sevakarahmedabad.nic.insevakarahmedabad.nic.in/doc/cmmr/2012/04-2012.doc · web viewdev arc...

TRANSCRIPT

35

BRIEF FACTS OF THE CASE :-

M/s. Dev Arcade Pvt. Ltd., "Dev Arc", (hereinafter referred to as “M/s Devarc”) Near Fun Republic, Isckon Cross Roads, S.G. Highway, Ahmedabad are engaged in the business of Construction of Commercial & Residential Building and Real Estate Service and holding service tax registration for Real Estate Agent. Intelligence gathered revealed that the service provider had under taken some big construction projects under the brand name of 'Dev' and they had not paid service tax either in the category of Real Estate Agent Service or Construction of Commercial & Residential services, since July'2005.

02. Searches were carried out at the residence and office premises of “M/s. Devarc” on 15.03.2007 under the authority of Search Warrant No. 51 & 52 / 2006-07 respectively. Relevant records were withdrawn under panchnama dtd.15.03.2007 drawn at the office premises.

03. During the search at said office and from the examination of the records withdrawn from their office, it was observed that the said company was incorporated in June 2005 and presently was engaged in organization / supervision of construction work of 'Dev Arc Mall’ being constructed by M/s. Dev Arc (Jodhpur) Commercial Co.Op Society Ltd., Jodhpur, Ahmedabad. There are approximately 158 shops / offices in ‘Dev Arc Mall’ and booking of shops / offices had been done. Further, approximately 60% of construction was completed at the time of search. M/s. Dev Arcade Pvt. Ltd., had entered into an agreement with the said society for helping in arranging of labours, supervisors and experts in the field of construction and to supervise the scheme. As per the agreement, “M/s. Devarc” were entitled to receive organization / supervision charges equal to 7% of the amount of construction work. Vide letter dtd. 19.05.2009 “M/s. Devarc” had informed that organizing fees had been increased from 7% to 10.65% of the project cost during the year 2007-08. Shri Sanjay Hiralal Thakkar, Chairman of the said company had admitted that their company was liable to pay Service Tax under the category of 'Real Estate Agent' (which includes 'Real Estate Consultant's Service') on such organization / supervision charges. As per Profit & Loss Account during the year 2005-06, Income-Tax return filed by them for the assessment year 2006-07 alongwith Balance Sheet ending 31.03.2006 and Ledger for the period 2005-06, “M/s. Devarc” had charged Rs.30,25,068/- as organization / supervision charges from M/s. Dev Arc (Jodhpur) Commercial Co-Op Society, Jodhpur, Ahmedabad.

04. “M/s. Devarc” had furnished profit & Loss Accounts and the Balance sheet for the year ending March 31, 2007. Thereafter, they had also furnished ledger account for the years 2005-06 & 2006-07. From which it was noticed that they had collected an amount of Rs.2,16,88,624/- during the year 2006-07 as organization / supervision charges. As per statement showing the construction cost, they had also collected supervision charges amounting to Rs.3,13,99,053/- for the year 2007-08. On this account, “M/s. Devarc” had produced a cheque of Rs.7,00,000/- towards payment of Service Tax for the year 2005-06, 2006-07 under the category of 'Real Estate Agent service' which includes services of 'Real Estate Consultant'. They had also made payment of service tax of Rs.8,11,725/- + Ed. Cess Rs.16,234/- + Rs.2,000/- as penalty vide challan dated 19.05.08.

05. The Real Estate Agent Services were brought in the Service Tax net by the Finance (ii) Act, 1998 w.e.f. 16.10.1998.

The taxable service means any service provided or to be provided, to any person, by a Real Estate Agent in relation to Real Estate (Section 65(105)(v). As per Section 65 (88) of he Finance Act, 1994, ‘Real Estate Agent’

35

which includes services of ‘Real Estate Consultant’ has been defined as follows :-“Real Estate Agent” means a person who is engaged in rendering any service in relation to sale, purchase, leasing or renting, of real estate and includes a real estate consultant which is defined in Section 65(89) as follows :“Real Estate Consultant” means a person who renders in any manner, either directly or indirectly, advice, consultancy or technical assistance, in relation to evaluation, conception, design, development, construction, implementation, supervision, maintenance, marketing, acquisition or management, of real estate.”

06. As per agreement dtd. 01.10.2005 executed between M/s. Dev Arc (Jodhpur) Commercial Co. Society Ltd. and “M/s. Devarc” it was agreed upon vide Point No.5 which reads as 'As a consideration for execution and carrying out of various job-work or functions entrusted by the society to the company, the society shall pay and company would receive, amount as organization / supervision charges equal to 7% for the year 2005-06, 2006-07 and @ 10.65% for the year 2007-08, of the amount of construction work as certified by Architect of the society. The company would raise its bills on the society in respect of the job-work or functions executed by it once every year, on or before the end of the financial year ending on 31st March and the society would make payment to the company, subject to deduction of income tax, as early as possible after 31st March every year, of such amounts against the bills so raised by company, as are certified by separate experts engaged by the society.

07. On examination of the records, such as Balance sheets, profit & loss account for the year 2005-06 to 2008-09, it was noticed that “M/s. Devarc” had collected the supervision charges of Rs.30,25,068/-, Rs.2,16,88,624/-, Rs.3,13,99,053/- and Rs.1,26,96,322/- for the year 2005-06, 2006-07, 2007-08 and 2008-09 respectively from M/s. Dev Arc (Jodhpur) Commercial Co-Op Society Ltd., as per terms and conditions laid down in the said agreement between them. Therefore, their services were liable to be charged under 'Real Estate Agent's Service' (which includes Real Estate Consultant) as defined here in above.

08. “M/s. Devarc” had been issued certificate of registration under Section 69 the Finance Act, 1994 (32 of 1994) on 11.07.2007 for services of “Real Estate Agent” and their Registration No. was AACCD1788PST001 given by Range Superintendent, Service Tax, Ahmedabad.

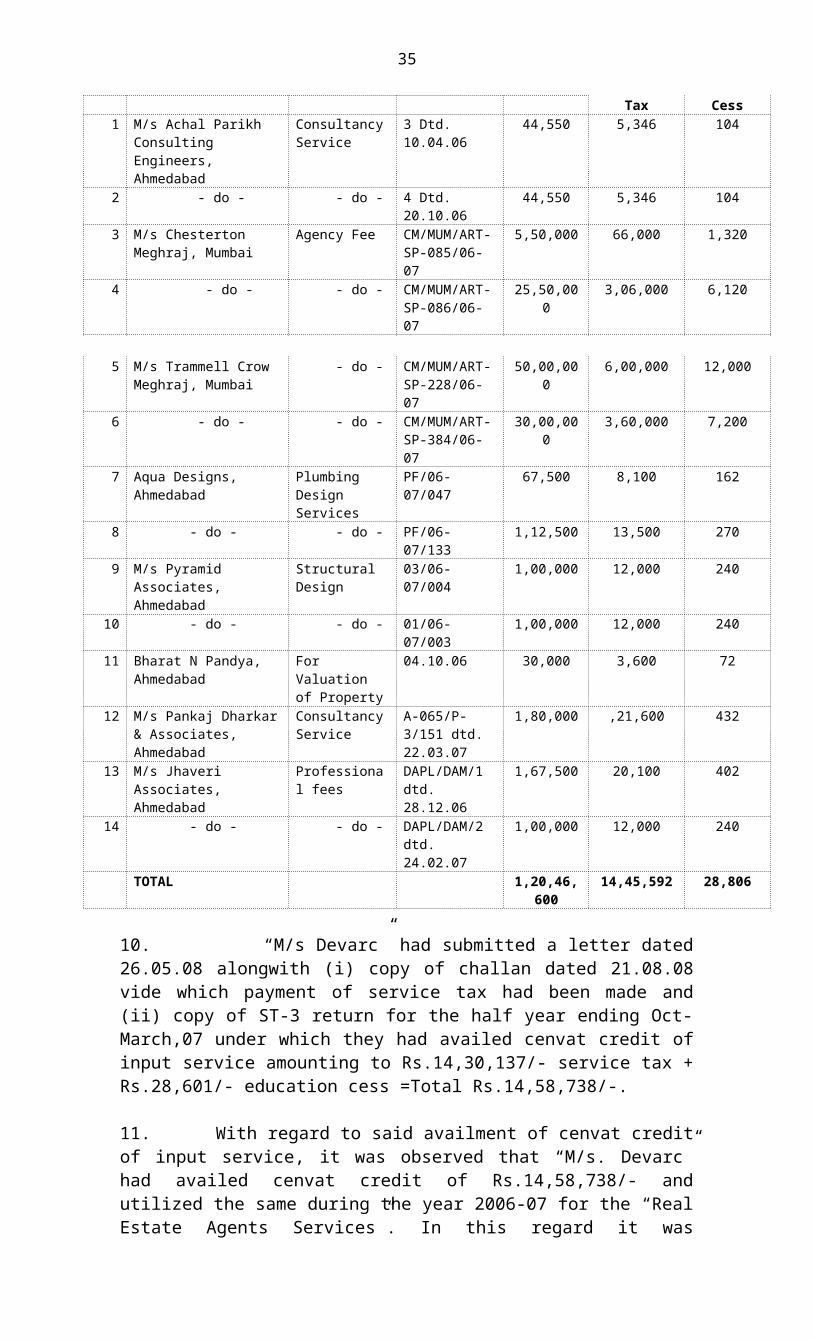

09. “M/s. Devarc” vide their letter dtd.10.10.07 had furnished Profit & Loss A/C (Provisional) for the year 2006-07 and the copy of invoices of their clients, as per details given in following table, who had provided the services such as consultancy services, agency fee, plumbing design services, structural design services, preparing valuation of property services, electrical design services etc. under which Service Tax + Edu. Cess had been paid.

Sr. No.

Name of the party Particulars Bill No. & Date Amt. of Bill charged

Amt. of Service Tax paid

Service Tax Edu. Cess1 M/s Achal Parikh

Consulting Engineers, Ahmedabad

Consultancy Service

3 Dtd. 10.04.06 44,550 5,346 104

2 - do - - do - 4 Dtd. 20.10.06 44,550 5,346 1043 M/s Chesterton Meghraj,

MumbaiAgency Fee CM/MUM/ART-

SP-085/06-075,50,000 66,000 1,320

4 - do - - do - CM/MUM/ART-SP-086/06-07

25,50,000 3,06,000 6,120

35

5 M/s Trammell Crow Meghraj, Mumbai

- do - CM/MUM/ART-SP-228/06-07

50,00,000 6,00,000 12,000

6 - do - - do - CM/MUM/ART-SP-384/06-07

30,00,000 3,60,000 7,200

7 Aqua Designs, Ahmedabad

Plumbing Design Services

PF/06-07/047 67,500 8,100 162

8 - do - - do - PF/06-07/133 1,12,500 13,500 2709 M/s Pyramid Associates,

AhmedabadStructural Design

03/06-07/004 1,00,000 12,000 240

10 - do - - do - 01/06-07/003 1,00,000 12,000 24011 Bharat N Pandya,

AhmedabadFor Valuation of Property

04.10.06 30,000 3,600 72

12 M/s Pankaj Dharkar & Associates, Ahmedabad

Consultancy Service

A-065/P-3/151 dtd. 22.03.07

1,80,000 ,21,600 432

13 M/s Jhaveri Associates, Ahmedabad

Professional fees

DAPL/DAM/1 dtd. 28.12.06

1,67,500 20,100 402

14 - do - - do - DAPL/DAM/2 dtd. 24.02.07

1,00,000 12,000 240

TOTAL 1,20,46,600 14,45,592 28,806

10. “M/s Devarc” had submitted a letter dated 26.05.08 alongwith (i) copy of challan dated 21.08.08 vide which payment of service tax had been made and (ii) copy of ST-3 return for the half year ending Oct-March,07 under which they had availed cenvat credit of input service amounting to Rs.14,30,137/- service tax + Rs.28,601/- education cess =Total Rs.14,58,738/-.

11. With regard to said availment of cenvat credit of input service, it was observed that “M/s. Devarc” had availed cenvat credit of Rs.14,58,738/- and utilized the same during the year 2006-07 for the “Real Estate Agents Services”. In this regard it was submitted that “M/s. Devarc” had provided their services to supervise the scheme in the field of construction of "Dev Arc Mall" to M/s. Dev Arc (Jodhpur) Society and collected supervision charges during the year 2005-06 to 2007-08. The construction work of said “Dev Arc Mall” was carried out by the said society. Further, on going through input invoices, it was noticed that the said input invoices furnished by “M/s. Devarc” were meant for services of structural consultancy, Agency fee for leasing of retail space to Magnet, Plumbing Design as professional fees, structural design, fees for valuation of property, fees for electrical design, etc., which were input services for the said Dev Arc (Jodhpur) Commercial Co. Op. Soc. Ltd. which had carried out the construction work. The said “M/s. Devarc” had provided only their supervision services for construction. Thus, the services sought for and claimed by “M/s. Devarc” can not be considered as their input services. In fact these services were input services of the construction service. Therefore, it appeared that Cenvat Credit amounting to Rs. 14,58,738/- of various services mentioned therein was not available to them as these services were not input services for Real Estate Consultant services and was required to be recovered from them. On the similar ground cenvat credit of Rs.16,28,569/- availed and utilized during the year 2007-08 was also required to be demanded and recovered from them.

12. A statement of Shri Deepakbhai A. Thakkar, Director of the said M/s. Dev Arcade Pvt. Ltd., was recorded on 21.04.2010 wherein he agreed to the supervision charges income as reflected in their Balance sheet/ledgers. The same are as under:

Year Supervision charges charged (Rs.)2005-06 30,25,0682006-07 2,16,88,6242007-08 3,13,99,0532008-09 1,26,96,322Total 6,88,09,067

35

12.1 He also agreed and confirmed to income of rent reflected in their balance sheet / ledgers. The same were as under :-

Year Amount of rent collected (Rs.)2007-08 2,36,23,6222008-09 2,61,30,751Total 4,97,54,373

12.2 He had also submitted photocopies of rent agreement of following parties viz. Infinity Retail Ltd dated 26.03.2007, M/s Net Hot Zone Media Pvt. Ltd dated 27.01.2009, M/s Mx Foods Pvt Ltd dated 26.04.2008, M/s Reliance Communications Ltd. dated 27.01.2009, M/s Fascel Ltd. (Vodafone) dated 11.01.2007, M/s Weizman Forex Ltd. dated 27.12.2008, M/s Astha Enterprise (Baskin & Robbins) dated 15.04.2008, M/s Havmor Restaurant Pvt. Ltd. dated 08.05.2008, M/s Peora Fashions Pvt. Ltd. dated 18.04.2008, M/s Wireless TT Info Services Ltd. dated 03.12.2008. In respect of agreement with M/s. Fascel (Vodafone) Ltd, he stated that they had provided facility for display of hoardings to advertise their products and therefore income earned from them fall under the service category of Selling of Space or Time Selling' services for Advertisement. The year wise income were produced by him, which was as follows as an amount of rent under “Selling of Space or Time Selling services for Advertisement”. Except M/s. Fascel Ltd. (Vodafone) all the income received as per ledger of Rent/financial account were income towards giving space/area (kiosk) on rent for selling their products and therefore the same fall under the category of “Renting of Immovable property” and the amount towards the same were detailed in the table as below.

Amount of Rent under Amount of Rent under" Selling Amount of Year "renting of immovable of Space or Time Selling' Rent collected

properties" services for Advertisement" (Rs.) 2007-08 2,19,39,986/- 16,83,636/- 2,36,23,622/- 2008-09 2,44,49,515/- 16,81,236/- 2,61,30,751/-

Total 4,63,89,501/- 33,64,872/- 4,97,54,373/-

12.3. Further he stated that as per ledger 2008-09 of rent income, their company had earned rent income from 14 different parties as mentioned in the ledger and out of said 14 parties, they had submitted copies of agreements in respect of 10 parties as mentioned in above para. In respect of other parties viz. M/s Bunjee Jumping, Mama Mukhwas, Khushi Advt., Cookie Man Australia, he stated that they had not entered into written agreement and their firm was earning income of rent as per oral agreements towards space provided to them for selling their products which fell under the category of under "renting of immovable properties" as per provision of Finance Act, 1994 relating to Service tax matter.

12.4. He further stated that M/s Dev Arcade Pvt. Ltd. had entered into agreements with M/s Infinity Retail Ltd. dated 26.03.2007, M/s Reliance Communications Ltd. dated 27.01.2009 and M/s Wireless TT Info Services Ltd. dated 03.12.2008.

12.5. He also stated that Dev Arc (Jodhpur) Commercial Co-operative Society had entered into agreements with M/s. Net Hot Zone Media Pvt. Ltd. dated 27.01.2009, M/s Mx Foods Pvt. Ltd. dated 26.04.2008, M/s Weizman Forex Ltd. dated 27.12.2008, M/s Astha Enterprise (Baskin & Robbins) dated 15.04.2008, M/s Havmor Restaurant Pvt. Ltd. dated 08.05.2008, M/s Peora Fashions Pvt. Ltd. dated 18.04.2008.

35

12.6. He also stated that Mr. Sanjaybhai Hiralal Thakkar had entered into agreement with M/s Fascel Ltd. (Vodafone) dated 11.01.2007.

12.7. He also stated that “M/s Devarc” had agreed orally with M/s. Bunjee Jumping, Mama Mukhwas, Khushi Advt. and Cookie Man, Australia for giving space / area for renting purpose. No written agreement was worked out so they had not submitted the same.

12.8. He had also stated that ownership of Dev Arc mall was vested with the M/s. Dev Arc (Jodhpur) Commercial Society Ltd. The said society had given authorization to them to enter into agreement with various parties and to collect rent and to utilize the same by their firm. He has also stated that they had not availed any Cenvat Credit for Rent Income but had availed / utilized Cenvat Credit for providing Organizing services as the said input services were solely utilized by their firm.

13. Statement of said Shri Deepak Ajitbhai Thakkar was again recorded on 01.10.2010. He was shown his company's letter dated 07.09.2010 addressed to the Superintendent (Preventive), Service Tax, Group I, Ahmedabad wherein total amount of Rs.6,88,09,067/- was shown for the period 2005-06 to 2008-09 as the total amount of Supervision charges. He also submitted in the said letter that as per the provision of Rule 6, the Service provider was liable to make payment of service tax on the realization of value of services. He also further added in the said letter that they had charged their said fees to the society at the end of every year and the said value of their fees was still unrealized and outstanding with the society. However, in order to co operate with the department, they had paid Service Tax on their said fees under the category of Real Agents Services .. In this regard he had confirmed in his said statement dated 01.10.2010 that they had paid Service Tax liability of Rs. 13,07,721/- vide Challan dated 01.09.2010, Rs. 22,52,354/- vide challan dated 03.09.2010, Rs. 7,00,000/- vide challan dated 15.03.2007 and Rs. 8,29,959/- vide challan dated 19.05.2008. Thus they had paid total Rs. 50,90,035/- vide cash payment vide GAR 7 Challan for the period 2005-06 to 2008-09.

13.1. He also stated that they had also made payment through cenvat credit account amounting to Rs. 30,87,307/- for the period 2006-07 and 2007-08. That they had discharged total Service Tax liability of Rs. 81,77,342/- (Rs. 50,90,035/- by cash GAR Challan + Rs. 30,87,307/- by debiting Cenvat Credit) as mentioned in their letter dated 07.09.2010.

13.2 He had also produced a copy of a resolution passed by the committee of the Dev Arc (Jodhpur) Commercial Co. Operative Society Ltd. dated 01.02.2007 vide which it was suggested that against the huge outstanding amount which was due from the Society to “M/s. Devarc” the society may give a lien over the un-allotted property in favour of “M/s. Devarc” the Supervisor of the said Society, for their own use or for renting out the same. Therefore, it was resolved to give lien over the un-allotted property in favour of “M/s Devarc” for their own use or for renting out the same. However, “M/s Devarc” was not entitled to sell the un-allotted property but the income realized was to belong to “M/s Devarc”.

13.3. He also stated that they had collected rent from various companies who were allotted such property and they had realized an amount of Rs. 4,97,54,373/- from them as follows:

35

Year Amount of

Rent collected (Rs.)

Amount of Rent under "renting of immovable

properties"

Amount of Rent under" Selling of Space or Time Selling'

services for Advertisement"

2007-08 2,36,23,622/- 2,19,39,986/- 16,83,636/-

2008-09 2,61,30,751/- 2,44,49,515/- 16,81,236/-Total 4,97,54,373/- 4,63,89,501/- 33,64,872/-

13.4. He was explained provisions of "renting of immovable property" service as defined under clause (90a) of Section 65 of Finance Act, 1994 as amended which is liable to Service Tax w.e.f. 01.06.2007. The same is as under:

(90a) “renting of immovable property” includes renting, letting, leasing, licensing or other similar arrangements of immovable property for use in the course or furtherance of business or commerce but does not include —(i) renting of immovable property by a religious body or to a religious body; or(ii) renting of immovable property to an educational body, imparting skill or knowledge or lessons on any subject or field, other than a commercial training or coaching centreExplanation 1—For the purposes of this clause, “for use in the course or furtherance of business or commerce” includes use of immovable property as factories, office buildings, warehouses, theatres, exhibition halls and multiple-use buildings;]Explanation 2.— For the removal of doubts, it is hereby declared that for the purposes of this clause “renting of immovable property” includes allowing or permitting the use of space in an immovable property, irrespective of the transfer of possession or control of the said immovable property

13.5 He was explained provisions of “Selling of Space or Time Selling” services for Advertisement as defined under sub clause (zzzm) of clause (105) of Section 65 of Finance Act, 1994 as amended which is liable to service tax w.e.f. 1.5.06. The same is as under :-

(zzzm) to any person, by any other person, in relation to sale of space or time for advertisement, in any manner; but does not include sale of space for advertisement in print media and sale of time slots by a broadcasting agency or organisation.

Explanation 1.-For the purposes of this sub-clause, "sale of space or time for advertisement" includes,-

(i) providing space or time, as the case may be, for display, advertising, showcasing of any product or service in video programmes, television programmes or motion pictures or music albums, or on billboards, public places, buildings, conveyances, cell phones, automated teller machines, internet; (ii) selling of time slots on radio or television by a person, other than a broadcasting agency or organisation; and (iii) aerial advertising.

[Explanation 2.-For the purposes of this sub-clause, "print media" means,- (i) "newspaper" as defined in sub-section (1) of section 1 of the Press and Registration of Books Act, 1867;

(ii) "book" as defined in sub-section (1) of section 1 of the Press and Registration of Books Act, 1867, but does not include business directories, yellow pages and trade catalogues which are primarily meant for commercial purposes; (Section 65(105)

35

(zzzm)]*

13.6. He was explained that service tax was required to be paid under the "Renting of Immovable Properties" services under section 65(90a) of the Finance Act, 1994 as amended w.e.f. 01.06.2007 and "Selling of Space or Time Selling' services for Advertisement" under section 65(105)(zzzm) of the Finance Act, 1994 as amended w.e.f. 01.05.2006, on the above income of Rs. 4,63,89,5011- and Rs. 33,54,872/- respectively. In this regard he stated that the Hon;ble High Court of New Delhi vide order W.P. (C) No. 1659 of 2008, with W.P. (C) Nos. 4130-4131, 4749,5036,5643, 5976, 5978, 6033, 6734, 6744, 6993, 7004, 7122, 7164, 7212, 7654, 7664, 7722-7723, 8538, 7964 and 8771 of 2008, decided on 18-4-2009, reflected at 2009 (237) EL T 209 (del.) in respect of HOME SOLUTION RETAIL INDIA LTD. Versus UNION OF INDIA had held that Renting of Immovable Property was not liable to Service tax but services in relation to Renting of Immovable Property was taxable.

13.7. He therefore, requested that demand of service tax for the same may not be raised. However, he gave undertaking that if the final decision in the matter was found to be in favour of the department then they would pay the service tax. He also requested to wait till the final decision in the matter before issuance of any SCN.

14. “M/s Devarc” vide letter dated 20.10.2010 had submitted Provisional Balance Sheet for the year 2009-10. On going through the said Provisional Balance Sheet it was observed that they had shown amount of Rs. 75,00,000/- as Supervision charges under credit head and Rs. 1,93,95,9661- as Rent Income received.

15. As per letter dated 07.09.2010 “M/s. Devarc” submitted that total amount of Rs.6,88,09,067/- was shown as receivable from Dev Arc(Jodhpur) Commercial Co. Op. Society Ltd. for the period 2005-06 to 2008-09 for Supervision Fees under the category of “Real Estate Agent Services” under Section 65(88) of the Finance Act, 1994. But till date they had not received the said amount along with amount of Rs. 75,00,000/- for the year 2009-10. On scrutiny of the Balance Sheet for the period 2005-06 to 2008-09, it was found that the said Supervision Charges were shown as Income. On scrutiny of Provisional balance Sheet for the year 2009-10, it was found that the said Supervision Charges were shown under the head of credit.

16. On the basis of the above the service tax payable under the category of “Real Estate Agent Services” defined under Section 65(105)(v) of the Finance Act, 1994 as amended was worked out as Rs.89,24,389/- for the period 2005-06 to 2009-10 as under and was also reflected in Annexure-A attached to the SCN.

Year Amount of Rate Rate Amount of Amount of Total Service Amt. of ST Supervision of of Service Education Tax Payable paid (Rs.) (*)

Charges Servi Edu. Tax Cess (Rs.) ce Cess payable payable

Tax (Rs.) 2005-06 30,25,068 10% 2% 3,02,507 6,050 3,08,557 3,08,557 2006-07 2,16,88,624 12 % 2% 26,02,635 52,053 26,54,688 26,54,688 2007-08 3,13,99,053 12% 3% 37,67,886 1,13,037 38,80,923 38,80,923 2008-09 1,26,96,322 10% 3% 12,69,632 38,089 13,07,721 13,07,721 2009-10 75,00,000 10% 3% 7,50,000 22,500 7,72,500 0 TOTAL 7,63,09,067 86,92,660 2,31,729 89,24,389 81,77,342

35

(*) Payment particulars: They had paid Service Tax as details as follows which is

also reflected in Annexure "A" attached herewith.

Year Amount of

Supervision Charges (Rs.)

Amt. of Service tax

payable

Amt. of Service tax

paid Remarks

2005-06 30,25,068 3,08,557 3,08,557 Ch. Dtd. 15.03.07 2006-07 2,16,88,624 26,54,688 14,58,738 from Cenvat credit account

3,91,443 Ch. Dtd. 15.03.07 8,29,959 Ch. Dtd. 19.05.08

2007-08 3,13,99,053 38,80,923 22,52,354 Ch. Dtd. 14.09.10 16,28,569 from Cenvat credit account

2008-09 1,26,96,322 13.07.721 13.07.721 Ch. Dtd. 0809.10 2009-10 75,00,000 7,72,500 0 ST Not paid

Total 7,63,09,067 81,77,341 Total ST paid

17. Likewise, on the basis of the above the Service tax payable under the category of Renting of Immovable Property Services defined under clause (90a) of Section 65 of the Finance Act, 1994, as amended was worked out as Rs. 77,31,526/- for the period 2007-08 to 2009-10 as under and was also reflected in Annexure "A" attached to the SCN.

Year Amount of Rent from 'Renting of immovable Properties' collected

Rate of Service Tax %

Total Service I Tax payable I

2007-08 2,19,39,986 12.36 27,11,782

2008-09 2,44,49,515 12.36 30,21,960

2009-10 1,93,95,966 10.30 19,97,784Total 6,57,85,467 77,31,526

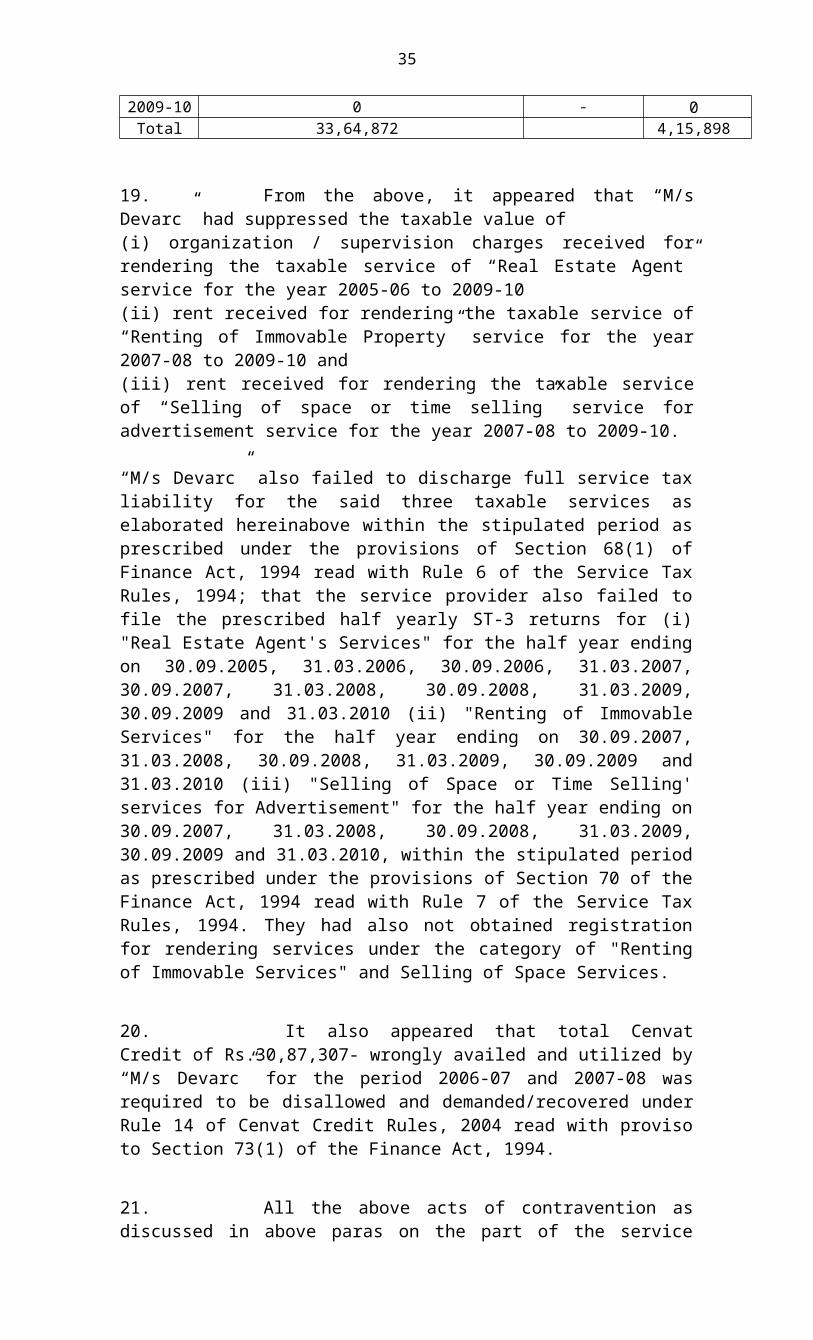

18. On the basis of the above the Service tax payable under the category of "Selling of Space or Time Selling' services for Advertisement" services defined under sub clause (zzzm) of clause (105) of Section 65 of the Finance Act, 1994, as amended was worked out as Rs. 4,15,898/- for the period 2007-08 to 2009-10 as under and was also reflected in Annexure "A" attached herewith.

Year Amount of Rent from 'Selling of Space or Time Selling' services for Advertisement'

collected

Rate of Service Tax %

Total Service Tax payable

2007-08 16,83,636 12.36 2,08,0972008-09 16,81,236 12.36 2,07,8012009-10 0 - 0

Total 33,64,872 4,15,898

19. From the above, it appeared that “M/s Devarc” had suppressed the taxable value of(i) organization / supervision charges received for rendering the taxable service of “Real Estate Agent” service for the year 2005-06 to 2009-10(ii) rent received for rendering the taxable service of “Renting of Immovable Property” service for the year 2007-08 to 2009-10 and(iii) rent received for rendering the taxable service of “Selling of space or time selling” service for advertisement service for the year 2007-08 to 2009-10.

“M/s Devarc” also failed to discharge full service tax liability for the said three taxable services as elaborated hereinabove within the stipulated period as

35

prescribed under the provisions of Section 68(1) of Finance Act, 1994 read with Rule 6 of the Service Tax Rules, 1994; that the service provider also failed to file the prescribed half yearly ST-3 returns for (i) "Real Estate Agent's Services" for the half year ending on 30.09.2005, 31.03.2006, 30.09.2006, 31.03.2007, 30.09.2007, 31.03.2008, 30.09.2008, 31.03.2009, 30.09.2009 and 31.03.2010 (ii) "Renting of Immovable Services" for the half year ending on 30.09.2007, 31.03.2008, 30.09.2008, 31.03.2009, 30.09.2009 and 31.03.2010 (iii) "Selling of Space or Time Selling' services for Advertisement" for the half year ending on 30.09.2007, 31.03.2008, 30.09.2008, 31.03.2009, 30.09.2009 and 31.03.2010, within the stipulated period as prescribed under the provisions of Section 70 of the Finance Act, 1994 read with Rule 7 of the Service Tax Rules, 1994. They had also not obtained registration for rendering services under the category of "Renting of Immovable Services" and Selling of Space Services.

20. It also appeared that total Cenvat Credit of Rs.30,87,307- wrongly availed and utilized by “M/s Devarc” for the period 2006-07 and 2007-08 was required to be disallowed and demanded/recovered under Rule 14 of Cenvat Credit Rules, 2004 read with proviso to Section 73(1) of the Finance Act, 1994.

21. All the above acts of contravention as discussed in above paras on the part of the service provider, appeared to have been committed by suppression of the facts and contravention of the aforesaid provisions with an intent to evade payment of service tax in as much as the service provider had not paid / short paid service tax on such taxable value of supervision charges received for rendering Real estate Agent Service, rent received for rendering Renting of Immovable Property service and Selling of Space or Time Selling' services for Advertisement; not filed proper ST-3 returns for the said three taxable services; also not disclosed/intimated to the Service tax department about any material fact.

22. Therefore, the said service tax not paid / short paid by them was required to be demanded and recovered from them with interest under the proviso to Section 73(1) read with Section 75 of the Finance Act, 1994 by invoking extended period of five years in as much as “M/s Devarc” had suppressed the facts to the department and contravened the provisions with an intent to evade payment of service tax. The cenvat credit wrongly availed was also required to be demanded and recovered under Rule 14 of the Cenvat Credit Rules, 2004. All these acts of contravention of the provisions of Section 68(1), 69 and 70 of the Finance Act, 1994 read with Rules 4, 6 and 7 of the Service Tax Rules, 1994 appeared to be punishable under the provisions of Section 76, 77 and 78 of the Finance Act, 1994.

23. A show cause notice bearing F.No.STC/4-104/O&A/10-11 dated 22.10.2010 was issued to M/s. Dev Arcade Pvt. Ltd. to show cause as to why -

(i) services rendered by them to their clients for the amounts charged and collected on which no service tax was paid / short paid, should not be considered as "taxable service" under the category of (i) "Real Estate Agent" and the total/gross amount of Rs.7,63,09,067, (ii) Renting of Immovable Property" and the total/gross amount of Rs.6,57,85,467/- and (iii) "Selling of Space or Time Selling' services for Advertisement" the total/gross amount of Rs.33,64,872/- respectively should not be considered as value of the said taxable services charged by them as discussed in foregoing paras;

(ii) service tax amount of Rs.89,24,389/- (Rupees Eighty Nine Lakh Twenty Four Thousand Three Hundred and Eighty Nine Only) as shown in the

35

foregoing para on ‘Real Estate Agent’s Service’ should not be demanded and recovered from them under the proviso to Section 73(1) of the Finance Act, 1994, read with Section 68 of the Finance Act, 1994 as amended. And the amount of Rs.50,90,035/- paid vide GAR challan as discussed in the foregoing paras, should not be appropriated against the aforesaid demand;

(iii) the Cenvat Credit of Rs.30,87,307/-(Rupees Thirty lakh Eighty Seven Thousand and Three Hundred and Seven) wrongly availed by them should not be disallowed and recovered from them under Rule 14 of Cenvat Credit Rules, 2004, read with proviso to Section 73(1) of the Finance Act, 1994;

(iv) service tax amount of Rs.77,31,526/- (Rupees Seventy Seven Lakh Thirty One Thousand and Five Hundred and Twenty Six only) as shown in the foregoing para on 'Renting of Immovable Property Service' should not be demanded and recovered from them under the proviso to Section 73(1) of the Finance Act, 1994, read with Section 68 of the Finance Act, 1994 as amended;

(v) service tax amount of Rs.4,15,898/- (Rupees Four Lakh Fifteen Thousand and Eight Ninty Eight only) as shown in the foregoing para on 'Selling of Space or Time Selling' services for Advertisement should not be demanded and recovered from them under the proviso to Section 73(1) of the Finance Act, 1994, read with Section 68 of the Finance Act, 1994 as amended;

(vi) interest at the prescribed rate should not be charged and recovered from them on the said amount of service tax not paid/paid belatedly under the provisions of Section 75 of the Finance Act, 1994, as amended;

(vii) interest as applicable on cenvat credit of Rs.30,87,307/- wrongly availed and utilized should not be recovered from them under Section 14 of Cenvat Credit Rules, 2004 read with under section 75 of the Finance Act, 1994;

(viii) penalty under the provisions of Section 76 of the Finance Act, 1994, as amended, should not be imposed on them for failure to pay /short pay Service Tax and Education Cess as mentioned hereinabove within stipulated time;

(ix) penalty under Section 77 of the Finance Act, 1994, as amended, should not be imposed on them in as much as they had not filed proper ST-3 returns for the Real Estate Agents Service and had failed to file ST -3 returns for the Renting of Immovable Property" and "Selling of Space or Time Selling' services for Advertisement", within stipulated period as required under the provisions of aforesaid Section 70 read with Rule 7 as amended;

(x) penalty under Section 78 of the Finance Act, 1994, as amended, should not be imposed on them for suppressing the full value of taxable services provided by them before the department with an intent to evade payment of Service Tax.

(xi) penalty under Rule 15 of the Cenvat Credit Rules, 2004, should not be imposed on them for wrongly availing and utilizing the Cenvat Credit of input services.

DEFENCE REPLY& PERSONAL HEARING:-

25 “M/s Devarc” replied the show cause notice vide their defence reply dated 22.12.2010. However, vide their letter dated 21.12.2011 “M/s Devarc” requested to replace their earlier submission dated 22.12.2010 and submitted their written submission which is as follows :-

35

A. 'Real Estate Agent's Service':-26.1 They had entered into an Agreement with the Society for supervising its

scheme and according to the terms and conditions of the Agreement, they were entitled to the fees at a fixed percentage of the cost of construction incurred by the Society during every financial year till the continuation of the Agreement.

26.2 They were entitled to charge the fees after the end of the financial year. They could charge the fees only after the completion of the financial year of the Society because the basis of fees was percentage of the construction cost which could be arrived at every year only after finalizing the books of account of the Society. Accordingly they charged their fees to society as under :

Financial year

Fees charged

Charged on

Fees received

on

Service tax paid on

2005-06 30,25,068 31-3-2006 Not recd. 15-3-20072006-07 2,16,88,624 31-3-2007 Not recd. 15-3-2007

19-05-20082007-08 3,13,99,053 31-3-2008 Not recd. 06-09-2010

14-09-20102008-09 1,26,96,322 31-3-2009 Not recd. 08-09-20102009-10 75,00,000 31-3-2010 Not recd.

26.3 They, submitted that in fact they did not receive any amount towards their fees from the Society as was evident from the copy of the account of the Society, which was given during the inquiry and also attached with this submission. Till date, they had not received its fees from the Society. They enclosed a certificate of CA in this regard. They submitted that the above facts clearly establish that they were not at all liable to pay service tax on amount charged. According to the service tax laws also, the service provider is liable to pay the service tax on the amount realized and not on the amount charged and therefore, when they had not received their fees, they was not liable to pay service tax and therefore, were also not required to get registered u/s. 69 of the Act. Thus, the allegations/charges that the amount of fees was received, was factually incorrect and therefore, the other allegations made were irrelevant and were liable to be dropped on this ground alone. They relied on the judgment of Bharat Sanchar Nigam Ltd. Versus.Commissioner of Central Excise & Customs, Thiruvananthapuram [2010] 27 STT 57 (BANG. - CESTAT).

26.4 They submitted that though they were not liable to pay service tax under Rule-6, they had paid the entire amount of service tax and therefore in the light of what was stated hereinabove, there was no need to issue the Show Cause Notice. The Show Cause Notice issued upon them was bad in law, within the meaning of section 73(3) of the Act. In view of the above clear provisions of the law, the Show Cause Notice could not have been issued. This view was also supported by CBEC circular No. 137/167/2006 dated 3-10-2007. This view has also been confirmed by the Hon'ble CESTAT in the following cases:-

(i) U. B. Engineering vs. CCE, Rajkot [2009] 23 STT 194 [AHD. CESTAT].

35

(ii) Bhoruka Alluminium Ltd. vs. CCE, Mysore [2008] 15 STT 198 [Bang. CESTAT].

(iii) Vista Infotech vs. CST Bangalore 2010 [17] STR 343 [Tri. Bangalore].

26.5 In view of the above, when no Show Cause Notice could be issued, no penalty could be imposed.

26.6 They submitted that the above facts clearly showed that they had not contravened the provisions of the service tax laws and had paid service tax, though they were not liable to pay service tax, on fees receivable from society, only in order to co-operate the Department and not to prolong the litigations. The entire set of facts clearly proved that they were not at all required to be issued the Show Cause Notice for which there was no suppression of value as well as facts and non-payment of service tax, and service tax was already paid in advance and therefore there was no question of recovery of service tax not paid or less paid.

B. Renting of Immovable Property:

26.7 They submitted that they had received amount towards rent from various parties but such parties did not give service tax in the light of the decision of Delhi High Court in the case of Home Solutions India Ltd. Vs. UOI & ORS. and they, simultaneously relied upon the said decision and did not pay service tax. After amendment in the provision in Finance Act, 2010, Delhi High Court had granted a stay against the levy of service tax on Renting of Immovable Property. They submitted that in view of the above they had sufficient reason and had a bonafide belief for non making payment of service tax on renting services.

26.8 The above facts are undisputed and also reiterated by the Department in the Show Cause Notice itself, which proved that they had not contravened any of the provisions of the Act and that too, with an intent to evade the payment of service tax by a reason of fraud, collusion, suppression of facts or mis-statement.

C. Sale of Space or Time for Advertisement Services:26.9 It was proposed in the said Show Cause Notice to charge service tax under the category of “Sale of space or time for advertisement” on gross amount of Rs. 33,64,872/- charged by way of rent for display of hoardings. They submitted that they were under a bonafide belief that the rent charged for display of hoardings was chargeable to service tax under the category of “Renting of Immovable Property”. They relied on the plea taken in the case of Home Solutions India Ltd. Vs. UOI & ORS. [Delhi High Court] and did not pay service tax. After amendment in the provision in Finance Act, 2010, Delhi High Court had granted a stay against the levy of service tax on Renting of Immovable Property. In view of the above they had sufficient reason and had a bonafide belief for non payment of service tax on rent income received from display of hoardings.

D. CENVAT CREDIT ON INPUT SERVICES

26.10 They were engaged by Dev Arc (Jodhpur) Commercial Co-op. Society Ltd. (“the society”) to supervise its scheme as a whole. Their Directors were not technically qualified and therefore they obtained various services of technical persons/ agency such as consultancy services, plumbing design services, structural design services, services for valuation of property, electrical design services, etc.

35

and accordingly they made payment for such services alongwith service tax, which it availed as Cenvat Credit.

26.11 According to the Show Cause Notice the input services availed by them were in relation to construction service and therefore the Cenvat Credit on service tax paid for the same was wrongly availed by them and therefore it was proposed to be disallowed. The relevant period under consideration was that of F.Y.s 2006-07 and 2007-08.

26.12 They drew attention to the definition of ‘input service’ under Rule 2(l) of CENVAT Credit Rules, 2004 for the relevant period:

“l) "input service" means any service,- (i) used by a provider of taxable service for providing an output service; or (ii) used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products from the place of removal, and includes services used in relation to setting up, modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage upto the place of removal, procurement of inputs, activities relating to business, such as accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, and security, inward transportation of inputs or capital goods and outward transportation upto the place of removal;”

26.13 The definition of the term ‘input service’ has two parts- the ‘means’ part which is the main part of the definition; and the ‘inclusive’ part which is illustrative and not exhaustive.

The ‘means’ part of the definition covers any service used by a provider of taxable service for providing an output service. A service would qualify as ‘input service’ even if it is not covered by the ‘means’ portion, if it satisfies the ‘includes’ portion of the definition. Therefore in order to qualify as an input service, a service has to fall either within the first part of the definition or the second part of the definition. Thus the two parts of the definition of ‘input service’ – the ‘means’ part and the ‘inclusive’ part - are to be construed harmoniously.

26.14 They relied on the judgment of ‘SEMCO Electrical Private Limited V. Commissioner of Central Excise, Pune’ – 2010 (18) S.T.R. 177 (Tri. - Mumbai). They further submitted that the Hon’ble Supreme Court has explained the scope of the term ‘includes’ in ‘Regional Director V. High Land Coffee Works’ – (1991) 3 SCC 617. They also relied on the judgment of Corporation of City of Nagpur v. Its Employees AIR SC 675, Narmada Bachao Andolan v. UOI AIR 2005 SC 2994 (SC 3 member bench), CTO v. Rajasthan Taxchem Ltd. (2007) 3 SCC 124, Karnataka Bank Ltd. v. State of AP (2008) 12 VST 459 (SC), K N Farms Industries v. State of Bihar AIR 2009 SC 3031.

26.15 They further submitted that the purpose of using the words ‘such as’ is illustrative only and not exhaustive. This view has been expressed in Royal Hatcheries (P.) Ltd. v. State of AP – (1994) 92 STC 239 (SC); Jalal Plastic Industries v. UOI – 1981 (8) ELT 653 (Guj.); Gramophone Co. of India

35

Ltd. v. CCE – 1991 (52) ELT 247 (CEGAT); Victor Gaskets India Ltd. v. CCE (2008) 14 STT 403 (Mum.-CESTAT).

They also relied on the following judgments in this regard:i) ‘Good Year India Ltd., V. Collector of Customs’ – [1997 (95) E.L.T.

450 (S.C.)], ii) Force Motors Limited V. Commissioner of Central Excise, Pune’ –

[2009 (13) S.T.R. 692 (Tri. - Mumbai.)],

They submitted that definition of input service uses the term ‘such as’ which is purely illustrative and not exhaustive. Therefore the term ‘such as’ establishes that whatever activities are enumerated in the Rule are only illustrations of service that relate to the business and are not of exhaustive of it. Hence any activity relating to their business would be covered as input service.

26.16 They further submitted that the word ‘activities’ in the phrase ‘activities relating to business’ signifies the wide import of the phrase. The Rule making authority has not employed any qualifying words before the word ‘activities’ like ‘main’ activities or ‘essential’ activities. Therefore all and any activities relating to business fall within the definition of ‘input service’. Expenses incurred on the ground of commercial expediency by them were covered by the term ‘activities’ relating to business.

26.17 They further submitted that definition of ‘input service’ employs the phrase ‘in relation to’. They relied on the following judgments explaining the said phrase: Doypack System (P) Limited V. Union of India – [1988 (36) E.L.T. 201 (S.C.)], Tamil Nadu Kalyana Mandapam Association v. UOI 2004 (167) ELT 3, CCE v. Solaris Chemtech (2007) 7 SCC 347, Shyam Lal v. M. Shayamlal –AIR 1933 ALL. 649, State of Karnataka v. Azad Coach Builders (2010) 9 SCC 524 (SC 5 member bench).

26.18 They further submitted that business is an integrated/continuous activity and is not confined restricted to mere manufacture of the product. Therefore, activities in relation to business cover all the activities that are related to the functioning of a business. Therefore, the term ‘business’ cannot be given a restricted definition. Business is an integrated activity comprising of provision of service, advertising such services, entering into agreements with the clients, etc. They relied on the following judgments in this regard:i) ‘Mazgaon Dock Limited V. Commissioner of Income Tax and Excess

Profits Tax’ – AIR 1958 SC 861ii) ‘Narrain Swadesh Weaving Mills V. Commissioner of Excess Profits

Tax’ – 1955 1 SCR 952 iii) Victor Gaskets India Limited V. Commissioner of Central Excise – [2008

(10) S.T.R. 369 (Tri-Mumbai)], iv) ABB Ltd. v. CCE 2009 (15) S.T.R. 23 (Tri.- LB);v) Cadila Pharmaceuticals Ltd. v. CCE Ahmedabad 2010 (17) STR 31

(Tribunal-Ahmedabad).vi) M/s. Coca Cola India Pvt. Ltd. Versus The Commissioner of Central

Excise, Pune-III [2009 (15) S.T.R. 657 (Bom.)] vii) Commissioner of Customs & Central Excise, Raipur V. HEG Limited –

[2010 (18) S.T.R. 446 (Tri. - Del.)], viii) Commissioner of Central Excise V. GTC Industries Ltd. – [2008 (12)

S.T.R. 468 (Tri.-LB)],

35

26.19 The services such as agency, consultancy services, plumbing design services, structural design services, services for valuation of property, electrical design services, etc were nothing but services received by them because such services were vital to enable them to render its service to the Society. Taking into account the afore-mentioned interpretation of the various words and phrases used in the definition of ‘input Service’, they submitted that they were entitled to take, and had rightly taken, the Cenvat credit of the service tax paid by them to the service providers in relation to these input services. In light of what is stated herein, there was no justification in coming to the conclusion that they had wrongly availed the CENVAT Credit and was liable to penalty under Section 15(3) of the CENVAT Credit Rules, 2004. They submitted that no Penalty under Rule 15(3) of Cenvat Credit Rules is imposable.

27. They submitted that invocation of extended period under Section 73 of the Act is incorrect and bad in law. It was submitted that there was no fact which was not known to the Department. The Department never asked for any information which they failed to disclose. They had always cooperated with the Department in their proceedings and had always provided the details asked for by the Department and never suppressed any facts from the Department. They relied on the following judgments:

i) Padmini Products Limited v CCE 1989 (43) ELT 195 (SC) ii) CCE Vs. Chemphar Drugs and Liminents 1989 (40) ELT 276 (SC),

27.1 They also relied on the following decisions.

(A) Real Estate Agent Services :

(i) Karnataka State Ware Housing Corp. Ltd. Vs VST Bangalore 2010 (19) STR 32 (Tri-Bang.)

(ii) Vista Infotech Vs. CST Bangalore, 2010(17) STR 343 (Tri-Bangalore)

(iii) CCE Vishakhapattnam Vs. Sri Koduri Enter (P) Ltd. (2010) 26 STT 53 (Bang- CESTAT)

(iv) U. B. Engineering Vs. CCE Rajkot (2009) 23 STT 194 (Ahd-CESTAT)

(B) Renting of Immovable Property:(1) Continental Foundation Vs. CCE, Chandigarh 2007

(216) ELT 177 (SC) (2) Secretary Town Hall Committee, Mysore City Corp.

Vs. CCE, Mysore (2007) 9 VST 471 (CESTAT Bangalore)

(3) CCE Jalandhar Vs. Esskay Eng. Co. Ltd. (2008) 13 STJ 11 (CESTATE, New Delhi)

(4) Bharat Wagon & engg. Co. Ltd., V. CCE. Patna,(146) ELT 118 (Tri. – Kolkata),

(5) Goenka Woollen Mills Ltd., V. CCE. Shillong 2001 (135) ELT 873 (Tri. – Kolkata)

(6) Bhilwara Spinners Ltd., V. CCE, Jaipur, 2001 (129) ELT 458 (Tri.-Del).

27.2 They submitted that since the demand of service tax on the value so arrived at was not sustainable and also they had not contravened any of the provisions of the Act or Rules. Therefore, no interest or penalty was imposable under sections 76, 77 and 78 of the Act. It was submitted however, that for imposing penalty,

35

there should be an intention to evade payment of service tax on their part supported by documentary evidences.

27.3 W.e.f 10-05-2008 by the Finance Act, 2008 the amendments had been made in the provisions of section 78, according to which if the penalty has been payable under section 78, the provisions of section 76 shall not apply. This is a settled law. They relied on the following decisions

a.) SIVA SANKAR MOTORS Versus CCE, VISAKHAPATNAM-II [2009] 18 STT 306 (KOL.-

CESTAT)b.) Opus Media and Entertainment vs. CCE, Jaipur [2007] 10 STJ 259 [CESTAT-New Delhi].c) Hindustan Steel Ltd., v. The State of Orissa reported in AIR 1970 (SC) 252. d) Kellner Pharmaceuticals Ltd., Vs. CCE, reported in 1985 (20) ELT 80, e) Catalyst Capital Services (P) Ltd. Vs. CCE Mumbai (2005) 1 STT 241 (Mumbai CESTAT), f) Akbar Badruddin Jiwani V. Collector of Customs, 1990 (047) ELT 061 SC,

27.4 There was no mens rea or contumacious conduct on their part to evade service tax. The non payment of service tax and failure to follow the other formalities occurred not due to their intention to evade the payment of tax.

27.5 It is settled principle of law that the information, which was not required under the statute to be submitted, if not submitted, does not amount to suppression. There was no requirement in the Finance Act, 1994 or the Rules made there under that any information was required to be submitted for collecting those amounts, which were not liable for payment of service tax.

27.6 They submitted that even if any contravention of provision was alleged it was solely on account of their bonafide belief that the amount received was not at all taxable. Such bonafide belief was based on the reasons stated above. The contravention, if any, was not with the intention to willfully evade payment of service tax. Reliance was placed on the judgment of Hon’ble Supreme Court in the case of Pushpam Pharmaceuticals Company V. CCE 1995 (78) ELT 401(SC) and CCE Vs. Chemphar Drugs and Liniments 1989 (4) ELT 276 (SC).

27.7 They further submitted that if the issue was relating to interpretation of law i.e. whether tax was payable, penalty cannot be imposed. They placed reliance on the following case laws in this regard:

CCE v. Sikar Ex-Serviceman Welfare Coop Society Ltd. (2006) 4 STT 289 (CESTAT); Universal Cables Ltd. v. CCE (2007) 10 STT 264 (CESTAT); India Japan Lighting (P.) Ltd. v. CCE (2007) 11 STT 498 (CESTAT); NRC Ltd. v. CCE (2007) 11 STT 245 (CESTAT); Jagdeep Singh Saluja v. CCE (2008) 15 STT 498 (CESTAT SMB); Rohan Builders Ltd. v.

CST (2008) 16 STT 372 (CESTAT); Hindustan Sanitaryware v. CCE (2009) 21 STT 49 (CESTAT SMB); Bharat Wagon & Engg. Co. Ltd., V. Commissioner of C.Ex. Patna, (146) ELT 118 (Tri. – Kolkata); Goenka Woollen Mills Ltd., V. Commissioner of C. Ex. Shillong 2001 (135) ELT 873 (Tri. – Kolkata); Bhilwara Spinners Ltd., V. Commissioner of Central

Excise, Jaipur, 2001 (129) ELT 458 (Tri.-Del).

35

27.8 They also relied on the following judgments for non imposition of penalty as no malafide is involved. Chitrita Virnave v. CCE (2007) 9 STT 545 (CEGAT) ARC. Hemant S Dugad v. CCE [2008] 17 STT 31 (Mum.-CESTAT SMB)

27.9 They relied on the following judgments for non imposition of penalty when there was doubt about taxability of service – CCE v. Hira Automobiles (2009) 23 STT 218 (CESTAT SMB); Vicas Corpn v. CCE (2009) 23 STT 228 (CESTAT SMB); M G Motors v. CCE (2009) 23 STT 230 (CESTAT SMB); Shri Raj Auto Centre v. CCE (2009) 23 STT 109 (CESTAT SMB).

27.10 If there was dispute about constitutional validity on the service and tax was being challenged, imposition of penalty was not justified. – Runanubhandh Mangal Karyalaya v. CCE&C (2008) 17 STT 329 (CESTAT SMB); CCE v. Ruchi Soya Industries Ltd. (2009) 19 STT 237 (CESTAT).

During the relevant period, there was dispute about chargeability of service tax on ‘Renting of Immovable Property’. Taking into account the afore-mentioned case laws, they submitted that no penalty whatsoever should be imposed for not paying service tax under ‘Renting of Immovable Property’.

27.11 They also requested to invoke section 80 of the Act, for non imposition of penalty under section 76, 77 and 78 as in the present case they had a bonafide belief that service tax was not payable on the amount received from members.

27.12 They submitted that a subordinate authority was bound to follow the decision of the higher authority and cannot take a different view. They in support, relied on the following judgements:-

i) Pratik Marbles vs. CCE, Jaipur-II 2007 (7) STR 240 [Tri. Delhi]. ii) CCE vs. L. H. Sugar Factories Ltd. 2006 (3) STR 715 SC.iii) Gujarat Ambuja Cement Ltd vs. UOI 2006 (3) STR 608 SC.iv) The Motor Industries Company Ltd. vs. CST, Bangalore [2007] 10

STJ 96 [CESTAT-Bangalore].v) CST, Bangalore vs. Indian Rayon Industries Ltd.[2007] 10 STJ 89

[CESTAT-Bangalore].

27.13 For the reasons discussed herein above, they submitted that, no penalty u/s. 77 could be imposed.27.14 They submitted that when the demand was not sustainable, the question of making payment of interest u/s. 75 does not arise.

28. A personal hearing was fixed for 22.11.2011 which was not attended by M/s Dec Arc. Thereafter, a personal hearing was fixed for 21.12.2011 which was attended by Shri Dinesh P Bahvsar, Chartered Accountant who explained the issue and gave a written submission dated 21.12.2011 in support thereof.

Discussion & Findings:

29. I have carefully gone through the records of the case, written submissions made by “M/s Devarc” in their defence reply to the show cause notice as well as during the course of personal hearing and the records/documents produced by them. I find that the issues to be decided in this case are:

i) Whether, “M/s Devarc” are liable to pay service tax on the amount charged but not received under the category of “Real Estate Agent’s Service”.

35

ii) Whether, the cenvat credit availed and utilized by “M/s Devarc” is for providing the output service of “Real Estate Agent’s Service” or for the “Commercial Construction Service”.

iii) Whether, “M/s Devarc” are liable to pay service tax on the amount charged as rent, under the category of “Renting of immovable property Service”.

iv) Whether, “M/s Devarc” are liable to pay service tax on the amount charged as rent for display of hoardings under the category of “Sale of Space or time for advertisement services”.

30. As regards, the non payment of service tax under the category of “Real Estate Agent’s Service”, I find that “M/s Devarc” have neither contested the provision of service to the said Co.op. society under Section 65(105(v) of the Finance Act,1994 nor have they contested their liability for payment of service tax. Their contention is that since the amount on which service tax has been demanded in the show cause notice has only been charged by them and which has not been received by them till date, they are liable to pay service tax only after the receipt of the said amount. They submitted copy of their ledger account, Profit & Loss account for the said years, ledger accounts of M/s Devarc (Jodhpur) Co.op. Society Ltd and a certificate dated 21.12.2010 issued by Nautam R. Vakil & Co. Chartered Accountants, who are also their statutory auditors to show that the amount of Rs. 30,25,068/- charged on 31.3.2006, Rs. 2,16,88624/- charged on 31.3.2007, Rs. 3,13,99,053/- charged on 31.3.2008, Rs. 1,26,96,322/- charged on 31.3.2009 and Rs. 75,00,000/- charged on 31.3.2010 is still outstanding and not received by them. They further submitted that despite the above facts they had paid service tax of Rs.81,77,341/- (Rs. 50,90,035/- through Challans + Rs. 30,87,306/- through cenvat credit) for the years 2005-06 to 2008-09. I agree with the contention of “M/s Devarc” that as per Rule 6(1) of Service Tax Rules, 1994 (as it then existed), the liability to pay service tax arises only after receipt of value towards taxable services, which in the case before me has yet not occurred as seen from the ledger account, Profit & Loss account, ledger accounts of M/s Devarc (Jodhpur) Co.op. Society Ltd and the above referred Chartered Accountant’s certificate. I accept the certificate dated 21.12.2010 issued by Nautam R. Vakil & Co. Chartered Accountants, statutory auditors of “M/s Devarc” in this regard.

30.1 I further find that the fact which is not in dispute is that “M/s Devarc” had paid service tax of Rs.81,77,341/- (Rs. 50,90,035/- through Challans + Rs. 30,87,306/- through cenvat credit) for the years 2005-06 to 2008-09 against their service tax liability of Rs. 81,51,889/- as detailed in table at para 16 of the show cause notice. Since “M/s Devarc” have willingly paid the service tax during the course of investigation even before their liability to pay service tax has arisen, the same shall be appropriated against their service tax liability.

30.2 As regards, the demand of Rs. 7,72,500/- for the year 2009-10, I find that the demand is premature and the liability to pay service tax would only arise after the receipt of value towards taxable services as per Rule 6(1) of Service Tax Rules, 1994. Therefore, the demand of Rs. 7,72,500/- for the year 2009-10 is legally unsustainable. Since, “M/s Devarc” are not contesting taxability on the said amount and have submitted that they shall pay service tax on the said amount on receipt of the said amount which is the value towards taxable service, I conclude that “M/s Devarc” must pay the due service tax on receipt of the value towards taxable service. The amount of service tax of Rs.25,452/- (Rs.81,77,341/- - Rs. 81,51,889/-) paid in excess by “M/s Devarc” against their service tax liability for the year 2005-06 to 2008-09 shall be adjusted against the service tax liability of Rs. 7,72,500/- for the year 2009-10.

35

30.3 Since “M/s Devarc” have paid service tax even before their liability to pay tax has arisen, they cannot be penalized as proposed in the show cause notice. Consequently, the proposal of interest also does not survive.

31. Now I come to the next issue of alleged wrong availment of Cenvat Credit amounting to Rs.30,87,307/-. I find from the table at para 9 of the show cause notice that “M/s Devarc” had availed cenvat credit on various input services as follows:-1. Structural Consultancy Service.2. Agency Fee.3. Plumbing Design Service.4. Structural Design Service.5. Preparing valuation of property Service.6. Electrical Design Service.

31.1 Definition of “input service” as given in Rule 2(l)(i) of Cenvat Credit Rules, 2004 reads as under:

“input service” means any service used by a provider of taxable service for providing an output service.

31.2 The above definition implies that input service can be any service but it must be utilized by the provider of output service for providing an output service. I find from the above definition that the basic requirement inherent in it for any service to be an “input service” is that it should be “used for providing an output service”. I also find from the simple language of the definition of “input service” that there must be a direct use of the input service for providing the output service. It implies that it must be established that, but for the use of the input service, the output service could not be provided. This apparently leads me to an inference that there must be a nexus between the input service and the output service. Thus, the primary condition for any service is that it should qualify as “input service” for an “output service” satisfying the “user test”.

31.3 I find it very necessary to refer to the definition of “output service” given in rule 2(p) of Cenvat Credit Rules, 2004 which reads as under:

“output service” means any taxable service, excluding the taxable service referred to in sub-clause (zzp) of clause (105) of Section 65 of the Finance Act, provided by the provider of taxable service, to a customer, client, subscriber, policy holder or any other person as the case may be, and the expressions “provider” and “provided” shall be construed accordingly;

31.4 I find from the definition of “output service” that it itself refers only to a taxable service. Thus the service on which the input service is used must be one of the taxable services specified in the various sub-clauses of section 65(105) of the Act. Thus, from the above definition it is amply clear that cenvat credit on input services would depend on requirement of the provision of output service.

31.5 In the case before me, I find that “M/s Devarc” have entered in to an agreement with M/s. Dev Arc (Jodhpur) Commercial Co.Op Society Ltd., for organization/supervision of the scheme of “M/s Devarc Mall”, the construction of which was to be carried out by the said society. “M/s Devarc” were to receive the fees for such services and were registered under the category of “Real Estate Agent’s Service” (which includes “Real Estate Consultant”) under section 65(105)(v) of the Act and had accordingly paid service tax under the said category. As discussed above, “M/s Devarc” were eligible to avail cenvat credit on those input services which were utilized by them for providing the output service of “Real

35

Estate Agent’s Service”. I find that “M/s Devarc” were not engaged in providing the taxable service of “Commercial or Industrial Construction Service”, but they were basically a project consultant having a distinct legal status and entity separate from the said society engaged in the construction of the said mall. I find that “M/s Devarc” had made payment of the value for receiving the said services. The services on which cenvat credit has been taken by “M/s Devarc” are uitlised for providing the output service of “Real Estate Agent’s Service” (which includes “Real Estate Consultant”) and not for providing the output services of “Commercial or Industrial Construction Service” as alleged in the show cause notice.

31.6 In view of the above discussion, I find that “M/s Devarc” have correctly availed Cenvat Credit of Rs.30,87,307/- under the category of “Real Estate Agent’s Service” (which includes “Real Estate Consultant”) and hold that the said Cenvat Credit is admissible to them. Therefore, the demand for recovery of Cenvat Credit of Rs.30,87,307/- is not sustainable. Consequently, the proposal for interest and penalty on the said demand do not survive.

32. I find that the Show Cause Notice alleges short payment of service tax amounting to Rs.77,31,526/- on the value of Rs.6,57,85,467/- for the years 2007-08 to 2009-10. The said amount of Rs.6,57,85,467/- was received by “M/s Devarc” towards the “Renting of Immovable Property”.

32.1 I find that the Finance Act, 2007 has brought the services of renting of immovable property for use in the course or furtherance of business or commerce under the service tax net with effect from 1.06.2007. Taxable service of ‘Renting of immovable property’ has been defined under Section 65(105) (zzzz) of the Finance Act, 1994. Renting included letting, leasing, licensing or other similar arrangement. For the purposes of this clause, “for use in the course or furtherance of business or commerce” includes use of immovable property as factories, office buildings, warehouses, theatres, exhibition halls and multiple-use buildings.

31.2 Further, by Finance Act, 2010, the Government amended the definition of “Renting of Immovable Property Services”, to provide that the activity of “renting” is itself a taxable service with retrospective effect from June 1, 2007. The Finance Act, 2010 has also inserted clause (v) in sub clause (zzzz) of clause 65(105) of the Finance Act,1994 so as to provide that service tax would be charged on rent of a vacant land if there is an agreement or contract between the lessor and lessee that a construction on such land is to be undertaken for furtherance of business or commerce.

32.3 Thus, in view of Section 65 (105) (zzzz) of Finance Act, 1994 the definition of taxable service of “Renting of Immovable property” means “any service provided or to be provided to any person, by any other person, by renting of immovable property or any other service in relation to such renting, for use in the course of or, for furtherance of, business or commerce.”

Explanation 1. — For the purposes of this sub-clause, “immovable property” includes —

(i) building and part of a building, and the land appurtenant thereto;(ii) land incidental to the use of such building or part of a building;(iii) the common or shared areas and facilities relating thereto; and(iv) in case of a building located in a complex or an industrial estate, all common areas and facilities relating thereto, within such complex or estate,[(v) vacant land, given on lease or license for construction of building or temporary structure at a later stage to be used for furtherance of business or commerce;] but does not include —

35

(a) vacant land solely used for agriculture, aquaculture, farming, forestry, animal husbandry, mining purposes;

(b) vacant land, whether or not having facilities clearly incidental to the use of such vacant land;

(c) land used for educational, sports, circus, entertainment and parking purposes; and

(d) building used solely for residential purposes and buildings used for the purposes of accommodation, including hotels, hostels, boarding houses, holiday accommodation, tents, camping facilities.

Explanation 2. — For the purposes of this sub-clause, an immovable property partly for use in the course or furtherance of business or commerce and partly for residential or any other purposes shall be deemed to be immovable property for use in the course or furtherance of business or commerce;

32.4 Vide section 76 of the Finance Act, 2010, validation of action taken under sub-clause (zzzz) of clause (105) of Section 65, is explained as under:-

Any action taken or anything done or omitted to be done or purported to have been taken or done or omitted to be done under sub-clause (zzzz) of clause (105) of section 65 of the Finance Act, 1994, at any time during the period commencing on and from the 1st day of June, 2007 and ending with the day, the Finance Bill, 2010 receives the assent of the President, shall be deemed to be and deemed always to have been, for all purposes, as validly and effectively taken or done or omitted to be done as if the amendment made in sub-clause (zzzz) of clause (105) of section 65, by sub-item (i) of item (h) of sub-clause (5) of clause (A) of section 75 of the Finance Act, 2010 had been in force at all material times and, accordingly, notwithstanding anything contained in any judgment, decree or order of any court, tribunal or other authority,—(a) any action taken or anything done or omitted to be taken or done in

relation to the levy and collection of service tax during the said period on the taxable service of renting of immovable property, shall be deemed to be and deemed always to have been, as validly taken or done or omitted to be done as if the said amendment had been in force at all material times;

(b) no suit or other proceedings shall be maintained or continued in any court, tribunal or other authority for the levy and collection of such service tax and no enforcement shall be made by any court of any decree or order relating to such action taken or anything done or omitted to be done as if the said amendment had been in force at all material times;

(c) Recovery shall be made of all such amounts of service tax, interest or penalty or fine or other Charges which may not have been collected or, as the case may be, which have been refunded but which would have been collected or, as the case may be, would not have been refunded, as if the said amendment had been in force at all material times.

Explanation.—For the removal of doubts, it is hereby declared that no act or omission on the part of any person shall be punishable as an offence which would not have been so punishable had this amendment not come into force.

32.5 The Finance Bill received President’s Assent on 27.7. 2010 and thereby became a law. The new statute is known as the Finance (No.2) Act, 2010. Accordingly, as discussed in para supra, renting of building and part of a building,

35

and the land appurtenant thereto for use in the course of or, for furtherance of, business or commerce became liable to service tax w.e.f 1.6.2007.

32.6 In this regard, I refer to the order passed by the Hon’ble High Court of Delhi on 23.9.2011 in the case of HOME SOLUTIONS RETAILS (INDIA) LTD. Vs UNION OF INDIA & ORS passed, as reported in 2011-TIOL-610-HC-DEL-ST-LB. The Hon’ble High Court of Delhi has in the said judgment overruled the law laid down in the first judgment reported at 2009(237)ELT208 (Del.) by observing as under:

(a) The provisions, namely, Section 65(105)(zzzz) and Section 66 of the Finance Act, 1994 and as amended by the Finance Act, 2010, are intra vires the Constitution of India.

(b) The decision rendered in the first Home Solution case does not lay down the correct law as we have held that there is value addition when the premises is let out for use in the course of or furtherance of business or commerce and it is, accordingly overruled.

(c) The challenge to the amendment giving it retrospective effect is unsustainable and, accordingly, the same stands repelled and the retrospective amendment is declared as constitutionally valid.

32.7 Further, in the Para 68, 69, 70, 71 and 72 the Hon,ble High Court of Delhi has clarified the conclusion drawn by them in the aforesaid judgement. The said paras are produced herein below:

68. When premises is taken for commercial purpose, it is basically to subserve the cause of facilitating commerce, business and promoting the same. Therefore, there can be no trace of doubt that an element of value addition is involved and once there is a value addition, there is an element of service.69. In view of our aforesaid analysis, we are disposed to think that the imposition of service tax under Section 65(105)(zzzz) read with Section 66 is not a tax on land and building which is under Entry 49 of List II. What is being taxed is an activity, and the activity denotes the letting or leasing with a purpose, and the purpose is fundamentally for commercial or business purpose and its furtherance. The concept has to be read in conjunction. As we have explained that service tax is associated with value addition as evolved by the judgments of the Apex Court, the submission that the base of the said decisions cannot be taken away by a statutory amendment need not be adverted to. Once there is a value addition and the element of service is involved, in conceptual essentiality, service tax gets attracted and the impost gets out of the purview of Entry 49 of List II of the Seventh Schedule of the Constitution and falls under the residuary entry, that is, Entry 97 of List I. 70. In view of our conclusion, the decision in the first Home Solution case does not lay down the law correctly inasmuch as in the said decision, it has been categorically laid down that even if a building/land is let out for commercial or business purposes, there is no value addition. Being of this view, we overrule the said decision.71. The next limb of attack is with regard to the retrospective applicability of the provision. The learned counsel for the petitioners have submitted that the tax and the penalty could not have been imposed with retrospective effect. It is worth noting that the Parliament, keeping in view the first Home Solution case, substituted sub-clause (zzzz) in the present incarnation and gave retrospective effect to cure the deficiency. It is well settled in law that it is open to the legislature to pass a legislation retrospectively and remove the

35

base on which a judgment is delivered. The said view has been stated in Bakhtawar Trust and others v. M.D. Narayan and others, (2003) 5 SCC 298. In the said case, in paragraphs 20 and 26, it has been held thus:

“20. In Vijay Mills Company Ltd. and Ors. v. State of Gujarat and Ors., (1993) 1 SCC 345, it was held-"18. From the above, it is clear that there are different modes of validating the provisions of the Act retrospectively, depending upon the intention of the legislature in that behalf. Where the Legislature intends that the provisions of the Act themselves should be deemed to have been in existence from a particular date in the past and thus to validate the actions taken in the past as if the provisions concerned were in existence from the earlier date, the Legislature makes the said intention clear by the specific language of the validating Act. It is open for the legislature to change the very basis of the provisions retrospectively and to validate the actions on the changed basis. This is exactly what has been done in the present case as is apparent from the provisions of Clauses (3) and (5) of the Amending Ordinance corresponding to Sections 2 and 4 of the Amending Act 2 of 1981. We have already referred to the effect of Sections 2 and 4 of the amending Act. The effect of the two provisions, therefore, is not only to validate with retrospective effect the rules already made but also to amend the provisions of Section 214 itself to read as if the power to make rules with retrospective effect were always available under Section 214 since the said section stood amended to give such power from the time the retroactive rules were made. The legislature had thus taken care to amend the provisions of the Act itself both to give the Government the power to make the rules retrospectively as well as to validate the rules which were already made.X X X X 26. Where a legislature validates an executive action repugnant to the statutory provisions declared by a court of law, what the legislature is required to do is first to remove the very basis of invalidity and then validate the executive action. In order to validate an executive action or any provision of a statute, it is not sufficient for the legislature to declare that a judicial pronouncement given by a court of law would not be binding, as the legislature does not possess that power. A decision of a court of law has a binding effect unless the very basis upon which it is given is so altered that the said decision would not have been given in the changed circumstances.”

72. In State of Himachal Pradesh v. Narain Singh, (2009) 13 SCC 165, it has been held that it would be permissible for the legislature to remove a defect in earlier legislation and the defect can be removed both retrospectively and prospectively by legislative action and the previous actions can be validated.

32.8 It is evident from the above judgment that the Service relating to Renting of immovable property for use in the course or furtherance of business or commerce is taxable under section 65(105) (zzzz) of the Finance Act, 1994 w.e.f 1.6.2007. Renting included letting, leasing, licensing or other similar arrangement. For the purposes of this clause, “for use in the course or furtherance of business or commerce” includes use of immovable property as factories, office buildings, warehouses, theatres, exhibition halls and multiple-use buildings.

35

32.9 This fact is further supported by recent judgment of Hon’ble Gujarat High Court dated 23.8.2011 in the case of Cinemax India Ltd., reported at 2011 (24) STR 3 (Gujarat). The Hon’ble High Court of Gujarat has in para 44 of the judgement held as follows:

“44. For the reasons aforesaid, while upholding Sec. 65(105)(zzzz) of Finance Act, 1994 as amended by Sec. 75(5)(h) and Sec. 76 of the Finance Act, 2010, we hold that the provision of Sec. 65(105)(zzzz) introducing service tax is not attracted if (i) the vacant land is used solely for agriculture, acquaculture, farming, forestry, animal husbandry, mining purposes; (ii) it is a vacant land, whether or not having facilities clearly incidental to the use of such vacant land; (iii) land is used for educational, sports, circus, entertainment and parking purposes and; (iv) building is used solely for residential purposes and buildings are used for the purposes of accommodation, including hotels, hostels, boarding houses, holiday accommodation, tents, camping facilities. The said provision levying service tax will be attracted if the immovable property is rented for the use in the course of or for furtherance of the business of commerce.”

32.10 Further, I also find that, the Hon’ble Punjab and Haryana High Court has in CWP No.11597 of 2010, in the case of M/s Shubh Timb Steels Ltd. v/s UOI passed an order dated 22/11/2010 reported at 2010 (20) STR 737 (P&H), upholding the validity of levy of service tax on Renting of Immovable Property. It also upheld Parliament legislative competence to levy Service Tax on Renting, with retrospective amendment.

32.11 The Hon’ble High Court of Orissa in the case of Utkal Builders Ltd., Vs UOI reported at 2011 (22) STR 257 (Ori.). The Hon’ble High Court of Orissa while dismissing the writ petition held that “….the nature of the transaction made by the petitioner with its tenant clearly amounts to renting of an immovable property for the purpose of business or commerce and is, therefore, clearly covered by Section 65(90-a) of the Finance Act, 1994 and “service tax” is clearly leviable thereon. Although challenge in the present case has been made to the Amendment Act of 2010 to Section 66(105)(zzzz), we find no justification to entertain the present writ application since we are also of the view that the amendment is clearly clarificatory in nature and Parliament certainly possesses the necessary legislative competence to declare the said amendment to be retrospective in operation and, therefore, we do not find any error or lack of competence in such legislation….” .