wd- company -k and proxy reaching households worldwide

TRANSCRIPT

WD-40 COMPANY 2006 FORM 10-K AND PROXY

REACHING HOUSEHOLDS WORLDWIDE:

FRANCE AUSTRALIA PORTUGAL GERMANY

AMERICAS 65%

ASIA PACIFIC 7%

EUROPE 28%

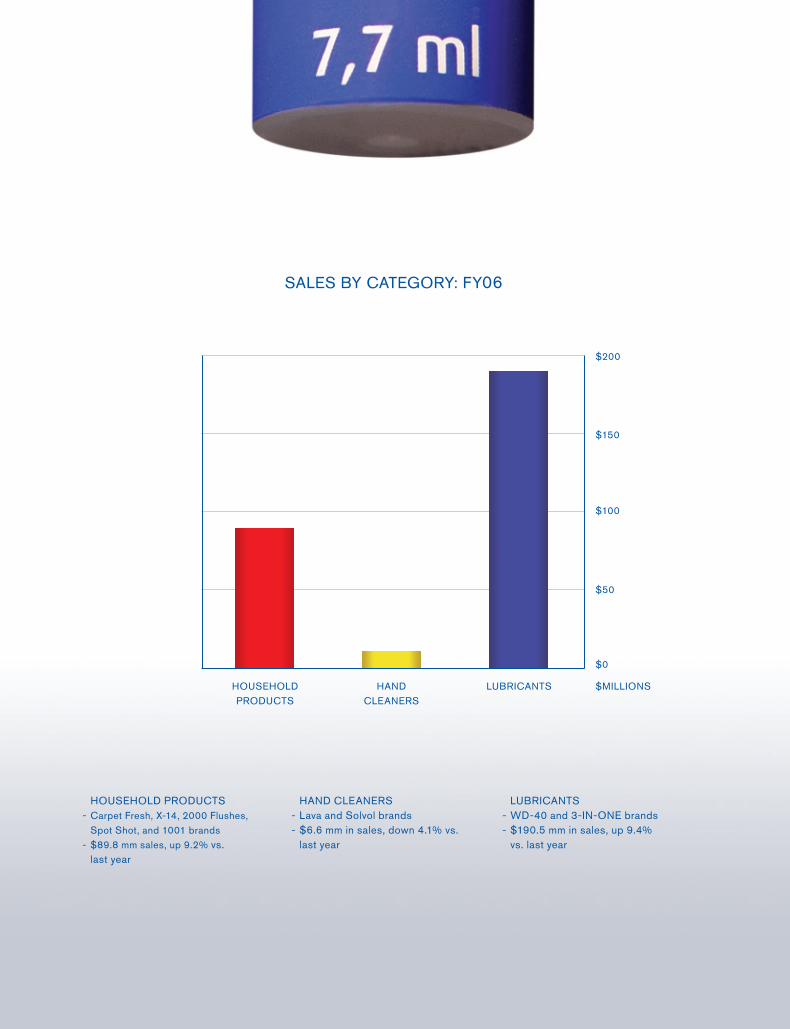

AMERICAS- $186.8mm, up 6.1% vs. last year- Lubricant sales up 3.5% vs. last year- Household products up 10.2% vs. last year- Hand cleaners down 1.6% vs. last year

ASIA-PACIFIC- $21.0mm, up 12.1% vs. last year- Asia sales up 17.4% vs. last year- Australia sales up 2.7% vs. last year

EUROPE- $79.1mm, up 15.7% in $US vs. last year- Strong growth in UK, France, Germany,

Italy, Spain, and Eastern Europe- Forex impact reduced sales by $2.9mm,

or 3.5% vs. last year

SALES BY SEGMENT: FY06

56% OF THE COMPANY’S TOTAL WD-40 BRAND SALES COMES FROM OUTSIDE OF THE U.S.

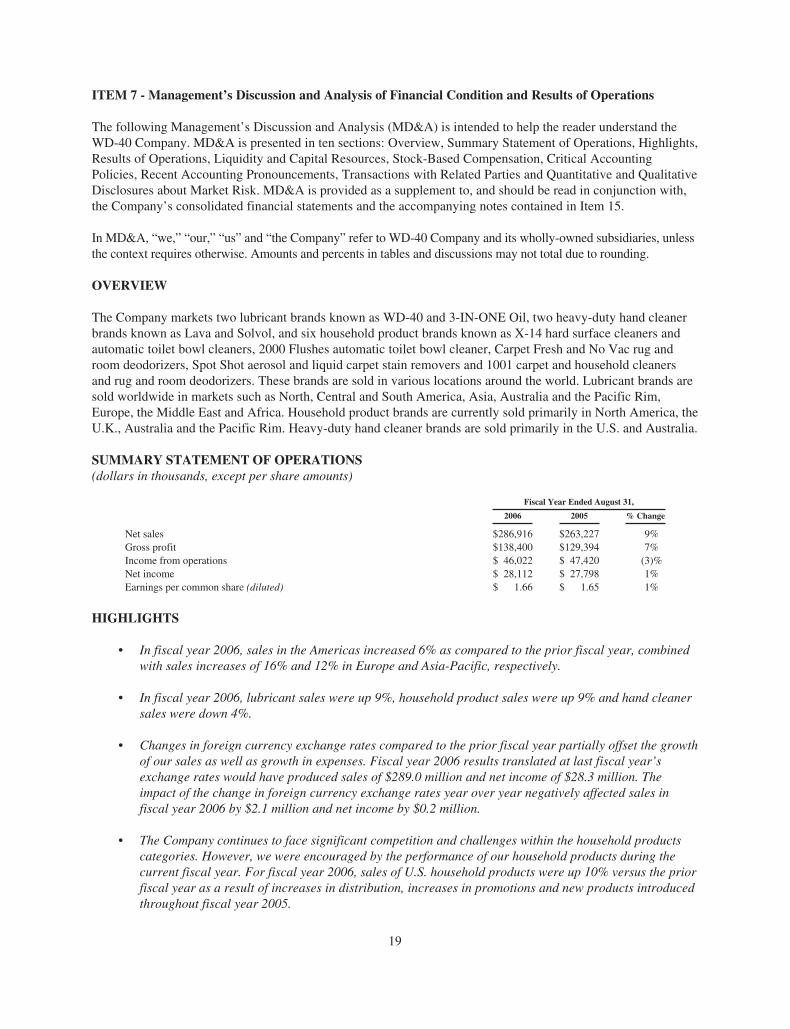

G’day,If I had to choose a headline for a news story for our 2006performance, it would read something like this:

“We only see one market, and it is global.”

It is satisfying to look back at the growth in all our trading blocslast year. Thanks to the hard work of our team, our great brandsand the strong infrastructure and market platforms we have builtover the years, we are anticipating steady growth in all geo-graphic markets. Our WD-40® brand is showing great promisein markets like China and Russia, and we anticipate stronggrowth over the next few years. This year, the Company hasdecided to open a direct sales office in Shanghai, China, andenter the next development phase for this important market.Other global markets—including Mexico, Germany, andIndonesia, just to name a few—show great promise.

Growth through innovation.Since we started on our path of innovative product developmentin 2002, each year we learn more about our consumers’ needsand how to deliver products that meet those needs. In the lastthree years our R&D group, which we call “Team Tomorrow,”has generated close to $86 million dollars in product innovationsalone. Some of the products that are showing early signs ofsuccess are the WD-40 Smart Straw, the WD-40 No-Mess Pen,and our Spot Shot® trigger spray. WD-40 brand salesincreased by 9.8% in fiscal 2006 compared to fiscal 2005. Thebrand has now experienced global growth for five consecutiveyears.

Other products have enjoyed significant growth. Sales of all ourhousehold brands grew in 2006.

As a company, we are especially proud that our emphasis oninnovation continues to result in the development of productsthat are mainstays in the home and workplace—not onlyperpetuating the WD-40 brand legacy but also opening up newopportunities for us in a variety of trade channels and markets. Inthe U.S., for example, our WD-40 and household brands aregaining traction in areas such as janitorial services, office sup-plies, and arts and crafts.

Controlling costs.We learned more about balancing our advertising and promo-tional investment to make every dollar we invest in these areascount. With new leadership in our U.S. marketing team, we haveseen many changes in this area that have already added value ina short time.

We also had to take a hard look at our cost of goods. Oursteel prices have increased in excess of 65% since 2000. Oilprices have impacted us with plastics, lubricant products, andfreight transportation. We implemented a price increase tooffset some of these increases and we created a team toreview costs of goods and trends, and to provide strategicsolutions to minimize the pressure on us in this area.

We hope you are pleased with our results this year despitethe market challenges. We feel we did a good job at manag-ing the business.

Looking ahead.Though there are still many mountains for us to climb, we arebecoming more global each day, and our innovation andgeographic expansion will continue to drive our growth. Ianticipate that we are going to experience the same chal-lenges in our cost of goods areas. However, we are confidentthat if we manage our business with rigor, we will minimizethe impact to the bottom line.

Business is not without risk, so you should be continuallyaware of some of the areas that could affect our company.Because litigation seems to be an ever-increasing part ofsociety, your company will always have some legal exposurearound the world.

Be assured, however, that our company will take a stanceagainst frivolous lawsuits.

In closing, I encourage you to read our 10-K, which providesdetailed highlights of our company’s performance.

Of course, I would be remiss if I didn’t thank our shareholdersfor their continued support, and thank our employees for theirhard work over the past year. Each and every one of youhelped make 2006 very productive.

As the company looks ahead, we remain confident in ouroutlook. As we say at WD-40 Company, “there is somethingsignificant yet to do.”

Garry Ridge

PROFITABILITY RATIOS

(after tax)Return on Sales

Return on Assets

Return on Equity10% 10% 18%

WTD AVERAGE SHARESOUTSTANDING, DILUTED (in millions)

SALES(in millions)

SALES PER EMPLOYEE (in thousands)

EARNINGS PER SHARE(in dollars)

YEAR EARNINGS(in millions)

03 04 05 06 03 04 05 06

03 04 05 06 03 04 05 06 03 04 05 06

16.8

17.1

16.816.9

238.1 242.5

263.2

286.9

1,1181,128

1,155

1,191

1.71

1.50

1.65 1.66

28.6

25.6

27.8 28.1

Table of Contents

WD-40 Company Proxy StatementWD-40 Company Annual Report Form 10-KWD-40 Company Corporate Information

[THIS PAGE INTENTIONALLY LEFT BLANK]

WD-40 COMPANY1061 Cudahy Place

San Diego, California 92110

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To the Stockholders:

The 2006 Annual Meeting of Stockholders will be held at the Mission Valley Hilton Hotel, 901 Camino del RioSouth, San Diego, California 92108, on Tuesday, December 12, 2006, at 2:00 p.m. for the following purposes:

1. To elect a Board of Directors for the ensuing year and until their successors are elected and qualified;

2. To ratify the appointment of PricewaterhouseCoopers LLP as the Company’s independent registeredpublic accounting firm for the fiscal year 2007; and

3. To consider and act upon such other business as may properly come before the meeting.

Only the stockholders of record at the close of business on October 17, 2006 are entitled to vote at the meeting.

By Order of the Board of DirectorsMaria M. Mitchell

Secretary

San Diego, CaliforniaNovember 6, 2006

PROXY STATEMENT

GENERAL INFORMATION

This Proxy Statement is furnished in connection with the solicitation of proxies by the Board of Directors ofWD-40 Company for use at its Annual Meeting of Stockholders to be held on December 12, 2006, and at anypostponements or adjournments thereof. This Proxy Statement and enclosed form of Proxy are first sent tostockholders on or about November 06, 2006.

At the meeting, the stockholders of WD-40 Company will vote to elect the Board of Directors for the ensuingyear and to ratify the selection of PricewaterhouseCoopers LLP as the Company’s independent registered publicaccounting firm. Detailed information concerning these matters is set forth below. Management knows of noother business to come before the meeting.

The close of business on October 17, 2006 is the record date for stockholders entitled to notice of and to vote atthe Annual Meeting of Stockholders of WD-40 Company. On October 17, 2006, WD-40 Company hadoutstanding 17,021,909 shares of $.001 par value common stock. Stockholders of record entitled to vote at themeeting will have one vote for each share so held on the matters to be voted upon. A majority of the outstandingshares will constitute a quorum at the meeting. Abstentions and broker non-votes are counted for purposes ofdetermining the presence or absence of a quorum.

If the enclosed form of Proxy is properly executed and returned, the shares represented thereby will be voted inaccordance with the instructions specified thereon. Except as described herein with respect to broker non-votes,if no specification is made, the shares will be voted by the proxy holder as set forth on the Proxy. A Proxy maybe revoked by attendance at the meeting or by filing a Proxy bearing a later date with the Secretary of theCompany.

The cost of soliciting proxies will be borne by the Company. Solicitations other than by mail may be made bytelephone or in person by employees of the Company for which the expense will be nominal.

1

PRINCIPAL SECURITY HOLDERS

The following table sets forth information concerning those persons known to the Company to be the beneficialowners of more than 5% of the common stock of the Company.

Name and Address of Beneficial Owner

Amount and NatureOf BeneficialOwnership

October 17, 2006Percentof Class

Allianz Global Investors Managed Accounts LLC 1,516,1931 8.9%680 Newport Center Dr. Suite 250Newport Beach, CA 92660

Capital Research and Management Company 926,0002 5.4%333 South Hope Street, 55th FloorLos Angeles, CA 90071

Mario L. Crivello 907,4883 5.3%San Diego, California

1 On February 14, 2006, Allianz Global Investors Managed Accounts LLC, an institutional investmentadviser, filed a report on Form 13F with the Securities and Exchange Commission to report beneficialownership, shared voting power and shared dispositive power of 865,100 shares. A breakdown of the sharedvoting power is unavailable. As of June 30, 2006, Allianz filed a report on Form 13F with the Securities andExchange Commission to report beneficial ownership of 1,516,193 shares. A current breakdown of theinvestment company holdings is not provided in the Form 13F report. Beneficial ownership information asof October 17, 2006 is unavailable.

2 On February 6, 2006, Capital Research and Management Company (“CRMC”), an institutional investmentadviser, Capital Income Builder, Inc. (“CIB”), an investment company, and SMALLCAP World Fund, Inc.(SWF), an investment company, filed a joint statement on Form 13G/A with the Securities and ExchangeCommission to report beneficial ownership of the Company’s common stock as of December 31, 2005. Atthat time, CRMC had sole dispositive power and sole voting power over all 1,562,650 shares reported, CIBhad sole voting power and no investment power over 636,650 shares, and SWF had no voting power and noinvestment power over 900,000 shares. CRMC has disclaimed beneficial ownership pursuant to Rule 13d-4under the Securities Exchange Act of 1934. As of June 30, 2006 CRMC filed a report on Form 13F with theSecurities and Exchange Commission to report beneficial ownership of 926,000 shares. A currentbreakdown of the investment company holdings is not provided in the Form 13F report. Beneficialownership information as of October 17, 2006 is unavailable.

3 Mr. Crivello has sole voting and investment power over 779,768 shares held in trust for the benefit ofothers. He also has sole voting and investment power over 14,780 shares held as custodian for others and100,940 shares held directly. Mr. Crivello also has the right to acquire 12,000 shares upon exercise of stockoptions.

2

ITEM NO. 1

NOMINEES FOR ELECTION AS DIRECTORS

AND SECURITY OWNERSHIP OF MANAGEMENT

Unless marked to the contrary, the Proxies received will be voted for the election of the ten nominees namedbelow to serve as Directors until the next Annual Meeting of Stockholders and until their successors are electedor appointed. In the event any nominee is unable or declines to serve as a Director at the time of the AnnualMeeting, any proxy granted to vote for such Director will be voted for a nominee designated by the presentBoard of Directors to fill such vacancy.

The nominees for election to the Board of Directors who receive a plurality the votes cast for the election ofDirectors by the shares present, in person or by proxy, shall be elected as Directors. Holders of common stock arenot entitled to cumulate their votes in the election of Directors. Withheld votes and broker non-votes (which aretreated as “withheld” votes) are not counted as votes in favor of any nominee. Since the nominees receiving themost votes will be elected as Directors, withheld votes and broker non-votes will have no effect upon theoutcome of the election.

Article III, Section 2 of the Bylaws of the Company, approved by stockholders on December 14, 1999, providesthat the authorized number of Directors of the Company shall be not less than nine nor more than twelve untilchanged by amendment of the Certificate of Incorporation or by a bylaw duly adopted by the stockholders. Theexact number of Directors is to be fixed from time to time by a bylaw or amendment thereof duly adopted by thestockholders or by the Board of Directors. The number of directors was fixed at ten by resolution of the Board ofDirectors adopted on November 3, 2005.

Director Independence

The Board of Directors has determined that each director nominee other than Garry O. Ridge is an independentdirector as defined in Rule 4200 of the Marketplace Rules of the Nasdaq Stock Market, Inc. (the “NasdaqRules”.)

3

Security Ownership of Directors and Executive Officers

The following table sets forth certain information, including beneficial ownership of the Company’s commonstock, for the ten nominees, for the executive officers named in the Summary Compensation Table on Page 13,and for all Directors and executive officers as a group.

Amount and Nature ofBeneficial Ownership

October 17, 20061

Director Nominee Age Principal OccupationDirector

Since Number Percent of Class

John C. Adams, Jr. 58 Investor; Retired Chairman and CEO, AutoZone, Inc. 2001 16,7262 *Giles H. Bateman 61 Investor 2003 11,1363 *Peter D. Bewley 60 Investor, Retired General Counsel, The Clorox Company 2005 7,8734 *Richard A. Collato 63 President & CEO, YMCA of San Diego County 2003 12,8643 *Mario L. Crivello 66 Investor 1994 907,4882,5 5.3%Linda A. Lang 48 Chairman & CEO, Jack in the Box, Inc. 2004 10,5346

Gary L. Luick 66 Principal, PointeBreak Solutions, Inc. 2000 13,7592 *Kenneth E. Olson 70 Investor; Former Chairman and CEO, Proxima Corporation 2000 16,9762 *Garry O. Ridge 50 President and CEO, WD-40 Company 1997 181,9607 1.1%Neal E. Schmale 60 Chairman of the Board, WD-40 Company; President and COO,

Sempra Energy2001 16,7262 *

* Less than one (1) percent

1 All shares owned directly unless otherwise indicated.

2 Mr. Adams, Mr. Crivello, Mr. Luick, Mr. Olson and Mr. Schmale each have the right to acquire 12,000shares upon exercise of stock options.

3 Mr. Bateman and Mr. Collato each have the right to acquire 10,000 shares upon the exercise of stockoptions.

4 Mr. Bewley has the right to acquire 6,000 shares upon the exercise of stock options.

5 Mr. Crivello has sole voting and investment power over 779,768 shares held in trust for the benefit ofothers. He also has sole voting and investment power over 14,780 shares held as custodian for others and100,940 shares held directly.

6 Ms. Lang has the right to acquire 8,000 shares upon the exercise of stock options.

7 Mr. Ridge has the right to acquire 172,000 shares upon exercise of stock options. Mr. Ridge has voting andinvestment power over 962 shares held under the Company’s 401(k) plan.

4

Amount and Nature ofBeneficial Ownership

October 17, 20061

Executive Officer Age Principal OccupationDirector

Since

Determined asof record date

NumberPercent of

Class

Michael L. Freeman 52 Division President, the Americas, WD-40 Company N/A 76,5182 *Michael J. Irwin 43 Executive Vice President, Chief Financial Officer and Treasurer, WD-

40 CompanyN/A

89,8743 *Graham P. Milner 51 Executive Vice President, Global Development, Chief Branding

Officer, WD-40 CompanyN/A

94,5884 *William B. Noble 47 Managing Director Europe, WD-40 Company Ltd. (U.K.) N/A 71,3005 *All Directors and

Executive Officersas a Group

1,528,3226 8.7%

* Less than one (1) percent.

1 All shares owned directly unless otherwise indicated.

2 Mr. Freeman has the right to acquire 66,000 shares upon exercise of stock options. Mr. Freeman has votingand investment power over 1762 shares held under the Company’s 401(k) plan.

3 Mr. Irwin has the right to acquire 84,804 shares upon exercise of stock options. Mr. Irwin has voting andinvestment power over 670 shares held under the Company’s 401(k) plan.

4 Mr. Milner has the right to acquire 86,200 shares upon exercise of stock options. Mr. Milner has voting andinvestment power over 1324 shares held under the Company’s 401(k) plan.

5 Mr. Noble has the right to acquire 70,100 shares upon exercise of stock options.

6 Total includes the rights of directors and executive officers to acquire 573,104 shares upon exercise of stockoptions and 4,718 shares held by executive officers under the Company’s 401(k) plan.

Nominees for Election as Directors

John C. Adams, Jr. was elected to the Board of Directors in 2001. Mr. Adams served as President and ChiefExecutive Officer of AutoZone, Inc. from 1996 until 1998, then serving as Chairman and Chief ExecutiveOfficer until his retirement in 2001. He previously served as President of the Miami division of Malone & Hyde,Inc., AutoZone’s former parent company from 1984 until 1990. Mr. Adams was an owner of NicotianaEnterprises, Inc., a food distribution company, from 1990 until 1995.

Giles H. Bateman was elected to the Board of Directors in 2003. Mr. Bateman was a co-founder and ChiefFinancial Officer of Price Club from 1976 until 1991. Mr. Bateman served as director and chairman ofCompUSA, Inc. from 1994 until 2000. Mr. Bateman is a director of Tuesday Morning, Inc, Lifetime Fitness Inc.,and United PanAm Finance Corp.

Peter D. Bewley was appointed to the Board of Directors on June 28, 2005. Mr. Bewley was the Senior VicePresident–General Counsel & Secretary of The Clorox Company from 1998 to 2005.

Richard A. Collato was elected to the Board of Directors in 2003. Mr. Collato is President & CEO of the YMCAof San Diego County. Mr. Collato is a director of Sempra Energy and Surge Global Energy.

Mario L. Crivello was elected to the Board of Directors in 1994. Mr. Crivello is retired, having been themanaging owner and master of Tuna Purse Seiners.

5

Linda A. Lang was elected to the Board of Directors in 2004. Ms. Lang has served as director, President andChief Operating Officer of Jack in the Box, Inc. since 2003. Ms. Lang was elected Chairman of the Board &Chief Executive Officer of Jack in the Box, Inc. as of October 2, 2005. Over the past 16 years, Ms. Lang has heldthe offices of Executive Vice President, Senior Vice President Marketing, Vice President and Regional VicePresident, Southern California Region, Vice President Marketing and Vice President of Products, Promotions andConsumer Research at Jack in the Box, Inc.

Gary L. Luick was elected to the Board of Directors in 2000. Mr. Luick is a Principal with PointeBreakSolutions, Inc., a provider of business transaction advisory services. Mr. Luick was the President and CEO ofClickgarden, Inc., an internet software company, from 2000 to 2001. He retired in 1988 from Allied Signal asDirector — Corporate Development. From 1989 through 1996 he served as President and CEO of GTI Corp., anetworking products company, and he was President and CEO of Coded Communications, a wireless networkingcompany, from 1997 to 1998.

Kenneth E. Olson was elected to the Board of Directors in 2000. Mr. Olson served as Chairman and CEO ofProxima Corporation, a digital imaging products company, from 1990 to 1998. He is a director of DigiradCorporation.

Garry O. Ridge joined WD-40 Company in 1987 as Managing Director, WD-40 Company (Australia) Pty. Limitedand he was responsible for Company operations throughout the Pacific and Asia. Mr. Ridge transferred to thecorporate office in 1994 as Director International Operations and was elected Vice President — International in1995. He was elected to the position of Executive Vice President/Chief Operating Officer in 1996 and he wasnamed President and Chief Executive Officer in 1997. He was also elected to the Board of Directors in 1997. Priorto joining WD-40 Company Mr. Ridge was Managing Director of Mermax Pacific Pty. Ltd. and held a number ofsenior management positions with Hawker Pacific Pty. Ltd. (a Hawker Siddeley PLC Group Company) which was alicensee for WD-40 until 1988.

Neal E. Schmale was elected to the Board of Directors in 2001. Mr. Schmale was named Chairman of the Boardin 2004. Mr. Schmale has served as President and COO of Sempra Energy since January 2006. Previously, hewas Executive Vice President and CFO of Sempra Energy from 1998 through 2005. Mr. Schmale is a director ofSempra Energy and Murphy Oil Corporation.

Board of Directors Meetings, Compensation and Committees

The Board of Directors is charged by the shareholders with managing the business affairs and exercising thecorporate power of the Company. The Board of Directors relies on the following standing committees to assist incarrying out the Board of Directors’ responsibilities: the Audit Committee, the Compensation Committee, theCorporate Governance Committee and the Finance Committee. Each of the committees has a written charterapproved by the Board of Directors and such charters are available on WD-40 Company’s Investor Relationsweb site at www.wd40.com under the “Officers & Directors” section. There were four scheduled meetings of theBoard of Directors during the last fiscal year. All directors serving for the full fiscal year attended at least 75percent of the aggregate of the total number of meetings of the Board and of all committees on which the directorserved.

Board of Directors Compensation

Effective as of the annual meeting of stockholders, each non-employee director will be entitled to receive anannual fee of $32,000 for services provided from the date of the Company’s annual meeting to the next annualmeeting. For the current year, the annual fee was $30,000. The annual fee is payable in March. The Chairman ofthe Board receives an additional annual fee of $14,000. Non-employee directors receive additional cashcompensation for service on committees. The Chairman of the Audit Committee receives $16,000 and each othermember of the Audit Committee receives $8,000. Each Chairman of the Compensation Committee, the Corporate

6

Governance Committee and the Finance Committee receives $8,000 and each other member of those committeesreceives $4,000. For service during the next year, non-employee directors will also receive non-qualified stockoptions to purchase 3,800 shares of the Company’s common stock. For the current year, the non-employeedirectors received stock options to purchase 3,500 shares. The options are granted on the date of the Company’sannual meeting pursuant to the Company’s 1990 Incentive Stock Option Plan. The stock options are immediatelyexercisable with a termination date ten years from the grant date. The exercise price for options granted to thedirectors is equal to the closing price of the Company’s shares as of the day of the annual meeting.

The Company maintains a Non-Employee Director Restricted Stock Plan providing for the issuance of shares ofrestricted common stock of the Company to each non-employee member of the Board of Directors. Shares areissued in lieu of cash compensation according to an election to be made by the director prior to November 30thof the year prior to the year of service. A director who holds shares of the Company having a value of at least$50,000 may elect to receive the entire annual director’s fee in cash. Otherwise, directors receive restricted stockin lieu of $5,500 of cash compensation and they may elect to receive restricted stock in lieu of the balance oftheir annual fee in increments of $5,500. The restricted shares are to be issued in accordance with a director’selection as soon as practicable after the first day of March. The number of shares to be issued is equal to theamount of compensation to be paid in shares divided by 90% of the closing price of the Company’s shares as ofthe first business day of March.

Restricted shares issued to a director do not become vested for resale for a period of five years or until thedirector’s retirement from the Board following the director’s 65th birthday. Unless a director has reached age 65,the shares are subject to forfeiture if, during the five year vesting period, the director resigns from service as adirector.

The Company maintains a Director Contributions Fund from which each incumbent director has the right, at aspecified time each fiscal year, to designate $6,000 in charitable contributions to be made by the Company toproperly qualified (under Internal Revenue Code Section 501(c)(3)) charitable organizations.

Stockholder Communications with Board of Directors

Stockholders may send communications to the Board of Directors by submitting a letter addressed to: WD-40Company, Corporate Secretary, 1061 Cudahy Place, San Diego, CA 92110.

The Board of Directors has instructed the Corporate Secretary to forward such communications to the chairmanof the Board of Directors. The Board of Directors has also instructed the Corporate Secretary to review suchcorrespondence and, at the Corporate Secretary’s discretion, to not forward correspondence which is deemed of acommercial or frivolous nature or inappropriate for Board of Director consideration. The Corporate Secretarymay also forward the stockholder communication within the Company to another department to facilitate anappropriate response.

7

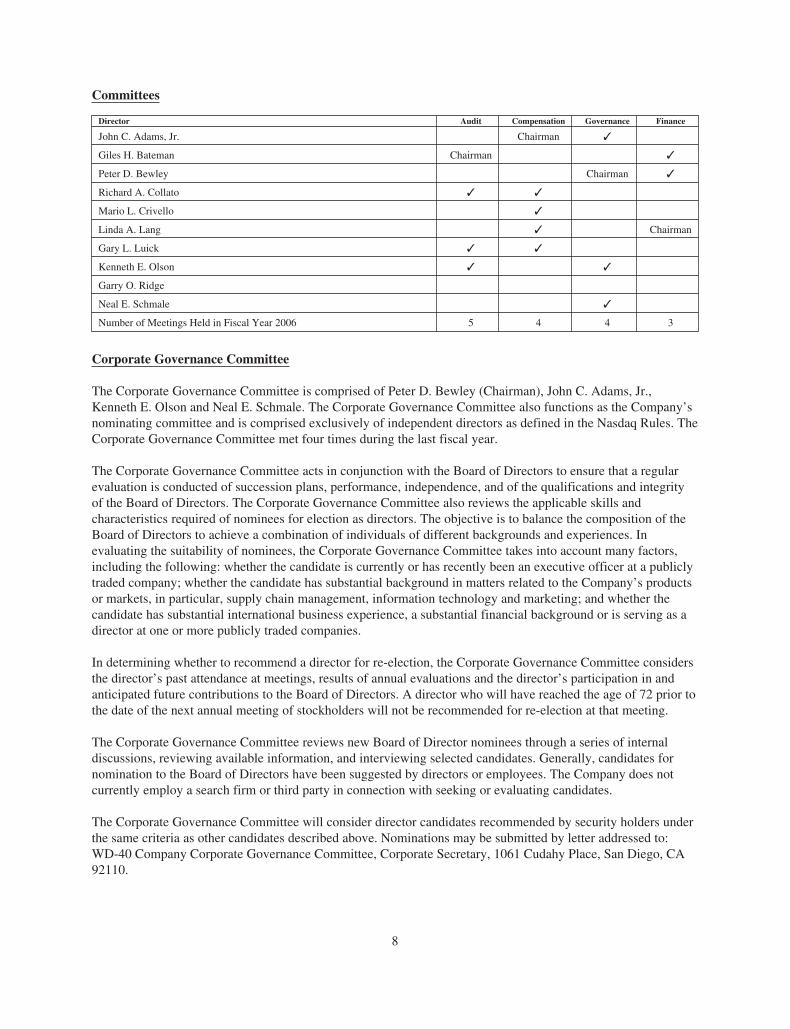

Committees

Director Audit Compensation Governance Finance

John C. Adams, Jr. Chairman ✓

Giles H. Bateman Chairman ✓

Peter D. Bewley Chairman ✓

Richard A. Collato ✓ ✓

Mario L. Crivello ✓

Linda A. Lang ✓ Chairman

Gary L. Luick ✓ ✓

Kenneth E. Olson ✓ ✓

Garry O. Ridge

Neal E. Schmale ✓

Number of Meetings Held in Fiscal Year 2006 5 4 4 3

Corporate Governance Committee

The Corporate Governance Committee is comprised of Peter D. Bewley (Chairman), John C. Adams, Jr.,Kenneth E. Olson and Neal E. Schmale. The Corporate Governance Committee also functions as the Company’snominating committee and is comprised exclusively of independent directors as defined in the Nasdaq Rules. TheCorporate Governance Committee met four times during the last fiscal year.

The Corporate Governance Committee acts in conjunction with the Board of Directors to ensure that a regularevaluation is conducted of succession plans, performance, independence, and of the qualifications and integrityof the Board of Directors. The Corporate Governance Committee also reviews the applicable skills andcharacteristics required of nominees for election as directors. The objective is to balance the composition of theBoard of Directors to achieve a combination of individuals of different backgrounds and experiences. Inevaluating the suitability of nominees, the Corporate Governance Committee takes into account many factors,including the following: whether the candidate is currently or has recently been an executive officer at a publiclytraded company; whether the candidate has substantial background in matters related to the Company’s productsor markets, in particular, supply chain management, information technology and marketing; and whether thecandidate has substantial international business experience, a substantial financial background or is serving as adirector at one or more publicly traded companies.

In determining whether to recommend a director for re-election, the Corporate Governance Committee considersthe director’s past attendance at meetings, results of annual evaluations and the director’s participation in andanticipated future contributions to the Board of Directors. A director who will have reached the age of 72 prior tothe date of the next annual meeting of stockholders will not be recommended for re-election at that meeting.

The Corporate Governance Committee reviews new Board of Director nominees through a series of internaldiscussions, reviewing available information, and interviewing selected candidates. Generally, candidates fornomination to the Board of Directors have been suggested by directors or employees. The Company does notcurrently employ a search firm or third party in connection with seeking or evaluating candidates.

The Corporate Governance Committee will consider director candidates recommended by security holders underthe same criteria as other candidates described above. Nominations may be submitted by letter addressed to:WD-40 Company Corporate Governance Committee, Corporate Secretary, 1061 Cudahy Place, San Diego, CA92110.

8

Compensation Committee

Compensation Committee Interlocks and Insider Participation

The Compensation Committee is comprised of John C. Adams, Jr. (Chairman), Mario L. Crivello, Richard A.Collato, Linda A. Lang and Gary L. Luick all of whom are independent directors as defined under the NasdaqRules. The Compensation Committee met four times during the last fiscal year.

The function of the Compensation Committee is to provide guidance to the Board of Directors and oversight forall executive compensation and benefit programs. The Committee provides recommendations for base salary andincentive compensation awards for the CEO and executive officers. The Compensation Committee also serves asthe Stock Option Committee with authority to grant options and administer the Company’s Incentive StockOption Plan. The Compensation Committee Report on Executive Compensation appears on page 17 below.

Audit Committee

The Audit Committee is comprised of Giles H. Bateman (Chairman), Gary L. Luick, Kenneth E. Olson, andRichard A. Collato. Five meetings were held during the last fiscal year to review quarterly financial reports, toconsider the annual audit and other audit services and to review the audit with the independent auditors after itscompletion. The Board of Directors has determined that Mr. Bateman is an “audit committee financial expert” asdefined by regulations adopted by the Securities and Exchange Commission. Mr. Bateman and each of the othermembers of the Audit Committee is an independent director as defined in the Nasdaq Rules. The AuditCommittee also has responsibility for the selection, appointment and oversight of independent accountants forthe Company. A separate report of the Audit Committee is set forth below.

9

AUDIT COMMITTEE REPORT

Each year the Board of Directors appoints an Audit Committee to fulfill regulatory requirements and to assist theBoard in oversight of the Company’s financial reporting, internal control functions and audit process. Eachmember of the Audit Committee meets the independence requirements set by the Nasdaq Stock Market.

The responsibilities of the Audit Committee include the selection and appointment of a independent registeredpublic accounting firm to be hired as the Company’s independent accountants. The Audit Committee is alsoresponsible for recommending to the Board that the Company’s consolidated financial statements be included inits annual report on Form 10-K.

With respect to the preparation and audit of the Company’s consolidated financial statements, management isresponsible for the preparation of the financial statements; the establishment of accounting and financialreporting principles; the establishment of disclosure controls and procedures; the establishment of internalcontrol over financial reporting; the evaluation of the effectiveness of both disclosure controls and proceduresand internal control over financial reporting; and the evaluation of changes in internal control over financialreporting that have materially affected, or are reasonably likely to materially affect, internal control overfinancial reporting. The Company’s independent registered public accountants are responsible for performing anindependent audit of the consolidated financial statements; expressing an opinion as to whether the consolidatedfinancial statements have been prepared in accordance with accounting principles generally accepted in theUnited States of America; and expressing an opinion on both management’s assessment of the effectiveness ofinternal control over financial reporting and specifically as to the effectiveness of the Company’s internal controlover financial reporting.

The Audit Committee has reviewed the consolidated financial statements of the Company for the fiscal yearended August 31, 2006. The Audit Committee has discussed the preparation of the consolidated financialstatements with management and with the Company’s independent registered public accounting firm,PricewaterhouseCoopers LLP, and the Audit Committee has met separately with PricewaterhouseCoopers LLPand with management to discuss issues relating to the preparation and audit of the financial statements.

For the fiscal year ended August 31, 2006, management has completed the documentation, testing and evaluationof the Company’s system of internal control over financial reporting as required by Section 404 of the Sarbanes-Oxley Act of 2002. The Audit Committee has been kept apprised of management’s activities in the completion ofsuch work and evaluation and the Audit Committee has provided oversight and advice with respect to the processundertaken by management. The Audit Committee will continue to oversee such work being undertaken by theCompany for the fiscal year ending August 31, 2007.

The Audit Committee has taken the following steps in making its recommendation that the Company’s financialstatements be included in its annual report on Form 10-K for the fiscal year ended August 31, 2006:

1. At regularly scheduled meetings of the Audit Committee, management and PricewaterhouseCoopersLLP provided periodic reports as to the work undertaken by the Company to complete thedocumentation, testing and evaluation of the Company’s system of internal control over financialreporting. Upon completion of such work and upon preparation of the Company’s consolidatedfinancial statements for the year ended August 31, 2006, the Audit Committee reviewed a reportprovided by management on the effectiveness of the Company’s internal control over financialreporting.

2. The Audit Committee discussed with PricewaterhouseCoopers LLP, the Company’s independentregistered public accounting firm for fiscal year ended August 31, 2006, those matters required to bediscussed by Statement on Auditing Standards No. 61 and PCAOB Auditing Standard No. 2, includinginformation concerning the scope and results of the audit. These communications and discussions areintended to assist the Audit Committee in overseeing the financial reporting and disclosure process.

10

3. The Audit Committee discussed with PricewaterhouseCoopers LLP its independence and receivedfrom PricewaterhouseCoopers LLP a letter concerning independence as required under applicableindependence standards for auditors of public companies. This discussion and disclosure helped theAudit Committee in evaluating such independence.

4. The Audit Committee reviewed and discussed with the Company’s management andPricewaterhouseCoopers LLP, the Company’s audited consolidated balance sheet at August 31, 2006,and consolidated statements of income, cash flows and stockholders’ equity for the fiscal year endedAugust 31, 2006.

5. The Audit Committee has reviewed PricewaterhouseCoopers LLP’s Report of Independent RegisteredPublic Accounting Firm and Management’s Report on Internal Control over Financial Reportingincluded in the Company’s annual report on Form 10-K.

Based on the reviews and discussions explained above, the Audit Committee recommended to the Board that theCompany’s financial statements be included in its annual report on Form 10-K for its fiscal year endedAugust 31, 2006. PricewaterhouseCoopers LLP has been selected to serve as the Company’s independentauditors for the fiscal year ending August 31, 2007.

Giles H. Bateman (Chairman)Richard A. Collato

Gary L. LuickKenneth E. Olson

Finance Committee

The Finance Committee is comprised of Linda A. Lang (Chairman), Giles H. Bateman and Peter D. Bewley.Three meetings of the Finance Committee were held during the last fiscal year. The Finance Committee isappointed by the Board for the primary purpose of assisting the Board in overseeing financial matters ofimportance to the company, including matters relating to acquisitions, investment policy, capital structure, anddividend policy. The Finance Committee also reviews the Company’s annual and long-term financial strategiesand objectives.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934 requires the Company’s directors and executive officers,and persons who own more than ten percent of the Company’s stock, to file with the Securities ExchangeCommission initial reports of stock ownership and reports of changes in stock ownership. Reporting persons arerequired by SEC regulation to furnish the Company with copies of all Section 16(a) reports they file.

To the Company’s knowledge, based solely on review of the copies of such reports furnished to the Companyduring the last fiscal year and written representations that no other reports were required, all Section 16(a)requirements were complied with by all persons required to report with respect to the Company’s stock duringthe last fiscal year.

11

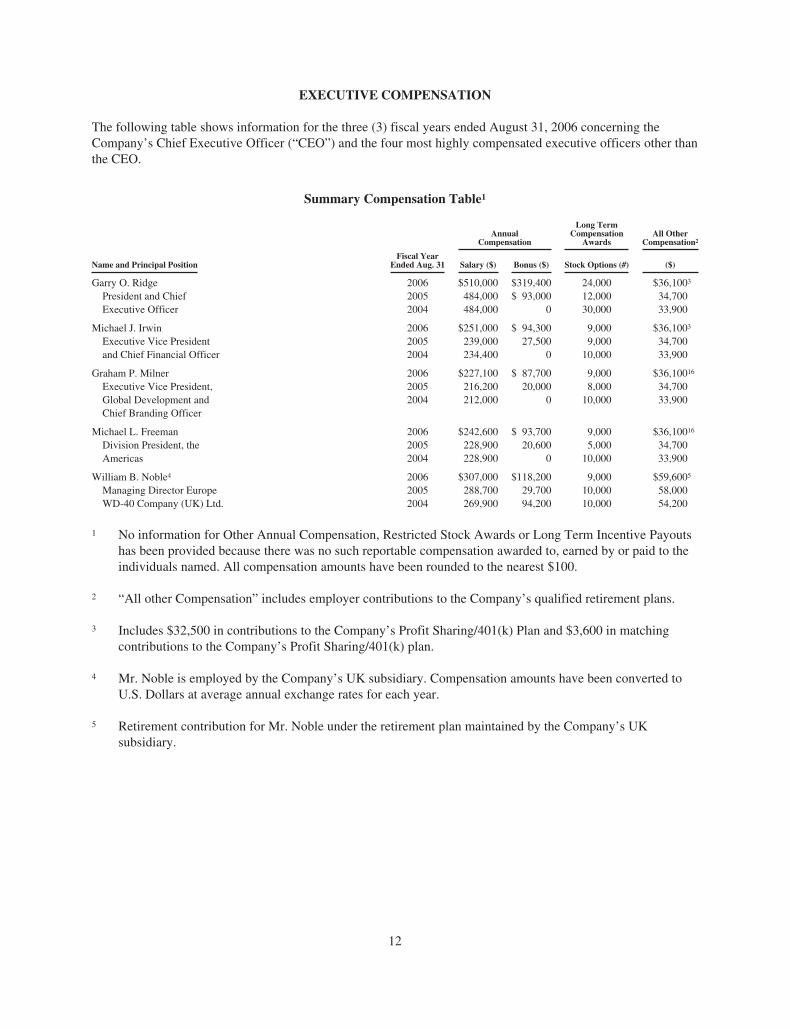

EXECUTIVE COMPENSATION

The following table shows information for the three (3) fiscal years ended August 31, 2006 concerning theCompany’s Chief Executive Officer (“CEO”) and the four most highly compensated executive officers other thanthe CEO.

Summary Compensation Table1

AnnualCompensation

Long TermCompensation

AwardsAll Other

Compensation2

Name and Principal PositionFiscal Year

Ended Aug. 31 Salary ($) Bonus ($) Stock Options (#) ($)

Garry O. Ridge 2006 $510,000 $319,400 24,000 $36,1003

President and ChiefExecutive Officer

2005 484,000 $ 93,000 12,000 34,7002004 484,000 0 30,000 33,900

Michael J. Irwin 2006 $251,000 $ 94,300 9,000 $36,1003

Executive Vice Presidentand Chief Financial Officer

2005 239,000 27,500 9,000 34,7002004 234,400 0 10,000 33,900

Graham P. Milner 2006 $227,100 $ 87,700 9,000 $36,10016

Executive Vice President,Global Development andChief Branding Officer

2005 216,200 20,000 8,000 34,7002004 212,000 0 10,000 33,900

Michael L. Freeman 2006 $242,600 $ 93,700 9,000 $36,10016

Division President, theAmericas

2005 228,900 20,600 5,000 34,7002004 228,900 0 10,000 33,900

William B. Noble4 2006 $307,000 $118,200 9,000 $59,6005

Managing Director EuropeWD-40 Company (UK) Ltd.

2005 288,700 29,700 10,000 58,0002004 269,900 94,200 10,000 54,200

1 No information for Other Annual Compensation, Restricted Stock Awards or Long Term Incentive Payoutshas been provided because there was no such reportable compensation awarded to, earned by or paid to theindividuals named. All compensation amounts have been rounded to the nearest $100.

2 “All other Compensation” includes employer contributions to the Company’s qualified retirement plans.

3 Includes $32,500 in contributions to the Company’s Profit Sharing/401(k) Plan and $3,600 in matchingcontributions to the Company’s Profit Sharing/401(k) plan.

4 Mr. Noble is employed by the Company’s UK subsidiary. Compensation amounts have been converted toU.S. Dollars at average annual exchange rates for each year.

5 Retirement contribution for Mr. Noble under the retirement plan maintained by the Company’s UKsubsidiary.

12

Stock Options

The following table sets forth stock options granted pursuant to the Restated WD-40 Company 1990 IncentiveStock Option Plan during the last fiscal year to each of the Company’s executive officers named in the SummaryCompensation Table above.

Option Grants in Last Fiscal Year

NameOptions

Granted (#)

Percent of TotalOptions Granted to

Employees inFiscal Year 20061

Exercise Price($/sh)

ExpirationDate

GrantDate

Value2

Garry O. Ridge3 24,000 11.14% $27.27 10/18/2015 $132,960Michael J. Irwin4 9,000 4.18% $27.27 10/18/2015 $ 49,860Graham P. Milner5 9,000 4.18% $27.27 10/18/2015 $ 49,860Michael L. Freeman6 9,000 4.18% $27.27 10/18/2015 $ 49,860William B. Noble7 9,000 4.18% $27.27 10/18/2015 $ 49,860

The options may be exercised for cash or in lieu of cash, an option holder may tender shares of the Company’scommon stock previously held by the option holder. In permitting the exchange of stock upon exercise ofoptions, the 1990 Incentive Stock Option Plan restricts the exercise of options with previously owned stock toshares held for a minimum of six months.

1 The total number of options granted to employees in fiscal year 2006 was 215,500.

2 The Grant Date Value of $5.54 per share has been determined as of October 18, 2005 using the Black-Scholes Option Valuation model. The following assumptions were used in determining the value: (i) adividend yield of 3.23%; (ii) expected volatility of 0.2511; (iii) a 4.77-year risk-free interest rate of 4.32%;and (iv) an expected option term/life of 4.77 years.

3 Mr. Ridge’s options are non-qualified stock options with 8,160 shares exercisable on October 18, 2006;7,920 shares exercisable on October 18, 2007; and 7,920 shares exercisable on October 18, 2008.

4 Mr. Irwin’s options are non-qualified stock options with 3,060 shares exercisable October 18, 2006; 2,970shares exercisable October 18, 2007; and 2,970 shares exercisable October 18, 2008.

5 Mr. Milner’s options are non-qualified stock options with 3,060 shares exercisable October 18, 2006; 2,970shares exercisable October 18, 2007; and 2,970 shares exercisable October 18, 2008.

6 Mr. Freeman’s options are non-qualified stock options with 3,060 shares exercisable October 18, 2006;2,970 shares exercisable October 18,2007; and 2,970 shares exercisable October 18, 2008.

7 Mr. Noble’s options are non-qualified stock options with 3,060 shares exercisable October 18, 2006; 2,970shares exercisable October 18, 2007; and 2,970 shares exercisable October 18, 2008.

13

The following table sets forth the number of shares acquired on exercise of stock options in the Company’s lastfiscal year, the aggregate dollar value realized on exercise of such options and the number and dollar value ofunexercised options as of August 31, 2006 for the Company’s executive officers named in the SummaryCompensation Table above.

Aggregated Option Exercises in Last Fiscal Year andFiscal Year End Option Values

Name

SharesAcquired on

Exercise

ValueRealized

($)

Number of UnexercisedOptions at August 31, 2006

(#)

Value of UnexercisedIn-The-Money Options at

August 31, 20061

Exercisable Unexercisable Exercisable Unexercisable

Garry O. Ridge 20,000 $239,000 152,200 19,800 $998,300 $146,520Michael J. Irwin 2,400 $ 17,330 75,894 8,910 $801,547 $ 65,459Graham P. Milner 5,000 $ 35,899 77,620 8,580 $767,576 $ 63,122Michael L. Freeman 25,000 $219,543 67,100 14,900 $513,629 $ 56,133William B. Noble 5,000 $ 54,235 60,760 9,340 $536,280 $ 69,195

Supplemental Death and Retirement Benefit Plans

The Company maintains Supplemental Death Benefit Plans for certain key employees. Under the Death BenefitPlan agreements, a participating employee’s designated beneficiary or the employee’s estate will receive a deathbenefit equal to the employee’s then current base salary in the event of death prior to retirement from theCompany. No death benefit is payable if retirement benefits become due upon the employee’s retirement underthe Retirement Benefit Plan agreement.

The Company also maintains Supplemental Retirement Benefit Plans for certain key employees. Under theRetirement Benefit Plan agreements, participating employees will receive retirement benefits in the event of theparticipant’s retirement on or after a designated retirement date. The annual retirement benefit for participatingemployees will be equal to twenty-five percent (25%) of the employee’s then current base salary, payable inquarterly installments over a period of fifteen years.

All benefits under the plans will be subject to payroll taxes and required withholding for state and federal incometaxes as deferred compensation. The benefits are funded by key man life insurance policies purchased and ownedby the Company. The Board of Directors determines which key employees will participate in the plans and theamount of benefits payable for each participant. Non-employee directors do not participate in the plans.

Based upon current (2007) base salaries, the death benefits and annual retirement benefits to be provided underthe plans to the executive officers named in the Summary Compensation Table above are set forth below. Theretirement benefit will not be payable unless the executive officer retires with the Company on or after reachingthe specified retirement age. In such event, the actual amount of the annual benefit will be dependent upon theexecutive’s then current annual salary.

NameDeath

Benefit

AnnualRetirement

BenefitRetirement

Age

Garry O. Ridge $535,500 $133,875 65Michael J. Irwin $266,500 $ 66,625 65Graham P. Milner $238,700 $ 59,675 65Michael L. Freeman $266,500 $ 66,625 65William B. Noble — $ 80,299 65

Change of Control Severance Agreements

On February 14, 2006, the Company terminated pre-existing employment agreements with the executive officersnamed in the Summary Compensation Table above. Each executive officer serves in office at the pleasure of the

14

Board of Directors. On February 14, 2006, the Company entered into Change of Control Severance Agreements(“Severance Agreements”) with each of the named executive officers and with one additional executive officer.The new Severance Agreements provide that each executive officer will receive certain severance benefits if heis terminated without “Cause” or resigns for “Good Reason”, as those terms are defined in the SeveranceAgreements, within two years after a “Change of Control” as defined in the Severance Agreements andsummarized below. If the executive officer’s employment is terminated during the aforementioned two-yearperiod by the Company without Cause or by the executive officer for Good Reason, the executive officer will beentitled to a lump sum payment (subject to limits provided by reference to Section 280G of the Internal RevenueCode which limits the deductibility of certain payments to executives upon a change in control) of twice theexecutive officer’s salary, calculated based on the greater of the executive officer’s then current annual salary ora 5-year average, plus twice the executive officer’s bonus compensation, calculated based on the greater of themost recent annual bonus compensation or a 5-year average. Further, any of the executive officer’s stock optionsand other equity incentive benefits that are not then fully vested will be accelerated and vested in full followingsuch termination of employment within such two-year period and the executive officer will be entitled tocontinuation of health and welfare benefits under the Company’s then existing benefit plans or equivalentbenefits. No employment rights or benefits other than the change of control severance benefits are provided bythe Severance Agreements.

For purposes of the Severance Agreements and subject to the express provisions and limitations containedtherein, Change of Control means a transaction or series of transactions by which a person or persons actingtogether acquire more than 30% of the Company’s outstanding shares; a change in a majority of the incumbentmembers of the Company’s board of directors as specified in the Severance Agreements, a reorganization,merger or consolidation as specified in the Severance Agreements or a sale of substantially all of the assets orcomplete liquidation of the Company. As specified more particularly in the Severance Agreements, Change ofControl does not include a reorganization, merger or consolidation or a sale or liquidation where a majority ofincumbent members of the board of directors continue in office and more than 60% of the Company’spre-transaction shareholders continue to maintain control of the resulting or successor company.

The Severance Agreements have a term of two years, subject to automatic renewal for successive two yearperiods unless notice of non-renewal is provided by the Company’s board of directors not less than six monthsprior to the end of the current term. The term of the Severance Agreements will be automatically extended for aterm of two years following any Change of Control.

15

COMPENSATION COMMITTEE REPORT ON EXECUTIVE COMPENSATION

Role and Membership of the Compensation Committee

The Compensation Committee of the Board (the “Committee”) is responsible for setting and administering thepolicies that govern executive compensation and the stock ownership programs for employees of the Company.The Committee also serves as the Stock Option Committee under the Company’s 1990 Incentive Stock OptionPlan. The Committee operates pursuant to a charter that further outlines the specific authority, duties andresponsibilities of the Committee. The charter is periodically reviewed and revised by the Committee and theBoard and is available on the Company’s website at www.wd40.com under the “Officers & Directors” section.

During the fiscal year ended August 31, 2006, the Compensation Committee was comprised of John C. Adams,Jr. (Chairman), Mario L. Crivello, Richard A. Collato, Linda A. Lang and Gary L. Luick. None of the Committeemembers is currently or has been at any time an officer or an employee of WD-40 Company. The Committeemeets at scheduled times during the year and holds additional meetings from time to time to review and discussexecutive compensation issues. The Committee may also consider and take action by written consent. TheCommittee met four times during fiscal year 2006.

The Company’s Human Resources Department supports the Compensation Committee in its work and in somecases acts pursuant to delegated authority to fulfill various functions in administering the Company’scompensation programs. The Committee has the authority to engage the services of outside advisers, experts andothers to assist the Committee with its responsibilities. In accordance with this authority, the Committee directlyengages Compensia, Inc. as independent outside compensation consultant to advise the Committee oncompensation practices and policies relating to the executive officers. The independent consulting firm does notadvise management of the Company, and receives no other compensation from the Company.

Executive Compensation Philosophy

WD-40 Company’s executive compensation program is designed to achieve four primary objectives:

• Attract and retain executive officers capable of leading WD-40 Company to the fulfillment of itsbusiness objectives.

• Offer competitive compensation opportunities that reward individual contributions and the achievementof key corporate milestones.

• Align the interests of executive officers and stockholders through long-term equity compensation.

• Ensure that total compensation is commensurate with the performance and value created forstockholders.

The main components used to support these objectives are base salary, performance incentive, pension/profitsharing and equity compensation (each of which is discussed in detail below). For each of these elements of pay,the Company’s strategy is to examine peer group compensation practices and deliver pay in the 25th to 75thpercentile of the peer group with an overarching goal of ensuring an appropriate pay-for-performance alignment.

Peer Group

The peer group the Committee examines to assess the competitiveness of the Company’s executive compensationincludes consumer products companies that are in a comparable range with respect to several metrics, principallybusiness strategy, market capitalization, and revenues. The peer group may include some or all of the companiesthat are included in the market indices in the graph included under “Stock Performance Graph” in this ProxyStatement, labor market competitors and other companies regarded as having executive compensation bestpractices.

16

The peer group is reviewed annually by the Committee and adjustments are made as necessary to ensure thegroup continues to properly reflect the market in which the Company competes for talent. The Committee alsoreviews annually the executive pay practices and levels of other similarly sized companies as reported in industrysurveys and reports from compensation consulting firms. This information is considered when makingrecommendations for each element of compensation.

Components of Executive Compensation Program

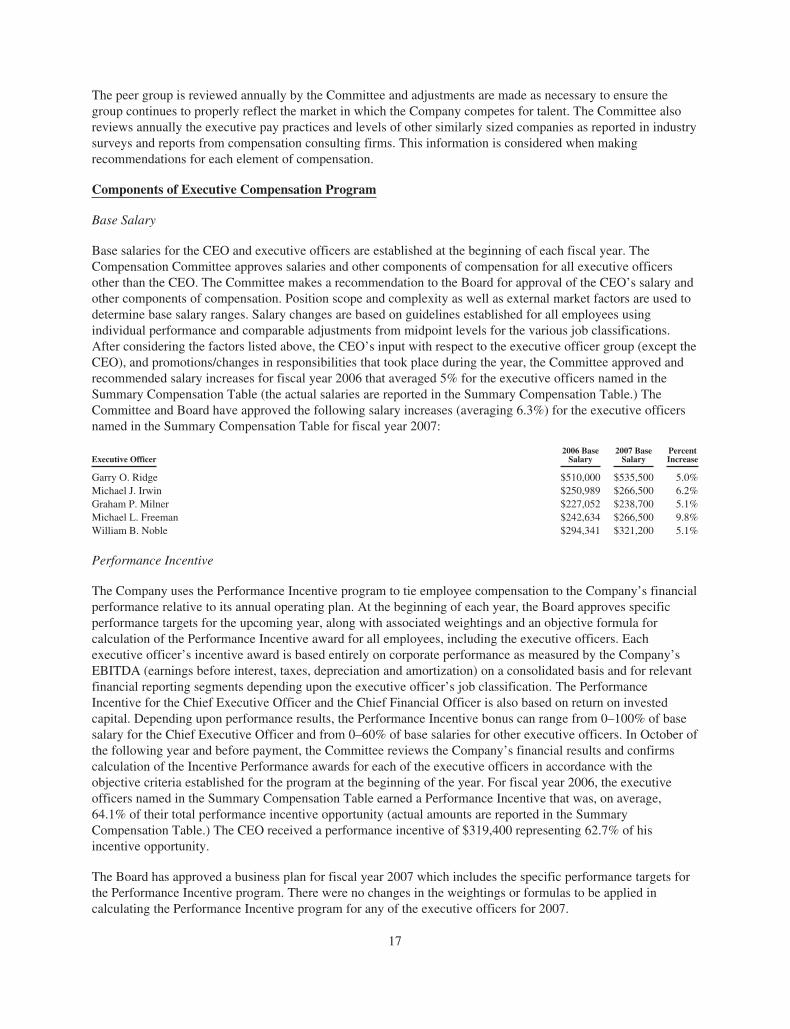

Base Salary

Base salaries for the CEO and executive officers are established at the beginning of each fiscal year. TheCompensation Committee approves salaries and other components of compensation for all executive officersother than the CEO. The Committee makes a recommendation to the Board for approval of the CEO’s salary andother components of compensation. Position scope and complexity as well as external market factors are used todetermine base salary ranges. Salary changes are based on guidelines established for all employees usingindividual performance and comparable adjustments from midpoint levels for the various job classifications.After considering the factors listed above, the CEO’s input with respect to the executive officer group (except theCEO), and promotions/changes in responsibilities that took place during the year, the Committee approved andrecommended salary increases for fiscal year 2006 that averaged 5% for the executive officers named in theSummary Compensation Table (the actual salaries are reported in the Summary Compensation Table.) TheCommittee and Board have approved the following salary increases (averaging 6.3%) for the executive officersnamed in the Summary Compensation Table for fiscal year 2007:

Executive Officer2006 Base

Salary2007 Base

SalaryPercentIncrease

Garry O. Ridge $510,000 $535,500 5.0%Michael J. Irwin $250,989 $266,500 6.2%Graham P. Milner $227,052 $238,700 5.1%Michael L. Freeman $242,634 $266,500 9.8%William B. Noble $294,341 $321,200 5.1%

Performance Incentive

The Company uses the Performance Incentive program to tie employee compensation to the Company’s financialperformance relative to its annual operating plan. At the beginning of each year, the Board approves specificperformance targets for the upcoming year, along with associated weightings and an objective formula forcalculation of the Performance Incentive award for all employees, including the executive officers. Eachexecutive officer’s incentive award is based entirely on corporate performance as measured by the Company’sEBITDA (earnings before interest, taxes, depreciation and amortization) on a consolidated basis and for relevantfinancial reporting segments depending upon the executive officer’s job classification. The PerformanceIncentive for the Chief Executive Officer and the Chief Financial Officer is also based on return on investedcapital. Depending upon performance results, the Performance Incentive bonus can range from 0–100% of basesalary for the Chief Executive Officer and from 0–60% of base salaries for other executive officers. In October ofthe following year and before payment, the Committee reviews the Company’s financial results and confirmscalculation of the Incentive Performance awards for each of the executive officers in accordance with theobjective criteria established for the program at the beginning of the year. For fiscal year 2006, the executiveofficers named in the Summary Compensation Table earned a Performance Incentive that was, on average,64.1% of their total performance incentive opportunity (actual amounts are reported in the SummaryCompensation Table.) The CEO received a performance incentive of $319,400 representing 62.7% of hisincentive opportunity.

The Board has approved a business plan for fiscal year 2007 which includes the specific performance targets forthe Performance Incentive program. There were no changes in the weightings or formulas to be applied incalculating the Performance Incentive program for any of the executive officers for 2007.

17

Pension and Profit Sharing Plans

Since 1963 the Company has maintained tax qualified Pension and Profit Sharing Plans for the benefit of all fulltime employees, including executive officers. The Company’s present WD-40 Company Profit Sharing/401(k)Plan provides for mandatory employer contributions for participating employees equal to 10% of their coveredcompensation and permits discretionary employer contributions up to 5% of their covered compensation. ThePlan also allows employees, with 401(k) tax treatment, to defer up to the allowable IRS limits for each calendaryear and provides a matching contribution equal to one-half of such amounts deferred, up to a maximum of 3.3%of their covered compensation. In calendar year 2006, covered compensation includes all salary and bonuscompensation up to $220,000 and the maximum amount permitted to be contributed to the Plan for an employee,including 401(k) deferrals and employer matching contributions, is $44,000. The Plan serves to provideCompany employees with tax-advantaged retirement savings as an additional component of overallcompensation. The Company’s contributions to the Plan may be invested by employees in a Company StockFund invested in shares of the Company’s common stock.

Equity Compensation

Equity compensation is a critical component to the Company’s efforts to attract and retain executives and keyemployees, encourage employee ownership in the Company, link pay with performance and align the interests ofexecutive officers with those of stockholders. The Company provides executive officers with a substantialeconomic interest in the long-term appreciation of the Company’s common stock through the grant of stockoptions at the beginning of each fiscal year, subject to vesting restrictions. Stock options provide value only if theCompany’s stock price increases (which benefits all stockholders), and only if the executive or employee remainswith the Company until his or her options vest. The Company’s standard practice is to grant options that vestover a three-year period.

The Company is sensitive to the concerns of its stockholders regarding the dilutive impact of stock options.Accordingly, the Company has designed its option grant practices to reflect an appropriate balance betweenstockholders’ dilution concerns and the Company’s need to remain competitive by recruiting and retaining high-performing employees.

• All of the Company’s equity plans have been approved by stockholders.

• The Company’s aggregate stock granting practices are conservative. For fiscal year 2006, the Boardgranted options to purchase a total of 215,500 shares to 64 Company employees, including the CEO andexecutive officers who, as a group, received 69,000 of the total options granted. The options weregranted on October 18, 2005 with an exercise price of $27.27 per share.

• The guidelines for equity grants are structured in consideration of peer group practice with respect to theeconomic value of equity compensation provided, but also taking company performance against theCompany’s internal business plan and compared to the peer group into account.

• Equity grants to individual executive officers are generally based on Company/individual performancein the preceding year, but also on the expected future contribution and long-term retention of theexecutive officer.

Due to changes in equity accounting regulations and the related shift in equity compensation practices, theCompensation Committee asked management to conduct a comprehensive review of the Company’s executiveand broader employee equity program in 2005 and 2006. The purpose of this review was to determine if thecurrent stock option program: i) supports the Company’s executive/employee attraction and retention initiatives;ii) provides the appropriate incentive to executives and employees to create long-term stockholder value; and iii)serves the best interests of the Company’s stockholders. At this time, the Committee believes that stock optionspriced at the full fair market value of the Company’s common stock on the date of grant best achieve theobjectives stated above. However, the Committee believes that it will be prudent to consider other forms ofequity compensation if business conditions and/or competitive practice change.

18

For fiscal year 2007, the Committee approved the following stock option grants to the executive officers namedin the Summary Compensation Table:

Executive Officer2007 Stock Option

Grant

Garry O. Ridge 35,000Michael J. Irwin 10,000Graham P. Milner 10,000Michael L. Freeman 10,000William B. Noble 10,000

The options were granted on October 17, 2006 with an exercise price of $35.99 per share.

Benefits and Perquisites

The benefits and perquisites offered to the Company’s executive officers are substantially the same as thoseoffered to all employees. The Company provides medical and other benefits to executives that are generallyavailable to other employees, as well as a company car, laptop computer and cellular telephone. Frequent flyermileage is available to employees for personal use and for upgrades from coach or business class as provided forbusiness travel according to the Company’s travel policies. The Company maintains Supplemental Death andRetirement Plans for certain key employees including all of the executive officers named in the SummaryCompensation Table. The plans are described in greater detail under the Executive Compensation section of thisProxy Statement.

Compliance with Internal Revenue Code Section 162(m)

Section 162(m) of the Internal Revenue Code (the “Code”) generally provides that publicly held companies maynot deduct compensation paid to certain of its top executive officers to the extent that such compensation exceeds$1 million per officer in a calendar year. Compensation that is “performance-based compensation” within themeaning of the Code does not count toward the $1 million limit. The Compensation Committee has determinedthat ordinary income recognized by the Company’s executive officers as a result of their exercise of stockoptions granted by the Board under the Company’s 1990 Incentive Stock Option Plan having an exercise price atleast equal to the fair market value of the Company’s common stock on the date of grant, qualifies asperformance-based compensation as defined under Section 162(m) of the Code. The Company expects thatamounts of compensation paid to each of its executive officers in 2006 will not exceed the $1 million limit underSection 162(m) of the Code. The Committee believes it is in the best interests of the Company to have executiveofficer compensation be fully deductible under Section 162(m). However, the Committee and Board neverthelessretain the discretion to provide compensation that potentially may not be fully deductible to reward performanceand/or enhance retention.

Conclusion

The Compensation Committee believes that the Company’s compensation program is consistent with itsphilosophy and goals for success. Furthermore, the executive officer compensation program is responsible toshareholder interests as evidenced by the Company’s less than 50th percentile overall compensation marketposition compared to above 60th percentile performance for fiscal year 2006 relative to peers in key measures ofrevenue growth, operating income growth, EBITDA growth, and growth in market capitalization.

John C. Adams, Jr. (Chairman)Richard A. CollatoMario L. Crivello

Linda A. LangGary L. Luick

19

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative total stockholder return on the Company’s Common Shares withthe cumulative total return of a Peer Group of consumer product companies, the Standard & Poor’s 500Composite Stock Index (“S & P 500”), the Standard & Poor’s Small Cap 600 Composite Stock Index (“S & P600”) and the Russell 2000 Composite Stock Index (“Russell 2000”) for the five fiscal years ending August 31,2006. The comparison assumes $100 invested on August 31, 2001 in the Company’s Common Shares and ineach of the indices.

COMPARISON OF FIVE-YEAR CUMULATIVE RETURNS

WD-40 Company, a Peer Group and the S&P 500 Index, S & P Small Cap 600 Index, Russell 2000 Index.

50.00

100.00

150.00

200.00

2001 2002 2003 2004 2005 2006

WD-40 COMPANYS & P 500S & P SMALLCAP 600RUSSELL 2000PEER GROUP

Year ended August 31

2001 2002 2003 2004 2005 2006

WD-40 Company 100.00 131.63 150.13 151.03 156.91 194.83S & P 500 100.00 82.01 91.90 102.43 115.29 125.53S & P Small Cap 600 100.00 90.47 111.00 127.50 161.28 172.77Russell 2000 100.00 84.56 109.15 121.55 149.62 163.63Peer Group 100.00 121.88 127.20 140.48 153.01 165.38

The Peer Group returns are based upon beginning-of-year market capitalization weighting of the cumulativereturns for the following 11 consumer product companies: Alberto-Culver Co., Church & Dwight, Inc., EnescoGroup, Inc., Kimball International, Lancaster Colony Corp., La-Z-Boy Chair Co., National Presto Industries,Inc., Oneida Ltd., RPM Inc.-Ohio, Scotts Company and Valspar Corp.

20

ITEM NO. 2

RATIFICATION OF APPOINTMENT OF INDEPENDENT ACCOUNTANTS

The Audit Committee of the Board of Directors has appointed PricewaterhouseCoopers LLP as the independentregistered public accounting firm for the Company to audit the consolidated financial statements of the Companyfor fiscal year 2007. Although ratification by stockholders is not required by law, the Audit Committee hasdetermined that it is desirable to request ratification of this selection by the stockholders. Notwithstanding itsselection, the Audit Committee, in its discretion, may appoint new independent accountants at any time duringthe year if the Audit Committee believes that such a change would be in the best interests of the Company and itsstockholders. If the stockholders do not ratify the appointment of Pricewaterhouse-Coopers LLP, the AuditCommittee may reconsider its selection.

A majority of the votes of the common stock present or represented at the meeting is required for approval.Broker non-votes will be voted in favor of approval. PricewaterhouseCoopers LLP acted as the Company’sindependent registered public accounting firm during the past fiscal year and, unless the Audit Committeeappoints new independent accountants, PricewaterhouseCoopers LLP will continue to act in such capacity duringthe current fiscal year. It is anticipated that a representative of PricewaterhouseCoopers LLP will attend theAnnual Meeting of Stockholders, will have an opportunity to make a statement if he or she desires to do so andwill be available to respond to appropriate questions.

The Audit Committee’s policy is to pre-approve all audit and permissible non-audit products and servicesprovided by the independent accountants. These products and services may include audit services, audit-relatedservices, tax services, software and other products or services. Pre-approval is generally provided for up to oneyear and any pre-approval is detailed as to the particular service or category of services and is generally subjectto a specific budget. The independent accountants and management are required to periodically report to theAudit Committee regarding the extent of services provided by the independent accountants in accordance withthis pre-approval, and the fees for the services performed to date. The Audit Committee may also pre-approveparticular services on a case-by-case basis. The possible effect on the independence of the accountants isconsidered by the Audit Committee. There is no direct or indirect understanding or agreement that places a limiton current or future years’ audit fees.

Audit Fees

PricewaterhouseCoopers LLP has provided audit services to the Company for each of the past two fiscal years.Audit fees consist of fees for professional services rendered for the audit of the Company’s consolidated annualfinancial statements and review of the interim consolidated financial statements included in quarterly reports andservices that are normally provided by PricewaterhouseCoopers LLP in connection with statutory and regulatoryfilings or engagements. Audit fees also include fees for professional services rendered for the audits of(i) management’s assessment of the effectiveness of internal control over financial reporting and (ii) theeffectiveness of internal control over financial reporting. The aggregate fees billed to the Company byPricewaterhouseCoopers LLP for audit services performed for the Company for the past two fiscal years were$891,000 for the year ended August 31, 2005 and $869,000 for the year ended August 31, 2006.

Audit-Related Fees

Audit-related services consist of assurance and related services that are reasonably related to the performance ofthe audit or review of the Company’s consolidated financial statements and are not reported under “Audit Fees.”No audit-related services were provided during the fiscal years ending on August 31, 2005 and August 31, 2006.

21

Tax Fees

PricewaterhouseCoopers LLP has provided tax compliance, tax advice, and tax planning services to theCompany for each of the past two fiscal years. The tax services provided to the Company by the auditors duringeach of the fiscal years ended August 31, 2005 and August 31, 2006 consisted of tax return preparation, taxpayment-planning services and assistance with tax audits and appeals (to the extent permitted.) The aggregatefees billed to the Company by PricewaterhouseCoopers LLP for tax services performed for the Company for thepast two fiscal years were $163,964 for the year ended August 31, 2005 and $35,000 for the year endedAugust 31, 2006.

All Other Fees

PricewaterhouseCoopers LLP provided access to online research reference material for the fiscal year endingAugust 31, 2005 and August 31, 2006. The aggregate fees billed to the Company by PricewaterhouseCoopersLLP for other services performed for the Company for the past two fiscal years were $3,000 for the year endedAugust 31, 2005 and $3,000 for the year ended August 31, 2006.

STOCKHOLDER PROPOSALS

Stockholder proposals must be received by the Company no sooner than May 9, 2007 and not later thanJuly 9, 2007 to be included in the Proxy Statement and form of Proxy for the next annual meeting.

By Order of the Board of DirectorsMaria M. Mitchell

Secretary

Dated: November 6, 2006

IT IS IMPORTANT THAT PROXIES BE RETURNED PROMPTLY. THEREFORE, STOCKHOLDERSARE URGED TO FILL IN, SIGN AND RETURN THE ACCOMPANYING FORM OR FORMS OF

PROXY IN THE ENCLOSED ENVELOPE.

22

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended August 31, 2006

Commission File No. 000-06936

WD-40 COMPANY(Exact Name of Registrant as specified in Charter)

Delaware 95-1797918(State or other jurisdiction of

incorporation or organization)(I.R.S. Employer

Identification No.)

1061 Cudahy Place, San Diego, California 92110(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code (619) 275-1400

Securities registered pursuant to Section 12(b) of the Act:

Title of Class: None

Securities registered pursuant to Section 12(g) of the Act:

Title of Class: Common Stock, $.001 par value

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct: Yes ‘ No È

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theAct: Yes ‘ No È.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant wasrequired to file such reports), and (2) has been subject to such filing requirements for the past 90days: Yes È No ‘.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not containedherein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K: È.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act:

Large accelerated filer ‘ Accelerated filer È Non-accelerated filer ‘

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the ExchangeAct): Yes ‘ No È

The aggregate market value (closing price) of the voting stock held by non-affiliates of the Registrant as ofFebruary 28, 2006 was $483,505,000.

As of October 17, 2006 the Registrant had 17,021,909 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The Proxy Statement for the annual meeting of stockholders on December 12, 2006 is incorporated by reference intoPART III, Items 10, 11, 12 and 14.

PART I

ITEM 1 - Business

(a) General Development of Business.

For more than four decades, WD-40 Company (the Company) sold only one product, WD-40®. WD-40 is amulti-purpose product which acts as a lubricant, rust preventative, penetrant, cleaner and moisture displacer. InDecember 1995, the Company acquired the 3-IN-ONE® Oil brand. 3-IN-ONE Oil is a lower cost general-purposelubricant that is useful when precise applications of a lubricant are needed. In April 1999, the Company acquiredthe Lava® brand heavy-duty hand cleaner and in October 2000, acquired the Solvol® brand heavy-duty handcleaner. The four brands complement each other, providing the Company with a line of both lubricant and heavy-duty hand cleaning products aimed at the Do-It-Yourself (“DIY”), hardware, automotive and other retail andindustrial markets. In April 2001, the Company acquired three additional brands of household cleaning products,2000 Flushes®, X-14® and Carpet Fresh®. The Company added to its fortress of brands through the acquisition inMay 2002 of the Spot Shot® brand, which is an aerosol and liquid carpet stain remover and a leading brand in thecarpet stain remover category. The Spot Shot brand fits well within the Company’s brand portfolio, alongside theother household product brands. In April 2004, the Company again added to its brands with its purchase of the1001® line of carpet and household cleaners. The 1001 brand provides the Company an opportunity to expand itshousehold products market in the U.K. with a recognized U.K. brand name.

The acquisition of the 3-IN-ONE Oil brand provided the Company with an existing network of distribution in 17countries, including several markets in which the WD-40 brand had not been sold. The Company used thisdistribution network to introduce the WD-40 brand to these markets and to add distribution channels in some ofthe markets that had been previously established.

The Lava brand is more than 100 years old and is well recognized by U.S. consumers. When the Lava brand wasacquired, the Company identified that the Lava consumer and the WD-40 consumer shared similar characteristicsand believed the distribution network developed through the WD-40 brand could effectively promote growth inthe U.S. With the Lava acquisition, the Company concluded that it would benefit by an increased position in theU.S. grocery channel. This was a catalyst for the Global Household Brands acquisition.

In fiscal 2001, the Company acquired the business, brand trademarks, patents and other tangible and intangibleassets known as Global Household Brands, which included the three principal brand trademarks 2000 Flushesand X-14 automatic toilet bowl cleaners, X-14 hard surface cleaners and Carpet Fresh rug and room deodorizers.The acquisition was made to move the Company forward in its fortress of brands strategy, while also providingeconomies of scale in sales, manufacturing, and administration, and to strengthen the Company’s position in thegrocery trade channel. The Global Household Brands’ broker network and grocery business, combined with theWD-40 Company’s DIY distribution, gave the Company growth potential for all brands across new tradechannels.

In fiscal 2001, the Company also acquired the Solvol brand of heavy-duty hand cleaners in Australia andsubsequently extended that brand into a liquid product, a benefit from the technology obtained in the acquisitionof the Lava brand. These liquid products have contributed to the growth of the Solvol brand.

In fiscal 2002, the Company completed the acquisition of the business, worldwide brand trademarks and otherintangible assets of Heartland Corporation. The principal brand acquired by the Company was the Spot Shotbrand, an aerosol carpet stain remover. The acquisition of this brand expanded the Company’s product offerings.The acquisition also included related Spot Shot products and a group of developing brands, which weresubsequently sold to former employees of Heartland.

1

In fiscal 2004, the Company purchased the 1001 line of carpet and household cleaners. The Company acquiredthis line of products to gain a presence in the U.K. market and to facilitate an introduction of the Company’s SpotShot and Carpet Fresh brands through the use of an existing brand currently recognized by market consumers.

As a result of the Solvol and 1001 acquisitions, the Company was able to introduce existing products to newmarkets. The Company is also focused on expanding its current brands in existing markets with new productdevelopment. In fiscal year 2003, a new product development team, known as Team Tomorrow, was created tosupport new product development and current product improvement for all of the Company’s brands.

(b) Financial Information About Industry Segments.