virginia retirement system update spring conference/presentations/11;10-12...howell creates the...

TRANSCRIPT

Virginia Retirement System Update

Virginia Government Finance Officers Association Spring Conference

Hilton Virginia Beach Oceanfront Hotel May 5, 2016

Barry C. Faison, CPA Chief Financial Officer

2

Agenda

• VRS Vision

• VRS Overview

• Hybrid Retirement Plan

• myVRS Changes

• 2016 Legislative Update

• Funded Status and Contribution Rates

• GASB 67/68 Update

3

VRS Vision

“To be the trusted leader in the delivery of benefits and services

to those we serve.”

The VRS Vision sets our direction and guides our plans and actions.

Our Vision serves as the foundation for our interactions with customers.

4

Our Vision in Action

Serve those who serve others

Act as good stewards

of the funds in our care

Help members plan for

tomorrow, today

5

Our Vision in Action

Leverage technology

for additional services

and increased efficiency

Outreach and engagement

with key constituents

and stakeholders

Continuous monitoring

and improvement

through benchmarking

VRS Overview

7

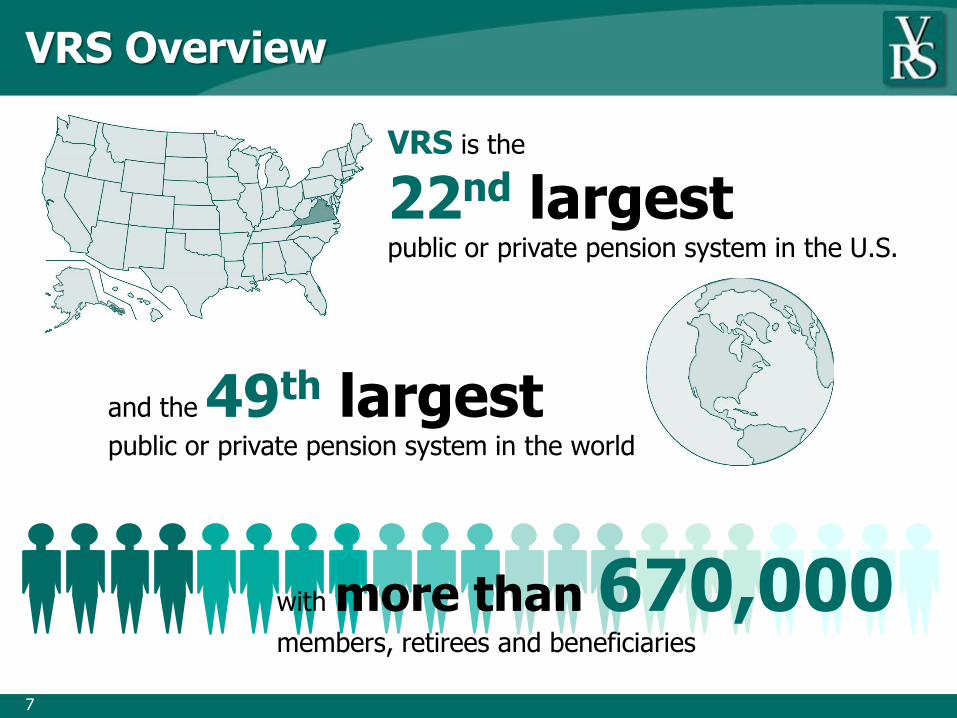

VRS Overview

with more than 670,000 members, retirees and beneficiaries

and the 49th largest

public or private pension system in the world

VRS is the

22nd largest

public or private pension system in the U.S.

8

As of December 31, 2015

Plan 1 Plan 2 Hybrid Total

Teachers 90,781 37,900 19,724 148,405

Political Subdivisions 59,439 32,872 13,421 105,732

State Employees 47,907 19,704 10,223 77,834

State Police Officers’ Retirement System (SPORS)

1,414 527 – 1,941

Virginia Law Officers’ Retirement System (VaLORS)

4,773 4,126 – 8,899

Judicial Retirement System (JRS) 278 69 81 428

Total Active Members 204,592 95,198 43,449 343,239

Total Active Members

Retirees/ Beneficiaries

Inactive/ Deferred Members

VRS Total Population

343,239 190,235 139,809 673,283

VRS Total Membership

9

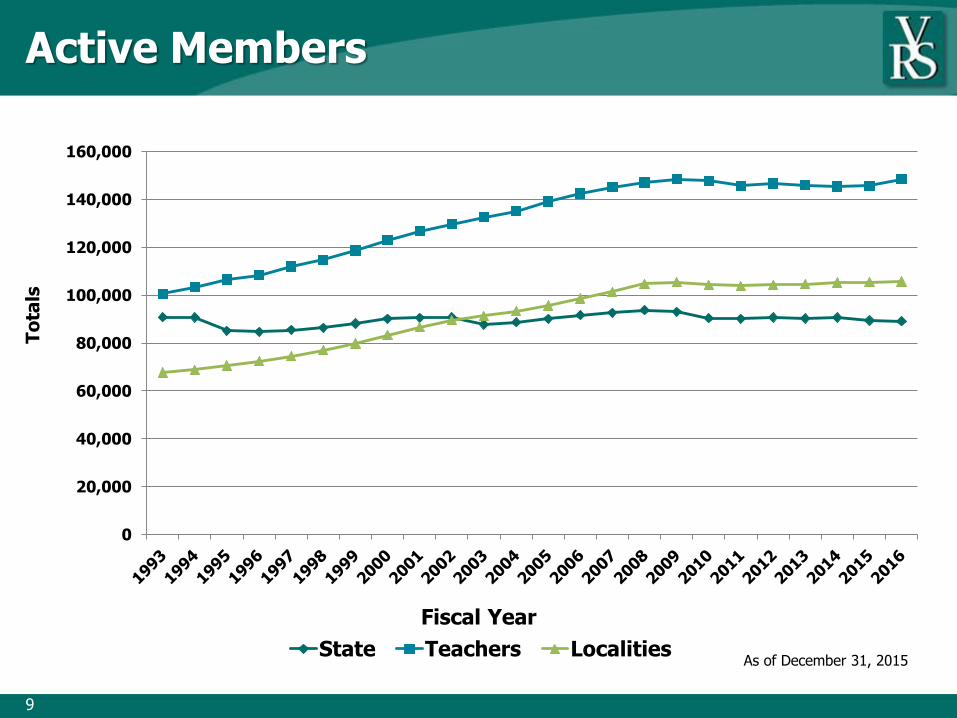

Active Members

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

State Teachers LocalitiesAs of December 31, 2015

Fiscal Year

To

tals

10

Retirees

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

State Teachers LocalitiesAs of December 31, 2015

Fiscal Year

To

tals

11

Benefit Comparison

11

State Teachers Local

Actives:

Average Age 48.3 45.1 46.3

Average Service 12.7 12.0 11.1

Average Salary $51,461 $50,720 $42,859

Retirees:

Avg. Age @ Retirement 63.7 62.3 62.3

Avg. Service @ Retirement 22.7 22.5 20.3

Avg. Benefit @ Retirement 38.6% 38.3% 33.5%

Avg. Annual Benefit $21,205 $22,216 $15,365

Avg. Social Security Benefit at Age 62

$19,488 $18,600 $15,480

Information is obtained from the June 30, 2015, actuarial valuations.

Hybrid Retirement Plan

13

Hybrid Retirement Plan

47,648 active Hybrid Retirement Plan

members as of April 1, 2016

• Total combined balance in the Hybrid 401(a) Cash Match Plan and the Hybrid 457 Deferred Compensation Plan is $53.6 million.

• Approximately 6,007, or 12.6%, of hybrid members are making voluntary

contributions.

14

Hybrid Retirement Plan

3.97%

6.66%

7.99%

8.99% 9.11%

10.57%

12.61%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

Hybrid Voluntary Contribution Participation Rate

As of April 1, 2016

15

133

6,741

10,827

6,725

5,418 4,821 4,704

3,728

2,698

1,163

400 140 0

2,000

4,000

6,000

8,000

10,000

12,000

<20 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70+

Hybrid Retirement Plan

Hybrid Retirement Plan Members by Age

As of April 1, 2016

16

Hybrid Retirement Plan

1.50%

6.18% 1.25%

5.81% 1.13%

2.73%

0.38%

81.02%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Percent of Voluntary Contribution Members Electing Each Voluntary Contribution Percentage

81% of the 6,007 members electing voluntary contributions chose to maximize their voluntary contributions at 4%

As of April 1, 2016

Changes

18

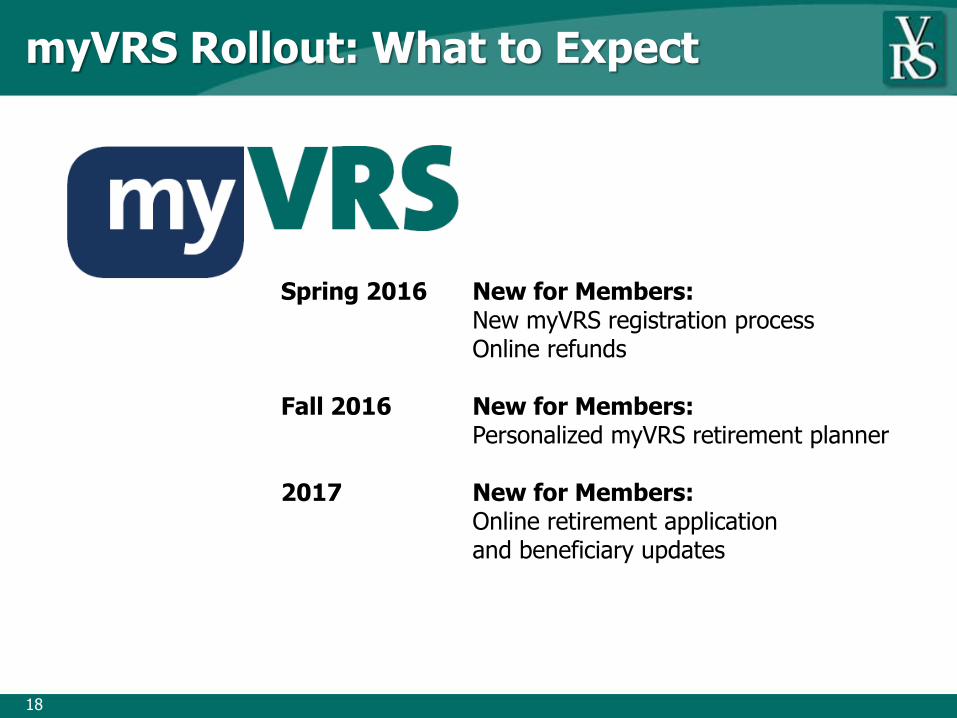

myVRS Rollout: What to Expect

Spring 2016 New for Members: New myVRS registration process Online refunds Fall 2016 New for Members: Personalized myVRS retirement planner 2017 New for Members: Online retirement application and beneficiary updates

19

Meet the new myVRS!

20

In the Future for Members

2016 Legislative Update

22

Reports Required: 2015 Legislative Session

Bill Number

Summary Report Date Due

HB 2204 Examine Line of Duty Act (LODA) recommendations from JLARC; develop proposals on issues from report; report to Chairmen of House Appropriations and Senate Finance; General Assembly will consider re-enacting the bill during 2016, including moving administration to VRS and health benefit administration to DHRM

Oct. 1, 2015

HB 1969 Review cash balance retirement plans implemented in other statewide retirement systems; compare long-term costs to current VRS plan designs; assess financial risks to employers and employees; administrative impact of cash balance plan; recommend funding structure

Nov. 1, 2015

HB 1998 Convene a working group to review current state and federal laws and regulations that encourage citizens of Commonwealth to save for retirement by participating in retirement savings plans; review options for self-employed, part-time employees, full-time employees without retirement savings plans, etc.

Jan. 1, 2017

23

2016 Legislative Update

Bill Number Patron Description

HB 409 and SB 51

Del. Ingram Sen. Howell (chief patron) and Sen. Dance (co-patron)

Makes technical amendments to the programs administered by VRS. • Forfeiture of unvested employer hybrid contributions § 51.1-169(B)(3)

• Clarifies that a Hybrid member does not forfeit unvested employer contributions to the DC component of the Hybrid Plan unless he or she ceases to be a VRS member

• Corrections to language changed in HB 1890 (2015 Session, PPS)

§ 51.1-142.2(A)(1) • Replaces “qualified child” with correct defined term

“qualifying child,” requested by the Division of Legislative Services

§ 51.1-142.2(A)(3) • Ensures that service members receive the full benefits

due to them under USERRA by applying the defined term to the subsection and not the entire section

VRS-Requested Legislation

24

2016 Legislative Update: LODA

Current LODA Provisions New LODA Provisions

Effective July 1, 2017 (assuming no further changes)

Eligibility determinations and health insurance benefits administered by the Department of Accounts (DOA)

Eligibility determinations administered by VRS; health insurance benefits administered by the Department of Human Resource Management (DHRM)

LODA health insurance benefits vary depending on the employer

All LODA beneficiaries will receive uniform health insurance benefits through a single health insurance pool administered by DHRM

Employers do not have a formal role in the eligibility determination or appeal processes

Employers may 1) submit evidence that could assist in making the eligibility determination, and 2) participate in any informal fact-finding proceeding at the agency-appeal level

Appeals of eligibility determinations are given a de novo review in circuit court (i.e., a completely new trial without regard for DOA’s determination)

Appeals of eligibility determinations handled through the Administrative Process Act (i.e., a circuit court will decide whether a determination is supported by “substantial evidence”)

Employers are generally required to train LODA-covered employees on LODA benefits (no timeframe or frequency requirements)

Employers are required to train LODA-covered employees within 30 days of employment and every two years thereafter; the training must include discussion of intestate succession rules (i.e., who will receive benefits)

Changes to LODA Administration

25

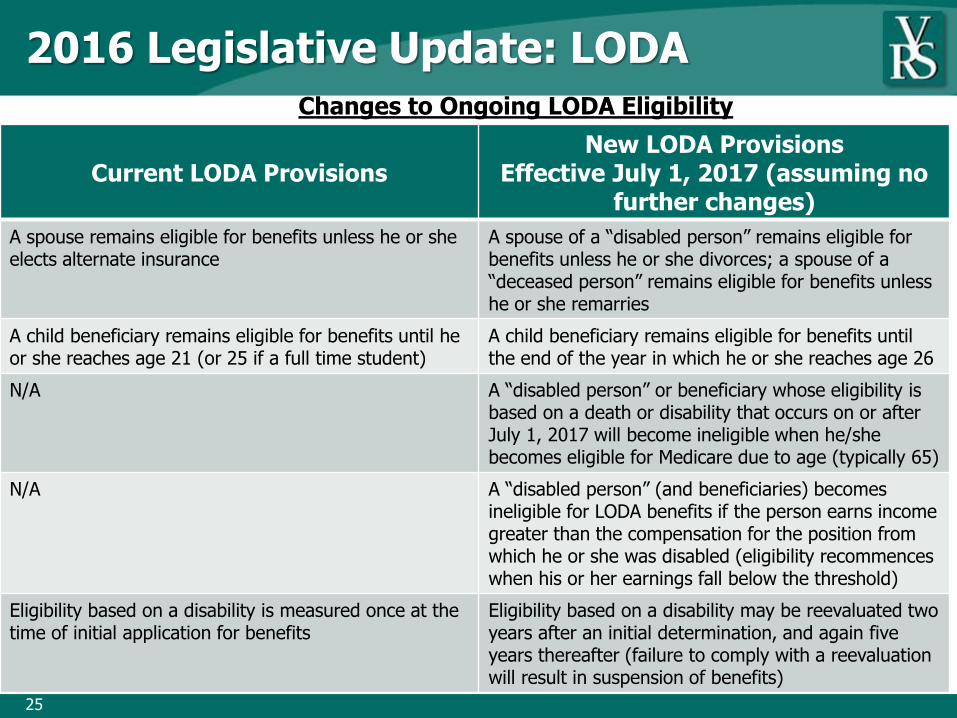

2016 Legislative Update: LODA

Current LODA Provisions New LODA Provisions

Effective July 1, 2017 (assuming no further changes)

A spouse remains eligible for benefits unless he or she elects alternate insurance

A spouse of a “disabled person” remains eligible for benefits unless he or she divorces; a spouse of a “deceased person” remains eligible for benefits unless he or she remarries

A child beneficiary remains eligible for benefits until he or she reaches age 21 (or 25 if a full time student)

A child beneficiary remains eligible for benefits until the end of the year in which he or she reaches age 26

N/A A “disabled person” or beneficiary whose eligibility is based on a death or disability that occurs on or after July 1, 2017 will become ineligible when he/she becomes eligible for Medicare due to age (typically 65)

N/A A “disabled person” (and beneficiaries) becomes ineligible for LODA benefits if the person earns income greater than the compensation for the position from which he or she was disabled (eligibility recommences when his or her earnings fall below the threshold)

Eligibility based on a disability is measured once at the time of initial application for benefits

Eligibility based on a disability may be reevaluated two years after an initial determination, and again five years thereafter (failure to comply with a reevaluation will result in suspension of benefits)

Changes to Ongoing LODA Eligibility

26

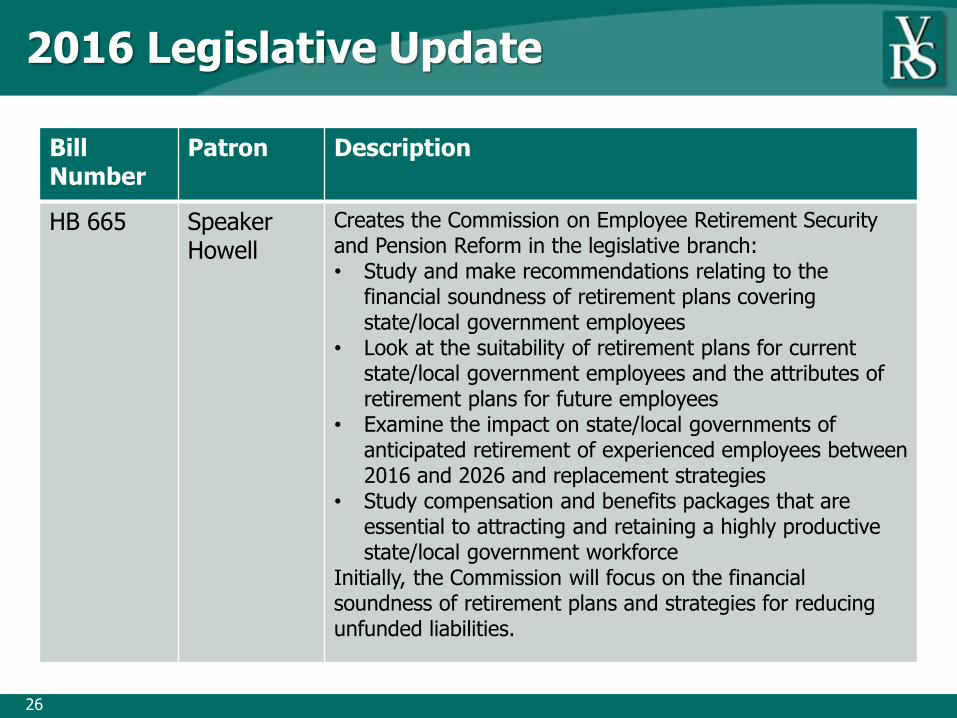

2016 Legislative Update

Bill Number

Patron Description

HB 665

Speaker Howell

Creates the Commission on Employee Retirement Security and Pension Reform in the legislative branch: • Study and make recommendations relating to the

financial soundness of retirement plans covering state/local government employees

• Look at the suitability of retirement plans for current state/local government employees and the attributes of retirement plans for future employees

• Examine the impact on state/local governments of anticipated retirement of experienced employees between 2016 and 2026 and replacement strategies

• Study compensation and benefits packages that are essential to attracting and retaining a highly productive state/local government workforce

Initially, the Commission will focus on the financial soundness of retirement plans and strategies for reducing unfunded liabilities.

27

2016 Legislative Update: Budget

• Local governments were given the option to elect either to fund the VRS-certified contribution rate or a temporary, “alternate” reduced rate.

• 2013 Appropriation Act – Item 468 H.1 – provided that localities that chose the alternate rate are scheduled to pay the higher of the contribution rate in effect for FY 2012 or 80% of the results from the June 30, 2013, actuarial valuation approved by the VRS Board for 2014-16 biennium.

• Item 475 I.1 of the Governor’s proposed budget for the 2016-18 biennium makes the VRS Board-certified rate the default.

– This relieves most local employers from having to pass a resolution simply to pay the VRS Board-certified rate.

Certified Rate Alternate Rate

Political Subdivisions 427 23

School Divisions 124 9

Total Received 551 32

28

2016 Legislative Update: Budget

Other Budget Highlights

• 100% funding of the actuarially determined retirement contribution rates for state employees, SPORS, VaLORS, and JRS in both years (earlier than required by the statutory schedule).

• 100% funding of the actuarially determined retirement contribution rate for teachers in the second year. The rate will be 89.84% of the actuarially determined rate in the first year.

• 100% funding of the actuarially determined OPEB contribution rates in both years with the exception of the HIC for teachers, which will be 90% funded in FY 2017.

• One-time payments totaling $189,482,547 to accelerate and complete the 10-year payback of contributions for the state plans deferred in the 2010-12 biennium. In FY 2017-18, the actuarially determined rates were adjusted downward to reflect the impact of the early payback of deferred contributions. Approximately $193 million was made last year to the Teacher Plan toward the 10-year payback of contributions.

Funded Status and

Contribution Rates

30

Funded Status: Teachers

30

0%

20%

40%

60%

80%

100%

120%

Notes: • Projected years’ investment returns assume 7.0% with 2.5% inflation rate. • Projected funded status reflects additional $192.9 million contribution to Teacher Plan on 6/30/15. • New GASB Accounting Rules reflect funded status using Market Value of Assets effective 6/30/14 for Plan Reporting and 6/30/15 for Employer Reporting.

Projected Funded Status using Market Value of Assets (New GASB Standard)

Projected Funded Status using Actuarial Value of Assets (Funding Standard)

The funded status for FY 2015 based on the actuarial value of assets was 69.2%.

Historical Funded Status using Actuarial Value of Assets (Funding Standard)

Teacher Plan Unfunded Liability as of 6/30/15 $13.1 Billion using Actuarial Assets $12.2 Billion using Market Assets

31

Projected Teacher Employer Contribution Rates

• Above contribution rates are net of employee contributions. • Teacher rates for FY 2016 were lowered due to additional contribution of $192.9 million applied to deferred contribution balance

during FY 2015. The subsequent rates for FY 2017-2020 were also lowered to reflect the accelerated payment received

2015 2016 2017 2018 2019 & 2020Phase-In of VRS Board Certified Rates

Agreed Upon in 2012 Legislative

Session 79.69% 79.69% 89.84% 89.84% 100%

Expected Employer Rates Based on

Phase-In Schedule 14.50% 14.06% 14.66% 14.66% 15.79%

Employer Rates Based on Governor's

Proposed Budget 14.50% 14.06% 14.66% 16.32% TBD

House & Senate Budget Conference

Report 14.50% 14.06% 14.66% 16.32% TBD

FISCAL YEAR

32

Funded Status: Political Subdivisions in Aggregate

32

0%

20%

40%

60%

80%

100%

120%

Notes: • Projected years’ investment returns assume 7.0% with 2.5% inflation rate. • New GASB Accounting Rules reflect funded status using Market Value of Assets effective 6/30/14 for Plan Reporting and 6/30/15 for Employer Reporting.

Projected Funded Status using Market Value of Assets (New GASB Standard)

Projected Funded Status using Actuarial Value of Assets (Funding Standard)

The funded status for FY 2015 based on the actuarial value of assets was 84.3%.

Historical Funded Status using Actuarial Value of Assets (Funding Standard)

Political Subdivisions Unfunded Liability as of 6/30/15 $3.1 Billion using Actuarial Assets $2.6 Billion using Market Assets

33

Funded Ratio – Political Subdivisions

All Pension Plans 80.50% 87.60% 84.30% 86.90%

Pension Plans with no Enhanced

Hazardous Duty Coverage 87.20% 94.90% 91.50% 94.40%

Pension Plans with Enhanced Hazardous

Duty Coverage 78.90% 85.70% 82.50% 85.10%

Actuarial Value

of Assets

Market Value

of Assets

Actuarial Value of

Assets

FY 2014 FY 2015

Market Value of

Assets

34

Average Contribution Rates Enhanced Hazardous Duty Coverage/Non-Enhanced Hazardous Duty Coverage

• Rates net of member contribution rate. • Rates beginning in 2014 include employer contribution rate for Hybrid defined contribution component.

35

GASB 67/68 Update

36

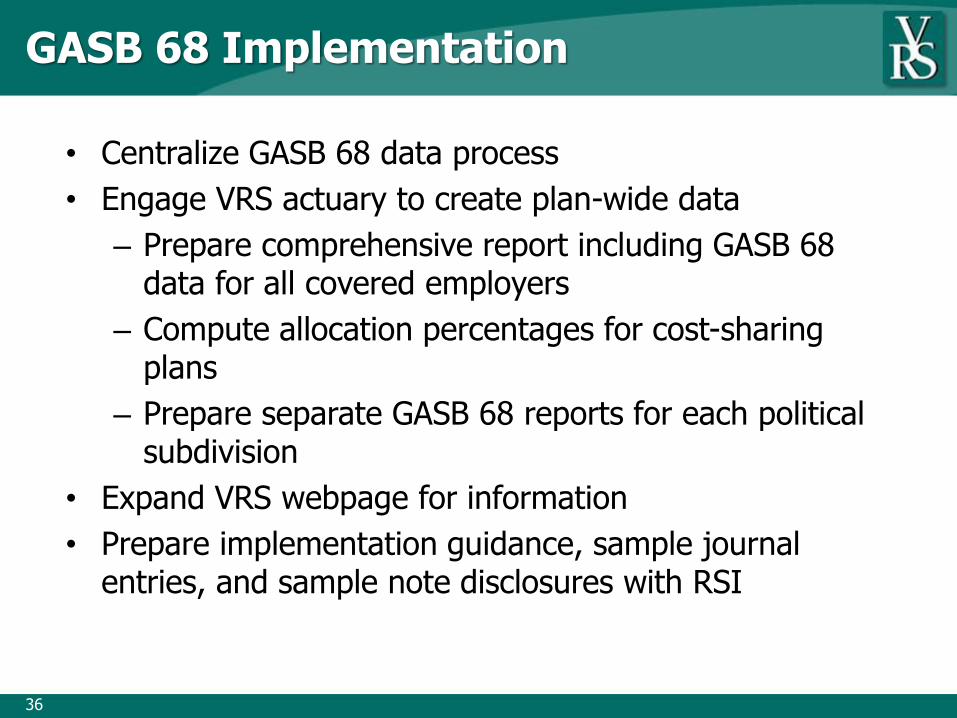

GASB 68 Implementation

• Centralize GASB 68 data process

• Engage VRS actuary to create plan-wide data

– Prepare comprehensive report including GASB 68 data for all covered employers

– Compute allocation percentages for cost-sharing plans

– Prepare separate GASB 68 reports for each political subdivision

• Expand VRS webpage for information

• Prepare implementation guidance, sample journal entries, and sample note disclosures with RSI

37

GASB 68 Implementation

• Expand availability of data in VNAV system

– Developed report for employer to extract VNAV data changes (hires, terminations, job changes, status changes, salary changes, etc.)

– Supplements monthly Snapshot reports

• Prepare supplemental information for Actuary

– Analysis of annual employer contribution revenue to identify variances from current contributions due

– Detailed report identifying components of change in plan assets between periods

– Report of employer contributions using current year creditable compensation for employer allocations

38

GASB Resources

• GASB 67 and GASB 68 standards

• GASB 67 and GASB 68 Implementation guides

• Complete GASB 67 report from VRS Actuary for the VRS plans

• Complete GASB 68 report from VRS Actuary for all covered employer groups

• Selected presentations on GASB 67 and GASB 68

39

GASB Resources

• Sample journal entries for each employer group

• Sample note disclosures for each employer group

• GASB 68 Reports from VRS with Audit Opinion from the Auditor of Public Accounts

– Selected state agencies

– Teacher cost-sharing pool

– Political subdivision plans

40

FY 2016 Plans

• Perform some GASB 67 and 68 procedures concurrently

• VRS and APA started the process earlier

• VRS will prepare standard calculations and allocations

• Develop additional reports, as needed

• Modify disclosure information and guidance using input from employers and their auditors

• Evaluate use of a service organization controls report to facilitate the audit process

• Begin preparation for implementation for OPEBs

41

Thank you!