weaning automobiles off gasoline onto electricity peter e gunther senior research fellow connecticut...

TRANSCRIPT

Weaning Automobiles off Gasoline onto Electricity

Peter E GuntherSenior Research Fellow

Connecticut Center for Economic Analysis

(613) [email protected]

Context• Electric Vehicles• Electric Generation• Peak Rates and Systems• Solar Rates• Strategy – Solar, Bio or Combination• Profit Potential• Timing of Adoption – 98.8% of New by 2031 or 2050

• Modeling• Possible Impacts

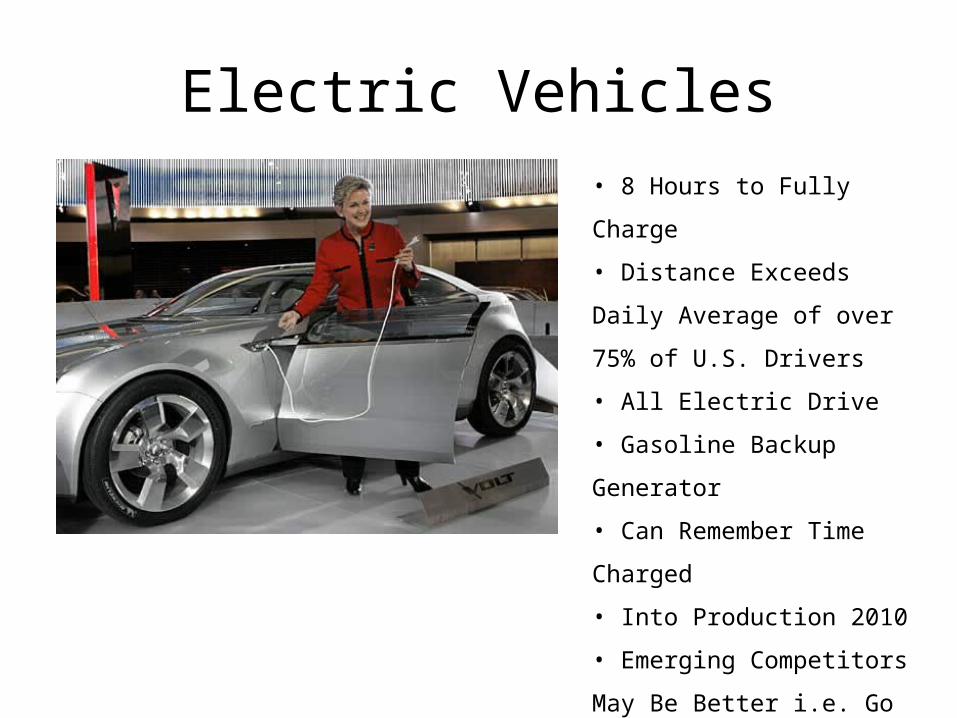

Electric Vehicles• 8 Hours to Fully Charge

• Distance Exceeds Daily Average

of over 75% of U.S. Drivers

• All Electric Drive

• Gasoline Backup Generator

• Can Remember Time Charged

• Into Production 2010

• Emerging Competitors May Be

Better i.e. Go Further

CT Registered Vehicles

2006 2010 2015 2020 2025 2030 2035 2040 2045 20500

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

CT Vehicle Registrations and New Sales (units)

Registered Vehicle Sales

CT Electricity Generation

Current # in MW• 2 Nuclear 2,035• 2 Coal-Fired 553• 26 Oil-Fired 2,487• 14 Natural Gas 1,463• 26 Hydro 149• Solid Waste Fac. 184

PROBLEM: IF ALL AIRCONDITINERS RUN THEY DEMAND 3+ GW.SUMMER INTERRUPTIBLE POWER PENALTIES COST $700 MILLION IN 2007ENVIRONMENTAL DIFFUCULTIES IN EXPANDING TRANSMISSION

Urgently Need to:

• Supply Locally to Meet

Peak Demands or

• Curtail Peak Demands

• Avoid Electric Vehicles

Compounding Problems

Peak Rates

FERC Finds Elasticities are Small but: • Response Improves with the size of the

Spreads Between Peak and Off-Peak Rates• Programmed Cuts in Consumption• Currently high CT interruption costs ≈

$200/capita

Solar RatesSolar and Peak Rates Based on Marginal

Opportunity Costs

0.000.100.200.300.400.500.600.70

Time of Day

$/k

Wh

Marginal Cost (kWh) Average solar rate Average peak rate

During Summer PeakHighest cost CT Generator at $1.17/kWh is Deployed Sparingly

Any Generation at Lower Cost Is Better

Menova Energy Solar Systems

Suitable for RooftopsNow 5 X SunExperimental @ 10 X Sun

Strategy• Build Green Generation to Reduce GHGs and PM• Produce at Peak to Reduce Interruptible Charges• Pay Above Peak Rates for Solar• Entice Vehicle Owners to Charge Off-Peak• Get Vehicle Dealers to Invest and Locally Feed the

Grid• Consider Rebating Electricity Used to Charge EVs• Maximize Value of Hot Water• Track CO2eq Credits

Regional Modeling Strategy

Use RETSCRREN To:• Assess Energy Expansion • Cost Alternatives• Meteorological Data• Examined:

– Solar– Wind– Chips

• Environmental Impacts– GHGs and PM

REMI For:• Dynamic Assessment

– Reduced Interruption Costs

• Impacts on Household– Energy cost & Peak Rates

• Import Substitution for Fossil Fuels

• CT Employment and Incomes

• Fiscal Impacts

Subsidy/ KW Installed GHG Credits$50/Tonne of CO2eq

Dealer Payments to Clients

Years to Payout Equity at various Electricity Rates:

Rates for Sale into Grid (cents/kWh)

16.62 (CT) 37.8 (NJ) 41.7 (CA) 47 (ON)

Subsidy/ KW Installed

1) None Y N 14.61 2.65 2.30 1.95

N N 70.06 3.09 2.63 2.18

Y Y Loss 4.17 3.37 2.67

N Y Loss 5.39 4.12 3.13

2) $251.25 Y N 12.78 2.32 2.01 1.71

N N 61.26 2.70 2.30 1.91

Y Y Loss 3.65 2.95 2.34

N Y Loss 4.71 3.60 2.73

3) $375.00 Y N 11.87 2.15 1.87 1.59

N N 56.92 2.51 2.14 1.77

Y Y Loss 3.39 2.74 2.17

N Y Loss 4.38 3.35 2.54

Years to Payout to Equity Holders from Electricity Revenues Only

Making It Pay Without Subsidy

• Dealers Producing Solar Will Be Paid Back within Three years if:

• Solar Rates Exceed California’s 41.7 kWh• Solar Rates Exceed Ontario’s 47 kWh and Environmental TCs are $50/tonne of CO2eq

and Dealers Rebate their Customers

Timing of AdoptionsSlow Adoption:

• Growth of 0.02% in year one, 2009, followed by +10% of previous year’s growth rate.

• 98.8% of new vehicles are plug-ins by 2050.

• Cumulative vehicle gasoline savings of 9.5 billion gallons.

• Cumulative fuel taxes foregone $2.4 billion gross.

• CO2eq reductions of 72.4 million

tonnes

Rapid Adoption:

• Growth of 0.02% in year one followed by +20% of previous year’s growth rate. •98.8% of new vehicles are plug-ins by 2031 and thereafter.• Cumulative vehicle gasoline savings of 29.9 billion gallons.• Cumulative fuel taxes foregone $7.5 billion gross.• CO2eq reductions of 226.7 million tonnes.

ModelingSolar Only

Due to closer proximity to demand than in bio-based transmission loses 10%.

Cumulative investment $23.9 billion (2008).

Cumulative operating costs $198.9 million 100% human resources.

Due to closer proximity to demand than in bio-based transmission loses 10%.

Cumulative investment $53.1 billion (2008).

Cumulative operating costs $442.0 million 100% human resources.

Bio-based Only

Transmission loses 25%.

Cumulative investment $4.9 billion (2008).

Cumulative operating costs $9.9 billion.

Transmission loses 25%.

Cumulative investment $10.6 billion (2008).

Cumulative operating costs $31.0 billion.

CT Fuel Saved Annually (Millions of Gallons)

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

200

400

600

800

1000

1200

1400

1600

1800

2000

Slow Conversion Fast Conversion

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

1

2

3

4

5

6

7

CT RGDP Impacts (Fixed Billions of 2000 $)

Slow Solar Adop-tion B

Rapid Solar Adop-tion B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Billi

ons 2

000$

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

1

2

3

4

5

6

7

8

9

CT Personal Income Impacts(Billions Nominal $)

Slow Solar Adop-tion B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Billi

ons N

omin

al $

All Scenarios Generate Sufficient to Cover Lost Fuel Tax Revenues

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

2049 -

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

CT Personal Income Tax Impacts(Million Nominal $)

Slow Solar Adop-tion B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Mill

ions

Nom

inal

$

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

2

4

6

8

10

12

14

16

CT Labor Force Impacts (1,000s)

Slow Solar Adop-tion B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Labo

r For

ce 1

000s

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

5

10

15

20

25

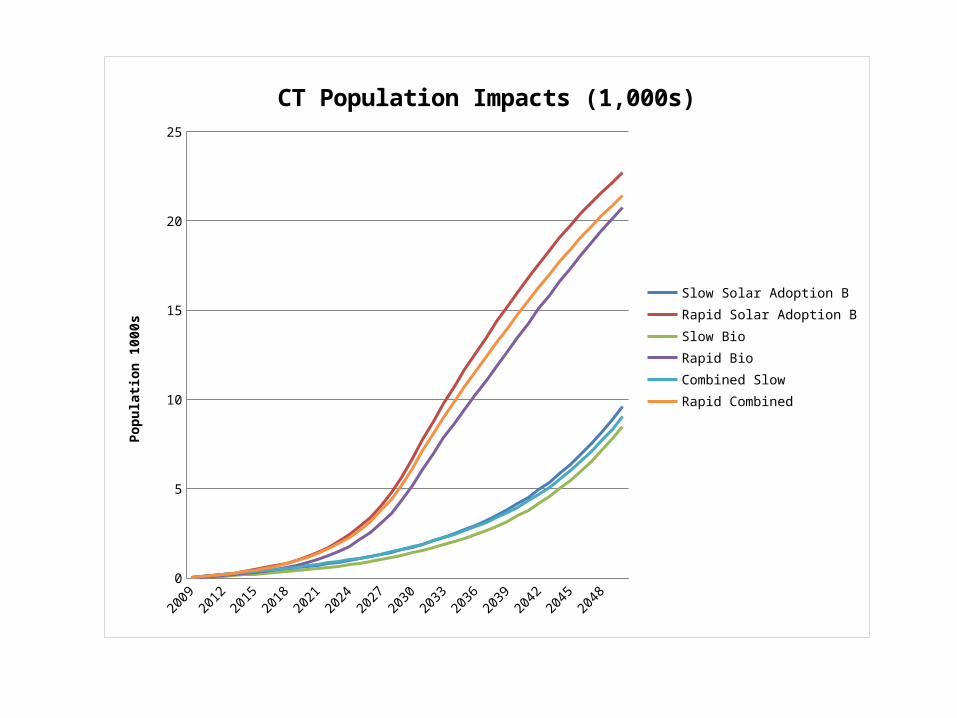

CT Population Impacts (1,000s)

Slow Solar Adoption BRapid Solar Adoption BSlow BioRapid BioCombined SlowRapid Combined

Popu

latio

n 10

00s

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

20490

5

10

15

20

25

30

CT Employment Impacts (1,000s)

Slow Solar Adop-tion B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Empl

oyed

1,0

00s

20092012

20152018

20212024

20272030

20332036

20392042

20452048

0

0.5

1

1.5

2

2.5

3

3.5

CT Employment Impacts in Fabricatated Metal (Employed 1,000s)

Slow Solar Adoption B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Empl

oyed

1,0

00s

20092012

20152018

20212024

20272030

20332036

20392042

20452048

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

CT Employment Impacts in Agricultural and Forestry Employment (1,000s)

Slow Solar Adoption B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

Eplo

ymen

t 1,0

00s

20092011

20132015

20172019

20212023

20252027

20292031

20332035

20372039

20412043

20452047

2049-2.5

-2

-1.5

-1

-0.5

0

0.5

1

CT Labor Productivity Impacts(2000 Fixed 1000s)

Slow Solar Adop-tion B

Rapid Solar Adoption B

Slow Bio

Rapid Bio

Combined Slow

Rapid Combined

2000

fixe

d 10

00 $

Conclusions• CT can build on its TOU smart metering to accelerate adoption of electric vehicles

• CT can overcome charges for interruptible power and strongly encourage electric vehicle owners to recharge their vehicles at off-peak

• Impacts to be positive in employment, labor force, population, personal income

• Over-reliance on bio-fuels could erode labor productivity, albeit that issue could be redressed with improved growing and harvesting technologies

• Increases in personal income taxes under all scenarios were sufficient to offset gasoline sales taxes foregone

• Impacts on labor productivity are mixed depending on the relative weights of solar or bio-fuels

Conclusions (Continued)Potential benefits are likely to exceed those modeled since no account has been taken of the health impacts of reduced emissions of both CO2eq and PM.

CO2eq reductions are 72.4 million tonnes in the slow adoption cases and 226.7 million tonnes in the rapid adoption cases out to 2050.

Estimating impacts on PM will require delineation of diesel vehicles by type and further evidence on the chip burning technologies where technology is improving.

Results will vary massively among jurisdictions depending on the current & future generating mixes, excess capacities, peak pricing and rates of adoption of electric vehicles.

Weaning Automobiles off Gasoline onto Electricity

Peter E GuntherSenior Research Fellow

Connecticut Center for Economic Analysis

REMI TORONTONovember 6, 2009

(613) [email protected]