volume 19 number 1 october 2016 rial opy -...

TRANSCRIPT

Volume 19 Number 1October 2016

PEFC Certified

This book has been produced entirely from sustainable papers that are accredited as PEFC compliant.

www.pefc.org

The Jo

urn

al of R

isk Volum

e 19 Num

ber 1 October 2016

■ Impact of nonstationarity on estimating and modeling empirical copulas of daily stock returns Marcel Wollschläger and Rudi Schäfer

■ Path-consistent wrong-way risk: a structural model approach Markus Hofer

■ Decomposition of portfolio risk into independent factors using an inductive causal search algorithm Brian D. Deaton

■ Optimal asset management for defined-contribution pension funds with default risk Shibo Bian, James Cicon and Yi Zhang

■ A fuzzy data envelopment analysis model for evaluating the efficiency of socially responsible and conventional mutual funds I. Baeza-Sampere, V. Coll-Serrano, B. M’Zali and P. Méndez-Rodríguez

The Journal of

Risk

JOR_19_1_Oct_2016.indd 1 30/09/2016 10:08

Tria

l Cop

y For all subscription queries, please call:

UK/Europe: +44 (0) 207 316 9300

USA: +1 646 736 1850 ROW: +852 3411 4828

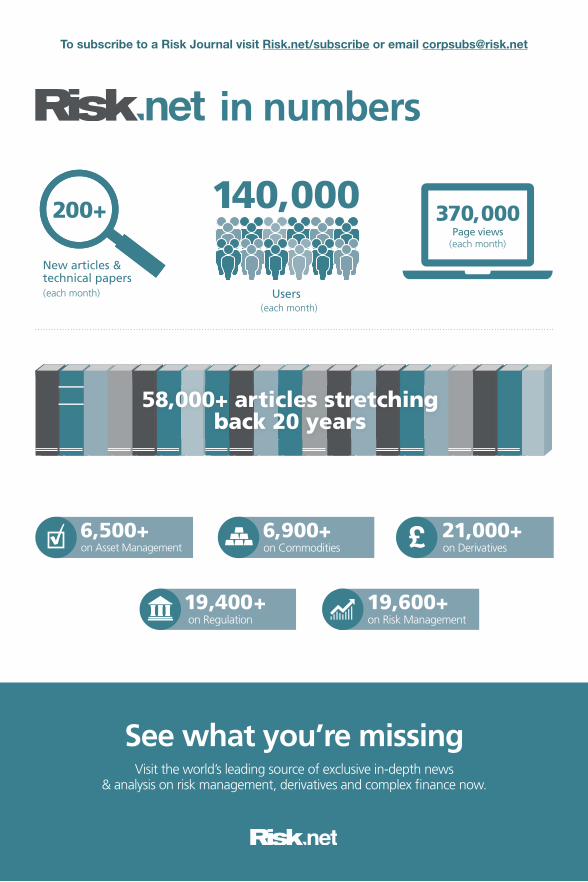

in numbers

140,000

Users

Page views

19,400+ on Regulation

6,900+ on Commodities

19,600+ on Risk Management

6,500+ on Asset Management

58,000+ articles stretching back 20 years

200+

New articles & technical papers

370,000

21,000+ on Derivatives £

Visit the world’s leading source of exclusive in-depth news & analysis on risk management, derivatives and complex fi nance now.

(each month)

(each month)

See what you’re missing

(each month)

RNET16-AD156x234-numbers.indd 1 21/03/2016 09:44

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

The Journal of RiskEDITORIAL BOARD

Editor-in-ChiefFarid AitSahlia University of Florida

Editor Emeritus and Chairman of the Editorial BoardStan Uryasev University of Florida

Associate EditorsCarlo Acerbi MSCI GroupAlper Atamturk University of California,

BerkeleyTuran G. Bali Georgetown UniversityJeremy Berkowitz University of HoustonPeter Carr Morgan Stanley

New York UniversityJon Danielsson London School of

EconomicsRobert F. Engle New York UniversityJohn Hull University of TorontoRobert Jarrow Cornell University

Paul H. Kupiec Federal Deposit InsuranceCorporation

François Longin ESSECElisa Luciano University of Torino &

Fondazione Collegio Carlo AlbertoNeil D. Pearson University of Illinois at

Urbana–ChampaignRiccardo Rebonato PIMCOTil Schuermann Oliver WymanRené M. Stulz Ohio State UniversityCasper G. De Vries Erasmus University

Rotterdam & Tinbergen Institute

SUBSCRIPTIONS

The Journal of Risk (Print ISSN 1465-1211 j Online ISSN 1755-2842) is published six times per yearby Incisive Risk Information Limited, Haymarket House, 28–29 Haymarket, London SW1Y 4RX,UK. Subscriptions are available on an annual basis, and the rates are set out in the table below.

UK Europe USRisk.net Journals £1945 €2795 $3095Print £890 €1265 $1595Risk.net Premium £2750 €3995 $4400

Academic discounts are available. Please enquire by using one of the contact methods below.

All prices include postage.All subscription orders, single/back issues orders, and changes of addressshould be sent to:

UK & Europe Office: Incisive Media (c/o CDS Global), Tower House, Sovereign Park,Market Harborough, Leicestershire, LE16 9EF, UK. Tel: 0870 787 6822 (UK),+44 (0)1858 438 421 (ROW); fax: +44 (0)1858 434958

US & Canada Office: Incisive Media, 55 Broad Street, 22nd Floor, New York, NY 10004, USA.Tel: +1 646 736 1888; fax: +1 646 390 6612

Asia & Pacific Office: Incisive Media, 20th Floor, Admiralty Centre, Tower 2,18 Harcourt Road, Admiralty, Hong Kong. Tel: +852 3411 4888; fax: +852 3411 4811

Website: www.risk.net/journal E-mail: [email protected]

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

The Journal of RiskGENERAL SUBMISSION GUIDELINES

Manuscripts and research papers submitted for consideration must be original workthat is not simultaneously under review for publication in another journal or otherpublication outlets. All articles submitted for consideration should follow strict aca-demic standards in both theoretical content and empirical results. Articles should beof interest to a broad audience of sophisticated practitioners and academics.

Submitted papers should follow Webster’s New Collegiate Dictionary for spelling,and The Chicago Manual of Style for punctuation and other points of style, apart froma few minor exceptions that can be found at www.risk.net/journal. Papers should besubmitted electronically via email to: [email protected]. Please clearlyindicate which journal you are submitting to.

You must submit two versions of your paper; a single LATEX version and a PDFfile. LATEX files need to have an explicitly coded bibliography included. All files mustbe clearly named and saved by author name and date of submission. All figures andtables must be included in the main PDF document and also submitted as separateeditable files and be clearly numbered.

All papers should include a title page as a separate document, and the full names,affiliations and email addresses of all authors should be included. A concise andfactual abstract of between 150 and 200 words is required and it should be includedin the main document. Five or six keywords should be included after the abstract.Submitted papers must also include an Acknowledgements section and a Declarationof Interest section. Authors should declare any funding for the article or conflicts ofinterest. Citations in the text must be written as (John 1999; Paul 2003; Peter and Paul2000) or (John et al 1993; Peter 2000).

The number of figures and tables included in a paper should be kept to a minimum.Figures and tables must be included in the main PDF document and also submittedas separate individual editable files. Figures will appear in color online, but willbe printed in black and white. Footnotes should be used sparingly. If footnotes arerequired then these should be included at the end of the page and should be no morethan two sentences. Appendixes will be published online as supplementary material.

Before submitting a paper, authors should consult the full author guidelines at:

http://www.risk.net/static/risk-journals-submission-guidelines

Queries may also be sent to:The Journal of Risk, Incisive Media,Haymarket House, 28–29 Haymarket, London SW1Y 4RX, UKTel: +44 (0)20 7004 7531; Fax: +44 (0)20 7484 9758E-mail: [email protected]

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

The Journal of

Risk

The journalThis international refereed journal publishes a broad range of original research papersthat aim to further develop understanding of financial risk management. As the onlypublication devoted exclusively to theoretical and empirical studies in financial riskmanagement, The Journal of Risk promotes far-reaching research on the latest innova-tions in this field, with particular focus on the measurement, management and analysisof financial risk.

The Journal of Risk is particularly interested in papers in the following areas.

� Risk management regulations and their implications.

� Risk capital allocation and risk budgeting.

� Efficient evaluation of risk measures under increasingly complex and realisticmodel assumptions.

� The impact of risk measurement on portfolio allocation.

� Theoretical development of alternative risk measures.

� Hedging (linear and nonlinear) under alternative risk measures.

� Financial market model risk.

� Estimation of volatility and unanticipated jumps.

� Capital allocation.

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

The Journal of Risk Volume 19/Number 1

CONTENTS

Letter from the Editor-in-Chief vii

RESEARCH PAPERSImpact of nonstationarity on estimating and modeling empirical copulasof daily stock returns 1Marcel Wollschläger and Rudi Schäfer

Path-consistent wrong-way risk: a structural model approach 25Markus Hofer

Decomposition of portfolio risk into independent factors using aninductive causal search algorithm 43Brian D. Deaton

Optimal asset management for defined-contribution pension funds withdefault risk 63Shibo Bian, James Cicon and Yi Zhang

A fuzzy data envelopment analysis model for evaluating the efficiencyof socially responsible and conventional mutual funds 77I. Baeza-Sampere, V. Coll-Serrano, B. M’Zali and P. Méndez-Rodríguez

Editor-in-Chief: Farid AitSahlia Subscription Sales Manager: Aaraa JavedPublisher: Nick Carver Global Key Account Sales Director: Michelle GodwinJournals Manager: Dawn Hunter Composition and copyediting: T&T Productions LtdEditorial Assistant: Carolyn Moclair Printed in UK by Printondemand-Worldwide

©Copyright Incisive Risk Information (IP) Limited, 2016. All rights reserved. No parts of this publicationmay be reproduced, stored in or introduced into any retrieval system, or transmitted, in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise without the prior written permission of thecopyright owners.

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

LETTER FROM THE EDITOR-IN-CHIEF

Farid AitSahliaWarrington College of Business Administration,University of Florida

This issue of The Journal of Risk contains papers that focus on modeling depend-ence via copulas and on identifying independent risk factors for better portfolio riskattribution. It also includes an extension of a classical portfolio selection problem toaccount for bond default, as well as an approach to compare mutual funds on the basisof hard-to-measure social and environmental criteria.

In the first paper of this issue, “Impact of nonstationarity on estimating and model-ing empirical copulas of daily stock returns”, Marcel Wollschläger and Rudi Schäferconduct an empirical study that systematically distinguishes between local and globalbehavior of correlated time series. Their findings suggest copulas that best captureasymmetry in the tails when dependence is not stationary, especially during periodsof high volatility.

In “Path-consistent wrong-way risk: a structural model approach”, the second paperin the issue, Markus Hofer considers wrong way risk, which is present when theprobability of default of a counterparty increases with the value of a credit portfolio.Here, too, the author uses copulas to capture dependence in a way that is useful forcredit valuation adjustment, satisfying a path-consistent weight requirement, whichin turn provides a framework for model calibration.

In our third paper, “Decomposition of portfolio risk into independent factors usingan inductive causal search algorithm”, Brian Deaton applies a search method to iden-tify the set of independent factors affecting the returns of a portfolio.As a consequence,risk attribution and decomposition in portfolio strategies is better conducted.

The issue concludes with two short notes.In “Optimal asset management for defined-contribution pension funds with default

risk”, Shibo Bian, James Cicon and Yi Zhang extend the classical portfolio selectionproblem involving a bond and a stock in the presence of a risk-free rate. They provideclosed-form solutions for non-self-financing strategies in the presence of defaultablebonds. They show, in particular, that investment in the defaultable bond increases withthe jump-risk premium and time to maturity.

In the second note, “A fuzzy data envelopment analysis model for evaluating theefficiency of socially responsible and conventional mutual funds”, I. Baeza-Sampere,V. Coll-Serrano, B. M’zali and P. Méndez-Rodríguez show how data envelopmentanalysis can be used to assess the performance of mutual funds along a dimensionthat goes beyond standard measures: namely, that of a social and environmental index,for which fuzzy set theory is useful given the difficulty in measuring the index inputs.

www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Journal of Risk 19(1), 1–23DOI: 10.21314/JOR.2016.342

Research Paper

Impact of nonstationarity on estimating andmodeling empirical copulas of dailystock returns

Marcel Wollschläger1,2 and Rudi Schäfer1,3

1Faculty of Physics, University of Duisburg-Essen, Lotharstrasse 1, 47048 Duisburg, Germany2Chair for Energy Trading and Finance, University of Duisburg-Essen, Universitätsstrasse 12,45141 Essen, Germany; email: [email protected] and Prototyping, Arago GmbH, Eschersheimer Landstraße 526–532,60433 Frankfurt am Main, Germany; email: [email protected]

(Received July 3, 2015; accepted November 30, 2015)

ABSTRACT

All too often, measuring statistical dependencies between financial time series isreduced to the study of a linear correlation coefficient. However, this may not cap-ture all facets of reality. We study empirical dependencies of daily stock returns bytheir pairwise copulas. Here, we investigate in particular the extent to which the non-stationarity of financial time series affects both the estimation and the modeling ofempirical copulas. We estimate empirical copulas from the nonstationary, originalreturn time series and stationary, locally normalized ones, and we are thereby ableto explore the empirical dependence structure on two different scales: globally andlocally. Additionally, the asymmetry of the empirical copulas is emphasized as a fun-damental characteristic. We compare our empirical findings with a single Gaussiancopula, with a correlation-weighted average of Gaussian copulas, with the K-copuladirectly addressing the nonstationarity of dependencies as a model parameter andwith the skewed Student t -copula. The K-copula covers the empirical dependence

Corresponding author: M. Wollschläger Print ISSN 1465-1211 j Online ISSN 1755-2842Copyright © 2016 Incisive Risk Information (IP) Limited

1

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

2 M. Wollschläger and R. Schäfer

structure on the local scale most adequately, whereas the skewed Student t -copulabest captures the asymmetry of the empirical copula found on the global scale.

Keywords: copulas; financial time series; nonstationarity; asymmetry; multivariate mixture;K-copula.

1 INTRODUCTION

The study of empirical dependencies of financial time series is not only important forrisk management and portfolio optimization, but a prerequisite for a deeper under-standing. It is common practice to reduce the question of statistical dependence to thestudy of the Pearson correlation coefficient; the most notable works in this directioninclude Markowitz (1952), Martens and Poon (2001), Pelletier (2006) and Engle andColacito (2006). The correlation coefficient, however, only measures the degree oflinear dependence between two random variables. Nonlinear dependencies or morecomplicated dependence structures are not captured appropriately. Here, we choosea copula approach to investigate the full range of statistical dependencies. In contrastwith the multivariate distribution, which also contains the marginal distributions, thecopula introduced by Sklar (1973) transforms these marginal distributions to uniformdistributions. This allows for statistical dependencies to be studied directly. Copulasfind application in many fields, eg, civil engineering (Kilgore and Thompson 2011),medicine (Onken et al 2009), climate and weather research (Schölzel and Friederichs2008) and the generation of random vectors (Strelen 2009). In finance, copulas areprimarily used in risk and portfolio management (see, for example, Brigo et al 2010;Embrechts et al 2003, 2002; Low et al 2013; McNeil et al 2005; Meucci 2011; Rosen-berg and Schuermann 2006). A compact survey of the growing literature of copulamodels by Patton (2012a,b) provides more detail. For a more general introduction tocopulas, the reader is referred to Joe (1997) and Nelsen (2006).

In all these contexts, easily tractable analytical copulas are used as a building blockin the multivariate distributions. Empirical studies that do not assume an analyticaldependence structure a priori are few and far between (see, for example, Münnixet al 2012; Ning et al 2008). This is where our contribution fits in. We study empir-ical dependencies of daily returns of S&P 500 stocks. To achieve a good statisticalsignificance for the estimation of a complete copula, a very large amount of data isnecessary. Therefore, we restrict ourselves to the bivariate case and average over manypairwise copulas. In addition, we consider a rather long time horizon. In consideringa long time horizon we are confronted with two problems: the nonstationarity of theindividual time series and their dependencies. The former (ie, time-varying trends andvolatilities) must be taken into account when we estimate empirical copulas. To thisend we apply the local normalization to the empirical return time series, which rids

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 3

them of nonstationary trends and volatilities. The local normalization was introducedby Schäfer and Guhr (2010) and yields stationary, standard normally distributed timeseries while preserving dependencies between different time series. In particular, itallows us to study the empirical dependence structure on a local scale, whereas thecopula of original returns reveals the dependence structure on a global scale.

We compare our empirical findings with different analytical copulas, addressing inparticular the question of how far the assumption of a Gaussian dependence structuremay carry. Since we average over many stock pairs, it would be naive to assumethat the resulting average pairwise copula could be described by a single Gaussiancopula where only the average correlation is included.And, indeed, we find rather pooragreement, especially on the global scale.A correlation-weighted average of Gaussiancopulas, which takes into account the different pairwise correlations, provides only aslightly better description. We have to consider the time-varying dependencies as well.These can be addressed by an ensemble average over random correlations (see Schmittet al 2013). This ansatz yields good agreement for multivariate return distributions.Here, we derive the pairwise K-copula resulting from this random matrix approachand compare it with our empirical findings. Overall, we find rather good agreement,especially on the local scale. However, the empirical copulas show an asymmetry inthe tail dependence, which our model cannot account for. As a model that allows foran asymmetry in the dependence structure, the skewed Student t -distribution, firstintroduced by Hansen (1994), and its corresponding copula, introduced by Demartaand McNeil (2005), are steadily gaining popularity, particularly with regard to creditrisk management (see, for example, Dokov et al 2008; Hu and Kercheval 2006) andthe study of asymmetric dependencies (see, for example, Sun et al 2008). On theglobal scale, where the asymmetry is more pronounced, the skewed Student t -copulayields improved agreement with our empirical copulas.

The paper is structured as follows. In Section 2, we briefly present our data setand the theoretical background for the local normalization, correlations and copulas.Additionally, we derive the K-copula.We present our results in Section 3 and concludein Section 4.

2 DATA SET AND THEORETICAL BACKGROUND

2.1 Prices and returns

In our empirical study, we consider the daily closing prices of stocks in the S&P 500stock index, which have been adjusted for splits and dividends. Our observation periodranges from March 1, 2006 to December 31, 2012. The data is obtained from http://finance.yahoo.com/. From the price time series we calculate the returns (later referred

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

4 M. Wollschläger and R. Schäfer

to as “original” returns) as

rk.t/ D Sk.t C �t/ � Sk.t/

Sk.t/; (2.1)

where Sk.t/ is the price at time t of a stock k and �t D 1 trading day. We finallyarrive at T D 1760 daily returns for K D 460 stocks that were continuously tradedand listed in the S&P 500 during the entire observation period. It is well known thatoriginal returns show strongly nonstationary behavior.

2.2 Local normalization

To correct for nonstationary trends and volatilities in the original returns, we employa method called local normalization, introduced by Schäfer and Guhr (2010). Here,the locally normalized return is defined as

�k.t/ D rk.t/ � �k.t/

�k.t/; (2.2)

with local average �k.t/ and local volatility �k.t/ of a stock k, which are bothestimated over a time window of the preceding thirteen trading days. As has beenshown in Schäfer and Guhr (2010), this interval of thirteen trading days for the localaverage and volatility yields the best approximation of stationary, standard normallydistributed time series.

2.3 Correlations

To measure the statistical dependence of two random variables X , Y , the Pearsoncorrelation coefficient,

CX;Y D Cov.X; Y /

�X �Y

; (2.3)

is often considered, where Cov.X; Y / is the covariance of both random variables and�X , �Y are their respective standard deviations. In our case, the random variables X ,Y are returns rk , rl . Nonstationarity of the individual time series is a fundamentalproblem for the estimation of correlation coefficients. For return time series, the time-varying volatilities lead to estimation errors in (2.3) (see, for example, Münnix et al2012; Schäfer and Guhr 2010). This can be taken into account by the local normaliza-tion introduced above. As already mentioned in Section 1, the correlation coefficientonly measures the linear dependence between two random variables. Therefore, itis not well suited to measuring arbitrary dependencies. For the latter purpose weconsider copulas in the following section.

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 5

2.4 Definition of copulas

In our short introduction to copulas, we shall confine ourselves to the bivariate case,since we only study empirical pairwise copulas. All the information about the stat-istical dependence of two random variables is certainly contained in their bivariatedistribution. However, it is difficult to compare bivariate distributions if the marginaldistributions are not the same for all random variables. To achieve comparability wecan transform each marginal distribution into a uniform distribution. The bivariatedistribution of such transformed variables is then called a copula.

We consider two continuous random variables X , Y with a joint probability densityfunction fX;Y .x; y/. Then, the joint cumulative distribution function is given by

FX;Y .x; y/ DZ x

�1dx0

Z y

�1dy0 fX;Y .x0; y0/: (2.4)

We denote the marginal distribution functions by FX .x/, FY .y/, and the corre-sponding probability density functions by

fX .x/ D d

dxFX .x/; fY .y/ D d

dyFY .y/:

According to Sklar (1973), we define the copula by

FX;Y .x; y/ D CopX;Y .FX .x/; FY .y//

() CopX;Y .u; v/ D FX;Y .F �1X .u/; F �1

Y .v//; (2.5)

where we used the transformations u D FX .x/, v D FY .y/, and F �1X , F �1

Y indicatethe inverse marginal distribution functions, also called quantile functions. Accordingto the usual definition of a probability density function, the copula density is definedby the partial derivatives with respect to u and v:

copX;Y .u; v/ D@2CopX;Y .u; v/

@u@v

@F �1Y .v/

@v

D @2FX;Y .x; y/

@x@y

ˇ̌ˇ̌xDF �1

X.u/

yDF �1Y

.v/

@F �1X .u/

@u

D fX;Y .x; y/

fX .x/fY .y/

ˇ̌ˇ̌xDF �1

X.u/

yDF �1Y

.v/

; (2.6)

where we used the inverse function rule in the last step.

2.5 Empirical pairwise copula

In order to calculate the empirical pairwise copula of two return time series rk , rl ,we have to transform their marginal distributions to uniformity. We then refer to the

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

6 M. Wollschläger and R. Schäfer

transformed time series as u D uk , v D ul . To achieve uniform distributed timeseries, we utilize the empirical distribution function

uk.t/ D Fk.rk.t// D 1

T

TX�D1

1frk.�/ 6 rk.t/g � 1

2T; (2.7)

where 1 is the indicator function. The term �12

in definition (2.7) simply ensures thatall values uk.t/ lie strictly in the interval .0; 1/. Finally, we arrive at the empiricalpairwise copula density as a two-dimensional histogram of data pairs .uk.t/; ul.t//.

2.6 Bivariate Gaussian copula

The Gaussian copula is the dependence structure that arises from a normal distribution.We consider two random variables X , Y , which follow a joint normal distributionwith correlation coefficient c. The bivariate Gaussian copula is then given by

CopGc .u; v/ D ˚c.˚�1.u/; ˚�1.v//; (2.8)

where ˚c describes the cumulative distribution function of a bivariate standard normaldistribution, and ˚�1 describes the inverse cumulative distribution function of aunivariate standard normal distribution:

˚c.x; y/ DZ x

�1dx0

Z y

�1dy0 1

2�p

1 � c2exp

�� .x0/2 � 2cx0y0 C .y0/2

2.1 � c2/

�;

(2.9)

˚.x/ DZ x

�1

1p2�

exp

�� .x0/2

2

�dx0: (2.10)

Partial differentiation yields the bivariate Gaussian copula density,

copGc .u; v/ D 1p

1 � c2exp

��c2˚�1.u/2 � 2c ˚�1.u/˚�1.v/ C c2˚�1.v/2

2.1 � c2/

�:

(2.11)In Figure 1, we show as an example two Gaussian copula densities copG

c .u; v/ for apositive and a negative correlation c, respectively. Here, we can distinguish the inher-ently symmetric character as a fundamental property. Gaussian copula densities withpositive correlations describe strong dependencies between events in the same tail ineach marginal distribution, while negative correlations describe strong dependenciesbetween events in the opposite tails.

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 7

FIGURE 1 Gaussian copula density copGc .u; v/ for different correlations c: (a) c D 0.8 and

(b) c D �0.5.

(a) (b)

2.7 Bivariate K -copula

Correlations between financial time series are time dependent (see, for example, Cap-piello et al 2006; Engle 2002; Münnix et al 2012; Schäfer and Guhr 2010; Tse andTsui 2002). To take this empirical fact into account, we consider a random matrixmodel, introduced by Schmitt et al (2013), which assumes, for each return vec-tor r.t/ D .r1.t/; : : : ; rK.t// at each time t D 1; : : : ; T , a multivariate normaldistribution

g.r.t/; ˙t / D 1pdet.2�˙t /

exp

��r�.t/˙�1

t r.t/

2

�(2.12)

with a time-dependent covariance matrix ˙t . Each ˙t is then modeled by a randommatrix ˙t ! AA�=N drawn from a Wishart distribution (see Wishart 1928). To thisend we choose a multivariate normal distribution,

w.A; ˙/ D 1

detN=2.2�˙/exp

�� tr A�˙�1A

2

�; (2.13)

for the matrix elements of A, which fluctuate around the empirical average covariancematrix ˙ D h˙t itD1;:::;T . The distribution of a sample of return vectors r is then givenby a multivariate normal–Wishart mixture: we are averaging a multivariate normaldistribution over an ensemble of Wishart-distributed covariances, which finally results

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

8 M. Wollschläger and R. Schäfer

in a K-distribution,

hgi.r; ˙; N / DZ

dŒA� g

�r;

1

NAA�

�w.A; ˙/

D 1

2N=2C1� .N=2/p

det.2�˙=N /

K.K�N /=2.p

N r�˙�1r/p

N r�˙�1r.K�N /=2

D 1

.2�/K� .N=2/p

det ˙

�Z 1

0

dz z.N=2/�1e�z

r�N

z

K

exp

�� N

4zr�˙�1r

�; (2.14)

whereR

dŒA� denotes the integral over all matrix elements of A, andK� is the modifiedBessel function of the second kind, of order �. The K-distribution (2.14) contains onlytwo parameters: the empirical average covariance matrix ˙ , and a free parameter N ,which characterizes the fluctuations of covariances around the empirical average ˙ .In this manner, the empirically observed nonstationarity of covariances enters directlyinto the random matrix model. Note that the K-distribution (2.14) is a special case ofthe multivariate generalized hyperbolic distribution (see, for example, Aas and Haff2006; Browne and McNicholas 2014; McNeil et al 2005; Necula 2009; Schmidt et al2006; Socgnia and Wilcox 2014; Vilca et al 2014).

By considering the K-distribution (2.14) for the bivariate case, we can now derivethe bivariate K-copula density via (2.6). In our case, the probability density functionis the bivariate K-distribution, fX;Y .x; y/ D hgi.r; ˙; N / with K D 2. Since thecopula density is independent of the marginal distributions, we can choose the standarddeviations �X D �Y D 1, leading to the covariance matrix

˙ D

�2X �X�Y c

�X�Y c �2Y

!D

1 c

c 1

!; (2.15)

which is now merely a correlation matrix with the empirical average correlationcoefficient c. Thus, the parameter N simply characterizes the fluctuation strength ofthe correlations around their mean value. The smaller the value of N , the larger thefluctuations. In the limit N ! 1 the fluctuations vanish and we arrive at a normaldistribution and a Gaussian copula, respectively. The marginal probability densityfunctions of the K-distribution (2.14) are identical (fX .�/ D fY .�/) with

fX .x/ DZ 1

�1dy fX;Y .x; y/

D 1

� .N=2/

Z 1

0

dz z.N=2/�1e�z

rN

4�zexp

�� N

4zx2

�; (2.16)

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 9

FIGURE 2 K-copula densities copKc;N

.u; v/ for average correlation c and parameter N :(a) c D 0, N D 5; (b) c D 0.2, N D 4.

(a) (b)

and the marginal cumulative distribution functions, FX .�/ D FY .�/, with

FX .x/ DZ x

�1d� fX .�/

D 1

� .N=2/

Z 1

0

dz z.N=2/�1e�z

Z x

�1d�

rN

4�zexp

�� N

4z�2

�; (2.17)

have to be calculated and inverted numerically. Insertion into (2.6) then yields the K-copula density copK

c;N .u; v/. For illustration, Figure 2 shows the K-copula densityfor an average correlation c D 0 and N D 5 on the one hand, and for c D 0:2 andN D 4 on the other. We observe that the K-copula density contains both positive andnegative correlations, in contrast to the Gaussian copula density. In particular, negativecorrelations are also covered if the average correlation c is positive but the fluctuationsaround it are large enough. However, the K-copula density is still symmetric withrespect to the facing corners.

2.8 Bivariate skewed Student t-copula

We consider a bivariate skewed Student t -distributed random variable Z D .X; Y /

represented by the normal mean–variance mixture

Z D � C �W C Qp

W ; (2.18)

where � D .�1; �2/ is a location parameter vector; W � IG.�=2; �=2/ follows aninverse gamma distribution with � degrees of freedom; Q � N.0; ˙/ is independent

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

10 M. Wollschläger and R. Schäfer

of W and drawn from a bivariate normal distribution with zero mean and covariancematrix ˙ ; and � D .�1; �2/ is the skewness parameter vector. Since we are aimingat deriving a skewed Student t -copula density from its corresponding distributionfollowing (2.6), we are able to drop the location parameter vector � in the stochasticrepresentation (2.18), ie, � D 0, and set the standard deviations to 1 such that ˙

conforms to the correlation matrix (2.15) again. In this case, the bivariate skewedStudent t probability density function reads

fZ .z/ D 1

2�=2� .�=2/��p

det ˙

exp.z�˙�1�/

.1 C .z�˙�1z=�//�=2C1

� K�=2C1.p

.� C z�˙�1z/��˙�1�/

.p

.� C z�˙�1z/��˙�1�/�.�=2C1/; (2.19)

where K� is the modified Bessel function of the second kind, of order �. The univariatemarginal probability density functions are identical (fX .�/ D fY .�/) with

fX .x/ D 1

2.1��/=2� .�=2/p

��p

det ˙

exp.x�1/

.1 C .x2=�//.�C1/=2

� K.�C1/=2.p

.� C x2/�21 /

.p

.� C x2/�21 /�.�C1/=2

; (2.20)

and the marginal cumulative distribution functions, FX .�/ D FY .�/, with

FX .x/ DZ x

�1d� fX .�/; (2.21)

have to be calculated and inverted numerically. Bringing it all together correspondingto (2.6) with fX;Y .x; y/ D fZ .z/ then yields the bivariate skewed Student t -copuladensity: copt

c;�;�.u; v/. In the limit � ! 1 we obtain the Gaussian copula density.

3 EMPIRICAL RESULTS AND MODEL COMPARISON

In Section 3.1 we present the empirical copula densities for original returns andlocally normalized returns, respectively. In Section 3.2 we discuss the asymmetryin the tails of the empirical copula densities in more detail. We then compare theempirical copulas to the Gaussian copula with mean correlation in Section 3.3, to acorrelation-weighted Gaussian copula in Section 3.4, to the K-copula in Section 3.5and to the skewed Student t -copula in Section 3.6.

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 11

FIGURE 3 Empirical pairwise copula densities for (a) original returns, cop(glob).u; v/, and(b) locally normalized returns, cop(loc).u; v/.

(a) (b)

3.1 Empirical copula densities

We consider empirical pairwise copula densities averaged over all K.K � 1/=2 stockpairs

cop.u; v/ D 2

K.K � 1/

KXk;lD1;l>k

copk;l.u; v/; (3.1)

where copk;l.u; v/ is calculated as a two-dimensional histogram of the data pairs.uk.t/; ul.t//, according to (2.7). For the bin size of these histograms we choose�u D �v D 1=20. In the following, we denote the empirical copula density bycop(glob).u; v/ for original returns, and by cop(loc).u; v/ for locally normalized returns.As mentioned above, the main difference between these two cases is the considerationof nonstationarity: the original returns exhibit time-varying trends and volatilities;thus, we might argue the return time series are nonstationary. The locally normalizedreturns, on the other hand, show stationary behavior. We compare the results forboth cases because each has its merits. The copula for the original returns providesthe statistical dependence over the full time horizon, ie, on a global scale, while thecopula for the locally normalized returns reveals the statistical dependence on a localscale.

In Figure 3, we compare the empirical copula densities. At first sight, the depend-ence structure seems very similar for both cases. Deviations exist mainly in the cor-ners. Overall, the statistical dependence is preserved rather well when we strip thetime series from time-varying trends and volatilities. For the local normalization,

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

12 M. Wollschläger and R. Schäfer

Schäfer and Guhr (2010) showed that correlations are preserved under this proce-dure. Apparently, this also holds for the copula to some degree. For the originalreturns, the two peaks in the corners are higher. This can be explained as follows:the returns of periods with high volatility are more likely to end up in the lowest orhighest quantile, ie, uk.t/ and ul.t/ are close to 0 or 1. Therefore, periods with highvolatility contribute strongly to the corners of this copula. Since high volatility typi-cally coincides with strong correlations in the market, the corners exhibit a strongerdependence.

Qualitatively, the empirical results resemble Gaussian copula densities except forthe corners, where an asymmetry is observed. This empirical asymmetry implies thatlarge negative returns of two stocks show stronger dependence than large positivereturns. Although the asymmetry cannot be captured either by the Gaussian copula, aGaussian mixture or by the K-copula, we shall investigate how well these analyticalcopulas can approximate the overall dependence structure of empirical data. In addi-tion, we shall compare our empirical copulas to the skewed Student t -copula, whichis able to model asymmetries in the dependence structure. First, however, we take acloser look at the empirical asymmetry of the tail dependence itself.

3.2 Asymmetry of the tail dependence

We now elaborate on the features of the empirical copula densities. Their essentialcharacteristic is the asymmetry between the lower–lower and upper–upper corners: thedependence between large negative returns is always stronger than that between largepositive returns. Consequently, we observe a stronger dependence between coincidingdownside movements than between coinciding upside movements. In other words, wedistinguish an asymmetry between the bearish and bullish markets. This asymmetryis particularly evident for the original returns. Ang and Chen (2002), studying thedependence between US stocks and the US market, observed the same asymmetry incorrelation.

To quantify this empirical asymmetry, we estimate the tail dependence by integrat-ing over the 0:2 � 0:2 area in all four corners for each of the K.K � 1/=2 empiricalpairwise copula densities. We obtain the tail-dependence asymmetries by subtractingthe integrated areas in the opposite corners of the empirical copula densities:

pk;l DZ 1

0:8

du

Z 1

0:8

dv copk;l.u; v/ �Z 0:2

0

du

Z 0:2

0

dv copk;l.u; v/; (3.2)

qk;l DZ 0:2

0

du

Z 1

0:8

dv copk;l.u; v/ �Z 1

0:8

du

Z 0:2

0

dv copk;l.u; v/: (3.3)

We call pk;l the positive tail-dependence asymmetry, and qk;l the negative tail-dependence asymmetry. The histograms of these tail-dependence asymmetries,

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 13

FIGURE 4 Histograms of the tail-dependence asymmetries.

0.02

–0.03 2

20

40

60

80

100

120

–0.03

–0.03 –0 01 0.02

20

00

0

40

60

80

100

120

40

60

80

100

120

0

40

60

80

100

120

f(p kl

(glo

b))

f(q kl

(glo

b))

f(p kl

(loc)

)

(ffq kl

(loc)

)

pklp (glob) qkl(glob)

pklp qkl

(a)

(c)

(b)

(d)

(a), (c) Asymmetry for the positive tail dependence, pk;l . (b), (d) Asymmetry for the negative tail dependence, qk;l .(a), (b) Original returns. (c), (d) Locally normalized returns.

f .pk;l/ and f .qk;l/, respectively, are shown in Figure 4 for both data sets. While thenegative tail-dependence asymmetries qk;l are centered around zero for both originaland locally normalized returns, we observe a distinct negative offset for the positivetail-dependence asymmetries pk;l . Hence, on average there is no asymmetry in thenegative tail dependence, ie, between coinciding large positive and large negativemovements, but there is an asymmetry in the positive tail dependence, ie, betweencoinciding large negative movements and coinciding large positive movements. Wenotice additionally that the locally normalized returns show a much weaker asym-metry in the positive tail dependence than the original returns. This empirical findingcan be interpreted as follows: for the original return time series, events in the tailsof the distribution reflect periods of high volatility. And since high volatility oftenoccurs simultaneously in most stocks, the tail dependence also reflects these periodsin particular. In contrast, the locally normalized returns are stationary with a constantvolatility of 1. Therefore, the tail dependence in this case reflects the average behaviorover the whole time period. Thus, our empirical results imply that the asymmetry inthe tail dependence is not stationary, but it is particularly strong in periods with high

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

14 M. Wollschläger and R. Schäfer

FIGURE 5 Differences in Gaussian copula densities.

(a)

(c)

(b)

(d)

(a), (c) Gaussian copula densities copGc .u; v/. (b), (d) Differences between the empirical copula density and the

Gaussian copula density, cop(glob).u; v/ � copGc .u; v/ and cop(loc).u; v/ � copG

c .u; v/, respectively. (a), (b) Originalreturns, Nc(glob) D 0.44. (c), (d) Locally normalized returns, Nc(loc) D 0.39.

volatility. In fact, periods with high volatility coincide both with strong correlationsand strong asymmetry in the dependence structure.

3.3 Comparison with the Gaussian copula

At first sight, our empirical copula densities seem to roughly resemble the Gaus-sian copula. How good is this agreement quantitatively? In Figure 5, we comparethe empirical copula densities with the respective analytical Gaussian copula densitycopG

c .u; v/. Here, we set the correlation coefficient in each Gaussian copula to theempirical average correlations: Nc(glob) D 0:44 for original returns and Nc(loc) D 0:39 forlocally normalized returns. In Figure 5, we observe clear deviations from the respec-tive Gaussian copula densities. This is to be expected since the empirical copula

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 15

TABLE 1 Least mean squares between analytical and empirical copula densities.

Original LocallyAnalytical density returns normalized

Gaussian copula 27.52 5.26Correlation-weighted Gaussian copula 26.42 5.11K-copula 6.26 2.27Skewed Student t -copula 0.65 2.87

FIGURE 6 Histograms of correlations for (a) original returns, f .C(glob)k;l

/, and (b) locallynormalized returns, f .C

(loc)k;l

/.

0 0.2 0.4 0.6 0.8 1.00

1

2

3

4

5

0 0.2 0.4 0.6 0.8 1.00

1

2

3

4

5

Ck,lC (loc)Ck,lC (glob)

f(ffC

k,l

C)

(glo

b)

f(ffC

)(lo

c)

(a) (b)

densities are in fact an average over K.K � 1/=2 pairwise copula densities with dif-ferent correlations. Hence, a comparison with a single Gaussian copula with averagecorrelation cannot yield suitable results. Indeed, for the original returns we find con-siderable deviations not only in the corners but over the entire dependence structure.For the locally normalized returns, the corners are rather well described. Nonetheless,deviations over the whole dependence structure are clearly visible. Table 1 summa-rizes the deviations between empirical and analytical copula densities in the form ofleast mean squares. For the original returns we find a least mean square of 27.52,while the locally normalized returns yield a smaller 5.26.

3.4 Comparison with a correlation-weighted Gaussian copula

Aiming for a more suitable description of the empirical copulas, we now consider aweighted average of Gaussian copulas for different correlation coefficients. This takesinto account the empirical average over different stock pairs (see (3.1)). Figure 6 showsthe histograms of empirical correlation coefficients f .Ck;l/ for original and locally

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

16 M. Wollschläger and R. Schäfer

FIGURE 7 Differences in weighted Gaussian copula densities.

(a)

(c)

(b)

(d)

(a), (c) Correlation-weighted Gaussian copula densities cop.u; v/CWG. (b), (d) Differences between the empir-ical copula density and the correlation-weighted Gaussian copula density, cop(glob).u; v/ � cop.u; v/CWG andcop(loc).u; v/ � cop.u; v/CWG, respectively. (a), (b) Original returns. (c), (d) Locally normalized returns.

normalized returns estimated on the entire time series. The bin size is �c D 0:02.In our data sets we only observe positive correlations. We now obtain a Gaussianmixture by weighting each Gaussian copula density with the value of the probabilitydensity function of the respective correlation, h.Ck;l/ D f .Ck;l/�c. This yields thecorrelation-weighted Gaussian copula density

copCWG.u; v/ D1X

Ck;l D�1

h.Ck;l/copGCk;l

.u; v/; (3.4)

which is compared with the empirical copula densities in Figure 7. For both datasets we find only slight improvement over the single Gaussian copula, as depictedin Figure 5. The least mean squares are only slightly smaller as well (see Table 1).

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 17

TABLE 2 Parameter values for the K-copula densities.

Original LocallyParameter returns normalized

Nc 0.44 0.39N 3.2 7.8

This can be attributed to the fact that correlations also vary in time (see, for example,Münnix et al 2012; Schäfer and Guhr 2010). Thus, it is not sufficient to take theaverage over different correlations into account. For a better approximation of theempirical copula densities, the correlations would have to be estimated on shortertime intervals. This, however, leads to increasing estimation errors for shorter esti-mation intervals. Consequently, the reliable attainment of time-dependent correla-tions is problematic. This is where the K-copula, discussed in Section 2.7, comesinto play.

3.5 Comparison with the K -copula

We now consider the K-copula density copKc;N .u; v/, which takes inhomogeneous and

time-varying correlations into account. Here, the fluctuations of correlations aroundtheir mean value c are characterized by the free parameter N . We calculate the meancorrelation coefficient for the original returns and the locally normalized returns. Asnoted above, we find Nc(glob) D 0:44 and Nc(loc) D 0:39, respectively. The free parameterN is fitted to the empirical copula densities by the method of least squares. We findN (glob) D 3:2 for original returns and N (loc) D 7:8 for locally normalized returns. Theparameter values for Nc and N are also summarized in Table 2. The lower value for theoriginal returns reflects the fact that the locally normalized returns have a constantvariance of 1. Hence, there are smaller fluctuations in the covariances, which are in thiscase simply the correlations. In the K-copula, smaller fluctuations of the covariancesor correlations are described by larger values of N .

In Figure 8, the resulting K-copula densities are compared with the empiricalcopula densities. In both cases we find improved agreement with the empirical results.This is also reflected in much lower values for the least mean squares (see Table 1).However, for the original returns, a large deviation between empirical and analyticalresults remains. The overall structure of the empirical dependence is not capturedvery well by the K-copula. For the locally normalized returns on the other hand, theK-copula yields a very good description of the empirical dependence. Only slightdeviations persist in the lower–lower and upper–upper corners. The asymmetry ofthe empirical copula densities cannot be captured by the K-copula density due to its

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

18 M. Wollschläger and R. Schäfer

FIGURE 8 Differences in K-copula densities.

(a)

(c)

(b)

(d)

(a), (c) K-copula densities copKc;N .u; v/. (b), (d) Differences between the empirical copula density and the

K-copula density, cop(glob).u; v/ � copKc;N .u; v/ and cop(loc).u; v/ � copK

c;N .u; v/, respectively. (a), (b) Originalreturns, Nc(glob) D 0.44, N (glob) D 3.2. (c), (d) Locally normalized returns Nc(loc) D 0.39, N (loc) D 7.8.

TABLE 3 Parameter values for the skewed Student t -copula densities.

Original LocallyParameter returns normalized

Nc 0.44 0.39� 3.3 8.0� 0.06 0.04

symmetric character. This asymmetry is only weakly present in the case of locallynormalized returns, which leads to a better agreement between the K-copula and theempirical copula.

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 19

FIGURE 9 "Differences in skewed Student t -copula densities.

(a)

(c)

(b)

(d)

(a), (c) Skewed Student t -copula densities coptc;�;� .u; v/. (b), (d) Differences between the empirical copula den-

sity and the skewed Student t -copula density, cop(glob).u; v/ � coptc;�;� .u; v/ and cop(loc).u; v/ � copt

c;�;� .u; v/,respectively. (a), (b) Original returns, Nc(glob) D 0.44, �(glob) D 3.3, � (glob) D 0.06. (c), (d) Locally normalized returns,Nc(loc) D 0.39, �(loc) D 8.0, � (loc) D 0.04.

3.6 Comparison with the skewed Student t-copula

The skewed Student t -copula allows for an asymmetry in the dependence structure.Hence, it is a natural candidate with which to compare our empirical findings. Sincewe observe no asymmetry on average in the negative tail dependence of the empiricalcopula densities (see histograms (b) and (d) in Figure 4), we choose the same valuefor both components of the skewness parameter vector � , �1 D �2 D � . This leavesonly an asymmetry in the positive tail dependence of the skewed Student t -copula andreduces the number of parameters. The parameter values for � and � are fitted to theempirical copula densities by the method of least squares, whereas the mean correla-tion c is empirically determined by Nc(glob) D 0:44 and Nc(loc) D 0:39, respectively. We

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

20 M. Wollschläger and R. Schäfer

find �(glob) D 3:3, � (glob) D 0:06 for original returns and �(loc) D 8:0, � (loc) D 0:04 forlocally normalized returns. The parameter values are summarized in Table 3.

Figure 9 illustrates the resulting skewed Student t -copula densities and their differ-ences from the empirical copula densities. For original returns, we find a remarkableagreement. The skewed Student t -copula is able to capture the overall dependencestructure very well, including the asymmetry in the positive tail dependence. There areonly small deviations in the corners: in particular a mild overestimation for the neg-ative tail dependence of extreme events. For locally normalized returns, the skewedStudent t -copula provides a slightly worse fit of the empirical data than the K-copula.There is not much asymmetry to capture in the empirical copula density. Hence,the skewness parameter plays only a minor role in this case. Further, the positivetail dependence is more pronounced for the skewed Student t -copula than for theK-copula. On a local scale, however, this is not reflected in the empirical dependencestructure.

4 CONCLUSION

We presented an empirical study on the statistical dependencies between daily stockreturns. To this end we estimated empirical pairwise copulas for the original returnsand for locally normalized returns. Considering the former allowed us to study thedependence structure on a global scale. In the latter case, the nonstationary charac-teristics of return time series, ie, time-varying trends and volatilities, were removed.This provided us with the dependence structure on a local scale.

How far does the concept of Gaussian dependence carry in light of our empiricalfindings? To answer this question, we compared the empirical results not only with asingle Gaussian copula, but also with a correlation-weighted average of Gaussian cop-ulas and with the K-copula. The latter arises from a random matrix approach that mod-els time-varying covariances with a Wishart distribution. This yields a K-distributionthat adequately describes multivariate returns. We derived the resulting K-copula forthe bivariate case and found very good agreement with empirical pairwise dependen-cies of the locally normalized returns. Thus, we arrived at a consistent picture withinthe random matrix model: the K-distribution is able to describe the tail behavior ofthe marginal return distributions, and the K-copula captures the overall empiricaldependence structure. This implies that Gaussian statistics, and thus also a Gaussiandependence structure, provide a good description on a local scale. However, on aglobal scale, ie, when the empirical distribution function, which is involved in theestimation of the copula, is applied to the original return time series instead, wefind rather significant deviations from the K-copula. In particular, we observe a pro-nounced asymmetry in the positive tail dependence. Therefore, we also comparedour empirical findings with a model that explicitly allows for such an asymmetry: the

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 21

skewed Student t -copula. And indeed, we found a rather compelling agreement withthe empirical dependence structure of original returns. For the local scale, however, theempirical copula exhibited only a mild asymmetry and is overall better described bythe K-copula. How can we understand this? For the original returns, the tail depend-ence reflects periods with high volatility, while for the locally normalized returns allperiods contribute equally to the tail dependence. Thus, our results imply that theasymmetry in the tail dependence is not stationary, and it is stronger in periods withhigh volatility.

DECLARATION OF INTEREST

The authors report no conflicts of interest. The authors alone are responsible for thecontent and writing of the paper.

ACKNOWLEDGEMENTS

We thank Desislava Chetalova for helpful discussions.

REFERENCES

Aas, K., and Haff, I. H. (2006). The generalized hyperbolic skew Student’s t -distribution.Journal of Financial Econometrics 4, 275–309 (http://doi.org/ddbcdv).

Ang, A., and Chen, J. (2002). Asymmetric correlations of equity portfolios. Journal ofFinancial Economics 63, 443–494 (http://doi.org/dn7xwv).

Brigo, D., Pallavicini, A., and Torresetti, R. (2010). Credit Models and the Crisis: A Journeyinto CDOs, Copulas, Correlations and Dynamic Models. Wiley Finance.

Browne, R. P., and McNicholas, P. D. (2014). A mixture of generalized hyperbolic distribu-tions. Preprint (http://bit.ly/2aUHrcK).

Cappiello, L., Engle, R. F., and Sheppard, K. (2006). Asymmetric dynamics in the correla-tions of global equity and bond returns. Journal of Financial Econometrics 4, 537–572(http://doi.org/cq5npb).

Demarta, S., and McNeil, A. J. (2005). The t copula and related copulas. InternationalStatistical Review 73(1), 111–129 (http://doi.org/b4f3x4).

Dokov, S., Stoyanov, S. V., and Rachev, S. (2008). Computing VaR and AVaR of skewed-tdistribution. Journal of Applied Functional Analysis 3, 189–209.

Embrechts, P., Lindskog, F., and McNeil, A. (2003). Modeling dependence with copulasand applications to risk management. In Handbook of Heavy Tailed Distributions inFinance Handbooks in Finance Volume 1, Rachev, S. T. (ed), pp. 329–384. Elsevier(http://doi.org/bq8k2d).

Embrechts, P., McNeil, A., and Staumann, D. (2002). Correlation and dependence in riskmanagement: properties and pitfalls. In Risk Management: Value at Risk and Beyond,Dempster, M.A.H. (ed), pp.176–223.Cambridge University Press (http://doi.org/b866j5).

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

22 M. Wollschläger and R. Schäfer

Engle, R. (2002). Dynamic conditional correlation: a simple class of multivariate gener-alized autoregressive conditional heteroskedasticity models. Journal of Business andEconomic Statistics 20, 339–350 (http://doi.org/fb46f2).

Engle, R., and Colacito, R. (2006). Testing and valuing dynamic correlations for asset allo-cation. Journal of Business and Economic Statistics 24, 238–253 (http://doi.org/fnzz62).

Hansen, B. E. (1994). Autoregressive conditional density estimation. International Eco-nomic Review 35, 705–730 (http://doi.org/cfz8bs).

Hu, W., and Kercheval, A. N. (2006). The skewed t distribution for portfolio credit risk.Advances in Econometrics 22, 55–83 (http://doi.org/cz57gc).

Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman and Hall/CRC(http://doi.org/bpj4).

Kilgore, R. T., and Thompson, D. B. (2011). Estimating joint flow probabilities at streamconfluences by using copulas. Transportation Research Record: Journal of the Trans-portation Research Board 2262, 200–206 (http://doi.org/bp43).

Low, R. K. Y., Alcock, J., Faff, R., and Brailsford, T. (2013). Canonical vine copulas in thecontext of modern portfolio management: are they worth it? Journal of Banking andFinance 37(8), 3085–3099.

Markowitz, H. M. (1952). Portfolio selection. Journal of Finance 7(1), 77–91 (http://doi.org/bhzd).

Martens, M., and Poon, S.-H. (2001).Returns synchronization and daily correlation dynam-ics between international stock markets. Journal of Banking and Finance 25(10),1805–1827 (http://doi.org/fm2hz5).

McNeil, A., Frey, R., and Embrechts, P. (2005). Quantitative Risk Management: Concepts,Techniques and Tools. Princeton University Press.

Meucci, A. (2011). A new breed of copulas for risk and portfolio management. Risk 24(10),122–126.

Münnix, M. C., Shimada, T., Schäfer, R., Leyvraz, F., Seligman, T. H., Guhr, T., and Stanley,H.E. (2012). Identifying states of a financial market.Scientific Reports 2(644), 1–6 (http://doi.org/bnkf).

Necula, C. (2009). Moduling heavy-tailed stock index returns using the generalizedhyperbolic distribution. Romanian Journal of Economic Forecasting 2, 118–131.

Nelsen, R. B. (2006). An Introduction to Copulas. Springer.Ning, C., Xu, D., and Wirjanto, T. (2008). Modeling the leverage effect with copulas and

realized volatility. Finance Research Letters 5(4), 221–227 (http://doi.org/frc9kn).Onken, A., Grünewälder, S., Munk, M. H. J., and Obermayer, K. (2009). Analyzing short-

term noise dependencies of spike-counts in macaque prefrontal cortex using copulasand the flashlight transformation. PLoS Computational Biology 5(11), e1000577 (http://doi.org/b49jbn).

Patton, A. J. (2012a). Copula methods for forecasting multivariate time series. In Hand-book of Economic Forecasting, Volume 2, Chapter 16, pp. 899–960. Elsevier (http://doi.org/bp44).

Patton, A. J. (2012b). A review of copula models for economic time series. Journal ofMultivariate Analysis 110, 4–18.

Pelletier, D. (2006). Regime switching for dynamic correlations. Journal of Econometrics131(1), 445–473 (http://doi.org/dgg3c8).

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Estimating and modeling empirical copulas of daily stock returns 23

Rosenberg, J. V., and Schuermann, T. (2006). A general approach to integrated risk man-agement with skewed, fat-tailed risks. Journal of Financial Economics 79, 569–614(http://doi.org/fnfzd9).

Schäfer, R., and Guhr, T. (2010). Local normalization: uncovering correlations in non-stationary financial time series. Physica A: Statistical Mechanics and Its Applications389, 3856–3865 (http://doi.org/cghcnp).

Schmidt, R., Hrycej, T., and Stätzle, E. (2006). Multivariate distribution models with gener-alized hyperbolic margins. Computational Statistics and Data Analysis 50, 2065–2096(http://doi.org/bqjksp).

Schmitt, T. A., Chetalova, D., Schäfer, R., and Guhr, T. (2013). Non-stationarity in financialtime series: generic features and tail behavior. Europhysics Letters 103, 58003 (http://doi.org/bp45).

Schölzel, C., and Friederichs, P. (2008). Multivariate non-normally distributed random vari-ables in climate research: introduction to the copula approach. Nonlinear Processes inGeophysics 15, 761–772 (http://doi.org/fqkx9m).

Sklar, A. (1973). Random variables, joint distribution functions, and copulas. Kybernetika9, 449–460.

Socgnia, V. K., and Wilcox, D. (2014). A comparison of generalized hyperbolic distribu-tion models for equity returns. Journal of Applied Mathematics 2014, 263465 (http://doi.org/bnkj).

Strelen, J. C. (2009). Tools for dependent simulation input with copulas. In SimuTools:Proceedings of the 2nd International Conference on Simulation Tools and Techniques,Number 30, p. 30. ICST, Brussels (http://doi.org/cpbhv9).

Sun, W., Rachev, S., Stoyanov, S. V., and Fabozzi, F. J. (2008). Multivariate skewed Stu-dent’s t copula in the analysis of nonlinear and asymmetric dependence in the Germanequity market. Studies in Nonlinear Dynamics and Econometrics 12(2), 1–37 (http://doi.org/dsqfvp).

Tse, Y. K., and Tsui, A. K. C. (2002). A multivariate generalized autoregressive condi-tional heteroscedasticity model with time-varying correlations. Journal of Business andEconomic Statistics 20, 351–362 (http://doi.org/d9r48q).

Vilca, F., Balakrishnan, N., and Zeller, C. B. (2014). Multivariate skew-normal generalizedhyperbolic distribution and its properties. Journal of Multivariate Analysis 128, 73–85(http://doi.org/bp46).

Wishart, J. (1928). The generalised product moment distribution in samples from a normalmultivariate population. Biometrika A 20(1), 32–52 (http://doi.org/bsd4qn).

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Journal of Risk 19(1), 25–42DOI: 10.21314/JOR.2016.343

Research Paper

Path-consistent wrong-way risk:a structural model approach

Markus Hofer

Quantitative Analytics, ING Bank, ING Financial Markets, Bijlmerdreef 109,1102 BW Amsterdam, The Netherlands; email: [email protected]

(Received June 26, 2015; revised December 15, 2015; accepted January 11, 2016)

ABSTRACT

We present a general and path-consistent wrong-way risk (WWR) model, whichdoes not require simulation of credit and market variables simultaneously. Althoughsimilar so-called copula models are well known, our approach is novel in severalways. First, our method can model a wide range of dependence structures whilealways guaranteeing path consistency of default probabilities (the possibility of path-inconsistencies in copula models was highlighted in a recent article). Second, weplace special emphasis on the difficult task of calibrating the underlying dependencestructure. In particular, we consider a default correction of the dependence structure.Third, our model serves as a bridge between structural model approaches, wheredependence between exposure and equity price is modeled, and copula models, whereexposure is directly correlated to default time. Finally, we apply our method in realisticsituations and show that we can achieve a wide range of WWR impacts.

Keywords: credit valuation adjustment; wrong-way risk; copula; structural credit model; modelcalibration.

Print ISSN 1465-1211 j Online ISSN 1755-2842Copyright © 2016 Incisive Risk Information (IP) Limited

25

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

26 M. Hofer

1 INTRODUCTION

In recent years, credit valuation adjustment (CVA) has received enormous attention,focused on both the computational and modeling aspects. (Unilateral) CVA is definedas the expected loss in a portfolio at default of the corresponding counterparty; moreprecisely,

CVA D EŒ.1 � RR/V C� 1.� < T /�;

where RR denotes the so-called recovery rate, V C� denotes the discounted, positive

exposure of the portfolio at the time of default � of the counterparty, and T is themaximal maturity of a derivative within the portfolio.

In this context, an important challenge is the modeling of the dependencies betweenVt and � or, more generally, between exposure and probability of default. Since thereare almost no liquidly traded products that depend on market and credit variablessimultaneously, modeling and calibration of these dependencies is extremely difficult.

A special case of dependence, usually denoted wrong-way risk (WWR), is presentif the probability of default of the counterparty is positively correlated with the valueof the portfolio. In particular, in times of crisis the increase in CVA due to WWR canbe significant. A typical example of very strong WWR is portfolios with emergingmarket counterparties, where the portfolio value depends heavily on foreign exchange(FX) rates involving the local currency.

Hull and White (2012) were among the first to publish a consistent WWR frame-work. They model WWR as (deterministic) dependence between hazard rates andexposure. This approach has the advantage of requiring only small changes to standardmethods for calculating CVA without WWR.

Another popular modeling approach was followed by a number of authors (see, forexample, Pykthin 2012; Rosen and Saunders 2012; Sokol 2010). In Sokol (2010) thedependence between default time and exposure is modeled by a copula, where thechoice of copula parameters depends on the correlation between the counterparty’screditworthiness and market risk factors. Recently, Böcker and Brunnbauer (2014)showed that these so-called copula models are prone to losing the path consistencyof default probabilities if the model is not set up properly. Böcker and Brunnbauergive a characterization of path-consistent WWR models and show, for instance, thatthe Rosen–Saunders model and the above-mentioned Hull–White model belong tothe class of path-consistent WWR models.

In contrast to the above examples, where dependence between credit and marketvariables is directly modeled, it is also possible to introduce dependencies betweenexposure at default and time of default, implicitly, by using a structural credit model;see, for instance, Buckley et al (2011) in which default occurs if the equity processof the counterparty hits a specific barrier, and exposure dynamics are modeled as astochastic process correlated with the equity process.

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Path-consistent WWR: a structural model approach 27

Finally, a number of articles focus on particular aspects of WWR such as systemicwrong-way risk (Pykthin and Sokol 2013; Turlakov 2013), econometric investigationsof the calibration of WWR models (Ruiz et al 2015) or modeling of exposure jumps atdefault (Pykthin and Sokol 2013). Furthermore, Glasserman andYang (2015) computemodel-independent upper bounds for WWR using linear programming. See Hofer andIacó (2014) for a general numerical method to compute worst case bounds when thedependence structure is unknown.

Here we pick up the ideas in Böcker and Brunnbauer (2014), Rosen and Saunders(2012), Buckley et al (2011) and Sokol (2010), to define a WWR model defined ona discrete-time grid, which is path consistent in the sense of Böcker and Brunnbauer(2014). The contribution of this paper is threefold. First, we present a general, real-istic WWR model in line with the path-consistency definition given in Böcker andBrunnbauer (2014). WWR is explicitly modeled by the joint distribution of the expo-sure and the equity value of the counterparty. Second, we motivate and provide acalibration strategy, since calibration of WWR models has not received much atten-tion in the literature. Finally, we provide a link between WWR models that definedependence between exposure and default time directly and those that model thedependence indirectly via a structural model.

The structure of the paper is as follows. In Section 2 we introduce our model setupand prove our main theoretical contribution: the path consistency of our model. InSection 3 we present a calibration methodology for our model, and in Section 4 weapply our model in realistic situations and show that it is able to capture a wide rangeof WWR impacts.

2 A PATH-CONSISTENT WRONG-WAY RISK MODEL

In this section, we consider only unilateral CVA, ie, we only model the default ofthe counterparty. The main result of this section is Theorem 2.5, in which we showthat our method defines path-consistent exposure weights in the sense of Böcker andBrunnbauer (2014).

The drift of the portfolio value can smoothly mimic sudden changes such as pay-ments or expiration of parts of the portfolio. Note that Vt depends only on the marketvalue of the portfolio and not on the default of the counterparty; thus, we call Yt thedefault-risk-free portfolio value.

We model default in a similar way to structural credit models (see, for example,Merton 1974). For a given time grid t0 D 0 < t1 < � � � < tM D T , we assume thecounterparty defaults at tj if its stock price QStj is smaller than a barrier level Bj . Inthis setting, default is only possible at a grid point tj . In our model the barrier levelsBj are defined such that the model default probabilities

pj D P. QStj < Bj ; QStk > Bk 8k < j /

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

28 M. Hofer

match market-implied values in the following sense:

pj D Pmarket implied.default in Œtj �1; tj / j no default before tj �1/: (2.1)

Since we work on a discrete-time grid, we are able to divide the total CVA intocontributions from each monitoring point tj . More precisely, we can write

CVA DMX

j D1

CVAj ;

which will simplify notation in the rest of this section.Assume RR D 0. We can compute the expected positive exposure at default at

time t1 in a straightforward way. Furthermore, we denote the value of the underlyingportfolio at time t as QVt . More precisely, we have QVt D Vt j SCP

tj> Bj for all tj < t .

In the same way, we have to consider the equity process conditionally on no-defaultin the past:

QSCPt D SCP

tjj SCP

tj> Bj 8tj < t:

Note that QVt depends only on the market value of the portfolio and not on thedefault of the counterparty. Thus, we call QVt the default-risk-free portfolio value.Since the dynamics of QVt are usually not available in closed form, we have to relyon Monte Carlo simulations. Assume that we have simulated N QVt -paths on the timegrid .tj /06j 6M and the resulting values are denoted by QV i

tjfor i D 1; : : : ; N and

j D 0; : : : ; M .When exposure and probability of default are not independent, we have to con-

sider risky portfolio values Vt . More precisely we correct the portfolio values QVt forprobability at default at s < t . Similarly, we will denote the default-adjusted equityprocess by Stj . The distributions of Vt and QVt can differ significantly, as we show inthe following simple example.

Example 2.1 Let the dynamics of the portfolio value be given by

QVtj D

8̂<̂ˆ̂:

0 with probability 0:9 if QVtj �1D 0;

1 with probability 0:1 if QVtj �1D 0;

1:000 with probability 1 if QVtj �1D 1;

where QVt0 D 0 and pj D 0:1 for all j . If we assume independence between theportfolio value and default events we get

Vtj D

8ˆ̂<ˆ̂:

0 with probability 0:9 if Vtj �1D 0;

1 with probability 0:1 if Vtj �1D 0;

1:000 with probability 1 if Vtj �1D 1:

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Path-consistent WWR: a structural model approach 29

However, if we assume comonotonicity between the default and the portfolio value,meaning that at every tj , j > 1, the top pj -quantile of Vtj defaults and the rest has a0% probability of default, then we have

Vtj D(

0 with probability 0:9 if Vtj �1D 0;

1 with probability 0:1 if Vtj �1D 0;

where Vt0 D 0. In this case the highest portfolio value, 1.000, can never be reached,although portfolio value and default are strongly positive correlated.

In our model, the dependence structure between market and credit variables isinduced by the dependence structure between the portfolio value and the counter-party’s equity value. More precisely, we assume that the joint distribution of Vtj , theportfolio value at tj , and Stj , the counterparty’s equity value, is defined as

FVtj;Stj

.v; s/ D Cj .FVtj.v/; FStj

.s//;

where Cj is a copula and FVtjis the empirical distribution of the portfolio value at tj .

In the following equations we denote the per-time-slice ordered exposures by U itj

,ie, U 1

tj6 � � � 6 U N

tj, and the position of V i

tjin the ordered set by g.j; i/; thus,

V itj

D Ug.j;i/tj

:

Under the above assumptions, the CVA contribution at time t1 can be written as

CVA1 D .1 � RR/

Z

.�1;1/�Œ0;B1/

max.v; 0/ dFVt1;St1

.v; s/

D .1 � RR/

NXiD1

max.U it1

; 0/

Z

Œ.i�1/=N;i=N /�Œ0;FSt1.B1//

dC1.x; y/

D .1 � RR/

NXiD1

max.U it1

; 0/wi1p1; (2.2)

where

0 6 wi1 6 min

�1

Np1

; 1

�8i

andNX

iD1

wi1 D 1;

which follows from copula properties and the Fréchet–Hoeffding bound (see, forexample, Nelsen 2006). Note that wi

1 D 1=N for all i (which replicates the no-WWRcase) holds if, for instance, C1.x; y/ is the independence copula or if p1 D 1.

www.risk.net/journal Journal of Risk

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

30 M. Hofer

Furthermore, in the above setting, no knowledge about the dynamics of St , exceptfor the parameters of the copula C1 and the counterparty’s default probabilities, isneeded to compute CVA1. Moreover, note that Vt1 D QVt1 and St1 D QSt1 .

Next we compute FVt2, ie, we have to adjust F QVt2

for a default at t1. For this reasonwe define survival probabilities P i

tjfor every simulated exposure path . QV i

tj/06j 6M ,

where P itj

denotes the probability that the counterparty did not default before tjconditional on having the exposures QV i

tkfor 0 6 k < j . Obviously, P i

t1D 1 for all

i , and, following (2.2), the P it2

can be computed as

P it2

D P it1

.1 � Nwg.1;i/1 p1/: (2.3)

In (2.3), we used the fact that at t1 every simulated exposure path accounts for 1=N

of the empirical distribution. We present a general version of (2.3) below.To further simplify notation, we use aggregated survival probabilities NP j

ti, ordered

according to the corresponding simulated exposures. More precisely,

NP itj

DiX

kD1

Pg�1.j;k/tj

;

where g�1 is defined such that i D g�1.g.j; i// for all i; j and NP 0tj

D 0 for all j .Now we can compute CVA2:

CVA2 D .1 � RR/

Z

.�1;1/�Œ0;B2/

max.v; 0/ dFVt2;St2

.v; s/

D .1 � RR/

NXiD1

max.U it2

; 0/

Z

Œ NP i�1t2

= NP Nt2

; NP it2

= NP Nt2

/�Œ0;FSt2.B2//

dC2.x; y/

D .1 � RR/

NXiD1

max.U it2

; 0/wi2p2;

and, in general,

CVAj D .1 � RR/

Z

.�1;1/�Œ0;Bj /

max.v; 0/ dFVtj;Stj

.v; s/

D .1 � RR/

NXiD1

max.U itj

; 0/

Z

Œ NP i�1tj

= NP Ntj

; NP itj

= NP Ntj

/�Œ0;FStj.Bj //

dCj .x; y/

D .1 � RR/

NXiD1

max.U itj

; 0/wij pj ; (2.4)

where

P itj C1

D P itj

�1 �

NP Ntj

P itj

wg.j;i/j pj

�: (2.5)

Journal of Risk www.risk.net/journal

To subscribe to a Risk Journal visit Risk.net/subscribe or email [email protected]

Path-consistent WWR: a structural model approach 31

Note that, since NP it1

D i and NP Nt1

D N , we have that (2.4) is equivalent to (2.2) forj D 1, and (2.5) is equivalent to (2.3) for j D 1 as P i

t1D 1 for all i .

The following lemma proves the nonnegativity of P itj

.

Lemma 2.2 P itj

> 0 for all i; j .

Proof First assume that P itj

D 0. Then wg.j;i/j D 0, since the corresponding

integration domain in (2.4) is empty.Next we assume that P i

tj> 0. Then

P itj C1

D P itj

�1 �

NP Ntj

P itj

wkj pj

�;

where k D g.j; i/. Thus, the statement is proved if

�1 �

NP Ntj

P itj

wkj pj

�> 0:

We have

NP Ntj

P itj

wkj pj D

NP Ntj

P itj

Z

Œ NP k�1tj

= NP Ntj

; NP ktj

= NP Ntj

/�Œ0;FStj.Bj //

dCj .x; y/

6NP Ntj

P itj

min

�pj ;

NP ktj

� NP k�1tj

NP Ntj

�

DNP Ntj

P itj

min

�pj ;

P itj

NP Ntj

�

6 1;