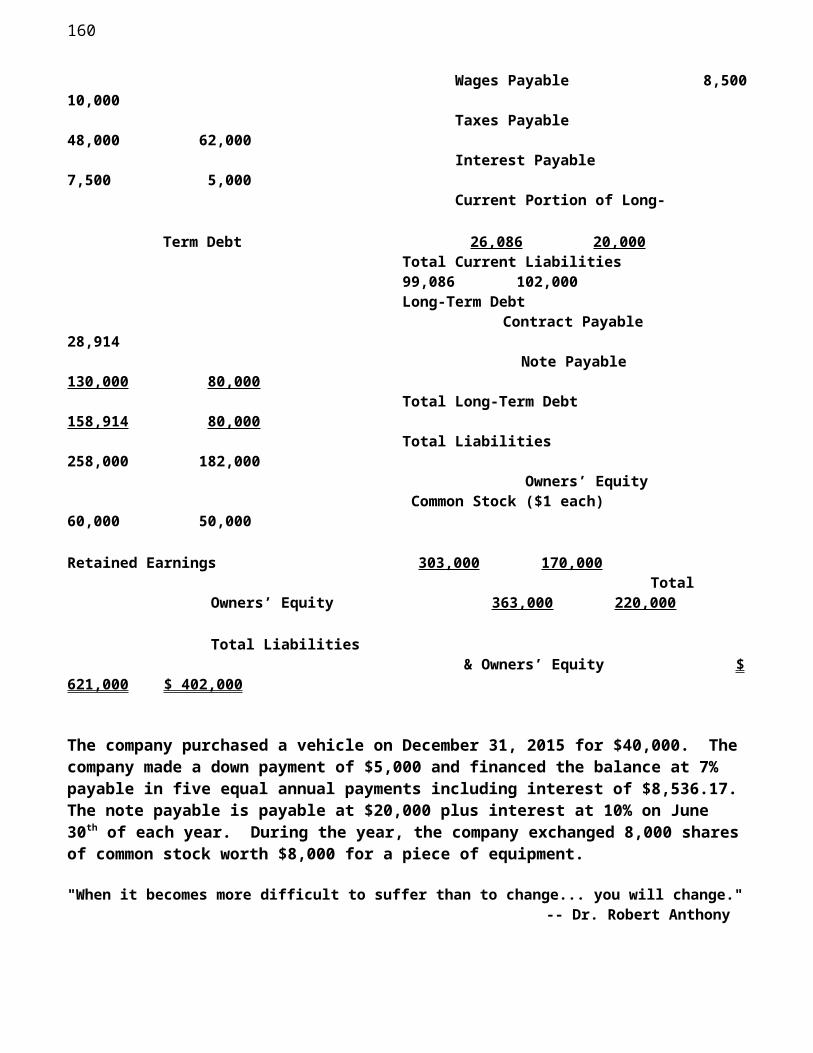

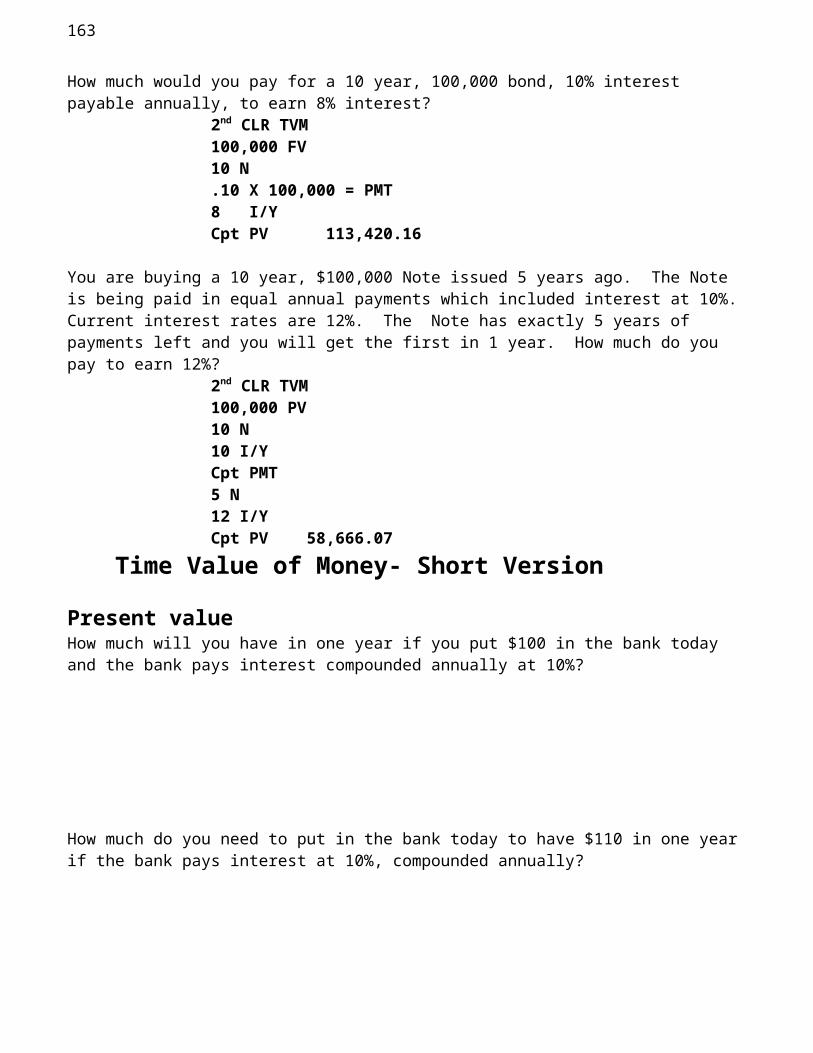

aspnet.cob.ohio.eduaspnet.cob.ohio.edu/isms/upload/documents/158... · web viewthe retained...

TRANSCRIPT

Learning Module #1 That was talking, this is

doing. Doing is different than talking.

Curly Sue

What this course is and what it isn’t

The Plan

The website

1

Where are you now?

From the following information for Laurel, Inc., prepare the financial statements for the year ending December 31, 2015.

Cash 58,000Accounts Receivable 15,000Inventory 80,000

Building200,00

0

Equipment100,00

0Accumulated Depreciation 20,000Security Deposit 3,000Accounts Payable 12,000Salaries Payable 4,000Taxes Payable 6,000

Note Payable, Long-Term 40,00

0 Common Stock 5,000 Paid In Capital- Ex Par 45,000 Retained Earnings 334,000 Treasury Stock 10,000 Sales 410,000 Cost of Goods Sold 200,000 Salary Expense 50,000 Rent Expense 36,000 Depreciation Expense 10,000 Office Expense 10,000 Interest Revenue 1,000 Interest Expense 5,000 Income Tax Expense 30,000

Laurel, Inc. declared and paid a $5,000 dividend in 2015. The beginning Common Stock was $50,000 and beginning Retained Earnings was $259,000. Prepare a Trial Balance, Income Statement, Balance Sheet and Statement of Owners’ Equity for Laurel.

2

3

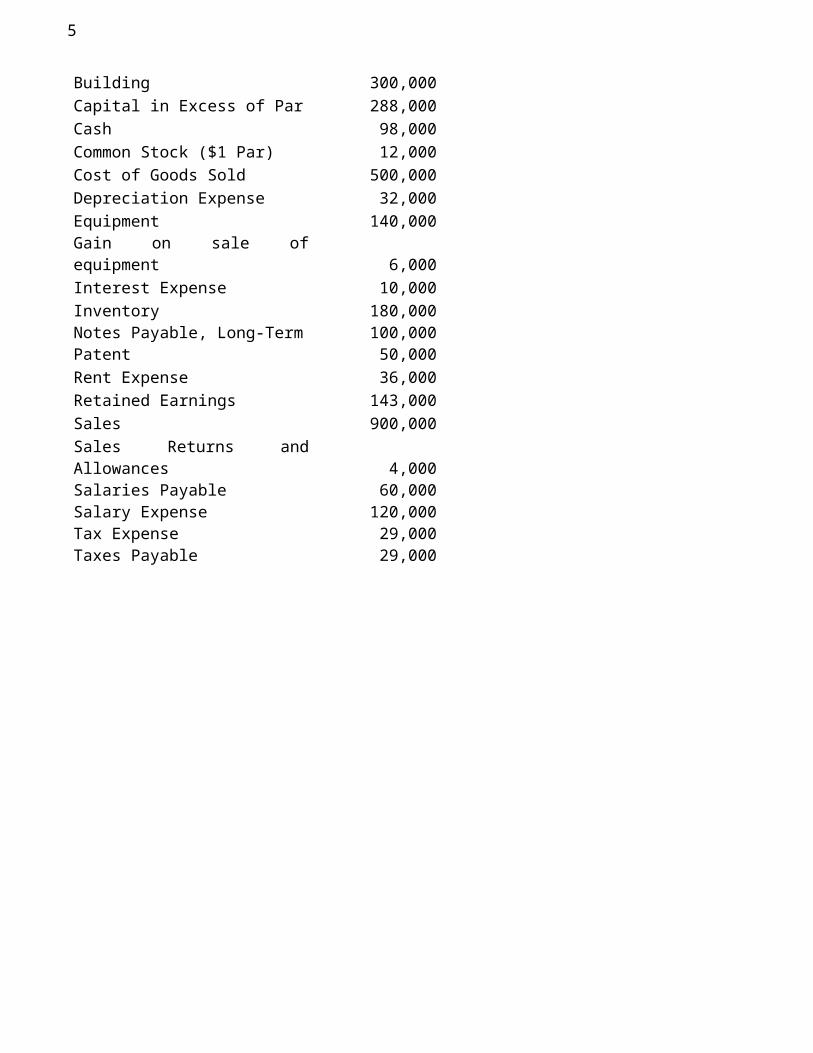

From the following for 2015 for CoJo, Inc. prepare an Income Statement and a Balance Sheet. assume a December 31 year end.

Accounts Payable 200,000Accounts Receivable 120,000Accumulated Depreciation 56,000Administrative Expenses 58,000Advertising Expense 20,000Building 300,000Capital in Excess of Par 288,000Cash 98,000Common Stock ($1 Par) 12,000Cost of Goods Sold 500,000Depreciation Expense 32,000Equipment 140,000Gain on sale of equipment 6,000Interest Expense 10,000Inventory 180,000Notes Payable, Long-Term 100,000Patent 50,000Rent Expense 36,000Retained Earnings 143,000Sales 900,000Sales Returns and Allowances 4,000Salaries Payable 60,000Salary Expense 120,000Tax Expense 29,000Taxes Payable 29,000

4

Calculating the Earnings Per Share

There are two levels of EPSB_____________

D_____________

Cash Flows

From the following information for Molly’s Munchies, prepare a Statement of Cash Flows for the year ended December 31, 2014 using the indirect method.

The following data is for Fred’s Follies: Balance Balance 12/31/15 12/31/14

5

Cash 80,000 20,000Accounts Receivable 68,000 35,000Inventory 70,000 90,000Prepaid Insurance 500 3,000 Equipment 340,000 270,000Accumulated Depreciation 80,000 20,000Land 120,000

Security Deposits 12,000 10,000 Accounts Payable 35,000 30,000

Wages Payable 6,000 10,000Rent Payable 7,500 6,000Interest Payable 6,000 7,000Taxes Payable 16,000 5,000Note Payable 120,000 140,000Common Stock ($1 each) 300,000 160,000Retained Earnings 120,000 50,000Sales 1,200,000Cost of Goods Sold 575,000Wage Expense 260,000Rent Expense 24,000Office Expenses 70,000Depreciation Expense 60,000Advertising Expense 15,000Insurance Expense 9,000Interest Expense 14,000Income Tax Expense 52,000

Some of the equipment was acquired on March 31, 2015 by exchanging 60,000 shares of common stock worth $60,000. The additional common stock (other than that issued for the purchase of the equipment) was sold on June 30, 2015 for $1 per share. The company did not sell any equipment during the year. All the rest of the equipment and the land purchased during the year was purchased for cash. The retained earnings balance for both years is after all closing entries have been made. The Note Payable requires payments of $20,000 principal plus interest at 10% on June 30th of each year.

6

Now you do one - Not dying is not the same as living.

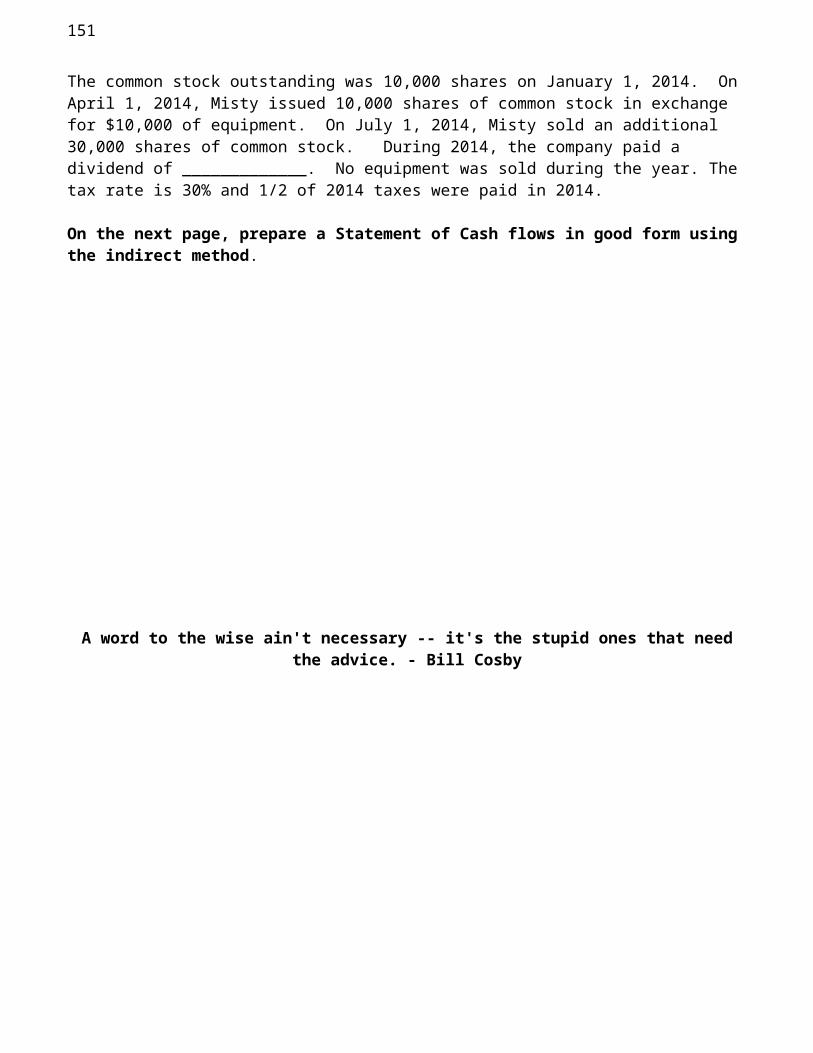

The following balances are for Misty Company at December 31,

2014 2015Cash 10,000 30,000Accounts Receivable 40,000 50,000Inventory 80,000 60,000Prepaid Rent 6,000 3,000

7

Equipment 180,000 210,000Accumulated Depreciation-Equipment 50,000 60,000Security Deposit 8,000 9,000Accounts Payable 40,000 50,000Salaries Payable 10,000 -0-Interest Payable -0- 5,000Taxes Payable -0- ______Note Payable 100,000 70,000Common Stock 10,000 50,000Retained Earnings 114,000 124,000Sales 200,000Cost of Goods Sold 100,000Salary Expense 40,000Rent Expense 24,000Interest Expense 6,000Depreciation Expense 10,000

The common stock outstanding was 10,000 shares on January 1, 2014. On April 1, 2015, Misty issued 10,000 shares of common stock in exchange for $10,000 of equipment. On July 1, 2015, Misty sold an additional 30,000 shares of common stock. During 2015, the company paid a dividend of _____________. No equipment was sold during the year. The tax rate is 30% and 1/2 of 2015 taxes were paid in 2015.

On the next page, prepare a Statement of Cash flows in good form using the indirect method.

8

The following data is for Calvin’s Catnip Treats, Inc.:

Balance Balance 12/31/16 12/31/15

Cash 120,000 66,000Accounts Receivable 70,000 35,000Allowance for Doubtful Accounts 10,000 5,000Inventory 30,000 80,000Prepaid Rent 5,000Equipment 320,000 240,000Accumulated Depreciation 60,000 40,000Land 20,000Security Deposit 1,000Patent 9,000 9,000Accounts Payable 79,000 60,000Wages Payable 6,000 10,000Rent Payable 5,000Taxes Payable 25,000 38,000

9

Interest Payable 5,000 2,000Note Payable 110,000 130,000Common Stock ($1 each) 120,000 60,000Retained Earnings 150,000 90,000Sales 1,000,000Cost of Goods Sold 600,000Wage Expense 155,000Rent Expense 60,000Office Expenses 27,000Depreciation Expense 20,000Bad Debt Expense 10,000Interest Expense 13,000Income Tax Expense 30,000

The land was acquired on April 1, 2016 by exchanging 20,000 shares of common stock worth $20,000. The additional common stock (other than that issued for the purchase of the land) was sold on July 1, 2016 for $1 per share. All equipment purchased during the year was purchased for cash. The retained earnings balance for both years is after all closing entries have been made. The Note Payable requires payments of $20,000 principal plus interest at 10% on December 31st of each year.

10

Learning Module #2

Managerial Elementtemerity Concentration comes out of

a combination of confidence and hunger.

(Arnold Palmer)

We have been studying Financial Accounting

Which deals with ___________________________________________

Managerial accounting is __________________________________________________

Cost BehaviorWe sell Tasteys. They cost $90 to make and sell for $ 300 each. Our only other expenses are the rent of $300 per month, utilities of $100 per month and a $10 per unit sales commission we pay to the salespeople. We sold ten during the year.

A Contribution Margin Statement

11

Fixed Costs are

Variable Costs are

Calculating Break-even

12

Target Profit

Using the Contribution Margin%

“ The art of conversation lies in listening. ” — Malcolm Forbes

Your Club is thinking about having a dinner. They expect to charge about $30 per head. They need to rent a room in Baker for $300 (includes servers). In addition to the $300, Baker will charge you $10 per dinner. How many dinners must you sell just to break even? How many dinners must you sell to make a profit of $600?

Sarah sells cookies. She uses ingredients that cost $.20 per cookie and sells them for $.50 each. She pays her sales force a 10% commission on all cookies sold. She pays rent of $1,000 per month. Her other fixed costs are $2,000 per month. How many cookies must she sell to

13

break-even? How many cookies does she need to sell to make $2,000 per month? Prepare a contribution margin statement at the level where she is making $2,000 per month.

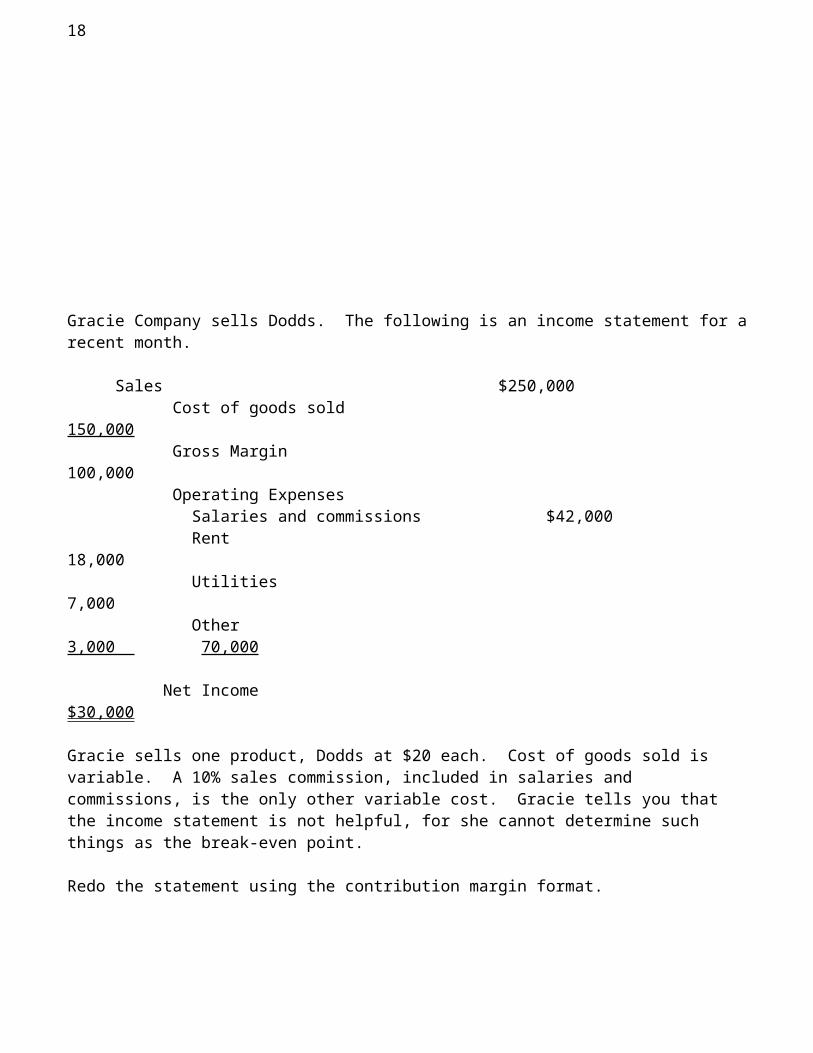

Gracie Company sells Dodds. The following is an income statement for a recent month.

Sales $250,000 Cost of goods sold 150,000 Gross Margin 100,000 Operating Expenses Salaries and commissions $42,000 Rent 18,000 Utilities 7,000 Other 3,000 70,000

Net Income $30,000

Gracie sells one product, Dodds at $20 each. Cost of goods sold is variable. A 10% sales commission, included in salaries and commissions, is the only other variable cost. Gracie tells you that the income statement is not helpful, for she cannot determine such things as the break-even point.

Redo the statement using the contribution margin format.

14

What is the breakeven in units and dollars

Acme Company sells anvils and the following is per anvil

Unit Selling Price $20Variable Costs 12

Total fixed costs $ 400,000

Total volume 100,000 units

Prepare an income statement using the contribution margin format

15

What is Acme’s Break Even point in units

In $

Now assume that Acme wants to make $1,000,000 per year. How many anvils does the company need to sell to accomplish this (in units and dollars).

The CFO of Garven Company provides the following per-unit analysis, based on a volume of 100,000 units

Selling Price $30Variable Costs $12

Fixed Costs 9 Total Costs 21 Profit per unit $ 9

Answer each of the following questions independent of your answers to the other questions

1) What total profit does Garven expect to earn?

16

2) What would be the total profit at 110,000 units? (Be careful- they are fixed costs)

3) What is the break-even point in units?

4) Garven’s managers think they can increase volume to 120,000 units by spending an

additional $ 60,000 on salespeople. What total profit would they earn if they make this move?

5) Break-even using Contribution Margin %

17

Now look at a Hot Dog Stand

You have decided to open a hot dog stand at the corner of Court and Union. The following is your opening balance sheet. You own the only 50,000 shares of stock outstanding for your company. You sell the dogs for $2.00 each. You pay your worker a fixed salary of $20,000 plus $.10 for each dog she sells. (Dogs cost $.40 each- how do I know that?)

AssetsCash 5,000Inventory 10,000Cart 35,000 Total 50,000

Liabilities

Owners’ EquityCommon Stock 50,000

Retained Earnings -0- Total 50,000

Income Statement Using Contribution Margin Format

For the First Year Sales 60,000 Sales Cost of Sales 12,000 Gross Margin 48,000

18

Operating Expenses Wages 23,000 Other 10,000 Total Operating Expenses 33,000 Operating Income 15,000

How many hot dogs do you need to sell to break-even Per Year

Per Month Per Week Per Day Per Hour

Professional tip In negotiating, go ___________ then ________________.Homework Managerial

Problem 1. Salmon Company makes Things. Things sell for $30 each and cost $10 each to make. Fixed costs are estimated to be $1,500,000 next year.

What is the breakeven point in units and sales dollars for Salmon based on the above information

How many Things must Salmon sell to make $1,200,000 next year?

Problem 2 Billy Bob’s has given you the following income statement for June 2013.

Sales $ 500,000Cost of goods sold 300,000

Gross margin 200,000

Operating expenses:

19

Salaries and commissions $ 80,000 Utilities 20,000 Rent 22,000

Other 18,000 Total operating expenses 140,000 Income 60,000

Billy Bob sells one product, a running shoe for $100 per pair. A 10% sales commission, included in Salaries and commissions is the only other variable cost. The manager tells you that this financial statement is not very helpful to her.

Redo the income statement using the contribution margin format.

For Billy Bob’s determine the break-even in sales dollars and in units

Learning Module #3 struthious Managerial Lazy people are always anxious sycophant Part 2 to be doing something. pugnacious Marquis De Vauvenargues

Susie is the new manager of Helming Clothing. The controller has given her the following information based on expected operations for the coming year.

Shirts Pants PulloversSelling Price $ 20 $ 30 $ 60Variable Costs 10 12 15Contribution Margin 10 18 45

Sales mix percentage, in dollar sales 50% 30% 20%

Total fixed costs are $1,189,000

What is the weighted average contribution margin%?

What is the break-even in sales?

20

Prepare an Income Statement by product line at the breakeven pointShirts Pants Pullovers Total

Sales $1,025,000Variable Costs 512,500Contribution Margin

Fixed Costs 1,189,000

Net Income

At the break-even point, how many of each item will be sold?

Shirts Pants Pullovers

The CEO wants a profit of $800,000. Determine the sales needed to achieve this goal?

The sales manager believes she can increase the sales of any of the three products by 20% by spending $25,000 in advertising on that product. Which product should she choose for the promotion?

21

Cleveland Cliffs produces three models of gel pens, regular, silver and gold. Price and costs of the three are as follows

Regular Silver GoldSelling Price $ 20 $ 30 $60Variable Costs 12 15 21

Monthly fixed costs are $600,000

Suppose the sales mix is Regular 50%, Silver 30% and Gold 20% What is the breakeven in sales dollars?

22

How much must the total sales dollars be to make $300,000 per month?

Freeland Company makes three products, Alpha, Beta, and Gamma

Below are the income statement for a recent month:

May Sales $160,000

Costs 120,000 Net Income 40,000

Selling price and cost data by product are as follows.Alpha Beta Gamma

Selling Price $40 $20 $10Variable costs 16 6 6Contribution margin 24 14 4

Sales mix (in dollars) 40% 40% 20%

1) Determine the break-even point in sales dollars

23

2) Which product is most profitable per unit sold?

3) Which product is most profitable per dollar of sales?

4) What total sales dollars are needed to earn $70,000 per month, and how many units of each product will be sold at that sales level if the usual mix is maintained?

5) The sales manager believes that he could increase sales of Gamma by 10,000 units per month if more attention were devoted to it and less to Beta. Sales of Beta would fall by 2,000 units per month. What change in income would occur if this action were taken?

24

6) June sales were $200,000 with a mix of 40% Alpha, 30% Beta and 30% Gamma. What was the income?

7) Suppose the company is currently selling 12,000 units of Gamma. Because this is the least profitable product, management believes it should be dropped from the mix. If Gamma is dropped, it is expected that sales of Beta would remain the same and those of Alpha would rise. By how much would sales of Alpha have to rise to maintain the same total income?

(Did you figure out that the fixed costs were $56,000? If yes, you are really good. If no, use the $56,000 as fixed costs anyway).

25

Managerial 2 Homework

Problem 1. Jenkins company sells three different laundry baskets. The controller has prepared the following estimates for next year

A B CSelling Price $12 $20 $30Variable Costs 4 5 8

Estimated sales mix 60% 30% 10%

Estimated Fixed Costs $1,590,000

What is the weighted average contribution margin %?

How many of each of the laundry baskets does Jenkins have to sell for the company to make $2,000,000?

Problem 2

Aisha Exterminating Company performs a wide variety of pest control services. Aisha, the owner, has been examining the following forecasts for 2013.

26

Type of Service Expected $ volume Contribution Margin %

Termites $480,000 60% Lawn Pests 360,000 50 Interior Pests 360,000 70

Total Fixed Costs are expected to be $560,000

1) What is the weighted average contribution margin %?

2) What profit does Aisha expect?

3) The actual sales mix turned out to be 20% termites, 30% lawn pests and 50% interior pests. Total actual sales were $1,200,000 and total fixed costs were $560,000. Determine the actual weighted-average contribution margin and the net income.

27

Learning Module #4

Managerial Part 3

The following data relate to the planned operations of BobKat Company before considering the changes described later.

Chair Table SofaSelling Price 120 400 600Variable Costs 40 160 360Annual volume 8,000 3,000 4,000

Fixed costs are $1,320,000 (if you dropped or changed your products these would not change).

1) What is the total profit expected to be?

28

2) What will happen to profit if BobKat drops Sofa?

3) What will happen to profit if BobKat drops chairs, but is able to shift the facilities to making more sofas so that volume increases to 7,000 units? (Total fixed costs remain constant)

4) Variable costs per sofa include $60 for parts that the company now buys outside. The company could make the parts at a variable cost of $45. If it did this, it would have to increase fixed costs by $35,000 annually. What would happen to profits if the company makes the part?

29

5) Bobkat has received a special order for 1,000 tables at $245 each. Capacity is sufficient to make the units, and sales at the regular price would not be affected. What will happen to profit if BobKat accepts the order?

Cost Allocation

Kreutzer’s Klutz Company sells backpacks, tote-bags and book-bags. The cost structure is as follows:

Backpacks Tote-bags Book-bagsSelling Price $40 $32 $40Variable Costs 24 8 20

Sales Mix 60% 10% 30%

Additionally, the company spends $4,000 per year advertising Backpacks, $1,000 per year advertising Tote-bags, and $3,000 to advertise bookbags. All other administrative costs equal $112,000. Sales are $400,000.

What is the breakeven?

30

Learning Module #5

Capital Budgeting Kreutzer Industries is introducing a new product expected to sell for $14 and to have variable costs of $7. The managers expect to sell 20,000 per year for 10 years. Making the product requires machinery that costs $400,000. Will last for 10 years, no salvage value and will increase annual fixed cash operating costs by $30,000. The machinery will be depreciated using the straight-line method. The tax rate is 30% and the required return is 12%Evaluate the feasibility of the project.

What is the expected increase in after-tax cash flows for the project?

31

The Net Present Value

Payback

32

IRR

Using Excel

Colton Company makes high-quality workshoes. Its managers believe the company can increase productivity by acquiring some new machinery but are unsure whether it would be profitable. The machinery costs $ 1,000,000, has a five-year life with no salvage value, and should save about $ 400,000 in operating costs annually. The company uses straight-line depreciation and has a 40% income tax rate and a 12% required rate of return.

What is the expected increase in after-tax cash flows for the project?

33

Calculate the NPV of the project

What is the Payback?

What is the IRR?

34

JD Company has the opportunity to introduce a new radio with the following expected results.Annual unit sales volume 300,000 Selling price per unit $60Annual cash fixed costs $ 4,200,000 Variable cost per unit $35

The product requires equipment costing $8,000,000 and having a four-year life with no salvage value. The company has a 12% hurdle rate. The tax rate is 40% and the company uses straight line depreciation.

What is the expected increase in after-tax cash flows for the project?

35

What is the NPV of the project?

What is the Payback?

What is the IRR of the project?

36

Stowe Company has the following three investment opportunities.

A B CCost $70,000 $70,000 $70,000

Cash inflow by year

Year 1 $35,000 $35,000 $4,000Year 2 35,000 10,000 8,000Year 3 - 45,000 10,000Year 4 5,000 20,000 98,000Total 75,000 110,000 120,000

Rank the investment opportunities in order of desirability using (a) payback, (b) NPV and, (c) irr.For the NPV, use a hurdle rate of 16%.

37

Gabriel company currently makes 200,000 large strawberry jars per year at a variable cost of $9.75. Equipment is available for $500,000 that will reduce the variable cost to $7.50 while increase cash fixed costs by $200,000. The equipment will have not salvage value at the end of its four-year life and will be depreciated using the straight-line method. Gabriel has a 30% tax rate and a 12% hurdle rate. Do it????

38

Debbie Stickle owns a driving range. She present pays several high school students $.8 a bucket to pick up the golf balls that his customers hit. A salesperson has shown her a machine that will pick up balls at an a cash cost of $6,600 plus $.05 per bucket. The machine costs $10,000 and has a five year life. Debbie would us straight line depreciation. Volume for the driving range is 21,000 buckets per year. Debbie’s combined state and federal tax rate is 30%. She believes the appropriate discount rate is 16%.

Do it? Other factors??

39

Homework1) The Masters’ Company has the opportunity to market a new product. The sales manager

believes the company could sell 10,000 units per year at $15 per unit for five years. The product requires machinery that costs $100,000, has a five year life and not salvage value. Variable costs per unit are $8. The machinery has fixed operating costs requiring cash disbursements of $25,000 annually. Straight-line depreciation will be used for both book and tax purposes. The tax rate is 40% and the cutoff rate is 14%.

Required:1) Increase in annual net income and cash flows expected from the investment.2) The NPV of the investment3) The Payback4) The approximate IRR

2) Grove City Pottery currently makes 200,000 large strawberry jars per year at a variable cost of $9.75. Equipment is available for $5000,000 that will reduce the variable cost to $7.50, while increasing cash fixed costs by $200,000. The equipment will have no slavage value at the end of its four-year life and will be depreciated using the straight-line method. Grove City has a 40% tax rate and a 12% hurdle rate.

1) Determine the NPV2) Determine the change in NPV if the equipment has a $25,000 residual value

40

41

Learning Module #6 \

Debits and CreditsThe Hot Dog Stand …

January 1, 2015…We formed a corporation, Hot Dogs, Inc., and you and everyone in the class invested $100 each in our venture. Everyone received ten shares of $1 par value stock for that $100 investment. Assume there are 30 of us. We elected a Board of Directors, a COO and we start to do business. First we sell 10 shares of $1,000, 6% convertible preferred stock to a venture capitalist. Each share of the preferred is convertible into 5 shares of stock. We borrowed $10,000 from the bank at 8% interest. The loan is repayable in five years. We bought a new cart for $10,000. During the year we bought 15,000 dogs and 15,000 buns. Dogs cost .15 and buns are .05 each. For our first year, we sold 14,000 dogs for $2 each. We paid our worker $7,200, paid office expenses of $3,600 and $800 for interest. On September 30 we sold 20 more shares for $300 each. On December 31, we paid the preferred dividend of $600. At the end of the year we owed our worker $100. The tax rate is 30% and we will pay our taxes next year. How did we do? Are we rich yet? Was it a good investment?

First what about that $100 we owe?

The matching concept is: Expenses must be _______________________________________________

_______________________________________________.

This is the basis of a_________________ a______________.

42

What is Preferred Stock?

Types C_______________________________________

C_______________________________________

P______________________________________ not so much

Plus anything ____________

Now we go to work----

We need to break the process down into simple steps.

Create a Ledger-----Create a Journal,---------- Write it down----- Post it ----

Create a Trial Balance------ Make Financial Statements

(When we say record transactions and Prepare Financial Statements, this is what we mean)

Breaking things into simple components may seem like “dumbing down.” Isn’t this an insult to the intelligence of our students? We aren’t in kindergarten are we?

When we are new at something, we are all basically in kindergarten.” (AoCtB, 185)

43

Write out in “accountanteze” what happened. This is done in a journal entry.

Rules of the Journal Entry: Journal entries are always numbered. Debits are to the left. Credits are to the right. The journal entry is always followed by an explanation. A blank line is left between journal entries.

44

45

Assets = Liabilities +Owners' Equity

CASH

46

47

Finally, we total and summarize what happened in a usable form- First a Trial Balance and then the financial statements.

The Trial Balance

A Chart of Accounts is ______________________________________________________

48

We will do the Income Statement first (Statement of Income, Statement of Earnings, P&L, Statement of Profit & Loss)

49

50

Balance Sheet (Statement of Financial Position, Statement of Financial Condition, Statement of Assets, Liabilities & Owners’ Equity)

Statement of Owners’ Equity (Statement of Shareholders’ Equity, Statement of Stockholders’ Equity, Statement of Retained Earnings)

51

BBBB, Inc. Balance Sheet

December 31, 2014 Assets Liabilities

Current Assets Current Liabilities Cash $ 151,000 Taxes Payable $ 18,600 Merchandise Inventory 8,000 Note Payable-Land 28,000Total Current Assets 159,000 Total Current Liabilities 46,600

Fixed Assets Long-Term Liabi l i t ies Land 30,000 Note Payable-Bank 100,000

Total Liabilities 146,600 Other Assets Security Deposit 6,000 Owners’ Equity

Common Stock ($1 Par) $ 500 Paid In Capital 4,500

Retained Earnings 43,400 Total Owners’ Equity 48,400 Total Liabil i t ies and Total Assets $ 195,000 Owners’ Equity $195,000

During 2015 the companyPurchased 15,000 biffs at $8 each. Paid $100,000 cash and will pay $20,000 next year.Sold 11,000 biffs at $20 eachPaid the $28,000 note on the land plus $2,000 interestPaid 11 months’ rent of $11,000Paid salaries of $36,000Issued 100 shares of common stock for $10,000 on June 1st.On December 31, bought a truck for $40,000, cash.On December 31, paid $50,000 on the note payable to bank and $10,000 interest.Paid 2014 taxes payableTax rate is 30% and paid ½ of 2015 taxes in 2015. The rest will be paid in 2016.

52

Assets = Liabilities +Owners' Equity

CASH

53

54

55

56

57

58

Homework

59

1) Debbie’s Doodles Inc. had the following account balances at December 31, 2014: Accounts Payable $ 34,000 Accounts Receivable 48,000 Notes Payable- long term 104,000 Cash 140,000Depreciation Expense 24,000 Common Stock 5,000 Paid In Capital 175,000Cost of Goods Sold 400,000 Equipment 136,000 Inventory 34,000 Land 180,000 Prepaid Insurance 30,000Accumulated Depreciation 48,000 Retained Earnings 240,000 Sales Revenue 820,000 Advertising Expense 73,000 Supplies Expense 16,000 Wages Expense 100,000 Security Deposits 50,000 Interest Expense 7,000 Wages Payable 12,000 Tax Expense ??

The tax rate is 30% of the Earnings Before Tax and there are 5,000 shares of common stock outstanding at December 31, 2014. The company sold 3,000 shares of common stock on November 1, 2014 for $40 per share, and declared and paid a dividend of $15,000. The beginning Common Stock was $ 60,000 and the beginning Retained Earnings was $115,000. Prepare Financial Statements for Debbie’s for the year 2014.

2) Beamer Business Year 2014 Chris opened a Beamer business on January 1, 2014. She started with $400,000 of her own money, for which she received 4,000 shares of $1 par common stock, and $100,000 borrowed from her Uncle Phil (Note Payable). The Note Payable to Uncle Phil requires that she pay the interest annually on December 31. She paid the $8,000 interest on December 31, 2013. She is required to repay the principal at the end of year 2019. She planned to operate her business as a corporation, Chris’s Beamer Biz, Inc. (CBB,Inc.). During the year she bought nine Beamers for $40,000 each. She sold seven of the Beamers for $60,000 each. Other expenses she paid cash for were: wages, $20,000; rent, $12,000; and utilities $1,000. She signed a 20-year lease and put down a rent security deposit of $1,000. In addition to the cash she invested on January 1st, on June 1st she also invested a piece of land she owned in the business that was worth $60,000 in exchange for 600 shares of common stock. At the end of the year she owed her worker wages of $1,000. She paid a dividend of $3,000. The tax rate is 30%. Chris pays 2014 taxes in 2015. So how did Chris do? (Do everything - Journal Entries, T-Accounts, Trial Balance and Financial Statements).

60

Debits, Credits and Related EnigmasChristine E. Kirch

David P. Kirch The Basics

Debit and credit are simply a way of keeping track of what happens in a business. It is the quintessential element of what is known as double entry bookkeeping. For this class you do not really need to understand everything about bookkeeping, you just need to be able to create enough rules for yourself that you can get by.

Each business transaction is recorded using specific rules. These rules fall under the general category we call “Debit and Credit”. Using these rules we keep track of the financial transactions that affect the business.

First, we will review the stuff we talked about earlier when we introduced accounting. Remember the basic accounting equation for keeping track of transactions is:

ASSETS = LIABILITIES + OWNERS’ EQUITY

A lot of beginning textbooks like to say that the assets equal claims against those assets. In other words, if you put $20,000 of your own money in a business, then you increase cash by $20,000 and you have a claim against that $20,000.

ASSETS = LIABILITIES + OWNERS’ EQUITY 20,000 = 20,000

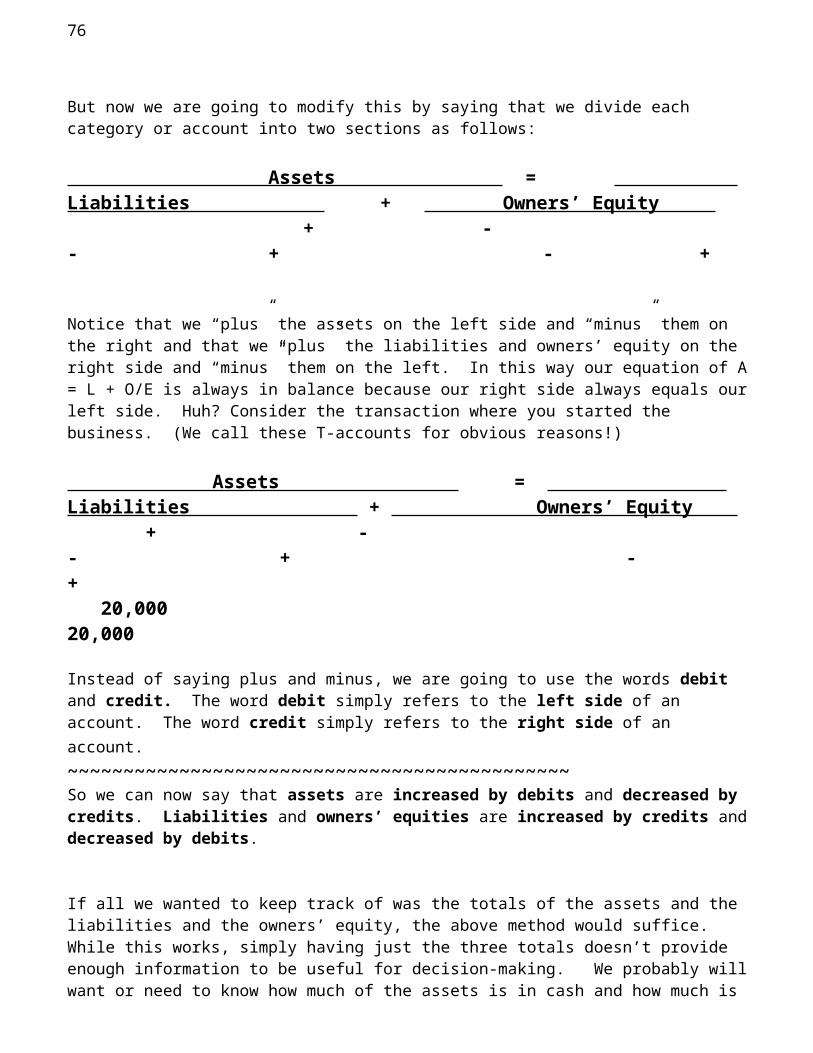

But now we are going to modify this by saying that we divide each category or account into two sections as follows:

Assets = Liabilities + Owners’ Equity + - - + - +

Notice that we “plus” the assets on the left side and “minus” them on the right and that we “plus” the liabilities and owners’ equity on the right side and “minus” them on the left. In this way our equation of A = L + O/E is always in balance because our right side always equals our left side. Huh? Consider the transaction where you started the business. (We call these T-accounts for obvious reasons!)

Assets = Liabilities + Owners’ Equity + - - + - + 20,000 20,000

Instead of saying plus and minus, we are going to use the words debit and credit. The word debit simply refers to the left side of an account. The word credit simply refers to the right side of an account. ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~So we can now say that assets are increased by debits and decreased by credits. Liabilities and owners’ equities are increased by credits and decreased by debits.

61

If all we wanted to keep track of was the totals of the assets and the liabilities and the owners’ equity, the above method would suffice. While this works, simply having just the three totals doesn’t provide enough information to be useful for decision-making. We probably will want or need to know how much of the assets is in cash and how much is in inventory. Therefore, we want to break the assets down into categories or “accounts”. Further, we will break down our main categories of Assets, Liabilities and Owners’ Equity into more descriptive sub-categories.

ASSETS = LIABILITIES + OWNERS’ EQUITY

Cash Owners’ Investment Debit Credit Debit Credit 20,000 = 20,000

Now assume your new company borrows $10,000 from the bank. You have an increase in the asset cash of $10,000 and an increase in the liability (or claim against assets) bank loan payable of $10,000.

ASSETS = LIABILITIES + OWNERS’ EQUITY Cash Bank Loan Payable Owners’ Investment Debit Credit Debit Credit Debit Credit20,000 = 20,00010,000 = 10,000 _________________30,000 = 10,000 + 20,000

Next, your company spends $15,000 for inventory. ASSETS = LIABILITIES + OWNERS’ EQUITY

Cash Inventory = Bank Loan Owners’ Investment Debit Credit Debit Credit Debit Credit Debit Credit20,000 = 20,00010,000 = 10,000 15,000 15,000 ______________ 15,000 15,000 = 10,000 20,000

Notice that we credited cash $15,000 and debited $15,000 to inventory. We used one asset (cash) to purchase another type of asset (inventory). Note also that the $15,000 balance in cash is the $30,000 debit total minus the $15,000 credit total.

As a final step to this stage of the accounting process, we introduce the process of journalizing or, preparing journal entries. Journal entries are simply a written record of the transaction. For instance, when we started the business above, our journal entry would have been:

DR CRCash 20,000 The debit Owners’ Investment 20,000 The creditTo record initial receipt of cash from the owner. The explanation of what the

journal entry is recording.

Note that we usually put the debit account name first and the debited account names are indented to the left. Debits are abbreviated dr. We then put the amount in the dr column, which is the left column. Next we put in the credit account name, indented to the right and the amount

62

in the credit column, which is the column on the right. (Credits are abbreviated cr). After the journal entry, we write a short description or explanation of the transaction the journal entry is recording.Now let’s try and put all this together.

PROBLEM:It is January 1, 2014. You and I have decided to go into the business of selling DVDs. I

heard from a friend that there is an excellent teacher at UCGA University who explains debit and credit so anyone can understand it. And she does it in exactly two hours. I have arranged with a studio near the University to tape her lecture. They will then produce the videos and sell them to us for $10 each. We will be the exclusive distributor of the DVD- Debit for Dummies. The studio which tapes the lecture will take care of paying the prof a royalty and has the equipment to make all the DVDs we want. We have decided to operate as a corporation- The Chillicothe Learning Company. I will put $9,000 in the business for 9,000 shares of stock. You are a little short right now so you will put only $1,000 in the business for 1,000 shares of stock. You will run everything and give me monthly financial statements. You will receive a salary of $3,000 per month. The following things happened in January. Remember, you must keep track of everything and report to me monthly.

First we will start by writing down what happened. We write this down in a special form or what we call journalizing the transaction. You know that assets must equal liabilities + owners’ equity. For this transaction we increase our assets by $10,000 and increase owners’ equity by $10,000. The journal entry to record the above transaction would look like:

Dr. Cr.(1) Cash 10,000

Common Stock 10,000 To record issuing capital stock in exchange for cash. The next step in the recording process is to post the amounts to their respective accounts. This recording process, the taking of the numbers from the journal to the T-Accounts is called posting. After posting, the T-Accounts would look like:

Cash Common Stock Dr. Cr. Dr. Cr.(1) 10,000 10,000 (1)

January 1: While we were at the bank we borrowed $6,000 which we agreed to repay in two years. The loan carries interest at 12% which we will pay at the end of each year.

Dr. Cr.(2) Cash 6,000

Note Payable-Bank 6,000 To record the loan from the bank.

Our T-accounts look like: Cash Note Payable-Bank Common Stock Dr. Cr. Dr. Cr. Dr. Cr.(1) 10,000 6,000 (2) 10,000 (1)

63

(2) 6,000 _________ 16,000

January 5: We purchased 1,250 DVDs with cash. Dr. Cr.

(3) Merchandise Inventory 12,500 Cash 12,500

To record purchase of inventory 1,250@$10.

The T-accounts will look like:

Merchandise Note Payable Cash Inventory Bank Common Stock Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.(1)10,000 12,500 (3) (3) 12,500 6,000 (2) 10,000 (1)(2) 6,000 _______ 16,000 12,500 3,500

January 31: We sold 900 DVDs for $20 each during the month of January. We paid your salary of $3,000, rent of $1,000, utilities of $350 and advertising of $250.

Dr. Cr.(4) Cash 18,000

Sales 18,000 To record January sales.

(5) Cost of Goods Sold 9,000 Merchandise Inventory 9,000

To record the cost of the sales for January.

(6) Salary Expense 3,000 (These could have Rent Expense 1,000 been have been Utilities Expense 350 recorded as separate Advertising Expense 250 journal entries. This

Cash 4,600 is what is known as To record expenses paid with a compound journal

cash in January. e ntry .)

64

Sales and expenses are special accounts in the owners’ equity section of the balance sheet. Revenues (sales) increase owners’ equity and expenses decrease owners’ equity. (We will go into the why of this later). Expenses are increased by debits and revenues, or sales, are increased by credits. Cash Merchandise Inventory Note Payable-Bank Common Stock Dr. + Cr. - Dr. + Cr. - Dr. - Cr. + Dr. - Cr. +(1) 10,000 12,500 (3) (3) 12,500 6,000 (2) 10,000 (1)(2) 6,000 9,000 (5)(4) 18,000 ____________ 4,600 (6) 12,500 9,000 34,000 17,100 3,500 16,900 Sales Cost of Goods Sold

Dr. - Cr. + Dr. + Cr. - 18,000(4) (5) 9,000

Salary Expense Rent Expense Dr. + Cr. - Dr. + Cr. - (6) 3,000 (3) 1,000

Utilities Expense Advertising ExpenseDr. + Cr. - Dr. + Cr. -

(6) 350 (6) 250

Some final notes concerning T-Accounts and Journal Entries. All accounts that eventually wind up on the balance sheet (Cash, Merchandise Inventory, Note Payable - Bank and Common Stock are termed real accounts. All the accounts that end up on the income statement are called temporary accounts. At the end of each year, the temporary accounts are closed to a balance sheet account called Retained Earnings. This closing process allows us to keep track of only the current year’s sales and expenses. This allows the data to be much more relevant to decision makers. If we assume that the above transactions were for the whole year instead of just of the month, then our closing entry would be:

(7) Sales 18,000 COGS 9,000 Salary Expense 3,000 Rent Expense 1,000 Utilities Expense 350 Advert Expense 250 Retained Earnings 4,400To close the temporary accounts for the year

Retained Earnings is an owners’ equity account where we accumulate the earnings for each year. Note that after you post the above entry, all the temporary accounts (Sales, Cost of Goods Sold, Salary Expense, Rent Expense, Utilities Expense and Advertising Expense) would now have -0- balances. They are ready to begin accumulating the data for the next year.

65

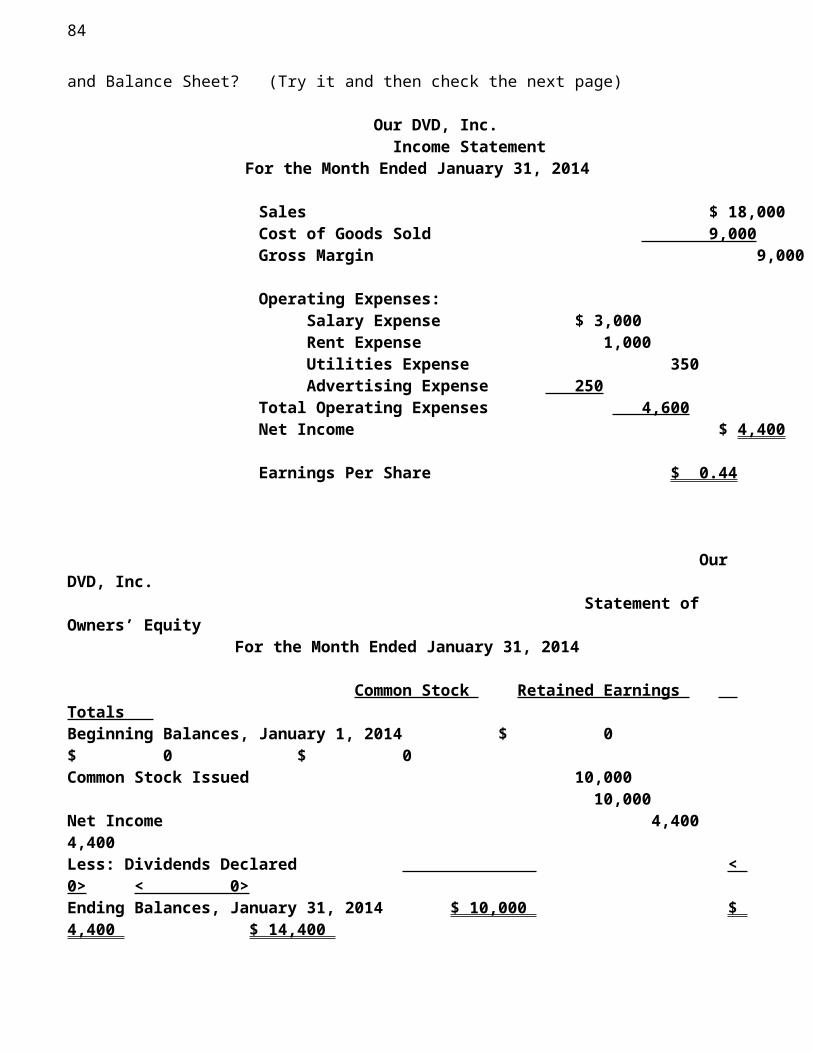

From these balances now, can you construct an Income Statement, Statement of Owners’ Equity and Balance Sheet? (Try it and then check the next page)

Our DVD, Inc. Income Statement

For the Month Ended January 31, 2014

Sales $ 18,000 Cost of Goods Sold 9,000Gross Margin 9,000 Operating Expenses:

Salary Expense $ 3,000 Rent Expense 1,000 Utilities Expense 350 Advertising Expense 250

Total Operating Expenses 4,600 Net Income $ 4,400

Earnings Per Share $ 0.44

Our DVD, Inc. Statement of Owners’ Equity

For the Month Ended January 31, 2014

Common Stock Retained Earnings Totals Beginning Balances, January 1, 2014 $ 0 $ 0 $ 0Common Stock Issued 10,000 10,000Net Income 4,400 4,400Less: Dividends Declared < 0> < 0>Ending Balances, January 31, 2014 $ 10,000 $ 4,400 $ 14,400

Our DVD, Inc. Balance Sheet

January 31, 2014

Assets LiabilitiesCurrent Assets Current Liabilities Cash $16,900 None Merchandise Inventory 3,500 Total Current Liabilities $ -0- Total Current Assets 20,400 Long-Term Liabilities Note Payable-Bank 6,000 Fixed Assets Total Liabilities 6,000 None 0 Owners’ Equity

Common Stock $10,000 Other Assets Retained Earnings 4,400 None 0 Total Owners’ Equity 14,400 Total Liabilities and Total Assets $ 20,400 Owners’ Equity $ 20,400

66

(Note the only time that Retained Earnings and Net Income will be the same is after the first year of operations).

Module 7 It’s a round ball and a round bat,

but you have to hit it square.Pete Rose

Continuing those accursed Debits and Credits

It is a shallow life that doesn’t give

a person a few scars.

67

Garrison Keillor

“Great occasions do not make heroes or cowards; they simply unveil them to the eyes of men. Silently and perceptibly, as we wake or sleep, we grow strong or weak; and last some crisis shows what we have become. ” ― Brooke Foss Westcott

Beamer Biz - 2015 On January 1, she issued a $100,000, 5 year, 5%, convertible bond. The bond is convertible into 500 shares of common stock. During 2015 (the second year) Chris bought 9 Beamers and sold 8 Beamers. Same prices as last year. When she bought the Beamers in the second year, she paid 40% down and will pay the balance in the following year. Also, when she sold the Beamers, she got 60% down and will receive the balance in the following year. During the year she paid cash for wages $24,000; utilities of $3,000; and rent of $8,000. She paid last year’s taxes. On May 1, she issued 200 shares of common stock for $ 25,000. At the end of the year, in addition to what she owed on the Beamers, she owed rent of $4,000 and wages of $2,000. At December 31, she paid a dividend of $5,000. At December 31 she paid the interest + $50,000 of principal due to Uncle Phil, the interest on the convertible bond. Tax rate is 30% and she paid ½ of 2015 taxes in 2015 with the remainder to be paid in 2016.

Remember the matching concept is _____________________________________________________________________________________________________________________!!

68

69

70

T Accounts

71

CASH

72

Financial Statements

73

74

Types of Income Statements

M___________________

Or S___________________

And C___________________

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Accounts ReceivableControlling and Subsidiary Accounts

Most sales of businesses, especially business to business sales, are on credit. When a business sells something, we debit accounts receivable and credit sales. The Accounts Receivable account is what is known as a controlling account. If we sell $100 worth of goods on credit to Jack and $150 worth of goods to Jill, also on credit, up to now, our two journal entries would look like this:

Accounts Receivable 100Sales 100

To record sale1

1For all the illustrations in this section, we are assuming that the appropriate entries to record the cost of goods sold would also be made.

75

Accounts Receivable 150 Sales 150

To record sale

Note that we have put all of the sales in the same receivable account. That is not really how a business handles these transactions. Actually, in a real business, the journal entries for the sales would be:

Accounts Receivable- Jack 100Sales 100

To record sale

Accounts Receivable- Jill 150 Sales 150

To record sale

Note that each customer has their own accounts receivable account. This makes sense as we want to keep track of collections and sales by customer. These individual accounts are called subsidiary accounts. Whenever we debit or credit accounts receivable, we debit and credit both the controlling and the subsidiary accounts. Thus, at any time, the balance in the controlling account is exactly equal to the total of the balances of all the subsidiary accounts.

Let’s go back to Jack and Jill. Assume that Jack buys $100 and Jill $150 as above. The next week Jill buys another $100 worth of stuff. During that week, Jack comes in the store and pays $50 on his bill. Prepare journal entries for all these transactions and prepare “T” accounts for both the controlling account and the subsidiary accounts.

1) Accounts Receivable- Jack 100 Control AccountSales 100

To record sale Accounts Receivable 1) 100 50 (4

2) Accounts Receivable- Jill 150 2) 150Sales 150 3) 100_________

To record sale 350______50 300

3) Accounts Receivable- Jill 100 Sales 100

To record sale Subsidiary Accounts Accounts Rec-Jack Accounts Rec-Jill

4) Cash 50 1) 100 50 (4 2) 150

76

Accounts Rec- Jack 50 50 3) 100_______ To record cash payment by Jack 250

Notice that each time an entry is made to the control account, an entry is also made to the appropriate subsidiary account(s) and that the ending balance in the control account (300), equals the total of all the ending balances in the subsidiary accounts (50 + 250).

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

When you pay for your purchase using a national credit card such as Master Card, the retail store you are buying the merchandise from, books the sale as a cash sale not as a credit sale. They deposit your Master Card slip in the bank just like they deposit the cash from sales. The bank deducts a collection fee- usually from 2-3%, and credits the net amount to the store’s account immediately. If the store has followed proper procedure in accepting the credit card, then any losses from bad debts or fraud belong to the bank, not the retail store.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Bad Debt ExpenseBusinesses that sell on credit will have bad debts (customers who do not pay). If they do not, they

might not be good business people-why?Now if we have people who do not pay us, two questions arise. When is the nonpayment

recognized? And is it an expense or a reduction in revenue?

Think about these questions then look at the next the page.

Answers:It should be recognized as an expense during the year the sale was made. Many times this is

impossible because it is much later that we find out the bum is not going to pay us. Businesses treat them as expenses because they are considered a normal cost of doing business. Secondly, they are treated as an expense to allow users of the financial statements to clearly see how much is being written off by the company.

So how do we decide how much the expense is? If we knew who wasn’t going to pay, we wouldn’t have sold to them! What companies do in these situations is make an estimate of how much of the current accounts receivable will ultimately be uncollected. They recognize this amount as an expense for the period. A problem arises as to what to credit. We credit a contra account which we call Allowance for Doubtful Accounts.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

A contra account is also known as a valuation account. You have already encountered another valuation account - remember accumulated depreciation? A valuation account is an

77

account which is used to adjust the balance of another account to which it is directly related. Contra accounts have a balance opposite to the account to which they are attached. Because Accounts Receivable has a debit balance, the Allowance for Doubtful Accounts will have a credit balance.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

In the instance at hand, we create an account called Allowance for Doubtful Accounts which is used to reduce the total Accounts Receivable to the amount we eventually expect to collect. Let’s work out an example.

At December 31, 2014, our company had a balance of $400,000 in Accounts Receivable and $12,000 in the Allowance for Doubtful Accounts. The allowance account was a normal balance. (A “normal balance” is one which is as expected. Thus, the normal balance for cash would be a debit balance. A normal balance for the Allowance for Doubtful Accounts would be a credit balance). During the year, we sold $1,200,000 worth of merchandise on account. (“On account” means that we sold the merchandise on credit). On May 1, 2014 we got notice that one of our customers, Mr. Redhawk, had gone bankrupt. Mr. Redhawk owed us $8,000 at the time of his bankruptcy. Additionally, the bill we sent to Mrs. Herd on July 1, 2014 had been returned marked “not at this address, no forwarding address available” so we wrote off the balance. The bill to Mrs. Herd had been for $500.00. On October 17, Mrs. Herd sent us a letter from Phoenix with a check that paid her bill in full. During the year we collected $1,250,000 from our credit customers. At December 31, 2014, we estimated that 3% of our receivables will never be collected. Prepare the journal entries to record all these transactions. (Record both the write off and the subsequent payment of Mrs. Herd). Prepare “T” accounts to record the transactions.

A) Accounts Receivable 1,200,000Sales 1,200,000

To record sales for the year

B) Cash 1,250,000Accounts Receivable 1,250,000

To record collections on accounts receivable during the year.

May 1, 2014 Allowance for Doubtful Accounts 8,000Accounts Receivable-Redhawk 8,000

To write off Mr. Redhawks’s receivable

July1, 2014 Allowance for Doubtful Accounts 500

78

Accounts Receivable- Herd 500To write off Mrs. Herd

Oct 17, 2014 Accounts Receivable-Herd 500Allowance for doubtful accounts 500

To reverse write off of Mrs. Herd’s account

Cash 500Accounts Receivable-Herd 500

To record Mrs. Herd’s paying of her account

Dec 31, 2014 Bad Debt Expense 6,245Allowance for Doubtful Accounts

6,245 To adjust ADA to 3% of ending Accounts Receivable balance.

(ADA= Allowance for Doubtful Accounts)

Accounts Receivable Allowance for Doubtful Accounts BB 400,000 1,250,000 (B 5/1 8,000 12,000 BB A) 1,200,000 8,000 5/1 7/1 500 500 10/17 10/17 500 500 7/1 8,500 12,500 500 10/17 4,000 1,600,500 1,259,000 6,245 12/31 341,500 10,245

341,500 * .03 = 10,245 amount needed as ending balance in ADA

onomatopoeia Module #3 "There's no business like show

taciturn Accounts Receivable business, but there are several businesses like accounting."

David LettermanAccounts Receivable

Controlling and subsidiary accounts

79

Slammin’ Sammy had $600,000 in Accounts Receivable at the beginning of the year. He also had $12,000 in the Allowance for Doubtful Accounts. Allowance for Doubtful Accounts is

and the T-Accounts look like

and the Balance Sheet looks like

Two ways of accounting for Bad Debts, % of ___________________ and % of A_____________ R_______________

The % of ________________ focuses on the I____________ S_________________

And the % of A_____________ R_______________, focuses on the B_________ S_________

We will be using __________________________

During the year Slammin’ Sammy sold $1,200,000 on account, he collected $900,000 from the customers and he wrote off $5,000 owed him by companies that went bankrupt. One of the companies who he wrote off, came back and paid him $1,000. At the end of the year, SS

80

estimates that 2% of his receivables will eventually prove uncollectible. Prepare journal entries for all these transactions and post the accounts receivable and allowance for doubtful accounts t-accounts.

81

Smokin’ Yokum sold $2,000,000 worth of Begees during the year on credit. At the beginning of the year his Accounts Receivable was $400,000 and his Allowance for Doubtful Accounts was $18,000. During the year he collected $1,500,000 of his Accounts Receivable. During the year he wrote off $22,000 in bad accounts. One of the customers who had owed him $2,000 and who he had written off, came back and paid in in full. At the end of the year he estimates that 5% of his receivables will never be collected. Prepare the all journal entries related to Accounts Receivable for the year and post the A/R & ADA T-accounts. Show how the results will appear on the financial statements.

82

2015 - Simms had total sales of $300,000. All of the company’s sales are on credit with terms of 2/10, net 30. At the beginning of the year, the company had a balance in Accounts Receivable of $26,000 and an Allowance for Doubtful Accounts of $1,000. At the end of the year, Accounts Receivable had a balance of $37,000 and an Allowance for Doubtful Accounts of $2,000.

First as to terms- 2/10 n/30 means

and costs

83

so why do?

now as to the receivable turn

Which tells us

and dividing the turn into 365

gives us A__________________ C___________________ P___________________.

Also known as D___________ S________________ O____________________.

What is an aging schedule?

Total Receivable Current 30-60 60-90 over 90

Able Co. 60,000.0

0 60,000.0

0

Acme Corp 40,000.0

0 38,000.0

0 2,000.

00

Baker Co 20,000.0

0 12,000.0

0 4,000.

00 4,000.

00

84

Zollar Co 80,250.0

0 60,250.0

0 20,000.0

0

Totals

236,965,374.87

223,885,462.25

9,000,486.57

3,236,582.95

842,843.10

Accounts Receivable and the Cash Flow Statement - Use N_____ Accounts Receivable

Homework

Problem 1 Sally sold $300,000 worth of stuff during the year (all on account). Her beginning balance in Accounts Receivable was $200,000 and her beginning credit balance in Allowance for Doubtful Accounts was $6,000. During the year she collected $280,000 on her receivables, and wrote off $9,000. She estimates that 3% of her receivables at any one time will not be collectable.Prepare all journal entries for the year related to the receivables (including any year end adjustment).

85

Problem 2 What is Sally’s average collection period?

Problem 3At December 31, 2012 Makenna’s balance in Accounts Receivable was $200,000 and the balance in Allowance for Doubtful Accounts was $4,000. During 2013 she had credit sales of $1,000,000. She collected $850,000 on her accounts receivable during 2013. She wrote off $3,000 of accounts receivable during 2013. One of the customers she wrote off came back and paid her $500. Makenna estimates that 2% of her receivables will never be collected. Prepare all journal entries and T-Accounts for 2013 related to the receivables, including any year-end adjustment. Show how this information will appear on the financial statements and calculate the accounts receivable turn and the average collection period.

86

Depreciation

When a company buys a fixed asset (accountanteze for buildings, machines, furniture, trucks and so forth) the cost of the asset, except land, must be allocated over the period the asset helps the company generate revenues. The period over which the asset is useful to the company in generating revenues is called its economic or useful life. Therefore, a definition of depreciation expense is the allocation of the cost of a fixed asset over its estimated useful life. To figure the amount of the expense for each year under the straight-line method of depreciation, we use the following formula:

87

Cost - Estimated Salvage ValueDepreciation Expense per year = Estimated Life of the Asset

Suppose we bought a truck to deliver our product. The truck cost us $30,000 and we estimate that we will use it for 3 years before it becomes too expensive to keep it going. We further estimate that at the end of the three years we will be able to sell it for $3,000. This $3,000 is the estimated salvage value (also termed the residual value).

So, when we buy the truck our journal entry is:

Truck 30,000 Cash (or loan payable) 30,000To record purchase of truck.

Then, at the end of the year, we would have the journal entry:

Depreciation expense 9,000 Accumulated Depreciation 9,000To record depreciation for the year.

Accumulated Depreciation is an enigmatic account for many students. It is a valuation account. It is also a contra account. Now let’s see what it really is. The truck account will remain the same, $30,000, until we sell or trade in the truck. The amount of depreciation we take on the truck will accumulate over the years we own it in the Accumulated Depreciation account. The cost minus the accumulated depreciation of any fixed asset is known as its book value. Consider the P & L and the Balance Sheet for each of the following years:

P&L Year 1 Year 2 Year 3 Sales

Cost of Good SoldGross MarginOperating Expenses: Xxxxx Expense Xxxxx Expense Depreciation Expense 9,000 9,000 9,000

Balance SheetCurrent Assets Xxxxxxx Xxxxxxx XxxxxxxTotal Current Assets

88

Fixed AssetsTruck 30,000 30,000 30,000Less: Accumulated

Depreciation < 9,000> <18,000> <27,000>Net Fixed Assets 21,000 12,000 3,000

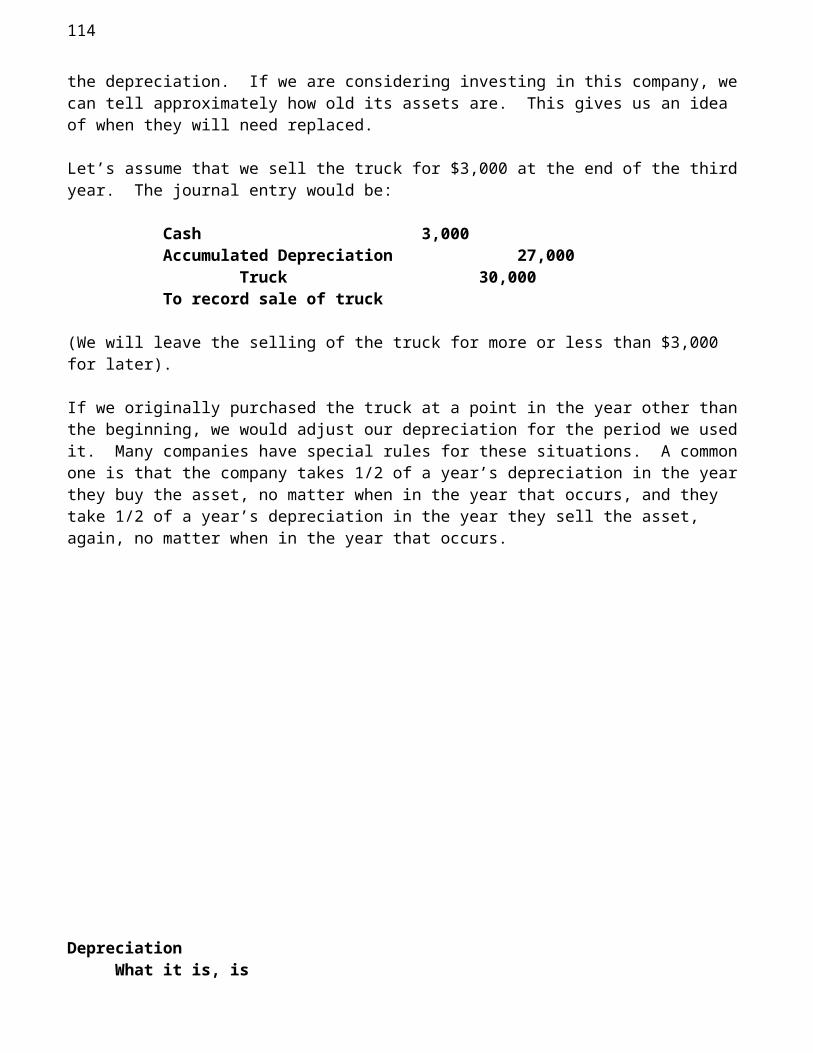

By accounting for the truck and its depreciation in this manner, we are imparting a lot more information than if we just credited the truck for the depreciation. If we are considering investing in this company, we can tell approximately how old its assets are. This gives us an idea of when they will need replaced.

Let’s assume that we sell the truck for $3,000 at the end of the third year. The journal entry would be:

Cash 3,000Accumulated Depreciation 27,000

Truck 30,000To record sale of truck

(We will leave the selling of the truck for more or less than $3,000 for later).

If we originally purchased the truck at a point in the year other than the beginning, we would adjust our depreciation for the period we used it. Many companies have special rules for these situations. A common one is that the company takes 1/2 of a year’s depreciation in the year they buy the asset, no matter when in the year that occurs, and they take 1/2 of a year’s depreciation in the year they sell the asset, again, no matter when in the year that occurs.

DepreciationWhat it is, is

89

You bought a new truck to use to deliver the Whatevers that you sell. The truck cost $30,000, will last for 4 years. At the end of 4 years, you figure you could sell it for $2,000.

Formula for Straight-Line Depreciation:

Journal Entries

T-Accounts

Goes on the Balance Sheet

Sale of Fixed AssetsOn June 30, 2015, Billy Bob sold a piece of equipment which he used in his business for $20,000. Billy Bob bought the equipment on January 1, 2011, for $60,000. When he bought the equipment, he estimated the life at 5 years and a $6,000 salvage value.

90

What if the equipment had been sold for $5,000?

InventoriesSpecific Identification

91

Weighted Average

LIFO _____________________________________

(Not used much anymore because of the I______________.)

FIFO means ___________ ___, __________ _____.

Inventory “turn”

and taking that one step further,

gives us the A____________ days __________ _____ _____________

And “Working Capital” is

Forensic Accounting

Cindy’s Best Buy Company had a fire. We know that her beginning inventory was $250,000. We also know that she purchased $400,000 worth of goods prior to the fire. Her gross margin averaged 40% of sales. Sales to the date of the fire, as best can be estimated, were $500,000. How much inventory did Cindy lose in the fire?

92

Estimating Inventory- (a forensic accounting tool)First a detailed Cost of Goods Sold Section

Mike K’s Golf Business (he left the CPAing to Terri and the staff) had a fire. Beginning inventory was $100,000. During the period up to the fire he had sales of $1,000,000. By calling all his vendors, he was able to establish that he purchased about $750,000 in merchandise prior to the fire. Assume that his average mark-up is 50%, how much inventory did he lose in the fire?

93

HomeworkProblem 1 Suzie’s Gymnastic Supply Company had a flood. Her ending inventory last year was $300,000. Her average markup is 140% of the cost of an item. Her sales to the date of the flood were 600,000. She had purchased $400,000 in inventory prior to the flood. How much inventory did she lose? Show your calculations.

94

Problem 2Gracie’s Gobbers, Inc. was robbed! She needs to file a claim for the loss with her insurance company. She knows that last year she ended the year with $475,000 in inventory and after going through her invoices she finds she had purchased $350,000 in inventory this year up to the date of the robbery. Her sales so far this year were $1,200,000. She estimates that her gross margin averages 45%. How much inventory did she lose in the robbery? Show your calculations

Problem 3Comparative Balance Sheets for Darby’s Doodles, Inc. are listed below:

December 31, 2015 2016

Cash 400 650

95

Accounts Receivable 600 800Inventory 1,000 1,300Plant and Equipment 1,000 1,050Accumulated Depreciation 325 600Accounts Payable 600 640Common Stock 1,000 1,000Retained Earnings 900 1,560

The following data relate to 2016:a) collections from credit customers, $30,000, cash sales $6,000b) payments to suppliers of merchandise $ 40,000c) purchases of equipment for cash, $50d) dividends paid to shareholders $500e) no plant and equipment was retired or sold during the year

1) For Darby, the Depreciation Expense for 2016 was

2) For Darby, the Sales Revenue for 2016 was

3) For Darby, the Net Income for 2016 was

4) The Cost of Goods Sold for 2016 was

MRyan Co., purveyor of fine, fine things, had the following balances at December 31, 2015:

Cash 40,000Accounts Receivable 60,000Allowance for doubtful accts 1,000Inventory 50,000 (1 thing)Equipment 190,000

96

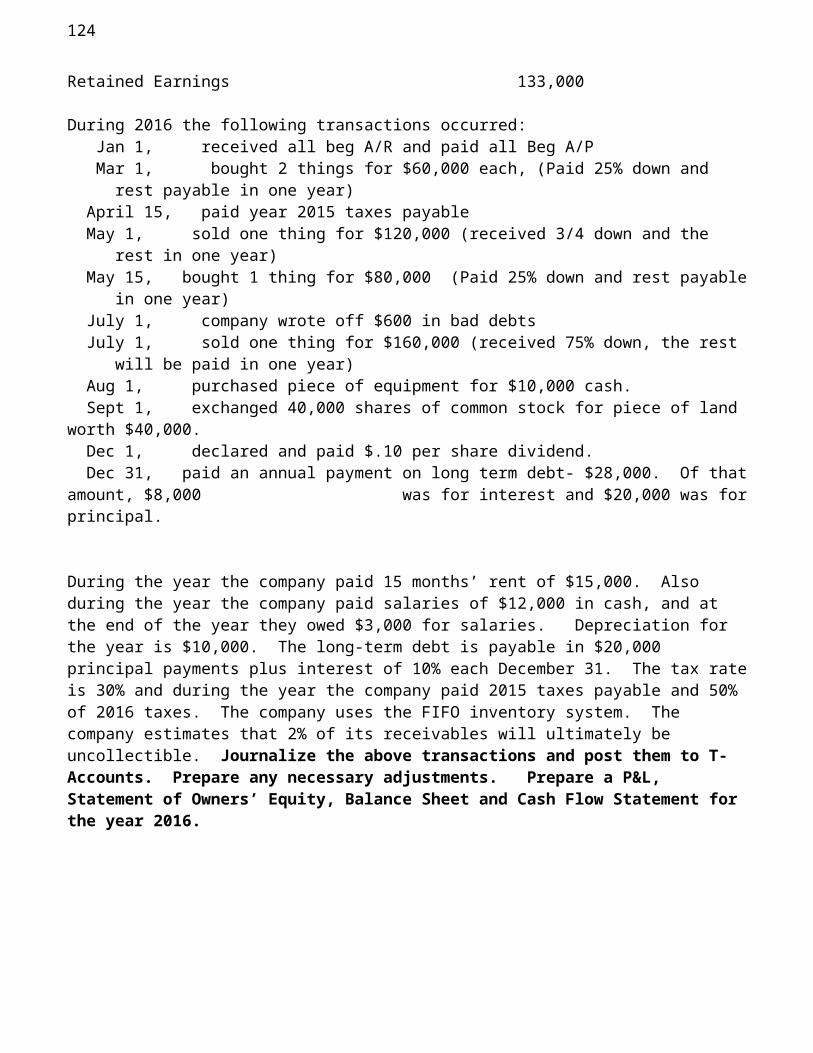

Accumulated Depreciation-Equipment 60,000Land 50,000Patent 20,000Accounts Payable 40,000Salary Payable 1,000Rent Payable 2,000Taxes Payable 3,000Long-Term Debt 80,000Common Stock ($1 per share) 90,000Retained Earnings 133,000

During 2016 the following transactions occurred: Jan 1, received all beg A/R and paid all Beg A/P Mar 1, bought 2 things for $60,000 each, (Paid 25% down and rest payable in one year) April 15, paid year 2015 taxes payable May 1, sold one thing for $120,000 (received 3/4 down and the rest in one year) May 15, bought 1 thing for $80,000 (Paid 25% down and rest payable in one year) July 1, company wrote off $600 in bad debts July 1, sold one thing for $160,000 (received 75% down, the rest will be paid in one year) Aug 1, purchased piece of equipment for $10,000 cash. Sept 1, exchanged 40,000 shares of common stock for piece of land worth $40,000. Dec 1, declared and paid $.10 per share dividend. Dec 31, paid an annual payment on long term debt- $28,000. Of that amount, $8,000

was for interest and $20,000 was for principal.

During the year the company paid 15 months’ rent of $15,000. Also during the year the company paid salaries of $12,000 in cash, and at the end of the year they owed $3,000 for salaries. Depreciation for the year is $10,000. The long-term debt is payable in $20,000 principal payments plus interest of 10% each December 31. The tax rate is 30% and during the year the company paid 2015 taxes payable and 50% of 2016 taxes. The company uses the FIFO inventory system. The company estimates that 2% of its receivables will ultimately be uncollectible. Journalize the above transactions and post them to T-Accounts. Prepare any necessary adjustments. Prepare a P&L, Statement of Owners’ Equity, Balance Sheet and Cash Flow Statement for the year 2016.

Prepaid Expenses and Accruals

(remember the matching principal is __________________________________________

____________________________________________________________________________

You started the year with a beginning balance in Rent Payable of $2,000.

97

You paid 15 months’ rent of $15,000. Record the journal entry.

You started the year with a beginning balance in Prepaid Rent of $2,000.You paid 8 months of rent of $16,000. Record the journal entry.

You started the year with $3,000 in Wages Payable. You paid $40,000 to your worker. You owed her $ 7,000 at the end of the year. Record the journal entries.

98

You started the year with $1,200 in Prepaid Insurance. This was for the final two years of a three year policy. What is the journal entry you would prepare at the end of the year to recognize the insurance expense for the year.

Extra Prepaid/Accrual ProblemsYou started the year with a beginning balance in Prepaid Rent of $2,000. You paid 13 months’ rent of $26,000. Record the journal entry.

99

You started the year with a beginning balance in Prepaid Rent of $4,000.You paid 6 months of rent of $12,000. Record the journal entry.

You started the year with $4,000 in Wages Payable. You paid $40,000 to your worker. You owed her $ 3,000 at the end of the year. Record the journal entry(s).

You started the year with $1,000 in Prepaid Insurance. This was six months of insurance on a policy that expires this year. On June 30, you purchased a two year policy for $3,000. Record the journal entries.

100

You started the year with a beginning balance in Rent Payable of $1,000.You paid 14 months’ rent of $14,000. Record the journal entry.

You started the year with a beginning balance in Prepaid Rent of $4,000.You paid 9 months of rent of $18,000. Record the journal entry.

You started the year with $5,000 in Wages Payable. You paid $50,000 to your worker. You owed her $ 10,000 at the end of the year. Record the journal entries.

You started the year with $ 750 in Prepaid Insurance. This was four months of insurance on a policy that expires this year. On May 1, you purchased a two year policy for $4,800. Record the journal entries.

101

You started the year with a beginning balance in Rent Payable of $1,000.You paid 14 months’ rent of $14,000. Record the journal entry.

You started the year with a beginning balance in Rent Payable of $4,000.You paid 9 months of rent of $18,000. Record the journal entry.

Without data, you are just another person with an opinion.

102

103

104

New Bunch of Difficulties“What we have here is just a bunch of difficulties” Cindy Kirch

Cindy, doing business as CK, Inc., had the following balances at the end of 2015:

Cash $100,000Accounts Receivable 52,000Allowance for Doubtful Accounts (2,000)

105

Inventory (80 difficulties @ 400 each) 32,000Prepaid Insurance 2,400Equipment 90,000Accumulated Depreciation 16,000Security Deposit 3,000Accounts Payable 13,000Wages Payable 6,000Taxes Payable 5,000Rent Payable 4,000 Note Payable 100,000Common Stock (20,000 shares) 2,000Capital In Excess of Par 18,000Retained Earnings 113,400

During 2016, the following transactions occurredPaid beginning accounts payable and received beginning accounts receivable.Purchased 600 difficulties at $450 each, 25% down and the rest payable in one yearSold 500 Difficulties for $800 each. Customers paid 1/2 down and the rest in one year.Paid cash wages of $40,000 and owed $5,000 at the end of the year.Paid last year’s taxes.

The prepaid insurance is for a three-year policy taken out in 2015. The policy had exactly two years left on it at the beginning of 2016.

The beginning equipment originally cost $90,000, had a $10,000 salvage value and was expected to last ten years from the date of its purchase. On January 1, Cindy purchased a new truck. The cost was $60,000. She put $10,000 down and will pay the rest in 4 equal annual payments of $14,429.57, which include interest at 6%. She made the first payment on December 31, 2016.The truck is expected to last for 6 years and then be worth $6,000.The rent is $4,000 per month and during 2016 Cindy paid the landlord $56,000.On December 31, 2016, Cindy paid the annual payment on the Note Payable of $20,000 plus

interest at 10%.Paid $10,000 in advertising during the year and owed $2,000 in advertising at end of year.On October 1, 2016, CK, Inc. paid cash of $5,000 and issued 1,000 shares of common stock in

exchange for a piece of land worth $15,000.The tax rate is 30% and she paid ½ of 2016 taxes in 2016. She will pay the rest in 2017.During the year the company wrote off $1,500. One customer who was written off, came back

and paid $200. The company estimates that 2% of accounts receivable will ultimately not be collected.

During the year the company paid $25,000 in dividends.Cindy uses the FIFO inventory system.

Prepare Journal Entries, T-Accounts, an Income Statement, a Statement of Owners’ Equity, and a Balance Sheet for CK, Inc.

106

107

108

109

110

111

112

113

Cash Flows Happiness is different from pleasure

114

Happiness has something to do with struggling and enduring and accomplishing.

George Sheehan Back Brain Stuff-

Format for the Cash Flow Statement Two Types of Format, D________ and I__________ Vast majority of world uses __________________ and we will use both _________________________

Company NameStatement of Cash Flows

For the (Period) Ending (Date)

Operating ActivitiesNet Income $ xx,xxxAdd: Depreciation Expense x,xxxAdd: Amortization Expense x,xxxAdd: Loss on Sale of Fixed Asset(s) x,xxxLess: Gain on Sale of Fixed Asset(s) <x,xxx>Increase in (current asset account name) < x,xxx>Decrease in (current asset account name) x,xxxDecrease in (current asset account name) x,xxxIncrease in (current liability account name) x,xxxDecrease in (current liability account name) < x,xxx>

Increase in (current liability account name) x,xxx Cash Provided By Operating Activities -or-Cash Used For Operating Activities xx,xxx or <xx,xxx> Investing Activities

Purchase(s) of (fixed asset account name) <$ xx,xxx>Purchase(s) of (fixed asset account name) < xx,xxx>Sale(s) of (fixed asset account name) x,xxxPayment of Security Deposit < x,xxx>Refund of Security Deposit x,xxx

Cash Provided By Investing Activities -or- Cash Used For Investing Activities xx,xxx or <x,xxx>

Financing ActivitiesNew Borrowing(s) xx,xxxPayment(s) on (description of debt) < x,xxx>Issuance(s) of Common Stock x,xxxPurchase(s) of Treasury Stock < x,xxx>Payment of Dividends < x,xxx>Issuance(s) of Bonds x,xxxRedemption of Bonds < xx,xxx>

Cash Provided By Financing Activities -or- Cash Used for Investing Activities xx,xxx or <xx,xxx>Increase in Cash -or- Decrease in Cash xx,xxx or <xx,xxx>Beginning Cash, (Date) xx,xxxEnding Cash, (Date) $ xx,xxx

Supplemental Cash Flow Information Cash payments for income taxes $ x,xxx Cash payments for interest x,xxx Noncash investing and financing activities

(Description of transaction) x,xxx(Description of transaction) x,xxx

From the following information for Molly’s Munchies, prepare a Statement of Cash Flows for the year ended December 31, 2014 using the indirect method.

115

The following data is for Molly’s Munchies: Balance Balance 12/31/14 12/31/13

Cash 80,000 20,000Accounts Receivable 68,000 35,000Inventory 70,000 90,000Prepaid Insurance 500 3,000 Equipment 340,000 270,000Accumulated Depreciation 80,000 20,000Land 120,000

Security Deposits 12,000 10,000 Accounts Payable 35,000 30,000

Wages Payable 6,000 10,000Rent Payable 7,500 6,000Interest Payable 6,000 7,000Taxes Payable 16,000 5,000Note Payable 120,000 140,000Common Stock ($1 each) 300,000 160,000Retained Earnings 120,000 50,000Sales 1,200,000Cost of Goods Sold 575,000Wage Expense 260,000Rent Expense 24,000Office Expenses 70,000Depreciation Expense 60,000Advertising Expense 15,000Insurance Expense 9,000Interest Expense 14,000Income Tax Expense 52,000

Some of the equipment was acquired on March 31, 2014 by exchanging 60,000 shares of common stock worth $60,000. The additional common stock (other than that issued for the purchase of the equipment) was sold on June 30, 2014 for $1 per share. The company did not sell any equipment during the year. All the rest of the equipment and the land purchased during the year was purchased for cash. The retained earnings balance for both years is after all closing entries have been made. The Note Payable requires payments of $20,000 principal plus interest at 10% on June 30th of each year. Current market price is $5.00 per share

116

Now you do one - Not dying is not the same as living.

117

The following balances are for Misty Company at December 31,

2013 2014Cash 10,000 30,000Accounts Receivable 40,000 50,000Inventory 80,000 60,000Prepaid Rent 6,000 3,000Equipment 180,000 210,000Accumulated Depreciation-Equipment 50,000 60,000Security Deposit 8,000 9,000Accounts Payable 40,000 50,000Salaries Payable 10,000 -0-Interest Payable -0- 5,000Taxes Payable -0- ______Note Payable 100,000 70,000Common Stock 10,000 50,000Retained Earnings 114,000 124,000Sales 200,000Cost of Goods Sold 100,000Salary Expense 40,000Rent Expense 24,000Interest Expense 6,000Depreciation Expense 10,000

The common stock outstanding was 10,000 shares on January 1, 2014. On April 1, 2014, Misty issued 10,000 shares of common stock in exchange for $10,000 of equipment. On July 1, 2014, Misty sold an additional 30,000 shares of common stock. During 2014, the company paid a dividend of _____________. No equipment was sold during the year. The tax rate is 30% and 1/2 of 2014 taxes were paid in 2014.

On the next page, prepare a Statement of Cash flows in good form using the indirect method.

A word to the wise ain't necessary -- it's the stupid ones that need the advice. - Bill Cosby

118

Bobcat Bob, Inc. Bobcat Bob, Inc. Income Statement Balance Sheet

For the Year Ended December 31, 2015 December 31,

119

Sales $ 480,000 2015 2014Cost of Goods Sold 240,000 Assets Gross Margin 240,000 Current AssetsOperating Expenses Cash $ 26,200 $ 16,800 Salary Expense $124,000 Accounts Receivable 45,000 38,000 Insurance Expense 12,000 Allowance for Bad Debt Expense 300 Doubtful Accounts 1,200 1,000 Depreciation Expense 2,400 Net Accounts Receivable 43,800 37,000 Total Operating Expenses 138,700 Inventory 10,000 11,000 Operating Income 101,300 Prepaid Insurance _ 100 ______ Other Revenues & <Expenses> Total Current Assets 80,100 64,800 Interest Expense (4,200) Property and Equipment Gain on sale of Equipment 500 Furniture & Fixtures 186,000 130,000 Net Other Revenue (Expense) (3,700) Less: AccumulatedTaxable Income 97,600 Depreciation (19,400) (20,000) Tax Expense 29, 280 Net Property and Equipment 166,600 110,000 Net Income $68,320 Other Assets

Patents 500 100

Earnings Per Share $22.57 Total Assets $247,200 $174,900

Liabilities Current Liabilities Accounts Payable $ 17,000 $ 2,000 Salaries Payable 1,000 Taxes Payable 12,100 13,120 Advertising Payable 100

Current Portion of Long-term Debt 10,000 10,000

Total Current Liabilities 40,100 25,220 Long-Term Debt

Note Payable-Bank 50,000 60,000 Total Long-Term Debt 50,000 60,000

Total Liabilities 90,100 85,220 Owners’ Equity Common Stock ($1 par) 3,100 3,000

Capital in Excess Par 30,000 21,000 Retained Earnings 124,000 65,680

Total Owners’ Equity 157,100 89,680 Total Liabilities

& Owners’ Equity $247,200 $174,900

On June 30, the company sold a piece of equipment which had cost $3,500, had accumulated depreciation of $3,000 for $1,000. The Note Payable-Bank is payable at $10,000 per year plus interest at 6% on December 31 of each year. The company wrote off one account which owed $100 during the year. The company paid a dividend during the year. On June 30, the company exchanges 10 shares of stock for equipment worth $1,000. The additional common stock, other that traded for equipment was sold on October 1, 2015 for cash. The additional equipment, other than that exchanged for stock, was purchased for cash.

120

Cash Flow Homework

121

Problem 1 From the following information for Kevin’s Kennels, prepare a Statement of Cash Flows for the year ended December 31, 2014.

The land was acquired on March 31, 2014 by exchanging 60,000 shares of common stock worth $60,000 and cash for the balance of the purchase price. The additional common stock (other than that issued for the purchase of the land) was sold on September 30, 2014 for $1 per share. The company did not sell any equipment during the year. All equipment purchased during the year was purchased for cash. The retained earnings balance for both years is after all closing entries have been made. The Note Payable requires payments of $20,000 principal plus interest at 10% on June 30th of each year.

Problem 2 CoJo’s Colts, Inc. Balance Balance

12/31/15 12/31/14

122

Balance 12/31/13

Balance 12/31/14

Cash 28,900 81,900Accounts Receivable 45,000 78,000Inventory 90,000 70,000Prepaid Insurance 2,600 3,600Equipment 280,000 320,000Accumulated Depreciation 20,000 80,000Land 130,000Security Deposits 20,000 32,000Accounts Payable 30,000 35,000Wages Payable 10,000 6,000Rent Payable 4,000 8,000Interest Payable 7,500 6,500Taxes Payable 5,000 10,000Note Payable 150,000 130,000Common Stock ($1 each) 160,000 310,000Retained Earnings 80,000 130,000Sales 1,200,000Cost of Goods Sold 700,000Wage Expense 220,000Rent Expense 48,000Office Expenses 46,000Depreciation Expense 60,000Utilities Expense 15,000Insurance Expense 6,000Interest Expense 14,000Income Tax Expense 27,000

Cash 97,600 88,900Accounts Receivable 90,000 50,000Allowance for Doubtful Accounts 3,600 2,000Inventory 120,000 40,000Prepaid Insurance 2,900 3,600Prepaid Rent 0 3,000Equipment 320,000 220,000Accumulated Depreciation 50,000 20,000Land 100,000

Security Deposits 8,000 10,000 Accounts Payable 35,000 30,000

Salaries Payable 6,000 10,000Rent Payable 3,000 0Interest Payable 9,000 10,000Taxes Payable 10,000 5,000Note Payable 180,000 200,000Common Stock ($1 each) 160,000 50,000 Retained Earnings 281,900 88,500Sales 1,400,000Cost of Goods Sold 700,000Salary Expense 185,000Rent Expense 36,000Advertising Expense 85,000Office Expenses 27,000Depreciation Expense 30,000Utilities Expense 12,000Bad Debt Expense 6,500Insurance Expense 6,000Miscellaneous Expense 3,000Interest Expense 9,500Income Tax Expense 90,000