webinar slides: new partnership audit rules - planning ideas and practical observations

TRANSCRIPT

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

New Partnership Audit Rules: Planning Ideas and Practical Observations Nate Smith February 8 and 15, 2017

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent

accounting firms

MHM (Mayer Hoffman McCann P.C.) is an independent CPA firm that provides audit, review and attest services, and works closely with CBIZ, a business consulting, tax and financial services provider. CBIZ and MHM are members of Kreston International Limited, a global network of independent accounting firms.

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

CBIZ & MHM 6

Nathan Smith is a Director in the CBIZ National Tax Office, bringing over

19 years of experience in public accounting to provide technical support

and strategic solutions for the firm’s tax practice. Nathan leads the

development of practice aids and tactical approaches used in

responding to industry and Federal tax developments in a variety of

subject matter areas. Nathan also consults nationally to facilitate

delivery of client service opportunities and solutions, contributes as an

author and editor to the firm's tax thought leadership publications and

assists with the development and implementation of national tax

policies and procedures.

727.572.1400 • [email protected]

Nathan Smith, CPA Director

Presenter

#cbizmhmwebinar 7

Topics for Today

• Overview of New Partnership Audit Rules • Example 1: Net increase from exam; one partner leaves • Thoughts About Revised Partnership and LLC Member

Agreements • Example 2: Net increase from exam; prior distribution gain • Example 3: Re-allocation from exam; decrease partner

leaves • Example 4: Re-allocation from exam; increase partner

leaves

#cbizmhmwebinar 8

Overview of New Rules

#cbizmhmwebinar 9

Overview of New Partnership Audit Rules

• IRS facing significant challenges in conducting audits under existing TEFRA rules • Identification of Tax Matters Partner • Administration of required notice and participation rights • Processing of examination adjustments for ultimate partners

• Bipartisan Budget Act of 2015 (“BBA”) signed into law on November 2, 2015

• New audit rules generally apply to partnership tax years beginning on or after December 31, 2017

• Many strategies to consider under new rules; specific concerns of partners effectively require every partnership and LLC to amend its partnership/member agreement

#cbizmhmwebinar 10

Overview of New Partnership Audit Rules

• New rules fundamentally change the IRS examination and tax collection process for partnerships • Underpaid tax, interest and penalties resulting from

unfavorable exam adjustments (“imputed underpayment”) assessed against and collected from partnership itself

• Payable by partnership during the “adjustment year,” which is the year when “final partnership adjustment” IRS notice is mailed; reported on partnership’s adjustment year tax filing

• Exam adjustments not resulting in imputed underpayment (favorable adjustments) do not produce a refund; instead are reported as income adjustments in partnership’s adjustment year tax filing

#cbizmhmwebinar 11

Overview of New Partnership Audit Rules

• Eligible partnerships provided with annual election to “opt out” of new rules. Eligible partnerships: • Cannot issue more than 100 “statements” (Schedules K-1) • Cannot have a partner that is a partnership or a trust • Under proposed regulations, cannot have a partner that is a

disregarded entity, nominee, or non-partner’s estate • Can have foreign partners, if such partners have TIN, and

would be treated as C Corporations if they were domestic • Under proposed regulations, shareholders of S corporation

partners count toward 100-statement limit

Does the partnership always want to opt out? How will it ensure ineligible partners are not admitted?

#cbizmhmwebinar 12

Overview of New Partnership Audit Rules

• Tax Matters Partner eliminated • Partnership Representative (“PR”) installed and given

exclusive authority to bind the partnership and its partners to strategies employed during audit • PR can be any person (partner or non-partner), as long as

the person has a “substantial presence in the United States” • Partners have no rights to participate in audit, receive notice

of key audit stages, or contest audit results • Under proposed regulations, PR can be entity, as long as

U.S. individual also is identified to act for entity • IRS can name a PR if a designation is not in effect

Do partners want separately-negotiated rights to notification and participation?

#cbizmhmwebinar 13

Overview of New Partnership Audit Rules

• An imputed underpayment is calculated by netting exam adjustments of similar character, and multiplying the netted positive amounts by the highest rate of tax in effect (for any type of taxpayer) for the year to which the adjustment relates • Adjustments to partnership’s credit items then increase or

decrease the tentative calculation • Remember, netted non-positive amounts reported as

income adjustments in partnership’s adjustment year tax filing

• Under proposed regulations, decrease side of reallocations and recharacterizations do not net; treated as separate non-positive adjustments (picked up in adjustment year)

#cbizmhmwebinar 14

Overview of New Partnership Audit Rules

• PR can request alternative to the default imputed underpayment calculation, using “modification” procedures, or using a “push-out” election • Modification procedures and push-out elections operate to

reduce or eliminate a portion or all of the partnership’s liability for an imputed underpayment

• The PR is the only person with IRS authority to choose a modification procedure or to make a push-out election

• Proposed regulations provide for the ability to bifurcate a general imputed underpayment into multiple specific imputed underpayments, with any modification procedure or push-out election generally available to each

Will the PR be obligated to choose a procedure that benefits certain partners?

#cbizmhmwebinar 15

Overview of New Partnership Audit Rules

• Modification procedures: Amended returns • Amended returns for “reviewed year” (the year pertaining

to the exam adjustment) filed by some or all partners • Amended returns can include non-positive adjustments • Default imputed underpayment does not include exam

adjustments taken into account on amended returns • In the case of a reallocation adjustments, all affected partners

must file amended returns

How will former partners be bound by this when PR determines it is in the current partners’ interest?

#cbizmhmwebinar 16

Overview of New Partnership Audit Rules

• Modification procedures: Amended returns (cont’d) • Under proposed regulations, amended returns must also be

filed for “intervening years” if affected by adjustment • Under proposed regulations, amended returns can be filed

by “indirect partners” (e.g., owners of S Corporation partners and Partnership partners) to satisfy modification criteria for adjustments allocable to pass-through partners

• Under proposed regulations, pass-through partners (e.g., partnership partners and S corporation partners) can elect to file an amended return that calculates an entity-level tax using a safe-harbor rate equal to the maximum rate for any type of partner, instead of providing for amended returns from indirect partners

#cbizmhmwebinar 17

Overview of New Partnership Audit Rules

• Modification Procedures: Rate Modification • Rate of tax used to compute imputed underpayment is

reduced when shown that the highest tax rate for particular partners is lower than the highest rate for any partner • C Corporations have a maximum rate of 35% • Individuals have a maximum rate of 20% for the portion of

adjustments allocable to qualified dividend income or long-term capital gains

• S Corporation partners considered to be individuals • Under proposed regulations, partnership partners are

eligible to substantiate rate modification to the extent adjustments are allocable to its own partners who have the above criteria

#cbizmhmwebinar 18

Overview of New Partnership Audit Rules

• Modification Procedures: Tax-exempt Partners • Rate of tax used to compute imputed underpayment is

reduced when shown it is allocable to a “tax-exempt” partner as defined under IRC §168(h)(2)

• Under proposed regulations, the tax-exempt partner must also demonstrate its adjustment is not subject to unrelated business income tax

Is there a procedure to provide for dynamic data sharing so PR can have timely access to this data?

#cbizmhmwebinar 19

Overview of New Partnership Audit Rules

• Push-out election • In lieu of imputed underpayment, partnership elects to have

the exam adjustment “pushed out” to all reviewed year partners affected by adjustment • No amended returns filed; reviewed year returns recomputed

with adjustment to identify tax increase • Tax increase payable by reviewed year partners during the year

that the adjustments are reported • Interest on underpaid tax includes a 2% surcharge • Non-positive adjustments do not result in tax decrease

• Under proposed regulations, non-positive adjustments allocated to reviewed year partners (not adjustment year)

• Corollary adjustments to “intervening years” also required

#cbizmhmwebinar 20

Overview of New Partnership Audit Rules

• Push-out election (cont’d) • Proposed regulations reserve on issue of allowing exam

adjustment push out to indirect partners (e.g., owners of partnership partners and S corporation partners)

• Proposed regulations provide that pass-through partners are treated as individuals (thereby taxed at entity level)

• Proposed regulations allow for any partner (including a pass-through partner) impacted by push-out election to elect a “safe harbor” tax calculation, which permits the partner to simply use the maximum rate of tax with respect to a push out adjustment, and removes the need to calculate intervening year adjustments

#cbizmhmwebinar 21

Overview of New Partnership Audit Rules

• Other modifications • Proposed regulations provide for additional types of

modification procedures to default imputed underpayment • Publicly-traded partnerships demonstrating a net

decrease to passive activity losses • Adjustment relates to “deficiency dividends” of a

regulated investment company or a real estate investment trust

• Adjustment taken into account by a partner in a closing agreement with IRS (similar effect to amended return)

#cbizmhmwebinar 22

Example 1

Net increase from exam; one partner leaves

#cbizmhmwebinar 23

Ex. 1: Net increase from exam; one partner leaves

• Partnership “P” is formed during Year 1 by Partners “A” and “B,” with agreement to share 50/50

• Assume the beginning tax basis of A’s and B’s partnership interest is $0 each

• P has Year 1 income of $1,000, allocated 50/50 to A and B • P has Year 2 income of $0, and during Year 2, A sells her

entire interest in P to new Partner “C” for $600 • A recognizes $100 gain on sale (the difference between her

Year 2 sales proceeds and basis of $500 that results from her Year 1 and Year 2 allocations from P)

• P’s Year 1 tax return is audited during Year 3, where Year 1 income is re-determined to be $1,200 instead of $1,000

#cbizmhmwebinar 24

Ex. 1: Net increase from exam; one partner leaves

• Under the default imputed underpayment rule, tax on the $200 unfavorable adjustment is paid by P during Year 3 • B and C economically bear the cost of the imputed

underpayment, which is “unfair” to C • Under the “push-out” election, the $200 unfavorable

adjustment is pushed out to A and B, who re-compute their Year 1 taxes to account for the adjustment, and then report the resulting tax on their Year 3 tax returns • “Fairer” to C, in that A remains responsible for the tax

increase attributable to A • A and B are subject to the 2% interest surcharge • BUT, what about “intervening year” adjustments?

#cbizmhmwebinar 25

Ex. 1: Net increase from exam; one partner leaves

• Under the “push-out” election, A must include “intervening year” adjustments • Once A makes her $100 Year 1 push-out adjustment, her

basis in P at the end of Year 2 is increased from $500 to $600. As a result, A’s Year 2 gain on sale to C is reduced from $100 to $0.

• A’s Year 2 tax decrease (resulting from this gain reduction) does not net against the amount A must pay with her Year 3 tax return, since the “push-out” election allows only for increases

• Since A no longer is a partner, has she been whipsawed? • Proposed regulations provide that non-positive exam

adjustments subject to push-out election are taken into account by reviewed year partners, but do not clearly articulate whether a non-positive intervening year adjustment can also be taken into account by a reviewed year partner

#cbizmhmwebinar 26

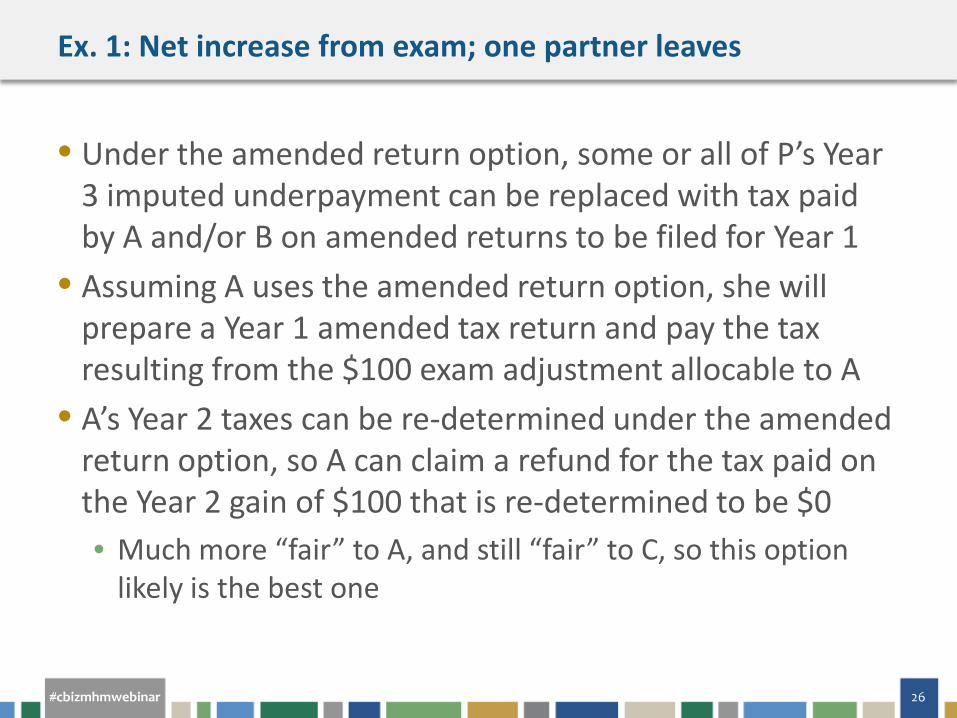

Ex. 1: Net increase from exam; one partner leaves

• Under the amended return option, some or all of P’s Year 3 imputed underpayment can be replaced with tax paid by A and/or B on amended returns to be filed for Year 1

• Assuming A uses the amended return option, she will prepare a Year 1 amended tax return and pay the tax resulting from the $100 exam adjustment allocable to A

• A’s Year 2 taxes can be re-determined under the amended return option, so A can claim a refund for the tax paid on the Year 2 gain of $100 that is re-determined to be $0 • Much more “fair” to A, and still “fair” to C, so this option

likely is the best one

#cbizmhmwebinar 27

Ex. 1: Net increase from exam; one partner leaves

• Practical concerns • Who will help the Partnership Representative make the

appropriate choice? • What if A is subject to different tax rates on ordinary income

and capital gains? A will not care much for the amended return option in that case, and would prefer the default rule (which hurts C). Note that the partnership must rely on A’s cooperation to take advantage of this modification procedure (the partnership cannot force A to amend, unless there is a previous contractual consent). On the other hand, the partnership could make a push-out election, without a need for A’s consent.

• Will A have recourse against P if A is not consulted on choice between “push-out” election or amended return option?

• These contingencies must be addressed in a revised partnership agreement

#cbizmhmwebinar 28

Thoughts about Revised Partnership And LLC Member Agreements

#cbizmhmwebinar 29

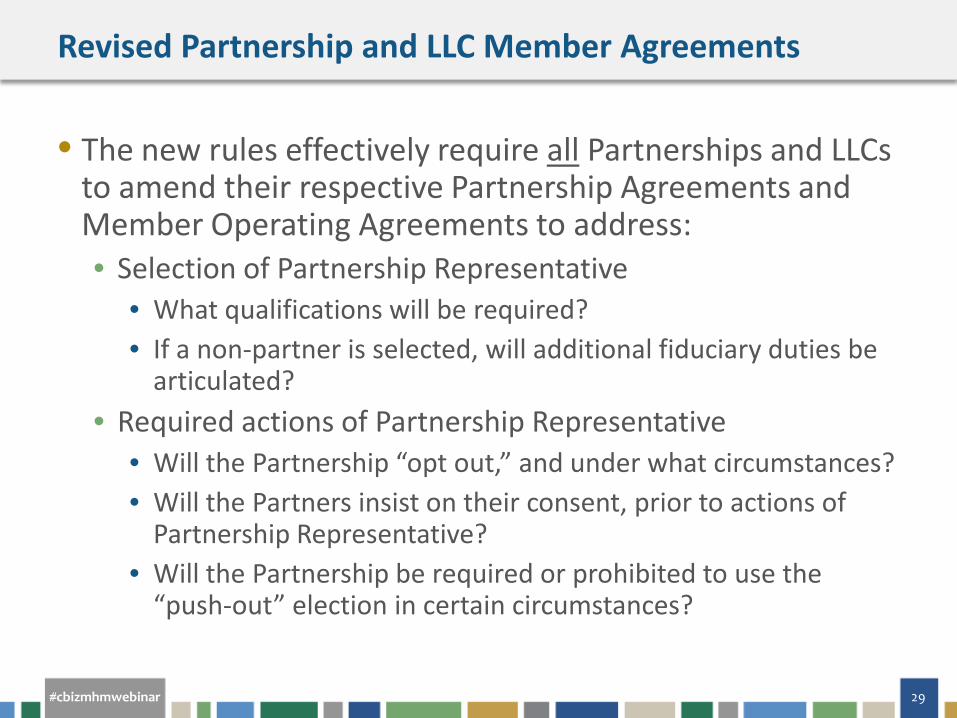

Revised Partnership and LLC Member Agreements

• The new rules effectively require all Partnerships and LLCs to amend their respective Partnership Agreements and Member Operating Agreements to address: • Selection of Partnership Representative

• What qualifications will be required? • If a non-partner is selected, will additional fiduciary duties be

articulated? • Required actions of Partnership Representative

• Will the Partnership “opt out,” and under what circumstances? • Will the Partners insist on their consent, prior to actions of

Partnership Representative? • Will the Partnership be required or prohibited to use the

“push-out” election in certain circumstances?

#cbizmhmwebinar 30

Revised Partnership and LLC Member Agreements

• The new rules effectively require all Partnerships and LLCs to amend their respective Partnership Agreements and Member Operating Agreements to address (cont’d): • Required actions of Partners

• Will Partners be required to provide timely information to help Partnership mitigate Partnership-level tax?

• Will Partners be required to amend returns when requested by Partnership Representative?

• Indemnities • Will indemnities be put in place, requiring former

partners to make payments for their “share” of tax that cannot be offset through distributions?

#cbizmhmwebinar 31

Example 2

Net increase from exam; prior distribution gain

#cbizmhmwebinar 32

Ex. 2: Net increase from exam; prior distribution gain

• Partnership “P” is formed during Year 1 by Partners “A” and “B,” with agreement to share 50/50

• Assume the beginning tax basis of A’s and B’s partnership interest is $90 each

• P has Year 1 loss of $100, allocated 50/50 to A and B • P has Year 2 income of $0, and during Year 2, A receives a

$100 cash distribution from P • A recognizes tax benefit from $50 loss in Year 1, and tax on

$60 distribution gain in Year 2 (the difference between her Year 2 distribution and basis of $40 that results from her Year 1 and Year 2 allocations from P)

• P’s Year 1 tax return is audited during Year 3, where Year 1 loss is re-determined to be $0 instead of $100

#cbizmhmwebinar 33

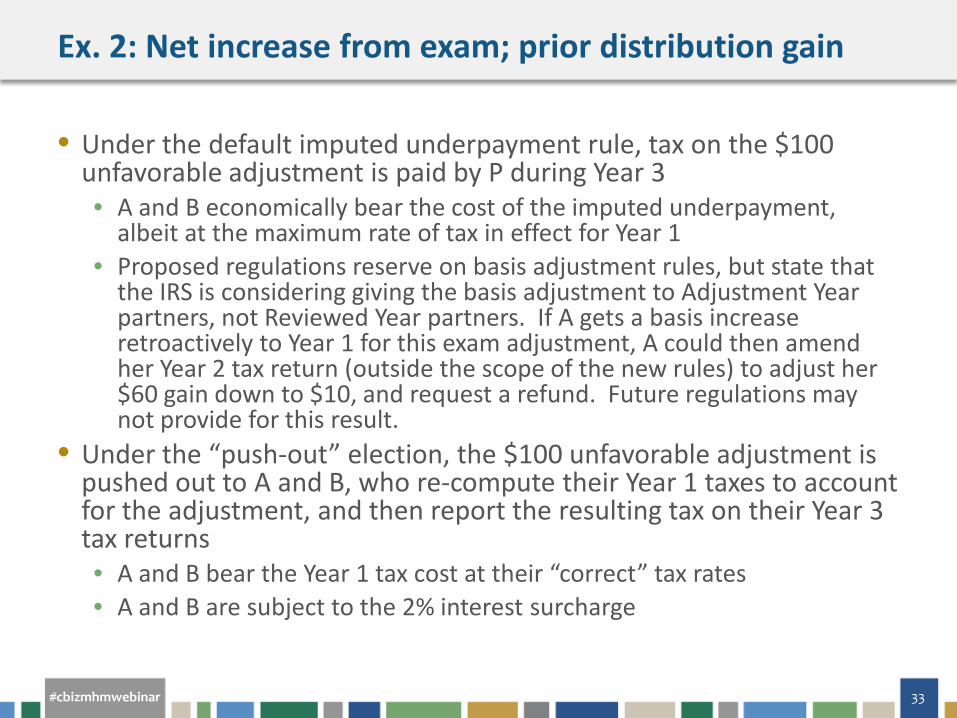

Ex. 2: Net increase from exam; prior distribution gain

• Under the default imputed underpayment rule, tax on the $100 unfavorable adjustment is paid by P during Year 3 • A and B economically bear the cost of the imputed underpayment,

albeit at the maximum rate of tax in effect for Year 1 • Proposed regulations reserve on basis adjustment rules, but state that

the IRS is considering giving the basis adjustment to Adjustment Year partners, not Reviewed Year partners. If A gets a basis increase retroactively to Year 1 for this exam adjustment, A could then amend her Year 2 tax return (outside the scope of the new rules) to adjust her $60 gain down to $10, and request a refund. Future regulations may not provide for this result.

• Under the “push-out” election, the $100 unfavorable adjustment is pushed out to A and B, who re-compute their Year 1 taxes to account for the adjustment, and then report the resulting tax on their Year 3 tax returns • A and B bear the Year 1 tax cost at their “correct” tax rates • A and B are subject to the 2% interest surcharge

#cbizmhmwebinar 34

Ex. 2: Net increase from exam; prior distribution gain

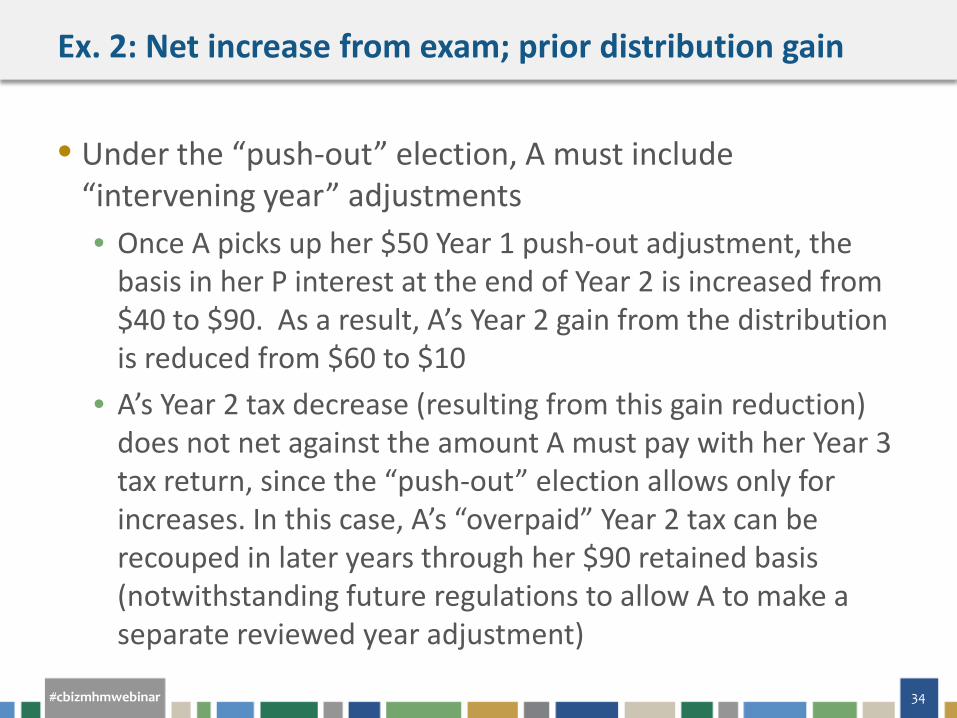

• Under the “push-out” election, A must include “intervening year” adjustments • Once A picks up her $50 Year 1 push-out adjustment, the

basis in her P interest at the end of Year 2 is increased from $40 to $90. As a result, A’s Year 2 gain from the distribution is reduced from $60 to $10

• A’s Year 2 tax decrease (resulting from this gain reduction) does not net against the amount A must pay with her Year 3 tax return, since the “push-out” election allows only for increases. In this case, A’s “overpaid” Year 2 tax can be recouped in later years through her $90 retained basis (notwithstanding future regulations to allow A to make a separate reviewed year adjustment)

#cbizmhmwebinar 35

Ex. 2: Net increase from exam; prior distribution gain

• Under the amended return option, some or all of P’s Year 3 imputed underpayment can be replaced with tax resulting from amended returns to be filed for Year 1 by A and/or B

• Assuming A uses the amended return option, she will prepare a Year 1 amended tax return and pay the tax resulting from the $50 exam adjustment allocable to A

• A’s Year 2 taxes can be re-determined under the amended return option, so A can claim a refund for the tax paid on the Year 2 gain decrease of $50

#cbizmhmwebinar 36

Example 3

Re-allocation from exam; decrease partner leaves

#cbizmhmwebinar 37

Ex. 3: Re-allocation from exam; decrease partner leaves

• Partnership “P” is formed during Year 1 by Partners “A” and “B,” with agreement to allocate profits and losses according to a specified “waterfall” schedule

• P has Year 1 income of $1,000, allocated entirely to A according to the interpretation of the waterfall schedule

• During Year 2, A sells his entire interest in P to new Partner “C”

• P’s Year 1 tax return is audited during Year 3, where Year 1 income is re-determined to be allocable 50/50 between A and B, rather than 100% allocable to A

#cbizmhmwebinar 38

Ex. 3: Re-allocation from exam; decrease partner leaves

• Under the default imputed underpayment rule, re-allocations of distributive shares are not netted, so the decrease item is disregarded when determining the partnership-level tax deficiency. Tax on the $50 unfavorable adjustment is paid by P during Year 3. • B and C economically bear the cost of the imputed underpayment, which is

“unfair” to C • Under proposed regulations, B and C also pick up the decrease item as an

income adjustment in P’s Adjustment Year tax filing, which perhaps rectifies C’s outcome

• Under the “push-out” election, the $50 unfavorable adjustment is pushed out to B, who re-computes his Year 1 taxes to account for the adjustment, and then reports the resulting tax on his Year 3 tax return • “Fairer” to C, in that B remains responsible for the tax increase attributable to B • Under proposed regulations, A picks up the decrease item in A’s Reviewed Year

tax filing (Year 1) • A would then pay tax for the “intervening year” adjustment to A’s Year 2 sale

transaction (which would be a tax increase)

#cbizmhmwebinar 39

Ex. 3: Re-allocation from exam; decrease partner leaves

• Under the amended return option, P’s Year 3 imputed underpayment can be replaced with tax paid by A and B on Year 1 amended returns, but only if both A and B file • A’s Year 1 refund potential is preserved in this case, and

B’s Year 1 tax increase still does not impact C, so this appears to be the best choice in terms of overall “fairness” (the push-out election under proposed regulations will be the second-best)

#cbizmhmwebinar 40

Example 4

Re-allocation from exam; increase partner leaves

#cbizmhmwebinar 41

Ex. 4: Re-allocation from exam; increase partner leaves

• Partnership “P” is formed during Year 1 by Partners “A” and “B,” with agreement allocate profits and losses according to a specified “waterfall” schedule

• P has Year 1 income of $1,000, allocated entirely to A according to the interpretation of the waterfall schedule

• During Year 2, B sells his entire interest in P to new Partner “C”

• P’s Year 1 tax return is audited during Year 3, where Year 1 income is re-determined to be allocable 50/50 between A and B, rather than 100% allocable to A

#cbizmhmwebinar 42

Ex. 4: Re-allocation from exam; increase partner leaves

• Under the default imputed underpayment rule, re-allocations of distributive shares are not netted, so the decrease item is disregarded when determining the partnership-level tax deficiency. Tax on the $50 unfavorable adjustment is paid by P during Year 3. • A and C economically bear the cost of the imputed

underpayment, which is “unfair” to both A and C • C had nothing to do with the Year 1 allocation, and A

already paid tax on the over-allocation • Under proposed regulations, A and C also pick up the

decrease item as an income adjustment in P’s Adjustment Year tax filing, which perhaps rectifies A’s and C’s outcome

#cbizmhmwebinar 43

Ex. 4: Re-allocation from exam; increase partner leaves

• Under the “push-out” election, the $50 unfavorable adjustment is pushed out to B, who re-computes his Year 1 taxes to account for the adjustment, and then reports the resulting tax on his Year 3 tax return • “Fairer” to A and C, in that B remains responsible for

the tax increase attributable to B • B will be subject to the 2% interest surcharge, which B

would not have incurred had B been given the option to file an amended return

• Under proposed regulations, A picks up the decrease item in A’s Reviewed Year tax filing (Year 1)

#cbizmhmwebinar 44

Ex. 4: Re-allocation from exam; increase partner leaves

• Under the amended return option, P’s Year 3 imputed underpayment can be replaced with tax paid by A and B on Year 1 amended returns, but only if both A and B file • A’s Year 1 refund potential is preserved in this case, and B’s

Year 1 tax increase still does not impact C, so this appears to be the best choice in terms of overall “fairness”

• But, what would motivate B to cooperate? Without any express agreement requiring B to cooperate, B is not required to file an amended return. Perhaps P can suggest to B that a push-out election would be forthcoming if B does not cooperate. On the other hand, a push-out election may be easier to administer from P’s standpoint. What if B wants the choice to file an amended return?

• Here again, an amended partnership / LLC agreement will be required to address this potential dilemma

#cbizmhmwebinar 45

? QUESTIONS

#cbizmhmwebinar 46

If You Enjoyed This Webcast…

Upcoming Courses: • 2/9, 2/14: Eye on Washington – Quarterly Business Tax Update, Q4 2016

Recent Publications: • Your Presence May No Longer Be Needed: Implications of the DMA Litigation • New York Reduces Unclaimed Property Look-Back Period for Voluntary

Compliance Program • Lay of the Accounting Landscape: Definition of a Business and Other Topics • Changes in the Tax Code Could Affect Not-for-Profits

#cbizmhmwebinar 47

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ