[email protected] thank you!webcasts.acc.com/handouts/2.26.13_webcast_slidesa.pdf · juan carlos...

TRANSCRIPT

This Webcast Will Begin Shortly

If you have any technical problems with the Webcast or the streaming audio, please

contact us via email at: [email protected]

Thank You!

Banking Crisis in the Euro Zone

February 26, 2013

Presenters:

Pádraig Ó Ríordáin, Arthur Cox

Juan Carlos Machuca, Uría Menéndez

Irish Banking/Financial Crisis

Pádraig Ó Ríordáin, Arthur Cox

3

Roots of Irish Banking/Financial Crisis • Fiscal problem • Systemic Banking problem • Both related to property investment • Bank Lending

“It appears now, with hindsight, to be almost unbelievable that intelligent professionals in the banking sector appear not to have been aware of the size of the risk they were taking.” Nyberg Report, March 2011

• Design of Eurozone

4

September 2008 Background • Crisis of confidence • Bank share prices plummet • Deposit levels in banks quickly eroding • “Liquidity, not Solvency Problem”

Response • Irish Government issues blanket bank guarantee covering all deposits and senior debt

5

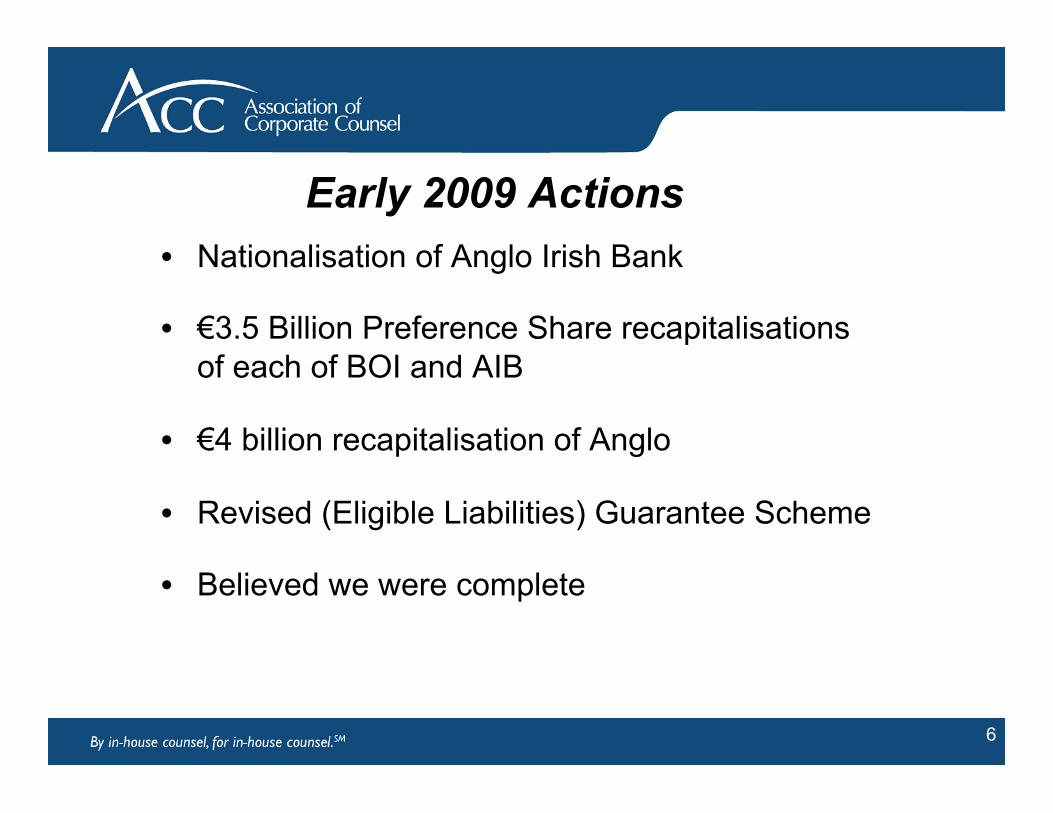

Early 2009 Actions • Nationalisation of Anglo Irish Bank

• €3.5 Billion Preference Share recapitalisations of each of BOI and AIB

• €4 billion recapitalisation of Anglo

• Revised (Eligible Liabilities) Guarantee Scheme

• Believed we were complete

6

Reality

• Total recapitalisations now over €70 billion

• 30 separate transactions in restructuring the banking system with total value of €140 billion

• Human ability to adjust reference points

7

Late 2009 Actions Creation of the National Asset Management

Agency (NAMA)

• Designed to stabilise banks by removing toxic development land assets from balance sheets

• Structure designed for speed and efficiency • €74 billion in book value of assets bought by NAMA for €33

billion • Crystallised losses on banks’ balance sheets • NAMA is asset management company with 10 year sunset

8

2010 Actions • Further recapitalisations including issuance of €33 billion

promissory note to Anglo Irish Bank

• Progressive reduction by banks of loan to deposit ratios to circa 122.5% and strengthening of balance sheets • Liability Management Exercises • Asset disposals • Increase in deposits • Other capital injections (e.g. rights issue)

• Required regulatory capital levels in banks 8% base CT1, 4% stress CT1

9

EU/IMF Programme of Support for Ireland - 28 November 2010

• The “Troika” = IMF, EU, ECB

• 22.5bn from EFSM • 22.5bn from IMF • 22.5bn from EFSF / bilateral loans • 17.5bn NPRF / Irish cash reserves

• Programme memorandum – economic and structural conditions including restructuring of banking system

• Debt refinancing, not debt repayment

2010 Troika Refinancing

10

2011 Actions - Powers • Complete restructuring of banking system in 6 months • Powers based on Credit Institutions (Stabilisation) Act 2010 • Toolbox included Direction Orders, Transfer Orders,

Subordinated Liability Orders • Constitutionality and Court Process • Impact on UK law denominated debt instruments and

Credit Institutions Winding Up Directive – “preserve and restore”

• Switched off default triggers

11

2011 Actions - Implementation

• Demutualised Building Societies • Merged Building Societies into banks • Transferred Anglo and INBS deposit books to AIB and ILP • Recapitalised banks to 10.5% CT1 base and 6% stress • State-underwritten rights issue in Bank of Ireland • Investment by US syndicate in Bank of Ireland reducing

State ownership in Bank of Ireland from 52% to 15%

12

2011 Actions Haircutting of subordinated debt in solvent banks

• Subordinated Liability Orders • Liability Management Exercises • Voluntary to the extent possible

Recovered over €5 billion in capital

Only time this has been achieved.

13

2012 Actions

• Transfer of Irish Life from ILP to Minister for Finance

• Throughout the whole of 2012 there were no further recapitalisations

14

February - 2013 Actions • 7 February – liquidation of the Irish Bank Resolution Corporation

(IBRC), formerly the Anglo Irish Bank, and the Irish Nationwide Building Society, the first liquidation of a major bank in the eurozone

• The Irish government replaced €25bn (£21.3bn) of promissory notes, which were used to bail out Anglo Irish and Irish Nationwide, with long-term government bonds with maturities of up to 40 years

• The agreement will mean Irish taxpayers avoid a payment of €3.1bn due in March, reduce the need to borrow over the next 10 years by €20 billion, materially improve our budget deficit and enhance our ability to access capital markets and exit the IMF/EC programme

15

Banking Landscape Now Bank of Ireland Listed 15% State owned AIB Listed 99% State owned ILP Listed 99% State owned Anglo In liquidation 100% State owned INBS In liquidation Merged into Anglo EBS Demutualised Merged into AIB

• State Bank Guarantee continues, at substantial cost to banks

• €70 billion total recapitalisation cost to State to date

16

Current Position • Continued Restructuring of Banks

• Deleveraging to ‘core’ business • Liquidation of IBRC/INBS

• On going interaction at European/Troika level • ESM • Replacement of Promissory Note financing and ending of ELA

• Stability

• Sovereign Debt • Continuing Austerity Budgets • Beginning of return to markets

17

Thank You

18

19

The Spanish Banking Crisis

A late but (probably) fruitful reform

Juan Carlos Machuca, Uría Menéndez

20

A. The Emergence of the Crisis The three axes of bank restructuring: 1) Market concentration – circumstantial perspective 2) Reorganisation

• Structural perspective • Collapse of the real estate sector

3) The problem of savings banks

21

B. The Steps Taken to Reinforce the Banks 1) General features of the process

• Delayed reaction (2009) – in comparison with other EU countries.

• Reorganisation – structural perspective • Political aspect of savings banks

22

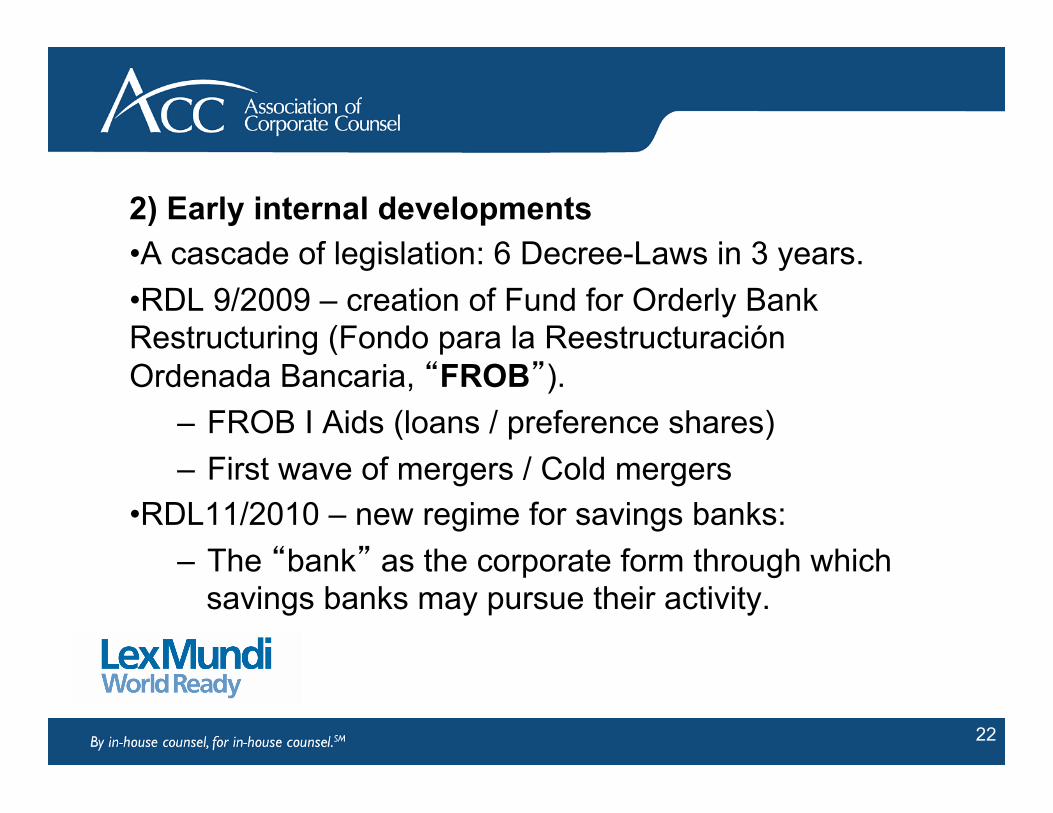

2) Early internal developments • A cascade of legislation: 6 Decree-Laws in 3 years. • RDL 9/2009 – creation of Fund for Orderly Bank Restructuring (Fondo para la Reestructuración Ordenada Bancaria, “FROB”).

– FROB I Aids (loans / preference shares) – First wave of mergers / Cold mergers

• RDL11/2010 – new regime for savings banks: – The “bank” as the corporate form through which

savings banks may pursue their activity.

23

• RDL 2/2011: – New capital requirements – FROB II (contributions to capital)

• RDL 2/2012 – Provisions and additional capital to cover potential

expenses related to risky/non-performing real estate assets.

– FROB III (Contingent Convertible Bonds, CoCos) • RDL18/2012

– Provisions and additional capital to cover potential expenses related to normal/performing real estate assets.

– General Asset-Management Companies (AMC).

24

3) European intervention • Memorandum of Understanding (June 2012): EUR

100,000 million loan granted by the Eurogroup for the reorganisation of the Spanish banking system.

• Road map: a) Stress tests (Oliver Wyman) b) Classification of credit entities into 4 groups

• RDL 24/2012, on restructuring and resolution of credit entities (later, Law 9/2012). – Early intervention (G3) / Restructuring (G1/G2) /

Resolution (G1/G2) – New core capital ratio: 9% (applicable since 01/01/2013)

25

26

Group Description Entities involved Measures applied

Group 0 Do not have any capital shortfall

Unicaja, Sabadell, Bankinter, Caixabank,

Kutxabank, Santander, BBVA

N/A

Group 1 Owned by FROB BFA-Bankia, CatalunyaBanc, NCG

Banco, Banco de Valencia

Recapitalisation plan Restructuring plan

Burden sharing Transfer to AMC

Group 2 Need state aid to meet capital requirements

Banco Mare Nostrum, Banco Caja 3,

Liberbank, CEISS

Recapitalisation plan Restructuring plan

Burden sharing Transfer to AMC

Group 3 Do not need state aid to meet capital

requirements

Ibercaja, Banco Popular

Investment of Convertible Contingent Bonds (CoCos)

27

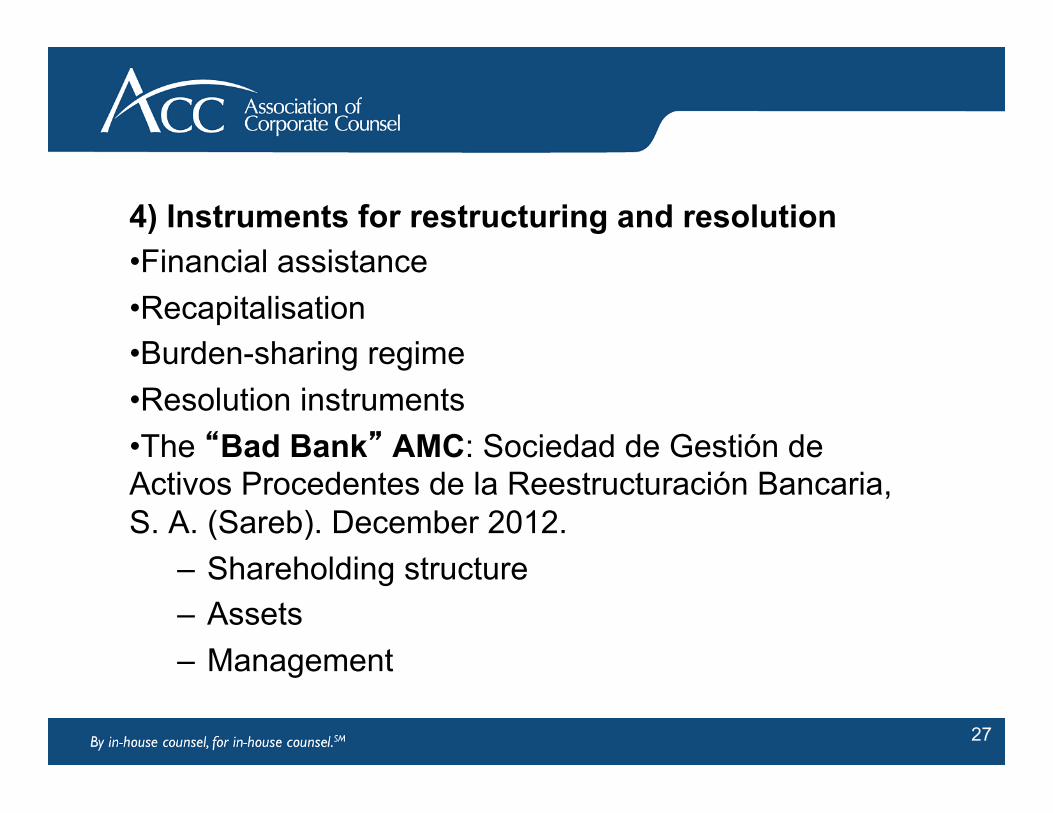

4) Instruments for restructuring and resolution • Financial assistance • Recapitalisation • Burden-sharing regime • Resolution instruments • The “Bad Bank” AMC: Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria, S. A. (Sareb). December 2012.

– Shareholding structure – Assets – Management

28

C. Progress to Date (“Working in Progress”) • Recapitalisation of banks is already on its way:

– Group 1 banks – 28 November 2012, the EC approved the restructuring plans for the four banks in that group; 26 December 2012, the FROB implements the recapitalisation (around €37 billion).

– Group 2 – 20 December 2012, the EC approved the restructuring plans for the four banks in that group (around €2 billion).

• Significant reduction in the number of savings banks (vid. charts on next slides).

29

30

31

• Reduction of capital needs as a result of burden sharing.

• The AMC is now operational. Some of the assets that were transferred to it are already being offered to the public.

• Still some uncertainty on some nationalised banks.

32

D. Objectives 1) Unresolved problems 2) Main goals • Generally improve core capital ratio of credit entities (increase of equity or reduction of RWAs) • Reduce the minimum level of core capital (long-term) • Admission to trading (stock exchange, private placing) • Elimination of the savings banks’ controlling stakes in commercial banks • Specifically for Sareb: optimise recovery of assets and the preservation of their value, minimising negative impacts on Spanish economy • Return of credit liquidity

33

¡Muchas gracias!

Questions?

Lex Mundi – the law firms that know your markets.

34

Speaker Contact Information Pádraig Ó Ríordáin

Arthur Cox (Lex Mundi member firm for Ireland and Northern Ireland)

Earlsfort Centre Earlsfort Terrace

Dublin 2 Ireland

http://www.arthurcox.com [email protected]

www.lexmundi.com

35

Speaker Contact Information Juan Carlos Machuca

Uría Menéndez (Lex Mundi Member Firm for Spain)

London

http://www.uria.com [email protected]

www.lexmundi.com

36

Thank you for attending another presentation from

ACC’s Webcasts

Please be sure to complete the evaluation form for this program as your comments and ideas are helpful in planning future programs.

If you have questions about this or future webcasts, please contact ACC at [email protected]

This and other ACC webcasts have been recorded and are available,

for one year after the presentation date, as archived webcasts at http://webcasts.acc.com.