wealth management cio insights reflections - db.com · in ancient times, global ... in 1492, when...

TRANSCRIPT

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 1

Deutsche BankWealth Management

EMEA Edition

CIO Insights Reflections

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 2

Globalisation is accompanied by trade and both of them mean growth. But current political debate shows us that many people feel that they do not benefit from this. Their concerns may have contributed to the UK’s decision to leave the European Union and the election of Donald Trump as the 45th president of the USA.

Whatever President Trump’s trade policy turns out to be, fears around global trade barriers and the fragmentation of trading blocs will continue to unsettle capital markets and society alike. So now is a good time to explore the theory around free trade, and consider what it takes to make sure that it benefits all parts of society – so called “inclusive growth”.

A little light economic history is a good way to understand how patterns of trade have evolved over the centuries and how economists’ trade theories have followed suit. So our report starts (Section 1) by setting out the various phases of globalisation and the economic innovation that they have encouraged. But the process has often been resisted and the economic arguments for free trade (Section 2) have taken several centuries to evolve and become more sophisticated. Initially, political arguments against globalization were often intended to preserve the role of the state; now they are often focused on the position of the labour force in both developed and developing economies.

Trade protection is often done with the best of intentions but, as the report goes on to consider, the possible effects of import taxes and duties, for instance, may not be what is expected. Then we quickly look forward (Section 3) to consider the possible implications of some suggested policies of the new US administration. Undesirable side effects are common, both over the short and long term. This applies both to the real economy and, for better or worse, to the financial markets’ reactions.

We conclude (Section 4) by summarizing the case for free trade. Economic history, we note, is full of examples showing that protectionism offers no long-term benefit and can often have unfortunate side-effects – both economic and political. Major industrial economies cannot avoid the implications of globalization and should accept the proven benefits of market economies. It can be difficult to make the rather abstract economic arguments for globalisation persuasive, when set against the associated uncomfortable realities of economic change. The time has come to grasp the dynamics of global trade and to shape its evolution for the benefit of everybody.

By Christian Nolting, Global Chief Investment Officer, and Markus Müller, Global Head CIO Office

Introduction

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 3

Figure 1: Globalization over 5 centuriesShown is the sum of world exports and imports as a share of world GDP

Source: Estevadeordal, Franz & Taylor, 2003, upper/lower estimate; Klasing & Milionis, 2014 and Klasing & Milionis, 2014 based on data by Maddison; Penn World Tables (8.1); Deutsche Bank Wealth Management; Data at March 2017.

Estevadeordal Penn World Tables Frantz & Taylor Klasing & Milionis

60%

50%

40%

30%

20%

10%

0%

1500 17001600 1800 1900 2011

First siege of Vienna 30-Year War War of Spanishsuccession

7-Year War Napoleonic Wars Franco-German WarW

W I

WW

II

Industrial Revolution Depre

ssio

n

Age of Religious Discord

Trade has existed from the earliest civilisations. For thousands of years, the exchange of goods has not only increased prosperity, but it has also led to a constructive exchange of experience, knowledge and culture, and has been an important driver of innovation. In ancient times, global trade was conducted largely across well-established trade routes. The fabled journey of the Queen of Sheba, mentioned in the Bible and the Koran, to the legendary court of King Solomon in the 10th century BC is said to have been along the Frankincense Road, one of the world’s oldest trade routes. Probably even better known is the Silk Road – a network of caravan routes that for over 1,500 years was used for the exchange of goods and culture between Asia and Europe.

The discovery of the New World by Europeans was driven by trade interests. In 1492, when Christopher Columbus obtained assistance for his westward sea voyage, his aim was the discovery of a new trade route to India. In 1600, the royal charter of the British East India Company (originally the English East India Company), granted the company the rights to all trade between the Cape of Good Hope and the Straits of Magellan. At times, in over its 250-year history, the East India Company controlled around a fifth of global trade, and it is closely associated with the development of Britain into a colonial power. There were comparable developments in other European countries to extend their colonies and share of global trade. For example the Netherlands established extensive global trade and colonial interests through the

Dutch East India Company and the Dutch West India Company.

The age of colonialism is also described as the age of the First Globalisation. During the Age of Discovery, much trade was in ‘colonial goods’, e.g. spices such as pepper and saffron; semi-luxury products such as coffee and cocoa; cloths such as silk and cotton; and other goods or commodities that could not be produced in Europe and for which there were no competing products. With the development of colonialism, the availability of products was increasingly superseded by cost as the main reason for trade. This in turn encouraged technological progress.Typical innovations of the “First Globalisation” correspond with the unfolding “Industrial Revolution”. Technologically, it resulted in better

1. The historical development of global trade

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 4

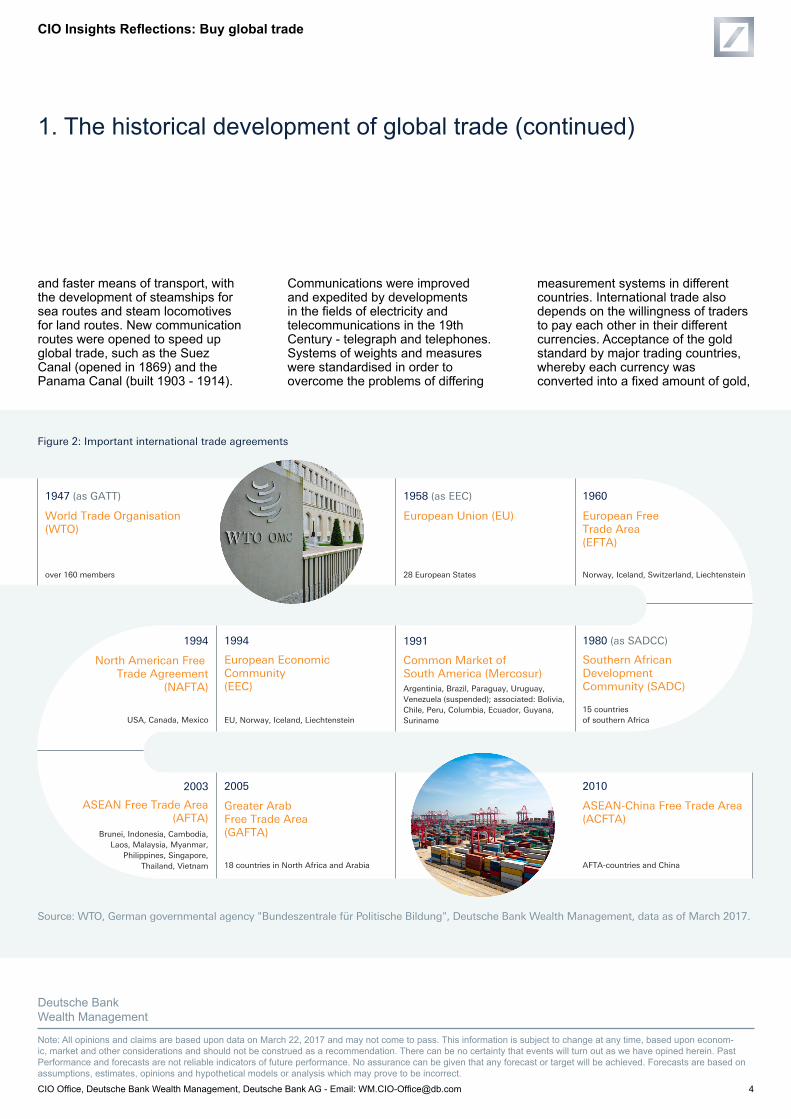

1947 (as GATT)

European Union (EU)

28 European States

1958 (as EEC)

European Free Trade Area (EFTA)

Norway, Iceland, Switzerland, Liechtenstein

1960

Southern African Development Community (SADC)

15 countries of southern Africa

1980 (as SADCC)

EU, Norway, Iceland, Liechtenstein

European Economic Community (EEC)

1994

North American Free Trade Agreement

(NAFTA)

USA, Canada, Mexico

1994

Greater Arab Free Trade Area (GAFTA)

18 countries in North Africa and Arabia

2005

ASEAN-China Free Trade Area(ACFTA)

AFTA-countries and China

2010

World Trade Organisation(WTO)

over 160 members

Common Market of South America (Mercosur)

1991

Argentinia, Brazil, Paraguay, Uruguay, Venezuela (suspended); associated: Bolivia, Chile, Peru, Columbia, Ecuador, Guyana, Suriname

ASEAN Free Trade Area(AFTA)

2003

Brunei, Indonesia, Cambodia, Laos, Malaysia, Myanmar,

Philippines, Singapore, Thailand, Vietnam

Figure 2: Important international trade agreements

Source: WTO, German governmental agency "Bundeszentrale für Politische Bildung", Deutsche Bank Wealth Management, data as of March 2017.

and faster means of transport, with the development of steamships for sea routes and steam locomotives for land routes. New communication routes were opened to speed up global trade, such as the Suez Canal (opened in 1869) and the Panama Canal (built 1903 - 1914).

Communications were improved and expedited by developments in the fields of electricity and telecommunications in the 19th Century - telegraph and telephones. Systems of weights and measures were standardised in order to overcome the problems of differing

measurement systems in different countries. International trade also depends on the willingness of traders to pay each other in their different currencies. Acceptance of the gold standard by major trading countries, whereby each currency was converted into a fixed amount of gold,

1. The historical development of global trade (continued)

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 5

facilitated the development of global trade during the 19th Century.

The First World War (1914-1918) had a huge impact on global trade. The War restricted the global exchange of goods and money, and also ended Europe’s dominance of international trade. The USA became the dominant global trading nation. At the beginning of the 20th century, US President Roosevelt began the transformation of the USA from economic isolationism to increasing international influence. This influence increased during the First World War, with the USA avoiding military involvement until 1917. The late 19th Century and early 20th Century were a period when commerce was dominated by major US ‘trust’ corporations, such as Rockefeller’s Standard Oil. New mass production technologies (for example, for the motor car and electrical devices) became affordable for ever-greater numbers of the population. In the transport sector, the age of civil aviation developed from the early 20th Century.

New York took over from London as the most important centre for international trade and finance. Global economic growth came to a halt, and went into reverse, following the Wall Street Crash in October 1929, leading on to the era of the Great Depression in the USA (characterised by protectionist trade policies). The Second World War and the end of the gold standard eroded the basis

of a global trading system that had functioned for many generations.

After the end of the Second World War, the world divided into East, dominated by the USSR, and West, dominated by the USA. Over time, countries of the former colonial empires became independent, and a period of bilateral and multilateral trade agreements began. In establishing the Commonwealth of Nations in 1947 (originally the British Commonwealth of Nations), Britain linked its former colonies into a loose union of states and trading partners. The main Western nations established the General Agreement on Tariffs and Trade (GATT) in 1947. This eventually developed into the World Trade Organization (WTO) in 1995. US aid for the reconstruction of Europe facilitated the development of The Organisation for European Economic Cooperation (OEEC), established in 1948 to run the US-financed Marshall Plan for the reconstruction of Europe. This expanded from 1961 into the Organisation for Economic Cooperation and Development, with countries such as the USA and Canada becoming members. Collaboration between a number of Western European countries to form the European Coal and Steel Community (ECSC) in 1951 led to the creation of the European Economic Community (EEC) in 1957. Among the USSR-led countries of the Eastern bloc, the Council for Mutual Economic Assistance (CMEA) was set up in

1949. A global monetary system was established in 1944, before the end of the Second World War, at Bretton Woods in New Hampshire, USA.

The ultimate aim of all international trading and monetary agreements is the creation of a basis for the international exchange of capital, goods and services. Further growth in global trade depends to a large extent on the removal of trade barriers such as import taxes and other regulatory restrictions like import quotas. Following the Second World War, the economic momentum from reconstruction came to an end, and countries sought to pursue continuing economic growth through international trade. Within just a few decades, an enormous wealth gap developed between the economically prosperous ‘open economies’ of the West and the closed ‘planned economies’ of Eastern Europe, which were characterised by a low level of economic momentum and widespread product shortages. By 1973 the Bretton Woods system had broken down, and the global economy was adjusting to the need for floating exchange rates.

From the 1990s onwards, the collapse of the USSR, partly a consequence of the enormous economic differences, accelerated the Second Globalisation, which had started shortly before. Technological progress - computers, satellites, mobile communications and container-based global transport systems - all helped revolutionise the global division of labour and international trade. Emerging economies in Asia and the Pacific region, commodity-rich countries of the former Soviet Union as well as China, as it started opening up

Market economy and free international trade have been key drivers of prosperity throughout

the 20th century.

1. The historical development of global trade (continued)

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 6

associatedmembers

NAFTA

MERCOSURSADC

EU

Figure 3: Trading blocks and inhabitants

Source: WTO, EAEU, NAFTA, MERCOSUR, SADC, ASEAN Deutsche Bank Wealth Management, data as of March 2017

EAEU

~360 mln.

~260 mln. ~300 mln.

~510 mln.

~610 mln.

~180 mln.

ASEAN

to the world economy, became increasingly important participants in global trade. The creation of global supply chains gained momentum, with product design and development, component manufacture and final assembly spread across different parts of the world. Falling transport costs facilitated this ever-increasing division of production processes and the transfer of various stages of production to whatever was the most favourable geographical location. Development of new products in the think tanks of highly-developed countries, manufacture of components all over the world and wage-intensive assembly in low-wage countries became a common feature of production in the global economy.

The products developed for the global market can now be bought, with minimal variations or modifications, throughout the world. Customs duties, tax differences and non-tariff barriers have emerged as a major barrier to the further expansion of global trade. Import duties and import quotas in particular are intended to protect domestic producers against cheaper (and more efficient) foreign competition. There is an argument that import duties do not protect a country that imposes them, but instead damages it. With imported intermediate goods (components or raw materials), import duties mean higher input costs for domestic producers. This makes domestic production more expensive, and so tends to encourage the migration of production to other countries by companies with a high proportion of imported intermediate goods in their end-products. Higher domestic production costs mean that the people of the country cannot afford to buy as many of the product, or

they suffer from the transfer of jobs, production sites and even entire industries to other countries. Another feature of increasing globalisation, however, is that through the greater involvement of low-wage countries and the automation of production in international production processes, wages are depressed for large parts of the population in more advanced industrial countries. This is one of the reasons for the ever-increasing criticism of globalisation, in political circles and helps to explain the growing opposition to globalisation which is on the political agenda in a number of states. Calls for an end to globalisation, the rejection of multilateral trade agreements, a

return to national economies and their protection through import duties, tariffs and other regulations have become commonplace.

However, in the past open national economies have usually created greater prosperity for more people than closed (protected) economies. Competition and free markets foster innovation and keep costs low. Division of labour and the use of comparative cost advantages reduce inefficiencies and protect resources.

1. The historical development of global trade (continued)

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 7

EFFECT OF FLOATING EXCHANGE RATES

International trade requires an exchange of currencies between the countries that trade with each other. The currencies are converted through an exchange rate that is determined by the legal framework of the respective countries and their political agreements with each other, reflecting each country‘s economic policy interests. While there is no such thing as one ideal exchange rate system that best suits all countries in all circumstances, since the introduction of a flexible exchange rate system between the British Pound and the US-Dollar in 1972, flexible exchange rate systems have increasingly gained ground. One year after the UK and the US, Japan and the most important European countries adopted flexible exchange rate systems as well, and abolished capital controls. Flexible exchange rates are determined by demand and supply. Through upward and downward adjustments in the exchange rate, an equilibrium in the trade balance with the respective trading partners can be reached over time. Generally, central banks act very cautiously in the foreign exchange markets and intervene only (and typically in accordance with other relevant central banks) if an exchange rate overshoots or when special circumstances call for it, for instance if the normal functioning of the currency market is at stake.

EFFECT OF TRADE ON INFLATION

Free international trade in general leads to specialisation in the production of goods by countries, for which they are particularly competitive. This competitive advantage may exist because the country can produce them more cheaply or because they are of a quality that is particularly sought after in the market. Globalisation increases competition between producers, which tends to depress prices and dampen inflationary tendencies. Conversely, import duties tend to lead to price increases and higher rates of inflation. The effect of import duties on the price of goods in domestic markets depends on the importance of the taxed goods for the national economy and on how they are represented in the national goods basket used to calculate the country‘s rate of inflation.

Economic Focus

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 8

In the history of the global economy, there have been numerous attempts by governments to keep foreign goods away from the domestic market. Import duties have commonly been used as measures to restrict the amount of imports. The view taken by government in these circumstances is that duties make foreign goods more expensive and so help domestic producers gain a temporary competitive advantage over foreign rivals. They increased government revenues. Import duties were used extensively as sources of government finance in the 18th and 19th centuries.However a classic example of this mercantilist economic approach was, in France, which in the 17th century, under Jean-Baptist Colbert, Finance Minister for King Louis XIV, imposed both duties also quotas on imported goods.

THE PRINCIPLE OF MERCANTILISM:

Mercantilism is an approach to economics that lends support to the view that protectionism benefits national economies. Mercantilism was commonly practised by countries in Europe between the 16th and 18th Centuries. It promoted government regulation of the national economy, with the objective of increasing the country’s economic strength and wealth at the expense of other countries. It was considered that the total amount of global wealth was more or less fixed, so the only way in which a country could gain wealth was to take a bigger share of global trade from other countries. An excess of exports over imports would result in a ‘profit’ – extra wealth, in the form of a bigger hoard of gold. At a time of slowdown in global trade, such as occurred in recent years,

some commentators (and politicians) have given support to mercantilist ideas, arguing that trade policy should be aimed at reducing balance of trade deficits or protecting balance of trade surpluses.

Mercantilism fell out of favour towards the end of the 18th Century. The beginning of the end of mercantilism is associated with the publication of The Wealth of Nations (1776). Its author, Adam Smith, argued against mercantilism. He argued that there was no benefit in increasing a country’s stock of gold – doubling the quantity of precious metal would only lead to a doubling of the prices of goods - and that it is therefore harmful to swap scarce goods (exported abroad) for precious metals. Adam Smith was also convinced that free trade with other countries was of great advantage to a national economy, in particular because of division of labour (specialisation). He believed that international trade in goods should accordingly be the result of creating free market prices, i.e. prices for imports or exports should not be changed by duties or subsidies, because these would reduce the quantity of goods produced globally and the prosperity of protectionist countries. According to Adam Smith, each country should specialise in producing the goods where it has a clear competitive advantage over other countries, and it should export these goods in exchange for other goods that it needs.

The free trade arguments of Adam Smith were advanced further by the economist David Ricardo. One of the issues that Adam Smith had not addressed was how global free trade is beneficial when one country is at a

competitive disadvantage to another in the production of all goods. In this situation, should the inefficient or high-cost country avoid participating in global trade, because imported goods might destroy its domestic producers? The country might be flooded by cheaper goods from abroad, thereby paralysing domestic production. In his 350-page book “On the Principles of Political Economy and Taxation” (1817), Ricardo on just half a page illustrated a famous example which represents a breakthrough in economic thinking. He used a simplified a model in which there are two economies, and two goods.

In order to avoid restricting each country to the benefit of what can be produced locally, there needs to be an exchange of goods between countries. The fact that an open economy favourable to trade can produce more than an autarky, allows more consumption and prosperity for all. Ricardo‘s example can be developed even further in order to show the significant meaning of his theory.

Ricardo’s conclusion was that no country can just import goods without at the same time exporting other goods. The simple mechanisms of foreign trade described by Ricardo might be considered no longer appropriate, as economies have become ever more complex over time. However the principle advanced by Ricardo remains valid. Ricardo’s ideas became the founding principle of economic liberalism, which was adopted by many countries throughout most of the 19th and 20th Centuries. For example, in the early 19th century the average rate of import duties in the USA exceeded 40%, but in the second half of

2. The theoretical basis for free trade or protectionism

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 9

this century it decreased to 20%.1 England was a leading exponent of economic liberalism, spearheading growth in international trade through industrialisation.

One of the most skilled protagonists of the doctrine of free trade was the French economist Frederic Bastiat. He wrote The Candle Maker’s Petition in the mid-19th century as a satire against protectionism.

In the arguments of Bastiat, as with Ricardo, the advantages of free trade prevail, since it lowers costs through specialisation and the division of labour. But only if relevant rules of ‘fair play’ are established and adhered to. Labour and capital must be flexible and able to adapt if the general economic conditions change. If these conditions are met, international trade should not lead to long-term (structural) unemployment in any country. The assumption is that every country has a comparative cost advantage in the production of some item or commodity. Economic policies, however, must create and protect the necessary ‘fair play’ framework for the open economy so that it operates efficiently.To facilitate international exchange, there is a need, among other things, for relevant market places, trade routes, free movement of capital, and business contacts with the relevant language skills. A regulatory framework is required to ensure that incentives exist for an economy to adapt to change (flexibility in labour and capital markets), so that the national economy is able to

operate at close to its full theoretical potential. In Germany this concept is known as ordoliberalism. An ordoliberal framework facilitates adaptation of the national economy to the constantly changing realities – on the part of the companies through innovation and efficiency, and on the part of employees through education and training.

In the 19th Century, a well-known critic of the doctrine of free trade was the German economist Friedrich List. He argued for a type of capitalism called a ‘National System’. He

of productivity, which was putting it at a clear advantage by virtue of its extensive industrialisation. This protection should last until such time as the economy of the country in Continental Europe was on an equal footing with that of Britain as regards the state of industrial development. This approach is known as the Infant Industry Argument. List’s ideas have a growing number of supporters today. Opponents of List’s ideas argue that customs barriers created through protectionist measures would be hard to break down again. They might not be temporary, as List intended.

2. The theoretical basis for free trade or protectionism (continued)

The ongoing debate between free marketers and protectionists has been a key feature of

economic thinking over the past two centuries.

above all criticised the fact that most economists shared a view of the national economy that was too static. In reality, economies were continuing to grow, driven by technological change and innovation. Countries that were slow to innovate were at risk of competition from countries that were more advanced technologically. List therefore argued that the productive forces in a country’s economy should receive support from the government to encourage technical progress. List was therefore developing aspects of modern growth theory that deem technical progress to be something that can be influenced. List’s main line of argument (at the beginning of the 19th Century in Continental Europe) was that a national government should levy protective or educational tariffs against imports, particularly from Britain. This would protect it against Britain’s high levels

If protectionist measures remain in place over the long term, this would create a risk of the country’s protected economy not developing any further, but getting stuck in their current state, and thereby forfeiting competitiveness over the longer term.

Another concern of opponents of free trade is that cheap jobs in emerging and less-developed countries would lead to cutbacks in expensive jobs in developed countries. In this context, it is useful to look at the Heckscher-Ohlin model, which was developed by two Swedish economists in the early 1930s. According to this model, countries will export products that make abundant use of their cheap factors of production, and import products that would use the country’s scarce resources. The competitive advantage of a country is therefore determined by its ‘ownership’ of

1 Tariffs and growth in late nineteenth century America, Douglas A. Irwin, Working Paper 7639, National Bureau of Economic Research, Cambridge, Massachusetts, April 2000.

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 10

various factors of production. This means for example that capital-rich countries would tend to export capital-intensive goods, whilst labour-rich countries would tend to concentrate on labour-intensive goods. A consequence of free trade, however, would be a fall in countries with developed economies. This argument will be explained in more detail.

From the Stolper-Samuelson theorem (1941), which extended the Heckscher-Ohlin model, suggests that in a capital-intensive economy, wage increases for low-skilled workers without foreign trade would be greater without foreign trade than in an economy with free trade and an open economy. This conclusion

from the Heckscher-Ohlin model can be used to argue that foreign trade is not worthwhile, and might even be harmful. However this conclusion does not take several factors into consideration. Firstly the argument ignores the impact of technological progress and the resultant increases in productivity in capital-intensive business. Furthermore it should be noted that over half of global trade is between developed countries, where the Heckscher-Ohlin model does not apply.

In reality, every country can produce both capital-intensively and labour-intensively, and even with foreign trade they need not restrict themselves to either capital-intensive

or labour-intensive production. Free trade certainly favours national economies which are innovative and which concentrate on products for which they can use their natural advantages. To this end, to obtain the most benefit from free trade, workers must continuously receive further training and retraining. It is then possible – through improvements in productivity – that real wages will increase for less-skilled workers. Protectionist measures, on the other hand, above all else protect the status quo. With protectionist measures, a nation’s prosperity distributed more evenly in the short term. However in the longer term the wealth of these closed economies will not grow. They will suffer productivity losses

2. The theoretical basis for free trade or protectionism (continued)

North America South America Europe Commonwealth of Independent States Africa Middle East AsiaSource: World Trade Organisation(2016): World Trade Statistical Review 2016, p.12. Data as of March 2017.

Merchandise trade of WTO members by region, 2005-2015

40%

50%

60%

70%

80%

90%

100%

30%

20%

10%

0%2005 2010 2011 2012 2013 2014 20152009200820072006

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 11

example the USA’s current account deficit might be a warning signal. (The USA’s deficit is matched by balance of trade surpluses for other countries such as Germany.) The deficit may, for example, indicate a lack of competitiveness in the US economy.

THE PRINCIPLE OF BALANCE OF TRADE SURPLUSES:

Let us assume (for simplicity) that Germany exports goods to the value of €1bn to the USA and imports US goods to the value of $500m. At an assumed exchange rate of 1:1, Germany would achieve an export surplus of €500m or $500m. The German exporters can either convert their profits from US dollars into euros, allowing them to invest in the domestic market, or they can invest their dollars in the USA (direct investment). This means that a capital export from Germany to the USA follows on from the trade surplus of German exporters. If the trade surplus continues over time, German companies would increasingly shift their investments abroad. This could become problematic if there is a resulting lack of domestic investment and job losses. For the USA, there is the perceived problem of a current account deficit. As interest also has to be paid on the capital imported from Germany, the USA will become increasingly indebted to Germany, interest payments to Germany will increase over time. Continual export surpluses and constant balance of trade deficits over time could be problematical for both countries. A flexible currency can help here. For the country with a balance of trade deficit, there will be increasing sales of its currency in the currency markets, as German exporters

exchange their dollar income for euros, or US importers by euros in order to pay German suppliers. In theory, supply and demand for the two currencies ought eventually to result in an equilibrium rate of exchange. (cf. also the J-Curve effect)

On the other hand, however, it may also mean that the USA becomes an attractive investment target where German investors like to invest their money, though a prerequisite would be that the incoming is capital really invested. As a result of increasing investment in the USA by German investors, the effect of capital flows will offset the flows in payments for goods, and the exchange rate could remain at a level where the US balance of trade deficit becomes ‘permanent’. Current account deficits and surpluses are neither not good or bad in themselves – it is rather their structure that is important.

and a falling standard of living, and ultimately a loss in international competitiveness. Another argument against free trade is the use by some countries of unfair trade practices. International trade agreements can offer a degree of protection against such practices, such as dumping.

THE PRINCIPLE OF DUMPING:

Undercutting of domestic producers’ prices through imports from cheaper foreign competitors is frequently cited as an argument against free trade and in favour of import barriers. In the strict sense of the word, dumping only takes place if a foreign competitor offers goods in the domestic market at a price below their cost of production (and so is ‘getting rid’ of surplus production at a loss). A justifiable criticism of dumping is that foreign competitors may keep prices low for a time, in order to squeeze competitors out of the markets. When they have been successful with this aim, they are then able to operate as an oligopoly or monopoly, raising prices to relatively high levels. In such circumstances, the introduction of protective customs duties is reasonable and is even permitted within the WTO’s guidelines.

Another issue to consider in the context of free trade is the issue of countries with a surplus in their balance of international trade. For the exporting country, an export surplus improves the domestic employment and income, and so is likely to be regarded favourably by that country. International movement of capital is held to be a kind of reflex in response to previous flows of goods. However, there are other various ways of looking at this. For

2. The theoretical basis for free trade or protectionism (continued)

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 12

DAVID RICARDO: PART I –

England needs 20 hours of work for the production of one unit of cloth and 30 hours for the production of one unit of wine. Portugal only needs 10 hours for the production of each of these goods. Therefore, Portugal has a clear absolute advantage in the production of both goods. As per Ricardo, it isn’t the absolute but the relative cost difference that matters. Portugal‘s relative cost advantage is greater in the production of wine than in the production of cloth, because the former is three times more time-intensive to produce in England than in Portugal, whereas the production of cloth is only twice as time-intensive in England. Both countries would benefit if England

were to specialise in the production of cloth and Portugal in the production of wine. How does

this work? Let‘s assume that both countries have a total of 40 working hours at their

disposal. Without trade, England could produce half a unit of cloth and one unit of wine, while Portugal could produce one unit of cloth and three units of wine. Therefore, in total one and a half units of cloth and four units of wine would be produced. In the next step, each country focuses on producing just one product. The total production of both

countries would thus reach four units of wine (produced by Portugal) and two units

of cloth (produced by England). This way, thanks to specialisation, an additional half unit

of cloth could be produced, in spite of unchanged total input of 40 hours of labour.

DAVID RICARDO: PART II – TRADE LEADS TO DIVISION OF LABOUR

Since the production of both commodities in Portugal is less labour-intensive than in England, the question is how the free trade between them can nevertheless work to the benefit of both countries. If each labour unit in both countries is paid in one monetary unit, then the production of both products is cheaper in Portugal (since Portugal is less labour-intensive). England would import both products, because they are cheaper than similar items made by domestic producers. This would result in an outflow of monetary units from England to Portugal, leading to lower wages and lower prices in England for English-produced goods. In Portugal, on the other hand, prices and wages would rise. This process would continue until England

can produce one of the products, wine or cloth, more cheaply in terms of monetary units than Portugal can. This product might be cloth.If England can now make cloth more cheaply than Portugal, the two countries will exchange cloth for wine. England’s relative cost advantage in cloth production takes the form of an absolute price advantage. Ultimately, trade automatically brings about a division of labour between the two countries with England specialising in cloth and Portugal in wine. The total volume of production in both wine and cloth will be greater than in the original situation, with both countries using their labour resources to the full and in an efficient way. Source: vgl. David Ricardo, On the principles of political economy and taxation (1817).

FREDERIC BASTIAT: PETITION DES FABRICANTS DE CHANDELLES, OEUVRES COMPLETES [THE CANDLE MAKER’S PETITION, COMPLETE WORKS], GUILLAUMIN, 1863

The Candle Makers’ Petition (1863) was an imaginary petition by the candle makers of France to the Chamber of Deputies, claiming that they suffered from ruinous competition at the hands of a foreign rival, the sun. The sun was flooding the domestic market for light at a ridiculously low price (for free), and when the sun is present, all use of candles ceases. The candle makers also argued that the sun was encouraged in its attack on the French market for light by the English candle makers: the sun did not damage the English market as much, since England was continually covered by fog. The candle makers therefore asked the Chamber of Deptuties to introduce regulations that all windows and similar apertures should be closed up, to keep out the sun, because in this way demand for candles and lamp oil would be increased. They further argued that this would lead to more employment – not only for producers of candle and lamp oil but also in other associated economic sectors. The entire national economy would thereby benefit (ignoring the fact that consumers of candles and lamp oil would suffer, by having to pay more for their light). The candle makers claimed that they were by all means in favour of competition, but only if it was fair. Competition on the part of the sun was unfair, however, as the energy offered by the sun didn’t have a price.

The history of economic thought

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 13

But a competitive advantage for English candle makers over competitors in other countries would also be unfair, because English fog created a more favourable market for sales of candles.

Source: vgl. Frederic Bastiat, Petition des fabricants de chandelles (1863).

HECKSCHER-OHLIN-THEOREMLet us assume that two national economies have the same quality of production factors (production technology, labour skills and education, capital and land). Let us further assume that Country A has an abundance of capital and Country B has cheap labour. A further assumption is that both capital and labour are immobile and cannot be transferred to other countries.

Country A will then concentrate on the production of goods involving a high level of capital input whilst Country

B will specialise in labour-intensive goods. Because the same technologies are

available, Country B could also produce capital-intensive goods, but it will not do so, because capital is not abundantly available, and so in relative terms production of these goods would not be cheaper. This argument might seem to put forward the merits of free global trade.

However there is a question about how the level of wages and interest rates are

determined in the global market. As Country A will continue with the production and

export of capital-intensive goods, the previously abundant amounts of capital will decrease and as

capital becomes more scarce, the cost of capital costs, i.e. the rate of interest, will increase. For similar reasons, in Country B the price of labour, i.e. wage levels, will increase because of the growing scarcity of labour as the country produces more labour-intensive goods for export.

As Country A was already able to produce capital-intensively, it can be assumed that, even before the start of trade with Country B, wage levels would be higher in Country A than in Country B, just as interest rate levels in Country B would be higher than in Country A because of the scarcity of capital. Through foreign trade, the prices of labour and capital in both countries would come more into line with each other (interestingly, without the production factors leaving their country of location).

In conclusion, over the course of time wages in Country A will fall towards wage levels in Country B. The national economy in Country A will profit overall from foreign trade but workers will experience lower wages. The adverse effect of lower wages is not offset by their ability to buy goods at cheaper prices. The ultimate reason for this is that increasing interest rates in Country A will result in decreasing capital input, which in turn results in falling productivity. Lower productivity causes real wages to fall.

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 14

The economic policies of the new Trump administration in the USA would appear to focus on encouraging domestic production and reducing the volume of foreign trade, especially imports to the US.

To achieve a reduction in a balance of trade deficit, it might be argued that there should be more import duties (and bilateral trade agreements between two countries rather than broader multilateral trade agreements). However, import duties not only affect prices but can also have further effects, such as a fall in trade volumes and possibly retaliatory action by other countries. It will probably be some time before the tax policy measures of the Trump

administration have been drawn up, and the legislation process has run its course and the relevant laws implemented. At the moment, only the outlines of the planned restructuring of the US tax legislation are known. We currently expect that the broad characteristics of US policy objectives will be along the lines of alignment with the tax legislations in the OECD countries, reorientation of the taxation to the country in which the goods are consumed, the Destination Principle, and a reduction in incentives for companies to transfer production of goods abroad. It is thus highly probable that trade taxes will be

THE PRINCIPLE OF BORDER TAX ADJUSTMENT (BTA):

Border Tax Adjustment (BTA), a concept briefly considered by President Trump but now apparently abandoned, could subject imports to additional taxation and at the same time free export revenues from taxes. For US companies that import goods from abroad, the effect of BTA would be that the costs of the imported goods would no longer be allowable as a charge when calculating taxable profits.In comparison, US companies that buy their intermediate products from domestic producers would continue to offset these costs for tax purposes.

3. A look ahead – current policy and its restrictive momentum

′The spirits I summoned up, I now cannot rid myself of’, Goethe wrote as long as 200 years

ago about the unforeseen consequences of well-meant ideas.

part of the tax policy changes. The jury is out on whether and to what extent taxation of international trade would be consistent with established international trade agreements. It is anticipated that taxation of US companies with high imports will rise, as a result of a Border Tax Adjustment. Under such an arrangement, costs of imported goods would not be eligible for set-off against revenue when computing a company’s taxable profits. The economic effect of this non-eligibility of costs for offsetting against tax would be similar to the effects of an import tax.

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 15

POSSIBLE EFFECTS OF IMPORT TAXES AND DUTIES

Microeconomic theory states that when the price of a good is increased, demand for the good will fall. The effect on demand of the price increase can be separated into a substitution effect and an income effect. The substitution effect occurs because some consumers of the product switch to buying an equivalent product of a similar quality but at a lower price. The income effect occurs because consumers continue to buy the product, but in smaller quantities, because they cannot afford to buy as much within their fixed income and choose not to spend more money. Because of the higher price they have to spend a higher proportion of their income on acquiring the more expensive product. This concept of the effect of a price change can also be applied to foreign trade. If a tax is levied on imports of a commodity from a particular country, this leads to a trade diversion effect (similar to a substitution effect), since imports of the commodity from this country might be replaced by equivalent goods, either from another country or from a domestic source. There is also a repulsion effect (similar to an income effect), since because of the higher price for the imported commodity, fewer goods might be imported over the course of time. The effects of an increase in price for a commodity on the global market may take some time to be felt. Producers of the commodity might try to offer it on the global market and there might be pressure on the price. With the introduction of an import tax, the prices of the goods affected are immediately increased for domestic buyers. Buyers will as far as possible respond fairly quickly to the price change, with

evasive reactions, buying less and switching to the purchase of similar alternative products. Volume adjustments are usually slower to take effect, as there are often longer-term contractual relationships between suppliers and commercial buyers that as a rule can only be adjusted over the course of time. This means that in the short term, domestic buyers of foreign imports may be locked into buying the same quantities of goods, but at the higher price that includes import duty. Thus, in the event of state intervention in foreign trade to impose import duties, the short-term effect may be precisely the opposite of what is expected. It is only in due course of time, usually after about 6 to 12 months, when existing supply contracts come to an end, that the expected fall in the volume of the imported goods occurs. This phenomenon is known as the J-Curve effect.

Economic Focus

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 16

Economic history and economic theory are replete with examples showing that in the longer term interventionism and protectionism hardly have any chance of generating lasting benefit. In the past, they served rather for temporary protection of particular interests than the common good. Heavily- regulated isolated economies have historically not been successful in the long term. More or less prosperity for more or fewer people is as a rule associated with more or less freedom of trade. Innovation and competition as well as people and markets need rules of engagement and freedom to prosper. Stopping the clock doesn’t generate time, building walls doesn’t create space, restricting trade doesn’t create prosperity. Limitation benefits the redistribution of available resources rather than the creation of new resources.

Financial markets’ already observable pattern of reaction could continue. Investors might transfer funds from asset classes that are suffering from the expected measures to ones that are benefiting from them: from other currencies into US dollars, from shares in export-oriented companies in Europe and Asia to US shares – to mention just two examples. But when, as a consequence of politicians’ interventions, the US dollar apparently became too strong, the same politicians might think that immediate new – hitherto verbal – interventions were necessary. Not really a

successful start to a supposedly new economic order. ‘The first time we are free, the second time we are servants’ and ‘The spirits I summoned up, I now cannot rid myself of’, Goethe wrote as long as 200 years ago.

As regards the longer-term effects, we return to two interlinked observations. First, that nowhere in the major industrial countries can politics withdraw from the realities of globalisation. Second, that open markets appear to be the economically superior response in the medium to long term. Open markets strengthen competition, promote innovation, increase influx of capital, improve investment conditions – including for domestic investors – and in the longer term increase a country’s growth potential. This potential, however, is often stifled by restrictive locally-driven political decisions, above all in order to provide a quick fix to meet current challenges, without taking into consideration their effects as a whole. In reality, economic-added value is threatened not by globalisation but by interventions that serve the interests of individuals and not the general public.

Therefore a replacement of globalisation and free trade by the state is not what is needed. This fundamental principle applies unrestrictedly, even today. What is crucial is the recognition that globalisation, with its international division of labour and the associated

specialisation, differentiation and more intense competition, remains a strong driver of economic growth and prosperity. One should trust in market incentives, and for precisely this reason it is vital that one adjusts to a rapid change of pace, rather than try to ignore it.

So, in conclusion, we return to the point that we made earlier. Ever since Adam Smith, economists have been arguing that of all the well-known and achievable economic systems, the market economy is essentially the one that is superior to all the others in terms of its economic potential. Even though neither Adam Smith nor the economists after him have expressed it exactly in these terms, they nevertheless acknowledge the market economy as the order that mutually benefits all participants, one on which free and equal people can agree and that deserves recognition as a just order.

This requires courage and decisiveness on the part of politicians and companies, as well as readiness for change on the part of the people. People are by all means ready for change, but they want to know that any immediate privations will be worthwhile and that ultimately things will get better. Long-term economic gains may appear rather abstract, while the threat of short-term disruption can appear much more real. Moreover, public skepticism and confusion may be increased by the fact that appropriate reforms are often envisaged but implemented only half-heartedly due to concerns about people’s acceptance and political feasibility. This is a time for clear communication and the need for a solid commitment to continued free trade.

4. Conclusion: the case for free trade

Stopping the clock doesn’t generate time, trade barriers don‘t increase prosperity.

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 17

Global Chief Investment OfficerChristian Nolting1

Global Chief Investment Officer (CIO)

Regional Chief Investment OfficerLarry V. Adam4

CIO Americas

Tuan Huynh5

CIO Asia

Stéphane Junod8

CIO EMEA

Johannes Müller1

CIO Germany

International locations1. Deutsche Bank AG

Mainzer Landstrasse 11-17 60329 Frankfurt am Main Germany

2. Deutsche Bank AG, London 105/108 Old Broad St (Pinners Hall) EC2N 1EN London UK

3. Deutsche Bank Trust Company 345 Park Avenue 10154-0004 New York, NY United States

4. Deutsche Bank Securities 1 South Street 21202-3298 Baltimore, MD United States

5. Deutsche Bank AG, Singapore One Raffles Quay, South Tower 048583 Singapore Singapore

6. Deutsche Bank AG, Hong Kong 1 Austin Road West Hong Kong Hong Kong

7. Deutsche Bank (Switzerland) Ltd. Hardstrasse 201 8005 Zurich Switzerland

8. Deutsche Bank (Switzerland) Ltd. Place des Bergues 3 1211 Geneva 1 Switzerland

9. Deutsche Bank Trust Company Floor 1, 5022 Gate Parkway, Suite 400 32256 Jacksonville, FL United StatesContact us on [email protected]

Strategy GroupLarry V. Adam4

Global Chief Strategist

Dr. Helmut Kaiser1

Chief Strategist Germany

Daniel Kunz7

Strategist EMEA

Chief Investment OfficeMarkus Müller1

Global Head CIO Office

Sebastian Janker1

Head CIO Office Germany

Jürg Schmid7

Head CIO Office EMEA

Jeff Ng5

Head CIO Office Asia

Graham Richardson2

Financial Writer, CIO Office

Khoi Dang9

CIO Office Americas

Enrico Börger8

CIO Office EMEA

Contacts CIO Wealth Management

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 18

Important Note

Deutsche Bank Wealth Management offers wealth management solutions for wealthy individuals, their families and select institutions worldwide. Deutsche Bank Wealth Management, through Deutsche Bank AG, its affiliated companies and its officers and employees (collectively “Deutsche Bank”) are communicating this document in good faith and on the following basis.

This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by Deutsche Bank, are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not constitute an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice.

Deutsche Bank does not give tax or legal advice. Investors should seek advice from their own tax experts and lawyers, in considering investments and strategies suggested by Deutsche Bank. Investments with Deutsche Bank are not guaranteed, unless specified. Unless notified to the contrary in a particular case, investment instruments are not insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other governmental entity, and are not guaranteed by or obligations of Deutsche Bank AG or its affiliates.

Investments are subject to various risks, including market fluctuations, regulatory change, counterparty risk, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you may not recover the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of the investment are possible even over short periods of time.

This publication contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward looking statements expressed constitute the author’s judgment as of the date of this material. Forward looking statements involve significant elements of subjective judgments and analyses and changes thereto and/or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by Deutsche Bank as to the reasonableness or completeness of such forward looking statements or to any other financial information contained herein. The terms of any investment will be exclusively subject to the detailed provisions, including risk considerations, contained in the Offering Documents. When making an investment decision, you should rely on the final documentation relating to the transaction and not the summary contained herein.

This document may not be reproduced or circulated without our written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Deutsche Bank to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

Past performance is no guarantee of future results; nothing contained herein shall constitute any representation or warranty as to future performance. Further information is available upon investor’s request.

This document may not be distributed in Canada, Japan, the United States of America, or to any U.S. person.

© 2017 Deutsche Bank AG

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 19

Important Note

Kingdom of Bahrain For Residents of the Kingdom of Bahrain: This document does not constitute an offer for sale of, or participation in, securities, derivatives or funds marketed in Bahrain within the meaning of Bahrain Monetary Agency Regulations. All applications for investment should be received and any allotments should be made, in each case from outside of Bahrain. This document has been prepared for private information purposes of intended investors only who will be institutions. No invitation shall be made to the public in the Kingdom of Bahrain and this document will not be issued, passed to, or made available to the public generally. The Central Bank (CBB) has not reviewed, nor has it approved, this document or the marketing of such securities, derivatives or funds in the Kingdom of Bahrain. Accordingly, the securities, derivatives or funds may not be offered or sold in Bahrain or to residents thereof except as permitted by Bahrain law. The CBB is not responsible for performance of the securities, derivatives or funds.

State of Kuwait This document has been sent to you at your own request. This presentation is not for general circulation to the public in Kuwait. The Interests have not been licensed for offering in Kuwait by the Kuwait Capital Markets Authority or any other relevant Kuwaiti government agency. The offering of the Interests in Kuwait on the basis a private placement or public offering is, therefore, restricted in accordance with Decree Law No. 31 of 1990 and the implementing regulations thereto (as amended) and Law No. 7 of 2010 and the bylaws thereto (as amended). No private or public offering of the Interests is being made in Kuwait, and no agreement relating to the sale of the Interests will be concluded in Kuwait. No marketing or solicitation or inducement activities are being used to offer or market the Interests in Kuwait.

United Arab Emirates Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as defined by the Dubai Financial Services Authority.

State of Qatar Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial Centre Regulatory Authority. Deutsche Bank AG - QFC Branch may only undertake the financial services activities that fall within the scope of its existing QFCRA license. Principal place of business in the QFC: Qatar Financial Centre, Tower, West Bay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related financial products or services are only available to Business Customers, as defined by the Qatar Financial Centre Regulatory Authority.

Kingdom of Saudi Arabia Deutsche Securities Saudi Arabia LLC Company, (registered no. 07073-37) is regulated by the Capital Market Authority. Deutsche Securities Saudi Arabia may only undertake the financial services activities that fall within the scope of its existing CMA license. Principal place of business in Saudi Arabia: King Fahad Road, Al Olaya District, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.

United Arab Emirates Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as defined by the Dubai Financial Services Authority.

CIO Insights Reflections: Buy global trade

Deutsche BankWealth Management

Note: All opinions and claims are based upon data on March 22, 2017 and may not come to pass. This information is subject to change at any time, based upon econom-ic, market and other considerations and should not be construed as a recommendation. There can be no certainty that events will turn out as we have opined herein. Past Performance and forecasts are not reliable indicators of future performance. No assurance can be given that any forecast or target will be achieved. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

CIO Office, Deutsche Bank Wealth Management, Deutsche Bank AG - Email: [email protected] 20

Important disclosures UK

In the UK this publication is considered a financial promotion and is approved by Deutsche Asset Management (UK) Limited on behalf of all entities trading as Deutsche Bank Wealth Management in the UK.

Deutsche Bank Wealth Management (DBWM) offers wealth management solutions for wealthy individuals, their families and select institutions worldwide and is part of the Deutsche Bank Group. DBWM is communicating this document in good faith and on the following basis.

This document is a financial promotion and is for general information purposes only and consequently may not be complete or accurate for your specific purposes. It is not intended to be an offer or solicitation, advice or recommendation, or the basis for any contract to purchase or sell any security, or other instrument, or for Deutsche Bank to enter into or arrange any type of transaction as a consequence of any information contained herein. It has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor.

This document does not identify all the risks (direct and indirect) or other considerations which might be material to you when entering into a transaction. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by Deutsche Bank, are suitability and appropriate, in light of their particular investment needs, objectives and financial circumstances. We assume no responsibility to advise the recipients of this document with regard to changes in our views.

Past performance is no guarantee of future results.