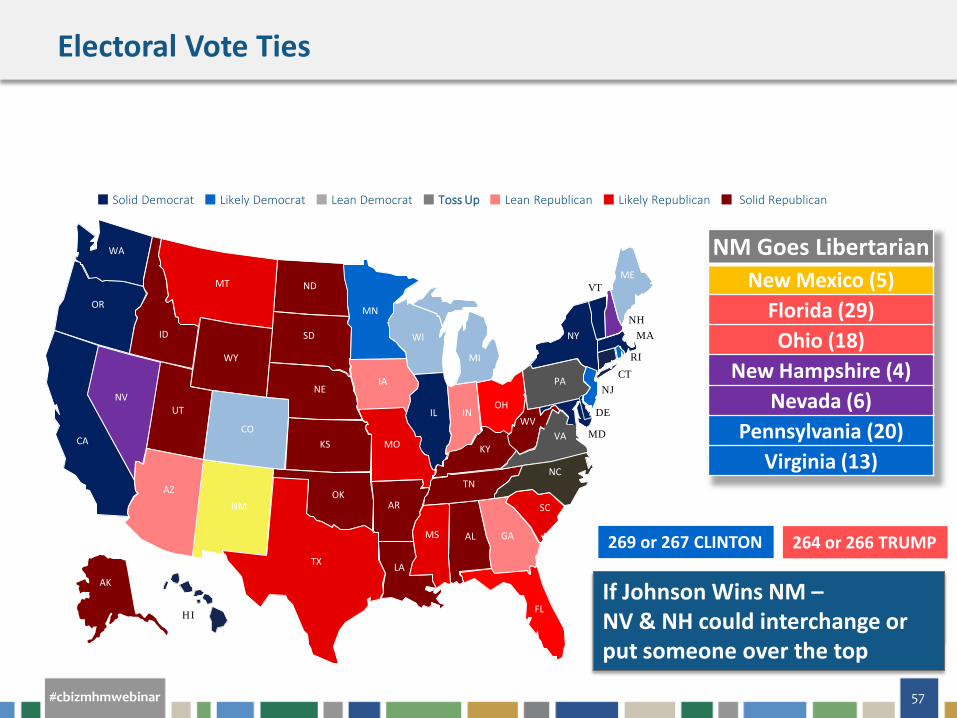

97 Possible Combinations If Maines 2nd or Nebraska 2nd District goes Blue

If Johnson Wins NM ndash NV amp NH could interchange or put someone over the top

269 or 267 CLINTON

Electoral Vote Ties

cbizmhmwebinar 58

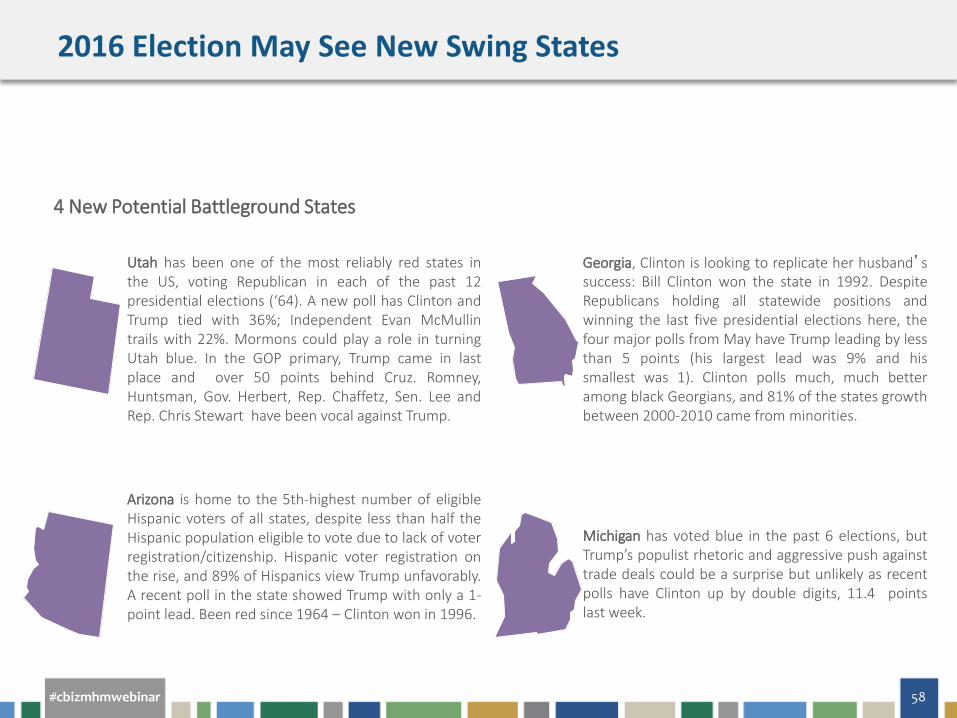

4 New Potential Battleground States

Utah has been one of the most reliably red states in the US voting Republican in each of the past 12 presidential elections (lsquo64) A new poll has Clinton and Trump tied with 36 Independent Evan McMullin trails with 22 Mormons could play a role in turning Utah blue In the GOP primary Trump came in last place and over 50 points behind Cruz Romney Huntsman Gov Herbert Rep Chaffetz Sen Lee and Rep Chris Stewart have been vocal against Trump

Arizona is home to the 5th-highest number of eligible Hispanic voters of all states despite less than half the Hispanic population eligible to vote due to lack of voter registrationcitizenship Hispanic voter registration on the rise and 89 of Hispanics view Trump unfavorably A recent poll in the state showed Trump with only a 1-point lead Been red since 1964 ndash Clinton won in 1996

Georgia Clinton is looking to replicate her husbandrsquos success Bill Clinton won the state in 1992 Despite Republicans holding all statewide positions and winning the last five presidential elections here the four major polls from May have Trump leading by less than 5 points (his largest lead was 9 and his smallest was 1) Clinton polls much much better among black Georgians and 81 of the states growth between 2000-2010 came from minorities

Michigan has voted blue in the past 6 elections but Trumprsquos populist rhetoric and aggressive push against trade deals could be a surprise but unlikely as recent polls have Clinton up by double digits 114 points last week

2016 Election May See New Swing States

cbizmhmwebinar 59

Electors cast their votes on First Monday after the second Wednesday in December at state capitols (Dec 14)

If no candidate receives 270 Electoral votes the House elects the President from the 3 candidates who received the most Electoral votes Each state delegation has one vote Each Senator would cast one vote for Vice President from the 2 candidates with the most Electoral votes

If the House fails to elect a President by Inauguration Day (Jan 20) the Vice-President Elect serves as acting President until the deadlock is resolved in the House (12th Amendment) The new Congress sworn in on Jan 3 2017 would be those that break the tie (20th Amendment moved the start of the new session of Congress from March) The GOP will likely retain at least 30 state delegations in the 115th Congress (2017) ndash thus select Donald Trump as POTUS

If the Senate goes Democratic then Sen Tim Kaine would become president (could vote for himself) If Republicans maintain control then Gov Mike Pence will be the 45th president If the Senate also deadlocksmdashthe unlikeliest of unlikely scenariosmdashthen according to the Presidential Succession Act of 1947 the presidency would go to Speaker of the House Paul Ryan (R-WI)

Electoral College Votes

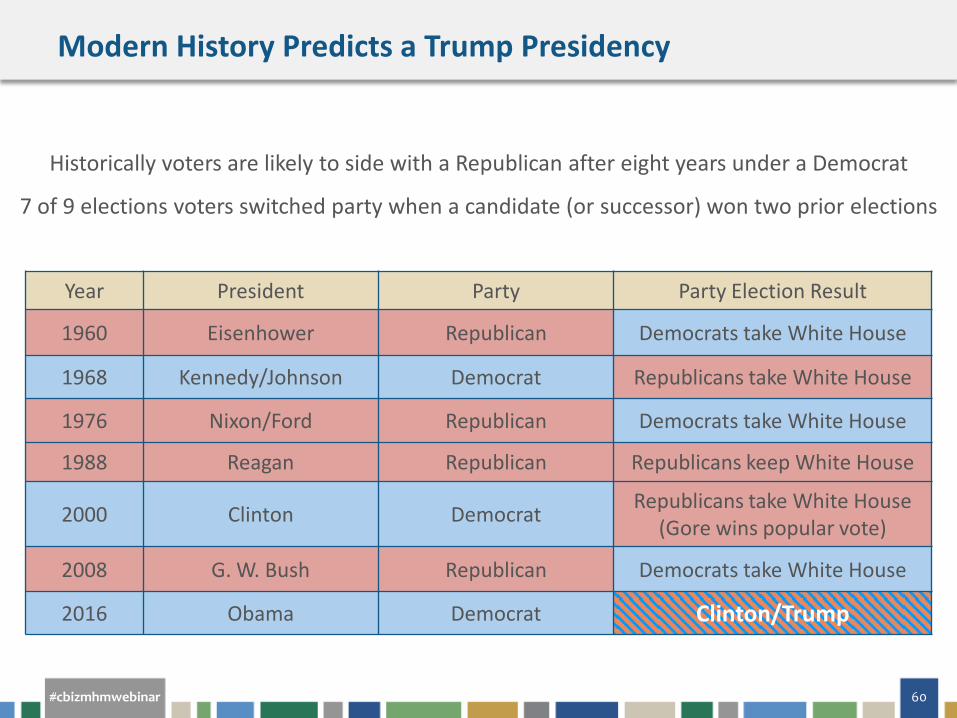

cbizmhmwebinar 60

Historically voters are likely to side with a Republican after eight years under a Democrat

7 of 9 elections voters switched party when a candidate (or successor) won two prior elections

Year President Party Party Election Result

1960 Eisenhower Republican Democrats take White House

1968 KennedyJohnson Democrat Republicans take White House

1976 NixonFord Republican Democrats take White House

1988 Reagan Republican Republicans keep White House

2000 Clinton Democrat Republicans take White House (Gore wins popular vote)

2008 G W Bush Republican Democrats take White House

2016 Obama Democrat ClintonTrump

Modern History Predicts a Trump Presidency

cbizmhmwebinar 61

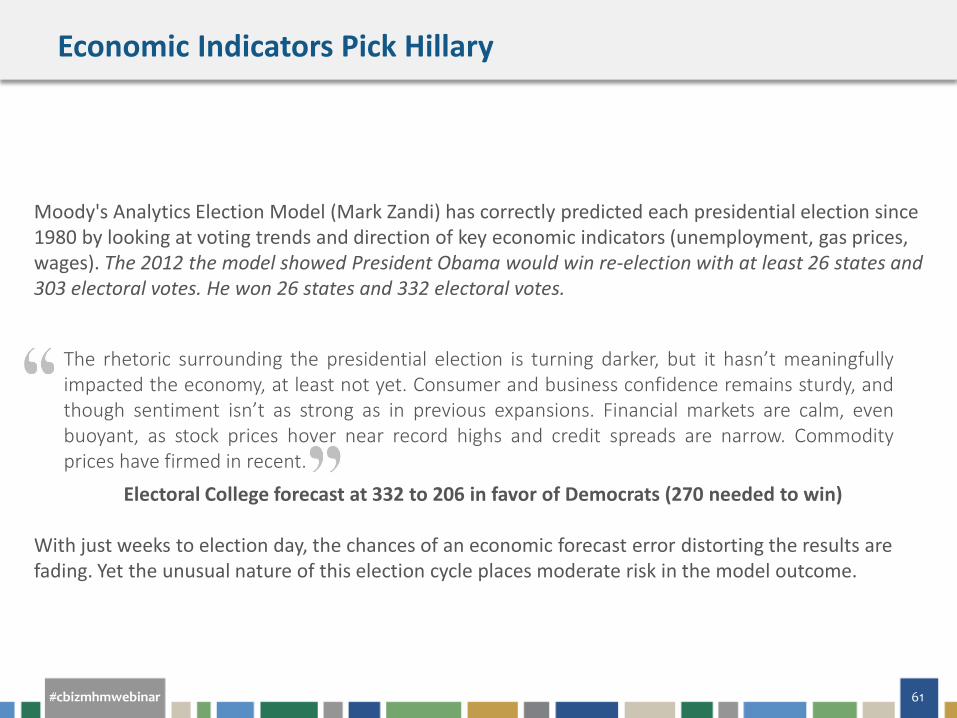

Moodys Analytics Election Model (Mark Zandi) has correctly predicted each presidential election since 1980 by looking at voting trends and direction of key economic indicators (unemployment gas prices wages) The 2012 the model showed President Obama would win re-election with at least 26 states and 303 electoral votes He won 26 states and 332 electoral votes

Electoral College forecast at 332 to 206 in favor of Democrats (270 needed to win) With just weeks to election day the chances of an economic forecast error distorting the results are fading Yet the unusual nature of this election cycle places moderate risk in the model outcome

The rhetoric surrounding the presidential election is turning darker but it hasnrsquot meaningfully impacted the economy at least not yet Consumer and business confidence remains sturdy and though sentiment isnrsquot as strong as in previous expansions Financial markets are calm even buoyant as stock prices hover near record highs and credit spreads are narrow Commodity prices have firmed in recent

Economic Indicators Pick Hillary

cbizmhmwebinar 62

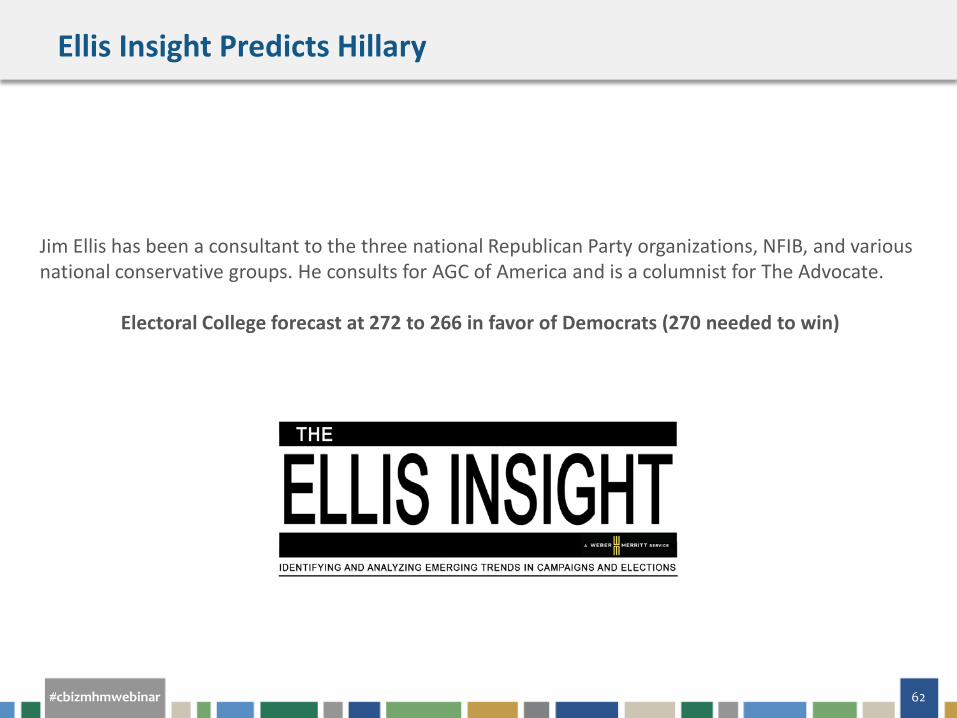

Jim Ellis has been a consultant to the three national Republican Party organizations NFIB and various national conservative groups He consults for AGC of America and is a columnist for The Advocate

Electoral College forecast at 272 to 266 in favor of Democrats (270 needed to win)

Ellis Insight Predicts Hillary

cbizmhmwebinar 63

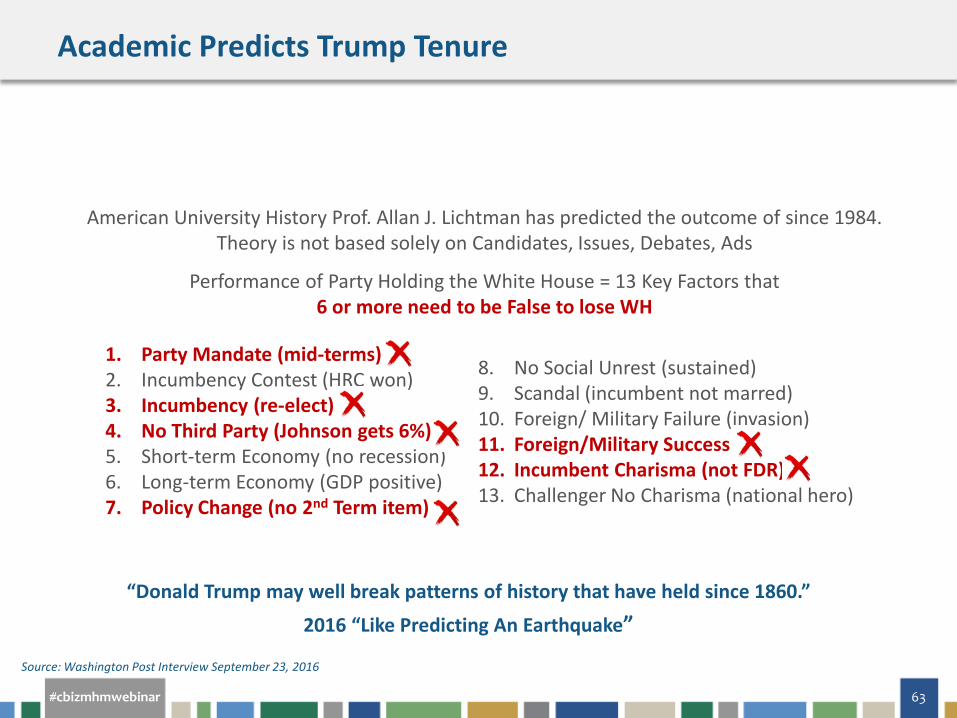

1 Party Mandate (mid-terms) 2 Incumbency Contest (HRC won) 3 Incumbency (re-elect) 4 No Third Party (Johnson gets 6) 5 Short-term Economy (no recession) 6 Long-term Economy (GDP positive) 7 Policy Change (no 2nd Term item)

American University History Prof Allan J Lichtman has predicted the outcome of since 1984 Theory is not based solely on Candidates Issues Debates Ads

Performance of Party Holding the White House = 13 Key Factors that 6 or more need to be False to lose WH

8 No Social Unrest (sustained) 9 Scandal (incumbent not marred) 10 Foreign Military Failure (invasion) 11 ForeignMilitary Success 12 Incumbent Charisma (not FDR) 13 Challenger No Charisma (national hero)

ldquoDonald Trump may well break patterns of history that have held since 1860rdquo

2016 ldquoLike Predicting An Earthquakerdquo

Source Washington Post Interview September 23 2016

Academic Predicts Trump Tenure

cbizmhmwebinar 64

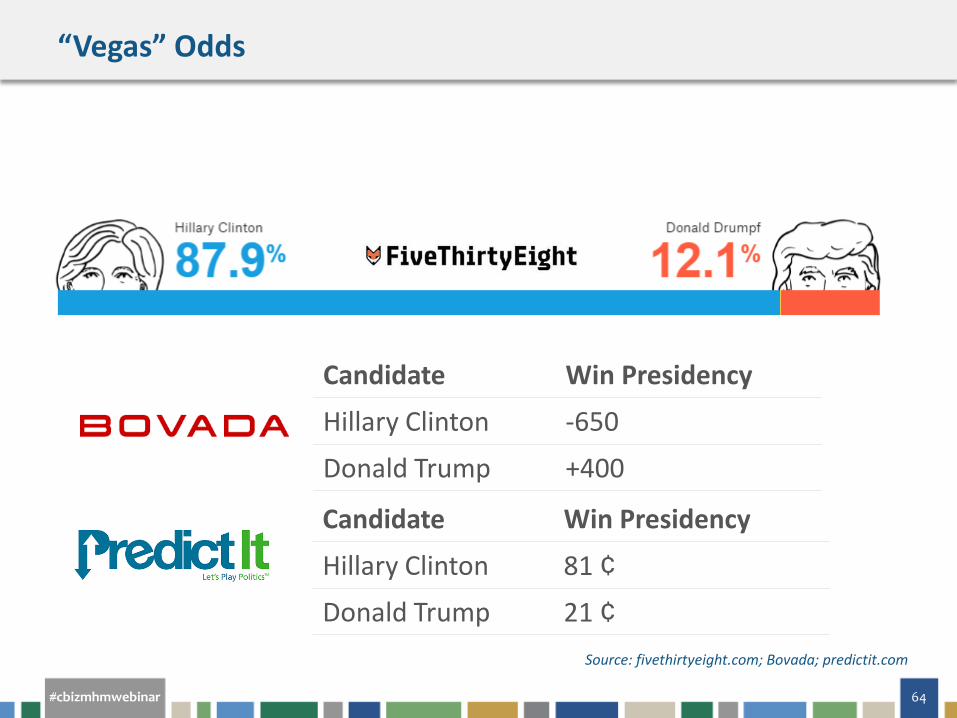

Source fivethirtyeightcom Bovada predictitcom

Candidate Win Presidency

Hillary Clinton -650

Donald Trump +400

Candidate Win Presidency

Hillary Clinton 81 cent

Donald Trump 21 cent

ldquoVegasrdquo Odds

cbizmhmwebinar 65

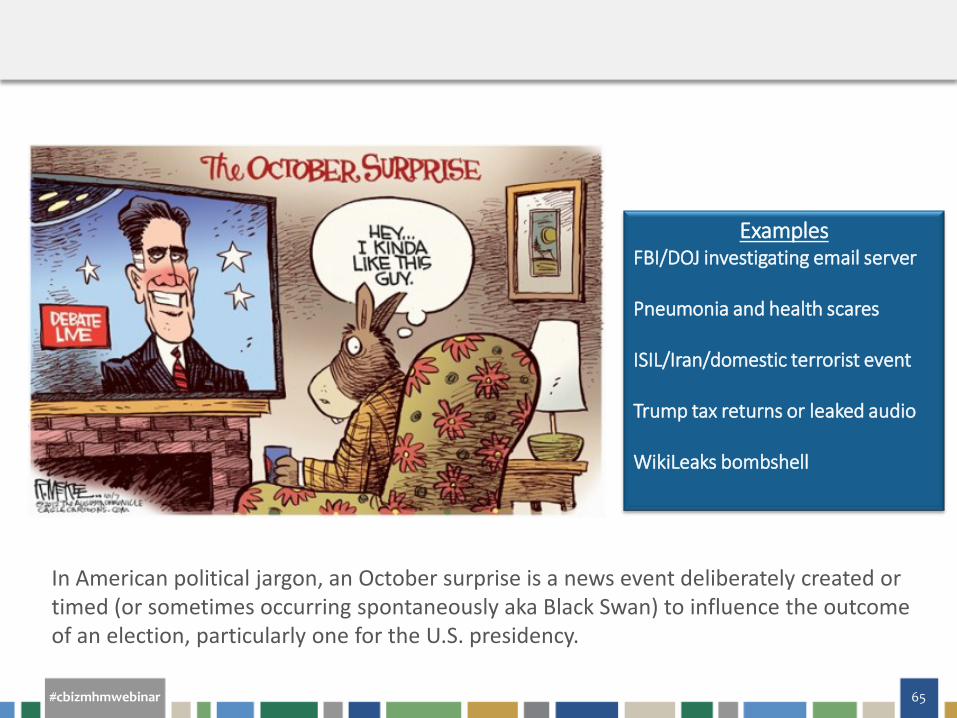

In American political jargon an October surprise is a news event deliberately created or timed (or sometimes occurring spontaneously aka Black Swan) to influence the outcome of an election particularly one for the US presidency

Examples FBIDOJ investigating email server Pneumonia and health scares ISILIrandomestic terrorist event Trump tax returns or leaked audio WikiLeaks bombshell

cbizmhmwebinar 66

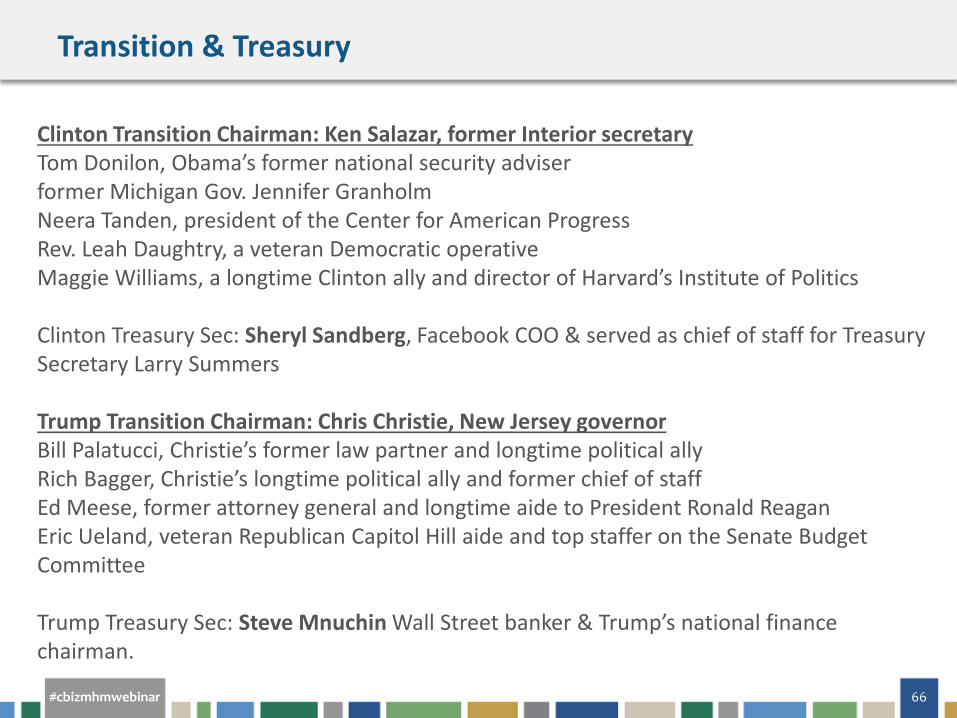

Clinton Transition Chairman Ken Salazar former Interior secretary Tom Donilon Obamarsquos former national security adviser former Michigan Gov Jennifer Granholm Neera Tanden president of the Center for American Progress Rev Leah Daughtry a veteran Democratic operative Maggie Williams a longtime Clinton ally and director of Harvardrsquos Institute of Politics Clinton Treasury Sec Sheryl Sandberg Facebook COO amp served as chief of staff for Treasury Secretary Larry Summers Trump Transition Chairman Chris Christie New Jersey governor Bill Palatucci Christiersquos former law partner and longtime political ally Rich Bagger Christiersquos longtime political ally and former chief of staff Ed Meese former attorney general and longtime aide to President Ronald Reagan Eric Ueland veteran Republican Capitol Hill aide and top staffer on the Senate Budget Committee Trump Treasury Sec Steve Mnuchin Wall Street banker amp Trumprsquos national finance chairman

Transition amp Treasury

cbizmhmwebinar 67

cbizmhmwebinar 68

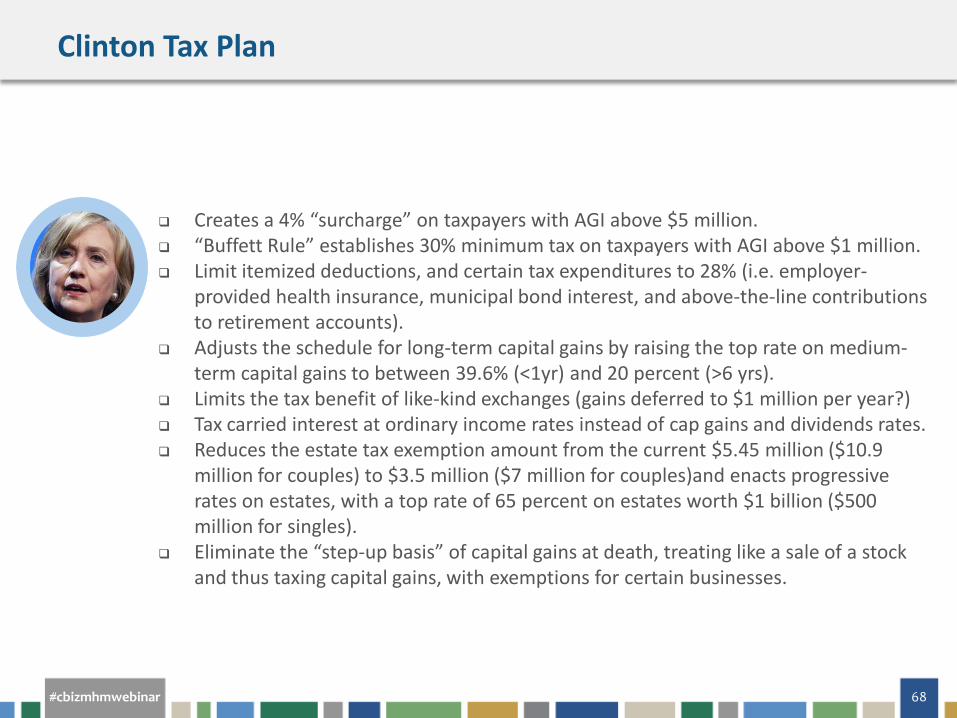

Creates a 4 ldquosurchargerdquo on taxpayers with AGI above $5 million ldquoBuffett Rulerdquo establishes 30 minimum tax on taxpayers with AGI above $1 million Limit itemized deductions and certain tax expenditures to 28 (ie employer-

provided health insurance municipal bond interest and above-the-line contributions to retirement accounts)

Adjusts the schedule for long-term capital gains by raising the top rate on medium-term capital gains to between 396 (lt1yr) and 20 percent (gt6 yrs)

Limits the tax benefit of like-kind exchanges (gains deferred to $1 million per year) Tax carried interest at ordinary income rates instead of cap gains and dividends rates Reduces the estate tax exemption amount from the current $545 million ($109

million for couples) to $35 million ($7 million for couples)and enacts progressive rates on estates with a top rate of 65 percent on estates worth $1 billion ($500 million for singles)

Eliminate the ldquostep-up basisrdquo of capital gains at death treating like a sale of a stock and thus taxing capital gains with exemptions for certain businesses

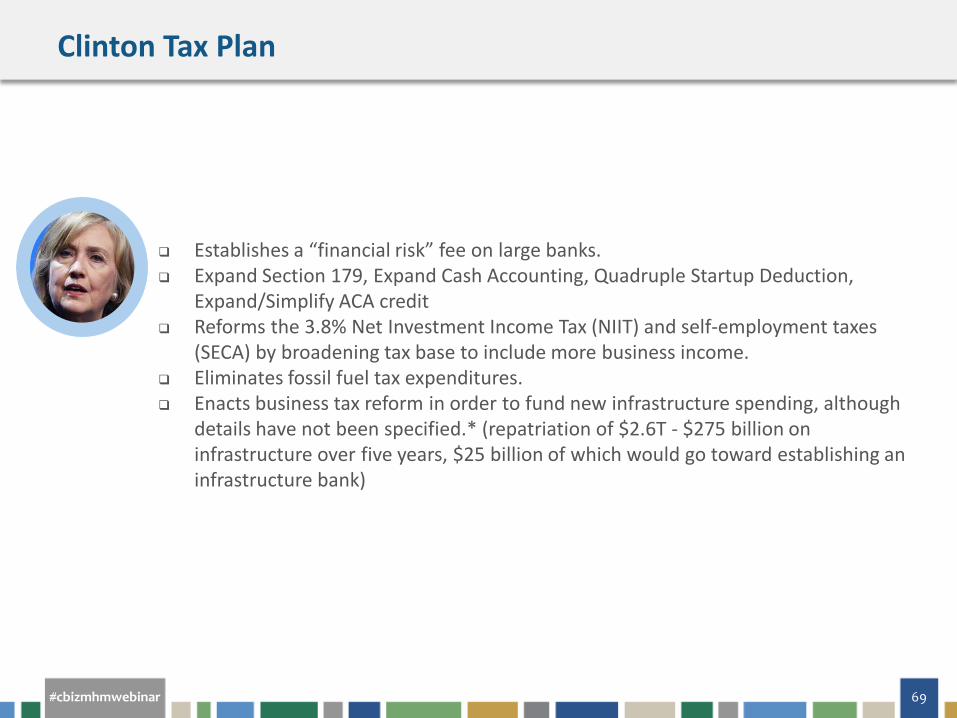

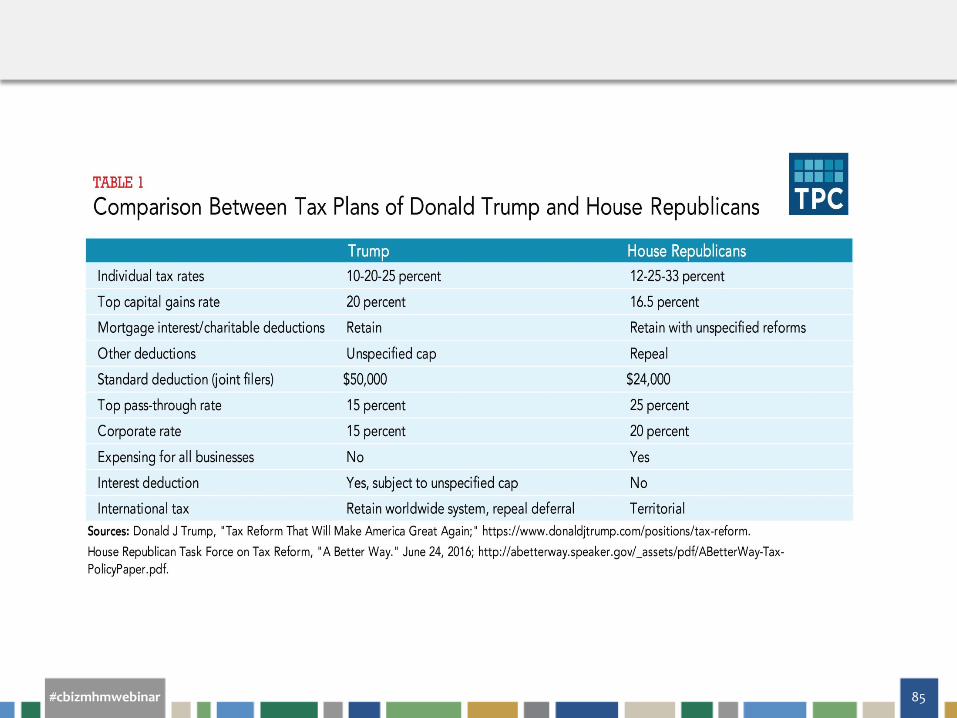

Clinton Tax Plan

cbizmhmwebinar 69

Establishes a ldquofinancial riskrdquo fee on large banks Expand Section 179 Expand Cash Accounting Quadruple Startup Deduction

ExpandSimplify ACA credit Reforms the 38 Net Investment Income Tax (NIIT) and self-employment taxes

(SECA) by broadening tax base to include more business income Eliminates fossil fuel tax expenditures Enacts business tax reform in order to fund new infrastructure spending although

details have not been specified (repatriation of $26T - $275 billion on infrastructure over five years $25 billion of which would go toward establishing an infrastructure bank)

Clinton Tax Plan

cbizmhmwebinar 70

Consolidates current 7 tax brackets into 3 with rates on ordinary income of 12 percent 25 percent and 33 percent

Adapts current rates for qualified capital gains and dividends to 3 new brackets Eliminates the Net Investment Income Tax Increases the standard deduction from $6300 to $15000 for singles and from

$12600 to $30000 for married couples filing jointly Eliminates the personal exemption and introduces other childcare-related tax

provisions Caps itemized deductions at $100000 for single filers and $200000 for married

couples filing jointly Taxes carried interest as ordinary income Eliminates the individual amp corporate alternative minimum tax Eliminates estate and gift taxes but disallows step-up in basis for estates over $10m

Trump Tax Plan

cbizmhmwebinar 71

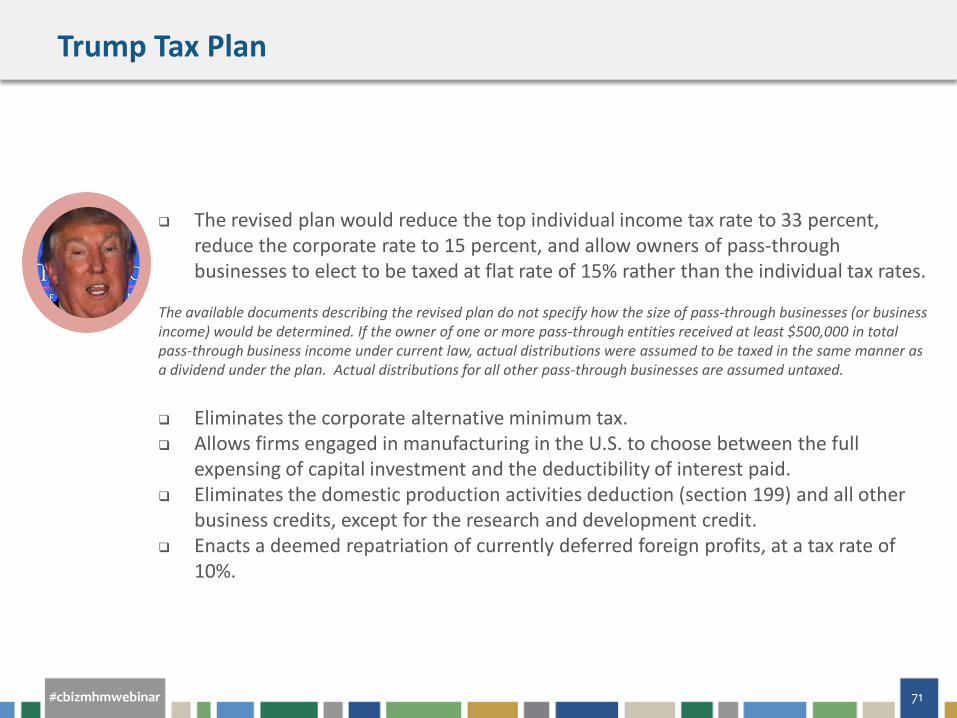

The revised plan would reduce the top individual income tax rate to 33 percent reduce the corporate rate to 15 percent and allow owners of pass-through businesses to elect to be taxed at flat rate of 15 rather than the individual tax rates

The available documents describing the revised plan do not specify how the size of pass-through businesses (or business income) would be determined If the owner of one or more pass-through entities received at least $500000 in total pass-through business income under current law actual distributions were assumed to be taxed in the same manner as a dividend under the plan Actual distributions for all other pass-through businesses are assumed untaxed

Eliminates the corporate alternative minimum tax Allows firms engaged in manufacturing in the US to choose between the full

expensing of capital investment and the deductibility of interest paid Eliminates the domestic production activities deduction (section 199) and all other

business credits except for the research and development credit Enacts a deemed repatriation of currently deferred foreign profits at a tax rate of

10

Trump Tax Plan

cbizmhmwebinar 72

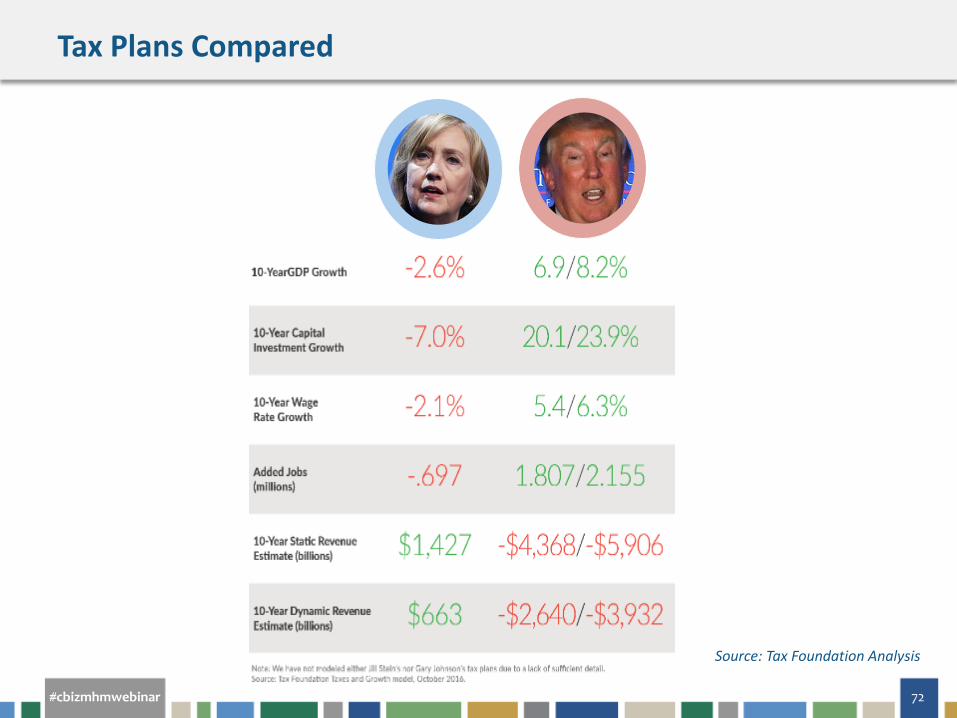

Source Tax Foundation Analysis

Tax Plans Compared

cbizmhmwebinar 73

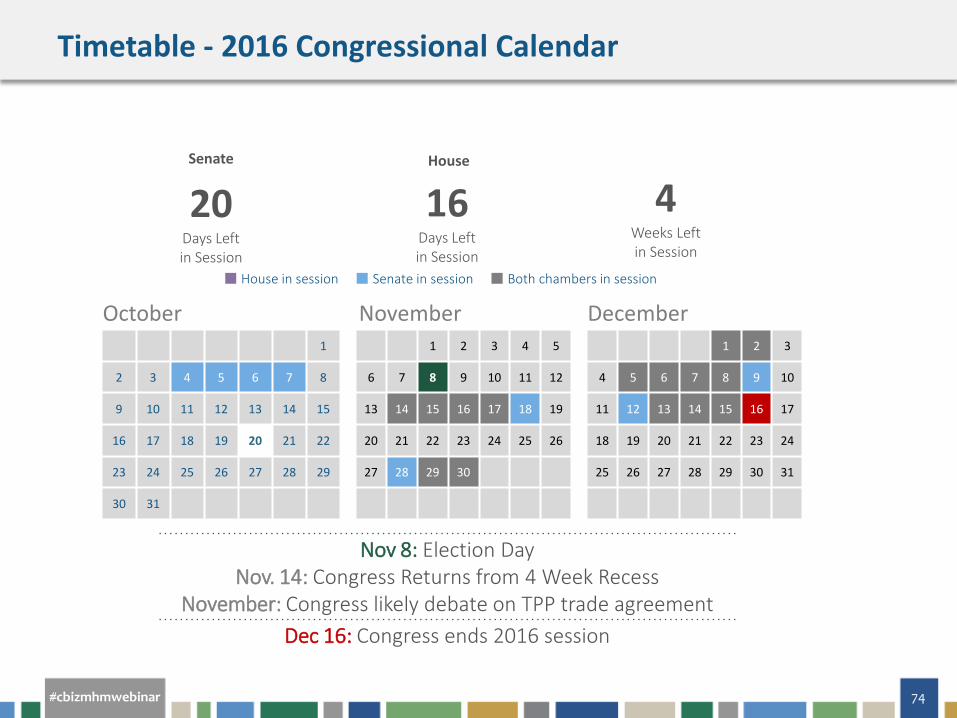

cbizmhmwebinar 74

House in session Senate in session Both chambers in session

1

2 3 4 5 6 7 8

9 10 11 12 13 14 15

16 17 18 19 20 21 22

23 24 25 26 27 28 29

30 31

1 2 3

4 5 6 7 8 9 10

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 27 28 29 30 31

1 2 3 4 5

6 7 8 9 10 11 12

13 14 15 16 17 18 19

20 21 22 23 24 25 26

27 28 29 30

October November December

Nov 8 Election Day Nov 14 Congress Returns from 4 Week Recess

November Congress likely debate on TPP trade agreement Dec 16 Congress ends 2016 session

House

16 Days Left in Session

Senate

20 Days Left in Session

4 Weeks Left in Session

Timetable - 2016 Congressional Calendar

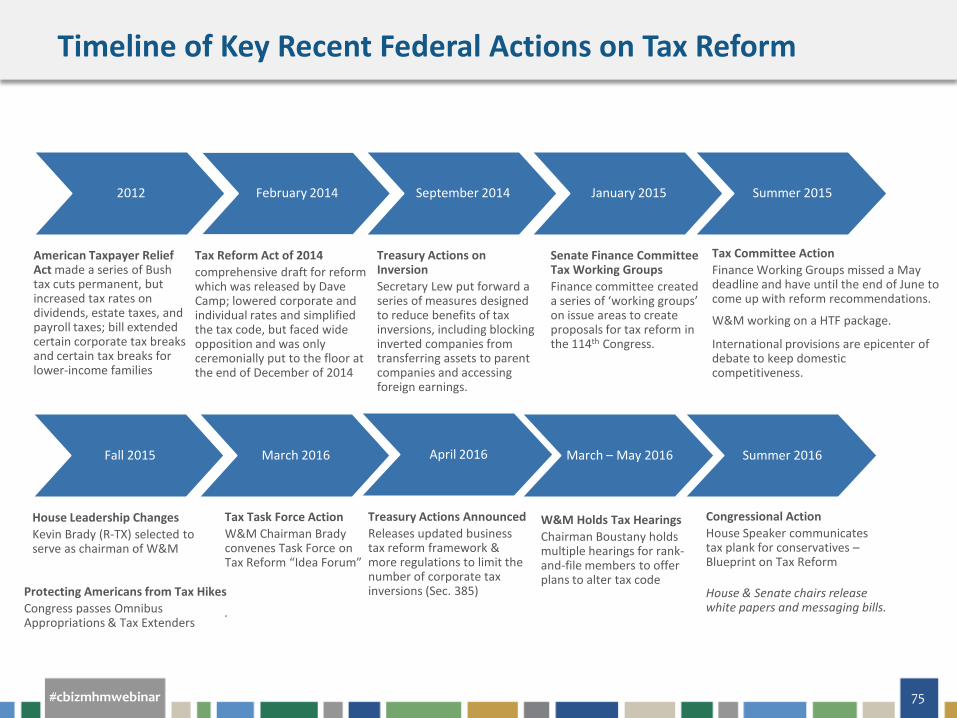

cbizmhmwebinar 75

2012

American Taxpayer Relief Act made a series of Bush tax cuts permanent but increased tax rates on dividends estate taxes and payroll taxes bill extended certain corporate tax breaks and certain tax breaks for lower-income families

February 2014

Tax Reform Act of 2014 comprehensive draft for reform which was released by Dave Camp lowered corporate and individual rates and simplified the tax code but faced wide opposition and was only ceremonially put to the floor at the end of December of 2014

September 2014

Treasury Actions on Inversion Secretary Lew put forward a series of measures designed to reduce benefits of tax inversions including blocking inverted companies from transferring assets to parent companies and accessing foreign earnings

January 2015

Senate Finance Committee Tax Working Groups Finance committee created a series of lsquoworking groupsrsquo on issue areas to create proposals for tax reform in the 114th Congress

Summer 2015

Tax Committee Action Finance Working Groups missed a May deadline and have until the end of June to come up with reform recommendations

WampM working on a HTF package

International provisions are epicenter of debate to keep domestic competitiveness

Fall 2015

House Leadership Changes Kevin Brady (R-TX) selected to serve as chairman of WampM

March 2016

Tax Task Force Action WampM Chairman Brady convenes Task Force on Tax Reform ldquoIdea Forumrdquo

March ndash May 2016

WampM Holds Tax Hearings Chairman Boustany holds multiple hearings for rank-and-file members to offer plans to alter tax code

April 2016

Congressional Action House Speaker communicates tax plank for conservatives ndash Blueprint on Tax Reform House amp Senate chairs release white papers and messaging bills

Summer 2016

Treasury Actions Announced Releases updated business tax reform framework amp more regulations to limit the number of corporate tax inversions (Sec 385) Protecting Americans from Tax Hikes

Congress passes Omnibus Appropriations amp Tax Extenders

Timeline of Key Recent Federal Actions on Tax Reform

cbizmhmwebinar 76

ndash Comprehensive Tax Reform ndash promote tax rate parity for all business types

ndash Conventional thinking ndash comprehensive reform will follow the 2016 elections ndash and at a minimum committee reports will serve as place markers as the tax reform debate continues in the next Congress with a new Administration

ndash Defend against adverse policy changes in the tax code for the remaining legislative weeks

ndash Vehicles for tax policy riders - discussions of attaching a tax title to any bills set for passage

ndash Tax Extenders ndash retroactively renewing expired provisions while abhorred is the new normal for extending expired provisions

ndash one (1) industry tax priority expires in 2016 amp four (4) in 2019

Areas of Focus

cbizmhmwebinar 77

Construction Industry Legislative Priorities ndash Extend the energy efficient commercial buildings deduction under Section 179D

(Expires this year) ndash Promote Private Activity Bonds for Social Infrastructure (new $5b allocation for

public buildings - HR 5361S 3177 the Public Buildings Renewal Act of 2016 ndash Reintroduction of American Job Builders Tax Reform Act (increase gross receipts

threshold for determining whether a small contractor may adopt an accounting method for reporting income from a construction contract other than the percentage of completion method)

Area of Focus

cbizmhmwebinar 78

Section 385 ndash Debt Recharacterization Rulemaking is complex and expands well beyond the Administrationrsquos attempt to restrict corporate ldquoinversionsrdquo and eliminate the tax consequences of ldquoearnings strippingrdquo Applies to larger companies (publicly traded or above $50 million in annual revenue or $100 million in total assets) and it sets a scary precedent Allows IRS wide discretion to characterize common business practices (like loans between related companies) as tax avoidance techniques and unilaterally recharacterize company debt as equity for federal tax purposes This recharacterization will likely force S-corps to reincorporate as C-corps or consolidate related S-corps It also imposes significant IRS reporting requirements meant to uncover offshore tax avoidance techniques even on companies that have no offshore holdings

Treasury Regulations

cbizmhmwebinar 79

Section 2704 ndash Valuation Discounts Proposed rule relating to the valuation of interests in businesses for estate gift and generation-skipping transfer (GST) tax purposes and the treatment of lapsing rights and restrictions on liquidation in determining the value of transferred interests under Section 2704 Treasury officials outlined in Priority Guidance in 2015 and they appear to be consistent with the Obama budget proposal offered in 2012 that was estimated to raise $18 billion over ten years The bottom line is that these broad regulations will force more companies to contend with complicated and costly estate taxes Broad new rule when coupled with the pending 385 regulations will limit the ability of companies to invest and create jobs AGC is preparing to submit comments before the November 2 deadline A public hearing on the proposed regulations has been scheduled for December 1

Treasury Regulations

cbizmhmwebinar 80

Section 199 ndash Substantial Renovation Issued August 2015 regulations involving the domestic production activities deduction (DPAD) under Section 199 addressing the definition of ldquosubstantial renovationrdquo in Prop Treas Reg sect1199-3(m)(5) which indicates that activities constitute substantial renovation where they would be a capitalizable improvement under Section 263(a) Over the years proposed and temporary regulations originally have intended to address a number of legislative changes to Section 199 However the IRS determined that it also needed to address a variety of other issues that have arisen over the years at IRS exam Appeals and in the courts The proposed definition of substantial renovation would lead to significant controversies between taxpayers and the IRS since it does not comport with the broad rules for determining construction activities and would not be administrable since it would require construction firms to step into the shoes of property owners and determine whether costs are capitalizable under Section 263(a) where the EampC taxpayers lack the information to make such determinations

Treasury Regulations

cbizmhmwebinar 81

Content

cbizmhmwebinar 82

Senator Orrin Hatch (R-UT) (Corp Integration thru Dividends Received Deduction) bull Allowing corporations to deduct the dividends they pay to shareholders it equalizes the treatment of debt and

equity financed investment it lowers the cost of capital and moves towards treating all business forms equally bull Some capital income could escape taxation completely with a dividend deduction system (no tax when tax-

exempt organization receive the dividend) bull A dividend deduction doesnrsquot address the high entity level tax that will remain at 35 percent Senator Ron Wyden (D-OR) (Depreciation Schedules) bull Replace the current MACRS and ADS system with the Accelerated Mass Asset Cost Recovery and Reinvestment

System (A-MACRRS) A-MACRRS would reduce the depreciation schedules to six asset ldquopoolsrdquo Assets would be assigned to each pool based on their current MACRS property class assignment Taxpayers would have to calculate depreciation EampP and AMT adjustments only once on a unified schedule

bull For firms that manage large bundles of assets this pooling system provides a simpler alternative to using the

current ldquomass asset accountsrdquo for depreciation which impose an additional tax on the disposition of assets

Senate Tax Plans

cbizmhmwebinar 83

5 major congressional tax plans

bull The Tax Reform Act of 2014 introduced by former Congressman Dave Camp (R-MI)

bull The Progressive Consumption Tax Act introduced by Senator Ben Cardin (D-MD)

bull The American Business Competitiveness Act introduced by Congressman Devin Nunes (R-CA)

bull The ldquoA Better Wayrdquo Tax Reform Blueprint issued by Speaker Paul Ryan (R-WI)

bull The ldquoSimplifying Americarsquos Tax Systemrdquo Plan issued by Congressman Jim Renacci (R-OH)

These tax plans will likely play a large role in framing the tax policy debate in 2017

House Tax Plans

cbizmhmwebinar 84

June 2016 - House GOP Taskforce on Tax Reform

bull Lower the corporate tax rate from 35 to 20 percent and ldquoterritorialrdquo system bull Allow individuals to deduct 50 of dividends capital gains and interest

received from stocks and mutual funds (6 125 165) bull 3 individual tax brackets 12 25 and 33 bull Eliminates all itemized deductions except the MID and charitable contribution

deduction bull 25 rate for small businesses and pass-through income bull Provide full and immediate business expensing bull Eliminates the interest deduction bull A move toward a consumption-based tax system bull Repatriation of foreign earnings at 875 bull Eliminates the Section 199 deduction bull Retain a RampD credit similar to form passed under PATH Act bull Blueprint does not include a value-added tax (VAT) a sales tax or any other

tax as an addition to the fundamental reforms bull Eliminates AMT amp Estate taxes

GOP Agenda for 2017

cbizmhmwebinar 85

cbizmhmwebinar 86

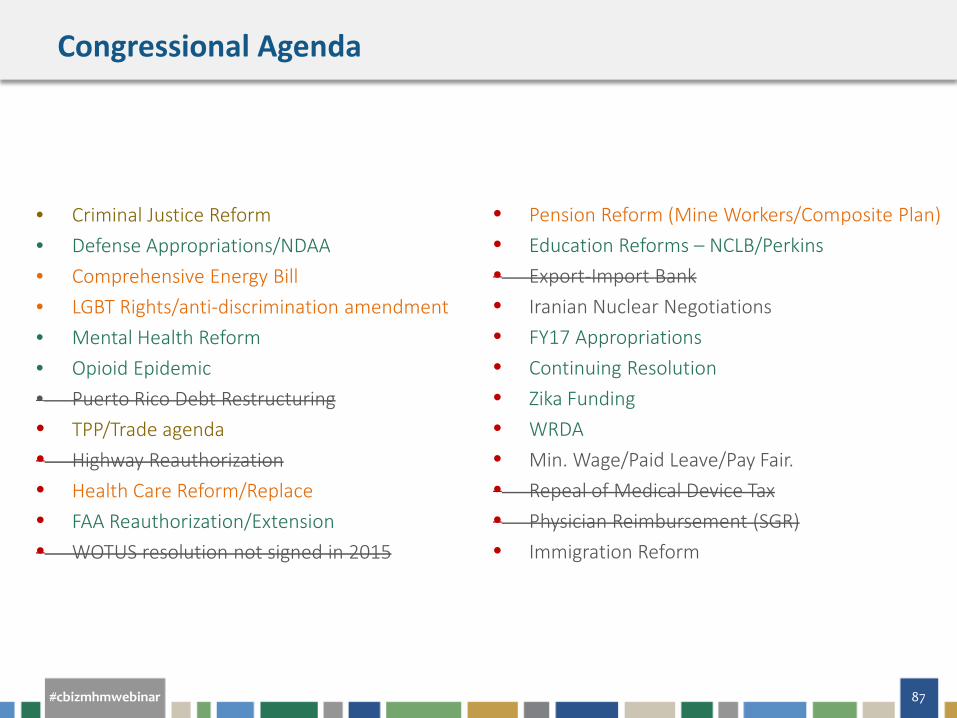

Laws Enacted Action but not Enactment Debate Beginning No Action Yet TRIA PACE Delay of HIT

Cadillac Med Device taxes (ACA Changes)

Tax Extenders Highway Reauth VA Construction Procurement

Reform FAA Authorization

bull PLAs bull Health Care bull Workforce bull WOTUS bull Civilian BRAC bull Regulatory Comments bull Block Unilateral

Policymaking bull Contractor Due Process bull Oversight of Regulations bull Water Resources

Development Act bull PAC Prior Approval

bull Highway Trust Fund

bull Multiemployer Pensions

bull Safety bull Immigration

bull NLRBDOLCard Check bull Keep Debt from Harming

Construction Climate bull Tax Reform and Entitlement

bull Criminal Justice Reform bull Defense AppropriationsNDAA bull Comprehensive Energy Bill bull LGBT Rightsanti-discrimination amendment bull Mental Health Reform bull Opioid Epidemic bull Puerto Rico Debt Restructuring bull TPPTrade agenda bull Highway Reauthorization bull Health Care ReformReplace bull FAA ReauthorizationExtension bull WOTUS resolution not signed in 2015

Whether providing consultation to key legislative decision-makers regarding ongoing legislation and regulatory language or helping construction firms to interpret Federal laws tax rules and GAAP standards participants in the Committee play a critical role in guiding firms and shaping the industry

Issues identified and addressed by AGCrsquos FIC have wide-ranging ramifications for the industry

bull FAS 150 bull FIN 46R bull 3 Percent Withholding

bull Leases Project bull Revenue Recognition bull Multiemployer Plan Disclosure

AGC Financial Issues Committee

The next Winter Meeting is scheduled for January 10-11 2017 at Trump National Doral National in Miami FL

meetingsagcorgfic

cbizmhmwebinar 89

CONSTRUCTIONVOTESCOM

bull One-stop-shop on election information bull Individuals can register to vote learn about candidates and find

their polling location bull Employers can download GOTV activity guide and sample

messages

cbizmhmwebinar 90

QUESTIONS

cbizmhmwebinar 91

If You Enjoyed This Webinarhellip

Upcoming Courses bull 1027 amp 112 Eye on Washington ndash Quarterly Business Tax Update

bull 112 How Changes to the Accounting for Consolidation Will Impact Private Company Financial Reporting

Recent Publications bull Highlights from the IRS Tax-Exempt and Government Entities Division 2017 Work

Plan

bull Understanding the Leasing Standard Sale and Leaseback and Other Types of Lease Transactions

bull Write-Downs and Other Impairment Considerations for Oil and Gas Companies

cbizmhmwebinar 92

Connect with Us

linkedincomcompany mayer-hoffman-mccann-pc

mhm_pc

youtubecom mayerhoffmanmccann

slidesharenetmhmpc

linkedincomcompany cbiz-mhm-llc

cbizmhm

youtubecom BizTipsVideos

slidesharenetCBIZInc

MHM CBIZ

cbizmhmwebinar 93

THANK YOU CBIZ amp Mayer Hoffman McCann PC cbizmhmwebinarscbizcom

Slide Number 1

About CBIZ amp MHM

About AGC of America

About ABC

Before We Get Startedhellip

CPE Credit

Disclaimer

Presenter ndash Brian Lenihan

Presenter ndash Chris Singerling

Moderators

Agenda

Admin amp Congress

Major Events in 2015

Major Events in 2016

Major Events in 2016 - YTD

Players

US Congress

Players - Key Decision-Makers

House Tax Committee

Slide Number 20

Slide Number 21

Slide Number 22

Slide Number 23

Senate Tax Committee

Who is in Driverrsquos Seat

Candidates

2016 Gubernatorial Races

2016 Gubernatorial Races

2016 Gubernatorial Races

2016 Senate Races

Straight vs Split Tickets

Senate Races Map

Top Races to Watch

Top Races to Watch

2018 Senate Races

2016 House Races

GOP Has More at Stake in 2016 But Arenrsquot Expected to See Big Losses

Slide Number 38

POTUS

Slide Number 40

Slide Number 41

Slide Number 42

Major 3rd Party Candidates

Do You Like Them

Use One Word

Use One Word

Presidential Polls

Debate Viewership

Views Foreshadow Turnout

Most Voters in History

Debates to Date

2008 Electoral College Map

2012 Electoral College Map

Prior to 1st Debate

Prior to Webinar

Florida Matters

Electoral Vote Ties

2016 Election May See New Swing States

Electoral College Votes

Modern History Predicts a Trump Presidency

Economic Indicators Pick Hillary

Ellis Insight Predicts Hillary

Academic Predicts Trump Tenure

ldquoVegasrdquo Odds

Slide Number 65

Transition amp Treasury

Slide Number 67

Clinton Tax Plan

Clinton Tax Plan

Trump Tax Plan

Trump Tax Plan

Tax Plans Compared

Slide Number 73

Timetable - 2016 Congressional Calendar

Timeline of Key Recent Federal Actions on Tax Reform

Areas of Focus

Area of Focus

Treasury Regulations

Treasury Regulations

Treasury Regulations

Content

Senate Tax Plans

House Tax Plans

GOP Agenda for 2017

Slide Number 85

Progress on Construction Agenda

Congressional Agenda

Slide Number 88

CONSTRUCTIONVOTESCOM

Slide Number 90

If You Enjoyed This Webinarhellip

Connect with Us

Slide Number 93

Obama

Romney

Column2

Column1

332

206

To update the chart enter data into this table The data is automatically saved in the chart

332

206

Obama

McCain

Column2

Column1

365

173

To update the chart enter data into this table The data is automatically saved in the chart

365

173

Lean Democrat

Toss-Up

Lean Republican

Democrats

-3

-3

0

Republicans

4

16

14

Lean Democrat

Lean Democrat

Toss-Up

Toss-Up

Lean Republican

Lean Republican

cbizmhmwebinar 2

About CBIZ amp MHM

bull Together CBIZ amp MHM are a Top Ten accounting provider bull Offices in most major markets bull Tax audit and attest and advisory services bull Over 2900 professionals nationwide

A member of Kreston International A global network of independent

accounting firms

MHM (Mayer Hoffman McCann PC) is an independent CPA firm that provides audit review and attest services and works closely with CBIZ a business consulting tax and financial services provider CBIZ and MHM are members of Kreston International Limited a global network of independent accounting firms

cbizmhmwebinar 3

About AGC of America

The Associated General Contractors of America (AGC) is the leading association for the construction industry

AGC represents more than 26000 firms including over 6500 of Americarsquos leading general contractors and over 9000 specialty-contracting firms

More than 10500 service providers and suppliers are also associated with AGC all through a nationwide network of chapters

cbizmhmwebinar 4

About ABC

Associated Builders and Contractors (ABC) is a national construction industry trade association representing nearly 21000 chapter members

Founded on the merit shop philosophy ABC and its 70 chapters help members develop people win work and deliver that work safely ethically profitably and for the betterment of the communities in which ABC and its members work

ABCs membership represents all specialties within the US construction industry and is comprised primarily of firms that perform work in the industrial and commercial sectors

cbizmhmwebinar 5

Before We Get Startedhellip

bull To view this webinar in full screen mode click on view options in the upper right hand corner

bull Click the Support tab for technical assistance

bull If you have a question during the presentation please use the QampA feature at the bottom of your screen

cbizmhmwebinar 6

CPE Credit

This webinar is eligible for CPE credit To receive credit you will need to answer periodic participation markers throughout the webinar External participants will receive their CPE certificate via email immediately following the webinar

cbizmhmwebinar 7

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation

Please contact your service provider to further discuss the impact on your business

cbizmhmwebinar 8

Presenter ndash Brian Lenihan

Brian is a government affairs professional with over 13 years of experience As AGCrsquos Director

of Tax amp Fiscal Affairs he oversees the development and advocacy of the industryrsquos positions

on tax and accounting issues in consultation with AGCrsquos CFO and CPA membership owners

and other AGC subject matter experts

Previously as a senior aide for a member of the House Ways amp Means Committee Brian

formulated and executed a legislative agenda focusing on tax and health issues In previous

positions he represented a number of clients before Congress including top publically-traded

companies municipalities defense contractors development authorities small businesses and

non-profit organizations

Brian has worked on over 30 House and Senate campaigns since 2004 A core team member

recruiting managing and coordinating over 150 volunteers each cycle he has fundraised and

implemented six-figure campaign budgets for get-out-the-vote ground operations in the

perennial battleground state of Ohio

Brian is involved with over 15 business coalitions focused on tax health pension and employer

issues Brian is a frequent speaker and panelist for tax meetings and briefings in DC and

around the country Brian earned a Political Science degree from the

University of Central Florida and resides with his wife amp children in

Virginia

cbizmhmwebinar 9

Presenter ndash Chris Singerling

Chris is senior director of political affairs at Associated Builders and

Contractors Inc in Washington DC In this capacity he supervises plans

and directs ABCrsquos political action committee (ABC PAC) its issue

advocacy arm the Free Enterprise Alliance and all other national political

efforts

Mr Singerling brings to ABC more than 12 years of experience on Capitol

Hill

Prior to joining ABC he served in a variety of positions for five different

Members of Congress most recently as political director for former

Congressman John Boehner (R-Ohio)

cbizmhmwebinar 10

Moderators

ANTHONY HAKES National Construction Industry

Practice Group Leader CBIZ amp MHM

TONY STAGLIANO National Construction Industry Practice

Group Member CBIZ amp MHM

cbizmhmwebinar 11

Agenda

Year to Date

02

01

03

04

Players in 2016

Candidates

POTUS and Veep

05 Timetable

06 Content

07 Strategy

08 Outlook

cbizmhmwebinar 12

White House priorities Regulations bull Section 385 ndash related-party debt as equity (inversions) bull Section 2704 ndash Minority Valuation Discounts (estate tax) bull Section 199 ndash substantial renovation

Congress passed bull Significant Medicare overhaul (Doc Fix) bull Overhaul of domestic surveillance programs (FISA) bull Fast-track trade authority coveted by GOP leadership and President Obama bull 6-year Highway Authorization (3 years of funding in FAST Act) bull 2-year budget deal amp various tax provisions made permanent (PATH Act) bull A bill to strengthen the Miscellaneous Tariff Bill (MTB) process bull Puerto Rico Oversight and Economic Stability Act (PR Default Relief)

Admin amp Congress

cbizmhmwebinar 13

bull July 30 - Treasury announced extraordinary measures to avoid govrsquot default

bull September 25 - Speaker Boehner announced that he will resign from his position

bull October 29 - WampM Chairman Paul Ryan (R-WI) is elected Speaker of the House

bull November 2 - President signed budget package (includes debt limit suspension)

bull November 5 - Kevin Brady (R-TX) selected to serve as chairman of WampM

bull November 19 - Treasury announced additional actions to curb corporate inversions

bull December 3 - Congress approved 6-year highway authorization (FAST Act)

bull December 18 - Govrsquot funded via Omnibus Appropriations amp Tax Extenders (PATH Act)

Major Events in 2015

cbizmhmwebinar 14

bull January 12 - President Obamarsquos 8th amp final State of the Union Address

bull January 14 amp 17 - First debates of 2016 for Republicans (6th) and Democrats (4th)

bull February 9 - President released FY17 budget

bull March 1 - Super Tuesday Clinton amp Trump both won 7 of 11 states

bull March 10 - 12th and final GOP debate (Foxrsquos debate canceled Trump and Kasich back out)

bull March 16 - Obama nominated Merrick Garland to fill the Supreme Court (Scalia passed 213)

bull April 4 - Treasury released updated tax reform framework amp issued 385 regulations

bull April 14 - 10th and final Democratic primary debate

Major Events in 2016

cbizmhmwebinar 15

bull May 3 - Indiana GOP Primary solidifies Trump as presumptive GOP presidential nominee

bull May 17 amp 24 - Finance hearings on chairmanrsquos Corporate Integration proposal

bull May 25 - WampM hearing on need for tax reform

bull May 26 - Trump officially surpassed the 1237 delegates required to secure nomination

bull June 7 - Clinton secured the nomination during final Democratic primaries

bull June 24 - House Speaker released tax blueprint (sixth plank of GOP platform)

bull July 15 - Congressional Summer Recess and Major Party Conventions held (OH amp PA)

bull August 2 - Treasury released NPRM Section 2704 on valuation discounts

bull November 8 - Election day

Major Events in 2016 - YTD

cbizmhmwebinar 16

Players

cbizmhmwebinar 17

bull Republicans won their largest majority since 1928 when the party won 270 bull Vacancies ndash Rep Mark Takai (HI) passed away resigned Reps Chaka Fattah (IL) amp Ed Whitfield (KY) bull Republicans have a 4 seat majority in the Senate

2

3

US Congress

cbizmhmwebinar 18

The Chairmen

Kevin Brady (R-TX) Elected 1996 10th term

Secretary Jack Lew Assumed 2013

Asst Secretary Mark Mazur Assumed 2010

The Administration

Orrin Hatch (R-UT) Elected 1977 6th term

Players - Key Decision-Makers

cbizmhmwebinar 19

Current WampM Members

Ranking Member Levin (D-MI) Charlie Rangel (D-NY) Jim McDermott (D-WA) John Lewis (D-GA) Richard Neal (D-MA) Xavier Becerra (D-CA) Lloyd Doggett (D-TX) Mike Thompson (D-CA) John Larson (D-CT) Earl Blumenauer (D-OR) Ron Kind (D-WI) Bill Pascrell (D-NJ) Joseph Crowley (D-NY) Danny Davis (D-IL) Linda Saacutenchez (D-CA)

Dynamics amp Issues in House Ways amp Means Committee Tax Policy

bull Released a ldquoblueprintrdquo for reform in lead up to GOP Convention

bull Held 5 meetings on need for reforms and approving misc bills Health Reform

bull Congress passed a comprehensive package in December 2015 Highway Funding

bull Chairman specifically called out that a HTF fix will not be pursued

Diane Black (R-TN) Tom Reed (R-NY) Todd Young (R-IN) Mike Kelly (R-PA) Jim Renacci (R-OH) George Holding (R-NC) Kristi Noem (R-SD) Pat Meehan (R-PA) Jason Smith (R-MO) Bob Dold (R-IL) Tom Rice (R-SC)

Chairman Kevin Brady (R-TX) Sam Johnson (R-TX) Devin Nunes (R-CA) Pat Tiberi (R-OH) Dave Reichert (R-WA) Charles Boustany (R-LA) Peter Roskam (R-IL) Tom Price (R-GA) Vern Buchanan (R-FL) Adrian Smith (R-NE) Lynn Jenkins (R-KS) Erik Paulsen (R-MN) Kenny Marchant (R-TX)

Two Retiring after 2015 Two Running for Senate One in Competitive Race

House Tax Committee

cbizmhmwebinar 20

Politically Endangered ndash eked out a victory in March primary but he is likely to have a target on his back for years to come Opponent held Brady to 53 of the vote one of the lowest re-election totals in his 18 year career

Seventh Texan as Chairman ndash Won out over Pat Tiberi (OH) in 2015 to become 7th Texan with a gavel

Ch a i r m a n K ev in Br a d y

cbizmhmwebinar 21

Unlikely to Regain Gavel ndash Chairman 2010-2011

At 84 likely to announce retirement next Congress

R a n k in g M em b er S a n d y L ev in

cbizmhmwebinar 22

Senate Flips or WH remains Dem ndash At 82 likely to announce retirement next year Next in line Sen Charles Grassley (IA) previously was a chair and currently chairman of the Judiciary Committee Heir apparent is Sen Mike Crapo (ID)

Ch a i r m a n Or r in H a tc h

cbizmhmwebinar 23

Senate Flips ndash regains gavel lost in 2015 Has a moderate record with construction industry and businesses groups Next in line Sen Charles Schumer will be Democratic Leader in next Congress (an Ex officio member and thus a vacancy will be filled on the committee)

R a n k in g M em b er R on Wyd en

cbizmhmwebinar 24

Tax Reform and Inversions

bull Continue to address inversions comprehensive reform remains unlikely in the short term due to brevity of calendar

bull Working Groups formed in 2015 to propose recommendations (eg 2013 WampM groups)

bull Dividends Received Deduction ndash Integration proposal

Highway Trust Fund bull No plans to address funding shortfall

IRS Oversight

bull Advancing proposals to protect taxpayers from fraud and identity theft

Obamacare

bull CMS ldquo Part B Drug Payment Modelrdquo

Trade amp Trans-Pacific Partnership

bull Administration must submit a description of changes in law

bull Chairman Orrin Hatch (R-UT) dagger bull Chuck Grassley (R-IA) bull Mike Crapo (R-ID) bull Pat Roberts (R-KS) bull Mike Enzi (R-WY) bull John Cornyn (R-TX) bull John Thune (R-SD) bull Richard Burr (R-NC) bull Johnny Isakson (R-GA) bull Rob Portman (R-OH) bull Pat Toomey (R-PA) bull Dan Coats (R-IN) bull Dean Heller (R-NV) dagger bull Tim Scott (R-SC)

bull Ranking Member Ron Wyden (R-OR) bull Chuck Schumer (D-NY) bull Debbie Stabenow (R-MI) dagger bull Maria Cantwell (D-WA) dagger bull Bill Nelson (D-FL) dagger bull Bob Menendez (D-NJ) dagger bull Tom Carper (D-DE) dagger bull Ben Cardin (D-MD) dagger bull Sherrod Brown (D-OH) dagger bull Michael Bennet (D-CO) bull Bob Casey (D-PA) dagger bull Mark Warner (D-VA)

One Retiring after 2015 11 2016 re-election dagger 2017 re-elect

Dynamics amp Issues in Senate Finance Committee

Senate Tax Committee

cbizmhmwebinar 25

Presidential Candidates Clinton amp Trump have set tone for down ballot races

President ObamaAdministration IRS does not intend to put out any ldquosignificantrdquo regulations past Labor Day

Speaker of the House Rep Paul Ryan (WI) is GOP policy standard bearer

Conservative ldquoHouse Pestsrdquo 25 ndash 41 House Republicans seeking to push policy riders on spending bills amp punish IRS

Committee Chairs Bottom-up process is a double edge sword ndash more input and more expectations

Summary bull 12 seats are up for election in 2016 bull 3 incumbent Democrats and

2incumbent Republicans are running for re-election

bull There are seven open seats ndash bull 5 formerly Democrat bull 2 formerly Republican

Open Democrat Seat Incumbent Democrat Seeking Re-election Open Republican Seat Incumbent Republican Seeking Re-election

OH

WV VA

PA

NY

ME

NC

SC

GA

TN

KY

IN

MI

WI

MN

IL

LA

TX

OK

ID

NV

OR

WA

CA

AZ NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS

AL

NE

KS

AK

2016 Gubernatorial Races

cbizmhmwebinar 28

Two Key Republican-Held Gubernatorial Seats Democrats are Targeting

North Carolina

bull Incumbent Gov Pat McCrory (R) has been affected by low polling and backlash from the ldquobathroom billrdquo

bull Both public and private polls show McCroryrsquos opponent Attorney General Roy Cooper (D) holding a narrow lead

bull North Carolina is also a key battleground state in the presidential election where Trump and Clinton will both be highly visible This may cause Trumprsquos negative down-ballot effect to impact McCrory

bull The NC bill regarding transgender bathroom legislation will be a key topic in this race

Indiana

bull Indiana polling shows former state House Speaker John Gregg (D) running relatively even with Lt Gov Eric Holcomb (R)

bull Holcomb was picked late in the election cycle because incumbent Mike Pence was tapped to run as Donald Trumprsquos vice presidential candidate

bull Pence leaves the office amid criticism from equal rights activists for his controversial religious liberty bill and a low approval rating

bull Democrats will likely try to associate Holcomb as much as possible with the Pence administration

2016 Gubernatorial Races

cbizmhmwebinar 29

Two Key Democrat-Held Gubernatorial Seats Republicans are Targeting

Missouri

bull Gov Jay Nixon (D) is retiring from his position and the GOP sees his seat as the primary pick-up opportunity among gubernatorial races

bull Polls show a tight race between Attorney General Chris Koster (D) and Eric Grietens (R) a veteran of the wars in Iraq and Afganistan

bull Koster is a Republican-turned-Democrat campaigning with $11 million in the bank

bull Grietens is a newcomer to politics but beat three more experienced candidates in his run for the Republican nomination

West Virginia

bull West Virginia was initially a likely pick-up opportunity for the GOP but state Senate President Bill Colersquos (R) chances have been hurt by a fight over state budget problems

bull Meanwhile billionaire Jim Justice (D) has a slight lead in the polls

bull Republicans seem to be moving their focus to other races as Colersquos outlook looks grim in this election

2016 Gubernatorial Races

cbizmhmwebinar 30

Dynamics of the 2016 Senate

bull Republicans took control in 2014 and have more seats at risk from the 2010 class

bull Senate Democrats are defending 10 seats vs 24 for Republicans

bull 7 Republican Senate seats and only 2 Democratic Seats in play

bull Democrats need to net 4 (w VP Kaine) or 5 seats (w VP Pence) to retake the Senate

bull During Presidential years demographics of ldquolikely votersrdquo heavily favors Democrats

bull The opposite is true during mid-term elections when Republicans tend to be favored

bull 2018 fares better for GOP Senate Races ndash when Dems have 23 seats up vs 10 GOP

2016 Senate Races

cbizmhmwebinar 31

Since the 1970s the share of voters who split their tickets mdashsupporting one party for president and the other in Senate racesmdash has steadily declined to 23 on average during the 1980s 16 across Clintonrsquos two races 13 in 2008 and just 10 in 2012 The goal is no longer to identify and persuade those in the squishy middle of the ideological spectrum to split their tickets Instead campaigns try to find sporadic voters who if they could be persuaded to go to the polls would vote straight down the ticket ndash GET OUT THE VOTE Overall just 8 of voters in the 34 states with Senate races say they will vote for either Clinton or Trump for president and a Senate candidate from the opposing party 4 will vote for a Democrat or Republican for president and a House candidate from other party

Source Pew Research Center Survey 927- 1010 National Election Studies analyzed by Emory Univ Prof Abramowitz

Straight vs Split Tickets

cbizmhmwebinar 32

Solid Democrat Likely Democrat Lean Democrat Toss Up Lean Republican Likely Republican Solid Republican No Senate Race

NY

SC

KY

LA

OK

ID

OR

WA

ND

SD

UT

AR

AL

KS

HI

VT

MD

CT

GA

CA

IA

AK

MI

MN

TX

NM

WY

MT

NE

WV VA

TN

MS

ME

RI

MA

NJ

DE OH

PA

IN

WI

IL NV

FL

NH

NC

MO

AZ

CO

Senate Races Map

cbizmhmwebinar 33

Top Races to Watch

Republican running for reelection

Toss Up Race

Democrat running for reelection

Likely to switch to Democrat seat

OH NV

CO

FL

NH

FL Sen Marco Rubio announced re-election before June filing deadline being attacked on voting record Rep Patrick Murphy is hurting from resume embellishments as CPA amp police record +36+47 LEAN GOP

PA Sen Pat Toomey (R) may be too conservative in a presidential year but has worked to moderate his record Dems got a boost when Fmr chief of staff Katie McGinty (D) won primary Turnout in Philadelphia area is deciding factor +67+04 TILT DEM

WI Sen Ron Johnson (R) is a relatively unknown businessman in his home state and may be too conservative for a presidential-year Dems are hoping that Fmr Sen Russ Feingold (D) has a strong showing LEAN DEM (FLIP)

IL Sen Mark Kirk (R) won a close in 2010 and voted against defunding Planned Parenthood and in favor of gun-sale restriction Rep Tammy Duckworth is a combat-wounded helicopter pilot and former VA official under Obama LIKELY DEM (FLIP)

AZ

SAFE LIKELY LEAN TILT

TOSS UP

MO

NC

WI

IL

PA

IN