wawanesa insurance annual report · wawanesa is a canadian mutual company owned by its...

TRANSCRIPT

WaWanesa Insurance2011 annual report

The WaWanesa Life insurance company

400–200 Main street Winnipeg, Manitoba r3c 1a8Book value of shares $93,165,000

WaWanesa GeneraL insurance company

9050 Friars road san Diego, california 92108Book value of shares $260,067,000

WaWanesa hoLdinGs u.s. inc.

9050 Friars roadsan Diego, california 92108Book value of shares $13,627,000

Wawanesa is a Canadian mutual company owned by its policyholders. With assets of

over $7 billion and nearly 2 million policies inforce, Wawanesa is one of the 10 largest

property and casualty insurers in Canada.

Wawanesa has a rich history dating back to September 25, 1896, when it was founded in

the Village of Wawanesa, Manitoba. Today, our head office continues to be located in the

Village of Wawanesa with the executive offices located in Winnipeg, Manitoba.

Wawanesa has 100% ownership of three subsidiary companies.

1

MIssIon anD Values

MIssIon

“Earning your trust since 1896”… As a policyholder-owned mutual insurance company,

we will continue to earn trust by providing quality products and services at the lowest

price which supports long-term growth and financial stability.

Values

• We treat others in a respectful and truthful manner.

• We conduct business with integrity, honesty, consistency and fairness.

• We act ethically and lawfully.

• We take pride in making service a priority.

• We encourage collaboration, innovation and excellence.

• We support the communities in which we work and live.

2

The year just ended proved to be a challenging one for our Company.

While we made significant progress on many chosen

initiatives and grew our business at a reasonable pace,

we are reporting disappointing underwriting results.

Renewal of our major insurance systems has been a

high priority in recent years and I am pleased to report

that we made major strides forward in 2011.

During the year, we successfully implemented a

new claims system (Guidewire’s ClaimCentre) across

the entire organization. Final conversions and

decommissioning of the old system will be complete

by mid-2012. The project team did a tremendous job

on this two-year project that was completed on time

and on budget. The team consisted of a combination

of Wawanesa staff from information services, executive

office claims and

each regional

claims department

augmented by

external consultants.

This is the first step

in our renewal of all

insurance systems

and the success has

certainly provided confidence in our ability to complete

the renewal of all systems in the coming years.

Also in 2011, we completed the introduction of our

broker transaction portal which provides brokers

with the ability to send insurance transactions to

us electronically. This is our first transaction portal

offering and will provide an improved service offering

to our brokers. We are actively transferring brokers to

this environment.

Work continues on a number of other initiatives.

Progress was made on the development of an enterprise

data warehouse. Late in the year, a project was initiated

to replace our financial reporting systems with a new

state-of-the-art system. This work will be conducted

during 2012 and 2013. Furthering our renewal of core

insurance systems, during 2012 we will initiate the

project to replace our policy administration system.

Development of a formal Enterprise Risk Management

program began in earnest during the year. We recognize

the value of an increased focus on managing individual

risks but also the need to consider combinations of risks

through modeling and stress testing.

We implemented a completely new rating system in

Quebec late in the year. It was clear to us that a more

sophisticated rating approach was required to reinforce

our competitive position in the market. This was a

major undertaking that has significantly changed our

business approach. We will be monitoring the impact

quite carefully throughout 2012.

Since 1995, we have

operated in the

United States both as

a branch of Wawanesa

Mutual and through

our wholly-owned

subsidiary,

Wawanesa General.

We completed

a corporate reorganization during 2011 and now

operate solely as Wawanesa General. This simplifies

our corporate structure and will reduce future

administrative costs.

Our plans for 2012 include continuing with enterprise

system renewal and taking the actions required to

improve our underwriting results whether by rate

increases, product changes or other means. As well,

we are considering two emerging issues. Regulatory

During the year, we successfully implemented a new claims system (Guidewire’s ClaimCentre) across the entire organization.

presIDent’s report

3

capital requirements are increasing. While we have

always reported very strong capital ratios and would

continue to do so under these new requirements,

the new requirements related to certain investment

types could reduce the reported ratio. Accordingly,

we will be reviewing our investment policies during

2012. We are also studying our earthquake exposure.

Prudent management of earthquake risk requires that

we maintain an extensive reinsurance program with

highly rated reinsurers. But earthquake exposures have

grown dramatically in recent years and reinsurance

rates have increased due to recent global earthquake

activity. This has resulted in increased reinsurance costs

and as a result, higher premiums for our policyholders

purchasing earthquake coverage. We intend to continue

carefully monitoring our earthquake exposures and

coverages as part of our management of this risk.

consolIDateD FInancIal results

For the first time, our financial statements have been

prepared in accordance with International Financial

Reporting Standards (IFRS). The preparation for the

transition to IFRS was a major undertaking conducted

over a number of years

by our accounting

and finance staff. The

preparation was well

done and provided for a

very successful transition

to IFRS. As a result of

the transition to IFRS,

Wawanesa Life has

been consolidated into

the Wawanesa Mutual

financial statements for the first time. This required

a change in the presentation of the Statements of

Operations and the new format does not provide

traditional property and casualty disclosures.

Accordingly, there is expanded note disclosure which

provides appropriate presentation of the results of both

our property and casualty and life operations. Separate

financial statements will continue to be prepared for

Wawanesa Life.

On a consolidated basis, premium revenues increased

by 5.6% while investment income increased 6.2%.

Profit for the year was $108 million, down from

$129 million in 2010. Profits declined in both property

and casualty and life operations with severe weather

negatively impacting property and casualty results and

the low interest rate environment requiring reserve

increases in life operations.

Total assets increased to $7 billion and total capital

increased to $2.3 billion. Our capital ratio remains

very strong at 302%, much in excess of regulatory

requirements while our A.M. Best rating was stable at

A+ (Superior).

property anD casualty operatIons

Financial Results

Overall business growth was good but somewhat

reduced from 2010’s growth rate. While inforce policies

increased by 2% and written premiums increased

by 5.4%, regional results varied considerably. Many

regions grew quite well, some reported moderate

growth and a couple of regions declined slightly.

Our underwriting results

were disappointing and

the story is severe weather,

mainly in Western Canada.

We are reporting an

underwriting loss in our

property and casualty

operations of $90 million

compared to a $50 million

loss in 2010.

Property results, both personal and commercial,

were very poor in 2011. Our underwriting loss

was $120 million with a combined ratio of 115%.

While a number of areas reported poor results, the

increased severe weather activity in Western Canada

was the primary driver of the results. Total weather

catastrophe costs were $259 million in 2011, up almost

$100 million from 2010 and more than double the

2009 levels.

3

For the first time, our financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS).

4

The severe weather was most extreme in Alberta where

catastrophe costs increased by $100 million to total

$200 million in 2011. The catastrophic events started

early with the Slave Lake wildfire in May, continued

through the summer with many wind and hail

storms and ended with a major Calgary windstorm

in November. It is very difficult to address these fast

ramp-ups in claims costs but we are responding in an

appropriate but aggressive manner. Our reinsurance

arrangements certainly helped cushion the financial

blow of this increased catastrophe activity. However,

catastrophe reinsurance is designed to assist companies

with unexpected extreme events and if the level of

catastrophe activity experienced in the last couple of

years becomes the norm in the future, reinsurance costs

and availability may be impacted.

Our automobile results improved significantly in

2011. The main contributor to the improvement was

the Ontario automobile line of business, but while

improving significantly, we are still reporting an

underwriting loss in the line. It appears the Ontario

market has stabilized to a significant extent as result of

the September, 2010 reforms but there are still elements

of the reforms that have not been completed. It is

hoped that the government and regulator maintain

their resolve to take the necessary actions to further

stabilize the market. All other regions reported

good results except for disappointing results in the

United States.

Further declines in the interest rate environment

required an increase in policy reserves which reduced

underwriting income in the amount of $13 million.

Net investment income increased from $232 million

to $245 million. Overall, profit before taxes in

our property and casualty operations declined to

$155 million from $183 million.

Regional Results

The Maritime Region operated very effectively in

2011 with continued growth and overall underwriting

profitability. Policy counts increased by over 3% and

premiums increased by 8%. Auto results were good

but offset somewhat by losses in the property line.

While the auto insurance environment in the region

has been quite stable for many years, governments in

both New Brunswick and Nova Scotia are introducing

modifications to the auto insurance systems. It is

hoped that these changes do not threaten the premium

stability that has existed for the last number of years.

Our business in the Quebec Region has been declining

in recent years. We are reporting modest business

reductions in 2011. In response, we introduced a

completely updated pricing and rating approach late

in 2011 that is designed to re-establish our competitive

position and reverse recent business declines. The

impact of this major change will be monitored carefully

in 2012.

The Ontario Region grew significantly in 2011. Policy

counts increased by 5% while premium income

increased by 14%. A significant portion of the growth

occurred in the property line. After a number of

difficult years in the automobile line, underwriting

results improved significantly in 2011, although an

underwriting loss was still reported for 2011. There

is still uncertainty in the automobile environment

as the 2010 reforms are not fully in effect thus there

is still doubt that the desired results will be realized.

Accordingly, we continue to carefully monitor

the environment.

The Winnipeg Region had another stable operating year

in 2011. Policy growth of nearly 2%, premium growth

of 11% and a break-even underwriting position are

being reported. Much of the growth occurred in NW

Ontario where an underwriting loss was reported, while

Manitoba results were profitable.

The Prairie Region grew nicely in 2011 with a 2%

increase in policies and a 10% increase in premiums.

Severe weather events impacted the region again in

2011 although not to the same extent as in 2010. While

this resulted in a reduced underwriting loss, the loss is

still substantial in spite of significant rate increase in

recent years. We will continue to address this shortfall.

Southern Alberta and Northern Alberta Regions are

reporting very similar results for 2011. Policy counts

increased by 2–3% while written premiums increased

5

5–6%. Both reported overall underwriting losses with

very good auto profitability but disastrous underwriting

results in the property line. The underwriting loss for

property in all of Alberta was $86 million. The poor

property results were the result of the severe weather

mentioned above. Seventeen events occurred in Alberta

with a gross loss cost of $200 million. Of this total,

$183 million was property losses and $17 million

was auto losses. As mentioned, it is very difficult to

address rapid claims increases. We are responding in

an appropriate but aggressive manner via a variety of

product and pricing changes. Heavy catastrophic claims

activity also creates

a very challenging

environment for our

claims department staff.

The British Columbia

Region reported another

year of substantial

growth. Policies

increased by over 5%

with written premium

growth of 12%. This growth came in spite of substantial

premium rate increases for earthquake coverage

made necessary by the increasing costs of securing

reinsurance protection for earthquake exposures. While

a modest underwriting loss was reported, we believe

actions taken during 2011 and early 2012 will improve

the region’s 2012 results.

Our United States operation was challenged in 2011

by poor economic conditions in California and a

very competitive environment. A small decline in

policies was experienced along with a small increase

in premiums. Underwriting results were disappointing

with a significant loss being reported. Our focus for

2012 is on improving underwriting results while

maintaining business levels.

lIFe operatIons

Financial Results

Wawanesa Life achieved good results in new business

activity and strong policy persistency which are both

contributing to record premium revenues. Premium

income net of reinsurance grew to $106 million in

2011, surpassing $100 million for the first time. All

lines of business contributed to this achievement.

However, like others in the life insurance industry, we

continued to encounter challenges with low interest

rates, stock market volatility and actuarial standards

updates. The stock market decline and record low

interest rates required reserve increases. Significant

mortality assumption changes related to the valuation

of individual insurance contract liabilities also served

to increase reserves. These changes generally had

a negative impact on permanent products and a

favourable impact on

term products which

created a significant

loss from participating

business, offsetting

positive results reported

for non-participating

business. Wawanesa Life

is reporting a net loss of

$1.7 million for the year.

Operational Comments

New business sales of individual insurance totaled

$5.3 million, 11% ahead of 2010 and consistent with

the results achieved over the last few years. Production

was strong across Wawanesa Life with eight of nine

regions surpassing 2010 numbers. Policy persistency

was very good with inforce net premium growing by

4% to $40.7 million.

Management action was taken this year to address

the prolonged period of low interest rates being

experienced. These actions included changes to

investment mix and increases in asset duration.

Premium increases were required to lessen the new

business strain of current permanent business.

During 2011, plans were put in motion to replace the

Individual Operation’s various legacy systems. Much

of the year was spent detailing the current system

strengths and weaknesses, scoping areas of desirable

business process improvement and evaluating possible

vendor solutions. Vendor selection was completed

by year end and work is now beginning on the

Wawanesa Life achieved good results in new business activity and strong policy persistency which are both contributing to record premium revenues.

6

implementation. This is a significant investment

for Wawanesa Life. The objective is to modernize

the technology environment and gain efficiencies

in the back office environment which will enhance

policyholder and broker servicing. When complete,

Wawanesa Life will be in a good position to continue

its history of steady growth.

New business sales of group insurance reached

$4.7 million. While this is off the record numbers of

2010, it is well ahead of historical production levels.

Net premium revenue was $34.3 million, an increase of

29% from 2010.

Action was taken early in the year to mitigate the

unfavourable claim trends that were emerging from the

newly launched 3-9 life group plan. Premium and plan

design changes were made to the product, returning it

to a solid financial footing.

New business activity

continues to meet targeted

expectations.

While we have experienced

recent success in growing

the group insurance base,

we want to ensure that our

approach will continue to

produce steady, profitable

growth in the long term. Accordingly, an operational

review of our group product pricing and underwriting

approach was undertaken in 2011. As a result of

this review, we will be updating some of our current

underwriting and pricing practices during 2012.

Wawanesa Life continued to demonstrate its financial

strength despite the economic and financial market

challenges in 2011. The MCCSR (Minimum Continuing

Capital and Surplus Requirements) ratio is well in

excess of 200%, significantly above the requirement

set by the Office of the Superintendent of Financial

Institutions. In addition, Wawanesa Life continues to

be rated as A (Excellent) by A.M. Best.

acknoWleDgeMents

While there were no senior management changes in

2011, there were some changes in the composition of

our Board of Directors.

At the annual meeting in May, 2011, two long-serving

members retired from the Board of Directors. Both

were dedicated to Wawanesa and committed to the

long-term success of the Company. Barry W. Harrison

retired after 17 years of service including serving as

Board Chair from 2006 until his retirement. Susan M.

Van De Velde served Wawanesa for 18 years and chaired

various Board committees. Both Susan and Barry

were instrumental in the development of enhanced

governance processes over a number of years. We

thank them both for their significant contribution

to Wawanesa.

As a result of Barry’s

retirement, the Board selected

Richard R. Bracken as the

new Board Chair. Richard

has been a member of the

Board since 2004. He is an

experienced business person

and very involved in the

Winnipeg community.

Also at the annual meeting, Robert O. Landry was

elected as a director of all Wawanesa companies.

Mr. Landry is a resident of Toronto and a former

property and casualty insurance industry executive,

having served as President and CEO of a leading

commercial property and casualty company. He is

a former Board member of the Insurance Bureau of

Canada and a Past Chair of The Insurance Institute

of Canada.

Our Company continues to grow and prosper in a

challenging environment. We are clear in our direction

and we are preparing for the future by developing

operational depth and flexibility. I would like to

offer sincere thanks to our employees and brokers

who continued to demonstrate their commitment to

Wawanesa in 2011.

Ken McCrea, CA, FLMI

President and Chief Executive Officer

We are clear in our direction and we are preparing for the future by developing operational depth and flexibility.

7

February 21, 2012

to the DIrectors oF the WaWanesa Mutual Insurance coMpany

The accompanying summary consolidated financial statements, which

comprise the summary consolidated balance sheets as at December 31,

2011 and 2010 and the summary consolidated statements of operations for

the years ended December 31, 2011 and 2010, are derived from the audited

consolidated financial statements of The Wawanesa Mutual Insurance

Company for the years ended December 31, 2011 and 2010. We expressed

an unmodified audit opinion on those consolidated financial statements in

our report dated February 21, 2012.

The summary consolidated financial statements do not contain all the

disclosures required by International Financial Reporting Standards.

Reading the summary consolidated financial statements, therefore, is not

a substitute for reading the audited consolidated financial statements of

The Wawanesa Mutual Insurance Company.

Management’s Responsibility for the Summary Consolidated Financial Statements

Management is responsible for the preparation of a summary of the

audited consolidated financial statements in accordance with International

Financial Reporting Standards.

Auditor’s Responsibility

Our responsibility is to express an opinion on the summary consolidated

financial statements based on our procedures, which were conducted in

accordance with Canadian Auditing Standards (“CAS”) 810, “Engagements

to Report on Summary Financial Statements.”

Opinion

In our opinion, the summary consolidated financial statements derived

from the audited consolidated financial statements of The Wawanesa

Mutual Insurance Company for the years ended December 31, 2011 and

2010 are a fair summary of those consolidated financial statements, in

accordance with International Financial Reporting Standards.

Chartered Accountants

Winnipeg, Manitoba

the WaWanesa Mutual Insurance coMpany

report oF the InDepenDent auDItor on the suMMary consolIDateD FInancIal stateMents

Founded in 1896

Incorporated May 1, 1929

Head Office

Wawanesa, Manitoba

Executive Office

900–191 Broadway

Winnipeg, Manitoba

oFFIcers anD corporate ManageMent

K. E. McCrea, CA, FLMI President and Chief Executive Officer

G. N. Bass, Q.C. Vice President, General Counsel and Secretary

B. A. MacKinnon, FCAS, FCIA, MAAA Vice President and Chief Actuary

G. J. Timlick, CA Vice President and Chief Financial Officer

S. J. Goy, ACAS, CIP Vice President, Insurance Products

R. G. LaPage, FCIP, CRM Vice President, Regional Insurance Operations

C. R. Loeppky, BScCS Vice President, Information Services

C. B. Luby, FCIP, CRM Vice President, Marketing and Business Development

B. K. MacIntyre, BBA, FCIP Vice President, Claims

T. L. Nelson, FLMI/M, CHRP, CIP Vice President, Human Resources

K. P. Boyd, CA Controller

P. R. Mulaire, CMA, FCIP, CIA Manager, Internal Audit

8

February 21, 2012

to the DIrectors oF the WaWanesa Mutual Insurance coMpany

I have valued the insurance contract liabilities of the Company for its

consolidated balance sheets as at December 31, 2011 and their change

in the consolidated statements of operations for the year then ended

in accordance with accepted actuarial practice including selection of

appropriate assumptions and methods.

In my opinion, the amount of insurance contract liabilities makes

appropriate provision for all policyholder obligations, and the consolidated

financial statements fairly present the result of the valuation.

Brett A. MacKinnon, FCAS, FCIA, MAAA

Winnipeg, Manitoba

the WaWanesa Mutual Insurance coMpany

appoInteD actuary’s reportregIonal oFFIces

Maritime 1010 St. George Boulevard Moncton, New Brunswick B. E. MacKenzie, CIP Vice President, Maritime Region

Québec 8585 Décarie Boulevard Montréal, Québec C. Auclair, PAA Vice President, Québec Region

Ontario 100–4110 Yonge Street Toronto, Ontario T. R. Greer Vice President, Ontario Region

Winnipeg 700–200 Main Street Winnipeg, Manitoba E. Rossong, FCIP Vice President, Winnipeg Region

Prairie Wawanesa, Manitoba W. G. McGregor, FCIP Vice President, Prairie Region

Northern Alberta 100, 8657–51st Avenue Edmonton, Alberta K. E. Hartry, FCIP, MBA Vice President, Northern Alberta Region

Southern Alberta 600, 708–11th Avenue S.W. Calgary, Alberta M. M. Cote-Johnson, CIP Vice President, Southern Alberta Region

British Columbia 400–1985 West Broadway Vancouver, British Columbia G. R. Haigh, FCIP, CAIB Vice President, British Columbia Region

United States 9050 Friars Road San Diego, California D. G. Fitzgibbons, CPCU Vice President, United States Operations

9

As at December 31

2011 2010

(000s)

Assets

Cash and cash equivalents $ 90,211 $ 59,262

Accrued investment income 30,774 29,873

Investments 5,622,206 5,310,015

Other assets 1,312,578 1,189,937

Total assets $ 7,055,769 $ 6,589,087

Liabilities

Insurance contract liabilities $ 4,209,645 $ 3,835,944

Other liabilities 513,638 514,953

Total liabilities 4,723,283 4,350,897

Equity 2,332,486 2,238,190

Total liabilities and equity $ 7,055,769 $ 6,589,087

the WaWanesa Mutual Insurance coMpany

suMMary consolIDateD Balance sheets

A complete set of audited consolidated financial statements are available at www.wawanesa.com

10

For the year ended December 31

2011 2010

(000s)

Revenue

Net premiums written $ 2,416,305 $ 2,298,202

Change in unearned premiums (71,298) (94,768)

Net premiums earned 2,345,007 2,203,434

Net investment income 294,994 277,672

Instalment service charges earned 35,660 33,886

2,675,661 2,514,992

Expenses

Net claims and insurance benefits incurred $ 1,905,568 $ 1,757,365

Other expenses incurred 616,878 2,522,446 573,644 2,331,009

Profit before income taxes 153,215 183,983

Provision for income taxes 45,365 54,563

Profit for the year $ 107,850 $ 129,420

Profit (loss) for the year attributed to:

Policyholders of the Company $ 114,543 $ 130,013

Participating policyholders’ interest (6,693) (593)

$ 107,850 $ 129,420

the WaWanesa Mutual Insurance coMpany

suMMary consolIDateD stateMents oF operatIons

A complete set of audited consolidated financial statements are available at www.wawanesa.com

11

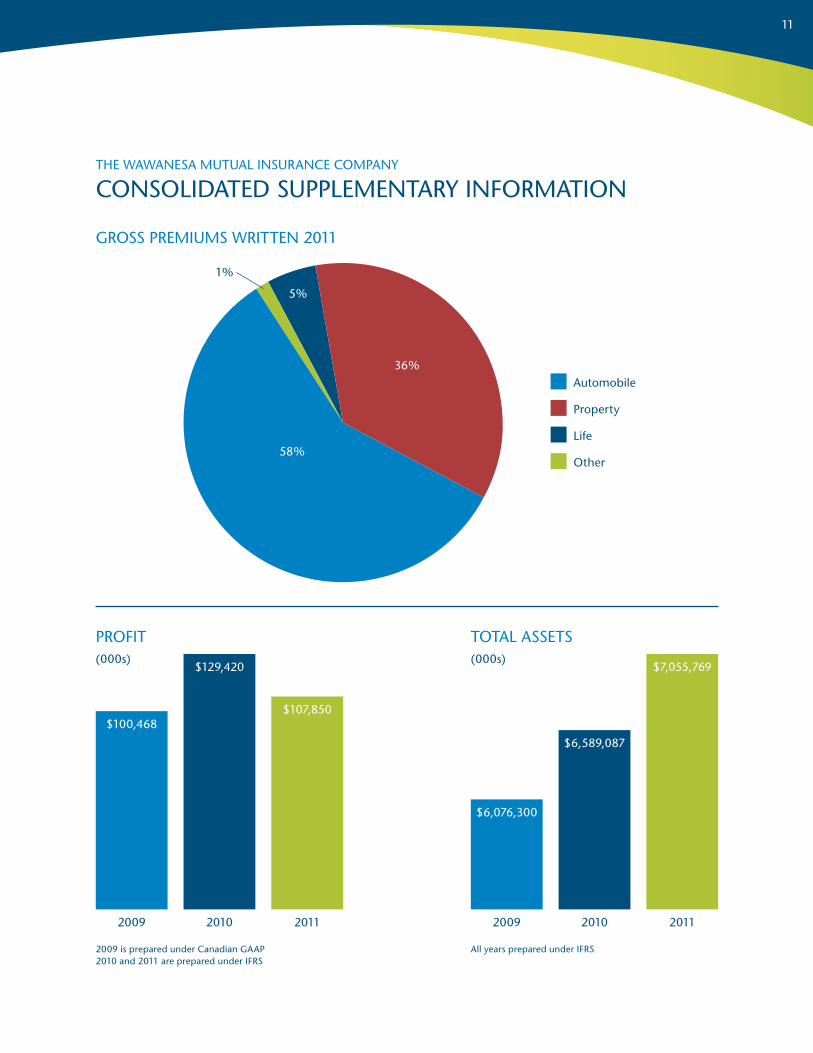

the WaWanesa Mutual Insurance coMpany

consolIDateD suppleMentary InForMatIon

automobile

property

life

other

gross preMIuMs WrItten 2011

proFIt total assets

58%

36%

5%

1%

2009 2009

$100,468

$6,076,300

2010 2010

$129,420

$6,589,087

2011 2011

$107,850

$7,055,769

2009 is prepared under canadian gaap 2010 and 2011 are prepared under IFrs

all years prepared under IFrs

(000s) (000s)

12

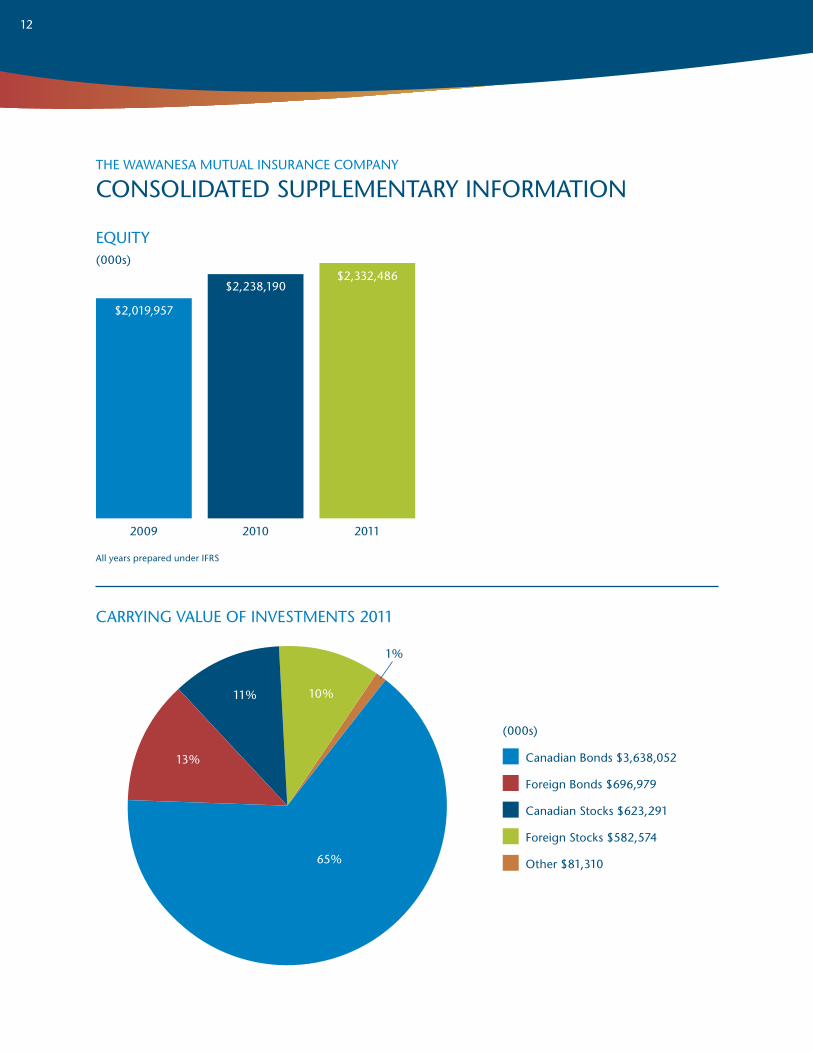

the WaWanesa Mutual Insurance coMpany

consolIDateD suppleMentary InForMatIon

equIty

carryIng Value oF InVestMents 2011

2009 2010 2011

all years prepared under IFrs

$2,019,957

$2,238,190$2,332,486

canadian Bonds $3,638,052

Foreign Bonds $696,979

canadian stocks $623,291

Foreign stocks $582,574

other $81,31065%

13%

11% 10%

1%

(000s)

(000s)

13

P&C Operations consist of The Wawanesa Mutual Insurance Company in Canada and Wawanesa General Insurance Company in the U.S. Our P&C Operations have conducted business in Canada and the U.S. for over 100 years and 35 years, respectively.

P&C Operations provide automobile, personal and

commercial property, and liability insurance products

in all major areas of Canada as well as in California

and Oregon. Wawanesa’s P&C insurance products

are distributed by over 1,300 independent insurance

brokers except in Quebec and the U.S. where products

are distributed through company agents.

Key Facts

• Total assets of $6.3 billion

• Strong financial position with equity of $2.3 billion

• Over $2.3 billion in annual policy premiums

• Over 2,300 employees across Canada and in the U.S.

key FInancIal Measures

The following information and charts may not be IFRS

measurements, but are derived from elements of the

financial statements (2011 and 2010 are prepared under

IFRS, 2009 is prepared under Canadian GAAP), and are

consistent with financial measures used in the P&C

insurance industry.

property anD casualty (p&c) operatIons proFIle

(000s)

gross preMIuMs WrItten

Gross premiums written is the premiums for all insurance policies placed inforce during the period including new

policies and renewals. It is a measure of how much insurance P&C Operations sold to our customers during the period.

2009 2010 2011

automobile

personal property

commercial property

other

$1,3

38,4

26

$543

,540

$176

,768

$32,

923

$195

,136

$35,

542

$211

,261

$38,

080$61

9,81

7

$68

3,40

2

$1,4

09,0

48

$1,4

48,1

40

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

14

unDerWrItIng loss

Underwriting loss is the loss from insurance operations. It includes net premiums earned and instalment service

charges less net claims and other expenses incurred.

net InVestMent IncoMe

Net investment income is comprised of interest income, dividends and distributions, the realized gain on sale of

available-for-sale financial assets, and other investment income and expenses.

2009

2009

2010

2010

2011

2011

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

(000s)

(000s)

$182,248

$232,436 $244,920

$(78,740)

$(49,745)

$(90,334)

p&c operatIons

15

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

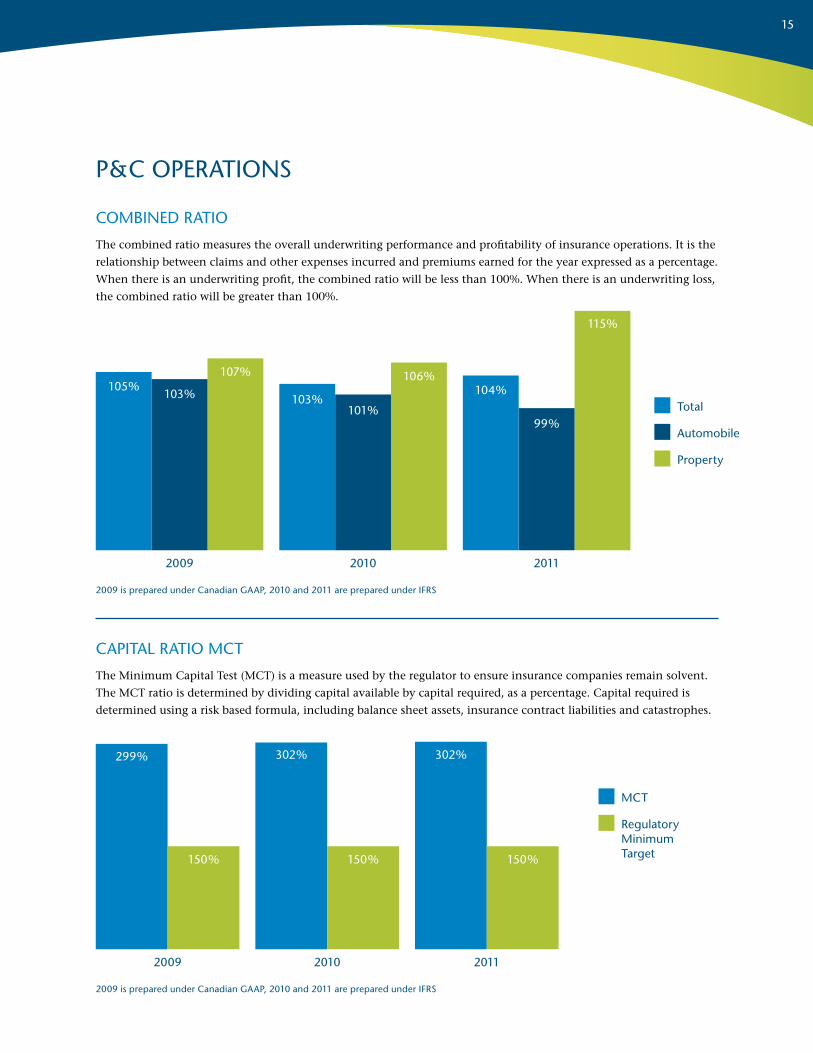

capItal ratIo Mct

The Minimum Capital Test (MCT) is a measure used by the regulator to ensure insurance companies remain solvent.

The MCT ratio is determined by dividing capital available by capital required, as a percentage. Capital required is

determined using a risk based formula, including balance sheet assets, insurance contract liabilities and catastrophes.

coMBIneD ratIo

The combined ratio measures the overall underwriting performance and profitability of insurance operations. It is the

relationship between claims and other expenses incurred and premiums earned for the year expressed as a percentage.

When there is an underwriting profit, the combined ratio will be less than 100%. When there is an underwriting loss,

the combined ratio will be greater than 100%.

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

2009

2009

2010

2010

2011

2011

150% 150% 150%

299% 302% 302%

Mct

regulatory Minimum target

total

automobile

property

105%103%

107%

103%101%

106%104%

99%

115%

p&c operatIons

16

Our life insurance operations are conducted by The Wawanesa Life Insurance Company. It is a Canadian life and health insurance company that has been in operation for over 50 years.

Wawanesa Life provides term, permanent and critical

illness insurance plus investment product options

including segregated funds to individuals through its

independent broker channel. Group life and health

insurance products are designed to service the needs

of employers, associations and unions by working

with group benefit brokers. Wawanesa Life maintains

regional sales offices across the country to support its

many broker and client relationships.

Key Facts

• Total assets of $830 million

• Individual life insurance volumes of $14 billion

insured through 65,000 polices

• Insures more than 24,000 employees through

group benefit plans

key FInancIal Measures

The following information and charts may not be

IFRS measurements, but are derived from elements

of Wawanesa Life’s financial statements (2011 and

2010 are prepared under IFRS, 2009 is prepared under

Canadian GAAP), and are consistent with financial

measures used in the life insurance industry.

lIFe operatIons proFIle

(000s)

2009 2010 2011

Individual

group

annuity

$37,668 $39,080$40,731

$23,486$26,967

$34,738

$27,402

$32,482 $33,907

net preMIuMs anD equIValents

Net premiums and equivalents are the sum of billed insurance premiums, contributions received for investment in

annuities or segregated funds, management fees earned on segregated fund balances and fee income earned from the

administration of group business where the policyholder retains the insurance risk.

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

17

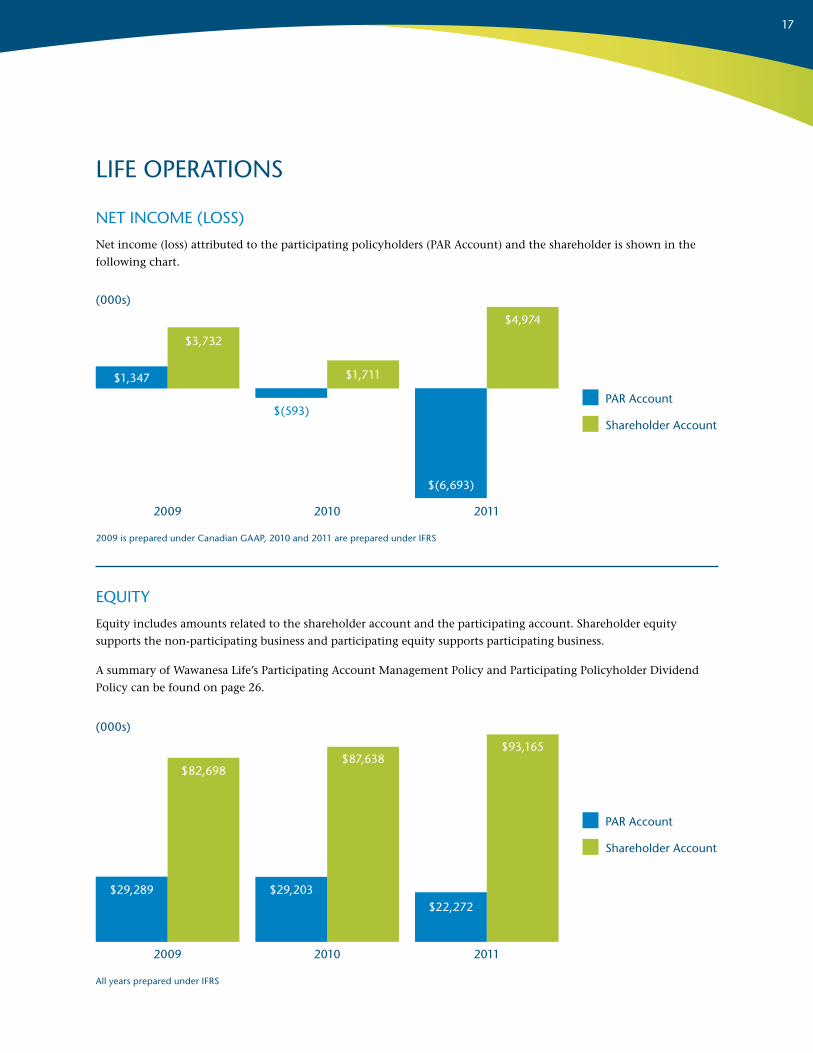

net IncoMe (loss)

Net income (loss) attributed to the participating policyholders (PAR Account) and the shareholder is shown in the

following chart.

(000s)

(000s)

2009

2009

2010

2010

2011

2011

par account

shareholder account

par account

shareholder account

$3,732

$1,347

$(6,693)

$4,974

$1,711

$(593)

equIty

Equity includes amounts related to the shareholder account and the participating account. Shareholder equity

supports the non-participating business and participating equity supports participating business.

A summary of Wawanesa Life’s Participating Account Management Policy and Participating Policyholder Dividend

Policy can be found on page 26.

$29,289

$82,698

$29,203

$87,638

$22,272

$93,165

lIFe operatIons

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

all years prepared under IFrs

18

total assets

Represents total assets managed by Wawanesa Life which include its general fund assets and policyholder

contributions to the segregated funds that are held separate and apart from the general fund assets.

(000s)

(000s)

2009

2009

2010

2010

2011

2011

general Fund assets

segregated Funds net assets

Bonds

stocks

other

$591,519

$139,896

$636,847

$167,842

$666,278

$163,636

InVestMents

Investments are managed in a conservative manner to provide steady, consistent investment income to support

the cash flow and liquidity needs of Wawanesa Life. The Board of Directors has approved the Investment Policy

Statement that sets out the guidelines followed by management to prudently manage these assets.

$436

,489

$59,

413

$38,

912

$70,

506

$34,

259

$73,

605

$30,

021

$476

,877

$519

,348

lIFe operatIons

all years prepared under IFrs

all years prepared under IFrs

19

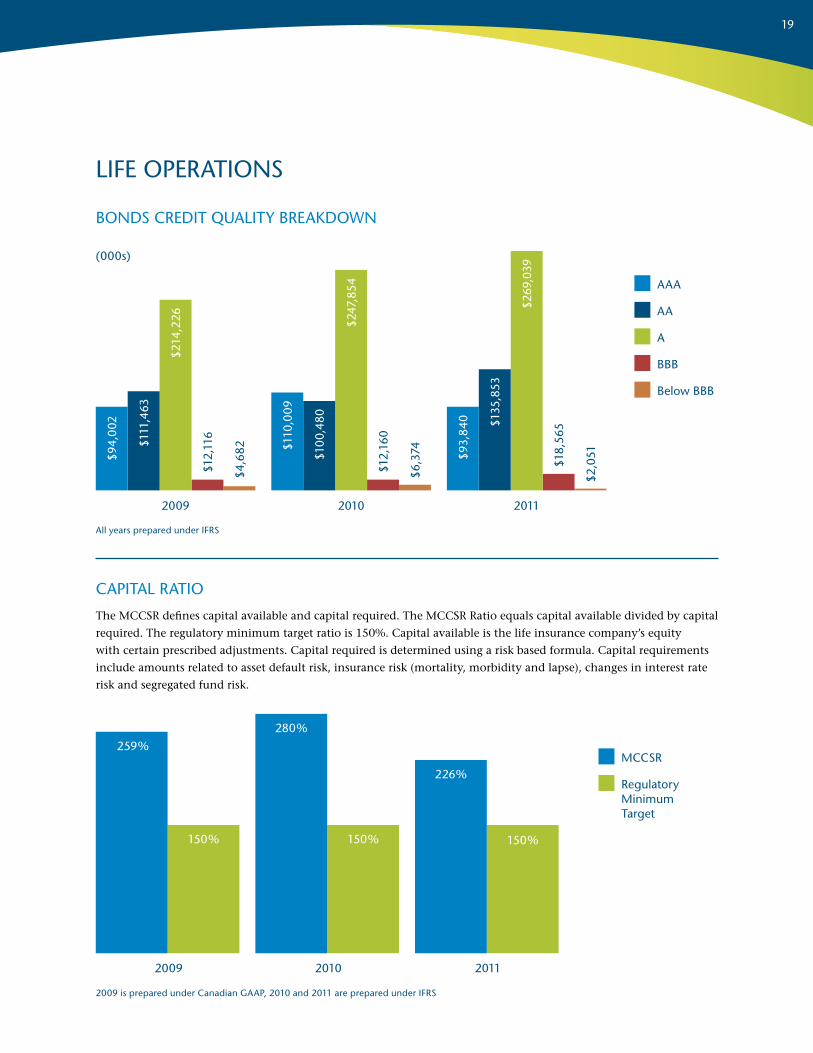

capItal ratIo

The MCCSR defines capital available and capital required. The MCCSR Ratio equals capital available divided by capital

required. The regulatory minimum target ratio is 150%. Capital available is the life insurance company’s equity

with certain prescribed adjustments. Capital required is determined using a risk based formula. Capital requirements

include amounts related to asset default risk, insurance risk (mortality, morbidity and lapse), changes in interest rate

risk and segregated fund risk.

BonDs creDIt qualIty BreakDoWn

aaa

aa

a

BBB

Below BBB

2009 2010 2011

$94,

002

$111

,463

$214

,226

$110

,009

$10

0,48

0

$247

,854

$93,

840 $1

35,8

53

$269

,039

$12,

116

$4,6

82

$12,

160

$6,

374

$18,

565

$2,0

51

2009 2010 2011

Mccsr

regulatory Minimum target

259%

150%

280%

150%

226%

150%

(000s)

lIFe operatIons

all years prepared under IFrs

2009 is prepared under canadian gaap, 2010 and 2011 are prepared under IFrs

20

February 21, 2012

to the shareholDer anD polIcyholDers oF the WaWanesa lIFe Insurance coMpany

The accompanying summary financial statements, which comprise the

summary balance sheets as at December 31, 2011 and 2010 and the

summary statements of operations for the years ended December 31,

2011 and 2010, are derived from the audited financial statements of

The Wawanesa Life Insurance Company for the years ended December 31,

2011 and 2010. We expressed an unmodified audit opinion on those

financial statements in our report dated February 21, 2012.

The summary financial statements do not contain all the disclosures

required by International Financial Reporting Standards. Reading

the summary financial statements, therefore, is not a substitute

for reading the audited financial statements of The Wawanesa Life

Insurance Company.

Management’s Responsibility for the Summary Financial Statements

Management is responsible for the preparation of a summary of the

audited financial statements in accordance with International Financial

Reporting Standards.

Auditor’s Responsibility

Our responsibility is to express an opinion on the summary financial

statements based on our procedures, which were conducted in accordance

with Canadian Auditing Standards (“CAS”) 810, “Engagements to Report

on Summary Financial Statements.”

Opinion

In our opinion, the summary financial statements derived from the

audited financial statements of The Wawanesa Life Insurance Company

for the years ended December 31, 2011 and 2010 are a fair summary of

those financial statements, in accordance with International Financial

Reporting Standards.

Chartered Accountants

Winnipeg, Manitoba

the WaWanesa lIFe Insurance coMpany

report oF the InDepenDent auDItor on the suMMary FInancIal stateMents

Incorporated July 7, 1960

Head Office

Wawanesa, Manitoba

Executive Office

400–200 Main Street

Winnipeg, Manitoba

oFFIcers anD ManageMent

Corporate

K. E. McCrea, CA, FLMI President and Chief Executive Officer

M. K. Nemeth, CA, FLMI, GBA Vice President and Chief Operating Officer

G. N. Bass, Q.C. Vice President, General Counsel and Secretary

I. R. MacDonald, FSA, FCIA Vice President and Actuary

C. R. Loeppky, BScCS Vice President, Information Services

T. L. Nelson, FLMI/M, CHRP, CIP Vice President, Human Resources

E. Elvebo, CA Manager, Corporate Reporting

P. M. Horncastle, CGA Controller

P. R. Mulaire, CMA, FCIP, CIA Manager, Internal Audit

K. J. Richtik, FSA, FCIA Manager, Actuarial Financial Reporting

Insurance Operations

G. G. Sadler, CLU, ChFC, CHS Director, Individual Sales and Marketing

M. M. Nolin, DDM, ALHC, ACS, AIAA Manager, Group Benefit Services

D. M. Smook Manager, National Group Sales and Marketing

D. I. Verwey Manager, Group Underwriting and Policy Administration

A. E. Waller, MBA, CFP, ChFC, CLU, FALU Manager, Individual Life Administration

Medical Director

Dr. R. B. Boyd, MD

21

February 21, 2012

to the shareholDer anD polIcyholDers oF the WaWanesa lIFe Insurance coMpany

I have valued the insurance contract liabilities of The Wawanesa Life

Insurance Company for its balance sheet at December 31, 2011 and

their change in the statement of operations for the year then ended

in accordance with accepted actuarial practice, including selection of

appropriate assumptions and methods.

In my opinion, the amount of insurance contract liabilities makes

appropriate provision for all policyholder obligations and the financial

statements fairly present the result of the valuation.

Ian R. MacDonald

Fellow, Canadian Institute of Actuaries

Winnipeg, Manitoba

the WaWanesa lIFe Insurance coMpany

appoInteD actuary’s reportregIonal oFFIces

Atlantic 1010 St. George Boulevard Moncton, New Brunswick

S. B. Brydges, CFP, CHS Regional Life Manager

Ontario 100–4110 Yonge Street Toronto, Ontario

B. I. Lang, RHU Regional Life Manager

R. J. Rowe, GBA Regional Group Manager

Western Manitoba 208–740 Rosser Avenue Brandon, Manitoba

G. L. C. Goymer, CFP, ChFC, CLU, CHS Regional Life Manager

Eastern Manitoba and NW Ontario 700–200 Main Street Winnipeg, Manitoba

J. A. Kien Regional Life Manager

T. A. McDowell Regional Group Manager

Saskatchewan 201–3501 8th Street East Saskatoon, Saskatchewan

205, 2631–28th Avenue Regina, Saskatchewan

G. F. M. Kurmey, FLMI Regional Life Marketing Representative

Northern Alberta 100, 8657–51st Avenue Edmonton, Alberta

L. P. J. Addison Regional Life Manager

S. Lambert Regional Group Manager

Southern Alberta 600, 708–11th Avenue S.W. Calgary, Alberta

B. A. Reid Galarnyk Regional Life Manager

British Columbia 310–1985 West Broadway Vancouver, British Columbia

S. F. Engmann Regional Life Manager

B. R. Wyne, MBA Regional Group Manager

22

As at December 31

2011 2010

(000s)

Assets

Cash and cash equivalents $ 30,281 $ 12,448

Investments 622,974 581,642

Other assets 13,023 42,757

General fund assets 666,278 636,847

Segregated funds net assets 163,636 167,842

Total assets $ 829,914 $ 804,689

Liabilities

Other liabilities $ 7,006 $ 6,188

Insurance contract liabilities 543,835 513,818

General fund liabilities 550,841 520,006

Segregated funds contract liabilities 163,636 167,842

Total liabilities 714,477 687,848

Equity 115,437 116,841

Total liabilities and equity $ 829,914 $ 804,689

the WaWanesa lIFe Insurance coMpany

suMMary Balance sheets

A complete set of audited financial statements are available at www.wawanesa.com

23

For the year ended December 31

2011 2010

(000s)

Net premiums and equivalents $ 109,376 $ 98,529

Net investment income 50,074 45,236

Total income 159,450 143,765

Net claims and benefits incurred 73,775 65,815

Net change in insurance contract liabilities 58,370 49,976

Expenses incurred 28,676 26,682

Total benefits and expenses 160,821 142,473

Income (loss) before income taxes (1,371) 1,292

Provision for income taxes 348 174

Net income (loss) for the year $ (1,719) $ 1,118

Net income (loss) for the year attributed to:

Shareholder $ 4,974 $ 1,711

Participating policyholders (6,693) (593)

$ (1,719) $ 1,118

the WaWanesa lIFe Insurance coMpany

suMMary stateMents oF operatIons

A complete set of audited financial statements are available at www.wawanesa.com

24

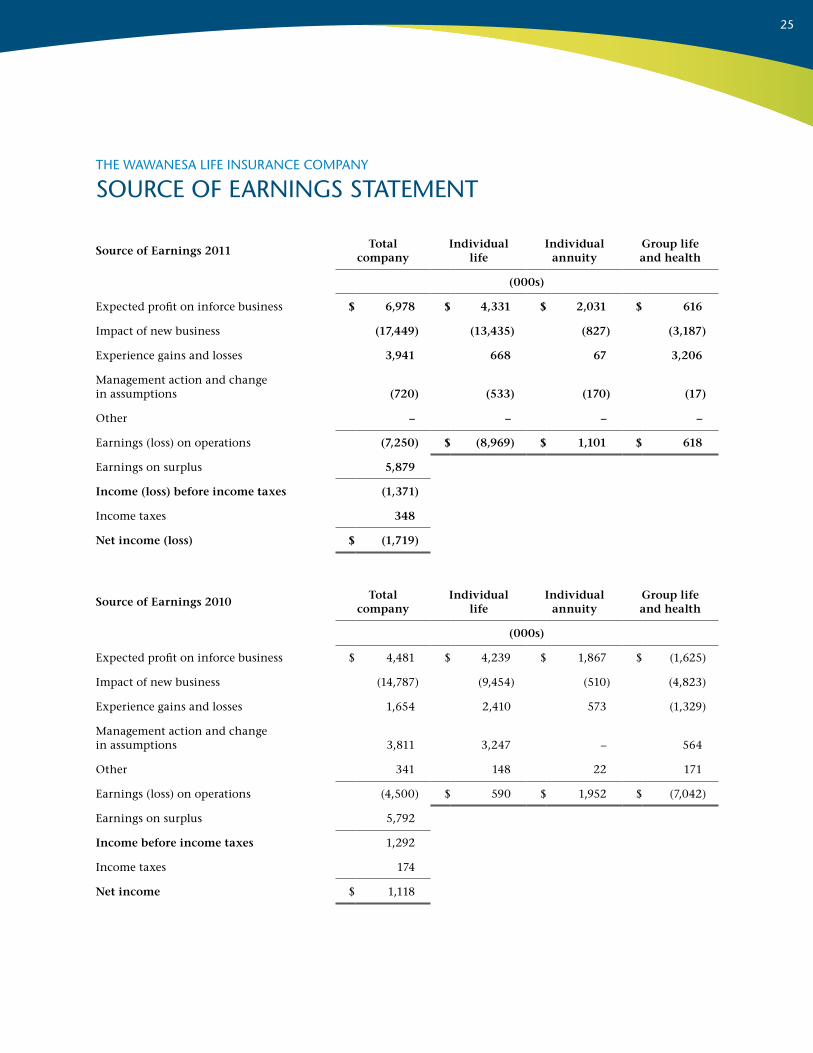

The Source of Earnings are attributable to one of the

following categories:

expecteD proFIt on InForce BusIness

This includes the release of the Provision for Adverse

Deviations (PFADs) plus the expected profits on

Segregated Funds. The release of the PFADs is the

profit arising on the inforce business if the expected

assumptions used in calculating the actuarial liabilities

are realized.

IMpact oF neW BusIness

This represents the overall loss during the first year

on new business. The PFADs in the actuarial liabilities

contribute to an overall initial loss on issuing new

business. These PFADs are anticipated to be released

into income in future years to the extent they are not

required to cover future adverse experience.

experIence gaIns anD losses

The experience gains result from items such as

investment returns, claims and expenses where the

actual experience during the year differs from the

expected experience assumed in the actuarial liabilities.

It also includes the amount the fee income generated

on Segregated Funds differs from expected.

ManageMent actIon anD changes In assuMptIons

This section includes specific management actions and

the impact of changes in assumptions used to calculate

actuarial liabilities.

earnIngs on surplus

This reflects the earnings on the surplus and capital of

the Company.

other

This represents all other sources of earnings not

included above.

the WaWanesa lIFe Insurance coMpany

source oF earnIngs stateMent

25

the WaWanesa lIFe Insurance coMpany

source oF earnIngs stateMent

Source of Earnings 2011Total

companyIndividual

lifeIndividual

annuityGroup life and health

(000s)

Expected profit on inforce business $ 6,978 $ 4,331 $ 2,031 $ 616

Impact of new business (17,449) (13,435) (827) (3,187)

Experience gains and losses 3,941 668 67 3,206

Management action and change in assumptions (720) (533) (170) (17)

Other – – – –

Earnings (loss) on operations (7,250) $ (8,969) $ 1,101 $ 618

Earnings on surplus 5,879

Income (loss) before income taxes (1,371)

Income taxes 348

Net income (loss) $ (1,719)

Source of Earnings 2010Total

companyIndividual

lifeIndividual

annuityGroup life and health

(000s)

Expected profit on inforce business $ 4,481 $ 4,239 $ 1,867 $ (1,625)

Impact of new business (14,787) (9,454) (510) (4,823)

Experience gains and losses 1,654 2,410 573 (1,329)

Management action and change in assumptions 3,811 3,247 – 564

Other 341 148 22 171

Earnings (loss) on operations (4,500) $ 590 $ 1,952 $ (7,042)

Earnings on surplus 5,792

Income before income taxes 1,292

Income taxes 174

Net income $ 1,118

A Participating Account is maintained in respect of the

Company’s participating business which is separate

from the Shareholder Account. Revenue and expenses

that are directly related to participating business are

recorded to the Participating Account. Allocation

methods are also used to record certain expense and

revenue items to the Participating Account.

The Expense Allocation Method is designed to allocate

expenses and taxes fairly and equitably between the

Participating Account and the Shareholder Account.

The Investment Income Allocation Method is

designed to allocate investment income fairly and

equitably between the Participating Account and the

Shareholder Account.

The Investment Policy Statement (IPS) governs the

investment activities of the Company. Assets have been

segmented into funds to facilitate managing assets with

liabilities. The IPS specifies the investment objectives,

investment risks, and management of these risks for

each of the funds.

Surplus exists in the Participating Account for the needs

of the current inforce business and future new business.

Surplus is managed to meet the continuing financial

stability of the Participating Account and to exceed any

minimum regulatory requirements.

Participating policyholders are eligible to receive

distributions from the Participating Account when

experience justifies their payment. The Board of

Directors determines the amount of dividends

to be paid in accordance with the Company’s

Dividend Policy.

The Company is allowed to transfer an amount from

the Participating Account to the Shareholder Account

each year as described in the Insurance Companies Act.

The Company intends to transfer an amount equal

to the lesser of 10% of the amount of the dividends

paid to the participating policyholders during the

year and the maximum permitted by the Insurance

Companies Act.

partIcIpatIng InDIVIDual lIFe Insurance

Participating Earnings are generated when collective

experience related to investment, mortality, lapse,

expenses and taxes is more favourable than assumed

in developing the premiums. The Company may

distribute a portion of the participating account

earnings to the participating policyholders. The

distribution is in the form of dividends payable to

the policyholders. The amount available to be paid

as dividends is determined based on various factors

including the Company’s earnings, any regulatory

requirements and the amount of surplus required

to ensure the continuing financial stability of the

Participating Account.

The dividend scale sets out a formula for the

allocation of distributable earnings to the participating

policies. The principle factors used to distribute

earnings are investment earnings, mortality, and

expense experience. The dividend scale allocates

distributable earnings among policies in the same

proportion as the policies are considered to have

contributed to distributable earnings. Dividends are

credited to the policies on their policy anniversary

date. The distribution of dividends is designed

to maintain reasonable equity between classes of

participating business.

Dividends are declared at the discretion of the Board

of Directors.

the WaWanesa lIFe Insurance coMpany

suMMary oF the partIcIpatIng account ManageMent polIcy*

suMMary oF the partIcIpatIng polIcyholDer DIVIDenD polIcy*

*Complete policies are available upon request

26

27

28

standing (l to r): e. J. Beale, D. g. unruh, M. e. northey, J. s. Mccallum, g. J. hanson, r. o. landry, k. l. Matchett, D. c. crewson seated (l to r): r. r. Bracken, k. e. Mccrea

BoarD oF DIrectors the Wawanesa Mutual Insurance company, Wawanesa general Insurance company and the Wawanesa life Insurance company

r. r. Bracken 1,2,3,4

chairman of the Board

e. J. Beale 2,3

D. c. crewson 1,2

g. J. hanson 3,4

r. o. landry 2,3

k. l. Matchett 1,4

J. s. Mccallum 3,4

k. e. Mccrea

M. e. northey 1,2

D. g. unruh 1,4

1. Member of the audit committee2. Member of the conduct review and corporate governance committee3. Member of the Investment committee4. Member of the human resources committee