virginia housing development authority housing’s impact on local government finance meeting of the...

TRANSCRIPT

Virginia Housing Development Authority

Housing’s Impact onHousing’s Impact onLocal Government FinanceLocal Government Finance

Meeting of the Virginia GovernmentFinance Officers Association

Virginia Beach, VirginiaJune 9, 2011

2

vhda.com | 800-227-VHDA

Impact of Home Values on Local Revenue Streams

3

vhda.com | 800-227-VHDA

Housing is a critical directgenerator of local tax revenues.

• In FY08, over half (50.7%) of local revenues in Virginia were derived from real property taxes.*

• In 2009, 71.2 percent of the assessed real property in Virginia was single-family homes and 4.8 percent was multifamily residential property.**

• Together, these data show that the assessed value of residential property accounts for fully 38 percent of local tax bases.

*Staff, Virginia Commission on Local Governments

**John Knapp, Weldon Cooper Center for Public Service, UVA based on unpublished VA Dept. of Taxation data provided by Josh Silverman in Nov. 2010

4

vhda.com | 800-227-VHDA

Local tax bases benefitedsubstantially from the housing boom.

• Rising residential property values drove local revenue increases during the past decade.

• Unfortunately, this short-term increase in local tax bases was unsustainable.

Source: John Knapp, Weldon Cooper Center for Public Service, UVA

Increase in VirginiaTaxable Assessed Value by

Type of Property, 2000 to 2006

149%

92%

68%

61%

Single-Family

Residential

MultifamilyResidential

Commerical

Agricultural

5

vhda.com | 800-227-VHDA

Housing is not leading the economyout of recession as it has in the past.

• Historically, the lowering of interest rates during a recession stimulated housing construction and home purchase, which then led economic recovery by increasing jobs and retail sales.

• This time, the inventory of distressed homes and tightened lending standards are stifling housing construction and home sales.

• In addition, the sharp drop in home equity is putting a damper on retail sales.

6

vhda.com | 800-227-VHDA

Lack of a housing recovery is retarding local economic and revenue growth.

• With housing as a drag rather than a stimulus, the economy is struggling to regain momentum.

• Limited employment growth is reinforcing a vicious cycle in which:

– Loss of income puts more homeowners into foreclosure and increases the inventory of distressed properties.

– Weak home sales reinforce price declines, which in turn put more homeowners “underwater.”

– That increases the risk of loan defaults and foreclosures, and further depresses consumer confidence and willingness to spend.

• Local tax revenues will not revive until more progress is made in a housing recovery.

7

vhda.com | 800-227-VHDA

Current Market Trends

8

vhda.com | 800-227-VHDA

Home sales have fallen to a 13-year low following the end of the federal tax credit.

Source: Virginia Association of Realtors (VAR)

• Existing home sales appear once again to be bottoming out.

• However, sales are unlikely to see any meaningful rebound until employment increases and home prices fully stabilize.

Virginia Existing Home Sales4-Quarter Rolling Average

15,000

20,000

25,000

30,000

35,000

40,000

98-1

99-1

00-1

01-1

02-1

03-1

04-1

05-1

06-1

07-1

08-1

09-1

10-1

11-1

Calendar Year Quarter

3rd Qtr 2005

- 45%

Federal Homebuyer

Tax Credit

9

vhda.com | 800-227-VHDA

Prices are still declining in most markets, and NoVA’s earlier rebound has ended.

Source: Federal Housing Finance Agency (FHFA) Home Price Index

Annual Change in Metropolitan Home Prices1st Qtr 2010 to 1st Qtr 2011

-5.4%

-5.1%

-4.0%

-2.2%

-1.6%

-1.5%

-1.1%

-0.5%

0.7%

-0.9%

Richmond

Harrisonburg

Hampton Roads

Virginia

Washington, Winchester & Lynchburg

Roanoke

Charlottesville

Kingsport-Bristol

Blacksburg

Danville

VIRGINIA

10

vhda.com | 800-227-VHDA

Prices, especially in Northern Virginia,remain significantly below their peak.

Source: Federal Housing Finance Agency (FHFA) Home Price Index

Metropolitan Home Prices Relative to Their Peak1st Quarter 2011

-31%

-23%

-15%

-14%

-13%

-11%

-8%

-6%

-5%

-4%

Winchester

Washington, DC

Richmond

VIRGINIA

Hampton Roads

Harrisonburg

Charlottesville

Blackburg, Danville & Roanoke

Lynchburg

Kingsport-Bristol

VIRGINIA

11

vhda.com | 800-227-VHDA

In most markets, home prices are correcting to historic affordability norms.

Source: MRIS, Virginia Association of Realtors (VAR) and U.S. Census Bureau

Ratio of Median Home Price to Median Household Income

Northern Virginia Localities Downstate Metropolitan Areas

0.0 1.0 2.0 3.0 4.0 5.0 6.0

Spotsylvania

Stafford

Frederick

Pr. William

Fauquier

Loudoun

Fairfax

Arlington

Alexandria

Pre-Boom: April2000

Peak of Boom:May 2006

Current: April 2011

Traditional affordability range

0.0 1.0 2.0 3.0 4.0 5.0

Danville

Roanoke

Richmond

Lynchburg

HamptonRoads

Charlottes-ville

Pre-Boom: April 2000

Peak of Boom:2nd-4th Qtrs2007

Current: 1st Qtr 2011

Traditional affordability range

12

vhda.com | 800-227-VHDA

Experience from past recessions shows that inflation-adjusted prices recover very slowly.

Source: Federal Housing Finance Agency (FHFA) Home Price Index

Current(thru 2011-Q1)

Real Decline in Prices: -20.9% -27.3%

Peak to Trough: 7.8 Yrs. 4.3 Yrs.

Time to Regain Loss: 12.7 Yrs. ?

Real Decline in Prices: -14.5% -15.5%

Peak to Trough: 7.0 Yrs. 4.3 Yrs.

Time to Regain Loss: 15.2 Yrs. ?

Real Decline in Prices: -9.8% -20.6%

Peak to Trough: 5.5 Yrs. 4.0 Yrs.

Time to Regain Loss: 12.1 Yrs. ?

Washington MSA

Late 80's - Early 90'sHousing Downturn:

Hampton Rds MSA

Richmond MSA

13

vhda.com | 800-227-VHDA

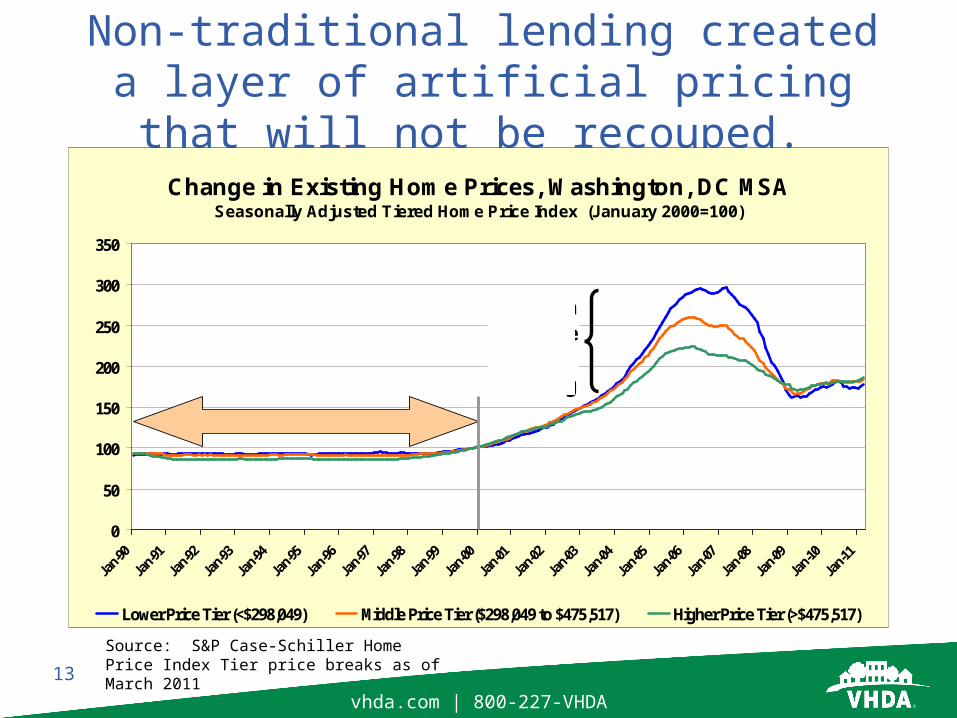

Non-traditional lending created a layer of artificial pricing that will not be recouped.

Source: S&P Case-Schiller Home Price Index Tier price breaks as of March 2011

Change in Existing Home Prices, Washington, DC MSASeasonally Adjusted Tiered Home Price Index (January 2000=100)

0

50

100

150

200

250

300

350

Lower Price Tier (<$298,049) Middle Price Tier ($298,049 to $475,517) Higher Price Tier (>$475,517)

Surge in subprimeand alt-A

lending

Decade of flat home values

14

vhda.com | 800-227-VHDA

Impact of Foreclosures

15

vhda.com | 800-227-VHDA

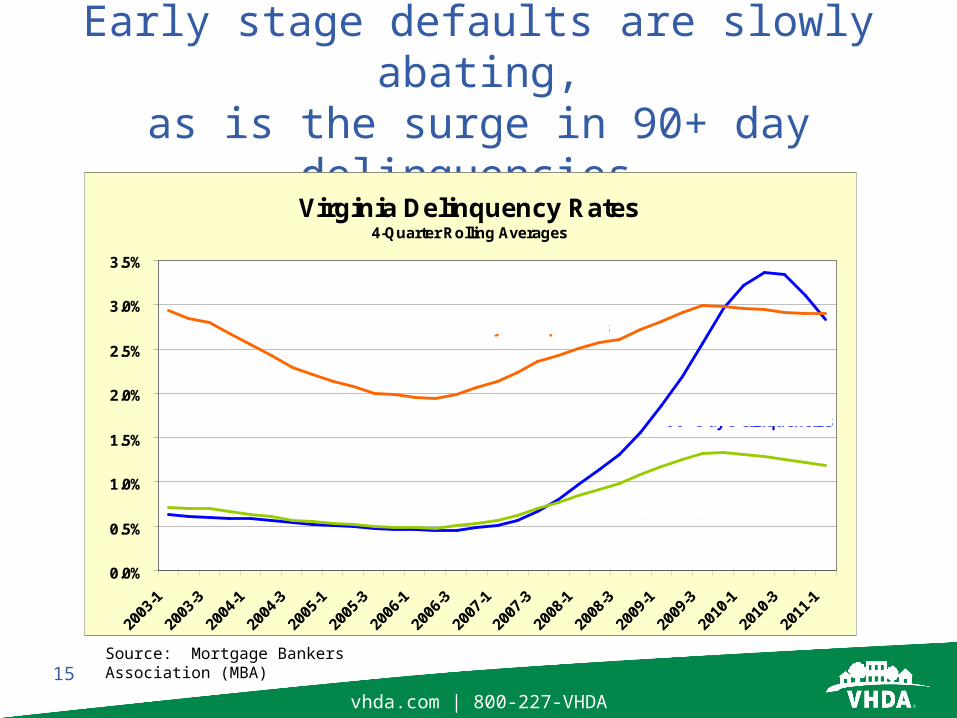

Early stage defaults are slowly abating,as is the surge in 90+ day delinquencies.

Source: Mortgage Bankers Association (MBA)

Virginia Delinquency Rates4-Quarter Rolling Averages

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

30 Day Delinquencies

90+ Day Delinquencies

60 Day Delinquencies

16

vhda.com | 800-227-VHDA

In contrast, initial progress in resolving foreclosures has been set back.

Source: Mortgage Bankers Association (MBA)

Virgina Loans in Foreclosureas a Share of Loans Serviced

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

17

vhda.com | 800-227-VHDA

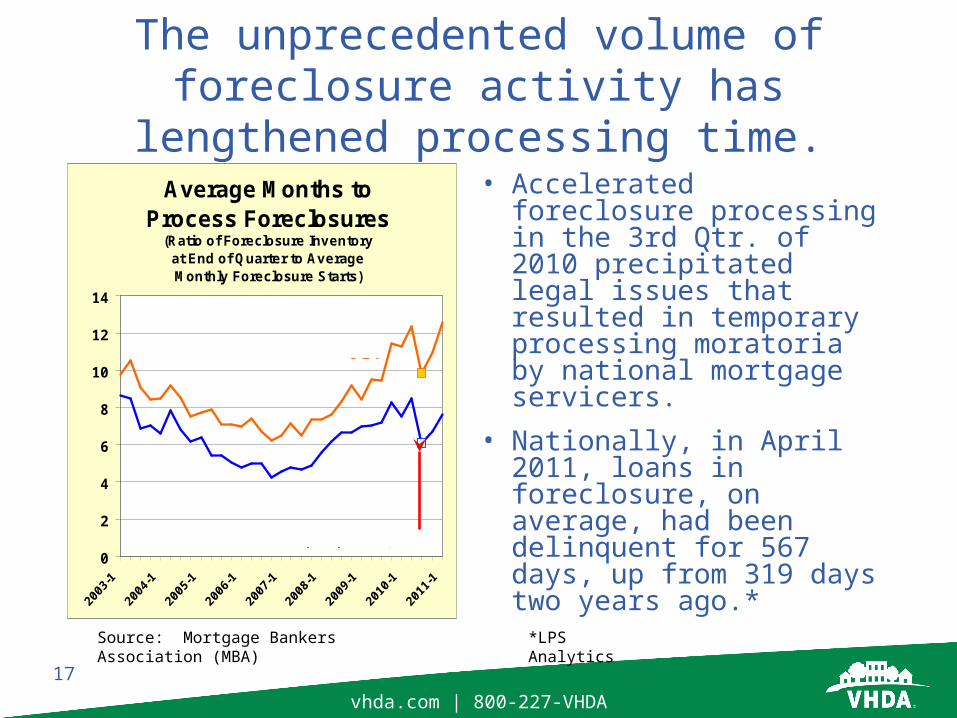

The unprecedented volume of foreclosure activity has lengthened processing time.

Source: Mortgage Bankers Association (MBA)

• Accelerated foreclosure processing in the 3rd Qtr. of 2010 precipitated legal issues that resulted in temporary processing moratoria by national mortgage servicers.

• Nationally, in April 2011, loans in foreclosure, on average, had been delinquent for 567 days, up from 319 days two years ago.*

*LPS Analytics

Average Months to Process Foreclosures

(Ratio of Foreclosure Inventoryat End of Quarter to AverageMonthly Foreclosure Starts)

0

2

4

6

8

10

12

14

U.S.

Virginia

Sharp drop in 3rd Qtr. 2010

18

vhda.com | 800-227-VHDA

Source: RealtyTrac and Census Bureau

Foreclosure completions have moderatedin the inner part of Northern VA (PD8).Now, the highest activity is in theouter part of NoVA, HamptonRoads and Richmond.

Northern Tier

Inner

Outer

Foreclosure Completions* March 2011

0.08%

0.14%

0.15%

0.30%

0.32%

0.38%

0.41%

0.45%

Southern T ier

Charlottesville-Central Valley

Roanoke-Blacksburg-Lynchburg

Northern T ier -- Inner (PD 8)

VIRGINIA

Greater Richmond

Hampton Rds-Chesapeake Bay

Northern T ier -- Outer

Share of Homes with a Mortgage

VIRGINIA

*Trustee sales and lender repossessions

Northern T ier -- Outer

Northern T ier -- Inner (PD 8)

19

vhda.com | 800-227-VHDA

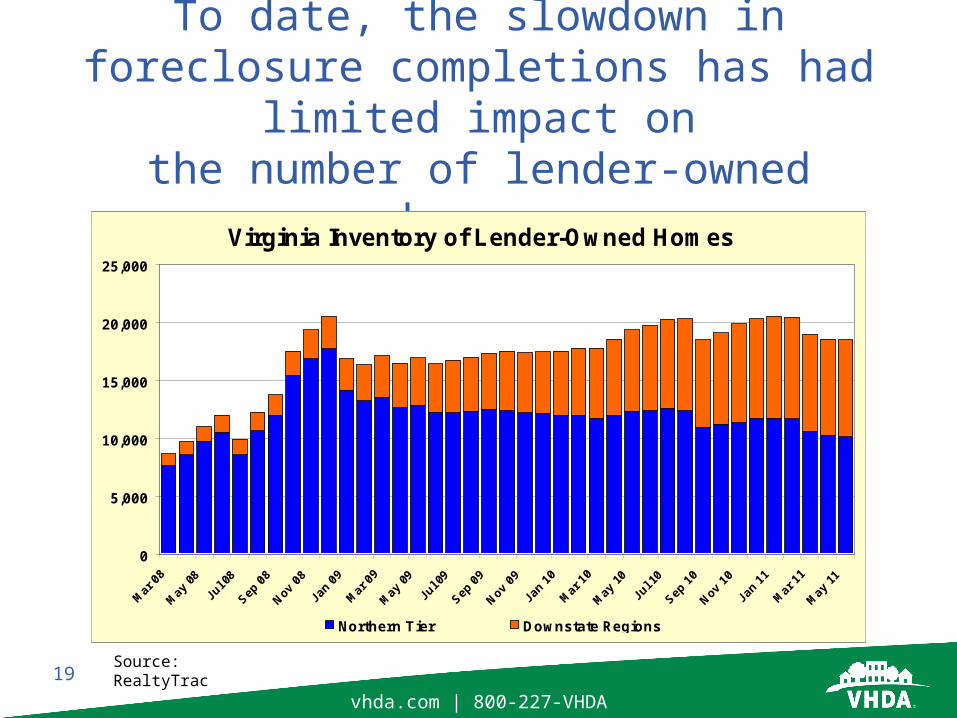

To date, the slowdown in foreclosure completions has had limited impact onthe number of lender-owned homes.

Source: RealtyTrac

Virginia Inventory of Lender-Owned Homes

0

5,000

10,000

15,000

20,000

25,000

Northern T ier Downstate Regions

20

vhda.com | 800-227-VHDA

Timely disposition of the substantiallender-owned inventory is proving difficult,

and is undermining market recovery.

• Investor sales are rising, but remain insufficient to substantially reduce lender-owned inventories.

• The increased market shares of distressed sales is undercutting prices and keeping traditional buyers and sellers on the sidelines.

• A renewed decline in home sales is reinforcing price weakness and keeping large numbers of homeowners “under water.”

• Any substantial further drop in prices would risk renewed increases in mortgage defaults and a set back in the limited progress in reducing foreclosures.

21

vhda.com | 800-227-VHDA

Investor sales are rising, but are not substantially reducing lender inventories.

Source: MRIS

Cash Sales Share of Total Existing Home SalesNorthern T ier Region

0%

5%

10%

15%

20%Feb '11 18.8%

Jan '10 17.1%

Apr '063.1%

Feb '09 15.5%

22

vhda.com | 800-227-VHDA

Inventories have risen year over year except in Northern Tier markets wherethere have been modest reductions.

Source: RealtyTrac and Census Bureau

Inventory of Lender-owned Homes

0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Southern Tier

Charlottesville-Central Valley

Roanoke-Blacksburg-Lynchburg

Greater Richmond

Virginia

Hampton Rds-Chesapeake Bay

Northern Tier -- Inner

Northern Tier -- Outer

Share of Homes w ith a Mortgage

May 30, 2010

May 30, 2011

VIRGINIA

23

vhda.com | 800-227-VHDA

Future Outlook

24

vhda.com | 800-227-VHDA

Demographic change will play adominate role in housing’s recovery.

• The housing downturn has focused attention on the impact of mortgage lending on home construction and overall market health.

• Less attention has been paid to the critical role that shifting demographics play in shaping the magnitude and nature of housing demand.

• We are now in a new a market cycle that will be heavily influenced by large shifts in housing demand driven by demographic change.

25

vhda.com | 800-227-VHDA

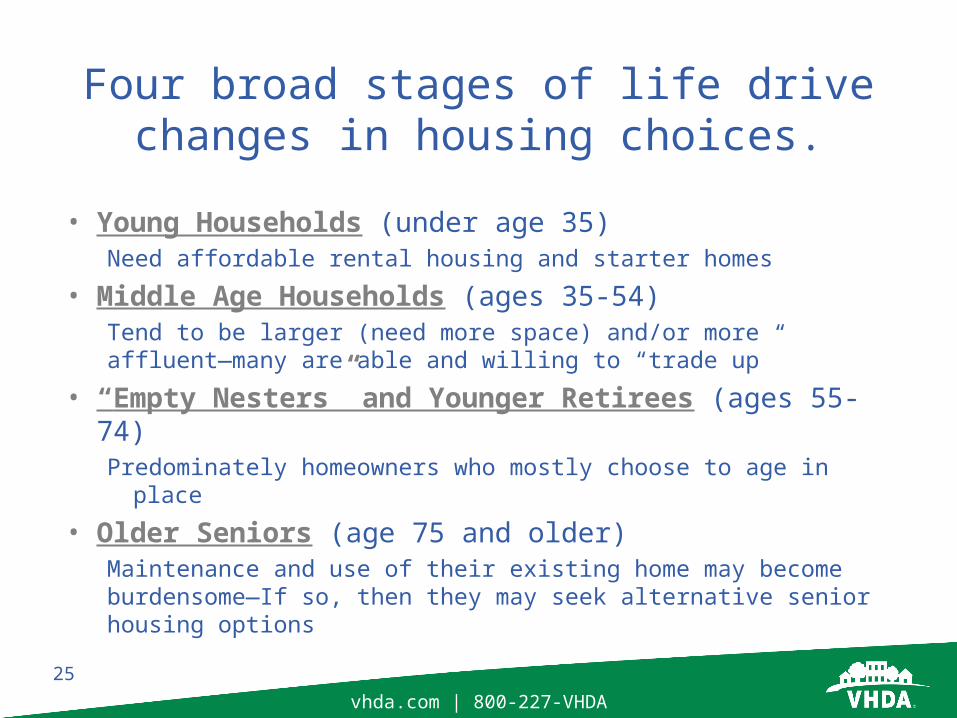

Four broad stages of life drivechanges in housing choices.

• Young Households (under age 35)Need affordable rental housing and starter homes

• Middle Age Households (ages 35-54)Tend to be larger (need more space) and/or more affluent—many are able and willing to “trade up”

• “Empty Nesters” and Younger Retirees (ages 55-74)Predominately homeowners who mostly choose to age in place

• Older Seniors (age 75 and older)Maintenance and use of their existing home may becomeburdensome—If so, then they may seek alternative seniorhousing options

26

vhda.com | 800-227-VHDA

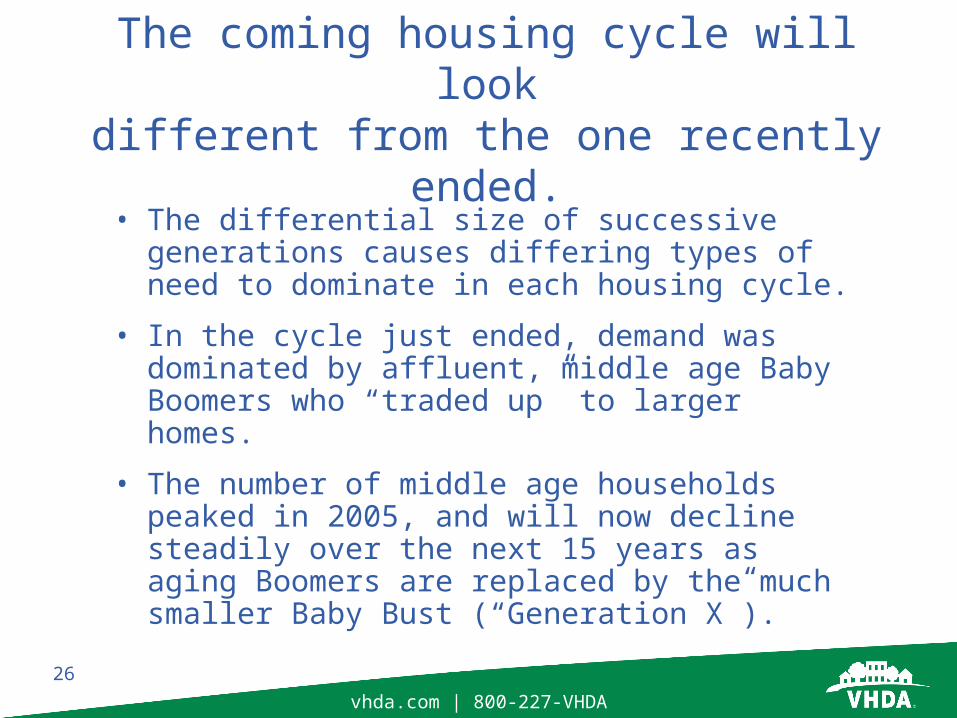

The coming housing cycle will lookdifferent from the one recently ended.

• The differential size of successive generations causes differing types of need to dominate in each housing cycle.

• In the cycle just ended, demand was dominated by affluent, middle age Baby Boomers who “traded up” to larger homes.

• The number of middle age households peaked in 2005, and will now decline steadily over the next 15 years as aging Boomers are replaced by the much smaller Baby Bust (“Generation X”).

27

vhda.com | 800-227-VHDA

The “Trade-Up” Era is Over.

We are now in a new

market cycle in which young households, empty nesters and younger retirees will dominate.

13,878

-71,103-57,707

39,604

140,322

213,561 227,529205,278

99,502

26,828 32,336 32,29748,547 50,599

20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

Young Renters &1st-Time Homebuyers

Middle AgeTrade-up Homebuyers

Empty Nester & YoungerSenior Homeowners

Older Seniors w/Special Needs

65,937

118,488109,840

17,931

-68,932-53,235

30,955

119,900

189,787 192,947

167,928

42,74732,013

63,409

20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

Estimated Population Change 1990-2005

Projected Population Change 2005-2020

Source: U.S. Census and estimates based on Census Bureau and VEC Virginia population projections

28

vhda.com | 800-227-VHDA

Today’s housing stock is notadequate to meet emerging needs.

• Relatively little starter home and new rental construction occurred in the recent housing cycle.

• Except in the fastest growing regions, existing apartments and starter homes that were vacated by Baby Boomers “trading up” to newly built larger homes, served much of the needs of Generation X.

• Now, as Generation X replaces Baby Boomers in the “trade up” market, and Generation Y forms independent households, we face an over-supply of larger “trade up” homes and a shortage of smaller affordable units.

29

vhda.com | 800-227-VHDA

Quality, affordable rental housingwill be especially needed.

• A large and growing majority of young households are renters, while middle age and older households are mostly owners.

• In the past housing cycle, a large share of rental investment involved the upgrade of existing properties.

• In the coming cycle, a larger net increase in rental units will be needed in order to accommodate the growth in young households.

Source: American Community Survey

Share of Virginia Households that Rent by Age

58%

26%

17%21%

63%

29%

17%

22%

UnderAge 35 Age 35-54 Age 55-74 Age 75 andOlder

2006 2009

30

vhda.com | 800-227-VHDA

Generation Y will likely have moredifficulty achieving homeownership.

• Over the past two decades, young households have incurred substantial debt compared to previous generations.

• Credit card debt has risen dramatically, and many are burdened by student loans.

• For the Class of 2011, student loan debt is estimated to average $22,900.

• Significant tightening of credit standards and down payment requirements will likely delay home purchase by Generation Y despite lower home prices.

$2,873 $4,358

1989 2004

+52%

Average credit card debt among households age 25 to 34 with credit card debt (2004 dollars)

Source: Survey of Consumer Finance, 1989 and 2004

31

vhda.com | 800-227-VHDA

Housing affordability will continueto be an issue in a housing recovery.

54%

95%

115%

132%

112%

74%

52%

Under 25 25 to 34 35 to 44 45 to 54 55 to 64 65 to 74 75+

Age Group

Overall Median

Median income by age as a shareof overall median household income

• In the past housing cycle, demand was concentrated in the age group with the highest income.

• Now, demand is shifting to age groups with more limited means.

• The current surplus of “trade up” homes is mismatched with future needs.

Source: 2000 Census

32

vhda.com | 800-227-VHDA

We continue to face housing challenges that require strong public/private partnerships.

• Recovery of local housing markets and real estate tax revenues will require new public land use strategies that facilitate the private development of affordable rental and ownership opportunities to meet emerging demand.

• The public sector must also help the private market address the housing inventory imbalances resulting from demographic shifts, the overhang of foreclosed inventories, and the ongoing need to revitalize aging housing stock and neighborhoods.

• Finally, federal, state and local officials will need to work in partnership to ensures the affordability of housing for all people in a manner that is fiscally sound and builds more sustainable local communities.